Embed Size (px)

Citation preview

Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

Darren O’Connell

Barry O’Grady

© May 2012.

Curtin University of Technology

2

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

» May 2012

» Palisade Risk Conference

Disclaimer

The views expressed are those of the presenters, and may not necessarily reflect those of Curtin University of Technology.

The information in this presentation is not intended as investment advice. The presenter is not offering or making recommendations in relation to securities or other financial or investment products.

Use of information contained in this presentation is at your own risk. The presenter recommends you seek independent professional advice prior to making any investment decisions.

3

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

» May 2012

» Palisade Risk Conference

Presentation Programme

1. Motivation for Study

2. Asset Selection

3. Data Sampling

4. Modelling Approach

5. Results

6. Conclusion

4

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller May 2012 Palisade Risk Conference

Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

Motivation for Study

5

Motivations

Excel® remains the tool of choice for many risk management units in Australia because:

Risk management functions are starved of resources

Customised solutions are expensive and must be tailored to specific requirements

System implementation and project risks are very high

Staff training costs increase accordingly

Recipients of risk management output are generally not “quants” and have little appetite for statistical and econometric content

“Close Enough” is “Good Enough” attitude

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

» May 2012

» Palisade Risk Conference

6

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

» May 2012

» Palisade Risk Conference

Motivations

From experience, Excel® continues to be utilised heavily for financial risk management in Australia

Excellent “blank canvas” in which to test ideas:

Cheap to purchase

easy-to-use intuitive interface

Wide availability allowing model portability

Wide range of statistical functions

Large data sets can be analysed

Low staff training costs

In short, Excel is a popular development medium

7

Motivations

There are some significant drawbacks that directly affect the accuracy and robustness of statistical models:

Precision of numerical calculations questionable

Statistical functionality frequently inaccurate

Many commonly-used statistics and methods are NOT included

I could go on but…

“... it is not safe to assume that Microsoft Excel’s statistical procedures give the correct answer. Persons who wish to conduct statistical analyses should use some other package.”

McCullough and Heiser (2008)

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

» May 2012

» Palisade Risk Conference

8

Motivations

Many risk management personnel learn their trade in University

Excel is used to build simple time-series models that analyse the risk and return structure of traded securities

Normal distribution is most commonly cited in text books and is best understood – particularly in the work place

Excel’s in-built probability distributions are used to illustrate simple risk management problems

Practice persists in the work place through direct transfer of this learning

Limited knowledge coupled with Excel’s statistical limitations results in sub-optimal risk models

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

» May 2012

» Palisade Risk Conference

9

Motivations

These drawbacks are easily remedied!

Simple, easy-to-use COTS software exists that deliver superior statistical capabilities without the need for a PhD in the mathematical sciences

Many can be integrated into Excel

Others compliment Excel and interface in other ways

These solutions do not require a large capital outlay or expensive training

They provide the means to achieve much higher degrees of precision in risk modelling

Model output will better service the needs of decision makers

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

» May 2012

» Palisade Risk Conference

10

Motivations

We road-test Palisade’s @Risk add-in for Excel within a simple VaR framework to demonstrate how model precision increases

Our road-test is applied to a couple of (highly) illiquid securities

We fit a theoretical distribution to the historical data using then examine whether the @Risk choice passes the @Risk distribution palette

We test whether the choice passes the empirical distribution test with Eviews

We compare the violation outcomes produced by the normal distribution versus the @Risk choice

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

» May 2012

» Palisade Risk Conference

11

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller May 2012 Palisade Risk Conference

Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

Asset Selection

12

Asset Selection

GFC caused liquidity to evaporate and asset class correlations converged

Significant residual volatility remains, liquidity concerns persists due to Euro currency and debt crisis

Global asset price volatility and illiquidity his Australian securities particularly hard

To demonstrate @Risk’s usefulness in selecting theoretical distributions more closely aligned to the historical data, we selected the following securities:

