Embed Size (px)

Citation preview

PRIVATE & CONFIDENTIALNOT FOR CIRCULATION

INDUSTRIAL DEVELOPMENT BANK OF INDIA(Established under the Industrial Development Bank of India Act, 1964)

IDBI Tower, WTC Complex, Cuffe Parade, Mumbai 400 005.Tel: (022) 22189117/22161746/22161913/22152882 Fax: (022) 22188137, 22181155

Grams: INDBANKIND. Website : www.idbi.com

MEMORANDUM OF PRIVATE PLACEMENTINDUSTRIAL DEVELOPMENT BANK OF INDIA

PRIVATE PLACEMENT OF OMNI BONDSOF RS.10 LAKHS EACH FOR CASH AT PAR

IDBI OMNI BONDS 2004/A

Note: This memorandum of private placement is neither a prospectus nor a statement in lieu of prospectus. This is only aninformation brochure intended for private use and should not be construed to be a prospectus and / or an invitation to thepublic for subscription to bonds.

Applications to Omni Bonds 2004/Awould be accepted between January 5, 2004 to January 9, 2004

Rating : AA+ by CRISIL, AA+(ind) by FITCH and LAA by ICRA

Head Office

INDUSTRIAL DEVELOPMENT BANK OF INDIAIDBI TOWER, WTC COMPLEX, CUFFE PARADE, MUMBAI – 400 005

TEL : (022) 22161746, 22152882; FAX : (022) 2218 1155, 2218 8137

2

DISCLAIMER

This Memorandum of Private Placement is neither a Prospectus nor a statement in lieu of Prospectus. It does not constitutean offer or an invitation to subscribe to the bonds issued by Industrial Development Bank of India “IDBI”. Apart from thisMemorandum of Private Placement, no offer document or prospectus has been prepared in connection with the offering ofthis Bond Issue or in relation to the Issuer nor is such a prospectus required to be registered under the applicable laws.Accordingly, this Memorandum of Private Placement has neither been delivered for registration nor is it intended to beregistered.

This Memorandum of Private Placement is not intended to form the basis of evaluation for the potential investors to whomit is addressed and who are willing and eligible to subscribe to these Bonds issued by IDBI. This Memorandum of PrivatePlacement has been prepared to give general information regarding IDBI to persons proposing to invest in this issue of Bondsand it does not purport to contain all the information that any such person may require. IDBI believes that the informationcontained in this Memorandum of Private Placement is accurate in all respects as of the date hereof. IDBI does not undertaketo update this Memorandum of Private Placement to reflect subsequent events and thus it should not be relied upon withoutfirst confirming its accuracy with IDBI.

Potential investors are required to make their own independent evaluation and judgment before making the investment. Itis the responsibility of potential investors to have obtained all consents, approvals or authorisations required by them tomake an offer to subscribe for, and purchase the Bonds. Potential investors should also consult their tax advisor(s) on thetax implications of the acquisitions, ownership, sale and redemption of Bonds and income arising thereon either by way ofinterest or capital gains.

This Memorandum of Private Placement is not intended for distribution and it is meant solely for the consideration of theperson to whom it is addressed and should not be reproduced by the recipient. The Bonds mentioned herein are being issuedon a private placement basis and this offer does not constitute nor should it be considered a public offer/invitation.

FORCE MAJEURE

IDBI reserves the right to withdraw the issue any time in the event of any unforeseen development adversely affecting theeconomic and regulatory environment. In such an event, IDBI will refund the application money, if any, alongwith the interestpayable on such application money.

This Memorandum of Private Placement is issued by IDBI and signed by its authorized signatory.

R.K. BANSALGeneral Manager

January 2, 2004

Industrial Development Bank of India has been established under the Industrial Development Bank of India Act, 1964(IDBI Act).

In terms of Section 11(1) (a) of the IDBI Act, IDBI is authorised to issue and sell Bonds with or without the guaranteeof the Central Government for the purpose of raising resources for carrying out its functions under the Act.

This offer is being made on a Private Placement basis and cannot be acted upon by any person other than the oneto whom the offer has been made.

3

RISK FACTORSInternal Factors(a) Redemption Reserve: Creation of Redemption Reserve is not envisaged for the proposed issue of Bonds.

IDBI being a public financial institution has been raising resources both from domestic market andoverseas market in the form of unsecured borrowings. In respect of the monies borrowed from overseasmarkets, IDBI has agreed to create pari passu charge if any other lender is offered security on the assetsof IDBI. Since the resources raised by IDBI are being utilised for the purpose of its business i.e. providingcredit and other facilities to the industry, the assets of IDBI are mostly in form of loans and advances.Hence it is proposed that the Bonds shall be unsecured in nature in that they shall not be secured againstany asset of IDBI. IDBI has appointed a trustee to protect the interest of the investors.

(b) Credit Risk: The business of lending carries the risk of default by borrowers.

Any term lending activity is exposed to credit risk arising from the risk of default by the borrowers. IDBI has putup a systematic credit evaluation process in place. Necessary control measures like maintaining a diversifiedportfolio with industry-wise, promoter group-wise and specific client-wise exposure limits are set to avoidconcentration of lending to any specific industry segment/ promoter group/ company. These limits helpminimise credit risk. With a view to derisk the portfolio the exposure limits have been reviewed and exposure byway of Project Finance assistance to greenfield projects have been reduced as a matter of deliberate strategy.A Credit Risk Monitoring Group (CRMG) has been set up at the Head Office to monitor the risk associated withlending to individual projects, business groups and industries. IDBI monitors the performance of its assetportfolio on a regular basis and also constantly evaluates the changes and developments in industries to whichit has substantial exposure.

(c) Market Risk: Increased interest rate volatility exposes IDBI to market rate risk arising out of maturity/rate mismatches.Risk arising from interest rate volatility is inherent to the business of financial intermediation and termlending. This risk is minimised by linking the interest rates on term lending to a base rate (PLR / MTPLRetc), which varies in accordance with overall movement in market rates. Further, the rate applicable to eachtranche of disbursement varies in accordance with the prevailing base rate. In case of lending pegged tofloating rates, they are generally matched by floating rate liability (both rupee and foreign currency). IDBImanages market risks through active Asset Liability Management (ALM), viz. liquidity, interest rate andforeign exchange risk by way of Gap/Duration Analysis so as to optimize matching of the Assets andLiabilities. Active Asset Liability Management with efforts to match Duration of Assets and Liabilities as alsoavailability of hedging mechanisms help moderate the market risk.

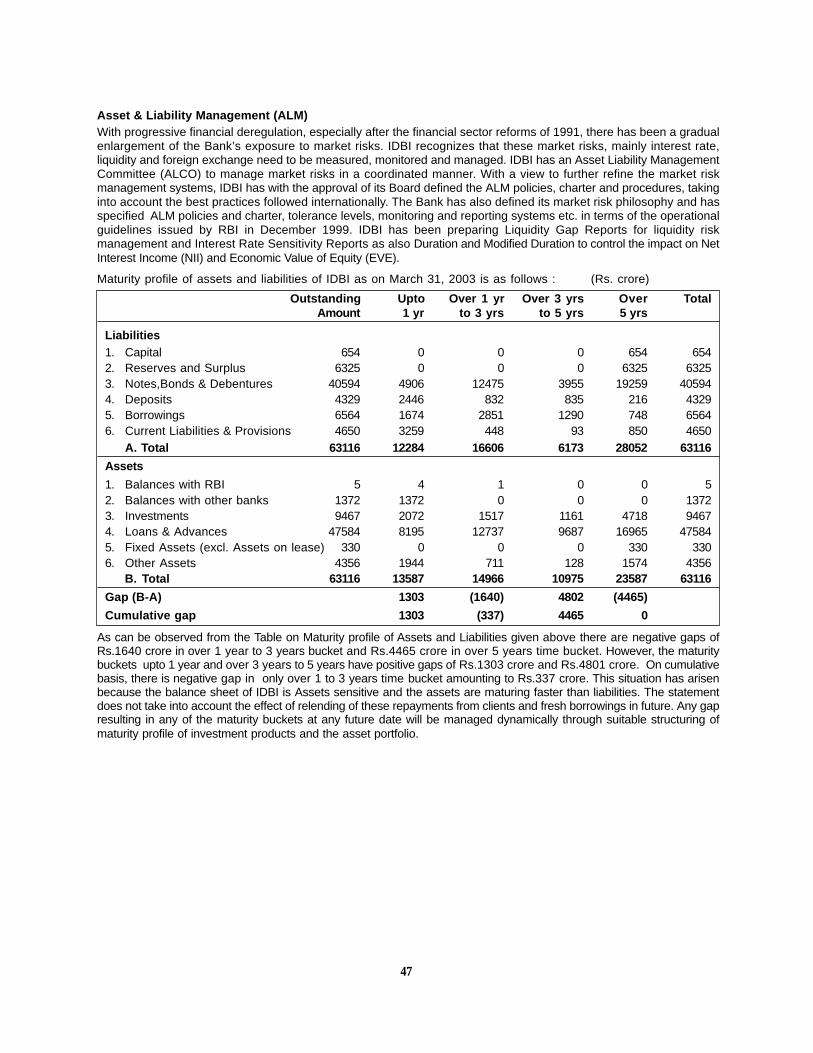

(d) Asset Liability mismatch : The maturity profile of assets and liabilities as on March 31, 2003 showsnegative gaps in over 1 to 3 years bucket and Over 5 years bucket.As can be observed from the Table on Maturity profile of Assets and Liabilities given on page 47 there arenegative gaps of Rs.1640 crore in over 1 year to 3 years bucket and Rs.4465 crore in over 5 years timebucket. However, the maturity buckets upto 1 year and over 3 years to 5 years have positive gaps of Rs.1303crore and Rs.4801 crore. On cumulative basis, there is negative gap in only over 1 to 3 years time bucketamounting to Rs.337 crore. This situation has arisen because the balance sheet of IDBI is Assets sensitiveand the assets are maturing faster than liabilities. The statement does not take into account the effect ofrelending of these repayments from clients and fresh borrowings in future. Any gap resulting in any of thematurity buckets at any future date will be managed dynamically through suitable structuring of maturityprofile of investment products, asset portfolio and liability products.

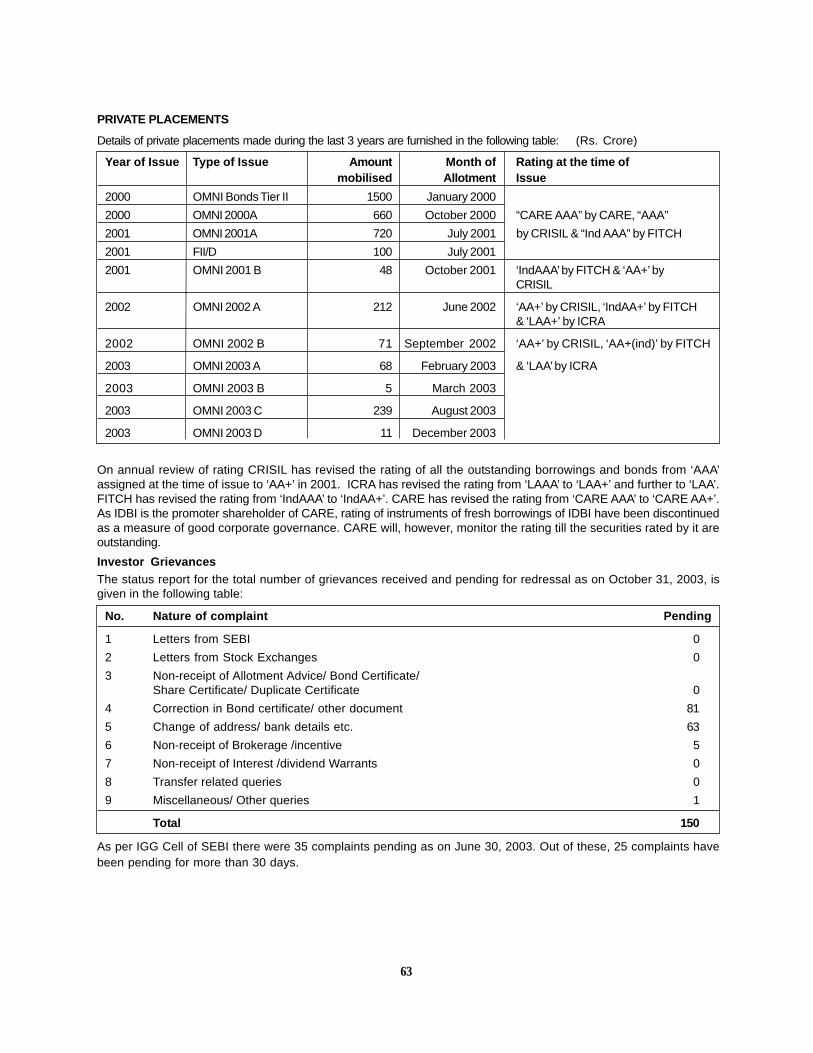

(e) Credit Rating: The credit rating of outstanding bond issues of IDBI has been revised from “AAA” to “AA+”by CRISIL, from “LAAA to “LAA” by ICRA and from “Ind AAA” to “Ind AA+” by FITCH.

