Embed Size (px)

Citation preview

ImplementingGAAS

2010–11

A Practical Guideto Auditing and Reporting

Peter ChidgeySarah Nendick

BDO LLP

Wolters Kluwer (UK) Limited145 London Road

Kingston upon ThamesSurrey

KT2 6SRTelephone: 144(0) 844 561 8166Facsimile: 144(0) 870 247 1184

email: [email protected]: www.cch.co.uk

DisclaimerThis publication is sold with the understanding that neither the publisher nor theauthors, with regard to this publication, are engaged in rendering legal orprofessional services. The material contained in this publication neitherpurports, nor is intended to be, advice on any particular matter.

Although this publication incorporates a considerable degree of standardisation,subjective judgment by the user, based on individual circumstances, isindispensable. This publication is an ‘aid’ and cannot be expected to replacesuch judgment.

Neither the publisher nor the authors can accept any responsibility or liability toany person, whether a purchaser of this publication or not, in respect of anythingdone or omitted to be done by any such person in reliance, whether sole orpartial, upon the whole or any part of the contents of this publication.

Telephone Helpline Disclaimer NoticeWhere purchasers of this publication also have access to any TelephoneHelpline Service operated by Wolters Kluwer (UK), then Wolters Kluwer’s totalliability to contract, tort (including negligence, or breach of statutory duty)misrepresentation, restitution or otherwise with respect to any claim arising outof its acts or alleged omissions in the provision of the Helpline Service shall belimited to the yearly subscription fee paid by the Claimant.

Q 2010 Wolters Kluwer (UK) Ltd

Auditing Practices Board material Q 2010 Reproduced with the permission ofthe Auditing Practices Board.

ISBN 978-1-84798-250-6

All rights reserved. No part of this publication may be reproduced, stored in aretrieval system, or transmitted in any form or by any means, electronic,mechanical, photocopying, recording or otherwise, without the prior permissionof Wolters Kluwer (UK) Limited or the original copyright holder.

No responsibility for loss occasioned to any person acting or refraining fromaction as a result of any material in this publication can be accepted by theauthor or publisher.

Material is contained in this publication for which copyright is acknowledged.Permission to reproduce such material cannot be granted by the publisher andapplication must be made to the copyright holder.

Crown copyright is reproduced with the permission of the Controller of HerMajesty’s Stationery Office.

British Library Cataloguing-in-Publication DataA catalogue record for this book is available from the British Library.

Typeset in-house at Wolters Kluwer (UK) LtdPrinted and bound in the UK by Hobbs the Printers Ltd

CONTENTS

Preface xxxv

PART 1 INTRODUCTION

1 The nature of Auditing Standards 31.1 Introduction 31.2 Limitations of Standards 31.3 Authoritative bodies 41.4 The Auditing Practices Board 4

1.4.1 International Standards of Auditing (UK and Ireland) 71.4.2 Practice Notes 81.4.3 Bulletins 9

1.5 International Auditing and Assurance Standards Board 91.5.1 IAASB’s Clarity Project 91.5.2 APB Adoption of clarified ISAs 91.5.3 Transition 10

1.6 Other guidance 111.7 Other sources of Auditing Standards 11

2 Audit regulation 132.1 Introduction 132.2 Qualification 142.3 Control of audit firms 142.4 Fit and proper person 142.5 Professional integrity and independence 15

2.5.1 Ethical Standard 1 (Revised): Integrity, Objectivityand Independence 16

2.5.2 Ethical Standard 2 (Revised): Financial, Business,Employment and Personal Relationships 20

2.5.3 Ethical Standard 3 (Revised): Long Association withthe Audit Engagement 23

2.5.4 Ethical Standard 4 (Revised): Fees, Remunerationand Evaluation Policies, Litigation, Gifts andHospitality 24

2.5.5 Ethical Standard 5 (Revised): Non-Audit ServicesProvided to Audited Entities 25

2.6 Ethical Standard, Provisions Available for Small Entities 262.6.1 Background 262.6.2 Non-audit services 272.6.3 Economic dependence 282.6.4 Parties joining an audit client 282.6.5 Audit report wording 29

2.7 Review of Ethical Standards 312.7.1 Background 312.7.2 Remuneration of key partners 31

v

Contents

2.7.3 Governance 322.7.4 Restructuring and securitisation services 322.7.5 Internal auditors 322.7.6 Affiliates 332.7.7 Financial interests of new partners 33

2.8 Consultation on non-audit services 332.8.1 Background 332.8.2 Services provided 342.8.3 Managing the risks 35

2.9 ICAEW Code of Ethics 352.9.1 Background 352.9.2 The fundamental principles 362.9.3 Threats and safeguards 372.9.4 Conflict resolution 38

2.10 Technical standards 382.10.1 Acceptance of appointment and reappointment 392.10.2 Quality control 392.10.3 Control of confidentiality and independence 39

2.11 Maintaining competence 392.12 Meeting of claims 402.13 Other areas 402.14 The Professional Oversight Board for Accountancy 402.15 The Quality Assurance Directorate 412.16 Audit reports 412.17 Working papers 42

2.17.1 Retention of working papers 422.17.2 Work carried out by other auditors 43

PART 2 REPORTING

3 The audit report 473.1 Introduction 473.2 The Standards 47

3.2.1 Other guidance 483.3 ISA (UK and Ireland) 700 (Revised) 49

3.3.1 Main changes 493.3.2 Discussions with those charged with governance 49

3.4 Aim of the audit report 493.5 Contents of an audit report 503.6 Title 513.7 Addressee 513.8 Introductory paragraph 513.9 Respective responsibilities of those charged with governance

and auditors 513.10 Scope of the audit of the financial statements 523.11 Auditor’s opinions 52

3.11.1 True and fair 52

vi

Contents

3.11.2 Opinion on other matters 533.12 Signature 53

3.12.1 Senior Statutory Auditor 533.12.2 Signing 553.12.3 Joint auditors 55

3.13 Date 553.14 Unmodified auditor’s reports examples 563.15 Directors’ responsibilities statements 593.16 Small companies 633.17 APB Bulletin 2002/2, the United Kingdom Directors’

Remuneration Report Regulations 663.17.1 Introduction 663.17.2 Companies affected by the rules 663.17.3 The ‘auditable part’ of the Directors’ Remuneration

Report 663.17.4 Reporting on the Directors’ Remuneration Report 673.17.5 The Directors’ Remuneration Report as a separate

document 673.18 Changes to audit reports resulting from electronic publication 68

3.18.1 Background 683.18.2 Electronic publication of audit reports 683.18.3 The Companies Act 2006 73

3.19 Departure from SORPs 733.19.1 Requirements of FRS 18 743.19.2 Audit considerations 743.19.3 Audit opinion 74

3.20 The Bannerman case 753.20.1 Introduction 753.20.2 Auditors’ responsibilities 763.20.3 Recommended wording 763.20.4 Engagement letters 76

3.21 Reading audit reports 76

4 Modified auditor’s reports 794.1 Introduction 794.2 Types of modification 79

4.2.1 Emphasis of matter 814.2.2 Qualified opinions 834.2.3 Limitation of audit scope 834.2.4 Disagreement 884.2.5 Adverse opinions or disclaimers of opinion 904.2.6 Multiple uncertainties 90

5 Other reports on financial statements 915.1 Introduction 915.2 Summary financial statements 92

5.2.1 Legal background 92

vii

Contents

5.2.2 Auditing Standards and Guidelines 925.2.3 Audit procedures 935.2.4 Reporting 95

5.3 Abbreviated accounts 965.3.1 Legal background 965.3.2 Guidance 975.3.3 Audit procedures 97

5.4 Exemptions for small and medium-sized groups 995.4.1 Legal background 995.4.2 Audit procedures 100

5.5 Revised financial statements 1005.5.1 Legal background 1005.5.2 Auditing Guideline 1005.5.3 Types of revision 1005.5.4 Procedures 106

5.6 Preliminary announcements 1075.6.1 Background 1075.6.2 Guidance 1075.6.3 Terms of engagement 1085.6.4 Procedures 1085.6.5 Pro forma information 1115.6.6 Management commentary 1125.6.7 Directors’ approval 1125.6.8 Modification of the auditor’s report 1125.6.9 Reporting 1125.6.10 Announcements not agreed 114

5.7 ISRE 2400 1145.7.1 Introduction 114

6 Other statutory audit reports 1176.1 Introduction 1176.2 Distributions: qualified reports 117

6.2.1 Legal background 1176.2.2 Guidance 118

6.3 Distributions: initial distributions 1206.3.1 Legal background 1206.3.2 Guidance 121

6.4 Purchase and redemption of own shares 1226.4.1 Legal background 1226.4.2 Guidance 122

6.5 Re-registration of companies 1236.5.1 Legal background 1236.5.2 Guidance 124

6.6 Allotment of shares otherwise than for cash 1286.6.1 Legal background 1286.6.2 Guidance 129

viii

Contents

6.7 Transfer of non-cash assets to a public company by one of itsmembers 1306.7.1 Legal background 130

7 Reports on accounts prepared by accountants 1337.1 Introduction 1337.2 Guidance 1337.3 Incorporated entities 134

7.3.1 Terms of engagement 1347.3.2 Directors’ responsibilities 1367.3.3 Accountants’ procedures 1367.3.4 Misleading financial statements 1367.3.5 Approving financial statements 1377.3.6 Accountants’ reports 137

7.4 Unincorporated entities 1387.4.1 Scope of guidance 1387.4.2 Professional ethics 1397.4.3 Accounting basis 1397.4.4 Terms of engagement 1397.4.5 Client’s responsibilities 1417.4.6 Planning 1417.4.7 Procedures 1417.4.8 Misleading financial information 1417.4.9 Approval of financial information 1427.4.10 Accountants’ reports 142

7.5 Considerations following the increase in the audit exemptionlimit 143

8 Reports to the FSA on investment businesses 1458.1 Legal background 1458.2 Types of report 1458.3 Auditing Standards and guidance 1458.4 Respective responsibilities 1468.5 Client assets 147

8.5.1 Custody assets and collateral 1488.5.2 Client money 1498.5.3 No client assets 1508.5.4 Other audit considerations 1518.5.5 Further guidance 1518.5.6 Reporting 1518.5.7 Qualified reports 154

