Embed Size (px)

Citation preview

www.intrasoft-intl.com

PROFITS Fundamental Concepts White Paper - Core Banking Systems Dept.

2/14 v1.00

DOCUMENT HISTORY

Ed. Rev. Date Description Pages

0 10 02/09/2011 Initial Version 14

0 20 02/09/2011 Implement internal review comments

14

1 00 05/09/2011 Final Version 14

FOR INTERNAL USE ONLY

Prepared by: G. N. Skarmoutsos Date: 02/09/2011 Reviewed by: A. Diamandeas Date: 02/09/2011 Approved by: G. Manos (Deputy CEO/CTO) Date: 05/09/2011 Owner: G. N. Skarmoutsos Date: 05/09/2011

www.intrasoft-intl.com

PROFITS Fundamental Concepts White Paper - Core Banking Systems Dept.

3/14 v1.00

TABLE OF CONTENTS 1 PROFITS® Universal Core Banking Information System.............................4 2 PROFITS® Subsystems...................................................................................5 3 Products Generation Engine..........................................................................9 4 Customer – Member management ..............................................................12 5 Configurable Services – Business Rules Based Architecture..................13

www.intrasoft-intl.com

PROFITS Fundamental Concepts White Paper - Core Banking Systems Dept.

4/14 v1.00

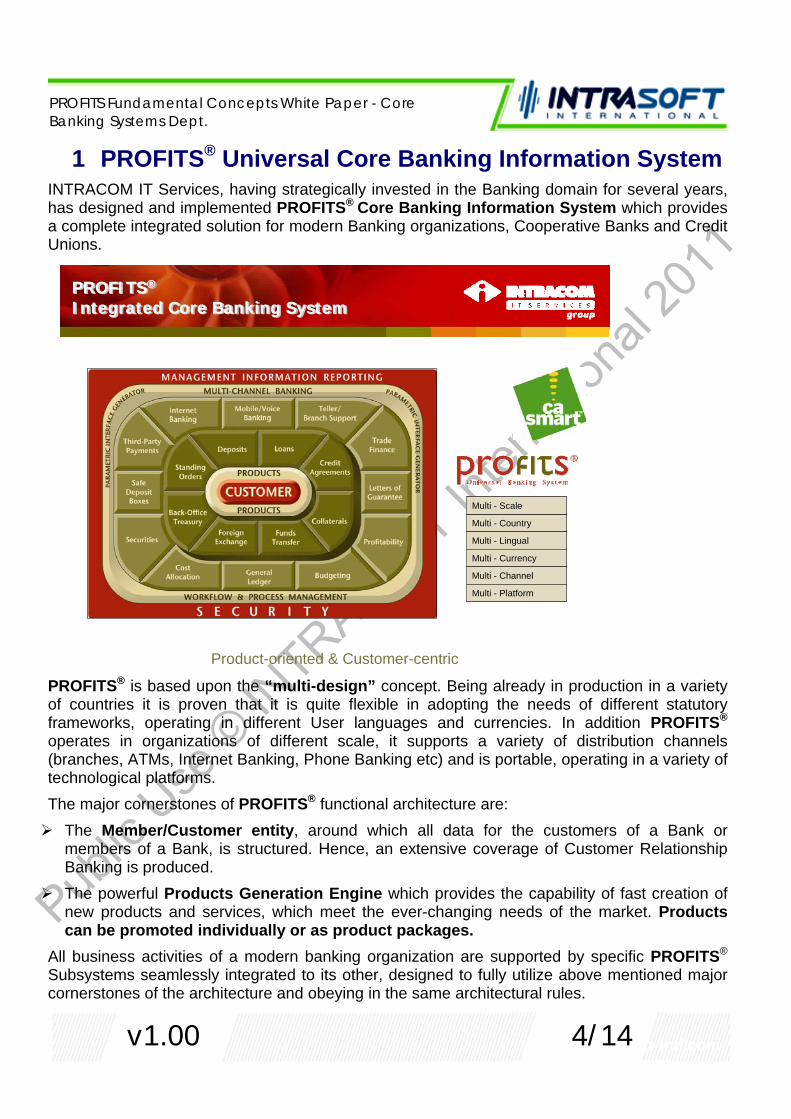

1 PROFITS® Universal Core Banking Information System INTRACOM IT Services, having strategically invested in the Banking domain for several years, has designed and implemented PROFITS® Core Banking Information System which provides a complete integrated solution for modern Banking organizations, Cooperative Banks and Credit Unions.

