Embed Size (px)

Citation preview

IIInnntttrrroooddduuuccciiinnnggg DDDeeessspppeeerrraaadddooosss iiinnn BBBooossstttooonnn

MMMaaarrrkkkeeetttiiinnnggg PPPlllaaannn 222000000777

SSSaaammmuuueeelll RRRaaabbbiiinnnooo VVViiiccceee PPPrrreeesssiiidddeeennnttt ooofff MMMaaarrrkkkeeetttiiinnnggg

BBBrrraaasssssseeerrriiieeesss FFFiiisssccchhheeerrr

MMMKKKTTT GGG222111222 CCCooonnnsssuuullltttaaannntttsss

RRRooowwwaaannn BBBrrreeennnnnnaaannn SSSttteeefffaaannn GGGeeebbbaaauuueeerrr

MMMaaarrrtttiiinnn HHHeeegggeeerrr MMMaaarrriiieee PPPaaayyymmmaaalll

PPPeeettteeerrr ZZZooouuummmmmmaaarrr

OOOccctttooobbbeeerrr 222333rrr ddd,,, 222000000666

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

2

Table of contents

TABLE OF CONTENTS .......................................................................................................................................2

EXECUTIVE SUMMARY .....................................................................................................................................3

1. PRELIMINARY ANALYSIS........................................................................................................................3

A. COUNTRY AND INDUSTRY PROFILE.....................................................................................................................3 B. FISCHER (HEINEKEN) COMPANY PROFILE..........................................................................................................7 C. SWOT ANALYSIS .................................................................................................................................................8

2. STRATEGIC GOALS AND OBJECTIVES..........................................................................................10

3. STRATEGIC OPTIONS .............................................................................................................................10

A. MODE OF ENTRY AND MARKETING STRATEGY ...............................................................................................10 B. SEGMENTATION AND TARGET GROUP..............................................................................................................11 C. POSITIONING AND COMPETITIVE STRATEGY...................................................................................................11

4. OPERATIVE MARKET ENTRY STRATEGY FOR 2007 ..............................................................12

A. GLOBAL PRODUCT .............................................................................................................................................12 B. PREMIUM PRICING .............................................................................................................................................12 C. ESTABLISHED DISTRIBUTION CHANNELS.........................................................................................................13 D. EXTENSIVE ADVERTISING AND PROMOTION CAMPAIGNS ..............................................................................14

5. CONCLUSION...............................................................................................................................................15

SOURCES ...............................................................................................................................................................16

EXHIBITS................................................................................................................................................................18

REFERENCES .......................................................................................................................................................48

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

3

Executive Summary

Despite severe regulations and high competition due to frequent new product launches and a large

number of substitutes, the American (and more precisely Bostonian) alcoholic drinks presents a great

potential for selling Desperados. The large portion of the population falling in the target group, who

showed high interest (46%, survey) in buying Tequila flavored beer, as well as Heineken’s strong

presence in the area, which provide tacit market knowledge and established distribution channels, are

essential factors for success. Fischer’s global marketing strategy will be applicable to a large extent to

this new market entry, yet adapted to legal constraints and market conditions. The product range will

not have to be altered (ideal for exports) and the global premium price strategy will be followed,

though the prices will be adapted to the highest of market. Fischer will receive full support from

Heineken concerning distribution but also the financing and design of extensive advertising and

promotion. Should Fischer achieve the market sales objectives of $182,000 without exceeding its

budget of $465,000 by too far, it will beginning its expansion to other major U.S. cities. Yet, it is highly

recommended to analyze carefully the laws and other environmental factors specific to the different

states.

1. Preliminary Analysis

a. Country and Industry Profile

i. Macroenvironmental Analysis

Politics Economy

The United States is a constitution-based federal republic with a strong democratic

tradition. The U.S. government has quite a liberal position towards alcohol

consumption, accepting it as a part of the American culture as long as the legal

framework is respected. Yet, it advises moderate consumption as it widely

broadcasted the results of a study by the National Institute on Alcohol Abuse and

Alcoholism (NIAAA) stating both the negative effects of alcohol abuse and the

positive effects of moderate drinking on heart health1.

The USA has the largest economy in the world with a per capita GDP of $42,000 in

20052 ($44,861 in Massachusetts (MA)3). Recently soaring oil prices threatened

inflation and unemployment. Yet, rise in prices is forecast at 2.0%4 p.a. over 2006-

07 and unemployment at 5.1%5. The real GDP growth was 3.7% p.a. over 2004-06

and is expected to slow down to 2.4% in 20076. The current median family income

is $59,600 in the U.S. (vs. $82,600 in Boston city), and has risen at 1.8% p.a. since

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

4

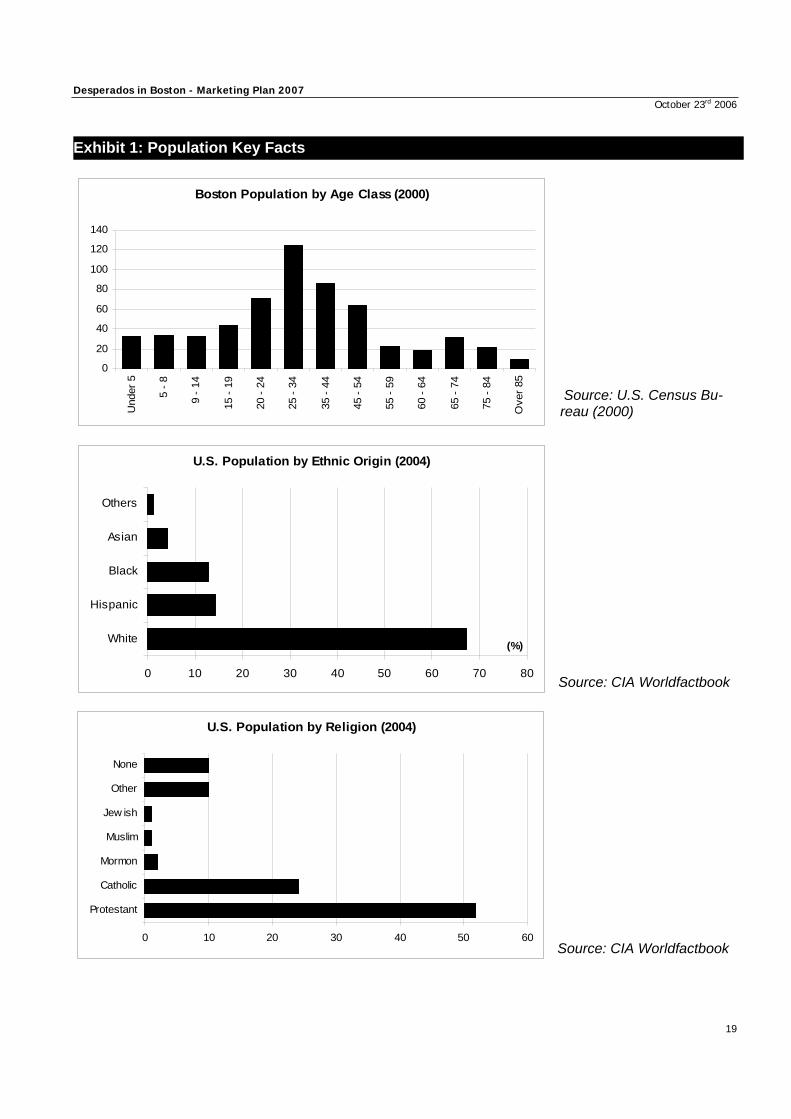

Social Technology Environment Laws and regulations

20037. The current currency rate of 0.8 €/$8 is not favorable to European exports.

The total population is 298.5 million people (almost 0.6 m in Boston city) with a

growth rate of 0.91% p.a. The U.S. median age of 36.5 years is significantly higher

than the Boston median age of 31. One third of all Bostonians are between 20-34.

In both the U.S. and Boston the gender ratio approximates a 1:1 repartition. Over

14% of Americans (and Bostonians) are Hispanic. 76% of all Americans are

Christians and only 3% of the population (Muslims and Mormons) are prohibited to

drink alcohol by religion. English is the dominant language (82% of natives), but

Spanish becomes increasingly important (11%)9 (Exhibit 1). Alcohol, and

especially beer, is a part of the American culture10. More than one third of

Americans between 12-20 years report alcohol consumption. Binge drinking is a

major issue threatening America’s youth (25%)11.

New technologies mainly affect the brewing process and result in both quality and

efficiency improvements. For instance, recent production chains reduce the

bottling time and the setup-time from one bottle format to another12. Some

innovations also concern packaging, as e.g. the pressure-sensitive labels

developed by Spear Systems® for Anheuser-Busch that deliver a frost effect on

the clear glass of the Bacardi Silver bottles13.

The container deposit legislation is different from state to state. Massachusetts

passed its bottle bill, the Beverage Container Recovery Law, in 1981. The law

requires a 5-cent deposit on deposit beverage containers, which is refunded when

empty containers are brought back to the selling point. Unclaimed deposits all go

directly to the state’s Clean Environment Fund (CEF)14.

Alcohol related laws15 are passed on the State level (e.g. Massachusetts General

Laws, Exhibit 2) and not by the American government. The legal drinking and

alcohol purchasing age is 21 in MA. The distribution of alcohol requires a selling

license delivered by the State and strict ID controls of each buyer. License holders

must pay a tax on their alcohol gross sales. The license for beers and other soft

alcohols is easier to obtain and tax is lower than for hard alcohols. Alcohol

consumption in public places is forbidden. Bars and pubs have to close at 2am. It

is strictly against law to drive under the influence of alcohol (limit of 0.08% of

alcohol in blood) or any intoxicating substance. Additionally to State laws, the

alcohol industry agreed on voluntary advertising regulations. At least 70% of the

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

5

viewership of any advertisement must be over 21 years old.16

ii. Alcoholic drinks Market Analysis

U.S. alcoholic drinks market volume and value Market segmentation Massachusetts alcohol drinks market volume and value Main demand drivers

The United States alcoholic drinks market is a mature market with a modest

growth of 1.9% p.a. over 2000-2004. The market value was $138.7 billion in 2004

and is forecast to reach about $151.9 billion in 2009 (+9.5% since 2004). The

market volume grew even slower over this period (1.1% p.a.) to reach 28.6 billion

liters in 2004, pointing out a shift toward premium products17.

The market is divided into five product categories: beer, spirits, wine, FABs

(flavored alcoholic beverages) and cider. Beer, FAB’s and cider (BFC) are

generally considered as one segment, due to the similar alcohol level. The BFC

segment still holds 55.7% of the market value in 2004 (59.0% in 1995), but it has

continuously been losing share to the spirits segment which now stands for 29.1%

of market value (26.4% in 1995). Yet, the BFC market value, which only grew by

0.8% over 2000-2004, is expected to accelerate its pace to a 1.1% growth over

2005-2009. Half of all beers are light, and about 60% are premium lager (Exhibit 3). The BFC market volume reached 24.2 billion liters in 2004, thus accounting for

84.6% of the alcoholic drinks market volume18.

The state of Massachusetts stood for 2.08% (502.5 million liter) of the U.S. beer

consumption in 2004. It is one of the states with the highest part of import beers

(nearly one fifth). However, it is, after New Jersey, the state where beer

consumption represents the smallest part of total alcohol consumption (79.4% in

volume and 51.6% in value)19 (Exhibit 4).

The growth of the alcoholic drinks market is closely positively correlated to the

economical performance of the USA20. The four key demand drivers are

trendsetters, personal taste, brand recognition and income. Trendy bars or clubs

as well as stars are the main trendsetters which initiated over the past years a shift

toward premium products and especially FABs and distilled spirits at the expense

of beer. Personal taste further influences both the type of alcohol (i.e. beer, spirit or

wine) and the brand choice. Also, product differentiation and advertising play a

major role as alcohol and in particular beer is no longer considered as a

commodity. This fact is illustrated by the tremendous advertising budget of all

major alcohol selling companies. Finally, income must be taken into consideration

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

6

as the price gap between premium and low-end products grows (Exhibit 5).

iii. Microenvironmental Analysis

Analyzing the micro-environmental influences as researched by Michael E. Porter shall support the

assessment of the US alcohol industry’s attractiveness. The crucial forces are bargaining power of

buyers, competition from substitutes, and rivalry between established players (Exhibit 6).

Industry rivalry and competition (high)

Supplier power (low) Buyer power (middle)

The significant buyer power combined with the high number of substitutes lead to

an aggressive internal rivalry among established players. As the beer industry

offers a relatively homogenous high volume product, the competitive focus lies first

and foremost on marketing, though R&D is very important. The U.S. alcoholic

drinks (and especially beer) industry is an oligopoly with three major players. In

2004, Anheuser-Busch (A-B), SAB Miller and Coors shared 68% of the market

(79% of beer only). However, A-B is the one dominating firm (43% total, 52% beer)

(Exhibit 7). These strong market positions are the result of many mergers and

acquisitions, through which traditional breweries acquired a significant stake in the

growing distilled spirits market. Another tendency is the joint product development.

For instance, A-B entered a partnership with Bacardi in 2002 to launch Bacardi

Silver, a “malternative” to beer combining malt, rum and diverse flavors (e.g. apple,

strawberry etc). In most cases, foreign alcoholic drinks producers who wish to

enter the US market have done so through licensing agreements or joint ventures

with a domestic manufacturer who is already established in the market21.

The supplier power in this industry is very low because of the large number of

suppliers. Thus, changing a supplier is relatively easy and triggers relatively low

costs. Quality consistency is quite easy to manage as purchased goods are raw

materials that most suppliers extract from the same sources. No stronger

backward integration, which would raise supplier power, is to be expected.

Most commonly alcohol distribution is organized as a three-tier system22. The

immediate buyers of an alcoholic drinks producing firm are usually wholesaler or

distribution chains. These are in charge of selling the products to retailers (e.g.

liquor shops, groceries) and to pubs, bars, and clubs. These finally sell them to the

final consumer. Some distribution chains like supermarkets sell directly to the end-

consumer (two-tier system) but represent a small part of sales in the USA. Due to

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

7

Threat of entry (low) Threat of substitutes (high)

the alcohol market structure (three major players), the wholesaler and distributor

power is limited. Of course, the market is driven by consumer demand. The

consumer does not have any transition costs when switching the product/brand,

and there is a huge variety of substitute products. However, “brand switching” is

limited by the very high brand loyalty in the U.S. alcoholic drinks market. In

addition, switching brands does not mean switching the company, as the three

major players hold about 60% of all existing brands, hence a reduced buyer power.

High capital requirements (infrastructure, advertising expense) lead to the

necessity of economies of scale, which can only be achieved by mass production

and consolidated sales on a global scale. High brand recognition, customer loyalty,

and the existing alliances between the major market players are also significant

barriers to entry. Small successful firms are often subject to acquisition. Thus, the

entry of new competitors is highly improbable.

In contrast, existing players regularly launch new products on the market. Alone A-

B is launching up to three new beer products a year. This results in a highly

competitive market and also strong product cannibalization (e.g. between

Budweiser and BudLight). As many alcoholic drinks actually address the same

target groups and basically accomplish the same role (e.g. party drinks), they are

all, to some extent, substitutes for one another. This has been shown in the last

few years by the increasing wine and spirit consumption resulting in relatively

lower beer consumption. Also, FABs are more and more appreciated substitutes

for beer, especially among young people (21-30).

b. Fischer (Heineken) company profile23 The Fischer Brewery in brief

Fischer was founded in Strasbourg (France) in 1821 and has ever since been

one of the most innovative and creative European beer breweries. Fischer also

stands for the quality of its beer: it is the only French brewery that integrates the

full production process in-house, for which it was given all the main ISO quality

labels since 1997. To ensure irreproachable quality worldwide, Fischer produces

all its beers in one site and then exports about 21% of its production. Indeed, the

brewing process requires high expertise and newest technologies, which the

company does not want to diffuse outside its Alsatian stronghold. In 2005, the

company counted 335 employees and had revenues of 210 million euros.