8.6 Special ad hoc reports 1558.6.1 Guidance 1558.6.2 Right and duty to report 1558.6.3 ‘material significance’ 1568.6.4 Procedures 1598.6.5 Reporting 162

ix

Contents

8.6.6 Form of report 1638.6.7 Communication by the regulator 1648.6.8 Relationship with other reporting responsibilities 164

9 Reports to management 1659.1 Introduction 1659.2 Auditing Standards 1659.3 Those charged with governance 1659.4 Aims of reports to those charged with governance 1669.5 Establishing expectations 1679.6 Form of communication 1679.7 Effectiveness of communications 1689.8 Matters to be communicated 168

9.8.1 Definition 1689.8.2 Listed companies 1689.8.3 Integrity, independence and objectivity 1699.8.4 Planning information 1699.8.5 Findings from the audit 170

9.9 Addressees 1719.10 Groups 1729.11 Third parties 1729.12 Form of reports 1739.13 Clarified ISA 265 Communicating deficiencies in internal

control to those charged with governance and management 1749.13.1 Background 1749.13.2 Identifying and reporting deficiencies 1749.13.3 Significant deficiency 1749.13.4 Reporting of significant deficiencies 176

10 Fraud and error 17710.1 Introduction 17710.2 Auditing Standards 17710.3 Definitions 178

10.3.1 Fraud 17810.3.2 Error 179

10.4 Responsibilities of those charged with governance 17910.5 Auditors’ responsibilities 179

10.5.1 Professional scepticism 18010.5.2 Engagement team discussion 18110.5.3 Risk assessment 18110.5.4 Identification and assessment of fraud risk 18310.5.5 Responses to fraud risk 184

10.6 Evaluating audit evidence 18710.7 Auditor unable to continue the engagement 18810.8 Management representations 18810.9 Communication with management and those charged with

governance 189

x

Contents

10.10 Communication with the authorities 18910.11 Documentation 190

11 Consideration of law and regulations 19111.1 Introduction 19111.2 Auditing Standards 19111.3 Legal and regulatory framework 19211.4 Management responsibility 19211.5 Responsibility of the auditors 19311.6 Consideration of compliance 194

11.6.1 Laws with a direct effect on the financial statements 19411.6.2 Laws affecting the operations of the entity 195

11.7 Money laundering 19511.8 Non-compliance 19511.9 Reporting 197

11.9.1 Reporting to those charged with governance 19711.9.2 Reporting to owners/members 19711.9.3 Reporting to third parties 198

11.10 Resignation 199

12 Money laundering 20112.1 Background 20112.2 Consequences for accountants in practice 201

12.2.1 Changes in the 2007 Regulations 20212.3 Auditors’ responsibilities 20212.4 Practice Note 12 (Revised) 203

12.4.1 Introduction 20312.4.2 What is money laundering? 20312.4.3 Procedures 20512.4.4 Tipping off 21012.4.5 Reporting to the MLRO and SOCA 21112.4.6 Privilege reporting exemption 21112.4.7 Auditors’ report on the financial statements 213

12.5 Consideration of laws and regulations 21312.6 Other guidance 214

13 Going concern 21713.1 Introduction 21713.2 Auditing Standards 21713.3 General requirement 21813.4 The entity’s responsibilities 21813.5 The auditors’ responsibilities 220

13.5.1 Planning the audit 22013.5.2 Evaluating the entity’s assessment of going concern 22113.5.3 Period covered by auditors’ review 22313.5.4 Events after the period considered by those charged

with governance 225

xi

Contents

13.6 Audit conclusions and reporting 22513.6.1 Entity considered not to be a going concern 22513.6.2 Inadequate disclosures 22613.6.3 Those charged with governance not taking adequate

steps 22613.6.4 Material uncertainty 22613.6.5 Example report extracts 227

13.7 Regulated entities 23513.8 Groups 23513.9 Preliminary announcements 23513.10 Bulletin 2008/10 235

13.10.1 The need for guidance 23513.10.2 General principles 23513.10.3 Detailed considerations 23613.10.4 Availability of finance 23713.10.5 Smaller companies 23813.10.6 Ethical issues 238

14 Other information in documents containing audited financialstatements 239

14.1 Introduction 23914.2 Auditing Standards 23914.3 ISA (UK and Ireland) 720 24014.4 Auditors’ responsibility 24014.5 Auditors’ consideration of other information 241

14.5.1 Misstatements 24214.5.2 Inconsistencies 24214.5.3 Matters of fact and judgement 243

14.6 Access to information 24414.7 Electronic publication 24414.8 Statutory Instrument 2005/1011 244

15 Corporate governance 24715.1 Background 24715.2 Guidance 24915.3 Terms of engagement 25115.4 Statement of auditors’ responsibilities 25315.5 Auditors’ responsibilities for the ‘Comply or Explain’

statement 25415.6 Procedures 254

15.6.1 General procedures 25515.6.2 Non-compliance with the Code 25515.6.3 Specific procedures – the nine verifiable code

provisions 25615.6.4 Going concern 260

15.7 Other disclosures 26215.7.1 Disclosures under the FRC guidance 262

xii

Contents

15.7.2 Disclosures under the ‘Disclosure Rules andTransparency Rules’ 262

15.7.3 Changes to the Listing Regime 26515.8 Other matters 265

15.8.1 Assurance on internal control 26515.8.2 Directors’ remuneration 26715.8.3 Independent non-executives 26915.8.4 Other matters 269

15.9 Communication between external auditors and auditcommittees 27015.9.1 Understanding the audit committee role 27015.9.2 Designing communication to complement the audit

committee role 27015.9.3 Communicating plans for conducting the audit 27115.9.4 Private communication between the auditors and

audit committee 27115.9.5 Communicating audit findings 271

15.10 Providing assurance on internal control 27115.10.1 Background 27115.10.2 Framework 27215.10.3 Providing assurance 27315.10.4 Narrative reports 274

15.11 Effective communication between audit committees andexternal auditors 27915.11.1 Introduction 27915.11.2 Establishing the expectations of both parties 27915.11.3 The scope of the audit 28015.11.4 Findings from the audit 28015.11.5 The independence of the auditors 282

15.12 The Power of Three 28215.13 ICAEW guidance booklets 283

15.13.1 Working with your auditors 28315.13.2 Company reporting and audit requirements 28315.13.3 Reviewing auditor independence 28415.13.4 Evaluating your auditors 28415.13.5 Monitoring the integrity of financial statements 28415.13.6 The internal audit function 28515.13.7 Whistle-blowing arrangements 285

16 Review of interim reports 28716.1 Introduction 28716.2 Guidance for auditors 28716.3 General principles 28716.4 Assurance provided 28816.5 Engagement letters 28816.6 Planning 29016.7 Procedures and evidence 291

xiii

Contents

16.8 Documentation 29316.9 Subsequent events 29316.10 Going concern 29316.11 Comparative periods 29316.12 Management representations 29416.13 Other information 29416.14 Evaluating misstatements 29616.15 Communication 29616.16 Reporting 297

16.16.1 Modification of the review report 29816.16.2 Prior period modifications 29916.16.3 Date of review report 299

16.17 Complete set interim financial information 29916.18 Requests to discontinue an interim review engagement 300

17 Planning 30117.1 Auditing Standards 30117.2 Planning the work 30117.3 Preliminary engagement activities 30217.4 The overall audit strategy 30217.5 Documentation 30517.6 Initial audit engagements 30517.7 Changes to planning decisions during the course of the audit 30617.8 Direction, supervision and review 30617.9 Communications with those charged with governance 306

18 Materiality and the audit 30718.1 Auditing Standards 30718.2 Materiality 30718.3 The need to consider materiality 30818.4 Materiality and audit risk 30918.5 Revision to materiality assessments 30918.6 Uncorrected misstatements 310

18.6.1 During the audit 31018.6.2 At the completion phase 311

18.7 Documentation 31118.8 Communication of errors 31118.9 Written representations 312

19 Documentation 31319.1 Auditing Standards 31319.2 Purpose of documentation 31319.3 Form and content 314

19.3.1 Documenting characteristics of items tested 31619.3.2 Judgement areas 31619.3.3 Documentation of departures from ISAs (UK and

Ireland) 317

xiv

Contents

19.3.4 Identification of the preparer and reviewer ofdocumentation 317

19.4 Assembly of the final audit file 31719.5 Changes to audit documentation 31819.6 Confidentiality, custody and ownership of working papers 31819.7 Access to working papers 319

19.7.1 Work paper ownership and access 32019.7.2 Further explanations 32819.7.3 Access for other parties 32819.7.4 Investigating accountants from the same firm as the

auditors 331

20 Quality control for audit work 33320.1 Introduction 33320.2 Guidance 33320.3 ISQC (UK and Ireland) 1: Quality Control for Firms that

Perform Audits and Reviews of Historical FinancialInformation, and Other Assurance and Related ServicesEngagements 33420.3.1 Basic requirement 33420.3.2 Elements of a system of quality control 33420.3.3 Leadership 33520.3.4 Ethical requirements 33520.3.5 Client acceptance and continuance 33520.3.6 Human resources 33620.3.7 Engagement performance 33720.3.8 Engagement documentation 33920.3.9 Monitoring 34020.3.10 Complaints 34120.3.11 Documentation of quality control system 341

20.4 ISA (UK and Ireland) 220, Quality Control for Audits ofHistorical Financial Information 34120.4.1 General requirement 34120.4.2 Engagement partner responsibilities 342

