Embed Size (px)

DESCRIPTION

Citation preview

Turning high risk into high potentialGrant Thornton International Mining Report 2013

Contents

02 The search for cash continues

07 Government and public pressures increase

14 Miners remain optimistic despite challenges

17 Minimise risk, maximise opportunity

18 Methodology and participants

19 Industry knowledge, local expertise

20 Global contacts

It is a challenging time for the sector, especially junior miners. But growth can return; the risk-return equation will change once investors develop a renewed enthusiasm for potential high returns that few other opportunities offer.”

Mark Zastre Global industry leader mining Grant Thornton LLP, Canada

“

1

Challenges abound for the mining sector

Mining executives face numerous challenges around the globe:

• sluggish economies keep risk-averse investors on the sidelines

• many junior miners seek alternatives to traditional equity funding due to depressed share prices

• producing companies face rising input costs that outpace generally high commodity prices

• governments look for additional taxes from the mining sector while increasing regulatory burdens

• uncertainties about asset ownership delay projects and worry hesitant investors

• concerns about environmental impacts and business ethics harm the sector’s image among the general public and investors.

The Grant Thornton international mining survey explored mining executives’ thoughts on these trends, finding that, even amid challenges, mining executives remain optimistic about their business prospects. Perhaps part of the reason is the innate optimism of those who choose mining for a career, scouring the earth for chances at outsized returns on investment despite long odds. But it’s also because many miners (54% of those surveyed) expect commodity prices for their flagship assets to rise, which will eventually release pent-up demand for their projects.

“The mining industry has always come with its fair share of risks, particularly for miners venturing beyond their own borders,” says Mark Zastre, global industry leader mining, Grant Thornton Canada. “It is a challenging time for miners, and especially for junior miners. But growth can return; the risk-return equation will change once investors develop a renewed enthusiasm for potential high returns that few other opportunities offer. Other factors that will enable growth include the improved efficiencies that technology and automation can bring as miners evolve into the 21st century, expansion of supply globally as mining companies identify new resources around the world, and the adoption of best practices for dealing with the many socioeconomic challenges that await miners.”

This Grant Thornton International Mining Report highlights the difficulties facing mining companies today and illustrates how these issues will impact mining operations in the coming year. More importantly, this report underscores that there are opportunities for mining executives to leverage creative solutions to these challenges.

Report findings highlight ways in which mining executives can react to challenges by:

• pursuingfinancinginwaysthataddressinvestorconcerns about the sector in general (for example, viability of assets, security of title) while positioning their own organisations as sound, strategic enterprises led by professional management teams — and deserving of additional investment

• navigatingtheircompaniesthroughuncertainbusiness conditions and wavering public support that can derail projects around the globe, by developing and implementing strategies to adapt to rapidly changing local sentiment and regulatory environments

• protectingtheirorganisationsbyidentifying,understanding, managing and mitigating risks to their assets, operations and supply chains

• preparingforever-presentcostpressures(forexample, energy, labour) by implementing procedures, technologies and automation to minimise their impacts.

2

The search for cash continues

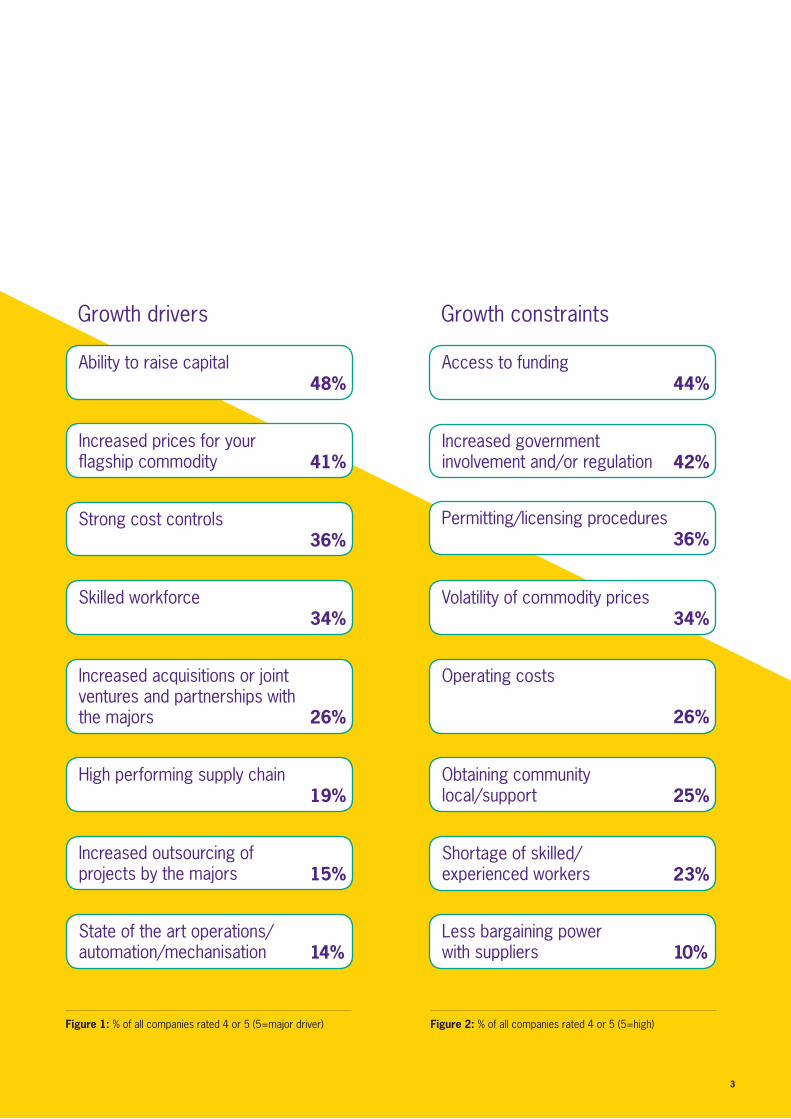

Mining companies face a complex array of factors impacting their ability to succeed — or even to remain solvent. Yet the Grant Thornton international mining survey reveals an interesting juxtaposition of industry constraints and drivers — indicating that effective and adaptive management is the key to long-term success for individual junior miners. Indeed, where some executives see barriers to their company’s ability to compete, others see trends that can be leveraged for growth (Figures 1 and 2).

Nowhere is this more apparent than with the issue of funding. Access to funding is rated by executives as the top constraint on their ability to expand/grow their business: 44% rated it 4 or 5 on a scale of 1-5 where 5 is “high” for constraining their ability to expand/grow their business. Similarly, the ability to raise capital is the top driver of growth: 48% rated it 4 or 5 on a scale of 1-5 where 5 is “major driver” of the growth/value of their business.

