Embed Size (px)

Citation preview

IMI plcIMI plcFluid PowerFluid Power

October 2010October 2010

IMI Fl id PIMI Fluid PowerRoy TwiteRoy TwitePresident and IMI Executive Director

Gordon ScottGlobal Sector Head - Commercial Vehicles

Richard EdwardsUK Technical DirectorUK Technical Director

Kelvin AustinGlobal Sector Head – Rail

F k GFrank GeversTechnical Director – Rail Sector

Agenda

• Norgren Overview Roy Twite– Strategy– Strategy– Growth Drivers

M i D i– Margin Drivers

• Sector Presentations – Commercial Vehicles Gordon ScottCommercial Vehicles Gordon Scott– Life Sciences Richard Edwards

R il K l i A ti– Rail Kelvin Austin

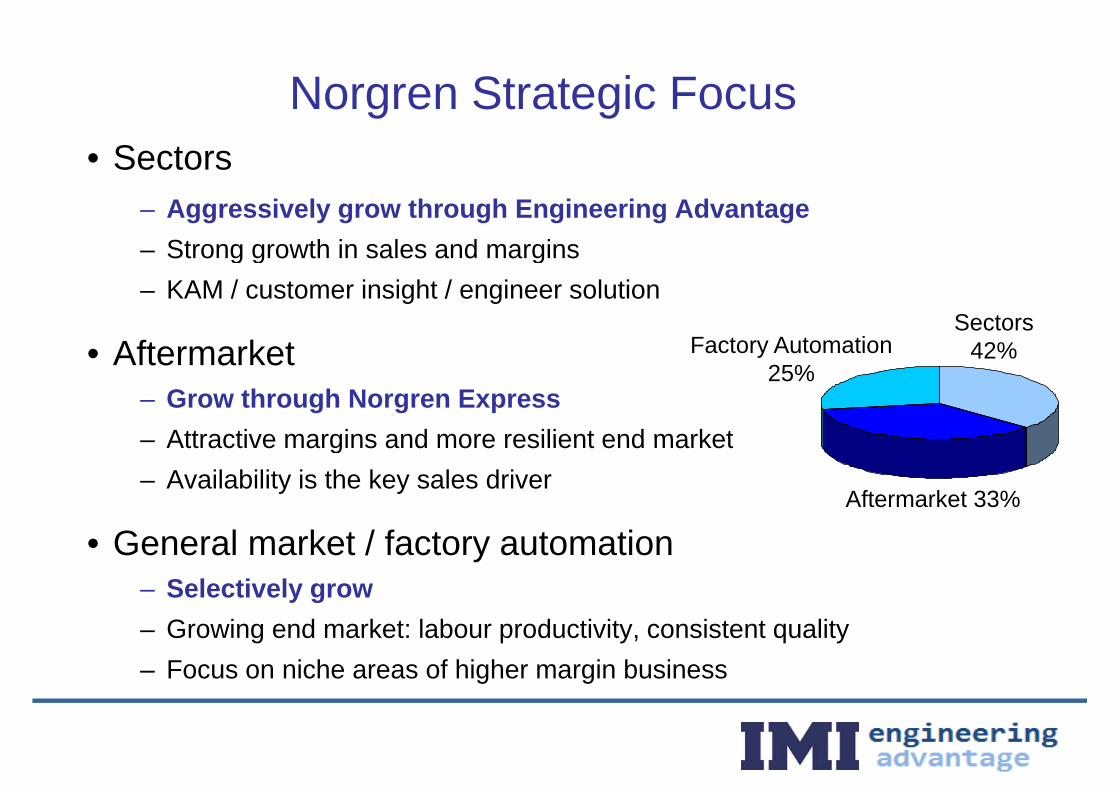

Norgren Strategic FocusNorgren Strategic Focus• Sectors

– Aggressively grow through Engineering Advantage– Strong growth in sales and marginsg g g– KAM / customer insight / engineer solution

• AftermarketSectors

42%Factory Automation• Aftermarket– Grow through Norgren Express

Attractive margins and more resilient end market

42%Factory Automation 25%

– Attractive margins and more resilient end market– Availability is the key sales driver

Aftermarket 33%

• General market / factory automation– Selectively grow– Growing end market: labour productivity, consistent quality– Focus on niche areas of higher margin business

Norgren Sector Sales

Other7%

Commercial Vehicles16%

7%Rail2%

Energy 4%

Food & Beverage Lif S i

4%

Food & Beverage6% Life Sciences

7%

Norgren Major Global CustomersNorgren Major Global Customers

F d tFocused sectorsS t Market Market H1 th C titiSector Market

growthMarket Share* H1 growth Competition

CommercialParker, Voss,

W b R fCommercialVehicles ++ 20-25% 50% Wabco, Raufoss,

Bosch

T H iltLife Sciences +++ 10-15% 25%

Tecan, Hamilton, Parker, Burkert

A F t B hFood & Beverage + 10-15% 50%

Asco, Festo, Bosch,SMC

Energy ++ 10-15% 7% Asco, Parker

P k B hRail + 10-15% 30%

Parker, Bosch Rexroth, Festo, SMC

* IMI management estimates - market share within addressable market.