20.5 Conflicts of interest 34220.5.1 Chinese Walls 343

20.6 Audit quality 34320.7 FRC Discussion Paper: Promoting Audit Quality 344

20.7.1 Background 34420.7.2 Audit quality 34520.7.3 Factors outside auditors’ control 346

20.8 The Audit Quality Framework 346

21 Engagement letters 34921.1 Auditing Standards 34921.2 Purpose 34921.3 Preconditions for an audit 350

xv

Contents

21.4 Contents 35121.4.1 Recurring audits 35421.4.2 Groups of companies 35521.4.3 Changes in terms 355

21.5 Liability limitation 35621.5.1 FRC guidance 35621.5.2 Background 35621.5.3 Liability limitation agreements 356

PART 3 ACCOUNTING SYSTEMS AND INTERNALCONTROLS

22 Audit risk assessment 36122.1 Guidance 36122.2 General overview 36122.3 ISA (UK and Ireland) 315 363

22.3.1 Guidance 36322.3.2 Background 36322.3.3 Risk assessment procedures 36422.3.4 Understanding the entity, its environment and

internal control 36622.3.5 Internal control 37022.3.6 Assessing the risks of material misstatement 37622.3.7 Communicating with those charged with governance 37822.3.8 Documentation 378

22.4 ISA (UK and Ireland) 330 37822.4.1 Overall responses 37922.4.2 Responses at the assertion level 37922.4.3 Presentation and disclosure 38322.4.4 Evaluating audit evidence 38422.4.5 Documentation 384

22.5 Auditing in an economic downturn 38422.5.1 Introduction 38422.5.2 The use of judgement 38522.5.3 Factors affecting financial reporting 38522.5.4 Warning signs 38622.5.5 Auditors’ actions 386

23 Auditing in an information systems environment 38923.1 Existing guidance 38923.2 Background 38923.3 Skills and competence 38923.4 Planning 39023.5 Assessment of risk 39123.6 Audit procedures 39123.7 Computer-assisted audit techniques 391

xvi

Contents

PART 4 EVIDENCE

24 Audit evidence 39524.1 Auditing Standards 39524.2 ISA (UK and Ireland) 500 395

24.2.1 Concept of audit evidence 39524.2.2 Sufficient appropriate evidence 39624.2.3 Using assertions to gather audit evidence 39724.2.4 Audit procedures 398

24.3 ISA (UK and Ireland) 501 40024.3.1 Attendance at stocktaking 40024.3.2 Enquiries about litigation and claims 40124.3.3 Segment information 401

24.4 ISA (UK and Ireland) 505 40224.4.1 Use of external confirmations 402

25 Analytical procedures 40525.1 Auditing Standards 40525.2 What is meant by analytical procedures? 40525.3 Problems in practice 40625.4 Use of analytical procedures in risk assessment 40725.5 Analytical procedures as a substantive procedure 408

25.5.1 Suitability of using analytical procedures 40825.5.2 Reliability of data 40925.5.3 Precision of expected results 40925.5.4 Acceptable differences 409

25.6 Analytical procedures in the overall review at the end of theaudit 410

25.7 Investigating unusual items 41025.8 Recording 411

26 The audit of FRS 17 41326.1 Background 41326.2 Guidance 41326.3 Respective responsibilities 41426.4 Planning 414

26.4.1 Risks of material misstatement 41526.4.2 Communication 41726.4.3 Materiality 418

26.5 Audit evidence 41926.5.1 Understanding the schemes involved 41926.5.2 Scheme assets 41926.5.3 Using the work of the scheme auditors 42026.5.4 Multi-employer schemes 42026.5.5 Scheme liabilities 42126.5.6 Competence and objectivity of the actuary 42126.5.7 The actuary’s work as audit evidence 421

xvii

Contents

26.5.8 Actuarial assumptions 42226.5.9 Assessing the results of the actuary’s work 42226.5.10 Valuation of scheme liabilities and materiality 42326.5.11 Disclosures 42426.5.12 Going concern 42426.5.13 Recognition in the profit and loss account and the

STRGL 42426.5.14 Expected return on scheme assets and discount rate 42526.5.15 Disclosures 42626.5.16 Distributable profits 42626.5.17 Management representations 427

26.6 Smaller entities with insured schemes 427

27 Audit of accounting estimates 42927.1 Auditing Standards 42927.2 Accounting estimates 42927.3 Assessing the risk of audit estimates 43027.4 Audit procedures 431

27.4.1 Testing management’s methods 43227.5 Evaluation of results 43327.6 Disclosure 433

28 Auditing fair value 43528.1 Introduction 43528.2 Guidance 43528.3 Understanding the entity’s process 43628.4 Evaluating the entity’s approach 43728.5 Using the work of an expert 43828.6 Audit procedures 438

28.6.1 Testing the entity’s assumptions, model and data 43928.6.2 Independent fair value estimates 44028.6.3 Subsequent events 440

28.7 Disclosures 44128.8 Communication with those charged with governance 44128.9 Practice Note 23 (Revised) 441

28.9.1 Background 44128.9.2 Complex financial instruments 44128.9.3 Responsibilities 44228.9.4 Understanding the entity 44328.9.5 Reliance on controls 44428.9.6 Audit procedures 44528.9.7 Evaluating audit evidence 44728.9.8 Management representations 44828.9.9 Considerations in difficult market conditions 448

29 Audit sampling 45129.1 Auditing Standards 451

xviii

Contents

29.2 Use of sampling 45129.3 Risk assessment 452

29.3.1 Sampling risk 45229.3.2 Non-sampling risk 453

29.4 Design of the sample 45329.4.1 Deciding whether to sample 45329.4.2 Designing the sample 454

29.5 Sample size 45529.6 Selecting the sample 45729.7 Performing audit procedures 45729.8 Errors 457

29.8.1 Tolerable misstatement 45829.8.2 Expected error 45829.8.3 Projecting errors 458

29.9 Evaluating results 45929.10 Statistical and non-statistical sampling 460

30 Management representations 46330.1 Auditing Standards 46330.2 Requirement to obtain written confirmation 46330.3 Acknowledgement of directors’ responsibility 46430.4 Representations by management as audit evidence 46530.5 Contradictory audit evidence 46630.6 Basic elements of a management representation letter 46630.7 Refusal to provide written confirmation 46730.8 Audit 4/02: Management Representation Letters, Explanatory

Note 46830.8.1 The case 46830.8.2 Increasing the usefulness of representation letters as

audit evidence 469

31 Opening balances and comparatives 47131.1 Auditing Standards 47131.2 Auditors’ responsibilities 47131.3 Opening balances 472

31.3.1 Continuing auditors 47331.3.2 Incoming auditors 473

31.4 Comparatives 47531.4.1 Qualified reports 476

31.5 Incoming auditors – comparatives 480

32 Related parties 48132.1 Introduction 48132.2 Auditing Standards 48232.3 General requirement 48232.4 Materiality 48332.5 Existence and disclosure of related parties 484

xix

Contents

32.5.1 Responses to assessed risks 48432.6 Evidence 48732.7 Materiality 48832.8 Control disclosures 48832.9 Representations from those charged with governance 48832.10 Communication with those charged with governance 48832.11 Documentation 48932.12 Reporting 48932.13 The audit of related parties in practice 490

32.13.1 Introduction 49032.13.2 The five point action plan 490

32.14 Improving the auditing of entities under common control 49232.14.1 Introduction 492

33 Other information in documents containing financialstatements 493

33.1 Introduction 49333.2 ISA (UK and Ireland) 720, Section A 493

33.2.1 Scope 49333.2.2 Reading other information 49433.2.3 Material inconsistencies 49433.2.4 Material misstatement of fact 495

33.3 ISA (UK and Ireland) 720, Section B 49533.3.1 Guidance 49533.3.2 Procedures 49633.3.3 Inconsistencies 496

34 Subsequent events 49734.1 Introduction 49734.2 Auditing Standards 49734.3 Before the date of the audit report 49834.4 Before the financial statements are issued 49934.5 Revising or withdrawing financial statements 500

35 The audit of small business 50135.1 Introduction 50135.2 Existing guidance 50135.3 Characteristics of small businesses 50235.4 The relationship between small businesses and their auditors 50235.5 Responsibilities 503

35.5.1 SAS 110 Fraud and error/ISA (UK and Ireland) 240The Auditor’s Responsibility to Consider Fraud in anAudit of Financial Statements 503

35.5.2 SAS 120 Consideration of Law and Regulations/ISA(UK and Ireland) 250 Part A Consideration of Lawsand Regulations in an Audit of Financial Statements 504

xx

Contents

35.5.3 SAS 130 The Going Concern Basis in FinancialStatements/ISA (UK and Ireland) 570 Going Concern 504

35.5.4 SAS 140 Engagement Letters/ISA (UK and Ireland)210 Terms of Audit Engagements 504

35.5.5 SAS 150 Subsequent Events/ISA (UK and Ireland)560 Subsequent Events 505

35.6 Planning, controlling and recording 50535.6.1 SAS 200 Planning/ISA (UK and Ireland) 300

Planning an Audit of Financial Statements 50535.6.2 SAS 210 Knowledge of the Business/ISA (UK and

Ireland) 315 Understanding the Entity and itsEnvironment and Assessing the Risks of MaterialMisstatement 506

35.6.3 SAS 220 Materiality and the Audit/ISA (UK andIreland) 320 Audit Materiality 506

35.6.4 SAS 230 Working Papers/ISA (UK and Ireland) 230Documentation 507

35.6.5 SAS 240 Quality Control for Audit Work/ISA (UKand Ireland) 220 Quality Control for Audits ofHistorical Financial Information and ISQC 1 QualityControl for Firms that Perform Audits and Reviewsof Historical Financial Information, and OtherAssurance and Related Service Engagements 507

35.7 Accounting systems and internal control 50735.7.1 SAS 300 Accounting and Internal Control Systems

and Audit Risk Assessments/ISA (UK and Ireland)315 Understanding the Entity and its Environmentand Assessing the Risks of Material Misstatementand ISA (UK and Ireland) 330 The Auditor’sProcedures in Response to Assessed Risks 507

35.8 Evidence 50835.8.1 SAS 400 Audit Evidence/ISA (UK and Ireland) 500

Audit Evidence, 501 Audit Evidence – AdditionalConsiderations for Specific Items and 505 ExternalConfirmations 508

