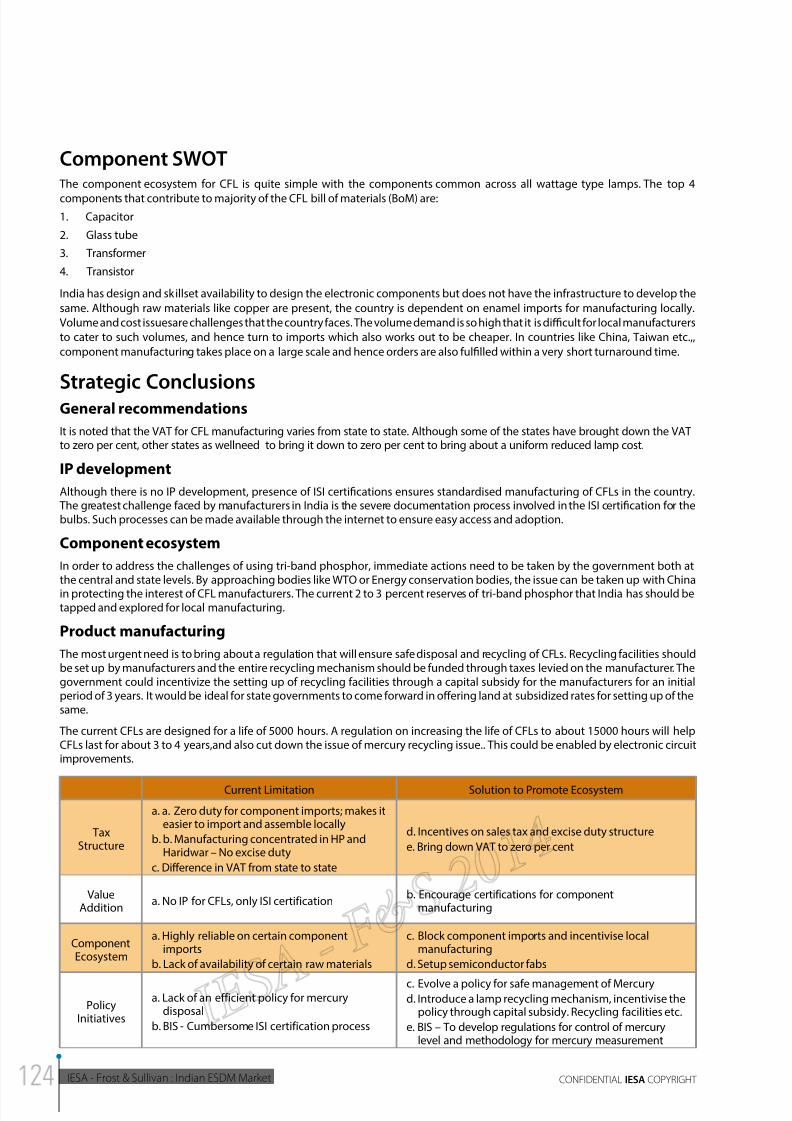

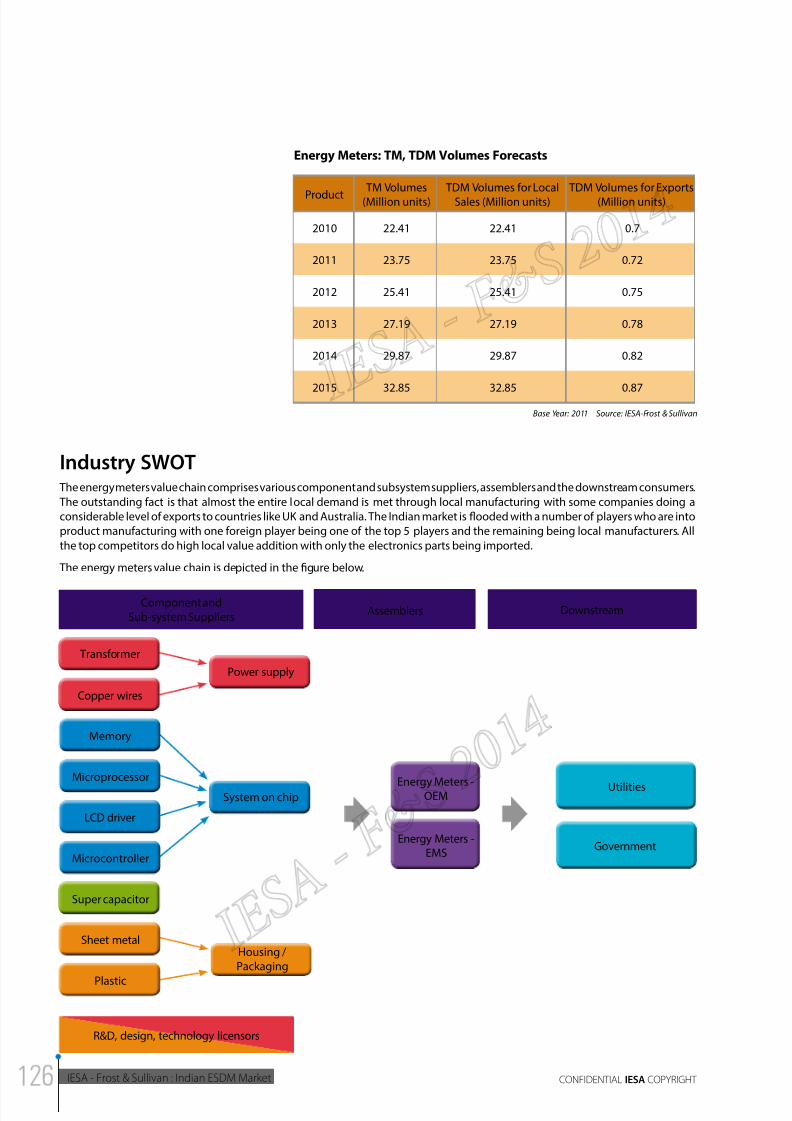

Embed Size (px)

Citation preview

8/11/2019 IESA FS Report Indian ESDM Market

http://slidepdf.com/reader/full/iesa-fs-report-indian-esdm-market 1/172

F R O S T & S U L L I VA N

INDIAN ESDM MARKET - ANALYSIS OF

OPPORTUNITY AND GROWTH PLANAn IESA - Frost & Sullivan Report

Supported by the Department of Electronics & Information Technology,

Ministry of Communications & Information Technology

Government of India

8/11/2019 IESA FS Report Indian ESDM Market

http://slidepdf.com/reader/full/iesa-fs-report-indian-esdm-market 2/172

IESA - Frost & Sullivan : Indian ESDM Market CONFIDENTIAL IESA COPYRIGHT

Copyright © 2014, India Electronics & Semiconductor Association

8/11/2019 IESA FS Report Indian ESDM Market

http://slidepdf.com/reader/full/iesa-fs-report-indian-esdm-market 3/172

2014INDIAN ESDM MARKET - ANALYSIS OF

OPPORTUNITY AND GROWTH PLAN

IESA - Frost & Sullivan : Indian ESDM MarketCONFIDENTIAL IESA COPYRIGHT

Report released by

Shri J. Satyanarayana, IAS

Secretary

Department of Electronics & Information Technology

Ministry of Communications & Information Technology

Government of India

8/11/2019 IESA FS Report Indian ESDM Market

http://slidepdf.com/reader/full/iesa-fs-report-indian-esdm-market 4/172

COPYRIGHT

All content included in this study, such as text, graphics, logos, images, data compilations, etc. is the property of India Electronics & Semiconductor

Association (“IESA”). The study is for customers’ internal use and not for general publication or disclosure to third parties. No part of this study may

be given, lent, resold, or disclosed to non-customers or exploited for any commercial purposes. Furthermore, the Study in its entirety or any part

cannot be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording,

or otherwise, without the prior written consent of IESA.

DISCLAIMER OF WARRANTIES AND LIMITATION OF LIABILITY

This study is provided by IESA on an “as is” and “as available” basis. IESA has provided information that is provided by market par ticipants, survey

respondents and secondary research of publicly available information. IESA takes no responsibility for any incorrect information supplied to us

by market participants (manufacturers or users). Quantitative market information is based primarily on interviews and therefore is subject to

fluctuation. No claims are made for the accuracy or applicability of the information to any specific situation.

IESA makes no representations or warranties of any kind, express or implied, as to the information, content, materials, etc., included in this study.

The user of the study shall do so at the user’s sole risk. In the event the user intends taking any steps that could have an adverse effect on the users

business, IESA expressly states that the user should consult its legal, tax or other advisors, in order to protect the interests of the user, which maybe

specific from case to case. It is emphasized that IESA has participated in preparation of this study in an independent manner and should not be

construed as necessarily being reflective of the views or position of any individual member company of the IESA or of the representatives of such

member companies that may serve on the IESA’s executive council or other member forums.

To the full extent permissible by applicable law, IESA disclaims all warranties, express or implied, including, but not limited to, implied warranties of

merchantability and fitness for a particular p urpose. IESA will not be liab le for any damages of any kind arising from the use of this study, including,

but not limited to direct, indirect, incidental, punitive, and consequential damages.

Copyright © 2014, India Electronics & Semiconductor Association

India Electronics & Semiconductor Association

Prestige Terminus II, Unit-G-02, 901, Ground Floor,

Civil Aviation Road, (HAL Old Airport Exit Road),Konena Agrahara, Bangalore - 560017

Phone: +91 80 4147 3250

Facsimile: +91 80 4122 1866

Email: [email protected]: www.iesaonline.org

IESA is the premier trade body representing the Indian Electronic System Design and Manufacturing ESDM industry and has represented it since

2005. It has over 200 members - both domestic and multinational enterprises. IESA is committed towards building global awareness for the Indian

ESDM industry and supporting its growth through focused initiatives in developing the ecosystem. This is through publishing credible data,

networking events and alliances with other international associations IESA works closely with the Government as a knowledge partner on the

sector, both at the centre and at the state level.

www.iesaonline.org

The material in this publication is copyrighted. No part of this book can be reproduced either on paper or on electronic media without permissionin writing from the publisher. Requests for permission to reproduce portions of it should be sent to the IESA at the above address.

First print: January 2014

Published by:

India Electronics & Semiconductor Association, Bangalore

Edited by:

Debanjan Sinha, IESA

Designed by:

Cocoon Creative Concepts, Bangalore

8/11/2019 IESA FS Report Indian ESDM Market

http://slidepdf.com/reader/full/iesa-fs-report-indian-esdm-market 5/172

Indian ESDM Market

ANALYSIS OF OPPORTUNITY AND GROWTH PLANAn IESA - Frost & Sullivan Report

Assessment of challenges and identification of steps to develop ecosystem and

increase indigenous value addition for top 25 high priority electronic products

and corresponding components market

Supported by the Department of Electronics & Information Technology,

Ministry of Communications & Information Technology

Government of India

8/11/2019 IESA FS Report Indian ESDM Market

http://slidepdf.com/reader/full/iesa-fs-report-indian-esdm-market 6/172

Acknowledgements

The research report on the Indian ESDM industry will be incomplete without acknowledging the contribution of all the

individuals associated with this exercise. These individuals have been untiring in their efforts to bring in their wealth of

experience and knowledge base to add value to the exercise. The research exercise could leverage their acumen and count on

their unwavering support till the stage of its completion.

India Electronics & Semiconductor Association and Frost & Sullivan would wish to thank them wholeheartedly for their valuable

time and guidance whenever we needed them.

8/11/2019 IESA FS Report Indian ESDM Market

http://slidepdf.com/reader/full/iesa-fs-report-indian-esdm-market 7/172

Room No : 105, Sanchar Bhawan, 20 Ashoka Road, New Delhi - 110001

Phone: 91-11-23739191, 23372177 Fax: 91-11-23723330

MESSAGE

The India ESDM industry presents a huge opportunity and is expected to

emerge as a vital contributor to the nation’s economy. While we continue to dominate

the high-end semiconductor design space, we are also seeing a major shift in focus

from just design to end-to-end product conception and manufacturing to truly

dominate the global ESDM industry.

The Department of Electronics and Information Technology (DeitY),

Government of India has been actively working towards reviving indigenous

manufacturing in a big way. IESA has also played a prominent role in supporting the

Government in its initiatives.

In order to realize the vision of the ESDM industry, we would need to promote

the opportunities presented by the ESDM industry to attract investments in the sector.

As the electronic products have a pervasive role in all industry verticals, it is desirablethat the industry reports on the market opportunities in key products are carried out,

which would serve as useful reference to the various stakeholders, and, thereby, help

them in taking informed decisions on their plans of investing in India.

The IESA - Frost & Sullivan Report 2014 on the ‘ Indian ESDM Market-

Analysis of Opportunity and Growth Plan’ is a right step in this direction. This report

includes an extensive study and analysis of the top 25 high priority electronic

products and their related components in the Indian ESDM industry. This report also

gives insightful information on resolving the current challenges and the

recommendations to move ahead.

I congratulate DeitY and IESA for putting together this important and timely

report for the benefit of all the stakeholders of the Indian ESDM industry. I am sure it

will help us in achieving our vision of taking India to global leadership in the ESDM

industry.

(KAPIL SIBAL)

8/11/2019 IESA FS Report Indian ESDM Market

http://slidepdf.com/reader/full/iesa-fs-report-indian-esdm-market 8/172

8/11/2019 IESA FS Report Indian ESDM Market

http://slidepdf.com/reader/full/iesa-fs-report-indian-esdm-market 9/172

Message

With the Indian ESDM industry is expected to touch the USD 400 billion

mark in the coming decade, the Government of India has identied the

electronics hardware manufacturing sector as a major thrust area for the

country. IESA has done a commendable job of catalysing the growth of thedomestic ESDM industry and is relentlessly working towards this objective.

Taking cognizance of the demands of the economy and the industry, the

Government of India has taken a number of steps to promote the Indian

ESDM industry.

The Department of Electronics & Information Technology (DeitY) and IESA,

as the Knowledge Partner to the Government, have brought out the report on

‘Indian ESDM Market – Analysis of Opportunity and Growth Plan’. This report

identies the top 25 electronics product markets with large opportunities anddraws a roadmap for their growth. It also identies the major components

used in these products and evaluates strategies to promote their ecosystem

in India.

I am sure that this credible report would be extremely valuable for decision

makers both in the government and the industry. I congratulate DeitY and

IESA for their excellent work in putting together this informative and timely

report.

(J. Satyanarayana)

New Delhi

January 02, 2014

8/11/2019 IESA FS Report Indian ESDM Market

http://slidepdf.com/reader/full/iesa-fs-report-indian-esdm-market 10/172

8/11/2019 IESA FS Report Indian ESDM Market

http://slidepdf.com/reader/full/iesa-fs-report-indian-esdm-market 11/172

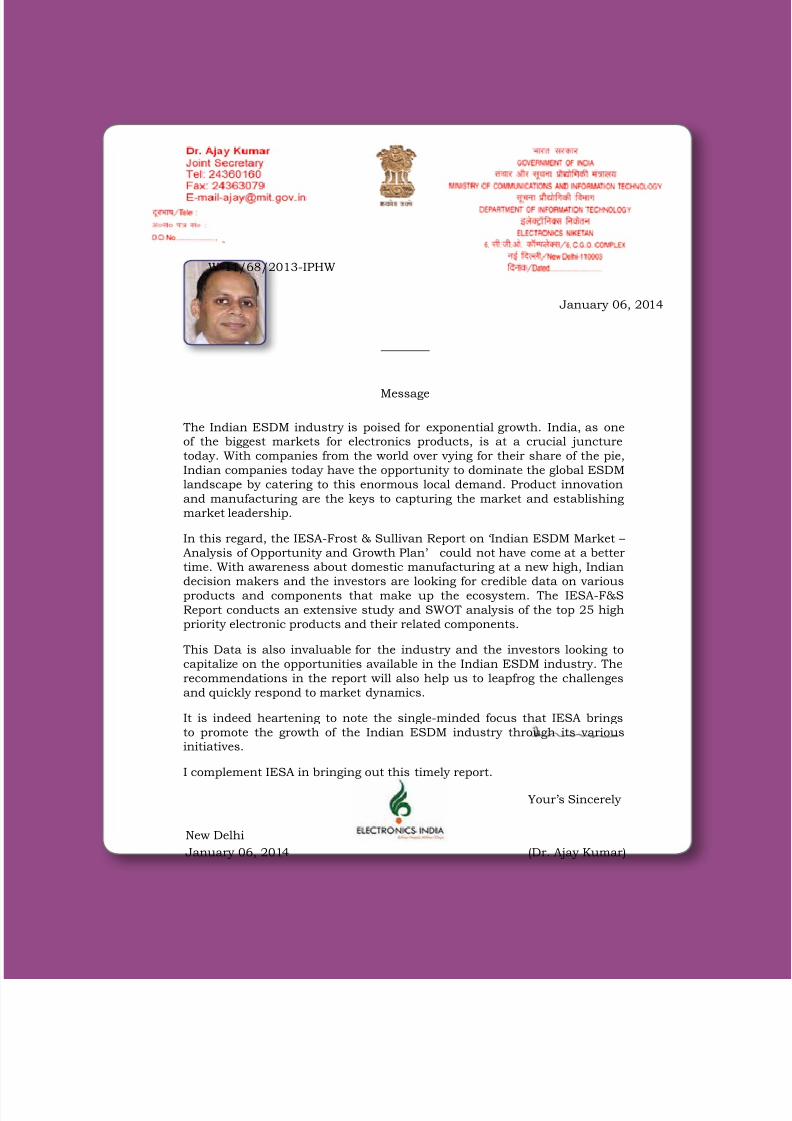

Message

The Indian ESDM industry is poised for exponential growth. India, as oneof the biggest markets for electronics products, is at a crucial juncture

today. With companies from the world over vying for their share of the pie,

Indian companies today have the opportunity to dominate the global ESDM

landscape by catering to this enormous local demand. Product innovation

and manufacturing are the keys to capturing the market and establishing

market leadership.

In this regard, the IESA-Frost & Sullivan Report on ‘Indian ESDM Market –

Analysis of Opportunity and Growth Plan’ could not have come at a bettertime. With awareness about domestic manufacturing at a new high, Indian

decision makers and the investors are looking for credible data on various

products and components that make up the ecosystem. The IESA-F&S

Report conducts an extensive study and SWOT analysis of the top 25 high

priority electronic products and their related components.

This Data is also invaluable for the industry and the investors looking to

capitalize on the opportunities available in the Indian ESDM industry. The

recommendations in the report will also help us to leapfrog the challenges

and quickly respond to market dynamics.

It is indeed heartening to note the single-minded focus that IESA brings

to promote the growth of the Indian ESDM industry through its variousinitiatives.

I complement IESA in bringing out this timely report.

New Delhi

January 06, 2014

Your’s Sincerely

(Dr. Ajay Kumar)