PROFITS® is based upon the “multi-design” concept. Being already in production in a variety of countries it is proven that it is quite flexible in adopting the needs of different statutory frameworks, operating in different User languages and currencies. In addition PROFITS® operates in organizations of different scale, it supports a variety of distribution channels (branches, ATMs, Internet Banking, Phone Banking etc) and is portable, operating in a variety of technological platforms. The major cornerstones of PROFITS® functional architecture are: The Member/Customer entity, around which all data for the customers of a Bank or

members of a Bank, is structured. Hence, an extensive coverage of Customer Relationship Banking is produced.

The powerful Products Generation Engine which provides the capability of fast creation of new products and services, which meet the ever-changing needs of the market. Products can be promoted individually or as product packages.

All business activities of a modern banking organization are supported by specific PROFITS® Subsystems seamlessly integrated to its other, designed to fully utilize above mentioned major cornerstones of the architecture and obeying in the same architectural rules.

Multi - Country

Multi - Scale

Multi - Lingual

Multi - Currency

Multi - Channel

Multi - Platform

Multi - Country

Multi - Scale

Multi - Lingual

Multi - Currency

Multi - Channel

Multi - Platform

PROFITS®

Integrated Core Banking SystemPROFITSPROFITS®®

Integrated Core Banking SystemIntegrated Core Banking System

Product-oriented & Customer-centric

www.intrasoft-intl.com

PROFITS Fundamental Concepts White Paper - Core Banking Systems Dept.

