Embed Size (px)

Citation preview

Implementationof Interagency Guidance on

Concentrations in Commercial Real Estate Lending,

Sound Risk Management Practices

January 30, 2007Denise Dittrich [email protected] Reserve Board

2

Background

Proposed guidance issued in January 2006

Considerable feedback from the industry

Final guidance issued by the Federal Reserve, OCC and FDIC on December 12, 2006

OTS separately issued similar CRE guidance

3

Why are Supervisors Concerned about CRE Concentrations?

CRE lending is a significant business line for many small to medium-sized institutions

CRE has historically been highly cyclical which led to large losses in the banking industry

CRE concentration ratios are at record levels

Rising interest rates could affect debt service coverage ratios and property values

Risk management practices and strategic and capital planning have not always kept pace with growth in CRE lending

Source: Call Report

Trend in CRE Concentrations by Asset SizeAll Commercial & Savings Banks

(Total CRE Loans / Total Risk-based Capital)

0

50

100

150

200

250

300

350

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006Q3

Per

cent

Total Assets < $100 Mn

Total Assets $100 Mn - $1 Bn

Total Assets $1 - $10 Bn

Total Assets > $10 Bn

5

What’s Different From the Past?

More disciplined underwriting Regulatory lending standards Appraisal profession better regulated Transactions not tax driven More liquid CRE markets Better market data

6

What’s Happening Now?

Frothy CRE markets – cap rates, prices, debt service coverage

Slowing housing markets – residential construction

New sources of market liquidity – CMBS, hedge funds

Plus, lender surveys reveal:

Declining underwriting standards Hyper competition Expectations for declining asset quality

7

A Tour of The Guidance

Directed to institutions with significant CRE lending

Applies to banks but principles are broadly applicable to bank holding companies and their non-bank subsidiaries

Outlines key risk management expectations

Reinforces and builds upon existing regulations and supervisory guidelines

8

Focus of the Guidance

Focus is on concentrations in types of CRE loans that expose institutions to cyclical conditions in real estate markets, includes:

“Non-owner occupied loans” where repayment is dependent on the rental income or sale or refinancing of the real estate held as collateral

Residential and commercial construction and development loans

Excludes “owner-occupied” RE loans where repayment is from cash flow from operations

Consistent with Call Report changes

Excludes real estate taken as a secondary source of repayment or in an abundance of caution

9

Guidance establishes numerical criteria for identifying institutions with potentially significant CRE concentration risk

Using Call Report data, supervisors will focus on institutions with:

(1) Construction & land development loans ≥ 100% of capital; or

(2) Total CRE loans ≥ 300% of capital and ≥ 50% growth in CRE portfolio over last 36 months

Supervisory Monitoring Criteria

10

Purpose of Supervisory Criteria

Used to identify institutions with potential concentration risk

Criteria should not be viewed as limits on lending activity

There is no “safe harbor” if other risk indicators are present, such as:

Rapid growth in CRE lending Significant growth in CRE credit concentrations Concentrations in certain property types

Criteria is only to be used as a starting point for conducting further analysis

11

Purpose of Supervisory Criteria (cont.)

Institutions meeting criteria would be expected to be able to demonstrate the risk characteristics of their CRE portfolio by property type, market, and borrower

Institutions are expected to perform their own assessment of CRE concentration risk

Examiners will avoid an extended discussion on segmentation of individual loans, focus should be on the portfolio management

12

Implementation of Guidance

Effective as of December 12, 2006

This is not a “one size fits all” process

Examiners will use a risk-based approach and exercise examiner discretion

Examiners will be flexible with institutions on the timeframe for meeting risk management expectations

Agencies will provide training to examiners on proper implementation of the guidance

13

Expectations for Risk Management

Guidance applies to institutions of all sizes

Sophistication of risk management systems will vary with CRE portfolio’s risk characteristics, size and complexity

Evaluation of risk management systems will consider varying risk profiles of loans secured by different property types

Relatively simple systems may work for some banks

14

Expectations for Risk Management

Board and management oversight

Management information systems

Market analysis

Portfolio stress testing and sensitivity analysis

Credit underwriting standards

15

Board and Management Oversight

The Board has ultimate responsibility for risk assumed Approve overall CRE strategy and risk tolerance

levels Monitor how the strategy is progressing and if its

policies are being complied with Approve contingency plan

Management is responsible for implementing the CRE strategy on a day-to-day basis in compliance with board approved policies

Design operating policies and procedures that enable it to identify, manage, monitor, and control CRE risks