35.8.2 SAS 410 Analytical Procedures/ISA (UK andIreland) 520 Analytical Procedures 509

35.8.3 SAS 430 Audit Sampling/ISA (UK and Ireland) 530Audit Sampling and other Means of Testing 510

35.8.4 SAS 440 Management Representations/ISA (UK andIreland) 580 Management Representations 510

35.8.5 SAS 450 Opening Balances and Comparatives/ISA(UK and Ireland) 510 Initial Engagements – OpeningBalances and Continuing Engagements – OpeningBalances and ISA (UK and Ireland) 710Comparatives 510

xxi

Contents

35.8.6 SAS 460 Related Parties/ISA (UK and Ireland) 550Related Parties 511

35.9 Reporting 51135.9.1 SAS 600 Auditors’ Reports on Financial Statements/

ISA (UK and Ireland) 700 The Auditor’s Report onFinancial Statements 511

35.9.2 SAS 610 Reports to Directors or Management/ISA(UK and Ireland) 260 Communication of AuditMatters with those Charged with Governance 511

35.10 Practice Note 26 51235.10.1 Background 51235.10.2 The purpose of audit documentation 51235.10.3 Special considerations for smaller entities 51235.10.4 Audit documentation requirements in the ISAs (UK

and Ireland) 51535.10.5 Assembling the final audit file 51535.10.6 Exposure Draft 515

36 Bank confirmations 51736.1 Introduction 51736.2 Guidance 51736.3 Authority 51736.4 Disclaimers 51836.5 Bank confirmation process 518

36.5.1 Timing of requests 51936.5.2 Information required 51936.5.3 Type of report 52036.5.4 Where to send the request 52636.5.5 Acknowledgement letters 52736.5.6 Other issues 52736.5.7 Non-BBA Banks 527

36.6 Confirmation of ongoing facilities 52736.6.1 Procedures 52836.6.2 Level of reliance to be placed on reply 529

37 Other operational issues 53137.1 Introduction 53137.2 Debtors’ confirmations 53137.3 Pending legal matters 53337.4 Paid cheques 535

37.4.1 Existing guidance 53537.4.2 Audit evidence 53637.4.3 Cheques Act 1992 53637.4.4 Obtaining paid cheques 536

37.5 Stock 53737.5.1 Introduction 53737.5.2 Assessment of risks and internal controls 537

xxii

Contents

37.5.3 Audit evidence 53837.5.4 Audit procedures before, during and after the

stocktake 53837.5.5 Work in progress 53937.5.6 The use of experts 54037.5.7 Stock held by third parties 540

37.6 Service organisations 54037.6.1 Identification and assessment 54137.6.2 Considering the responsibilities of those charged with

governance 54237.6.3 Assessing risk 54237.6.4 Designing procedures and audit evidence 54637.6.5 Fraud, non-compliance with laws and regulations and

uncorrected misstatements 54737.6.6 Reporting 547

37.7 Auditing derivative financial instruments 54737.7.1 Introduction 54737.7.2 Responsibilities 54837.7.3 Risks 55037.7.4 Types of audit procedures 55137.7.5 Materiality 55137.7.6 Other areas 551

37.8 Auditing when financial market conditions are difficult 55237.8.1 Introduction 55237.8.2 Risk assessment 55337.8.3 Going concern 55537.8.4 Fair values 55537.8.5 Disclosures in the directors’ report 55637.8.6 Auditor’s report 55637.8.7 Ethical issues 556

37.9 XBRL tagging of information in financial statements 55637.9.1 Background 55637.9.2 Auditors’ involvement 557

38 Change of auditors 55938.1 Introduction 55938.2 Statements of cessation of office 559

38.2.1 The Companies Act 2006 requirements 55938.2.2 Section 519 statements 56138.2.3 Section 522 statements 568

38.3 Access to information by successor auditors 57038.3.1 Changes introduced by the Act 57038.3.2 Technical Release AAF 01/08 571

39 Reliance on others 57939.1 Introduction 57939.2 Internal audit 579

xxiii

Contents

39.2.1 Auditing Standards 57939.2.2 Effect of internal audit on external audit procedures 57939.2.3 Understanding and assessment of internal audit 58039.2.4 Evaluating specific internal audit work 581

39.3 Other auditors 58239.3.1 Auditing Standards 58239.3.2 Definitions 58339.3.3 Acceptance as group auditors 58339.3.4 The group engagement team’s procedures 58439.3.5 Co-operation between auditors 58739.3.6 The consolidation process 58739.3.7 Reporting to those charged with governance 58839.3.8 Reporting considerations 58839.3.9 Documentation 58939.3.10 Promoting Best Practice in Group Audits 589

39.4 Experts 59339.4.1 Auditing Standards 59339.4.2 Using experts 59339.4.3 Competence and objectivity of experts 59439.4.4 The experts’ scope of work 59439.4.5 Assessing the work of experts 59539.4.6 Applying the guidance in practice 59539.4.7 Using the work of an actuary with regard to

insurance provisions 597

40 Reporting in accordance with Global InvestmentPerformance Standards (GIPS) 599

40.1 Global Investment Performance Standards (GIPS) 59940.2 Reporting in accordance with GIPS 59940.3 Engagement letters 60040.4 The reporting accountants’ review 60340.5 The reporting package 606

40.5.1 Report by the investment management firm 60640.5.2 Report by the reporting accountants 60740.5.3 Material weaknesses 609

41 Auditing in an e-commerce environment 61141.1 Introduction 61141.2 Involvement in e-commerce 61141.3 Knowledge of the business 61241.4 E-fraud 61541.5 Law and regulations 615

41.5.1 Relevant regulations 61541.5.2 Commercial law 61641.5.3 Taxation 617

41.6 Audit risk 61741.6.1 Issues relating to e-commerce 617

xxiv

Contents

41.6.2 Assessing risk 61841.6.3 Accounting risks 61941.6.4 Assessing the control environment 619

41.7 Audit evidence 62241.7.1 Difficulties in obtaining evidence 62241.7.2 Use of specialists 62241.7.3 Types of evidence 62341.7.4 Materiality 62541.7.5 Other performance indicators 62541.7.6 Work papers 625

41.8 Going concern 62541.9 Certification 626

42 Reports for special purposes and to third parties 62742.1 Introduction 62742.2 Development of guidance 62742.3 General guidance 629

42.3.1 Accepting an engagement 62942.3.2 Managing professional liability 62942.3.3 Agreeing the terms of the engagement 630

42.4 Duties to lenders 63042.4.1 Case law 63042.4.2 Duties of care for the statutory audit report 63142.4.3 Draft accounts 63242.4.4 Disclaimer of responsibility 63242.4.5 The Contracts (Rights of Third Parties) Act 1999 63342.4.6 Separate engagements to provide specific assurances

to lenders 63342.5 Covenants in agreement for loans and other facilities 634

42.5.1 The lender’s requirement for evidence of covenantcompliance 635

42.5.2 The firm’s duty of care when reporting on thedirectors’ statement of covenant compliance 636

42.5.3 The firm’s consideration of acceptance of theengagement 639

42.6 Engagements to report on covenant compliance 63942.6.1 Scope of work performed 63942.6.2 The report 640

42.7 Duties of care for non-statutory audits or reviews 64242.7.1 Background 64242.7.2 Accepting the engagement 64342.7.3 Reliance by third parties 64542.7.4 Reporting 645

42.8 Reports on internal controls of service organisations 64842.8.1 Background 64842.8.2 Responsibilities of the service organisation 64942.8.3 Accepting the engagement 650

xxv

Contents

42.8.4 Reporting accountant’s procedures 65342.8.5 Reporting 65442.8.6 ED ISAE 3402 656

42.9 Reports to other third parties 65642.9.1 Introduction 65642.9.2 Audit 1/01: Reporting to third parties 65642.9.3 Audit 2/01: Requests for references on clients’

financial status and their ability to service loans 66342.10 Assurance on non-financial information 665

42.10.1 Background 66542.10.2 Non-financial information 66542.10.3 Current practices and guidance 66642.10.4 Consideration for practitioners 667

42.11 Audit liability: claims by third parties 66942.11.1 Potential investors 67042.11.2 Creditors and lenders 67142.11.3 Regulators and trade bodies 67142.11.4 Affiliates or associates of the audit client 671

42.12 ISRS 4400 672

PART 5 SPECIALIST AUDITS

43 Charities 67543.1 Legal background 675

43.1.1 General 67643.1.2 Independent examination 67743.1.3 Whistle-blowing duties for auditors and examiners 678

43.2 Audit guidance 67843.3 Background 67943.4 ISA (UK and Ireland) 200 Objective and General Principles

Governing the Audit of the Financial Statements 67943.5 ISA (UK and Ireland) 210 Terms of Audit Engagements 68043.6 ISA (UK and Ireland) 220 Quality Control for Audits of

Historical Financial Information 68043.7 ISA (UK and Ireland) 240 The Auditor’s Responsibility to

Consider Fraud in an Audit of Financial Statements 68143.8 ISA (UK and Ireland) 250 Part A Consideration of Laws and

Regulations in an Audit of Financial Statements 68243.8.1 Laws relating directly to the preparation of financial

statements 68243.8.2 Laws central to a charity’s conduct of business 682

43.9 ISA (UK and Ireland) 250 Part B The Auditor’s Right andDuty to Report to Regulators in the Financial Sector 683

43.10 ISA (UK and Ireland) 260 Communication of Audit Matterswith those Charged with Governance 686

43.11 ISA (UK and Ireland) 300 Planning an Audit of FinancialStatements 686

xxvi

Contents

43.12 ISA (UK and Ireland) 315 Understanding the Entity and itsEnvironment and Assessing the Risks of MaterialMisstatement 68743.12.1 Inherent risk 68843.12.2 Control environment 68943.12.3 Control activities 69043.12.4 Accounting policies 693

43.13 ISA (UK and Ireland) 320 Audit Materiality 69343.14 ISA (UK and Ireland) 330 The Auditor’s Procedures in

Response to Assessed Risks 69443.15 ISA (UK and Ireland) 402 Audit Considerations Relating to

Entities using Service Organizations 69643.16 ISA (UK and Ireland) 505 External Confirmations 69743.17 ISAs (UK and Ireland) 510 Initial Engagements – Opening