W-11/68/2013-IPHW

January 06, 2014

8/11/2019 IESA FS Report Indian ESDM Market

http://slidepdf.com/reader/full/iesa-fs-report-indian-esdm-market 12/172

8/11/2019 IESA FS Report Indian ESDM Market

http://slidepdf.com/reader/full/iesa-fs-report-indian-esdm-market 13/172

Table of Contents

Foreword 15

Preface 17Executive Summary 19

Top 10 Products and Components Markets to Focus for

Near Term Local Value Addition Improvement33

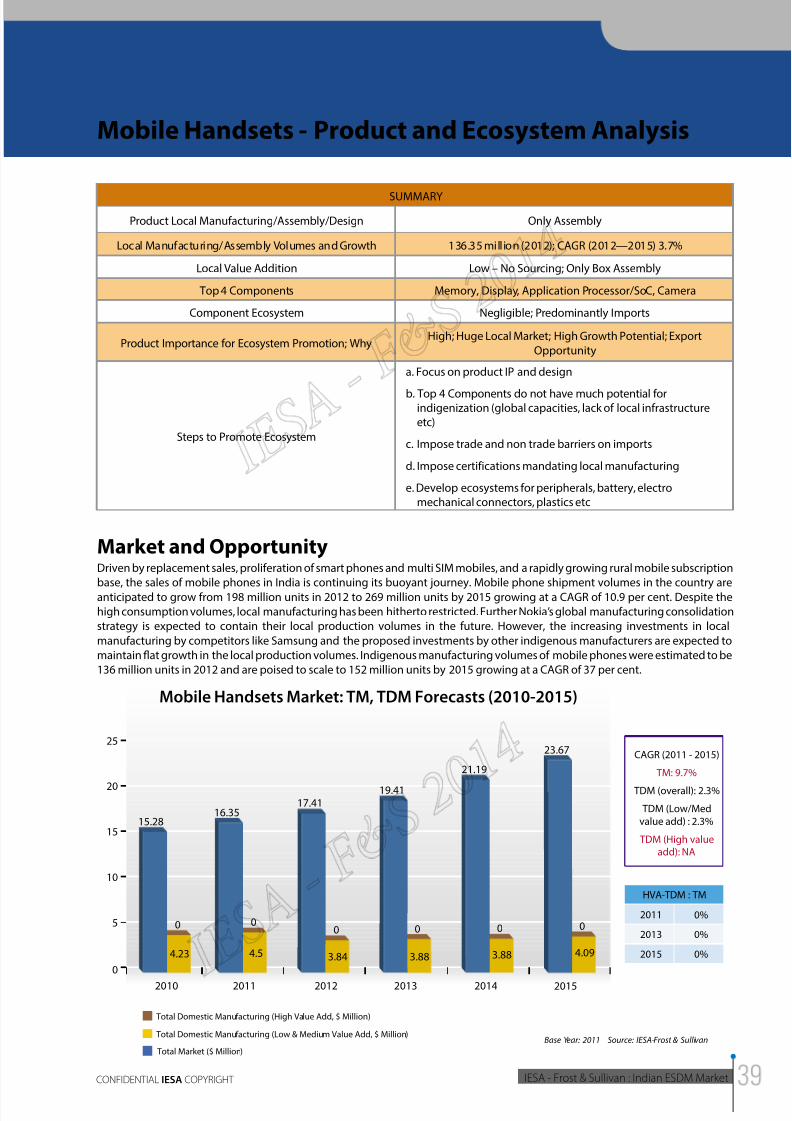

Mobile Handsets - Product and Ecosystem Analysis 39

Flat Panel Display TV - Product and Ecosystem Analysis 45

Notebooks - Product and Ecosystem Analysis 49

Desktops - Product and Ecosystem Analysis 53

Digital Camera - Product and Ecosystem Analysis 59

Inverters and UPS - Product and Ecosystem Analysis 65

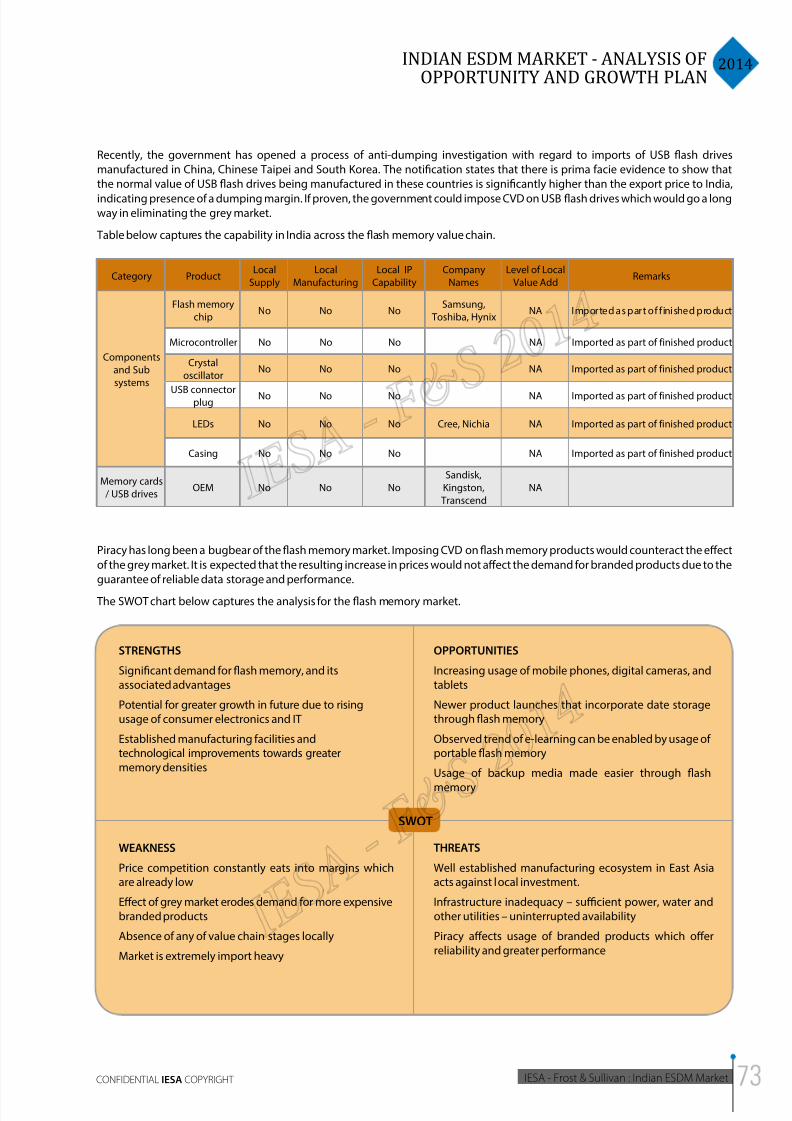

Memory Cards and USB drives - Product and Ecosystem Analysis 71

4W EMS - Product and Ecosystem Analysis 75

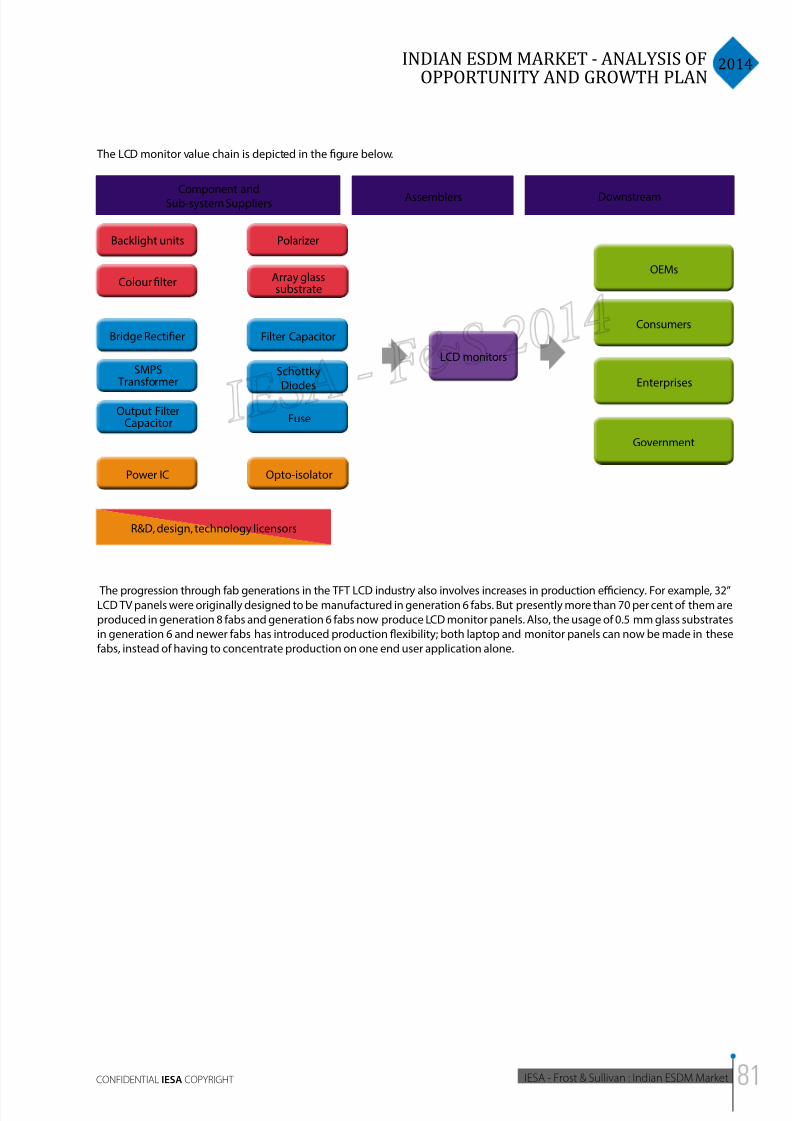

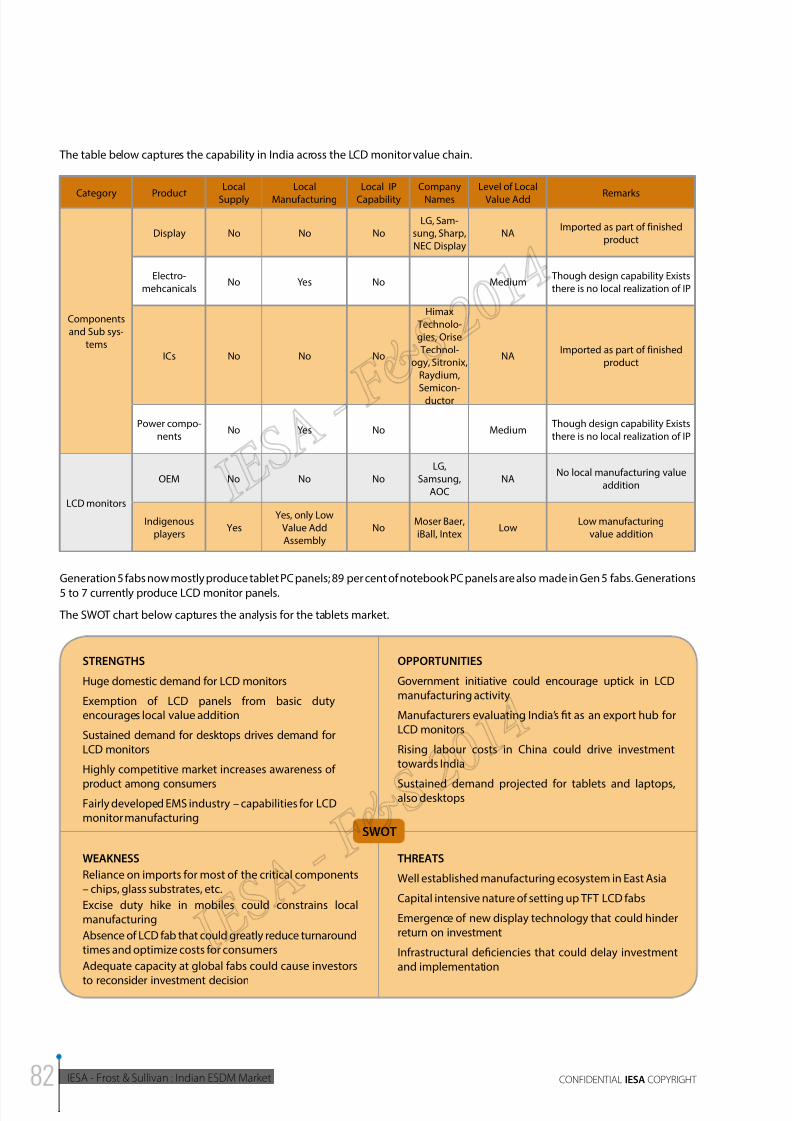

LCD Monitor - Product and Ecosystem Analysis 79

Servers - Product and Ecosystem Analysis 85

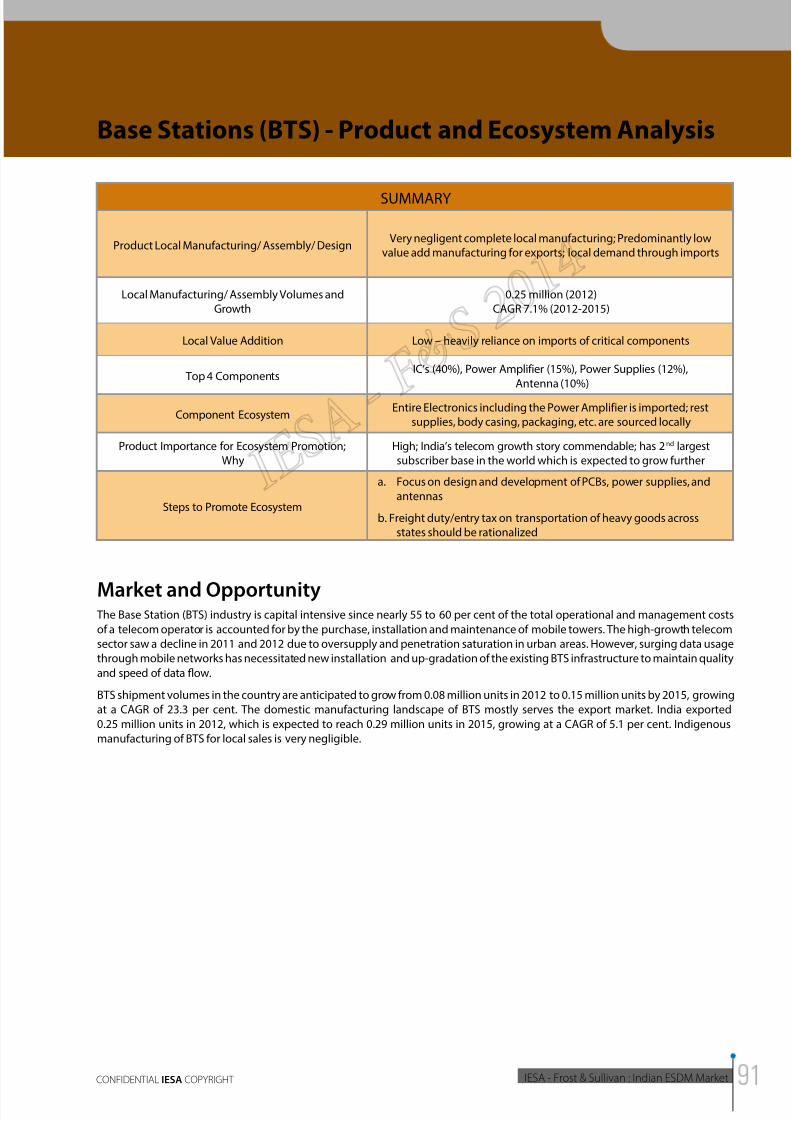

Base Stations (BTS) - Product and Ecosystem Analysis 91Power supplies - Product and Ecosystem Analysis 97

Set Top Boxes - Product and Ecosystem Analysis 101

Printers and MFDs - Product and Ecosystem Analysis 107

Router/Switches - Product and Ecosystem Analysis 113

Car Radio - Product and Ecosystem Analysis 117

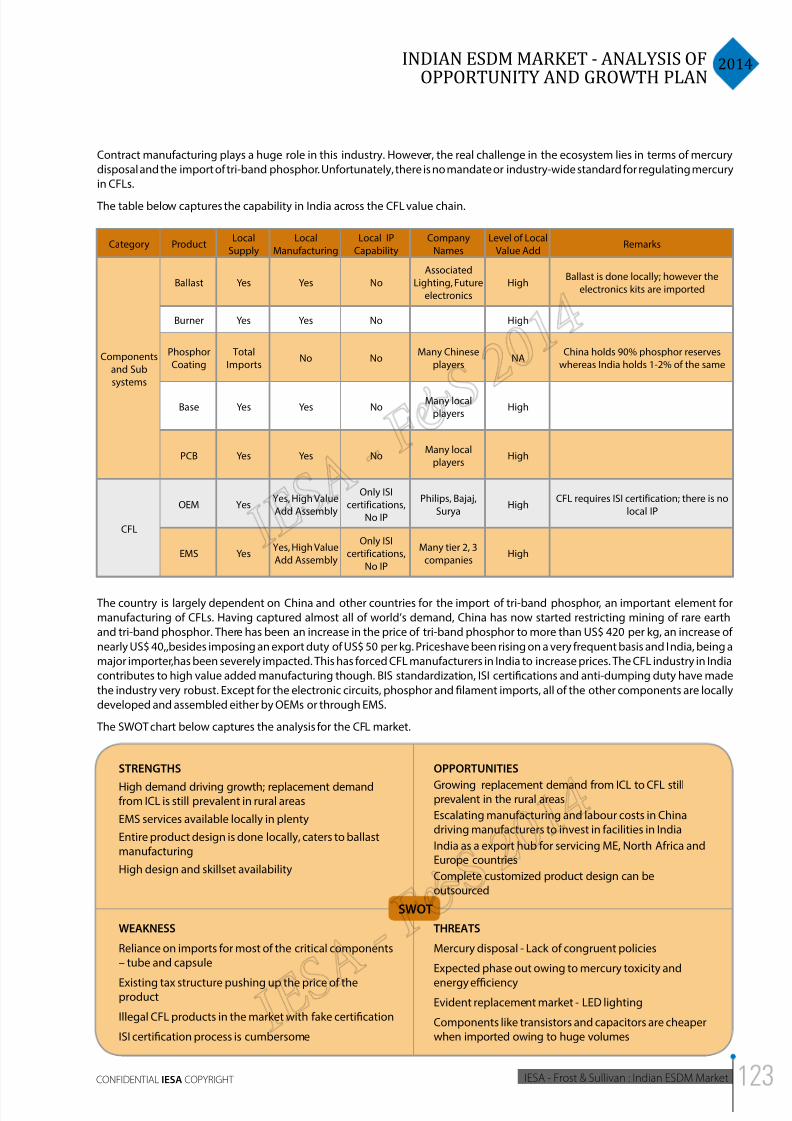

CFL - Product and Ecosystem Analysis 121

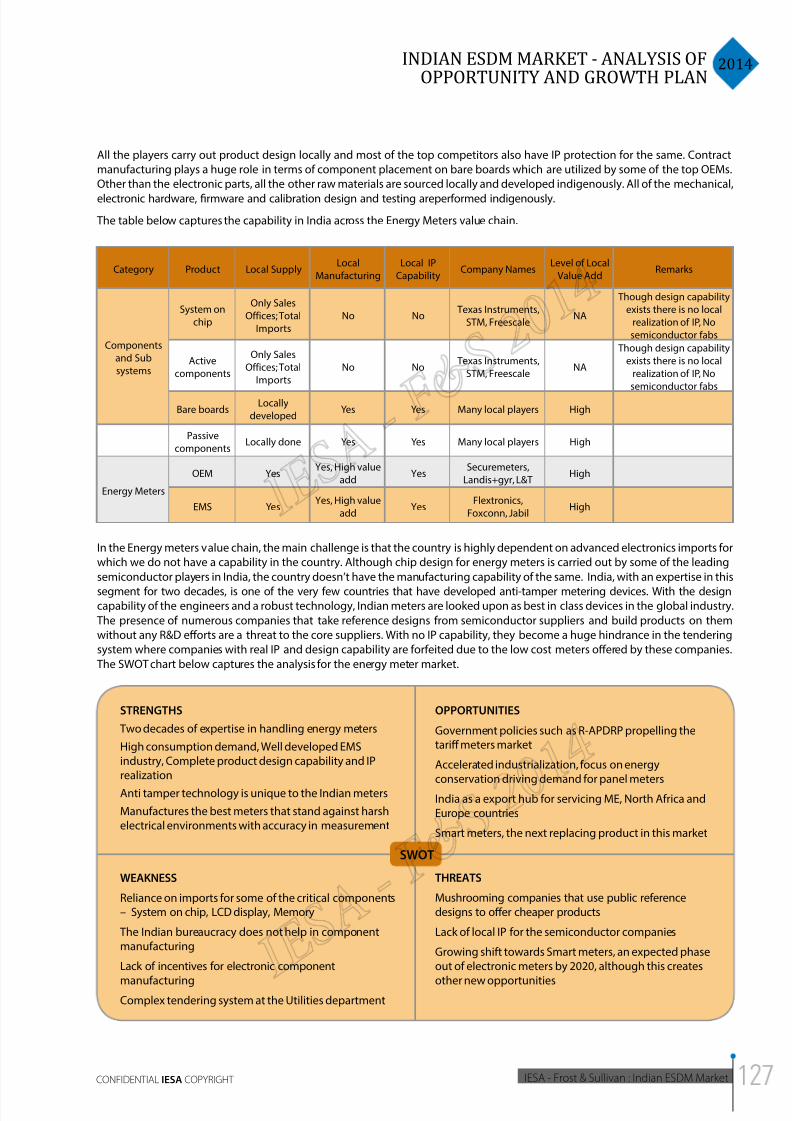

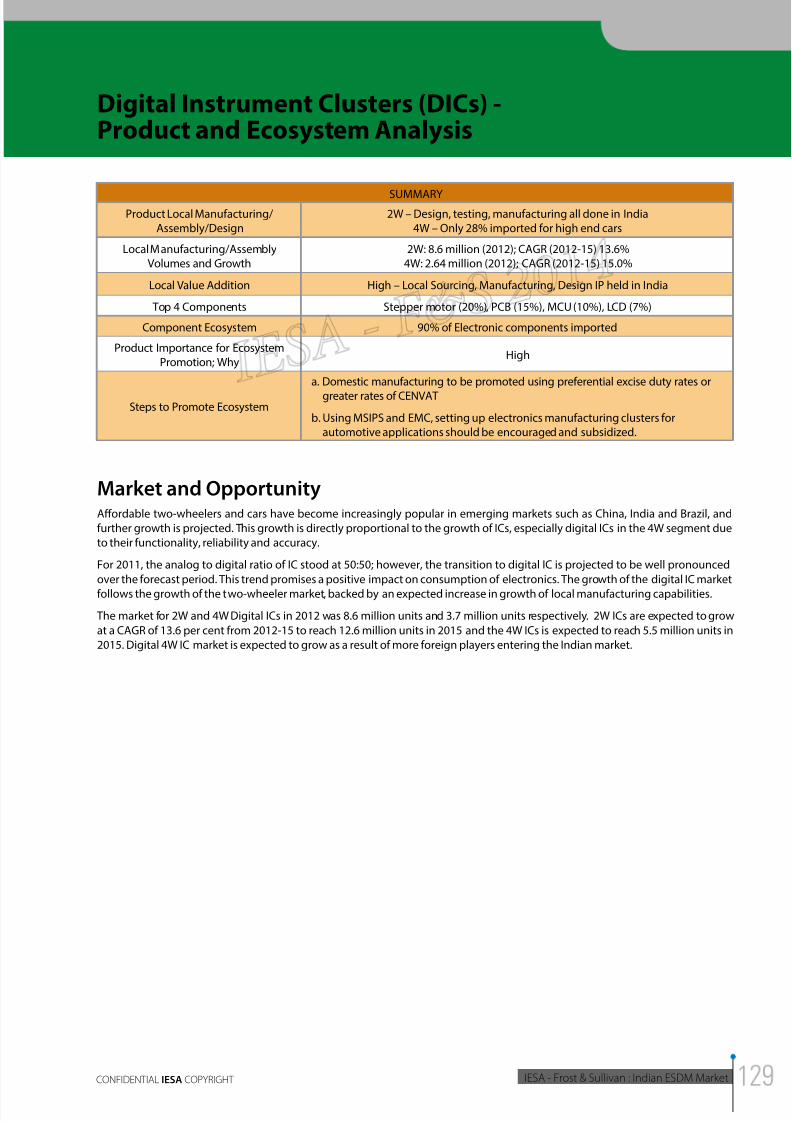

Energy Meters - Product and Ecosystem Analysis 125Digital Instrument Clusters (DICs) - Product and Ecosystem Analysis 129

