Embed Size (px)

Citation preview

Tax Management Department

Immediate

Supply of

Information on

VAT

Immediate

Supply of

Information on

VAT

Tax Management Department

1. WHAT IS THE SII PROJECT?

• It is a change to the current VAT management system.

• It modifies the system of keeping the VAT registration books which will be made

through the AEAT's Electronic Office by supplying invoicing records. (The invoice is

not sent, nor is it an electronic invoice).

•The supply will be made IMMEDIATELY which allows the time between invoice

registration and the effective realisation of the economic operation to be shortened.

2. OBJECTIVES

HELP TO THE CONTRIBUTOR:

1st stage: Tax information

2nd stage: Pre-populated tax returns for VAT self-assessment

IMPROVEMENT IN CONTROL: New control model with information available

immediately.

2

Immediate Supply of Information: analysis of the new system

Tax Management Department

3. COLLECTIVE:

Obligatory

Elective: by census tax return in November of the previous year. The option will be

valid for at least one year.

In 2017, the option colud be made in June.

It would be a collective of 63,000 companies which make up 80% of the total VAT

invoicing in Spain.

- Large companies- VAT groups- REDEME

Monthly settlement period

3

Immediate Supply of Information: analysis of the new system

Tax Management Department

Advantages for the party liable for the tax payment

1. Simplification of formal obligations:

• Removal of informative obligations

*The information from the form 390 which cannot be obtained via the SII would be supplied as

additional information on the forms 303 and 322 of the final settlement period.

2. Contrast information:

Possibility of offering "Tax Information"

In the Electronic Office, a "declared" and “contrasted” Records Book with the

contrast information (from third parties who choose this system, from the AEAT

databases) will be available.

Reduction in errors in compliance with formal obligations and in the tax returns

themselves.

3. Increase in the deadline to submit self-assessments:

First 30 calendar days of the month following the monthly settlement period

- Forms 347, 340 and 390- VAT Records Books

4

Tax Management Department

Improvement in taxpayer control in transactions between business owners

1. Anticipate the information: the time of accounting for invoices is

brought closer to the effective realisation of the economic operation

2. The information is cross-referenced if the client and supplier are

hosted by the system.

5

Tax Management Department

Deadlines / submission frequency:

- Invoices issued Send the record of the invoice within four

calendar days, excluding Saturdays, Sundays and national holidays, from

the date of issue of the invoice.

In any case, before the 16th of the following month.

In 2017, the submission deadline was eight days.

- Invoices received Send the record of the invoice within four

calendar days, excluding Saturdays, Sundays and national holidays from

the invoice's accounting date or the single customs document.

In any case, before the 16th of the following month.

In 2017, the submission deadline was eight days.