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

8

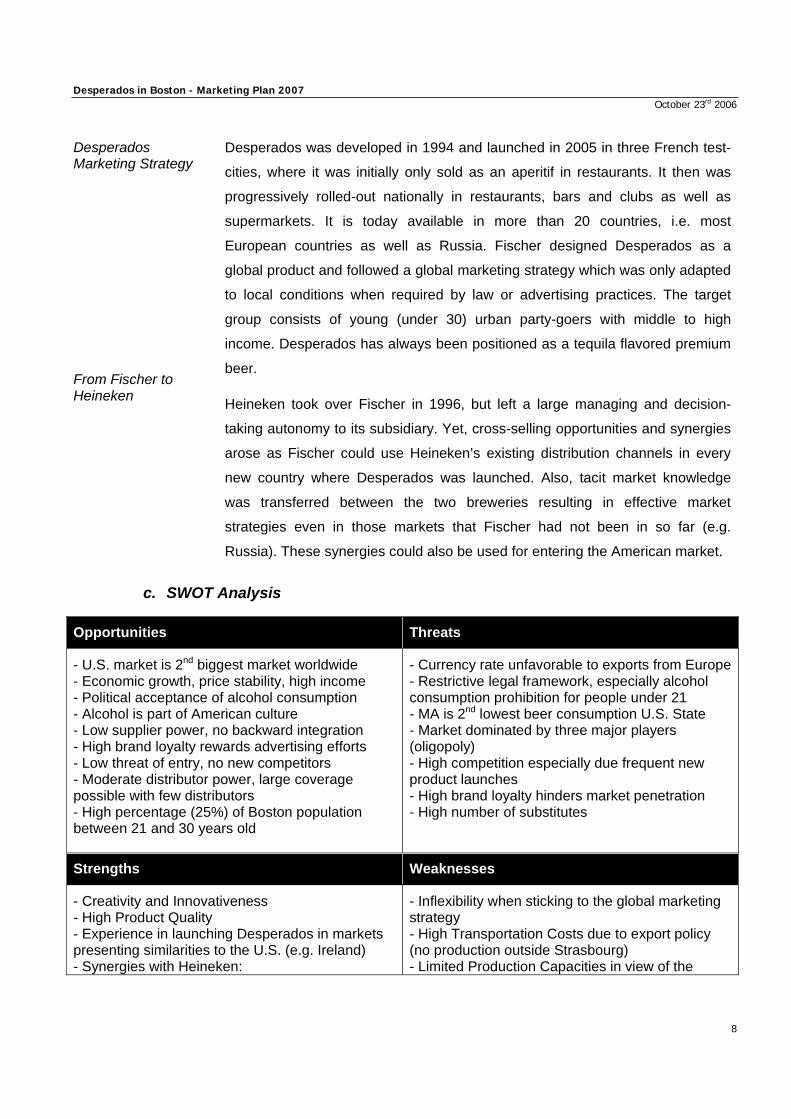

Desperados Marketing Strategy From Fischer to Heineken

Desperados was developed in 1994 and launched in 2005 in three French test-

cities, where it was initially only sold as an aperitif in restaurants. It then was

progressively rolled-out nationally in restaurants, bars and clubs as well as

supermarkets. It is today available in more than 20 countries, i.e. most

European countries as well as Russia. Fischer designed Desperados as a

global product and followed a global marketing strategy which was only adapted

to local conditions when required by law or advertising practices. The target

group consists of young (under 30) urban party-goers with middle to high

income. Desperados has always been positioned as a tequila flavored premium

beer.

Heineken took over Fischer in 1996, but left a large managing and decision-

taking autonomy to its subsidiary. Yet, cross-selling opportunities and synergies

arose as Fischer could use Heineken’s existing distribution channels in every

new country where Desperados was launched. Also, tacit market knowledge

was transferred between the two breweries resulting in effective market

strategies even in those markets that Fischer had not been in so far (e.g.

Russia). These synergies could also be used for entering the American market.

c. SWOT Analysis

Opportunities

Threats

- U.S. market is 2nd biggest market worldwide - Economic growth, price stability, high income - Political acceptance of alcohol consumption - Alcohol is part of American culture - Low supplier power, no backward integration - High brand loyalty rewards advertising efforts - Low threat of entry, no new competitors - Moderate distributor power, large coverage possible with few distributors - High percentage (25%) of Boston population between 21 and 30 years old

- Currency rate unfavorable to exports from Europe- Restrictive legal framework, especially alcohol consumption prohibition for people under 21 - MA is 2nd lowest beer consumption U.S. State - Market dominated by three major players (oligopoly) - High competition especially due frequent new product launches - High brand loyalty hinders market penetration - High number of substitutes

Strengths

Weaknesses

- Creativity and Innovativeness - High Product Quality - Experience in launching Desperados in markets presenting similarities to the U.S. (e.g. Ireland) - Synergies with Heineken:

- Inflexibility when sticking to the global marketing strategy - High Transportation Costs due to export policy (no production outside Strasbourg) - Limited Production Capacities in view of the

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

9

+ Existent Distribution Network + Good Market Knowledge

American market size

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

10

2. Strategic Goals and Objectives Long-term vision

Objectives for 2007

Fischer’s Desperados operation in the USA is expected to reach the break even

in 2010. By 2015, Desperados will be available for purchase in all U.S. cities

counting more than 500,000 inhabitants. Sales market value (end consumer

price x volume) is forecast at $11.4 million (Exhibit 8), which would bring

Desperados in the top 15 of best selling beer brands and make it the best selling

specialty beer in the U.S. market. Fischer’s U.S. revenues from Desperados are

expected to attain $3.6 million in 2015 with a profit before tax of about $434,000.

Fischer’s central objective regarding its Desperados launch in Boston is to reach

its market sales goal of $182.000 in 2007 (which should bring Fischer revenues

of about $58.000) without extending the market entry budget too far over

forecast ($465,000) (Exhibit 9). On average (over the year), half of the target

group is forecast to know the brand. One third of those is further expected to

buy the product and 40% of the first trial buyers to buy Desperados repeatedly.

Desperados will have the image of a wild party beer in peoples’ minds.

3. Strategic Options

a. Mode of Entry and Marketing Strategy Mode of entry and Expansion Global Marketing Strategy

In accordance with Fischer’s production and quality control strategy,

Desperados will be produced in Strasbourg and exported to the U.S. To reduce

transportation costs, joint shipments with Heineken export beers are to be

organized. In 2007, Desperados will be launched only in Boston city which has

been identified as a meaningful test market given the high part of the population

corresponding to the defined target group (see section 3.b.). Depending on the

encountered success, the product will be rolled-out progressively to other big

U.S. cities presenting a high demand potential (Exhibit 8).

Desperados will, to a large extent, be marketed in the U.S. following Fischer’s

global marketing strategy which already proved to be successful in markets

where consumers have similar alcohol preferences and consumption behaviours

(Ireland and the United-Kingdom). Yet, adaptations will be made that take into

account the specific U.S. alcohol market structure, competition and legislation.

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

11

b. Segmentation and Target Group Strategic Product Segmentation

Target Group

The U.S. alcohol market consists of three main product segments: spirits, wine

and BFC (Section 1.a.ii.). The BFC segment is split into beer, FABs, and cider.

The beer segment can again be broken down into premium lager, specialty

beers, standard lager, and stouts and ales (Exhibit 3). Desperados being a

tequila flavored beer, it potentially competes both against flavored beers on the

specialty beer segment and malternatives on the FAB segment. As a result of

the competitive strategy (Section 3.c.), Desperados will be positioned as a

specialty beer (segment value of $18.2 billion in 2004). Yet, it will also closely

compete with malternatives and indirectly against other beers (mostly lager).

Given the mixture (beer + tequila), the alcohol content (5.9%) and the openness

of partygoers to try innovative alcoholic creations, Desperados will be targeted

at partygoers in the U.S. The focus will lie on people between 21 (minimum legal

age) and 30, as the interest of over 30 year old Americans for beer mixtures has

shown to be limited (Exhibit 12) and a strong brand loyalty is already

established. Thus, targets are primarily students and young professionals

concentrating in major U.S. cities, which will allow economies of scale in

distribution. In accordance with the global premium strategy, Desperados is

designed for upper-middle class citizens. To avoid the loss of potential

customers, no restriction will be made concerning the gender or ethnic group.

To sum up, the target group are 21-30 years old upper-middle class urban

partygoers.

c. Positioning and Competitive Strategy Product Identification & Differentiation

Positioning and Competitive Strategy

Desperados is first and foremost a lager beer which differentiates by an

additional wild tequila flavor, a high alcohol content (5.9% compared 4.5% or

less for a standard beer) and a unique “cool” bottle design. Unlike malternatives,

the authentic taste of beer remains a key characteristic of Desperados, which

makes it a high quality specialty beer rather than a flavored alcoholic beverage.

The differentiation criteria lead to the definition of the strategic positioning

relative to Desperados’ closest premium competitors (brands). Desperados will

be positioned as a premium flavored beer for wild and trendy partygoers. The

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

12

positioning is visualized on more details in Exhibit 10.

4. Operative Market Entry Strategy for 2007

a. Global Product Global Strategy

Branding

Product Range

Packaging, Use and

Place

Desperados is a global product which is not being altered to suit local market

tastes. In turn, markets are selected for their potential tequila flavored beer

advocates. According to our survey (Exhibit 13), 37% of 21-30 years old

Bostonians were highly or very highly interested in buying tequila flavored beer.

Desperados is an international brand name which makes people think of

“Mexico” and “wildness” in every country, and also in the USA (Exhibit 13). This

name is a good brand recognition facilitator as it reflects both the product

identification and differentiation (“Mexican tequila” flavored beer) and the target

group (it appeals to “wild” partygoers).

Desperados will be available for purchase in the main package sizes that

already exist in the European market, i.e. in classic small 12oz (0.33l) bottles, in

large 22oz (0,65l) bottles and as well 169oz (5l) kegs. Because of the

differences of products and positioning, there will be no internal cannibalization

between Desperados products and other Heineken beers in the U.S. market.

The classic 12oz longneck bottle of Desperados has the perfect size for both

private parties and bars and clubs. Experience in the home markets France and

Germany has shown that this mythic Desperados bottle is the ultimate

trendsetter product. For house parties, Desperados will be also available in

supermarkets and liquor stores in six-packs or 24-boxes of 12oz bottles, which

are easy to carry and store. The unique XL keg provides freshness and an air of

exclusivity. They are ideal for private parties only, i.e. Desperados will not be for

sale from the keg in bars and pubs to preserve the premium image (Exhibit 14).

b. Premium Pricing Premium Strategy

In accordance with the high quality/high price (premium) positioning (Exhibit 10), retail prices will be aligned with the premium competitors both on the

specialty beer and the FAB segment (i.e. Tequiza, Smirnoff Ice and Bacardi

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

13

Strict Control over Retail Prices Average Retail Price

Fischer Selling Price Policy

Tax, Deposit and Currency issues

Silver). Desperados will thus compete on the value added of the product rather

than directly on price, which is a key characteristic of the global pricing strategy.

In order to have an effective control over consumer prices, Fischer will negotiate

with each retailer a contract that will install a yearly fix retail price equal to the

competing products’ price at the retail place. This price should not be out of a

10% range around the average target price (Exhibit Z). In the case of three tier

distribution (Section 4.c.), the intermediary wholesaler will hold the

responsibility of negotiating a contract with the end-retailer following the same

conditions.

Considering the average prices of the basket of brands identified as

Desperados’ closest competitors (see above), the average retail price for the

standard 12oz bottle will be $3.75 ($11.25 a liter) in pubs, bars and clubs (PBC)

and $1.30 ($3.90 a liter) in supermarkets, convenience and liquor stores

(Exhibit Z).

Fischer will have to negotiate appropriate selling prices to intermediate

distributors in accordance with the above defined pricing strategy, taking into

account the margins of each link of the chain. Though the selling prices change

in function of the chosen distribution channel (Section 4.c.), no incentive will be

given to retailers (in particular PBC) to short-circuit the distribution system. The

results of this calculation are summarized in Exhibit 12.

In addition to the standard sales tax of 5%, the state of MA raises a beer tax

worth $0.11 per gallon (i.e. $0.01 per 12oz bottle). Also, a 5 cent deposit is

required on each glass bottle sold. These represent additional costs for the

consumer, but as they are also applicable to competing products, the pricing

alignment strategy is not affected. In 2007 there will be no issue of currency

because revenues will be reinvested in the company (expenses higher than

revenue).

c. Established Distribution Channels Using established channels

Three tier channel

For the launch of Desperados in the USA, Fischer will use Heineken's

established distribution channels. Three channels must be distinguished

(Exhibit 16).

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

14

Two tier channels

Strict Control over Distributors

The most common distribution channel for any alcohol exporter to the U.S.

market is the three tier system involving a wholesaler which resells the product

to different types of retailers24. These retailers will be pubs, bars and clubs

(PBC-retailers) as well as liquor stores and convenience stores. Unlike

traditional Heineken beer, the party drink Desperados will not be for sale in

restaurants.

American alcoholic drinks wholesalers present the advantage of achieving a

large coverage (presence in many cities) which can be useful for the expansion

after 2007. In 2007, Heineken will add Fischer’s Desperados to the list of brands

it already distributes via Burke Distributing, one of the biggest beer wholesalers

for the Boston area25. This channel will account for approximately 60% of the

total sales volume in 2007, as it is an effective means of reaching a large

number of, especially small, retailers.

The other type of distribution channels, which in contrast is more efficient in

terms of price control (Section 4.b.) and margins, is the two tier system

consisting in direct sales to both (a) large supermarket chains (10% of sales

volume) and (b) PBC-retailers (30%). In 2007, Desperados will be included in

the contract Heineken negotiates yearly with Shaws. Also, Heineken disposes of

a competent sales team responsible for canvassing PBC customers throughout

the USA. Desperados will thus be added to the list of distributed brands.

Salespeople in charge of the Boston area will be trained on marketing the new

brand.

The key of a successful market positioning and implementation of the product

and price strategies is a good control over all links of the distribution chain. This

controls is guaranteed here by the long experience and excellent contacts that

Heineken has with its distributors.

d. Extensive Advertising and Promotion Campaigns Legal Constraints Target Audience and Promise

This advertising and promotion strategy will comply with applicable regulations.

Indeed, Desperados needs not to be associated with a brand inviting people to

break laws (e.g. incite underage teenies to drink, Exhibit 17).

According to the target group, the targeted audience is all Bostonian partygoers

between 21 and 30 with middle-high income. The advertising promise is that

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

15

Advertising Channels 12-months Plan Highlights Budget Planning

Desperados is a premium Tequila flavored that consumers will enjoy when

going on wild parties with their friends.

Desperados will use several media channels for its advertising: the radio,

specialized local magazines, outdoor and indoor billboards and the Internet.

Sponsorships with local sports events (baseball and football) are also

forecasted, as well as exclusive Desperados’ events in night clubs. These two

latter places will benefit from special billboards (Exhibit 18). In shop advertising

and promotions (including free trial and discounts) will also be designed for

liquor stores.

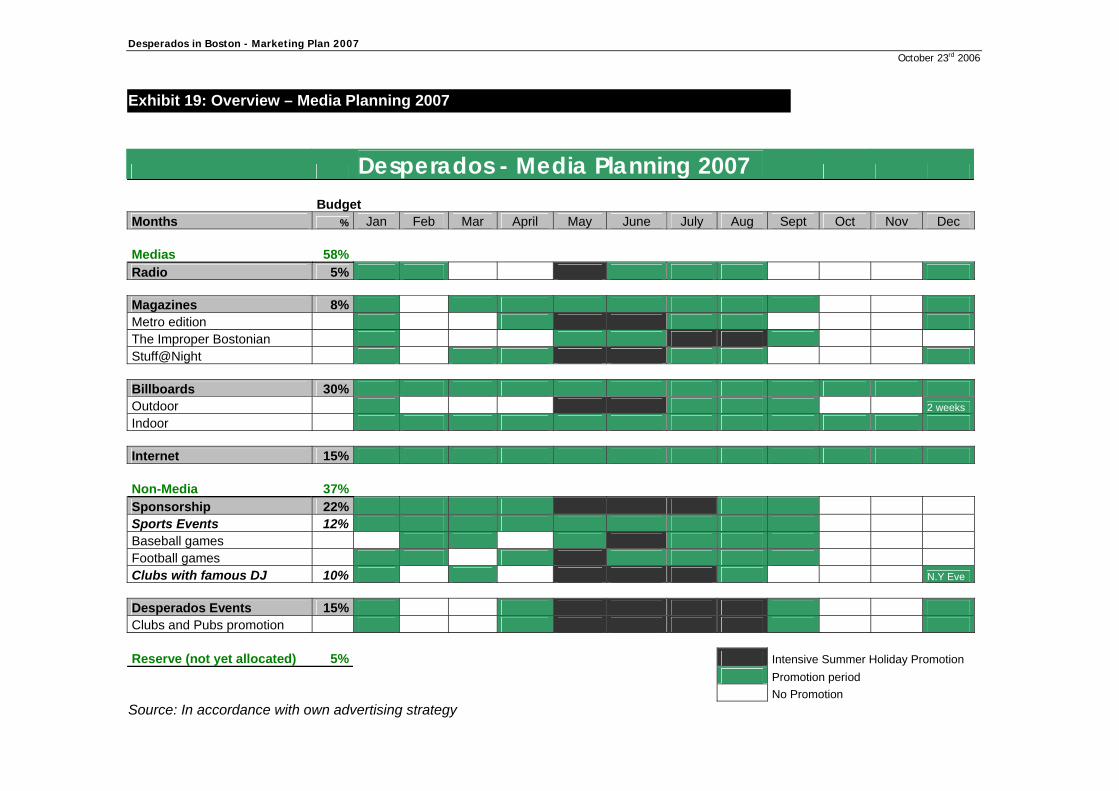

Advertising is planned from January to December 2007 (Exhibit 19). An

emphasis will be put on the first month of the launching and on the summer

months as beer consumption is higher during that period. Obviously one of the

capital aspects is to keep the coherence between all messages spread through

the different medias by always focusing on the promise.

A detailed advertising plan is given in Exhibits 18 and 19. In accordance with

the results of our survey (Exhibit 13), the main focus will lie on bill boarding and

promotion in PBCs. Happy hours (where Desperados will be sold for $2/bottle)

will also be organized to encourage first trial. As most of the target group spends

a lot of time on the Internet, a Desperados dedicated website providing both

information and animation is a must. Also, product related goodies and clothes

will be for sale online. The website will be advertised through an intensive

emailing campaign. In summer months, sports events will be the place where to

enhance brand awareness e.g. through free trials from the keg.

Heineken and Fischer will invest $425,000 for advertising/promotion in 2007.

58% (246.500 $) of the advertising budget will be allocated to media advertising

(including creation agencies fee and rent of consumer data bases) and 37%

(157.250 $) in “non-media” advertising including sponsorships and Desperados

own events in clubs or pubs. The remaining will be hold as a security provision

(5%) to enable the company to face non-forecasted additional expenses.