5/14 v1.00

2 PROFITS® Subsystems

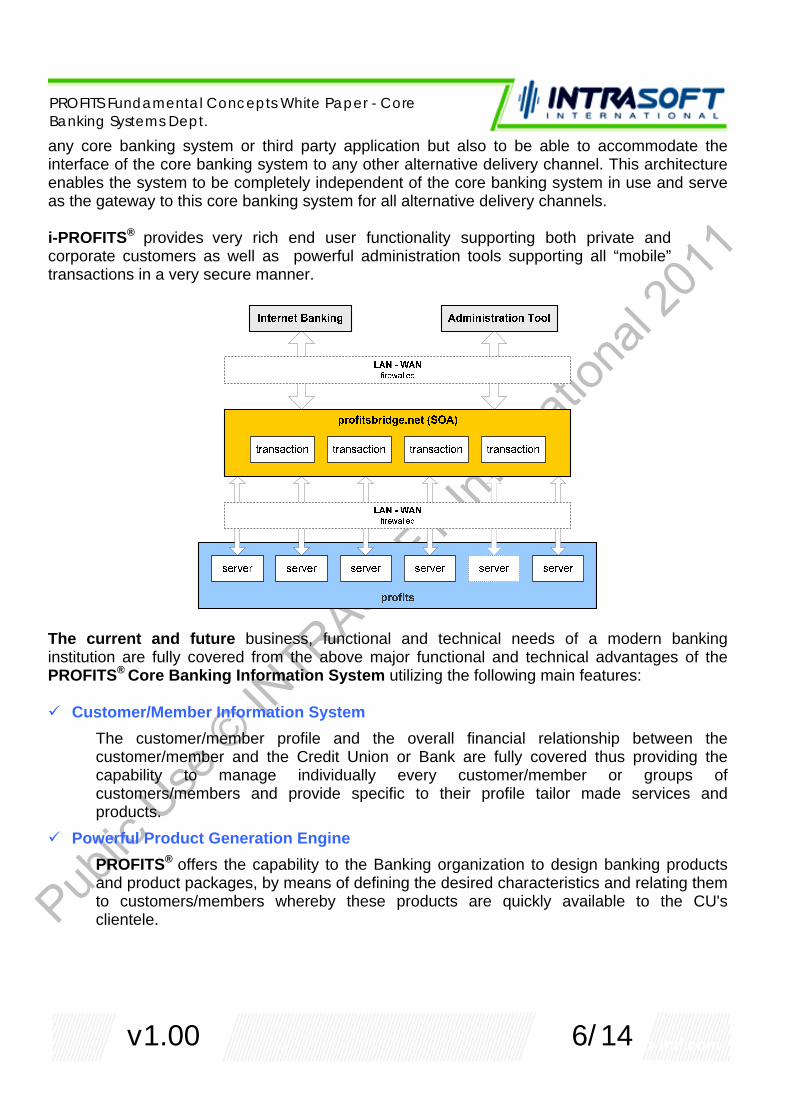

PROFITS® is a complete Core Banking Solution, consisting by Subsystems seamlessly integrated to its other and obeying in the same architectural rules. Hence, PROFITS® can be installed either as a whole System or by Subsystems in accordance with the business needs of a Banking Organization. In the latter case, additional Subsystems can be installed in a “plug and play” manner. (Please refer to PROFITS® Functional Description document for a detailed presentation of PROFITS® Subsystems’ functionality) PROFITS®, being entirely developed with CA Gen (by CA) is a portable System that can be deployed in a variety of technology platforms and architectures. The System can be deployed either on a J2EE or .Net architecture. In addition, it can be deployed in a client-server architecture (with graphical or web enabled client) running on Mainframe environment with CICS and DB2 or on any flavor of UNIX or Win 2003 Server with Oracle, also being able to fully incorporate TUXEDO. Due to its modern technical architecture, the System can be easily interfaced with any SOA compliant 3rd party system or application using Web Services. For the area of Internet Banking, Phone / Mobile Banking, INTRACOM IT Services Group has designed and implemented i-PROFITS® Internet Banking, Phone / Mobile Banking System. Although i-PROFITS® is fully integrated with PROFITS® Core Banking Information System, the Open Architecture of the PROFITS® Gateway platform, upon which i-PROFITS® is based, is designed and developed in such a way so that the proposed solutions not only can interface to

BudgetingCost AllocationFixed Assets / Third Party TransactionsSecuritiesUnderwritingSafety Deposit BoxesATM/POS & Card ManagementInternet BankingTelephone/Mobile/Voice Banking

Extended Choice in FunctionalityCustomer MgmtProduct MgmtDeposits & Cheques (all types)Third-Party PaymentsStanding OrdersLoans (all types)Credit Agreements/LimitsCollateralsForeign ExchangeBack-Office TreasuryFunds Transfer & SWIFT PaymentsGeneral LedgerTeller / Branch SupportUser Security & Electronic Auth/tionsParametersParametric Interface GeneratorManagement Information ReportingLetters of GuaranteeLetters of Credit / Trade Finance

NEXT GENERATION CORE BANKING – SECURE INVESTMENT FOR FUTURE GROWTH

AlertsLoansDepositsFXFT

DBMSDBMSHost Host

PROFITS® SubsystemsPROFITSPROFITS®® SubsystemsSubsystems

www.intrasoft-intl.com

PROFITS Fundamental Concepts White Paper - Core Banking Systems Dept.

6/14 v1.00

any core banking system or third party application but also to be able to accommodate the interface of the core banking system to any other alternative delivery channel. This architecture enables the system to be completely independent of the core banking system in use and serve as the gateway to this core banking system for all alternative delivery channels. i-PROFITS® provides very rich end user functionality supporting both private and corporate customers as well as powerful administration tools supporting all “mobile” transactions in a very secure manner.

The current and future business, functional and technical needs of a modern banking institution are fully covered from the above major functional and technical advantages of the PROFITS® Core Banking Information System utilizing the following main features:

Customer/Member Information System The customer/member profile and the overall financial relationship between the customer/member and the Credit Union or Bank are fully covered thus providing the capability to manage individually every customer/member or groups of customers/members and provide specific to their profile tailor made services and products.

Powerful Product Generation Engine PROFITS® offers the capability to the Banking organization to design banking products and product packages, by means of defining the desired characteristics and relating them to customers/members whereby these products are quickly available to the CU's clientele.

www.intrasoft-intl.com

PROFITS Fundamental Concepts White Paper - Core Banking Systems Dept.

7/14 v1.00

Modular Structure PROFITS® parametric and modular design allows for expansions and adaptations according to specific needs thus fully covering the current and future business needs of a Bank.

