Embed Size (px)

Citation preview

Toolkit

2013

Implementation of the AIFM Directive

in Luxembourg.

Implementation of the AIFM Directive in Luxembourg

Outline.

CSSF FAQ

Structure of the AIFMD Law

Part I: Implementation of the AIFM Directive

Part II: Amendments to sectorial laws

Your contacts

1

Implementation of the AIFM Directive in Luxembourg

CSSF FAQ.

2

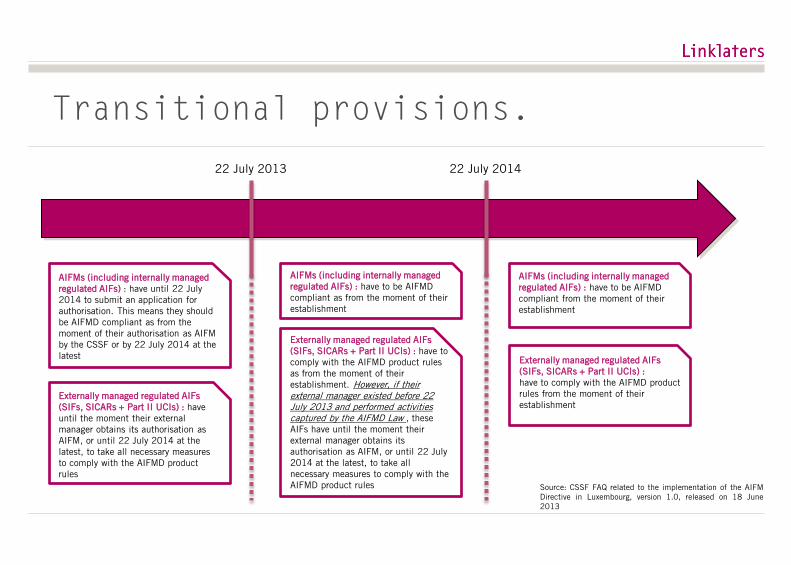

Transitional provisions.

22 July 2013 22 July 2014

AIFMs (including internally managed

regulated AIFs) : have until 22 July

2014 to submit an application for

authorisation. This means they should

be AIFMD compliant as from the

moment of their authorisation as AIFM

by the CSSF or by 22 July 2014 at the

latest

Externally managed regulated AIFs

(SIFs, SICARs + Part II UCIs) : have

until the moment their external

manager obtains its authorisation as

AIFM, or until 22 July 2014 at the

latest, to take all necessary measures

to comply with the AIFMD product

rules

AIFMs (including internally managed

regulated AIFs) : have to be AIFMD

compliant as from the moment of their

establishment

AIFMs (including internally managed

regulated AIFs) : have to be AIFMD

compliant from the moment of their

establishment

Externally managed regulated AIFs

(SIFs, SICARs + Part II UCIs) :

have to comply with the AIFMD product

rules from the moment of their

establishment

Externally managed regulated AIFs

(SIFs, SICARs + Part II UCIs) : have to

comply with the AIFMD product rules

as from the moment of their

establishment. However, if their

external manager existed before 22

July 2013 and performed activities

captured by the AIFMD Law , these

AIFs have until the moment their

external manager obtains its

authorisation as AIFM, or until 22 July

2014 at the latest, to take all

necessary measures to comply with the

AIFMD product rules Source: CSSF FAQ related to the implementation of the AIFM

Directive in Luxembourg, version 1.0, released on 18 June

2013

Implementation of the AIFM Directive in Luxembourg

CSSF FAQ.

On 18 June 2013, the CSSF FAQ provided additional clarifications in relation to the provisions of the AIFMD Law.

The key points are inter alia the following:

> Further details regarding the authorisation and registration procedures (the application form being released the same day)

> Transitional provisions:

New sub-fund(s) of an umbrella AIFs created prior to 22 July 2013 will benefit from the transitional provisions granted to the umbrella even if

the sub-fund is launched on or after 22 July 2013

> Letter box entities :

In order to ensure that an AIFM is not considered as a letter-box entity under the AIFMD Law, the following texts have to be taken into

consideration: (i) the Commission delegated act supplementing the AIFMD (article 82) and (ii) section 7 of CSSF Circular 12/546 which

specifies the delegation rules with respect to Chapter 15 ManCos and self-managed UCITS under the Law of 2010 (these principles apply by

analogy to Luxembourg AIFMs delegating investment management functions)

