Embed Size (px)

Citation preview

8/7/2019 im project-1

http://slidepdf.com/reader/full/im-project-1 1/37

INVESTMENT MANAGEMENT

PROJECT

METHODS OF COMPUTATION OFSTOCK INDICES AND CONTRAST

BETWEEN NSE NIFTY AND NYSE

DOW JONES.

SUBMITTED BY:

TRISHA ARORA

B.COM (HONS) III, B

ROLL NO.: 146

8/7/2019 im project-1

http://slidepdf.com/reader/full/im-project-1 2/37

TUT GROUP: B 8

Table of contents

S. No. Heading Page No.

1 Introduction 3

2 NSE NIFTY 8

3 Dow Jones Industrial Average 22

4 Correlation 28

5 Conclusion 37

2

8/7/2019 im project-1

http://slidepdf.com/reader/full/im-project-1 3/37

CHAPTER 1

INTRODUCTIONINTRODUCTION

3

8/7/2019 im project-1

http://slidepdf.com/reader/full/im-project-1 4/37

INTRODUCTION

Stock is a certificate representing partial ownership in a corporation. They are issued by

corporations that need long-term funds. Although the issuing corporation is not

obligated to repurchase this stock at any time in the future, shareholders can sell it to

other investors in the secondary market.

Stock Market is a secondary market where already issued financial assets are traded.

The key distinction between a primary market and secondary market is that in the

secondary market the issuer of the asset does not receive funds from the buyer. Rather,

the existing issues changes hands in the secondary market, and funds flow from the buyer

of the asset to the seller.

The Stock Exchange provides the issuer with regular information about the value of its

outstanding stocks or bonds. It also offers investor’s liquidity for their assets, information

about them as well as prices for the assets they are holding or want to buy. Further, they

bring together many interested buyers and sellers of assets and so can reduce the costs of

searching for them.

Thus, stock markets facilitate the equity investment into firms and the transfer of

funds in exchange of stocks.

A Stock Market Index is a representative sample that makes it simple to understand and

interpret market performance. It is a comprehensive measure of market trends, intended

for investors who are concerned with general stock market price movements. It helps in

evaluating the performance of a given market. It comprises stocks that have large

liquidity and market capitalization. Each stock is given a weightage in the Index

4

8/7/2019 im project-1

http://slidepdf.com/reader/full/im-project-1 5/37

equivalent to its market capitalization. The Index value compares the day’s market

capitalization vis-à-vis base capitalization and indicates how prices in general have

moved over a period of time. Now-a-days, many stock market indices are computed so as

to understand the behavior of the market. Some of them are as follows:

AT BOMBAY STOCK EXCHANGE (BSE):

Sensex representing 30 most active shares

BSE 100

BSE 200

BSE 500

Sectoral Indices like BSE Teck, PSU Index, Healthcare Index, Bankex etc.

AT NATIONAL STOCK EXCHANGE (NSE):

S & P CNX Nifty representing 50 most active shares

CNX MIDCAP 200

CNX Nifty Junior

S & P CNX 500

S & P CNX Defty

CNX IT

However the most well known indices and generally acceptable by all kinds of investors

in the Indian Equity Market are the BSE Sensex and S & P CNX Nifty which reflect the

movement of 30 stocks on the Bombay Stock Exchange and 50 stocks on the National

Stock Exchange (NSE) respectively. The BSE Sensex has grown from a base of 100 in

5

8/7/2019 im project-1

http://slidepdf.com/reader/full/im-project-1 6/37

1979-80 to over 7000 in recent times. On the other hand, S & P CNX Nifty has grown

from a base of 1000 in 1994-95 to 2000 in recent times.

1.2 CREATING A STOCK MARKET INDICATOR

In general, three factors differentiate stock market indicators:

The universe of stocks represented by the indicator

the relative weights assigned to the stocks , and

the method of averaging used

A Stock Market indicator can include all publically traded stocks or a sample of

publically traded stocks. No stock market indicator currently available is based on all

publically traded stocks. However, breadth of coverage is different for each market

indicator.

The stocks included in a stock index must be combined in certain proportions to construct

the index. Therefore, one of the following three methods or approaches is employed to

assign the relative weights to the stock market indicators:

a. Weighing by the market value of the company (i.e., market capitalization, which

is the price of the stock multiplied with the no. of shares outstanding)

b. Weighing by the price of the company’s stock; and

c. Weighing each company equally regardless of its market value or price.

6

8/7/2019 im project-1

http://slidepdf.com/reader/full/im-project-1 7/37

With the exception of DJIA, VLCA and MMI, the preeminent stock market indices are

market value weighed. The DJIA is a price weighed index, with the index adjusted for

stock splits and stock dividends. The VLCA and MMI are equally weighed indices.

Given the stocks and the relative weightage to be assigned to each one of them, it is then

necessary to average the individual components. Two methods of Averaging are

possible: Arithmetic and Geometric.

An Arithmetic Mean is basically a simple average of the component stocks, calculated

by summing the components after weighing them and dividing by the sum of the weights.

A Geometric Mean involves the multiplication of the components, after which the

product is raised to the power of one divided by the number of components.

All properly constructed stock market indicators are constructed using Arithmetic

Averaging.

Globally, so far, the major application of a market index has been to examine the level of

index and know how the overall market has been faring. Therefore, for a market index to

excel at this application, it must have the following three features:

1. It should capture the behavior of a large variety of different portfolios in the

country.

2. The index set should be highly liquid.

7

8/7/2019 im project-1

http://slidepdf.com/reader/full/im-project-1 8/37

3. It should have a long historical time series of index performance.

Keeping this in mind, let us now study in detail the two most recognized and employed

indices of the Indian Equity Market.

CHAPTER 2CHAPTER 2

S & P CNX NIFTYS & P CNX NIFTY

8

8/7/2019 im project-1

http://slidepdf.com/reader/full/im-project-1 9/37

S & P CNX NIFTY

The NSE –50 Index was launched by the National Stock Exchange of India Limited,

taking as base the closing prices of November 3, 1995 when one year of its Capital

Market segment was completed. It was subsequently renamed S & P CNX Nifty- with

S & P indicating endorsement of the Index by Standard and Poor’s and CNX standing for

CRISIL NSE Index.

The S & P CNX NIFTY, also popularly known as the Nifty 50, is one of the most

scientific indices in India that reflects the price movement of 50 blue- chips, large cap,

liquid and highly traded stocks of 23 sectors. The Nifty is managed by India Index

Services & Products Ltd. (IISL). The total value of all Nifty stocks is approximately 70%

of the traded value of all stocks on the NSE. Nifty stocks represent about 59% of the total

market capitalization.

2.1 OBJECTIVES

The basic idea of this index is to ascertain the movements of the stock market as a whole

by tapping the news which can affect the stock. The index also averages out the good

stock - specific news for a few companies and bad stock - specific news for others and

left with the news that is common to all stocks. The news that is common to all stocks is

news about India, which is the sole purpose of NSE Nifty. According to NSE, the Indexwas introduced with the objectives of:

Reflecting market movement more accurately,

Providing Fund Managers with a tool for measuring portfolio returns vis-à-vis

market returns, and

9

8/7/2019 im project-1

http://slidepdf.com/reader/full/im-project-1 10/37

Providing a basis for introducing Index based derivatives.

