Embed Size (px)

Citation preview

IFRS 16 - Tax accounting

KPMG 2019 IFRS 16 Tax accounting seminar—October 2019

2© 2019 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

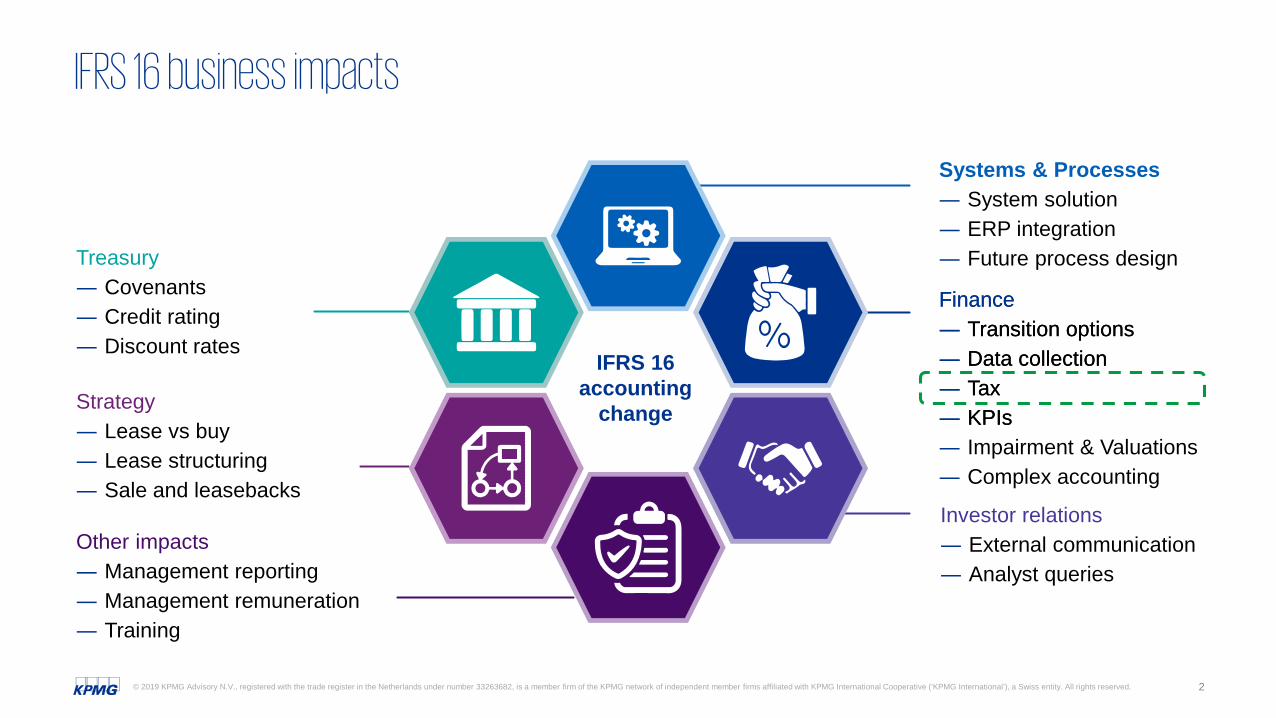

IFRS 16 business impacts

Systems & Processes― System solution― ERP integration― Future process design

Finance― Transition options― Data collection― Tax― KPIs

Investor relations― External communication― Analyst queries

Other impacts― Management reporting― Management remuneration― Training

Strategy― Lease vs buy― Lease structuring ― Sale and leasebacks

Treasury― Covenants― Credit rating― Discount rates

IFRS 16 accounting

change

Finance― Transition options― Data collection― Tax― KPIs― Impairment & Valuations― Complex accounting

3© 2019 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

With you today

Presenters

Stefan PaantjensSenior ManagerTax accounting specialist CMAAS

4© 2019 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

Agenda for today

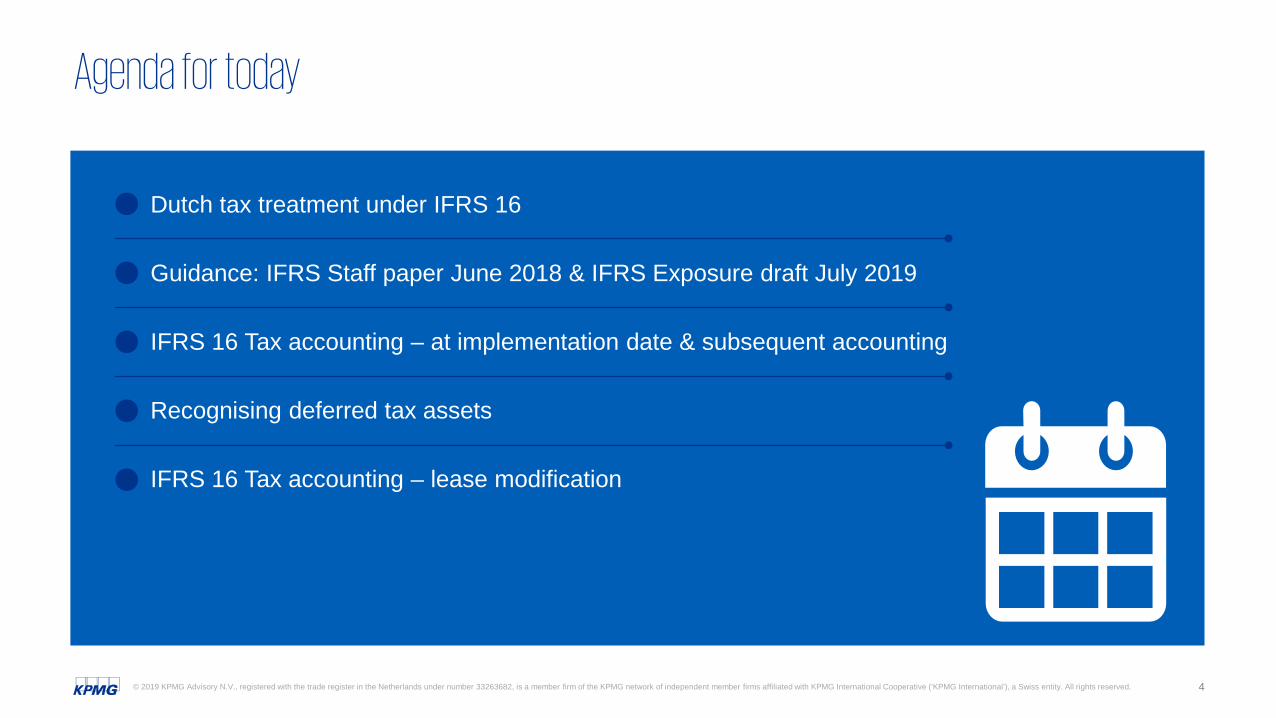

Dutch tax treatment under IFRS 16

Guidance: IFRS Staff paper June 2018 & IFRS Exposure draft July 2019

IFRS 16 Tax accounting – at implementation date & subsequent accounting

Recognising deferred tax assets

IFRS 16 Tax accounting – lease modification

5© 2019 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

Can IFRS 16 also be applied for Dutch tax purposes?

― The accounting treatment under IFRS 16 is not followed for Dutch tax purposes, as a result of which deductible and taxable temporary differences could arise between the commercial and tax books.

― These temporary differences generally result in the recognition of deferred tax assets and liabilities.

