Embed Size (px)

Citation preview

ICT at Work

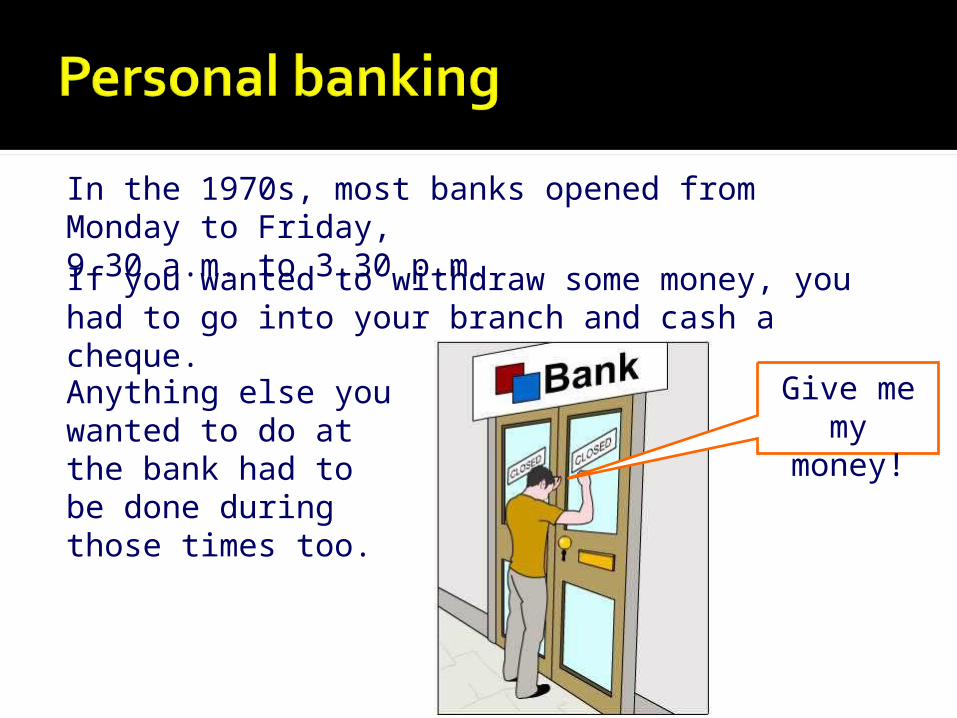

In the 1970s, most banks opened from Monday to Friday,9.30 a.m. to 3.30 p.m.

Anything else you wanted to do at the bank had to be done during those times too.

If you wanted to withdraw some money, you had to go into your branch and cash a cheque.

Give me my money!

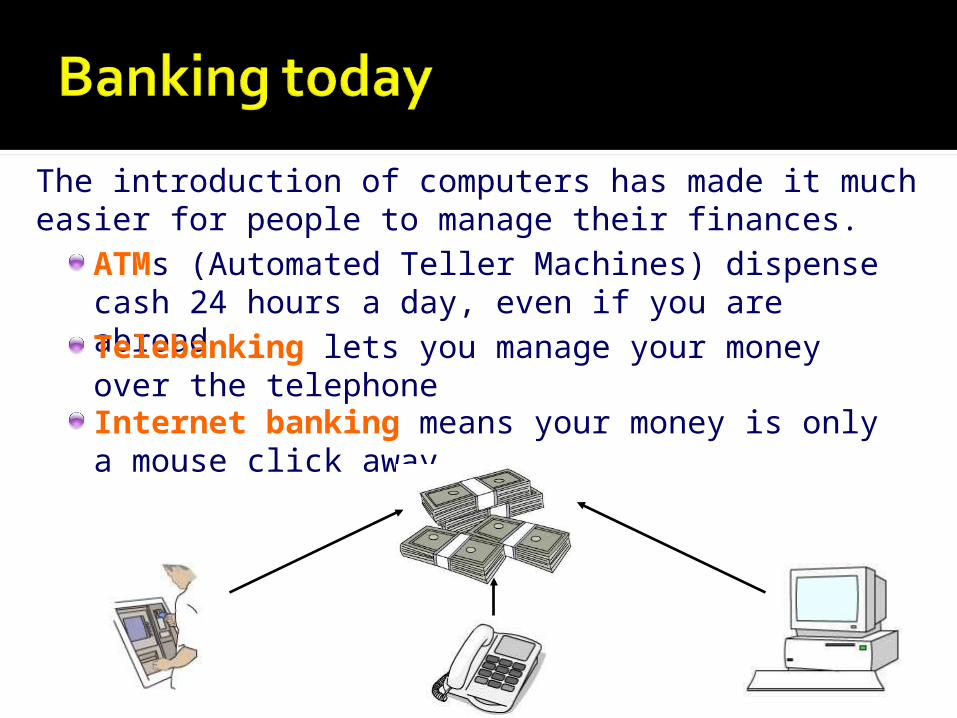

The introduction of computers has made it much easier for people to manage their finances.

