Embed Size (px)

Citation preview

Impact of reforming exchange rate system on economic policy & broader policies: Some thoughts

Day Month Year

Standing Committee on Finance and Select Committee on FinanceParliament of the Republic of South Africa, Cape Town.10 November 2010

Lumkile MondiChief Economist

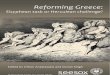

Rand performance in nominal and real terms

2

40

60

80

100

120

140

160

180

200

220

240

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

Ind

ex: 2

000

= 1

00

Real and nominal effective exchange rates

Nominal effective exchange rate

Real effective exchange rate

Source: SARB

Appreciation

Depreciation

Over the past 21 years, the REER was at similar level s, or stronger than currently for 41% of the time (i.e. 102 months

out of 247 months) => current predicament is that of overvalued currency +

weak global demand => loss of export markets + reduced import competitiveness

3

Rand performance vs select currencies

PeriodRand per

EuroRand per US dollar

Rand per British Pound

SA cents per Japanese

Yen

Rand per Chinese

Yuan

Rand per Brazil Real

Rand per Indian Rupee

Rand per Russian Rubble

Rand per Australian

Dollar

January 2008 10.27 6.99 13.75 6.47 0.96 3.94 0.18 0.29 6.16

December 2008 13.37 9.95 14.81 10.91 1.45 4.15 0.20 0.35 6.69

December 2009 10.95 7.49 12.17 8.35 1.10 4.28 0.16 0.25 6.75

October 2010 9.60 6.91 10.95 8.45 1.04 4.11 0.16 0.23 6.79

Jan '08 - Oct '10 -6.5 -1.1 -20.4 30.4 7.5 4.2 -12.3 -20.0 10.2

Dec '08 - Oct '10 -28.2 -30.5 -26.0 -22.6 -28.5 -1.0 -23.8 -35.3 1.5

Dec '09 - Oct '10 -12.3 -7.7 -10.0 1.1 -5.5 -4.0 -3.1 -8.4 0.6

Source: SARB, Bloomberg, IDC calculations

The exchange rate movement of the Rand over different time periods

Rand per Foreign Currency Unit (monthly averages)

Appreciation (-) or Depreciation (+) of the Rand (% change over period)

4

Evolution of SA’s trade balance with the rest of the world

• During the period of progressive rand weakness (Feb. 2006 to Dec. 2008) …

– value of overall exports rose across the board,

– but so did imports, on the back of increased investment activity (i.e. capital equipment) and production levels (i.e. intermediate goods & raw materials), as well as consumer spending propelled by rising incomes and easy credit.

• As the rand appreciated since Jan 2009, adverse impact on export trade was anticipated, but the negative effect on import values was of a similar nature …

• … currency competitiveness not the sole determining factor within a global and local environment where many serious adverse forces are at play, particularly demand-related.

-500

-400

-300

-200

-100

0

100

200

300

400

1

2003

2

|

1

2004

2

|

1

2005

2

|

1

2006

2

|

1

2007

2

|

1

2008

2

|

1

2009

2

|

1

2010

R billion SA trade balance

Imports Exports Trade balance

(per semester)

5

0

20

40

60

80

100

120

140

1

2003

2

|

1

2004

2

|

1

2005

2

|

1

2006

2

|

1

2007

2

|

1

2008

2

|

1

2009

2

|

1

2010

SA exports by broad economic classification

Capital goods

Consumer goods

Intermediate goods

Raw material

R billion per semester (current values)

0

20

40

60

80

100

120

140

160

1

2003

2

|

1

2004

2

|

1

2005

2

|

1

2006

2

|

1

2007

2

|

1

2008

2

|

1

2009

2

|

1

2010

SA imports by broad economic classification

Capital goods

Consumer goods

Intermediate goods

Raw material

R billion per semester (current values)

• Despite rand appreciation since Jan. 2009, value of SA exports of raw materials and intermediate goods recovered to some extent in 1st semester of 2010, particularly due to Asian demand.

