Embed Size (px)

Citation preview

Impact Evaluation of Business License Simplification in Peru

October 2012

An Independent Assessment of an International Finance Corporation-Supported Project

Impact Evaluation of Business License Simplification in Peru: An Independent Assessment of an International Finance Corporation-Supported Project

i

© 2013 Independent Evaluation Group The World Bank Group 1818 H Street NW, Washington DC 20433 Telephone: 202-458-4497

Internet: http://ieg.worldbankgroup.org

E-mail: [email protected]

Some rights reserved

1 2 3 4 5 15 14 13

This work is a product of the staff of the Independent Evaluation Group (IEG). Note that IEG and the World Bank Group do not necessarily own each component of the content included in the work. IEG and the World Bank Group therefore do not warrant that the use of the content contained in the work will not infringe on the rights of third parties. The risk of claims resulting from such infringement rests solely with you.

The findings, interpretations, and conclusions expressed in this work do not necessarily reflect the views of IEG, the World Bank, its Board of Executive Directors, or the governments they represent. IEG and the World Bank Group do not guarantee the accuracy of the data included in this work. The boundaries, colors, denominations, and other information shown on any map in this work do not imply any judgment on the part of IEG and the World Bank Group concerning the legal status of any territory or the endorsement or acceptance of such boundaries.

Nothing herein shall constitute or be considered to be a limitation upon or waiver of the privileges and immunities of IEG or the World Bank Group, all of which are specifically reserved.

Rights and Permissions

This work is available under the Creative Commons Attribution 3.0 Unported license (CC BY 3.0) http://creativecommons.org/licenses/by/3.0. Under the Creative Commons Attribution license, you are free to copy, distribute, transmit, and adapt this work, including for commercial purposes, under the following conditions:

Attribution—Please cite the work as follows: IEG (Independent Evaluation Group). 2012. Impact Evaluation of Business License Simplification in Peru: An Independent Assessment of an International Finance Corporation-Supported Project. Washington, DC: World Bank. License: Creative Commons Attribution CC BY 3.0.

Translations—If you create a translation of this work, please add the following disclaimer along with the attribution: This translation was not created by the Independent Evaluation Group or the World Bank Group and should not be considered an official IEG/World Bank Group translation. IEG and the World Bank Group shall not be liable for any content or error in this translation.

All queries on rights and licenses should be addressed to IEG, 1818 H Street, NW, Washington, DC 20433, USA; fax: 202-522-3125; e-mail: [email protected].

Cover photo: Lima, Peru, fruit stall. © Holger Mette/iStock.

Library of Congress Cataloging-in-Publication Data have been applied for.

i

Contents

ACKNOWLEDGMENTS ........................................................................................................................ III

OVERVIEW ............................................................................................................................................. V

ABBREVIATIONS ................................................................................................................................. IX

1. INTRODUCTION ................................................................................................................................. 1

IFC’s Support to Licensing Reform in Lima ............................................................................................................... 3 Broader Issues .......................................................................................................................................................... 5 Previous Evaluations on Business Licensing ............................................................................................................ 6

2. IMPACT OF REFORM ON COSTS AND REGISTRATIONS ............................................................. 9

3. POTENTIAL BENEFITS FROM LICENSE SIMPLIFICATION—EVIDENCE FROM ENTERPRISE OUTCOMES ......................................................................................................................................... 12

Data and Regression Methodology ......................................................................................................................... 12 Evidence from the First Four Rounds of the Enterprise Survey .............................................................................. 13 Evidence from the Fifth Round of the Enterprise Survey ........................................................................................ 18 Benefits from License Simplification—Evidence from Enterprise Behavior ............................................................ 19

4. COST-BENEFIT ASSESSMENT OF THE LICENSE REFORM ....................................................... 23

5. CONCLUSIONS, POLICY IMPLICATIONS, AND IMPLICATIONS FOR IFC .................................. 30

Conclusions ............................................................................................................................................................. 30 Policy Implications ................................................................................................................................................... 32 Implications for IFC ................................................................................................................................................. 33

APPENDIX: DATA TABLES ................................................................................................................ 35

REFERENCES ...................................................................................................................................... 39

ENDNOTES .......................................................................................................................................... 41

Tables

Table 2.1. Summary of Reduction in Costs and Procedures to Obtain a License ................................. 10 Table 3.1. Before-and-After and Double-Difference Estimates of Impact .............................................. 14 Table 3.2. Impact on Revenues (in constant price Peruvian Nuevo Soles) ........................................... 14 Table 3.3. Impact on Profits per Worker ................................................................................................ 15

CONTENTS

ii ii

Table 3.4. Impact on Employment (including owner) .............................................................................15

Table 3.5. Impact on Revenues (constant Nuevo soles) .......................................................................18 Table 3.6. Impact on Profits per Worker (constant Nuevo soles) ...........................................................19 Table 3.7. Impact on Employment (including owner) .............................................................................19

Table 3.8. Costs and Benefits of Getting Licenses—Number of Times Each Item Mentioned by Survey Respondents in First Round of Survey ..................................................................................................22 Table 4.1. Baseline Values and Assumptions Used in Simulations .......................................................26 Table 4.2. Simulation Results: Number of Formal and Informal Firms ...................................................26 Table 4.3. Simulation Results: Number of Firms Experiencing Licensing Costs ....................................26

Table 4.4. Reduction in Waiting Time and Fees Used in the Cost-Benefit Analysis ..............................27 Table 4.5. Sensitivity Analysis ...............................................................................................................28

Figures

Figure 1.1. Central District in Lima Where Reforms Were Implemented . Error! Bookmark not defined. Figure 3.1. Eligible Enterprise Owners Judging the License Worth Getting If the Full License Fee Were Paid .......................................................................................................................................................21

iii

Acknowledgments

This evaluation was prepared by Andrew M. Warner (Task Manager) with

management oversight and valuable comments provided by Marvin Taylor-

Dormond, Ade Freeman, and Stoyan Tenev. In Lima, Miguel Jaramillo and

colleagues at Grupo para Analysis de Desarollo provided valuable assistance in

organizing and collecting new data. Additional helpful comments at various stages

of this evaluation were received from Geeta Batra, Hans-Martin Boehmer, Alexis

Diamond, Surajit Goswami, Caroline Heider, Ali Khadr, Michael Pomerleano,

Alexandra Santillana, Christine Wallich, and Izlem Yenice. Peer review comments

were received from Jeffrey Tanner (Economist, IEG) and Markus Goldstein (Senior

Economist, Africa Poverty Reduction and Economic Management Network, front

office, and Development Economics/Chief Economist, Poverty and Inequality,

World Bank).

v

Overview

It is often claimed that inefficient business regulations and procedures lock enterprises into a vicious circle of informality, where firms have little effective access to financing and are constrained in their ability to grow and prosper beyond the status of microenterprises. At issue are not only the merits of specific business regulations but also the drag on development represented by informality itself.

This evaluation verifies and validates previous conclusions and findings and also presents new evidence. It looks at the effects of reforms supported by the International Finance Corporation’s (IFC’s) Business License Simplification Project in the municipality of Lima, Peru. Under this project, IFC’s Foreign Investment Advisory Services worked with the municipality of Lima to reform the administrative process for obtaining a business license in Cercado de Lima, one of 44 districts that comprise metropolitan Lima. Two evaluations of the project were conducted, sponsored by IFC (see Schnabl, Mullainatha, and Kronberger 2007 and Alcázar, Andrade, and Jaramillo 2011). The first asked whether simplification of business regulations increased registrations; the second asked whether registrations caused improved enterprise outcomes.

New evidence is also presented from an additional survey of the Peru project sponsored by the Independent Evaluation Group (IEG). The IEG survey collected information on a question left unanswered by the earlier evaluations: whether the lack of evidence for impact in those evaluations was the result of insufficient passage of time between the implementation of the project and the collection of data.

In answering whether the license simplification and cost reductions in Peru did in fact lead to greater registration, this evaluation separates the question into two components: Did the reforms reduce costs and procedures, and did the reduction in procedures increase registrations?

