Embed Size (px)

Citation preview

8/12/2019 Impact of Monetray Policy on Stock Market

http://slidepdf.com/reader/full/impact-of-monetray-policy-on-stock-market 1/13

Impact of Monetary Policy on the Volatility of Stock

Market in Pakistan

Abdul Qayyum

Professor Pakistan Institute of Development Economics

and

Saba Anwar

Research EconomistPakistan Institute of Development Economics

Pakistan Institute of Development EconomicsP. O. Box 1091, Islamaa!P"#I$%"&

1

8/12/2019 Impact of Monetray Policy on Stock Market

http://slidepdf.com/reader/full/impact-of-monetray-policy-on-stock-market 2/13

Impact of Monetary Policy on the Volatility of Stock

Market in Pakistan

%his paper a!!resses the linka'es et(een the monetar) polic) an! the stock market inPakistan. %he estimation techni*ue emplo)e! inclu!es En'le +ran'er t(o step proce!urean! the ivariate E+"R- metho!. %he results in!icate that an) chan'e in the monetar)

polic) stance have a si'nificant impact on the volatilit) of the stock market. %huscontriutin' to the on'oin' !eate in the monetar) polic) rule literature re'ar!in' the

proactive an! reactive approach1.

E/ co!e +10, E230.

#e)(or!s Interest Rate, $tock 4arket, 4onetar) Polic).

! Introduction

5inancial sector in Pakistan has een experiencin' the process of reforms since ei'hties. %het(o important outcomes of the financial sector reforms in Pakistan has een the openin' upof the stock markets for forei'n investors an! a!option of market ase! instruments, such asinterest rate, of monetar) polic). Openin' up of the stock markets resulte! in a sharp increasein the inflo(s of portfolio investment 65a7al an! 8a))um 00:;<. On one si!e such aninvestment helps in raisin' the investale fun!s an! on other si!e it pro!uce! (il! s(in's inthe stock market. 5or example, the #arachi $tock #$E;=100 In!ex increase! to >00 in 199?

ut !ecline! sharpl) to @ust A:A in 199A. 5rom this lo( level it crosse! 10 thousan! marks inearl) 00? an! ) 4a) 00? it ha! !ecline! to aroun! : thousan! mark 65a7al an! 8a))um00:;<. It is ar'ue! that the volatilit) is hi'h in the ullishC market than in the earC market.%he Repo rate as in!icator of monetar) polic) these )ears has also sho(n volatilit). $ince199? the Repo rates have een fluctuatin' et(een 3.? to 0.1.

%heoreticall), monetar) polic) affects the stock prices throu'h the (ealth effect channel an!the alance sheet channel as pointe! out ) Bernanke, +ertler an! +ilchrist 199>;, Bernankean! +ertler 1999; an! +oo!hart an! -ofmann 000;. %he tra!itional interest rate channel(hich implies that a ti'hter monetar) polic) lea!s to an increase in the interest rate that at

(hich the firmCs future cash flo(s are capitali7e! causin' stock prices to !ecline. hile theeasin' of the monetar) polic) increases the overall level of economic activit) an! stock pricerespon!s in a positive manner as in!icate! ) assola an! 4orana 002;. %he tra!itionalinterest rate channel (as also investi'ate! ) Bernanke an! Blin!er 199;, %horecke199:; an! Ri'oon an! $ack 003;. One thir! of the chan'es in the e*uit) prices areassociate! (ith ne(s on monetar) polic) 5air, 00;.

-o(ever, there is no stu!) availale in Pakistan that has investi'ate! the relationship et(een the stock prices an! the monetar) polic). %he core o@ective of the stu!), therefore,is to explore the impact of monetar) polic) on the returns to stock market.

1 %he authors are thankful to $a'hir Pervai7, ma! 4a7har an! E@a7 Ba@(a for the !ata.

8/12/2019 Impact of Monetray Policy on Stock Market

http://slidepdf.com/reader/full/impact-of-monetray-policy-on-stock-market 3/13

%he stu!) is arran'e! as follo(s. "fter this intro!uctor) part, section II overvie(s the stockmarket an! the monetar) polic) !evelopments in Pakistan. %he section III elaorates the

metho!olo'ical frame(ork. %he !ata availailit) an! preliminar) !ata anal)sis is !iscusse! insection IF. %he cointe'ration anal)sis an! E+"R- mo!el results are presente! in sectionF. %he FI section conclu!es the stu!).