Among junior miners1 participating in the survey, 55% rated access to funding as a constraint. Among countries participating in the survey, the need for funding was most pronounced in Australia, where 66% of executives rated access to funding as a constraint. Similarly on the driver side of the survey, 56% of junior miners rate access to capital as a driver, and Australia had the highest percentage of executives

rating access to capital as a driver (64% of executives). “This is a big issue in the industry right now. The capital markets have effectively seized up for risk capital, and it’s very difficult for high-risk companies in the exploration stage to raise equity capital, which is the traditional source of funding for these companies,” says Zastre.

“I can see a situation at the upstream end of the market where explorers have either managed to raise cash in order to fulfill their business objectives or they have deferred or delayed their activities because of lack of funding,” says Gerry Beaney, head of capital markets, Grant Thornton UK. “At the opposite end of the mining spectrum are those companies engaged in production, which because of relatively high commodity prices and/or well-run operations, are sitting on piles of cash. Companies in between are struggling to raise money because investors are risk-averse at the moment and they’re faced with limited options.”

Five years ago it was generally assumed that the public investment community would supply junior miners with the funds needed to explore and further develop assets. Today, only a solid project nearing feasibility is likely to appeal to investors, who are looking for projects close to production and

who focus primarily on the risk of the investment and, secondarily, on an asset’s potential. Exploration companies are commonly selling or spinning off earlier stage projects to focus on more advanced projects, in order to increase their appeal to investors and to maximise prospects for securing investment.

1 Miners grouped by the primary stage of flagship asset of “greenfield exploration,” “brownfield exploration,” or “pre-feasibility.”

I can see a situation at the upstream end of the market where explorers have either managed to raise cash in order to fulfill their business objectives or they have deferred or delayed their activities because of lack of funding.”

Gerry BeaneyHead of capital markets Grant Thornton, UK

“

3

Growth drivers

Figure 1: % of all companies rated 4 or 5 (5=major driver) Figure 2: % of all companies rated 4 or 5 (5=high)

Growth constraints

Less bargaining power with suppliers 10%

State of the art operations/automation/mechanisation 14%

Shortage of skilled/ experienced workers 23%

Increased outsourcing of projects by the majors 15%

Obtaining community local/support 25%

High performing supply chain19%

Operating costs

26%

Increased acquisitions or joint ventures and partnerships with the majors 26%

Volatility of commodity prices34%

Skilled workforce34%

Permitting/licensing procedures36%

Strong cost controls36%

Access to funding44%

Ability to raise capital48%

Increased government involvement and/or regulation 42%

Increased prices for your flagship commodity 41%

4

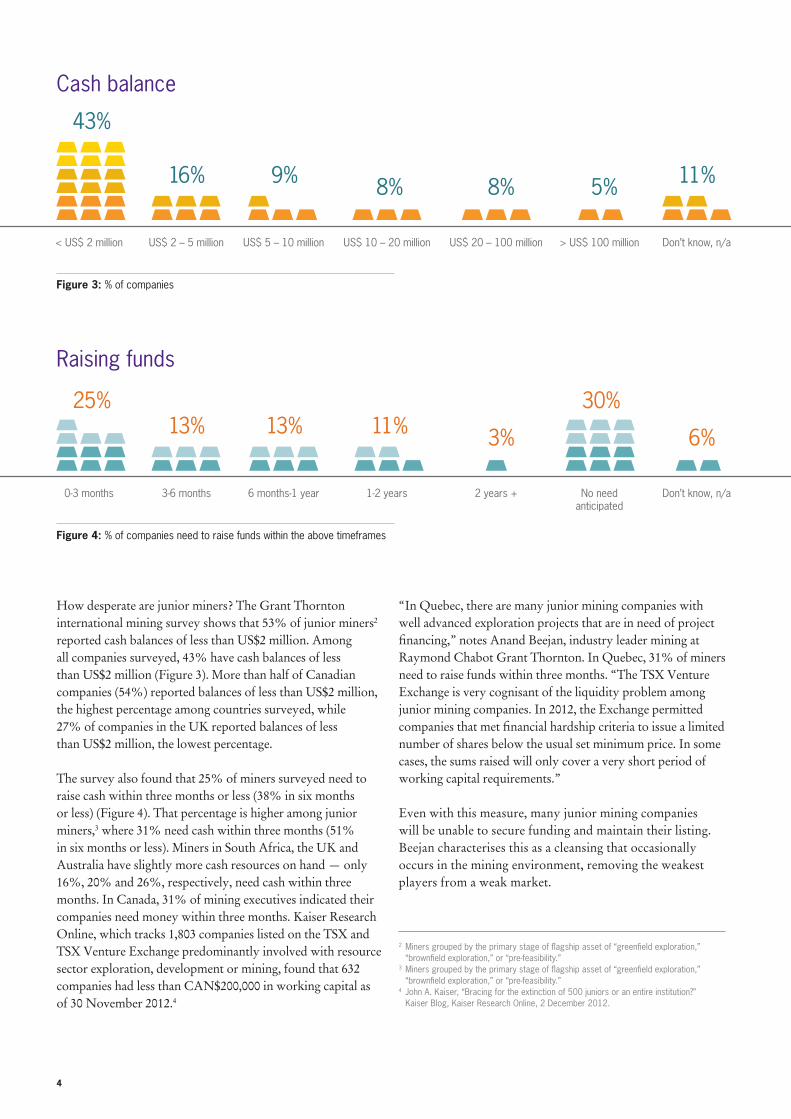

How desperate are junior miners? The Grant Thornton international mining survey shows that 53% of junior miners2 reported cash balances of less than US$2 million. Among all companies surveyed, 43% have cash balances of less than US$2 million (Figure 3). More than half of Canadian companies (54%) reported balances of less than US$2 million, the highest percentage among countries surveyed, while 27% of companies in the UK reported balances of less than US$2 million, the lowest percentage.

The survey also found that 25% of miners surveyed need to raise cash within three months or less (38% in six months or less) (Figure 4). That percentage is higher among junior miners,3 where 31% need cash within three months (51% in six months or less). Miners in South Africa, the UK and Australia have slightly more cash resources on hand — only 16%, 20% and 26%, respectively, need cash within three months. In Canada, 31% of mining executives indicated their companies need money within three months. Kaiser Research Online, which tracks 1,803 companies listed on the TSX and TSX Venture Exchange predominantly involved with resource sector exploration, development or mining, found that 632 companies had less than CAN$200,000 in working capital as of 30 November 2012.4

2 Miners grouped by the primary stage of flagship asset of “greenfield exploration,” “brownfield exploration,” or “pre-feasibility.”3 Miners grouped by the primary stage of flagship asset of “greenfield exploration,” “brownfield exploration,” or “pre-feasibility.”4 John A. Kaiser, “Bracing for the extinction of 500 juniors or an entire institution?” Kaiser Blog, Kaiser Research Online, 2 December 2012.

Figure 3: % of companies

Figure 4: % of companies need to raise funds within the above timeframes

Cash balance

Raising funds

“In Quebec, there are many junior mining companies with well advanced exploration projects that are in need of project financing,” notes Anand Beejan, industry leader mining at Raymond Chabot Grant Thornton. In Quebec, 31% of miners need to raise funds within three months. “The TSX Venture Exchange is very cognisant of the liquidity problem among junior mining companies. In 2012, the Exchange permitted companies that met financial hardship criteria to issue a limited number of shares below the usual set minimum price. In some cases, the sums raised will only cover a very short period of working capital requirements.”