The answer to the first question is yes. Even though various sources cite different statistics, they all point to significant reductions in time required, monetary costs, and number of procedures. Available evidence suggests that the median number of days to obtain a license fell from 40 to 16; the average number of requirements to register a business fell from 8 to 4; the median cost fell from $188 to $91; and both the number of visits to municipal offices and the number of inspections fell from 4 to 2. The rise in registrations after the reforms was dramatic: from 1,711 to 8,457 in the first year before settling down to 1,978 in the third year.

Did the increased level of formality lead to better enterprise outcomes? Some have argued that productivity will increase as formal status improves access to financing, facilitates investment, and removes implicit barriers to business growth. IFC and the Business Registration Evaluation Group (BREG) sponsored a second evaluation of the effects of the reforms and found no evidence to support this hypothesis. That evaluation attracted attention because the data collected and the methods used were unusually high quality; in particular, the data collected permitted controls to be introduced for possibly confounding variables and offered a new instrumental variables approach to confront the problem of self-selection bias.

In the present review, the conclusions based on these data were confirmed and the results

OVERVIEW

vi

were replicated. The group of enterprises that obtained licenses in response to the offer of a financial incentive did not exhibit significantly higher average revenues, profits per worker, or employment. Furthermore, the empirical results confirmed here are similar to the results cited in a study of enterprises in Sri Lanka (De Mel, McKenzie, and Woodruff 2012). This latter study found that enterprise sales and employment were not higher after formal status was obtained but that average profits were higher, only because very few firms made huge gains. As in the present evaluation, they found no evidence for broad gains across many firms and many outcome variables.

Three arguments against these findings should be considered. The first is that the (moderately) small sample and the low statistical power of the financial incentive mean that the estimates have a large statistical error. In reply, the maximum possible impact consistent with the data was estimated using new data, and it was found that even these maximum estimates were not large either, ranging from 2 to 28 percent of the relevant means. A second critique is that the results may only apply for the kinds of enterprises in the study, which are mostly retail establishments in service sectors in the center of a city. The response to these arguments is that IFC should test this hypothesis with equally good evidence, as in the IFC-BREG evaluation, to see if positive effects exist for other kinds of enterprises.

A final concern about the potential validity of the findings of the IFC-BREG-sponsored evaluation is that it did not allow sufficient time to elapse for impacts to emerge. To test this criticism, IEG conducted a fifth round of the enterprise survey in May 2012, a further 18 months after the fourth-round survey of November 2010. Overall, the new data offer no evidence that the short passage of time from the earlier evaluation was responsible for the lack of results. There are no statistically

significant positive results for either revenues or profits per worker. There is evidence that employment rose, but only because it declined by a greater amount in the control group, compared with the treatment group. The maximum possible effect is a 28 percent increase in revenues, a 25 percent increase in employment, and a 2 percent increase in profits per worker.

What does this say about policy toward informality? In general, the case for state intervention to promote formality would be strengthened by evidence first that there are large positive effects for enterprise outcomes; second, that enterprises were uninformed about these or tended to underestimate the benefits; or third, that informal status imposes negative externalities on others in society. The evidence here casts doubt on the first argument and in doing so, tends to undercut the premise from the second argument, because it is difficult to argue that firms are poorly informed about the benefits of formal status if little evidence has been found for those benefits.

On the related point of whether enterprise owners were acting rationally by avoiding registration, the evidence is consistent with rational behavior that 55 percent of the enterprises were willing to register when presented with the offer to pay the license fee. This does not necessarily constitute irrational behavior, given all the other costs and benefits of registration, and may in fact be surprisingly high.

When surveyed, enterprise owners show they were aware of items on both the cost and benefit side of the ledger. On the cost side, they most often mentioned the license fees; on the benefit side, the stress and worry of not being registered was frequently mentioned, as was the risk of paying fines. On the final point, however, the evidence here does not say anything either way about the effect of further externalities associated with

OVERVIEW

vii

informalities, such as unfair competition for the formal sector or higher taxes for legitimate enterprises.

What does the evidence say on the ultimate question of whether the license reform was worthwhile based on a cost-benefit analysis? IEG’s calculations indicate that the value to the enterprise owners of the reduction in required office visits, in terms of time savings, would alone justify the cost of the program to IFC. Adding to this the value of the reduction in time to obtain a license further reinforces the point. Saving time and less hassle are benefits that are pure gains to society, as there are no groups that gain from enterprise owners waiting in line or wasting their time on redundant procedures.

In contrast, the reduction in the license fee, although a clear and significant benefit for enterprise owners, means a reduction in municipal revenues, which in turn has some costs to society that are difficult to quantify. The fact that saved time and hassle are quantitatively significant also means that the fundamental justification for projects such as license simplification does not hinge on the question of whether formality causes extra productivity-related benefits to firms.

Regarding IFC, the second IFC-BREG evaluation is a notable example of good practice for several reasons: It addressed a fundamental question at the heart of the justification for the project; and it was based on unique data collected to conduct a test that was capable of delivering accurate answers, and for that reason was influential. The double-difference results (see tables 3.2–3.7) illustrate the pitfalls of relying on before-and-after evidence, as is done in many current

evaluations—conclusions can look very different when there is a control group.

Overall, the results suggest there is little evidence for benefits of higher enterprise profits, revenues, or employment from formalization. This evidence enables IFC to advance the debate and work toward a more focused understanding of what is reasonable to expect from reforms that are being supported.

Recommendations

IFC should follow up this set of evaluations of business licensing for small service-oriented enterprises in the center of Lima with evaluations of different kinds of enterprises, for example, small or medium manufacturing enterprises. These evaluations will help address the issue of whether this kind of enterprise is responsible for the results reviewed here.

IFC should continue to invest in collecting high-quality data to address critical issues that are at the heart of the justification for projects. The evidence reviewed here has attracted attention precisely because conclusions based on good evidence are perceived to be reliable. As tables 3.2–3.7 illustrate, conclusions reached solely on before-and-after evidence can lead to important mistakes.

IFC should construct a base of evidence on other projects to generate a better understanding of which outcomes can be expected for different kinds of projects under what circumstances.

ix

Abbreviations

BREG Business Registration Evaluation Group

ERR Economic rate of return

FIAS Foreign Investment Advisory Service

GRADE Grupo para Analysis de Desarollo

IEG Independent Evaluation Group

IFC International Finance Corporation

1

1. Introduction

Programs to reduce the costs of doing business, replicated in many countries over

the past 15 years, represent one of the major initiatives of the World Bank Group,

particularly the International Finance Corporation (IFC). Apart from the direct

burden of unnecessary procedures and delays, it is often claimed that inefficient

business regulations and procedures lock enterprises into a vicious circle of

informality, where firms have little effective access to financing and are constrained

in their ability to grow and prosper beyond the status of microenterprises. At issue

are not only the merits of specific business regulations but also the drag on

development represented by informality itself.

This evaluation assesses the impact of IFC’s Business License Simplification Project

in the municipality of Lima, Peru. It reviews two previous evaluations sponsored by

IFC and adds new evidence.

Under the project, IFC’s Foreign Investment Advisory Services (FIAS) worked with

the municipality of Lima to reform the administrative process for obtaining a

business license in Cercado de Lima, one of 44 districts that comprise metropolitan

Lima. According to the municipality, 64 percent of the businesses in this district

lacked a business license in 2005, and most of them were microenterprises. The

project was implemented from January 2005 to March 2007.

IFC has since sponsored two evaluations (Schnabl, Mullainatha, and Kronberger

2007; Alcázar, Andrade, and Jaramillo 2011), which asked separate questions. The

first evaluation in 2007 asked whether the project led to reductions in time and

procedures and increased the number of licenses; that study found that it did. A

second evaluation conducted between 2008 and 2011 used an experimental

methodology with treatment and control groups to ask whether the project led to

improved business outcomes. This second evaluation found no evidence of positive

outcomes on businesses.

