Embed Size (px)

Citation preview

Impact of Energy Crops on World markets

Alastair Dickie

Director, Crop Marketing, HGCA

If we want biofuels, …

• are we going to starve?

• can Food and Fuel from agriculture co-exist?

• will we damage the Environment?

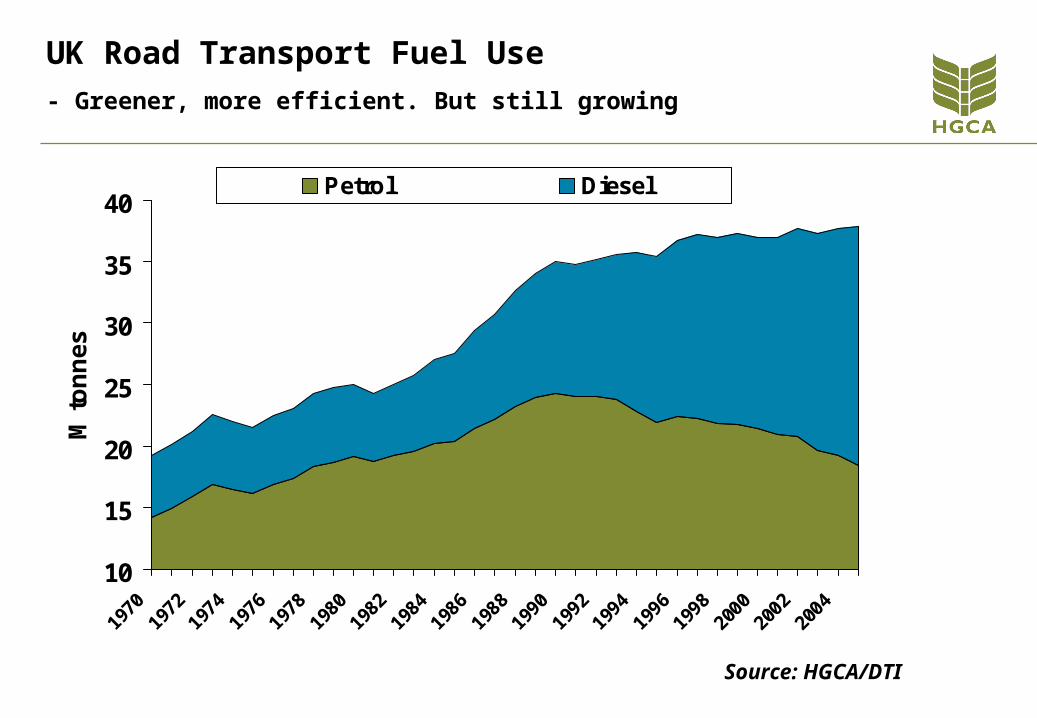

Source: HGCA/DTI

UK Road Transport Fuel Use- Greener, more efficient. But still growing

10

15

20

25

30

35

40

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

M t

on

ne

s

Petrol Diesel

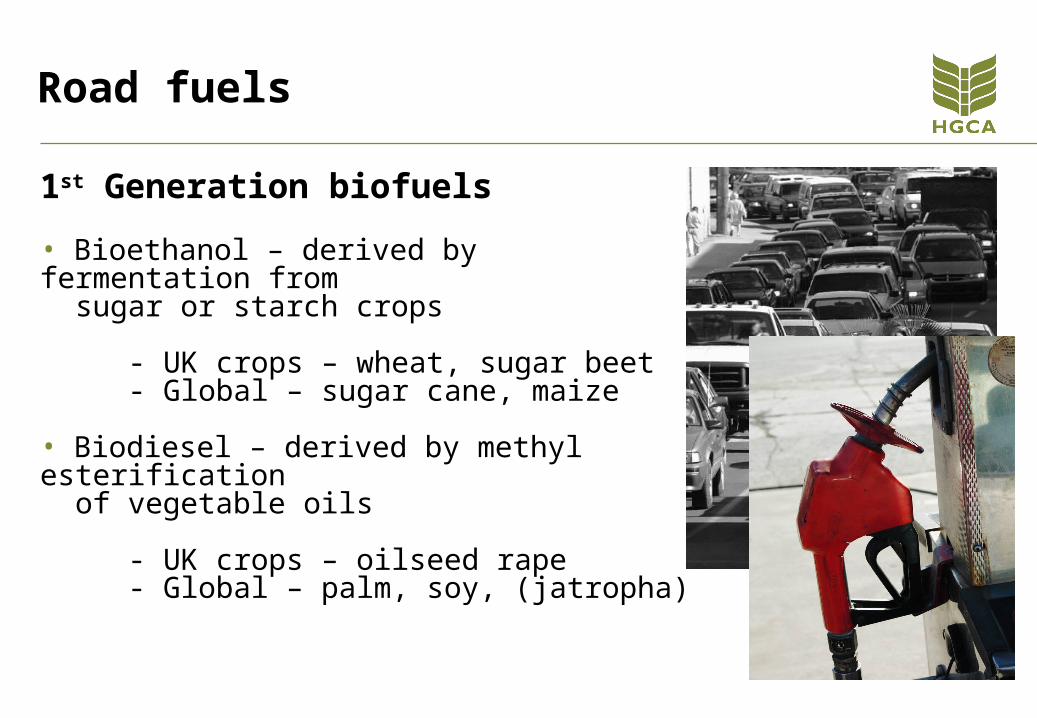

Road fuels

1st Generation biofuels

• Bioethanol – derived by fermentation from sugar or starch crops