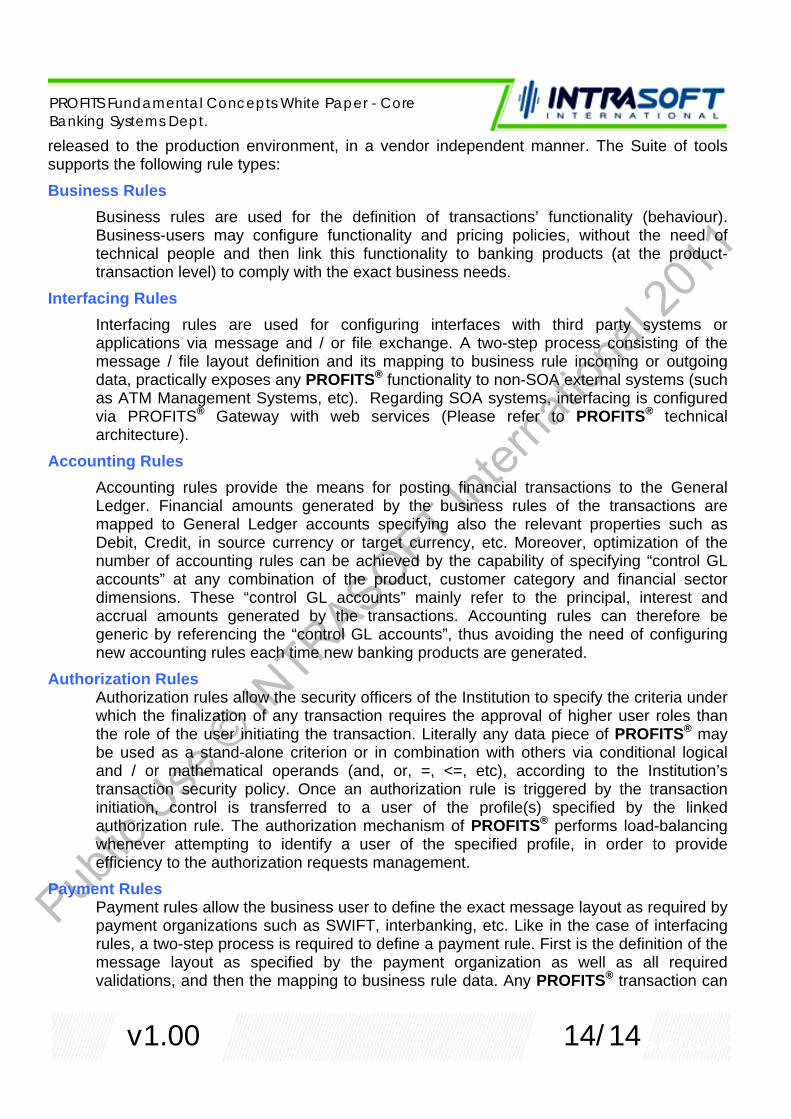

Business Rules Base Architecture PROFITS® is offered with the Rule definition Suite of tools that provides the organization with the highest possible degree of agility, since functionality may be configured, simulated and then released to the production environment, in a vendor independent manner. The Suite of tools supports the following rule types:

• Business Rules

• Interfacing Rules

• Accounting Rules

• Authorization Rules

• Payment Rules

• Statement Rules

• Reporting Rules In conclusion, PROFITS® rule-base architecture allows functionality definition without coding, since the rules can be configured by the organization itself. The main advantages of PROFITS® rule-based architecture are the drastic decrease in development and testing effort, the enhanced vendor independency, system manageability and maintainability. In addition, flexibility in functional changes is appreciated by PROFITS® customers by functionality being transparent to a larger group of users, including non-technical personnel.

Portability The System can be deployed in a variety of technology platforms and architectures. The System can be deployed either on a J2EE or .Net architecture. In addition, it can be deployed in a client-server architecture (with graphical or web enabled client) running on Mainframe environment with CICS and DB2 or on any flavor of UNIX or Win 2003 Server with Oracle, also being able to fully incorporate TUXEDO.

Integrated Internet Banking, Phone / Mobile Banking System i-PROFITS® Internet Banking, Phone / Mobile Banking System is fully integrated with PROFITS®. The Technical Architecture of i-PROFITS® is based upon cutting edge technologies, and provides for high availability (built in Load Balancing and Fail over) with minimal configuration efforts. Transactions via i-PROFITS® are performed in a very secured manner since security is handled by SSL protocol and OTP electronic pin generator and PKIs, as well as by other well established authentications methods and standards. In addition, the architecture provides for vertical and horizontal scalability so that the Bank can accommodate not only future transactions’ high volumes but can also easily introduce additional functionality.

www.intrasoft-intl.com

PROFITS Fundamental Concepts White Paper - Core Banking Systems Dept.