The revision in ratings reflects the perception of the rating agencies. While CRISIL has reaffirmed its ratingsassigned to Fixed Deposit program of IDBI at “FAAA” and assigned the highest rating “P1+” to the Term MoneyBonds, Commercial Papers and Corporate Deposits of IDBI, it has revised during 2001-02 its rating assigned tothe outstanding bond issues and Certificate of Deposit program of IDBI from “AAA” to “AA+”. ICRA has assignedthe highest rating “A1+” to Commercial Paper, Term Money Bonds, Inter Corporate Deposits and Certificate ofDeposits of IDBI. The ratings for Fixed Deposit Programme has been reaffirmed at “MAA+”. ICRA has revisedits rating from “LAAA” to LAA+ during FY 2001-02 and to “LAA” during FY 2002-03 for bonds. FITCH hasrevised its rating during FY 2002-02 from “IndAAA” to “IndAA+” for bonds and Fixed Deposits program. While“AAA” denotes highest safety in terms of timely payment of interest and principal, “AA+” denotes high safety of

4

timely payment of interest and principal. “LAA” indicates high safety. Risk Factors are modest and may varyslightly. The protective factors are strong and the prospect of timely payment of principal and interest as perterms under adverse circumstances, as may be visualized, differs from LAAA only marginally.

(f) Contingent Liabilities: As on March 31, 2003, IDBI had contingent liabilities of about Rs.4494 crore onaccount of Guarantees, Letters of credit, Underwriting Commitments, uncalled monies on partly paidshares/debentures, claims against IDBI not acknowledged as debt and Disputed Tax claims.

The contingent liabilities are solely on account of normal operations and are subject to the prudential normsapplicable to lending and investment operations.

(g) Pending Grievances : As on October 31, 2003 there were 17 references pending pertaining to Flexibonds-6, 12 pertaining to Flexibonds–8, 15 pertaining to Flexibonds-9, 52 pertaining to Flexibonds-10, 7 pertainingto Flexibonds-11, 20 pertaining to Flexibonds-12, 21 pertaining to Flexibonds-13, 5 pertaining to Flexibonds-14 and 1 pertaining to Equity shares. Further no complaint was pending for more than 60 days.

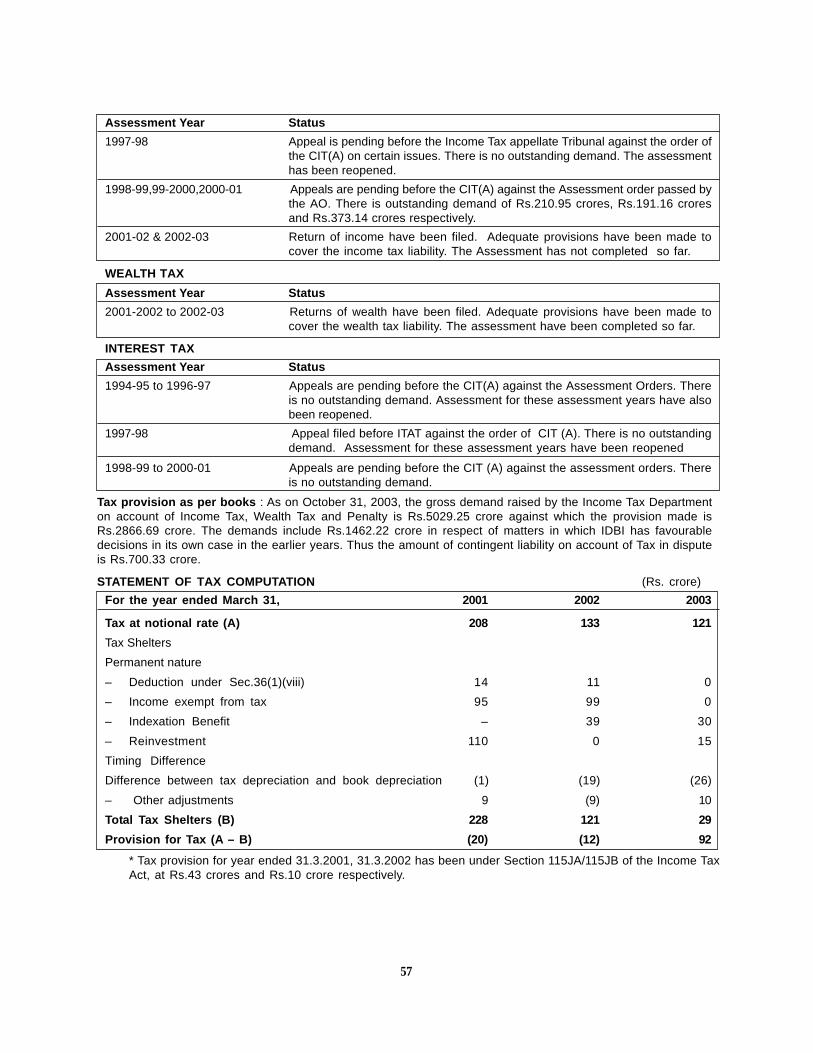

(h) Tax Liabilities: As on October 31, 2003, the gross demand raised by the Income Tax Department onaccount of Income Tax, Wealth Tax and Penalty is Rs.5029.25 crore against which the provision made isRs.2866.69 crore. The demands include Rs.1462.22 crore in respect of matters in which IDBI has favourabledecisions in its own case in the earlier years. Thus the amount of contingent liability on account of Tax indispute is Rs.700.33 crore.

Although the entire amount is in dispute, an amount of Rs.3851.24 crore has been paid.

Appeals have been filed on matters covered by the disputed amount.

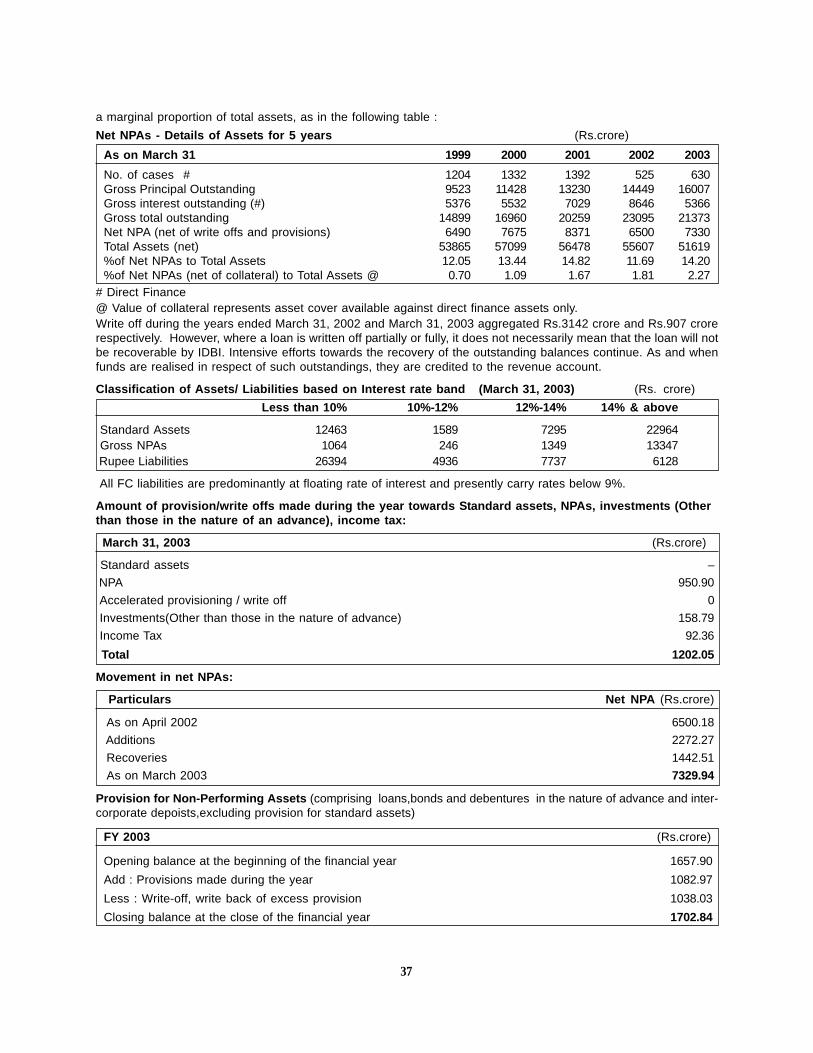

(i) Non Performing Assets (NPA) : The total NPAs of IDBI in amount terms has been increasing over the past5 years. Movement of Net NPAs over the past 5 years is detailed in the Table on page 36. Net NPAs (percentof total assets) has increased from Rs.6490 crore (12.05%) as on March 31, 1999 to Rs.7330 crore as onMarch 31, 2003 (14.20%).

IDBI has initiated measures for NPA containment by setting up Close Monitoring Cells and RestructuringCommittees. IDBI actively monitors all assisted companies for timely recovery of dues. With respect todefaulting accounts, IDBI places emphasis on recovery, settlement and containment of NPAs. The CloseMonitoring Cells constantly monitor performance of assisted companies to improve recovery and initiate pro-active remedial actions. Efforts of Close Monitoring Cells are reinforced by Empowered Committee and HighPower Committee at Head Office. These committees assess and advise necessary restructuring and one-timesettlement process. Wherever the long-term viability of assisted companies is in question, legal measures areinitiated and securities are enforced. In cases where financial restructuring is under consideration,discussions are held with other term lenders as also with working capital bankers to have a co-ordinatedapproach to ensure quicker recovery. A Corporate Debt Restructuring (CDR) mechanism has been set up tofacilitate this. Further, there has been substantial changes in the legislative and operating environment enablingFIs and banks to aggressively pursue recovery of overdues. Besides the Debt Recovery Tribunal (DRT) set upfor faster settlement of recovery litigation, GOI has recently promulgated ‘The Securitisation andReconstruction of Financial Assets and Enforcement of Security Interest (SRES) Act, 2002’, enabling FIs andbanks to securitise and reconstruct the financial assets and enforce security of FIs and banks without pursuingthe available legal route. As on May 31, 2003 IDBI has issued notices to 49 defaulting borrowers with anoutstanding assistance of Rs.1588 crore by invoking provisions under the said Act. Further in 33 cases IDBIhas sought consent of other secured creditors for initiating action under the Act. After the SRES Act has comeinto effect IDBI has initiated action against chronic defaulters resulting in many defaulters willinglly comingforward for settlement of their dues. IDBI has been taking recourse to all available methods for recovery ofoverdues including reporting to RBI the name of wilful defaulters simultaneous with initiation of necessarysteps for recovery. IDBI has also initiated aggressive One Time Settlement (OTS) measures to recoveroverdues. Aggregate of provisions / write offs as a percentage of Gross NPAs stood at 54% as on March 31,2003. To facilitate recovery of overdues and reconstruction of weaker assets, IDBI in participation with SBI,ICICI Bank and a few other institutions and Banks have set-up an Asset Reconstruction Company (ARC). Withthe changes in operating and legislative environment including formation of the ARC coupled with the NPAmanagement measures initiated the NPA levels are expected to be contained/ reduced.

(j) Overdues : The overdues of Videocon Group Companies, in which Shri R. N. Dhoot (industrialist director inthe Board of IDBI) was associated, as on December 29, 2003 amounted to Rs.30.77 crore. The group hasindicated that it would clear the overdues by January 2004.