6

Immediate Supply of Information: submission deadlines

Tax Management Department

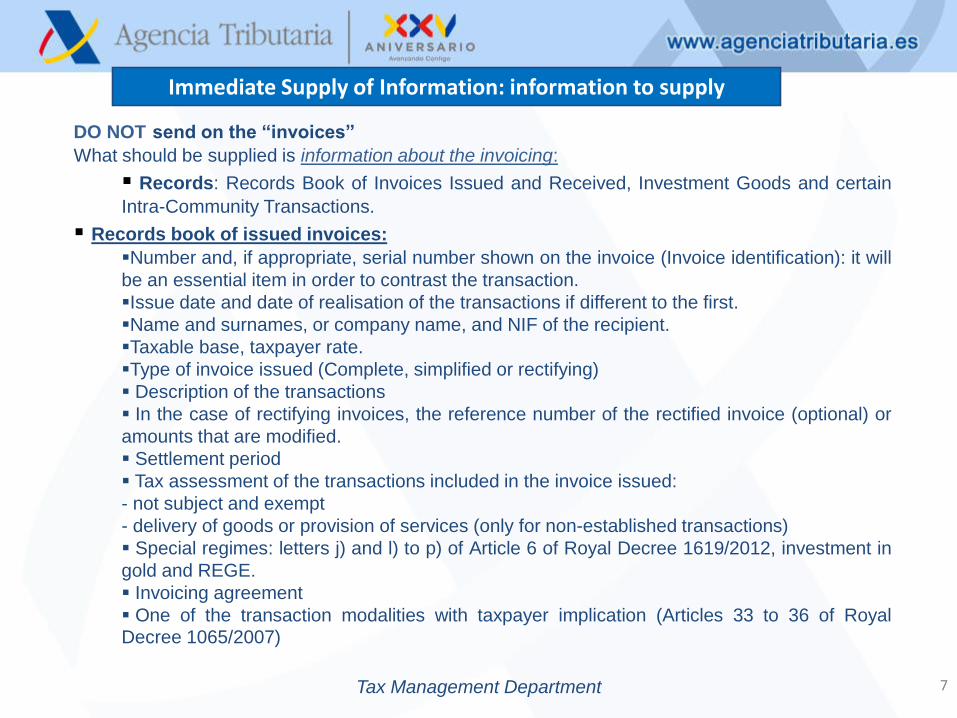

DO NOT send on the “invoices”

What should be supplied is information about the invoicing:

Records: Records Book of Invoices Issued and Received, Investment Goods and certain

Intra-Community Transactions.

Records book of issued invoices:

Number and, if appropriate, serial number shown on the invoice (Invoice identification): it will

be an essential item in order to contrast the transaction.

Issue date and date of realisation of the transactions if different to the first.

Name and surnames, or company name, and NIF of the recipient.

Taxable base, taxpayer rate.

Type of invoice issued (Complete, simplified or rectifying)

Description of the transactions

In the case of rectifying invoices, the reference number of the rectified invoice (optional) or

amounts that are modified.

Settlement period

Tax assessment of the transactions included in the invoice issued:

- not subject and exempt

- delivery of goods or provision of services (only for non-established transactions)

Special regimes: letters j) and l) to p) of Article 6 of Royal Decree 1619/2012, investment in

gold and REGE.

Invoicing agreement

One of the transaction modalities with taxpayer implication (Articles 33 to 36 of RoyalDecree 1065/2007)