6© 2019 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

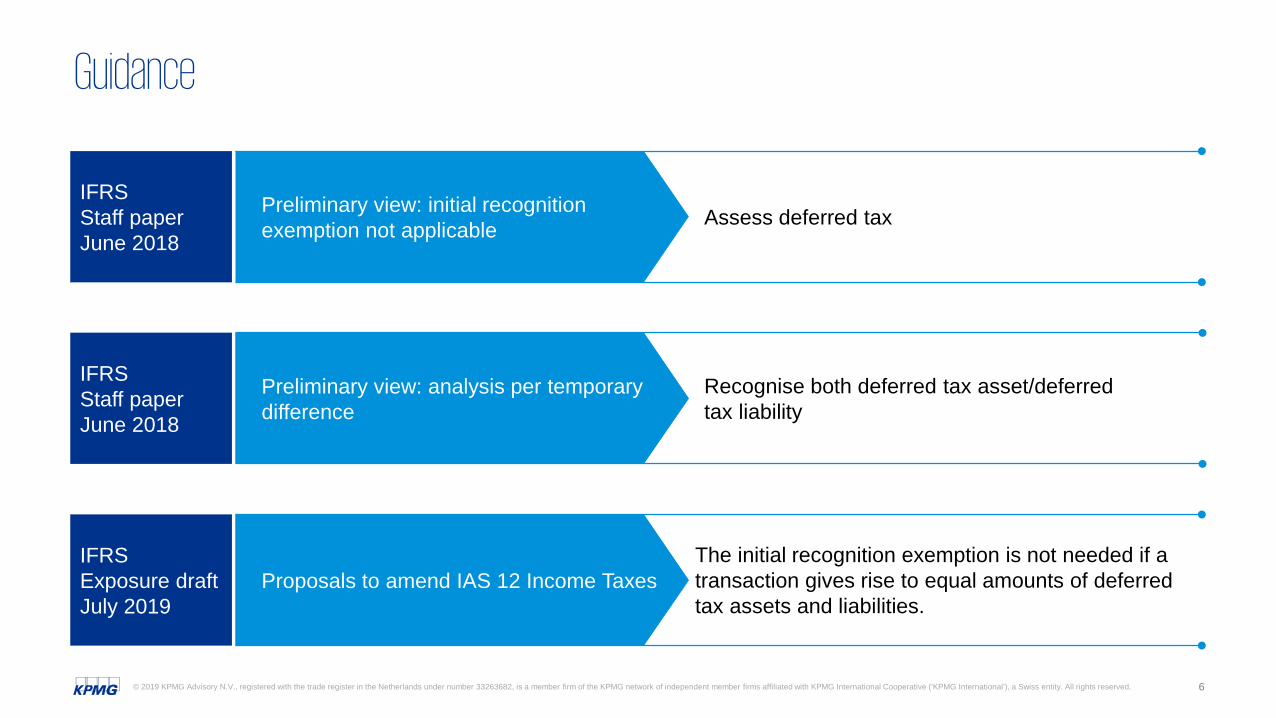

Guidance

Preliminary view: initial recognition exemption not applicable Assess deferred tax

IFRS Staff paperJune 2018

Preliminary view: analysis per temporary difference

Recognise both deferred tax asset/deferred tax liability

IFRS Staff paperJune 2018

Proposals to amend IAS 12 Income TaxesThe initial recognition exemption is not needed if a transaction gives rise to equal amounts of deferred tax assets and liabilities.