• Value of imports also started recovering in most categories (except raw materials) in 1st semester 2010

Evolution of SA’s trade balance with the rest of the world

6

Excessive rand volatility from an emerging market perspective

Excessive volatility …

• Compromises business decisions, leads to strategic indecisiveness (re. X, M, I);

• Affects policy decisions & strategies re. industrial development ,trade promotion, capex, interest rates, reserve levels, exchange rate management etc;

• SA’s inflation record & its management over time encouraged carry trade … problem intensified by higher yield seeking investment funds in recent times;

• Quantitative easing in US, easy credit policies in several advanced economies => further speculation in EM currencies => strengthening bias and possible volatility for longer.

0

500

1000

1500

2000

2500

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Selected Spot Exchange Rate Volatility, 1995 - 2009

South Africa (rand) Indonesia (rupiah)

Korea, Rep. of (won) Brazil (real)

Phillipines (peso)

Source: Bloomberg, IDC calculations

South Africa

Inde

x: 1

995=

100

7

Recent capital control interventions globally

• Brazil – Oct ‘09 imposed 2% Tobin tax on foreigners fixed-income purchases => 4 Oct 2010 doubled to 4% => later same month to 6%; also raised to 6% (from 0.38%) the so-called IOF tax that foreigners must pay to invest in local derivatives.

Outcome ... short-term impact on capital flows & the real, but real reverted to levels similar to those pre-intervention. Recent adjustment impact still to be seen. Finance Minister says he’s ready to take additional measures to stem the currency’s rally and has “large calibre” weapons that haven’t been used.

• Thailand – Oct 2010 imposed 15% tax on interest payments & capital gains from government & state-owned company bonds. Outcome …not much impact on the local bond market and the baht remained strong in subsequent days.

• South Korea – no financial transaction taxes, but rather a series of policy measures (e.g. new restrictions on trades in currency derivatives; new ceilings on domestic banks & branches of foreign banks dealing with forex, forwards & derivatives; restrictions on use of bank loans in foreign currency; further tightening of regulations on foreign currency liquidity ratios for domestic banks). Outcome …

8

• Indonesia – 1-month minimum holding period on SBIs (Sertifikat Bank Indonesia - favourite debt instruments amongst foreign & local investors), SBIs non-transferable over this period; central bank to issue longer dated SBIs (9- & 12-months) to retain investor money for longer; new regulations on banks’ net foreign exchange open positions; central bank widened short-term overnight money market interest rate corridor & introduced non-securities monetary instrument in the form of terms deposits.

Impact yet to be manifested, with expectations that stronger measures may be taken in future if strong capital inflows continue.

• Taiwan – restricted foreign investors from buying time deposits. Outcome … decline in foreign speculative capital inflows and the NT dollar depreciated ?

• Philippines – intervention in the forex market (i.e. forex accumulation) not bold enough to prevent the peso from appreciating further.

Recent capital control interventions globally

Some of the potential implications of exchange rate management:

9

Potential favourable implications:•Raises price competitiveness of exports, at least temporarily (bearing in mind the progressive erosion of such competitiveness depending on inflationary impact) => increased export market penetration, assuming demand is there.

•If price competitiveness and stability are sustained, progressive recapturing of foreign markets and securing new external customer bases.

•Alleviate import competition in local markets, but again this improved price competitiveness could be progressively eroded.

•If price competitiveness and stability are sustained, progressive regaining of local markets.

•Positive implications for the bottom line of commodity exporters whose external sales are denominated in foreign currencies, while operational costs are rand-based.

•Increased foreign tourism earnings as weaker rand raises SA’s attractiveness as a holiday destination, with the reverse tending to occur with respect to international travel by South Africans.

•All the above bullets may => increased local production => employment gains => higher investment propensity => again, job gains.

Some of the potential implications of exchange rate management:

10

Potential favourable implication (cont.):

•Higher dividend receipts (in rand terms) from SA investments abroad.

•Potentially enhanced wealth effect for SA holders of offshore assets.

•Positive fiscal implications include potentially higher tax revenues due to increased economic activity, improved corporate returns, higher household incomes through employment gains etc.