5

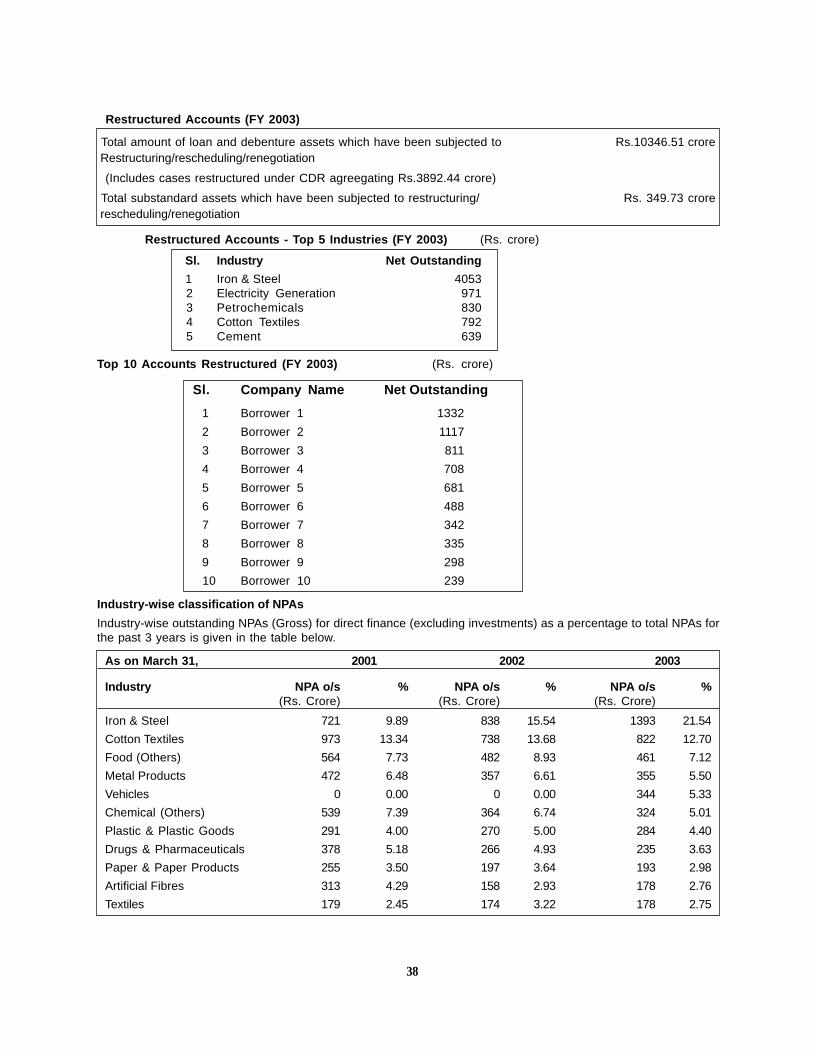

(k) Asset concentration to few industries : The top 5 industries account for 48.17% of the total outstandingassistance as on March 31, 2003. Large exposures to specific industries will be impacted by global trendsin these industries.

IDBI’s loan portfolio is well diversified among industries. The major outstandings are to the iron and steel, power,cotton textiles, telecom services and petrochemicals, which together accounted for about 48% of theoutstandings as at March 31, 2003. As a prudential measure, IDBI has recently revised the exposure limit toindividual industry at 10% of its total portfolio or Rs.5000 crore whichever is lower. As on March 31, 2003 onlytwo industries viz. Iron & Steel (18.31%) and Electricity Generation (12.58%) exceeded the limit. This excesshas been largely due to historical factors wherein IDBI had been extending assistance to core sector projectsin line with overall national objectives. IDBI particularly monitors both domestic and global trends anddevelopments in industries accounting for higher exposure within its portfolio and takes necessary actions andremedial measures to maintain its portfolio quality and reduce any possible adverse impact on its financials.

(l) Change In Balance Sheet size : IDBI’s total asset and liabilities have decreased from Rs.66,643 crore toRs.63,116 crore during FY 2003.

To improve the asset quality, IDBI has restricted new assistance and extends assistance only on veryselective basis. On the liability side, IDBI has exercised call option on its high cost borrowings during theyear. Change in the Balance Sheet size is a part of the deliberate strategy of IDBI to pursue quality assetgrowth and profitability in operations.

(m) Nature of Bonds : The Bonds/Letter of Allotment/ Certificate of Holding are valuable documents and shouldbe kept safely. Duplicate bonds will be issued only in accordance with the procedure specified later in theoffer document. The bonds are also offered in demat mode.

(n) Decrease in profit : The profit after tax of IDBI is Rs.401 crore for FY 2003 as against Rs.424 crore forFY 2002 and Rs.691 crore for FY 2001. IDBI’s profit after Tax for the half year ended September 2003 stoodat Rs.176 crore as against Rs.152 crores in the corresponding half year ended September 30, 2002.

General economic slowdown in the recent past has led to lower industrial activity. During the last couple ofyears credit off-take has been low due to lower industrial growth in spite of fall in interest rates and othersteps taken by the Government to boost the industrial performance. Foray of commercial banks into termlending has also resulted in increased competition to extend assistance to creditworthy clients at verycompetitive rates. Resultant lowering of interest income and overall squeezing of margin has impacted theprofit after tax. However with the expected economic upturn the position is expected to improve. Furtherrecovery out of written off cases will directly add to the profit of IDBI.

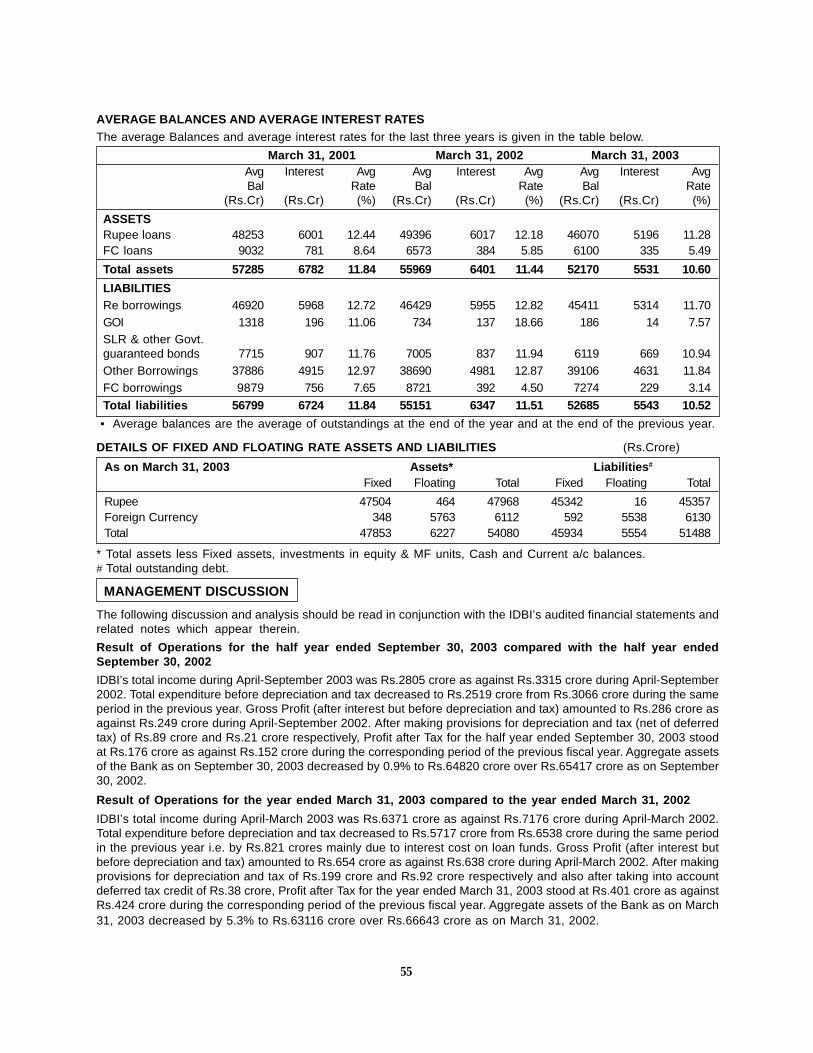

(o) Return on Assets : The return on average assets has declined from 10.4% in FY 2002 to 9.8% in FY2003 while the average cost of funds has also gone down from 9.2% to 8.5% over the same period.

The major factor impacting the returns and costs is the sharp drop in interest rates during the last few years.This has resulted in prepayment of borrowing by high credit clients which in turn has, to some extentimpacted credit composition of the portfolio. This coupled with NPAs adversely affected return on assets.On the cost front, impact of drop in incremental cost of rupee borrowing (12.08% in FY 2000 to 11.21%in FY 2001, to 9.81% in FY 2002 and further down to 8.35% in FY 2003) and exercising of call optionon high cost borrowings by IDBI has resulted in decline in cost of borrowing. The average cost of loanfunds has reduced from 11.5% in FY 2002 to 10.5% in FY 2003. As may be observed from above, thedecline in average cost of funds has been more than the decline in average return on assets. Further asmentioned on page 43 of this Memorandum of Private Placement a proposal has been formulated under theauspicies of GOI wherein the liabilities of IDBI to public sector Banks, Institutions etc. will be restructuredwhich will bring down the average cost of funds significantly.

(p) Quoted Investments : IDBI has in its portfolio quoted investments aggregating Rs.2730.22 crore as onMarch 31, 2003 which are booked at cost whose market value amounted to Rs.2152.54 crore. As onMarch 31, 2003, IDBI had debentures of Rs.4389.16 crore in its portfolio. All the debentures are securedby hypothecation/mortgage of fixed assets. However, in case of debentures amounting to Rs.795 crore,the final security by way of mortgage was yet to be created as on March 31, 2003.

IDBI’s investment portfolio is predominantly of long term and strategic nature. Temporary diminution in valueof securities arises on account of price volatility due to factors and forces affecting the stock market, interestrates, etc. IDBI has been classifying its investment portfolio and making appropriate provision for diminutionin value as per RBI guidelines issued from time to time in this regard. The investments are classified underthe following categories (i) Held to Maturity, (ii) Available for Sale (iii) Held for Trading. These investments were

6

valued according to the prevailing valuation norms.

(q) Foreign Exchange Risk : IDBI may be exposed to foreign exchange risk on account of changes in foreignexchange rates.

IDBI maintains a currency-wise matching of assets and liabilities. IDBI makes foreign currency loans onterms that are similar to its foreign currency borrowings thereby transferring the foreign exchange risk tothe borrower. In case of certain foreign currency borrowings that are re-lent in rupees, the Govt. of Indiabears the foreign exchange risk on these borrowings pursuant to certain agreements between IDBI and GOI.IDBI’s foreign currency cash balances are generally maintained abroad in currencies matching with theunderlying borrowings. IDBI also operates a USD denominated single currency pool (SCP) and interest raterisks under the SCPs are hedged through basic SWAPs. IDBI is therefore not exposed to any significantrisk on account of foreign exchange fluctuations.

External Factors(a) Changes in Government policies may impact the performance of the industrial sector, which may in

turn affect IDBI

Indian industry has demonstrated remarkable resilience in adjusting to the changed environment andcompetition in the wake of the economic reforms initiated by the Government. Further, IDBI’s diversifiedportfolio provides a sufficient cushion against any downtrend in a particular industry or sector.

(b) Risk of Competition : Competition in the financial sector has increased and is likely to increase furtherwith the entry of commercial banks and other new players in term lending. IDBI faces competition bothin corporate lending and in raising resources.

While focusing attention on its core business of project financing and infrastructure financing in particular,IDBI has taken steps to diversify its operations in various other areas like working capital financing,merchant banking, corporate advisory services, forex services, venture capital, non-fund based activities etc.IDBI, through its subsidiary/ associate companies also addresses the needs of its clients for commercialbanking requirements, depository services, capital market related services, information technology servicesetc.

On the resource-raising front, avenues like Mutual Funds,Charitable and Religious Trusts, Private insurancecompanies, Pension Funds, etc. hold good potential. IDBI has over the years strengthened its reach to retailsegment through its public issues of retail bonds and Fixed Deposits marketed through its 35 branch offices,large agent network, broking outfits and debt market intermediaries. IDBI is also in the process of convertingitself into a commercial bank.

(c) Development of the capital markets may lead to disintermediation by borrowers.