IFRS Exposure draft July 2019

7© 2019 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

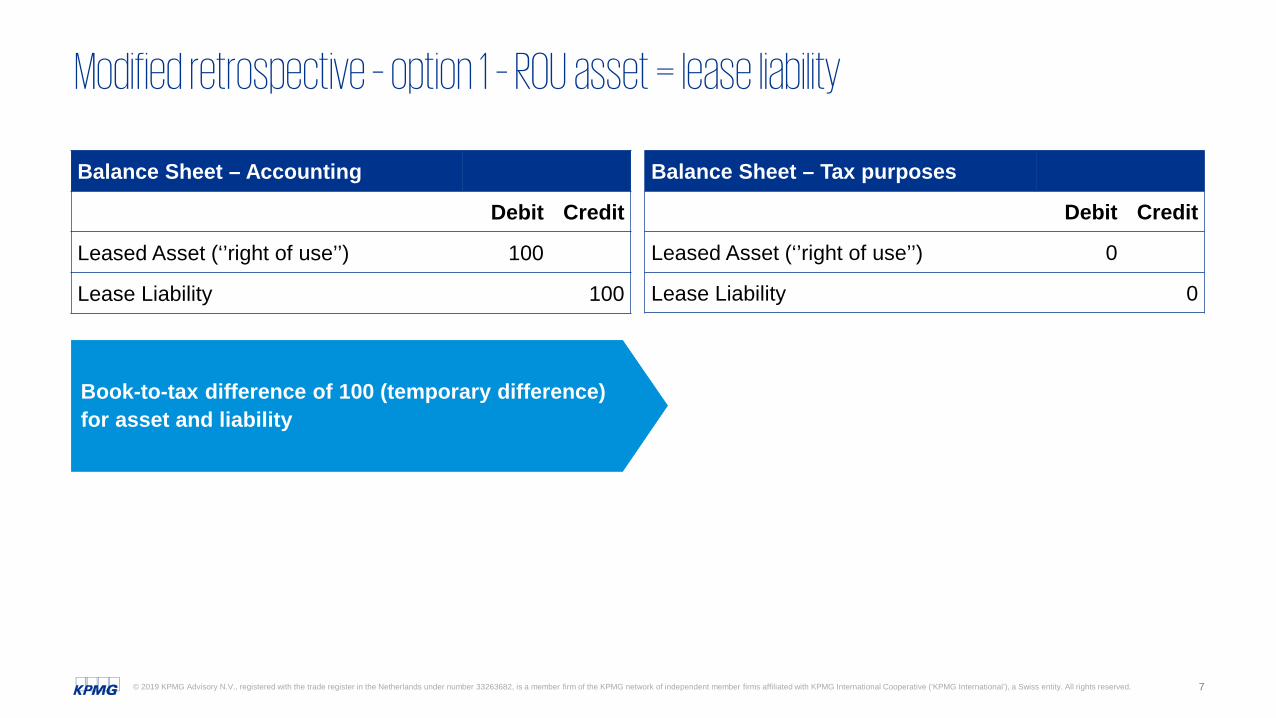

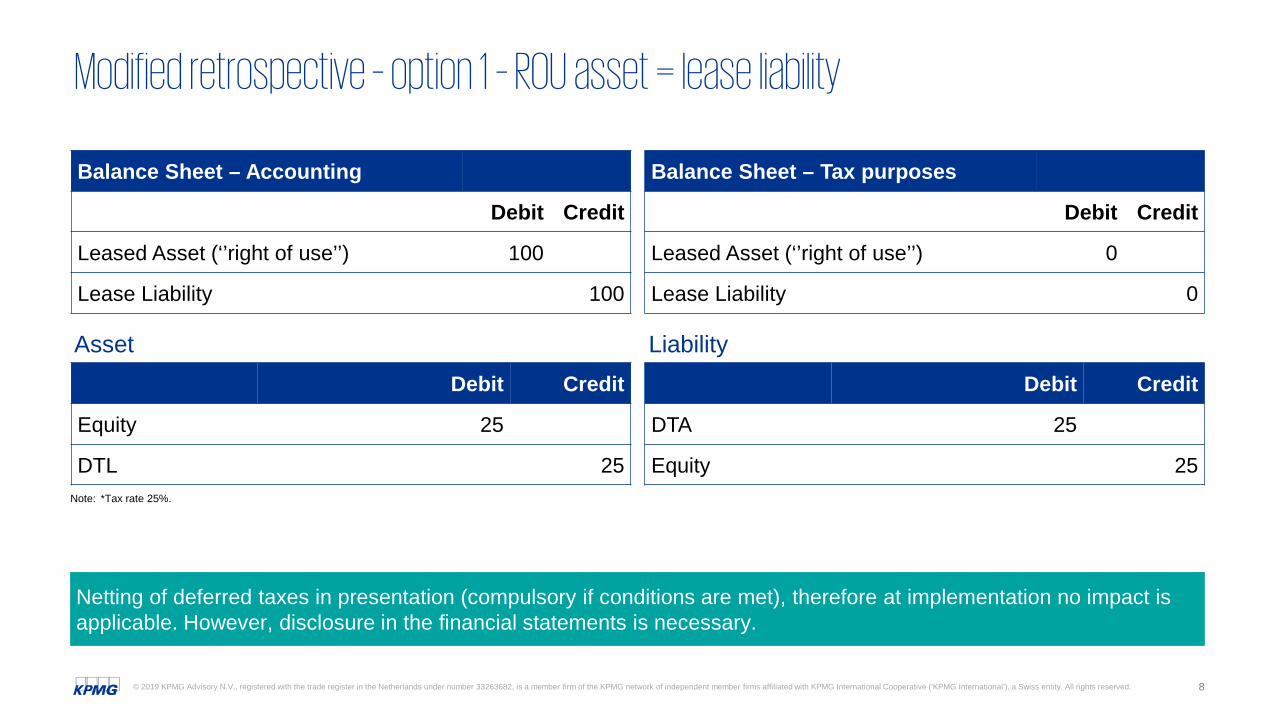

Modified retrospective – option 1 – ROU asset = lease liability

Balance Sheet – Accounting

Debit Credit

Leased Asset (‘’right of use’’) 100

Lease Liability 100

Balance Sheet – Tax purposes

Debit Credit

Leased Asset (‘’right of use’’) 0

Lease Liability 0

Book-to-tax difference of 100 (temporary difference) for asset and liability

8© 2019 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

Modified retrospective – option 1 – ROU asset = lease liability

Asset

Netting of deferred taxes in presentation (compulsory if conditions are met), therefore at implementation no impact is applicable. However, disclosure in the financial statements is necessary.

Balance Sheet – Accounting

Debit Credit

Leased Asset (‘’right of use’’) 100

Lease Liability 100

Balance Sheet – Tax purposes

Debit Credit

Leased Asset (‘’right of use’’) 0

Lease Liability 0

Debit Credit

Equity 25

DTL 25

Debit Credit

DTA 25

Equity 25Note: *Tax rate 25%.

Liability

9© 2019 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

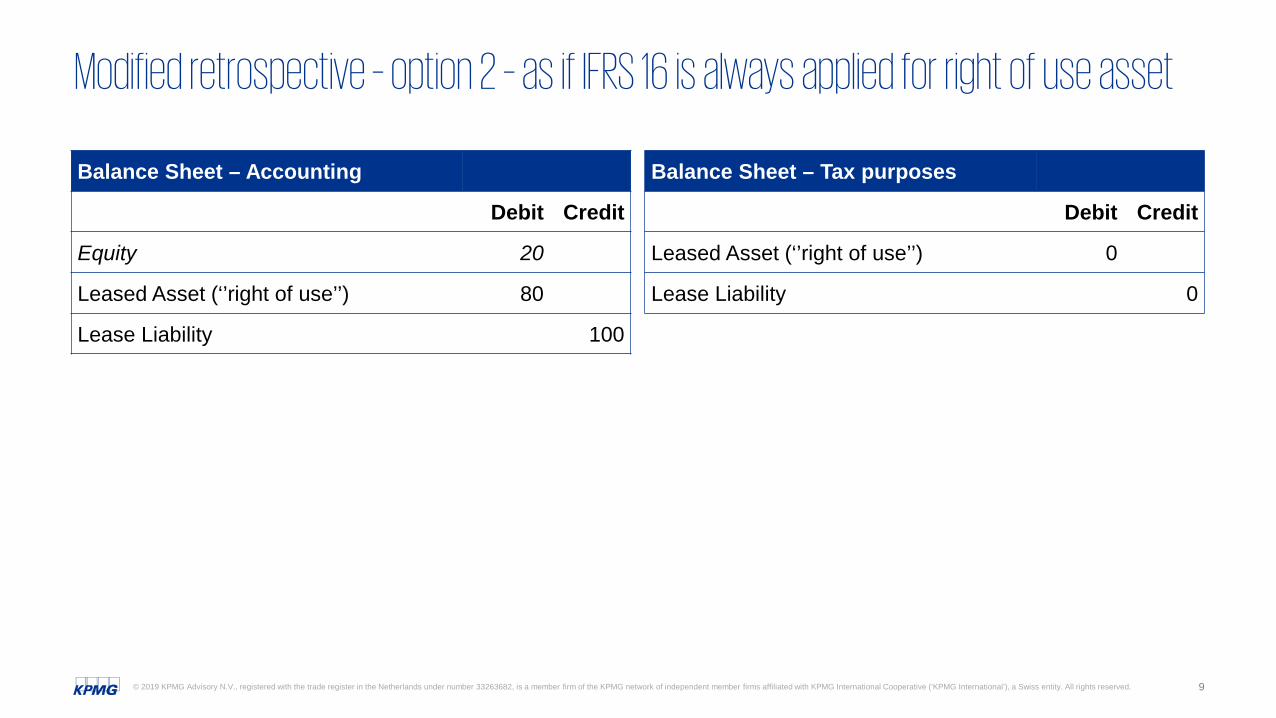

Modified retrospective – option 2 – as if IFRS 16 is always applied for right of use asset

