Embed Size (px)

Citation preview

8/6/2019 IFRS 8 Guide

http://slidepdf.com/reader/full/ifrs-8-guide 1/36

A practical guide to

segment reportingSeptember 2008

8/6/2019 IFRS 8 Guide

http://slidepdf.com/reader/full/ifrs-8-guide 2/36

IFRS technical publications

Adopting IFRS – A step-by-step illustration ofthe transition to IFRS

Illustrates the steps involved in preparing the firstIFRS financial statements. It takes into account theeffect on IFRS 1 of the standards issued up to andincluding March 2004.

Financial instruments under IFRSHigh-level summary of the revised financialinstruments standards issued in December 2003,updated to reflect IFRS 7 in September 2006. Forexisting IFRS preparers and first-time adopters.

Financial Reporting in HyperinflationaryEconomies – Understanding IAS 292006 update (reflecting impact of IFRIC 7) of aguide for entities applying IAS 29. Provides an

overview of the standard’s concepts, descriptionsof the procedures and an illustrative example of itsapplication.

IFRS 3R: Impact on earnings –the crucial Q&A for decision-makersGuide aimed at finance directors, financialcontrollers and deal-makers, providing backgroundto the standard, impact on the financial statementsand controls, and summary differences withUS GAAP.

Illustrative Consolidated Financial Statements

• Banking, 2006• Corporate, 2008

• Insurance, 2006

• Investment funds, 2006• Investment property, 2006

Realistic sets of financial statements – for existingIFRS preparers in the above sectors – illustrating therequired disclosure and presentation.

Share-based Payment –a practical guide to applying IFRS 2 Assesses the impact of the new standard, looking atthe requirements and providing a step-by-stepillustration of how to account for share-basedpayment transactions.

Similarities and Differences –a comparison of IFRS and US GAAPPresents the key similarities and differencesbetween IFRS and US GAAP, focusing on thedifferences commonly found in practice. It takes intoaccount all standards published up to August 2007.

SIC-12 and FIN 46R – The Substance of Control

Helps those working with special purpose entities toidentify the differences between US GAAP and IFRSin this area, including examples of transactions andstructures that may be impacted by the guidance.

IFRS Pocket Guide 2008Provides a summary of the IFRS recognition andmeasurement requirements. Including currencies,assets, liabilities, equity, income, expenses,business combinations and interim financialstatements.

IAS 39 – Achieving hedge accounting in practiceCovers in detail the practical issues in achievinghedge accounting under IAS 39. It provides answersto frequently asked questions and step-by-stepillustrations of how to apply common hedgingstrategies.

Illustrative interim financial informationfor existing preparersIllustrative information, prepared in accordance withIAS 34, for a fictional existing IFRS preparer.Includes a disclosure checklist and IAS 34application guidance. Reflects standards issued upto 31 March 2008.

IFRS NewsMonthly newsletter focusing on the businessimplications of the IASB’s proposals and newstandards.

IFRS for SMEs (proposals) – Pocket Guide 2007Provides a summary of the recognition andmeasurement requirements in the proposed ‘IFRSfor Small and Medium-Sized Entities’ published bythe International Accounting Standards Board inFebruary 2007.

PricewaterhouseCoopers’ IFRS and corporate governance publications and tools 2008

IFRS Manual of Accounting 2008Provides expert practical guidance on howgroups should prepare their consolidatedfinancial statements in accordance with IFRS.Comprehensive publication including hundredsof worked examples, extracts from companyreports and model financial statements.

Understanding financial instruments – A guide to IAS 32, IAS 39 and IFRS 7Comprehensive guidance on all aspects of therequirements for financial instruments accounting.Detailed explanations illustrated through workedexamples and extracts from company reports.

Disclosure Checklist 2007Outlines the disclosures required by all IFRSspublished up to September 2006.

A practical guide to segment reportingProvides an overview of the key requirements ofIFRS 8, ‘Operating Segments’ and some points toconsider as entities prepare for the application ofthis standard for the first time. Includes a questionand answer section.

2 | PricewaterhouseCoopers – A practical guide to segment reporting

8/6/2019 IFRS 8 Guide

http://slidepdf.com/reader/full/ifrs-8-guide 3/36PricewaterhouseCoopers – A practical guide to segment reporting | 3

Page

Introduction 4

Key implementation issues 5

Key dierences between IFRS 8 and IAS 14 6

What to do on rst-time adoption o IFRS 8 7

IFRS 8 at a glance 8

Questions and answers 12

1. Identiying operating segments 14

2. Aggregating and reporting segments 19

3. Segment disclosures 27

4. Other matters or consideration 33

Contents

8/6/2019 IFRS 8 Guide

http://slidepdf.com/reader/full/ifrs-8-guide 4/364 | PricewaterhouseCoopers – A practical guide to segment reporting

IFRS 8 (‘the standard’) aligns the identication and reporting o operating segments withinternal management reporting. Segment reporting under IFRS 8 should highlight the

inormation and measures that management believes are important and are used to make

key decisions. It should also provide a better link between the nancial statements and the

inormation reported in management commentaries such as the Operating and Financial

Review or Management Discussion and Analysis. The standard converges IFRS with US

Accounting Standard SFAS 131 ‘Disclosure about Segments o an Enterprise and Related

Inormation’.

This publication explains the key requirements o the standard and some practical issues or

entities to consider when it is applied or the rst time.

Introduction

8/6/2019 IFRS 8 Guide

http://slidepdf.com/reader/full/ifrs-8-guide 5/36PricewaterhouseCoopers – A practical guide to segment reporting | 5

Key implementation issues

The International Accounting Standards Board issued IFRS 8, ‘Operating segments’ inNovember 2006. The standard replaces IAS 14, ‘Segment reporting’. It applies to annual

reporting periods beginning on or ater 1 January 2009. Early adoption is permitted.

The key implementation issues are as ollows:

n The IASB did not intend to change the range o entities required to present segment

inormation, but we believe IFRS 8 has a wider scope than IAS 14. It applies to

entities whose equity or debt securities are publicly traded or that issue, or

are in the process o issuing, any class o instrument in a public market. The

scope also includes entities that le nancial statements with a regulatory

organisation or purpose o issuing any instruments in a public market. We believe

this means that some entities whose equity and debt securities are not traded

publicly and were not within the scope o IAS 14 will have to provide segmentdisclosures.

n The standard introduces a ‘management approach’ to identiying and measuring

the nancial perormance o an entity’s operating segments. Reported segment

inormation will be based on the inormation used internally by management. This

means that:

n the way entities identiy segments and measure and present segment inormation

could change;

n there will be more diversity in reported segment inormation;

n segment inormation may not be measured in accordance with IFRS – entities are

required to reconcile segment nancial inormation to the consolidated nancial

statements; and

n entities will no longer need to prepare two sets o inormation or internal andexternal reporting.

n Reportable segments are no longer limited to those that earn a majority o revenue

rom sales to external parties, so entities may now be required to report the dierent

stages o vertically integrated operations as separate segments.

Practical experience

IFRS 8 aligns segment reporting under IFRS with the requirements o the equivalent US

standard SFAS 131. IFRS 8 adopts the requirements o the US standard almost in its entirety.

Insight

Experience rom PwC in the US shows that:

Identiying the chie operating decision maker (CODM) can be dicult. Judgements•

about the components o an entity that are regularly reviewed by the CODM have

been challenging and subject to regulatory scrutiny.

The regulator has challenged companies about the identication o operating•

segments and the appropriateness o aggregating operating segments.

Companies subject to Sarbanes-Oxley Section 404 requirements may incur•

additional costs in ensuring that internal processes and systems are sucientlyrobust in capturing internal segment inormation.

8/6/2019 IFRS 8 Guide

http://slidepdf.com/reader/full/ifrs-8-guide 6/366 | PricewaterhouseCoopers – A practical guide to segment reporting

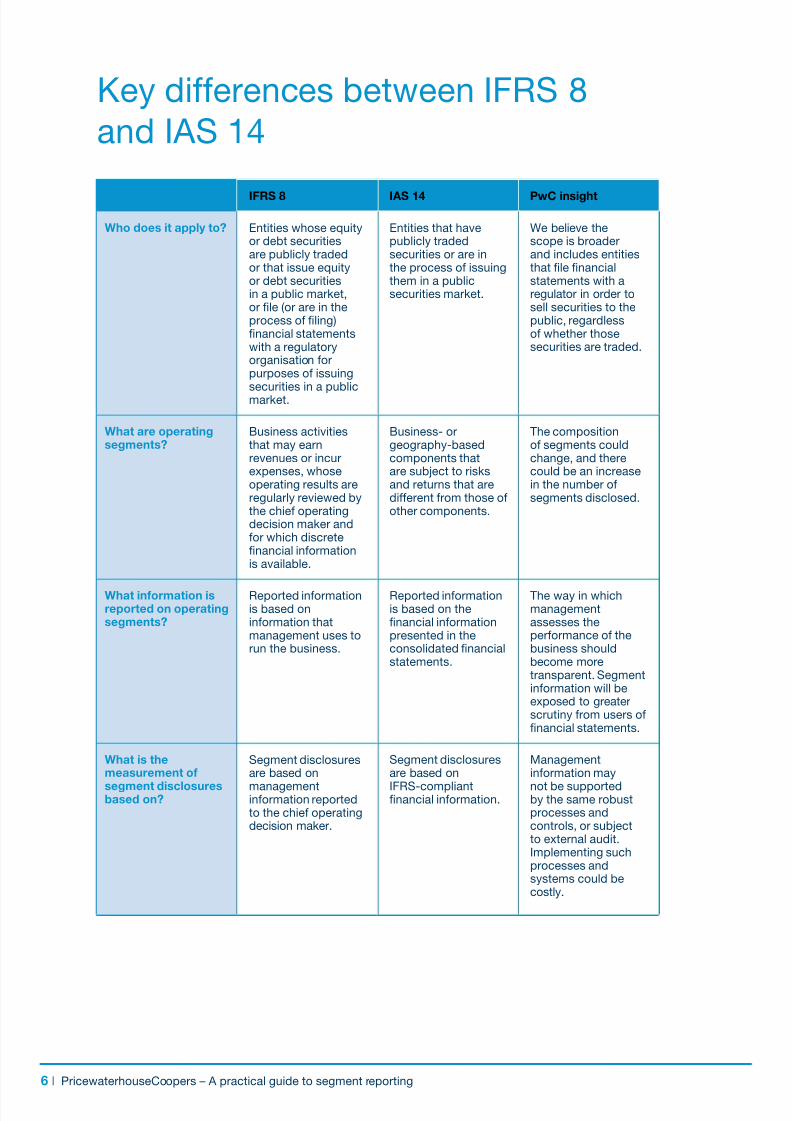

Key dierences between IFRS 8

and IAS 14

IFRS 8 IAS 14 PwC insight

Who does it apply to? Entities whose equityor debt securitiesare publicly tradedor that issue equityor debt securitiesin a public market,or le (or are in theprocess o ling)nancial statementswith a regulatoryorganisation orpurposes o issuing

securities in a publicmarket.

Entities that havepublicly tradedsecurities or are inthe process o issuingthem in a publicsecurities market.

We believe thescope is broaderand includes entitiesthat le nancialstatements with aregulator in order tosell securities to thepublic, regardlesso whether thosesecurities are traded.

What are operatingsegments?

Business activitiesthat may earnrevenues or incurexpenses, whoseoperating results areregularly reviewed bythe chie operatingdecision maker andor which discretenancial inormationis available.

Business- orgeography-basedcomponents thatare subject to risksand returns that aredierent rom those oother components.

The compositiono segments couldchange, and therecould be an increasein the number osegments disclosed.

What inormation isreported on operatingsegments?

Reported inormationis based oninormation thatmanagement uses torun the business.

Reported inormationis based on thenancial inormationpresented in theconsolidated nancialstatements.

The way in whichmanagementassesses theperormance o thebusiness shouldbecome moretransparent. Segmentinormation will beexposed to greaterscrutiny rom users onancial statements.

What is themeasurement o

segment disclosuresbased on?

Segment disclosuresare based on

managementinormation reportedto the chie operatingdecision maker.

Segment disclosuresare based on

IFRS-compliantnancial inormation.

Managementinormation may

not be supportedby the same robustprocesses andcontrols, or subjectto external audit.Implementing suchprocesses andsystems could becostly.