Even with this measure, many junior mining companies will be unable to secure funding and maintain their listing. Beejan characterises this as a cleansing that occasionally occurs in the mining environment, removing the weakest players from a weak market.

< US$ 2 million

0-3 months

US$ 5 – 10 million

6 months-1 year

> US$ 100 million

No need anticipated

US$ 2 – 5 million

3-6 months

US$ 20 – 100 million

2 years +

US$ 10 – 20 million

1-2 years

Don’t know, n/a

Don’t know, n/a

43%

25% 30%

16%

13% 13% 11%

9% 8% 8%

3%

5%

6%

11%

5

Insight: Funding

Junior miners can still find financing, but must rigorously improve the effectiveness of their exploration activities, management expertise, and how they present their opportunities to investors.

Simon Gray, national head of energy and resources, Grant Thornton Australia, says, “The need for funding is a global issue. Many exploration companies are really down to the wire and are finding fundraising more challenging now than it has been for many years. It’s an indication of where we are in the market at the moment, that companies are really struggling to raise money. Investors are very picky about where they put their money, and many of them are sitting on cash. They’re just not deploying it, and certainly they’re not deploying it at the high-risk end of the market, which is early-stage exploration. Raising money for early-stage companies is extremely hard, whether it’s in Australia, Canada, the UK or other parts of the world.”

A troubling combination of factors are damaging the ability of junior miners to raise funds and maintain sufficient cash balances — and many of these factors are not within a company’s control: general risk aversion on the part of investors and purchasers of assets, stagnant economies, volatile capital markets around the globe, the high-risk/high-reward nature of exploration, and a rising number of labour disputes in the mining sector.

Simply waiting out this investment environment isn’t possible for many junior miners, and so, even with funding tight, savvy executives have found ways to get the funding they require. These deals are done using alternative funding approaches (including private equity or hybrid financial instruments), realistic expectations on market valuations of their companies and projects, and presentation of strong leadership/management teams to investors.

“What is currently happening to miners is largely beyond their control, but there are ways in which they can manage things,” says Canada’s Zastre. “Companies with noncore assets are looking to monetise them to the extent they can, trying to consolidate with other companies to increase their attractiveness to raise capital. In this tough environment, looking to alternate sources of financing presents a few options, but right now the options are quite limited.”

One alternative route is the use of streaming companies, which seek viable projects and then buy future production at a discount in return for exploration or development cash now. But companies hoping to interest streaming companies will need to be reasonably advanced, with their projects significantly de-risked, in order to get upfront cash payments in exchange for a percentage of future mineral production.

Even when projects are at or near feasibility stage and are therefore likely to be more attractive to investors, mining executives will require patience and a well-planned approach. Strategies for easing investor concerns rely heavily on the strength of technical data and on the underlying viability of

31% of junior miners need to raise funds in 0-3 months.

6

the company itself. Investors have always focused on projects and assets, but they now are also scrutinising boards and management teams. Investors are increasingly demanding that mining companies be run by experienced professionals. The days of exploration as a “lifestyle business” for maverick entrepreneurs may have passed forever.

“When you’re investing in an early stage company, the board and management are just as important, sometimes more important, than the quality of the assets themselves,” says Gray. “Looking back at the IPOs of exploration companies in Australia in 2012, it was the companies with well-credentialed boards and management that were most successful.”

“It is tough out there, but it’s not tough for everybody, and I have clients who have a good team with a strong network,” notes Zastre. “People in this industry over the last few years have made a lot of money. There is significant wealth in the hands of players who appreciate the risks and have been very successful at playing the odds. They invest with people that they know and trust. There are those ‘inside that circle’ who are raising significant sums of money, but most often it’s because of who they are, and who they know.”

It’s not all doom and gloom, notes Beaney: “Look at the London AIM Market. The most popular sector for fundraising during 2012 was mining, and the FTSE 100 index broke through

It’s tough out there, but it’s not tough for everybody, and I have clients who have a good team with a strong network. There is significant wealth in the hands of players who appreciate the risks and have been very successful at playing the odds. They invest with people that they know and trust.”

Mark Zastre Global industry leader mining Grant Thornton LLP, Canada

5 “Mergermarket M&A roundup for Q1-Q3 2012,” Mergermarket, 2 October 2012.

6 Stephen Cranston, “2012 M&A less than half what it was in 2007,” Financial Mail, 21 January 2013.

recent history,” suggests Beaney. “Executives need to be more realistic on valuations because we live in a difficult environment at the moment, people are scared, there’s a lot of risk aversion. Maybe they can raise a little bit less than they were looking for, but deploy it differently, more cautiously.”

“

the 6,000 barrier in January 2013, largely as a result of investor interest in the sector. We’re seeing a more bullish approach to equities as investors see the downside to the bond market.”

Mergers and acquisitions also remain an option for junior miners in need of cash or looking for alternative ways to achieve value for shareholders. A quarter of mining executives (26%) rated increased acquisitions or joint ventures and partnerships with majors as drivers of growth for their organisations (rated 4 or 5 on a scale of 1-5 where 5 is “major driver”). Thirty-two percent of junior miners rated acquisitions/joint ventures as a driver.

Looking back, M&A activity in the global energy, mining and utilities sector fell for the nine months through Q3 2012 (847 deals valued at US$379 billion) vs. Q3 2011 (912 deals valued at US$412.5 billion).5 But mining deals are still being completed. In South Africa, metal and metal products remained the single largest source of deals, at US$3 billion.6

M&A activity can stall due to valuation disparities among buyers and sellers, which are often more common when experienced mining executives are involved. Veteran mining leaders may still consider pre-downturn asset ratios as valid, refusing to acknowledge changes in the market and investor attitudes. “I think it’s more acute at the moment than I have seen in

7

Government and public pressures increase

Miners around the world are experiencing increased governmental and public pressures: tighter permitting and licensing procedures, increased environmental controls and expectations, and growing lists of regulations. For example, Bolivia has enacted a “Mother Earth” law that gives nature equal rights with humans and human activities, such as mining, and in Venezuela the gold industry was nationalized. Miners remain concerned there and elsewhere.

Forty-two percent of executives responding to the Grant Thornton international mining survey cited increased government involvement and/or regulation as a constraint on growth, and another 36% rated permitting/licensing procedures as a constraint (rated 4 or 5 on a scale of 1-5 where 5 is “high”). A majority of miners in Australia (58%) rated increased government involvement and/or regulation as a constraint on growth, the highest percentage among countries surveyed.