With the development and maturing of the capital markets, there has been a distinct shift in the pattern ofindustrial financing. However, it will be noteworthy that while a part of the financial requirement of theindustrial projects may be met by direct borrowing from the investors, a major portion will still need to beserviced by financial intermediaries. Consequent to the opening up of the economy, large projects ininfrastructure, power, petroleum, telecom, etc. with huge financial outlays are being set up. Their large fundrequirements are unlikely to be met by private investments alone. Accordingly, the requirement of funds bothfrom lending institutions/banks and the capital market is likely to increase substantially. Also, thedisintermediation brings with it the opportunity for IDBI to expand its fee based activities.

General Risks

Investors are advised to read the risk factors carefully before taking an investment decision in thisoffering. For taking an investment decision, the investor must rely on his/her own examination of theissuer and the issue including the risks involved. The Bonds have not been recommended or approvedby SEBI nor does SEBI guarantee the accuracy or adequacy of this document.

Notes

1. IDBI would like to clarify that inspction by RBI is a regular exercise and is carried out periodically by RBIfor all banks and Financial Institutions. IDBI is in dialogue with RBI in respect of observation made by RBIin their report for the previous year. The reports of RBI are strictly cnfidential. RBI does not allow disclosureof its inspection report and that all the disclosures in the Memorandum of Private Placement are on the basisof Management and Audit Reports of the issuer.

2. The Networth of IDBI as on March 31, 2003 was Rs.6945 crore.

3. The Book Value per share of IDBI as on March 31, 2003 was Rs.106.4. Cost per share to the promoter of

7

IDBI i.e. GOI is Rs.10 (i.e. at par).

4. Shri R. N. Dhoot, a director on the board of IDBI, nominated by the Government of India, was on the boardof some of the Videocon group companies during the last 5 years. SEBI had taken action against one ofthe Videocon group companies viz. Videocon International Ltd. and 3 of its officials. On an appeal filed byVideocon International Ltd, the SAT vide its order dated June 20, 2002 has set aside SEBI’s order directingVideocon International Ltd. in so far as not to raise money from the public in the capital market for a periodof 3 years. SEBI has filed an appeal against the said SAT order in the Hon’ble High Court of Mumbai andthe appeal is not so far admitted. Shri R.N. Dhoot is, however, not a Director on the Board of VideoconInternational Ltd., nor does he figure in the list of 3 officials mentioned above.

5. As on March 31, 2003, loan outstanding to companies with which industrialist directors presently on theBoard of IDBI were associated in the past, amounted to Rs.908.64 crore, comprising of loans to (i) 8companies engaged in the electronics and electronics appliances industry (Rs.567.44 crore), (ii) a companyin petroleum industry (Rs.341.20 crore). These loans constituted 1.76% of the total loan outstanding and13.08% of IDBI’s Net Worth as on March 31, 2003.

6. The bonds may have various features/options. Such features need specific attention of the investor.

7. Summary of transactions of IDBI with its subsidiaries for three years ended

(Rs. crore)

March 31, 2001 March 31, 2002 March 31, 2003

Interest income 145.42 5.81 2.91

Dividend, fees, commission and other revenue 93.09 51.51 152.00

Interest expense 5.86 2.57 0.17

Administrative and other expenses 1.75 8.37 7.73

Outstanding BalancesLoans 809.76 1.20 58.00

Investments 648.10 388.10 296.60

Current assets 0.27 19.47 105.73

Long term debt 112.58 50.00 4.61

Current Liabilities 2.20 7.67 8.63

8. The financial information as contained in the Auditor’s Report, including the notes to accounts, significantaccounting policies as well as Auditor’s qualifications have been duly certified by the Auditors of IDBI. asfar as possible, the Audited numbers have been used for computation of or arriving at the other financialinformation contained in the Memorandum of Private Placement. However, such other financial informationcontained in the Memorandum of Private Placement except as contained in the Auditor’s Report has beencertified by the management of IDBI.

8

DEFINITIONSThe Corporation/IDBI/Issuer Industrial Development Bank of India, has been established in July, 1964 under

the IDBI Act, 1964Issue/Offer/Private Placement Private Placement of OMNI Bonds 2004/AThe Act The Industrial Development Bank of India Act, 1964The Bond(s) IDBI OMNI BondsBondholder/Debenture holder The Holder of the BondsRegistered Bondholder Bondholder whose name appears in the register of Bondholders maintained by

IDBI or its Registrar and beneficial ownersRegistrars Investor Services of India Ltd (ISIL) has been appointed by IDBI to monitor

the applications while the Private Placement is open and co-ordinate thepost private placement activities of allotment, dispatching interest warrantsetc.Contact Address:Investor Services of India Ltd.IDBI Building, Plot No.39-41; Sector 13, CBD Belapur,Navi Mumbai - 400 614.Tel. : (022) 27579636 Fax : (022) 27579650.

ON TAP ISSUE OF OMNI BOND OF RS.10 LAKHS EACH FOR CASH AT PAR UNDER OMNI BOND PRIVATEPLACEMENT

OPTIONS AT A GLANCE

Brief particulars of the options offered are tabulated below.

IDBI OMNI BONDS 2004/A

RRB I RRB II RRB III RRB IV(Floating)

Face Value Rs.10 Lakhs Rs.10 Lakhs Rs.10 Lakhs Rs.10 Lakhs

Minimum One Bond One Bond One Bond One BondInvestment i.e. Rs.10 Lakhs i.e. Rs.10 Lakhs i.e. Rs.10 Lakhs i.e. Rs.10 Lakhs

Additional Multiples of Multiples of Multiples of Multiples ofone bond one bond one bond one bond one bond

Interest Rate* 6.00% p.a. 115 bps over 6.20% p.a. 6.30% p.a.5 year G-Sec

Tenor 5 years 5 years 7 years 10 years

Put/ Call option None None None None

* Subject to TDS as applicable. Investors are advised to read the Tax Treatment for more details.

Dates of Private Placement

Application to OMNI Bonds 2004/A would be accepted between January 5, 2004 and January 9, 2004. IDBI at its solediscretion may close the issue earlier or extend the date of closure.

Deemed Date of Allotment

Deemed date of allotment for OMNI Bonds 2004/A would be January 16, 2004.

9

Rating

The bonds have been rated AA+ (Rating Watch with Developing Implications) by CRISIL, AA+(ind) (the outlook on the ratingis ‘Evolving’) by FITCH and LAA by ICRA.

Institution Rating Category Meaning of the rating

CRISIL(Credit Rating and “AA+” Debentures (Bonds) High safety with regard to timely payment ofInformation Services principal and interest. Though the circumstancesIndia Ltd) providing this degree of safety are likely to change,

of such changes as can be envisaged are mostunlikely to affect adversely the fundamentallystrong position of such issues

FITCH Ratings “AA+(ind)” Long term debt High credit quality, AA(ind) ratings indicate a lowIndia Pvt Ltd expectation of credit risk. They indicate strong

capacity for timely payment of financialcommitments. This capacity may vary slightly fromtime to time because of economic conditions.

ICRA (Investment “LAA” Debentures, High safety. Risk factors are modest and may varyInformation and Bonds, slightly. The protective factors are strong and theCredit Rating Agency) Preference Shares prospect of timely payment of principal and

interest as per terms under adversecircumstances, as may be visualised, differs from‘LAAA’ only marginally.

The Rating(s) are not a recommendation to buy, sell or hold securities and Investors should take their owndecisions. The rating may be subject to revision or withdrawal at any time by the assigning Rating Agency on thebasis of new information. Each rating should be evaluated independently of any other rating.

10

PART – I

PRIVATE PLACEMENT STRUCTURE

GENERAL INFORMATIONIndustrial Development Bank of India is offering for subscription, on private placement basis, the OMNI Bonds of the facevalue of Rs.10 lakhs each for cash at par.

The minimum investment shall be one bond i.e. Rs.10 lakhs and in multiples of one bond thereafter.

AUTHORITY FOR THE ISSUEThe Issue is made pursuant to Section 11(1)(a) of the IDBI Act. The Board of Directors of IDBI at its Meeting held on June20, 2003 and October 29, 2003, passed resolution approving the the borrowing programme for the FY 2003-04.

The current issue of IDBI is in accordance with the terms of RBI’s letter No. DBS.FID. 21/09.01.02/1999-2000 dated June 21,2000 and DBS.FID No.966/09.01.02/2001-02 dated March 2, 2002 regarding issue of bonds by Financial Institutions.

IDBI, being a public financial institution, has been raising resources both from domestic and overseas market in the formof unsecured borrowings. In respect of the monies borrowed from overseas markets, IDBI has agreed to create pari passucharge, if any other lender is offered security on the assets of IDBI. Since the resources raised by IDBI are being utilisedfor the purpose of its business i.e. providing credit and other facilities to the industry, the assets of IDBI are mostly in formof loans and advances. Hence it is proposed that the Bonds shall be unsecured in nature in that they shall not be securedagainst any assets of IDBI.

TERMS OF THE ISSUEThe Bonds will be subject to the provisions of the IDBI Act, the Industrial Development Bank of India General Regulations,1994, Industrial Development Bank of India (Issue and Management of Bonds) Regulations, 1972, Industrial DevelopmentBank of India Bonds and Deposits (Nomination) Regulations, 1997, relevant other statutory guidelines and the terms of thismemorandum.

OBJECTS OF THE ISSUEThe Issue is for augmenting the medium to long-term rupee resources of IDBI for the purpose of carrying out its functionsauthorised under the IDBI Act.

The Main Object Clause of IDBI, as contained in the IDBI Act, authorises IDBI to undertake the activities for which the fundsare being raised under the present issue. Also, the main objects of IDBI as contained in IDBI Act adequately cover theactivities undertaken by IDBI.

NATURE OF BONDSThe Bonds are unsecured and are in the form of entry in the books of IDBI and are issued in the form of Letter of Allotment/Certificate of Holding governed by the Industrial Development Bank of India (Issue Management of Bonds) Regulations, 1972(the Bond Regulations).

The Bonds shall rank pari passu, inter se, and subject to any obligations preferred by mandatory provisions of the lawprevailing from time to time and with regard to repayment of principal and payment of interest, with all other unsecuredunsubordinated borrowings of IDBI. These Bonds will rank superior to all the existing and future unsecured subordinatedborrowings of IDBI.

FUTURE BORROWINGSIDBI will be entitled to borrow/raise loans or avail financial assistance in whatever form as also issue of debentures/bonds/other securities in any manner having such ranking in priority, pari-passu or otherwise and change the capital structureincluding issue of shares of any class or redemption or reduction of any class of paid-up capital on such terms and conditionsas IDBI may think appropriate without the consent of or intimation to the bondholders.

PRINCIPAL TERMS OF THE BONDS

Issue Size : Rs.600 crore with green shoe option of Rs.600 crore

Interest RateThe Investor in the IDBI OMNI Bonds 2004/A will have the following options.

IDBI Regular Return Bond I (RRB I)The Investor receives interest at 6.00% p.a. annually for 5 years.

11

IDBI Regular Return Bond II(Floating)(RRB II)Interest Rate on the bonds will be linked to the 5 year Government of India Securities of residual maturity 5 years. These rates willbe reset on January 16 every year. The applicable rate will be fixed at 115 bps above the average yield (simple average) of the 5 yearbenchmark security for the 6 business days preceding the date of allotment (for the first interest payment period)/due date ofpayment of interest.

The benchmark 5 year rate will be the 5 year G-Sec rate put out by Reuters at 12.00 hrs IST on its page 0#INBMK=. The rate asappearing on the reference page is a semi annual rate and the same will be annualised while fixing the rate.

If the above mentioned Screen has either been renamed or if the identical information is being presented by Reuters on a differentscreen (the Replacement screen), the rate will be determined by utilizing the methodology set out above but with reference to theReplacement Screen. If such a rate does not appear on the Reuters Screen 0#INBMK= without a replacement being provided, therate for the Reset will be the 5 yr bench mark rate appearing on Reuters page INCMT.

IDBI Regular Return Bond III (RRB III)The Investor receives interest at 6.20% p.a. annually for 7 years.

IDBI Regular Return Bond IV (RRB IV)

The investor receives interest at 6.30% p.a. annually for 10 years.

Minimum InvestmentEach bond has a issue price of Rs.10 Lakhs. The minimum investment shall be 1 bond i.e. Rs.10 Lakhs and in multiples of1 bond i.e. Rs.10 Lakhs thereafter.