The Index is based on the prices of the shares of 50 companies (chosen from among the

companies traded on the NSE), each with a market capitalization of at least Rs 500 crores

and having high degree of liquidity. The methodology used for the computation of this

Index is market capitalization weighted as followed by the S & P 500. The base value of

this Index has been set as 1000. The Index allows the corporate actions like stock splits,

rights issues etc without affecting its value.

2.2 SELECTION CRITERIA

The constituents and the criteria for the selection judge the effectiveness of the index. S

& P CNX Nifty is unique in this respect. The criteria for selection and review of scrips

for the S & P CNX NIFTY are:

Liquidity ( or Impact Cost)

Average Market Capitalization for the last six months

Floating Stock, which is traded in the market

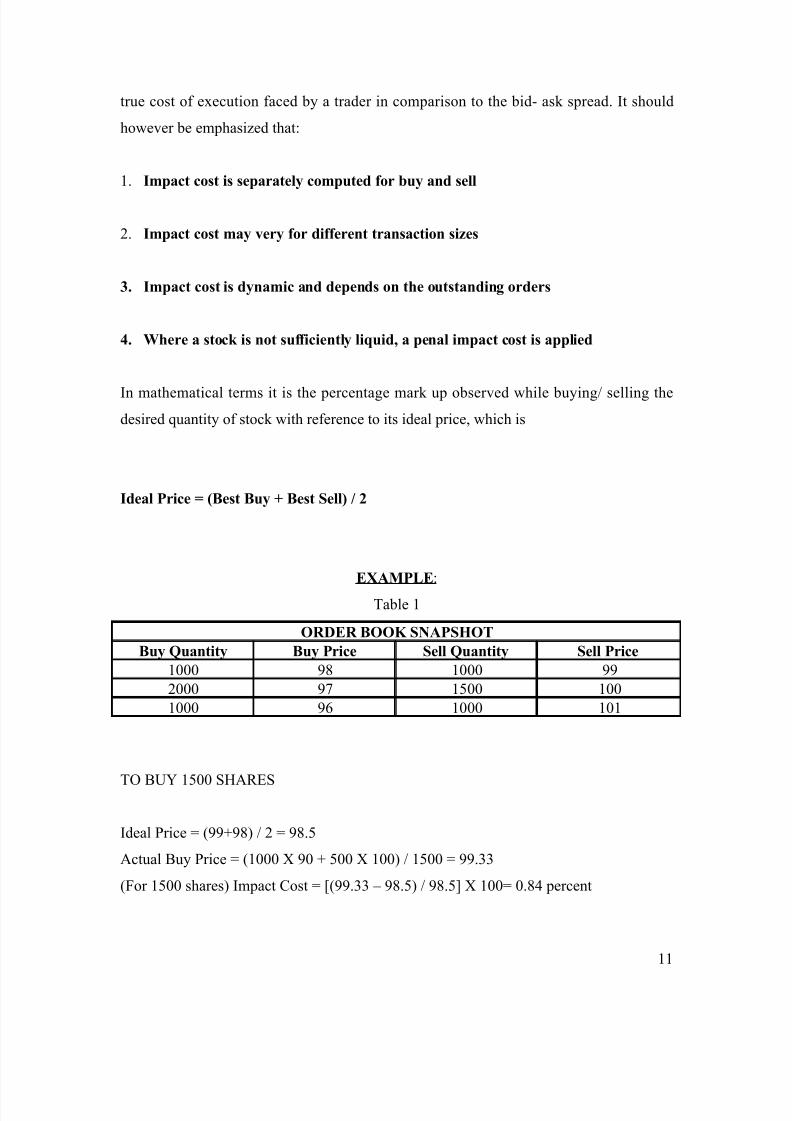

IMPACT COST

For inclusion in the index, the security should have traded at an average impact cost of

0.75 percent or less during the last six months for 90 percent of the observations. Impact

cost is cost of executing a transaction in a security in proportion to the weight age of its

market capitalization as against the index market capitalization at any point of time.

Impact cost is a practical and realistic measure of market liquidity; it is closer to the

10

8/7/2019 im project-1

http://slidepdf.com/reader/full/im-project-1 11/37

true cost of execution faced by a trader in comparison to the bid- ask spread. It should

however be emphasized that:

1. Impact cost is separately computed for buy and sell

2. Impact cost may very for different transaction sizes

3. Impact cost is dynamic and depends on the outstanding orders

4. Where a stock is not sufficiently liquid, a penal impact cost is applied

In mathematical terms it is the percentage mark up observed while buying/ selling the

desired quantity of stock with reference to its ideal price, which is

Ideal Price = (Best Buy + Best Sell) / 2

EXAMPLE :

Table 1

ORDER BOOK SNAPSHOT

Buy Quantity Buy Price Sell Quantity Sell Price

1000 98 1000 99

2000 97 1500 100

1000 96 1000 101

TO BUY 1500 SHARES

Ideal Price = (99+98) / 2 = 98.5

Actual Buy Price = (1000 X 90 + 500 X 100) / 1500 = 99.33

(For 1500 shares) Impact Cost = [(99.33 – 98.5) / 98.5] X 100= 0.84 percent

11

8/7/2019 im project-1

http://slidepdf.com/reader/full/im-project-1 12/37

The Electronic Limit Order Book (ELOB) as available on NSE is an ideal provider of

market liquidity. This style of market dispenses with market makers, and allows anyone

in the market to execute orders against the best available counter orders. The market may

thus be thought of as possessing liquidity in terms of outstanding orders laying on the buy

and sell side of the order book, which represent the intention to buy or sell.

When a buyer or seller approaches the market with an intention to buy a particular stock,

he can execute his order in the stock against such sell orders, which are already lying in

the order book, and vice versa.

An example of an order book for a stock at a point in time is detailed below:

Table 2

BUY SELL

S. No. Quantity Price Quantity Price S. No.

1 1,000 3.5 2,000 4 5

2 1,000 3.4 1,000 4.05 6

3 2,000 3.4 500 4.2 7

4 1,000 3.3 100 4.25 8

There are four buy and four sell orders lying in the order book. The difference between

the best buy and the best sell orders (in this case, Rs. 0.50) is the bid - ask spread. If a

person places an order to buy 100 shares, it would be matched against the best available

sell order at Rs. 4 i.e. he would buy 100 shares for Rs. 4. If he places a sell order for 100

shares, it would be matched against the best available buy order at Rs. 3.50 i.e. the shares

would be sold at Rs. 3.5. Hence if a person buys 100 shares and sells them immediately,

he is poorer by the bid-ask spread. This spread may be regarded as the transaction cost

which the market charges for the privilege of trading (for a transaction size of 100

shares). Progressing further, it may be observed that the bid-ask spread as specified above

is valid for an order size of 100 shares upto 1000 shares. However for a larger order size

the transaction cost would be quite different from the bid- ask spread.