ATMs (Automated Teller Machines) dispense cash 24 hours a day, even if you are abroad

Telebanking lets you manage your money over the telephoneInternet banking means your money is only a mouse click away.

Input devices

card reader

key pad

deposit slot

cash dispenser

Output devicesspeaker

display screenprinter

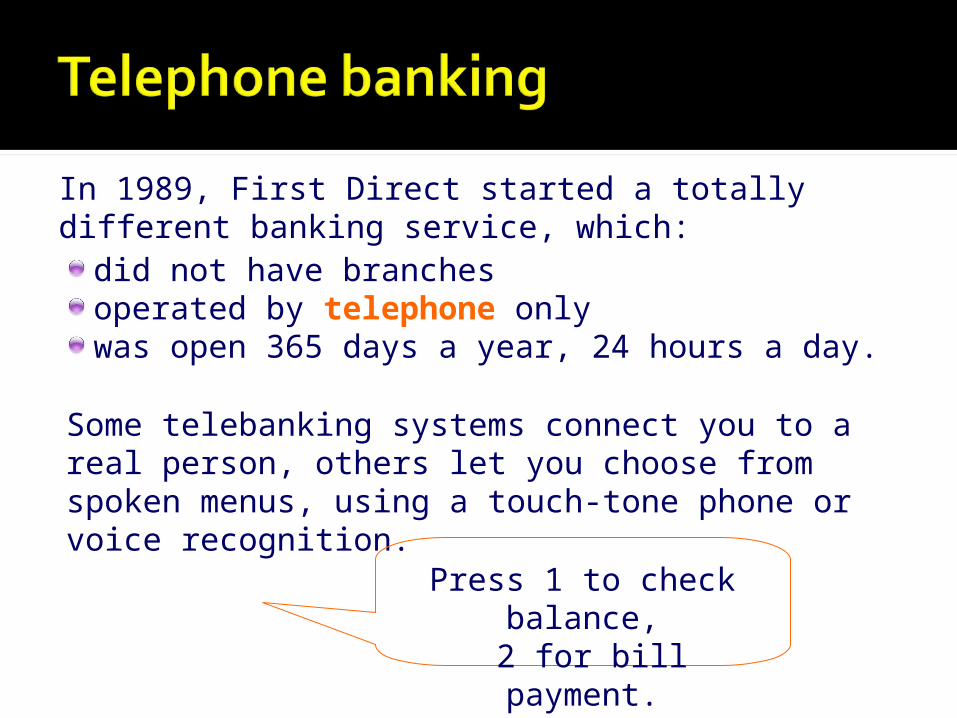

In 1989, First Direct started a totally different banking service, which:

did not have branchesoperated by telephone onlywas open 365 days a year, 24 hours a day.

Some telebanking systems connect you to a real person, others let you choose from spoken menus, using a touch-tone phone or voice recognition.

Press 1 to check balance, 2 for bill payment.