The present evaluation conducted an independent review of both previous studies,

collected additional data, verified the previous findings, and placed the findings in

the context of related studies and evaluations. The goal was to take stock of the

results, collect and use other evidence, and draw lessons for future IFC and World

Bank operations.

This chapter describes and compares the divergent evidence on which procedures

were simplified by the license reform and by how much. A second chapter reviews

CHAPTER 1 INTRODUCTION

2 2

existing evaluations and previous relevant findings from other countries; a third

replicates and extends the regression evidence on the impact of license reform on

critical business outcomes, such as revenues and employment. The fourth chapter, a

cost-benefit assessment of the desirability of the whole program, reviews what the

behavior of businesses and their own testimony reveals about the benefits of

registration. The final chapter takes into account the findings reviewed in previous

chapters, as well as new evidence in this study, and offers policy implications and

recommendations for IFC.

The overarching evaluation questions concern the nature and the magnitude of the

cost savings and other benefits of business license simplification. The evaluation

questions are as follows:

1. Did the license simplification and cost reductions in fact lead to greater

registration?

2. Is there evidence that greater registrations lead to better enterprise outcomes?

Can the econometric results of the second IFC-sponsored evaluation by

Grupo para Analysis de Desarollo (GRADE)1 be replicated and confirmed?

Are the inferences reached by that study warranted in light of revised

empirical results or additional data?

3. Does a full cost-benefit assessment of the license simplification project

suggest that it improved welfare? On what does the conclusion depend? How

sensitive is the conclusion to plausible changes in the assumptions?

The methodology used to answer these questions will range from a desk review of

previous evaluations and project documents (for question 1); replication of

regression results using survey data collected for the second IFC-sponsored

evaluation (question 2); and computer simulations with a spreadsheet using data

from evaluations and previous sections of this evaluation (question 3). A unique

feature of the second IFC-sponsored evaluation and the follow-on data in this

evaluation is that the data were collected in a manner that permits sharper evidence

than is normally available about causality from license simplification to firm

outcomes (question 2). These data and the reason they permit an answer to the

causality question is discussed further in chapter 3.

In addition to shedding light on the justification for license simplification projects,

the answers to these questions will affect what role the state should have in actively

promoting formal status. The more there are benefits to license simplification, the

more such benefits redound to society in general, rather than solely to individual

enterprises; the more individual enterprises underestimate such benefits, the greater

the justification for state involvement. State involvement could range from simple

CHAPTER 1 INTRODUCTION

3

reduction of fees and red tape, to the offering of financial incentives, to greater

police enforcement of laws requiring enterprises to be formal.

IFC’s Support to Licensing Reform in Lima

The Business License Simplification Project originated in late 2004 as IFC began

work with the municipality of Lima to simplify licensing procedures. Several related

developments, however, had led up to this point. The World Bank publication Doing

Business 2006 found that starting a business in Lima, Peru, entailed 10 separate

procedures, required 102 days, and cost 38 percent of the average per capita gross

domestic product of the country (World Bank 2005). This was relatively high,

compared with Colombia (42 days) or Canada (3 days).

A further study, conducted jointly by the World Bank’s FIAS and the municipal

government in Lima, had identified municipal procedures and bureaucracy as the

main obstacle to registering enterprises. Before the reform, registering an enterprise

required the following 10 major procedures:

Verification of the uniqueness of the proposed name of the enterprise

Notarization of the enterprises constitution

Deposit of capital in a bank

Inscription in the Mercantile Registry

Legalization of the accounting books

Tax registration

Validation of the payroll books at the Ministry of Labor

Obtaining a zoning certificate

Obtaining a technical clearance

Obtaining an operating license.

Of these 10 procedures, only the final three were the responsibility of the municipal

government; yet these three were estimated to consume 60 percent of the total time

to obtain a license (Schnabl, Mullainathan, and Kronberger 2007).

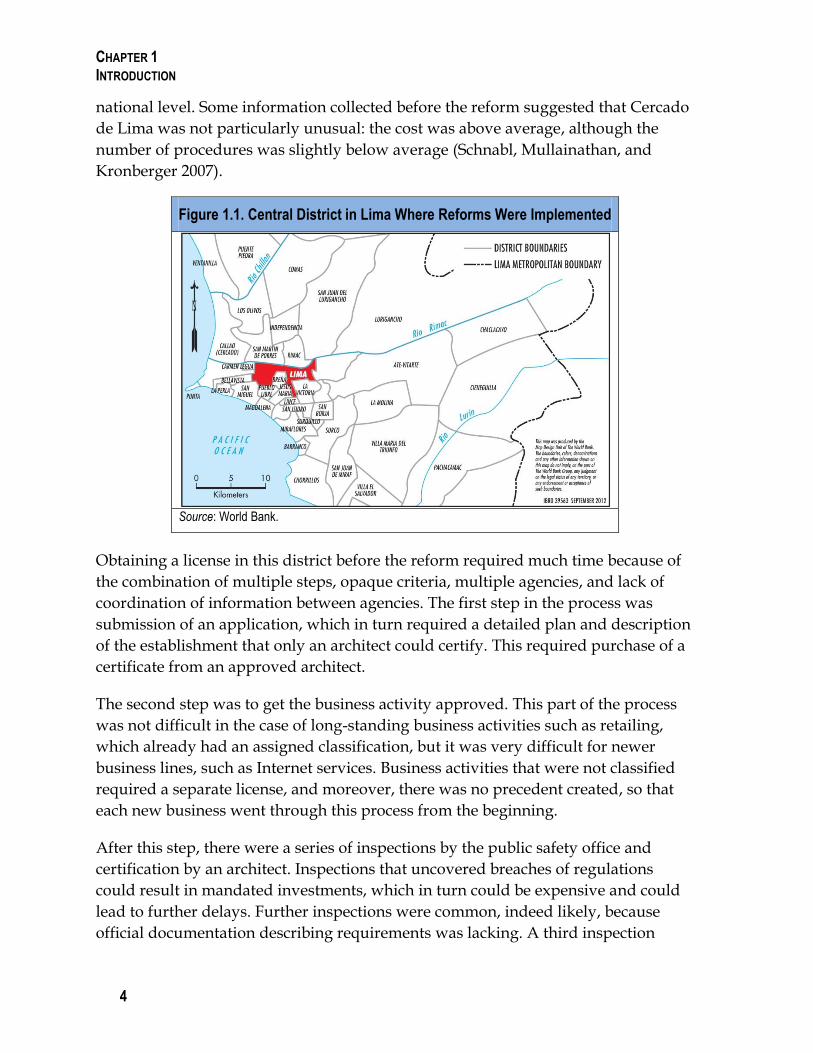

This justified the focus on municipal governments and eventually led to the idea of

conducting a trial program with the municipal government in the district of Cercado

de Lima (figure 1.1). This is one of 45 districts in Lima and was chosen because of

the prohibitive cost of reforming the procedures in many districts at once and to

provide evidence to inform future reform efforts. The district is the historical center

of Lima and was thought to have a large number of businesses operating without

licenses. Licensing procedures in the districts tended to be idiosyncratic, with each

district creating its own rules and procedures, despite attempts to fix policy at the

CHAPTER 1 INTRODUCTION

4 4

national level. Some information collected before the reform suggested that Cercado

de Lima was not particularly unusual: the cost was above average, although the

number of procedures was slightly below average (Schnabl, Mullainathan, and

Kronberger 2007).

Figure 1.1. Central District in Lima Where Reforms Were Implemented

Source: World Bank.

Obtaining a license in this district before the reform required much time because of

the combination of multiple steps, opaque criteria, multiple agencies, and lack of

coordination of information between agencies. The first step in the process was

submission of an application, which in turn required a detailed plan and description

of the establishment that only an architect could certify. This required purchase of a

certificate from an approved architect.

The second step was to get the business activity approved. This part of the process

was not difficult in the case of long-standing business activities such as retailing,

which already had an assigned classification, but it was very difficult for newer

business lines, such as Internet services. Business activities that were not classified

required a separate license, and moreover, there was no precedent created, so that

each new business went through this process from the beginning.