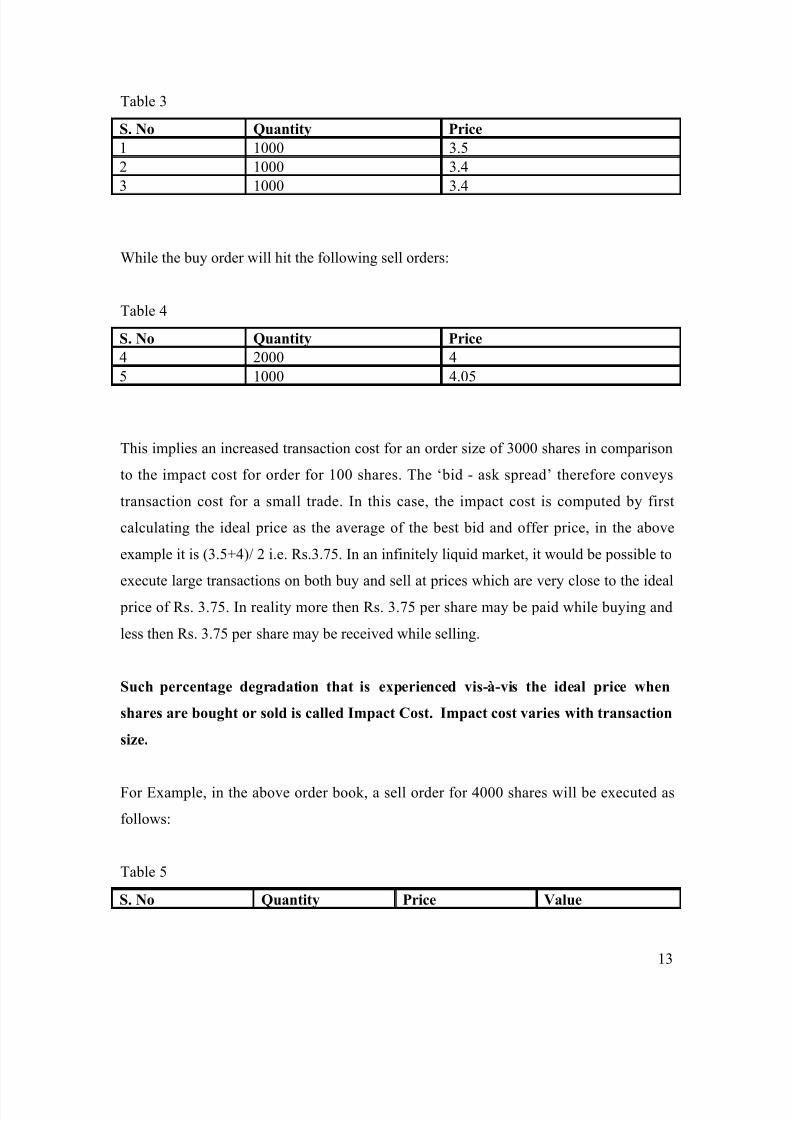

Suppose a person wants to buy and then sell 3000 shares. The sell order will hit the

following buy orders.

12

8/7/2019 im project-1

http://slidepdf.com/reader/full/im-project-1 13/37

Table 3

S. No Quantity Price

1 1000 3.5

2 1000 3.4

3 1000 3.4

While the buy order will hit the following sell orders:

Table 4

S. No Quantity Price

4 2000 4

5 1000 4.05

This implies an increased transaction cost for an order size of 3000 shares in comparison

to the impact cost for order for 100 shares. The ‘bid - ask spread’ therefore conveys

transaction cost for a small trade. In this case, the impact cost is computed by first

calculating the ideal price as the average of the best bid and offer price, in the above

example it is (3.5+4)/ 2 i.e. Rs.3.75. In an infinitely liquid market, it would be possible to

execute large transactions on both buy and sell at prices which are very close to the idealprice of Rs. 3.75. In reality more then Rs. 3.75 per share may be paid while buying and

less then Rs. 3.75 per share may be received while selling.

Such percentage degradation that is experienced vis-à-vis the ideal price when

shares are bought or sold is called Impact Cost. Impact cost varies with transaction

size.

For Example, in the above order book, a sell order for 4000 shares will be executed as

follows:

Table 5

S. No Quantity Price Value

13

8/7/2019 im project-1

http://slidepdf.com/reader/full/im-project-1 14/37

1 1,000 3.5 3,500

2 1,000 3.4 3,400

3 2,000 3.4 6,800

Total Value

Wt. Average Price

13,700

3.43

The sale price for 4000 shares is Rs. 3.43, which is 8.53 percent worse than the ideal

price of Rs. 3.75. Hence we say, ‘The impact cost faced in buying 4000 shares is 8.53

percent.’

Liquidity in the context of stock markets means a market where large orders can be

executed without incurring a high transaction cost. The transaction cost referred here

is not the fixed costs typically incurred like brokerage, transaction charges, depository

charges etc. but is the cost attributable to lack of market liquidity as explained

subsequently. Liquidity comes from the buyers and sellers in the market, who are

constantly on the look out for buying and selling opportunities. Lack of liquidity

translates into a high cost for buyers and sellers.

MARKET CAPITALISATION

Companies eligible for inclusion in Nifty must have six monthly average market

capitalizations of Rs. 500 crores or more during the last six months.

FLOATING STOCK

Companies eligible for inclusion in S & P CNX Nifty should have at least 12 percent

floating stock. For this purpose, floating stock shall mean stocks which are not held by

the promoters and associated entities (where identifiable) of such companies.

