Embed Size (px)

DESCRIPTION

Implications of Global Financial Crisis on South East Europe: Lessons Learned by Serbia. Diana Dragutinovic. Main Themes. Serbia before the crisis Crisis imported into SEE Serbia hit at an unfortunate moment Solid banking system, but with typical weak spots - PowerPoint PPT Presentation

Citation preview

Implications of Global Financial Crisis on South East Europe:Lessons Learned by Serbia

Diana Dragutinovic

Main Themes Serbia before the crisis Crisis imported into SEE

• Serbia hit at an unfortunate moment Solid banking system, but with typical weak spots So far mostly indirect contagion channels related to credibility

of the FX denominated banking system, compounded by • Macroeconomic vulnerabilities• Behavior of mother banks towards the local banking

systems

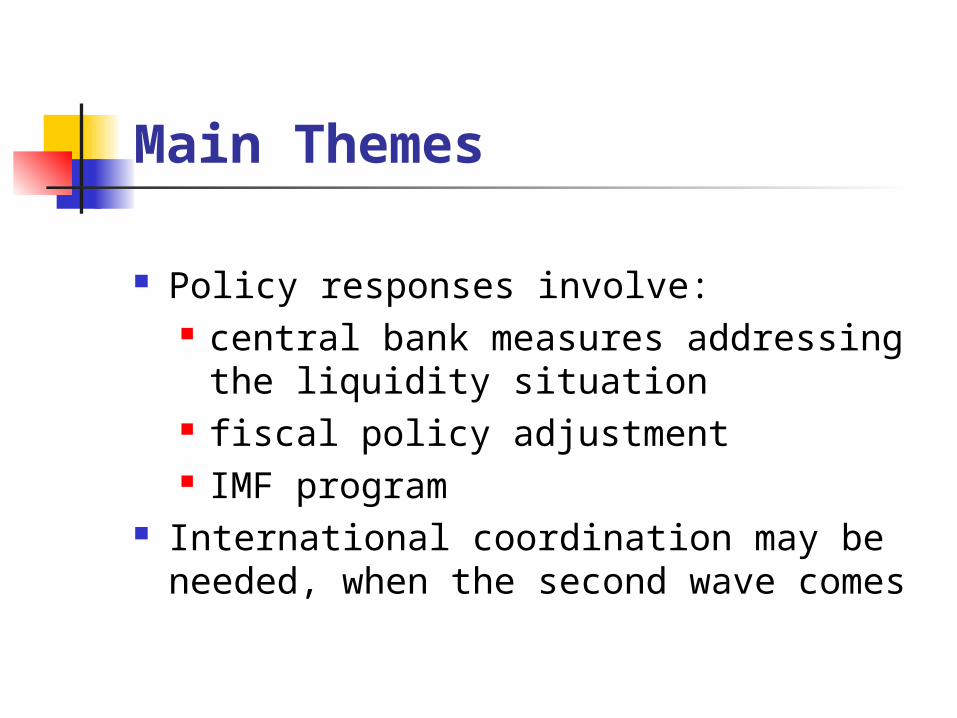

Main Themes

Policy responses involve: central bank measures addressing the liquidity

situation fiscal policy adjustment IMF program

International coordination may be needed, when the second wave comes

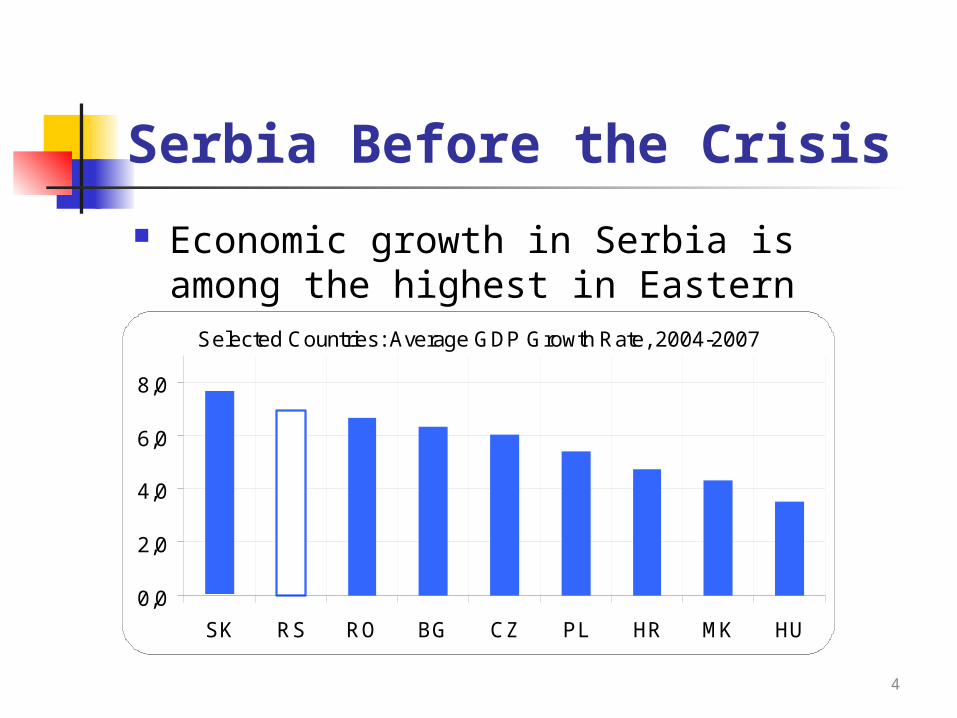

Serbia Before the Crisis

4

Economic growth in Serbia is among the highest in Eastern Europe

Selected Countries: Average GDP Growth Rate, 2004-2007

0,0

2,0

4,0

6,0

8,0

SK RS RO BG CZ PL HR MK HU

Serbia 2004-2007: Brief Background Growth fueled mainly by domestic demand (both private

and government spending driven by election cycles ) Domestic demand fueled by:

Strong external financing / capital inflows such as: Privatization of socially-owned companies, banking sector /

