Embed Size (px)

Citation preview

IAS 27, 28 and 31Consolidated and Separate Financial Statements

Investment is Associates Interests in Joint Ventures

Prakash C BishtSr. Vice President ( Group Accounts)Jubilant Life Sciences Ltd

Agenda

n Classification of Investmentn Identifying a subsidiary / associate / joint – venturen Presentation of Consolidated Financial Statementsn Exclusionsn Separate Financial Statementsn Disclosuresn Differences – IFRS / IND AS

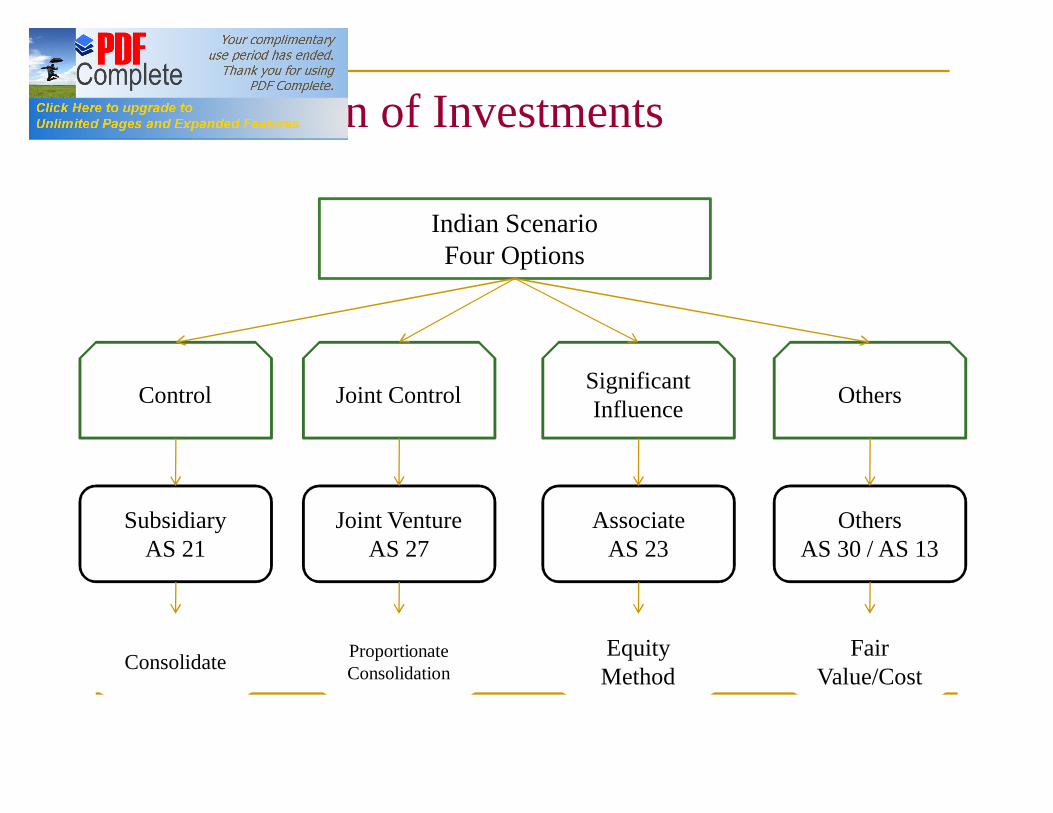

Indian ScenarioFour Options

Classification of Investments

Joint Control Significant InfluenceControl Others