“It is such a key issue here in Australia. The government is doing little to support exploration companies, and it doesn’t really have the interest of junior miners on its agenda,” says Gray. Increased regulation has driven project approval times from months to years. “From an industry perspective, the only key changes government has made in recent times have been to

unexpectedly add new taxes.” Adding to uncertainty in Australia is a debate over the effectiveness of the new Minerals Resource Rent Tax (MRRT). The MRRT imposes a tax on profits generated from the exploitation of non-renewable resources in Australia. From iron ore and coal projects, the tax has only generated AU$126 million in the six months ended 31 December 2012,7 compared to forecasts of AU$2 billion for the full financial year to end 30 June 2013.

Increased regulation and the impost of new taxes have placed more demands on executives to prove the viability of projects, and have dampened the enthusiasm of international investors in the Australian mining sector. A Grant Thornton survey conducted among miners in Australia in mid-2012 also found permitting/licensing procedures to be a major constraint on growth, specifically the slow and complex procedures to obtain licenses.8 “Governments should consider increasing incentives to encourage exploration to ensure that the industry continues to progress, and that the mines of the future are identified,” argues Gray. “A prolonged period of reduced exploration could set back future discoveries significantly. This impacts employment and the viability of the industry.”

7 “Parlimentary Business: Mineral Resource Rent Tax Installments,” Australian Taxation Office, Feb. 8, 2013.8 JUMEX Survey, Grant Thornton Australia, October 2012.

8

Exploration is a high-risk business made even riskier by increased government regulations. Many countries’ bureaucratic procedures are becoming more numerous and difficult, some to the point of discouraging both investors and, therefore, exploration: a planned EU law will require resource companies and certain other industries to disclose country-by-country reporting. The law may go into effect as early as 2014, which would mean data collection beginning in late 2013. There also are calls for extractive companies to disclose how they support local economies through taxes, payments for exploitation rights, contributions to local infrastructure, etc. Similarly in the United States, an SEC ruling on conflict minerals — issued as part of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 — will impact miners by requiring public companies that manufacture products containing designated minerals, or that use designated minerals in a manufacturing process, to annually disclose whether the minerals originated from the Democratic Republic of

the Congo (DRC) and neighboring countries. These companies will also be required to disclose their efforts to trace the conflict minerals back to their sources.9

In South Africa, which holds some of the world’s largest precious metals reserves — and where mining is the country’s largest employer — authorities continue to investigate labour unrest that resulted in deaths and injuries at a Marikana mine. Other pending government activity there could dramatically alter the mining landscape: legislation that would require contributions from mining companies for local economic development via the Spatial Planning and Land Use Management Bill of 2012, and the draft Mineral and Petroleum Resources Development Amendment Bill of 2012. Already in place is the Mining Charter, which, among its provisions, requires that holders of mining rights achieve 26% ownership participation by historically disadvantaged South Africans in their mining operations by 30 April 2014 (15% was required by 30 April 2009).

A prolonged period of reduced exploration could set back future discoveries significantly. This impacts employment in the industry and the viability of the industry.”

Simon GrayNational head of energy and resourcesGrant Thornton, Australia

“

9

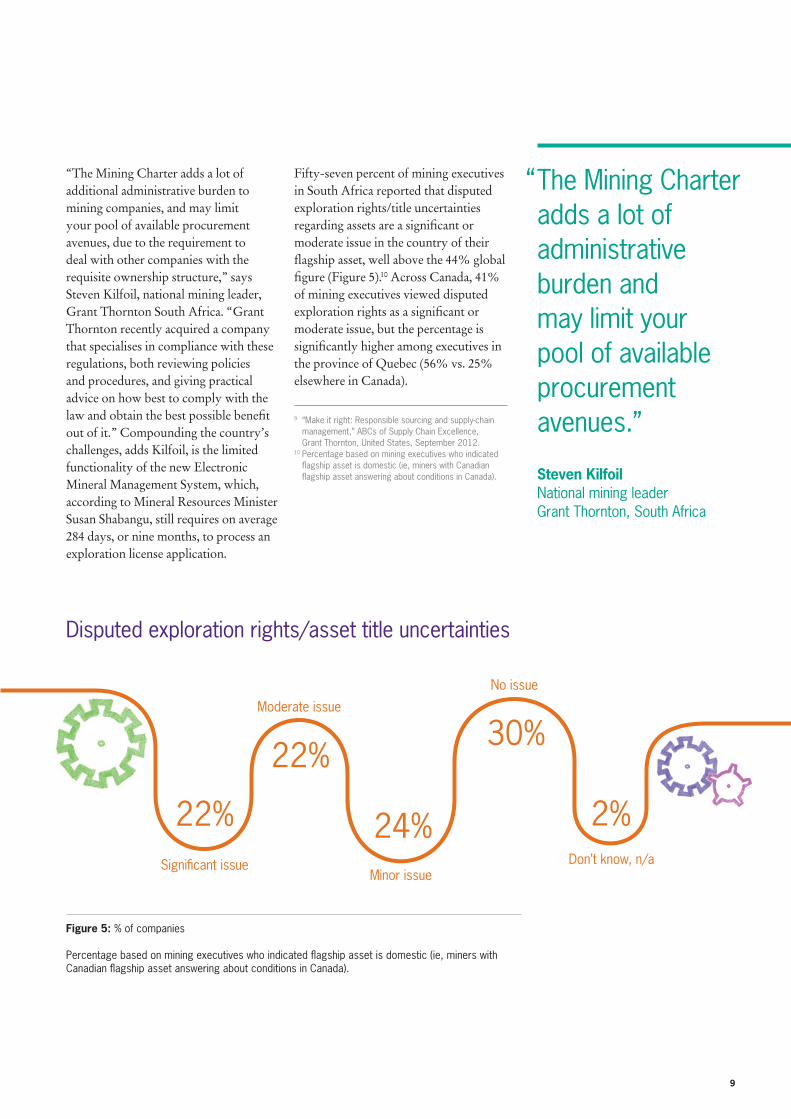

Figure 5: % of companies

Percentage based on mining executives who indicated flagship asset is domestic (ie, miners with Canadian flagship asset answering about conditions in Canada).

Significant issueMinor issue

Don’t know, n/a

Moderate issue

No issue

22%

22%

24%

30%

2%

9 “Make it right: Responsible sourcing and supply-chain management,” ABCs of Supply Chain Excellence, Grant Thornton, United States, September 2012.10 Percentage based on mining executives who indicated flagship asset is domestic (ie, miners with Canadian flagship asset answering about conditions in Canada).

“The Mining Charter adds a lot of additional administrative burden to mining companies, and may limit your pool of available procurement avenues, due to the requirement to deal with other companies with the requisite ownership structure,” says Steven Kilfoil, national mining leader, Grant Thornton South Africa. “Grant Thornton recently acquired a company that specialises in compliance with these regulations, both reviewing policies and procedures, and giving practical advice on how best to comply with the law and obtain the best possible benefit out of it.” Compounding the country’s challenges, adds Kilfoil, is the limited functionality of the new Electronic Mineral Management System, which, according to Mineral Resources Minister Susan Shabangu, still requires on average 284 days, or nine months, to process an exploration license application.