Balances and Continuing Engagements – Opening Balances 69743.18 ISA (UK and Ireland) 520 Analytical Procedures 69743.19 ISA (UK and Ireland) 540 Audit of Accounting Estimates 69843.20 ISA (UK and Ireland) 545 Auditing Fair Value Measurements

and Disclosures 69843.21 ISA (UK and Ireland) 550 Related Parties 69943.22 ISA (UK and Ireland) 560 Subsequent Events 69943.23 ISA (UK and Ireland) 570 Going Concern 69943.24 ISA (UK and Ireland) 580 Management Representations 70143.25 ISA (UK and Ireland) 600 Using the Work of Another

Auditor 70143.26 ISA (UK and Ireland) 700 The Auditor’s Report on Financial

Statements 70243.27 ISA (UK and Ireland) 720 Part A Other Information in

Documents Containing Audited Financial Statements and PartB The Auditor’s Statutory Reporting Responsibility inRelation to Directors’ Reports 703

43.28 Summarised financial statements 70443.29 Audit exemption reports 705

44 Pension schemes 70744.1 Guidance for auditors of pension schemes 70744.2 Legal background 70744.3 Accounting guidance 70944.4 Schemes exempt from audit 71044.5 Consideration of fraud 71044.6 Communication with trustees 71144.7 Control activities 71244.8 Contributions 71444.9 Schemes in the process of winding up 71644.10 Other reporting situations 71744.11 ‘Whistle-blowing’ responsibilities 718

xxvii

Contents

45 Solicitors’ Accounts Rules 71945.1 Background 719

45.1.1 Objective 71945.2 Existing guidance 72145.3 Engagement letter 721

45.3.1 ‘Whistle-blowing’ 72245.3.2 Termination of appointment 72345.3.3 Independence 72345.3.4 Place of examination 724

45.4 Procedures 72445.5 Problem areas 725

45.5.1 Debit balances 72545.5.2 Client confidentiality 72545.5.3 Trivial breaches 72645.5.4 ‘Without delay’ 72645.5.5 Other areas 726

45.6 Reporting 72645.7 Checklist 727

46 Investment businesses 72946.1 Introduction 72946.2 Rules and reporting requirements 72946.3 The audit of financial statements 731

46.3.1 ISA (UK and Ireland) 200 Objective and generalprinciples governing an audit of financial statements 731

46.3.2 ISA (UK and Ireland) 210 Terms of auditengagements 731

46.3.3 ISA (UK and Ireland) 240 The auditor’sresponsibility to consider fraud in an audit offinancial statements 732

46.3.4 ISA (UK and Ireland) 250 Part A Consideration oflaws and regulations in an audit of financialstatements 732

46.3.5 ISA (UK and Ireland) 300 Planning an audit offinancial statements 734

46.3.6 ISA (UK and Ireland) 315 Understanding the entityand its environment and assessing the risks ofmaterial misstatement 734

46.3.7 ISA (UK and Ireland) 330 The auditor’s proceduresin response to assessed risks 735

46.3.8 ISA (UK and Ireland) 402 Audit considerationsrelating to entities using service organizations 736

46.3.9 ISA (UK and Ireland) 520 Analytical Procedures 73746.3.10 ISA (UK and Ireland) 540 Audit of Accounting

Estimates 73746.3.11 ISA (UK and Ireland) 545 Auditing Fair Value

Measurements and Disclosures 737

xxviii

Contents

46.3.12 ISA (UK and Ireland) 570 Going concern 73846.3.13 ISA (UK and Ireland) 580 Management

representations 73846.3.14 ISA (UK and Ireland) 700 The auditor’s report on

financial statements 73946.4 High level standards and conduct of business rules 739

46.4.1 Impact on the audit 73946.4.2 Audit approach 740

46.5 Review reports on interim profits 74146.6 CREST 744

46.6.1 Understanding the business 74446.6.2 Evaluating internal controls 74546.6.3 Detailed audit procedures 745

47 Registered providers of social housing 74747.1 Existing audit guidance 748

47.1.1 Practice Note 14 74847.1.2 Regulatory Circulars and Good Practice Notes 749

47.2 Background 75047.2.1 The nature of Registered Providers of Social Housing 75047.2.2 Responsibilities of the Board or the Committee of

Management 75247.2.3 Responsibilities of audit committees 75247.2.4 Financial reporting requirements 75347.2.5 Responsibility of auditors 75547.2.6 Features of social housing audits 75547.2.7 The auditors’ relationship with the Regulators 759

47.3 ISA (UK and Ireland) 210: Terms of Audit Engagements 75947.4 ISA (UK and Ireland) 220: Quality Control for Audits of

Historical Financial Information 76547.5 ISA (UK and Ireland) 240: The Auditor’s Responsibility to

Consider Fraud in an Audit of Financial Statements 76547.6 ISA (UK and Ireland) 250: Consideration of Laws and

Regulations in an Audit of Financial Statements 76647.7 ISA (UK and Ireland) 260: Communication of Audit Matters

with those Charged with Governance 76747.8 ISA (UK and Ireland) 300: Planning an Audit of Financial

Statements 76847.9 ISA (UK and Ireland) 315: Understanding the Entity and its

Environment and Assessing the Risks of MaterialMisstatement 769

47.10 ISA (UK and Ireland) 320: Audit Materiality 77047.11 ISA (UK and Ireland) 330: The Auditor’s Procedures in

Response to Assessed Risks 77047.12 ISA (UK and Ireland) 402: Audit Considerations Relating to

Entities Using Service Organisations 77147.13 ISA (UK and Ireland) 500: Audit Evidence 772

xxix

Contents

47.14 ISA (UK and Ireland) 505: External Confirmations 77247.15 ISA (UK and Ireland) 520: Analytical Procedures 77347.16 ISA (UK and Ireland) 540: Audit of accounting estimates 77447.17 ISA (UK and Ireland) 545: Auditing Fair Value

Measurements and Disclosures 77447.18 ISA (UK and Ireland) 550: Related Parties 77547.19 ISA (UK and Ireland) 560: Subsequent Events 77547.20 ISA (UK and Ireland) 570: Going Concern 77647.21 ISA (UK and Ireland) 580: Management Representations 77747.22 ISA (UK and Ireland) 610: Considering the Work of Internal

Audit 77747.23 ISA (UK and Ireland) 620: Using the Work of an Expert 77847.24 ISA (UK and Ireland) 700: The Independent Auditor’s Report

on a Complete Set of General Purpose Financial Statements 77847.25 ISA (UK and Ireland) 720: Other Information in Documents

Containing Audited Financial Statements 78147.26 Miscellaneous reports 78247.27 Service charge audits 782

48 Public sector audits 78548.1 Introduction 78548.2 The role of the public sector auditor 786

48.2.1 Auditor responsibilities 78648.2.2 Financial statements 78748.2.3 Regularity 78748.2.4 Other assignments 788

48.3 Standards governing public sector audits 78848.4 International Standard on Quality Control (UK and Ireland) 1 78948.5 ISA (UK and Ireland) 200 Objective and General Principles

Governing an Audit of Financial Statements 78948.6 ISA (UK and Ireland) 210 Terms of Audit Engagements 79048.7 ISA (UK and Ireland) 220 Quality Control for Audits of

Historical Financial Information 79048.8 ISA (UK and Ireland) 230 Documentation 79048.9 ISA (UK and Ireland) 240 The Auditor’s Responsibility to

Consider Fraud in an Audit of Financial Statements 79048.9.1 Responsibilities of the entity and auditors 79148.9.2 Fraud in the context of the regularity assertion 79148.9.3 Consideration of fraud risk factors 79248.9.4 Auditors’ other responsibilities 79248.9.5 Reporting to third parties 793

48.10 ISA (UK and Ireland) 250 Consideration of Laws andRegulations in an Audit of Financial Statements 793

48.11 ISA (UK and Ireland) 260 Communication of Audit Matterswith those Charged with Governance 794

48.12 ISA (UK and Ireland) 300 Planning an Audit of FinancialStatements 795

xxx

Contents

48.13 ISA (UK and Ireland) 315 Understanding the Entity and itsEnvironment and Assessing the Risks of MaterialMisstatement and ISA (UK and Ireland) 330 The Auditor’sProcedures in Response to Assessed Risks 795

48.14 ISA (UK and Ireland) 320 Audit Materiality 79648.15 ISA (UK and Ireland) 402 Audit Considerations Relating to

Entities Using Service Organisations 79748.16 ISA (UK and Ireland) 500 Audit Evidence 79748.17 ISA (UK and Ireland) 510 Initial Engagements – Opening

Balances and Continuing Engagements – Opening Balances 79748.18 ISA (UK and Ireland) 520 Analytical Procedures 79848.19 ISA (UK and Ireland) 550 Related Parties 79948.20 ISA (UK and Ireland) 560 Subsequent Events 79948.21 ISA (UK and Ireland) 570 Going Concern 800

48.21.1 Auditors’ other responsibilities relating to goingconcern 800

48.21.2 Entities that prepare their financial statements on thegoing concern basis 800

48.21.3 Circumstances affecting going concern 80148.21.4 Consideration of the foreseeable future 80148.21.5 Auditors’ responsibilities in considering going

concern 80148.21.6 Written representations on going concern 801

48.22 ISA (UK and Ireland) 580 Management Representations 80248.23 ISA (UK and Ireland) 600 Using the Work of Another

Auditor 80248.24 ISA (UK and Ireland) 610 Considering the Work of Internal

Audit 80348.25 ISA (UK and Ireland) 700 The Auditor’s Report on Financial

Statements 80348.26 ISA (UK and Ireland) 720 Other Information in Documents

Containing Audited Financial Statements 80448.27 Corporate Governance 805

48.27.1 Central government 80548.27.2 National Health Service bodies 81048.27.3 Local government bodies 812

48.28 Grant claims 81348.28.1 Background 81348.28.2 Terms of engagement 81448.28.3 Types of engagement 82448.28.4 Reporting 82548.28.5 Access to accountants’ working papers 825

48.29 Bulletin 2008/7 82748.30 Practice Note 10 (Revised) consultation draft 828

49 Regulated entities 82949.1 Introduction 829

xxxi

Contents

49.2 Duty of care and engagement contracts 82949.2.1 Tri-partite engagement contracts 83049.2.2 Bi-partite engagement contracts 837