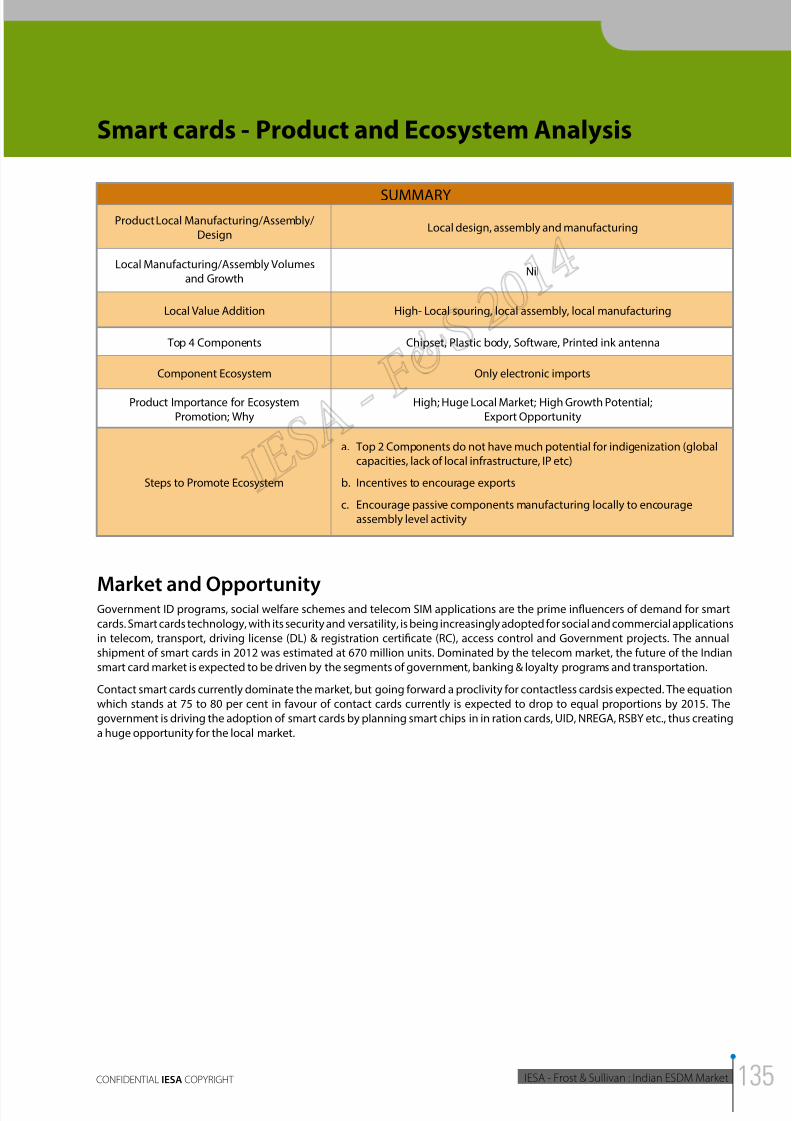

Smart cards - Product and Ecosystem Analysis 135

GPON ONT - Product and Ecosystem Analysis 141

Tablets - Product and Ecosystem Analysis 145

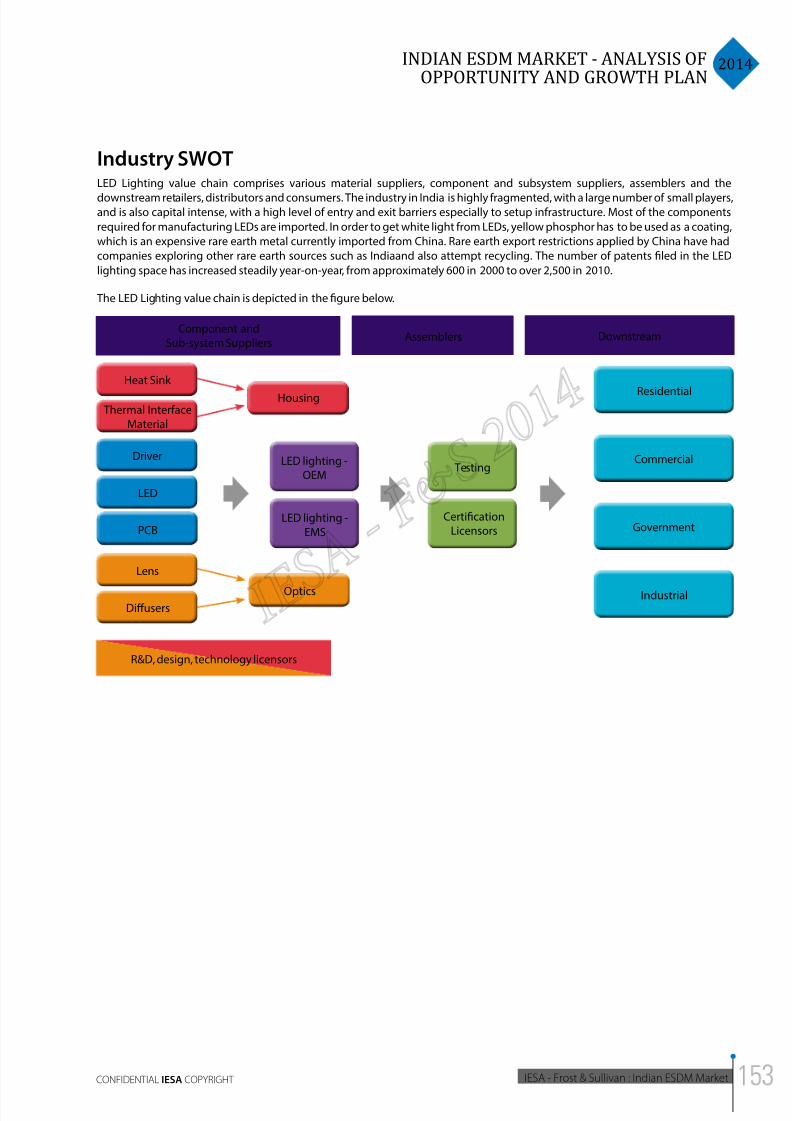

LED Lighting - Product and Ecosystem Analysis 151

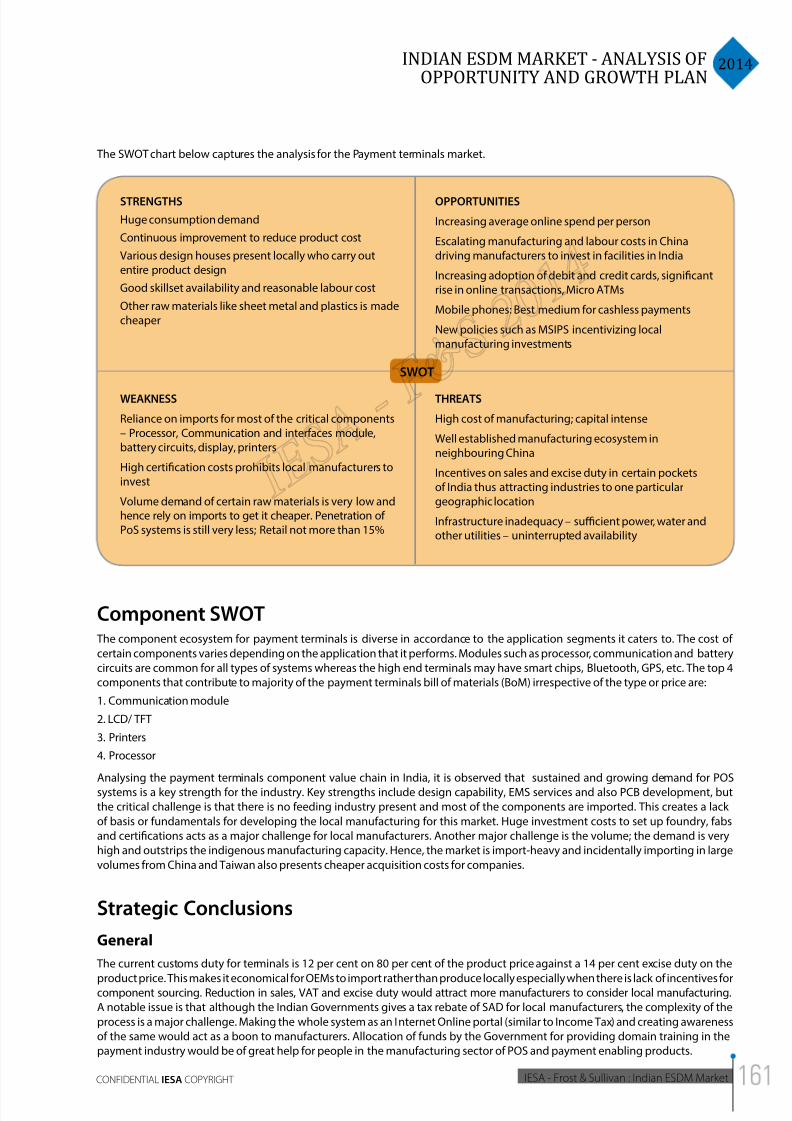

Payment Terminals - Product and Ecosystem Analysis 157

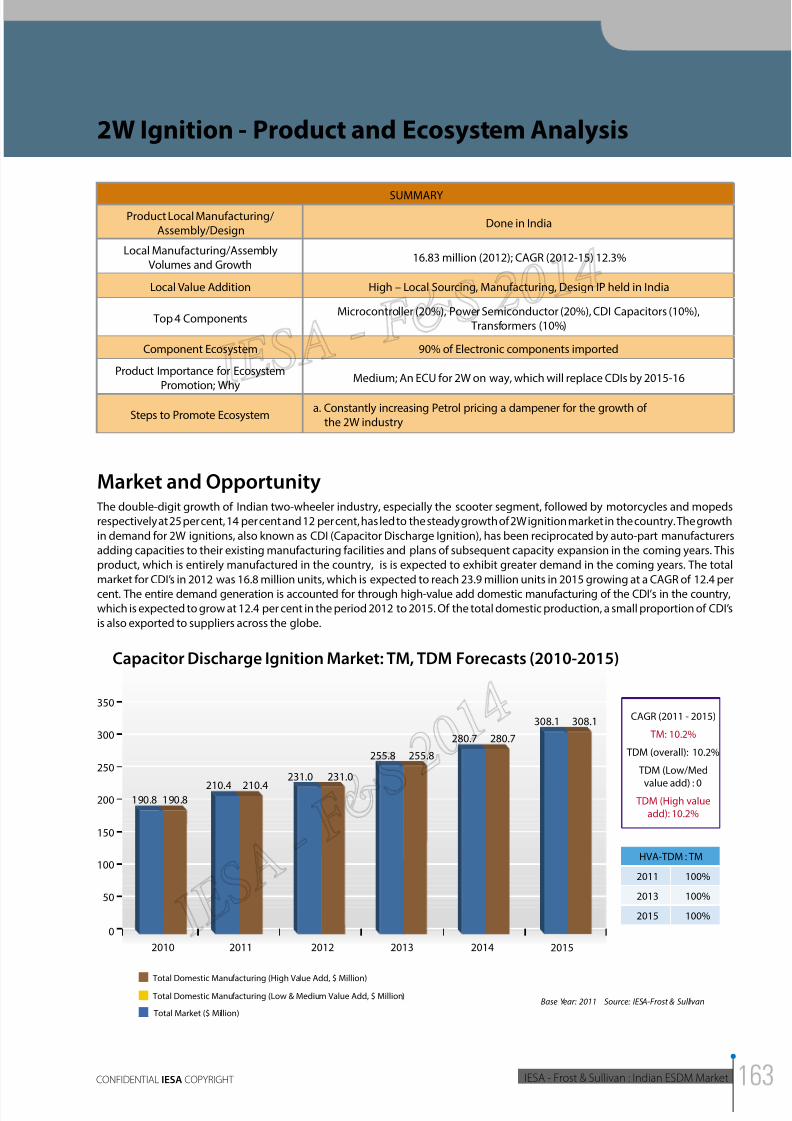

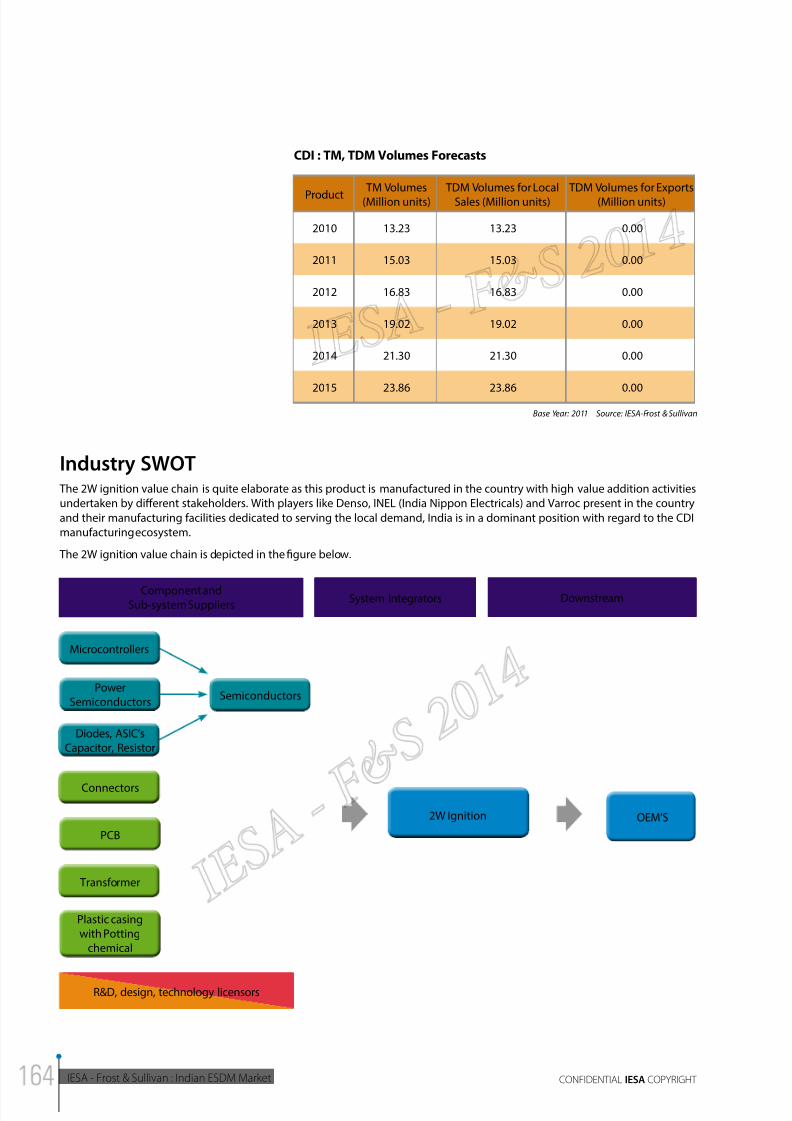

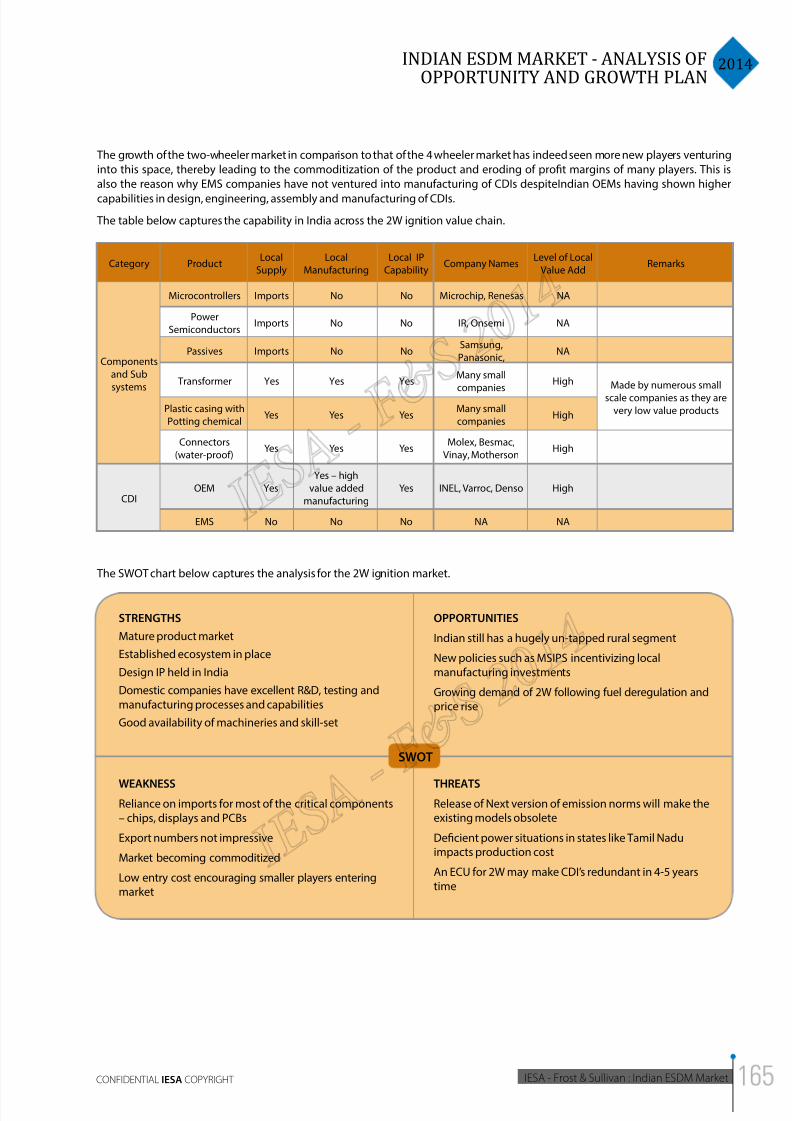

2W Ignition - Product and Ecosystem Analysis 163Appendix 167

8/11/2019 IESA FS Report Indian ESDM Market

http://slidepdf.com/reader/full/iesa-fs-report-indian-esdm-market 14/172

8/11/2019 IESA FS Report Indian ESDM Market

http://slidepdf.com/reader/full/iesa-fs-report-indian-esdm-market 15/172

Foreword

The Indian electronics system design and manufacturing (ESDM) industry is at a huge inflection point.

From being predominantly consumption driven, the Indian ESDM industry has a major potential to

become a design led manufacturing industry. Concerted efforts from both the Government and the

industry are required to propel the Indian ESDM industry into one of the critical GDP contributors

in the near future.

The Indian Electronics and Semiconductor Association (IESA), a premier representative body for the

ESDM industry in India commissioned a full-fledged research in its efforts to map the current status

and future opportunities in the industry. The objective of the report was to establish the current

status of all the value chain components in the ESDM industry and identify the growth trends. This

exhaustive report developed by IESA’s consulting partner, Frost & Sullivan, and released in early

2013 is the only authentic detailed report on the overall ESDM industry in India. As a next step, there

was the pertinent need to identify the high growth product markets within the overall electronics

industry and do a deep dive evaluation of the existing ecosystem for these products. This study

would help identify the appropriate initiatives needed for further developing the ecosystem for

these high priority products.

The Department of Electronics and Information Technology (DeitY) has been very active in

formulating and announcing various policy measures aimed at developing the ESDM industry in

India. To ensure the effective implementation of these policies and for directing the focus in the right

direction, this extended analysis of the top 25 high priority electronic products was commissioned

by IESA.

The report on the ecosystem SWOT analysis of the top 25 high priority products covers the following

product markets:

1. Mobile Phones

2. Flat Panel Display (FPD) TV

3. Notebooks

4. Desktops

5. Digital Cameras

6. Inverters and UPS

7. Memory Cards and USB Drives

8. 4W EMS

9. LCD Monitors

10. Servers

11. Base Stations

12. Power Supplies

13. Set Top Box

14. Printers and MFD

15. Routers and Switches

16. Car Radio

17. CFL

18. Energy Meters

19. Digital Instrument Clusters

20. Smart Cards

21. PON, GPON ONT

22. Tablets

23. LED Lighting

24. Payment Terminals

25. 2W Ignition

8/11/2019 IESA FS Report Indian ESDM Market

http://slidepdf.com/reader/full/iesa-fs-report-indian-esdm-market 16/172

8/11/2019 IESA FS Report Indian ESDM Market

http://slidepdf.com/reader/full/iesa-fs-report-indian-esdm-market 17/172

Preface

IESA is today recognized as the most credible voice of the Indian ESDM industry. As

the knowledge partner to the Government of India and the foremost trade body

representing the interests of over 200 member companies in the Indian ESDM

landscape, IESA regularly undertakes research and publication activities. The IESA-Frost & Sullivan annual report on the Indian ESDM industry is one such report that

is much awaited and widely referred by decision makers in the government as well

as the industry.

The IESA- Frost & Sullivan report 2014 is the seventh publication since its inception

in 2005. This year we have conducted an extensive study and SWOT analysis on

the Top 25 high priority electronic products and their related components in the

Indian ESDM industry. As we aggressively promote indigenous manufacturing

and reduction of our dependence on imports, this report aims to uncover the

challenges associated with manufacturing these top 25 electronic products and

associated components domestically.

The findings of the report are interesting. And as always, we have proposed a range

of measures to overcome these challenges and kick-start high-value addition

manufacturing activities in a big way in India.

We sincerely hope that you will find these facts and statistics beneficial for strategic

decision making and join us in taking the right steps to further enrich the Indian

ESDM industry.

Mr. Sanjeev Keskar

Chairman

Mr. PVG Menon

President

8/11/2019 IESA FS Report Indian ESDM Market

http://slidepdf.com/reader/full/iesa-fs-report-indian-esdm-market 18/172

8/11/2019 IESA FS Report Indian ESDM Market

http://slidepdf.com/reader/full/iesa-fs-report-indian-esdm-market 19/172

2014INDIAN ESDM MARKET - ANALYSIS OF

OPPORTUNITY AND GROWTH PLAN

IESA - Frost & Sullivan : Indian ESDM MarketCONFIDENTIAL IESA COPYRIGHT

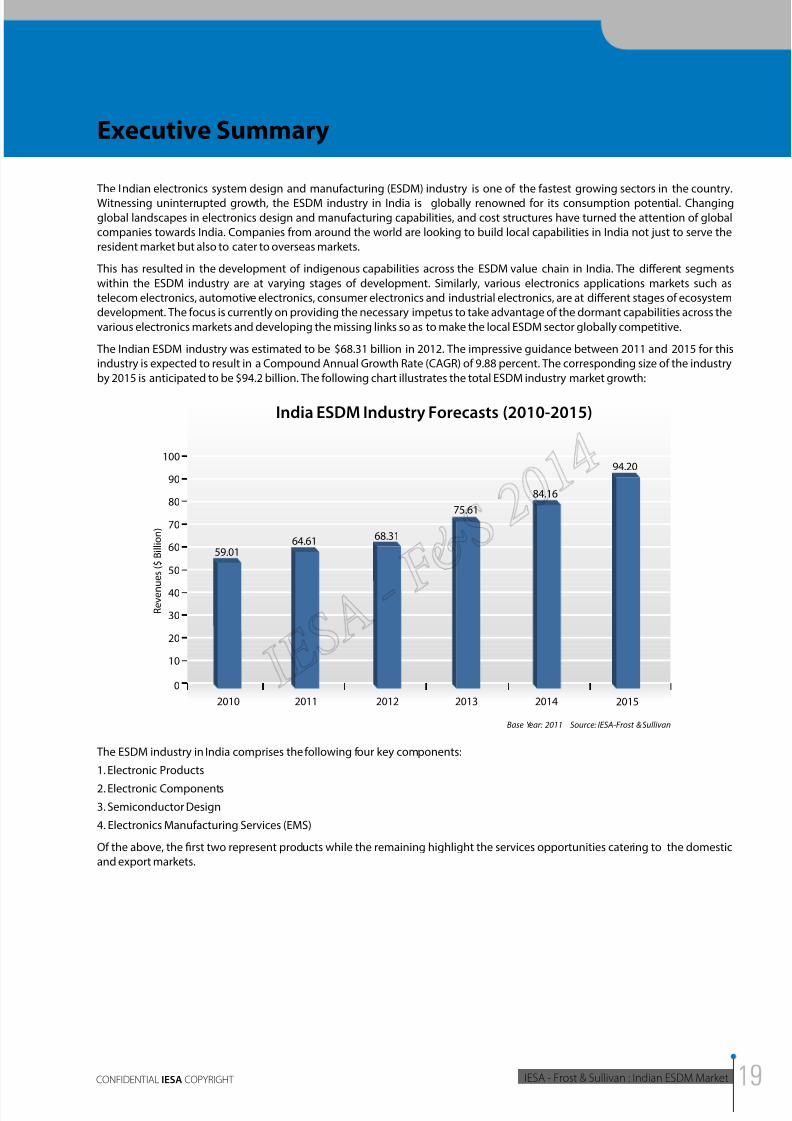

Executive Summary

The Indian electronics system design and manufacturing (ESDM) industry is one of the fastest growing sectors in the country.

Witnessing uninterrupted growth, the ESDM industry in India is globally renowned for its consumption potential. Changing

global landscapes in electronics design and manufacturing capabilities, and cost structures have turned the attention of global

companies towards India. Companies from around the world are looking to build local capabilities in India not just to serve the

resident market but also to cater to overseas markets.

This has resulted in the development of indigenous capabilities across the ESDM value chain in India. The different segments

within the ESDM industry are at varying stages of development. Similarly, various electronics applications markets such as

telecom electronics, automotive electronics, consumer electronics and industrial electronics, are at different stages of ecosystem

development. The focus is currently on providing the necessary impetus to take advantage of the dormant capabilities across the

various electronics markets and developing the missing links so as to make the local ESDM sector globally competitive.

The Indian ESDM industry was estimated to be $68.31 billion in 2012. The impressive guidance between 2011 and 2015 for this

industry is expected to result in a Compound Annual Growth Rate (CAGR) of 9.88 percent. The corresponding size of the industry

by 2015 is anticipated to be $94.2 billion. The following chart illustrates the total ESDM industry market growth:

94.20

0

10

20

30

40

50

70

80

90

100

60

20112010 2012 2013 2014 2015

India ESDM Industry Forecasts (2010-2015)

Base Year: 2011 Source: IESA-Frost & Sullivan

R e v e n

u e s ( $

B i l l i o n )

84.16

75.61

68.3164.61

59.01

The ESDM industry in India comprises the following four key components:

1. Electronic Products

2. Electronic Components

3. Semiconductor Design

4. Electronics Manufacturing Services (EMS)

Of the above, the first two represent products while the remaining highlight the services opportunities catering to the domestic

and export markets.

8/11/2019 IESA FS Report Indian ESDM Market

http://slidepdf.com/reader/full/iesa-fs-report-indian-esdm-market 20/172

IESA - Frost & Sullivan : Indian ESDM Market CONFIDENTIAL IESA COPYRIGHT

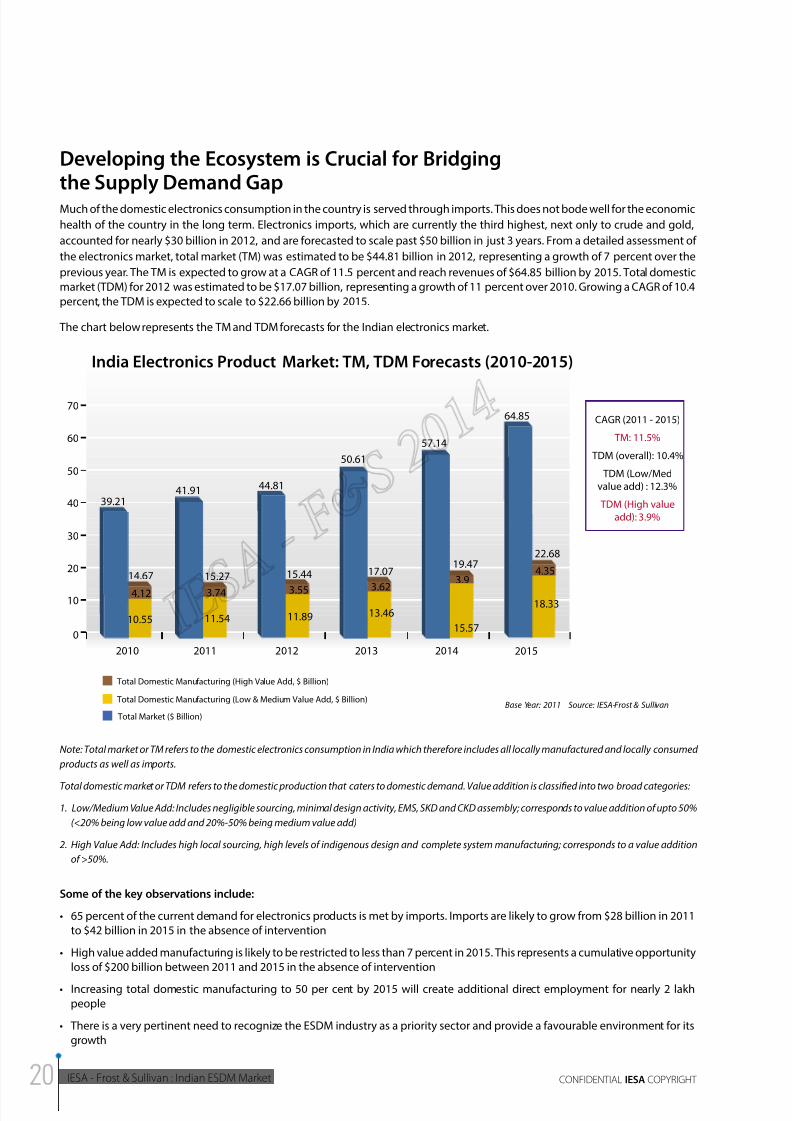

Developing the Ecosystem is Crucial for Bridgingthe Supply Demand GapMuch of the domestic electronics consumption in the country is served through imports. This does not bode well for the economic

health of the country in the long term. Electronics imports, which are currently the third highest, next only to crude and gold,

accounted for nearly $30 billion in 2012, and are forecasted to scale past $50 billion in just 3 years. From a detailed assessment of

the electronics market, total market (TM) was estimated to be $44.81 billion in 2012, representing a growth of 7 percent over the

previous year. The TM is expected to grow at a CAGR of 11.5 percent and reach revenues of $64.85 billion by 2015. Total domestic

market (TDM) for 2012 was estimated to be $17.07 billion, representing a growth of 11 percent over 2010. Growing a CAGR of 10.4

percent, the TDM is expected to scale to $22.66 billion by 2015.