14

8/7/2019 im project-1

http://slidepdf.com/reader/full/im-project-1 15/37

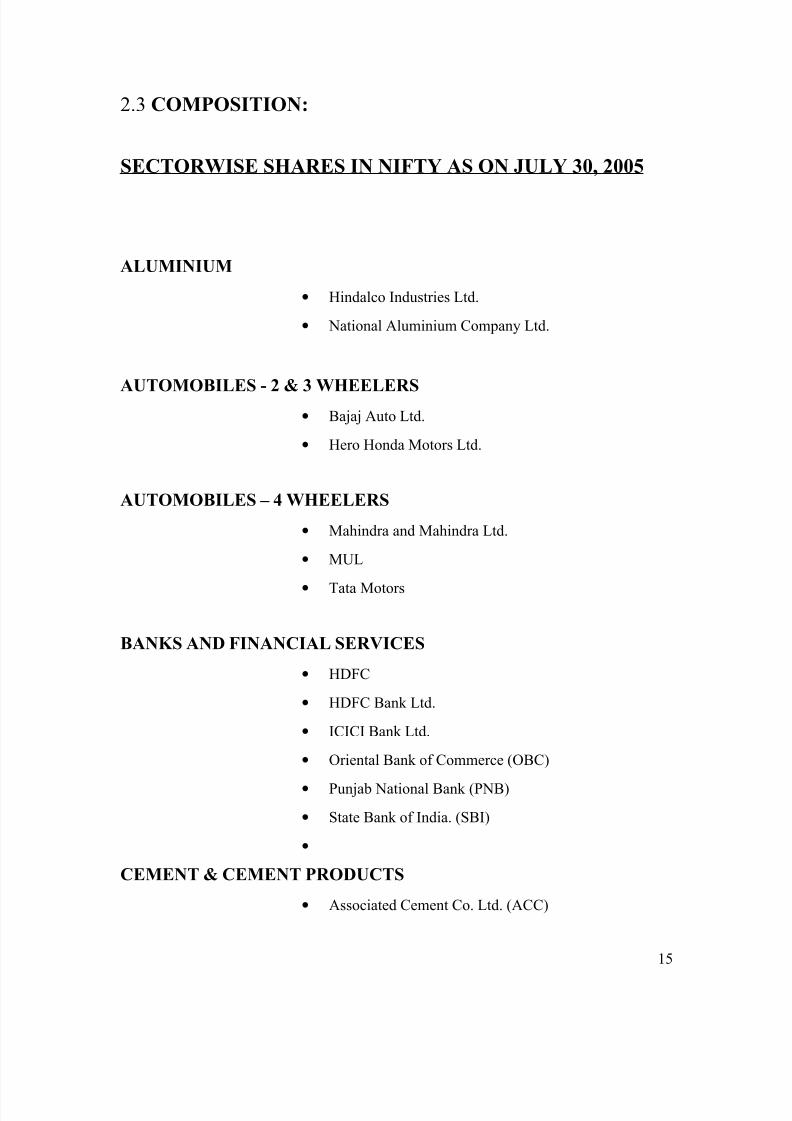

2.3 COMPOSITION:

SECTORWISE SHARES IN NIFTY AS ON JULY 30, 2005

ALUMINIUM

• Hindalco Industries Ltd.

• National Aluminium Company Ltd.

AUTOMOBILES - 2 & 3 WHEELERS• Bajaj Auto Ltd.

• Hero Honda Motors Ltd.

AUTOMOBILES – 4 WHEELERS

• Mahindra and Mahindra Ltd.

• MUL

• Tata Motors

BANKS AND FINANCIAL SERVICES

• HDFC

• HDFC Bank Ltd.

• ICICI Bank Ltd.

• Oriental Bank of Commerce (OBC)

• Punjab National Bank (PNB)

• State Bank of India. (SBI)

•

CEMENT & CEMENT PRODUCTS

• Associated Cement Co. Ltd. (ACC)

15

8/7/2019 im project-1

http://slidepdf.com/reader/full/im-project-1 16/37

• Grasim Industries Ltd.

• Gujarat Ambuja Cements Ltd.

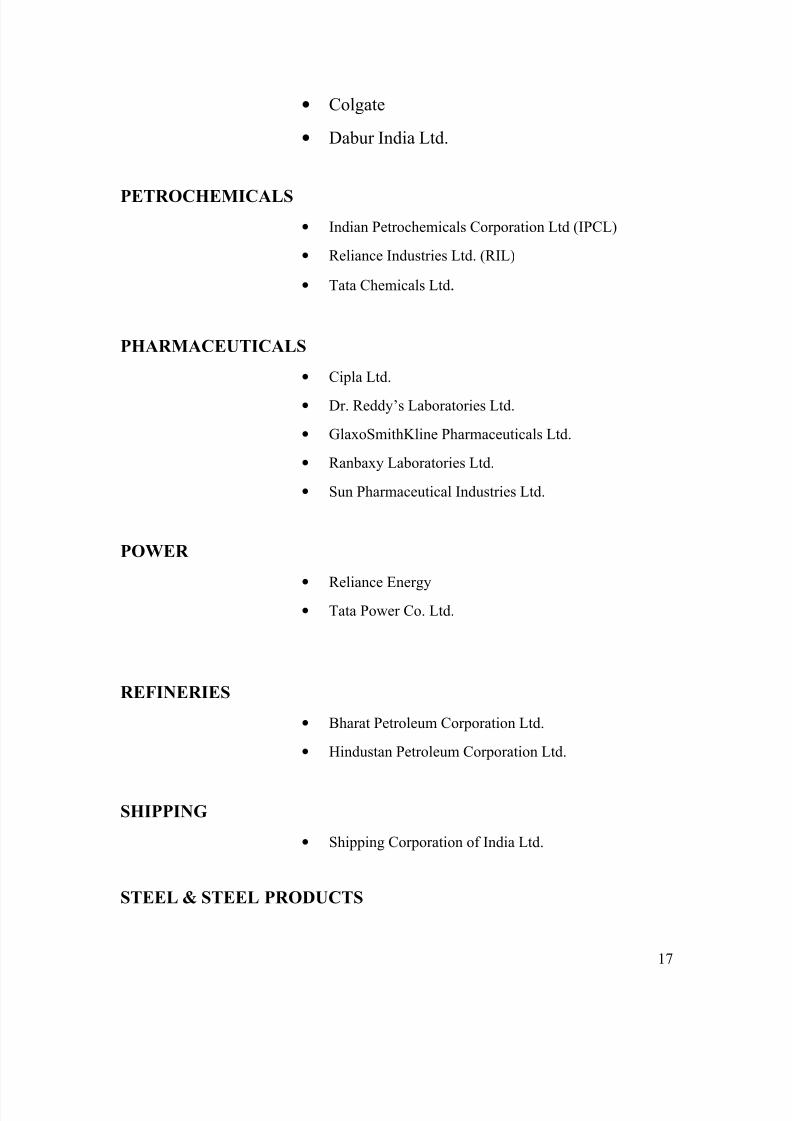

FMCG• HUL.

• ITC Ltd.

ENGINEERING GOODS

• ABB

• BHEL

• L & T

INFORMATION TECHNOLOGY

• Infosys Technologies Ltd.

• HCL Technologies Ltd.

• Satyam Computers Ltd.

• TCS

• Wipro Ltd.

OIL AND GAS

• Gas Authority of India Ltd. (GAIL)

• ONGC

MEDIA & ENTERTAINMENT

• Zee Telefilms Ltd.