Fifty-seven percent of mining executives in South Africa reported that disputed exploration rights/title uncertainties regarding assets are a significant or moderate issue in the country of their flagship asset, well above the 44% global figure (Figure 5).10 Across Canada, 41% of mining executives viewed disputed exploration rights as a significant or moderate issue, but the percentage is significantly higher among executives in the province of Quebec (56% vs. 25% elsewhere in Canada).

Disputed exploration rights/asset title uncertainties

“The Mining Charter adds a lot of administrative burden and may limit your pool of available procurement avenues.”

Steven Kilfoil National mining leader Grant Thornton, South Africa

10

Insight: Regulations and land rights

Although regulations and land disputes threaten mining projects worldwide, local partners and professional services firms can help junior miners navigate to success.

“Most of the exploration work is done up north,” says Beejan of Quebec, “where there are many First Nations communities, and there are issues about disputed rights, ability to build infrastructure, and bringing mines to commercial production. There is a general perception that wealth-sharing is unequal between mining companies and the First Nations, and this is something mining companies need to acknowledge and are working to address. Companies that have taken the time to build relationships with local communities have been able to conclude successful agreements.”

“This highlights one of the risks of the industry,” adds Zastre. “The Grant Thornton international mining survey finds that nearly half of mining executives are concerned with uncertainties around titles to assets. Without clear title to your asset, you may have nothing. Imagine this situation occurring in another industry, such as car manufacturing, in which executives worry about having unfettered access to their facilities.” He explains, for example, that in some Canadian provinces, there are significant and widespread areas over which unsettled land claims are outstanding.

22% of respondents stated that disputed

exploration rights/title uncertainties are a

significant issue.

11

• mineral exploration tax credits in British Columbia

• venture capital incentives in South Africa

• exploration tax incentives in Australia.

In September 2012, Western Australian Minister for Mines and Petroleum Norman Moore announced AU$5 million funding for 2013 drilling programs; previous funding has provided (in aggregate) AU$27 million in grants since 2009 and is expected to provide AU$138 million in grants to explorers by 2016.12 Gray, however, notes these are modest sums, given recent declines in exploration activity in Australia and other parts of the world. “If you’re looking to the future, you can’t find the next mine unless you do exploration. So governments looking to increase revenues from mining companies need to make sure that those mines are going to continue to be found and developed.”

The industry in Australia has been calling for a flow-through scheme, similar to the one in Canada, to encourage investment in junior exploration companies. The flow-through share scheme has been in place in Canada for many years; under the programme investors who purchase flow-through shares are able to obtain mineral resource company tax deductions. These deductions effectively “flow through” from the company to the investor. The investor pays for the shares, and the corporation transfers certain mining expenditures to the investor. Flow-through share investors can then deduct their investments from otherwise taxable income.

11 Participants could select more than one answer.12 Kathryn Diss, “Miners call for exploration tax incentives,” ABC News, Sept. 4, 2012.

“There are dozens of in-process treaty negotiations, and each one is a process that can take years. Within many of these areas there are mines or good potential for mines. Mining companies can and do work with the local authorities to try to obtain the necessary permits, but if they haven’t considered the needs and rights of the local First Nations communities affected, their projects could be in jeopardy. If companies don’t involve all the stakeholders at the initial stages of the project, the project risk goes up dramatically.”

Title disputes are not an issue in every country. Gray says that within Australia there may be red tape in licensing, but once a company has a license, it’s rare for titles to be disputed. “But it’s a major issue for Australian companies that have projects in Africa, and also in certain parts of Asia. In those areas, companies that have lost titles to their assets have not had strong local partners and have tried to do things remotely. That hasn’t worked. Engagement and involvement of local partners is critical. Local expertise helps explorers ask the questions they don’t know they should ask.”

Managing widely dispersed assets can be challenging, yet most mining executives say they coordinate government relations activity with their internal staffs (81%). Another 49% of miners use external legal counsel in lieu of, or in addition to, their own staff; another 38% use external agents/consultants.11 External assistance is especially helpful in securing government incentives and grants, such as:

• flow-through share tax credits in Canada

• investment credits for pre-production mining in Quebec

Companies that have taken the time to build relationships with local communities have been able to conclude successful agreements. If companies don’t involve all stakeholders at the initial stage ofthe project, the project risk goes up dramatically.”

Anand Beejan Industry leader miningRaymond Chabot Grant Thornton Quebec

“

12

Yet even with government programmes that can benefit the industry, Zastre says miners still face wavering public support. “The hurdles — land tenure, environmental restrictions, First Nations claims, permitting requirements — in front of companies that want to explore or exploit mineral resources are on the upswing. Our federal minister of natural resources is working to create a permitting system that is more streamlined, but he’s definitely swimming upstream in terms of public sentiment, the weight of the media, and the perception that mining is not environmentally friendly.”

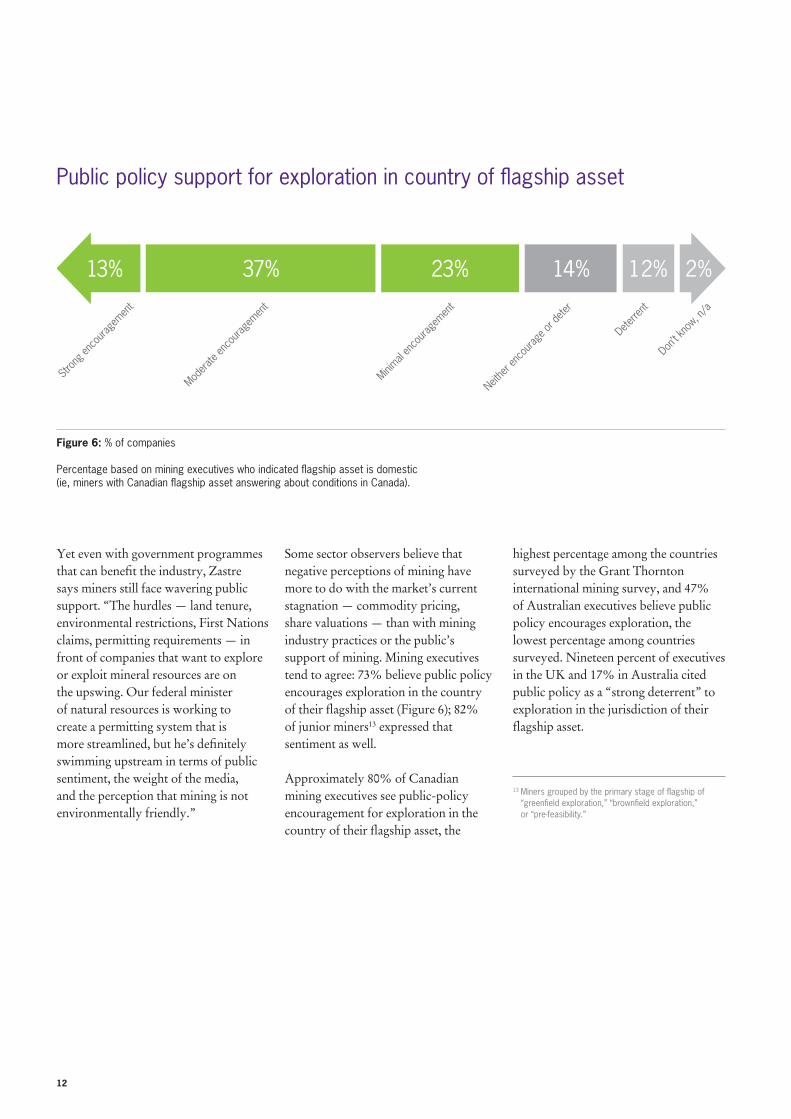

Figure 6: % of companies

Percentage based on mining executives who indicated flagship asset is domestic (ie, miners with Canadian flagship asset answering about conditions in Canada).