The chart below represents the TM and TDM forecasts for the Indian electronics market.

64.85

22.68

0

10

20

30

40

50

70

60

20112010 2012 2013 2014 2015

India Electronics Product Market: TM, TDM Forecasts (2010-2015)

Total Market ($ Billion)

Total Domestic Manufacturing (High Value Add, $ Billion)

Total Domestic Manufacturing (Low & Medium Value Add, $ Billion)Base Year: 2011 Source: IESA-Frost & Sullivan

CAGR (2011 - 2015)

TM: 11.5%

TDM (overall): 10.4%

TDM (Low/Med

value add) : 12.3%

TDM (High value

add): 3.9%

18.33

15.57

19.47

57.14

50.61

17.07

13.46

44.81

15.44

11.8911.54

15.27

41.91

14.67

39.21

10.55

4.12 3.74 3.55 3.62

3.94.35

Note: Total market or TM refers to the domestic electronics consumption in India which therefore includes all locally manufactured and locally consumed

products as well as imports.

Total domestic market or TDM refers to the domestic production that caters to domestic demand. Value addition is classified into two broad categories:

1. Low/Medium Value Add: Includes negligible sourcing, minimal design activity, EMS, SKD and CKD assembly; corresponds to value addition of upto 50%

(<20% being low value add and 20%-50% being medium value add)

2. High Value Add: Includes high local sourcing, high levels of indigenous design and complete system manufacturing; corresponds to a value addition

of >50%.

Some of the key observations include:

• 65 percent of the current demand for electronics products is met by imports. Imports are likely to grow from $28 billion in 2011

to $42 billion in 2015 in the absence of intervention

• High value added manufacturing is likely to be restricted to less than 7 percent in 2015. This represents a cumulative opportunity

loss of $200 billion between 2011 and 2015 in the absence of intervention

• Increasing total domestic manufacturing to 50 per cent by 2015 will create additional direct employment for nearly 2 lakh

people

• There is a very pertinent need to recognize the ESDM industry as a priority sector and provide a favourable environment for its

growth

8/11/2019 IESA FS Report Indian ESDM Market

http://slidepdf.com/reader/full/iesa-fs-report-indian-esdm-market 21/172

2014INDIAN ESDM MARKET - ANALYSIS OF

OPPORTUNITY AND GROWTH PLAN

IESA - Frost & Sullivan : Indian ESDM MarketCONFIDENTIAL IESA COPYRIGHT

Government as an Enabler for the ESDM Sector The Indian Government, through the Department of Electronics and Information Technology (DeitY), has instituted a number of

forward-looking policies to foster the growth of the Indian electronics ecosystem. These policies are aimed at holistic development

of the ESDM industry by offering specific incentives for the development of each element in the value chain. These forward looking

policy measures include:

National Policy on Electronics (NPE): The objective of the NPE is to create an ecosystem for a globally competitive

ESDM sector in the country by attracting investment of about USD 100 billion and generating employment for around 28 million

people at various levels. The ultimate aim of the policy is for the Indian ESDM sector to develop core competencies in strategic and

core infrastructure sectors like telecommunications, automobile, avionics, industrial, medical, solar, information and broadcasting,

railways, intelligent transport systems, etc.

National Manufacturing Policy (NMP): The government has brought out the NMP to increase the growth of the

manufacturing sector to 12 to 14 percent over the medium term and enable manufacturing to contribute at least 25 percent to

the National GDP by 2022.

Modified Special Incentive Package Scheme (MSIPS): The MSIPS aims to offset cost disabilities and attract

investments in the India ESDM sector through an INR 10,000 crore corpus. Subject to certain investment thresholds, subsidies to the

tune of 20 per cent for SEZ units and 25 per cent for non-SEZ units will be given on capital expenditure along with reimbursement

of excise/CVD.

Setting up semiconductor fabrication units: The Government of India has received the applications of two

consortia (IBM, Jaypee Group, TowerJazz; STMicroelectronics, HSMC) to establish 2 semiconductor wafer fabrication units in Gujarat

and Noida with the aim of operating at 20 nm process node within two years of initial operations and reaching a capacity of at least

40,000 WSPM of at least 300 mm size. Various incentives are being offered by the government to this effect: 25 per cent subsidy

on capital expenditure and growth capital expenditure, reimbursement of CVD and excise duty, exemption from basic customs

duties and 200 per cent deduction on R&D activities, among other incentives such as reimbursement of training costs, deductionfor income tax and various forms of viability gap funding.

Electronic Manufacturing Clusters (EMCs): The government is offering financial support for the development

of EMCs. For greenfield EMCs, assistance will be given up to 50 per cent of the project cost subject to a ceiling of INR 50 crore for

every 100 acres of land. For brownfield EMCs, assistance will be given up to 75 percent of the project cost subject to a ceiling of

INR 50 crore.

Electronics Development Fund (EDF): The EDF aims to create an ecosystem of R&D in electronics in India which

will promote IP generation and large scale manufacturing, while simultaneously fostering the growth of the ESDM ecosystem. The

focus of EDF will largely revolve around small and medium enterprises (SME) in line with the goal of promoting innovation and job

creation.

8/11/2019 IESA FS Report Indian ESDM Market

http://slidepdf.com/reader/full/iesa-fs-report-indian-esdm-market 22/172

IESA - Frost & Sullivan : Indian ESDM Market CONFIDENTIAL IESA COPYRIGHT

The chart below captures the salient features of the various government initiatives to promote the Indian ESDM sector.

To attractinvestment of

USD 100 billionand generate

employment of28 million

Aim to reach20nm process

node within 2 yearsof initial phase,

and reach at least40,000 WSPM of

300 mm

IBM, Jaypee,and TowerJazz;

and STMicroelectronics and

HSMC got approval

in principleto establish 2

semiconductorfabs

MSIPS makesavailable a corpus

of INR 10,000crore to attractinvestment in

ESDM

25% subsidy oncapex; CVD and

excise reimbursed;BCD exempted;

200% R&Ddeduction; etc.

EDF is a plannedscheme of DEITY to

create ecosystemof electronics R&D

and promote IPgeneration

Focus will largelybe on SMEs in line

with the goalsof promoting

innovation and jobcreation

Brownfield: 75 percent of project costsubject to ceiling of

INR 50 crore

Greenfield: 50percent of project

cost subject toceiling of INR 50

crore for every 100acres of land

Financial supportwill be offered fordevelopment of

EMCs to aid growth

of ESDM throughinnovation and

entrepreneurship

Scope of policy

includes:nanoelectronic,semiconductorfab, solar, LED,LCD, passivecomponents,

and EMS

20% Capexsubsidy for SEZ

units; 25% Capexsubsidy for non-SEZ

units and CVD/excise

reimbursed

NPE’s vision is“to createa globally

competitive ESDMecosystem to

meet the country’sneeds and servethe international

market.”

NPE’s missionis to promote

manufacturingand R&D acrossthe value chain,

especially instrategic

electronics

Source: IESA-Frost & Sullivan

Indian ESDM Industry: Snapshot of Government Policies

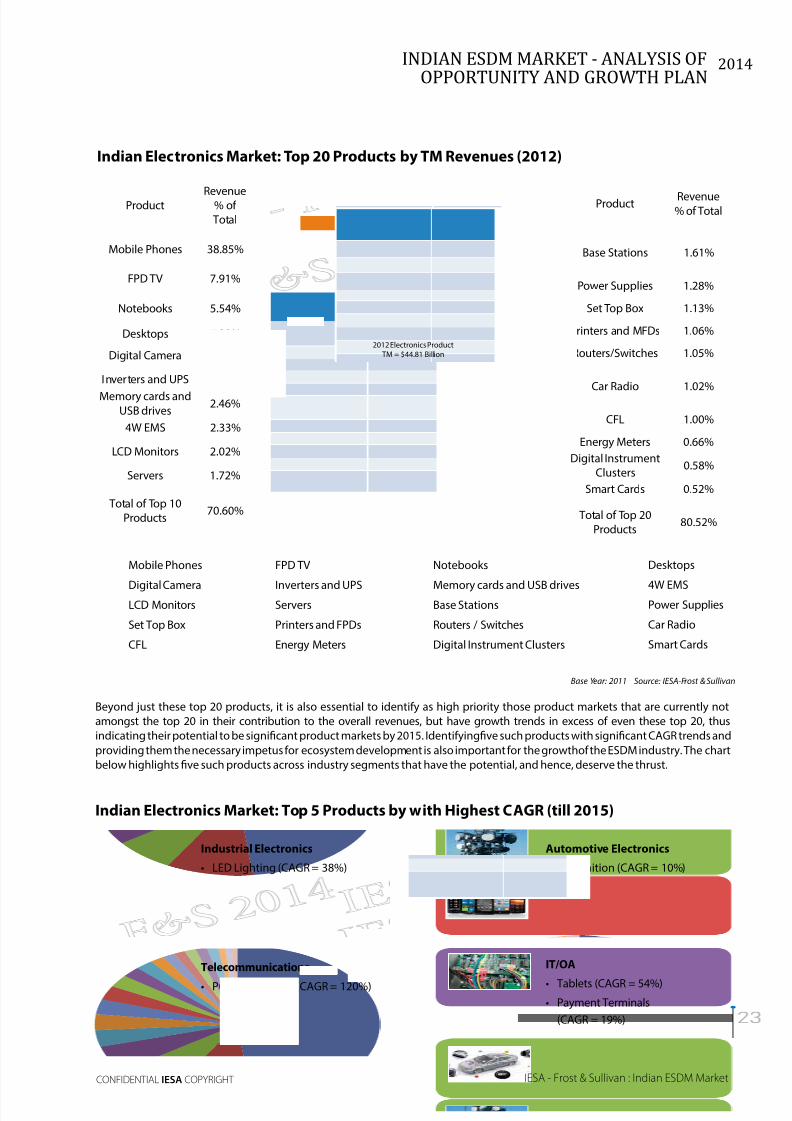

Identification of High Priority Product MarketsHolistic development of the ecosystem can be the panacea to all of the woes of the Indian ESDM industry. However, application of

the Pareto principle at a broad level suggests that identifying the products that accounts for nearly 80 per cent of the electronics

market revenues and provide the necessary support and incentives required to eliminate the disability costs associated with localmanufacturing/value addition in these products shall enable enormous development in the overall ecosystem. Initiatives aimed at

promoting indigenous value addition in the top 20-25 percent of products is expected to have a cascading effect on the remaining

75-80 percent of the products. In line with the Pareto principle, it is observed that the top 20 product markets accounts for 80

percent of the overall electronics TM revenues for 2012, as indicated by the chart next page.

8/11/2019 IESA FS Report Indian ESDM Market

http://slidepdf.com/reader/full/iesa-fs-report-indian-esdm-market 23/172

2014INDIAN ESDM MARKET - ANALYSIS OF

OPPORTUNITY AND GROWTH PLAN

IESA - Frost & Sullivan : Indian ESDM MarketCONFIDENTIAL IESA COPYRIGHT

Mobile Phones

Digital CameraLCD Monitors

Set Top Box

CFL

FPD TV

Inverters and UPSServers

Printers and FPDs

Energy Meters

Notebooks

Memory cards and USB drivesBase Stations

Routers / Switches

Digital Instrument Clusters

Desktops

4W EMSPower Supplies

Car Radio

Smart Cards

Product Revenue% of Total

Mobile Phones 38.85%

FPD TV 7.91%

Notebooks 5.54%

Desktops 4.39%

Digital Camera 2.73%

Inverters and UPS 2.65%

Memory cards andUSB drives

2.46%

4W EMS 2.33%

LCD Monitors 2.02%

Servers 1.72%

Total of Top 10Products

70.60%

Product Revenue% of Total

Base Stations 1.61%

Power Supplies 1.28%

Set Top Box 1.13%

Printers and MFDs 1.06%

Routers/Switches 1.05%

Car Radio 1.02%

CFL 1.00%

Energy Meters 0.66%

Digital InstrumentClusters

0.58%

Smart Cards 0.52%

Total of Top 20Products

80.52%

Indian Electronics Market: Top 20 Products by TM Revenues (2012)

Base Year: 2011 Source: IESA-Frost & Sullivan

Beyond just these top 20 products, it is also essential to identify as high priority those product markets that are currently not

amongst the top 20 in their contribution to the overall revenues, but have growth trends in excess of even these top 20, thus

indicating their potential to be significant product markets by 2015. Identifyingfive such products with significant CAGR trends and

providing them the necessary impetus for ecosystem development is also important for the growthof the ESDM industry. The chart

below highlights five such products across industry segments that have the potential, and hence, deserve the thrust.

Indian Electronics Market: Top 5 Products by with Highest CAGR (till 2015)

Industrial Electronics

• LED Lighting (CAGR = 38%)

Automotive Electronics

• 2W Ignition (CAGR = 10%)

IT/OA

• Tablets (CAGR = 54%)

• Payment Terminals

(CAGR = 19%)

Telecommunications

• PON, GPON ONT (CAGR = 120%)

2012 Electronics Product TM = $44.81 Billion

8/11/2019 IESA FS Report Indian ESDM Market

http://slidepdf.com/reader/full/iesa-fs-report-indian-esdm-market 24/172

IESA - Frost & Sullivan : Indian ESDM Market CONFIDENTIAL IESA COPYRIGHT

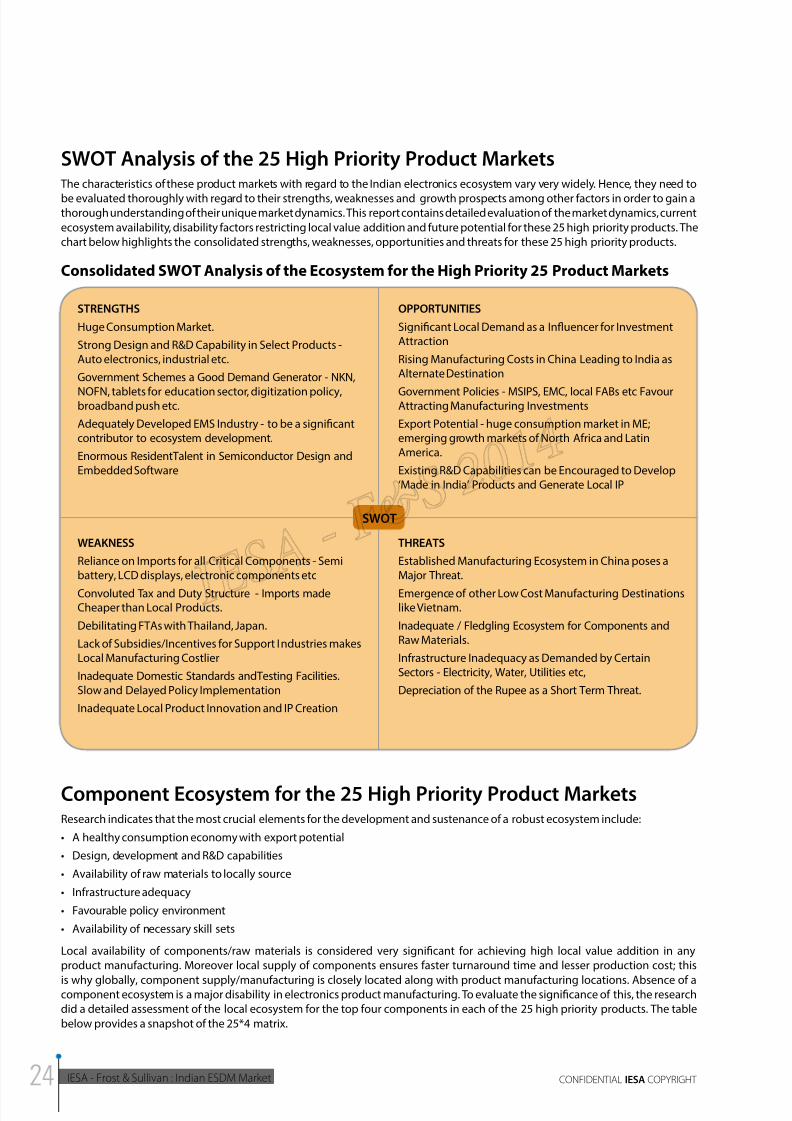

SWOT Analysis of the 25 High Priority Product Markets

The characteristics of these product markets with regard to the Indian electronics ecosystem vary very widely. Hence, they need to

be evaluated thoroughly with regard to their strengths, weaknesses and growth prospects among other factors in order to gain athorough understanding of their unique market dynamics. This report contains detailed evaluation of the market dynamics, current

ecosystem availability, disability factors restricting local value addition and future potential for these 25 high priority products. The

chart below highlights the consolidated strengths, weaknesses, opportunities and threats for these 25 high priority products.

Consolidated SWOT Analysis of the Ecosystem for the High Priority 25 Product Markets

SWOT

STRENGTHS

Huge Consumption Market.

Strong Design and R&D Capability in Select Products -Auto electronics, industrial etc.

Government Schemes a Good Demand Generator - NKN,

NOFN, tablets for education sector, digitization policy,broadband push etc.

Adequately Developed EMS Industry - to be a significantcontributor to ecosystem development.

Enormous ResidentTalent in Semiconductor Design andEmbedded Software

OPPORTUNITIES

Significant Local Demand as a Influencer for InvestmentAttraction

Rising Manufacturing Costs in China Leading to India asAlternate Destination

Government Policies - MSIPS, EMC, local FABs etc FavourAttracting Manufacturing Investments

Export Potential - huge consumption market in ME;emerging growth markets of North Africa and LatinAmerica.

Existing R&D Capabilities can be Encouraged to Develop‘Made in India’ Products and Generate Local IP

WEAKNESS

Reliance on Imports for all Critical Components - Semibattery, LCD displays, electronic components etc

Convoluted Tax and Duty Structure - Imports madeCheaper than Local Products.

Debilitating FTAs with Thailand, Japan.

Lack of Subsidies/Incentives for Support Industries makesLocal Manufacturing Costlier

Inadequate Domestic Standards andTesting Facilities.Slow and Delayed Policy Implementation

Inadequate Local Product Innovation and IP Creation

THREATS

Established Manufacturing Ecosystem in China poses aMajor Threat.

Emergence of other Low Cost Manufacturing Destinationslike Vietnam.

Inadequate / Fledgling Ecosystem for Components andRaw Materials.

Infrastructure Inadequacy as Demanded by CertainSectors - Electricity, Water, Utilities etc,

Depreciation of the Rupee as a Short Term Threat.

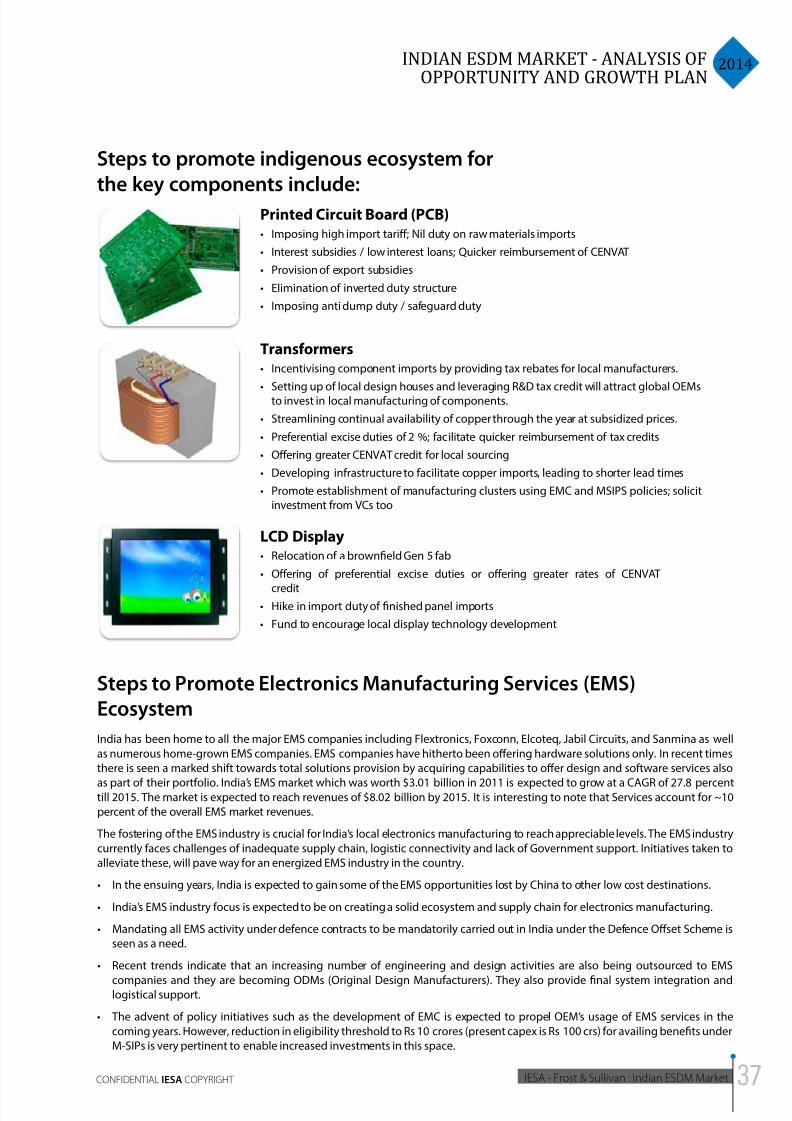

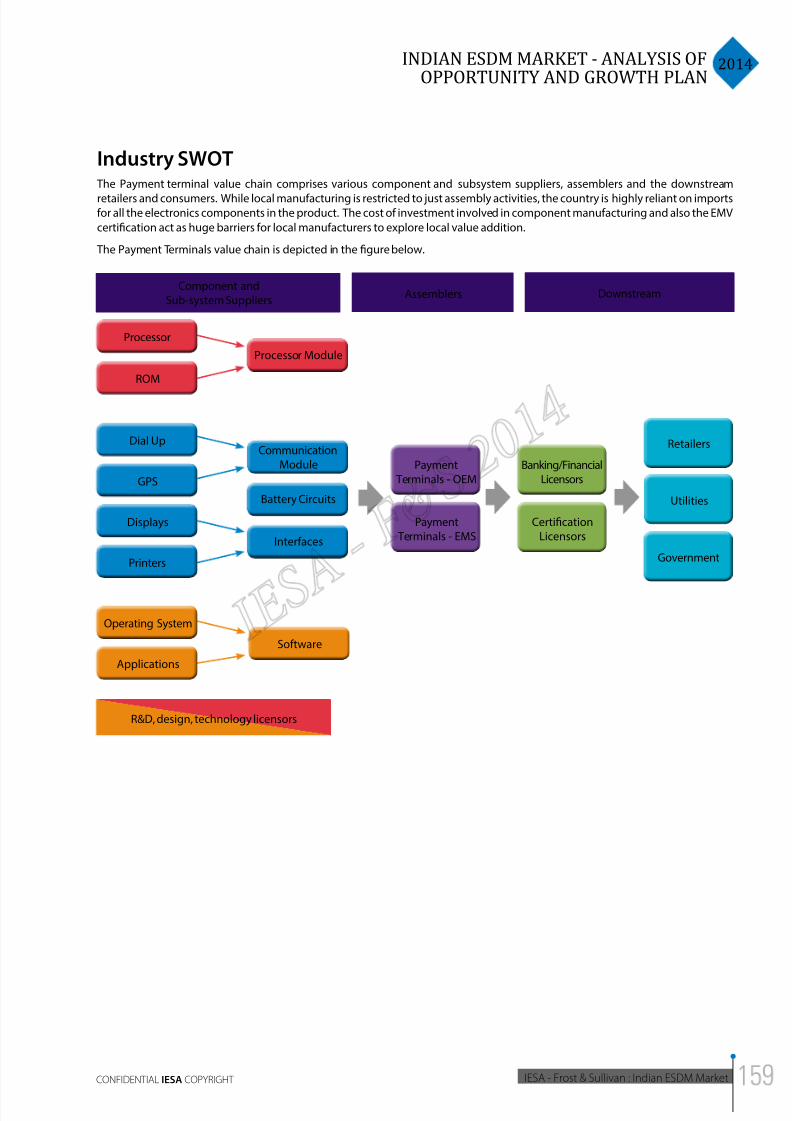

Component Ecosystem for the 25 High Priority Product MarketsResearch indicates that the most crucial elements for the development and sustenance of a robust ecosystem include:

• A healthy consumption economy with export potential

• Design, development and R&D capabilities

• Availability of raw materials to locally source

• Infrastructure adequacy

• Favourable policy environment

• Availability of necessary skill sets

Local availability of components/raw materials is considered very significant for achieving high local value addition in any

product manufacturing. Moreover local supply of components ensures faster turnaround time and lesser production cost; this

is why globally, component supply/manufacturing is closely located along with product manufacturing locations. Absence of acomponent ecosystem is a major disability in electronics product manufacturing. To evaluate the significance of this, the research

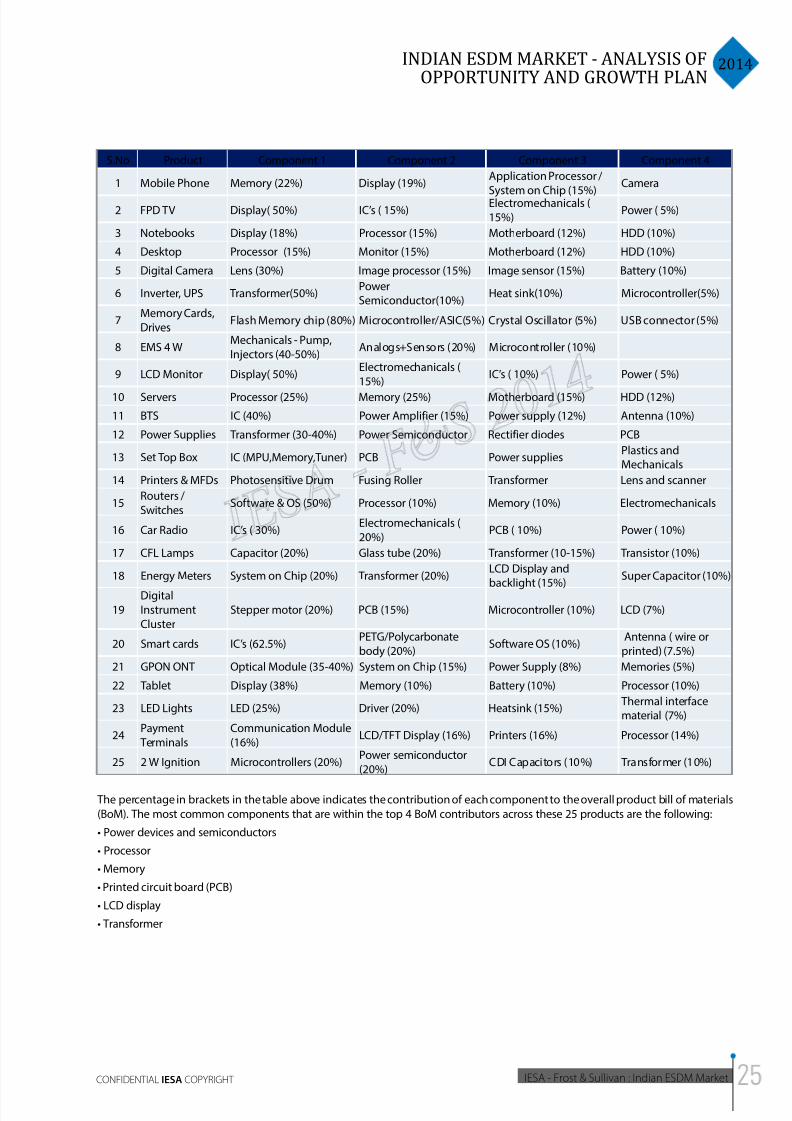

did a detailed assessment of the local ecosystem for the top four components in each of the 25 high priority products. The table

below provides a snapshot of the 25*4 matrix.

8/11/2019 IESA FS Report Indian ESDM Market

http://slidepdf.com/reader/full/iesa-fs-report-indian-esdm-market 25/172

2014INDIAN ESDM MARKET - ANALYSIS OF

OPPORTUNITY AND GROWTH PLAN

IESA - Frost & Sullivan : Indian ESDM MarketCONFIDENTIAL IESA COPYRIGHT

S.No Product Component 1 Component 2 Component 3 Component 4

1 Mobile Phone Memory (22%) Display (19%)Application Processor /

System on Chip (15%)

Camera

2 FPD TV Display( 50%) IC’s ( 15%)Electromechanicals (15%)

Power ( 5%)

3 Notebooks Display (18%) Processor (15%) Motherboard (12%) HDD (10%)

4 Desktop Processor (15%) Monitor (15%) Motherboard (12%) HDD (10%)

5 Digital Camera Lens (30%) Image processor (15%) Image sensor (15%) Battery (10%)

6 Inverter, UPS Transformer(50%)PowerSemiconductor(10%)

Heat sink(10%) Microcontroller(5%)

7Memory Cards,Drives

Flash Memory chip (80%) Microcontroller/ASIC(5%) Crystal Oscillator (5%) USB connector (5%)

8 EMS 4 WMechanicals - Pump,Injectors (40-50%)

Analogs+Sensors (20%) Microcontroller (10%)

9 LCD Monitor Display( 50%)Electromechanicals (15%)

IC’s ( 10%) Power ( 5%)

10 Servers Processor (25%) Memory (25%) Motherboard (15%) HDD (12%)

11 BTS IC (40%) Power Amplifier (15%) Power supply (12%) Antenna (10%)

12 Power Supplies Transformer (30-40%) Power Semiconductor Rectifier diodes PCB

13 Set Top Box IC (MPU,Memory,Tuner) PCB Power suppliesPlastics andMechanicals

14 Printers & MFDs Photosensitive Drum Fusing Roller Transformer Lens and scanner

15Routers /Switches

Software & OS (50%) Processor (10%) Memory (10%) Electromechanicals

16 Car Radio IC’s ( 30%)Electromechanicals (20%)

PCB ( 10%) Power ( 10%)

17 CFL Lamps Capacitor (20%) Glass tube (20%) Transformer (10-15%) Transistor (10%)

18 Energy Meters System on Chip (20%) Transformer (20%)LCD Display andbacklight (15%)

Super Capacitor (10%)

19DigitalInstrumentCluster

Stepper motor (20%) PCB (15%) Microcontroller (10%) LCD (7%)

20 Smart cards IC’s (62.5%)PETG/Polycarbonatebody (20%)

Software OS (10%) Antenna ( wire orprinted) (7.5%)

21 GPON ONT Optical Module (35-40%) System on Chip (15%) Power Supply (8%) Memories (5%)

22 Tablet Display (38%) Memory (10%) Battery (10%) Processor (10%)

23 LED Lights LED (25%) Driver (20%) Heatsink (15%) Thermal interfacematerial (7%)

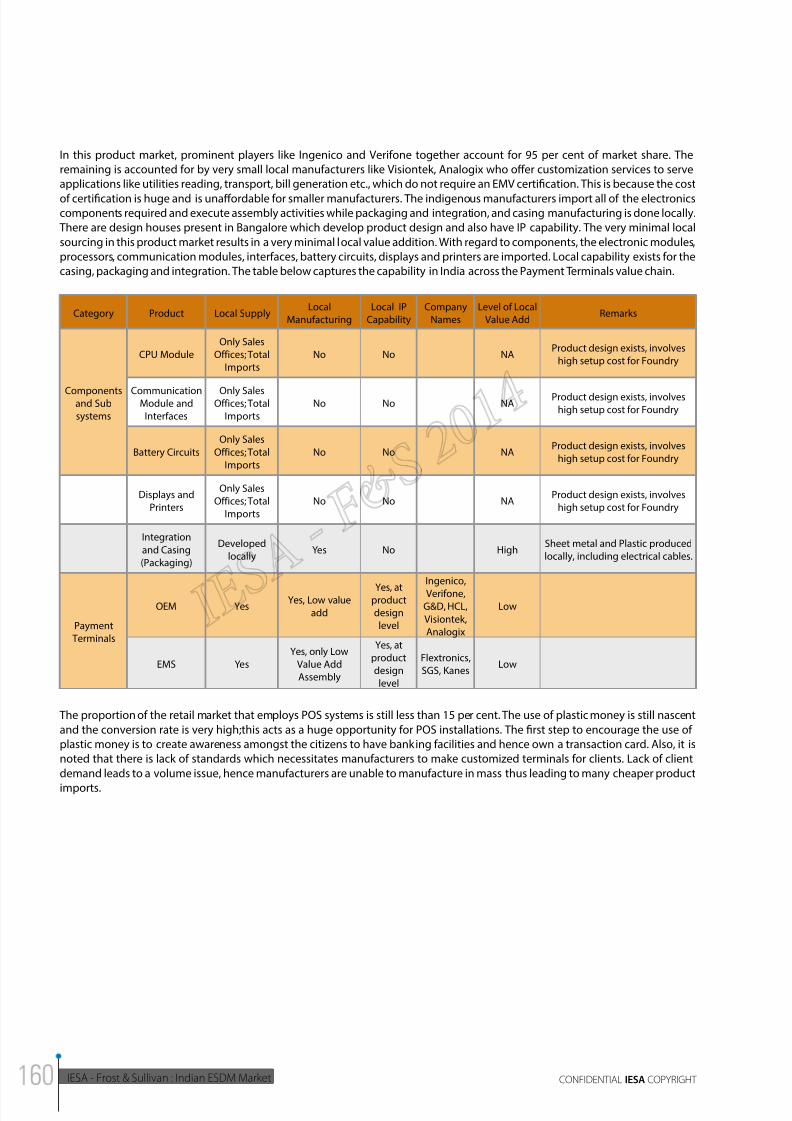

24Payment

TerminalsCommunication Module(16%)

LCD/TFT Display (16%) Printers (16%) Processor (14%)

25 2 W Ignition Microcontrollers (20%)Power semiconductor(20%)

CDI Capacitors (10%) Transformer (10%)

The percentage in brackets in the table above indicates the contribution of each component to the overall product bill of materials

(BoM). The most common components that are within the top 4 BoM contributors across these 25 products are the following:

• Power devices and semiconductors

• Processor

• Memory

• Printed circuit board (PCB)

• LCD display

• Transformer

8/11/2019 IESA FS Report Indian ESDM Market

http://slidepdf.com/reader/full/iesa-fs-report-indian-esdm-market 26/172

IESA - Frost & Sullivan : Indian ESDM Market CONFIDENTIAL IESA COPYRIGHT

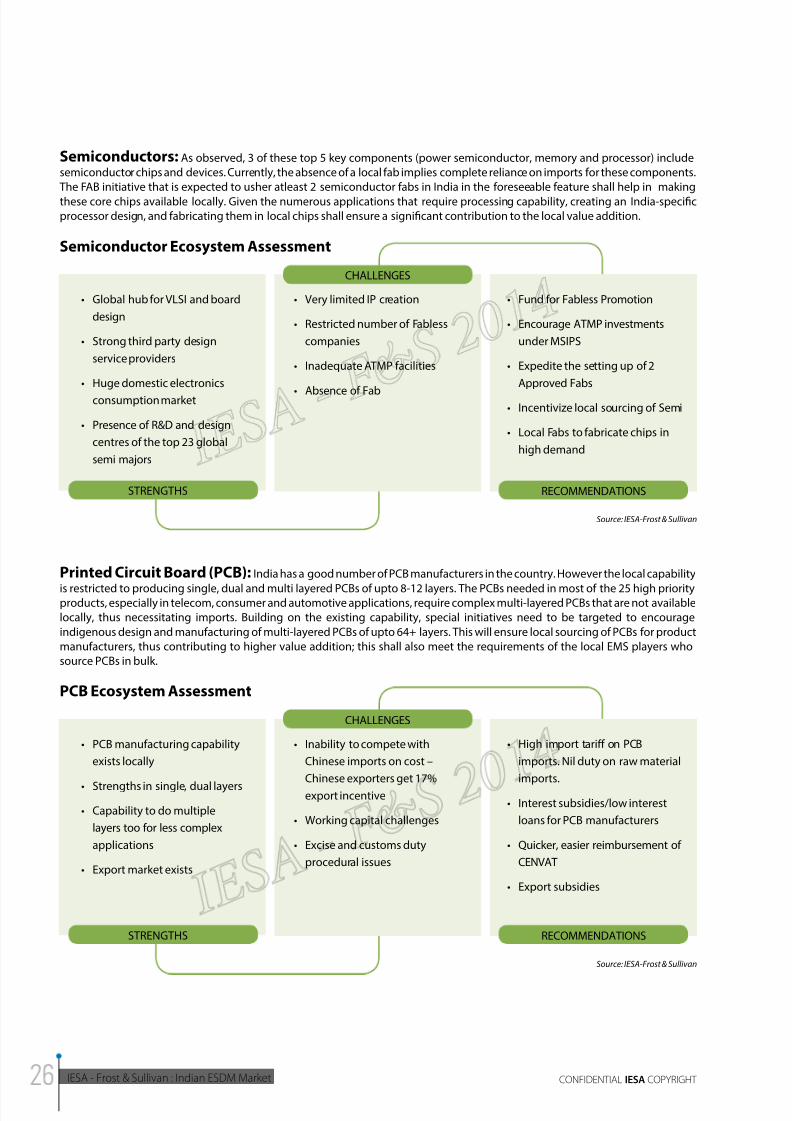

Semiconductor Ecosystem Assessment

• Global hub for VLSI and board

design

• Strong third party design

service providers

• Huge domestic electronics

consumption market

• Presence of R&D and design

centres of the top 23 global

semi majors

• Very limited IP creation

• Restricted number of Fabless

companies

• Inadequate ATMP facilities

• Absence of Fab

• Fund for Fabless Promotion

• Encourage ATMP investments

under MSIPS

• Expedite the setting up of 2

Approved Fabs

• Incentivize local sourcing of Semi

• Local Fabs to fabricate chips in

high demand

CHALLENGES

Source: IESA-Frost & Sullivan

STRENGTHS RECOMMENDATIONS

Semiconductors: As observed, 3 of these top 5 key components (power semiconductor, memory and processor) include

semiconductor chips and devices. Currently, the absence of a local fab implies complete reliance on imports for these components.

The FAB initiative that is expected to usher atleast 2 semiconductor fabs in India in the foreseeable feature shall help in making

these core chips available locally. Given the numerous applications that require processing capability, creating an India-specific

processor design, and fabricating them in local chips shall ensure a significant contribution to the local value addition.

Printed Circuit Board (PCB): India has a good number of PCB manufacturers in the country. However the local capability

is restricted to producing single, dual and multi layered PCBs of upto 8-12 layers. The PCBs needed in most of the 25 high priorityproducts, especially in telecom, consumer and automotive applications, require complex multi-layered PCBs that are not available

locally, thus necessitating imports. Building on the existing capability, special initiatives need to be targeted to encourage

indigenous design and manufacturing of multi-layered PCBs of upto 64+ layers. This will ensure local sourcing of PCBs for product

manufacturers, thus contributing to higher value addition; this shall also meet the requirements of the local EMS players who

source PCBs in bulk.

PCB Ecosystem Assessment

• PCB manufacturing capability

exists locally

• Strengths in single, dual layers

• Capability to do multiple

layers too for less complex

applications

• Export market exists

• Inability to compete with

Chinese imports on cost –

Chinese exporters get 17%

export incentive

• Working capital challenges

• Excise and customs duty

procedural issues

• High import tari on PCB

imports. Nil duty on raw material

imports.

• Interest subsidies/low interest

loans for PCB manufacturers

• Quicker, easier reimbursement of

CENVAT

• Export subsidies

CHALLENGES

Source: IESA-Frost & Sullivan

STRENGTHS RECOMMENDATIONS

8/11/2019 IESA FS Report Indian ESDM Market

http://slidepdf.com/reader/full/iesa-fs-report-indian-esdm-market 27/172

2014INDIAN ESDM MARKET - ANALYSIS OF

OPPORTUNITY AND GROWTH PLAN

IESA - Frost & Sullivan : Indian ESDM MarketCONFIDENTIAL IESA COPYRIGHT

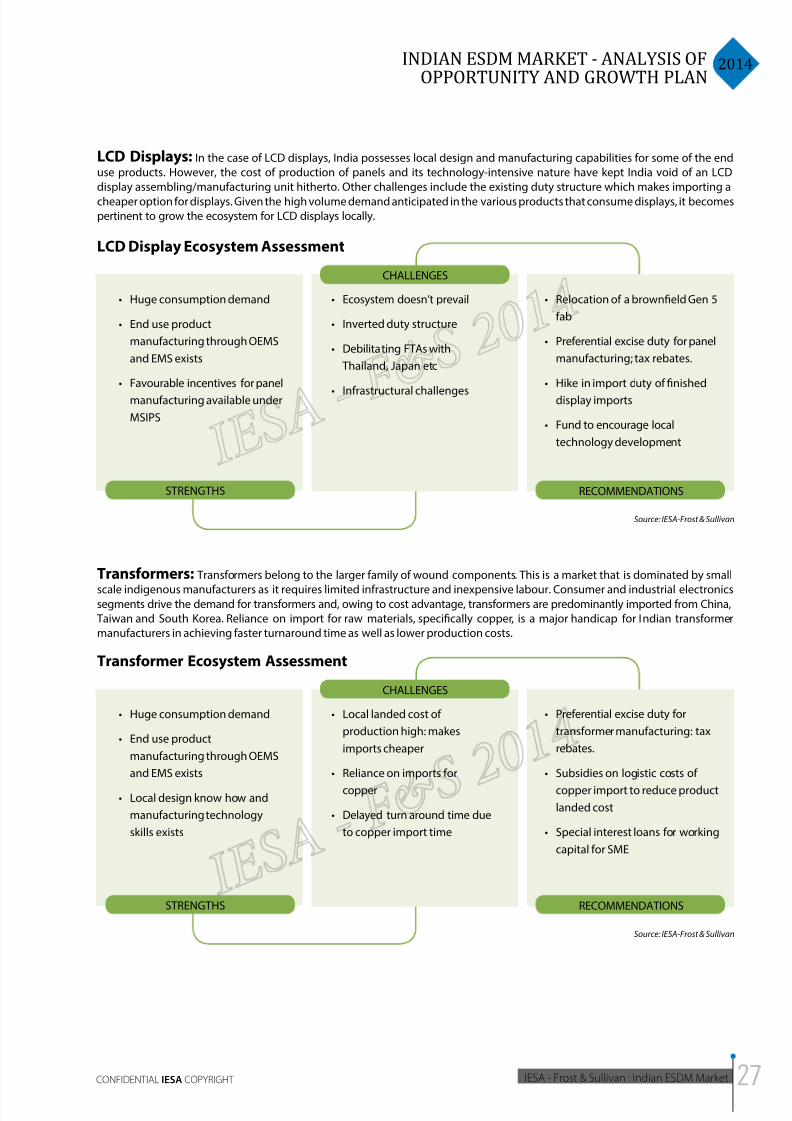

LCD Displays: In the case of LCD displays, India possesses local design and manufacturing capabilities for some of the end

use products. However, the cost of production of panels and its technology-intensive nature have kept India void of an LCD

display assembling/manufacturing unit hitherto. Other challenges include the existing duty structure which makes importing a

cheaper option for displays. Given the high volume demand anticipated in the various products that consume displays, it becomes

pertinent to grow the ecosystem for LCD displays locally.

LCD Display Ecosystem Assessment

• Huge consumption demand

• End use product

manufacturing through OEMS

and EMS exists

• Favourable incentives for panel

manufacturing available under

MSIPS

• Ecosystem doesn’t prevail

• Inverted duty structure

• Debilitating FTAs with

Thailand, Japan etc

• Infrastructural challenges

• Relocation of a browneld Gen 5

fab

• Preferential excise duty for panel

manufacturing; tax rebates.

• Hike in import duty of nished

display imports

• Fund to encourage local

technology development

CHALLENGES

Source: IESA-Frost & Sullivan

STRENGTHS RECOMMENDATIONS

Transformer Ecosystem Assessment

• Huge consumption demand

• End use product

manufacturing through OEMS

and EMS exists

• Local design know how and

manufacturing technology

skills exists

• Local landed cost of

production high: makes

imports cheaper

• Reliance on imports for

copper

• Delayed turn around time due

to copper import time

• Preferential excise duty for

transformer manufacturing: tax

rebates.

• Subsidies on logistic costs of

copper import to reduce product

landed cost

• Special interest loans for working

capital for SME

CHALLENGES

Source: IESA-Frost & Sullivan

STRENGTHS RECOMMENDATIONS

Transformers: Transformers belong to the larger family of wound components. This is a market that is dominated by small

scale indigenous manufacturers as it requires limited infrastructure and inexpensive labour. Consumer and industrial electronicssegments drive the demand for transformers and, owing to cost advantage, transformers are predominantly imported from China,

Taiwan and South Korea. Reliance on import for raw materials, specifically copper, is a major handicap for Indian transformer

manufacturers in achieving faster turnaround time as well as lower production costs.