5. Conclusion

With a strong 46% interest for Tequila flavored beer within its target group, Desperados has the best

chances to be successfully launched in the US market, after its huge success in the Europe. Should

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

16

Fischer achieve the market sales objectives of $182,000 in the end of 2007 without exceeding its budget

of $465,000, it will begin its expansion to other major U.S. cities. Otherwise Fischer should exit the US

market in 2008 and stop selling Desperados in the USA.

With the support of its mother company Heineken, Fischer’s objective of reaching the break even point in

2010 is realistic. Heineken’s financial helping hand and established distribution power will be precious

assets to Desperados’ expansion throughout the USA. Desperados operates in a highly profitable niche

on the specialty beer market, where it can become one the top 15 best selling beer brands within a ten

year horizon.

Sources Adams Beverages Group (2005), Beer Handbook Australian Government (http://www.austrade.gov.au/australia/layout/0,,0_s2-1_CLNTXID0019-2_-3_PWB110752488-4_marketing-5_-6_-7_,00.html, 10/16/2006) Brasseries Fischer (http://www.brasseriefischer.com/brasserie-fischer.htm, 10/08/2006) Business Insights (2003), Alcoholic Drinks in the United States (Market Report) CIA World Factbook (https://www.cia.gov/cia/publications/factbook/geos/us.html#Econ, 10/14/2006) CIA World Factbook (https://www.cia.gov/cia/publications/factbook/geos/us.html#People, 10/16/2006) Datamonitor (October 2005), Alcoholic Drinks in the United States (Market Report) Datamonitor (October 2005), Beer market in the United States (Market Report) DataPlace (http://www.dataplace.org/charttable/index.html?groupBy=per, 10/14/2006) Dimensional Insights (http://www.dimins.com/News/PressReleases/2005/burke/, 10/21/2006) FreedomWorks (http://www.freedomworks.org/massachusetts/index.php, 10/15/2006) Global Insight (Q1 2006), The World Outlook (Report) Massachusetts Institute of Technology (MIT) (http://web.mit.edu/alcohol/www/laws.html, 10/12/2006) OnVista (http://waehrungen.onvista.de/, 10/14/2006) State Environmental Resource Center (http://www.serconline.org/bottlebill/stateactivity.html, 10/15/2006) State University of New York (Sociology Department), U.S. Government: Moderate drinking benefits health (http://www2.potsdam.edu/hansondj/InTheNews/MedicalReports/Longevity/1088617919.html, 10/15/2006)

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

17

Stuff @Night magazine (http://stuffatnight.com/, 10/21/2006) USA Today (11/06/2005), Alcohol makers on tricky path in marketing to college crowd (Article) U.S. Department for Health and Human Services (http://ncadi.samhsa.gov/govpubs/rpo995/, 10/16/2006)

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

18

Exhibits Exhibit 1: Population Key Facts Exhibit 2: Legal Framework in the alcoholic drinks industry in Massachusetts Exhibit 3: Segmentation of the American alcoholic drinks market (2004) Exhibit 4: Massachusetts beer consumption statistics Exhibit 5: Key demand drivers on the American alcohol market Exhibit 6: Porter’s Five Forces in the American alcoholic drinks market Exhibit 7: Competitors on the U.S. alcoholic drinks (and beer) market (2004) Exhibit 8: Demand Forecast for 2007, 2010 and 2015 Exhibit 9: Income Statements for 2007, 2010 and 2015 Exhibit 10: Positioning and Competitive Strategy Exhibit 11: Prices per category of alcoholic drink and brand Exhibit 12: Survey Questionnaire Exhibit 13: Survey – Main Results Exhibit 14: Desperados Product Range and Characteristics Exhibit 15: Premium Pricing Strategy Exhibit 16: Overview of Distribution Channels Exhibit 17: Compliance Strategy with Advertising and Promotion Regulations Exhibit 18: Detailed Advertising Strategy Exhibit 19: Overview – Media Planning 2007

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

19

U.S. Population by Religion (2004)

0 10 20 30 40 50 60

Protestant

Catholic

Mormon

Muslim

Jew ish

Other

None

U.S. Population by Ethnic Origin (2004)

0 10 20 30 40 50 60 70 80

White

Hispanic

Black

Asian

Others

(%)

Boston Population by Age Class (2000)

0

20

40

60

80

100

120

140

Und

er 5

5 - 8

9 - 1

4

15 -

19

20 -

24

25 -

34

35 -

44

45 -

54

55 -

59

60 -

64

65 -

74

75 -

84

Ove

r 85

Exhibit 1: Population Key Facts

Source: U.S. Census Bu-reau (2000)

Source: CIA Worldfactbook Source: CIA Worldfactbook

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

20

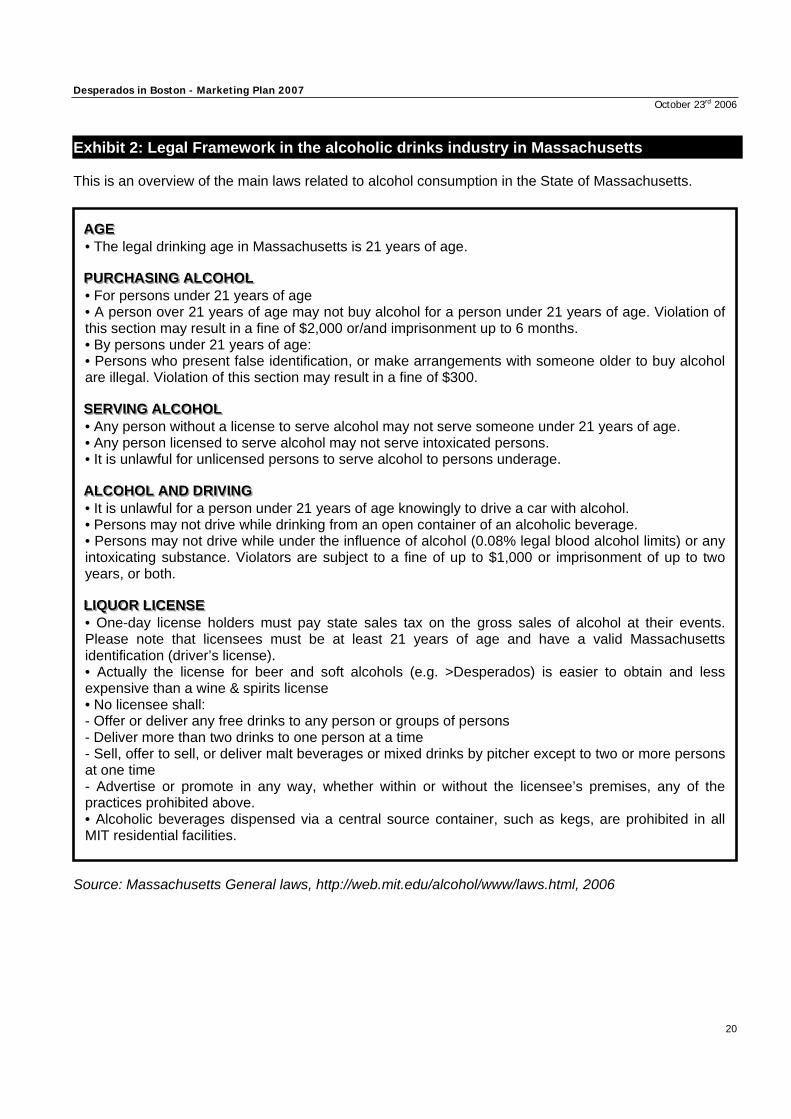

Exhibit 2: Legal Framework in the alcoholic drinks industry in Massachusetts This is an overview of the main laws related to alcohol consumption in the State of Massachusetts.

AAAGGGEEE • The legal drinking age in Massachusetts is 21 years of age. PPPUUURRRCCCHHHAAASSSIIINNNGGG AAALLLCCCOOOHHHOOOLLL • For persons under 21 years of age • A person over 21 years of age may not buy alcohol for a person under 21 years of age. Violation of this section may result in a fine of $2,000 or/and imprisonment up to 6 months. • By persons under 21 years of age: • Persons who present false identification, or make arrangements with someone older to buy alcohol are illegal. Violation of this section may result in a fine of $300. SSSEEERRRVVVIIINNNGGG AAALLLCCCOOOHHHOOOLLL • Any person without a license to serve alcohol may not serve someone under 21 years of age. • Any person licensed to serve alcohol may not serve intoxicated persons. • It is unlawful for unlicensed persons to serve alcohol to persons underage. AAALLLCCCOOOHHHOOOLLL AAANNNDDD DDDRRRIIIVVVIIINNNGGG • It is unlawful for a person under 21 years of age knowingly to drive a car with alcohol. • Persons may not drive while drinking from an open container of an alcoholic beverage. • Persons may not drive while under the influence of alcohol (0.08% legal blood alcohol limits) or any intoxicating substance. Violators are subject to a fine of up to $1,000 or imprisonment of up to two years, or both. LLLIIIQQQUUUOOORRR LLLIIICCCEEENNNSSSEEE • One-day license holders must pay state sales tax on the gross sales of alcohol at their events. Please note that licensees must be at least 21 years of age and have a valid Massachusetts identification (driver’s license). • Actually the license for beer and soft alcohols (e.g. >Desperados) is easier to obtain and less expensive than a wine & spirits license • No licensee shall: - Offer or deliver any free drinks to any person or groups of persons - Deliver more than two drinks to one person at a time - Sell, offer to sell, or deliver malt beverages or mixed drinks by pitcher except to two or more persons at one time - Advertise or promote in any way, whether within or without the licensee’s premises, any of the practices prohibited above. • Alcoholic beverages dispensed via a central source container, such as kegs, are prohibited in all MIT residential facilities.

Source: Massachusetts General laws, http://web.mit.edu/alcohol/www/laws.html, 2006

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

21

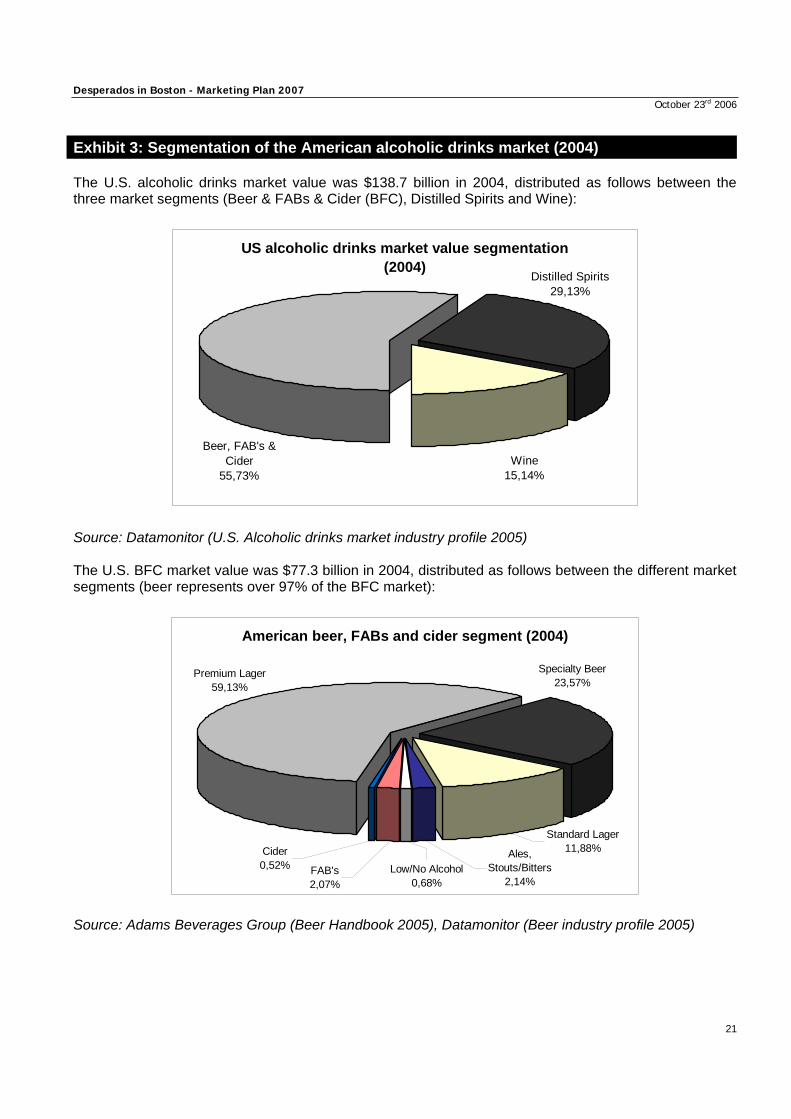

Exhibit 3: Segmentation of the American alcoholic drinks market (2004) The U.S. alcoholic drinks market value was $138.7 billion in 2004, distributed as follows between the three market segments (Beer & FABs & Cider (BFC), Distilled Spirits and Wine):

US alcoholic drinks market value segmentation (2004)

Beer, FAB's & Cider

55,73%

Distilled Spirits29,13%

Wine15,14%

Source: Datamonitor (U.S. Alcoholic drinks market industry profile 2005) The U.S. BFC market value was $77.3 billion in 2004, distributed as follows between the different market segments (beer represents over 97% of the BFC market):

American beer, FABs and cider segment (2004)

Low/No Alcohol0,68%

Ales, Stouts/Bitters

2,14%

Specialty Beer23,57%

Premium Lager59,13%

Standard Lager11,88%

FAB's2,07%

Cider0,52%

Source: Adams Beverages Group (Beer Handbook 2005), Datamonitor (Beer industry profile 2005)

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

22

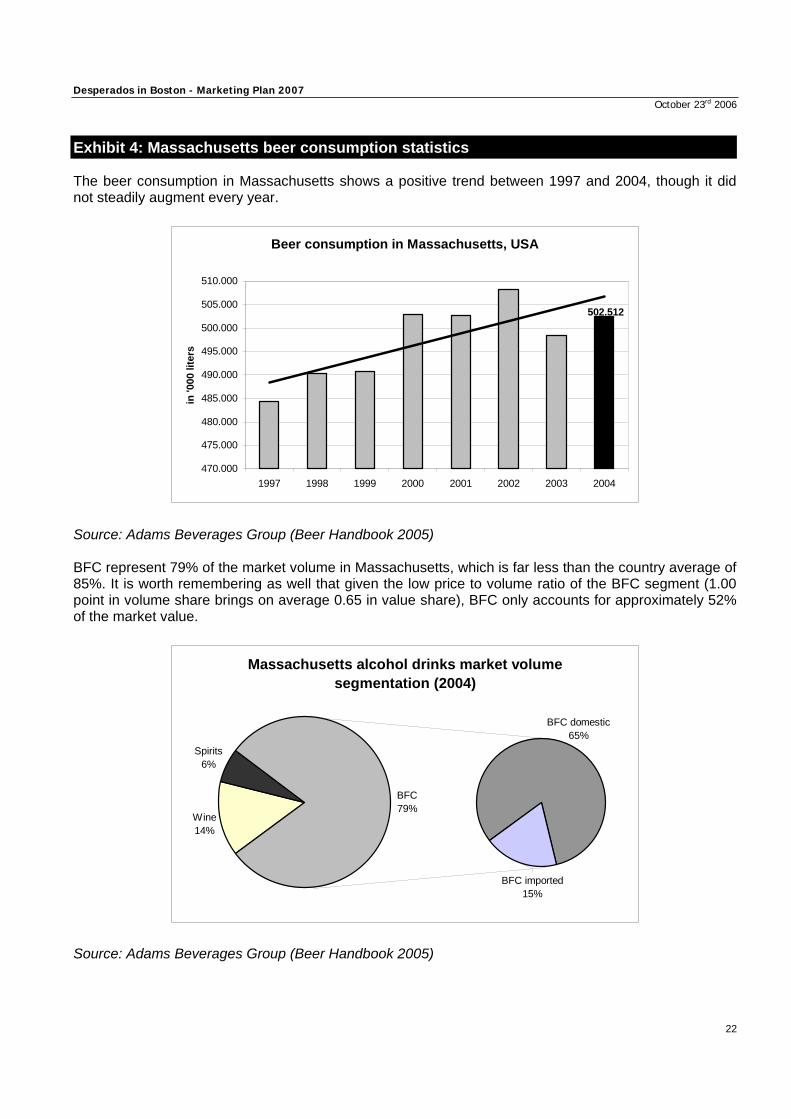

Exhibit 4: Massachusetts beer consumption statistics The beer consumption in Massachusetts shows a positive trend between 1997 and 2004, though it did not steadily augment every year.

Beer consumption in Massachusetts, USA

502.512

470.000

475.000

480.000

485.000

490.000

495.000

500.000

505.000

510.000

1997 1998 1999 2000 2001 2002 2003 2004

in '0

00 li

ters

Source: Adams Beverages Group (Beer Handbook 2005) BFC represent 79% of the market volume in Massachusetts, which is far less than the country average of 85%. It is worth remembering as well that given the low price to volume ratio of the BFC segment (1.00 point in volume share brings on average 0.65 in value share), BFC only accounts for approximately 52% of the market value.