Interest Payment Dates for Options RRB I to IVInterest on bonds under IDBI Regular Return Bond I to IV accrues from the deemed date of allotment, i.e. January 16, 2004.Interest will be due and payable on January 16 every year. The first payment of interest for the period from the deemed dateof allotment upto January 15, 2005 will be made on January 16, 2005. In case, the date of payment of interest falls on Saturday/Sunday/Public Holiday, payment of interest will be made on immediately preceeding business day without any adjustmentto the actual days vis-a-vis the notified interest payment date.

MaturityIDBI Regular Return Bond I and II: The Bonds under these options will mature on the expiry of 5 years from the deemeddate of allotment. i.e. January 16 2004. The date of maturity will be January 16, 2009. On maturity, the Bonds will be redeemedat face value (Rs. 10 Lakhs per bond).

IDBI Regular Return Bond III: The Bonds under this option will mature on the expiry of 7 years from the deemed date ofallotment i.e. January 16, 2004. The date of maturity will be January 16, 2011. On maturity, the bonds will be redeemed at theface value (Rs.10 Lakhs per bond).

IDBI Regular Return Bond IV: The Bonds under this option will mature on the expiry of 10 years from the deemed dateof allotment. i.e January 16, 2004. The date of maturity will be January 16, 2014. On maturity, the bonds will be redeemedat the face value (Rs.10 Lakhs per bond).

Put/ Call Option

There is no put option to the investor or call option for IDBI in the IDBI OMNI Bonds 2004/A.

Deemed Date of Allotment

Deemed Date of Allotment of the Bonds under 2004/A will be January 16, 2004.

Tax Deduction at SourcePayment of interest will be subject to deduction of tax at source as per prevailing tax laws. Please refer to the section ‘TaxTreatment’.

Interest on Application moneySuccessful applicants will be paid interest on their application money, at the coupon rate for the respective Regular ReturnBond from the date of realisation of cheque/DD by IDBI up to the Deemed Date of Allotment. In case of Regular ReturnBond II (Floating), interest on application will be paid at the rate arrived at for the first setting i.e. as on the Deemed Date

12

of Allotment. Interest on application money will be paid within 30 days from the Deemed Date of Allotment. These wouldbe despatched by registered post at the allotteess’ risk. Income Tax as applicable will be deducted at source at the time ofpayment of interest on application money. Those desirous of claiming exemption from tax are required to submit a certificateissued by the income-tax officer concerned in form 15AA or submit Form 15G in duplicate as applicable along with theapplication form.

TAX TREATMENTTax Deduction at Source :No Income tax will be deducted at source from interest payable on Bonds in the following cases:

(a) On listing of the bonds, in case of payment of interest to a Bondholder, who is an individual and resident in India, where theinterest payment in the aggregate during the financial year does not exceed Rs.2,500/-.

(b) Where the Bondholder submits a declaration (wherever applicable), every financial year, in the prescribed form (15G/15H asthe case may be) and verified in the prescribed manner.

(c) Where on application by any Bondholder, the Assessing Officer issues a certificate that the total income of the bondholderjustified no deduction, as per the provisions of Section 197(1) of the IT Act (Form 15AA).

(d) Tax will be deducted at a lower rate where the Assessing Officer, on an application of any Bondholder, issues a certificatefor deduction of tax at such lower rate as per provisions of the Section 197(1) of the IT Act (Form 15AA).

Capital GainsThe difference between the sale price on transfer and the cost of acquisition of the Bond held by the bondholder as a capitalasset, will be treated as long-term capital gain/loss in the hands of the investor, provided that such Bond was held for acontinuous period of more than twelve months (on listing on The Stock Exchange, Mumbai). It may be noted that the variousBonds under consideration, being debt instruments, will not have the benefit of cost indexation.

Investors who wish to avail of the exemption from tax on capital gains on transfer of capital asset as provided in sections54EC, 54ED or 54F of IT Act, may do so subject to the conditions as prescribed in those sections. Moreover, investors areadvised to consult their tax advisors in this matter.

Income from the BondsInterest payable on these bonds in any financial year will be taxable in that year.

WEALTH TAXThe Bonds are exempt from Wealth Tax without any monetary limit, as per the present provisions of the Wealth Tax Act,1957.

GENERAL TERMSISSUE OF BONDSThe necessary arrangements for dematerialisation of bonds will be done with National Securities Depository Ltd. (NSDL) andCentral Depository Services Ltd. (CDSL). Investors should indicate the necessary details in the application form. Theapplication forms without these details will not be accepted. Bonds will be credited in the demat account on allotment.

REDEMPTIONThe investors should furnish a receipt in the prescribed form (Form XIV) of the Bonds Regulations for the principal amountalongwith relevant certificate of holding for obtaining the repayment. The bondholders should get his/her/its name registeredwith IDBI.

RIGHT TO ACCEPT OR REJECT APPLICATIONSIDBI is entitled at its sole and absolute discretion, to accept or reject any application in part or in full, without assigningany reason. The application forms which are not complete in all respects are liable to be rejected. Application Forms withoutthe Phone and/or Fax numbers of the applicant would be treated as incomplete.

NOTICESAll notices to the Bond holder(s) required to be given by IDBI shall be deemed to have been given if published in one Englishand one regional language daily newspaper, or may, at the sole discretion of IDBI, but without any obligation, be sent to

13

the Bonds holder(s) at the address stated in the Application Form, or at the address as notified by the Bonds holder(s) indue course. All notices to IDBI by the Bonds holder(s) must be sent by registered post or by hand delivery to IDBI at itsHead Office or to such person(s) at such address as may be notified by IDBI from time to time.

REGISTER OF BONDHOLDERSThe register of Bondholders containing necessary particulars will be maintained by IDBI/Registrar to the Issue at their HeadOffices.

RIGHTS OF ALL BONDHOLDERSThe bondholder(s) shall not be entitled to any of the rights and privileges of shareholders other than those available to themunder statutory provisions. The bonds shall not confer upon the holders the right to receive notice or to attend and voteat the General Meetings of IDBI. The bonds shall be subject to other usual terms and conditions incorporated in theCertificate(s) of Holding that will be issued to the allottees of such bonds by IDBI, this memorandum and the IDBI BondRegulations.

TRUSTEE TO THE BONDHOLDERS

IDBI Trusteeship Services Ltd. is proposed to be appointed as trustee for the bondholders. IDBI and the Trustees will enterinto a Trustee Agreement, specifying inter alia, the powers, authorities and obligations of the Trustees and IDBI. Thebondholders shall, without further act or deed, be deemed to have irrevocably given their consent to the Trustees or anyof their agents or authorised officials to do all such acts, deeds, matters and things in respect of or relating to the Bondsas the Trustees may in their absolute discretion deem necessary or require to be done in the interest of the bondholders.

AMENDMENT OF THE TERMS OF BONDSIDBI may amend the terms of the Bond(s) at any time by a resolution passed at a meeting of the bondholders with the consentof the bondholders holding in the aggregate more than 50% in nominal value of the Bonds outstanding out of those presentand voting.

TRANSFERABILITY OF BONDSThe transfer can be effected through NSDL or CDSL, as the case may be.

LOSS OF INTEREST WARRANT(S)Loss of Interest warrant(s) should be intimated to IDBI along with the request for issue of a duplicate certificate(s) of holding/Interest warrant(s).

ISSUE OF DUPLICATE INTEREST WARRANT(S)If any, Interest Warrant(s) is lost, stolen or destroyed, then upon production of proof thereof, to the satisfaction of IDBIand upon furnishing such indemnity, as IDBI may deem adequate and upon payment of any expenses incurred by IDBI inconnection thereof, new interest warrants shall be issued. A fee will be charged by IDBI, not exceeding such sum as maybe prescribed by law on each duplicate interest warrant(s) issued in accordance with this provision. If any interest warrant(s)is/are mutilated or defaced, then, upon surrender of such interest warrant(s), IDBI shall cancel the same and issue a duplicateinterest warrant(s) in lieu thereof. The procedure for issue of the duplicate shall be governed by the provisions of the BondRegulations.

RECORD DATEThe Record Date for all interest payments and for the repayment of the face value amount upon redemption of the Bondswill be one month prior to the due date of payment of interest or repayment of face value. The interest accruing upto January15 every year will be paid on January 16 every year. Therefore, December 16 of the previous year shall always be consideredas Record Date for the purpose of such payment of interest. Interest will be paid as mentioned under the head ‘InterestPayment Dates’ under key terms of each bond.

REDEMPTION OF BONDThe investors should furnish a receipt in the prescribed form (Form XIV) of the Bond Regulations for the principal amountfor obtaining the repayment/redemption. The bondholders should get his/her name registered with IDBI.

The record date in such instances will be one month prior to the date of redemption.

In case, the date of payment of redemption proceeds falls on Saturday/ Sunday/ Public Holiday, the same will be paid onthe immediately succeeding business day with interest at the coupon rate for the intervening period.

14

BUY-BACK

IDBI may buyback the OMNI Bonds issued by it before maturity. Also, IDBI reserves the right to prematurely redeem theBonds at its sole discretion at the express request of the bondholder in exceptional cases, subject to regulatory provisions.

LISTINGIDBI has requested The Stock Exchange, Mumbai (BSE) for listing the Bonds. Final application for listing the bonds on theBSE will be made after allotment.

NOMINATIONThe sole Bondholder or all the holders jointly (or the surviving holder or holders) not being person(s) holding the Bondas holder of an office, or acting for a trust, or acting in any other capacity for any other person with a beneficialinterest in the Bond, may nominate one or more persons not exceeding four, including a minor, who shall in theevent of death of the sole holder or all the joint-holders, be entitled to the amount payable by IDBI in respect ofthe bond. The nomination made at the time of Application may be substituted or cancelled at a later date by arequest in writing to IDBI or Registrars to the Issue, signed by all the bondholders. A nomination shall standrescinded upon the transfer of the Bond by the person nominating. A transferee will be entitled to make a freshnomination for which request in writing should be made to IDBI or the Registrars to the Issue. When the Bond isheld by two or more persons, the nominee shall become entitled to receive the amount only on the demise of allthe holders. Nominations so made by investors will be subject to the Industrial Development Bank of India Bondsand Deposits (Nomination) Regulations, 1997. The share of each nominee may also be specified.

SUCCESSIONOn the death of the sole holder or in the case of a Bond held in joint names, IDBI will recognise the title of such person(s)in accordance with the provisions of the Bond Regulations.

WHO CAN APPLYThe eligible applicants include individuals, HUFs, Corporations, Banks (including Co-operative Banks and Regional Rural

Banks), Companies, Trusts, Mutual Funds, Provident/Super Annuation/Gratuity/Pension Funds/Societies/Associationsof Persons, FIs, Inusrance/Investment Companies. Non-Resident Indians may also subscribe to Omni Bonds but only onNON-REPATRIABLE basis. Such bonds cannot be endorsed to another Non-Resident Indian in the secondary market.

HOW TO APPLYInvestors are advised to comply with the following General Instructions:

1. Instructions for filling in Application Forms

a) Application for the Bonds must be in the prescribed form and completed in BLOCK LETTERS in English as per theinstructions contained therein.

b) Thumb impressions and signatures other than in English, Hindi or any of the other languages specified in the EighthSchedule of the Constitution of India must be attested by a Magistrate or a Notary Public or a Special ExecutiveMagistrate under his/her official seal.

c) Application Form Number (including the prefix) should be mentioned on the reverse of the cheque/draft.

d) A separate cheque/draft must accompany each application form.

2. Applications under Power of Attorney or by Authorised Representatives

A certified copy of the Power of Attorney and/or the relevant authority, as the case may be, alongwith the names andspecimen signatures of all the authorised signatories and the tax exemption certificate/document, if any, must be lodgedalongwith the submission of the completed application form. Future modifications/additions in the Power of Attorney orAuthority should also be notified with the Registrar of Issue.

3. PAN/GIR Number

All the applicants should mention their Permanent Account Number (PAN) allotted under the IT Act or where the same hasnot been allotted, the GIR No. and the Income Tax Circle/Ward/District. In case neither the PAN nor the GIR No. has beenallotted, or the Applicant is not assessed to income tax, the appropriate information should be mentioned in the spaceprovided. Application Forms without this information will be considered incomplete and are liable to be rejected.

15

Commissioner of Income Tax has advised that the Finance Act, 2001 has made it mandatory for the deductors (IDBI) toquote the correct PAN of deductees (investors) on TDS certificates (on Form 16 & Form 16A) and TDS Returns. Investorswhose interest income from the bonds will attract provisions of tax deduction at source (TDS) are advised to furnish thePAN in the appropriate Box in the Application Form.