8/11/2019 IESA FS Report Indian ESDM Market

http://slidepdf.com/reader/full/iesa-fs-report-indian-esdm-market 28/172

IESA - Frost & Sullivan : Indian ESDM Market CONFIDENTIAL IESA COPYRIGHT

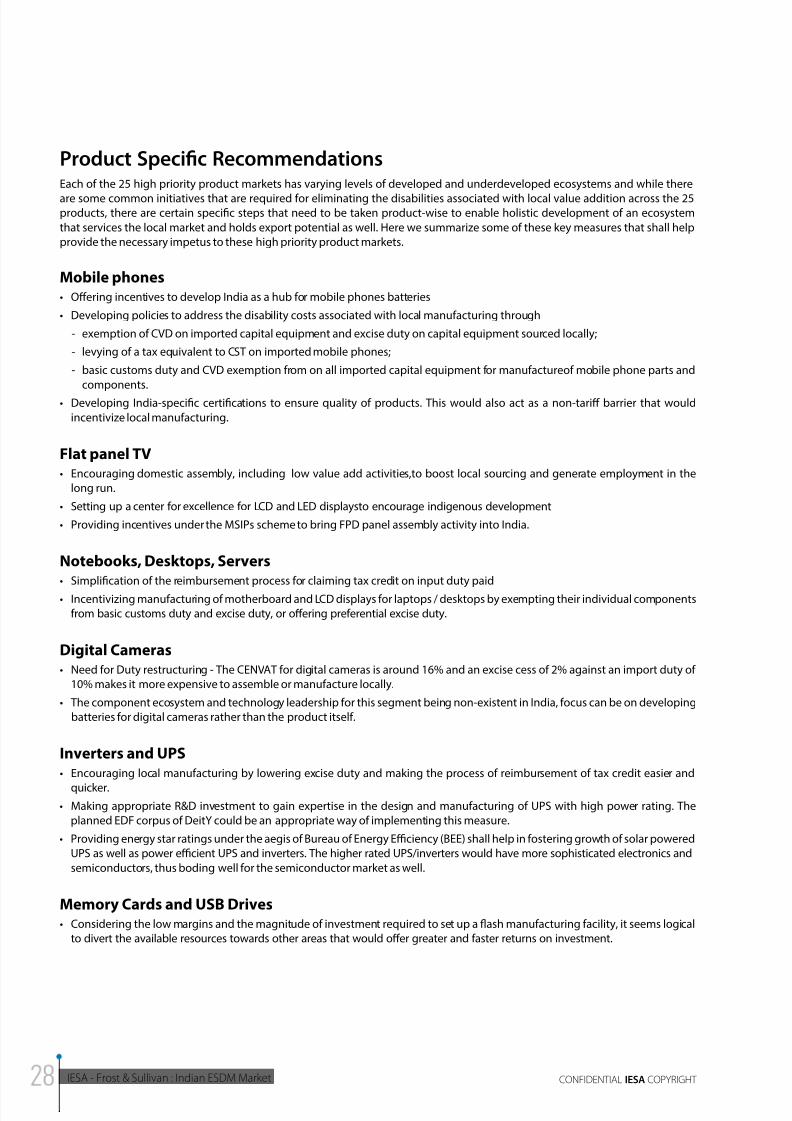

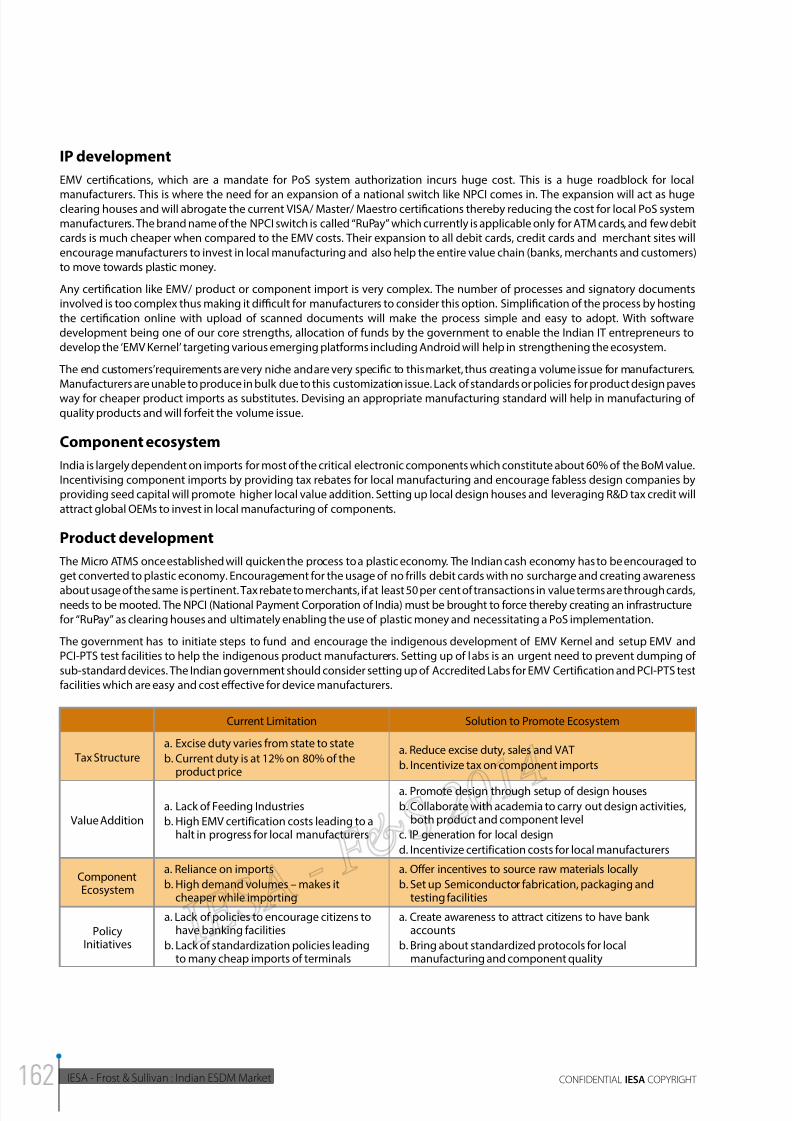

Product Specific RecommendationsEach of the 25 high priority product markets has varying levels of developed and underdeveloped ecosystems and while there

are some common initiatives that are required for eliminating the disabilities associated with local value addition across the 25products, there are certain specific steps that need to be taken product-wise to enable holistic development of an ecosystem

that services the local market and holds export potential as well. Here we summarize some of these key measures that shall help

provide the necessary impetus to these high priority product markets.

Mobile phones• Oering incentives to develop India as a hub for mobile phones batteries

• Developing policies to address the disability costs associated with local manufacturing through

- exemption of CVD on imported capital equipment and excise duty on capital equipment sourced locally;

- levying of a tax equivalent to CST on imported mobile phones;

- basic customs duty and CVD exemption from on all imported capital equipment for manufactureof mobile phone parts and

components.

• Developing India-specic certications to ensure quality of products. This would also act as a non-tari barrier that would

incentivize local manufacturing.

Flat panel TV• Encouraging domestic assembly, including low value add activities,to boost local sourcing and generate employment in the

long run.

• Setting up a center for excellence for LCD and LED displaysto encourage indigenous development

• Providing incentives under the MSIPs scheme to bring FPD panel assembly activity into India.

Notebooks, Desktops, Servers• Simplication of the reimbursement process for claiming tax credit on input duty paid

• Incentivizing manufacturing of motherboard and LCD displays for laptops / desktops by exempting their individual components

from basic customs duty and excise duty, or offering preferential excise duty.

Digital Cameras• Need for Duty restructuring - The CENVAT for digital cameras is around 16% and an excise cess of 2% against an import duty of

10% makes it more expensive to assemble or manufacture locally.

• The component ecosystem and technology leadership for this segment being non-existent in India, focus can be on developing

batteries for digital cameras rather than the product itself.

Inverters and UPS• Encouraging local manufacturing by lowering excise duty and making the process of reimbursement of tax credit easier and

quicker.

• Making appropriate R&D investment to gain expertise in the design and manufacturing of UPS with high power rating. The

planned EDF corpus of DeitY could be an appropriate way of implementing this measure.

• Providing energy star ratings under the aegis of Bureau of Energy Eciency (BEE) shall help in fostering growth of solar powered

UPS as well as power ecient UPS and inverters. The higher rated UPS/inverters would have more sophisticated electronics and

semiconductors, thus boding well for the semiconductor market as well.

Memory Cards and USB Drives• Considering the low margins and the magnitude of investment required to set up a ash manufacturing facility, it seems logical

to divert the available resources towards other areas that would offer greater and faster returns on investment.

8/11/2019 IESA FS Report Indian ESDM Market

http://slidepdf.com/reader/full/iesa-fs-report-indian-esdm-market 29/172

2014INDIAN ESDM MARKET - ANALYSIS OF

OPPORTUNITY AND GROWTH PLAN

IESA - Frost & Sullivan : Indian ESDM MarketCONFIDENTIAL IESA COPYRIGHT

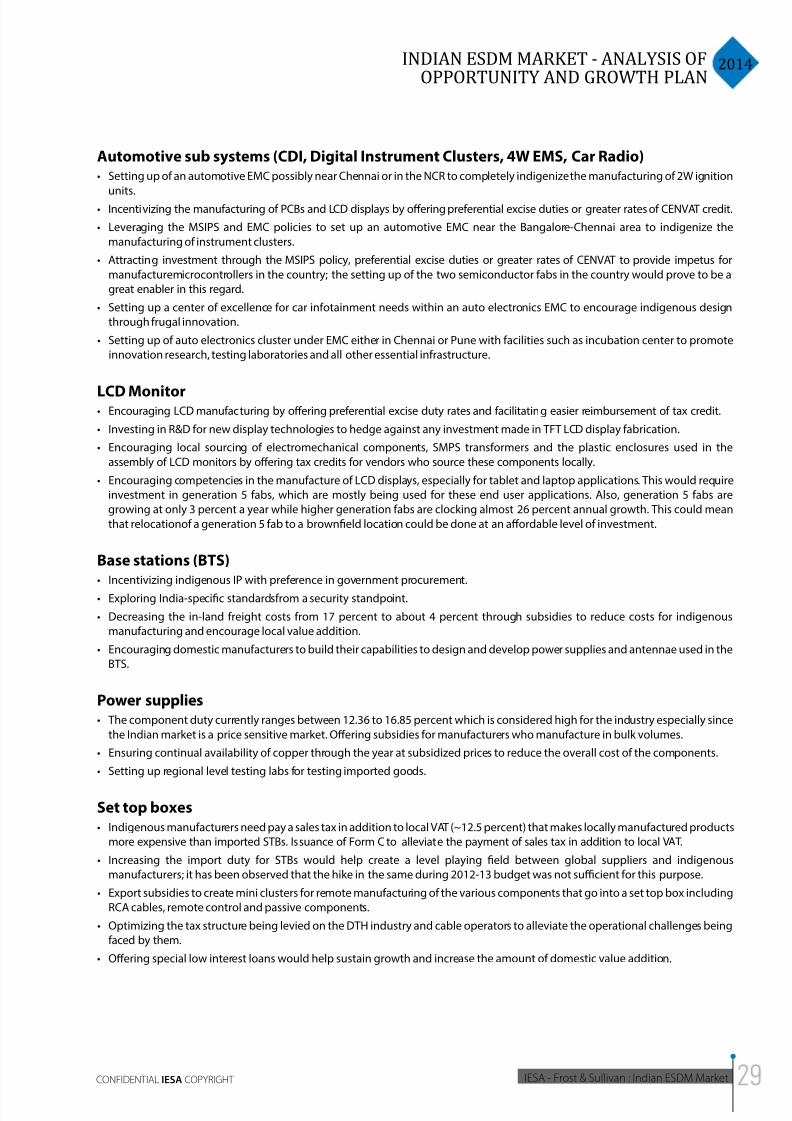

Automotive sub systems (CDI, Digital Instrument Clusters, 4W EMS, Car Radio)• Setting up of an automotive EMC possibly near Chennai or in the NCR to completely indigenize the manufacturing of 2W ignition

units.• Incentivizing the manufacturing of PCBs and LCD displays by oering preferential excise duties or greater rates of CENVAT credit.

• Leveraging the MSIPS and EMC policies to set up an automotive EMC near the Bangalore-Chennai area to indigenize the

manufacturing of instrument clusters.

• Attracting investment through the MSIPS policy, preferential excise duties or greater rates of CENVAT to provide impetus for

manufacturemicrocontrollers in the country; the setting up of the two semiconductor fabs in the country would prove to be a

great enabler in this regard.

• Setting up a center of excellence for car infotainment needs within an auto electronics EMC to encourage indigenous design

through frugal innovation.

• Setting up of auto electronics cluster under EMC either in Chennai or Pune with facilities such as incubation center to promote

innovation research, testing laboratories and all other essential infrastructure.

LCD Monitor• Encouraging LCD manufacturing by oering preferential excise duty rates and facilitating easier reimbursement of tax credit.

• Investing in R&D for new display technologies to hedge against any investment made in TFT LCD display fabrication.

• Encouraging local sourcing of electromechanical components, SMPS transformers and the plastic enclosures used in the

assembly of LCD monitors by offering tax credits for vendors who source these components locally.

• Encouraging competencies in the manufacture of LCD displays, especially for tablet and laptop applications. This would require

investment in generation 5 fabs, which are mostly being used for these end user applications. Also, generation 5 fabs are

growing at only 3 percent a year while higher generation fabs are clocking almost 26 percent annual growth. This could mean

that relocationof a generation 5 fab to a brownfield location could be done at an affordable level of investment.

Base stations (BTS)• Incentivizing indigenous IP with preference in government procurement.

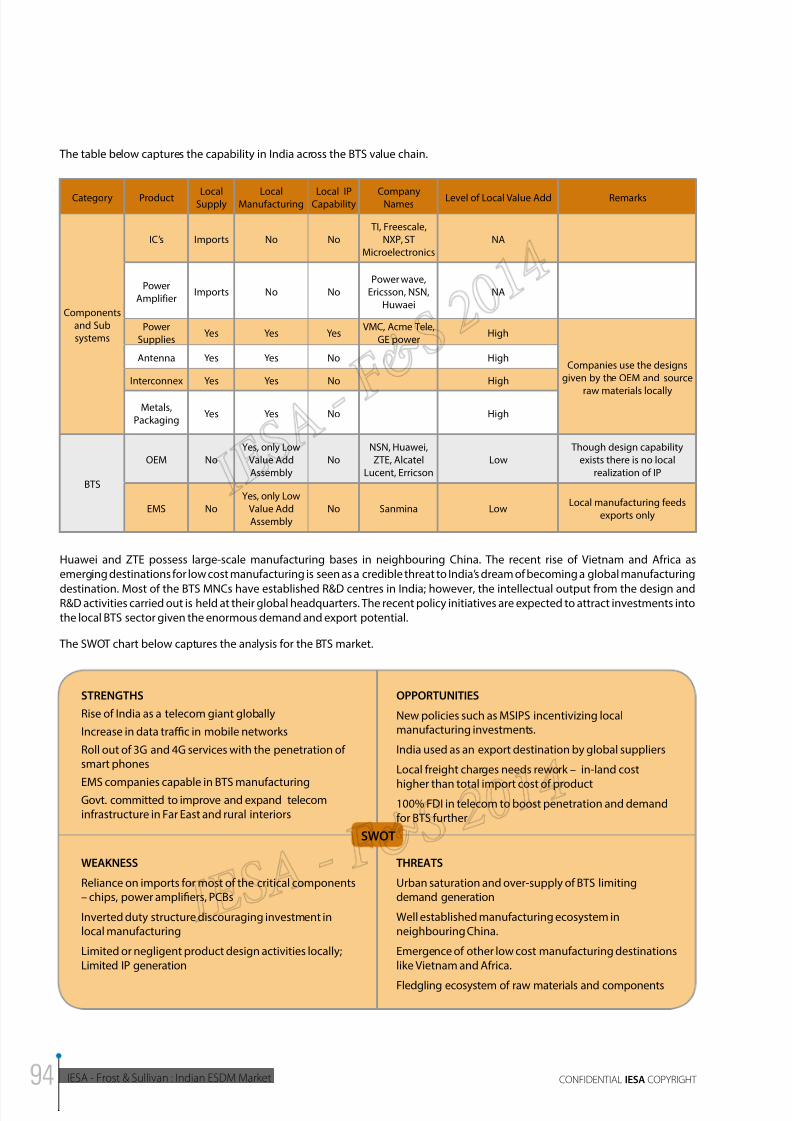

• Exploring India-specic standardsfrom a security standpoint.

• Decreasing the in-land freight costs from 17 percent to about 4 percent through subsidies to reduce costs for indigenous

manufacturing and encourage local value addition.

• Encouraging domestic manufacturers to build their capabilities to design and develop power supplies and antennae used in the

BTS.

Power supplies• The component duty currently ranges between 12.36 to 16.85 percent which is considered high for the industry especially since

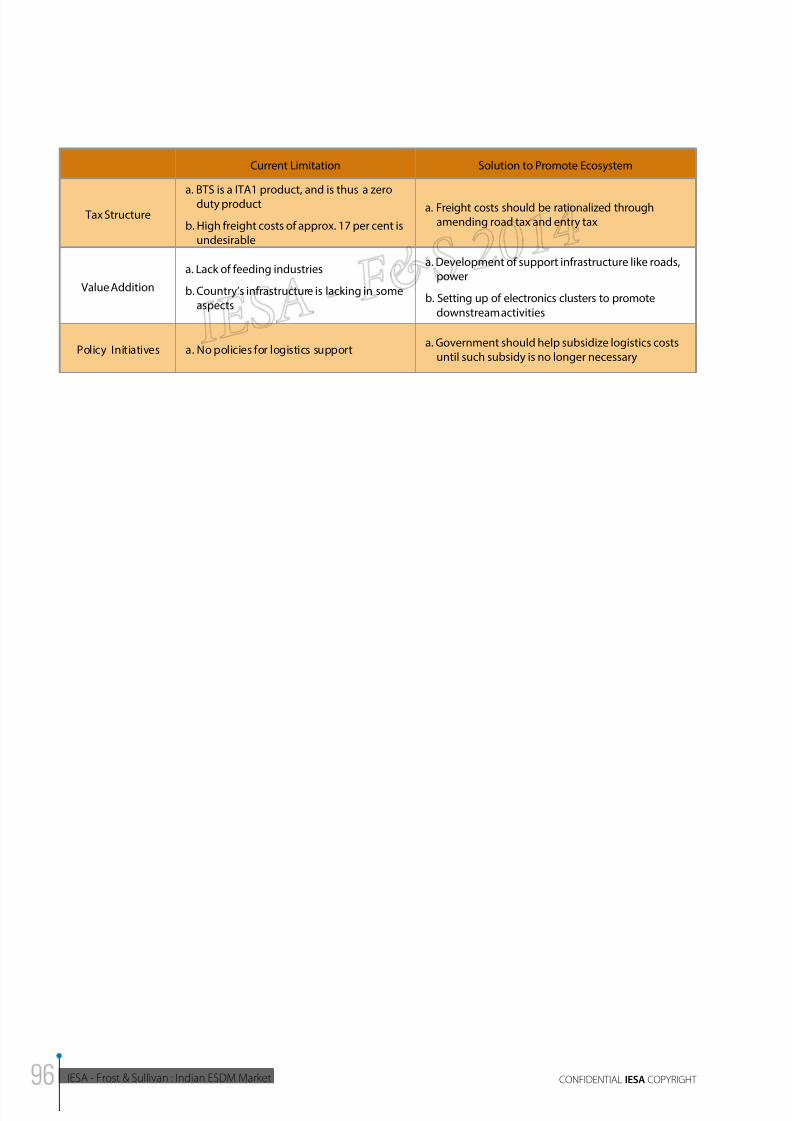

the Indian market is a price sensitive market. Offering subsidies for manufacturers who manufacture in bulk volumes.

• Ensuring continual availability of copper through the year at subsidized prices to reduce the overall cost of the components.

• Setting up regional level testing labs for testing imported goods.

Set top boxes• Indigenous manufacturers need pay a sales tax in addition to local VAT (~12.5 percent) that makes locally manufactured products

more expensive than imported STBs. Issuance of Form C to alleviate the payment of sales tax in addition to local VAT.

• Increasing the import duty for STBs would help create a level playing eld between global suppliers and indigenous

manufacturers; it has been observed that the hike in the same during 2012-13 budget was not sucient for this purpose.

• Export subsidies to create mini clusters for remote manufacturing of the various components that go into a set top box including

RCA cables, remote control and passive components.

• Optimizing the tax structure being levied on the DTH industry and cable operators to alleviate the operational challenges being

faced by them.

• Oering special low interest loans would help sustain growth and increase the amount of domestic value addition.

8/11/2019 IESA FS Report Indian ESDM Market

http://slidepdf.com/reader/full/iesa-fs-report-indian-esdm-market 30/172

IESA - Frost & Sullivan : Indian ESDM Market CONFIDENTIAL IESA COPYRIGHT

Printers and MFDs• Oering tax credits on R&D activity in high-end laser printing and MFDs. The government could also facilitate the formation of

joint ventures between indigenous players and global OEMs to take advantage of latent manufacturing capabilities; there couldbe export opportunities to the Middle East, Sri Lanka, and Africa due to India’s geographical location.

• Incentivizing local value addition for components such as transformers, PCBs and cabling, that are currently being manufactured

in India, by offering preferential excise duties and greater CENVAT credit for suppliers.

Routers/switches• Creation of funds for local technology know-how development and incentivizing local IP generation

• Focusingon promoting local manufacturing of components such as complex PCBs for routers by either oering preferential

excise duty rates for the manufacturing of complex PCB designs or offering greater rates of CENVAT.

• Prioritizing /inviting investment in PCBs manufacturing under the MSIPS scheme and oer associated benets to those investors.

CFL• Reducing VAT for CFL manufacturing to zero per cent across all states

• Developing ISI certications to standardise manufacturing of CFLs in the country.

Energy meters• Development of standards for manufacturing of smart meters, create a R&D fund for innovations in smart meters, and also create

opportunities for manufacturing of key individual components such as communication modules and transceivers.

• Incentivizing export duty and establishing India as an export hub by encouraging product modications suiting international

requirements

• Setting up an R&D fund for smart meters to encourage SME manufacturers to invest in innovation

• Incentivize manufacturing of communication modules and transceivers

• Global marketing support for cash-strapped SME suppliers

Smart cards• Incentivizing software development and customization services

• Creation of indigenous standards that are application specic with the aim to ensure higher security in the smart cards consumed

in the country.

• Setting up of subsidized testing facilities for EMV compliance

• The Indian ecosystem has enormous skillset availability in the software and integration part of smart cards which could be

incentivized through offering appropriate R&D deductions.

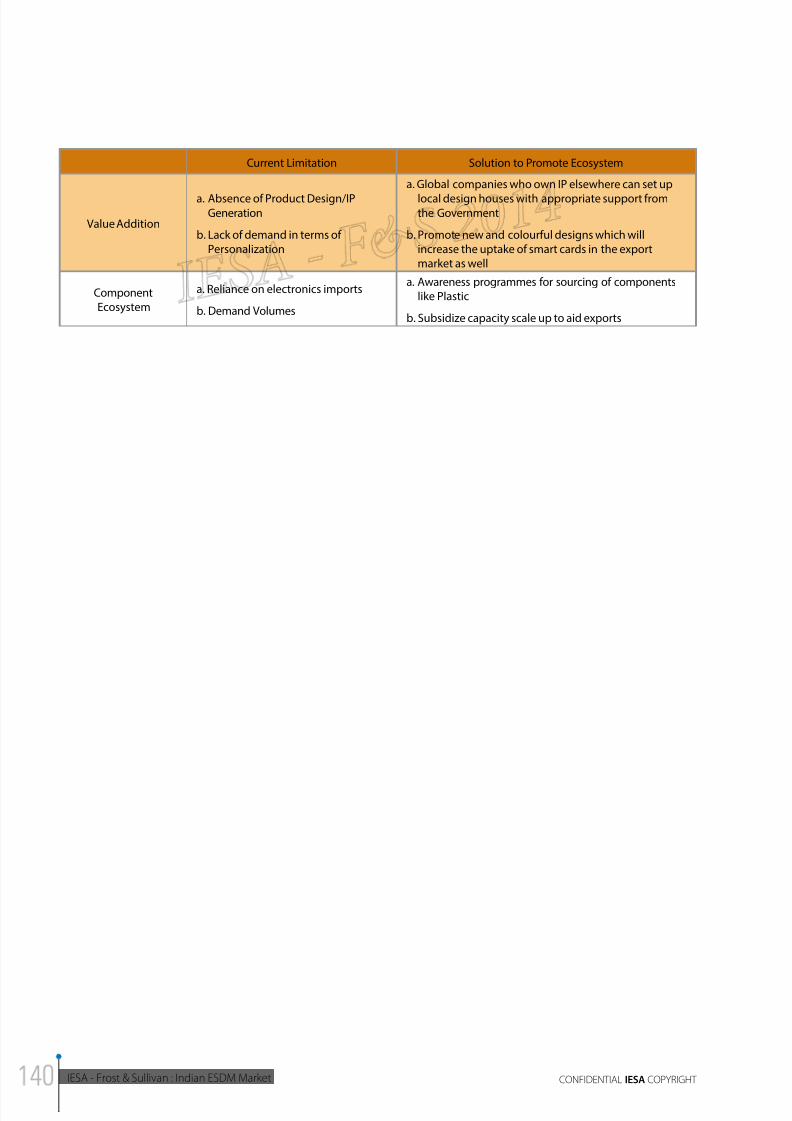

• Encouraging local sourcing of plastic (PETG) by oering preferential excise rates when raw materials are locally sourced.

GPON ONT• Creating supportive policies like reduced excise duties to encourage domestic manufacturing.

Tablets• Repealing the levy of SAD individual electronic components or individual components of LCD monitors and motherboards.

• Incentivizing the manufacture of motherboard and LCD monitors by exempting their individual components from basic customs

duty and excise duty, or offering preferential excise duty.

• Simplifying the reimbursement process for claiming tax credit on input duty paid

• Creating a centre of excellence for tablets to consolidate the dierent design eorts in the private and public sectorsto develop

world-class commercial ‘Made in India’ tablets.