> Delegation of portfolio management and/or risk management functions :

An AIFM may delegate the two functions (i.e. portfolio management and/or risk management functions) in the understanding that the AIFM

does not delegate both functions in whole at the same time and to the extent that the AIFM does not become a letter box entity. It is clarified

that portfolio management and risk management are multi faceted functions consisting of various core activities and may in that respect be

partially delegated

> Domiciliary services provided to SOPARFIs :

An AIFM is allowed to provide SOPARFI domiciliary services provided that such SOPARFI either (i) qualifies as AIF and that AIFM is the

designated manager of that SOPARFI/AIF or (ii) such SOPARFI is a subsidiary controlled by an AIF

> List of the cooperation agreements required under the AIFMD signed by the CSSF

4

Implementation of the AIFM Directive in Luxembourg

Structure of the AIFMD Law.

5

Implementation of the AIFM Directive in Luxembourg

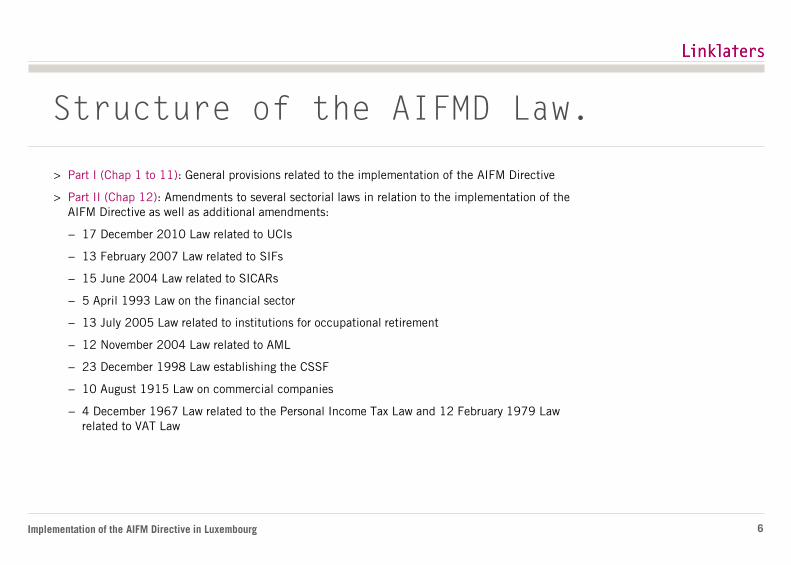

> Part I (Chap 1 to 11): General provisions related to the implementation of the AIFM Directive

> Part II (Chap 12): Amendments to several sectorial laws in relation to the implementation of the

AIFM Directive as well as additional amendments:

− 17 December 2010 Law related to UCIs

− 13 February 2007 Law related to SIFs

− 15 June 2004 Law related to SICARs

− 5 April 1993 Law on the financial sector

− 13 July 2005 Law related to institutions for occupational retirement

− 12 November 2004 Law related to AML

− 23 December 1998 Law establishing the CSSF

− 10 August 1915 Law on commercial companies

− 4 December 1967 Law related to the Personal Income Tax Law and 12 February 1979 Law

related to VAT Law

Structure of the AIFMD Law.

6

Implementation of the AIFM Directive in Luxembourg

Part I: Implementation of the AIFM

Directive.

7

Implementation of the AIFM Directive in Luxembourg

AIFM

Directive

Capital

requirements

Conduct of

business

rules

Organisational

requirements

Delegation

Depositary

duties Controlling

stakes

Leverage

disclosure

Transparency

and reporting

Passport

How will AIFMD affect the landscape?

AIFMD aims to create a comprehensive and effective

regulatory and supervisory framework for alternative

investment fund managers (AIFM) within the EU.

The Luxembourg law provides for a literal implementation of

AIFMD into Luxembourg law.

Luxembourg AIFs will have to ensure the compliance with a

certain number of requirements under AIFMD. In this

respect, it is anticipated that Luxembourg regulated vehicles

should be in a position to proceed to a smooth transition

under AIFMD as a substantial part of the new requirements

are already embedded in the Luxembourg legal and regulatory

framework.

The AIFMD introduces a new framework for managers of AIFs.