4. Joint Applications in the case of Individuals

Applications may be made in single or joint names (not more than three). In the case of joint applications, all payments willbe made out in favour of the first applicant. All communications will be addressed to the applicant whose name appears firstat the address stated in the Application Form.

5. Bank Account Details

The applicant must fill in the relevant column in the application form giving particulars of their Bank Account number andname of the bank with whom such account is held, to enable the Registrars to the Issue to print the said details in theredemption / interest warrant. This is in the interest of the applicant for avoiding misuse of the redemption / interest warrant.Furnishing this information is mandatory and applications not containing such details are liable to be rejected.

TERMS OF PAYMENTThe full amount of issue price of the Bonds applied for should be paid along with the application.

PAYMENT INSTRUCTIONS(a) Payment may be made by way of cheque/drafts only. Cheques/drafts may be drawn on any bank, including a Co-operative

Bank which is situated at and is a member or sub-member of the Bankers’ Clearing House located at the IDBI Branch Officewhere the Application Form is submitted. Outstation cheques/bank drafts or cheques/bank drafts drawn on a bank notparticipating in the clearing process will not be accepted. Money orders/Postal orders/Cash/Stock Invest will also not beaccepted.

(b) All cheques/drafts must be made payable to “INDUSTRIAL DEVELOPMENT BANK OF INDIA” and crossed “A/C PAYEEONLY”.

SUBMISSION OF COMPLETED APPLICATION FORMSApplications, duly completed and accompanied by cheque/demand draft must be lodged, while the issue under privateplacement of the bond is open, with the IDBI Offices as mentioned in the last page of the Memorandum.

AcknowledgementsNo separate receipts will be issued for the application money. However, the IDBI Offices receiving the duly completedApplication Form will acknowledge receipt of the application by stamping and returning to the applicant theAcknowledgement slip at the bottom of each Application Form.

REGISTRARSInvestor Services of India Ltd. has been appointed as Registrars to the Issue. The Registrar will monitor the applicationswhile the private placement is open and will coordinate the post private placement activities of allotment, dispatching interestwarrants etc. any query/complaint regarding application/ allotment/ transfer should be forwarded to ISIL at their address givenbelow. All requests for registration of transfer along with appropriate documents should also be sent to the registrars.

Investor Services of India Ltd.IDBI Building, Plot No.39-41Sector 11, CBD Belapur, Navi Mumbai - 400 614Tel. : (022) 27579636 Fax : (022) 27579650

Investor Relations and Grievance RedressalArrangements have been made to redress investor grievances expeditiously. All grievances related to the Issue, quoting theApplication Number (including prefix), number of Bonds applied for, amount paid on application and the IDBI Office wherethe Application was submitted, may be addressed to the Registrars at the address given above.

16

Compliance OfficerShri R.K. Bansal, General Manager

Domestic Resources Department,

22nd Floor, IDBI Tower, WTC Complex,Cuffe Parade, Mumbai - 400 005

Tel: (022) 2216 1746

Fax: (022) 2218 1155, 2218 8137E-Mail: [email protected]

Applicants may also get in touch with the Domestic Resources Department of IDBI for assistance, at the following address:

Deputy General ManagerDomestic Resources DepartmentIndustrial Development Bank of India22nd Floor, IDBI Tower, WTC Complex, Cuffe Parade, Mumbai - 400005Tel : (022) 22161763/22152882, Fax : (022) 22181155/22188137

17

PART II

INDUSTRIAL DEVELOPMENT BANK OF INDIA

Constitution and MilestonesIndustrial Development Bank of India (IDBI) was established in 1964 by the Government of India under an Act ofParliament, the Industrial Development Bank of India Act, 1964 (the IDBI Act). The functions and working of IDBI aregoverned by the IDBI Act. Initially, IDBI was set up as a wholly-owned subsidiary of Reserve Bank of India (RBI) toprovide credit and other facilities for the development of industry. In 1976, the ownership of IDBI was transferred tothe Government of India and it was entrusted with the additional responsibility of acting as the principal financialinstitution for co-ordinating the activities of institutions engaged in the financing, promotion or development of industry.

In 1982, IDBI’s portfolio relating to its International Finance Division (which was providing export finance to industry),was transferred to Export-Import Bank of India (EXIM Bank), which was established as a wholly owned corporationof the Government of India under the Export-Import Bank of India Act, 1982.

In 1990, IDBI’s portfolio relating to the small scale industrial sector was transferred to the Small IndustriesDevelopment Bank of India (SIDBI) which was established as a wholly-owned subsidiary of IDBI under the SmallIndustries Development Bank of India Act, 1989 (SIDBI Act, 1989).

RBI vide its circular No.C-24/01-02-00/2000-2001 dated 28-April-2001 has mentioned that DFI’s can eitherconvert themselves into a commercial bank or a Non Banking Finance Company (NBFC). The Board of Directorsof IDBI has decided ‘in-principle’ to convert IDBI into a Commercial Bank.

The Hon’ble Finance Minister while presenting the Union Budget for the year 2002-03 to the Parliament announced theproposal to make legislative changes to corporatise IDBI to provide greater flexibility.

Accordingly, the Govt. of India had introduced ‘The Industrial Development Bank (Transfer of Undertaking andRepeal) Bill, 2002’, wherein, inter-alia, repeal of IDBI Act, 1964 and corporatisation of IDBI was proposed, inthe Winter Session of Parliament. The said Bill was referred to the Standing Committee on Finance. Thecommittee’s report was placed in the Parliament in its Monsoon Session and again in the Winter Session.

The Bill proposing the repeal of IDBI Act, 1964 has been approved by both the Houses of Parliament viz. Lok Sabha(Lower House) and Rajya Sabha (Upper House) on December 8 and December 15, 2003 respectively. The Billenvisages transfer of all assets and liabilities to a company to be named as “Industrial Development Bank of India Ltd.”.All the existing shareholders of IDBI will become shareholders of the new company. The Bill facilitates the newcompany to become a banking company, without the need to obtain a separate banking license under BankingRegulation Act, 1949 and thus enable it to access funds at cheaper cost. It envisages, inter alia, the conversion ofIDBI into a Commercial Bank while continuing to be a Development Bank which will provide term lending to industry- large, medium and small. The Bank will be given certain regulatory forbearance which include reserve requirementsand tax benefits. All the assets and liabilities of IDBI shall, with effect from a date to be notified (appointed date) vestin the new company and be discharged by it. The IDBI Act, 1964 will stand repealed. Any guarantee given for or infavour of IDBI with respect to any loan, finance or other assistance shall continue to be operative in relation to thecompany. The Bill has also received the assent of the President of India. The Bill would require a notification in theOfficial Gazette and further notification of the appointed date after the fulfilment of the formalities connected withincorporation of a new company under the Companies Act, 1956.

FunctionsOver the last thirty eight years, IDBI’s role as a catalyst to industrial development has encompassed broad spectrumof activities. IDBI can finance all types of industrial concerns covered under the provisions of the IDBI Act, irrespectiveof the size or form of organisation. IDBI primarily provides finance to large and medium industrial enterprises and isauthorised to finance all types of industrial concerns engaged or to be engaged in the manufacture, processing orpreservation of goods, mining, shipping, transport, hotel industry, information technology, medical and health services,leasing, generation or distribution of power, maintenance, repair, testing or servicing of vehicles, vessels and othertypes of machinery and the setting up and development of industrial estates. IDBI may also assist industrial concernsengaged in the research and development of any process or product or in the provision of special technical knowledgeor other services for the promotion of industrial growth. In addition, floriculture, road construction and the establishmentand development of tourism related facilities including amusement parks, cultural centres, restaurants, travel andtransport facilities and other tourist services, film industry and construction activity have been recognised as industrialactivities eligible for finance from IDBI.

IDBI has been assigned a special role for co-ordinating the activities of institutions engaged in financing, promoting

18

or developing industries as also provision of technical, legal and marketing assistance to industry and undertakingmarket surveys, investment research as well as techno-economic studies in connection with the development ofindustry.

OfficesIDBI has its Head Office at Mumbai and has an all India presence through its branch network. It operates through anetwork of 5 Zonal offices, one each in Chennai, Guwahati, Kolkata, Mumbai and New Delhi. Besides, IDBI has 36branch offices located in state capitals and major commercial centres in India.

Government HoldingThe IDBI Act was amended in October 1994 which, inter alia, permitted IDBI to raise equity from the public subjectto the holding of the Government not falling below 51% of the issued capital. Pursuant to the amendment, in July 1995,IDBI made its initial public offering of equity shares aggregating Rs. 2184 crore. Simultaneously, the Government alsooffered for sale a part of its holding of equity shares in the capital of IDBI aggregating Rs.187.5 crore (includingpremium of Rs.120 per share) to the Indian public. On completion of the allotment of the shares offered to the public,the Government’s shareholding in IDBI reduced to 72.14%. The Government’s share holding has further come downto 57.76% with effect from June 5, 2000 as the Government of India converted 24.7 crore equity shares (out of itsholding of 48.6 crore equity shares) into 24.70 crore fully paid preference shares of Rs. 10 each (equivalent to Rs.247crore) redeemable within 3 years and carrying dividend @ 13% p.a. The preference shares have since beenredeemed. On August 25, 2000, 18,074,300 partly paid up equity shares of face value Rs. 10/- each were forfeitedand aggregate face value of Rs. 180,743,000 has been reduced from the subscribed and paid-up equity capital. Onaccount of this, Government’s shareholding has gone up to 58.5% with effect from August 25, 2000.

IDBI made its bonus issue in March 2001 in the ratio of 3 bonus shares for every 5 held. Accordingly, GOI has beenallotted 1,431,48,000 bonus shares. The shareholding of GOI remains at 58.5 % only.

Regulation and Supervision

IDBI, being a statutory organization is governed by the Industrial Development Bank of India Act, 1964 (IDBI Act). Thefunctions and business of IDBI are regulated by the IDBI Act. In addition, IDBI being a financial institution is subjectto regulatory supervision by RBI. Section 45L of the Reserve Bank of India Act, 1934 empowers RBI, inter alia, to callfor certain information relating to the business of IDBI and give directions relating to the conduct of its business. RBIhad set up a Board for Financial Supervision (BFS) in 1995 under the chairmanship of the Governor of Reserve Bankof India. Under the guidance of the Board for Financial Supervision, the department of Financial Supervision of the RBIsupervises Financial Institutions and Commercial Banks. The Department of Financial Supervision also undertakesoff-site and on-site supervision over banks and financial institutions. As part of such surveillance, the Reserve Bankof India carries out periodical inspection of IDBI. As clarified by RBI the contents of the inspection report is strictlyconfidential. It may be mentioned that IDBI has replied all the points referred to by the RBI in its latest inspection report.

The Reserve Bank of India has been issuing detailed guidelines to Financial Institutions on Asset Classification,Income Recognition and Provisioning, Capital Adequacy, Asset Liability Management etc. from time to time. IDBIadheres to all such guidelines and submits necessary information to RBI as per the guidelines.

MANAGEMENT AND ORGANISATION

CORPORATE GOVERNANCE

Corporate governance is administered in IDBI through the Board and three major committees of the Board, i.e. theExecutive Committee, Audit Committee and Shareholders/ Investors Grievances Committee. However the primaryresponsibility of upholding high standards of corporate governance in its operations and providing necessarydisclosures within the framework of legal provisions and banking conventions with commitment to enhance theshareholders’ value, lies with the Board of IDBI.

IDBI has complied with SEBI guidelines in respect of Corporate Governance specially with respect to broad basingof Board, Constituting the Committees such as Shareholders/ Investors Grievances Committee and Audit Committeeetc.

The Board

The general superintendence, direction and management of the affairs and business of IDBI is vested in the Boardof Directors which exercises all powers and does all acts and things which may be done by IDBI under the IDBI Act.The Board may direct that any power exercisable by it may also be exercised by the Chairman, Managing Directoror Wholetime Director.

19

As per the IDBI Act, 1964 the Board can have maximum 12 directors, consisting of a Chairman and a ManagingDirector appointed by the Government of India (both functions can be assumed by the same person), a wholetimeDirector appointed by the Government on the recommendations of the Board, two Government nominees, threedirectors having special knowledge/ professional experience in diverse fields nominated by the Central Governmentand four directors elected by the shareholders other than the Government of India.