LED Lighting• Restrictive tax structure with a high VAT of 14.5 percent obstructs LED lighting penetration. Reduction in the VAT and a uniform

VAT structure across all states will increase penetration.

• Mandating BIS technical specications to standardize manufacturing processes and products. Imported LED lamps should also

be tested rigorously to prevent dumping of goods in the local market.

8/11/2019 IESA FS Report Indian ESDM Market

http://slidepdf.com/reader/full/iesa-fs-report-indian-esdm-market 31/172

8/11/2019 IESA FS Report Indian ESDM Market

http://slidepdf.com/reader/full/iesa-fs-report-indian-esdm-market 32/172

IESA - Frost & Sullivan : Indian ESDM Market CONFIDENTIAL IESA COPYRIGHT

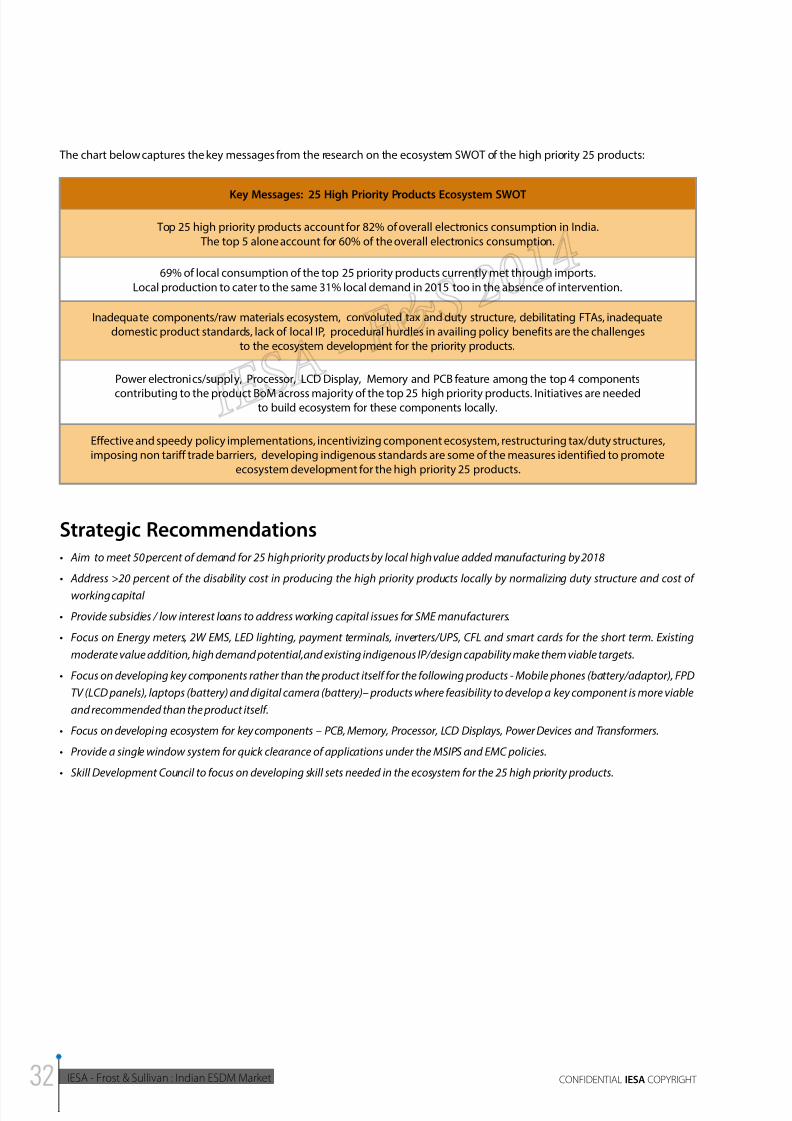

The chart below captures the key messages from the research on the ecosystem SWOT of the high priority 25 products:

Key Messages: 25 High Priority Products Ecosystem SWOT

Top 25 high priority products account for 82% of overall electronics consumption in India.

The top 5 alone account for 60% of the overall electronics consumption.

69% of local consumption of the top 25 priority products currently met through imports.

Local production to cater to the same 31% local demand in 2015 too in the absence of intervention.

Inadequate components/raw materials ecosystem, convoluted tax and duty structure, debilitating FTAs, inadequatedomestic product standards, lack of local IP, procedural hurdles in availing policy benefits are the challenges

to the ecosystem development for the priority products.

Power electronics/supply, Processor, LCD Display, Memory and PCB feature among the top 4 components

contributing to the product BoM across majority of the top 25 high priority products. Initiatives are neededto build ecosystem for these components locally.

Effective and speedy policy implementations, incentivizing component ecosystem, restructuring tax/duty structures,imposing non tariff trade barriers, developing indigenous standards are some of the measures identified to promote

ecosystem development for the high priority 25 products.

Strategic Recommendations• Aim to meet 50 percent of demand for 25 high priority products by local high value added manufacturing by 2018

• Address >20 percent of the disability cost in producing the high priority products locally by normalizing duty structure and cost of

working capital

• Provide subsidies / low interest loans to address working capital issues for SME manufacturers.

• Focus on Energy meters, 2W EMS, LED lighting, payment terminals, inverters/UPS, CFL and smart cards for the short term. Existing

moderate value addition, high demand potential,and existing indigenous IP/design capability make them viable targets.

• Focus on developing key components rather than the product itself for the following products - Mobile phones (battery/adaptor), FPD

TV (LCD panels), laptops (battery) and digital camera (battery)– products where feasibility to develop a key component is more viable

and recommended than the product itself.

• Focus on developing ecosystem for key components – PCB, Memory, Processor, LCD Displays, Power Devices and Transformers.

• Provide a single window system for quick clearance of applications under the MSIPS and EMC policies.

• Skill Development Council to focus on developing skill sets needed in the ecosystem for the 25 high priority products.

8/11/2019 IESA FS Report Indian ESDM Market

http://slidepdf.com/reader/full/iesa-fs-report-indian-esdm-market 33/172

2014INDIAN ESDM MARKET - ANALYSIS OF

OPPORTUNITY AND GROWTH PLAN

IESA - Frost & Sullivan : Indian ESDM MarketCONFIDENTIAL IESA COPYRIGHT

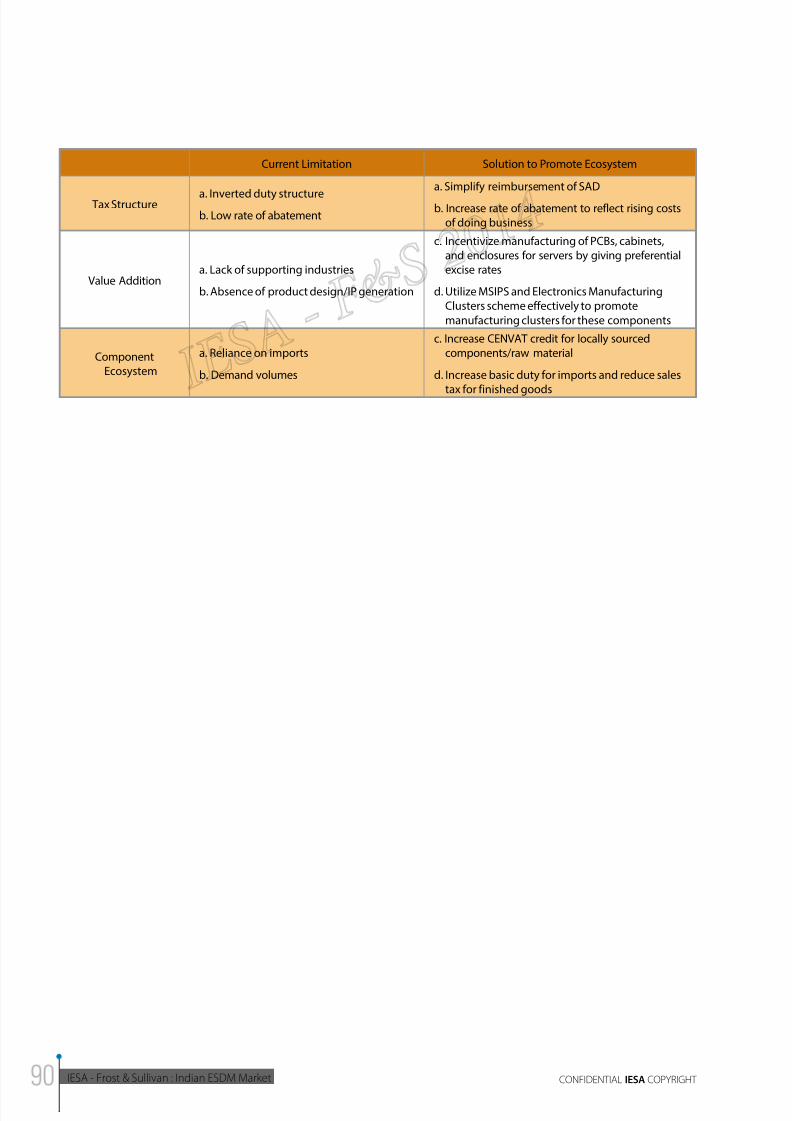

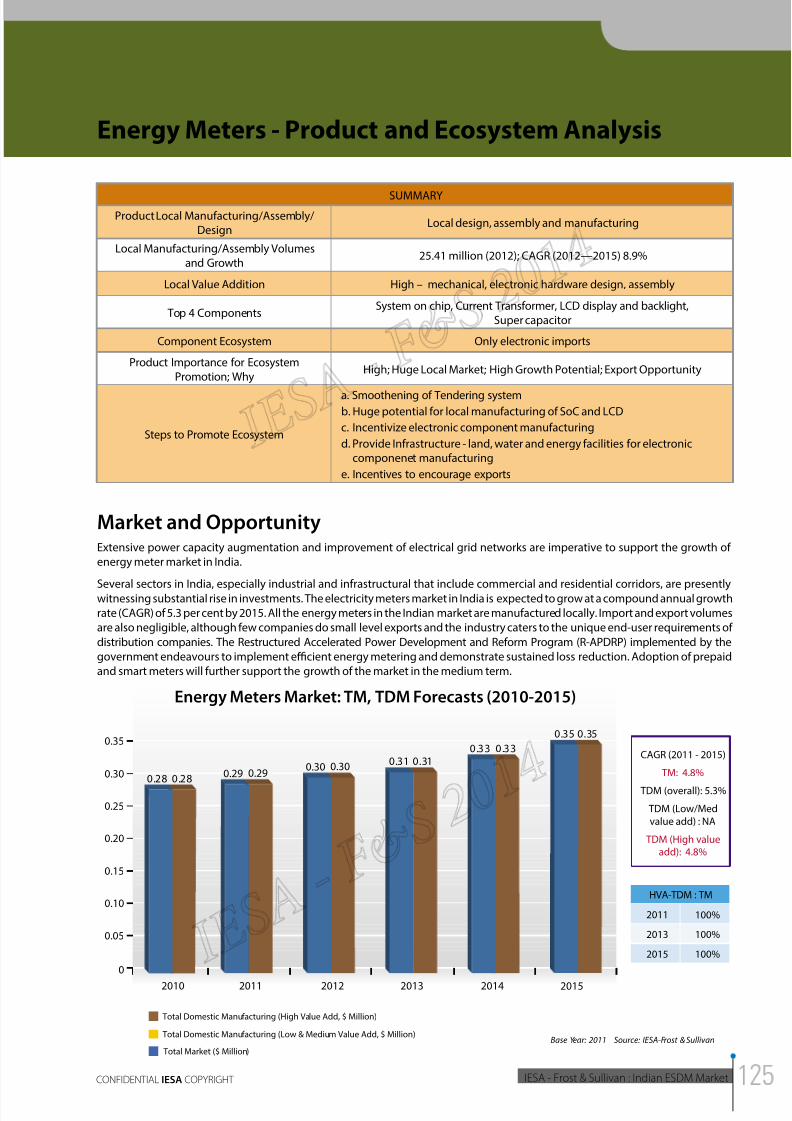

Top 10 Products and Components Markets to Focusfor Near Term Local Value Addition Improvement

This report provides a comprehensive ecosystem assessment of the top 25 electronic products that account for 82 percent of the

overall electronic products consumption and provides directions on steps needed to create viable ecosystems for these priority

products. The report also evaluates critical components that make up the bill of materials (BoM) of the high priority products

and provides similar prescriptive recommendations on the measures to create and build local ecosystems for these contributing

components. Research indicates according immediate priority and attention to a limited set of 10 products and components

including Energy Meters, Inverters & UPS, Smart Phones, LED Lighting, Smart Cards, Payment Terminals, 2W EMS, PCB, LCD Displays

and Transformers leveraging upon their existing ecosystem strengths shall result in marked increase in indigenous electronics

manufacturing in the next 2 years itself. Current limitations to high value addition and steps needed to improve the local ecosystem

for these 10 products/components are illustrated below.

1. A regional level single point testing laboratory to conduct all tests for the local and imported meters.

2. Incentivizing the export duty can boost exports

3. With an expected shift towards smart meters, preparing for the future by investing in R&D especially in developmentof relays by leveraging R&D tax credits

4. Notification of Preference Market Access

5. Notification of safety standards by Department of Electronics and IT

6. Product Specifications also need to be defined to prod indigenous manufacturing

STRATEGIC

RECOMMENDATIONS

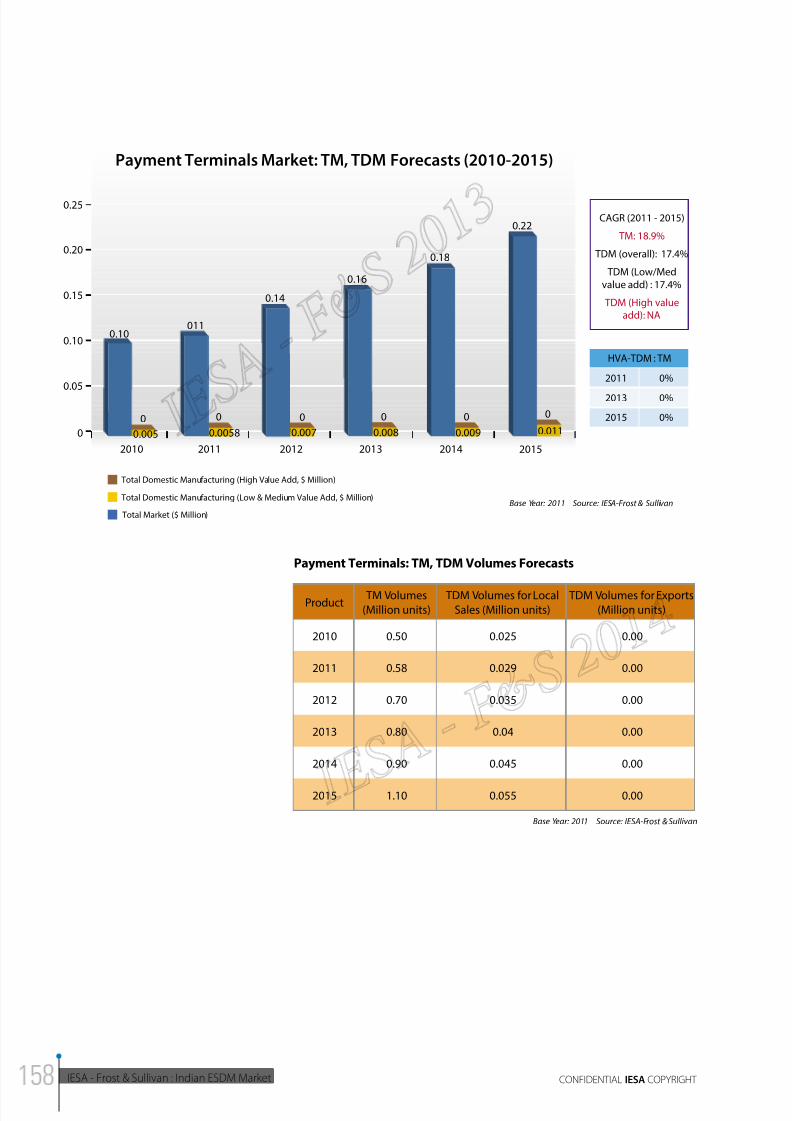

OPPORTUNITY SIZE TM ($ B) TDM ($ B)

2012 0.3 0.35

2015 0.3 0.35

Top 4 Components (BoM Contribution

SoC Transformer

LCD Display Super Cap

ENERGY METERS

Strengths

• High consumption demand

• Product design capability

• Anti tamper technology design IP

Opportunities

• Government policies like R-APDRP

• Focus on energy conservation

• India as export hub

• Smart meters

Weakness

• Import for critical

components

• Complex tendering system at

utilities departments

Threats

• Companies that use reference

designs and launch cheapproducts

8/11/2019 IESA FS Report Indian ESDM Market

http://slidepdf.com/reader/full/iesa-fs-report-indian-esdm-market 34/172

IESA - Frost & Sullivan : Indian ESDM Market CONFIDENTIAL IESA COPYRIGHT

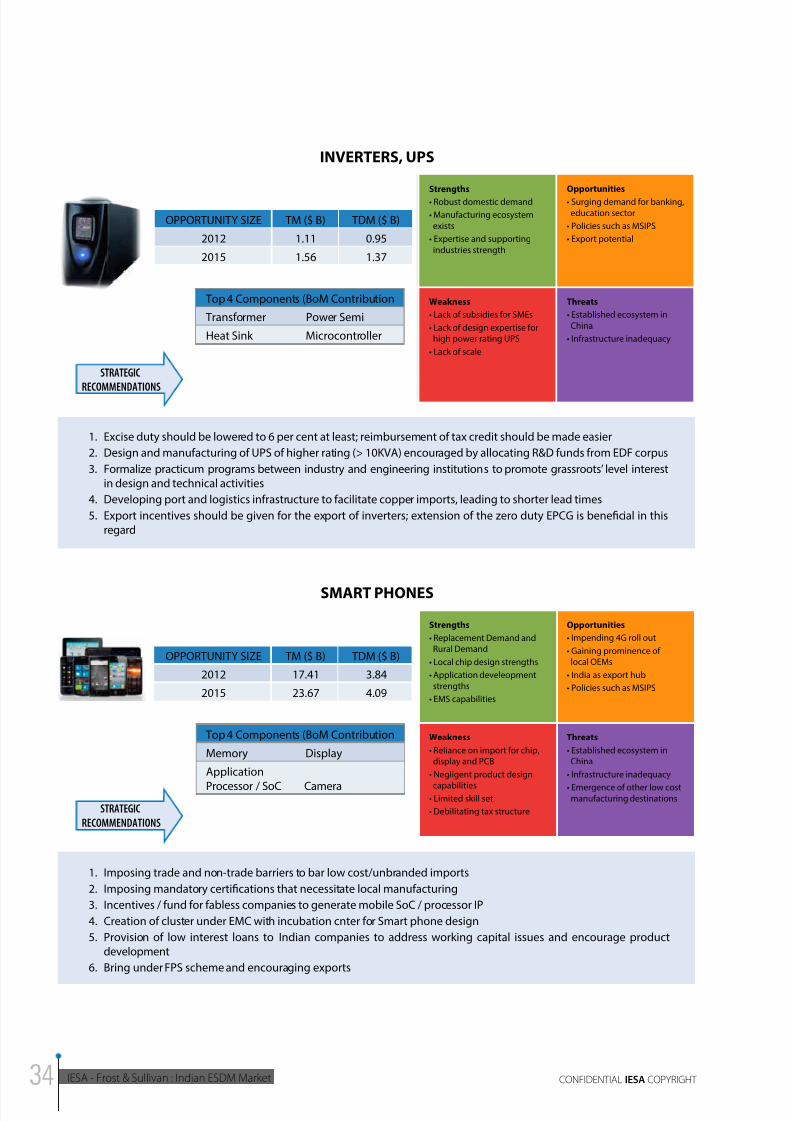

1. Excise duty should be lowered to 6 per cent at least; reimbursement of tax credit should be made easier

2. Design and manufacturing of UPS of higher rating (> 10KVA) encouraged by allocating R&D funds from EDF corpus

3. Formalize practicum programs between industry and engineering institutions to promote grassroots’ level interestin design and technical activities

4. Developing port and logistics infrastructure to facilitate copper imports, leading to shorter lead times

5. Export incentives should be given for the export of inverters; extension of the zero duty EPCG is beneficial in thisregard

1. Imposing trade and non-trade barriers to bar low cost/unbranded imports

2. Imposing mandatory certifications that necessitate local manufacturing

3. Incentives / fund for fabless companies to generate mobile SoC / processor IP

4. Creation of cluster under EMC with incubation cnter for Smart phone design

5. Provision of low interest loans to Indian companies to address working capital issues and encourage productdevelopment

6. Bring under FPS scheme and encouraging exports

STRATEGIC

RECOMMENDATIONS

STRATEGIC

RECOMMENDATIONS

OPPORTUNITY SIZE TM ($ B) TDM ($ B)

2012 1.11 0.95

2015 1.56 1.37

OPPORTUNITY SIZE TM ($ B) TDM ($ B)

2012 17.41 3.84

2015 23.67 4.09

Top 4 Components (BoM Contribution

Transformer Power Semi

Heat Sink Microcontroller

Top 4 Components (BoM Contribution

Memory Display

Application

Processor / SoC Camera

INVERTERS, UPS

SMART PHONES

Strengths

• Robust domestic demand

• Manufacturing ecosystem

exists

• Expertise and supporting

industries strength

Opportunities

• Surging demand for banking,

education sector

• Policies such as MSIPS

• Export potential

Weakness

• Lack of subsidies for SMEs

• Lack of design expertise for high power rating UPS

• Lack of scale

Threats

• Established ecosystem in

China

• Infrastructure inadequacy

Strengths

• Replacement Demand and Rural Demand

• Local chip design strengths

• Application develeopment

strengths

• EMS capabilities

Opportunities

• Impending 4G roll out

• Gaining prominence oflocal OEMs

• India as export hub

• Policies such as MSIPS

Weakness

• Reliance on import for chip, display and PCB

• Negligent product design

capabilities• Limited skill set

• Debilitating tax structure

Threats

• Established ecosystem in China

• Infrastructure inadequacy

• Emergence of other low cost manufacturing destinations

8/11/2019 IESA FS Report Indian ESDM Market

http://slidepdf.com/reader/full/iesa-fs-report-indian-esdm-market 35/172

2014INDIAN ESDM MARKET - ANALYSIS OF

OPPORTUNITY AND GROWTH PLAN

IESA - Frost & Sullivan : Indian ESDM MarketCONFIDENTIAL IESA COPYRIGHT

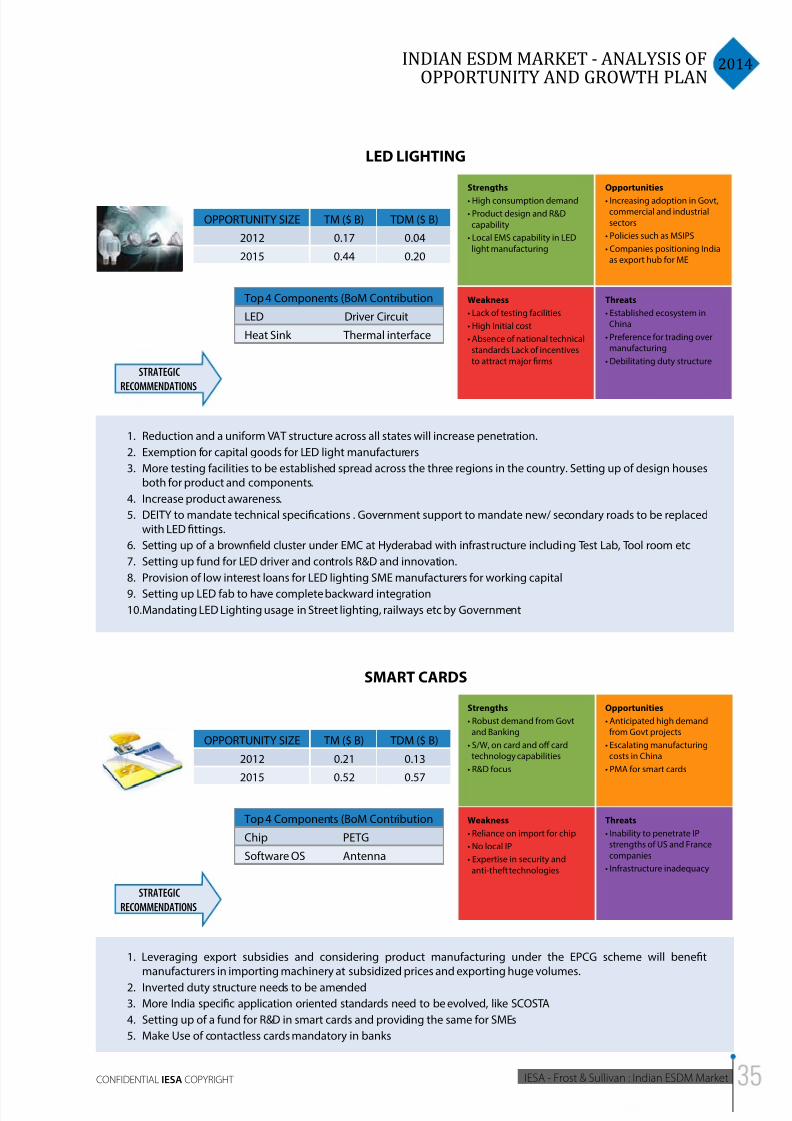

1. Reduction and a uniform VAT structure across all states will increase penetration.

2. Exemption for capital goods for LED light manufacturers

3. More testing facilities to be established spread across the three regions in the country. Setting up of design housesboth for product and components.