A Luxembourg AIF will have the option to either appoint an

AIFM or to decide to be self-managed.

EU AIFMs will have the possibility to market Luxembourg

AIFs throughout EU via a passport. Non-EU AIFMs will have

the possibility to take advantage of the passport under certain

conditions.

Private placement regimes will continue to exist but may be

abolished as from 2018.

8

Implementation of the AIFM Directive in Luxembourg

In scope Out of scope Exemptions

> EU AIFM managing EU or non-

EU AIF

> Non-EU AIFM managing EU

AIF

> Non-EU AIFM marketing EU or

non-EU AIF within the Union

> Holding companies

> Institutions for occupational retirement

> Supranational institutions (ECB, EIB, EIF, FSB, EBRD, IMF,

World Bank…)

> Luxembourg central bank and other national central banks

> National, regional and local governments and bodies or

institutions which manage funds supporting social security and

pension systems

> Employee participation or savings

> Securitisation vehicles*

> Group vehicles

> Lux AIFM managing leveraged AIFs and

AuM of less than EUR 100m

> Lux AIFM managing unleveraged AIFs,

no redemption for 5 years and AuM of

less than EUR 500m

> Lux AIFMs under these thresholds may

however opt-in under the Law

* provided their activities are covered by

ECB Regulation n°24/2009

> AIF under the Law means:

− any collective investment undertaking other than UCITS

− which raises capital from a number of investors (i.e. at least two)

− with a view to investing for the benefit of those investors in accordance with a defined investment policy

> AIFM under the Law means:

− legal persons whose regular business is to manage one or more AIFs

Scope.

9

Implementation of the AIFM Directive in Luxembourg

Vehicle In / Out of Scope

AIF

Part II UCI In Scope

SIF In Scope – unless dedicated to a single investor in its constitutional and/or issue document

SICAR In Scope – unless dedicated to a single investor in its constitutional and/or issue document

Unregulated investment vehicle Out of Scope – unless it meets the conditions laid down in the definition of AIF

Securitisation vehicle Out of Scope – provided it carries out activities which are covered by ECB Regulation 24/2009

ASSEP / SEPCAV (pension funds) Out of Scope

AIFM

Chap 15 Manco In Scope if (i) it manages AIF and (ii) it has not appointed an external AIFM

Chap 16 Manco In Scope if (i) it manages AIF and (ii) it has not appointed an external AIFM

Self-managed AIF In Scope

Managing GPs of SCA and SCS Out of Scope – unless it manages more than one SCA / SCS

Discretionary portfolio manager Out of Scope

Managers of non-coordinated foreign

UCIs

To be abolished on 22 July 2014

New sui generis AIFM status In Scope

What does this mean for Luxembourg?

10

Implementation of the AIFM Directive in Luxembourg

Part II: Amendments to sectorial laws.

Note: This document does not aim to cover all amendments to the sectorial laws and focuses on the key changes to the

following sectorial laws only:

> UCI Law

> SIF Law

> SICAR Law

> FSP Law

> Personal Income Tax Law and VAT Law

Amendments to the 1915 Law in respect of the new limited partnership vehicle are dealt with in a separate document

11

Implementation of the AIFM Directive in Luxembourg

The UCI Law.

12

Implementation of the AIFM Directive in Luxembourg

Content of the amendment

New provisions

regarding Part II UCIs

required to appoint an

AIFM

Depositary provisions:

> AIFMD depositary provisions applicable to those Part II UCIs

> Entities eligible to act as depositary :

> Credit institution having its registered office in Luxembourg or the Luxembourg branch of a credit institution

with registered office in another Member State (branches of non-EU banks are no longer acceptable)

> Investment firm whose licence authorises ancillary safe-keeping service for clients, subject to:

− Registered office in Luxembourg or the Luxembourg branch of an investment firm with registered office

in another Member State

− Minimum capital requirement: EUR 730k (minimum own funds to be specified by the CSSF)

− Compliance with organisational requirements applicable to depositary banks

> Professional depositary for assets other than financial instruments, subject to certain conditions (please see

section re. amendments to the 1993 Law).

Safekeeping and supervision of assets and liability provisions are subject to AIFMD requirements

Amendments to the UCI Law.