PERSONAL CARE

16

8/7/2019 im project-1

http://slidepdf.com/reader/full/im-project-1 17/37

8/7/2019 im project-1

http://slidepdf.com/reader/full/im-project-1 18/37

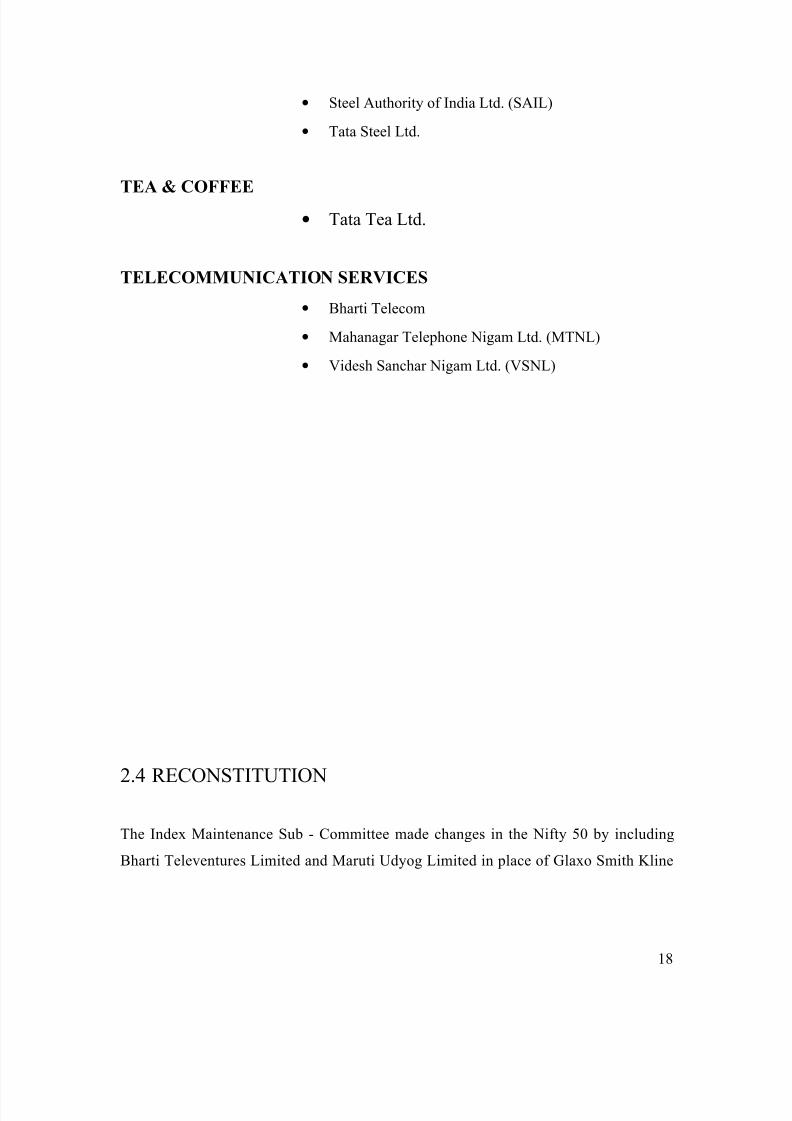

• Steel Authority of India Ltd. (SAIL)

• Tata Steel Ltd.

TEA & COFFEE• Tata Tea Ltd.

TELECOMMUNICATION SERVICES

• Bharti Telecom

• Mahanagar Telephone Nigam Ltd. (MTNL)

• Videsh Sanchar Nigam Ltd. (VSNL)

2.4 RECONSTITUTION

The Index Maintenance Sub - Committee made changes in the Nifty 50 by including

Bharti Televentures Limited and Maruti Udyog Limited in place of Glaxo Smith Kline

18

8/7/2019 im project-1

http://slidepdf.com/reader/full/im-project-1 19/37

Consumer Healthcare Limited and NIIT Limited respectively. These changes became

effective from March 01, 2004.

These type of reshuffling is done in order to achieve the objective with which Nifty is

formed. Also it ensures that all the fifty stocks are liquid stocks. The moment authorities

think that stocks are no longer liquid they brought changes in the composition of index.

S & P CNX Nifty uses clear researched and publicly documented rules for index revision.

These rules are applied regularly, to obtain changes to the index set. Index reviews are

carried out every quarter to ensure that each security in the index fulfills all the laid down

criteria. IDBI was once not listed; SBI was once illiquid; Infosys was once an obscure

software startup. The world changes, and one by one, these stocks have come into the

S & P CNX Nifty. Each change in the S & P CNX Nifty is small, so the continuity of the

Index is maintained.

2.5 COMPUTATION OF NIFTY 50

S & P CNX Nifty is computed using market capitalization weighted method, wherein the

level of the index reflects the total market value of all the stocks in the index relative to a

particular base period. The method also takes into account constituent changes in the

index and importantly corporate actions such as stock splits, rights, etc without affecting

the index value. The base period selected for S &P CNX Nifty index is the close of prices

on November 3, 1995, which marks the completion of one year of operations of NSE’s

Capital Market Segment. The base value of the index has been sat at 1,000 and a base

capital of Rs. 2.06 trillion.

The ‘Market Capitalization Weighted Method’ is same as explained for BSE Sensex. The

steps for computing the value of Sensex and Nifty are same as both uses same method of

computation.

19

8/7/2019 im project-1

http://slidepdf.com/reader/full/im-project-1 20/37

8/7/2019 im project-1

http://slidepdf.com/reader/full/im-project-1 21/37

1. The index levels are calculated from a highly liquid exchange with superior

surveillance procedures

2. S & P CNX Nifty has a large market capitalization so the consequence (upon the

index) of a given move in an individual stock price is smaller

3. S & P CNX Nifty calculation intrinsically requires liquidity in proportion to market

capitalization, thus avoiding weak links which a manipulator can attack. Users of the

S&P CNX Nifty benefit from the research that is possible owing to the long time-

series available: both S & P CNX Nifty and S&P CNX Nifty Total Returns Index

series are observed from July 1990 onwards. S&P CNX Nifty is backed by solid

economic research and three of the most respected institutions: NSE, S&P and

CRISIL.

21

8/7/2019 im project-1

http://slidepdf.com/reader/full/im-project-1 22/37

CHAPTER – 3

DOW JONES INDUSTRIAL

AVERAGE

DOWJONES INDUSTRIAL AVERAGE

22

8/7/2019 im project-1

http://slidepdf.com/reader/full/im-project-1 23/37

The Dow Jones Industrial Average (DJIA), also referred to as the Industrial Average,

the Dow Jones, the Dow 30, or simply the Dow, is a stock market index, and one of

several indices created by Wall Street Journal editor and Dow Jones & Company co-

founder Charles Dow. It is now owned by the CME Group, who is the majority owner

of Dow Jones Indexes. The average is named after Dow and one of his business

associates, statistician Edward Jones. It is an index that shows how 30 large, publicly

owned companies based in the United States have traded during a standard trading

session in the stock market.

The Industrial portion of the name is largely historical, as many of the modern 30

components have little or nothing to do with traditional heavy industry.

Along with the NASDAQ Composite, the S&P 500 Index, and the Russell 2000 Index,

the Dow is among the most closely watched benchmark indices tracking targeted stock

market activities. The index's performance continues to be influenced by not only

corporate and economic reports, but also by domestic and foreign political events such as

war and terrorism, as well as by natural disasters that could potentially lead to economic

harm.

COMPOSITION

The Dow Jones Industrial Average currently consists of the following 30 companies:

CONGLOMERATE

• 3M

• General Electric

• United Technologies Corporation

ALUMINIUM

• Alcoa

23

8/7/2019 im project-1

http://slidepdf.com/reader/full/im-project-1 24/37

CONSUMER FINANCE

• American Express

TELECOMMUNICATION

• AT&T

BANKING

• Bank of America

•JP Morgan Chase

AEROSPACE AND DEFENCE

• Boeing

CONSTRUCTION AND MINING EQUIPMENT

• Caterpillar

OIL AND GAS

• Chevron Corporation

• ExxonMobil

COMUTER NETWORKING

• Cisco System

BEVERAGES

• Coca – Cola

24

8/7/2019 im project-1

http://slidepdf.com/reader/full/im-project-1 25/37

CHEMICAL INDUSTRY

• DuPont

TECHNOLOGY

• Hewlett – Packard

• IBM

HOME IMPROVEMENT RETAILER

•The Home Depot

SEMICONDUCTORS

• Intel

PHARMACEUTICAL

• Johnson & Johnson

• Merck

• Pfizer

FOOD PROCESSING

• Kraft Foods

FAST FOOD

• McDonald’s

25

8/7/2019 im project-1

http://slidepdf.com/reader/full/im-project-1 26/37

SOFTWARE

• Microsoft

CONSUMER GOODS

• Procter & Gamble

INSURANCE

• Travelers

TELECOMMUNICATION• Verizon Communication

RETAIL

• Wal – Mart

BROADCASTING AND ENTERTAINMENT

• Walt Disney

RECONSTITUTION

The components of the DJIA have changed 48 times in its 114 year history. When

companies are replaced, the scale factor used to calculate the index is adjusted so that the

value of the average remains the same. A summary of the more recent changes to the

index include the following:

On February 19, 2008, Chevron and Bank of America replaced Altria

Group and Honeywell. Chevron had previously been a Dow component from July 18,

1930, to November 1, 1999. During Chevron's absence, its split-adjusted price per share

26

8/7/2019 im project-1

http://slidepdf.com/reader/full/im-project-1 27/37

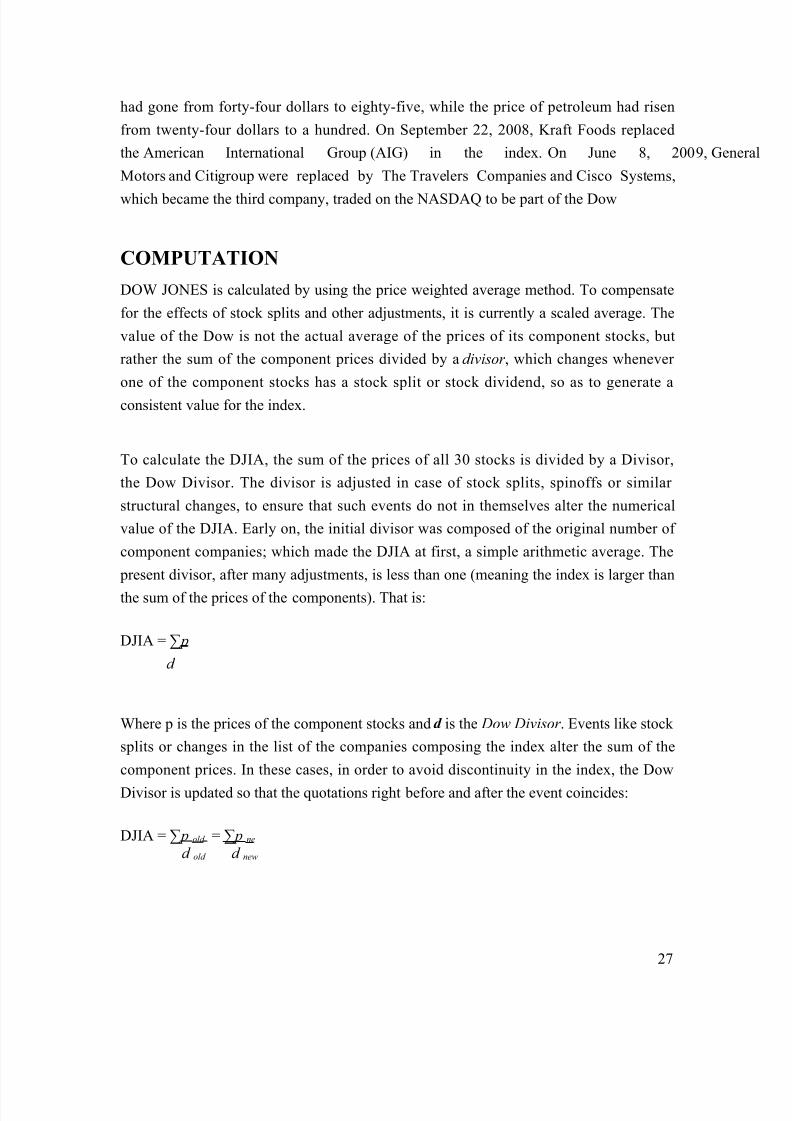

had gone from forty-four dollars to eighty-five, while the price of petroleum had risen

from twenty-four dollars to a hundred. On September 22, 2008, Kraft Foods replaced

the American International Group (AIG) in the index. On June 8, 2009, Gene

Motors and Citigroup were replaced by The Travelers Companies and Cisco Systems,

which became the third company, traded on the NASDAQ to be part of the Dow

COMPUTATION

DOW JONES is calculated by using the price weighted average method. To compensate

for the effects of stock splits and other adjustments, it is currently a scaled average. The

value of the Dow is not the actual average of the prices of its component stocks, but

rather the sum of the component prices divided by a divisor , which changes whenever

one of the component stocks has a stock split or stock dividend, so as to generate a

consistent value for the index.

To calculate the DJIA, the sum of the prices of all 30 stocks is divided by a Divisor,

the Dow Divisor. The divisor is adjusted in case of stock splits, spinoffs or similar

structural changes, to ensure that such events do not in themselves alter the numerical

value of the DJIA. Early on, the initial divisor was composed of the original number of

component companies; which made the DJIA at first, a simple arithmetic average. The

present divisor, after many adjustments, is less than one (meaning the index is larger than

the sum of the prices of the components). That is:

DJIA = ∑p

d

Where p is the prices of the component stocks and d is the Dow Divisor . Events like stock

splits or changes in the list of the companies composing the index alter the sum of the

component prices. In these cases, in order to avoid discontinuity in the index, the Dow

Divisor is updated so that the quotations right before and after the event coincides:

DJIA = ∑p old = ∑ p ne

d old d new

27

8/7/2019 im project-1

http://slidepdf.com/reader/full/im-project-1 28/37

The Dow Divisor is currently 0.132319125. Presently, every $1 change in price in a

particular stock within the average, equates to a 7.56 (1/0.132319125) point movement

CHAPTER 4CHAPTER 4

CORRELATIONCORRELATION

28

8/7/2019 im project-1

http://slidepdf.com/reader/full/im-project-1 29/37

4.1 CORRELATION BETWEEN BSE SENSEX AND NSE NIFTY

The cross – correlation coefficient r, which is a measure of linear association between

two variables, is defined as

∑1(x1-x) (y1-y)

∑1(x1-x) (y1-y)2

…… Equation 1….

A positive value of coefficient r indicates, that as one value increases the other tends to

increase whereas a negative value indicates as one variable increases the other tends to

decrease.

Here we are studying the correlation between the Bombay Stock Exchange Index Sensex

and the National stock exchange index Nifty. Both of these stock exchanges belong to

India and open and close at the same time i.e. they are synchronous.

The BSE index and the NSE index are known to be strongly correlated. Bombay Stock

exchange is the oldest stock exchange in whole of Asia. It was started in1875. The BSE

index is market capitalization weighted index of 30 stocks of sound Indian and

multinational companies. National stock exchange was established to provide access to

investors from all across India. NSE started equity operations in November 1994. The

NSE index also known as NIFTY is determined from 50 stocks of companies taken from

29

8/7/2019 im project-1

http://slidepdf.com/reader/full/im-project-1 30/37

23 sectors of economy. Following diagrams shows BSE index and NSE index

movements for the ten years from 1994 to 2003, both yearly and monthly. It is clear

from figure 1 and 2 that BSE and NSE indices are very similar in terms of the pattern of

share price movements.