13 Miners grouped by the primary stage of flagship of “greenfield exploration,” “brownfield exploration,” or “pre-feasibility.”

Public policy support for exploration in country of flagship asset

Some sector observers believe that negative perceptions of mining have more to do with the market’s current stagnation — commodity pricing, share valuations — than with mining industry practices or the public’s support of mining. Mining executives tend to agree: 73% believe public policy encourages exploration in the country of their flagship asset (Figure 6); 82% of junior miners13 expressed that sentiment as well. Approximately 80% of Canadian mining executives see public-policy encouragement for exploration in the country of their flagship asset, the

13% 37% 23% 14% 2%

Stron

g enc

ourag

emen

t

Modera

te en

coura

gemen

t

Minimal

enco

urage

ment

Neithe

r enc

ourag

e or d

eter

Deterre

nt

Don’t k

now, n

/a

highest percentage among the countries surveyed by the Grant Thornton international mining survey, and 47% of Australian executives believe public policy encourages exploration, the lowest percentage among countries surveyed. Nineteen percent of executives in the UK and 17% in Australia cited public policy as a “strong deterrent” to exploration in the jurisdiction of their flagship asset.

12%

13

14 Percentage based on mining executives who indicated flagship asset is domestic (ie, miners with Canadian flagship asset answering about conditions in Canada 15 Parliament of Canada.

Bribery and corruption

Governments around the globe are taking harsher stands against bribery and corruption. Most mining companies have implemented practices and procedures to prevent such illegal acts by employees or partners. Approximately 70% of mining executives indicated that their companies have a code of conduct that clearly addresses bribery and corruption issues, and another 9% reported that a code of conduct is planned.

This level of preparedness also is seen in statistics that show that 42% of mining executives said that bribery and corruption is “no concern” and 15% said it is a “minor concern” in the country of their flagship asset; 71% of executives in the UK and 69% in Australia cited bribery and corruption as no concern. Executives are most likely to rate bribery and corruption as a “significant concern” in South Africa (41%) and Canada (18%).14

“I think the percentage in South Africa is probably a little higher than I would have expected, but based on some events in the country, obviously mining executives are concerned,” says Kilfoil in South Africa. Quebec’s Beejan points to recent extensive media coverage in the province of a commission of inquiry into corruption in the construction industry. Publicity surrounding the case, he adds, influences the concerns of Quebec-based executives. “Isolated instances of corruption occasionally emerge in all industries and jurisdictions, but I think in Quebec we are currently more aware of the risks and consequences.”

Awareness of bribery and corruption is high for Canadian companies in any industry. In February, the government proposed amendments to the Corruption of Foreign Public Officials Act (CFPOA) to improve the enforcement of CFPOA and increase penalties for non-compliance.15

14

Miners remain optimistic despite challenges

A majority of mining executives surveyed expect rising energy and labour costs (see page 16) in the coming year, but many also expect the pricing of their flagship asset’s commodity to increase as well. Projections for employment, turnover/revenue, and profitability growth are less robust; for example, 34% of mining executives expect revenue to increase, while 12% expect a decrease (balance of +22 percentage points) (Figure 7).

Australia’s Gray notes, “Many junior miners are not in production, so they don’t make profits. What is more relevant is the financial viability and attractiveness of projects and the willingness to invest in these projects.” Here, too, miners are reasonably optimistic. The Grant Thornton international mining survey found that 46% of miners will increase exploration expenditures in the coming year; only 12% expect to decrease

expenditures (56% of junior miners will increase exploration expenditures).

Another important insight from the survey data, adds Gray, is the expectation that commodity prices will increase. “Junior miners are reliant on fundraising, and if their project isn’t expected to have an appropriate return (due to reduced commodity prices, increased costs), then they are less likely to be able to raise the capital to