7

Immediate Supply of Information: information to supply

Tax Management Department

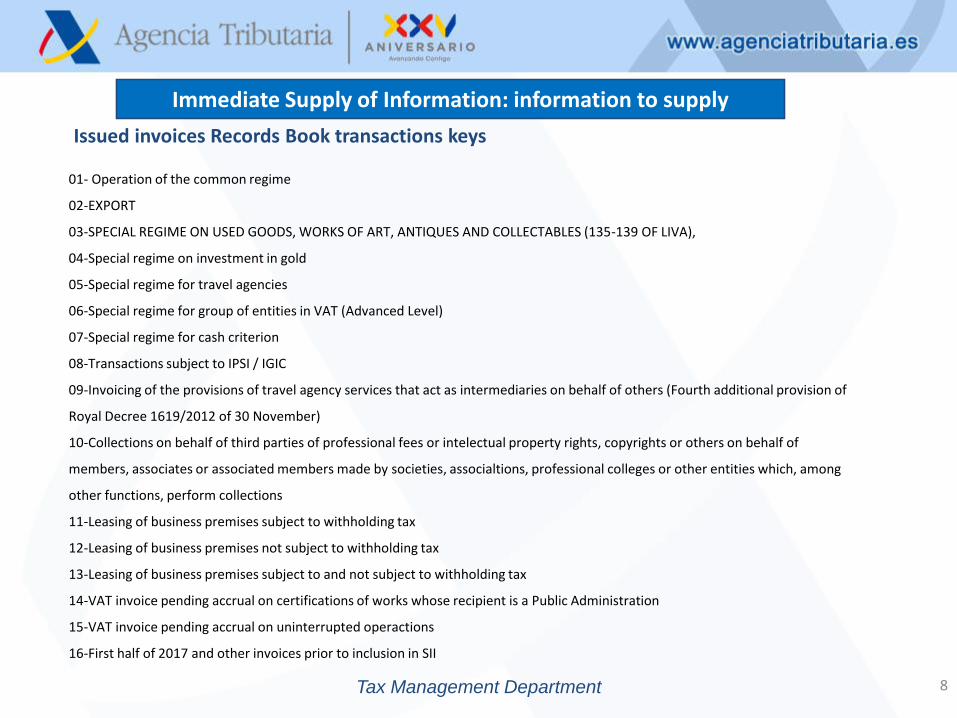

Issued invoices Records Book transactions keys

8

Immediate Supply of Information: information to supply

01- Operation of the common regime

02-EXPORT

03-SPECIAL REGIME ON USED GOODS, WORKS OF ART, ANTIQUES AND COLLECTABLES (135-139 OF LIVA),

04-Special regime on investment in gold

05-Special regime for travel agencies

06-Special regime for group of entities in VAT (Advanced Level)

07-Special regime for cash criterion

08-Transactions subject to IPSI / IGIC

09-Invoicing of the provisions of travel agency services that act as intermediaries on behalf of others (Fourth additional provision of

Royal Decree 1619/2012 of 30 November)

10-Collections on behalf of third parties of professional fees or intelectual property rights, copyrights or others on behalf of

members, associates or associated members made by societies, associaltions, professional colleges or other entities which, among

other functions, perform collections

11-Leasing of business premises subject to withholding tax

12-Leasing of business premises not subject to withholding tax

13-Leasing of business premises subject to and not subject to withholding tax

14-VAT invoice pending accrual on certifications of works whose recipient is a Public Administration

15-VAT invoice pending accrual on uninterrupted operactions

16-First half of 2017 and other invoices prior to inclusion in SII

Tax Management Department

Records book of received invoices:

Number and, if appropriate, serial number shown on the invoice

Imports: DUA number and accounting date.

Issue date and date of realisation of the transactions if different to the first.

Name and surnames, or company name, and NIF of the issuer: invoice

identification

Taxable base

Amount deductible

Description of the transaction

Settlement period

Special regimes: letters l) to p) of Article 6 of Royal Decree 1619/2012 and

REGE

One of the transaction modalities with taxpayer implication (Articles 33 to 36 of

Royal Decree 1065/2007)