8/6/2019 IFRS 8 Guide

http://slidepdf.com/reader/full/ifrs-8-guide 7/36PricewaterhouseCoopers – A practical guide to segment reporting | 7

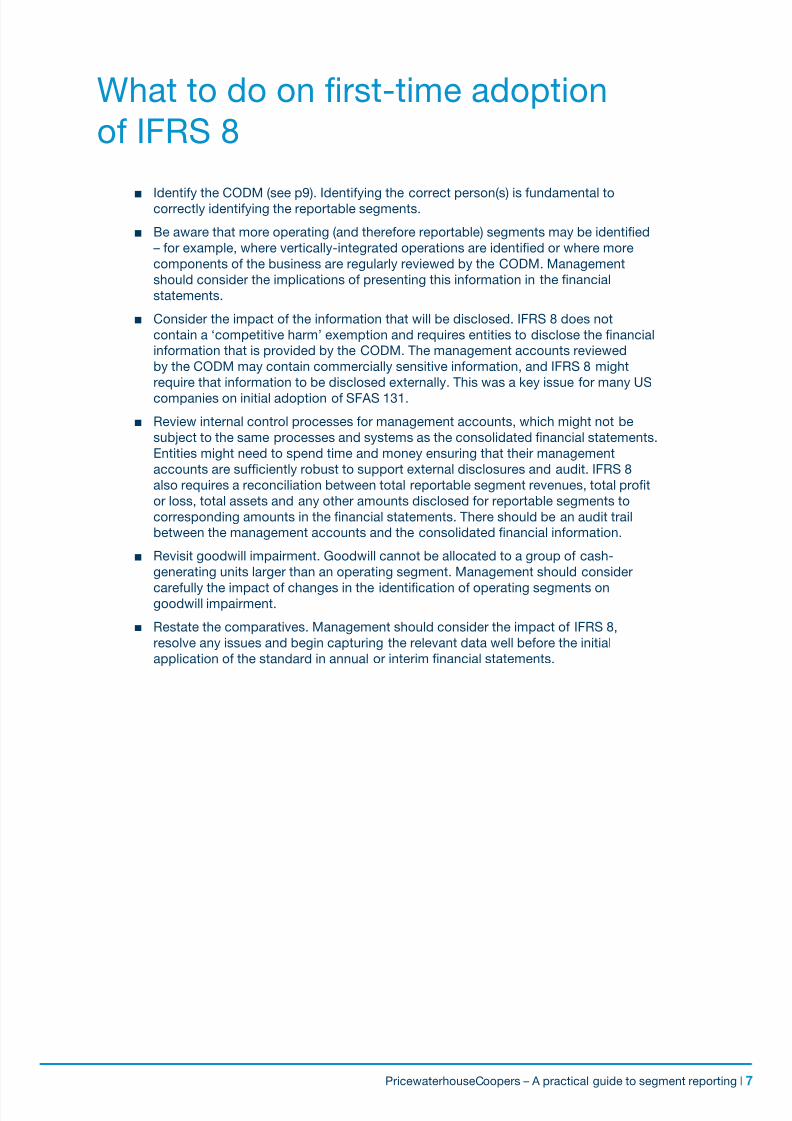

What to do on rst-time adoption

o IFRS 8

n Identiy the CODM (see p9). Identiying the correct person(s) is undamental tocorrectly identiying the reportable segments.

n Be aware that more operating (and thereore reportable) segments may be identied

– or example, where vertically-integrated operations are identied or where more

components o the business are regularly reviewed by the CODM. Management

should consider the implications o presenting this inormation in the nancial

statements.

n Consider the impact o the inormation that will be disclosed. IFRS 8 does not

contain a ‘competitive harm’ exemption and requires entities to disclose the nancial

inormation that is provided by the CODM. The management accounts reviewed

by the CODM may contain commercially sensitive inormation, and IFRS 8 might

require that inormation to be disclosed externally. This was a key issue or many US

companies on initial adoption o SFAS 131.

n Review internal control processes or management accounts, which might not be

subject to the same processes and systems as the consolidated nancial statements.

Entities might need to spend time and money ensuring that their management

accounts are suciently robust to support external disclosures and audit. IFRS 8

also requires a reconciliation between total reportable segment revenues, total prot

or loss, total assets and any other amounts disclosed or reportable segments to

corresponding amounts in the nancial statements. There should be an audit trail

between the management accounts and the consolidated nancial inormation.

n Revisit goodwill impairment. Goodwill cannot be allocated to a group o cash-

generating units larger than an operating segment. Management should consider

careully the impact o changes in the identication o operating segments ongoodwill impairment.

n Restate the comparatives. Management should consider the impact o IFRS 8,

resolve any issues and begin capturing the relevant data well beore the initial

application o the standard in annual or interim nancial statements.

8/6/2019 IFRS 8 Guide

http://slidepdf.com/reader/full/ifrs-8-guide 8/368 | PricewaterhouseCoopers – A practical guide to segment reporting

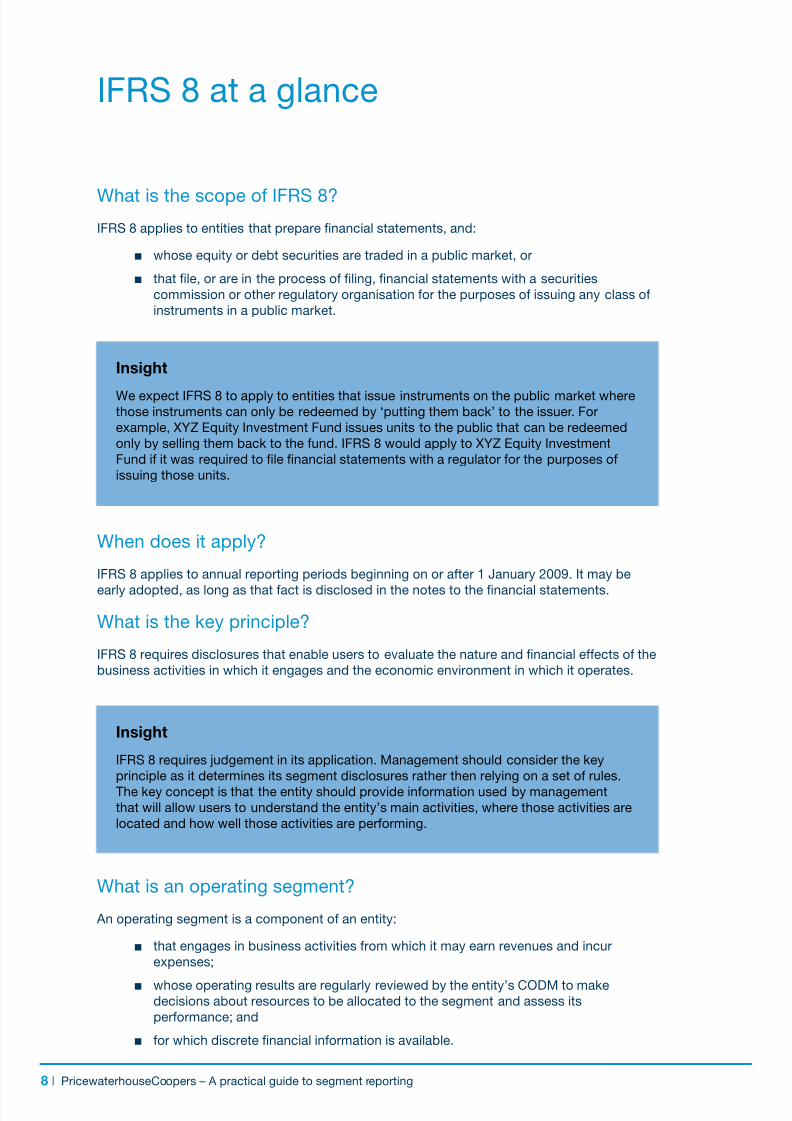

IFRS 8 at a glance

What is the scope o IFRS 8?

IFRS 8 applies to entities that prepare nancial statements, and:

n whose equity or debt securities are traded in a public market, or

n that le, or are in the process o ling, nancial statements with a securities

commission or other regulatory organisation or the purposes o issuing any class o

instruments in a public market.

Insight

We expect IFRS 8 to apply to entities that issue instruments on the public market wherethose instruments can only be redeemed by ‘putting them back’ to the issuer. For

example, XYZ Equity Investment Fund issues units to the public that can be redeemed

only by selling them back to the und. IFRS 8 would apply to XYZ Equity Investment

Fund i it was required to le nancial statements with a regulator or the purposes o

issuing those units.

When does it apply?

IFRS 8 applies to annual reporting periods beginning on or ater 1 January 2009. It may be

early adopted, as long as that act is disclosed in the notes to the nancial statements.

What is the key principle?

IFRS 8 requires disclosures that enable users to evaluate the nature and nancial eects o the

business activities in which it engages and the economic environment in which it operates.

Insight

IFRS 8 requires judgement in its application. Management should consider the key

principle as it determines its segment disclosures rather then relying on a set o rules.

The key concept is that the entity should provide inormation used by management

that will allow users to understand the entity’s main activities, where those activities are

located and how well those activities are perorming.

What is an operating segment?

An operating segment is a component o an entity:

n that engages in business activities rom which it may earn revenues and incur

expenses;

n whose operating results are regularly reviewed by the entity’s CODM to makedecisions about resources to be allocated to the segment and assess its

perormance; and

n or which discrete nancial inormation is available.

8/6/2019 IFRS 8 Guide

http://slidepdf.com/reader/full/ifrs-8-guide 9/36PricewaterhouseCoopers – A practical guide to segment reporting | 9

How are operating segments identied?

There are our key steps. Entities will need to:

1 Identiy the CODM.

2 Identiy their business activities (which may not necessarily earn revenue or incur

expenses).

3 Determine whether discrete nancial inormation is available or the business activities.

4 Determine whether that inormation is regularly reviewed by the CODM.

Insight

Identiying the CODM and the components that are regularly reviewed by the CODM

to make decisions can be dicult. It is also important to reassess regularly the

identication o the CODM, particularly ollowing a business reorganisation, acquisition

or disposal.

What or who is a chie operating decision maker?

The CODM is a unction and not necessarily a person. That unction is to allocate resources to,

and assess the perormance o, the operating segments. It is likely to vary rom entity to entity

– it may be the CEO, the chie operating ocer, the senior management team or the board o

directors. The title or titles o the person(s) identied as CODM is not relevant, as long as it is

the person(s) responsible or making strategic decisions about the entity’s segments.

See the ‘Questions and answers’ section or some o the practical implications identiying an

entity’s operating segments.

How do I determine an entity’s reportable segments?

Not all operating segments need to be separately reported. Operating segments are only

required to be reportable i they exceed quantitative thresholds.

Quantitative thresholds (IFRS 8 para 13)

Inormation on an operating segment should be separately reported i:

n reported revenue (external and inter-segment) is 10% or more o the combined

revenue o all operating segments;

n the absolute amount o the segment’s reported prot or loss is 10% or more o the

greater o:

n the combined reported prot o all operating segments that did not report a

loss, and

n the combined loss o all operating segments that reported a loss;

n the segment’s assets are 10% or more o the combined assets o all operating

segments.

Two or more operating segments may be combined (aggregated) and reported as one i certain

conditions are satised.

8/6/2019 IFRS 8 Guide

http://slidepdf.com/reader/full/ifrs-8-guide 10/3610 | PricewaterhouseCoopers – A practical guide to segment reporting

Aggregation o operating segments (IFRS 8 para 12)

Two or more operating segments may be combined as a single reportable segment i:

n aggregation provides nancial statement users with inormation that allows them to

evaluate the business and the environment in which it operates;

n they have similar economic characteristics; and

n they are similar in each o the ollowing respects:

n the nature o the products and services,

n the nature o the production processes,

n the type or class o customer or their products and services,

n the methods used to distribute their products or provide their services, and

n the nature o the regulatory environment (ie, banking, insurance or public

utilities), i applicable.

Minimum number o reportable segments

Ater determining the reportable segments, the entity should ensure that the total external

revenue attributable to those reportable segments is at least 75% o the entity’s total revenue.

When the 75% threshold is not met, additional reportable segments should be identied (even

i they do not meet the 10% thresholds), until at least 75% o the entity’s total external revenue

is included in its reportable segments.

The sections ‘Aggregating and reporting segments’ on p19 and ‘Segment disclosures’ on p27

address some o the practical implications o determining reportable segments.