Balance Sheet – Accounting

Debit Credit

Equity 20

Leased Asset (‘’right of use’’) 80

Lease Liability 100

Balance Sheet – Tax purposes

Debit Credit

Leased Asset (‘’right of use’’) 0

Lease Liability 0

10© 2019 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

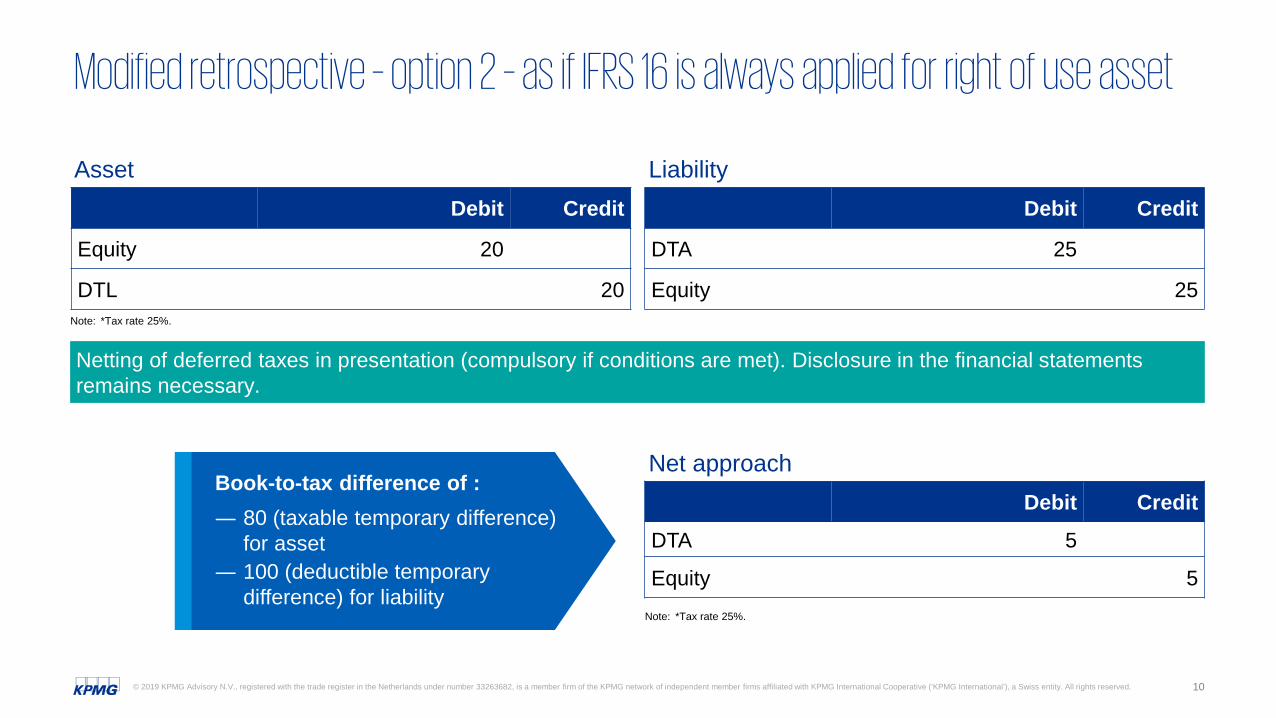

Modified retrospective – option 2 – as if IFRS 16 is always applied for right of use asset

Netting of deferred taxes in presentation (compulsory if conditions are met). Disclosure in the financial statements remains necessary.

Book-to-tax difference of :― 80 (taxable temporary difference)

for asset― 100 (deductible temporary

difference) for liabilityNote: *Tax rate 25%.

LiabilityDebit Credit

Equity 20

DTL 20

Debit Credit

DTA 25

Equity 25Note: *Tax rate 25%.

Net approachDebit Credit

DTA 5

Equity 5

Asset

11© 2019 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

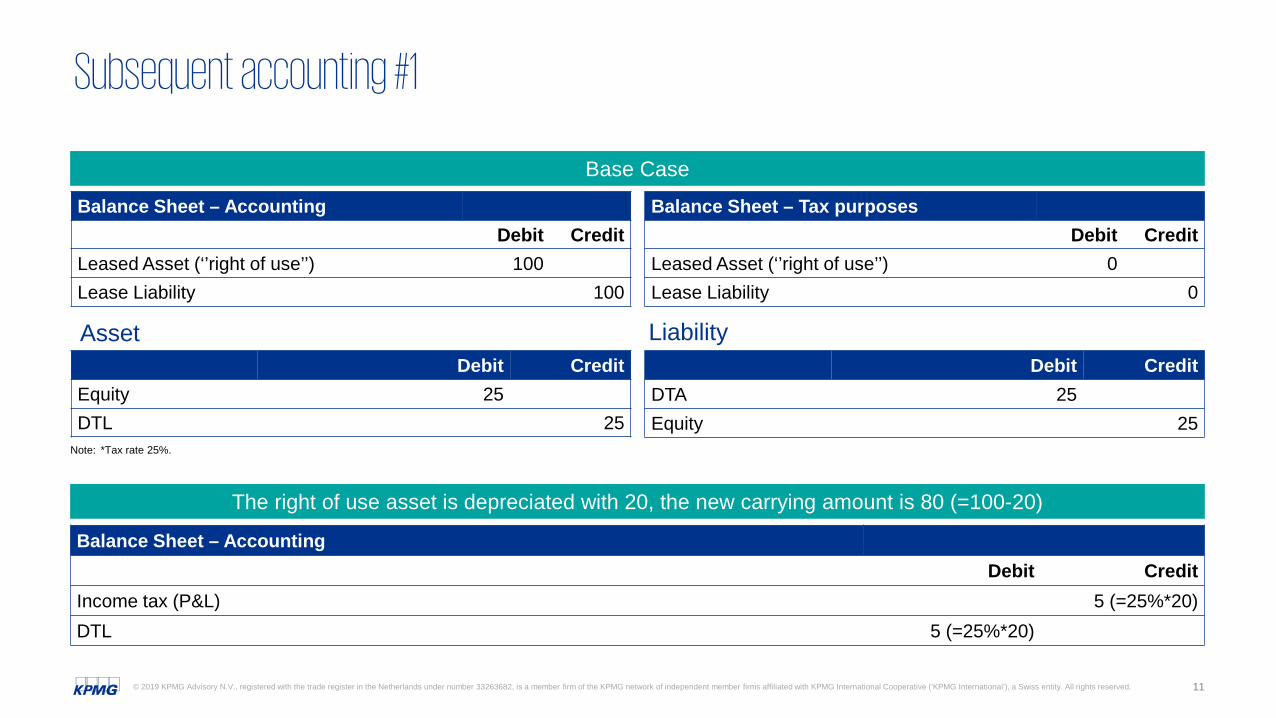

Subsequent accounting #1

Base Case

The right of use asset is depreciated with 20, the new carrying amount is 80 (=100-20)

Balance Sheet – AccountingDebit Credit

Income tax (P&L) 5 (=25%*20)DTL 5 (=25%*20)

Asset

Balance Sheet – AccountingDebit Credit

Leased Asset (‘’right of use’’) 100Lease Liability 100

Balance Sheet – Tax purposesDebit Credit

Leased Asset (‘’right of use’’) 0Lease Liability 0

Debit CreditEquity 25DTL 25

Debit CreditDTA 25Equity 25

Note: *Tax rate 25%.