Massachusetts alcohol drinks market volume segmentation (2004)

Wine14%

Spirits6%

BFC imported15%

BFC79%

BFC domestic65%

Source: Adams Beverages Group (Beer Handbook 2005)

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

23

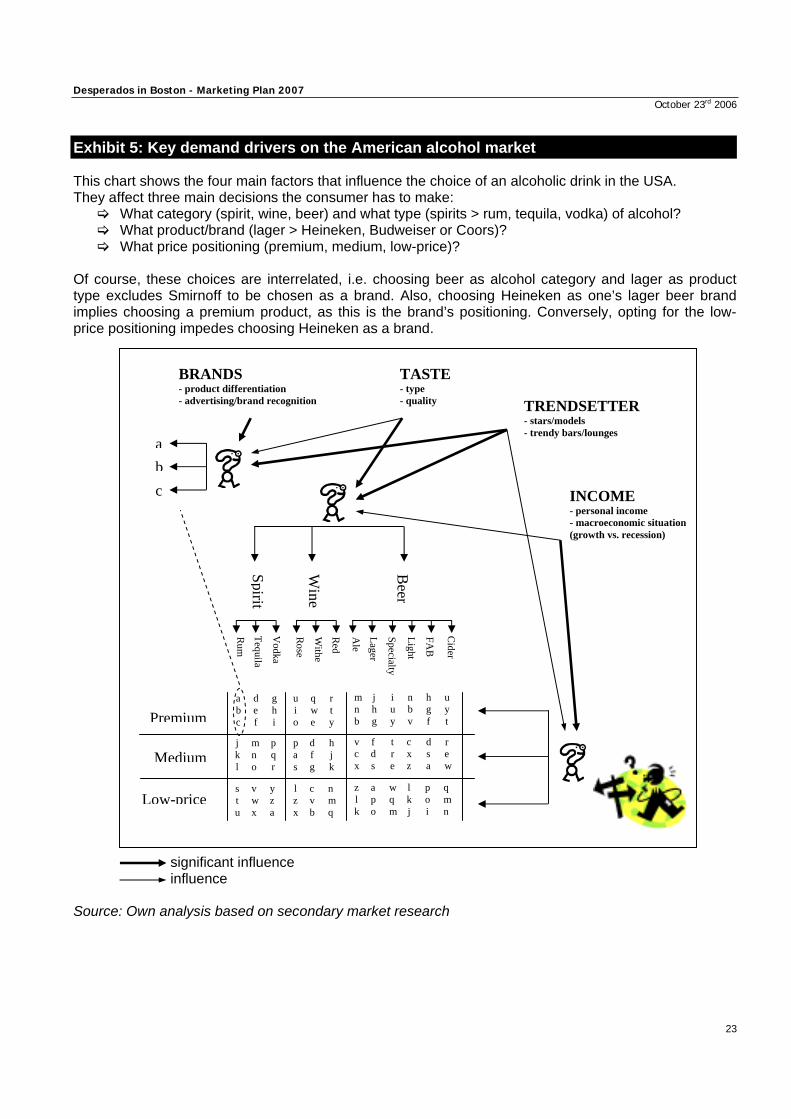

Exhibit 5: Key demand drivers on the American alcohol market This chart shows the four main factors that influence the choice of an alcoholic drink in the USA. They affect three main decisions the consumer has to make:

What category (spirit, wine, beer) and what type (spirits > rum, tequila, vodka) of alcohol? What product/brand (lager > Heineken, Budweiser or Coors)? What price positioning (premium, medium, low-price)?

Of course, these choices are interrelated, i.e. choosing beer as alcohol category and lager as product type excludes Smirnoff to be chosen as a brand. Also, choosing Heineken as one’s lager beer brand implies choosing a premium product, as this is the brand’s positioning. Conversely, opting for the low-price positioning impedes choosing Heineken as a brand. significant influence influence Source: Own analysis based on secondary market research

Spirit

Wine

Beer

Premium

Medium

Low-price

TRENDSETTER - stars/models - trendy bars/lounges

abc

BRANDS - product differentiation - advertising/brand recognition

INCOME - personal income - macroeconomic situation (growth vs. recession)

TASTE - type - quality

Specialty

Lager

Ale

Red

Withe

Rose

FAB

Cider

Rum

Tequila

Vodka

uio

qwe

rty

pas

lzx

dfg

hjk

cvb

nmq

jkl

stu

mno

pqr

vwx

yza

abc

def

ghi

mnb

jhg

iuy

vcx

zlk

fds

tre

apo

wqm

Light

nbv

hgf

cxz

dsa

lkj

poi

uyt

rew

qmn

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

24

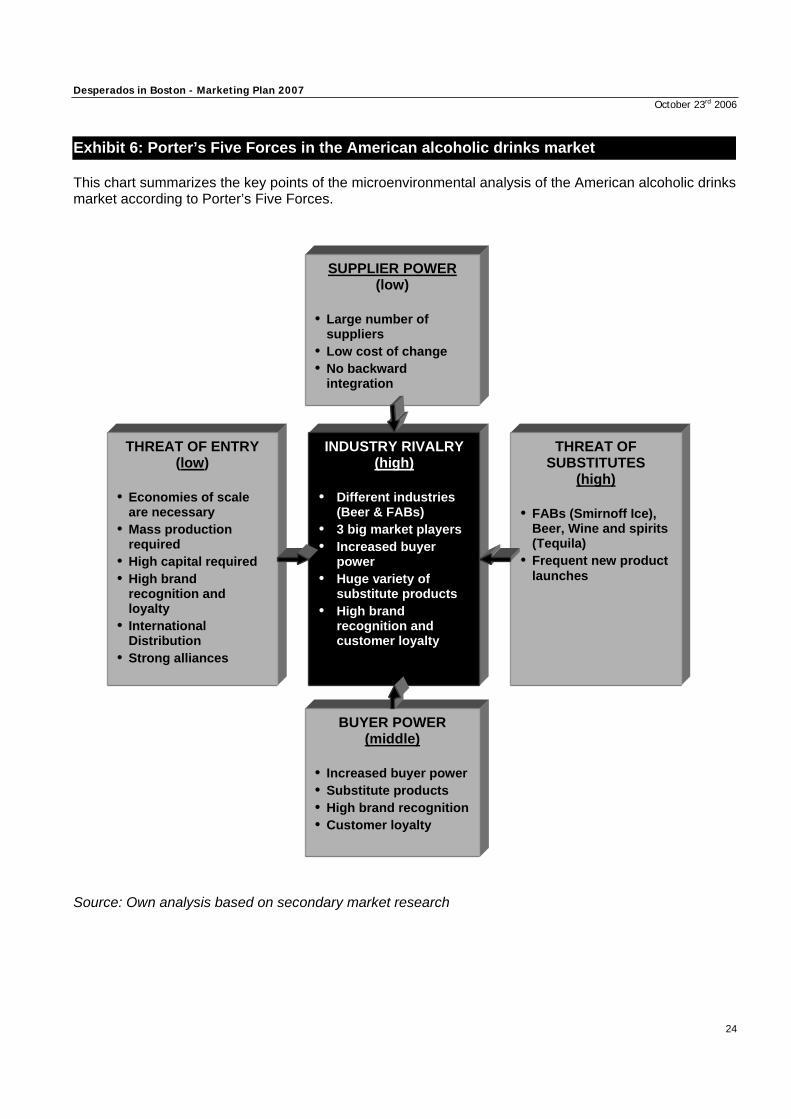

Exhibit 6: Porter’s Five Forces in the American alcoholic drinks market This chart summarizes the key points of the microenvironmental analysis of the American alcoholic drinks market according to Porter’s Five Forces. Source: Own analysis based on secondary market research

THREAT OF ENTRY (low)

• Economies of scale

are necessary • Mass production

required • High capital required • High brand

recognition and loyalty

• International Distribution

• Strong alliances

THREAT OF SUBSTITUTES

(high)

• FABs (Smirnoff Ice), Beer, Wine and spirits (Tequila)

• Frequent new product launches

SUPPLIER POWER (low)

• Large number of

suppliers • Low cost of change • No backward

integration

BUYER POWER (middle)

• Increased buyer power • Substitute products • High brand recognition • Customer loyalty

INDUSTRY RIVALRY (high)

• Different industries

(Beer & FABs) • 3 big market players • Increased buyer

power • Huge variety of

substitute products • High brand

recognition and customer loyalty

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

25

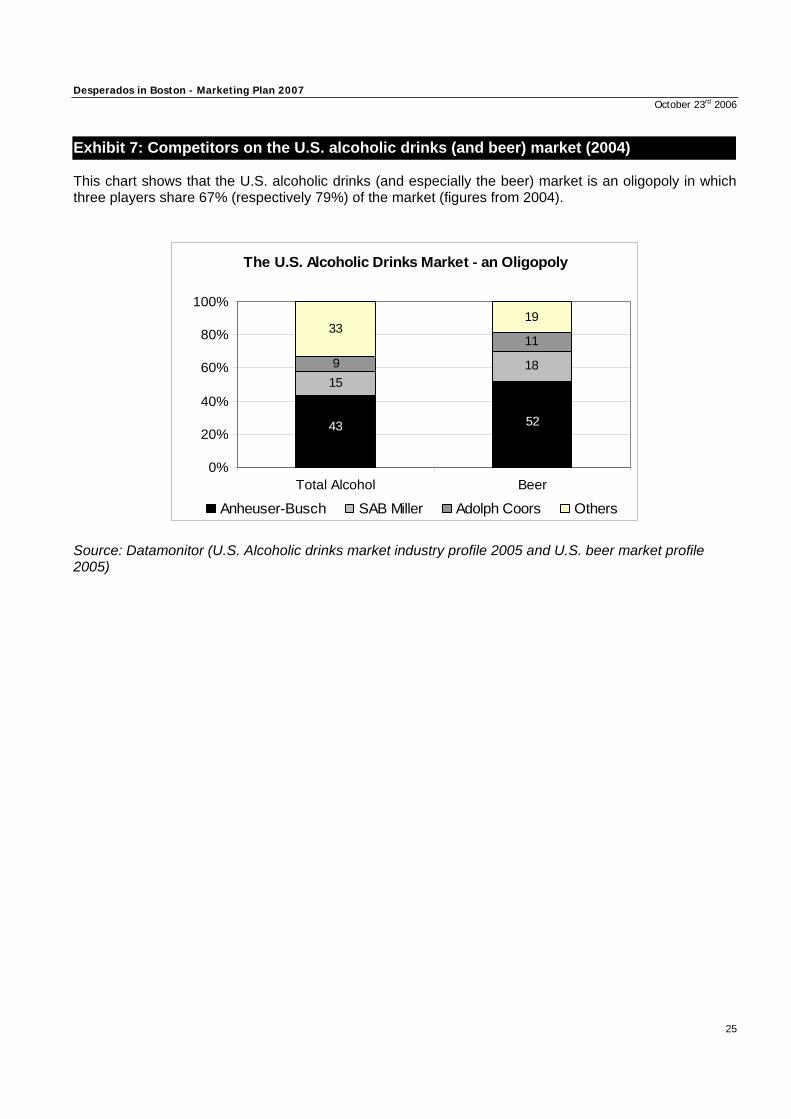

Exhibit 7: Competitors on the U.S. alcoholic drinks (and beer) market (2004) This chart shows that the U.S. alcoholic drinks (and especially the beer) market is an oligopoly in which three players share 67% (respectively 79%) of the market (figures from 2004).

The U.S. Alcoholic Drinks Market - an Oligopoly

15189

1133

19

43 52

0%

20%

40%

60%

80%

100%

Total Alcohol Beer

Anheuser-Busch SAB Miller Adolph Coors Others

Source: Datamonitor (U.S. Alcoholic drinks market industry profile 2005 and U.S. beer market profile 2005)

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

26

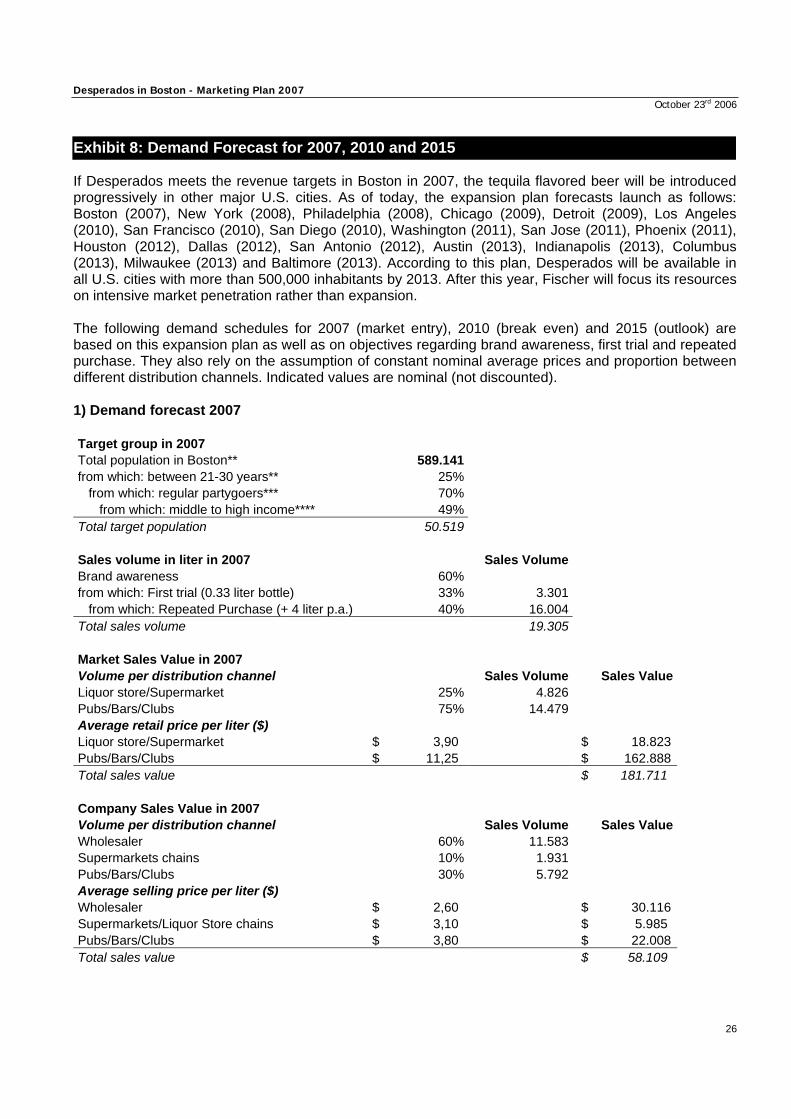

Exhibit 8: Demand Forecast for 2007, 2010 and 2015 If Desperados meets the revenue targets in Boston in 2007, the tequila flavored beer will be introduced progressively in other major U.S. cities. As of today, the expansion plan forecasts launch as follows: Boston (2007), New York (2008), Philadelphia (2008), Chicago (2009), Detroit (2009), Los Angeles (2010), San Francisco (2010), San Diego (2010), Washington (2011), San Jose (2011), Phoenix (2011), Houston (2012), Dallas (2012), San Antonio (2012), Austin (2013), Indianapolis (2013), Columbus (2013), Milwaukee (2013) and Baltimore (2013). According to this plan, Desperados will be available in all U.S. cities with more than 500,000 inhabitants by 2013. After this year, Fischer will focus its resources on intensive market penetration rather than expansion. The following demand schedules for 2007 (market entry), 2010 (break even) and 2015 (outlook) are based on this expansion plan as well as on objectives regarding brand awareness, first trial and repeated purchase. They also rely on the assumption of constant nominal average prices and proportion between different distribution channels. Indicated values are nominal (not discounted). 1) Demand forecast 2007 Target group in 2007 Total population in Boston** 589.141 from which: between 21-30 years** 25% from which: regular partygoers*** 70% from which: middle to high income**** 49% Total target population 50.519 Sales volume in liter in 2007 Sales Volume Brand awareness 60% from which: First trial (0.33 liter bottle) 33% 3.301 from which: Repeated Purchase (+ 4 liter p.a.) 40% 16.004 Total sales volume 19.305 Market Sales Value in 2007 Volume per distribution channel Sales Volume Sales ValueLiquor store/Supermarket 25% 4.826 Pubs/Bars/Clubs 75% 14.479 Average retail price per liter ($) Liquor store/Supermarket $ 3,90 $ 18.823 Pubs/Bars/Clubs $ 11,25 $ 162.888 Total sales value $ 181.711 Company Sales Value in 2007 Volume per distribution channel Sales Volume Sales ValueWholesaler 60% 11.583 Supermarkets chains 10% 1.931 Pubs/Bars/Clubs 30% 5.792 Average selling price per liter ($) Wholesaler $ 2,60 $ 30.116 Supermarkets/Liquor Store chains $ 3,10 $ 5.985 Pubs/Bars/Clubs $ 3,80 $ 22.008 Total sales value $ 58.109