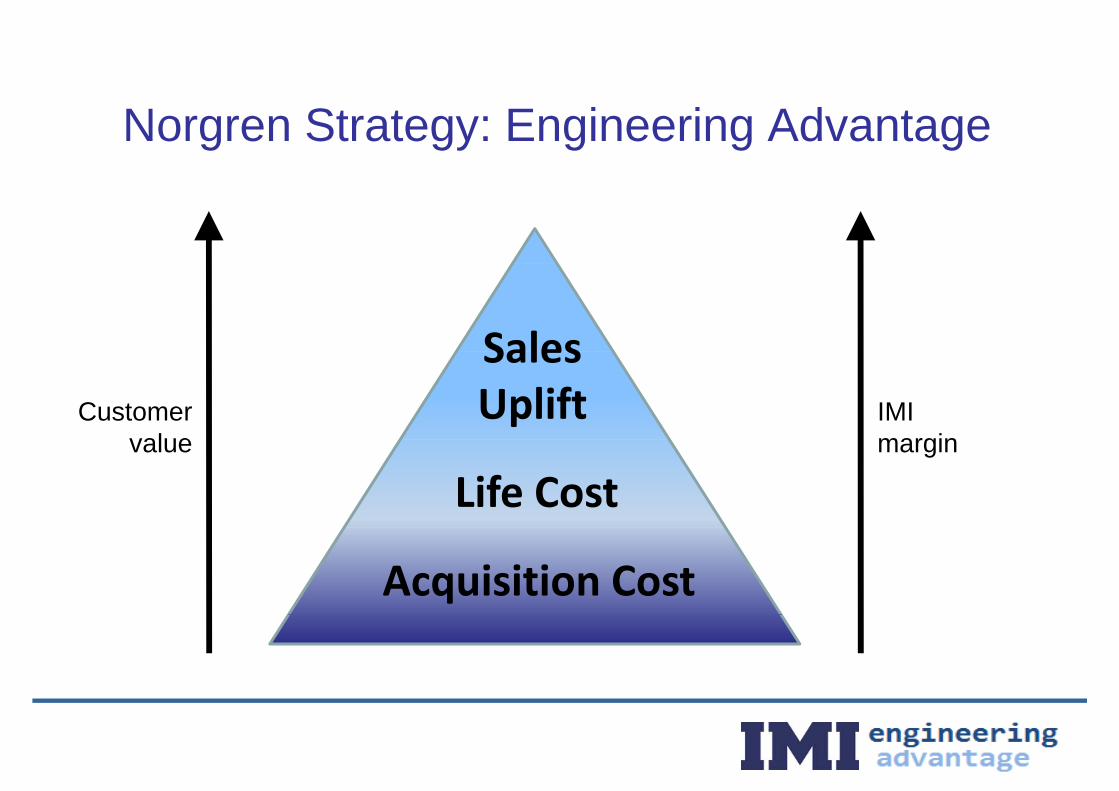

Norgren Strategy: Engineering Advantage

SalesCustomer

valueIMImargin

Sales Uplift

value margin

Life Cost

Acquisition Cost

Engineering Advantage: Commercial VehicleEngineering Advantage: Commercial Vehicle

Sales

Life Costs

Sales Uplift

Acquisition Cost

E i i Ad t R ilEngineering Advantage: Rail

Sales uplift

Life cost

Acquisition cost

Norgren Express Growth ChannelNorgren Express – Growth Channel Focused on the Aftermarket

General Market /

Aftermarket Buying Behaviour

Sectors 42%

General Market / Factory Automation

25% » Key customer requirements» Part identificationPart identification

» Easy to order

» Reliable and rapid delivery

Aftermarket

p y

Aftermarket 33%

2010 YTD Sales

N E G th PNorgren Express: Growth Programs

N C t• New Customers:– Web based lead generation activities e.g. email, catalogues