13

Implementation of the AIFM Directive in Luxembourg

Content of the amendment

New provisions

regarding Part II UCIs

required to appoint an

AIFM

Other provisions:

> Requirement to appoint an AIFM (external or internal)

> Central administration must be located in Luxembourg

> Independent valuation of Part II UCIs’ assets

> Delegation rules

> Transparency requirements (annual report, investors information, etc.)

> Rules for cross-border marketing and management of AIFs

Part II UCIs existing before 22 July 2013 shall comply with the new rules by 22 July 2014 at latest, with the exception of:

> Closed-ended Part II UCIs which do not make additional investments after 22 July 2013 (which will not be obliged to

comply with the new requirements)

> Closed-ended Part II UCIs whose investment period ended before 22 July 2011 and whose term will not exceed 22

July 2016 (which will not be obliged to comply with the new requirements, excepted reporting requirements)

Amendments to the UCI Law.

14

Implementation of the AIFM Directive in Luxembourg

Content of the amendment

New provisions

regarding Part II UCIs

benefiting from

exemption not to

appoint AIFM*

Depositary provisions:

> AIFMD depositary provisions not applicable

> Entities eligible to act as depositary :

> Credit institution having its registered office in Luxembourg or the Luxembourg branch of a credit institution

with registered office in another Member State or third country

> Investment firm whose licence authorises ancillary safe-keeping service for clients, subject to:

− Registered office in Luxembourg or the Luxembourg branch of an investment firm with registered office

in another Member State

− Minimum capital requirement: EUR 730k (minimum own funds to be specified by the CSSF)

− Compliance with organisational requirements applicable to depositary banks

> Professional depositary for assets other than financial instruments, subject to certain conditions (please see

section re. amendments to the 1993 Law).

Current safekeeping and supervision of assets and liability provisions remain unchanged (i.e. not subject to AIFMD requirements)

Other provisions:

Current regime applicable to Part II UCIs remain unchanged

Amendments to the UCI Law.

15

* Under article 3 of the Law

Implementation of the AIFM Directive in Luxembourg

Content of the amendment

New provisions

applicable to Chapter

15 (UCITS)

Management

Companies

Chapter 15 Management Companies may manage AIFs subject to CSSF approval

> Authorisation as AIFM under simplified procedure

Permitted activities: all activities permitted to Chapter 15 Management Companies + activities permitted to AIFM +

ancillary services when managing AIFs (including reception and transmission of orders on financial instruments)

> Chapter 15 Management Companies managing AIF before 22 July 2013 shall comply with the new rules and apply for

authorisation as AIFM by 22 July 2014 at latest

New regime for Chapter

16 (non-UCITS)

Management

Companies

> Article 125-1: Chapter 16 Management Companies are not required to become AIFM in order to:

− Act as management company for AIFs, which appoint an external AIFM

− Manage investment vehicles which are not AIFs

− Manage one or more AIFs, if their AuM do not exceed EUR100m (leveraged AIF) or EUR500m (unleveraged AIF)

(in this case only reporting and disclosure requirements apply)

> Article 125-2: Chapter 16 Management Companies are required to become AIFM in order to manage one or more AIF,

if their total AuM exceed EUR100m (leveraged AIF) or EUR500m (unleveraged AIF)

− These management companies are not authorised to managed non-AIF UCI

> Chapter 16 Management Companies managing AIF before 22 July 2013 shall comply with the new rules and apply for

authorisation as AIFM by 22 July 2014 at latest

Amendments to the UCI Law.

16

Implementation of the AIFM Directive in Luxembourg

Content of the amendment

Management Company

liquidation

Possibility for the CSSF to request the dissolution and liquidation of the management companies that have been

withdrawn from, or not registered on CSSF’s official list

Notarial deed

translation

Widening the exemption to translate notarial deeds drafted in English to all types of deeds (e.g. AGM, EGM, merger deeds

etc.)

Publication of reports Extended deadline for the publication of annual reports of Part II UCIs

> Semi-annual report: 3 months from the end of the relevant period

> Annual reports: 6 months from the end of the relevant period

Merger of UCITS When a UCITS SICAV is absorbed, notarial deed must certify the effective date of the merger

When a UCITS FCP is absorbed, the effective date of the merger is decided by the Management Company (unless provided

otherwise in the management regulations) and such decision shall be published in the RCS and Mémorial

KIID UCITS have only to be made available KIIDs to investors in a Non-EU country if required by local competent authority

Amendments to the UCI Law.