Business trends

Figure 7: % of companies increase/decrease

Energy costs

INCREASE

DECREASE

Pricing of the key commodity of your

flagship projectLabour costs Exploration

expenditure

Investment in plant and machinery

Employment Turnover/revenues Profitability

55%

3%

54%

6%

52%

9%

46%

12%

42%

9%

40%

10%

34%

12%

32%

12%

15

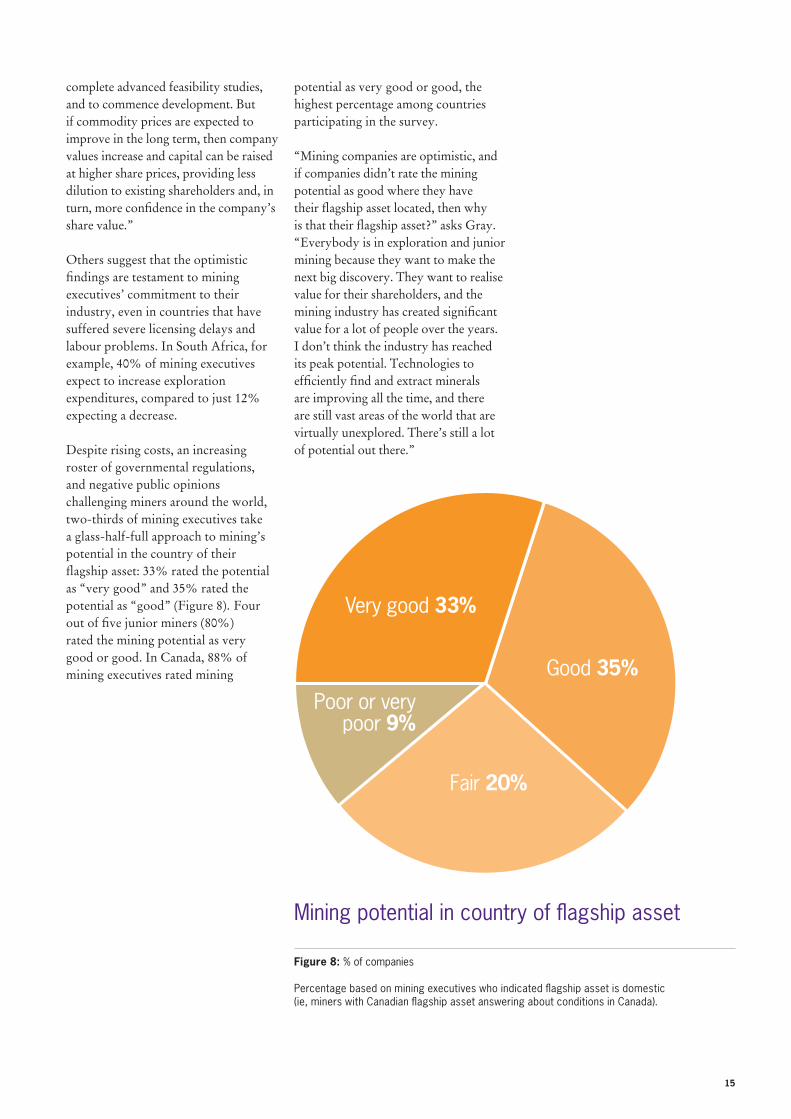

Very good 33%

Good 35%

Fair 20%

Poor or very poor 9%

Figure 8: % of companies

Percentage based on mining executives who indicated flagship asset is domestic (ie, miners with Canadian flagship asset answering about conditions in Canada).

Mining potential in country of flagship asset

complete advanced feasibility studies, and to commence development. But if commodity prices are expected to improve in the long term, then company values increase and capital can be raised at higher share prices, providing less dilution to existing shareholders and, in turn, more confidence in the company’s share value.”

Others suggest that the optimistic findings are testament to mining executives’ commitment to their industry, even in countries that have suffered severe licensing delays and labour problems. In South Africa, for example, 40% of mining executives expect to increase exploration expenditures, compared to just 12% expecting a decrease.

Despite rising costs, an increasing roster of governmental regulations, and negative public opinions challenging miners around the world, two-thirds of mining executives take a glass-half-full approach to mining’s potential in the country of their flagship asset: 33% rated the potential as “very good” and 35% rated the potential as “good” (Figure 8). Four out of five junior miners (80%) rated the mining potential as very good or good. In Canada, 88% of mining executives rated mining

potential as very good or good, the highest percentage among countries participating in the survey. “Mining companies are optimistic, and if companies didn’t rate the mining potential as good where they have their flagship asset located, then why is that their flagship asset?” asks Gray. “Everybody is in exploration and junior mining because they want to make the next big discovery. They want to realise value for their shareholders, and the mining industry has created significant value for a lot of people over the years. I don’t think the industry has reached its peak potential. Technologies to efficiently find and extract minerals are improving all the time, and there are still vast areas of the world that are virtually unexplored. There’s still a lot of potential out there.”

16

Rising employee salaries

More than half of mining executives (54%) report that their companies will increase employee salaries at the rate of inflation in the next 12 months, and another 21% will increase salaries above the rate of inflation. This trend makes it imperative for operators to focus on employee productivity. Many mining operations are deploying “lean” techniques, improving their management systems, and emphasizing development and training of front-line workers to drive out costs.

While salaries are increasing at many companies, executives are countering that trend with improved productivity and application of technologies that allow them to reduce headcounts — in effect, adding highly skilled workers and high-tech automation. “Instead of having a whole host of operators driving big trucks, you’ve got technicians doing it remotely from a control room,” says Beaney in the UK. Gray concurs, citing a big push, especially among majors in the Australia, to add automation. “They’re automating trucks, they’re automating trains, whatever is possible, because of the record labour costs that we’re facing at the moment.”

17

Minimise risk, maximise opportunity

The Grant Thornton International Mining Report highlights trends and their impact on mining companies based or operating within Australia, Canada, South Africa and the UK. How will your organisation overcome these challenges and leverage their corresponding opportunities?

Financing and transactions Is your company able to accurately evaluate your asset portfolio in light of new market conditions? These are challenging times for junior miners in need of financing. An independent perspective can help mining executives find the capital they need — via conventional equity routes, M&A, or alternative options. It is important to position your business where it makes the most sense given its development stage, the location of its assets, and commodity price trends.

Regulatory complianceDoes your company have the ability to monitor, measure and document regulatory compliance — or are you and your company at risk? Establish a robust compliance framework appropriate to your organisation and assets, including evaluation of current compliance, development of risk-mitigation strategies, and implementation of rigorous reporting and monitoring structures.

Risk managementHow do mining trends in your country and around the world translate into opportunities and risks for your organisation? Who will be accountable for these risks, and how should they be measured and managed? Research has shown that higher growth rates are more likely at companies with a formalised risk framework in place. Such an approach builds a risk-aware culture by ensuring that existing and emerging risks are identified, assessed and appropriately addressed, with clear assignments throughout the company for managing risks.

Ethical business behaviorsMining companies conducting business on a global scale face significant risks and severe penalties for bribery, corruption, fraud and money laundering. Companies of every size should develop policies and processes to navigate this legal landscape and establish consistent, documented ethical practices. This reduces the risk of conduct breaches while providing strong corporate defenses in the event that unethical business practices occur.

Process improvementsMining is a centuries-old industry, yet technologies and processes are evolving more rapidly than ever. Does your operation have the new tools, skilled talent and continuous improvement mindset to drive cost efficiencies and productivity improvements year after year? Have you comprehensively reviewed your cost structure for cash-flow improvement opportunities?

Every mining company can benefit from a fresh perspective. Grant Thornton is one of the world’s leading organisations of independent assurance, tax and advisory firms. These firms help dynamic organisations unlock their potential for growth by providing meaningful, actionable advice. Proactive teams, led by approachable partners in these firms, use insights, experience and instinct to understand complex issues for privately owned, publicly listed and public sector clients and help them to find solutions. Over 35,000 Grant Thornton people, across 100 countries, are focused on making a difference to clients, colleagues and the communities in which we live and work.