• Attractive margins, not price sensitive

Fl id P M i D iFluid Power Margin Drivers

• Increased new product sales, engineering advantage– From 12% to 20%

• Further expansion of low cost manufacturing– From 35% to 50%

• Increased low cost procurementp– From 20% to 45%

I i d t i• Improving product margins

Sales Growth and Margin DevelopmentSales Growth and Margin Development

31%40% Organic Growth

-9% -5% 5% 8% 4% 6% 2% 3% -31%

31%

20%

40% g

9% 5% 2% 3% 31%

-20%

0%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 H1

-40%

Operating Margin

12.2% 13.0% 13.2% 13.7%15.0%

13 0%

15.0%

17.0%

6.7% 6.7%7.6%

10.1%

6.3%7.0%

9.0%

11.0%

13.0%

5.0%2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 H1

Fl id P F t P tFluid Power Future Prospects

Cl t t f Fl id P i h k t• Clear strategy for Fluid Power in each market area

• Growth Drivers– Emissions control, healthcare, rail infrastructure, automation

• Margin Driversg– Increased new product sales, engineering advantage– Further expansion of LCM/LCPp– Improving product margins

Agenda

• Commercial Vehicle Sector

• AsiaAsia

E i i Ad t• Engineering Advantage

Long Term DriversLong Term Drivers

• Legislation driving industry globally.

• Engineering Advantage - differentiated product solutions, using proven core building blocks

• Globalisation of industry – Norgren well positioned

• Commercial Vehicle sector outlook improving

K i d t d i i di ti t th» Key industry drivers indicating strong growth

Short Term Drivers

• Key industry drivers indicating strong growth

- Freight requirements increasing- Freight requirements increasing

- Over capacity reducingp y g

- Age of fleet

- Truck inventory 6 year low

CV Sector - Global CustomersCV Sector Global Customers HD Truck

Transmission Engine

Norgren Commercial Vehicle Sector

Powertrain Chassis & CabNorgren Commercial Vehicle Sector …

Chassis & CabFluid Management & Transmission Controls Air Management & Vehicle Dynamics

IMPROVE F l E» IMPROVE Fuel Economy » IMPROVE Fuel Economy

» REDUCE Air Wastage

» IMPROVE Total Cost Ownership

» IMPROVE Fuel Economy

» REDUCE Emissions

» IMPROVE Reliability

Other Drivers – Minimal Cost, Minimal Engineering Impact to Customer

Powertrain» IMPROVE Fuel Economy

» REDUCE Emissions» IMPROVE Reliability

Fuel Efficiency & PerformanceAir and Gas Management

CustomizedAft T t t P Charge Air F ll I t t dCustomized Solenoid ValveApplication

After TreatmentComponents

Pressure Control Valves

Charge AirManagementSubsystem

Fully Integrated Control System

Chassis / Cab» IMPROVE Fuel Economy

REDUCE Ai W t» REDUCE Air Wastage» IMPROVE Total Cost Ownership

Vehicle DynamicsAir Management

Suspension Tire InflationSystem ControlsControl Valves Valve ArraysConnectors &

Accessories

Differentiated solutions - Building Blocks

T tTemperature range-40°...+130°C

Vibration2,500 Hz

A l ti 50Voltage

ToleranceAcceleration 50 g Tolerance-10% / +20%

Transmission Solutions

Engine Solutions

Legislation – Transformed IndustryE 1Euro 1

Euro 2

ollu

tion

Wh Euro 1

Wh Euro 1

Po

Soot

PM

g/k

WSo

ot P

M g

/kW

Euro 3Euro 2

E 3

Euro 2

E 3Euro 3

Euro 4 NOx g/kWh1 2 3 4 5 6 7 8

0

Euro 3Euro 4Euro 5Euro 6

NOx g/kWh1 2 3 4 5 6 7 8

0

Euro 3Euro 4Euro 5Euro 6

Euro 4

E 5

NOx g/kWhNOx g/kWh

Euro 5

E 6

92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

Euro 6

Engineering Advantageg g g

Existing Customer Solution

ValveValve V lV l • Multiple Individual Valves

Existing Customer Solution

ValveValve ValveValve • Multiple Individual Valves• Remote Sensing• Complex Electrical Installation• Complex Pneumatic Installation• Multiple Mounting• Difficult Diagnostics

ValveValve

• Difficult Diagnostics• Multiple Suppliers• High Warranty cost

ValveValve RegulatorRegulator

SensingSensing

Engineering Advantageg g g

Norgren - New Solution• Single Unit • Improved Reliability• Better Performance• Smaller Footprint

R d d I t ll ti Ti• Reduced Installation Time• Single Mounting

Sales Uplift

Life Cost

Acquisition Cost

Engineering AdvantageMulti-Function Control Valve

• Engine 11L and 13L - 3 Valve solution– Timing: In production

WasteWaste--gategate

• Engine 15L – 2 valve solution– Timing: February 2011

gategate

E i 24 V (Gl b l E l W ld T k)

SensorsSensors Exhaust Exhaust BrakeBrake

WasteWaste--tt

WasteWaste--Sales • Engine 24 V (Global Eagle World Truck)– Timing: April 2012

gategate gategateSales Uplift

Life Cost

SensorsSensors Exhaust Exhaust BrakeBrake

AmplificationAcquisition Cost

AsiaAsia

• Asia Truck technology / requirement developing quickly• Asia – Truck technology / requirement developing quickly- Legislation following Europe / USA