“Penny” stock PIE Networks

The enviro-asset Renewable Energy Certificate (REC)

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

» May 2012

» Palisade Risk Conference

13

PIE Networks

Australia possesses an embryonic IT sector but lacks the scale and scope of Europe and the US

ASX lists a number GICS dedicated to IT

PIE describes itself as a manager of WiFi services and public Internet solutions

Flagship product is a Hotspot Webphone – a replacement to the traditional public phone booth – offering telecoms, internet, payment channels and advertising

Currently undertaking trials at Australian airports

Revenue model is based on hardware sales, recurring software sales and service fees

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

» May 2012

» Palisade Risk Conference

14

PIE Networks

Listing date: 7 April 2000

Market high: $0.118

Market low: $0.007

Average price: $0.17

Average return: 0.13% per week

Return volatility: 16.16% per week

Average turnover: 35,000 shares

Largest marketable parcel: 1,188,863 shares for $140,285

Weekly data: 27/11/2002 to 29 June 2011

448 data points

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

» May 2012

» Palisade Risk Conference

15

PIE Networks

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

» May 2012

» Palisade Risk Conference

16

PIE Networks

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

» May 2012

» Palisade Risk Conference

17

PIE Networks

Use @Risk to estimate the most likely theoretical distribution

Rank fit using the Anderson-Darling test statistic which attempts to fit the tails – of most interest to the risk manager

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

» May 2012

» Palisade Risk Conference

Distribution A-D Statistic

Logistic 5.9769

Normal 10.8968

Weibull 19.6951

18

PIE Networks

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

» May 2012

» Palisade Risk Conference

19

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

» May 2012

» Palisade Risk Conference

Renewable Energy Certificates

August 2009 saw an amendment to the MRET scheme demanding 45,000 GWh or 20% to total energy by 2020.

The objective will be met through the creation, trading and annual surrender of Renewable Energy Certificates (RECs).

Generators create RECs for each MWh of renewable electricity which is sold to retailers.

Retailers obligated to surrender sufficient RECs to meet its total energy purchases each calendar year.

20

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

» May 2012

» Palisade Risk Conference

Renewable Energy Certificates

Retailers obligated to surrender sufficient RECs to meet its total energy purchases each calendar year.

RECs can be traded in the secondary market through over-the-counter (OTC) channels – poor liquidity

The price of certificates is a function of:

Cost of supplying renewable generation;

The level of generation required to meet the MRET target;

The structure of the wholesale electricity market; and

The level of trading in secondary market RECs.

A number of structural factors underpin price behaviour; namely the exercise of market power and ongoing regulatory uncertainty.

21

Renewable Energy Certificates

Data supplied by AFMA

Collected by polling members about the prevailing offers and bids

Indicative prices are sorted using the “Median of Mids” method

Outliers removed when one standard deviation from midpoint

Resulting time series is “corrected” for skewness

Weekly data: 27/11/2002 to 6/01/2011

Market high & low: $53.21 and $11.94

Average price: 36.21

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

» May 2012

» Palisade Risk Conference

22

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

» May 2012

» Palisade Risk Conference

Renewable Energy Certificates

23

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

» May 2012

» Palisade Risk Conference

Renewable Energy Certificates

24

Renewable Energy Certificates

Use @Risk to estimate the most likely theoretical distribution

Rank fit using the Anderson-Darling test statistic which attempts to fit the tails – of most interest to the risk manager

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

» May 2012

» Palisade Risk Conference

Distribution A-D Statistic

Logistic 22.3093

Normal 46.7965

Weibull 63.9391

25

Renewable Energy Certificates

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

» May 2012

» Palisade Risk Conference

26

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller May 2012 Palisade Risk Conference

Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

Data Sampling

27

Data Sampling

Lack of long-term price history will result in model calibration issues and unstable VaR estimates

Represents a plausible industry scenario – newly created securities?