8/14 v1.00

Built-in Interfacing Capabilities Interfacing rules provided by the Rule definition Suite of tools are used for configuring interfaces with third party systems or applications via message and / or file exchange. A two-step process consisting of the message / file layout definition and its mapping to business rule incoming or outgoing data, practically exposes any PROFITS® functionality to non-SOA compliant external systems (such as ATM Management Systems, etc). Regarding SOA compliant systems, interfacing is configured via PROFITS® Gateway with Web services

www.intrasoft-intl.com

PROFITS Fundamental Concepts White Paper - Core Banking Systems Dept.

9/14 v1.00

3 Products Generation Engine The business growth of all modern, financial institutions is directly dependent upon their flexibility in changing according to the market needs, as well as their quick response to new products and services that are introduced to the market. One of the most critical design assumptions that were taken into account during PROFITS® development is the ability of the system to incorporate new banking products by defining independent parametric characteristics, which are further synthesized to produce a new type of customer service. The powerful Products Generation Engine provides the capability of fast creation of new products and services, which meet the ever changing needs of the market. Products can be promoted individually or as product packages. Additionally, the Product Management Subsystem of PROFITS® offers the capability to the Bank to design banking products, by means of defining the desired characteristics and relating them to transactions whereby these products are available to the customers. A “Product” is defined as a type of Account or a type of Service, accompanied by all the rules / features that determine its behavior (e.g. pricing, distribution, book-keeping). The highly parameterized Product Management mechanism provides:

◊ Administration of Product Distribution Rules. ◊ Administration of Products Restrictions / Permissions in terms of Interests, Customer

Types, Currencies, Units, Subsidies (only for Loan Products), other (parametrically defined product restrictions/permissions on a system parameter)

◊ Administration of allowable operations. Each operation is denoted by means of a “triplet”: Product-Transaction-Justification. “Transaction” is any operation available in PROFITS®. “Justification” is a flexibly definable variation of a Transaction, used to further differentiate the behavior of PROFITS® within a given “Product-Transaction” combination.

◊ Pricing characteristics: • Availability Days, Value Days, Interest Rates, Commissions, Expenses,

Penalties, Taxes. • Parametric definition of transactions pricing characteristics. • Interest Rates are linked to the Product itself. All other pricing characteristics

are linked to the triplet “Product-Transaction-Justification”.

◊ Pricing characteristics maintenance: • Floating or Fixed Interest Rates connected to Base Rates. • Interest Rates (flat, scaled, tiered). • Flat (Single-Valued) commissions, charges, taxes and penalties. • Scaled commissions, charges, taxes and penalties. • Tiered commissions, charges, taxes and penalties.

www.intrasoft-intl.com

PROFITS Fundamental Concepts White Paper - Core Banking Systems Dept.

10/14 v1.00

• Min and Max limits on commissions, charges, taxes. • Charges per item. • Interest Calculation Rules (periodical accrual and posting of Debit and Credit

Interest). Interest is calculated according to mid-period balances or according to daily value-dated balances, or according to initial balances, separately for credit and debit

• balances. For Tiered Interest Rates, the rate is selected from the steps of the tier either according to the average balance of the calculation period, or according to the value-dated balance; rates can also be selected with the balances taken in segments according to the steps of the tier. Different base of interest calculation (360 or 365) is supported. When applicable, interest capitalization and on-line real time interest calculation are also supported.

• Dynamic definition of interest scales based upon base rates (for example EURIBOR).

◊ Special Agreements' limits (Special Agreements are modifications to standard pricing

for special Customers, Products or Transactions).

◊ Accounting Rules for linking Products with General Ledger. • The subsystem supports parametric definition of rules, for the automatic

conversion of financial transactions into General Ledger movements based on G.L. rules. One accounting rule is specified in one or more “Product-Transaction-Justification” combination. The rule contains all the required General Ledger movements and their generation rules (including General Ledger Account, General Ledger Justification and Type of movement) for each one of the amounts included in a given transaction.

• Capability of differentiating the General Ledger Control Accounts per duration of Time Deposit.

• Capability of differentiating the General Ledger Control Accounts per Economic Sector and/or Customer Category.