A i P t ti l 900k T k l th EU d USA- Asia Potential 900k Trucks – larger than EU and USA- Government Investment – Road Infrastructure- Significant Efforts Global Truck OEM (World Truck)- Norgren – Well positioned

Global Truck ProductionEurope 391k trucks

Asia 894k trucksAsia 894k trucks

America 358k trucks

Asia Region – IndiaAsia Region India

Customer Ashok LeylandCustomer - Ashok Leyland • Project – New Neptune Euro IV Engines.Customer unable to find reliable, accurate control for EGR system. High vibration and difficult environment. Timing, ready for 2010 launch

SolutionSolution• Norgren Proportional Technology. Used proven western technology.P “ hi l ” li bilit f d l “t k il ”Proven “on vehicle” reliability, performance and real “truck mileage”

Significant Amplification Potential - TechnologySales Uplift

Life Cost

Acquisition Cost

Life Cost

SummarySummary

• Legislation driving industry globally• Asia – Significant potential – Norgren well positioned• Asia – Significant potential – Norgren well positioned.• Economic outlook improving

A lifi ti• Amplification • Engineering Advantage

– Technology, differentiation

ENGINEERING ADVANTAGEIn CV Sector

Richard EdwardsUK Technical Director

Norgren Life Sciences

Why is Life Science Attractive?Why is Life Science Attractive?

• Long term global growth g g g

• Long program life (Instrument life & MRO)• Long program life (Instrument life & MRO)

Si ifi t b i t t• Significant barriers to entry

• High margin

Life Science Sector - Markets

A l ti l & Di ti

Life Science Sector Markets

Analytical & Diagnostic Instrumentation Medical

DevicesDevices

AnaesthesialVentilation

RespirationInfusionDialysis

Drug DiscoveryPatient Diagnosis

G iGenomicsBio Detection

35

Market Size• National healthcare spending:

Market SizeNational healthcare spending:– North America: 14% of GDP (@ 1.2 times GDP)– Europe: 9% of GDP (@ 1.4 times GDP)Europe: 9% of GDP ( @ 1.4 times GDP)– BRIC: 5% of GDP (@ 2 times GDP)

• Respiratory disease accounts for 10% of the total healthcare burden

Norgren Available Market - £500M

• 80 ventilator manufacturers worldwideworldwide

• 250,000 new machines produced heach year

Source: growth statements are IMI management estimates based on various external sources

Growth Drivers• Emerging Markets

Growth DriversEmerging Markets– Large population centers entering healthcare

• Technology/targeted therapies– Innovation, genomics, and drug discovery, g , g y

• Point of care/point of use

• Increase in chronic diseases worldwideIncrease in chronic diseases worldwide

• Aging populationg g p p– 65 and older (500m to 1bn in next 20 years)

Market Growth

• Global Respiratory Markets: 12% p a to 2016

Market Growth

• Global Respiratory Markets: 12% p.a. to 2016

Gl b l A l ti l/Di ti M k t 9% t 2020• Global Analytical/Diagnostic Markets: 9% p.a. to 2020

Emerging markets will lead growth

China 18% over the last 15 years, increasing to 25% through to 2015

India growing at 16% p.a. (85% of devices are imported)

Source: growth statements are IMI management estimates based on various external sources

Respiratory Disease• Chronic Obstructive Pulmonary Disease (COPD)

Respiratory DiseaseChronic Obstructive Pulmonary Disease (COPD)– Currently the 6th leading cause of death– Predicted to be the 3rd leading cause of death by 2030Predicted to be the 3 leading cause of death by 2030

• 500M people affected globally, 25M require advanced treatment– Mechanical Ventilation– Oxygen Therapy– Drug intervention