"! #verview of the Stock Market and the Monetary Policy Developments

%he capital market in Pakistan is re'ulate! ) the $ecurit) an! Exchan'e ommission ofPakistan $EP; estalishe! in 199: ) replacin' the orporate /a( "uthorit). %here arethree stock exchan'es in Pakistan, namel) the #arachi $tock Exchan'e #$E;, the /ahore$tock Exchan'e /$E; an! the Islamaa! $tock Exchan'e I$E;. %hese are estalishe! on

192:, 19:2, an! 199:, respectivel). %he #arachi $tock Exchan'e #$E; is the main an!lea!in' stock Exchan'e. %he 'ro(th of the e*uit) market !urin' the !eca!e of 19>0s (as !ueto in!ustriali7ation policies pursue! ) the 'overnment of Pakistan. %he !eca!e of 19:0Csstarte! (ith political turmoil an! unrest in the eastern part of the countr). %he (orsenin'!omestic situation in the East Pakistan an! (ar (ith In!ia !isa''re'ate! Pakistan. %he outcome (as the separation of former East Pakistan an! emer'ence of ne( countr) Ban'la!esh.%he +overnment of Pakistan has a!opte! the polic) of nationali7ation of all t)pes of privatesector in!ustries an! financial institutions in 19:3=:2, (hich ha! completel) eliminate!

private sector out of the countr). %he ne( 'overnment reverse! an! formulate! the polic) of!enationali7ation of in!ustries an! financial institutions in 19A?=A>.

%he !eca!e of 1990Cs (itnesse! chan'es in the policies an! functionin' of the stock market.In the e'innin' of 1991 si'nificant measures (ere taken inclu!in' the openin' of the marketto international investorsG removal of constraints to repatriation on investment procee!s,'ains, an! !ivi!en!G !ere'ulation of econom) an! allo(in' commercial anks in the privatesectorG lierali7ation of forei'n exchan'e restrictions an! allo(in' Pakistanis to have forei'ncurrenc) accounts. %he market respon!e! positivel) to lierali7ation measure an!unprece!ente! increase in all in!icators (as oserve! in the first )ear of the openin' of themarket. %he ullish tren!s (ere oserve! in the first )ear. In terms of its performance, themarket (as ranke! thir! in 1991 6-usain an! 8a))um 00>;<. &evertheless in terms oflistin's the market !eepene!. %he ne( companies i.e., A>; (ere liste! !urin' the )ear that

helpe! to increase the turnover of shares an! market capitali7ation. %he market improve!si'nificantl) in terms of si7e an! activit). "s a result, the ratio of market capitali7ation to+DP increase! from :H to almost 1AH in the first )ear of lierali7ation an! further to >Hafter t(o )ears.

In 199? Pakistani e*uities market collapse! !ue to !omestic political crisis an! a!iscoura'in' economic outlook. #$E estalishe! a Defaultin' ompanies ounterC in"u'ust 199: for those companies (hich ha! committe! various !efaults un!er listin're'ulations of the Exchan'e. %he #$E has sho(n improvement !urin' 199:=9A. 5urther, the#arachi $tock Exchan'e intro!uce! a computeri7e! tra!in' s)stem i.e. a #"%$ #arachi"utomate! %ra!in' $)stem;. Due to !ifferent measures the numer of liste! companies rose

to :> in 000. In a!!ition the liste! capital an! market capitali7ation are 9,312.A millionan! 392,22?.: million respectivel). On the other han!, the 'ro(th in activit) in!icate! )

3

8/12/2019 Impact of Monetray Policy on Stock Market

http://slidepdf.com/reader/full/impact-of-monetray-policy-on-stock-market 4/13

tra!in' value an! turnover ratio (as tremen!ous. $ince late 90s the turnover ratio has een phenomenal an! increase! to almost ?00H in 003. "s a result Pakistan ranks first in the

(orl! in terms of turnover ratio. %he #$E has een amon' the est performin' markets forthe last t(o )ears.