18

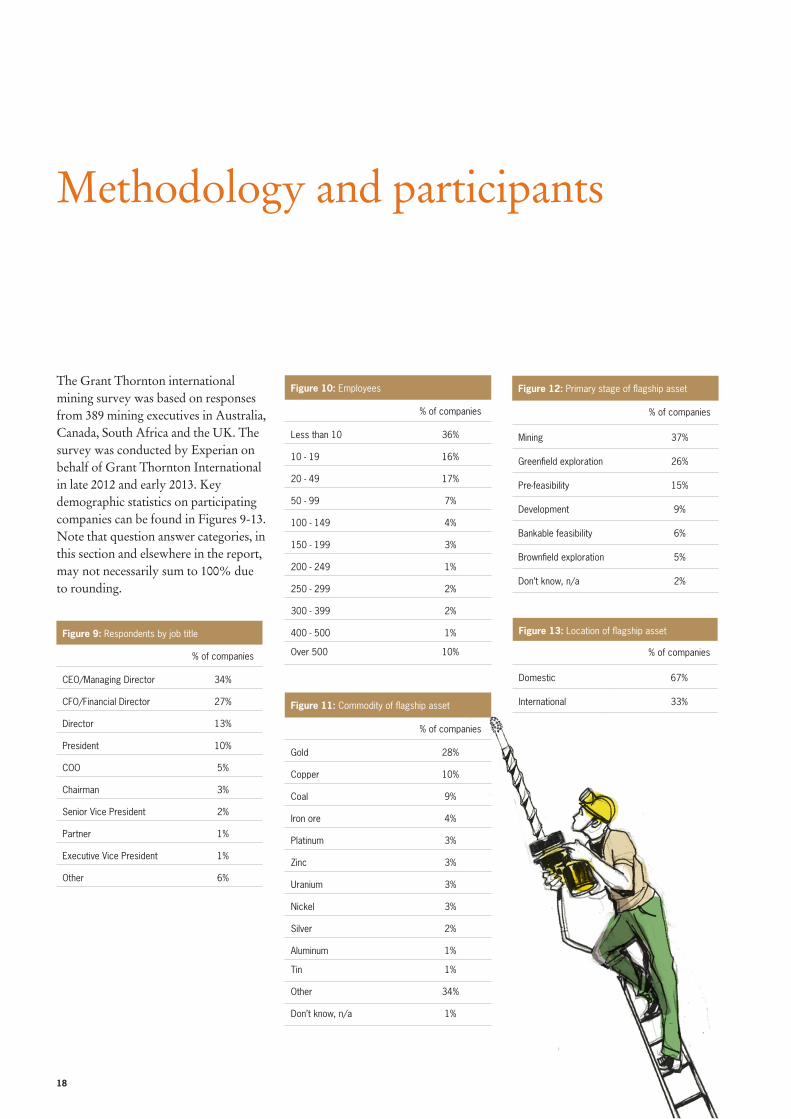

Methodology and participants

The Grant Thornton international mining survey was based on responses from 389 mining executives in Australia, Canada, South Africa and the UK. The survey was conducted by Experian on behalf of Grant Thornton International in late 2012 and early 2013. Key demographic statistics on participating companies can be found in Figures 9-13. Note that question answer categories, in this section and elsewhere in the report, may not necessarily sum to 100% due to rounding.

Figure 9: Respondents by job title

% of companies

CEO/Managing Director 34%

CFO/Financial Director 27%

Director 13%

President 10%

COO 5%

Chairman 3%

Senior Vice President 2%

Partner 1%

Executive Vice President 1%

Other 6%

Figure 10: Employees

% of companies

Less than 10 36%

10 - 19 16%

20 - 49 17%

50 - 99 7%

100 - 149 4%

150 - 199 3%

200 - 249 1%

250 - 299 2%

300 - 399 2%

400 - 500 1%

Over 500 10%

Figure 11: Commodity of flagship asset

% of companies

Gold 28%

Copper 10%

Coal 9%

Iron ore 4%

Platinum 3%

Zinc 3%

Uranium 3%

Nickel 3%

Silver 2%

Aluminum 1%

Tin 1%

Other 34%

Don’t know, n/a 1%

Figure 12: Primary stage of flagship asset

% of companies

Mining 37%

Greenfield exploration 26%

Pre-feasibility 15%

Development 9%

Bankable feasibility 6%

Brownfield exploration 5%

Don’t know, n/a 2%

Figure 13: Location of flagship asset

% of companies

Domestic 67%

International 33%

19

Industry knowledge, local expertise

At Grant Thornton we understand the mining landscape. We focus on understanding the core drivers of businesses, their goals and objectives and, with this knowledge, ensure they gain maximum advantage from our unique service offering. By identifying the key issues you are facing, we develop tailored solutions to meet your objectives by offering a combination of global mining knowledge and local expertise:

Assurance services• audit testing• corporate governance reviews• financial management• IFRS advisory• internal and external audit services• internal audit• risk assessment• statutory audits• sustainability reporting.

Capital markets• assistance with fund raising• mergers and acquisitions• Nominated Adviser (of the

London AIM market)• preparation for flotation.

Operational advisory• internal controls review• fraud investigation and

dispute services• productivity improvement services.

Transaction advisory• deal support• due diligence• information technology

and assurance• post deal integration• reporting accountant• sustainability and climate

change services.

Lead advisory• acquisitions• disposals• MBIs/MBOs• refinancing.

Sustainability• assurance against

international standards• integrated approach to

non-financial reporting.

Tax• business tax compliance• dispute resolution• employment tax• energy and emission trading• indirect taxes (VAT/GST)• international tax issues• managing capital tax issues• mergers and acquisitions tax services• shareholder tax planning• tax and risk advisory services• tax management consulting• transfer pricing.

20

Global mining contacts

AustraliaSimon GrayT +61 8 8372 6666E [email protected]

Holly StilesT +61 8 9480 2111E [email protected]

BotswanaVijay KalyanaramanT +2673952313E [email protected]

BrazilNelson BarretoT +55 (11) 38865111E [email protected]

CanadaJeremy JagtT +1 416 360 2369E [email protected]

Doug SteeleT +604 443 2198E [email protected]

Bill SurphlisT +1 416 777 7223E [email protected]

Mark ZastreT +604 443 2170E [email protected]

QuebecAnand BeejanT +1 (0) 514 393 4802E [email protected]

John CochraneT +514 390 4139E [email protected]

KazakhstanYerzhan DossymbekovT +7 72 73 111 340E [email protected]

MexicoEsteban Urióstegui BárcenasT +52 (55)5424 6500E [email protected]

MozambiqueDev PydannahT +25821311937E [email protected]

NamibiaTom NewtonT +26461381200E [email protected]

21

PeruJose Luis Sarrio AbadT +51 (1)615 6868E [email protected]

RussiaSergey TishakovT +7 495 775 0050E [email protected]

South AfricaSteven KilfoilT +27 (0)11 322 4550E [email protected]

Christel PretoriusT +27 (0)11 322 4782E [email protected]

Mohamed Zakaria Sadek (Zak)T +27 (0)11 322 4604E [email protected]

SwedenJohan ErikssonT +46 (0)8 563 073 28E [email protected]

United KingdomGerry BeaneyT +44 (0)20 7728 2589E [email protected]

Eddie BestT +44 (0)20 7728 [email protected]

Martin GoddardT +44 (0)20 7728 2770E [email protected]

Christopher Hall – ConsultantT +44 (0)20 7728 3196E [email protected]

Chris SmithT +44 (0)20 7728 [email protected]

United StatesPatrick GableT +1 216 858 3537E [email protected]

ZambiaEdgar HamuweleT +260211227722E [email protected]

ZimbabweTinashe MawereT +26 3444 2511E [email protected]

© 2013 Grant Thornton International Ltd. All rights reserved.

References to ‘Grant Thornton’ are to the brand under whichGrant Thornton member firms operate and refer to one or moremember firms, as the context requires.

Grant Thornton International Ltd and the member firms are not aworldwide partnership. Services are delivered independently bymember firms, which are not responsible for the services oractivities of one another.

Grant Thornton International Ltd does not provide services to clients.

www.gti.org