Option to use @Risk to synthetically create “history” or plausible “futures”

Using mean and variance parameters of each security to create another 500 (say) data points

Run a simulation to gain stable statistical estimates for normal and logistic distributions

Neither are perfect and both capture some of the stylised facts of the empirical distribtion

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

» May 2012

» Palisade Risk Conference

28

PIE Return Data vs Hypothetical Returns #1

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

» May 2012

» Palisade Risk Conference

-1.50

-1.00

-0.50

0.00

0.50

1.00

1.50

0 100 200 300 400 500 600 700 800

Return Normal

Statistic Historical Returns Normal samples

Mean Return 0.0012942 0.0107271

Standard

Deviation 0.1615584 0.1629046

Skewness -0.6370697 -0.0141445

Kurtosis 9.281909 -0.342546

Minimum Value -1.2299483 -0.5015656

Maximum Value 0.6505876 0.4428324

29

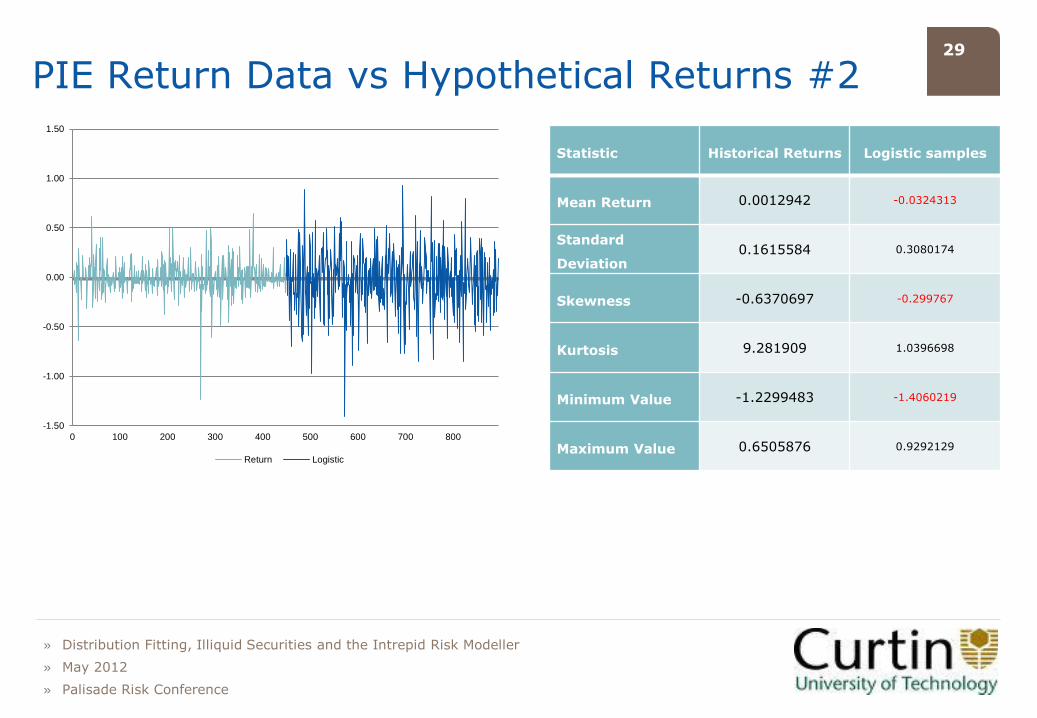

PIE Return Data vs Hypothetical Returns #2

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

» May 2012

» Palisade Risk Conference

-1.50

-1.00

-0.50

0.00

0.50

1.00

1.50

0 100 200 300 400 500 600 700 800

Return Logistic

Statistic Historical Returns Logistic samples

Mean Return 0.0012942 -0.0324313

Standard

Deviation 0.1615584 0.3080174

Skewness -0.6370697 -0.299767

Kurtosis 9.281909 1.0396698

Minimum Value -1.2299483 -1.4060219

Maximum Value 0.6505876 0.9292129

30

REC Return Data vs Hypothetical Returns #1

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

» May 2012

» Palisade Risk Conference

-0.40

-0.30

-0.20

-0.10

0.00

0.10

0.20

0.30

0 100 200 300 400 500 600 700 800

Return Normal

Statistic Historical Returns Normal samples

Mean Return -0.000492 0.000235

Standard

Deviation 0.0401726 0.037572

Skewness -0.6404766 -0.0298851

Kurtosis 21.325131 -0.1428352

Minimum Value -0.333154 -0.112075

Maximum Value 0.242703 0.097249

31

REC Return Data vs Hypothetical Returns #2

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

» May 2012

» Palisade Risk Conference

-0.40

-0.30

-0.20

-0.10

0.00

0.10

0.20

0.30

0 100 200 300 400 500 600 700 800

Return Logistic

Statistic Historical Returns Normal samples

Mean Return -0.000492 0.000235

Standard

Deviation 0.0401726 0.037572

Skewness -0.6404766 -0.0298851

Kurtosis 21.325131 -0.1428352

Minimum Value -0.333154 -0.112075

Maximum Value 0.242703 0.097249

32

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller May 2012 Palisade Risk Conference

Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

Modelling Approach

33

Modelling Approach

Risk managers need to understand the empirical characteristics of security prices, especially the volatility structure

If volatility is not mitigated, the probability of an extreme tail remains high

The impact of a tail event could cripple the capital reserves of the financial institution