insurance companies FDIs Banking sector recapitalization Foreign borrowing by banking sector Cross-border loans to private sector

5

Serbia 2004-2007: Brief Background

Competitiveness and export growth did not follow Low level of exports in GDP

Slow progress of structural reforms

Undersized private sector (which remains one of the smallest in the region)

Low competitiveness of the economy (85th by World Economic Forum Global Competitiveness Report)

Strong wage growth Appreciation of Dinar

Opportunities lost to increase competitiveness of the economy

6

Weak External Position Limits Policy Response to the Crisis

Side effects of high, but unbalanced growth - rising external disequilibrium

CA deficit has almost doubled since 2005, reaching 18% of GDP

Serbia was not able to avoid the problem of rapid debt accumulation by the private sector

…but Some Good Achievements

Recent achievements of the Serbian economy, such as Low sovereign debt level Comfortable level of FX reserves Strong capital and liquidity position of the banking system

…will help the economy to adjust in an orderly manner Shallow domestic capital markets protected the Serbian

economy from the abrupt capital flight experienced by other emerging market economies

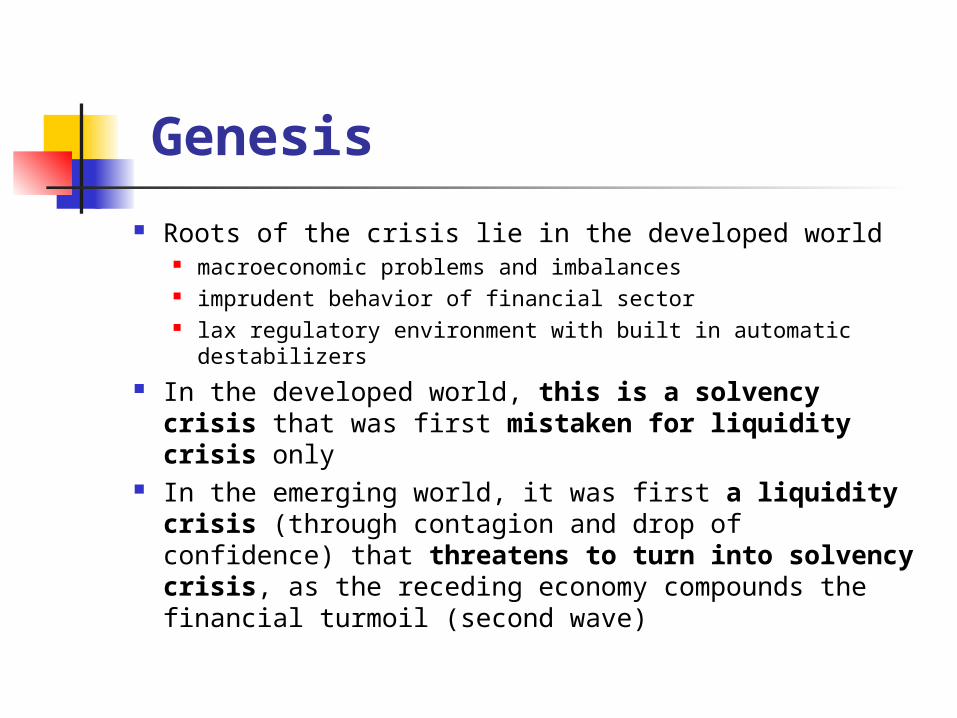

Genesis

Roots of the crisis lie in the developed world macroeconomic problems and imbalances imprudent behavior of financial sector lax regulatory environment with built in automatic destabilizers