The Product Management Subsystem provides flexibility regarding the functional behavior of all financial transactions of PROFITS®, utilizing PROFITS® Business Rules: A few of the strong points of the Business Rules are as follows:

◊ The ability to calculate commission, tax, expense and penalties by the system based on any algorithm, on any amount and in any currency dynamically.

◊ Unlimited pricing characteristics per transaction ◊ The ability to update tables on the database dynamically and based upon any

information available in the system. ◊ The ability to define what is to be printed and in which position to be printed on the

Financial Advice (voucher). ◊ The ability to define which amounts created by the system is to be included in the

General Ledger entries.

www.intrasoft-intl.com

PROFITS Fundamental Concepts White Paper - Core Banking Systems Dept.

11/14 v1.00

Product Packages The system also supports the functionality of combining different products to a product package. Each package may consist of many different products of any type, and the selected products are such that can be combined to fit the needs of specific customer groups. The package is available under conditions defined by business rules. For example, the business rule that is associated with the package may specify that the package is available only during the Christmas holidays and only to students. Furthermore, a package can be connected to a specific customer group only (e.g. for the employees of a specific company or for the members of a club, etc). The products involved in a package may be mandatory for the specific package or optional, or proposed by the System under conditions. That is, a package consisting of 3 products (A, B and C) can be configured so that product A is obligatory, B is optional and C to be proposed to the customer under conditions which are in this case, defined by business rules. When a customer chooses to participate in this package, the system will open automatically an account for the required product A, the customer will be asked for product B. Product C, will be automatically proposed by the System to the customer in dependent upon met requirements (conditions) (e.g. for students, the reported family income must exceed a specific figure, the customer should not have more than x overdue installments, etc). The products that can be used in the above process are either internal - any of the products of PROFITS® - or external products processed and maintained by a 3rd party application or system. In each product involved in a package, a different pricing policy can be set in interest rates or fees and charges for specific transactions. The different pricing policy may apply either on percentages or on dates of availability and interest amount computation. In the customers' subsystem, there is a maintenance screen through which, the user can monitor and maintain the packages that a customer has enrolled along with the accounts of these product packages. From this screen, it is possible to insert customer's accounts of external products (e.g. credit card accounts). Finally, the user may produce a printout of the screen's information.

www.intrasoft-intl.com

PROFITS Fundamental Concepts White Paper - Core Banking Systems Dept.

12/14 v1.00

4 Customer – Member management The Customer/Member Management Subsystem provides full coverage of the standard information needs concerning Customer activity by means of the following functions: ◊ Administration of Customer details, Companies, Individuals and Correspondents (e.g.

Name, Address, National ID/Passport, Marital Info, Nationality, Citizenship, Customer Origination Source, Financial Sector, Occupation, Language, Tax Office, Other Static Data, etc.).

◊ Automated generation and maintenance of unique, system-wide and bank-wide Customer identification code, in order to ensure centralization of customer data and the uniform linking of Customer with relevant Accounts (as beneficiary, co-beneficiary, guarantor), Agreements and Service Contracts.

◊ Presentation of the Customer global Position and Profitability from all Accounts and Services, Collaterals, Agreements etc.

◊ Statistical Analysis of Customer’s Profitability. ◊ Maintenance of Customer Signatures (digitized image). ◊ Maintenance of the responsible officer and branch for every customer and for every

account. ◊ Administration of associations between Customers (e.g. family relationship, business

relationship, employment relationship). Association types are defined parametrically. ◊ Capability to define Customer Groups according to the association between them. Groups

are defined parametrically. Examples of Groups: Holding Company and its members, Company and its owners.

◊ Maintenance of Customer Special Agreements (special treatment for specific customers in terms of the various standard pricing features of the relevant Products, e.g. Commissions, Charges, Penalties).

◊ Availability of Customer Activity data regarding the co-operation between the Customer and the Bank.

◊ Utilization of PROFITS® parameters in order to characterize Customers (e.g. Occupation, Economic Sector, etc.).

◊ Automated queries and reports for searching Customers (e.g. alphabetical, by Customer Code, by Account Code).

◊ Customer status maintenance according to their co-operation level with the Bank. ◊ User defined Customer Categorization ◊ User Defined Customer Communication Language ◊ Queries and Reports, based on Customer, in order to retrieve and present the basic

information entities that characterize banking operations of the given Customer (Account, Agreement, Transaction, and Collateral).