Liability

12© 2019 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

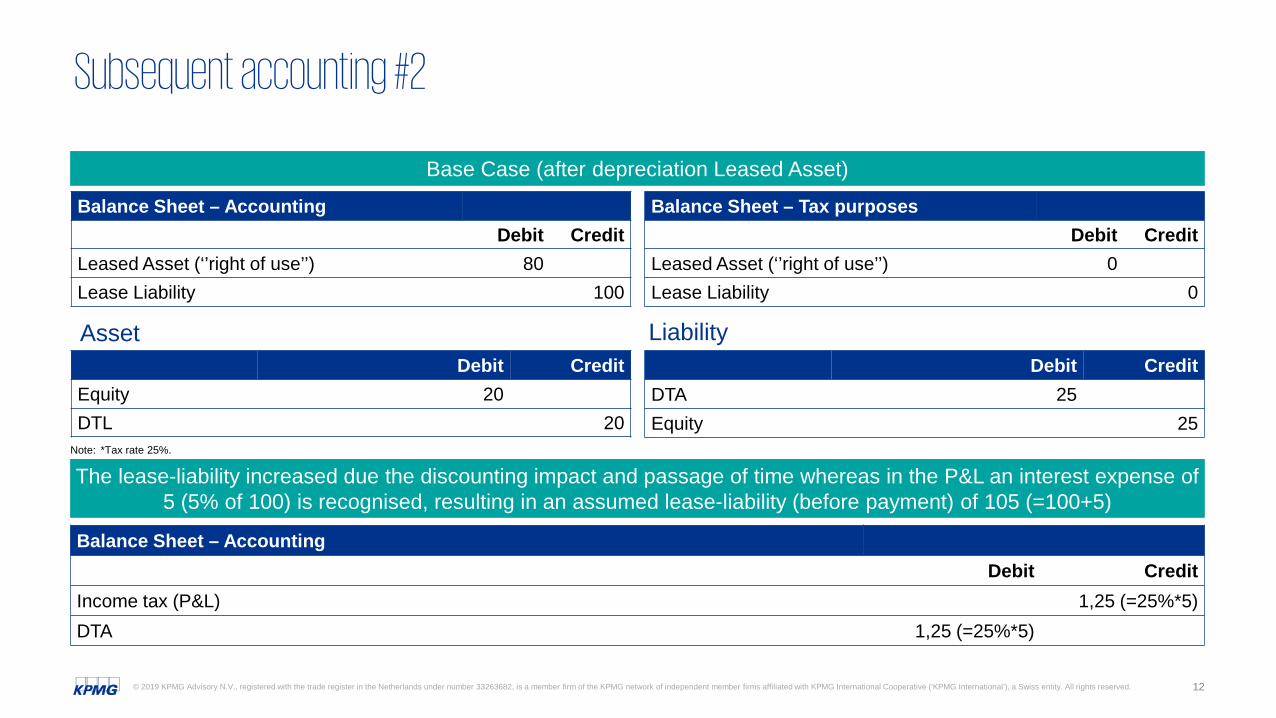

Subsequent accounting #2

Asset

Balance Sheet – AccountingDebit Credit

Leased Asset (‘’right of use’’) 80Lease Liability 100

Balance Sheet – Tax purposesDebit Credit

Leased Asset (‘’right of use’’) 0Lease Liability 0

Debit CreditEquity 20DTL 20

Debit CreditDTA 25Equity 25

Note: *Tax rate 25%.

Liability

The lease-liability increased due the discounting impact and passage of time whereas in the P&L an interest expense of 5 (5% of 100) is recognised, resulting in an assumed lease-liability (before payment) of 105 (=100+5)

Balance Sheet – AccountingDebit Credit

Income tax (P&L) 1,25 (=25%*5)DTA 1,25 (=25%*5)

Base Case (after depreciation Leased Asset)

13© 2019 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

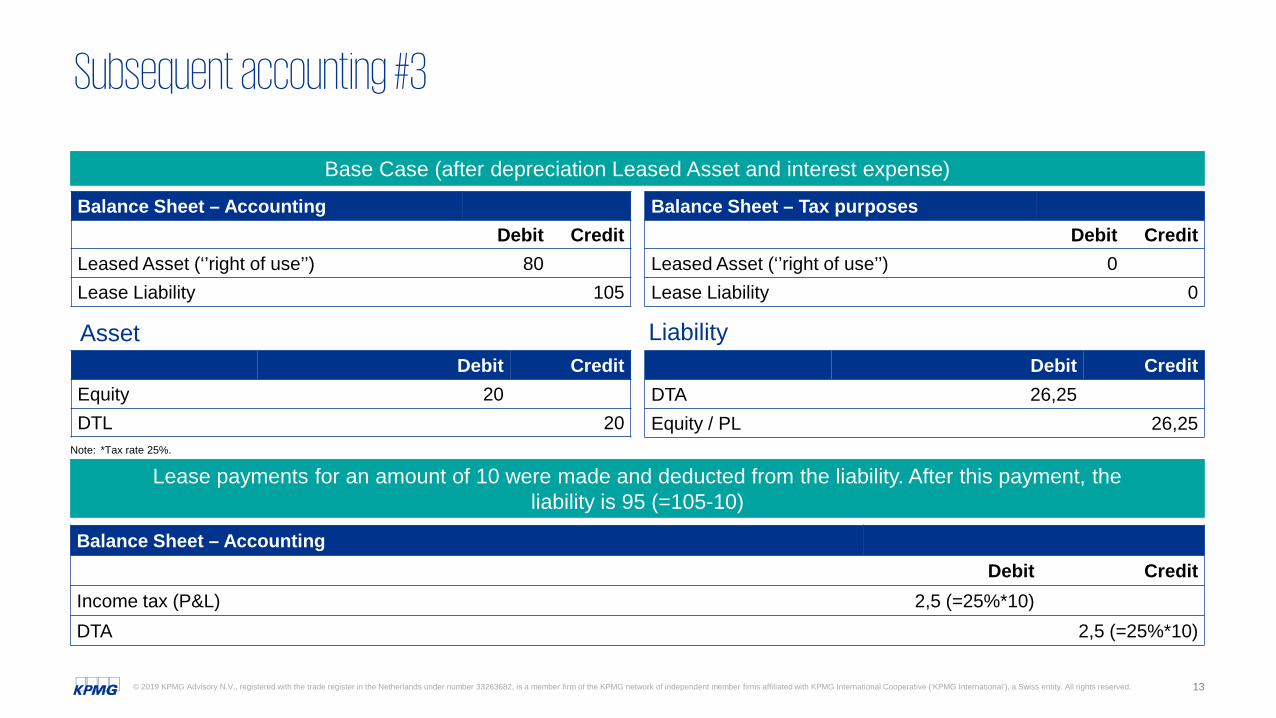

Subsequent accounting #3

Asset

Balance Sheet – AccountingDebit Credit

Leased Asset (‘’right of use’’) 80Lease Liability 105

Balance Sheet – Tax purposesDebit Credit

Leased Asset (‘’right of use’’) 0Lease Liability 0

Debit CreditEquity 20DTL 20

Debit CreditDTA 26,25Equity / PL 26,25

Note: *Tax rate 25%.

Liability

Balance Sheet – AccountingDebit Credit

Income tax (P&L) 2,5 (=25%*10)DTA 2,5 (=25%*10)

Lease payments for an amount of 10 were made and deducted from the liability. After this payment, theliability is 95 (=105-10)

Base Case (after depreciation Leased Asset and interest expense)