17

Implementation of the AIFM Directive in Luxembourg

The SIF Law.

18

Implementation of the AIFM Directive in Luxembourg

Content of the amendment

New provisions

regarding SIFs

qualifying as AIFs and

required to appoint an

AIFM

Depositary provisions:

> AIFMD depositary provisions applicable to those SIFs

> Entities eligible to act as depositary :

> Credit institution having its registered office in Luxembourg or the Luxembourg branch of a credit institution

with registered office in another Member State

> Investment firm whose licence authorises ancillary safe-keeping service for clients, subject to:

− Registered office in Luxembourg or the Luxembourg branch of an investment firm with registered office

in another Member State

− Minimum capital requirement: EUR 730k (minimum own funds to be specified by the CSSF)

− Compliance with organisational requirements applicable to depositary banks

> Professional depositary for assets other than financial instruments, subject to certain conditions (please see

section re. amendments to the 1993 Law).

Safekeeping and supervision of assets and liability provisions are subject to AIFMD requirements

Amendments to the SIF Law.

19

Implementation of the AIFM Directive in Luxembourg

Content of the amendment

New provisions

regarding SIFs

qualifying as AIFs and

required to appoint an

AIFM

Other provisions:

> Requirement to appoint an AIFM

> Central administration must be located in Luxembourg

> Independent valuation of SIFs’ assets

> Delegation rules

> Transparency requirements (annual report, investors information, etc.)

> Rules for cross-border marketing and management of AIFs

SIFs existing before 22 July 2013 shall comply with the new rules by 22 July 2014 at latest, with the exception of:

> Closed-ended SIFs which do not make additional investments after 22 July 2013 (which will not be obliged to comply

with the new requirements)

> Closed-ended SIFs whose investment period ended before 22 July 2011 and whose term will not exceed 22 July 2016

(which will not be obliged to comply with the new requirements, excepted reporting requirements)

Amendments to the SIF Law.

20

Implementation of the AIFM Directive in Luxembourg

Content of the amendment

New provisions

regarding SIFs which (i)

do not qualify as AIFs

or (ii) benefit from

exemption not to

appoint an AIFM*

Depositary provisions:

> AIFMD depositary provisions not applicable

> Entities eligible to act as depositary :

> Credit institution having its registered office in Luxembourg or the Luxembourg branch of a credit institution

with registered office in another Member State or third country

> Investment firm whose licence authorises ancillary safe-keeping service for clients, subject to:

− Registered office in Luxembourg or the Luxembourg branch of an investment firm with registered office

in another Member State

− Minimum capital requirement: EUR 730k (minimum own funds to be specified by the CSSF)

− Compliance with organisational requirements applicable to depositary banks

> Professional depositary for assets other than financial instruments, subject to certain conditions (please see

section re. amendments to the 1993 Law)

Current safekeeping and supervision of assets and liability provisions remain unchanged (i.e. not subject to AIFMD requirements)

Other provisions:

Current regime applicable to SIFs remain unchanged

New limited partnership

regime

SIF Law has been adjusted to accomodate the provisions of the new Luxembourg limited partnership regime

Amendments to the SIF Law.

21

* Under article 3 of the Law

Implementation of the AIFM Directive in Luxembourg

The SICAR Law.

22

Implementation of the AIFM Directive in Luxembourg

Content of the amendment

New provisions

regarding SICARs

qualifying as AIFs and

required to appoint an

AIFM

Depositary provisions:

> AIFMD depositary provisions applicable to those SICARs

> Entities eligible to act as depositary :

> Credit institution having its registered office in Luxembourg or the Luxembourg branch of a credit institution

with registered office in another Member State

> Investment firm whose licence authorises ancillary safe-keeping service for clients, subject to:

− Registered office in Luxembourg or the Luxembourg branch of an investment firm with registered office

in another Member State

− Minimum capital requirement: EUR 730k (minimum own funds to be specified by the CSSF)

− Compliance with organisational requirements applicable to depositary banks

> Professional depositary for assets other than financial instruments, subject to certain conditions (please see

section re. amendments to the 1993 Law).

Safekeeping and supervision of assets and liability provisions are subject to AIFMD requirements

Amendments to the SICAR Law.