Monetary Policy Developments

%he $tate Bank of Pakistan has een estalishe! on ul) 1, 192A as a central ank. %he ankin' s)stem ha! collapse! at the time of partitionG $BP at first ver) carefull) tookmeasures to rehailitate an! expan! the existent ankin' structure. %hese inclu!e! the!eclination of the forei'n anksC offer to open ranches in the interior of the countr) on the'roun!s that the local !ominance of the most po(erful financial sector of the econom) is inthe est interest of the ne( orn countr). %he &ational Bank of Pakistan (as thus estalishe!

in 1929. %o encoura'e the local anks to sprea! their ranches into the interior of the countr),the $BP provi!e! clearin' an! cheap remittance facilities. " numer of other speciali7e! anks an! (ere also set up namel) "'ricultural Development 5inance orporation in 19?an! "sian Development Bank in 19?9 J later mer'e! into "'ricultural Development Bank in19>1, Pakistan In!ustrial 5inance orporation in 19?: J later on converte! into In!ustrialDevelopment Bank, Pakistan In!ustrial re!it an! Investment orporation in 19?:, -ouseBuil!in' 5inance orporation in 19?, &ational Investment %rust, Investment orporation ofPakistan etc.

$BP has een usin' a selective cre!it control measures like the imposition of minimummar'in re*uirements as an instrument of monetar) polic). %he interest rate (as kept lo(!urin' 192A0=:0 to contain rise in the pulic !et an! to encoura'e lar'er expansion of the

ankin' cre!it for financin' the pulic an! private investment. %he $BP in a!!ition to the useof moral suasion (ith the anks to encoura'e len!in' to the small parties use! mar'inre*uirement as a tool. %o restraint the 'ro(th of mone) suppl) the reserve ratios (ere use!19>?. In a!!ition a 8uota $)stem (as intro!uce! in "u'ust 19>3, in respect of its a!vancesto the sche!ule! anks a'ainst 'overnment securities. n!er this a'reement anks (ereassi'ne! a *uota ever) *uarter e*ual to half of its statutor) reserves (ith the state ank in the

prece!in' *uarter. %he orro(in' e)on! this *uota (as su@ect to pro'ressivel) hi'h hi'herrates. In 19>? the *uota (as ma!e more strin'ent ) re!ucin' the amount from ?0 to ?

percent of the avera'e statutor) reserves an! makin' it applicale it for all t)pes of orro(in'of the anks from $BP.

" comprehensive ankin' reforms (as intro!uce! in 19: ) the 'overnment (ith

consultation of the ne( 'overnor $BP. %he emphasis (as on the flo( of the ank cre!it to priorit) sectors an! small usinessman in a'riculture an! in!ustr) throu'h the creation of the &ational re!it onsultative ouncil. -o(ever, o(in' to the ineffectiveness of the reformsthe $BP (as nationali7e! in 19:2. %he s)stem of the ceilin's on the cre!it ) the in!ivi!ual

anks to private sector remaine! a reall) potent (eapon to restrain 'ro(th of mone) an!cre!it. %hus the monetar) an! cre!it policies (ere !irecte! to(ar!s provi!in' a!e*uate cre!itto pro!uctive sectors in 'eneral an! priorit) sectors in particular

"s a result of Islami7ation of the econom), a compulsor) 7akat !e!uction of .? percent (aslevie! on savin' accounts an! other financial assets. %he elimination of ria interest; le! tothe s(itch of the &I%, IP an! $B5 to interest free operations. In 19A1, profit loss sharin'accounts (ere opene! in commercial anks alon'si!e the interest=earin' accounts. %he

capital (as provi!e! on the asis of profit an! loss sharin' mo!ara; an! mark=upmurahaa; asis in place of interest.

2

8/12/2019 Impact of Monetray Policy on Stock Market

http://slidepdf.com/reader/full/impact-of-monetray-policy-on-stock-market 5/13

%he e'innin' of the 90s (itnesse! the Bankin' Reforms II comprisin' of the market ase!

policies of s)stem an! cre!it mana'ement. In 199 the Pru!ential Re'ulations (ereintro!uce!. %his inclu!e! intro!uction of pulic !et auctionin', aolition of cre!it ceilin'an! cre!it !eposit ratio DR;, phasin' out of !irecte!, concessionar) cre!it an! finall)removal of cap on interest rates 6"shraf an@ua<. On 5eruar) 1, 199, the $BP exten!e! a 3!a) Repo facilit) for the %reasur) Bills. %he O4O, (hich $BP starte! on a! hoc asis inOctoer 1991, supplemente! ) the chan'es in the !iscount rates an! cash reservere*uirements an! issuance of % ills of !ifferent maturit) in une 199A, facilitate! in themana'ement of the monetar) an! cre!it expansion. In 1999 the multiple exchan'e rates)stem (as replace! ) unifie! exchan'e rate ) the $BP. 5rom ul) 1, 000, the inte'rationof the exchan'e rate an! the monetar) policies took place.