9

Immediate Supply of Information: information to supply

Tax Management Department

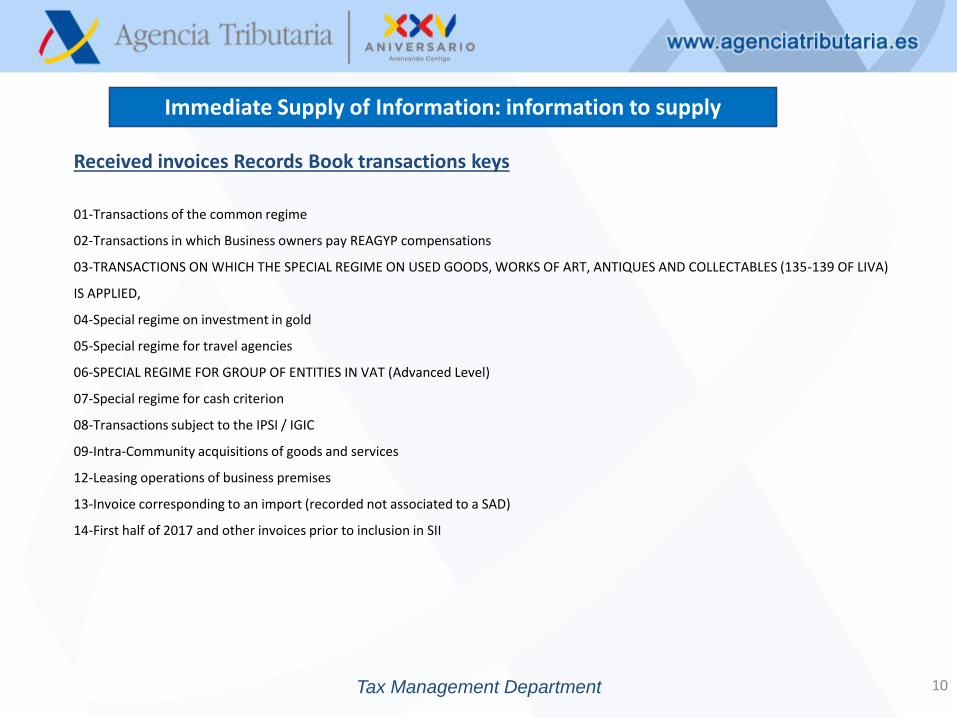

Received invoices Records Book transactions keys

01-Transactions of the common regime

02-Transactions in which Business owners pay REAGYP compensations

03-TRANSACTIONS ON WHICH THE SPECIAL REGIME ON USED GOODS, WORKS OF ART, ANTIQUES AND COLLECTABLES (135-139 OF LIVA)

IS APPLIED,

04-Special regime on investment in gold

05-Special regime for travel agencies

06-SPECIAL REGIME FOR GROUP OF ENTITIES IN VAT (Advanced Level)

07-Special regime for cash criterion

08-Transactions subject to the IPSI / IGIC

09-Intra-Community acquisitions of goods and services

12-Leasing operations of business premises

13-Invoice corresponding to an import (recorded not associated to a SAD)

14-First half of 2017 and other invoices prior to inclusion in SII

10

Immediate Supply of Information: information to supply

Tax Management Department

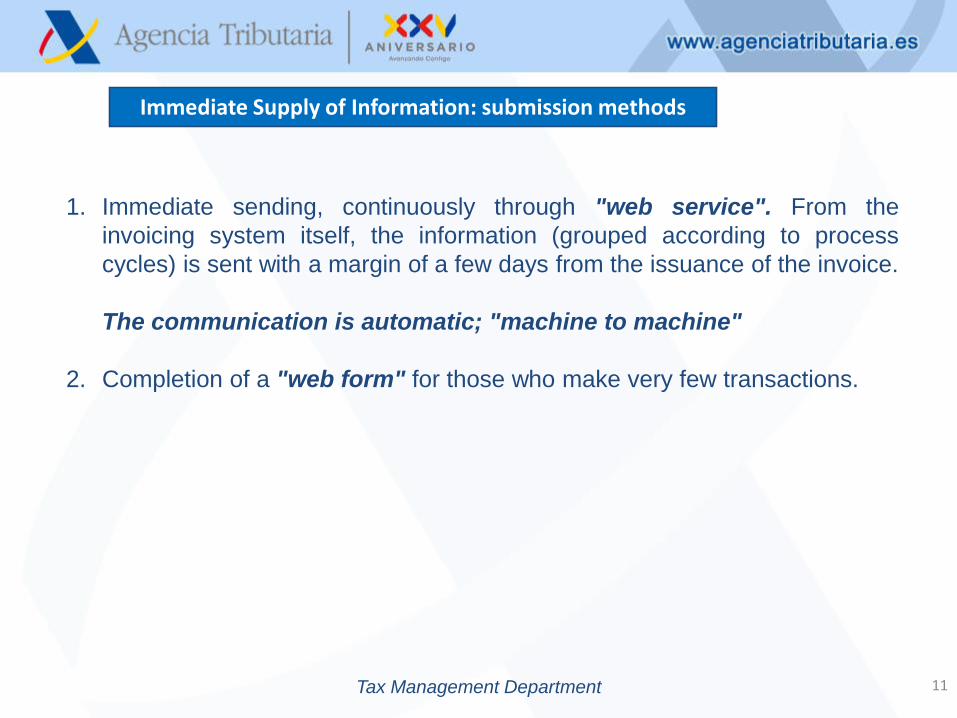

1. Immediate sending, continuously through "web service". From the

invoicing system itself, the information (grouped according to process

cycles) is sent with a margin of a few days from the issuance of the invoice.