• COPD is incurable– Patients require treatment for life

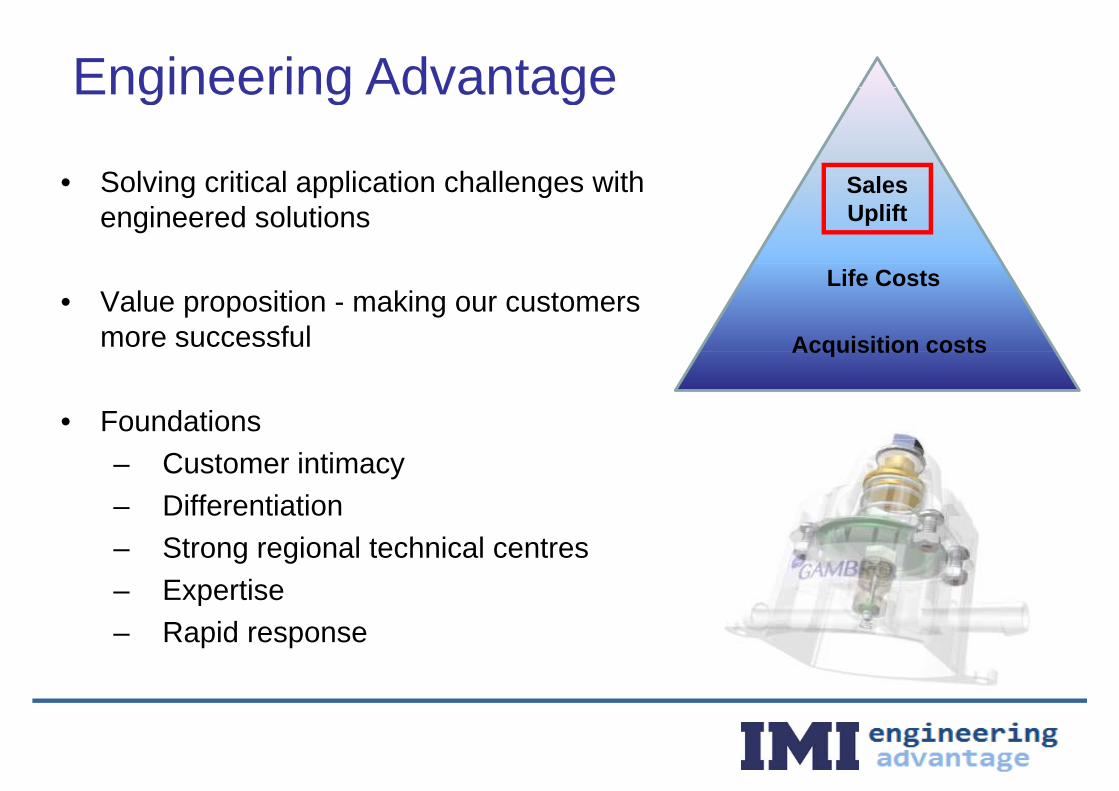

Engineering Advantage

S l i iti l li ti h ll ith

Engineering Advantage

• Solving critical application challenges with engineered solutions

Sales Uplift

• Value proposition - making our customers more successful

Life Costs

Acquisition costs

• Foundations

Acquisition costs

– Customer intimacy– Differentiation– Strong regional technical centres– Expertise– Rapid response