Advanced models anticipate volatility changes better than non-paratmetric models but are harder to implement

Any market risk modelling should be done in conjunction with stress testing and scenario analysis

This framework helps to mitigate model risk

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

» May 2012

» Palisade Risk Conference

34

Modelling Approach

Neither securities have an active options market so we are unable to use implied volatility

Historical volatility from empirical data becomes the starting point

The Monte Carlo techniques employed by @Risk help to alleviate this handicap

Resulting models are probabilistic, not deterministic

Both data sets subjected to diagnostic tests in Eviews

Squared returns of both data sets exhibit Auto Regressive Conditional Heteroskedacity (ARCH-LM test)

Minimal skewness present in historical data

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

» May 2012

» Palisade Risk Conference

35

GARCH Specification

GARCH is a popular choice for VaR modelling because of how “innovations” in price affect today’s volatility (Jorion, 2003)

Volatility assumed to be non-constant

Relatively simple to estimate for fixed weight portfolios

Captures stylized facts of empirical return series such as volatility clustering

For simplicity, we chose the basic GARCH incarnation

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

» May 2012

» Palisade Risk Conference

2

1

2

1

2

ttt

36

GARCH Specification

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

» May 2012

» Palisade Risk Conference

ii z

|

|

2

t

2

t

),(~ 2

1 tt NI

),(~1 LFIt

37

GARCH Specification

GARCH parameters are set to near zero, construct a time series of conditional variance

Calculate likelihood of each observation then summed to get log likelihood

RiskOptimiser maximises log likelihood as per GARCH constraints

Initial parameters derived from historical data (simulation 0)

Future estimates of conditional variance estimated from random draws from the theoretical distributions

The VaR is simply the product of the conditional standard deviation and the level of significance chosen, in this case, at 90 per cent

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

» May 2012

» Palisade Risk Conference

38

GARCH Estimates: PIE

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

» May 2012

» Palisade Risk Conference

0.00

0.05

0.10

0.15

0.20

0.25

1 41 81 121 161 201 241 281 321 361 401 441 481

Normal GARCH Logistic GARCH

39

GARCH Estimates: RECs

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

» May 2012

» Palisade Risk Conference

0.00

0.02

0.04

0.06

1 41 81 121 161 201 241 281 321 361 401 441 481

Normal GARCH Logistic GARCH

40

Model Validation

Back testing examines accuracy of VaR using out of sample data

Failure of back test indicates that the model may be mis-specified and that large estimation error exist

A “violation” is recorded in next week’s actual return exceeds the VaR forecast using the sample data