49.3 Reporting 84649.4 Materiality 84949.5 Working with independent experts 849

50 Investment circular reporting 85150.1 Legal background 85150.2 Guidance 85150.3 Structure of the SIRs 85250.4 SIR 1000 853

50.4.1 General 85350.4.2 Acceptance and continuance 85350.4.3 Terms of the engagement 85350.4.4 Independence and ethical standards 85450.4.5 Legal and regulatory requirements 85450.4.6 Quality control 85450.4.7 Planning and execution 85550.4.8 Documentation 85650.4.9 Professional scepticism 85650.4.10 Reporting 85650.4.11 Modified opinions 85750.4.12 Pre-existing financial information 85750.4.13 Consent 85750.4.14 Events after the reporting accountant’s report 859

50.5 SIR 2000 85950.5.1 General 85950.5.2 True and fair view 86050.5.3 Professional considerations 86150.5.4 Planning 86150.5.5 Understanding the entity and risk assessment 86250.5.6 Materiality 86250.5.7 Reporting accountant’s procedures 86250.5.8 Access to audit work papers 86350.5.9 Post balance sheet events 86350.5.10 Going concern 86450.5.11 Representations 86450.5.12 Joint reporting accountants 86450.5.13 Reporting 864

50.6 SIR 3000 86650.6.1 General 86650.6.2 Compilation process 86750.6.3 Agreeing the terms of the engagement 86850.6.4 Planning and performing the engagement 86950.6.5 Materiality 87050.6.6 Historical financial information 870

xxxii

Contents

50.6.7 Consistent accounting policies 87150.6.8 Presentation of the profit forecast 87150.6.9 Representation letter 87250.6.10 Reporting 87250.6.11 Consent 874

50.7 SIR 4000 87550.7.1 General 87550.7.2 Agreeing the terms of the engagement 87550.7.3 Planning and performing the engagement 87650.7.4 Materiality 87750.7.5 Presentation of the pro forma financial information 87750.7.6 Reporting 877

50.8 SIR 5000 87950.8.1 General 87950.8.2 Accepting the engagement 88050.8.3 Planning and performing the engagement 88150.8.4 Reporting 884

50.9 Ethical Standards for Reporting Accountants 88650.10 Limiting risks for reporting accountants 887

50.10.1 Background 88750.10.2 Inclusion of a statutory audit report in an investment

circular 88850.10.3 Special purpose reports 88950.10.4 Other financial information 88950.10.5 Addressing the report 889

Appendix: existing guidance at 30 April 2010 891

Index 903

xxxiii

PREFACE

From a UK GAAS perspective the major event of the year was clearly thepublication in October 2009 of the revised ISAs for UK and Ireland whichcomprised:

● 33 new International Standards on Auditing (UK and Ireland) (ISAs (UKand Ireland));

● A new International Standard on Quality Control (UK and Ireland) 1 (ISQC(UK and Ireland) 1); and

● A revised Statement of the Scope and Authority of APB Pronouncements.

This represents the culmination of the UK part of the IAASB’s Clarity Projectwhich reformatted the 33 standards in a ‘clarified’ form and also revised anumber to update them for changes in the business environment and for currentthinking. These were issued as exposure drafts in April 2009 and were referredto in last year’s edition, and incorporated as UK standards with very littlechange.

Because, for all intents and purposes the first audits required under the newstandards are those for 31 December 2010 year ends, this is a year of transitionin the UK as firms adjust their procedures and methodologies ready for thisdeadline. Therefore, we have taken the approach in this book of setting out theexisting pre-clarification requirements and showing what the changes will be aswe consider this is of most help to those coping with the new standards.

The expansion of the Statement of the Scope and Authority of APBPronouncements reflects the fact that standards are now in one of two kinds –the old-fashioned black-lined versions – requirements indicated by ‘should’ –which includes the Engagement Standards for Reporting Accountants and theEthical Standards for Auditors and Reporting Accountants as opposed to theclarified standards which use the international conventions of no black-liningand requirements indicated by ‘shall’. Whilst for the moment this should notpresent too many practical problems in the longer term it will prove unwieldy.

The question of whether the EU will adopt the standards is still an open one.Recent changes in both the European Parliament and in the EuropeanCommission have meant that the anticipated progress has not taken place andindeed there is now some doubt as to whether IAS will be eventuallyincorporated in European law. Whilst in the short term this will have no realeffect for the UK, for the longer term it raises the spectre of the EU developingits own rules as the PCOAB has done in the US. This would only lead toincreased complexity for multi-national audits.

As far as the future is concerned, the aftermath of the financial crisis hasproduced a number of voices calling for a fresh look at the audit function. It islikely attention will be focused particularly on the scope of audit reporting andwhether this can be developed to give additional assurance on such matters asvaluations and risk disclosures, both of which have become of increasingimportance in companies’ annual reports. These have traditionally been areas

xxxv

Preface

which auditors have been reluctant to go into because of potential liabilityissues, so it will be interesting to see whether any progress can be made here.

The other main developments in the UK for which we have updated the bookinclude:

● PN 26 – Audit documentation for a smaller entity

● Draft PN 10 (revised) – Money laundering – Guidance for Auditors

● Draft PN 10 – Audits in the Public Sector

● Bulletin 2009/3 – Audits of Charities in the UK – updated reports

● Bulletin 2009/4 – Guidance on Going Concern

● ES3 (revised) – Long association with the audit engagement.

As with earlier editions, we have kept to our conventions of:

● where there is an existing guideline in an area and a proposed Standard orPractice Note, we have, unless indicated in the text, examined the subjectfrom the point of view of the proposal on the basis that it is a moreauthoritative and up-to-date indication of GAAS;

● international standards and other overseas guidance are discussed in detailwhen they have been exposed by the APB in a national context although weindicate the main effects of significant proposals, and

● where new Standards have been issued but in a number of cases the oldguidelines have not been withdrawn, we have ignored the old guidelinesexcept where they have provided helpful insights.

Finally, we would like to acknowledge the contributions of Chris Kirton, DonBawtree, Peter Lewis, Philip Rego, Nick Carter-Pegg and Fiona Raistrick whohave helped in the drafting of various chapters. Their help has been invaluable.

Peter Chidgey

Sarah Nendick

BDO LLP

May 2010

xxxvi

3 THE AUDIT REPORT

3.1 INTRODUCTION

This Chapter examines the auditor’s report on the annual financial statements ofa company reporting in accordance with the Companies Act 2006. Modificationsto the auditor’s report are discussed in Chapter 4. Other Companies Act reportson annual financial statements are considered in Chapter 5, while other reportsunder the Companies Act are considered in Chapter 6 and reports to the FSA oninvestment businesses in Chapter 8. Reports on accounts prepared byaccountants are considered in Chapter 7.

3.2 THE STANDARDS

The current version of ISA 700 The Auditor’s Report on Financial Statementswas issued in October 2009 and provides standards on reporting covering:

● the aim of the audit report;● the contents of the audit report; and● modified reports.

The process of updating ISA 700 was removed from the introduction of revisedISAs (UK and Ireland) based on the IAASB’s Clarity Project because of theenactment of the Companies Act 2006. The revision to ISA (UK and Ireland)700 was published in March 2009, and reissued without further amendment inOctober 2009 as part of the suite of final clarified standards. Like the clarifiedstandards, ISA (UK and Ireland) 700 is effective for the audit of financialstatements for periods ending on or after 15 December 2010.

The main changes in the revision to ISA (UK and Ireland) 700 are set out in 3.3.

One of the changes made by the Companies Act 2006 is to require that auditreports are signed by the ‘Senior Statutory Auditor’. This is effective forfinancial periods beginning on or after 6 April 2008 and is further explained in3.12 below. In April 2008, the APB issued Bulletin 2008/6, The ‘SeniorStatutory Auditor’ under the United Kingdom Companies Act 2006 which setsout the role of the Senior Statutory Auditor and provides relevant sign offwordings for auditor’s reports. The example reports in this chapter andthroughout this publication that require a revised sign off for accounting periodscommencing on or after 6 April 2008 have been updated accordingly. Foraccounting periods before this date, reference should be made to earlier editionsof this publication.

47

3. The Audit Report

3.2.1 Other guidance

In ISA (UK and Ireland) 700, the APB refers readers to ‘the most recent versionof the APB Bulletin, Auditor’s Reports on Financial Statements in the UnitedKingdom’ for example company reports. The most recent version is Bulletin2009/2 which was released in April 2009 in response to the publication of ISA(UK and Ireland) 700 the previous month. Examples in this chapter have beenupdated in line with the recommendations of that Bulletin. The examples in theBulletin are effective for periods beginning on or after 6 April 2008 and endingon or after 5 April 2009.

In January 2001 the APB issued two bulletins in response to the changing focuson auditors’ reports as a result of the increasing use of the Internet as a mediumfor publishing financial material. Bulletins 2001/1 The Electronic Publication ofAuditors’ Reports and 2001/2 Revisions to the Wording of Auditors’ Reports onFinancial Statements and the Interim Review Report are considered in section3.18 below. The example audit reports in this chapter, and throughout the book,take into account these Bulletins. The issue of FRS 18 Accounting Policiesprompted the APB to issue Bulletin 2000/3 as guidance to auditors on theapplication of SAS 600 when reporting on financial statements which fall withinthe scope of a Statement of Recommended Practice (SORP), but contain adeparture from the SORP’s requirements. This guidance is still relevantfollowing the publication of the updated ISA (UK and Ireland) 700.

The Director’s Remuneration Report Regulations 2002 (‘the Regulations’) cameinto force on 1 August 2002. The Regulations require certain public companiesto produce a Remuneration Report containing detailed information aboutdirectors’ remuneration for periods ending on or after 31 December 2002. Someof the information specified for inclusion is to be audited, and auditors muststate in their report whether the ‘auditable part’ of the Directors’ RemunerationReport has been properly prepared in accordance with the Companies Act 1985.Reports in this Chapter for relevant listed companies have been updated inaccordance with the guidance in the related APB Bulletin, 2002/2, The UnitedKingdom Directors’ Remuneration Report Regulations 2002, which waspublished in October 2002. Details of the Bulletin are given in 3.17 below.