After this step, there were a series of inspections by the public safety office and

certification by an architect. Inspections that uncovered breaches of regulations

could result in mandated investments, which in turn could be expensive and could

lead to further delays. Further inspections were common, indeed likely, because

official documentation describing requirements was lacking. A third inspection

CHAPTER 1 INTRODUCTION

5

would trigger the need for a new license application and new payment of the

registration fees.

On verification that the establishment was in compliance, a certificate was issued.

During this process, the enterprise could be issued a temporary license, a

provisional license, or a permanent license. Provisional licenses were less expensive

but expired after one year. And any time an entrepreneur wanted to convert a

provisional license into a permanent license, an entirely new application process

was required.

There were further zoning requirements for establishments in historical districts, in

which case an inspector came from one agency, or for enterprises located in a

historical monument, in which case inspectors came from another agency. Further,

applications could be stopped or put on hold without advisement, and there was

little coordination between agencies, as the municipality operated with separate

databases.

Broader Issues

License simplification affects broader discussions about regulatory policy, the

informal economy, and the role of both in promoting or constraining development.

In the case of the project in Lima, a major potential social externality that regulations

were intended to respond to was the risk of public safety from fires caused by

exposed wires. Two others were the desire to avoid overcrowding and the

preservation of historical spaces. There is little public rationale for the number of

procedures, lack of coordination, delays, time requirements, redundancies, and lack

of record keeping. Hence, few will defend this aspect of the regulations, and to the

extent that the project was designed to address these issues, it cannot be said that the

project was removing a desirable aspect of regulation.

Licensing reform also bears on the merits and demerits of the informal economy.

One school sees an informal economy as a symptom, an outcome of regulatory

burdens. According to this line of thought, because informality is an outcome and

not a cause, it is not effective to intervene to try to suppress informality without

addressing the causes. Associated with this view is the claim that the informal

economy will tend to disappear with development, as the benefits of larger-scale

operations rise with development or as government institutions become more

efficient and technologically sophisticated. In other words, informality tends to be

viewed as a by-product of low development, not a constraint to development. This

line of reasoning would tend to favor intervention to simplify license regulations

CHAPTER 1 INTRODUCTION

6 6

and unnecessary red tape, but it would tend to be opposed to extra measures to

reduce informality, such as police enforcement.

A second view emphasizes additional issues. Farrell (2004) emphasizes that informal

status perpetuates a low-productivity trap. Formal status will likely improve access

to financing, facilitate investment, and promote higher productivity and business

growth. Informal firms develop networks of low-cost supply chains and build up

relationships that are costly to break; hence, once involved in this network, firms

tend not to escape. Here the informal economy has some staying power and will not

disappear passively with development.

Second, the informal economy is viewed as an unfair burden to the formal sector. It

is unfair competition because the informal sector evades taxes and regulations—

keeping costs low and undermining the ability of the formal sector firms to survive.

It is also unfair in that the informal sector lowers the tax base for business and

income taxes. For any given level of government spending, this raises the budget-

balancing tax on all formal business and further indirectly raises the cost of doing

business for everyone else. These externalities can in principle provide a rationale

for additional enforcement measures, such as police enforcement or punitive fines.

So this school sees the license reform as a step in the right direction but not sufficient

to fully deal with the problem of informality.

Previous Evaluations on Business Licensing

There have been two evaluations of the Business License Simplification Project, but

they evaluate different questions. The first evaluation is Schnabl, Mullainathan, and

Kronberger (2007); much of the same material is in Schnabl and Mullainathan (2012).

These two reports evaluate whether the project led to significant declines in

licensing costs (the same question that can be addressed by the data in table 2.1). The

data collection underlying the 2007 evaluation and the evaluation itself were both

commissioned by IFC.

A second evaluation was done by GRADE (commissioned by IFC and the Business

Registration Evaluation Group [BREG]); it investigated the question of whether and

to what extent the greater formalization caused by the license reform led to better

enterprise outcomes, such as higher revenues, higher investment, higher profits, and

higher employment. A third question that has been addressed in some documents is

the degree to which the benefits of the license simplification exceeded the costs

(Schnabl, Mullainathan, and Kronberger 2007; IFC 2009). Both approach the latter

question in different but incomplete ways. Thus, three major questions have been

CHAPTER 1 INTRODUCTION

7

addressed by previous evaluations: Did the project reduce costs and procedures?

Did formality lead to higher enterprise outcomes? And did benefits exceed the costs

of the project?

Some of the questions addressed by these evaluations are more important than

others. A case can be made that reductions in time and procedures and a greater

number of licenses (what Schnabl, Mullainathan, and Kronberger 2007 evaluate) are

intermediate objectives; the ultimate objective is to raise the welfare of the

businesses involved by saving time and expenses and raising productivity.

According to this line of reasoning, GRADE and IFC are really addressing the more

important questions; whether the reductions in procedures occurred and whether

they led to more licensing is a preliminary evaluation—an input—into the later

evaluations, but not ultimately important.

The informal sector and costly registration procedures have been studied in other

countries. De Soto (1989) argued that bureaucratic red tape and high entry barriers

caused high levels of informality, which in turn impeded firm growth. Empirical

evidence shows that informality and entry barriers are positively associated

(Djankov and colleagues 2002). A reform in Mexico reduced the time required to

register an enterprise at the municipal level from 30 to 2 days. Bruhn (2011) and

Kaplan, Piedra, and Seira (2011) find that registration increased after the reforms. A

critical issue is the degree to which informal status is not rational. Would firms

benefit from registering, even given the high costs of registration, including higher

taxes? In a study using data from Bolivia, McKenzie and Sakho (2010) find a mixed

message: some firms would gain, but many others would not.

Further evidence on the benefits of formal status is contained in a study by De Mel,

McKenzie, and Woodruff (2012), which reports the results of an experiment in

Colombo and Kandy, Sri Lanka, that, like the Peru evaluations considered here,

contained two parts. The first part was to offer enterprises assistance and monetary

incentives to register with the authorities and to observe the degree to which this

was done. The second was to follow the enterprises (both those that did and did not

register) to test whether the act of registration had detectable and significant impacts

on firm performance. Because the incentives were assigned in a random fashion, the

second test was free of selection bias.

These studies found, first, that firms would only register if payments were above the

registration costs. When firms were informed of procedures and costs of registering

and were reimbursed, none chose to register. When firms were offered

approximately $88 or $175 in addition, 17–22 percent chose to register; when they

CHAPTER 1 INTRODUCTION

8 8

were offered $350 in addition, 48 percent chose to register. Problems with land

tenancy were frequently mentioned as critical reasons for not registering.

Enterprises were tracked and observed several months after being offered the

incentives to register, at 15, 22, and 31 months afterward (for example, the incentives

were offered from February through July 2009, and the final survey was conducted

in December 2011). Characteristics of the group that registered were compared with

those of the group that did not register. Average enterprise profits were indeed

higher for those that registered than for those that did not. This is a result about

averages, however, and was driven by rapid growth and high profits of a few

enterprises. Most enterprises experienced no increase in income. No effect of formal

status on sales or employment was found.

The studies found further that formal firms had increased advertising but had no

increase in government contracts or use of bank accounts or loans. The set-up of this

study, examining only existing firms, cannot be used to shed light on entry of new

firms as a result of the reduction in barriers or impact on competing firms (which,

because of constraints in costs and time, could not be interviewed).

9

2. Impact of Reform on Costs and Registrations

This chapter focuses on the first evaluation question: Did the license simplification

and cost reductions in fact lead to greater registration? The effect of the reforms on

license procedures and costs has been recorded in a variety of sources (Schnabl,

Mullainathan, and Kronberger 2007; IFC 2009; Schnabl and Mullainathan 2012) and

in reports from the municipality cited in those documents.