%he $BP 'aine! autonom) in 90s (ith the reforms. In 00, to stren'then the $BP autonom),the $tate Bank of Pakistan "ct, 19?>, (as amen!e!. " section 9B (as intro!uce! (hichfurther clarifie! the role of 4onetar) an! 5iscal Policies oor!ination Boar!. %o stren'thenthe $BP core ankin' capailities an! for creation of $BP Bankin' $ervices orporation. %herestructurin' le! to the formation of t(o susi!iaries. %he $BP Bankin' $ervices orporationin anuar) 00 an! %he &ational Institute of Bankin' an! 5inance &IB"5; in anuar)199:. Durin' the 19A9J000 perio!, monetar) an! cre!it policies mainl) operate! (ithin the"nnual re!it Plan "P;. In Decemer 000, the 5e!eral Investment Bon!s (erecomplemente! (ith Pakistan Investment Bon!.

Durin' 5K01, the monetar) polic) (as initiall) ti'htene! ) increasin' the !iscount rate

t(ice from 11 to 1 percent an! from 1 to 13 percent in $eptemer an! Octoer 000respectivel) an! increasin' the cash reserve re*uirement ) percent to effectivel) cur the!epreciation of the rupee. 4onetar) polic) (itnesse! an important transition in 00?, thefocus of the monetar) polic) shifte! on controllin' inflation rather then revivin' 'ro(th inthe econom). %he monetar) polic) (as a''ressivel) ti'htene! in the secon! half of the fiscal)ear. In or!er to cur cost push inflation, $BP raise! the !iscount rate for the first time afterune 001; !urin' "pril 00?, ) 1?0 asis points. %his rise in interest rates (as supporte!

) hi'h li*ui!it) asorptions throu'h O4Os an! a slo( !o(n in reserve mone) 'ro(th. %hiscouple! (ith hi'her acceptance ratio in %=ill auctions !urin' these months compare! (ithinitial nine months of the fiscal )ear, further !raine! inter ank li*ui!it) an! resulte! in anincrease in !iscountin' activities.

$! Methodolo%y

%he stu!) is ase! on time series econometrics. %he financial time series, particularl) stockmarket return, are not !istriute! normall)G the) 'enerall) are assume! to e hi'hl) #urtic.%he tests of ske(ness, #urtosis an! ar*ue=Bera test of normalit) are use! to anal)se the nonnormalit) of the !ata. %he "u'mente! Dicke) 5uller "D5; test of unit roots is use! to teststationarit) of the !ata Dicke) an! 5uller, 19:9, 19A1;. %he volatilit) of the stock returnsan! the repo rate is also seen ) plottin' the !ata.

?

8/12/2019 Impact of Monetray Policy on Stock Market

http://slidepdf.com/reader/full/impact-of-monetray-policy-on-stock-market 6/13

En'le an! +ran'er 19A:; t(o step metho! is use! to test the existence of cointe'ratin'relationship et(een the stock market prices an! the mone) market rate. %he first step

estimates the lon' run e*uation an! in the secon! step "D5 test is applie! on the resi!ualfrom the cointe'ratin' e*uation. %he En'le=+ran'er t(o step metho! is

/R$t L M N /RR t N t 1a;Qt L t=1 N1Qt=1 N Qt= N S N pQt=p N Tt 1;

(here /$PIt is lo' of stock price in!ex, /REP t is lo' of Repo rate, εt is resi!ual fromcointe'ratin' e*uation an! Tt is resi!ual from the e*uation of "D5 unit root test (hich isassume! to e (hite noise.