8/6/2019 IFRS 8 Guide

http://slidepdf.com/reader/full/ifrs-8-guide 11/36PricewaterhouseCoopers – A practical guide to segment reporting | 11

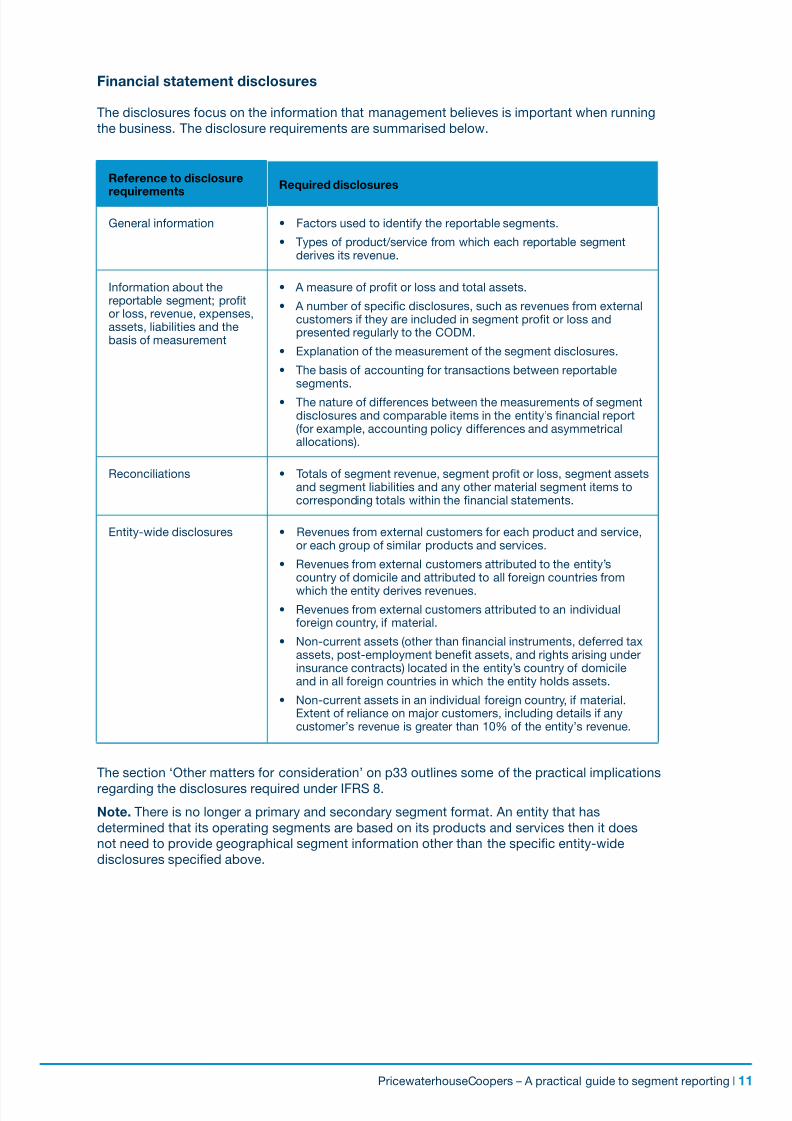

Financial statement disclosures

The disclosures ocus on the inormation that management believes is important when running

the business. The disclosure requirements are summarised below.

Reerence to disclosure

requirements

Required disclosures

General inormation Factors used to identiy the reportable segments.•

Types o product/service rom which each reportable segment•derives its revenue.

Inormation about thereportable segment; protor loss, revenue, expenses,assets, liabilities and thebasis o measurement

A measure o prot or loss and total assets.•

A number o specic disclosures, such as revenues rom external•customers i they are included in segment prot or loss andpresented regularly to the CODM.

Explanation o the measurement o the segment disclosures.•

The basis o accounting or transactions between reportable•segments.

The nature o dierences between the measurements o segment•disclosures and comparable items in the entity’s nancial report(or example, accounting policy dierences and asymmetricalallocations).

Reconciliations Totals o segment revenue, segment prot or loss, segment assets•and segment liabilities and any other material segment items tocorresponding totals within the nancial statements.

Entity-wide disclosures Revenues rom external customers or each product and service,•or each group o similar products and services.

Revenues rom external customers attributed to the entity’s•country o domicile and attributed to all oreign countries rom

which the entity derives revenues.

Revenues rom external customers attributed to an individual•oreign country, i material.

Non-current assets (other than nancial instruments, deerred tax•assets, post-employment benet assets, and rights arising underinsurance contracts) located in the entity’s country o domicileand in all oreign countries in which the entity holds assets.

Non-current assets in an individual oreign country, i material.•Extent o reliance on major customers, including details i anycustomer’s revenue is greater than 10% o the entity’s revenue.

The section ‘Other matters or consideration’ on p33 outlines some o the practical implications

regarding the disclosures required under IFRS 8.

Note. There is no longer a primary and secondary segment ormat. An entity that has

determined that its operating segments are based on its products and services then it does

not need to provide geographical segment inormation other than the specic entity-wide

disclosures specied above.

8/6/2019 IFRS 8 Guide

http://slidepdf.com/reader/full/ifrs-8-guide 12/3612 | PricewaterhouseCoopers – A practical guide to segment reporting

Questions and answers

1. Identiying operating segments

1.1 Can the CODM be a group o individuals?

1.2 Is the CODM always viewed as the highest level o management at which decisions are

made?

1.3 Can a head oce unction be an operating segment?

1.4 Does a component meet the denition o a segment i the CODM reviews revenue-only

inormation?

1.5 Is a segment balance sheet necessary to conclude that discrete nancial inormation is

available?

1.6 Can vertically integrated operations and cost centres that do not earn revenues beclassied as an operating segment?

1.7 Can a research and development unction be an operating segment?

1.8 Can a discontinued operation be an operating segment?

1.9 Are activities conducted through proportionally consolidated joint ventures or associates

considered under the denition o operating segment?

1.10 A CODM may receive multiple levels o inormation. How are operating segments

determined?

1.11 An entity is structured in a matrix style, where the CODM reviews two overlapping sets o

nancial inormation. How are the operating segments determined?

2. Aggregating and reporting segments

2.1 I operating segments are based on geography rather than products or services, can

they still be aggregated?

2.2 Can a company aggregate start-up businesses with mature businesses?

2.3 Can two similar operating segments be combined despite having dierent long-term

average gross margins?

2.4 How should an entity perorm the 10% test when each o its operating segments reports

dierent measures o segment protability and segment assets?

2.5 How should an entity identiy its operating segments under IFRS 8 para 13 (b) when ithas both prot- and loss-making segments?

2.6 Can inormation about non-reportable operating segments be combined and disclosed

in an ‘all other’ category, together with items that reconcile the segment inormation to

the statutory inormation?

2.7 Can a company aggregate an ‘immaterial non-reportable’ segment with a reportable

segment, even though the aggregation criteria under IFRS 8 para 12 have not been met?

2.8 When applying the 75% test under IFRS 8 para 15, should the next largest operating

segment always be selected?

8/6/2019 IFRS 8 Guide

http://slidepdf.com/reader/full/ifrs-8-guide 13/36PricewaterhouseCoopers – A practical guide to segment reporting | 13

3. Segment disclosures

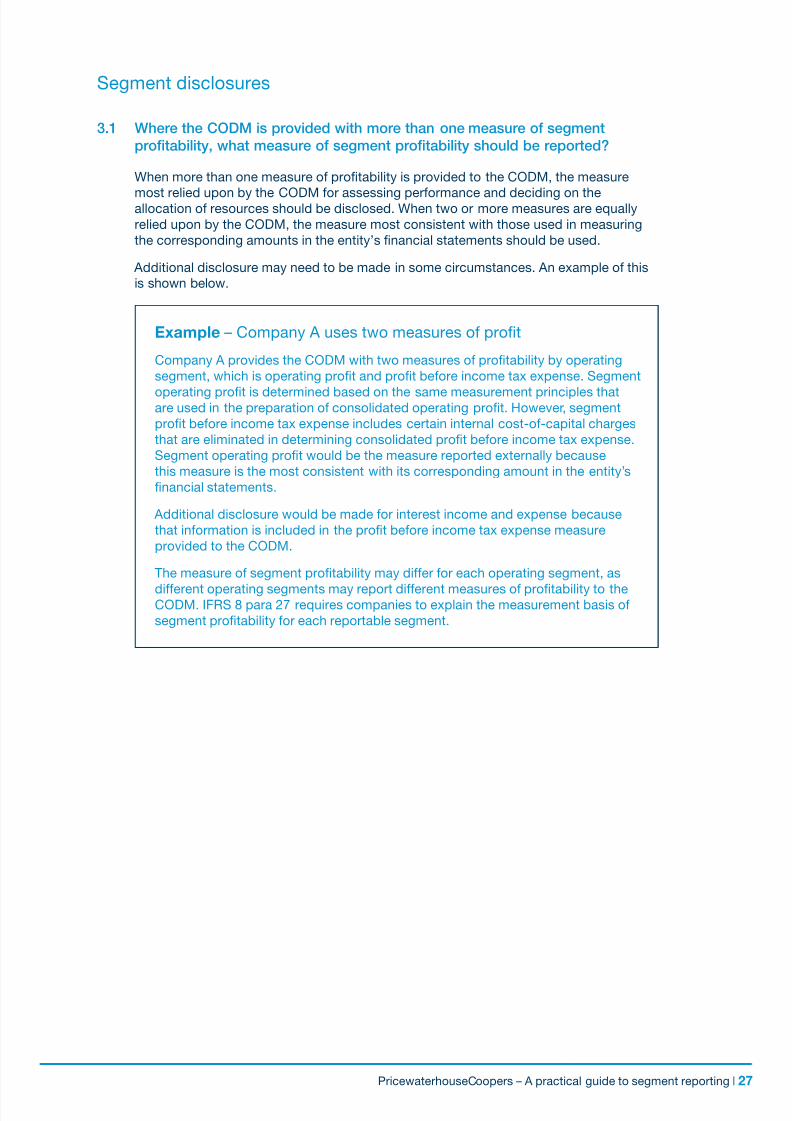

3.1 Where the CODM is provided with more than one measure o segment protability, what

measure o segment protability should be reported?

3.2 What measure should be reported when the asset inormation reported to the CODM is

limited or not reviewed at all?

3.3 Should the measures o prot or loss and assets and liabilities presented or each

operating segment comply with the IFRS accounting policies used in the consolidated

nancial statements?

3.4 Where the CODM only receives inormation with respect to the entity’s cash fows (that

is, the CODM receives no prot or asset inormation), what should that entity disclose in

its segmental disclosure?

3.5 When should an entity consider and review its segment reporting?

3.6 Is restatement o segment inormation required when a reorganisation causes the

composition o reportable segments to change?

3.7 Is restatement o segment inormation required when there is change in the measure o

segment prot or loss?

3.8 What is the denition o ‘material’ where an entity is required to disclose separately

material revenues and material non-current assets rom an individual oreign country?

4. Other matters or consideration

4.1 The impact o IFRS 8 on accounting or impairment o assets

4.2 Segment reporting in the separate company statements o subsidiaries

4.3 Convergence with US standard SFAS 131

4.4 What’s in the pipeline?

8/6/2019 IFRS 8 Guide

http://slidepdf.com/reader/full/ifrs-8-guide 14/3614 | PricewaterhouseCoopers – A practical guide to segment reporting

Identiying operating segments

1.1 Can the chie operating decision maker be a group o individuals?

Yes. The CODM may be an individual or a group o individuals.

Insight

A business activity usually has a unit manager who is directly accountable to, and

maintains regular contact with, an individual or group o individuals to discuss

operating activities, nancial results, orecasts, or plans or the business activity.

The CODM is that individual or group o individuals that is responsible or the

allocation o resources and assessing the perormance o the entity’s business

units.

1.2 Is the CODM always viewed as the highest level o management at whichdecisions are made?

Typically, yes. In almost every organisation, decisions about the entity’s resource

allocation and the assessment o the perormance o the entity’s businesses are made at

the highest level o management.

Insight

Judgement is required. The CODM will vary rom entity to entity and it may be the

chie executive ocer, chie operating ocer, senior management team or in some

jurisdictions, the board o directors. We believe that a supervisory board unction

that simply approves management’s decisions would not be the CODM, as it doesnot allocate resources.

1.3 Can a head oce unction be an operating segment?

Yes. A head oce unction that undertakes business activities (or example, a treasury

operation that earns interest income and incurs expenses) may be an operating segment

as long as its revenues earned are more than incidental to the activities o the entity, and

discrete nancial inormation is reviewed by the CODM.

A head oce unction (such as accounting, inormation technology, human resources

and internal audit) that earns revenue that is purely incidental to the entity’s activities

is not an operating segment and not part o one o the reportable segments. Such

unctions should be reported in the reconciliation o the segment totals as ‘other

reconciling items’.

8/6/2019 IFRS 8 Guide

http://slidepdf.com/reader/full/ifrs-8-guide 15/36PricewaterhouseCoopers – A practical guide to segment reporting | 15

Example – Incidental revenues

Examples o incidental revenues include interest income and expenses, realised

and unrealised oreign exchange gains and losses, and the net eect o pension

schemes.

1.4 Does a component meet the denition o a segment i the CODM reviews

revenue-only inormation?

In most cases, no. For most entities, the review o revenue-only data is not sucient or

decision-making related to resource allocation or perormance evaluation o a segment.