In January 2003 the Audit and Assurance Faculty of the ICAEW issuedTechnical Release Audit 1/03, The Audit Report and Auditors’ Duty of Care toThird Parties following an earlier judgement in the Scottish courts, Royal Bankof Scotland v Bannerman Johnstone Maclay and others (‘Bannerman’). The aimof 1/03 is to assist auditors in managing the risk of inadvertently assuming aduty of care to third parties in relation to their audit reports. Further details arediscussed in 3.20.

In April 2006, the Audit and Assurance faculty of the ICAEW issued AAF02/06, Identifying and managing certain risks arising from the inclusion ofreports from auditors and accountants in prospectuses (and certain other

48

Aim of the Audit Report

investment circulars). This publication develops the principles in 01/03 forreporting accountants. It is detailed in 50.9.

3.3 ISA (UK AND IRELAND) 700 (REVISED)

3.3.1 Main changes

As a result of the consultation process which followed the APB’s The AuditReport: A time for change? paper issued in December 2007, the two main areaswhere change was requested were:

● a shorter auditor’s report; and● making the report more informative.

Reducing the length of the audit report has been achieved in the new ‘Statementof the Scope of an Audit’ section, discussed in 3.10 below, as well as byreducing the length of the description of the auditor’s responsibilities.

The APB is of the opinion that wholesale changes to make the auditor’s reportmore informative is best coordinated on an international basis through the workof the IAASB. However, there is increased guidance in the updated ISA (UKand Ireland) relating to the ability of auditors to highlight matters which theyregard as relevant to a proper understanding of their work as additionalcomments in their report.

3.3.2 Discussions with those charged with governance

The APB recommends that auditors discuss the changes to their reports withthose charged with governance. The ISA (UK and Ireland) sets out the followingareas as ones of particular interest:

● the advantages and disadvantages of the various alternative approaches tothe description of the scope of the audit, permitted by ISA (UK and Ireland)700; and

● matters that auditors may wish to include in the auditor’s report under theheading ‘Other Matter’.

3.4 AIM OF THE AUDIT REPORT

The aim of the report is to provide information to the reader on the respectiveresponsibilities of the directors and the auditors and information on what anaudit entails.

ISA (UK and Ireland) 700 requires that auditors’ reports should contain a clearexpression of opinion based on review and assessment of the conclusions drawn

49

3. The Audit Report

from evidence obtained in the course of the audit. The other standards expandthis basic principle.

The auditor should evaluate whether:

● the financial statements adequately refer to or describe the relevant financialreporting framework;

● the financial statements adequately disclose the significant accountingpolicies selected and applied;

● the accounting policies selected and applied are consistent with theapplicable financial reporting framework, and are appropriate in thecircumstances;

● accounting estimates are reasonable;● the information presented in the financial statements is relevant, reliable,

comparable and understandable;● the financial statements provide adequate disclosures to enable the intended

users to understand the effect of material transactions and events on theinformation conveyed in the financial statements; and

● the terminology used in the financial statements, including the title of eachfinancial statements, is appropriate.

3.5 CONTENTS OF AN AUDIT REPORT

The ISA (UK and Ireland) requires that an audit report should contain thefollowing information:

● a title which identifies to whom the report is addressed;● an introduction that identifies the financial statements which have been

audited;● the responsibilities of those charged with governance;● the responsibilities of the auditors;● the scope of the audit of the financial statements (see 3.10 below);● the auditor’s opinions on the financial statements (see 3.11);● the manuscript signature of the Senior Statutory Auditor signing for and on

behalf of the audit firm (see 3.12);● the auditors’ address; and● the date of the auditors’ report.

The standard recommends that using a standard format with appropriateheadings will help the user to understand the report. However, it also points outthat the report should reflect the particular assignment.

50

Respective Responsibilities of those Charged with Governance and Auditors

3.6 TITLE

The term ‘Independent Auditor’ is usually used in the title in order to distinguishthe report from reports that might be issued by others who have not compliedwith the APB’s Ethical Standards for Auditors (see Chapter 2).

3.7 ADDRESSEE

Where the auditors are reporting on a company, the report should be addressedto the members as the audit is undertaken on their behalf. For other types ofreporting entity the addressee will depend on the terms of the engagement, forexample, where the auditors are reporting on a pension fund they will addresstheir report to the trustees.

3.8 INTRODUCTORY PARAGRAPH

This section should refer to the pages of the report that contain the financialstatements and the date of, and period covered by, the financial statements, andis to ensure that there is no confusion over the subject matter of the auditors’report. Bulletin 2001/1 (see 3.18) outlines the situation where the Annual Reportis to be published electronically and the statements covered by the audit reportmay not be determined from page numbers alone. Here, auditors are required torefer explicitly to the primary statements and notes covered by the audit report.

Technical Release Audit 1/03 was issued in January 2003 to assist auditors inmanaging the risk of inadvertently assuming a duty of care to third parties inrelation to their audit reports. The Technical Release is discussed in detail insection 3.20 below.

3.9 RESPECTIVE RESPONSIBILITIES OFTHOSE CHARGED WITH GOVERNANCEAND AUDITORS

Those charged with governance have a responsibility to prepare the financialstatements and auditors are responsible for auditing and expressing an opinionon those financial statements in accordance with applicable legal requirementsand International Standards on Auditing (UK and Ireland). A paragraph in theauditor’s report should state these responsibilities clearly.

51

3. The Audit Report

3.10 SCOPE OF THE AUDIT OF THEFINANCIAL STATEMENTS

This new section was introduced by the update to ISA (UK and Ireland) 700 inMarch 2009. In an attempt to reduce the length of auditor’s reports, the reportshould now either:

● cross refer to a ‘Statement of the Scope of an Audit’ that is maintained onthe APB’s website (www.frc.org.uk/apb/scope/UKP for publicly tradedcompanies or groups, or www.frc.org.uk/apb/scope/UKNP for non-publiclytraded companies or groups);

● cross refer to a ‘Statement of the Scope of an Audit’ that is includedelsewhere within the Annual Report; or

● include the description of the scope of an audit from Table 1 below.

When the Statement of the Scope of an Audit is included elsewhere in theAnnual Report, the format in Table 1 should also be used.

TABLE 1: Statement of the Scope of an Audit to be included in the auditor’sreport

’An audit involves obtaining evidence about the amounts and disclosures in thefinancial statements sufficient to give reasonable assurance that the financialstatements are free from material misstatement, whether caused by fraud or error. Thisincludes an assessment of:

● whether accounting policies are appropriate to the [describe nature of entity]circumstances and have been consistently applied and adequately disclosed;

● the reasonableness of significant accounting estimates made by [describe thosecharged with governance]; and

● the overall presentation of the financial statements.’

3.11 AUDITOR’S OPINIONS

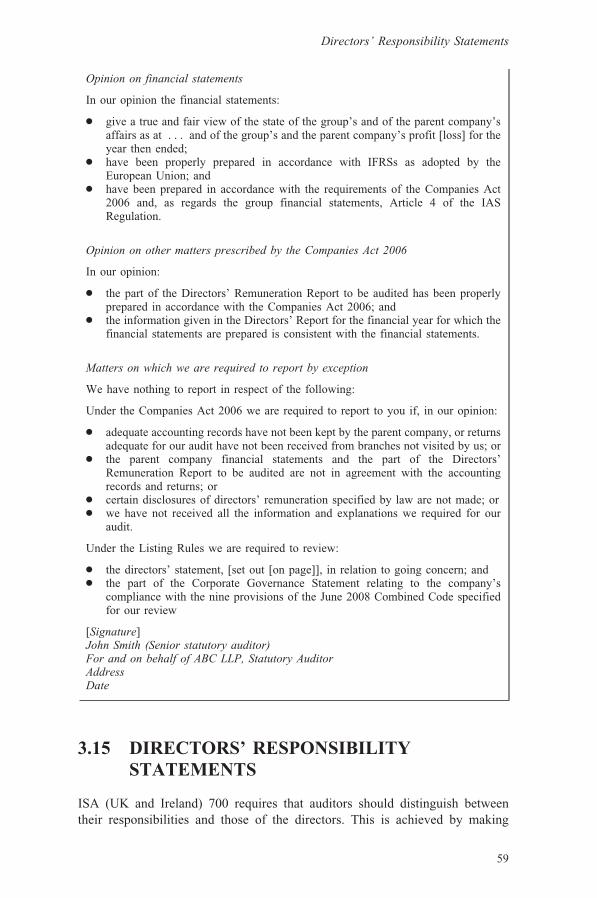

3.11.1 True and fair

ISA (UK and Ireland) 700 requires that the report should contain a clearexpression of the auditors’ opinion on the financial statements and on anyfurther requirements of statute or the particular assignment.

The opinion may be unqualified or qualified. Qualifications are considered indetail in Chapter 4.

Where the opinion is unqualified, this means that, in the auditors’ opinion, thefinancial statements give a true and fair view and have been properly prepared inaccordance with the relevant accounting framework.

52

Signature

The auditor’s opinion should indicate the financial reporting framework uponwhich the financial statements are based. In the UK these will normally be:

● International Financial Reporting Standards (IFRSs) as adopted by theEuropean Union and, for consolidated financial statements of fully listedcompanies, Article 4 of the IAS Regulation (1606/2002/EC); or

● UK Generally Accepted Accounting Practice, which comprises applicableUK Company Law and UK Accounting Standards as issued by the ASB.

Where an auditor is also required to report on compliance with a secondfinancial reporting framework, the second opinion must be clearly separated inthe opinion section by the use of a subheading.

3.11.2 Opinion on other matters

Other reporting requirements may be set out in legislation or by the terms ofengagement agreed with the entity. Such opinions may be required as:

● a positive statement in the auditor’s report (such as the opinion whether theinformation in the directors’ report is consistent with the accounts); or

● by exception (for example if the company has not maintained adequateaccounting records).

If the auditor is required to report by exception, the opinion should be givenunder the heading ‘Matters on which we are required to report by exception’. Ifthere is nothing to report by exception, the section must still be included in thereport, but would be set out in accordance with the wording stipulated in ISA(UK and Ireland) 700, which is reproduced in Table 2.