Shri M. Damodaran, Chairman, UTI, has assumed concurrent charge of the post of Chairman & Managing Directorof IDBI in addition to his own duties w.e.f. October 1, 2003 in terms of Notification F.No. 24(4)/2003-IF-I datedSeptember 29, 2003 issued by Government of India. Presently the Board comprises of 10 directors includingGovernment nominees and independent professionals. The primary responsibilities of the Board include:

1. Maintaining high standards of corporate governance and compliance with various laws and regulations.

2. Shaping the policies and procedures of the Bank.

3. Monitoring performance of the organization and evolving the growth strategy.

4. Setting up various prudential risk management limits.

5. Overseeing financial management of the Bank and approve various products and their policies.

The Executive Committee

The Executive Committee, presently comprising of 6 directors including the CMD of IDBI as the committee Chairman,deals with sanctions of assistance and other operational matters. All project proposals for sanction of assistanceabove the threshold limits applicable to Credit Committee are dealt with by the Executive Committee. The EC alsodecides on matters relating to Business Plans, Resource Mobilization, Investments, Capital Expenditure, RiskManagement Systems, assessment of performance against goals, initiating corrective measures etc.

Audit Committee

Audit Committee presently comprises of 5 directors including one independent professional director qualified asChartered and Cost Accountant as chairman of the committee. Executive Directors are invited as and whenconsidered necessary. The Audit Committee acts as an interface between the management and the statutoryand internal auditors overseeing the internal audit functions. The functions of the Audit Committee are asfollows:

1. To provide direction and oversee audit functions of the Bank.

2. To review periodically financial statements before submission to the Board focussing primarily on:

- Any changes in accounting policies and practices.

- Major accounting entries on exercise of judgement by management.

- Qualification in draft audit report.

- Significant adjustments arising out of credit.

- The going concern assumption

- Compliance of accounting standards.

- Compliance with stock exchange and legal requirements concerning financial statements.

- Any related party transactions i.e. transactions of the bank of material nature, with promoters or themanagement, their subsidiaries or associates etc. that may have potential conflict with the interestsof the bank at large.

3. Review with management, external and internal auditors, adequacy of internal control system.

4. Discussions with internal auditors and in house Audit Committee.

5. Review action taken on inspection reports of RBI and Statutory Auditors Report.

6. Review action taken on major findings of internal audit reports having bearing on policy, business risk, controland corporate governance.

7. To review cases of fraud and action taken.

8. Such other matters as may be delegated by the Board.

20

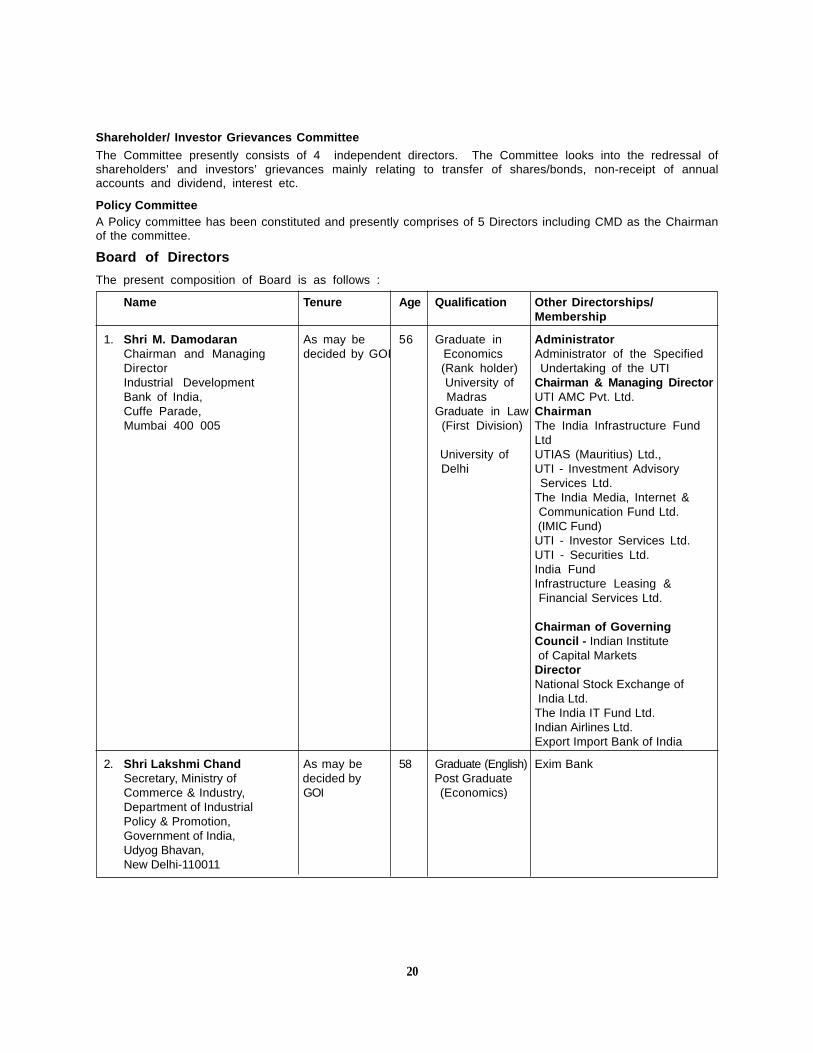

Shareholder/ Investor Grievances Committee

The Committee presently consists of 4 independent directors. The Committee looks into the redressal ofshareholders’ and investors’ grievances mainly relating to transfer of shares/bonds, non-receipt of annualaccounts and dividend, interest etc.

Policy CommitteeA Policy committee has been constituted and presently comprises of 5 Directors including CMD as the Chairmanof the committee.

Board of Directors

The present composition of Board is as follows :

Name Tenure Age Qualification Other Directorships/Membership

1. Shri M. Damodaran As may be 56 Graduate in AdministratorChairman and Managing decided by GOI Economics Administrator of the SpecifiedDirector (Rank holder) Undertaking of the UTIIndustrial Development University of Chairman & Managing DirectorBank of India, Madras UTI AMC Pvt. Ltd.Cuffe Parade, Graduate in Law ChairmanMumbai 400 005 (First Division) The India Infrastructure Fund

Ltd University of UTIAS (Mauritius) Ltd., Delhi UTI - Investment Advisory

Services Ltd.The India Media, Internet & Communication Fund Ltd. (IMIC Fund)UTI - Investor Services Ltd.UTI - Securities Ltd.India FundInfrastructure Leasing & Financial Services Ltd.

Chairman of GoverningCouncil - Indian Institute of Capital MarketsDirectorNational Stock Exchange of India Ltd.The India IT Fund Ltd.Indian Airlines Ltd.Export Import Bank of India

2. Shri Lakshmi Chand As may be 58 Graduate (English) Exim BankSecretary, Ministry of decided by Post GraduateCommerce & Industry, GOI (Economics)Department of IndustrialPolicy & Promotion,Government of India,Udyog Bhavan,New Delhi-110011

21

Name Tenure Age Qualification Other Directorships/ Memberships

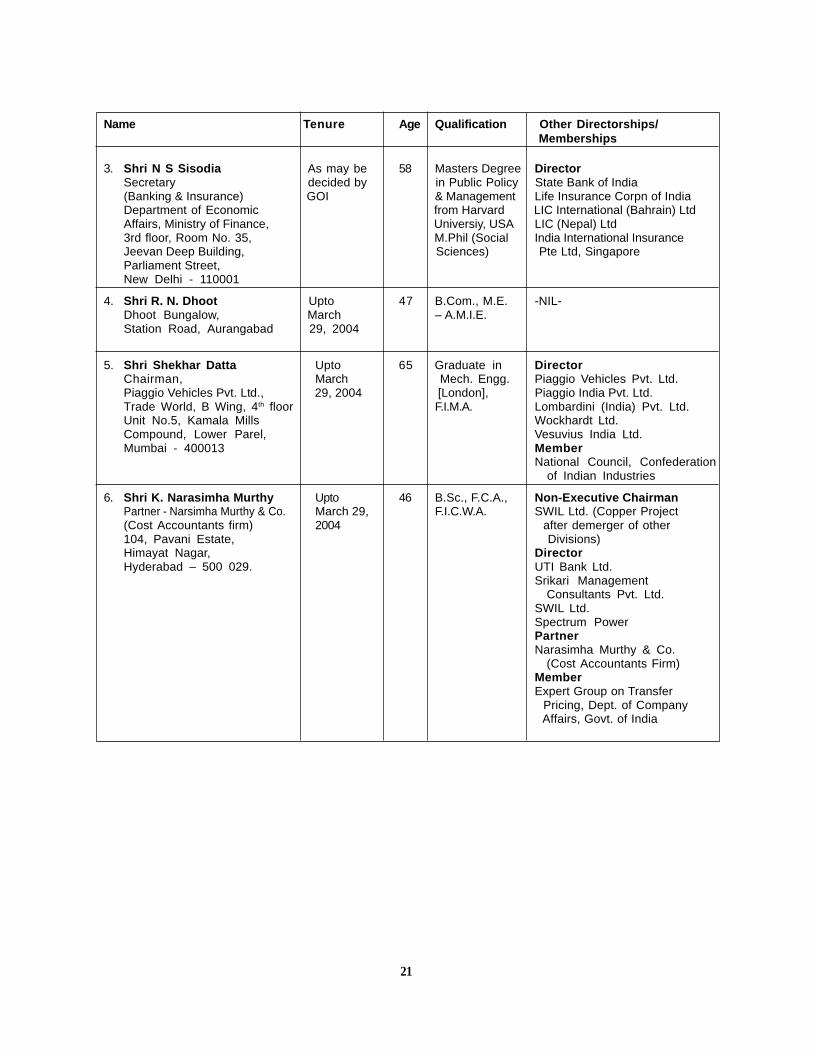

3. Shri N S Sisodia As may be 58 Masters Degree DirectorSecretary decided by in Public Policy State Bank of India(Banking & Insurance) GOI & Management Life Insurance Corpn of IndiaDepartment of Economic from Harvard LIC International (Bahrain) LtdAffairs, Ministry of Finance, Universiy, USA LIC (Nepal) Ltd3rd floor, Room No. 35, M.Phil (Social India International InsuranceJeevan Deep Building, Sciences) Pte Ltd, SingaporeParliament Street,New Delhi - 110001

4. Shri R. N. Dhoot Upto 47 B.Com., M.E. -NIL-Dhoot Bungalow, March – A.M.I.E.Station Road, Aurangabad 29, 2004

5. Shri Shekhar Datta Upto 65 Graduate in DirectorChairman, March Mech. Engg. Piaggio Vehicles Pvt. Ltd.Piaggio Vehicles Pvt. Ltd., 29, 2004 [London], Piaggio India Pvt. Ltd.Trade World, B Wing, 4th floor F.I.M.A. Lombardini (India) Pvt. Ltd.Unit No.5, Kamala Mills Wockhardt Ltd.Compound, Lower Parel, Vesuvius India Ltd.Mumbai - 400013 Member

National Council, Confederation of Indian Industries

6. Shri K. Narasimha Murthy Upto 46 B.Sc., F.C.A., Non-Executive ChairmanPartner - Narsimha Murthy & Co. March 29, F.I.C.W.A. SWIL Ltd. (Copper Project(Cost Accountants firm) 2004 after demerger of other104, Pavani Estate, Divisions)Himayat Nagar, DirectorHyderabad – 500 029. UTI Bank Ltd.

Srikari ManagementConsultants Pvt. Ltd.

SWIL Ltd.Spectrum PowerPartnerNarasimha Murthy & Co.