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

27

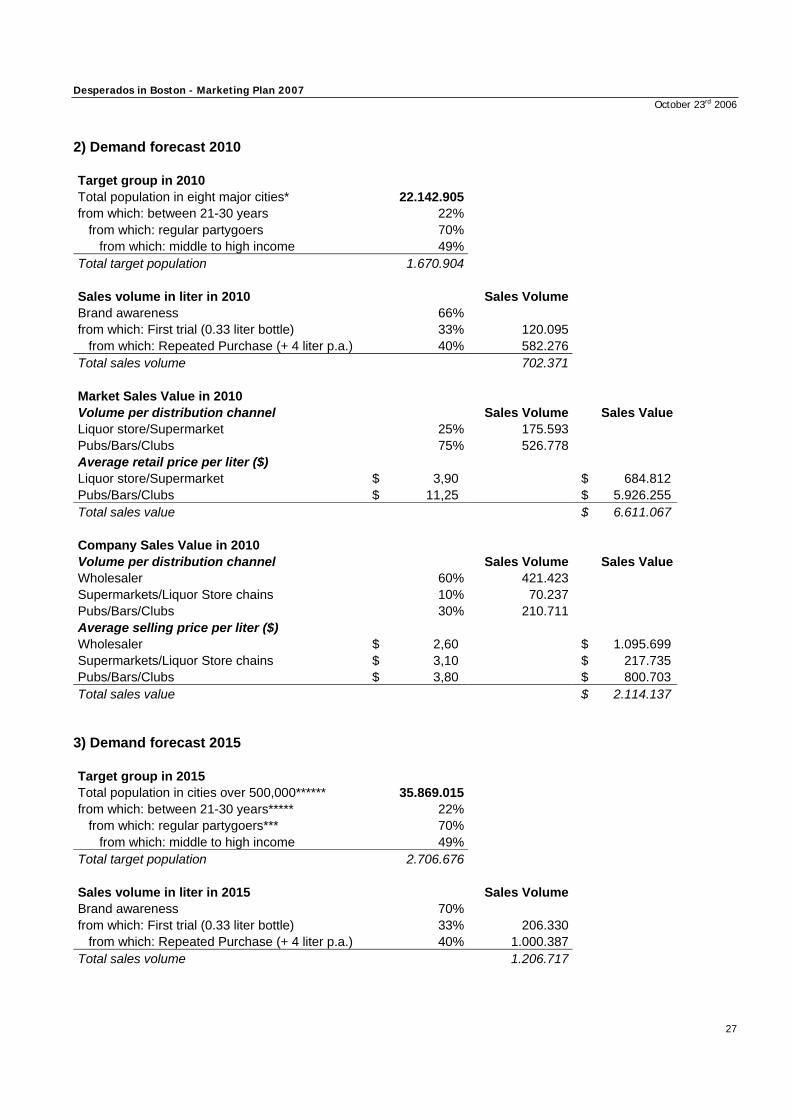

2) Demand forecast 2010 Target group in 2010 Total population in eight major cities* 22.142.905 from which: between 21-30 years 22% from which: regular partygoers 70% from which: middle to high income 49% Total target population 1.670.904 Sales volume in liter in 2010 Sales Volume Brand awareness 66% from which: First trial (0.33 liter bottle) 33% 120.095 from which: Repeated Purchase (+ 4 liter p.a.) 40% 582.276 Total sales volume 702.371 Market Sales Value in 2010 Volume per distribution channel Sales Volume Sales ValueLiquor store/Supermarket 25% 175.593 Pubs/Bars/Clubs 75% 526.778 Average retail price per liter ($) Liquor store/Supermarket $ 3,90 $ 684.812 Pubs/Bars/Clubs $ 11,25 $ 5.926.255 Total sales value $ 6.611.067 Company Sales Value in 2010 Volume per distribution channel Sales Volume Sales ValueWholesaler 60% 421.423 Supermarkets/Liquor Store chains 10% 70.237 Pubs/Bars/Clubs 30% 210.711 Average selling price per liter ($) Wholesaler $ 2,60 $ 1.095.699 Supermarkets/Liquor Store chains $ 3,10 $ 217.735 Pubs/Bars/Clubs $ 3,80 $ 800.703 Total sales value $ 2.114.137

3) Demand forecast 2015 Target group in 2015 Total population in cities over 500,000****** 35.869.015 from which: between 21-30 years***** 22% from which: regular partygoers*** 70% from which: middle to high income 49% Total target population 2.706.676 Sales volume in liter in 2015 Sales Volume Brand awareness 70% from which: First trial (0.33 liter bottle) 33% 206.330 from which: Repeated Purchase (+ 4 liter p.a.) 40% 1.000.387 Total sales volume 1.206.717

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

28

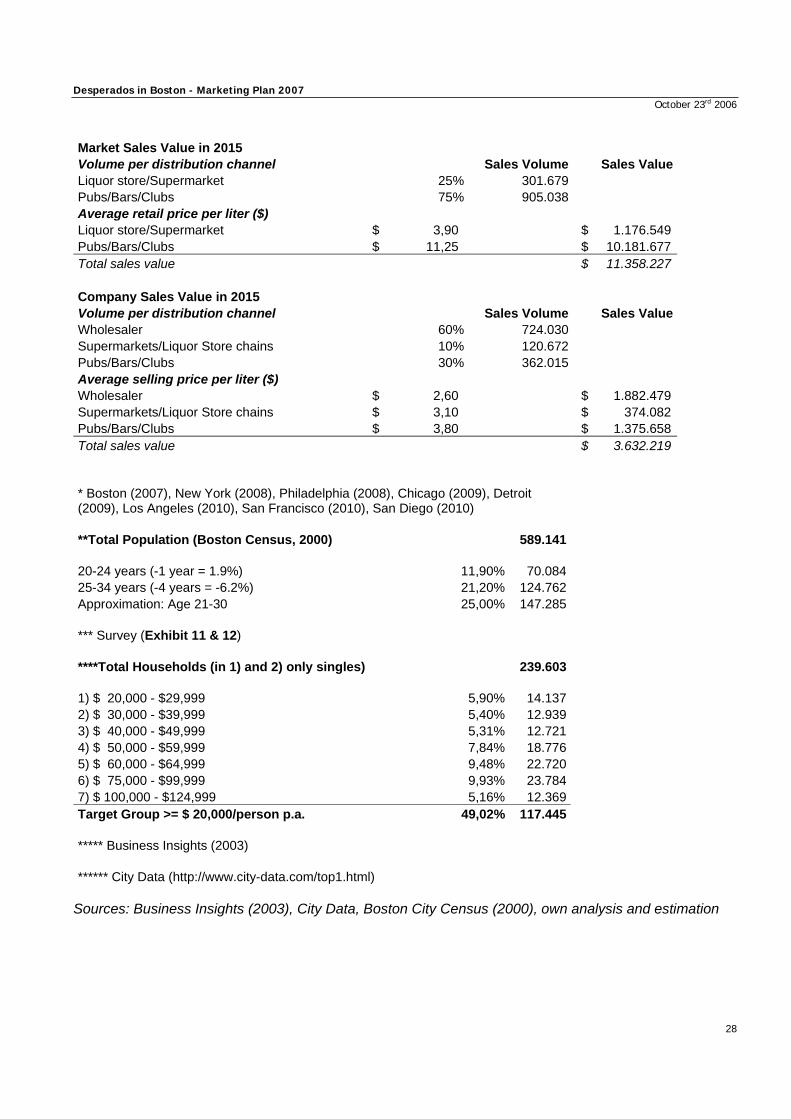

Market Sales Value in 2015 Volume per distribution channel Sales Volume Sales ValueLiquor store/Supermarket 25% 301.679 Pubs/Bars/Clubs 75% 905.038 Average retail price per liter ($) Liquor store/Supermarket $ 3,90 $ 1.176.549 Pubs/Bars/Clubs $ 11,25 $ 10.181.677 Total sales value $ 11.358.227 Company Sales Value in 2015 Volume per distribution channel Sales Volume Sales ValueWholesaler 60% 724.030 Supermarkets/Liquor Store chains 10% 120.672 Pubs/Bars/Clubs 30% 362.015 Average selling price per liter ($) Wholesaler $ 2,60 $ 1.882.479 Supermarkets/Liquor Store chains $ 3,10 $ 374.082 Pubs/Bars/Clubs $ 3,80 $ 1.375.658 Total sales value $ 3.632.219

* Boston (2007), New York (2008), Philadelphia (2008), Chicago (2009), Detroit (2009), Los Angeles (2010), San Francisco (2010), San Diego (2010) **Total Population (Boston Census, 2000) 589.141 20-24 years (-1 year = 1.9%) 11,90% 70.084 25-34 years (-4 years = -6.2%) 21,20% 124.762 Approximation: Age 21-30 25,00% 147.285 *** Survey (Exhibit 11 & 12) ****Total Households (in 1) and 2) only singles) 239.603 1) $ 20,000 - $29,999 5,90% 14.137 2) $ 30,000 - $39,999 5,40% 12.939 3) $ 40,000 - $49,999 5,31% 12.721 4) $ 50,000 - $59,999 7,84% 18.776 5) $ 60,000 - $64,999 9,48% 22.720 6) $ 75,000 - $99,999 9,93% 23.784 7) $ 100,000 - $124,999 5,16% 12.369 Target Group >= $ 20,000/person p.a. 49,02% 117.445 ***** Business Insights (2003) ****** City Data (http://www.city-data.com/top1.html)

Sources: Business Insights (2003), City Data, Boston City Census (2000), own analysis and estimation

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

29

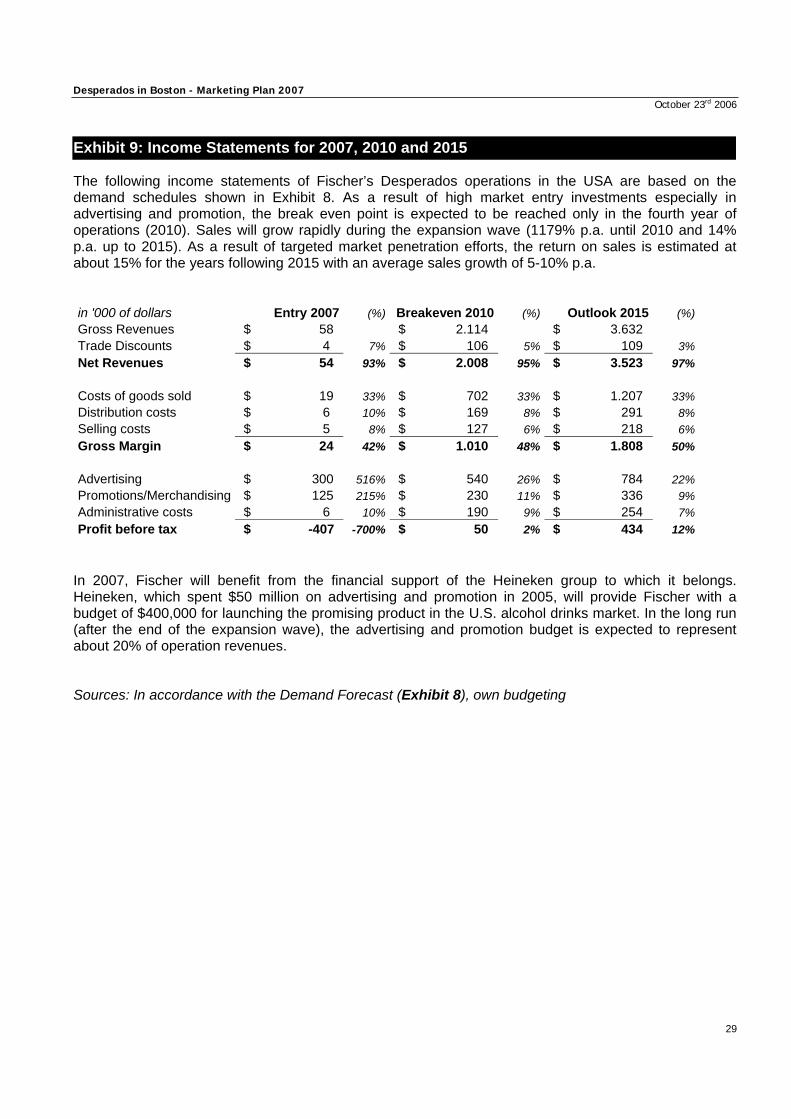

Exhibit 9: Income Statements for 2007, 2010 and 2015 The following income statements of Fischer’s Desperados operations in the USA are based on the demand schedules shown in Exhibit 8. As a result of high market entry investments especially in advertising and promotion, the break even point is expected to be reached only in the fourth year of operations (2010). Sales will grow rapidly during the expansion wave (1179% p.a. until 2010 and 14% p.a. up to 2015). As a result of targeted market penetration efforts, the return on sales is estimated at about 15% for the years following 2015 with an average sales growth of 5-10% p.a. in '000 of dollars Entry 2007 (%) Breakeven 2010 (%) Outlook 2015 (%)Gross Revenues $ 58 $ 2.114 $ 3.632 Trade Discounts $ 4 7% $ 106 5% $ 109 3%Net Revenues $ 54 93% $ 2.008 95% $ 3.523 97% Costs of goods sold $ 19 33% $ 702 33% $ 1.207 33%Distribution costs $ 6 10% $ 169 8% $ 291 8%Selling costs $ 5 8% $ 127 6% $ 218 6%Gross Margin $ 24 42% $ 1.010 48% $ 1.808 50% Advertising $ 300 516% $ 540 26% $ 784 22%Promotions/Merchandising $ 125 215% $ 230 11% $ 336 9%Administrative costs $ 6 10% $ 190 9% $ 254 7%Profit before tax $ -407 -700% $ 50 2% $ 434 12%

In 2007, Fischer will benefit from the financial support of the Heineken group to which it belongs. Heineken, which spent $50 million on advertising and promotion in 2005, will provide Fischer with a budget of $400,000 for launching the promising product in the U.S. alcohol drinks market. In the long run (after the end of the expansion wave), the advertising and promotion budget is expected to represent about 20% of operation revenues. Sources: In accordance with the Demand Forecast (Exhibit 8), own budgeting

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

30

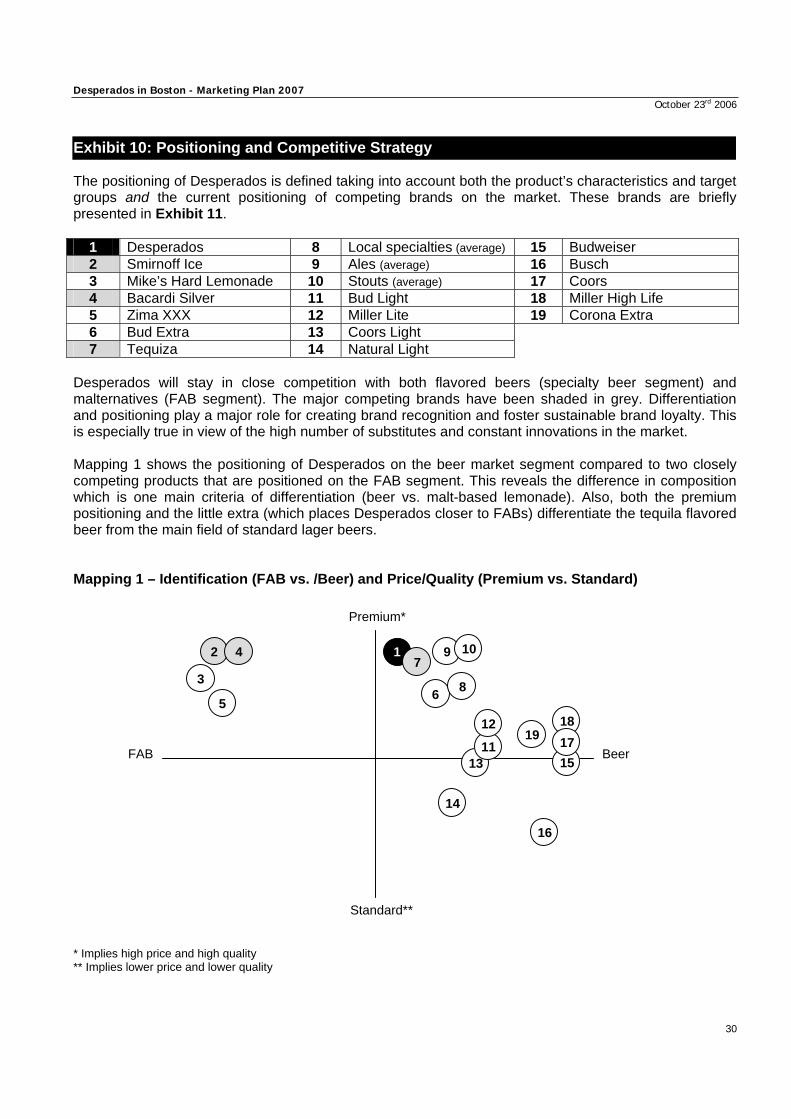

Exhibit 10: Positioning and Competitive Strategy The positioning of Desperados is defined taking into account both the product’s characteristics and target groups and the current positioning of competing brands on the market. These brands are briefly presented in Exhibit 11.