SubsidiaryAS 21

Joint VentureAS 27

AssociateAS 23

OthersAS 30 / AS 13

Consolidate Proportionate Consolidation

Equity Method

Fair Value/Cost

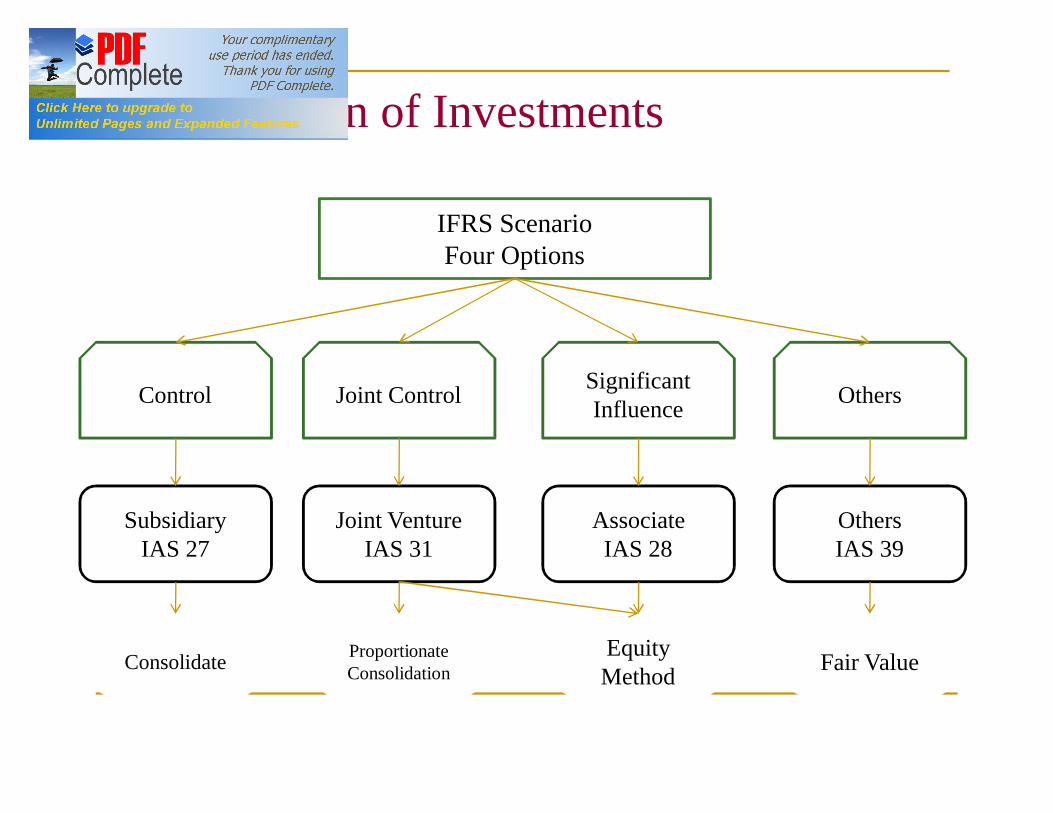

IFRS ScenarioFour Options

Classification of Investments

Joint Control Significant InfluenceControl Others

SubsidiaryIAS 27

Joint VentureIAS 31

AssociateIAS 28

OthersIAS 39

Consolidate Proportionate Consolidation

Equity Method Fair Value

i GAAP

Identifying a Subsidiary

The Starting Point

50% -100%

20% - 50%

0% - 20% No Influence

Significant Influence

Joint Control

Control

Level of Ownership

Level of Influence