The communication is automatic; "machine to machine"

2. Completion of a "web form" for those who make very few transactions.

11

Immediate Supply of Information: submission methods

Tax Management Department

A) LEGAL Modification:

- Modification of Article 164.One.4th of Law 37/1992 of 28 November on Value

Added Tax (LIVA), to reflect the specific obligation on how to comply with the

keeping of Records Books. (done)

"Bring the accounting and the records established in the form defined by law,

without prejudice to the provisions of the Commercial Code and other accounting

standards"

- Modification of the General Tax Law, Article 200. Taxpayer penalty for non-

compliance of accounting and records obligations. (Paragraphs 1 g and 3)

Classification: (Art. 200. 1 g))

The delay in the obligation of recording movements in Records Books through the

Tax Agency's Electronic Office through the supply of invoicing records in the terms

established by law.

12

Regulatory changes (I)

Tax Management Department

A) LEGAL Modification:

Amount of the penalty (Art. 200.3 LGT)

The delay in the obligation of recording movements in Records Books

through the Tax Agency's Electronic Office through the supply of invoicing

records in the terms established by law will result in a proportional

pecuniary fine of 0.5 per cent of the invoice amount in the record, with a

quarterly minimum of €300 and a maximum of €6,000.

13

Regulatory changes (II)

Tax Management Department

B) Regulatory Modification ( RD 596/2016):

Modification of the Value Added Tax Regulation (Articles 62 to 71 of RIVA)

– Recording movements of Records Books through the Electronic Office

– Submission and deposit of tax return deadline

Modification of the Regulation which regulates invoicing obligations, RD

1619/2012 of 30 November)

-For taxable persons who comply with the obligations to issue an invoice through a

third party or by the addressee, it establishes the obligation that it is communicated

through the filing of a census return (Article 5.9 and 10).

- They unify the invoice reference deadlines with those of the issue (Article 18).

Modification of General Regulation approved by Royal Decree 1065/2007:

– Elimination of Form 347 (Article 32 RGAT)

– Elimination of Form 340 (Article 36 RGAT)

– Modification of the current wording of Article 104.h) RGAT

14

Regulatory changes (III)

Tax Management Department

Regulatory changes (IV)

C) Ministerial Orders:

- Approval of Ministerial Order with the content of the invoicing

records of the Immediate Supply of Information and with the

modification of Ministerial Order of form 036 to include the

option for the SII.

Start of public hearing and public information: end January 2017.

Planned publication date in the BOE: May 2017.

- Modification of Ministerial Order Returns-summary VAT, form

390, to expand the group of those exonerated from filing of

Returns-summary in accordance with the provisions of Article

71 of RIVA and modification of forms 303 and 322 to include

certain information.

15

Tax Management Department

Software companies collaboration agreement

16

COLLABORATION AGREEMENT BETWEEN THE TAX AGENCY

AND .............., FOR THE ELECTRONIC SUPPLY OF INVOICING

RECORDS IN THIRD PARTY REPRESENTATION.

Social collaboration for the electronic supply of invoicing records

in third party representation for companies whose business purpose

is, amongst other activities, the supply of software related to business

management to companies of various productive and service sectors,

thus facilitating their customers to comply with their tax obligations.

Tax Management Department

Pilot project: January to June 2017

Entry into force: 1 July 2017

Obligation to send invoicing records from the first half of 2017 between 1 July and

31 December 2017.

17

IMPLEMENTATION

Tax Management Department

Communication channels: general dissemination of information.

SII Banner:

Access through the TAX - VAT banner

18

Tax Management Department

Communication channels: general dissemination of information.

SII Banner:

Access through the TAX - VAT banner

19

Tax Management Department 20

Tax Management Department 21

SII Content BANNER

Tax Management Department

SII GENERAL CONTENT BANNER:

• NEW ITEMS

• GENERAL INFORMATION:

‐ Information notes.

‐ Information leaflet.

‐ Frequently Asked Questions.