Because the ten!enc) of stock prices to e ne'ativel) correlate! (ith chan'es in the stock

volatilit), therefore, the relationship et(een the t(o markets, i.e., stock market an! Repomarket is estimate! ) utili7in' "R-=+"R- metho!s propose! ) En'le 19A;. %hesimple +"R- p, *; mo!el cannot capture the levera'e effect. #eepin' in vie( theimportance of levera'e effect in stock assets returns Bollerslev 19A>; an! &elson 1991;,amon'st others, have !evelope! the Exponential +eneralise! "utore'ressive on!itional-eteroske!ecit) E+"R-; mo!el. Braun et al 199?;, #roners an! &' 199>, 199A;, -enr)an! $herma 1999; an! En'le an! ho 1999; have exten!e! Exponential +eneralise!"utore'ressive on!itional -eteroscke!ecit) E+"R-; mo!el into ivariate version. %hemo!el helps us in the estimation oth static as (ell as !)namic forecast of the mean, forecaststan!ar! error an! the con!itional variance.

%his paper applies a ivariate F"R=E+"R- mo!el to investi'ate the relationship et(eenthe stock market an! Repo rate. %he F"R=E+"R- p, *; mo!el for the stock market is 'ivenin the follo(in' t(o e*uationsG

t t jt

m

j

jit

n

i

it ecsrr rsrs ε γ β β α ++++=

−−

=

−

=

∑∑ 1

01

0 a;

( ) ( )( )

1

111

1

lnln

lnln

−

−−−−

++

−+++=

t t

t t st st st

rr rr

zrs E zrs zrsrsrs

ϑ γ

β θ σ δ α σ ;

here i L 1, , .. , n an! @ L 0, 1, ..,m ε tUt=1 V &6 0, σs t;W<%he e*uation a; is vector autore'ressive F"R; mo!el of the con!itional mean e*uation ofreturns on stock market assets rst;. It in!icates that rst !epen!s on the past values of stockreturns rst=i;, the current an! past values of Repo rate rr t=@;, the error correction term ecs t=1;representin' the cointe'ratin' relationship et(een the stock market prices an! Repo rate,an! the ran!om variale. %he ran!om variale i.e., t; is assume! to have 7ero mean an!con!itional variance. -ence the secon! e*uation of the mo!el i.e., ; represents thecon!itional variance of the stock market returns.

%he exponential con!itional variance of stock market returns i.e., e*uation ; is !epen!ent

on the la''e! value of innovation of the stock returns an! the Repo rate returns, la' ofcon!itional variance of stock market an! the terms to capture as)mmetric effect. %he