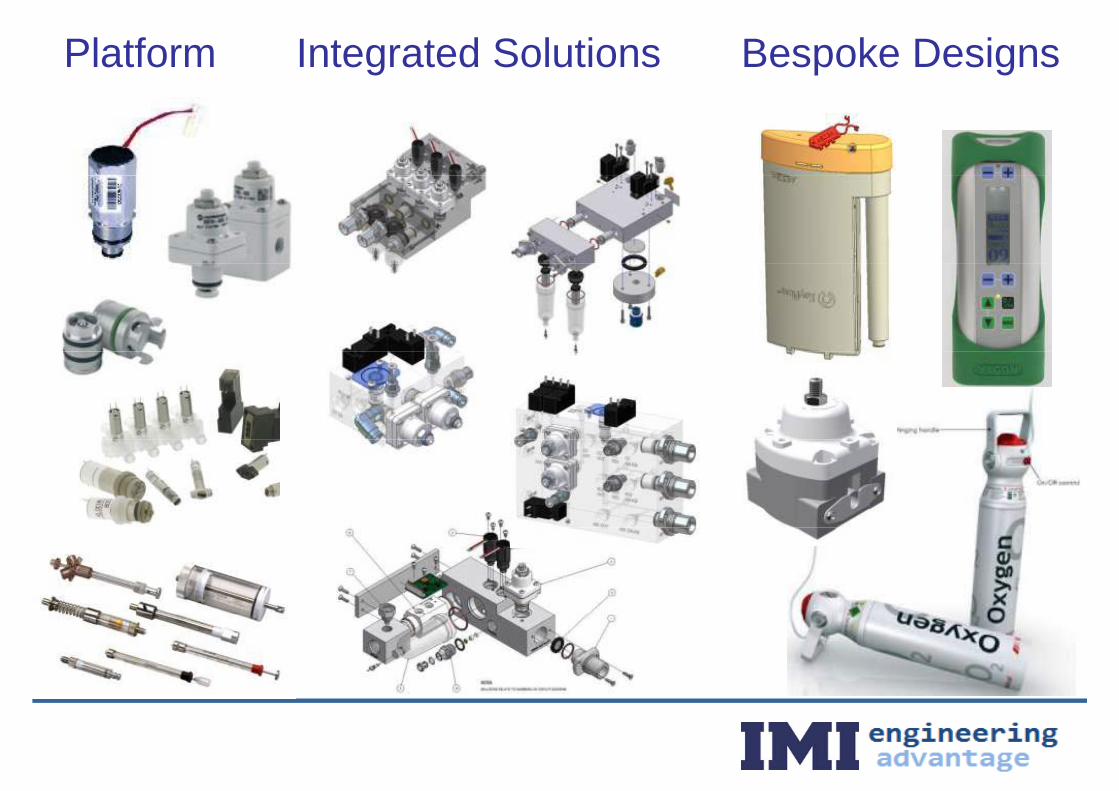

Platform Integrated Solutions Bespoke Designs

Proportional Valve• The Norgren “Flatprop” – A world beater…

Proportional Valve

• Design optimised for critical ventilation and life support applicationspp pp

• Highest flow, lowest power, lightest weight, most accurate proportional valve in themost accurate proportional valve in the world

• Enabling technology that has allowed the• Enabling technology that has allowed the development of truly portable ventilators

R l d i 2004• Released in 2004

• 200,000 valves sold since launch

• The heart of many integrated solutions

44

Genome SequencingGenome Sequencing• Completed in 2003, the human genome p , g

mapping project took almost 13 years and cost $3B

• It is now possible to have individual whole genome profiling within a week for less than $10,000

• Both leading manufactures of this gtechnology use integrated fluidic manifolds and syringe pump arrays developed by NNorgren

45

Anaesthesia & Ventilator ManifoldsAnaesthesia & Ventilator Manifolds• There are three main ventilator manufacturers

in China and Norgren has developed solutions for each of them

• In 2007, we started supplying an anaesthesia gas control module for Mindray, manufacturedgas control module for Mindray, manufactured locally at our Shanghai facility

• The success of the project and the close working relationship between the engineering t l d thi t d l tteams lead this year, to a development partnership for Mindray’s new flagship intensive care ventilator

46

Infusion PumpInfusion Pump• In-Patient care in US/European hospitals can

often exceed £1,000 per day

• Early de-hospitalisation is therefore a y psignificant driver for both national services and private healthcare providers

• Astra Tech (a subsidiary of Astra Zeneca), have developed a portable, disposable, infusion pump which helps to achieve this aim

• At the core of this solution is a bespokeAt the core of this solution is a bespoke pressure regulator developed and manufactured by Norgren

47

Life Science Sector SummaryLife Science Sector Summary

• Consistent double-digit annual growth

• Fragmented and innovative market

• True supply partnerships

E i i Ad t l ti• Engineering Advantage solutions

Re arding• Rewarding

Rail SectorOctober 2010

Kelvin AustinFrank Gevers

49

»Why is Rail Attractive?y»Market Analysis

»Engineering Advantage

Global Megatrends – shaping g gtomorrow's markets

Urbanization

» Today: 280 million people in megacities (>10 million)

» 2007: First time in human history more people living in cities than in rural areas

» 2015: 350 million people in megacities

Challenges for Transportation

Energy Consumption

Rail is on average 2 – 5 times more energy efficient than road, shipping and aviation

Final Energy Consumption in Europe

efficient than road, shipping and aviation

Railways’ share of transport energy 14%

2.5% 0.1%1.4%

consumption is less than 3%,

hil it k twhile its market share is between 6% ( )6% (passenger) and 10% (freight).