- UK crops – wheat, sugar beet- Global – sugar cane, maize

• Biodiesel – derived by methyl esterification of vegetable oils

- UK crops – oilseed rape- Global – palm, soy, (jatropha)

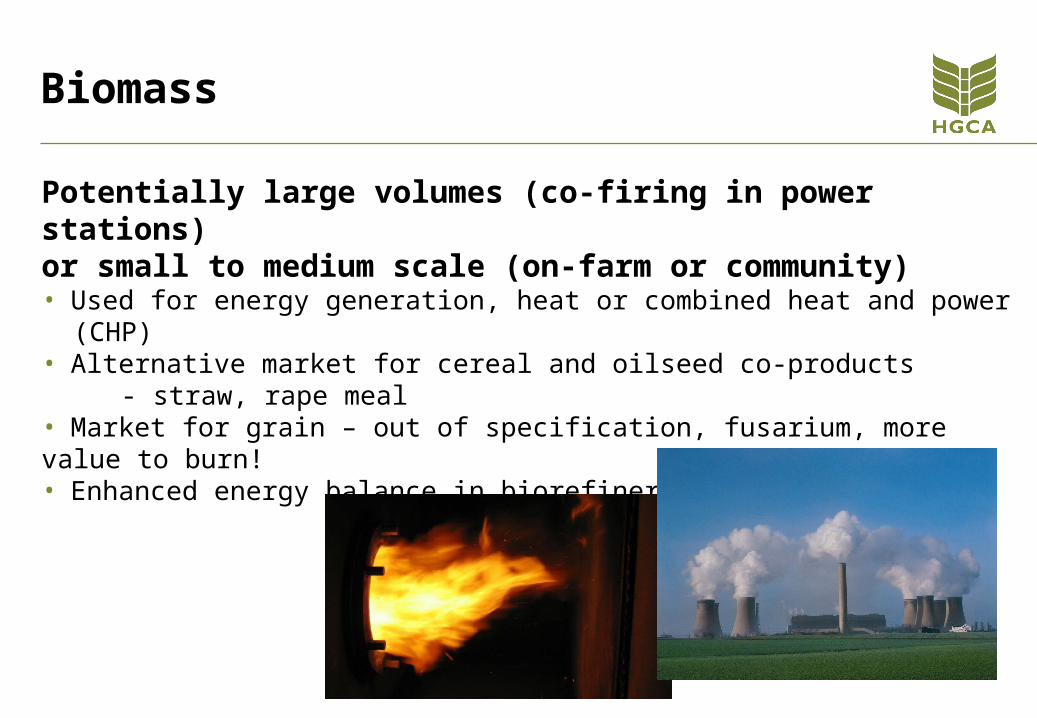

Biomass

Potentially large volumes (co-firing in power stations)or small to medium scale (on-farm or community)• Used for energy generation, heat or combined heat and power (CHP) • Alternative market for cereal and oilseed co-products

- straw, rape meal• Market for grain – out of specification, fusarium, more value to burn!• Enhanced energy balance in biorefinery