In 2004, IFC and the municipality established a technical secretariat to implement

and manage the reforms. The reforms created new zoning regulations and business

classifications, improved coordination within various offices of the municipality,

accelerated procedures for low-risk businesses, and created a single multipurpose

inspection. There was some divergence between what was created in theory and

what actually happened. Although the intent was to reduce the number of required

inspections to one, a survey immediately after the reforms revealed that the median

number of inspections was actually two, because inspections often led to better

understanding of the required regulations, further changes, and a second inspection.

The impact of the reforms on the number of procedures and time and cost measured

by a before-and-after comparison is summarized in table 2.1. As can be seen, there

are multiple sources reporting what actually happened and some inconsistency.

None of the sources attempt to reconcile disagreements between these numbers, but

they probably were caused by measurement occurring at different times with

different samples of firms. For a consistent source, one can focus on source ―A‖ in

the table, because all three observations are from a similar survey of a consistent

sample performed three times, twice before and once after the reform.

Despite these disagreements in the numbers, the overall picture confirms that there

was a major decline in procedures and costs of obtaining a business license.

Focusing on the study by Schnabl, Mullainathan, and Kronberger (2007) (―A‖ in

table 2.1), the median number of days to obtain a license declined from 40 to 16; the

cost declined from $188 to $91; the number of visits from 4 to 2; and the number of

inspections from 4 to 2. The same study revealed a drop in the percentage of small

business owners reporting that they paid a bribe, from 8 percent to 4 percent, and a

drop in those that reported paying an agent to help them with the process, from 24

percent to 18 percent (not shown in the table). These figures are generally on the

conservative side among all the possible figures in the table. For example, according

to an internal diagnostic report (―E‖ in the table), the number of days to obtain a

license declined from 160 to 16 rather than 40 to 16.

CHAPTER 2 IMPACT OF REFORM ON COSTS AND REGISTRATIONS

10 10

Table 2.1. Summary of Reduction in Costs and Procedures to Obtain a License

Outcome measured Source

Other sources

cited

Value(s) before reform Value(s) after reform

First measurement

Second measurement

First measurement

Second measurement

Third measurement

Days to obtain license

E A 160 16

Mean F D 60 5 10 5

Mean A,B 143 81 15

Median A,B 40 59 16

No. of requirements

Mean C A 8

Mean F D 33 4 4 4

Cost

Mean (―official and unofficial‖)

C A $212

Mean (―official and unofficial‖)

A $288 $212 $112

Mean (―official cost‖)

F D $170 $45 $52 $52

Median (―official and unofficial‖)

A $188 $185 $91

Number of visits to municipal offices

Mean A 4 3 2

Mean F D 11 2 2 2

Number of inspections

Mean A,B 4.3 3.9 2.6

Median A,B 4 3 2

Percentage who reported paying bribe

A 8 10 4

Number of licenses issued

F D 1,711 8,457 4,171 1,978

Sources: (A) Schnabl, Mullainathan, and Kronberger 2007; (B) and (C) Schnabl and Mullainathan 2012; (D) IFC 2009; (E) internal diagnostic report 2005; (F) municipality of Lima official records 2009.

There is also the question as to whether the changes in table 2.1 should be

attributable to the reform effort or to something else. However, it is reasonable to

attribute the changes to the reform, because the reform was the major event that

CHAPTER 2 IMPACT OF REFORM ON COSTS AND REGISTRATIONS

11

occurred during the period and the before-and-after measurements occurred close to

the reform. There is no plausible alternative explanation for the changes.

These data also indicate a large boom in licenses issued immediately after the

reform. The number of registrations ballooned from 1,711 to 8,457 in the year

following the reform, before settling down to 1,978 three years after the reform. This

is a positive development and shows that the reform did achieve its, intermediate

objective of increasing the number of formal official businesses in the district.

Note that this poses a methodological complication for the analysis, because this was

clearly a one-shot increase in licensing, and for some purposes it is desirable to

separate this short-term increase from the long-term or steady-state increase in

licensing caused by the reform. Specifically, the cost-benefit analysis will be based

on estimates of the short- and long-term increases in licensing separately, to analyze

the extent to which the reforms could be justified with and without the benefits of

the short-term increase.

12

3. Potential Benefits from License Simplification—Evidence from Enterprise Outcomes

This chapter focuses on the second set of evaluation questions. Is there evidence that

registration leads to better enterprise outcomes? Can the econometric results of the

GRADE analysis be confirmed, and are the inferences reached by that study

warranted in light of revised empirical results or additional data?

Data and Regression Methodology

A unique feature of the GRADE study was that the data were collected in a manner

that offers a solution to the causality problem, enabling the analyst to test whether

registration caused better business outcomes. The full data come from five rounds of

surveying small enterprises in a specific district of Lima: the first four rounds were

sponsored by IFC and BREG, and the final round by the Independent Evaluation

Group (IEG).

Data from the first four rounds were collected in a baseline survey (May 2008),

followed by three further rounds (November 2008, November–December 2009, and

November 2010). The fifth round of the survey uses exactly the same methodology

as the previous rounds: the same firm conducted the evaluation, the list of questions

came from the same questionnaire, and the same sample of enterprises was

interviewed. The fifth round was conducted in May 2012 and started with the

sample of 239 firms present in the fourth round (November 2010), interviewing

those still in business.

These data permit an analysis using something called an encouragement design,

which is different from a regular experimental design. In a regular experimental

design the treatment is assigned at random to one group; in an encouragement

design an encouragement is assigned at random to one group, and it is hoped that

many of these will decide to obtain the treatment. It is a procedure used when it is

not possible to guarantee that only a certain group will obtain a treatment. In the

IFC-BREG evaluation, a financial incentive was offered to 300 randomly selected

firms in summer 2008 (a few months after the baseline survey was conducted) to

encourage them to obtain a license.

CHAPTER 3 POTENTIAL BENEFITS FROM LICENSE SIMPLIFICATION

13

A special statistical procedure is required to adjust for the fact that the incentive,

rather than the treatment, was assigned randomly. This is what the instrumental

variables procedure does. It uses only the variation in the data caused by the

incentive because the rest could be affected by self-selection.

Evidence from the First Four Rounds of the Enterprise Survey

The main results to be reviewed in the GRADE study are contained in the sixth

GRADE report (Alcázar, Andrade, and Jaramillo 2011, section 5, tables 9–11). These

tables report estimates of the impact of licensing on several enterprise-level

outcomes.

Of all the outcomes that could be measured, labor productivity, or value added per

worker, is one of the most fundamental performance measures for society. Instead of

focusing on labor productivity, the GRADE study focuses on impacts on revenues,

profits, and number of workers (among other factors). This is not a drawback,

however, because understanding the impact on these three factors will provide a

good understanding of whether there has been an impact on labor productivity,

because the concepts are related as follows:

Labor productivity = (value-added)/worker

Value-added = revenues—all nonlabor costs

Total costs = labor costs + non-labor costs

Profits per worker = (revenues—total costs)/worker.

The outcome variables in the econometric work presented here will be revenues,

profits per worker, and number of workers. This list of outcome variables permits a

good understanding of the crucial effects. It also permits a distinction between

achieving intermediate versus final objectives.

Results will be shown first in the simplest possible way: a double-difference

presentation, which shows mean outcome variables for both treatment and control

groups before and after the incentive. These convey the basic message of the data

even though they are not the best methodology available. The best methodology

available is instrumental variables estimation. Tables reporting regressions using

this methodology are large and complicated and are presented in the appendix and

discussed in the text.

The first two estimates of impact will be given in table of the following form (shown

in table 3.1), with the before-and-after estimate of impact given in the right middle

cell and the double-difference estimate of impact given in the bottom right cell. As a

CHAPTER 3 POTENTIAL BENEFITS FROM LICENSE SIMPLIFICATION

14 14

reminder, the double-difference estimate of impact controls for selection biases that

are constant through time but not for selection biases that vary through time.

However, all methods of estimation yield similar conclusions, so the results

presented are not a by-product of selection of a particular method of analysis.

Table 3.1. Before-and-After and Double-Difference Estimates of Impact

Before After Difference

Group that did not get license Average value

Average value

Group that got license (―treated‖ group)

Average value

Average value

Before/After estimate of impact

Double-difference estimate Double-difference estimate of impact (standard error)

Source: IEG.