i GAAP

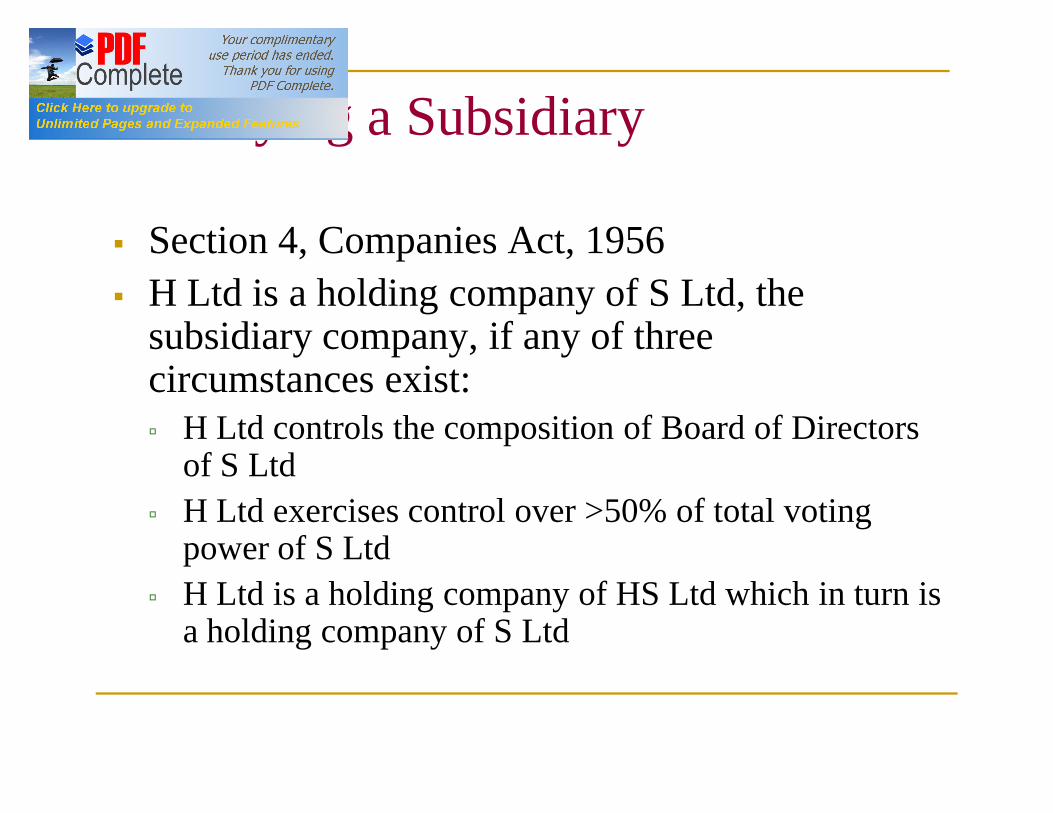

Identifying a Subsidiary

Identifying a Subsidiary

§ Section 4, Companies Act, 1956§ H Ltd is a holding company of S Ltd, the

subsidiary company, if any of three circumstances exist:ú H Ltd controls the composition of Board of Directors

of S Ltdú H Ltd exercises control over >50% of total voting

power of S Ltdú H Ltd is a holding company of HS Ltd which in turn is

a holding company of S Ltd

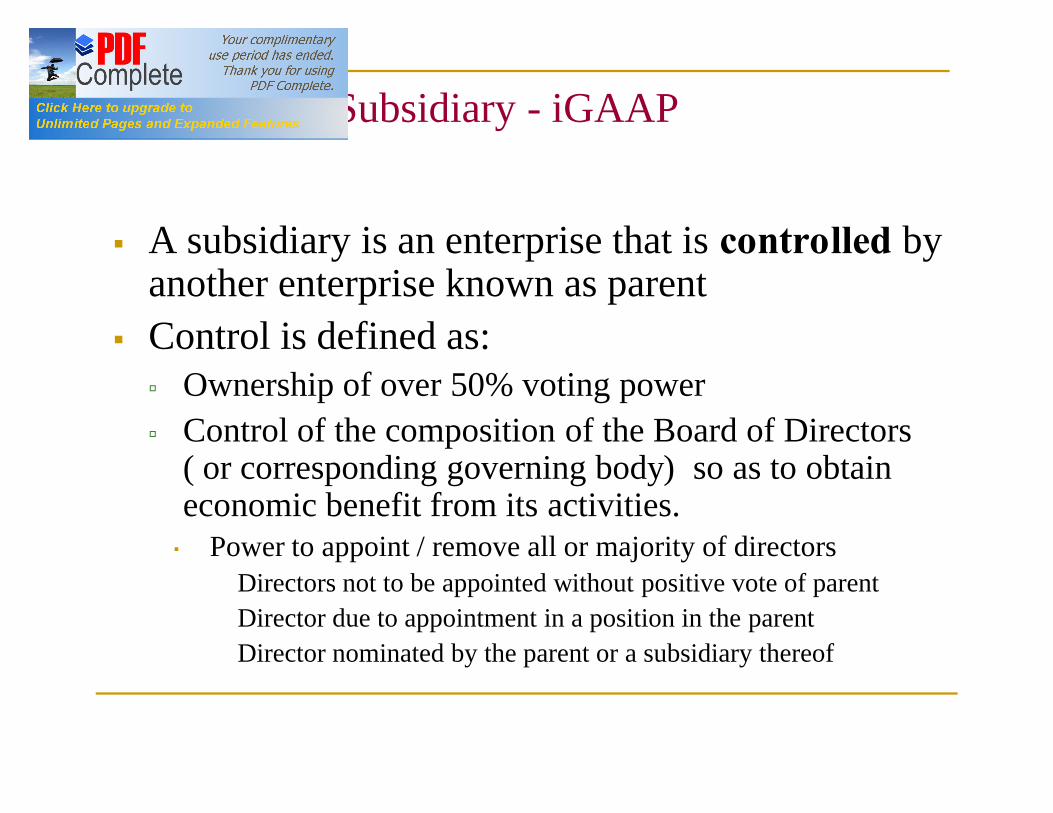

Identifying a Subsidiary - iGAAP

§ A subsidiary is an enterprise that is controlled by another enterprise known as parent