EU and World positions

EU• The 5.75% obligatory inclusion rate will require the equivalent of

24 MT of grain • Grain surplus 10-25 MT • 4M Ha in setaside plus land coming out of sugar production

World• Interest mainly with bioethanol• Brazil and US are leading producers in ethanol• US Energy Policy Act 2005

- Renewable Fuel Standard (Sec. 1501) 7.5 billion gallons by 2012

• Large biodiesel interest in EU only

World Fuel ethanol productionM

illi

on

lit

res

Brazil

US

Canada

EU

World

Source: FO Lichts

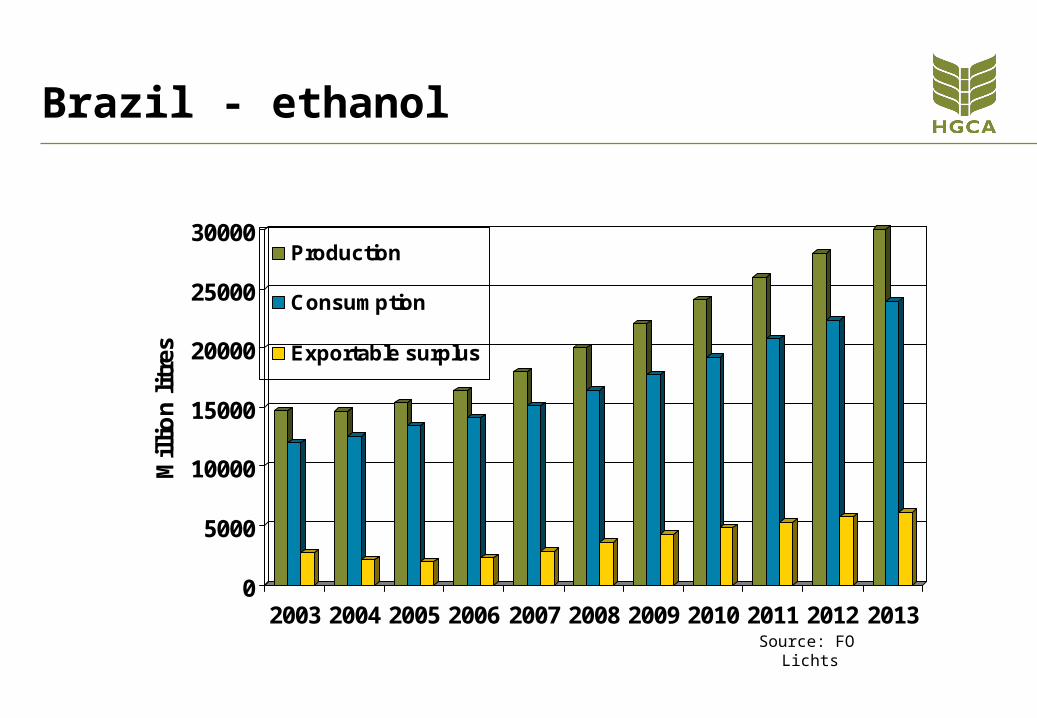

Brazil - ethanol

0

5000

10000

15000

20000

25000

30000

Mil

lio

n l

itre

s

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Production

Consumption