14© 2019 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

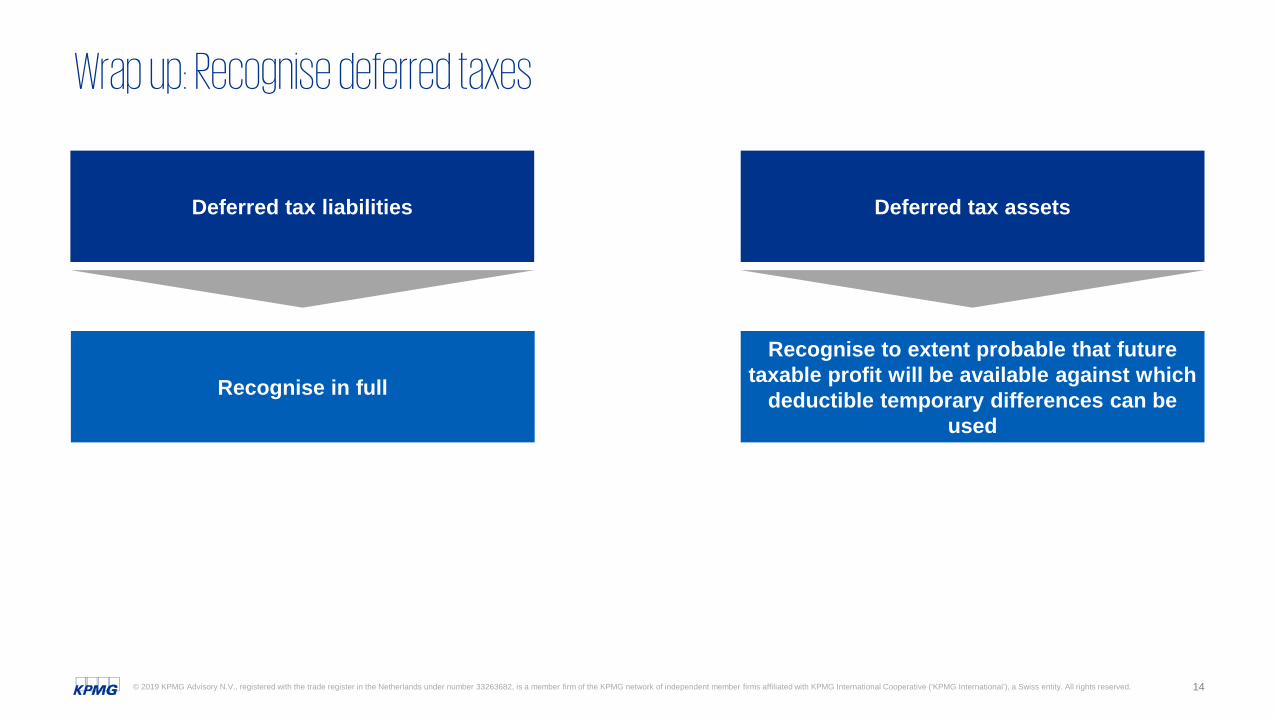

Wrap up: Recognise deferred taxes

Deferred tax liabilities

Recognise in full

Deferred tax assets

Recognise to extent probable that future taxable profit will be available against which

deductible temporary differences can be used

15© 2019 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

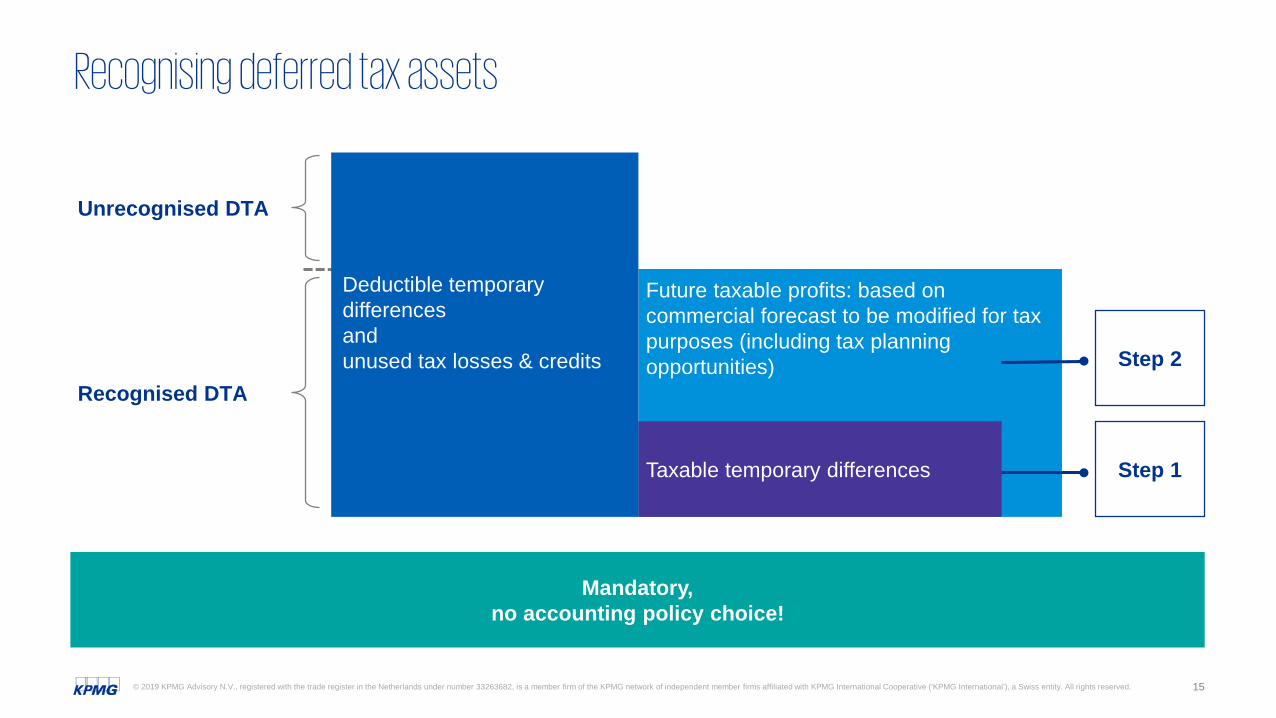

Recognising deferred tax assets

Future taxable profits: based on commercial forecast to be modified for tax purposes (including tax planning opportunities)

Deductible temporary differencesandunused tax losses & credits

Taxable temporary differences

Unrecognised DTA

Recognised DTAStep 2

Step 1

Mandatory, no accounting policy choice!

16© 2019 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

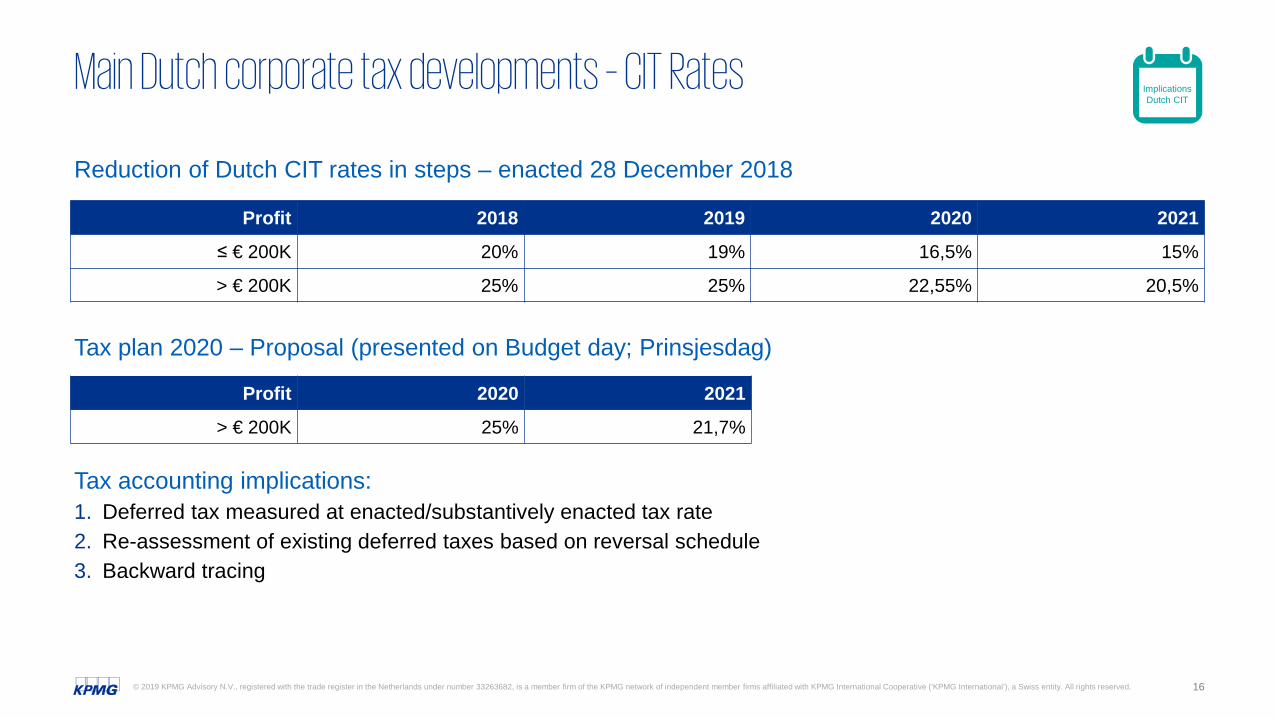

Main Dutch corporate tax developments – CIT Rates

Reduction of Dutch CIT rates in steps – enacted 28 December 2018

Tax plan 2020 – Proposal (presented on Budget day; Prinsjesdag)