>

8/12/2019 Impact of Monetray Policy on Stock Market

http://slidepdf.com/reader/full/impact-of-monetray-policy-on-stock-market 7/13

8/12/2019 Impact of Monetray Policy on Stock Market

http://slidepdf.com/reader/full/impact-of-monetray-policy-on-stock-market 8/13

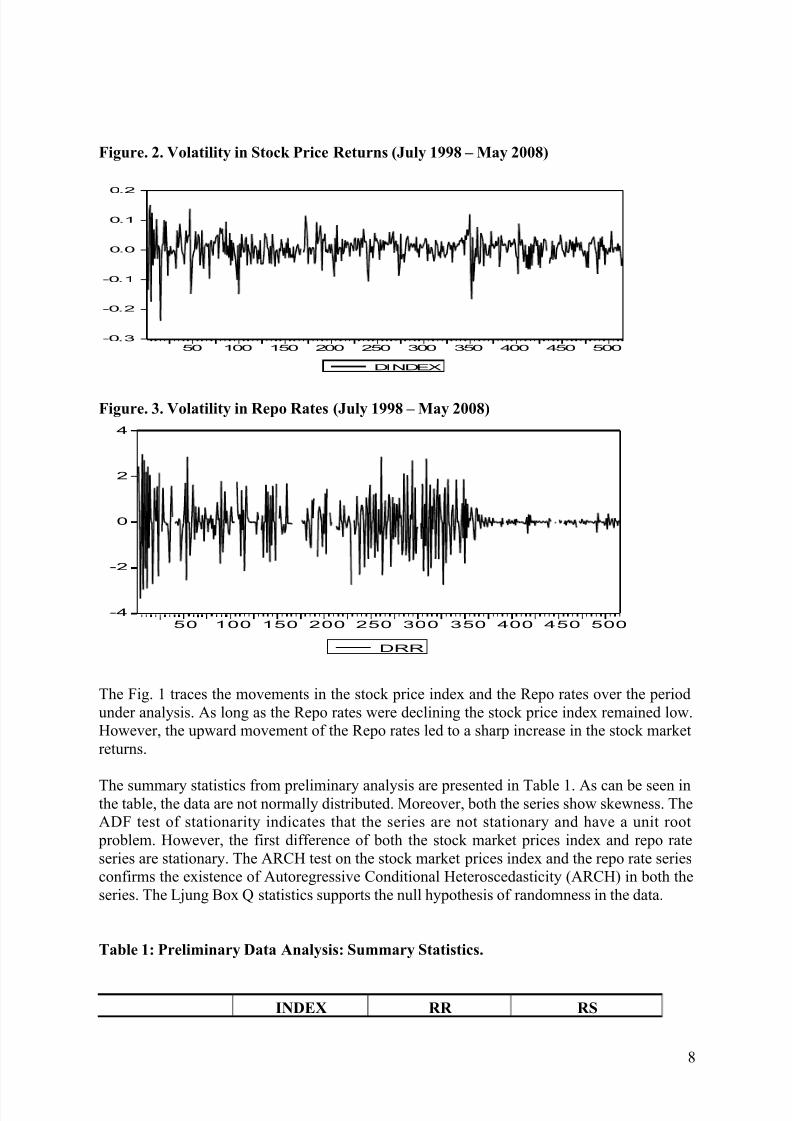

'i%ure! "! Volatility in Stock Price (eturns )*uly ++, - May "..,/

-0.3

-0.2

-0.1

0.0

0.1

0.2

50 100 150 200 250 300 350 400 450 500

DINDEX

'i%ure! $! Volatility in (epo (ates )*uly ++, - May "..,/

-4

-2

0

2

4

5 0 1 0 0 15 0 2 0 0 2 5 0 30 0 3 50 40 0 4 5 0 5 00

DRR

%he 5i'. 1 traces the movements in the stock price in!ex an! the Repo rates over the perio!un!er anal)sis. "s lon' as the Repo rates (ere !eclinin' the stock price in!ex remaine! lo(.-o(ever, the up(ar! movement of the Repo rates le! to a sharp increase in the stock marketreturns.

%he summar) statistics from preliminar) anal)sis are presente! in %ale 1. "s can e seen inthe tale, the !ata are not normall) !istriute!. 4oreover, oth the series sho( ske(ness. %he"D5 test of stationarit) in!icates that the series are not stationar) an! have a unit root

prolem. -o(ever, the first !ifference of oth the stock market prices in!ex an! repo rateseries are stationar). %he "R- test on the stock market prices in!ex an! the repo rate seriesconfirms the existence of "utore'ressive on!itional -eterosce!asticit) "R-; in oth theseries. %he /@un' Box 8 statistics supports the null h)pothesis of ran!omness in the !ata.

0able 1 Preliminary Data Analysis1 Summary Statistics!

I2DE3 (( (S

A

8/12/2019 Impact of Monetray Policy on Stock Market

http://slidepdf.com/reader/full/impact-of-monetray-policy-on-stock-market 9/13

4ean ?2.?1> >.:1A>A> 0.00?32:4e!ian 310?.1>0 :.A1?000 0.009:21

4aximum 1?>?2.:9 1:.A2000 0.1?014inimum ::2.:200 0. =0.3AA9?$t!. Dev 22>:.9A: 2.0339: 0.021A0$ke(ness 0.A02339 =0.010? =0.A030A#urtosis .21912 .1A2:? :.012A1:ar*ue = Bera >:.0392 12.1>2A9 39:.3>0AProailit) 0 0.000A20 0"D5 %est =1.A:A2A2 =A.?3A>:> -.39:39/@un' Box 12>::.13?? A2.???2A 29.19?0A

Oservations ?10 ?10 ?10

4! Empirical (esults

5ointe%ration Analysis

%he possiilit) of a lon' run relationship et(een the t(o series is investi'ate! ) appl)in'En'le=+ran'er 19A:; t(o step metho!. %his helps us to !etermine (hether an errorcorrection term shoul! e inclu!e! in the E+"R- mo!el or not. In the first step the stock

prices are re'resse! on the repo rates. %he results are presente! elo( t=statistics in

parenthesis;.