In the developed world, this is a solvency crisis that was first mistaken for liquidity crisis only

In the emerging world, it was first a liquidity crisis (through contagion and drop of confidence) that threatens to turn into solvency crisis, as the receding economy compounds the financial turmoil (second wave)

Emerging Markets as Victims

EMs entered the turmoil with relatively sound and solvent banking systems

However, big differences among EMs in vulnerabilities of macroeconomic policies, exposures to FX and roll-over risk

Elements speeding up the contagion high current account deficit and procyclical fiscal policy currency overvaluation highly euroized banking sector with large indirect FX

exposure of private sector's balance sheets without the central bank as the lender of last resort in FX

bank business model dependent on roll-over of foreign FX borrowing rather than domestic deposits

Cross – border borrowing by non – financial institutions high growth of FX denominated private debt

Many of the elements present in South-Eastern Europe and Serbia

Serbia: Solid Banking System (I)

Privatization and cleaning up of balance sheet in early 2000s.

Domestic financial institutions without substantial exposure to the U.S. sub-prime mortgage-linked toxic assets.

Low direct exchange rate risk exposure in the banking sector

Local banking system with a strong liquidity position reflected by sizeable reserves with central bank.

Serbia: Solid Banking System (II)

Dynamically growing economy provided good profit opportunities from traditional retail activities low penetration of exotic instruments

Relatively prudent lending standards credit standards until recently relatively strict transfer risk of credit risk outside the banking portfolios via

securitization nonexistent, Balanced credit growth rates

…with Weak Spots

High financial sector euroization High indirect ex rate risk exposure through the unhedged

positions of the real economy Exposes the banking sector to FX liquidity risks, because the NBS is not

a lender of last resort in FX Low deposit base

necessitating foreign borrowing to finance mortgage lending and other small retail business

Exposes to liquidity dry up and roll-over risks Large proportion of direct foreign lending going outside the

banking system

First Wave Contagion Channels and Other Contributing Factors Drop in market confidence Local banking sector forced to change behavior

following the problems of mothers in home countries Home (EU and Eurozone) national regulators and

authorities focusing strictly on Eurozone (home) problems, leaving the EMs largely on their own and thus indirectly compounding the EMs problems

Dependence of Eastern Europe on a common lender exposing the vulnerability to a regional contagion

Drop in Confidence

Domestic money, bond and FX market participants Because of uncertainties about parent companies,

exchange rate risks etc. International investors’ aversion towards the region

(flight to quality) Long-term investment sentiment (drop in expected FDI

inflows) Depositors’ confidence (especially in terms of FX)

Local Banking Sector Changing Following the Problems of Mothers in EU Countries

Cutting all but the most essential credit lines on shortest maturities to their daughters (without daughters having first order problems)

Applying pressure on daughters to change the business model from the one based on a roll-over of FX borrowing to the one dependent on a local deposit base

Applying pressure on daughters to apply more prudent lending standards

Cutting counterparty and trading limits for both secured and non-secured transactions

Withdrawing free FX liquidity from daughters Hedging out exposures to daughters’ capital in domestic currency

EU Authorities Focusing Strictly on Home Problems, Leaving the EMs Largely on Their Own

EU regulators encouraging (through moral suasion and perhaps other means) to limit the exposures of mother banks to the Central and Eastern Europe

EU public money used in propping up the capital adequacy of Eurozone banks are not designed to support the banks’ business in emerging Europe

Local EM currency bonds not accepted by ECB as a collateral Missing swap FX links between ECB and EM banks in need of FX

liquidity (exception Poland and Hungary) Coordination of policies and activities limited to Eurozone or EU,

non-EU left out

Dependence on a Common Lender Exposes Vulnerability to a Regional Contagion

In many EMs loan-to-deposit ratios increased rapidly in the recent decade Exposures of many SEE and CEE countries to EU banking groups are

geographically concentrated. Austria, Germany, and Italy account for more than 40% of EU bank claims on

emerging Europe; Sweden is the largest lender to the Baltics Some small lender countries exposure to emerging Europe is large in terms of

their GDP for instance for Austria, it is more than 70%

The concentrated home-host country exposure derives from concentrated activities of individual bank groups.