◊ Monitoring of various pending issues of Customers regarding their co-operation with the Bank (by means of maturity lists) provided by the operational subsystems of PROFITS®.

www.intrasoft-intl.com

PROFITS Fundamental Concepts White Paper - Core Banking Systems Dept.

13/14 v1.00

5 Configurable Services – Business Rules Based Architecture

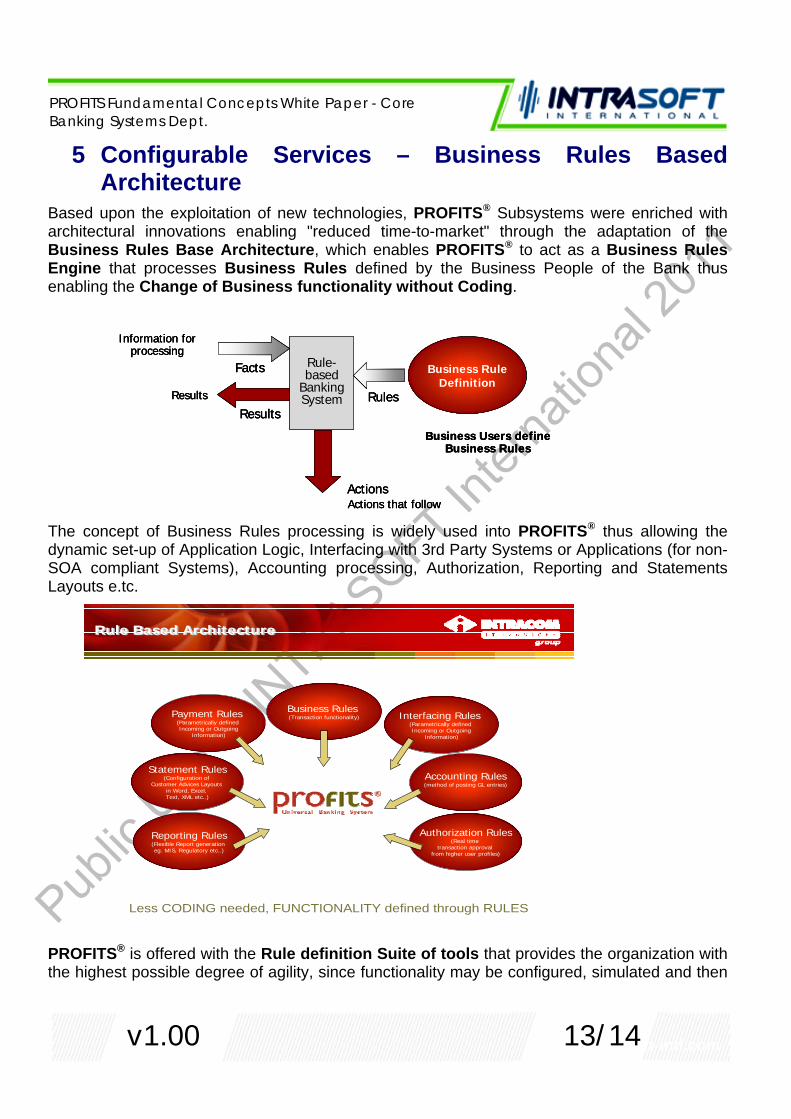

Based upon the exploitation of new technologies, PROFITS® Subsystems were enriched with architectural innovations enabling "reduced time-to-market" through the adaptation of the Business Rules Base Architecture, which enables PROFITS® to act as a Business Rules Engine that processes Business Rules defined by the Business People of the Bank thus enabling the Change of Business functionality without Coding.

The concept of Business Rules processing is widely used into PROFITS® thus allowing the dynamic set-up of Application Logic, Interfacing with 3rd Party Systems or Applications (for non-SOA compliant Systems), Accounting processing, Authorization, Reporting and Statements Layouts e.tc.

PROFITS® is offered with the Rule definition Suite of tools that provides the organization with the highest possible degree of agility, since functionality may be configured, simulated and then

Rule-based

Banking System

Information for processing

Facts

Results

Actions that follow

Results

Actions

Rules

Business Users define Business Rules

Business RuleDefinition

Rule-based

Banking System

Information for processing

Facts

Information for processing

Facts

Results

Actions that follow

Results

Actions

Results

Actions that follow

Results

Actions

RulesRules

Business Users define Business Rules

Business RuleDefinition

Business Users define Business Rules

Business RuleDefinition

Rule Based ArchitectureRule Based Architecture

Authorization Rules(Real time

transaction approval from higher user profiles)

Accounting Rules(method of posting GL entries)

Business Rules (Transaction functionality)

Statement Rules(Configuration of

Customer Advices Layouts in Word, Excel, Text, XML etc..)