/R$ L 6.612589 N 0.006121 % = 0.016951 /RR A>.12; 9?.9; =1.A;

R=s*uare! 0.9? 5=statistics 2>0:.3A "D5 -2.791505

In the secon! step, the presence of cointe'ration et(een the t(o variales is teste! )appl)in' the "D5 test of unit roots on the resi!ual otaine! from the cointe'ration e*uation1a. %he En'le=+ran'er five percent critical value is 3.1:;. %he results thus in!icate the

existence of a unit root test in the resi!ual series, impl)in' that the t(o series are notcointe'rate! for the perio! un!er anal)sis. %his lea!s to the estimation of the E+"R-mo!el (ithout error correction term in the con!itional mean e*uations.

E6A(57 Model of Stock (eturns

%he ivariate E+"R- mo!el is estimate! ) the 4aximum /ikelihoo! 4etho! propose! ) Bollerlov an! ool!ri!'e 199;. %he results are presente! in the follo(in' e*uations.

9

8/12/2019 Impact of Monetray Policy on Stock Market

http://slidepdf.com/reader/full/impact-of-monetray-policy-on-stock-market 10/13

=1.A:91A; 1.A:19A; 3.21302;

000:31.00A0:20.001001.0 11 −− −+=

t t t rr rsrs

3a;(

( ) ( ) ( )

( )( )( ) ( )1.9A>3?.>?>:>A

ln00>:A3.0199>33.0

.?:?002A:.220A:.?0A=

0>1932.0ln923131.0?:93>3>.0ln

111

1

1

−−−

−−

+−

+++−=

t t t

t t t

rr zrs E zrs

zrsrsrs σ σ

3;

%he mean e*uation 3a; reveals that the returns to the stock market are not onl) affecte!si'nificantl) ) its la' ut the monetar) polic) in terms of the repo rates also pla)s asi'nificant role in !eterminin' the returns to the stock market. %hus an) increase !ecrease;in the repo rates, in!icatin' a monetar) polic) ti'htenin' expansionin';, !ecreasesincreases; the returns to the stock market. %he same is true for the variance e*uation 3;(here) an) increase !ecrease; in the repo rates, in!icatin' a monetar) polic) ti'htenin'expansionin';, enhances the volatilit) of the stock market (ith one (eek la'. Impl)in'there) that the monetar) polic) has a positive impact on the volatilit) of the stock market.

%he parameter , in!icate as)mmetric impact of ne(s on the stock market return. If it is

ne'ative, a ne'ative innovation ten!s to reinforce the si7e effect, (hile a positive innovationten!s to partial out. In case of Pakistan, it is positive an! statisticall) si'nificant. %he positivean! si'nificant value implies that positive ne(s ten!s to amplif) the interest rate volatilit)more than the ne'ative ne(s.

%he relative importance of the ne'ative innovation to the positive innovation is 0.AA,measure! ) the ratio Z=1N Z[ 1N ;. %his ratio also consi!ers the !ifferin' impact of amarketCs o(n innovation on the current con!itional variance 6Kan' an! Doon' 002;<. Itreveals that the positive innovation in the stock market have a one time lar'er impact onvolatilit) of the stock market returns than the impact of ne'ative innovations in the stockmarket.

%he sum of "R- an! +"R- coefficients is 1. If it is close to one, it reflects the persistence in the volatilit) shocks. %he sum of "R- an! +"R- coefficients in case ofPakistan sho(s that the volatilit) shocks in the stock market returns have een ver) persistentan! the) !ie out rather slo(l).

Base! on the half=life of a shock, the life of volatilit) is measure! as ln 0.?;[ ln Y;. It turnsout to e almost 1 (eeks. %his implies that it takes almost t(elve (eeks for the stock marketto re'ress halfJ(a) ack to its stea!) state value 64ari +. Re)es 199>;<.

%he levera'e effect is statisticall) si'nificant in case of Pakistan. %his implies that the pastne'ative shocks increase current volatilit) more than !o past positive shocks.

10

8/12/2019 Impact of Monetray Policy on Stock Market

http://slidepdf.com/reader/full/impact-of-monetray-policy-on-stock-market 11/13

%he monetar) polic) (ith one (eek la' enhances the volatilit) of the stock market returns.