Turning to the results, note that ―treated‖ firms are defined as those enterprises

reporting to have a license in either the third or fourth rounds of the survey. In

addition, ―before‖ means the observation came from the baseline survey (or the first

round of the survey) and ―after‖ means the observation came from the fourth and

final round of the survey. In the next section, ―after‖ refers to the fifth round,

conducted in May 2012.

Table 3.2 displays the impact of licensing on revenues. Among the group of treated

firms, average revenues were in fact lower after the intervention than before. The

before-and-after estimate is thus positive (837);2 at face value this suggests licensing

improved revenues. Among the control group, revenues were slightly lower,

dropping from 3,422 to 3,129, a difference of –293. The ―double-difference‖ estimate

is thus 1,131, consistent with the idea that licensing positively influences revenues.

The estimate, however, is not statistically significant because the standard error of

1,389 implies a t-ratio of 0.81.

Table 3.2. Impact on Revenues (in constant price Peruvian Nuevo Soles)

Before (April 2008) After (Nov 2010) Difference

Group that did not get license (n = 207) 3,422 3,129 –293

Group that got license (―treated‖ group, n = 122) 7,246 8,084 837

Double-difference estimate –1,131 (s.e. = 1,389)

Source: IEG. Note: s.e. = standard error.

The conclusion from this study is that there is no statistically significant evidence of a

positive impact of licensing on revenues, as the standard error is fairly large. It may be

argued that these results nevertheless do not reject a large effect. What maximum

impact would be consistent with these results? To answer this question, consider the

CHAPTER 3 POTENTIAL BENEFITS FROM LICENSE SIMPLIFICATION

15

95 percent confidence interval of the estimated impact, which ranges from –1,591 to

3,852. If the impact were at the top of this range, at 3,852, it would represent an

increase of 53 percent over the mean of 7,246. By this measure, the maximum possible

impact would be that licensing increased revenues by 53 percent. With the new data,

however, the maximum possible effect is about half this amount.

Profits per worker show very little relation to licensing (table 3.3). Among treated

firms, profits per worker increased slightly, from 708 to 747; hence, the before-and-

after estimate is 39.6. Average profits rose among the control group, from 352 to 463.

So the double-difference estimate is negative (–71.6), casting doubt on the idea that

licensing improves enterprise profits.

Table 3.3. Impact on Profits per Worker

Before (April 2008) After (Nov 2010) Difference

Group that did not get license (n = 209) 351.6 462.8 112.2

Group that got license (―treated‖ group, n = 123) 707.5 747.1 39.6

Double-difference estimate –71.6 (s.e. = 98.6)

Source: IEG. Note: s.e. = standard error.

In this case, the standard error of the estimate is 98.6, so the 95 percent confidence

interval is between –265 and 122. The upper bound of this range (122) is 17 percent

of the mean of 707. By this measure, the maximum effect consistent with this data is

not even 20 percent, suggesting at most a very modest impact on profits.

There is mixed evidence for a rise in employment in response to licensing, and

employment levels of the enterprises under investigation are very small.

Employment declined slightly for both the treatment and control groups (table 3.4),

but more for the control group. Hence, the double-difference estimate is positive,

0.65 and is statistically significant (t-ratio = 2.31). The upper limit of the confidence

interval is 1.19, 39.7 percent of the mean of 3.00. This estimated impact is statistically

significant; nevertheless, a decline in employment, such as occurred for the

treatment group, is not the result proponents of licensing would predict. The

double-difference estimate is positive because employment declined by much more

in the control group than in the treatment group.

Table 3.4. Impact on Employment (including owner)

Before (April 2008) After (Nov 2010) Difference

Group that did not get license (n = 209) 2.44 1.67 –0.77

Group that got license (―treated‖ group, n = 128) 3.00 2.88 –0.13

Double-difference estimate 0.65 (s.e. = 0.28)

Source: IEG. Note: s.e. = standard error.

CHAPTER 3 POTENTIAL BENEFITS FROM LICENSE SIMPLIFICATION

16 16

These results generally cast doubt on the idea that licensing serves to improve

enterprise performance. The only positive result—for employment—came about

because average employment in the control group declined by more than the

treatment group. Although these estimates are potentially affected by selection bias,

selection bias goes in the direction of showing licensing to have a higher impact than

it really does. In other words, even with a positive assist from selection bias, there is

still little evidence that getting a license made a difference for the outcome variables.

Further, instrumental variables estimates, which deal with this selection bias in a

more rigorous manner, confirm and underline this basic conclusion.

The instrumental variables estimates of impact are presented in tables of regression

estimates shown in the appendix. A simplified depiction of the estimated

regressions is given immediately below. In the case of the license simplification

project, the ―treatment variable‖ is obtaining a license, measured as 1 if a license was

obtained and 0 if not. The variable measuring whether an incentive was given, again

1 if yes 0 if not, is said to be the ―instrument‖ for the treatment variable. The

coefficient b1 multiplying the treatment variable is said to give the ―instrumental

variables estimate‖ of impact, in the case where an instrument is used and b1 gives

the ordinary least squares estimate when no instrument is used. Regression tables

appear complicated because ―other control variables‖ can be a large list of variables.

But the coefficient b1 remains the result of interest.

Outcome variable = b0 + b1* treatment variable + b2* other control variables + e

The detailed regression estimates are presented in tables A.1–A.3 in the appendix.

Each table presents four regressions. The regressions in the first two columns are

ordinary least-squares regressions that do not adjust for selection bias. These are

provided for purposes of comparison. The regressions in the last two columns give

the instrumental variable regressions that adjust for selection bias. Both are given in

sets of two: the first in the set giving a regression with no control variables and the

second in the set giving a regression with a full set of control variables. The tables

thus enable a comparison of how the results depend on the estimation method

(instrumental variables or not) and whether there are control variables.

The regression estimates support the same broad conclusions as the double-

difference estimates. Table A.1 shows that although revenues and getting a license

are positively associated in the simplest specification (column 1), this association

disappears with either more controls (column 2) or adjusting for selection bias

(columns 3 and 4). Based on these results, there is no evidence that licenses cause

higher revenues.

CHAPTER 3 POTENTIAL BENEFITS FROM LICENSE SIMPLIFICATION

17

This confirms the results in the sixth GRADE report (Alcázar, Andrade, and

Jaramillo 2011), which contained similar conclusions. The sole difference between

the present results and those reported by GRADE is that the latter eliminated about

20 enterprises from the sample on the grounds that they were unusual observations

(and thus possibly measured in error). The results reported here thus serve as a

confirmation that the conclusions are not sensitive to this choice.

The final two tables of regressions of profits per worker and employment also

confirm previous conclusions. Profits per worker show no evidence of an empirical

relation to licensing (table A.2). There is also little evidence that licensing causes an

increase in employment, once adjustments have been made for selection bias, as

shown in table A.3. The first regression does suggest that licensing is associated with

an increase in employment, but the regressions that control for other variables

(columns 2 and 4) or adjust for selection bias (columns 3 or 4) overturn this result.

These results confirm the conclusion in Alcázar, Andrade, and Jaramillo (2011),

based on the same data:

Results from the fourth round survey confirm … that operating with municipal

license has no statistically significant effect on firms’ performance indicators. Neither

final outcome variables (outputs), such as revenues, sales, profits, profits per

workers, nor intermediate outcome variables, such as number of employees, access

to credit, investment in infrastructure, and machinery (inputs) are statistically

affected if the firms operate with license. For two variables (profits per worker and

number of workers) we obtain significant coefficients, but these are not robust to

alternative methods (§6, p. 28).

These inferences are warranted based on the data collected for the Lima program,

but questions remain. One potential criticism is that the standard errors of the

estimated impacts are large, as was discussed in the case of the double-difference

estimates, but even more so for the instrumental variables estimates. Ultimately this

can only be addressed by building up more data and information, but the estimates

to date do not inspire confidence that the true impacts are large.