The regional giants derive much of their operational income (often more than 50%) from the Eastern European markets

Macroeconomic Vulnerabilities in Serbia Contribute to Contagion High current account deficit

Financed through FDI and foreign borrowing Sustainability dependent on continued high export growth

Continued high inflation following the oil and food prices shocks from 2007/8 Does not provide much room for relaxing monetary policy High risk premium and exchange rate pressures

Worsening fiscal position the macroeconomic situation puts pressure on fiscal policy to

adjust and allow monetary policy relaxation

First Wave Effects: Money and FX Markets After long-lasting nominal and real

appreciation of CEE currencies (including dinar), the crisis led to strong currency depreciation

Pressure on the currency Sudden stop of external

financing Cross-border lending to

corporation stalled FDIs stopped

Fall in external demand Falling exports

Rising currency risk premiums

First Wave Effects: Money and FX Markets

Drop in liquidity and volumes in money and FX markets

Rising bid/ask spreads Shortening maturities Rising credit spreads

First Wave Effects: Banking Sector

Problems with handling FX deposit withdrawals in October and November ‘08 of almost 1 bn euro with limited credit lines because of mothers’ problems without a central bank as the lender of last resort

Difficulties in rolling over FX debt, even to mothers Difficulties in obtaining additional FX sources to support

the continuation of lending or trading Lending more based on the deposit base

More prudent lending standards

24

NBS measures provide additional FX liquidity Banking sector liquid, but does not lend Credit to non-government sector stopped

First Wave Effects: Real Economy

Falling export growth following the world output contraction despite currency depreciation

Slowing down in FX lending though still not yet credit crunch

Dinar lending impeded by high interest rates Balance sheet concerns of a depreciating currency for unhedged

sectors of the economy both households and businesses

First Wave Effects: FX Policy

Problem of a lender of last resort in FX insufficient FX reserves make the role of a lender or

market maker of last resort difficult Dilemma:

let the exchange rate depreciate in order to adjust the external imbalances and preserve the FX reserves for more difficult times

limit the extent of depreciation out of concern for inflation and balance sheet effects

First Wave Effects: Monetary Policy

Inflation still high and exchange rate has depreciated Effects of economic downturn on inflation not yet being felt Policy transmission more difficult

money market situation and ex rate expectations make lending interest rates less sensitive to key policy rates

exchange rate less sensitive to interest rate movements (because of high risk aversion and complications in hedging exposures)

Dilemma to cut in anticipating the recession and credit crunch, and falling inflation tighten to fight the capital flight and inflationary implications of depreciating

ex rate.

First Wave Effects: Fiscal Policy

Dilemma be prudent to decrease vulnerabilities and external

imbalances, and help support looser monetary policy support economic recovery, possibly beyond the

effect of automatic stabilizers

Policy Responses

Policy options limited owing to the initial sources of the contagion – trust into FX Monetary policy measures - addressing the FX market liquidity

Allowing banks to use FX reserves to address the liquidity problems Reducing reserve requirements to facilitate borrowing from abroad Frequent interventions injecting FX liquidity and cushioning the speed of the FX

adjustment Interest rates remaining high

Fiscal policy measures Rebalancing the budget for 2008 and moderate budget deficit for 2009

Coordinated actions IMF program Inflation Targeting declaration

Risks for The Future: Second Wave Further contagion channels may hit the economy More of the world recession:

Slowing export growth, exposing CA imbalances Rising default rates

Sudden stop: principal channel through which crisis hits Serbia

Fall in FDI Pressure on the exchange rate Pressure on the public revenues Pressure on the monetary policy

Capital outflows e.g. through transfers of retained earnings from the banking sector

Banking sector stability affected by rising default rates

Risks of The Second Wave for SEE Multiplication of interactions between the receding

economy and the financial sector within each economy Banking sector stability will be hit by rising default rates

during the recession. Fiscal policy may be put on further strain by the need to help

recapitalize the banking sector This will further spiral the drop of confidence

characterizing the first wave Potential second round contagion through regional

interlinkages systemic solvency problems in EMs may destabilize the

mothers and the financial system of home (EU) countries

International Response Needed to Address SEE Vulnerabilities Public sector assistance and/or international coordination may be

needed to handle the second wave most EMs and some small EU countries-concentrated lenders may be

unable to cope with the implications. The real danger of the second wave is that the situation in EMs may

soon look like that one in US or Western Europe however without the fiscal pockets or monetary credibility to allow

extraordinary measures on the scale seen in the West It would pay off by starting now – addressing the first wave problems

through better coordination between host-home countries being more forthcoming in terms of emergency swap lines and local

currency collateral applying equal treatment to Eurozone (domestic) as well as non Euro

businesses of Eurozone banks