Tax accounting implications: 1. Deferred tax measured at enacted/substantively enacted tax rate2. Re-assessment of existing deferred taxes based on reversal schedule3. Backward tracing

Profit 2020 2021

> € 200K 25% 21,7%

Implications Dutch CIT

Profit 2018 2019 2020 2021

≤ € 200K 20% 19% 16,5% 15%

> € 200K 25% 25% 22,55% 20,5%

17© 2019 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

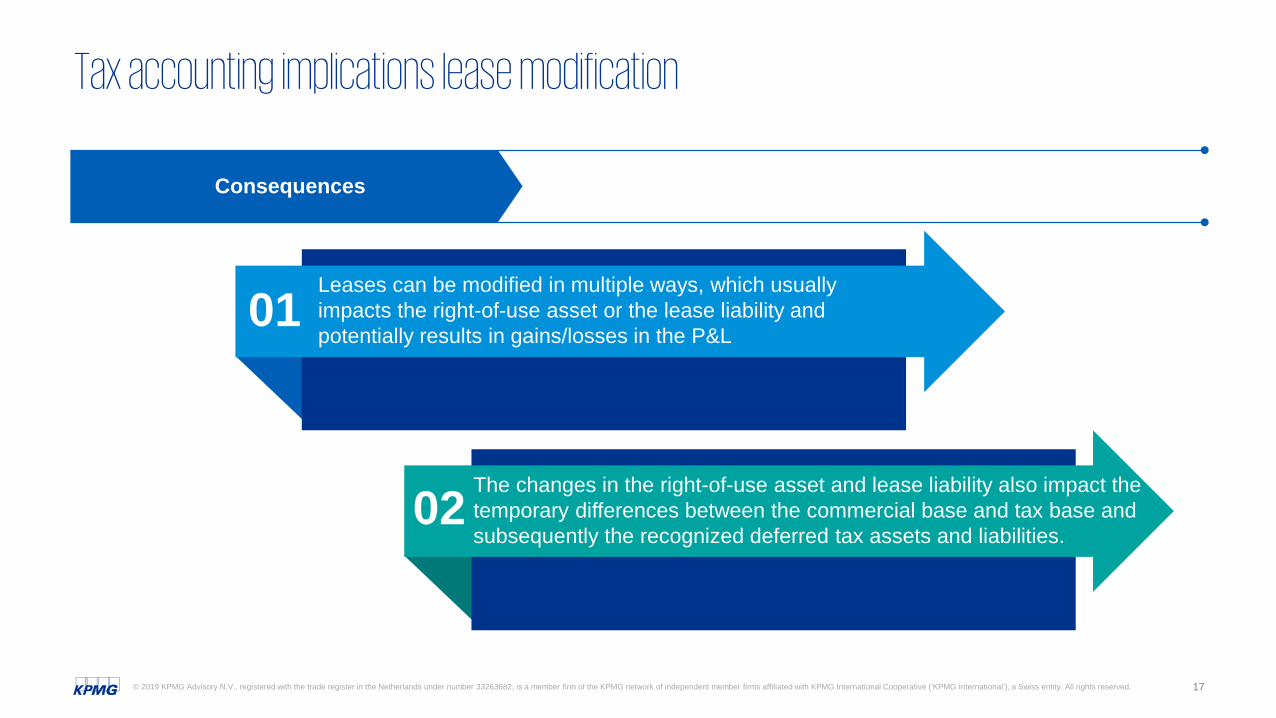

Tax accounting implications lease modification

01Leases can be modified in multiple ways, which usually impacts the right-of-use asset or the lease liability and potentially results in gains/losses in the P&L

The changes in the right-of-use asset and lease liability also impact the temporary differences between the commercial base and tax base and subsequently the recognized deferred tax assets and liabilities.

02

Consequences

18© 2019 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

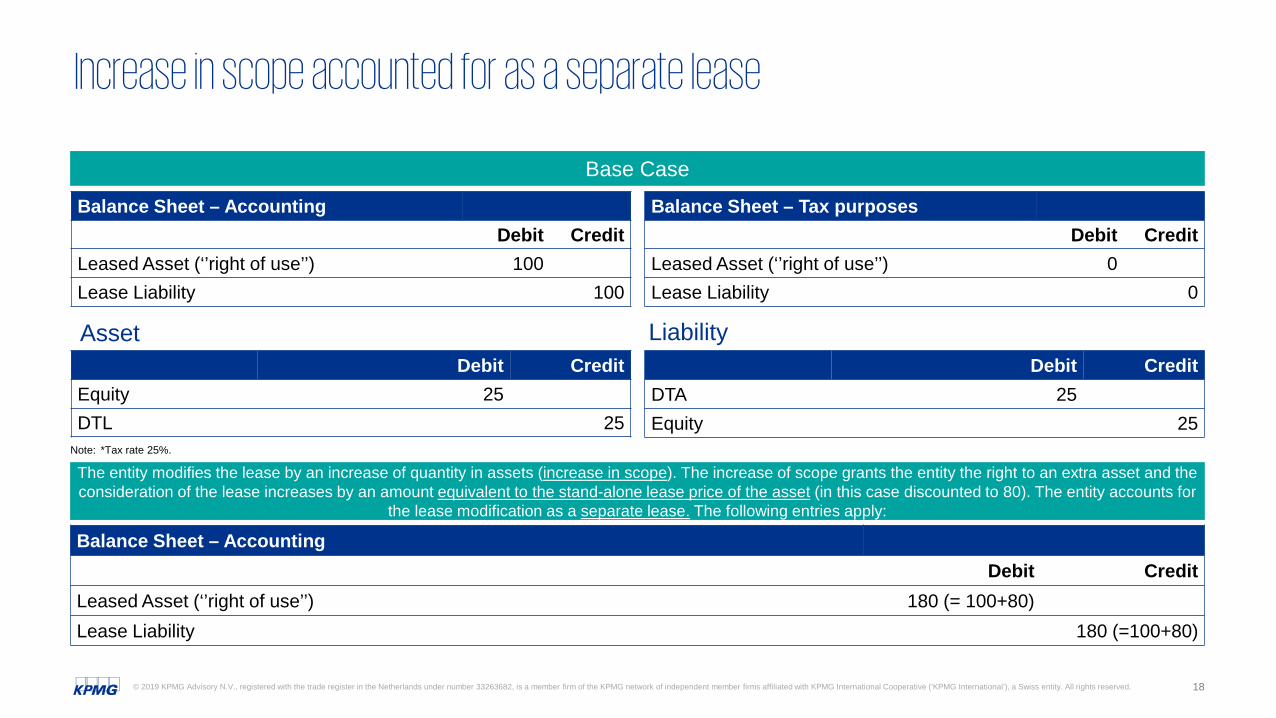

Increase in scope accounted for as a separate lease

Asset

Balance Sheet – AccountingDebit Credit

Leased Asset (‘’right of use’’) 100Lease Liability 100

Balance Sheet – Tax purposesDebit Credit

Leased Asset (‘’right of use’’) 0Lease Liability 0

Debit CreditEquity 25DTL 25

Debit CreditDTA 25Equity 25

Note: *Tax rate 25%.