A second possible criticism is that the data collected for this analysis did not allow

sufficient passage of time for impacts to be detected. The incentives were offered in

June–July 2008, and the final round of the enterprise survey was conducted in

November 2010, approximately two and a half years later. Whether this is sufficient

time is not possible to know a priori, and at some point the burden of proof should

shift to those who claim that impacts are just around the corner if we wait just a little

CHAPTER 3 POTENTIAL BENEFITS FROM LICENSE SIMPLIFICATION

18 18

longer. What can be done is to collect more data with longer time lags. The next

section reports results from that effort.

Finally, note that the empirical results here are similar to those cited in a study of

enterprises in Sri Lanka by De Mel, McKenzie, and Woodruff (2012). This study also

found that enterprise sales and employment were not higher after formal status was

obtained. In contrast to the evidence here, average profits were higher, but only

because a very few firms made huge gains. As in this evaluation, that study finds no

evidence for broad gains across many firms and many outcome variables.

Evidence from the Fifth Round of the Enterprise Survey

To test the idea that the lack of positive evidence discussed in the previous section

comes from insufficient time to see impacts, IEG conducted a fifth round of the

enterprise survey in May 2012.

Based on the new data, average enterprise revenues rose in the treated group from

7,261 to 8,221 between 2008 and 2012 (in constant Nuevo soles per month, deflated

by the Lima consumer price index). Average revenues in the control group also rose,

from 3,622 to 4,512 (table 3.5). This means that the double-difference estimate is now

only 68.9, not statistically significant at conventional levels (t = 0.07). Licensing has

no significant effect on revenues. According to the upper limit of the 95 percent

confidence interval, the maximum impact is 2,037.6, a rise of 28 percent, compared

with the mean of 7,261.

Table 3.5. Impact on Revenues (constant Nuevo soles)

Before (April 2008) After (May 2012) Difference

Group that did not get license (n = 153) 3,622.1 4,512.4 890.3

Group that got license (―treated‖ group, n = 96) 7,261.3 8,220.6 959.2

Double-difference estimate 68.9 (s.e. = 1,004.4)

Source: IEG. Note: s.e. = standard error.

Average profits per worker are higher among the treated group, but more so in the

control group, so the double-difference estimate is negative. Among the treated

group the difference is 225; among the control group it is 583. Hence, the double-

difference estimate is –358 (table 3.6). Given the standard error of 189.7, the upper

limit of the confidence interval works out to 14, only 2 percent higher than the mean

of 745 for the treated group in 2008.

CHAPTER 3 POTENTIAL BENEFITS FROM LICENSE SIMPLIFICATION

19

Table 3.6. Impact on Profits per Worker (constant Nuevo soles)

Before (April 2008) After (May 2012) Difference

Group that did not get license (n = 152) 367.8 950.7 582.9

Group that got license (―treated‖ group, n = 95) 745.4 970.6 225.2

Double-difference estimate -357.7 (s.e. = 189.7)

Source: IEG. Note: s.e. = standard error.

The new data show a decline in employment among both groups (table 3.7).

Among the treated group, average employment fell from 3.1 to 2.7; among the

control group, it fell from 2.5 to 1.7. The double-difference estimate is positive and

significant because the mean of the control group declined by more than the

treatment group (0.42). The maximum increase in employment consistent with the

data would be 0.76, or 25 percent of the mean of 3.1.

Table 3.7. Impact on Employment (including owner)

Before (April 2008) After (May 2012) Difference

Group that did not get license (n = 152) 2.47 1.72 –0.75

Group that got license (―treated‖ group, n = 97) 3.07 2.70 –0.33

Double-difference estimate 0.42 (s.e. = 0.17)

Source: IEG. Note: s.e. = standard error.

Taken together, the data offer little evidence that important positive effects would

have emerged if more time had passed before data for the earlier study were

collected. The evidence does not show positive effects for either revenues or profits

per worker. It shows small positive effects on employment, but only because

employment in the control groups declined, not because it rose in the treated group.3

Benefits from License Simplification—Evidence from Enterprise Behavior

In June and July 2008, after the reforms were implemented, a monetary incentive

was offered to 300 enterprises that had not yet registered to go to the municipal

offices and register as a formal business. The 300 enterprise owners were chosen

randomly to receive what was called the ―encouragement.‖ If they accepted, the

business owners would be accompanied to the municipal authorities and the group

offering the encouragement would pay part of the registration fee directly. Initially,

the offer was for a payment of 40 Nuevo soles. Of the 300 enterprises, 31 accepted

this offer, and a further 127 were found to be ineligible for a license (one common

reason was that their kind of business, for example, a restaurant, was not permitted

in their specific location). Hence, of those eligible, the acceptance rate was 20

percent.

CHAPTER 3 POTENTIAL BENEFITS FROM LICENSE SIMPLIFICATION

20 20

This take-up rate was deemed too low, and the offer was increased. After some

testing, the implementers found that they had to pay the full cost of the license to

induce a substantial number of enterprises to obtain a license. The offer was

increased to the full amount of the license, and a further 60 enterprises, or 35

percent, obtained a license with this inducement.

As stated previously, this encouragement generated the data used in the

instrumental variables estimation. According to some, the low take-up of the

incentive was seen as a disappointing outcome of the project. But it is not necessarily

disappointing. The business owners are simply revealing something about how

much they value a license.4 This section takes this idea at face value and asks what

can be learned about the value of licensing from this episode.

A rational business owner would assess the costs and benefits of licensing. If C

represents the nonmonetary costs of obtaining a license, F the monetary and time

costs, and B the benefits, we can infer from the fact that an owner decided not to

accept the incentive that he or she assessed C + Fa > B, where Fa represents the

monetary and time costs after the reform and after the encouragement was offered.

In other words, the business owner would register if net costs were below zero (C +

Fa – B < 0) but would not register if net costs were above zero (C + Fa – B > 0). A

summary of the changes that occurred after the incentives were offered is depicted

in figure 3.1. The 40 Nuevo soles incentive was sufficient to offset the net costs for 20

percent of the enterprises, and the full incentive was sufficient to offset the net costs

for a further 35 percent of the enterprises. The exact distribution of how the

enterprises judged the net costs prior to the incentives is unknown, but figure 3.1

shows one example that would be consistent with the facts.

This evidence shows that 55 percent of the enterprises were on the borderline where

refunding the cost of the license was sufficient to tilt the decision to getting a license.

The 40 soles incentive comes to approximately $17; the full cost of the license varied

between $79 and $130, depending on the kind of enterprise; average annual profits

for the firms were $6,060, and the annual minimum wage was $2,136. Hence, the

cost of the license was not large relative to other comparators, suggesting that a lot

of businesses are right on the border where small monetary incentives can tilt the

balance toward getting a license. These figures also show that if licensing caused

average profits to rise by only 10 percent, the gain to the average enterprise

(approximately $600) would far outweigh the cost of the license fee.

CHAPTER 3 POTENTIAL BENEFITS FROM LICENSE SIMPLIFICATION

21

Figure 3.1. Eligible Enterprise Owners Judging the License Worth Getting If the Full License Fee Were Paid

Source: IEG.

The enterprises also provided some information as to which of the costs and benefits

they considered most important. Table 3.8 summarizes costs and benefits, taken

from the list of questions in the enterprise survey.

The results show that on the cost side, the license fees are the most frequently

mentioned item. On the benefit side, the stress and worry of not being registered is

frequently mentioned, as is the risk of paying fines

CHAPTER 3 POTENTIAL BENEFITS FROM LICENSE SIMPLIFICATION

22 22

Table 3.8. Costs and Benefits of Getting Licenses—Number of Times Each Item Mentioned by Survey Respondents in First Round of Survey

Costs of getting a license Number

Benefits of getting a license Number

Have to pay taxes 18 Better prospects for doing business with formal firms

30

May have to pay inspectors

21 Lower risk of non-payment by customers

44

Must receive municipal inspections

20 Can display signs and advertise

41

Must receive civil-defense inspections

11 Easier to access formal credit

75

Have to pay for licenses and incur time costs

40 Have more price/quality options for buying inputs

4

Can participate in public tenders

13

Eligible for programs to assist small firms

22

Lower stress and worry 176

Lower risk of paying fines 151

Source: GRADE data.