82%82%

Road Air Railways Inland Water Other

Energy Consumption

-57%

R d R il WaterwayRoad Rail Waterway

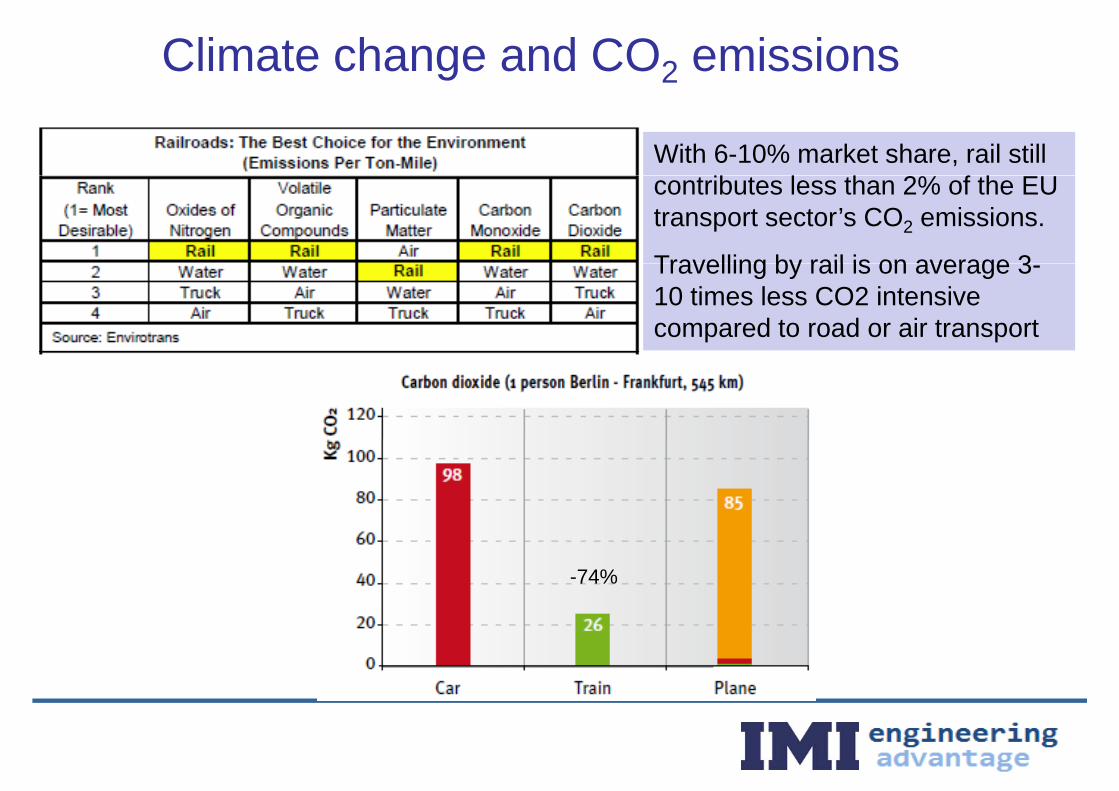

Climate change and CO2 emissions

GHG Output in Europe

12%

2% 1%

15%

70%

Road Sea Air Railways Other

Due to its use of electricity, rail is the only motorised mode of transport which is capable of shifting from fossil fuels to renewable energy without any separate investment in the propulsion units, simply by changing the energy sources in the electric energy production. Electric traction accounts for 80% of rail production in Europe.

Climate change and CO2 emissions

With 6-10% market share, rail still ib l h 2% f h EUcontributes less than 2% of the EU

transport sector’s CO2 emissions.

Travelling by rail is on average 3Travelling by rail is on average 3-10 times less CO2 intensive compared to road or air transport

-74%

Is it Safe to Travel?Fatality Risk as a Multiple of Rail

571600

400

500 Rail travel i 15 ti

201 189300

400 is 15 times safer than 189

15 1 8 1 5 1100

200 a car!15 1.8 1.5 1

0

ycle

rian

ycle Car ach Air

way

Motorcyc

Pedes

tria

Cyc CBus

/coac A

Railwa

per km basis

From this….

57

Beyond this….

Siemens - Deutsche Bahn ICE3Energy consumption is 0 33 litres per 100 km per seat 75% less emissions than an aircraft

To this….

Energy consumption is 0.33 litres per 100 km per seat, 75% less emissions than an aircraft

Tangshan (CNR) China Railways CRH3Norgren components in Brakes, Doors and Pantographsg p , g p

Velaro – Germany, Spain, China, Russia

Market AnalysisMarket Analysis

Global Rail Market ShareGlobal Rail Market Share15%

10%Parker

3%

NorgrenFestoSMC

8%53% SMC

BoschOthers

8%

6%

Source: IMI management estimates

Average Growth ’08 – ’13 = 5%g

Rail Market Forecast (sci Verkehr / IRJ Oct 08)

100 0120.0140.0 122.5100

40 060.080.0

100.0

£ bn

0.020.040.0

2007 2008 2009 2010 2011 2012 2013

Year

Openness of a country’s markets to foreign goods and services. Market access reflects the government’s economic policies regarding import substitution and free competition.

Study commissioned by the European Railway Industry Association - UNIFE

W ld R il A ibl M k t K S tRolling Stock pne matic potential £200m

World Rail - Accessible Market - Key Segments

World Rail Market = £74bn

Rolling Stock pneumatic potential = £200m

World Rail Market £74bn9 Rolling Stock Pneumatics Market = £200m

7.6 2.6

27

15

20.5

22.6

23 146.7Rolling Stock Services Infrastructure Train Control

Coaches Wagons Multiple Units Others Locomotives

Global Top Ten Vehicle OEMsGlobal Top Ten Vehicle OEMs

BombardierAlstomCNRCNRCSRSiemensSiemensTransmashGETrinityEMDKawasaki

CNR = China Northern Locomotive & Rolling Stock Industry

Electro-Motive Diesel, Inc

Norgren Railine – Dedicated Rail Products

Our strategy is to deliver value to vehicle OEMs and end-users

REGIONAL RAIL SALES ENGINEERSTactics – Top 30Engineering AdvantageTechnical solutionsService differentiation

REGIONAL RAIL SALES ENGINEERS

Se ce d e e a oGlobal support = Sales Uplift

Tactics Top 20Products which are:More reliableMore durableMore efficientIntegrated supply partners= Life Cost Advantage GLOBAL RAIL KAM’s

BRECKNELL WILLIS

Rail Sector Strategy

KEY ATTRIBUTES

References Experience Reliable

KEY APPLICATIONS

Brakes Couplers References Experience Reliable

Durable Proven Global Reach

Brakes Couplers

Doors Pantographs

Engineering AdvantageEngineering Advantagefor the Rail Sectorfor the Rail Sector

Opportunity: Reduce Complexitypp y p y

The ProblemThe Problem

• The customer wants to build Coupling Systems not pneumatic circuits• The customer wants to build Coupling Systems, not pneumatic circuits.