Insight

Only in rare cases where product sales or service provisions involve minimal costs

is the revenue-only data representative o the results. The review o the revenue-

only data by the CODM may be sucient in these rare cases to conclude that the

business activity alls within the denition o an operating segment.

1.5 Is a segment balance sheet necessary to conclude that discrete nancial

inormation is available?

No. We believe that in many cases the requirement or discrete nancial inormation can

be met with operating perormance inormation only, such as revenue and gross prot by

product line.

1.6 Can vertically integrated operations and cost centres that earn no revenues

be classied as an operating segment?

Yes. IFRS 8 denes an operating segment as a ‘component o an entity that engages

in business activities rom which it may earn revenues and incur expenses’. This

recognises that not all business activities earn revenues.

Example – Cost centres as a separate segment

Manuacturing entities that are managed by reerence to operating cost centres,

may not record cost centre revenues because the entity’s total customer revenuesare not allocated to each cost centre. Care should be exercised when determining

whether an internally reported activity constitutes an operating segment (see

question 1.3 or more inormation). As long as discrete nancial inormation is

prepared and reviewed by the CODM such components would be considered

operating segments.

Example – Vertically integrated operation

Where transer prices are charged between an entity’s stages o production (or

example, with oil and gas companies), the act that the transer prices are not

assessed by the CODM would not exempt such activities rom being considered

operating segments. The operating segments o an oil and gas company may

include exploration, development, production, rening and marketing – i theCODM manages the entity in this way.

8/6/2019 IFRS 8 Guide

http://slidepdf.com/reader/full/ifrs-8-guide 16/3616 | PricewaterhouseCoopers – A practical guide to segment reporting

1.8 Can a discontinued operation be an operating segment?

Yes. A discontinued operation can meet the denition o an operating segment i:

n it continues to engage in business activities;

n the operating results are regularly reviewed by the CODM; and

n discrete nancial inormation is available to acilitate the review.

1.7 Can a research and development unction be an operating segment?

Yes, as long as discrete inormation is reviewed by the CODM. Typically, an entity’s

research and development (R&D) unction is a vertically integrated operation (see

question 1.6), in which the R&D activities serve as an integral component o the entity’s

business. The denition o operating segment envisages that part o an entity that earns

revenue and incurs expenses relating to transactions with other components o the same

entity may still qualiy as an operating segment even i all o its revenue and expensesderive rom intra-group transactions.

Insight

Where entities allocate entity-wide R&D costs into the business activities or

which the R&D is specically being perormed, the R&D unction will be a separate

operating segment as long as the CODM separately reviews discrete R&D activity

and data. It will not be separate segment i the CODM does not review discrete

nancial data or the criteria.

Example – Insurance company disposing o its workers’

compensation business An insurance company discontinues its ‘workers’ compensation’ line o business.

The discontinuation meets the criteria or ‘discontinued operations’ under

IFRS 5, ‘Non-current assets held or sale and discontinued operations’. For

internal purposes, separate nancial results are maintained or this business,

and they are reviewed by the CODM until the discontinuance is complete. The

operation is still being managed by the CODM and would continue to meet the

denition o an operating segment.

Conversely, i the CODM no longer reviews discrete nancial inormation on the

discontinuing operation, it would no longer all within the denition o an operating

segment. For example, a urniture manuacturing plant shuts down its operations

in Asia. The plant is no longer producing inventory and it has been reclassied

under IFRS 5 as ‘assets held or sale’. Discrete nancial inormation is no longer

reported. As a result, it would not be considered an operating segment.

Note. Disclosures would still be presented in accordance with IFRS 5.

1.9 Are activities conducted through proportionally consolidated joint ventures or

associates considered under the denition o operating segment?

We believe that where (1) a company manages its joint-venture operations or associates

separately and (2) the criteria or identiying operating segments in (a)-(c) o IFRS 8 para5 are met, the joint-venture operations qualiy as an operating segment. The asset and

prot/loss inormation (reported to the CODM) regarding the joint-venture or

8/6/2019 IFRS 8 Guide

http://slidepdf.com/reader/full/ifrs-8-guide 17/36PricewaterhouseCoopers – A practical guide to segment reporting | 17

associate’s activities that comprise the segment are thereore disclosed. The external

reporting o the joint-venture activities may be on a proportionate consolidation basis or

a ull consolidation basis. I the ull nancial results are reviewed by the CODM, the total

o all segments’ nancial amounts should be reconciled to the corresponding amounts

reported in the consolidated nancial statements, so appropriate eliminations should be

refected in the reconciling column or amounts reported in excess o those amounts

refected in the consolidated nancial statements. For example, an associate revenue

inormation is not included in the revenue amount reported in the consolidated nancialstatements. An elimination o the revenue amount disclosed or the associate should be

refected as a reconciling item.

1.10 A CODM may receive multiple levels o inormation. How are operating

segments determined?

IFRS 8 para 8 states that the ollowing actors should be considered when an entity is

determining the set o components that constitutes its operating segments:

n The nature o business activities o each component. To the extent that the higher-

level segment inormation is represented by components that contain dissimilar

business activities, while the lower level components contain similar businessactivities, the lower level components may be more representative o the company’s

operating segments.

n The existence o managers responsible or each component. It is likely that those

components that have individuals responsible or the components’ results

(such as a segment manager, business-unit CFO, or vice president) and who are

directly accountable to, and maintain regular contact with, the CODM to discuss

operating activities, nancial results, orecasts, or plans or the segment, are an

entity’s operating segments. Segment managers may be responsible or more

than one operating segment. IFRS 8 para 9 states that generally, i there is only one

set o components or which segment managers are held responsible, that set o

components constitutes the operating segments.

n The inormation provided to the board o directors. The inormation provided to the

company’s board o directors, when not considered to be the CODM, may indicate

the level at which (1) overall perormance is assessed and (2) decisions are made

about resource allocation to dierent areas o an entity’s business.

We believe entities should consider qualitative actors in addition to those outlined above

in determining the appropriate operating segments. These should include an assessment

o whether the resultant operating segments are consistent with the core principle o

IFRS 8 and whether the identied operating segments could realistically represent the

level at which the CODM is assessing perormance and allocating resources. We would

also expect the identied operating segments to be consistent with other inormation

the entity produces, such as press releases, interviews with management, company

websites, management discussions and other public inormation about the entity.

Insight

In the US, this has been an area o the standard that has required signicant

judgement. It is also an area where several entities have been challenged by the

regulator.

8/6/2019 IFRS 8 Guide

http://slidepdf.com/reader/full/ifrs-8-guide 18/3618 | PricewaterhouseCoopers – A practical guide to segment reporting

1.11 An entity is structured in a matrix style, where the CODM reviews two

overlapping sets o nancial inormation. How are the operating segments

determined?

IFRS 8 para 10 addresses the issue o matrix structures. It uses the example o an entity

where some managers are responsible or product and service lines worldwide, whereas

other managers are responsible or specic geographical areas.

The CODM reviews the operating results o both sets o components, and discrete

nancial inormation is available or both. In this situation, the entity should determine

which set o components constitutes the operating segments, taking account o what

users o the nancial statements would need to know in order to evaluate the entity’s

business activities and the environment it operates in.

Insight

Matrix-structured entities use judgement to determine their operating segments.

Such entities should consider the importance o the actors that have led to

the matrix structure. For example, i an entity’s priority is to increase total

sales, market share and geographic spread, the most relevant inormationor shareholders would be based on geographic markets. An entity that aims

to improve the sales o individual products, with a CODM that believes that

improving and maintaining product quality is the key to achieving this, might

conclude that the most relevant inormation or shareholders would be based on

products.

This approach would be acceptable under IFRS 8 i:

• theentitycansufcientlysupportthebasisforhowitdetermineditssegments;

and

• theentity’sbasisfordeterminingsegmentsenablesusersofitsnancial

statements to evaluate its activities and nancial perormance, and thebusiness environment it operates in.

8/6/2019 IFRS 8 Guide

http://slidepdf.com/reader/full/ifrs-8-guide 19/36PricewaterhouseCoopers – A practical guide to segment reporting | 19

Aggregating and reporting segments

2.1 I operating segments are based on geography rather than products or

services, can they still be aggregated?

Yes, as long as the individual country segments have similar economic characteristics

and are similar in each o the other areas set out in IFRS 8 para 12.

Insight

The requirement or segments to have similar economic characteristics may

be dicult to overcome when combining individual countries. This is because

the individual countries need to have similar economic conditions, exchange

control regulations and underlying currency or them to have similar economic

characteristics.

Even when aggregation o geographic segments is permitted, IFRS 8 para 33

requires the separate disclosure o revenues and assets or each material oreign

country. This disclosure allows users o the nancial statements to assess thedependence o the entity on customers based in one particular country.

Example – A retail chain opens new stores

A retail chain has mature businesses (store locations) in ve major cities in a given

country. In the current year, the retail chain opens additional stores in those cities.

Each store constitutes a separate operating segment, as the CODM o the retail

chain reviews nancial results and makes decisions on a store-by-store basis.

These ‘start-up’ stores may meet the economic characteristics requirement or

aggregation with mature stores i management determines that the uture long-

term nancial perormance o the stores is expected to be similar.

2.2 Can a company aggregate start-up businesses with mature businesses?

Yes. One o the objectives o requiring disclosures about segments is to help users

assess the uture prospects o an entity’s business. Segments with similar economic

characteristics oten exhibit similar long-term nancial perormance. To the extent that

the uture nancial perormance (including the competitive and operating risks) o the

start-up businesses is expected to be similar to that o a company’s mature businesses,

the economic characteristics requirement or aggregation might be satised.

8/6/2019 IFRS 8 Guide

http://slidepdf.com/reader/full/ifrs-8-guide 20/3620 | PricewaterhouseCoopers – A practical guide to segment reporting

2.3 Can two similar operating segments be combined despite having dierent

long-term average gross margins?

Yes. Management should consider all relevant actors to determine whether the

economic characteristics o its segments are similar.

IFRS 8 states that similar long-term average gross margins or two operating segments

are expected i their economic characteristics are similar. However, other perormance

actors such as trends in sales growth, returns on assets employed and operating

cash fow may also be considered by management to assess whether segments have

substantially similar economic characteristics.

Insight

When management reviews nancial perormance measures and compares

segments, it should consider not only the quantitative results, but also the

reasons why the results are similar or dissimilar beore reaching a conclusion

about whether the economic characteristics are similar/dissimilar. The basis

or conclusions states that, “separate reporting o segment inormation will not

add signicantly to an investor’s understanding o an enterprise i its operatingsegments have characteristics so similar that they can be expected to have

essentially the same uture prospects”. We consider these comments regarding

aggregation to be consistent with the core principle o IFRS 8. Entities should

ensure their acts and circumstances support aggregation.

Management should be aware that:

n An entity that cannot demonstrate ‘similar economic characteristics’ cannot rely on

the other criteria in IFRS 8 para 12 to aggregate operating segments. This is a high

hurdle.

n It is important to consider a variety o actors, such as trends in growth o theproducts, gross margins and management’s long-term expectations or the product

lines.

n Several years o both historical and uture nancial perormance should be

considered.

n Segment reporting should be consistent with other public inormation and

disclosures, such as websites and other nancial inormation presented outside o

the nancial statements.

n Management should document their conclusion that segments are

economically similar.