FIGURE – 5.1 YEARLY MOVEMENT OF SENSEX & NIFTY

BSE SENSEX AND NSE NIFTY

0

5000

10000

15000

20000

25000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

YEARS

SE

NSEX & NIFTY

NIFTY

SENS

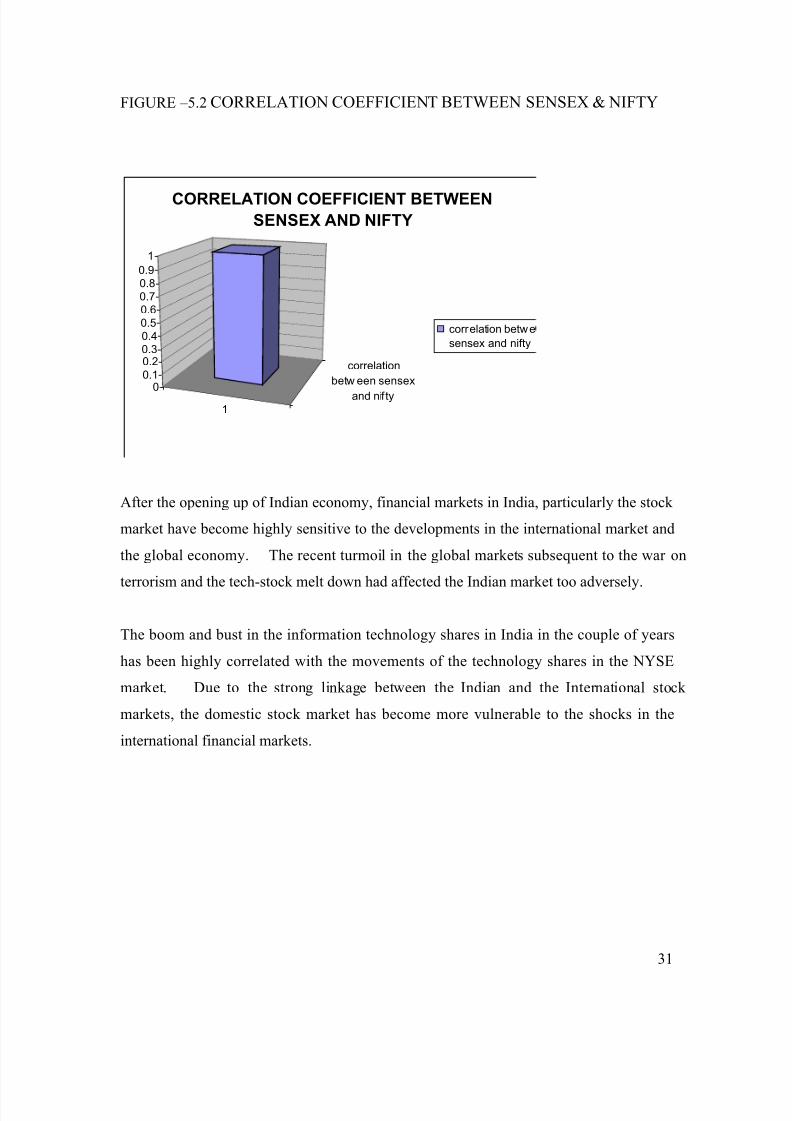

The calculated value of Correlation Coefficient (eauation1) between BSE and NSE

indices is r=0.999371 (yearly), which is represented in the following diagram. This value

of r also indicates that there exist strong positive correlation between BSE Sensex and

NSE Nifty. This is also evident form above two diagrams which show BSE and NSE

indices are highly correlated

30

8/7/2019 im project-1

http://slidepdf.com/reader/full/im-project-1 31/37

FIGURE –5.2 CORRELATION COEFFICIENT BETWEEN SENSEX & NIFTY

1

correlation

betw een sensex

and nif ty0

0.1

0.20.30.40.50.60.70.80.9

1

CORRELATION COEFFICIENT BETWEEN

SENSEX AND NIFTY

correlation betwe

sensex and nifty

After the opening up of Indian economy, financial markets in India, particularly the stock

market have become highly sensitive to the developments in the international market and

the global economy. The recent turmoil in the global markets subsequent to the war on

terrorism and the tech-stock melt down had affected the Indian market too adversely.

The boom and bust in the information technology shares in India in the couple of years

has been highly correlated with the movements of the technology shares in the NYSE

market. Due to the strong linkage between the Indian and the International stock

markets, the domestic stock market has become more vulnerable to the shocks in the

international financial markets.

31

8/7/2019 im project-1

http://slidepdf.com/reader/full/im-project-1 32/37

5.2 CORRELATION BETWEEN SENSEX, NIFTY & DOW

JONES

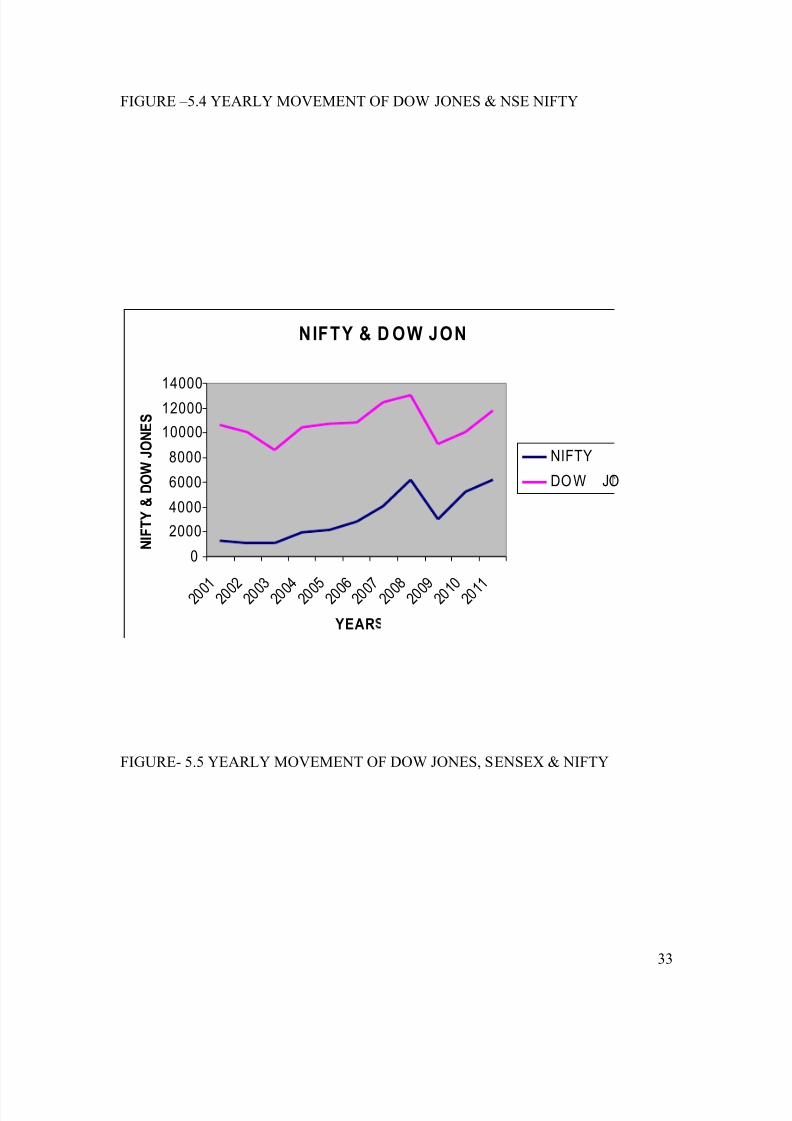

However, we have also calculated the correlation between Sensex, Nifty and Dow Jones.