Provide the board with reports showing strategic targets including portfolio risk levels

16

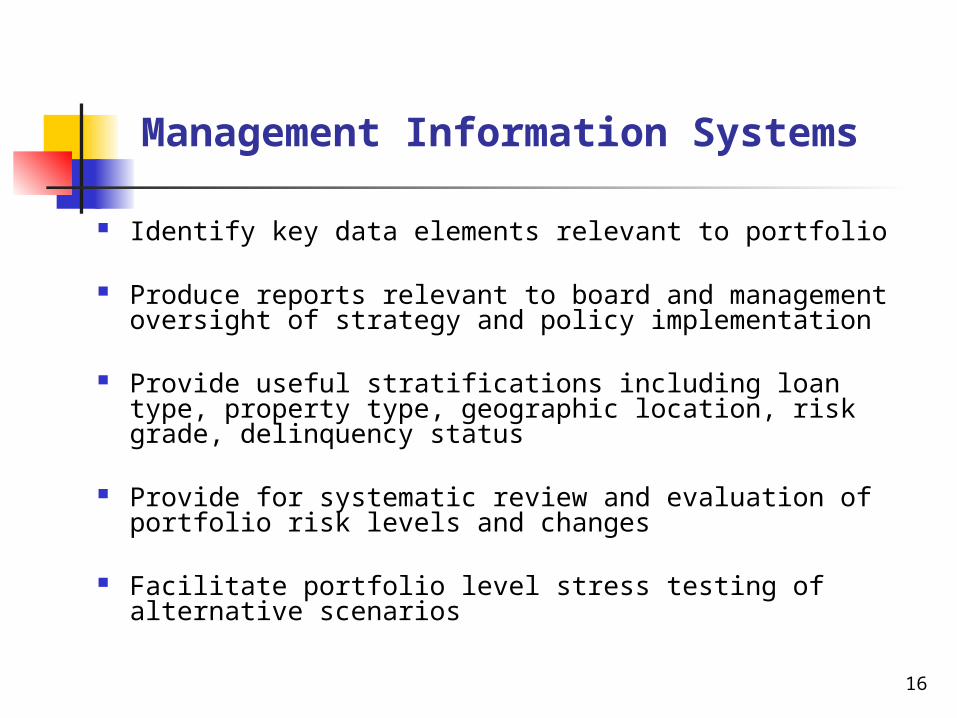

Management Information Systems

Identify key data elements relevant to portfolio

Produce reports relevant to board and management oversight of strategy and policy implementation

Provide useful stratifications including loan type, property type, geographic location, risk grade, delinquency status

Provide for systematic review and evaluation of portfolio risk levels and changes

Facilitate portfolio level stress testing of alternative scenarios

17

Market Analysis

Provide management with sufficient information on current market conditions and factors that could influence those conditions in the future

Incorporate data and anecdotal information to develop a reasoned view of market conditions and prospects

Should utilize multiple sources of information for a balanced view

Should be integrated into the strategic plan development and risk management

18

Market Analysis (cont.)

Types and sources will vary depending on composition of portfolio and markets served

Frequency of updates depends on size, scope and complexity of portfolio and stability of market conditions

Analysis may contribute variables for stress testing

19

Portfolio Stress Testing and Sensitivity Analysis

Analysis will assist management and the board in understanding how changes in relevant economic or market factors could affect the portfolio or key portfolio segments

Sophistication of process will vary with complexity of the portfolio

Analysis should measure the effect on earnings and capital and portfolio quality

Results should be considered in strategic planning and risk management

Results should be updated periodically and shared in writing with senior management and the board

20

Underwriting Standards

Lending policies should reflect the level of risk that is acceptable to the board

Underwriting criteria should be clear and measurable Maximum loan amount by type of property Loan terms Pricing LTV limits Collateral valuation Debt service coverage

Tight control over policy exceptions

Review and amend standards, as needed, based on results of market analysis

21

Evaluation of Capital Adequacy

Guidance does not imply that banks will necessarily need to increase capital just because they have a concentration

Institutions should consider the level of capital support for CRE concentrations in their strategic, financial and capital planning

Supervisors will take into account inherent risk and quality of risk management practices

22

Points of Emphasis

Supervisory criteria are not limits, rather they are to be used as supervisory monitoring tools

Banks should perform internal risk assessments Board and management oversight is critical Expectations for risk management practices will be

commensurate with risk profile of institution Capital adequacy will be evaluated on a case-by-

case basis Guidance does not supercede the Agencies’ real

estate lending and appraisal standards