1 Desperados 8 Local specialties (average) 15 Budweiser 2 Smirnoff Ice 9 Ales (average) 16 Busch 3 Mike’s Hard Lemonade 10 Stouts (average) 17 Coors 4 Bacardi Silver 11 Bud Light 18 Miller High Life 5 Zima XXX 12 Miller Lite 19 Corona Extra 6 Bud Extra 13 Coors Light 7 Tequiza 14 Natural Light

Desperados will stay in close competition with both flavored beers (specialty beer segment) and malternatives (FAB segment). The major competing brands have been shaded in grey. Differentiation and positioning play a major role for creating brand recognition and foster sustainable brand loyalty. This is especially true in view of the high number of substitutes and constant innovations in the market. Mapping 1 shows the positioning of Desperados on the beer market segment compared to two closely competing products that are positioned on the FAB segment. This reveals the difference in composition which is one main criteria of differentiation (beer vs. malt-based lemonade). Also, both the premium positioning and the little extra (which places Desperados closer to FABs) differentiate the tequila flavored beer from the main field of standard lager beers. Mapping 1 – Identification (FAB vs. /Beer) and Price/Quality (Premium vs. Standard) * Implies high price and high quality ** Implies lower price and lower quality

Premium*

Standard**

Beer FAB

1

15

3

2 4

5 6

7

19 18

16

14

13 11

12 17

8

9 10

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

31

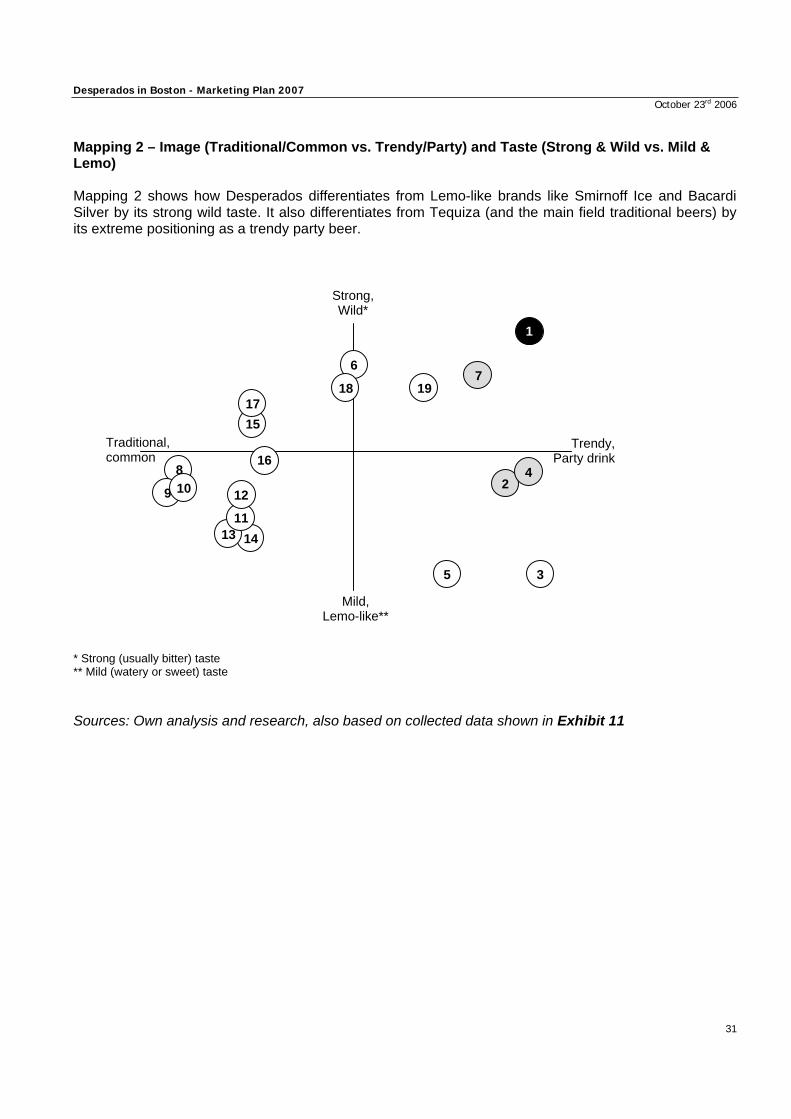

Mapping 2 – Image (Traditional/Common vs. Trendy/Party) and Taste (Strong & Wild vs. Mild & Lemo) Mapping 2 shows how Desperados differentiates from Lemo-like brands like Smirnoff Ice and Bacardi Silver by its strong wild taste. It also differentiates from Tequiza (and the main field traditional beers) by its extreme positioning as a trendy party beer. * Strong (usually bitter) taste ** Mild (watery or sweet) taste Sources: Own analysis and research, also based on collected data shown in Exhibit 11

Strong, Wild*

Mild, Lemo-like**

Trendy, Party drink

Traditional, common

1

15

3

2 4

5

6 7

19 18

16

14 13 11

12

17

8

9 10

Product Category or Brand

Company Description Packaging (in stores) Unit price Liter Price Unit price Liter price

Supermarket/ Liquor or Convenience Store Pubs/Bars/Clubs

Flavored alcoholic beverages Smirnoff (Ice/ Black Ice/ Twisted)

Smirnoff malt-based beverage with vodka available in different flavors (citrus, grape, apple…)

12oz bottle (6-pack)

$ 1.30 $3.90 $3.75 $11.25

Mike’s Hard Lemonade

Mike’s malt-based lemonade available in five different berry flavors

12oz bottle (6-pack)

$ 1.25 $3.75 Not for Sale* Not for Sale*

Bacardi Silver

Anheuser-Busch malt-based beverage with rum available in different flavors (apple, peach, orange…)

12oz bottle (6-pack)

$1.30 $3.90 $3.75 $11.25

Zima XXX Coors malt-based beverage available in different flavors (orange, lemon, cherry…)

12oz bottle (6-pack)

$1.20 $3.60 Not for Sale* Not for Sale*

Specialty beers Flavored beers Bud Extra Anheuser-Busch beer with caffeine,

ginseng and guarana, three aromas (blackberry, raspberry and cherry)

12oz bottle (6-pack)

$1.30 $3.90 Not for Sale* Not for Sale*

Tequiza Anheuser-Busch lager beer with real blue agave nectar and a natural flavor of lime and real Mexican tequila

12oz bottle (6-pack)

$1.40 $4.20 $3.75 $11.25

Regional beers Local Specialties (average)

Diverse Usually beers with a little ‘extra’ (e.g. British dark beer), generally imported

12oz bottle (6-pack) or 24oz bottle

$1.10-$1.60

$1.80-$2.60

$3.30-$4.80 $3.50-$5.00 $10.50-$15.00

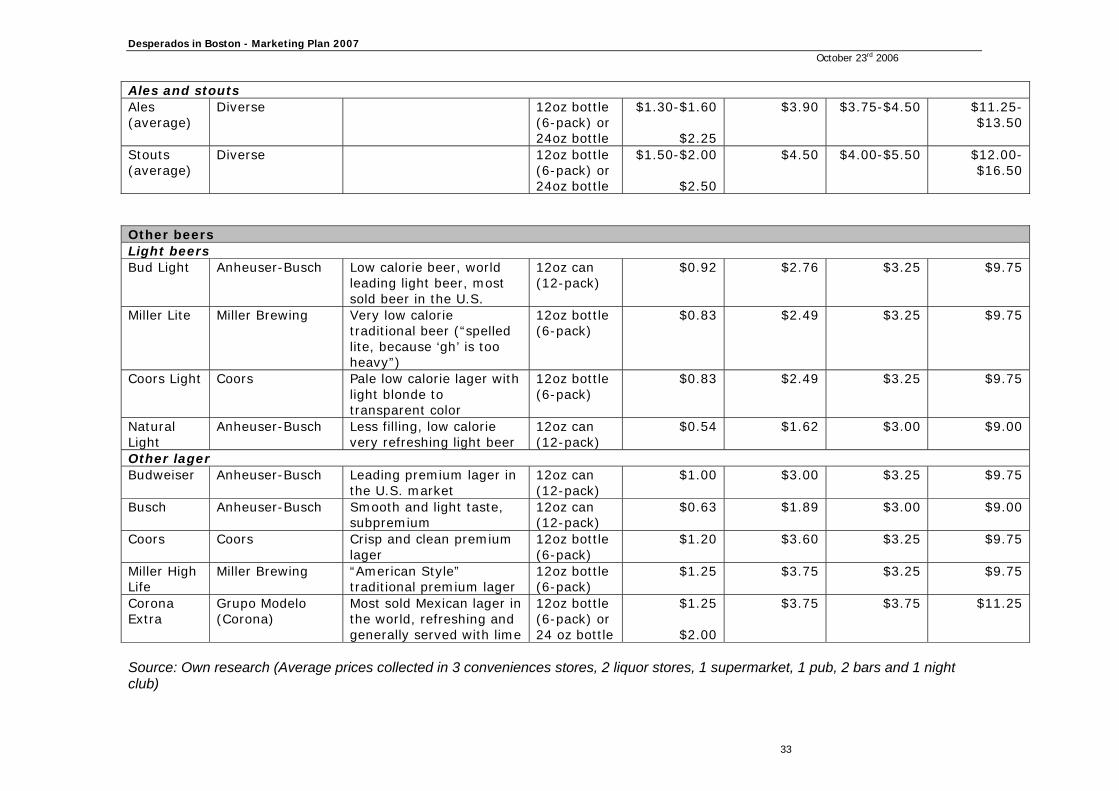

Exhibit 11: Prices per category of alcoholic drink and brand

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

33

Source: Own research (Average prices collected in 3 conveniences stores, 2 liquor stores, 1 supermarket, 1 pub, 2 bars and 1 night club)

Ales and stouts Ales (average)

Diverse 12oz bottle (6-pack) or 24oz bottle

$1.30-$1.60

$2.25

$3.90 $3.75-$4.50 $11.25-$13.50

Stouts (average)

Diverse 12oz bottle (6-pack) or 24oz bottle

$1.50-$2.00

$2.50

$4.50 $4.00-$5.50 $12.00-$16.50

Other beers Light beers Bud Light Anheuser-Busch Low calorie beer, world

leading light beer, most sold beer in the U.S.

12oz can (12-pack)

$0.92 $2.76 $3.25 $9.75

Miller Lite Miller Brewing Very low calorie traditional beer (“spelled lite, because ‘gh’ is too heavy”)

12oz bottle (6-pack)

$0.83 $2.49 $3.25 $9.75

Coors Light Coors Pale low calorie lager with light blonde to transparent color

12oz bottle (6-pack)

$0.83 $2.49 $3.25 $9.75

Natural Light

Anheuser-Busch Less filling, low calorie very refreshing light beer

12oz can (12-pack)

$0.54 $1.62 $3.00 $9.00

Other lager Budweiser Anheuser-Busch Leading premium lager in

the U.S. market 12oz can (12-pack)

$1.00 $3.00 $3.25 $9.75

Busch Anheuser-Busch Smooth and light taste, subpremium

12oz can (12-pack)

$0.63 $1.89 $3.00 $9.00

Coors Coors Crisp and clean premium lager

12oz bottle (6-pack)

$1.20 $3.60 $3.25 $9.75

Miller High Life

Miller Brewing “American Style” traditional premium lager

12oz bottle (6-pack)

$1.25 $3.75 $3.25 $9.75

Corona Extra

Grupo Modelo (Corona)

Most sold Mexican lager in the world, refreshing and generally served with lime

12oz bottle (6-pack) or 24 oz bottle

$1.25

$2.00

$3.75 $3.75 $11.25

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

Exhibit 12: Survey Questionnaire Source: Own creation

8

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

35

9

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

36

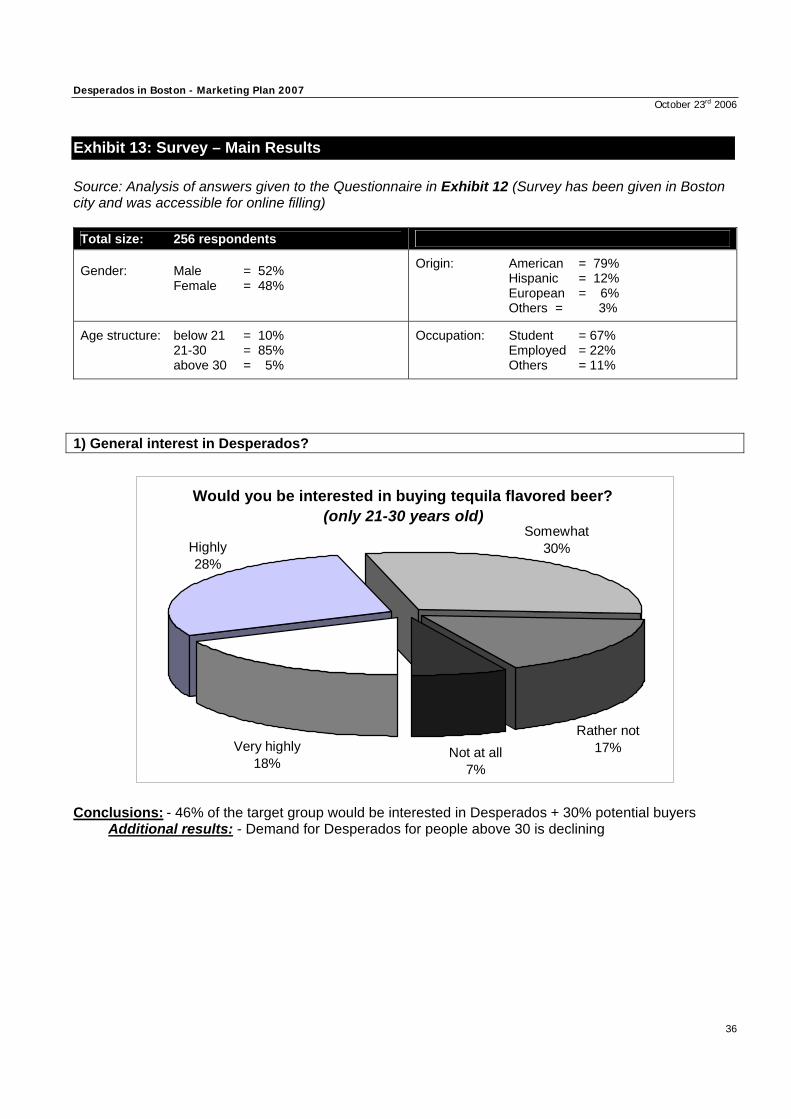

Exhibit 13: Survey – Main Results

Source: Analysis of answers given to the Questionnaire in Exhibit 12 (Survey has been given in Boston city and was accessible for online filling) Total size: 256 respondents

Gender: Male = 52% Female = 48%

Origin: American = 79% Hispanic = 12% European = 6% Others = 3%

Age structure: below 21 = 10% 21-30 = 85% above 30 = 5%

Occupation: Student = 67% Employed = 22% Others = 11%

1) General interest in Desperados?

Would you be interested in buying tequila flavored beer? (only 21-30 years old)

Very highly18%

Highly28%

Rather not17%Not at all

7%

Somewhat30%

Conclusions: - 46% of the target group would be interested in Desperados + 30% potential buyers Additional results: - Demand for Desperados for people above 30 is declining

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

37

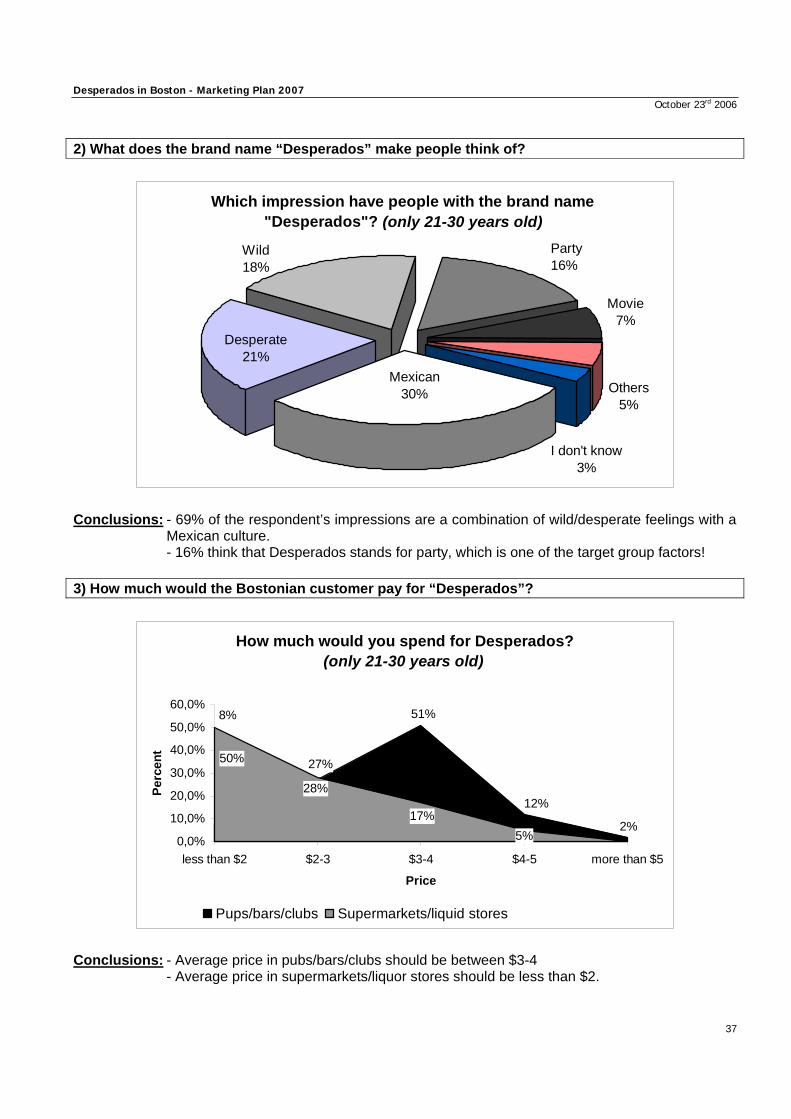

2) What does the brand name “Desperados” make people think of?

Which impression have people with the brand name "Desperados"? (only 21-30 years old)

Wild18%

Movie7%

Desperate21%

Mexican30%

I don't know3%

Others5%

Party16%

Conclusions: - 69% of the respondent’s impressions are a combination of wild/desperate feelings with a

Mexican culture. - 16% think that Desperados stands for party, which is one of the target group factors! 3) How much would the Bostonian customer pay for “Desperados”?