8/6/2019 IFRS 8 Guide

http://slidepdf.com/reader/full/ifrs-8-guide 21/36PricewaterhouseCoopers – A practical guide to segment reporting | 21

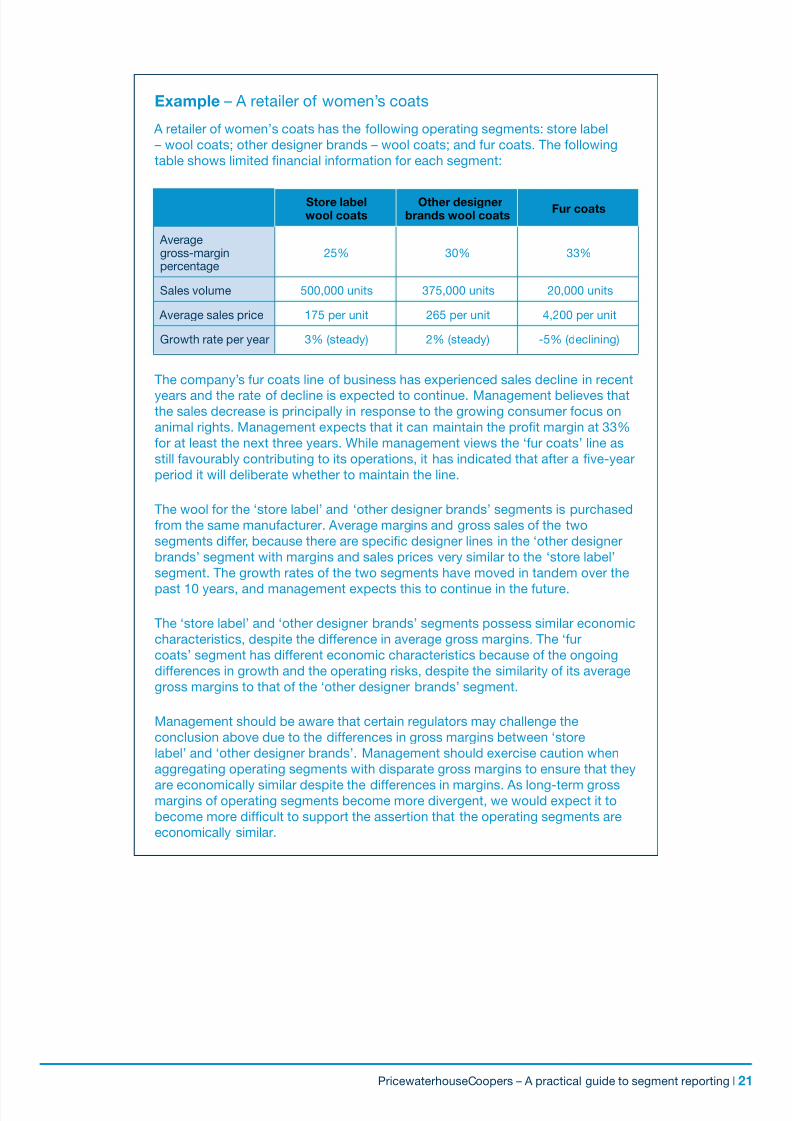

Example – A retailer o women’s coats

A retailer o women’s coats has the ollowing operating segments: store label

– wool coats; other designer brands – wool coats; and ur coats. The ollowing

table shows limited nancial inormation or each segment:

Store labelwool coats

“Other designer brands wool coats

Fur coats

Averagegross-marginpercentage

25% 30% 33%

Sales volume 500,000 units 375,000 units 20,000 units

Average sales price 175 per unit 265 per unit 4,200 per unit

Growth rate per year 3% (steady) 2% (steady) -5% (declining)

The company’s ur coats line o business has experienced sales decline in recent

years and the rate o decline is expected to continue. Management believes thatthe sales decrease is principally in response to the growing consumer ocus on

animal rights. Management expects that it can maintain the prot margin at 33%

or at least the next three years. While management views the ‘ur coats’ line as

still avourably contributing to its operations, it has indicated that ater a ve-year

period it will deliberate whether to maintain the line.

The wool or the ‘store label’ and ‘other designer brands’ segments is purchased

rom the same manuacturer. Average margins and gross sales o the two

segments dier, because there are specic designer lines in the ‘other designer

brands’ segment with margins and sales prices very similar to the ‘store label’

segment. The growth rates o the two segments have moved in tandem over the

past 10 years, and management expects this to continue in the uture.

The ‘store label’ and ‘other designer brands’ segments possess similar economic

characteristics, despite the dierence in average gross margins. The ‘ur

coats’ segment has dierent economic characteristics because o the ongoing

dierences in growth and the operating risks, despite the similarity o its average

gross margins to that o the ‘other designer brands’ segment.

Management should be aware that certain regulators may challenge the

conclusion above due to the dierences in gross margins between ‘store

label’ and ‘other designer brands’. Management should exercise caution when

aggregating operating segments with disparate gross margins to ensure that they

are economically similar despite the dierences in margins. As long-term grossmargins o operating segments become more divergent, we would expect it to

become more dicult to support the assertion that the operating segments are

economically similar.

8/6/2019 IFRS 8 Guide

http://slidepdf.com/reader/full/ifrs-8-guide 22/3622 | PricewaterhouseCoopers – A practical guide to segment reporting

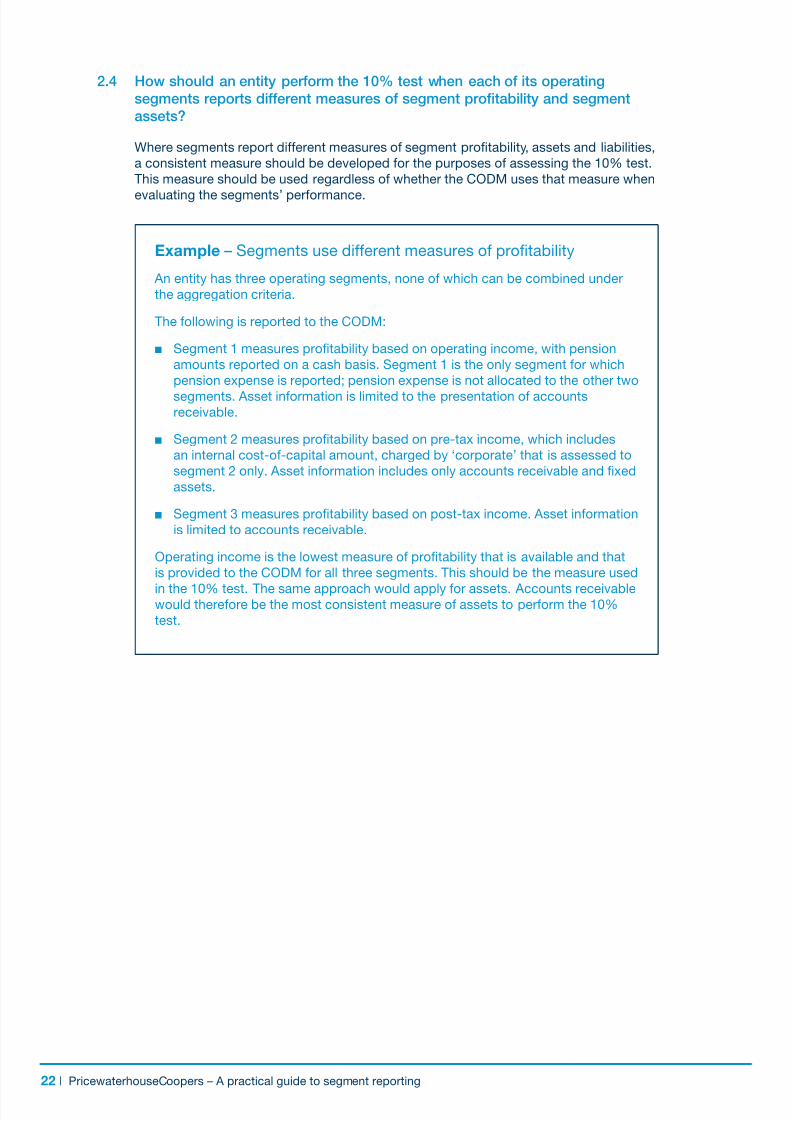

2.4 How should an entity perorm the 10% test when each o its operating

segments reports dierent measures o segment protability and segment

assets?

Where segments report dierent measures o segment protability, assets and liabilities,

a consistent measure should be developed or the purposes o assessing the 10% test.

This measure should be used regardless o whether the CODM uses that measure when

evaluating the segments’ perormance.

Example – Segments use dierent measures o protability

An entity has three operating segments, none o which can be combined under

the aggregation criteria.

The ollowing is reported to the CODM:

n Segment 1 measures protability based on operating income, with pension

amounts reported on a cash basis. Segment 1 is the only segment or which

pension expense is reported; pension expense is not allocated to the other two

segments. Asset inormation is limited to the presentation o accountsreceivable.

n Segment 2 measures protability based on pre-tax income, which includes

an internal cost-o-capital amount, charged by ‘corporate’ that is assessed to

segment 2 only. Asset inormation includes only accounts receivable and xed

assets.

n Segment 3 measures protability based on post-tax income. Asset inormation

is limited to accounts receivable.

Operating income is the lowest measure o protability that is available and that

is provided to the CODM or all three segments. This should be the measure used

in the 10% test. The same approach would apply or assets. Accounts receivablewould thereore be the most consistent measure o assets to perorm the 10%

test.

8/6/2019 IFRS 8 Guide

http://slidepdf.com/reader/full/ifrs-8-guide 23/36PricewaterhouseCoopers – A practical guide to segment reporting | 23

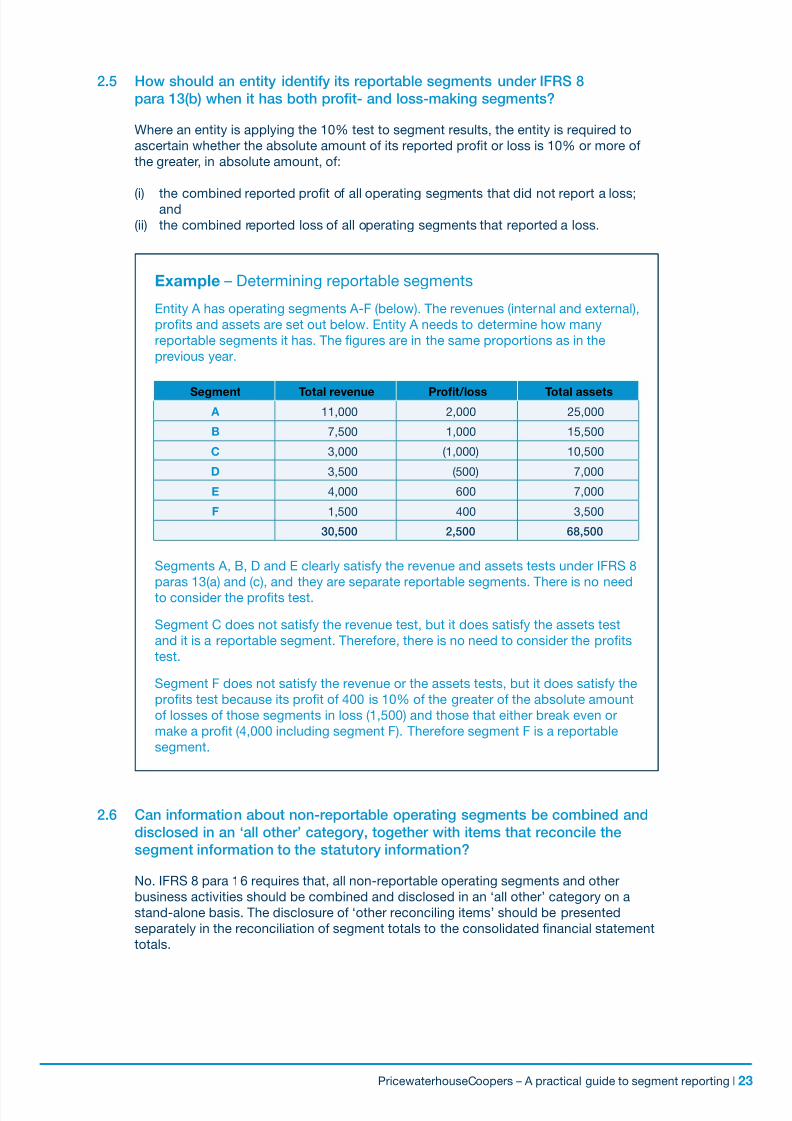

2.5 How should an entity identiy its reportable segments under IFRS 8

para 13(b) when it has both prot- and loss-making segments?

Where an entity is applying the 10% test to segment results, the entity is required to

ascertain whether the absolute amount o its reported prot or loss is 10% or more o

the greater, in absolute amount, o:

(i) the combined reported prot o all operating segments that did not report a loss;and

(ii) the combined reported loss o all operating segments that reported a loss.

Example – Determining reportable segments

Entity A has operating segments A-F (below). The revenues (internal and external),

prots and assets are set out below. Entity A needs to determine how many

reportable segments it has. The gures are in the same proportions as in the

previous year.

Segment Total revenue Proft/loss Total assets A 11,000 2,000 25,000

B 7,500 1,000 15,500

C 3,000 (1,000) 10,500

D 3,500 (500) 7,000

E 4,000 600 7,000

F 1,500 400 3,500

30,500 2,500 68,500

Segments A, B, D and E clearly satisy the revenue and assets tests under IFRS 8

paras 13(a) and (c), and they are separate reportable segments. There is no need

to consider the prots test.

Segment C does not satisy the revenue test, but it does satisy the assets test

and it is a reportable segment. Thereore, there is no need to consider the prots

test.

Segment F does not satisy the revenue or the assets tests, but it does satisy the

prots test because its prot o 400 is 10% o the greater o the absolute amount

o losses o those segments in loss (1,500) and those that either break even or

make a prot (4,000 including segment F). Thereore segment F is a reportable

segment.

2.6 Can inormation about non-reportable operating segments be combined and

disclosed in an ‘all other’ category, together with items that reconcile the

segment inormation to the statutory inormation?

No. IFRS 8 para 16 requires that, all non-reportable operating segments and other

business activities should be combined and disclosed in an ‘all other’ category on a

stand-alone basis. The disclosure o ‘other reconciling items’ should be presented

separately in the reconciliation o segment totals to the consolidated nancial statement

totals.