It is found out that movement of three popular indices i.e. BSE Sensex, NSE Nifty and

Dow Jones is more similar in direction, both year wise (shows in figures 3, 4 and 5).

Diagrammatically,

FIGURE- 5.3 YEARLY MOVEMENT OF DOW JONES & BSE SENSEX

SENSEX & DOW JONES

0

5000

10000

15000

20000

25000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

YEARS

SENSEX & DOW JONES

SENSEX

DOW JON

32

8/7/2019 im project-1

http://slidepdf.com/reader/full/im-project-1 33/37

FIGURE –5.4 YEARLY MOVEMENT OF DOW JONES & NSE NIFTY

NIFTY & D OW JON

0

2000

4000

6000

8000

10000

12000

14000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

YEAR

NIFTY & DOW JONES

NIFTY

DO W JO

FIGURE- 5.5 YEARLY MOVEMENT OF DOW JONES, SENSEX & NIFTY

33

8/7/2019 im project-1

http://slidepdf.com/reader/full/im-project-1 34/37

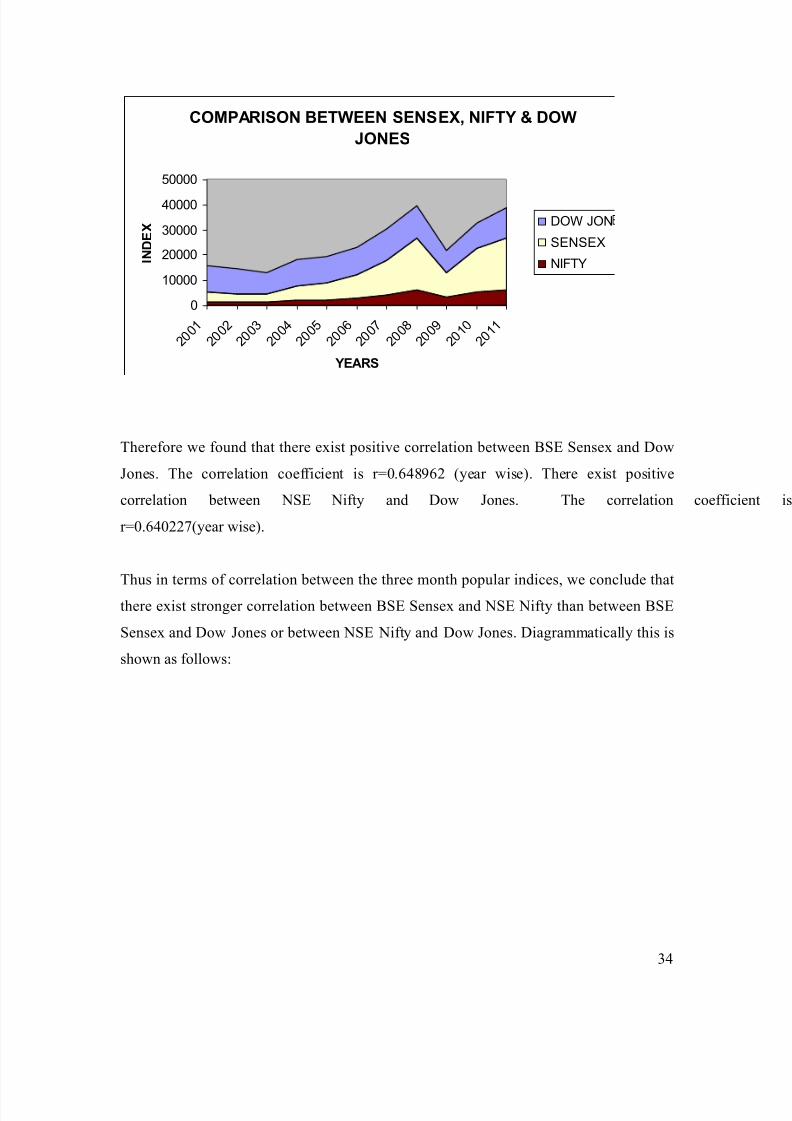

COMPARISON BETWEEN SENSEX, NIFTY & DOW

JONES

0

10000

20000

30000

40000

50000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

YEARS

INDEX

DOW JON

SENSEX

NIFTY

Therefore we found that there exist positive correlation between BSE Sensex and Dow

Jones. The correlation coefficient is r=0.648962 (year wise). There exist positive

correlation between NSE Nifty and Dow Jones. The correlation coeffici

r=0.640227(year wise).

Thus in terms of correlation between the three month popular indices, we conclude thatthere exist stronger correlation between BSE Sensex and NSE Nifty than between BSE

Sensex and Dow Jones or between NSE Nifty and Dow Jones. Diagrammatically this is

shown as follows:

34

8/7/2019 im project-1

http://slidepdf.com/reader/full/im-project-1 35/37

FIGURE 5.6 CORRELATION BETWEEN SENSEX, NIFTY & DOW JONES

0

0.2

0.4

0.6

0.8

1

correl nifty

sensex

correl nifty

dow jones

correl sensex

nd dow jones

CORRELATION

CORRELATI

35

8/7/2019 im project-1

http://slidepdf.com/reader/full/im-project-1 36/37

8/7/2019 im project-1

http://slidepdf.com/reader/full/im-project-1 37/37

CONCLUSION:

NSE C&P NIFTY is calculated using the average weighted market capitalization method.

Whereas NYSE Dow Jones Industrial Average (DJIA) is computed using the priceweighted method.

Though the method of computation is different but both the indices take into account all

the sectors and show the actual face of the markets.

The NSE NIFTY and the NYSE Dow Jones Industrial Average, have a positive

correlation. This shows as one increases the other also increases and vice versa. The BSE

SENSEX and the NYSE Dow Jones are also positively correlated showing as one

increases the other also increases. Whereas the NSE NIFTY and the BSE SENSEX are

highly correlated having correlation coefficient = 0.999 approximately showing that they

are similar in pattern and share price movements.

![SELF-CONTAINED CUBER IM-21CNE IM-30CNE IM-30CWNE€¦ · Outlet Hose 1 1 2 1 1/2-3/4 Nipple - - 2 - Leg - 4 4 5 Connector Cover 1 1 1 1 3/4-3/4 Nipple - - - 1 [IM-45CNE] Top Panel](https://img.pdfslide.us/doc/110x75/5f7b6508f72d951450780c36/self-contained-cuber-im-21cne-im-30cne-im-30cwne-outlet-hose-1-1-2-1-12-34-nipple.jpg)