‐ Regulations

• TECHNICAL INFORMATION:

‐ Technical documentation. (link to the documentation published

on the developer website)

22

Tax Management Department 23

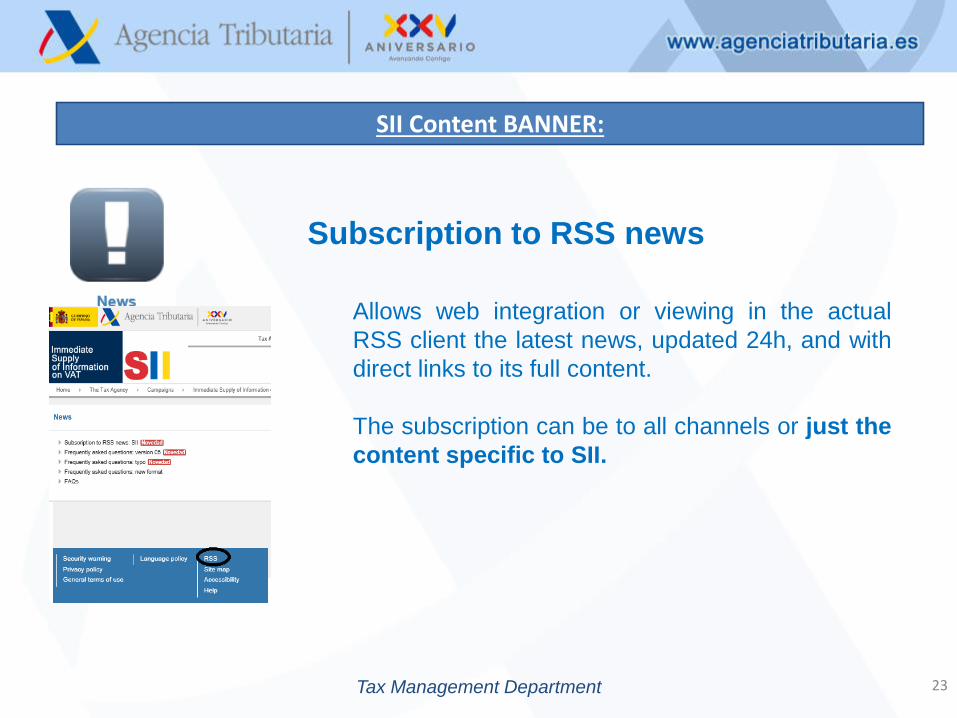

SII Content BANNER:

Allows web integration or viewing in the actual

RSS client the latest news, updated 24h, and with

direct links to its full content.

The subscription can be to all channels or just the

content specific to SII.

Subscription to RSS news

Tax Management Department

FORUM - FOR THOSE INVOLVED IN THE PILOT TEST.

Communication channel for companies which will be involved in the

Pilot Test.

* For questions not answered in the FAQs.

Large Companies FORUM.

Technical Secretary of the Large Companies Forum.

Remainder of those obligated to the SII– Emails:

Communication channels: information and specific help.