.

23

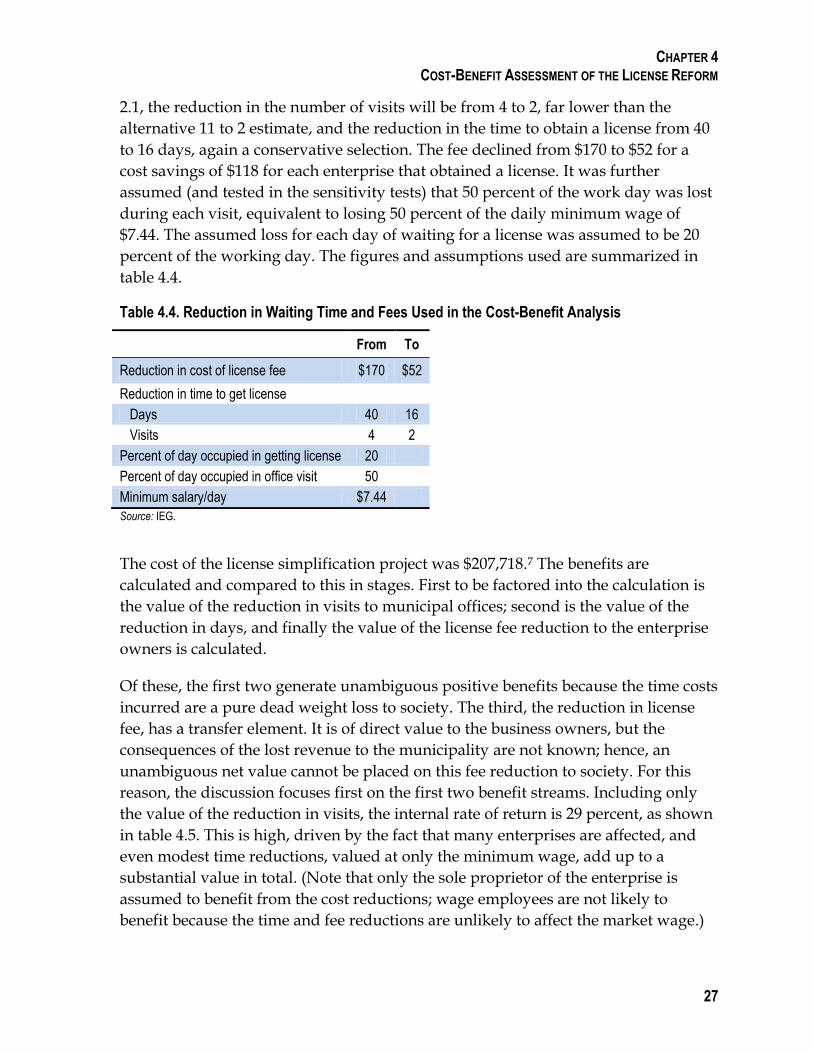

4. Cost-Benefit Assessment of the License Reform

The ultimate question concerning license reform was whether the whole effort was

worthwhile: did impacts and the benefits outweigh the time, effort, and costs

involved?

This chapter focuses on the third set of evaluation questions: Does a full cost-benefit

assessment of the license simplification project suggest that it raised welfare in light

of all the existing and new evidence collected? What does the conclusion depend on?

How sensitive is the conclusion to plausible changes in the assumptions? Although

the license simplification is only a few years old, having been implemented in 2006,

and although some of the consequences are still playing out, several pieces of

evidence can nevertheless be brought together to provide a pretty good picture of

the consequences of the program.

The focus will be on the three major aspects of the license simplification: the

reduction in the license fee, the reduction in the number of office visits required to

obtain a license, and the reduction in the total time to obtain a license. The license fee

is the fee charged for registering an enterprise. This varies with the size, precise

location, and nature of the enterprise and was estimated to average $170 before the

reforms for the district of Lima under analysis (IFC 2009). The fee is levied for new

enterprises and must be renewed each year at approximately the same cost. The

second major aspect of the reform was the reduction in time required to visit the

municipal offices, to wait in line, and to wait in the offices, and the third was

reduction in the overall time delay to obtain the license.

A full cost-benefit analysis of the license reforms must confront the following issues.

First the beneficiaries: the main beneficiary group is the population of current and

future enterprise owners who pay the license fees and experience the delays.

Employees of the enterprises are not necessarily beneficiaries if they earn a market

wage and the wage is set in the wider labor market that is unaffected by the reforms.

In any case, this sector is not a major employer of wage labor; many of the

enterprises employ only one or two casual laborers, if any. Other potential

beneficiary groups are employees of the municipality, beneficiaries of municipal

government expenditures, present and future taxpayers, and firms that may

compete with or complement the small enterprise sector.

CHAPTER 4 COST-BENEFIT ASSESSMENT OF THE LICENSE REFORM

24 24

A priori, which groups are expected to benefit and which to lose from the reforms? The

owners of any enterprise that are potentially in line to obtain licenses benefit from the

reduction in fees and procedures. Beyond that, matters hinge on what precisely happens

if and when the municipalities lose revenues from the reduction in license fees.

Rough estimates suggest that the lost revenue comprises 15 percent of municipal

budgets.5 The fiscal adjustment to lower license revenues could entail expenditure

cuts in other programs, in which case the losers would be the beneficiaries of these

programs. Other fees or taxes could be raised, burdening fee payers or taxpayers. If

funds are borrowed, the issue is sifted into the future, burdening future taxpayers.

Employment in municipal governments could be reduced, burdening employees

who would have to find other employment.

Therefore, the fee reduction aspect of the reforms entails an implicit transfer from

some of these groups to the enterprise owner. The small enterprise owners are low

income, earning close to the minimum wage, but difficulties in identifying the

potential losers make it difficult to determine whether this transfer will be

progressive or regressive.

The second part of the cost-benefit analysis is to determine the features of the reform

that generate benefit flows. In the present case, the fee reduction, the reduction in

office visits, and the reduction in required waiting time are the crucial items for

focus. As already noted, enterprises may benefit further if formal status raises

productivity, although considerable doubt has been cast over this possibility by the

econometric evidence; thus, it will not be formally considered. Benefits may also

stem from any effect of the reforms on the number of firms in formal status: if there

is a large reduction in informality, the competing formal sector would benefit.

People not involved in the enterprise sector may benefit to the extent that formal

status brings greater observance of safety standards by the small enterprises.

The discussion so far has mentioned a number of potential benefit flows, some

complicating factors, and some facts that will remain unknown. All of these are relevant

for a general treatment of the issue, but not to answer specific questions. Here the

bottom line question is whether the IFC project was a worthwhile use of public funds:

did the benefits exceed the costs? This section will demonstrate that it is sufficient to

quantify the benefits associated with saved time and hassle to answer this question.

Three pieces of information are required to estimate the value of a reduction in time

requirements and procedures: the number of beneficiaries likely to be affected over

time, the size of the reductions, and the value to the beneficiaries. In this chapter the

number of persons affected will be estimated using simulations, which in turn use data

CHAPTER 4 COST-BENEFIT ASSESSMENT OF THE LICENSE REFORM

25

and informed estimates from the specific part of Lima where the project occurred. The

size of the reductions will be drawn from the data in table 2.1, and the value of the

reductions to the beneficiaries will be estimated by use of wage data.

This chapter will pull this information together and present the results. After showing

the estimates of the number of enterprises affected by license simplification, it shows

data on the reduction in costs and then shows the results of the cost-benefit analysis as

well as the sensitivity analysis. The sensitivity analysis is used to understand which

assumptions are critical and whether, overall, the net benefit of the program hinges on

parameter assumptions.

Consider first the number of enterprises each year that will likely experience the

registration process. This group is composed of three separate sections: first, the new

entrants that enter formally from the beginning; second, firms that renew licenses; and