8/6/2019 IFRS 8 Guide

http://slidepdf.com/reader/full/ifrs-8-guide 24/3624 | PricewaterhouseCoopers – A practical guide to segment reporting

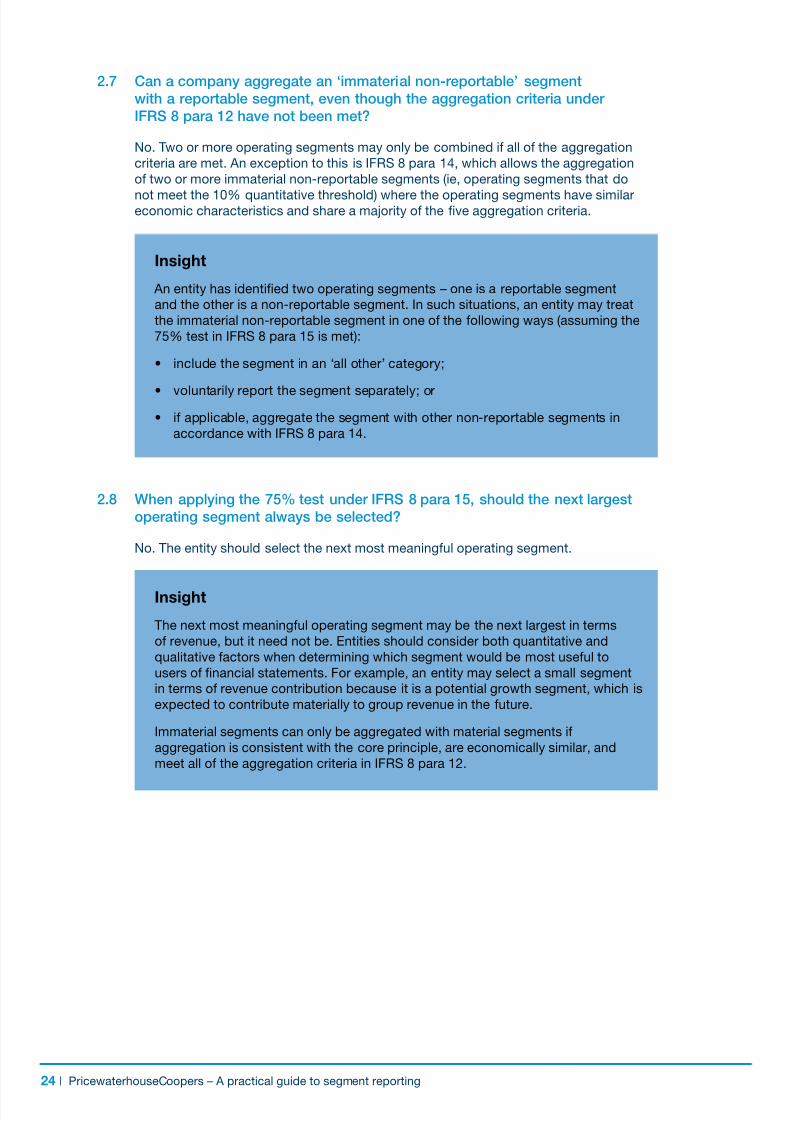

2.7 Can a company aggregate an ‘immaterial non-reportable’ segment

with a reportable segment, even though the aggregation criteria under

IFRS 8 para 12 have not been met?

No. Two or more operating segments may only be combined i all o the aggregation

criteria are met. An exception to this is IFRS 8 para 14, which allows the aggregation

o two or more immaterial non-reportable segments (ie, operating segments that do

not meet the 10% quantitative threshold) where the operating segments have similareconomic characteristics and share a majority o the ve aggregation criteria.

Insight

An entity has identied two operating segments – one is a reportable segment

and the other is a non-reportable segment. In such situations, an entity may treat

the immaterial non-reportable segment in one o the ollowing ways (assuming the

75% test in IFRS 8 para 15 is met):

• includethesegmentinan‘allother’category;

• voluntarilyreportthesegmentseparately;or

• ifapplicable,aggregatethesegmentwithothernon-reportablesegmentsin

accordance with IFRS 8 para 14.

2.8 When applying the 75% test under IFRS 8 para 15, should the next largest

operating segment always be selected?

No. The entity should select the next most meaningul operating segment.

Insight

The next most meaningul operating segment may be the next largest in terms

o revenue, but it need not be. Entities should consider both quantitative and

qualitative actors when determining which segment would be most useul to

users o nancial statements. For example, an entity may select a small segment

in terms o revenue contribution because it is a potential growth segment, which is

expected to contribute materially to group revenue in the uture.

Immaterial segments can only be aggregated with material segments i

aggregation is consistent with the core principle, are economically similar, and

meet all o the aggregation criteria in IFRS 8 para 12.

8/6/2019 IFRS 8 Guide

http://slidepdf.com/reader/full/ifrs-8-guide 25/36PricewaterhouseCoopers – A practical guide to segment reporting | 25

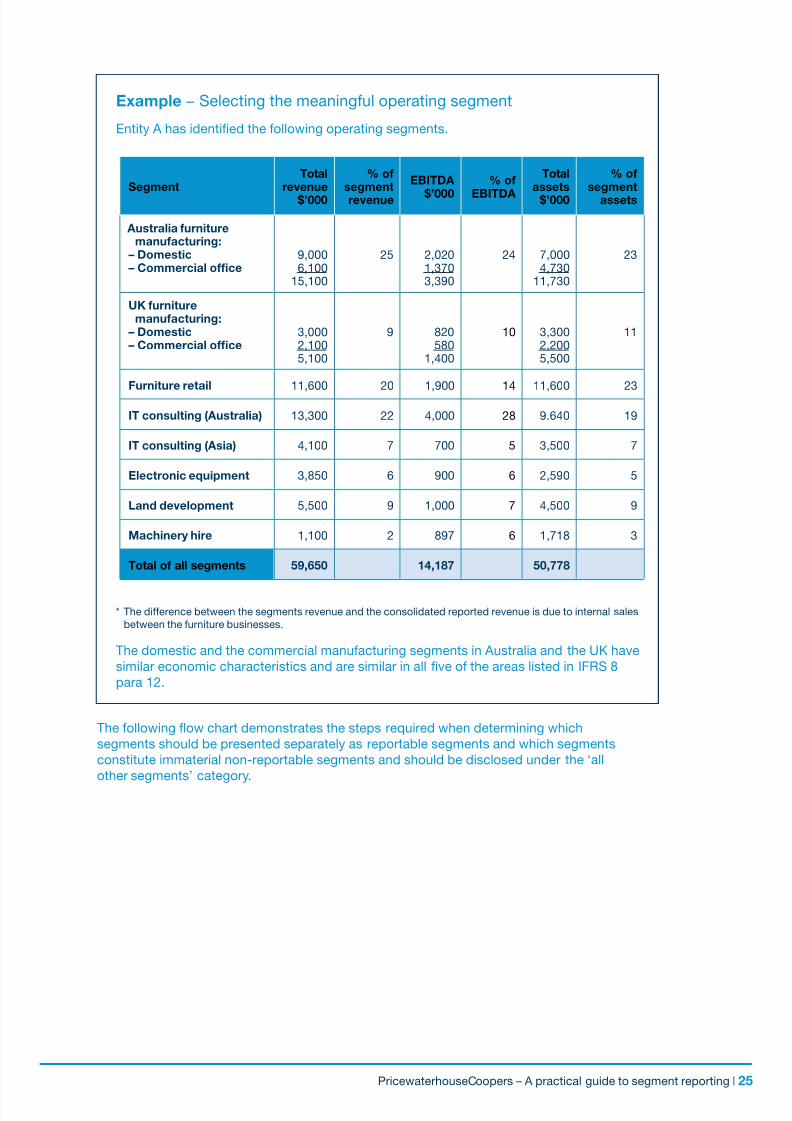

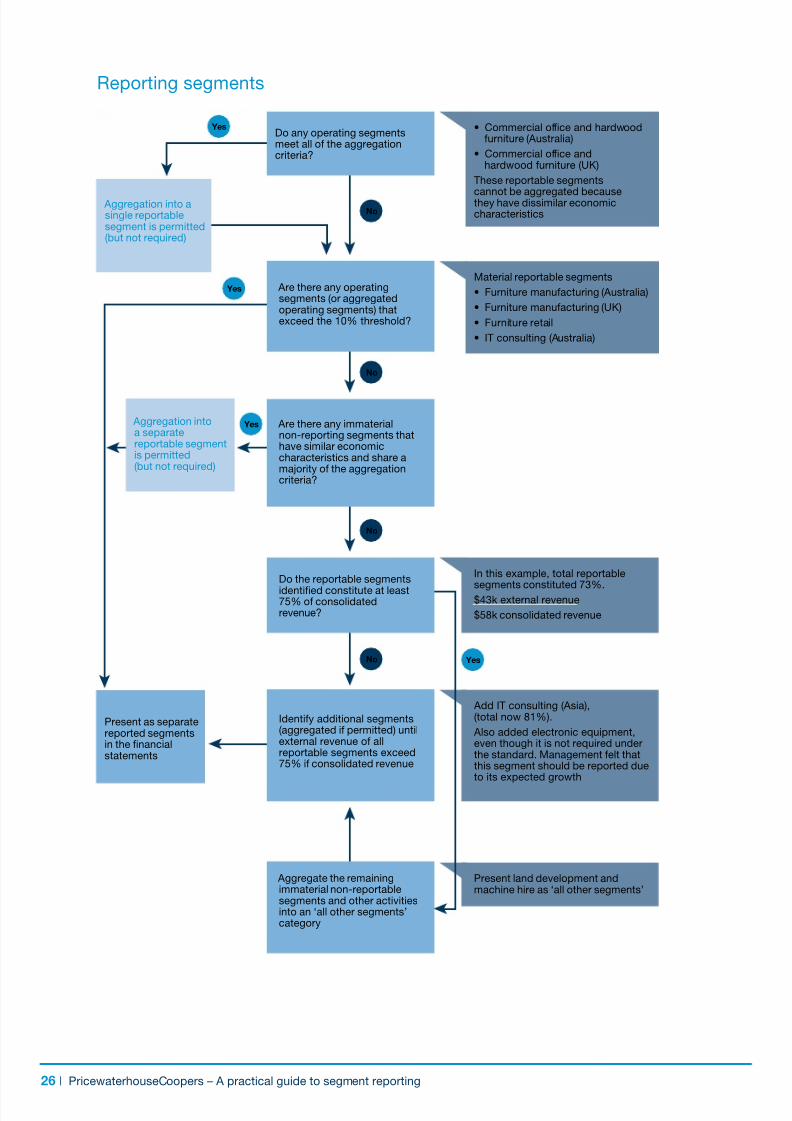

Example − Selecting the meaningul operating segment

Entity A has identied the ollowing operating segments.

SegmentTotal

revenue$’000

% osegmentrevenue

EBITDA

$’000

% o

EBITDA

Totalassets

$’000

% osegment

assets

Australia urnituremanuacturing:

– Domestic– Commercial ofce

9,0006,100

15,100

25 2,0201,3703,390

24 7,0004,730

11,730

23

UK urnituremanuacturing:

– Domestic– Commercial ofce

3,0002,1005,100

9 820580

1,400

10 3,3002,2005,500

11

Furniture retail 11,600 20 1,900 14 11,600 23

IT consulting (Australia) 13,300 22 4,000 28 9.640 19

IT consulting (Asia) 4,100 7 700 5 3,500 7

Electronic equipment 3,850 6 900 6 2,590 5

Land development 5,500 9 1,000 7 4,500 9

Machinery hire 1,100 2 897 6 1,718 3

Total o all segments 59,650 14,187 50,778

The ollowing fow chart demonstrates the steps required when determining which

segments should be presented separately as reportable segments and which segments

constitute immaterial non-reportable segments and should be disclosed under the ‘all

other segments’ category.

* The dierence between the segments revenue and the consolidated reported revenue is due to internal sales

between the urniture businesses.

The domestic and the commercial manuacturing segments in Australia and the UK have

similar economic characteristics and are similar in all ve o the areas listed in IFRS 8

para 12.

8/6/2019 IFRS 8 Guide

http://slidepdf.com/reader/full/ifrs-8-guide 26/3626 | PricewaterhouseCoopers – A practical guide to segment reporting

Do any operating segmentsmeet all of the aggregationcriteria?

Aggregation into asingle reportablesegment is permitted(but not required)

Aggregation intoa separatereportable segmentis permitted(but not required)

Present as separatereported segmentsin the financialstatements

furniture (Australia)

These reportable segments

cannot be aggregated becausethey have dissimilar economiccharacteristics

Material reportable segments

segments constituted 73%.