Reporting Rules(Flexible Report generation eg. MIS, Regulatory etc..)

Interfacing Rules (Parametrically defined Incoming or Outgoing

Information)

Payment Rules (Parametrically defined Incoming or Outgoing

Information)

Less CODING needed, FUNCTIONALITY defined through RULES

www.intrasoft-intl.com

PROFITS Fundamental Concepts White Paper - Core Banking Systems Dept.

14/14 v1.00

released to the production environment, in a vendor independent manner. The Suite of tools supports the following rule types: Business Rules

Business rules are used for the definition of transactions’ functionality (behaviour). Business-users may configure functionality and pricing policies, without the need of technical people and then link this functionality to banking products (at the product-transaction level) to comply with the exact business needs.

Interfacing Rules Interfacing rules are used for configuring interfaces with third party systems or applications via message and / or file exchange. A two-step process consisting of the message / file layout definition and its mapping to business rule incoming or outgoing data, practically exposes any PROFITS® functionality to non-SOA external systems (such as ATM Management Systems, etc). Regarding SOA systems, interfacing is configured via PROFITS® Gateway with web services (Please refer to PROFITS® technical architecture).

Accounting Rules Accounting rules provide the means for posting financial transactions to the General Ledger. Financial amounts generated by the business rules of the transactions are mapped to General Ledger accounts specifying also the relevant properties such as Debit, Credit, in source currency or target currency, etc. Moreover, optimization of the number of accounting rules can be achieved by the capability of specifying “control GL accounts” at any combination of the product, customer category and financial sector dimensions. These “control GL accounts” mainly refer to the principal, interest and accrual amounts generated by the transactions. Accounting rules can therefore be generic by referencing the “control GL accounts”, thus avoiding the need of configuring new accounting rules each time new banking products are generated.

Authorization Rules Authorization rules allow the security officers of the Institution to specify the criteria under which the finalization of any transaction requires the approval of higher user roles than the role of the user initiating the transaction. Literally any data piece of PROFITS® may be used as a stand-alone criterion or in combination with others via conditional logical and / or mathematical operands (and, or, =, <=, etc), according to the Institution’s transaction security policy. Once an authorization rule is triggered by the transaction initiation, control is transferred to a user of the profile(s) specified by the linked authorization rule. The authorization mechanism of PROFITS® performs load-balancing whenever attempting to identify a user of the specified profile, in order to provide efficiency to the authorization requests management.

Payment Rules Payment rules allow the business user to define the exact message layout as required by payment organizations such as SWIFT, interbanking, etc. Like in the case of interfacing rules, a two-step process is required to define a payment rule. First is the definition of the message layout as specified by the payment organization as well as all required validations, and then the mapping to business rule data. Any PROFITS® transaction can

www.intrasoft-intl.com

PROFITS Fundamental Concepts White Paper - Core Banking Systems Dept.

15/14 v1.00

be configured to produce a payment file or message according to the payment rule linked to the product-transaction combination.

Statement Rules Statement rules allow the organization to define the layout of the on-line advices produced by the transactions. The printable outcome of any transaction can be configured to be in any file format (e.g. text, MS-Word, XML, PDF, etc.). This capability enhances the external and external image of the organization since specific print-outs per transaction can be configured.

Reporting Rules Reporting rules allow the technical users of the organization to establish any database inquiry and the link the outcome to specific coordinates of excel files in order to meet any management information or regulatory reporting requirement. Once the report definition has been stored in PROFITS® Reporting Rules repository, it can be accessed by the authorized users in order to produce the necessary reports based on user-defined selection criteria.

In conclusion, PROFITS® rule-base architecture allows functionality definition without coding, since the rules can be configured by the organization itself. The main advantages of PROFITS® rule-based architecture are the drastic decrease in development and testing effort, the enhanced vendor independency, system manageability and maintainability. A smoother upgrade procedure of the software is resulting, due to the organization’s ability to differentiate using the same System. Flexibility in functional changes is appreciated by PROFITS® customers by functionality being transparent to a larger group of users, including non-technical personnel.