24

Tax Management Department

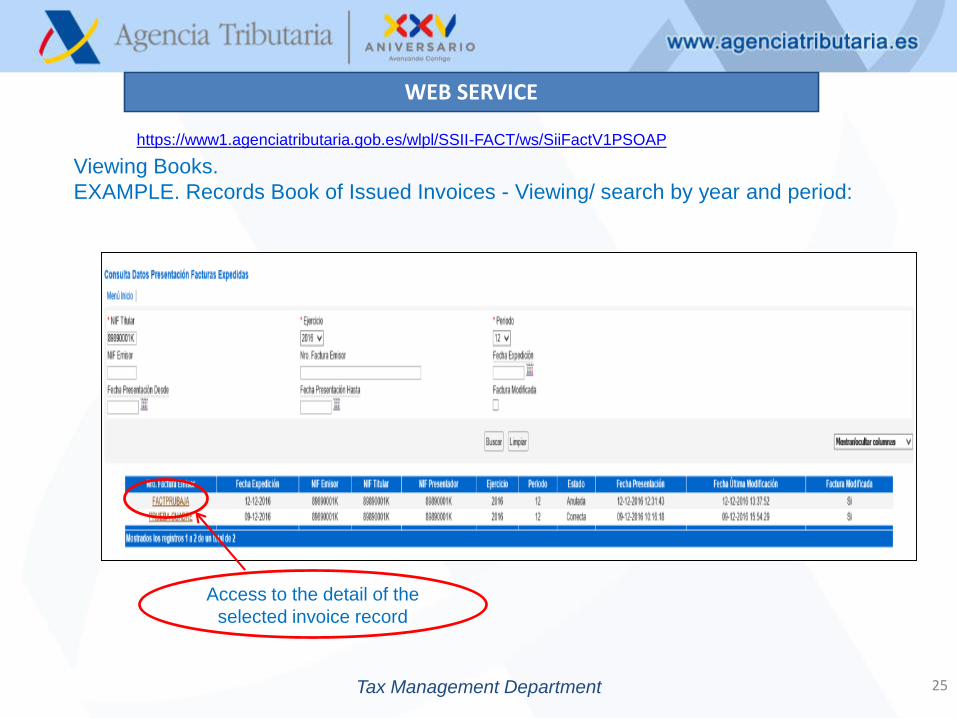

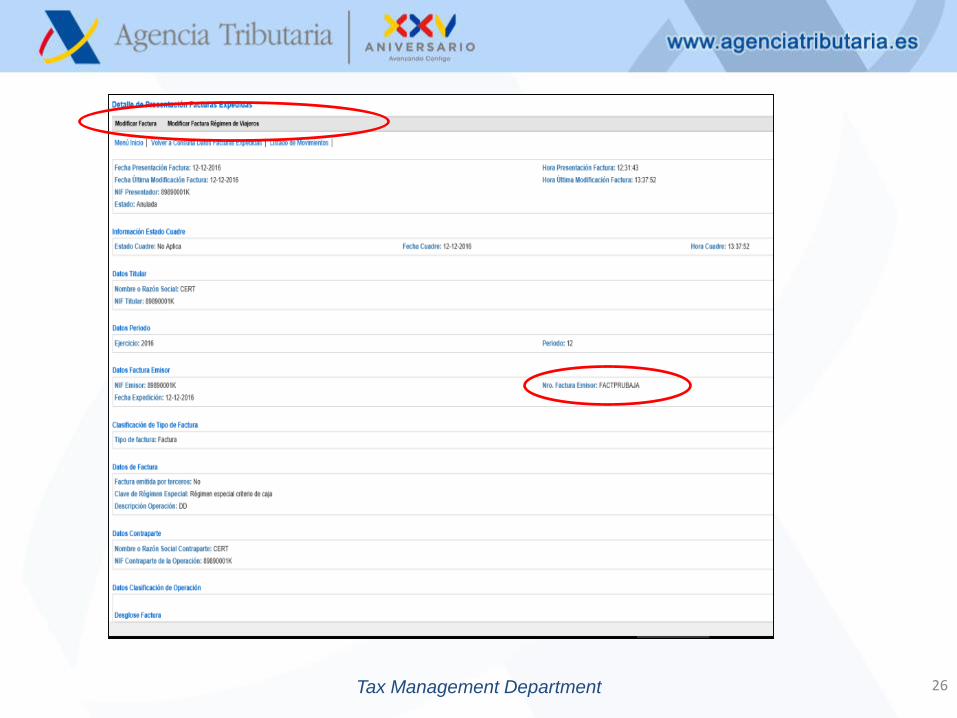

WEB SERVICE

Viewing Books.

EXAMPLE. Records Book of Issued Invoices - Viewing/ search by year and period:

Access to the detail of the

selected invoice record

https://www1.agenciatributaria.gob.es/wlpl/SSII-FACT/ws/SiiFactV1PSOAP

25

Tax Management Department 26

27

![TC04306 - Constable VAT Consultancy LLP · [2015] UKFTT 0101 (TC) TC04306 Appeal number: TC/2013/07424 VAT – Input tax – deductibility of input tax - supply to taxable person](https://img.pdfslide.us/doc/110x75/5fd8ef52a73bab3a1f4a108b/tc04306-constable-vat-consultancy-llp-2015-ukftt-0101-tc-tc04306-appeal-number.jpg)