Liability

The entity modifies the lease by an increase of quantity in assets (increase in scope). The increase of scope grants the entity the right to an extra asset and the consideration of the lease increases by an amount equivalent to the stand-alone lease price of the asset (in this case discounted to 80). The entity accounts for

the lease modification as a separate lease. The following entries apply:

Balance Sheet – AccountingDebit Credit

Leased Asset (‘’right of use’’) 180 (= 100+80)Lease Liability 180 (=100+80)

Base Case

19© 2019 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

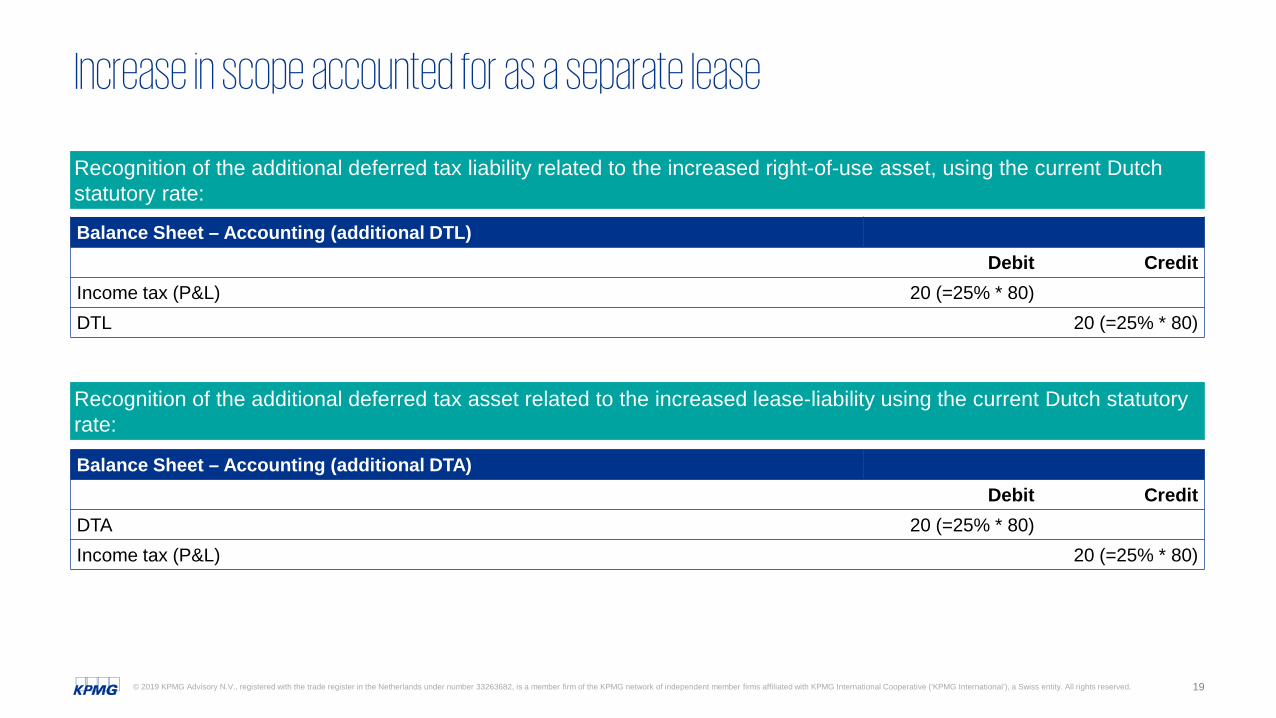

Increase in scope accounted for as a separate lease

Recognition of the additional deferred tax liability related to the increased right-of-use asset, using the current Dutch statutory rate:

Balance Sheet – Accounting (additional DTL)Debit Credit

Income tax (P&L) 20 (=25% * 80)DTL 20 (=25% * 80)

Recognition of the additional deferred tax asset related to the increased lease-liability using the current Dutch statutory rate:

Balance Sheet – Accounting (additional DTA)Debit Credit

DTA 20 (=25% * 80)Income tax (P&L) 20 (=25% * 80)

20© 2019 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

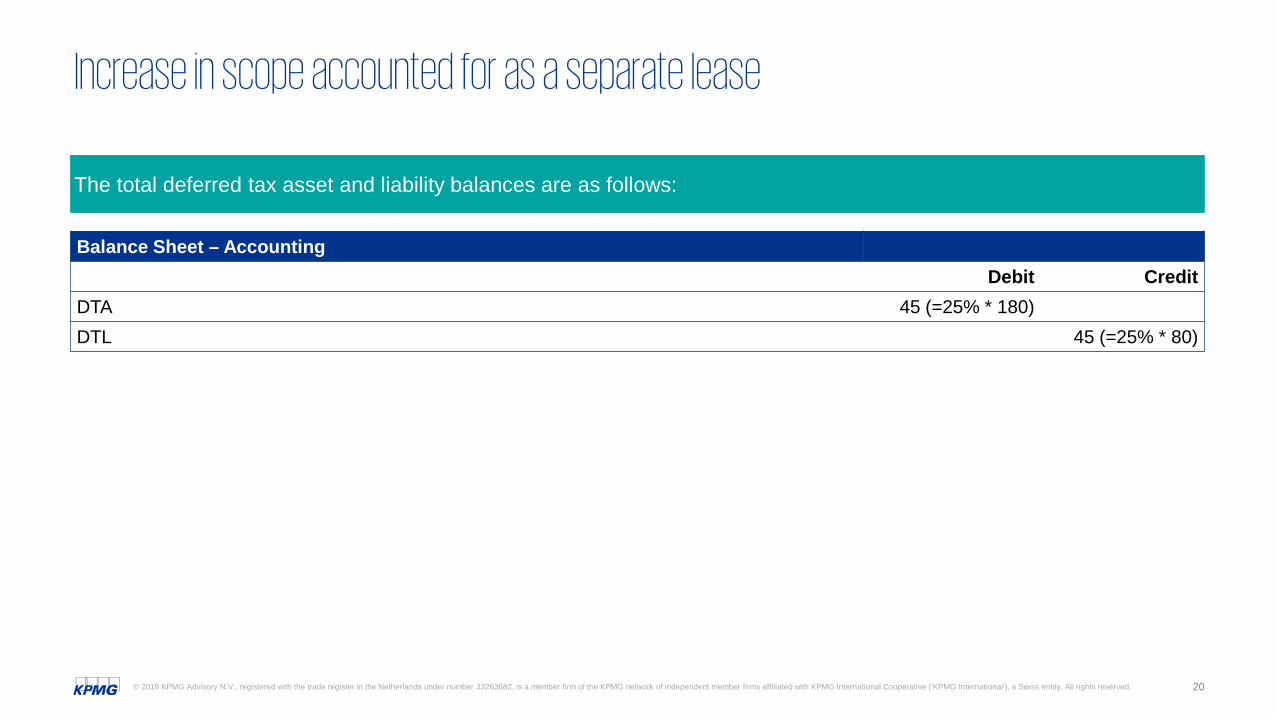

Increase in scope accounted for as a separate lease

The total deferred tax asset and liability balances are as follows:

Balance Sheet – AccountingDebit Credit

DTA 45 (=25% * 180)DTL 45 (=25% * 80)

KPMG on social media KPMG app

The KPMG name and logo are registered trademarks of KPMG International.

© 2019 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.