– Increase his capacity

– Retain flexibility

Solution: Customised ManifoldApplication: » Manifold to control the nose cone door system

Customer: » Coupler OEM

Advantage: » Compact unit easy to installAdvantage: » Compact unit, easy to install» Modular system - flexibility» Reduced installation time» Reduced re-work time» Reduced re-work time» Less inventory handling» Less purchasing & accounting administration

Key: » The customer had confidence in Norgren from ourexisting relationshipD i d th i it t it diff t i t» Designed the circuit to suit different variants

» -40°C capability = global standardisation Sales uplift

Acquisition cost

Life Cost

Opportunity: Ergonomic Access SystemsOpportunity: Ergonomic Access Systems

Designed for maximum comfort, efficiency, safety, and ease of use

• Automatic compartment and body p yend door systems

• Fire protection options• Fire protection options

• Automatic openingp g

• Entrapment protection

• Programmable motion

Opportunity: Ergonomic Access SystemsChallenges on Automatic Rail Door System Applications

Opportunity: Ergonomic Access Systems

ISO 16750EN 45545

• Rigorous safety and quality standardsVDE 0435DIN - EN60529EN 16509

• Low temperatures, down to –50°C IEC 61508EN 12015 und EN 12016DIN 5510• Demanding voltage ranges and high tolerances

– 24 – 110 VDC +/- 30%

DIN 5510EN 14752EN 50125 -1DIN EN 5015524 – 110 VDC +/- 30%

• Low lifecycle costs

DIN EN 50155DIN EN 50126DIN EN 50128DIN EN 50129DIN EN 50129

Solution: Engineering AdvantageSolution: Engineering Advantage

Differentiation on Automatic Door Systemsy

• Obstruction detection with memory function

• Robust guiding system capacity 150kg• Robust guiding system – capacity 150kg

• Plug and play actuator – no cabling workPlug and play actuator no cabling work

• Proven lifecycles >2.5 million

• Modular, flexible component layout

Solution: Engineering AdvantageElectric Door Actuator

Guiding System

I/O-board

ControllerController

Opportunity: Ergonomic Access SystemsOpportunity: Ergonomic Access Systems

Designed for maximum comfort efficiency safety and ease of useDesigned for maximum comfort, efficiency, safety, and ease of use

• Some markets require less complex systems

• Maintenance is problematic

• Long refurbishment intervals are required• Long refurbishment intervals are required

• Manual door systems are sufficient for some applicationsManual door systems are sufficient for some applications

Opportunity: Ergonomic Access SystemsOpportunity: Ergonomic Access SystemsChallenges on Manual Rail Door System Applications

Can we bring Engineering Advantage to manual doors?

Solution: Engineering Advantageg g gDifferentiation on Manual Door Systems

Yes!!S i i i !

Yes!!• Stops in any open position – no entrapment!

• Adjustable dwellAdjustable dwell

• Closes automatically y

• Integrated speed control

Solution: Engineering Advantageg g gSmart Manual Door Actuator

Engineering Advantage in Action!Engineering Advantage in Action!

In Norgren Brno, we have set up:

• A demonstration of 3 Door Systems

– Automatic

– Manual

– Smart Manual

• We will give you an opportunity to try them!• We will give you an opportunity to try them!

• We have excellent references and global reach

• The sector is resilient

• The sector is growing

• Th k t h• There are market share opportunities for Norgren

• Our target is to double our business every 3 – 4 years

• Engineering Advantage is delivering attractive marginsg g

Fl id P SFluid Power Summary

• Attractive long term growth drivers– Emissions legislation for trucksg

– Engineering solutions in growing healthcare segment

Increased government investment in rail– Increased government investment in rail

• Opportunities to improve margins further– New Products, growing proportion added value sector businessg g p p

– Increasing aftermarket through development of Norgren Express

Further expansion of low cost manufacturing capacity / LCP– Further expansion of low cost manufacturing capacity / LCP

– Product margin optimisation

Questions?

Summaryy

1. Highly cohesive group with shared

fundamentals

2. Significant exposure to high growth

end markets

3. Continuing margin momentum

4 L t t i bilit4. Long term sustainability