Exportable surplus

Source: FO Lichts

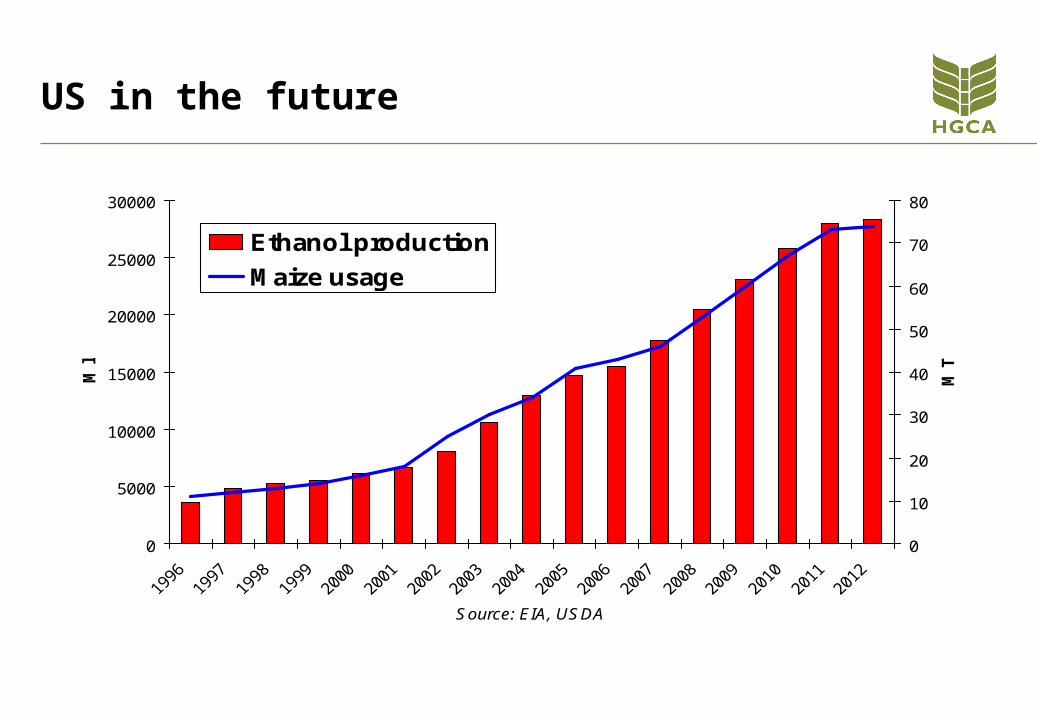

US in the future

0

5000

10000

15000

20000

25000

30000

Source: EIA, USDA

M l

0

10

20

30

40

50

60

70

80

M T

Ethanol production

Maize usage

Future Ethanol Consumption

Projected Fuel Ethanol Consumption. Source: IEA

0

20000

40000

60000

80000

100000

120000

140000

1975 1980 1985 1990 1995 2000 2005 2010 2015 2020

Year

Mill

ion

Lit

res

Brazil US & Canada EU World

EU biodiesel production

0

1000

2000

3000

4000

5000

6000

7000

2002 2003 2004 2005 2006

Source: EBB

Mt

Others

Czech Republic**

United Kingdom

Austria

Italy

France

Germany

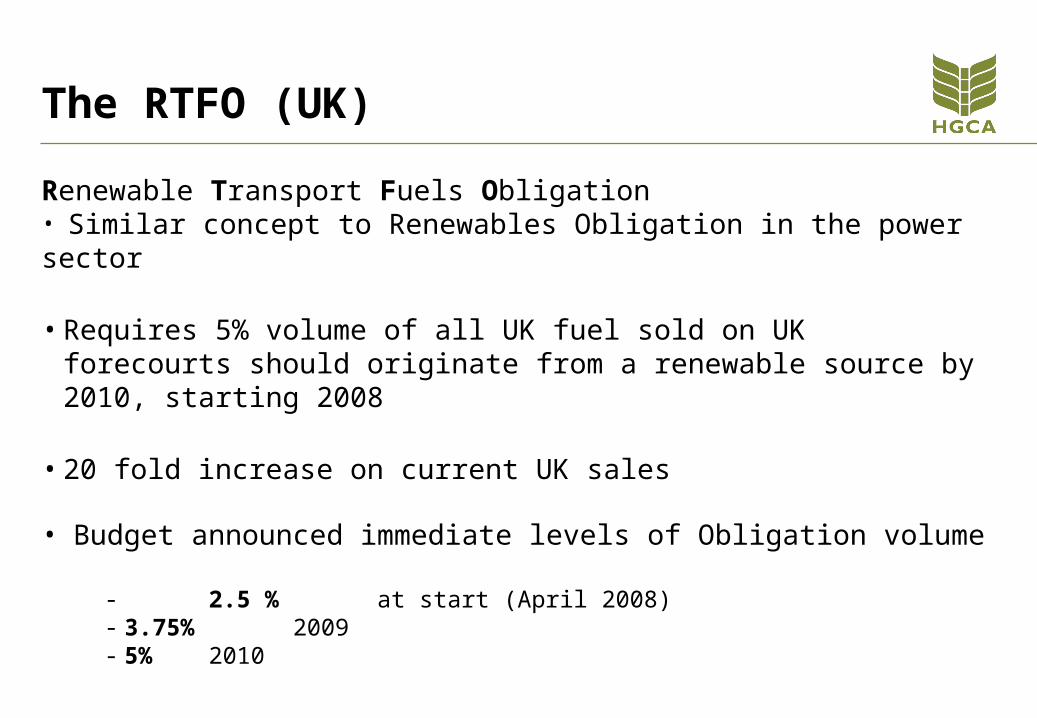

The RTFO (UK)