23

Implementation of the AIFM Directive in Luxembourg

Content of the amendment

New provisions

regarding SICARs

qualifying as AIFs and

required to appoint an

AIFM

Other provisions:

> Requirement to appoint an AIFM

> Central administration must be located in Luxembourg

> Independent valuation of SICAR’s assets

> Delegation rules

> Transparency requirements (annual report, investors information, etc.)

> Rules for cross-border marketing and management of AIFs

SICARs existing before 22 July 2013 shall comply with the new rules by 22 July 2014 at latest, with the exception of:

> Closed-ended SICARs which do not make additional investments after 22 July 2013 (which will not be obliged to

comply with the new requirements)

> Closed-ended SICARs whose investment period ended before 22 July 2011 and whose term will not exceed 22 July

2016 (which will not be obliged to comply with the new requirements, excepted reporting requirements)

Amendments to the SICAR Law.

24

Implementation of the AIFM Directive in Luxembourg

Content of the amendment

New provisions

regarding SICARs which

(i) do not qualify as

AIFs or (ii) benefit from

exemption not to

appoint an AIFM*

Depositary provisions:

> AIFMD depositary provisions not applicable

> Entities eligible to act as depositary :

> Credit institution having its registered office in Luxembourg or the Luxembourg branch of a credit institution

with registered office in another Member State or third country

> Investment firm whose licence authorises ancillary safe-keeping service for clients, subject to:

− Registered office in Luxembourg or the Luxembourg branch of an investment firm with registered office

in another Member State

− Minimum capital requirement: EUR 730k (minimum own funds to be specified by the CSSF)

− Compliance with organisational requirements applicable to depositary banks

> Professional depositary for assets other than financial instruments, subject to certain conditions (please see

section re. amendments to the 1993 Law).

Current safekeeping and supervision of assets and liability provisions remain unchanged (i.e. not subject to AIFMD requirements)

Other provisions:

Current regime applicable to SICARs remain unchanged

New limited partnership

regime

SICAR Law has been adjusted to accomodate the provisions of the new Luxembourg limited partnership regime

Amendments to the SICAR Law.

25

* Under article 3 of the Law

Implementation of the AIFM Directive in Luxembourg

The 1993 Law on the Financial Sector.

26

Implementation of the AIFM Directive in Luxembourg

Content of the amendment

New FSP licence:

Professional depositary

for assets other than

financial instruments

> A new financial sector professional (“FSP”) licence as “professional depositary for assets other than financial

instruments” to act as depositary of SIFs, SICARs and AIFs which are closed for redemptions during the first 5 years

and which generally invest in assets other than financial instruments (e.g. private equity and real estate funds),

subject to a minimum capital requirement of EUR 500k (minimum own funds to be specified by the CSSF)

These FSPs

> Can act under delegation received from the AIF’s depositary

> Can act as administration agent (subject to an appropriate hierarchical and organisational separation), registrar,

communication agent or domiciliary agent

> Can not perform management of UCIs or alternative funds

Managers of Non-

Coordinated UCIs (art.

28-8 of the FSP Law)

Managers of non-coordinated UCIs managing alternative investment funds before 22 July 2013 have until 22 July 2014 to

comply with AIFMD requirements

Amendments to the Law on the

Financial sector.

27

Implementation of the AIFM Directive in Luxembourg

The Personal Income Tax Law.