2ews Impact 5urve of Stock Market (eturns

0

500

1000

1500

2000

2500

3000

-10 -5 0 5

Z

S I G 2

+iven information up to current time, the ne(s impact curve examines the relationship et(een the ne(s an! future volatilit). %he ne(s impact curve plots ne(s scenarios on thehori7ontal axis a'ainst the resultin' volatilit) on the vertical axis. %he curve sho(s that thecon!itional variance of the stock market returns reacts !ifferentl) to e*ual ma'nitu!es ofne'ative an! positive shocks. "n increase in the stock market returns lea!s to moreuncertaint) (hen compare! to a !ecrease of e*ual ma'nitu!e.

8! 5onclusion

In an econom) there are several paths an! channels throu'h (hich monetar) polic) can effect

the real activit) of the econom). %he tra!itional transmission mechanisms of the monetar) polic) i.e. the cre!it an! the mone) channel, have one thin' common that the) operatethrou'h the financial market. 4ost economists a'ree that the stock market price in!ex, ein'one of the lea!in' in!icators in the !evelope! economies, is affecte! ) the monetar) polic)rules. %hus in!icatin' that i!entif)in' the link et(een the monetar) polic) an! the stockmarket is hi'hl) important to 'ain useful insi'ht of the transmission mechanism of themonetar) polic).

%his paper a!!resses the linka'es et(een the monetar) polic) an! the stock market inPakistan. %he estimation techni*ue emplo)e! inclu!es En'le +ran'er t(o step proce!ure an!the ivariate E+"R- metho!. %he results in!icate that in case of Pakistan the stock marketis sensitive to the chan'es in the monetar) polic).

11

8/12/2019 Impact of Monetray Policy on Stock Market

http://slidepdf.com/reader/full/impact-of-monetray-policy-on-stock-market 12/13

(eferences

Bernanke, B. an! #uttner, &. 00?; hat Explains the $tock 4arketCs Reaction to the5e!eral Reserve Polic)\, The Journal of Finance, Fol. /], 11=1?:

Bollerslev, %. 19A>; +enerali7e! "utore'ressive on!itional -eterosce!asticit), Journal of

Econometrics, 31

assola, &. an! 4orana, . 002; 4onetar) Polic) na! $tock 4arket in the Euro "rea.ouirnal of Polic) 4o!ellin' >, 3A: J 399.

En'le, R. 5., an! +ran'er, . . 19A:; ointe'ration an! Error orrection Representation,

Estimatin' an! %estin', Econometrica, ??, ?1, :>En'le, R. 5. 19A; "utore'ressive on!itional -eteroske!asticit) an! Estimates of the

Fariance of # Inflation, Econometrica, Fol. ?0, 9A:=100A

5air, Ra) . 00; Events that $hook the 4arket. ournal of Business, :?,:13 J :31.

+oo!hart, ., an! -ofmann, B. 000; 5inancial Fariales an! the con!uct of 4onetar)Polic)^, Sveriges Riskbank Working Paper , &o. 1.

Ioanni!is, . an! #ontonikas, ". 00>; 4onetar) Polic) an! the $tock 4arket $ome

International Evi!ence, Universit of !lasgo" Working Paper , &o. 00>_1.

an@ua, "sharf 003;, #istor of the State $ank of Pakistan %&''(%&)), $BP.

an@ua, "sharf 002;, #istor of the State $ank of Pakistan %&))(*++,, $BP.

&elson, D. B. 1991; on!itional -eterosce!asticit) in "sset Returns " &e( "pproach, Econometrica, Fol. ?9, 32:=3:0

&ia7i, ". #. 00?; 4onetar) Polic) in -istorical Perspective Pakistan Experience, 19:A=00?;, Pakistan $usiness Revie", Fol. A 3;, 3=23.

&ia7i, ". #. 00:; 4onetar) Polic) in -istorical Perspective Pakistan Experience, 19:0=19:A;, Pakistan $usiness Revie", Fol. A 2;, 3=20.

Patelis, "lex. D. 199:; $tock Return Pre!ictailit) an! the Role of 4onetar) Polic), The

Journal of Finance, Fol. ??;, 19?1=19:.

1

8/12/2019 Impact of Monetray Policy on Stock Market

http://slidepdf.com/reader/full/impact-of-monetray-policy-on-stock-market 13/13

13