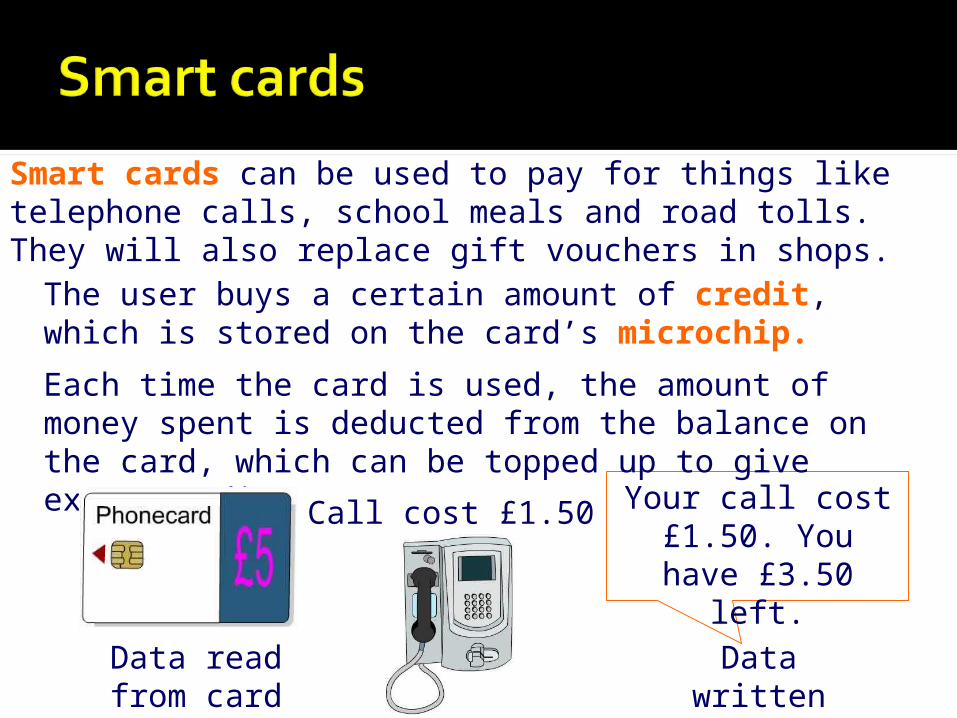

Smart cards can be used to pay for things like telephone calls, school meals and road tolls. They will also replace gift vouchers in shops.

Call cost £1.50 Your call cost £1.50. You have

£3.50 left.

Data read from card

Data written to card

Each time the card is used, the amount of money spent is deducted from the balance on the card, which can be topped up to give extra credit.

The user buys a certain amount of credit, which is stored on the card’s microchip.

Using a microchip to store data rather than a magnetic strip has some advantages:

microchips can store 100 times more datamicrochips are more secure as the technology required to read data on a chip is beyond the reach of virtually all counterfeiters.

However, the readers required by retailers to process the microchips are much more expensive than the technology required to read magnetic strips.

Another disadvantage of microchips is that if the customer loses their card, they lose the money on it, just as if it were cash.

The previous slides are all examples of Electronic Funds Transfer – dealing with financial transactions electronically instead of in cash. Other examples include:

BACS (Bankers Automated Clearing System): businesses use this to pay employees and suppliers. The money goes directly into their bank account, rather than giving them a cheque to pay in.

Direct debit: instead of paying bills every month by cash or cheque, many people set up a direct debit agreement which allows the money to be taken directly from their account.

The more people use technology to manage their money, the more concerns are raised about security and fraud.

Is it safe to use my credit card online?

Can hackers get my credit card details?

My card details must have been

stolen!

Will my goods ever

arrive?

There are security issues with EFT systems:

cards can be stolen

they can also be cloned by making an identical copy

web sites and data transmission can be hacked.

There are simple ways you can protect yourself:

keep your card safe – treat it as if it were cash

don’t write your PIN down or tell anyone what it is

don’t allow your card to be taken out of your sight

only buy from trustworthy web sites with secure servers

if your card is stolen, report it immediately. The bank will then usually cover anything charged to your card after that.

There are some simple ways to protect yourself:

1. keep your card safe – treat it as if it were cash 2. don’t write your PIN down or tell anyone what

it is 3. don’t allow your card to be taken out of your

sight 4. only buy from trustworthy web sites with

secure servers 5. if your card is stolen, report it immediately.

The bank will then usually cover anything charged to your card after that.

Security measures taken by banks to protect their customers include:

using PINs and passwords to allow access to ATMs, telebanking and Internet banking using encryption to protect data when it is being transmitted monitoring spending patterns so that they make checks if a customer suddenly spends more than usual, in case a card has been stolen some banks use PINs instead of signatures to authorize cards. The user taps in their number on a keypad. CCTV cameras record all transactions at most ATMs.

Summary

ATMs (Automatic Teller Machines) allow access to money at any time of day and night.

Telebanking allows banking transactions to take place over the phone.

Internet banking has also changed banking.

Smart cards are an alternative method of payment – storing credit on a microchip.

Credit can be topped up electronically at any time.

EFT (Electronic Funds Transfer) is when financial transactions occur electronically rather than with cash.

BACS (Bankers Automated Clearing System) and Direct Debit allow money to be credited/debited directly to/from a bank account.