Renewable Transport Fuels Obligation• Similar concept to Renewables Obligation in the power sector

• Requires 5% volume of all UK fuel sold on UK forecourts should originate from a renewable source by 2010, starting 2008

• 20 fold increase on current UK sales

• Budget announced immediate levels of Obligation volume

- 2.5 % at start (April 2008)- 3.75% 2009- 5% 2010

UK Biofuel Production capacity

0

500

1000

1500

2000

2500

'000 tonnes

2005

/06

2006

/07

2007

/08

2008

/09

2009

/10

2010

/11

Biodiesel

Bioethanol

Source: Industry and HGCA

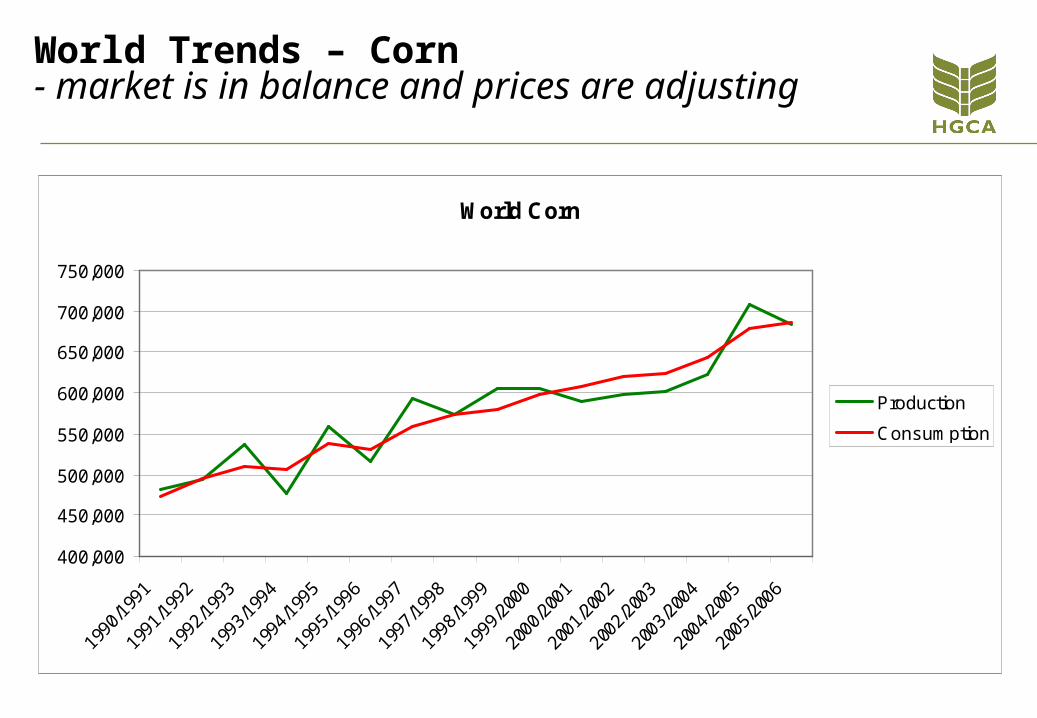

World Corn

400,000

450,000

500,000

550,000

600,000

650,000

700,000

750,000

Production

Consumption

World Trends – Corn- market is in balance and prices are adjusting

400,000

450,000

500,000

550,000

600,000

650,000

700,000

750,000

Production Consumption net

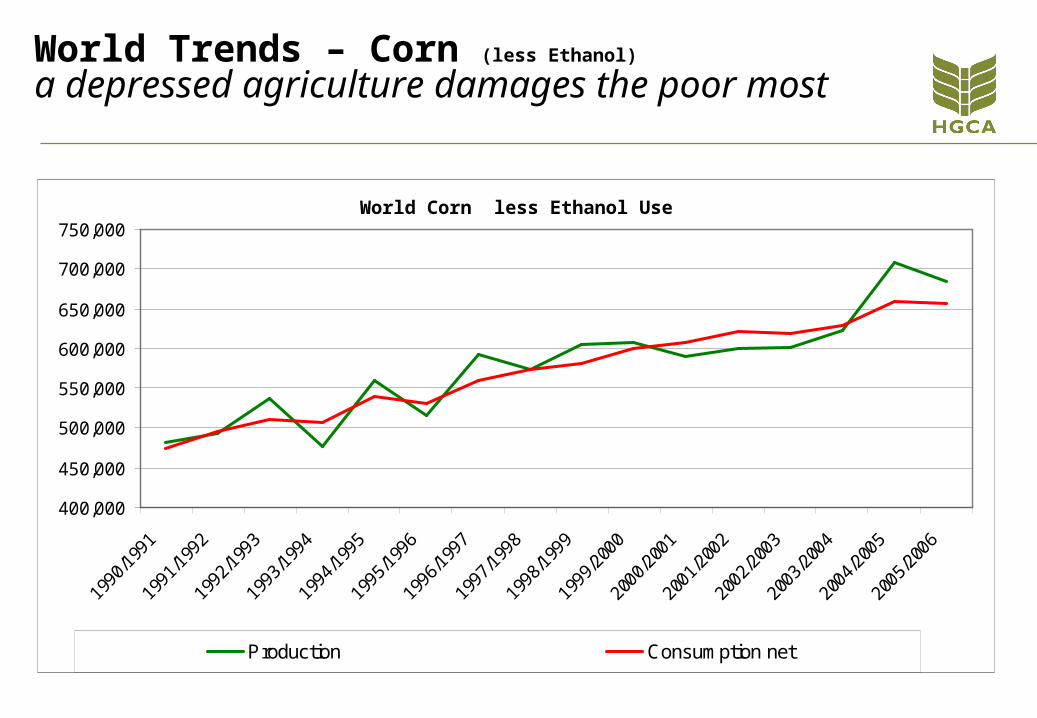

World Corn less Ethanol Use

World Trends – Corn (less Ethanol)