How much would you spend for Desperados?(only 21-30 years old)

8%

2%

27%

51%

12%

5%17%

28%

50%

0,0%

10,0%

20,0%

30,0%

40,0%

50,0%

60,0%

less than $2 $2-3 $3-4 $4-5 more than $5

Price

Perc

ent

Pups/bars/clubs Supermarkets/liquid stores

Conclusions: - Average price in pubs/bars/clubs should be between $3-4 - Average price in supermarkets/liquor stores should be less than $2.

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

38

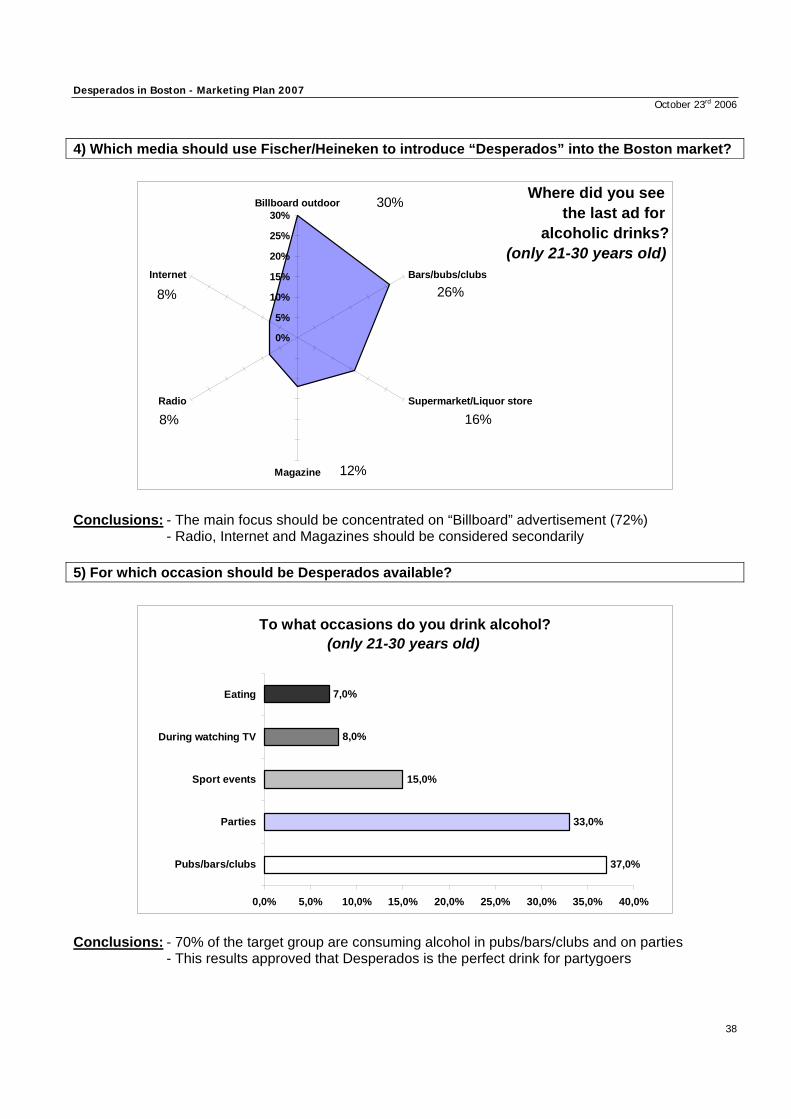

4) Which media should use Fischer/Heineken to introduce “Desperados” into the Boston market?

8% 16%

26%

12%

30%

8%

0%

5%

10%

15%

20%

25%

30%Billboard outdoor

Bars/bubs/clubs

Supermarket/Liquor store

Magazine

Radio

Internet

Where did you see the last ad for

alcoholic drinks?(only 21-30 years old)

Conclusions: - The main focus should be concentrated on “Billboard” advertisement (72%) - Radio, Internet and Magazines should be considered secondarily 5) For which occasion should be Desperados available?

To what occasions do you drink alcohol?(only 21-30 years old)

37,0%

33,0%

15,0%

8,0%

7,0%

0,0% 5,0% 10,0% 15,0% 20,0% 25,0% 30,0% 35,0% 40,0%

Pubs/bars/clubs

Parties

Sport events

During watching TV

Eating

Conclusions: - 70% of the target group are consuming alcohol in pubs/bars/clubs and on parties - This results approved that Desperados is the perfect drink for partygoers

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

39

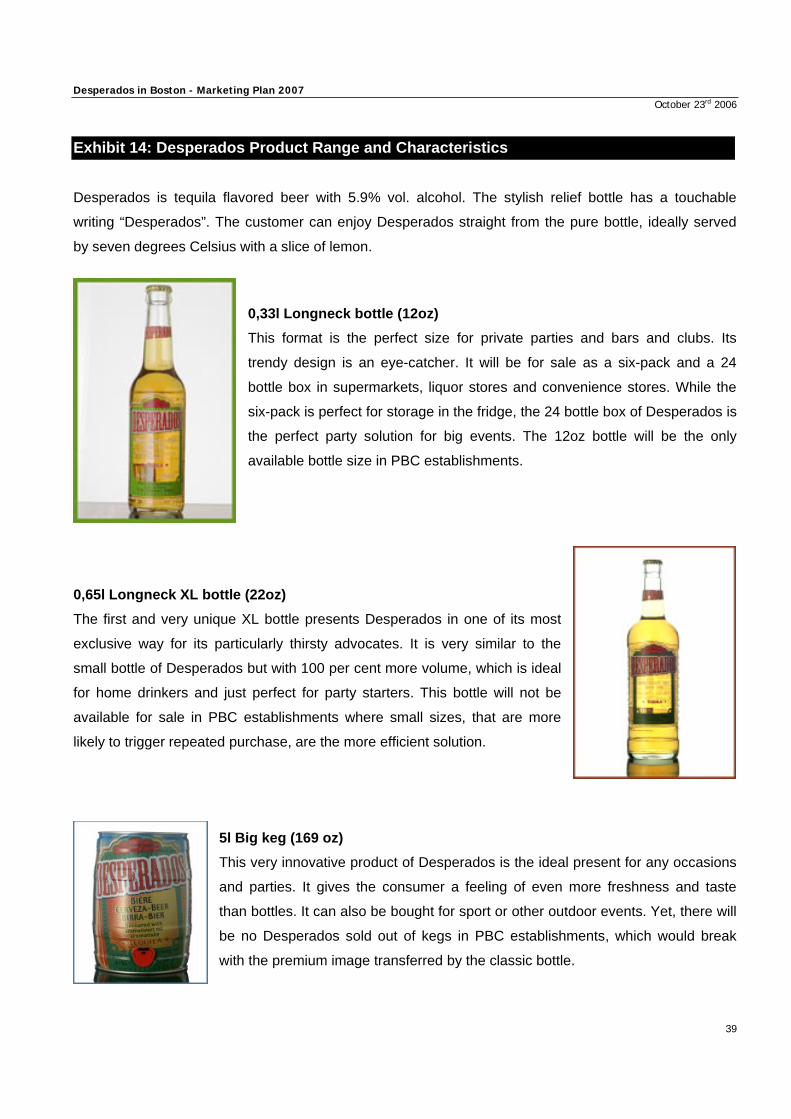

Exhibit 14: Desperados Product Range and Characteristics Desperados is tequila flavored beer with 5.9% vol. alcohol. The stylish relief bottle has a touchable

writing “Desperados”. The customer can enjoy Desperados straight from the pure bottle, ideally served

by seven degrees Celsius with a slice of lemon.

0,33l Longneck bottle (12oz) This format is the perfect size for private parties and bars and clubs. Its

trendy design is an eye-catcher. It will be for sale as a six-pack and a 24

bottle box in supermarkets, liquor stores and convenience stores. While the

six-pack is perfect for storage in the fridge, the 24 bottle box of Desperados is

the perfect party solution for big events. The 12oz bottle will be the only

available bottle size in PBC establishments.

0,65l Longneck XL bottle (22oz) The first and very unique XL bottle presents Desperados in one of its most

exclusive way for its particularly thirsty advocates. It is very similar to the

small bottle of Desperados but with 100 per cent more volume, which is ideal

for home drinkers and just perfect for party starters. This bottle will not be

available for sale in PBC establishments where small sizes, that are more

likely to trigger repeated purchase, are the more efficient solution.

5l Big keg (169 oz) This very innovative product of Desperados is the ideal present for any occasions

and parties. It gives the consumer a feeling of even more freshness and taste

than bottles. It can also be bought for sport or other outdoor events. Yet, there will

be no Desperados sold out of kegs in PBC establishments, which would break

with the premium image transferred by the classic bottle.

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

40

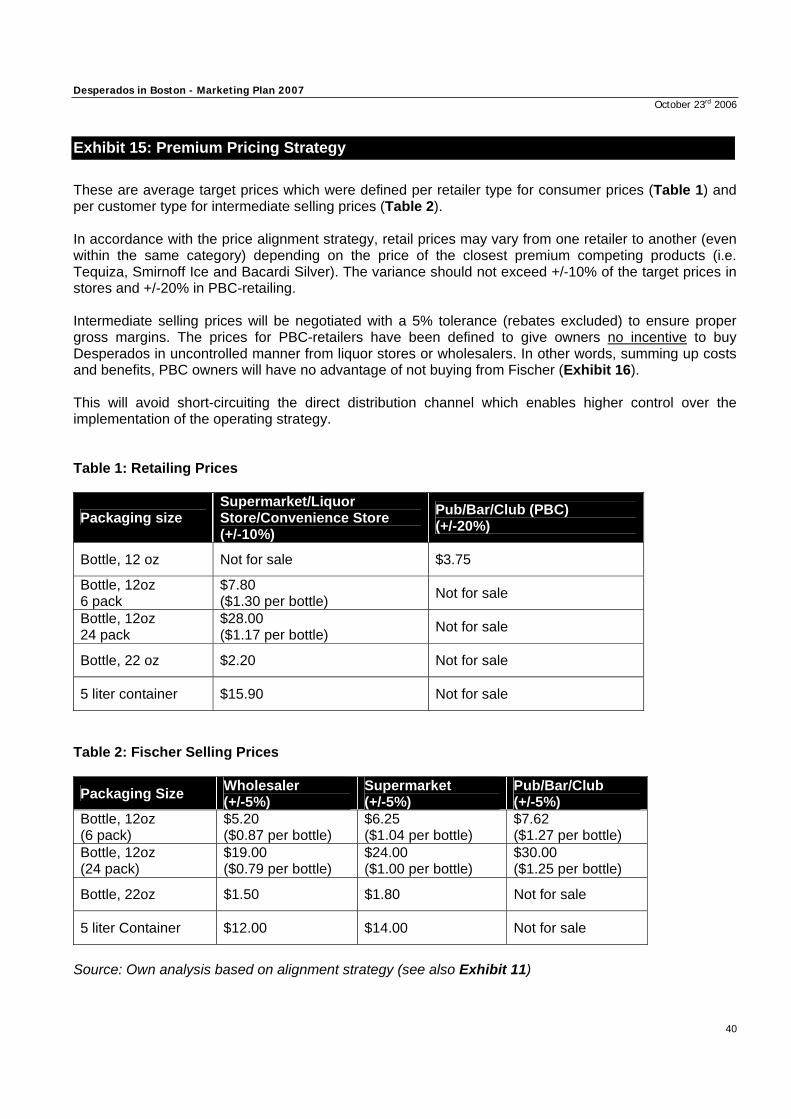

Exhibit 15: Premium Pricing Strategy These are average target prices which were defined per retailer type for consumer prices (Table 1) and per customer type for intermediate selling prices (Table 2). In accordance with the price alignment strategy, retail prices may vary from one retailer to another (even within the same category) depending on the price of the closest premium competing products (i.e. Tequiza, Smirnoff Ice and Bacardi Silver). The variance should not exceed +/-10% of the target prices in stores and +/-20% in PBC-retailing. Intermediate selling prices will be negotiated with a 5% tolerance (rebates excluded) to ensure proper gross margins. The prices for PBC-retailers have been defined to give owners no incentive to buy Desperados in uncontrolled manner from liquor stores or wholesalers. In other words, summing up costs and benefits, PBC owners will have no advantage of not buying from Fischer (Exhibit 16). This will avoid short-circuiting the direct distribution channel which enables higher control over the implementation of the operating strategy. Table 1: Retailing Prices

Packaging size Supermarket/Liquor Store/Convenience Store (+/-10%)

Pub/Bar/Club (PBC) (+/-20%)

Bottle, 12 oz Not for sale $3.75

Bottle, 12oz 6 pack

$7.80 ($1.30 per bottle) Not for sale

Bottle, 12oz 24 pack

$28.00 ($1.17 per bottle) Not for sale

Bottle, 22 oz $2.20 Not for sale

5 liter container $15.90 Not for sale

Table 2: Fischer Selling Prices

Packaging Size Wholesaler (+/-5%)

Supermarket (+/-5%)

Pub/Bar/Club (+/-5%)

Bottle, 12oz (6 pack)

$5.20 ($0.87 per bottle)

$6.25 ($1.04 per bottle)

$7.62 ($1.27 per bottle)

Bottle, 12oz (24 pack)

$19.00 ($0.79 per bottle)

$24.00 ($1.00 per bottle)

$30.00 ($1.25 per bottle)

Bottle, 22oz $1.50 $1.80 Not for sale

5 liter Container $12.00 $14.00 Not for sale

Source: Own analysis based on alignment strategy (see also Exhibit 11)

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

41

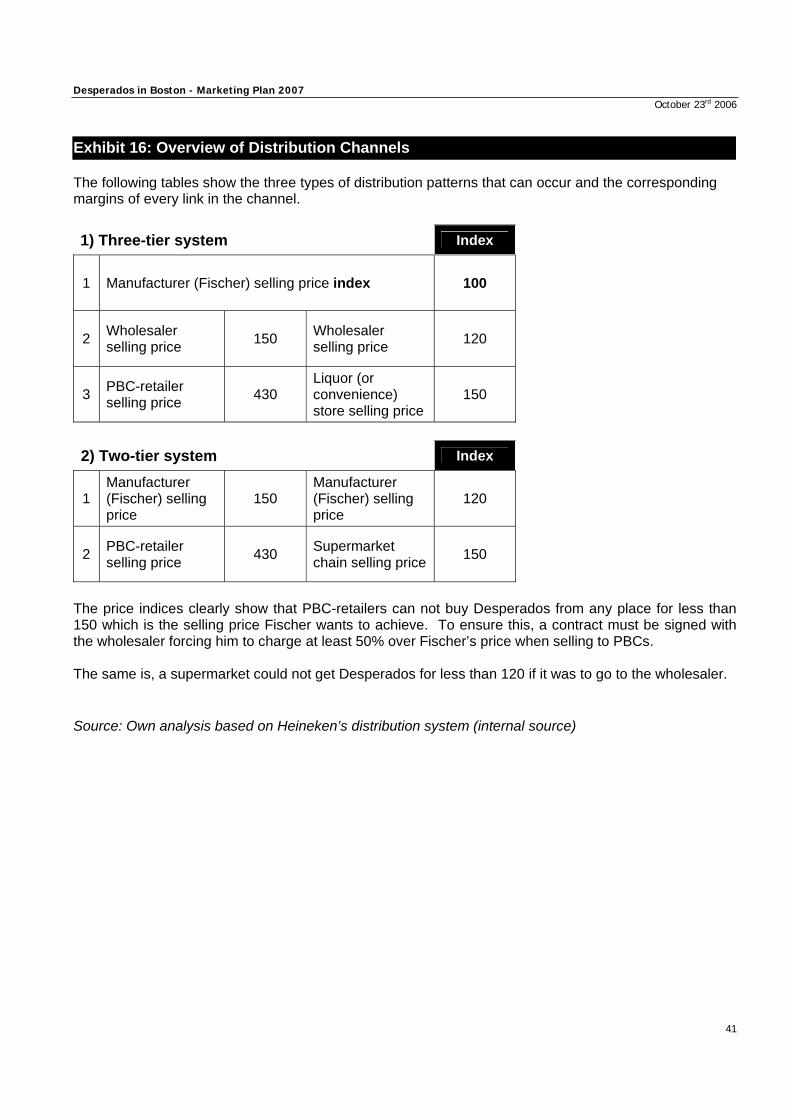

Exhibit 16: Overview of Distribution Channels The following tables show the three types of distribution patterns that can occur and the corresponding margins of every link in the channel. 1) Three-tier system Index

1 Manufacturer (Fischer) selling price index 100

2 Wholesaler selling price 150 Wholesaler

selling price 120

3 PBC-retailer selling price 430

Liquor (or convenience) store selling price

150

2) Two-tier system Index

1 Manufacturer (Fischer) selling price

150 Manufacturer (Fischer) selling price

120

2 PBC-retailer selling price 430 Supermarket

chain selling price 150

The price indices clearly show that PBC-retailers can not buy Desperados from any place for less than 150 which is the selling price Fischer wants to achieve. To ensure this, a contract must be signed with the wholesaler forcing him to charge at least 50% over Fischer’s price when selling to PBCs. The same is, a supermarket could not get Desperados for less than 120 if it was to go to the wholesaler. Source: Own analysis based on Heineken’s distribution system (internal source)