28

Implementation of the AIFM Directive in Luxembourg

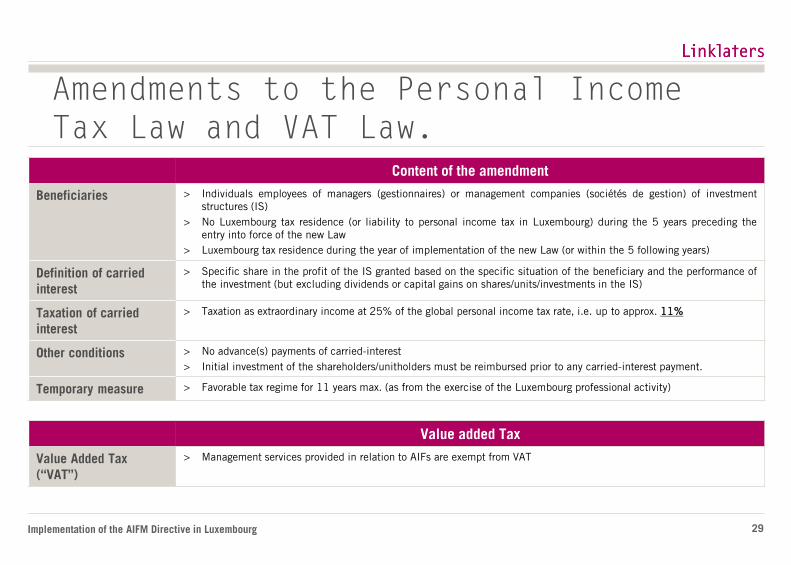

Content of the amendment

Beneficiaries > Individuals employees of managers (gestionnaires) or management companies (sociétés de gestion) of investment

structures (IS)

> No Luxembourg tax residence (or liability to personal income tax in Luxembourg) during the 5 years preceding the

entry into force of the new Law

> Luxembourg tax residence during the year of implementation of the new Law (or within the 5 following years)

Definition of carried

interest

> Specific share in the profit of the IS granted based on the specific situation of the beneficiary and the performance of

the investment (but excluding dividends or capital gains on shares/units/investments in the IS)

Taxation of carried

interest

> Taxation as extraordinary income at 25% of the global personal income tax rate, i.e. up to approx. 11%

Other conditions > No advance(s) payments of carried-interest

> Initial investment of the shareholders/unitholders must be reimbursed prior to any carried-interest payment.

Temporary measure > Favorable tax regime for 11 years max. (as from the exercise of the Luxembourg professional activity)

Amendments to the Personal Income

Tax Law and VAT Law.

Value added Tax

Value Added Tax

(“VAT”)

> Management services provided in relation to AIFs are exempt from VAT

29

Implementation of the AIFM Directive in Luxembourg

Well connected.

30

Implementation of the AIFM Directive in Luxembourg

Your AIFMD team in Luxembourg 1/2.

31

Hermann Beythan Partner, IMG

Tel: (352) 2608 8234 [email protected]

Emmanuel F. Henrion Partner, IMG

Tel: (352) 2608 8279

emmanuel-

Josiane Schroeder Counsel, IMG

Tel: (352) 2608 8275 [email protected]

Silke Bernard Managing Associate, IMG

Tel: (352) 2608 8223 [email protected]

Rodrigo Delcourt Counsel, IMG

Tel: (352) 2608 8293 [email protected]

Benoit Delzelle Managing Associate, IMG

Tel: (352) 2608 8220 [email protected]

Christian Hertz Managing Associate, IMG

Tel: (352) 2608 8207 [email protected]

Xenia Thomamüller Managing Associate, IMG

Tel: (352) 2608 8281 [email protected]

Freddy Brausch Partner, IMG

Tel: (352) 2608 8231 [email protected]

Implementation of the AIFM Directive in Luxembourg 32

Your AIFMD team in Luxembourg 2/2.

Emmanuel Avice Managing Associate, IMG

Tel: (352) 2608 8286 [email protected]

Marianna Tothova Managing Associate, IMG

Tel: (352) 2608 8338 [email protected]

Manfred Müller Counsel, Corporate

Tel: (352) 2608 8272 [email protected]

Jean-Paul Spang Partner, Corporate

Tel: (352) 2608 8253 [email protected]

Olivier Van Ermengem Partner, Tax

Tel: (352) 2608 8224 [email protected]

Aurélie Clementz Managing Associate, Tax

Tel: (352) 2608 8203 [email protected]

Nicolas Gauzès Partner, Corporate

Tel: (352) 2608 8284 [email protected]

Implementation of the AIFM Directive in Luxembourg 33

Linklaters LLP is a limited liability partnership registered in England and Wales with registered number OC326345. The term partner in relation to Linklaters LLP is used

to refer to a member of Linklaters LLP or an employee or consultant of Linklaters LLP or any of its affiliated firms or entities with equivalent standing and qualifications. A

list of the names of the members of Linklaters LLP and of the non members who are designated as partners and their professional qualifications is open to inspection at its

registered office, One Silk Street, London EC2Y 8HQ, England or on www.linklaters.com. A15076861

Nothing in this document should be construed as advice.

Please, feel free to

contact us.

© 2013

Any questions?

Linklaters LLP

35, avenue John F. Kennedy

L-1011 Luxembourg

Tél : (352) 2608-8372

Fax : (352) 2608-8888