$58k consolidated revenue

even though it is not required underthe standard. Management felt thatthis segment should be reported due

Present land development andmachine hire as ‘all other segments’

Are there any operatingsegments (or aggregatedoperating segments) that

Are there any immaterialnon-reporting segments thathave similar economiccharacteristics and share amajority of the aggregationcriteria?

Do the reportable segments

identified constitute at least75% of consolidatedrevenue?

(aggregated if permitted) until75% if consolidated revenue

Aggregate the remainingimmaterial non-reportablesegments and other activitiesinto an ‘all other segments’category

No

Yes

Yes

Yes

Yes

No

No

No

Reporting segments

8/6/2019 IFRS 8 Guide

http://slidepdf.com/reader/full/ifrs-8-guide 27/36PricewaterhouseCoopers – A practical guide to segment reporting | 27

Segment disclosures

3.1 Where the CODM is provided with more than one measure o segment

protability, what measure o segment protability should be reported?

When more than one measure o protability is provided to the CODM, the measure

most relied upon by the CODM or assessing perormance and deciding on theallocation o resources should be disclosed. When two or more measures are equally

relied upon by the CODM, the measure most consistent with those used in measuring

the corresponding amounts in the entity’s nancial statements should be used.

Additional disclosure may need to be made in some circumstances. An example o this

is shown below.

Example – Company A uses two measures o prot

Company A provides the CODM with two measures o protability by operating

segment, which is operating prot and prot beore income tax expense. Segment

operating prot is determined based on the same measurement principles thatare used in the preparation o consolidated operating prot. However, segment

prot beore income tax expense includes certain internal cost-o-capital charges

that are eliminated in determining consolidated prot beore income tax expense.

Segment operating prot would be the measure reported externally because

this measure is the most consistent with its corresponding amount in the entity’s

nancial statements.

Additional disclosure would be made or interest income and expense because

that inormation is included in the prot beore income tax expense measure

provided to the CODM.

The measure o segment protability may dier or each operating segment, as

dierent operating segments may report dierent measures o protability to theCODM. IFRS 8 para 27 requires companies to explain the measurement basis o

segment protability or each reportable segment.

8/6/2019 IFRS 8 Guide

http://slidepdf.com/reader/full/ifrs-8-guide 28/3628 | PricewaterhouseCoopers – A practical guide to segment reporting

3.2 What measure should be reported when the asset inormation reported to the

CODM is limited or not reviewed at all?

IFRS 8 para 25 states that only those assets that are included in the measure o the

segment’s assets that are used by the CODM should be reported.

Scenario Basis o asset measurement

Asset inormation, although available,is not reported or used by the CODM.

No measure o segment asset is disclosed*.Disclose in the notes that asset inormation isnot reported.

Asset inormation is reported but isnot used by the CODM.

Asset inormation is included in other reportsprovided to the CODM is disclosed even i theinormation is not used by the CODM.

Asset inormation reported is limitedto cash, inventory and accountsreceivables.

The sum o the total o those asset items isdisclosed as segment assets. The total o thereported segment assets is then reconciled tothe total consolidated assets. An explanation othe basis o measurement is disclosed.

The CODM is provided with, andreviews ratios derived rom, currentasset balances (ie, working capital).The components that orm the ratiosare not separately provided.

The specic asset inormation or workingcapital amount is not required to be disclosed. Although it has an asset component, the currentasset component is not what is relevant to theCODM’s decision-making. However, an entitymay elect to voluntarily report total workingcapital, and then reconcile that gure to totalconsolidated working capital.

Non-current assets by geographical area are also required to be disclosed

(IFRS 8 para 33(b)) even i such inormation is not reviewed by the CODM.

* The Basis o Conclusions to IFRS 8 para BC35 states that a measure o total segment assets should be

disclosed or all segments regardless o whether those measures are reviewed by the CODM. In December2007, the IASB concluded that BC35 should be changed to state that a measure o segment assets should

only be disclosed when such inormation is provided to the CODM. This change will become eective as part

o the IASB’s 2009 Annual Improvements project. Until this change becomes eective, we think it is best or

companies to disclose segment assets as required by BC35.

8/6/2019 IFRS 8 Guide

http://slidepdf.com/reader/full/ifrs-8-guide 29/36PricewaterhouseCoopers – A practical guide to segment reporting | 29

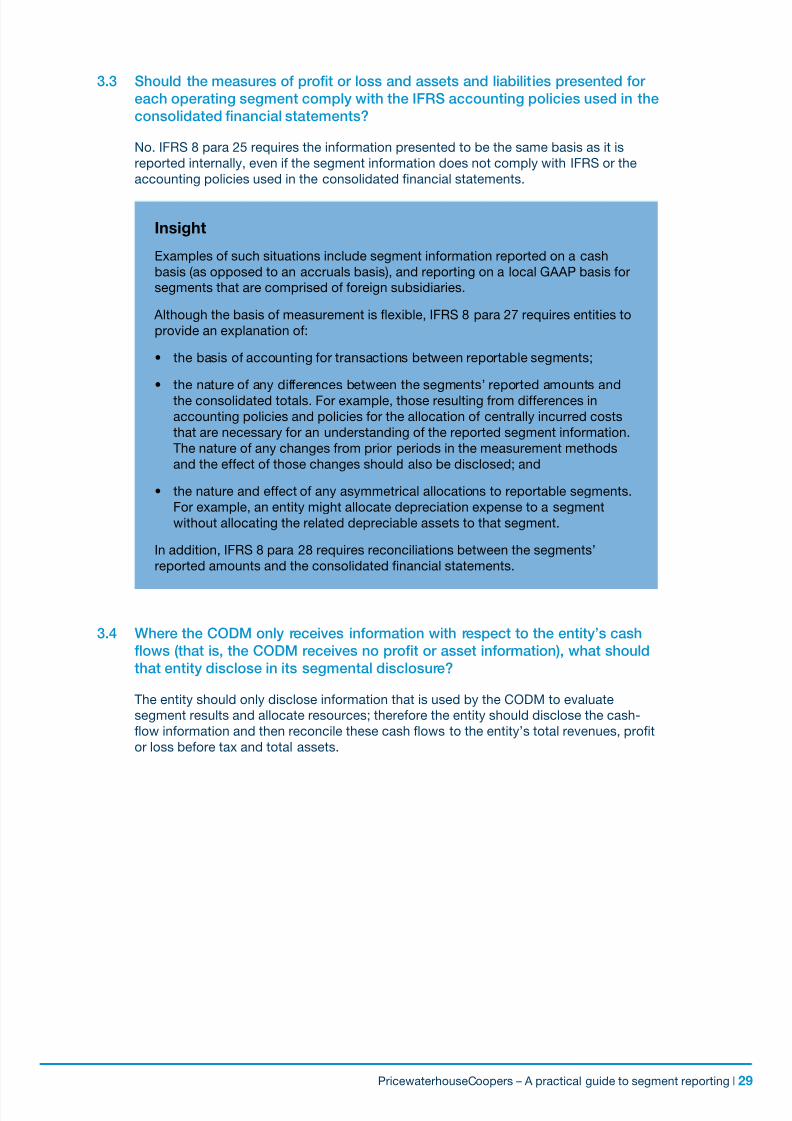

3.3 Should the measures o prot or loss and assets and liabilities presented or

each operating segment comply with the IFRS accounting policies used in the

consolidated nancial statements?

No. IFRS 8 para 25 requires the inormation presented to be the same basis as it is

reported internally, even i the segment inormation does not comply with IFRS or the

accounting policies used in the consolidated nancial statements.

Insight

Examples o such situations include segment inormation reported on a cash

basis (as opposed to an accruals basis), and reporting on a local GAAP basis or

segments that are comprised o oreign subsidiaries.

Although the basis o measurement is fexible, IFRS 8 para 27 requires entities to

provide an explanation o:

• thebasisofaccountingfortransactionsbetweenreportablesegments;

• thenatureofanydifferencesbetweenthesegments’reportedamountsand

the consolidated totals. For example, those resulting rom dierences in

accounting policies and policies or the allocation o centrally incurred costs

that are necessary or an understanding o the reported segment inormation.

The nature o any changes rom prior periods in the measurement methods

and the eect o those changes should also be disclosed; and

• thenatureandeffectofanyasymmetricalallocationstoreportablesegments.

For example, an entity might allocate depreciation expense to a segment

without allocating the related depreciable assets to that segment.

In addition, IFRS 8 para 28 requires reconciliations between the segments’

reported amounts and the consolidated nancial statements.

3.4 Where the CODM only receives inormation with respect to the entity’s cash

fows (that is, the CODM receives no prot or asset inormation), what should

that entity disclose in its segmental disclosure?

The entity should only disclose inormation that is used by the CODM to evaluate

segment results and allocate resources; thereore the entity should disclose the cash-

fow inormation and then reconcile these cash fows to the entity’s total revenues, prot

or loss beore tax and total assets.

8/6/2019 IFRS 8 Guide

http://slidepdf.com/reader/full/ifrs-8-guide 30/3630 | PricewaterhouseCoopers – A practical guide to segment reporting

Insight

Determining operating segments is an area o signicant judgement and scrutiny,

so it is important that entities consider how internal organisational change will

impact the identication and measurement o their operating segments.

Management should consider the ollowing when determining its operating

segments:

• WhoistheCODMandwhatisreviewedbytheCODM?

• HastheCODMchanged(ie,havereportinglineschanged)?

• HowhastheCODMreportingpackagechanged?

• Hastheorganisationalchartchanged(ie,acquisition/disposalofbusiness

activities)?

• HasthepersontheCODMmeetswithchanged?

• Havetherebeenanychangesinthebudgetingprocess,orlevelatwhich

budgets are set?

• Whatisthecompanycommunicatingtoexternalpartiessuchasinvestors,

creditors and customers?

Situations that may impact identied operating segments:

• Enteringanewlineofbusiness.

• Lineofserviceversusgeography(ie,acompanyhashiredanewCEOandthe

internal reporting structure is changing rom a model o geographical reporting

to that o product line reporting).

• Newsystemandreportingtools(ie,implementationofanewsystemthat

includes various reporting tools has enabled the entity to report on and

manage its business activities dierently).

3.5 When should an entity consider and review its segment reporting?

There is no specic guidance in IFRS 8 on what changes trigger a change in an entity’s

reportable operating segments. Change in the CODM and/or the inormation provided to

and reviewed by the CODM or the purposes o evaluating perormance and allocating

resources would impact the identied operating segments. Thereore, at each reporting

date management should consider whether the current operating segment disclosure

continues to be appropriate.

8/6/2019 IFRS 8 Guide

http://slidepdf.com/reader/full/ifrs-8-guide 31/36PricewaterhouseCoopers – A practical guide to segment reporting | 31

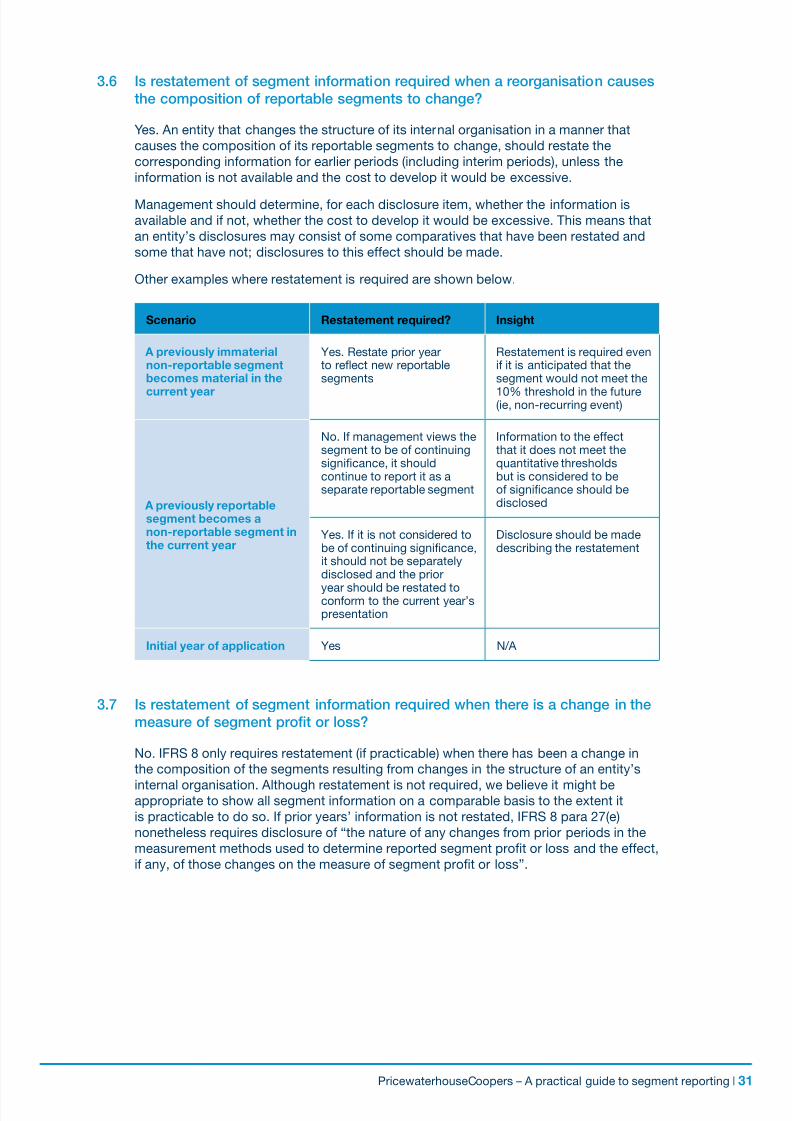

3.6 Is restatement o segment inormation required when a reorganisation causes

the composition o reportable segments to change?