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

42

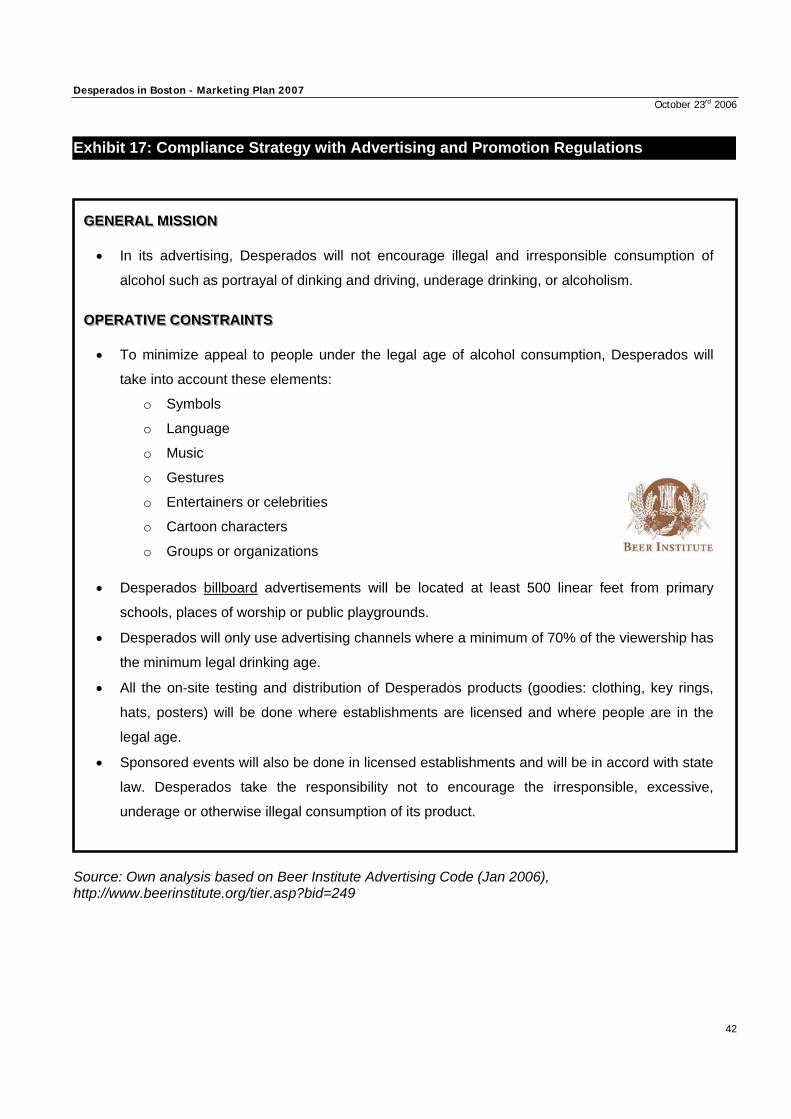

Exhibit 17: Compliance Strategy with Advertising and Promotion Regulations

GGGEEENNNEEERRRAAALLL MMMIIISSSSSSIIIOOONNN • In its advertising, Desperados will not encourage illegal and irresponsible consumption of

alcohol such as portrayal of dinking and driving, underage drinking, or alcoholism.

OOOPPPEEERRRAAATTTIIIVVVEEE CCCOOONNNSSSTTTRRRAAAIIINNNTTTSSS • To minimize appeal to people under the legal age of alcohol consumption, Desperados will

take into account these elements:

o Symbols

o Language

o Music

o Gestures

o Entertainers or celebrities

o Cartoon characters

o Groups or organizations

• Desperados billboard advertisements will be located at least 500 linear feet from primary

schools, places of worship or public playgrounds.

• Desperados will only use advertising channels where a minimum of 70% of the viewership has

the minimum legal drinking age.

• All the on-site testing and distribution of Desperados products (goodies: clothing, key rings,

hats, posters) will be done where establishments are licensed and where people are in the

legal age.

• Sponsored events will also be done in licensed establishments and will be in accord with state

law. Desperados take the responsibility not to encourage the irresponsible, excessive,

underage or otherwise illegal consumption of its product.

Source: Own analysis based on Beer Institute Advertising Code (Jan 2006), http://www.beerinstitute.org/tier.asp?bid=249

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

43

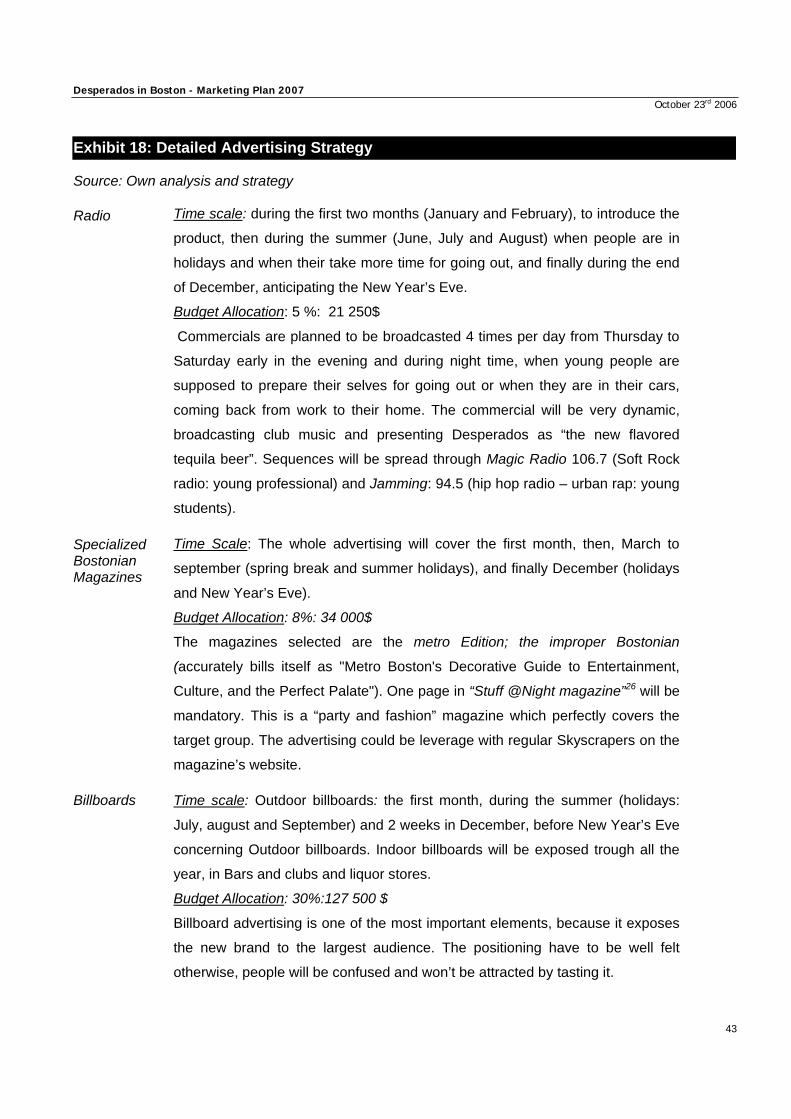

Exhibit 18: Detailed Advertising Strategy Source: Own analysis and strategy Radio

Specialized Bostonian Magazines

Billboards

Time scale: during the first two months (January and February), to introduce the

product, then during the summer (June, July and August) when people are in

holidays and when their take more time for going out, and finally during the end

of December, anticipating the New Year’s Eve.

Budget Allocation: 5 %: 21 250$

Commercials are planned to be broadcasted 4 times per day from Thursday to

Saturday early in the evening and during night time, when young people are

supposed to prepare their selves for going out or when they are in their cars,

coming back from work to their home. The commercial will be very dynamic,

broadcasting club music and presenting Desperados as “the new flavored

tequila beer”. Sequences will be spread through Magic Radio 106.7 (Soft Rock

radio: young professional) and Jamming: 94.5 (hip hop radio – urban rap: young

students).

Time Scale: The whole advertising will cover the first month, then, March to

september (spring break and summer holidays), and finally December (holidays

and New Year’s Eve).

Budget Allocation: 8%: 34 000$

The magazines selected are the metro Edition; the improper Bostonian

(accurately bills itself as "Metro Boston's Decorative Guide to Entertainment,

Culture, and the Perfect Palate"). One page in “Stuff @Night magazine”26 will be

mandatory. This is a “party and fashion” magazine which perfectly covers the

target group. The advertising could be leverage with regular Skyscrapers on the

magazine’s website.

Time scale: Outdoor billboards: the first month, during the summer (holidays:

July, august and September) and 2 weeks in December, before New Year’s Eve

concerning Outdoor billboards. Indoor billboards will be exposed trough all the

year, in Bars and clubs and liquor stores.

Budget Allocation: 30%:127 500 $

Billboard advertising is one of the most important elements, because it exposes

the new brand to the largest audience. The positioning have to be well felt

otherwise, people will be confused and won’t be attracted by tasting it.

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

44

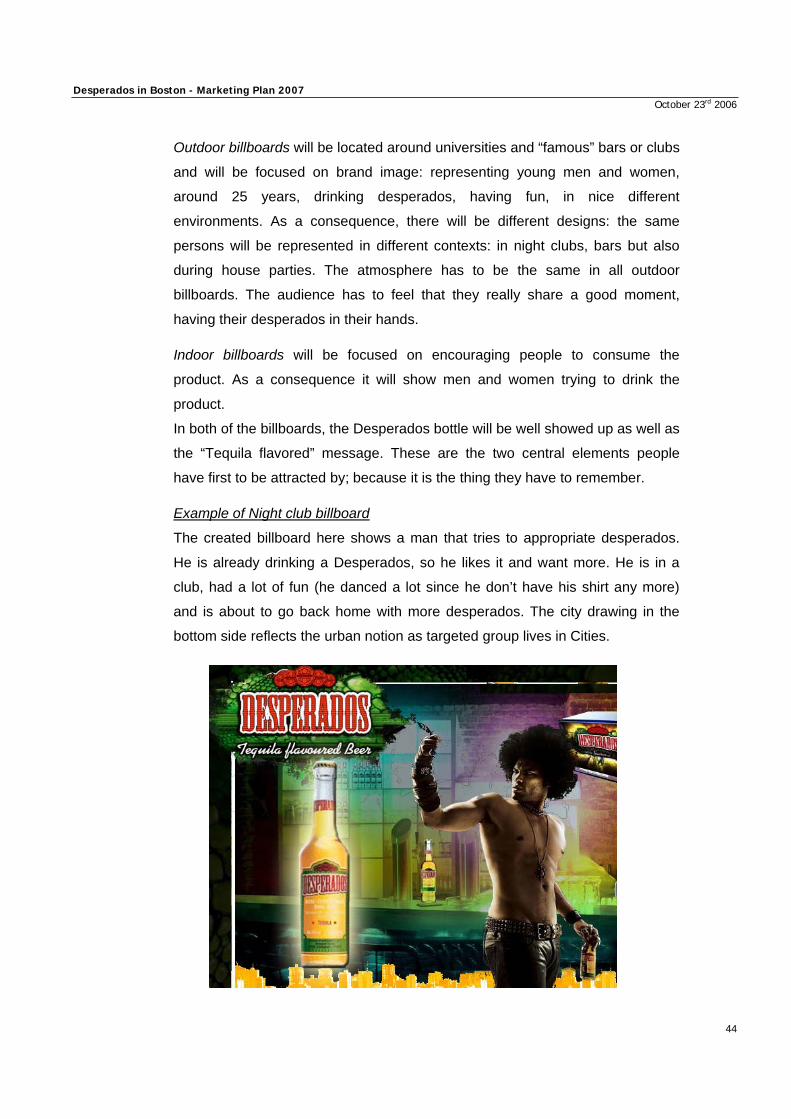

Outdoor billboards will be located around universities and “famous” bars or clubs

and will be focused on brand image: representing young men and women,

around 25 years, drinking desperados, having fun, in nice different

environments. As a consequence, there will be different designs: the same

persons will be represented in different contexts: in night clubs, bars but also

during house parties. The atmosphere has to be the same in all outdoor

billboards. The audience has to feel that they really share a good moment,

having their desperados in their hands.

Indoor billboards will be focused on encouraging people to consume the

product. As a consequence it will show men and women trying to drink the

product.

In both of the billboards, the Desperados bottle will be well showed up as well as

the “Tequila flavored” message. These are the two central elements people

have first to be attracted by; because it is the thing they have to remember.

Example of Night club billboard The created billboard here shows a man that tries to appropriate desperados.

He is already drinking a Desperados, so he likes it and want more. He is in a

club, had a lot of fun (he danced a lot since he don’t have his shirt any more)

and is about to go back home with more desperados. The city drawing in the

bottom side reflects the urban notion as targeted group lives in Cities.

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

45

Internet

Sponsorship (Sport events & DJs) Pubs & Night Clubs Promotion, Special Events

Time Scale: All year long

Budget allocation: 15%: 63 500$

Internet is a media regularly used by the targeted demographic group. Create a

flash web site with games could be a very powerful and entertaining way for

getting prospects accustomed with the brand. The web-site promotion will be

leveraged on an aggressive e-mailing campaign addressed to prospect

accurately defined with the rented databases.

A simple game example is bottles of desperados falling and the gamer have to

catch them in a crate at the bottom of the screen, the more he collects the better

the reward. This system was used by Pilsner Urquell and there were ladies

onscreen who got undressed the more bottles the gamer collected.

Time scale: 2 presences in sports matches per month during all the year, expect

during October, November. The partnerships with clubs will be done during one

week end on January (for the launching), March (spring break), August (summer

holidays) and December (New Year’s Eve)

Budget Allocation: 12 %: 51 000 $ for sports Events

10%: 42 500 $ for night clubs parties with famous DJ

Good looking girls will present Desperados in nice stands in stadiums. Cheap

offers will be organized in order to encourage people (older than 21 years old) to

taste it. In a long term vision, Desperados advertisements will be spread through

national sports events such as Superbowl or US open (where Heineken yet

developed partnership this year). Fischer must also look for partnerships with

local famous clubs and associate its image with famous DJs. During these

events, desperados branded products like clothing, posters, hats will be offered.

Time scale: January, April (Spring break events), July to September (summer

holidays) and December (winter holidays)

Budget Allocation: 15 %: 63 750 $

The Desperados Events will clearly be organized in Night clubs and Bars.

Special Desperados “happy hours” will take place in the most popular Bostonian

Bars (lounge bars but also bars near universities) where people will benefit from

discounts (e.g. $2/ 12oz bottle). Dedicated Desperados night will be promoted

on the website. In both bars and clubs, good looking women (hired by

Desperados in Boston - Marketing Plan 2007 October 23rd 2006

46

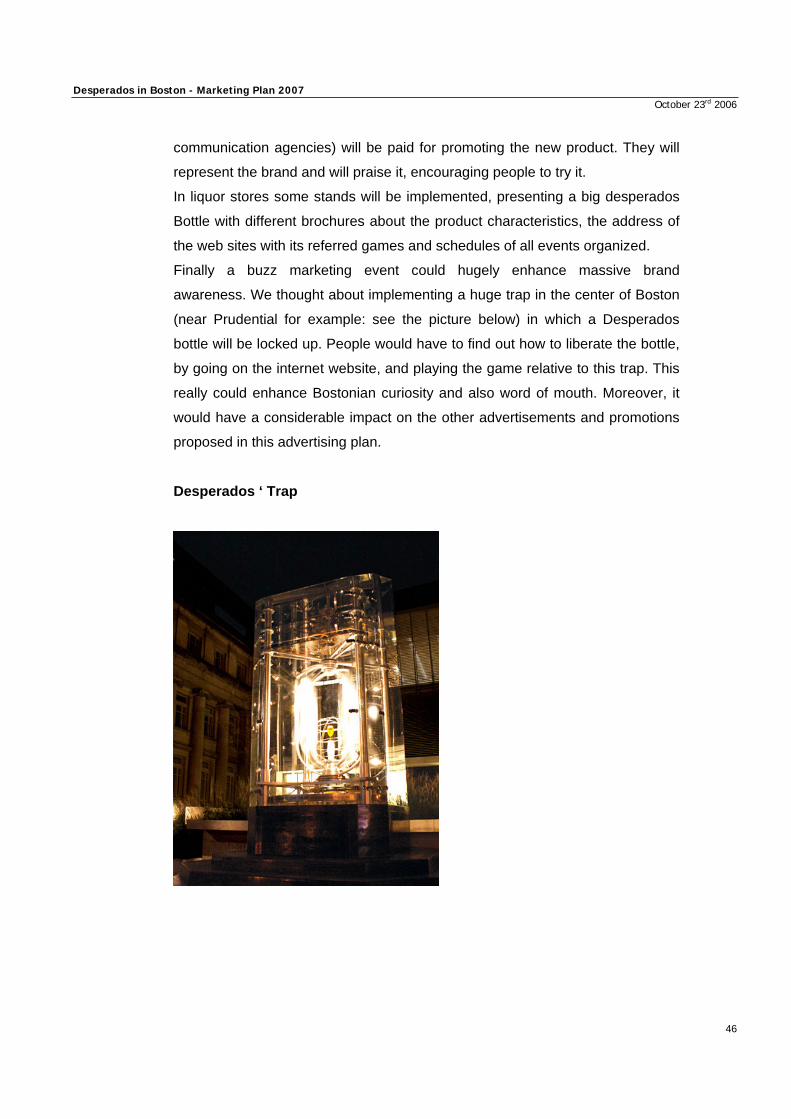

communication agencies) will be paid for promoting the new product. They will