•Balance of payments implications may be positive if export demand recovers substantially and significant import substitution is realised.

Some of the potential implications of exchange rate management:

11

Potential concerns and/or unfavourable implications:

•Uncertainty over potential impact of intervention in terms of desired outcomes and their sustainability.

•Cost of intervention/s, depending on the choice of instrument/s.

•Abrupt unwinding of substantial speculative positions could have a destabilising effect, at least in the short-term … effects could be long-lasting if investor perceptions unfavourable.

•Considering SA’s low savings propensity and its dependency on foreign capital inflows to finance its current account deficit and funding requirements, negative perceptions may have seriously adverse repercussions.

•Timing of the intervention is critical in order to minimise unintended consequences … e.g. negative impact on the cost of investment-related imports, while exports may not recover sufficiently due to weak global demand.

•Potentially higher inflation environment (via imported inflation, especially input costs such as fuel and food items), with negative implications for interest rates, investment activity, employment, general cost of living and domestic consumption demand.

Some of the potential implications of exchange rate management:

12

Potential concerns and/or unfavourable implications (continued):

•Higher import costs, impacting negatively on enterprises (private and public) that require foreign capital equipment and other items for investment purposes, or raw materials and intermediate products for production purposes => higher price tags on investment plans => possible adverse implications for private sector and infrastructure investment.

•If a higher quantum of foreign reserves is desirable, the cost of its accumulation will rise.

•Higher rand costs associated with the payment of licensing fees, royalties, interest commitments and loan capital re-payment obligations to foreign entities.

•Reduced wealth effect for holders of SA assets, with implications for portfolio investments by non-residents and foreign direct investment propensity.

•Negative fiscal implications include higher capex budgets for projects that have a substantial import intensity, increased foreign debt servicing costs, rising costs for international representations and commitments, potential costs associated with the exchange rate intervention itself etc.

•Balance of payments implications may be negative due to weak export demand over a prolonged period and dearer indispensable imports.

13

Concluding remarks

• Sluggish recovery in advanced economies … low interest rates sustained … interest rate differential may attract carry trade for longer.

• As long as the global economy remains sluggish, adversely affected countries like US & Japan will proceed with further quantitative easing … cheap credit … higher speculation vis-a-vis EM currencies … initiatives to discourage carry trade mostly unsuccessful.

• “Beggar thy neighbour” tendencies … currency manipulation across the globe => currency war => trade war => lose-lose outcome !

• Countries should thus refrain from competitive devaluations of their currencies … resist protectionist measures … make notable progress in the reduction of trade barriers and unfair forms of subsidisation (direct and indirect) in advanced and centrally planned economies.

• Effectiveness of currency intervention / capital controls is highly uncertain, with costs depending on instrument/s utilised … impact may not be sustained.

• In general, EM efforts to weaken their currencies have yet to bear fruit … minimal and short-lived success achieved in some cases (e.g. Brazil, Thailand), greater success in Taiwan.

14

Concluding remarks

• Non-floating currencies (i.e. renminbi) are enjoying unfair competitive advantage.

• ‘Korean Initiative’ … establishment of global financial safety nets through international cooperation.

• G20 Summit’s current account limiting proposals: insufficient details on implementation … effective enforcement highly improbable.

• Piecemeal efforts or quick-fixes by EM experiencing an influx of capital flows may not be sustained. Rather pursue a concerted and coordinated multilateral effort.

• Rand exchange rate movements ... other countries’ woes … SA authorities have limited control.

• May be preferable to focus on measures to reduce volatility (long-term objective), rather than attempt to target specific currency levels/ranges (shorter-term objective).

• Capital control measures should not be adopted in isolation, as their success is heavily reliant on supportive policies, strategies and initiatives across the economic and social arenas.

Day Month Year

The Industrial Development Corporation19 Fredman Drive, SandownPO Box 784055, Sandton, 2146South AfricaTelephone (011) 269 3000Facsimile (011) 269 2116E-mail [email protected]

Thank you