(Cost Accountants Firm)MemberExpert Group on Transfer Pricing, Dept. of Company Affairs, Govt. of India

22

Name Tenure Age Qualification Other Directorship/Memberhip

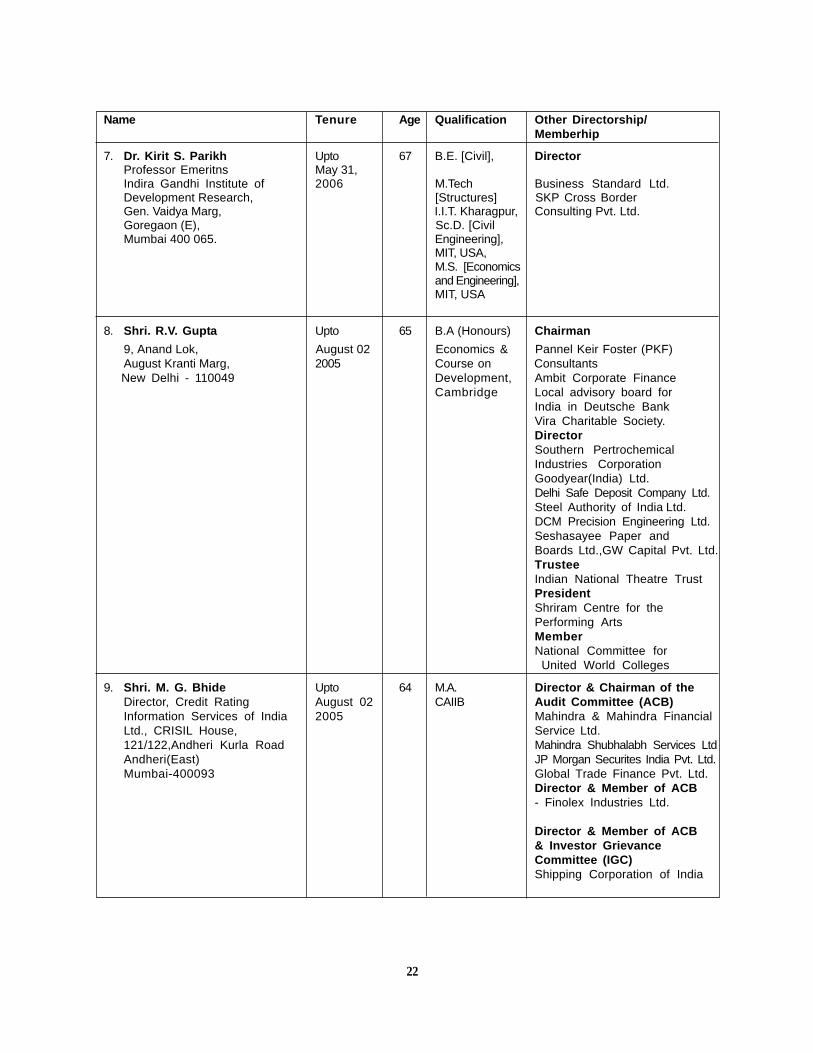

7. Dr. Kirit S. Parikh Upto 67 B.E. [Civil], DirectorProfessor Emeritns May 31,Indira Gandhi Institute of 2006 M.Tech Business Standard Ltd.Development Research, [Structures] SKP Cross BorderGen. Vaidya Marg, I.I.T. Kharagpur, Consulting Pvt. Ltd.Goregaon (E), Sc.D. [CivilMumbai 400 065. Engineering],

MIT, USA,M.S. [Economicsand Engineering],MIT, USA

8. Shri. R.V. Gupta Upto 65 B.A (Honours) Chairman

9, Anand Lok, August 02 Economics & Pannel Keir Foster (PKF)August Kranti Marg, 2005 Course on Consultants

New Delhi - 110049 Development, Ambit Corporate FinanceCambridge Local advisory board for

India in Deutsche BankVira Charitable Society.DirectorSouthern PertrochemicalIndustries CorporationGoodyear(India) Ltd.Delhi Safe Deposit Company Ltd.Steel Authority of India Ltd.DCM Precision Engineering Ltd.Seshasayee Paper andBoards Ltd.,GW Capital Pvt. Ltd.TrusteeIndian National Theatre TrustPresidentShriram Centre for thePerforming ArtsMemberNational Committee for United World Colleges

9. Shri. M. G. Bhide Upto 64 M.A. Director & Chairman of theDirector, Credit Rating August 02 CAIIB Audit Committee (ACB)Information Services of India 2005 Mahindra & Mahindra FinancialLtd., CRISIL House, Service Ltd.121/122,Andheri Kurla Road Mahindra Shubhalabh Services LtdAndheri(East) JP Morgan Securites India Pvt. Ltd.Mumbai-400093 Global Trade Finance Pvt. Ltd.

Director & Member of ACB- Finolex Industries Ltd.

Director & Member of ACB& Investor GrievanceCommittee (IGC)Shipping Corporation of India

23

Name Tenure Age Qualification Other Directorship/Memberhip

Inv. Com. & Executive Com.- The Credit Rating Information Services of India Ltd. (CRISIL)

DirectorDeposit Insurance andCredit Guarantee Corporation of India,IMO Communication Pvt. Ltd.Indian Oiltanking Ltd.

Asset Reconstructions Company (India) Ltd.AdviserBoard of Advisors of the Specified Undertaking of the Unit Trust of India (Transfer of Undertaking and Repeal Act, 2002)

10. Shri Hiralal Zutshi Upto 61 B.E. (Hons) ChairmanD-25, Defence Colony, August 22, Mechanical Petroleum, Coal and RelatedNew Delhi - 110 024 2006 Products, Division Council

DirectorRain Calcining Ltd.MemberMOU setting Committee of adhoctask Force for 2003-04,Department of Public Enterprise, Govt. Of India.

The holding of equity shares of IDBI by the above Directors is Nil.

24

MANAGEMENT

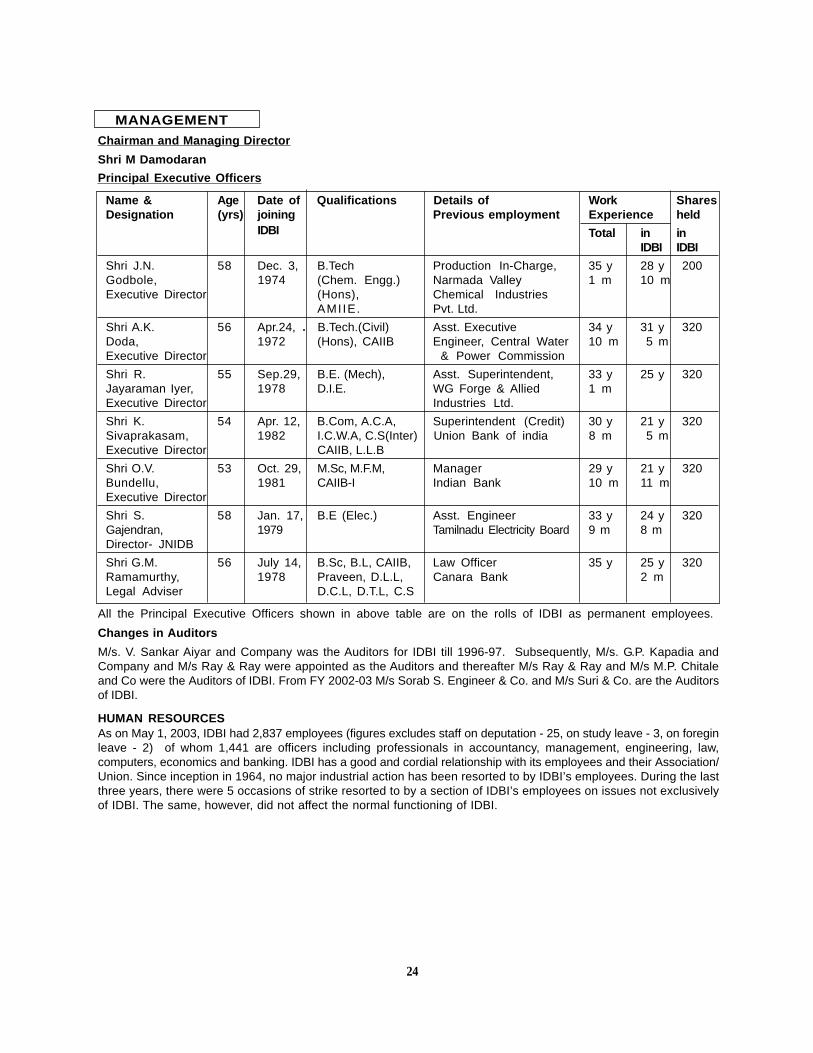

Chairman and Managing Director

Shri M Damodaran

Principal Executive Officers

Name & Age Date of Qualifications Details of Work SharesDesignation (yrs) joining Previous employment Experience held

IDBI Total in inIDBI IDBI

Shri J.N. 58 Dec. 3, B.Tech Production In-Charge, 35 y 28 y 200Godbole, 1974 (Chem. Engg.) Narmada Valley 1 m 10 mExecutive Director (Hons), Chemical Industries

AMI IE. Pvt. Ltd.

Shri A.K. 56 Apr.24, B.Tech.(Civil) Asst. Executive 34 y 31 y 320Doda, 1972 (Hons), CAIIB Engineer, Central Water 10 m 5 mExecutive Director & Power Commission

Shri R. 55 Sep.29, B.E. (Mech), Asst. Superintendent, 33 y 25 y 320Jayaraman Iyer, 1978 D.I.E. WG Forge & Allied 1 mExecutive Director Industries Ltd.

Shri K. 54 Apr. 12, B.Com, A.C.A, Superintendent (Credit) 30 y 21 y 320Sivaprakasam, 1982 I.C.W.A, C.S(Inter) Union Bank of india 8 m 5 mExecutive Director CAIIB, L.L.B

Shri O.V. 53 Oct. 29, M.Sc, M.F.M, Manager 29 y 21 y 320Bundellu, 1981 CAIIB-I Indian Bank 10 m 11 mExecutive Director

Shri S. 58 Jan. 17, B.E (Elec.) Asst. Engineer 33 y 24 y 320Gajendran, 1979 Tamilnadu Electricity Board 9 m 8 mDirector- JNIDB

Shri G.M. 56 July 14, B.Sc, B.L, CAIIB, Law Officer 35 y 25 y 320Ramamurthy, 1978 Praveen, D.L.L, Canara Bank 2 mLegal Adviser D.C.L, D.T.L, C.S

All the Principal Executive Officers shown in above table are on the rolls of IDBI as permanent employees.

Changes in Auditors

M/s. V. Sankar Aiyar and Company was the Auditors for IDBI till 1996-97. Subsequently, M/s. G.P. Kapadia andCompany and M/s Ray & Ray were appointed as the Auditors and thereafter M/s Ray & Ray and M/s M.P. Chitaleand Co were the Auditors of IDBI. From FY 2002-03 M/s Sorab S. Engineer & Co. and M/s Suri & Co. are the Auditorsof IDBI.

HUMAN RESOURCESAs on May 1, 2003, IDBI had 2,837 employees (figures excludes staff on deputation - 25, on study leave - 3, on foreginleave - 2) of whom 1,441 are officers including professionals in accountancy, management, engineering, law,computers, economics and banking. IDBI has a good and cordial relationship with its employees and their Association/Union. Since inception in 1964, no major industrial action has been resorted to by IDBI’s employees. During the lastthree years, there were 5 occasions of strike resorted to by a section of IDBI’s employees on issues not exclusivelyof IDBI. The same, however, did not affect the normal functioning of IDBI.

25

PRODUCTS AND SERVICES

IDBI provides project related finance for the establishment of new industrial projects as well as for expansion,diversification and modernisation of existing industrial enterprises. In view of the changed financial needs of theindustries, IDBI has also designed other products to meet the short term funding, core working capital and treasuryrequirements of the industrial clients. IDBI also extends non-fund based assistance, advisory services, forex servicesetc,. IDBI has also set up specialised subsidiaries and associates to extend mutual fund products, capital marketservices, banking services as also Registrar and transfer agent services.

IDBI currently offers the following major products and services to industrial concerns:

1. DIRECT FINANCE

The expression “direct finance” refers to the provision of finance directly to an industrial unit without the involvementof an intermediary financial institution. During FY 2002-03, approximately 91% of total sanctions and 94% of totaldisbursements of IDBI were accounted for by direct finance.

(a) Project Finance

Project Finance involves providing credit and other facilities to medium and large scale units for theestablishment of new projects as well as for expansion, diversification or modernisation of existingindustrial units. Project finance is granted directly to units established as companies in private, jointand public sectors, and to co-operatives.

As part of Project Finance, IDBI provides term loans in Rupee and in Foreign currency repayable over5-10 years depending upon the debt servicing capacity of the borrowing unit, and secured by a chargeover the immovable/ movable assets. It also provides financial guarantees, usually in foreign currency,to cover deferred payments and to enable corporates to raise loans from overseas. IDBI’s guaranteesare of near sovereign nature and have been an important segment of operations in the recent years.