The Conditional Coverage Test (CCT) is used to validate the models

The 500-sample represents one trial which is repeated 100,000 times using the simulation capabilities of @Risk to derive stable number of VaR violations

Test statistics are also recorded for each model

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

» May 2012

» Palisade Risk Conference

41

Coverage Tests

CCT is a flexible back testing methodology

CCT consists of an unconditional test based on actual number of violations against the theoretical number

There is an independence test to determine whether violations cluster

Null hypothesis for the unconditional test is whether the violations follow an IID Bernouli process and aligned to the significance level selected

Null hypothesis for independence is that the next violation is unrelated to the previous violation

For the model to be valid, and pass the CCT, it must pass the unconditional and independence tests respectively

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

» May 2012

» Palisade Risk Conference

42

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller May 2012 Palisade Risk Conference

Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

Results

43

Backtesting & Coverage: PIE

At the 10% level, similar number of violations

UC test under Normal will pass when 38 < V < 73

UC test under Logistic will pass when 41 < V <66

Violations outside these ranges are different from expected value (i.e. 50)

Will produce more violations due to persistence of volatility due to illiquidity

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

» May 2012

» Palisade Risk Conference

44

Backtesting & Coverage: RECs

Similar number of violations

UC test under Normal will pass when 38 < V < 75

UC test under Logistic will pass when 33 < V <63

As with PIE, the Logistic results in a tighter rejected band

Other factors in price action may account for wider bands (i.e. mean reversion)

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

» May 2012

» Palisade Risk Conference

45

Week-ahead VaR Estimates: PIE

The total number of consecutive violations was:

Normal = 8.33%

Logistic = 13.21%

For a difference of -4.88%

Logistic produces less stand-alone violations

Both models pass the independence test

Both models pass the Conditional Coverage Test

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

» May 2012

» Palisade Risk Conference

0

1

0%

10%

20%

30%

1 51 101 151 201 251 301 351 401 451

Normal VaR Exceedences

0

1

0%

10%

20%

30%

1 51 101 151 201 251 301 351 401 451

Logistic VaR Exceedences

46

Week-ahead VaR Estimates: RECs

The total number of consecutive violations was:

Normal = 13.46%

Logistic = 5.56%

For a difference of +7.90% per cent

Stand-alone violations almost equal

Both models pass the independence test

Both models pass the Conditional Coverage Test

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

» May 2012

» Palisade Risk Conference

0

1

0%

1%

2%

3%

4%

5%

6%

7%

1 51 101 151 201 251 301 351 401 451

Normal VaR Exceedences

0

1

0%

1%

2%

3%

4%

5%

6%

7%

1 51 101 151 201 251 301 351 401 451

Normal VaR Exceedences

47

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller May 2012 Palisade Risk Conference

Renewable Energy and Risk Modelling in an Australian Market Context

Conclusions

48

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

» May 2012

» Palisade Risk Conference

Conclusion

Ignoring textbook theory and adopting easy-to-use tools such as @Risk and Eviews in combination with Excel, we get:

An ability to model the price and return structure more accurately

A rich universe of theoretical distributions to model future price risk (in time-series analysis)

Econometrically robust frameworks without the PhDs

This study has shown that by adopting a better fitting PDF to a simple GARCH VaR framework, the resulting model is

More accurate

Sensitive to changes in external volatility

Better able to anticipate changes in risk profiles

49

Conclusion

@Risk and Eviews are powerful tools that provide intuitive insight into risk and reward opportunities contained within time-series securities data

Use these tools within the Excel development environment to build prototype enterprise models

Larger-scale customised solutions based on prototype models deployed at the enterprise level with the correct strategy and safeguards in place

May be a better, cheaper solution to COTS offerings

Start small and build up

No substitute for poor theory: do not let model results dictate theory

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

» May 2012

» Palisade Risk Conference

50

» Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller May 2012 Palisade Risk Conference

Distribution Fitting, Illiquid Securities and the Intrepid Risk Modeller

Questions & Comments?