a depressed agriculture damages the poor most

Source: HGCA

Bio-fuel and petroleum price linked – new market dynamics to manage

050

100150200250300350400450

Apr-05

Jul-05

Oct-05

Jan-06

Apr-06

Jul-06

Oct-06

US

cen

ts p

er

gall

on CBOT ethanol NYMEX petroleum

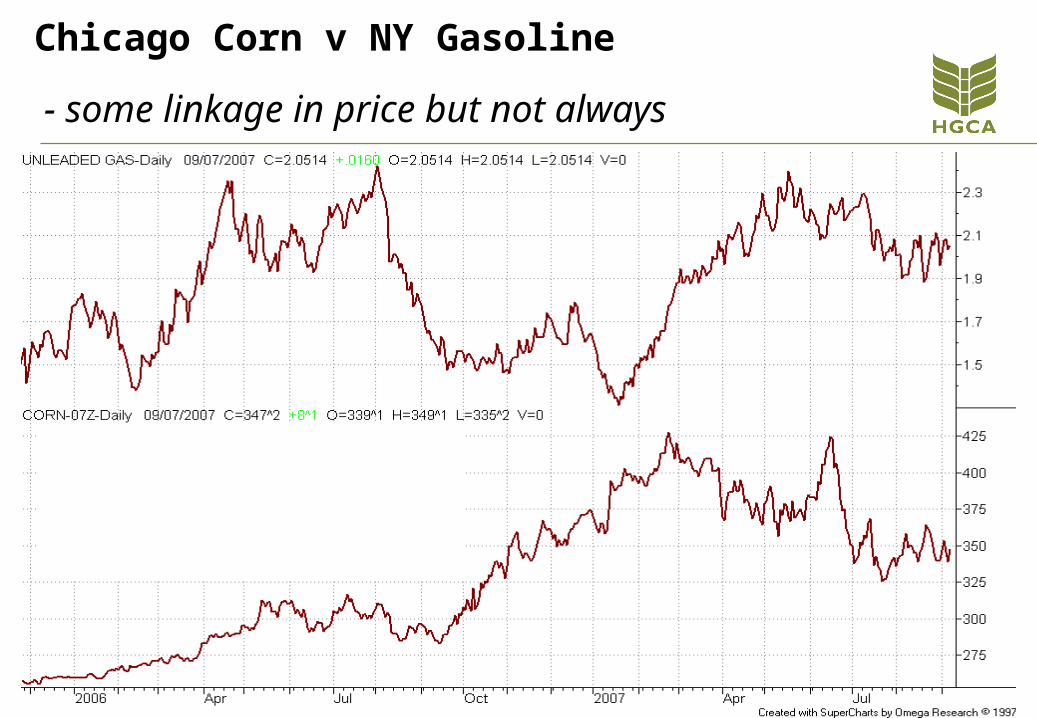

Chicago Corn v NY Gasoline

- some linkage in price but not always

Chicago Bean oil v NY Diesel - demand leakage gives price influence

-20

-10

0

10

20

30

40

50

60

70

80

Wo

rld

wh

ea

t e

nd

sto

cks M

to

nn

es

90

110

130

150

170

190

210

230

250

270

290

CB

OT

SR

W w

he

at fu

ture

s $

pe

r to

nn

e

Production response World wheat price at sowing

Source: USDA/HGCA/SAC

High forward prices - will lead to a global supply response

IranKey Exporters Key Importers

Key EU Importers New Exporters

Poor people can grow grain- export possibilities from new areas

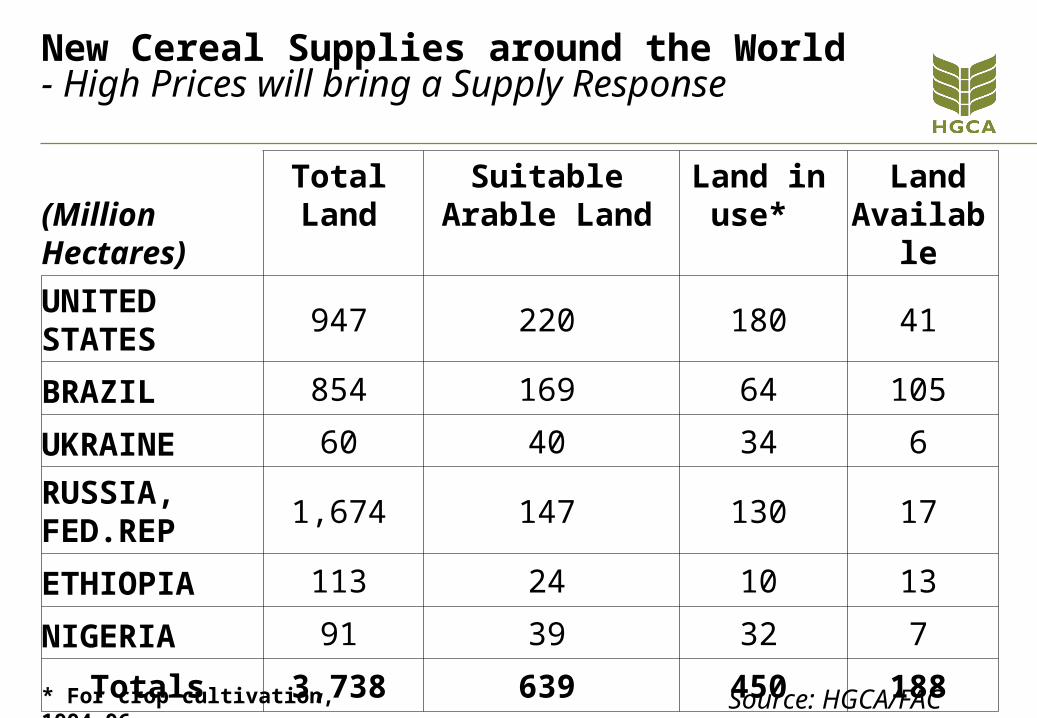

New Cereal Supplies around the World- High Prices will bring a Supply Response

(Million Hectares)

Total Land

Suitable Arable Land

Land in use*

Land Available

UNITED STATES

947 220 180 41

BRAZIL 854 169 64 105

UKRAINE 60 40 34 6

RUSSIA, FED.REP

1,674 147 130 17

ETHIOPIA 113 24 10 13

NIGERIA 91 39 32 7

Totals 3,738 639 450 188* For crop cultivation, 1994-96 Source: HGCA/FAC

So let’s answer the questions!• Are we going to starve?No we are going to increase the production of cereals and oilseeds to meet the new demands. This will involve cropping on land previously idle.

• Can Food and Fuel from agriculture co-exist?Of course they can, fuel crops and food crops will be balanced by the distribution of market prices so that supply & demand are balanced

• Will we damage the Environment?This is a more challenging question. As more land is drawn into production we have to beware of abuse to eco-systems and carbon efficiency

… let’s work together to improve our world

Thank you