4. Increase product awareness.

5. DEITY to mandate technical specifications . Government support to mandate new/ secondary roads to be replacedwith LED fittings.

6. Setting up of a brownfield cluster under EMC at Hyderabad with infrastructure including Test Lab, Tool room etc

7. Setting up fund for LED driver and controls R&D and innovation.

8. Provision of low interest loans for LED lighting SME manufacturers for working capital

9. Setting up LED fab to have complete backward integration

10. Mandating LED Lighting usage in Street lighting, railways etc by Government

STRATEGIC

RECOMMENDATIONS

OPPORTUNITY SIZE TM ($ B) TDM ($ B)

2012 0.17 0.04

2015 0.44 0.20

Top 4 Components (BoM Contribution

LED Driver Circuit

Heat Sink Thermal interface

LED LIGHTING

Strengths

• High consumption demand

• Product design and R&D

capability

• Local EMS capability in LED

light manufacturing

Opportunities

• Increasing adoption in Govt, commercial and industrial

sectors

• Policies such as MSIPS

• Companies positioning India as export hub for ME

Weakness

• Lack of testing facilities

• High Initial cost

• Absence of national technical

standards Lack of incentives

to attract major firms

Threats

• Established ecosystem in China

• Preference for trading over manufacturing

• Debilitating duty structure

1. Leveraging export subsidies and considering product manufacturing under the EPCG scheme will benefitmanufacturers in importing machinery at subsidized prices and exporting huge volumes.

2. Inverted duty structure needs to be amended

3. More India specific application oriented standards need to be evolved, like SCOSTA

4. Setting up of a fund for R&D in smart cards and providing the same for SMEs

5. Make Use of contactless cards mandatory in banks

STRATEGIC

RECOMMENDATIONS

OPPORTUNITY SIZE TM ($ B) TDM ($ B)

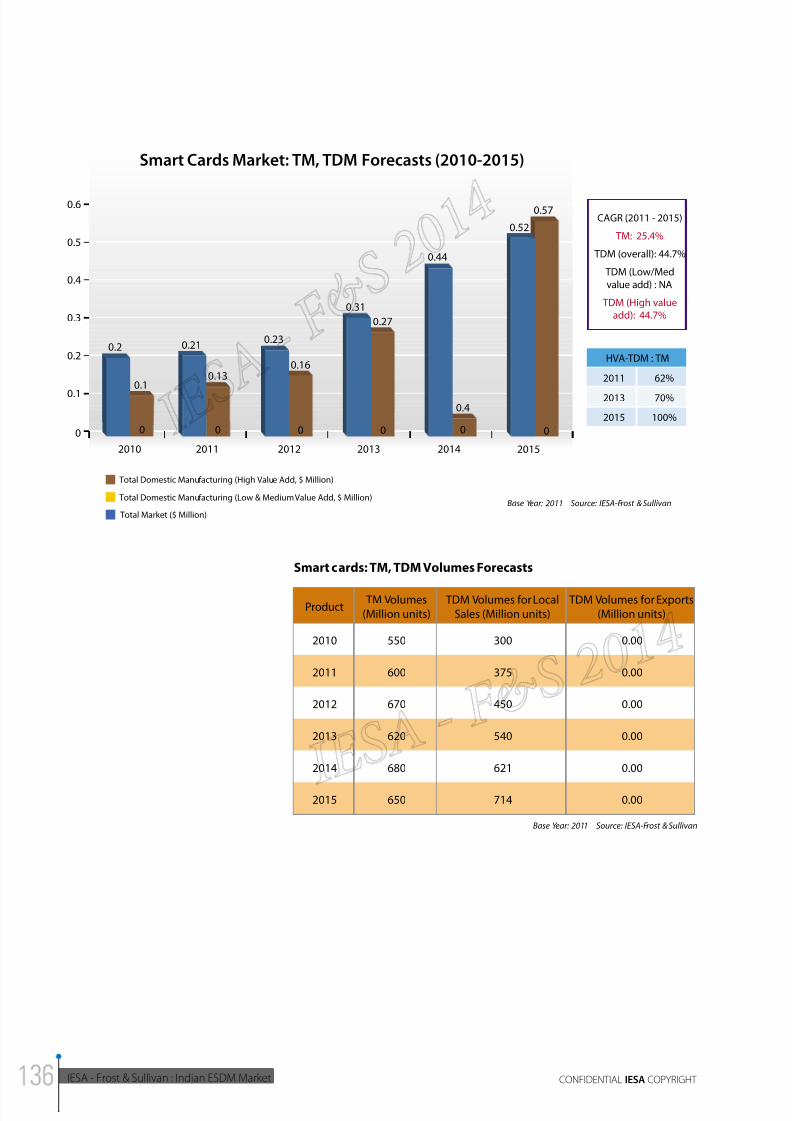

2012 0.21 0.13

2015 0.52 0.57

Top 4 Components (BoM Contribution

Chip PETG

Software OS Antenna

SMART CARDS

Strengths

• Robust demand from Govt and Banking

• S/W, on card and o card technology capabilities

• R&D focus

Opportunities

• Anticipated high demand from Govt projects

• Escalating manufacturing costs in China

• PMA for smart cards

Weakness

• Reliance on import for chip

• No local IP

• Expertise in security and

anti-theft technologies

Threats

• Inability to penetrate IP strengths of US and France

companies

• Infrastructure inadequacy

8/11/2019 IESA FS Report Indian ESDM Market

http://slidepdf.com/reader/full/iesa-fs-report-indian-esdm-market 36/172

IESA - Frost & Sullivan : Indian ESDM Market CONFIDENTIAL IESA COPYRIGHT

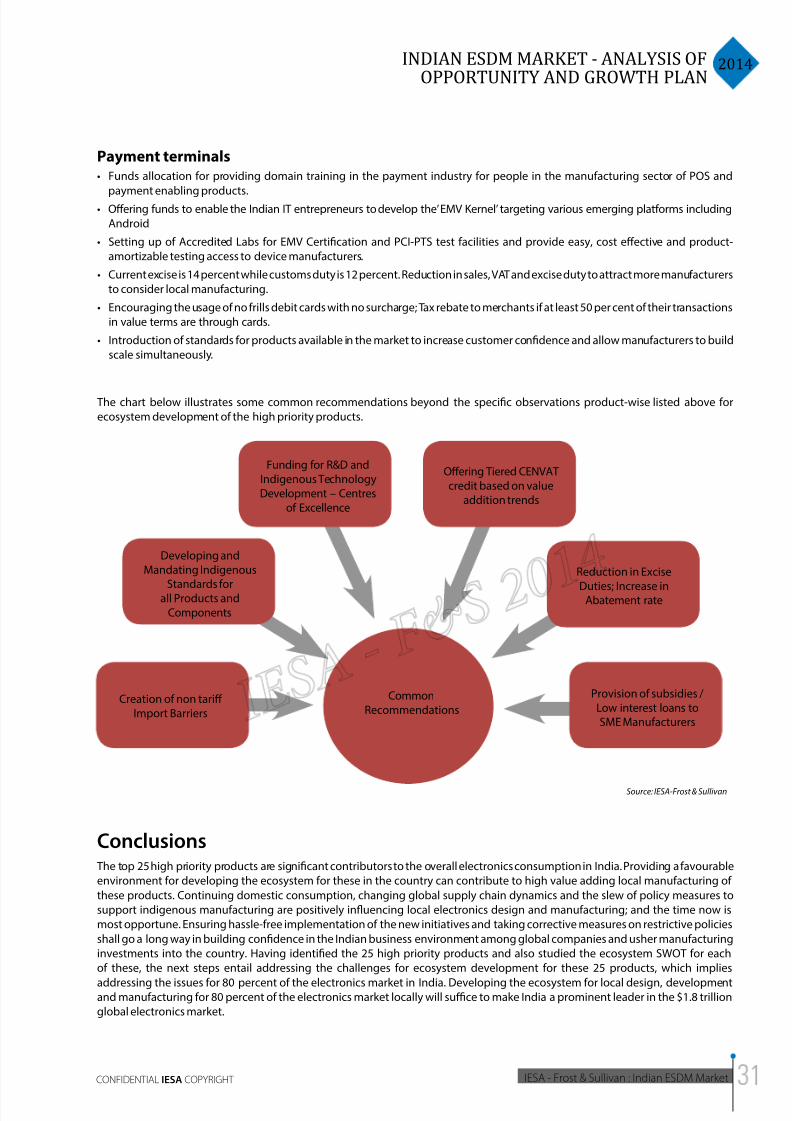

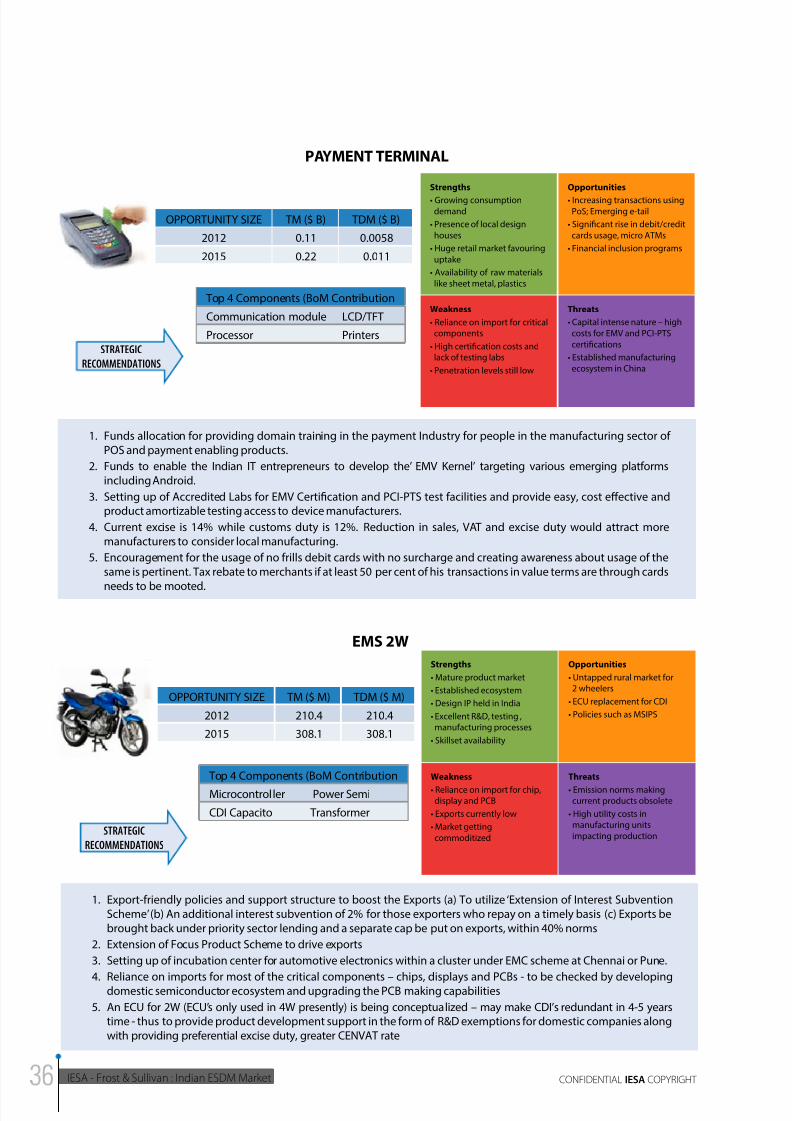

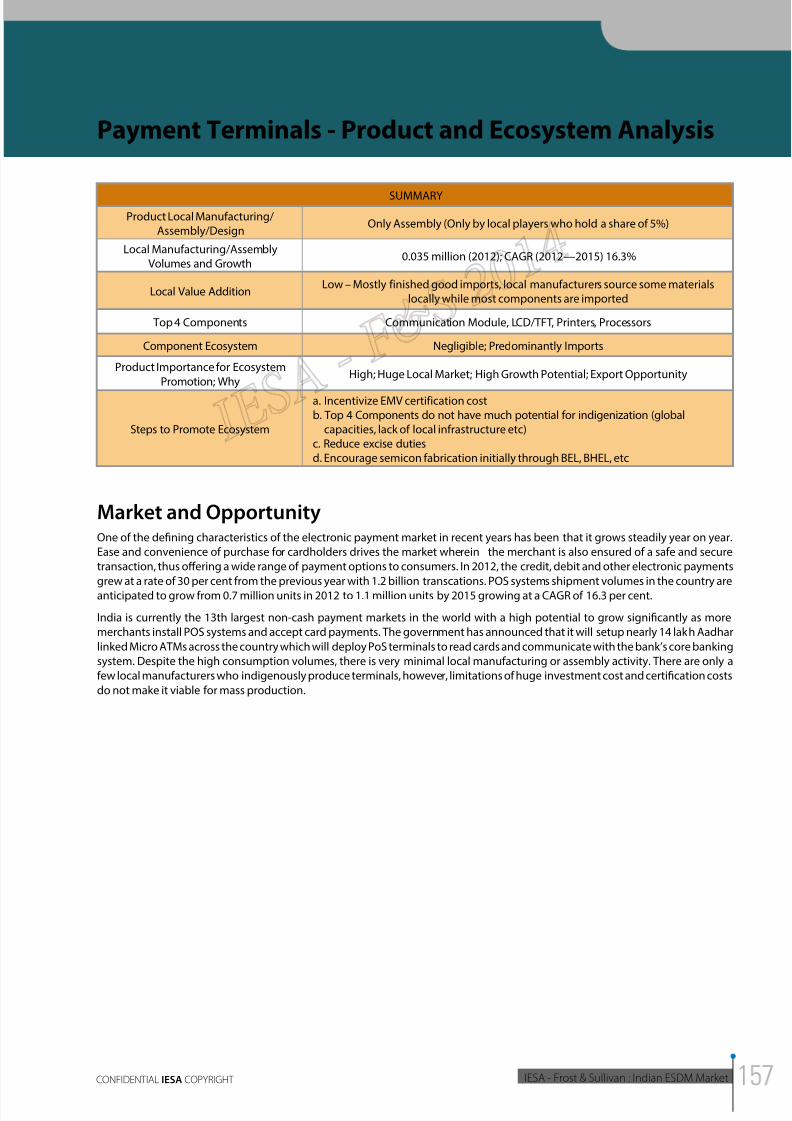

1. Funds allocation for providing domain training in the payment Industry for people in the manufacturing sector ofPOS and payment enabling products.

2. Funds to enable the Indian IT entrepreneurs to develop the’ EMV Kernel’ targeting various emerging platformsincluding Android.

3. Setting up of Accredited Labs for EMV Certification and PCI-PTS test facilities and provide easy, cost effective andproduct amortizable testing access to device manufacturers.

4. Current excise is 14% while customs duty is 12%. Reduction in sales, VAT and excise duty would attract moremanufacturers to consider local manufacturing.

5. Encouragement for the usage of no frills debit cards with no surcharge and creating awareness about usage of thesame is pertinent. Tax rebate to merchants if at least 50 per cent of his transactions in value terms are through cards

needs to be mooted.

STRATEGIC

RECOMMENDATIONS

OPPORTUNITY SIZE TM ($ B) TDM ($ B)

2012 0.11 0.0058

2015 0.22 0.011

Top 4 Components (BoM Contribution

Communication module LCD/TFT

Processor Printers

PAYMENT TERMINAL

Strengths

• Growing consumption

demand

• Presence of local design

houses

• Huge retail market favouring

uptake

• Availability of raw materials

like sheet metal, plastics

Opportunities

• Increasing transactions using

PoS; Emerging e-tail

• Signicant rise in debit/credit

cards usage, micro ATMs

• Financial inclusion programs

Weakness

• Reliance on import for critical components

• High certication costs and lack of testing labs

• Penetration levels still low

Threats

• Capital intense nature – high

costs for EMV and PCI-PTS

certifications

• Established manufacturing

ecosystem in China

1. Export-friendly policies and support structure to boost the Exports (a) To utilize ‘Extension of Interest SubventionScheme’ (b) An additional interest subvention of 2% for those exporters who repay on a timely basis (c) Exports bebrought back under priority sector lending and a separate cap be put on exports, within 40% norms

2. Extension of Focus Product Scheme to drive exports

3. Setting up of incubation center for automotive electronics within a cluster under EMC scheme at Chennai or Pune.

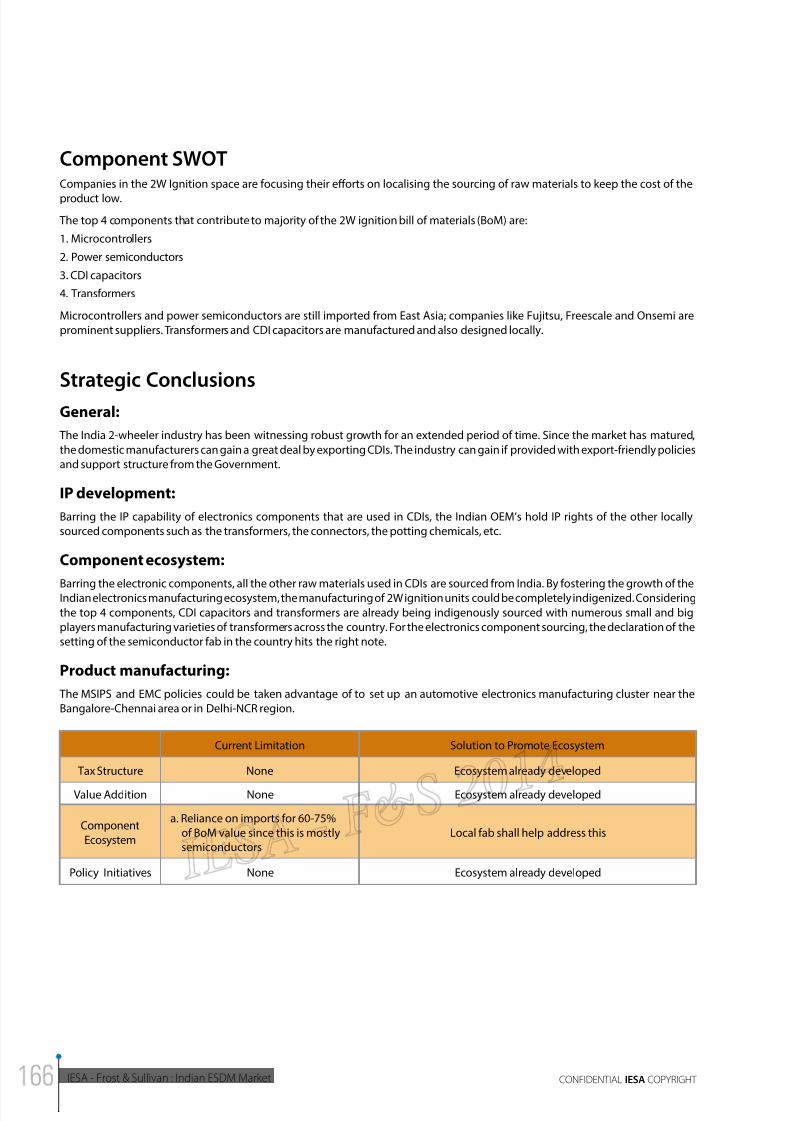

4. Reliance on imports for most of the critical components – chips, displays and PCBs - to be checked by developingdomestic semiconductor ecosystem and upgrading the PCB making capabilities

5. An ECU for 2W (ECU’s only used in 4W presently) is being conceptualized – may make CDI’s redundant in 4-5 yearstime - thus to provide product development support in the form of R&D exemptions for domestic companies alongwith providing preferential excise duty, greater CENVAT rate

STRATEGIC

RECOMMENDATIONS

OPPORTUNITY SIZE TM ($ M) TDM ($ M)

2012 210.4 210.4

2015 308.1 308.1

Top 4 Components (BoM Contribution

Microcontroller Power Semi

CDI Capacito Transformer

EMS 2W

Strengths

• Mature product market

• Established ecosystem

• Design IP held in India

• Excellent R&D, testing ,manufacturing processes

• Skillset availability

Opportunities

• Untapped rural market for2 wheelers

• ECU replacement for CDI

• Policies such as MSIPS

Weakness

• Reliance on import for chip, display and PCB

• Exports currently low

• Market getting

commoditized

Threats

• Emission norms making current products obsolete

• High utility costs in manufacturing units

impacting production

8/11/2019 IESA FS Report Indian ESDM Market

http://slidepdf.com/reader/full/iesa-fs-report-indian-esdm-market 37/172

8/11/2019 IESA FS Report Indian ESDM Market

http://slidepdf.com/reader/full/iesa-fs-report-indian-esdm-market 38/172

IESA - Frost & Sullivan : Indian ESDM Market CONFIDENTIAL IESA COPYRIGHT

Common Conclusions for the Near Term Focus Products/Components

Indian electronics industry has over the years grown in stature for its inherent strengths in fundamental R&D and consumption. The

missing link to the industry triangle is manufacturing. India’s electronics manufacturing has remained in obscurity due to multiple

reasons including scale impediments, infrastructural inadequacy, absence of large scale manufacturing ecosystems, proactive IP

orientation as well as debilitating tax and duty regimes. Recent policy initiatives to offset these disabilities clearly indicate the

identification of electronics manufacturing as a priority sector. Electronics manufacturing gains significance in that it can help

bridge a rapidly burgeoning trade imbalance while also create enormous employment opportunities for the skilled, semi-skilled

and unskilled labourers. From a strategic lens, it thus becomes prudent to evaluate Indian electronics manufacturing deficiencies

and develop capabilities that address the shortcomings as also strategize the short, medium and long term development plan for

promoting local electronics manufacturing ecosystem.

Key drivers for making India a globally attractive electronics manufacturing destination include competent costs, talent abundance,

quality focus, world-class infrastructure and business friendly environment. Of these, efforts have already been taken to improve

the country’s infrastructure apart from moderate initiatives in quality enhancement and skill set development that needs continued

acceleration. It becomes pertinent for newer policy measures to address/offer:

• Subsidies and/or tax and duty restructuring to alleviate the cost dierential arising from higher logistics cost and highertransformation cost

• Inclusion of Focus Product Scheme for select priority products in eorts to promote exports and extension of the scheme to all

EHTPs/SEZs

• Encouragement for R&D and IP generation through fund allocation and setting up of incubation centres within the EMC scheme

clusters with sector focus

• Setting up of Incubation Centres for Industry Verticals; priority products like Smart Energy Meters, Inverters & UPS, CFL, LED

Lighting and Energy Ecient products to be the areas of focus for these centres

• Provision of viability gap funding (VGF) for the priority products and components to be explored and implemented.

• Resolution of working capital issue through provision of low interest/special loans; Encouragement to nancial institutions to

offer the same by declaring electronics as a priority sector

• Simplication of processes involved in availing policy benets as well as processes involved in setting up and functioning of

businesses – creation of business friendly socio-political environment

8/11/2019 IESA FS Report Indian ESDM Market