§ Control is defined as:ú Ownership of over 50% voting powerú Control of the composition of the Board of Directors

( or corresponding governing body) so as to obtain economic benefit from its activities. Power to appoint / remove all or majority of directors Directors not to be appointed without positive vote of parent Director due to appointment in a position in the parent Director nominated by the parent or a subsidiary thereof

IFRS

Identifying a SUBSIDIARY

Identifying a Subsidiary - IFRS

n A subsidiary is an entity that is controlled by another entity known as parent

n Control is defined as:q the power to govern the financial and operating policies

of an entity q so as to obtain benefits from its activities

Identifying a Subsidiary - IFRS

§ Financial policiesú Capital expendituresú Budget approvalsú Dividend policiesú Capital Structuring

§ Operating policiesú Marketing and Salesú Manufacturingú Human Resourcesú Acquisitions and Mergers

Identifying a Subsidiary - IFRS

§ Can veto rights negate apparent power ?§ holding of veto rights may negate apparent power

if those rights are participative and not protective i.e. has ability to block actions if:ú Those veto rights relate to operating and financial

policies; andú Those veto rights relate to decisions in the ordinary

course of business and not only to fundamental changes in the organization such as disposal of business units or acquisitions of significant assets

Identifying a Subsidiary - IFRS

n Control is presumed to exist when the parent owns, directly or indirectly through subsidiaries, more than half of the voting power of an entity

n But a rebuttable presumption

Identifying a Subsidiary - IFRS

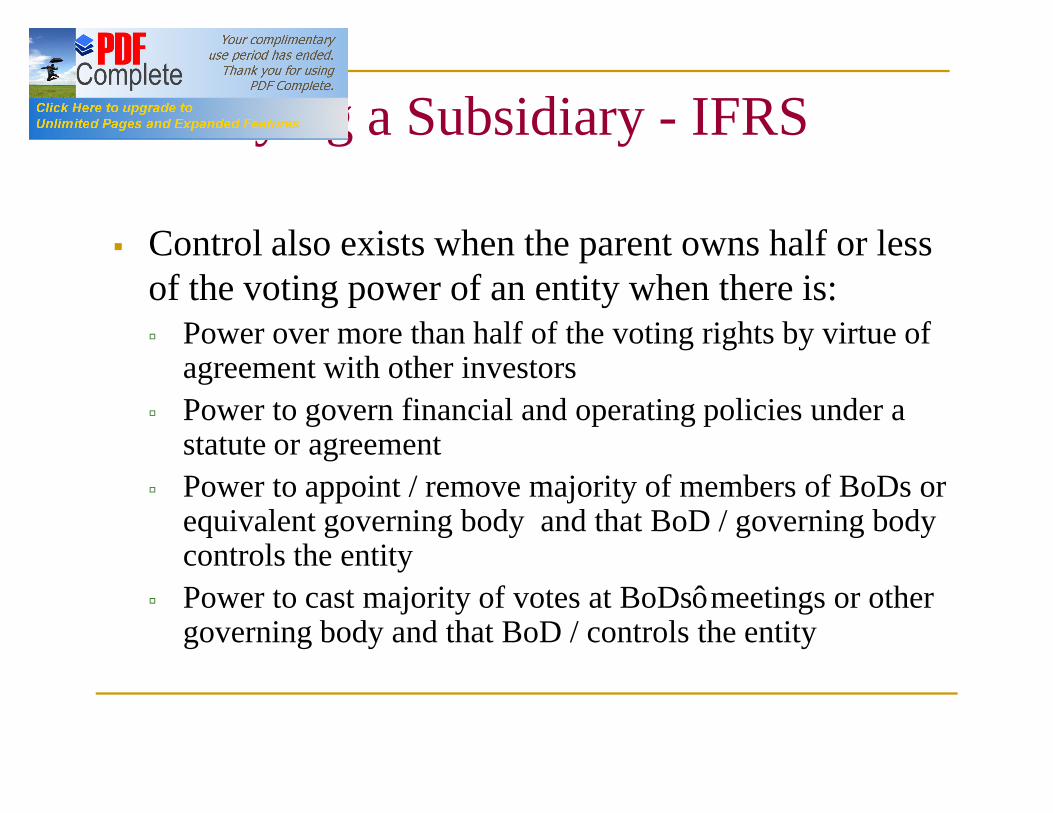

§ Control also exists when the parent owns half or less of the voting power of an entity when there is:ú Power over more than half of the voting rights by virtue of

agreement with other investorsú Power to govern financial and operating policies under a

statute or agreementú Power to appoint / remove majority of members of BoDs or

equivalent governing body and that BoD / governing body controls the entity

ú Power to cast majority of votes at BoDs’ meetings or other governing body and that BoD / controls the entity