Yes. An entity that changes the structure o its internal organisation in a manner that

causes the composition o its reportable segments to change, should restate the

corresponding inormation or earlier periods (including interim periods), unless the

inormation is not available and the cost to develop it would be excessive.

Management should determine, or each disclosure item, whether the inormation is

available and i not, whether the cost to develop it would be excessive. This means that

an entity’s disclosures may consist o some comparatives that have been restated and

some that have not; disclosures to this eect should be made.

Other examples where restatement is required are shown below.

Scenario Restatement required? Insight

A previously immaterialnon-reportable segmentbecomes material in the

current year

Yes. Restate prior yearto refect new reportablesegments

Restatement is required eveni it is anticipated that thesegment would not meet the

10% threshold in the uture(ie, non-recurring event)

A previously reportablesegment becomes anon-reportable segment inthe current year

No. I management views thesegment to be o continuingsignicance, it shouldcontinue to report it as aseparate reportable segment

Inormation to the eectthat it does not meet thequantitative thresholdsbut is considered to beo signicance should bedisclosed

Yes. I it is not considered tobe o continuing signicance,it should not be separatelydisclosed and the prior

year should be restated toconorm to the current year’spresentation

Disclosure should be madedescribing the restatement

Initial year o application Yes N/A

3.7 Is restatement o segment inormation required when there is a change in the

measure o segment prot or loss?

No. IFRS 8 only requires restatement (i practicable) when there has been a change in

the composition o the segments resulting rom changes in the structure o an entity’s

internal organisation. Although restatement is not required, we believe it might beappropriate to show all segment inormation on a comparable basis to the extent it

is practicable to do so. I prior years’ inormation is not restated, IFRS 8 para 27(e)

nonetheless requires disclosure o “the nature o any changes rom prior periods in the

measurement methods used to determine reported segment prot or loss and the eect,

i any, o those changes on the measure o segment prot or loss”.

8/6/2019 IFRS 8 Guide

http://slidepdf.com/reader/full/ifrs-8-guide 32/3632 | PricewaterhouseCoopers – A practical guide to segment reporting

3.8 What is the denition o ‘material’ where an entity is required to disclose

separately material revenues and material non-current assets rom an

individual oreign country?

IFRS 8 does not dene the term ‘material’ or the purpose o determining whether an

individual country’s revenue or non-current assets should be separately disclosed.

The entity should consider materiality rom both quantitative and qualitativeperspectives. When considering materiality quantitatively, the standard uses the

threshold o 10% or more in determining whether an operating segment is a reportable

segment. Thereore, it may be appropriate to apply the same test to determine whether

an individual country’s revenue or assets are material or the purpose o separate

disclosure.

Insight

PwC believes the materiality test should be applied by comparing the country’s

revenue or assets to total entity external revenue or assets (including the country

o domicile) rather than comparing those gures to the relevant totals o oreign

countries’ revenues and assets (excluding the country o domicile).

8/6/2019 IFRS 8 Guide

http://slidepdf.com/reader/full/ifrs-8-guide 33/36PricewaterhouseCoopers – A practical guide to segment reporting | 33

Other matters or consideration

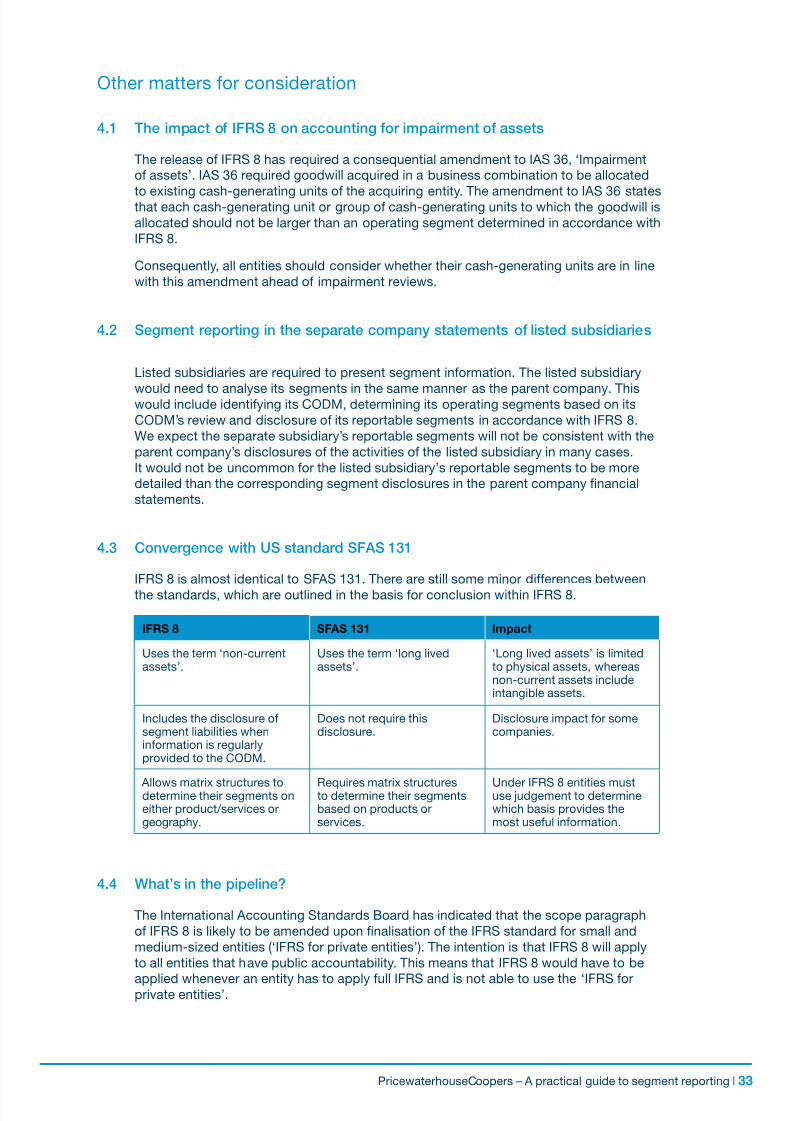

4.1 The impact o IFRS 8 on accounting or impairment o assets

The release o IFRS 8 has required a consequential amendment to IAS 36, ‘Impairment

o assets’. IAS 36 required goodwill acquired in a business combination to be allocated

to existing cash-generating units o the acquiring entity. The amendment to IAS 36 statesthat each cash-generating unit or group o cash-generating units to which the goodwill is

allocated should not be larger than an operating segment determined in accordance with

IFRS 8.

Consequently, all entities should consider whether their cash-generating units are in line

with this amendment ahead o impairment reviews.

4.2 Segment reporting in the separate company statements o listed subsidiaries

Listedsubsidiariesarerequiredtopresentsegmentinformation.Thelistedsubsidiary

would need to analyse its segments in the same manner as the parent company. Thiswould include identiying its CODM, determining its operating segments based on its

CODM’s review and disclosure o its reportable segments in accordance with IFRS 8.

We expect the separate subsidiary’s reportable segments will not be consistent with the

parent company’s disclosures o the activities o the listed subsidiary in many cases.

It would not be uncommon or the listed subsidiary’s reportable segments to be more

detailed than the corresponding segment disclosures in the parent company nancial

statements.

4.3 Convergence with US standard SFAS 131

IFRS 8 is almost identical to SFAS 131. There are still some minor dierences between

the standards, which are outlined in the basis or conclusion within IFRS 8.

IFRS 8 SFAS 131 Impact

Uses the term ‘non-currentassets’.

Uses the term ‘long livedassets’.

‘Longlivedassets’islimitedto physical assets, whereasnon-current assets includeintangible assets.

Includes the disclosure osegment liabilities wheninormation is regularlyprovided to the CODM.

Does not require thisdisclosure.

Disclosure impact or somecompanies.

Allows matrix structures todetermine their segments oneither product/services orgeography.

Requires matrix structuresto determine their segmentsbased on products orservices.

Under IFRS 8 entities mustuse judgement to determinewhich basis provides themost useul inormation.

4.4 What’s in the pipeline?

The International Accounting Standards Board has indicated that the scope paragraph

o IFRS 8 is likely to be amended upon nalisation o the IFRS standard or small and

medium-sized entities (‘IFRS or private entities’). The intention is that IFRS 8 will apply

to all entities that have public accountability. This means that IFRS 8 would have to be

applied whenever an entity has to apply ull IFRS and is not able to use the ‘IFRS orprivate entities’.

8/6/2019 IFRS 8 Guide

http://slidepdf.com/reader/full/ifrs-8-guide 34/3634 | PricewaterhouseCoopers – A practical guide to segment reporting

8/6/2019 IFRS 8 Guide

http://slidepdf.com/reader/full/ifrs-8-guide 35/36PricewaterhouseCoopers – A practical guide to segment reporting | 35

Corporate governance publications

Audit Committees –

Good Practices for

Meeting

Market Expectations

Provides PwC views on

good practice and

summarises audit

committee requirements

in over 40 countries.

Building the European Capital

Market –

A review of developments –

January 2007

This fourth edition includes the

key EU developments on IFRS,

the Prospectus and Transparency

Directives, and corporate

governance. It also summarises

the Commission’s single marketpriorities for the next five years.

IFRS surveys

IFRS for SMEs – Is it relevant for your

business?

It outlines why some unlisted SMEs have already

made the change to IFRS and illustrates what

might be involved in a conversion process.

Making the change to IFRS

This 12-page brochure provides a high-level

overview of the key issues that companies

need to consider in making the change to IFRS.

IFRS tools

COMPERIO®

Your Path to Knowledge

Presentation of income measures

Trends in use and presentation of non-GAAP income

measures in IFRS financial statements.

IFRS: The European investors’ view

Impact of IFRS reporting on fund managers’ perceptions

of value and their investment decisions.

Business review – has it made a difference?

Survey of the FTSE 350 companies’ narrative reporting

practices. Relevant globally to companies seeking to

benchmark against large UK companies.

IFRS 7: Ready or not

Key issues and disclosure requirements.

IFRS 7: Potential impact of market risks

Examples of how market risks can be calculated.

IFRS transition case studies

Companies in several industries share their experiences in

making the change to IFRS. Orders for these flyers should be

placed at [email protected]

World Watch magazine

Global magazine with

news and opinion

articles on the latest

developments and

trends in governance,

financial reporting,

broader reporting and

assurance.

IFRS market issues

Comperio Your path to knowledge

Online library of financial reporting and assurance literature. Provides the full text of IASB literature as well as ISAs,

International Auditing Practice Statements and IPSAS. Also contains PwC’s IFRS and corporate governance

publications, and Applying IFRS. For more information, visit www.pwc.com/comperio

To order copies of any of these publications, contact your local

PricewaterhouseCoopers office or visit www.cch.co.uk/ifrsbooks

About PricewaterhouseCoopers

PricewaterhouseCoopers (www.pwc.com) is the world’s largest professional services organisation. Drawing on theknowledge and skills of more than 146,000 people in 150 countries, we build relationships by providing services basedon quality and integrity.

Contacting PricewaterhouseCoopers

Please contact your local PricewaterhouseCoopers office to discuss how we can help you make the change toInternational Financial Reporting Standards or with technical queries. See inside front cover for further details of IFRSproducts and services.

© 2008 PricewaterhouseCoopers. All rights reserved. PricewaterhouseCoopers refers to the network of member firms of

PricewaterhouseCoopers International Limited, each of which is a separate and independent legal entity. PricewaterhouseCoopers

accepts no liability or responsibility to the contents of this publication or any reliance placed on it.

PricewaterhouseCoopers’ IFRS and corporate governance publications and tools 2008

8/6/2019 IFRS 8 Guide

http://slidepdf.com/reader/full/ifrs-8-guide 36/36

www.pwc.com/irs

UP/GCR070-BI8001