TABLE 2: Example paragraph where there is nothing to report by exception

Matters on which we are required to report by exception

We have nothing to report in respect of the following:

[give details of item to be reported on]

3.12 SIGNATURE

3.12.1 Senior Statutory Auditor

Where the auditor is a firm, the Companies Act 2006 sets out the requirementfor the Senior Statutory Auditor to sign the auditor’s report in his own name forand on behalf of the audit firm. The Auditing Practices Board was tasked withissuing guidance with respect to the term ‘Senior Statutory Auditor’ and this waspublished in April 2008 as Bulletin 2008/6, The ‘Senior Statutory Auditor’under the United Kingdom Companies Act 2006.

53

3. The Audit Report

The Senior Statutory Auditor is required to sign in his own name for reports:

● prepared in accordance with ss495, 496 and 497 of the Companies Act 2006,that is audit reports which provide a true and fair opinion;

● on voluntary revisions of annual accounts and reports (see 5.6); and● on auditor’s reports on abbreviated accounts (see 5.4).

This requirement is effective for accounting periods commencing on or after6 April 2008.

There are no legal requirements for eligibility to be appointed as a SeniorStatutory Auditor. In practical terms each partner in an audit firm previouslyauthorised to act as an engagement partner and sign the auditor’s report in thefirm’s name is likely to assume the role of Senior Statutory Auditor.

In signing auditor’s reports in their own name as the Senior Statutory Auditor,the individual does not take on any additional legal responsibility for the audit orthe report than they would previously have had prior to the Companies Act2006.

If more than one partner is involved in an audit it is important to determinewhich individual is acting as the engagement partner and therefore assumes therole of Senior Statutory Auditor.

The Bulletin suggests that it would be pragmatic for the audit firm to have acontingency plan as to who would succeed as senior statutory auditor in theevent that the audit is at an advanced stage but the senior auditor is unable tosign the auditor’s report.

If another audit partner is actively involved in the audit engagement, a suitablecontingency plan may be for that other partner to work in parallel with the seniorstatutory auditor and be able to take over as senior statutory auditor if the needarises.

If no other partner has worked in parallel with the senior statutory auditor, thenthe APB is of the view that in such exceptional circumstances it is permissiblefor the engagement quality control reviewer to be appointed as the replacementsenior statutory auditor where:

● the engagement quality control reviewer has completed his or her review;and

● the audit is at an ‘advanced stage’ as defined by Bulletin 2008/2 which dealswith the auditor’s association with preliminary announcements.

This is subject to the condition that the engagement quality control reviewer iseligible to be appointed as the senior statutory auditor.

Once an engagement quality reviewer has been appointed as a replacementsenior statutory auditor he or she can no longer act as the engagement quality

54

Date

control reviewer because his or her objectivity may have been impaired throughassuming the role of senior statutory auditor.

3.12.2 Signing

The requirements of the Companies Act 2006 for the Senior Statutory Auditor tophysically sign the auditors’ report in their own name, extends only to the copyof the auditors’ report to be provided to the client upon completion of the audit.In all but this ‘signing copy’, the name of the Senior Statutory Auditor needs tobe stated, but the signature does not need to be reproduced. The copy of theauditor’s report sent to the Registrar of Companies only requires the name of theSenior Statutory Auditor to be stated, not their signature, together with asignature in the name of the firm.

Under s503(3) of the 2006 Act, only the Senior Statutory Auditor can sign the‘signing copy’ of the auditors’ report. If they are absent at the time of signing,the signature can be obtained by electronic means, such as e-mail or fax.

3.12.3 Joint auditors

Where a company has appointed joint auditors, each audit firm will designatetheir own Senior Statutory Auditor. When the auditors’ report is signed, eachfirm’s Senior Statutory Auditor must sign the report in their own name for andon behalf of their firm.

3.13 DATE

ISA (UK and Ireland) 700 requires that:

● before the auditors can give an opinion on the financial statements they musthave been approved by the directors and the auditors must have consideredall of the available evidence; and

● the auditors’ report has to be dated as at the date the opinion is expressed.

The significance of the date of the auditors’ report is that they are informing thereader that they are aware of events up to that date and have considered theeffect of these on the financial statements.

Before they sign the audit report the following must have occurred:

● receipt of the approved financial statements, together with anyaccompanying information, from the directors;

● review of all the documents which the auditors are required to consider inaddition to the financial statements, for example, the directors’ report; and

● completion of all the procedures thought necessary by the auditor to be ableto form an opinion, including a post balance sheet event review.

55

3. The Audit Report

The Senior Statutory Auditor must sign in manuscript and date the reportexpressing an opinion on the financial statements for distribution with thefinancial statements. Firms must therefore have procedures to ensure reports arenot signed before the above events have occurred.

The report should also state the location of the auditors’ offices, typically thecity or town in which the office that has responsibility is based.

Although the date of the auditors’ report has to be after the directors haveapproved the financial statements, it does not mean that the auditors cannotcommence their work until the directors have approved the financial statements.Rather, they cannot conclude it until this has happened. In many cases thepreparation of the financial statements will take place at the same time as theauditors are gathering evidence.

Although they will normally be in a position to give their opinion at the samedate as the financial statements are approved, it does not have to be on the sameday. Unless the auditors have gathered all their evidence and completed theirwork at that time (including a post balance sheet event review) they are unableto sign their report despite the directors approving the financial statements.

Where the date the opinion is expressed is before the final printing of thefinancial statements, the auditors will have to ensure the drafts on which theyform their opinion are sufficiently clear for them to assess the overallpresentation. One area to be especially aware of is where the directors haveapproved the profit and loss account and the balance sheet, but the notes haveyet to be finally completed. In such cases the auditors will have to delay givingtheir opinion until they are finished.

Where the date the auditors sign their report is later than the date of approvalthey may need to obtain additional assurances from the directors that there havebeen no events in the intervening period that would affect the financialstatements. They will also need to have their own procedures for reviewingsubsequent events and assessing their impact on the financial statements.

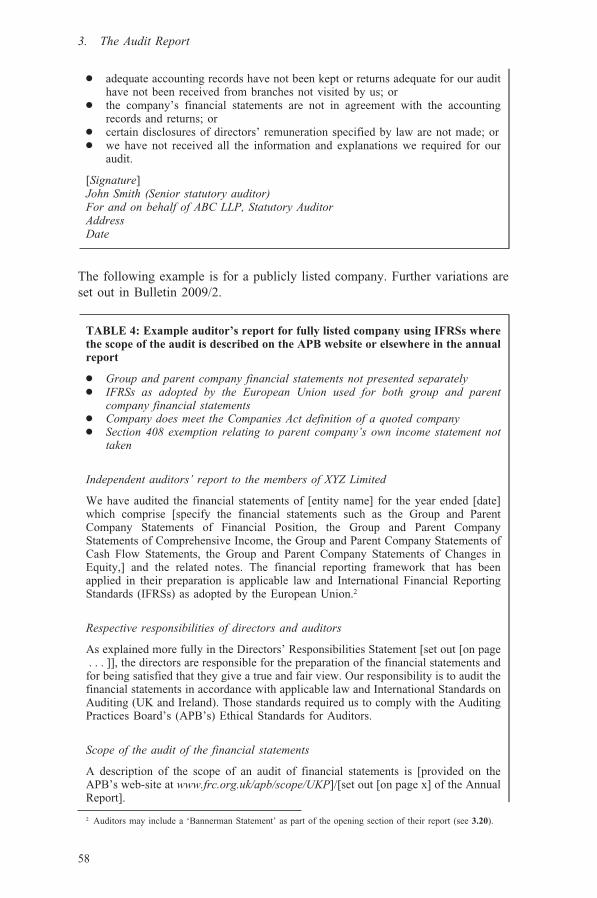

3.14 UNMODIFIED AUDITOR’S REPORTSEXAMPLES

ISA (UK and Ireland) 700 refers to example auditor’s report in the most recentversion of its Bulletin Auditor’s Reports on Financial Statements in the UnitedKingdom. The current version is Bulletin 2009/2 published in April 2009.

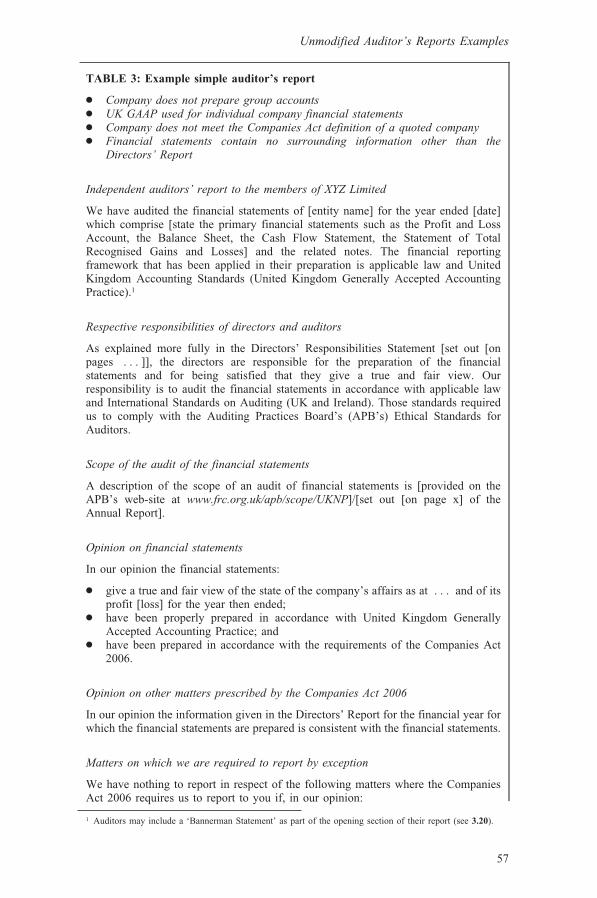

A simple auditor’s report for a non-listed company not preparing group accountsis provided in Table 3.

56

Unmodified Auditor’s Reports Examples

TABLE 3: Example simple auditor’s report

● Company does not prepare group accounts● UK GAAP used for individual company financial statements● Company does not meet the Companies Act definition of a quoted company● Financial statements contain no surrounding information other than the

Directors’ Report

Independent auditors’ report to the members of XYZ Limited