Identifying a Subsidiary - IFRS

n Nature of Controlq Direct Controlq Indirect Controlq Passive Controlq De-facto Controlq Potential Voting Rightsq Special Purpose Entity

IFRSDirect Control

Identifying a subsidiary

Identifying a Subsidiary - IFRS

n Direct Control n Illustration:q Entity H holds 60% of voting power and controls entity

S.q Entity S a subsidiary of entity H.

IFRSIndirect Control

IDENTIFYING A SUBSIDIARY

Identifying a Subsidiary - IFRS

§ Indirect Control§ Illustration – through subsidiary:ú Entity P holds 60% of voting power and controls entity

N. Entity N holds 60% of voting power and controls entity B.

ú Is entity B a subsidiary of entity P?

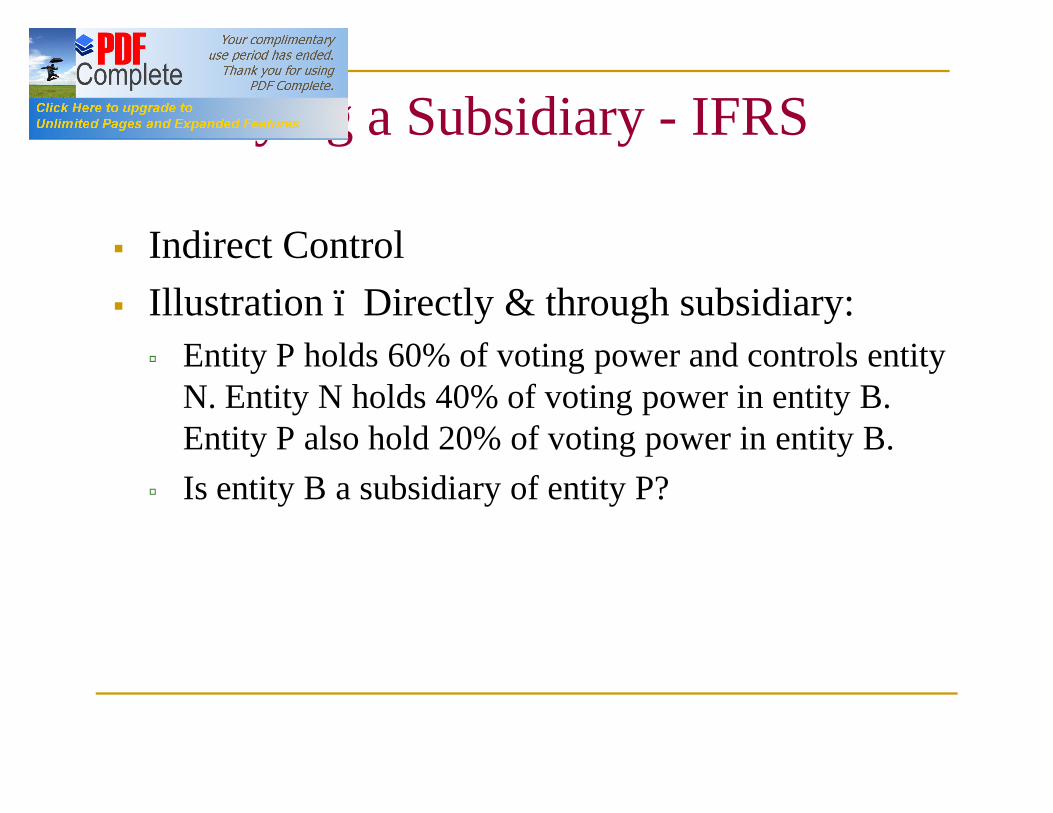

Identifying a Subsidiary - IFRS

§ Indirect Control§ Illustration – Directly & through subsidiary:ú Entity P holds 60% of voting power and controls entity

N. Entity N holds 40% of voting power in entity B. Entity P also hold 20% of voting power in entity B.

ú Is entity B a subsidiary of entity P?

Identifying a Subsidiary - IFRS

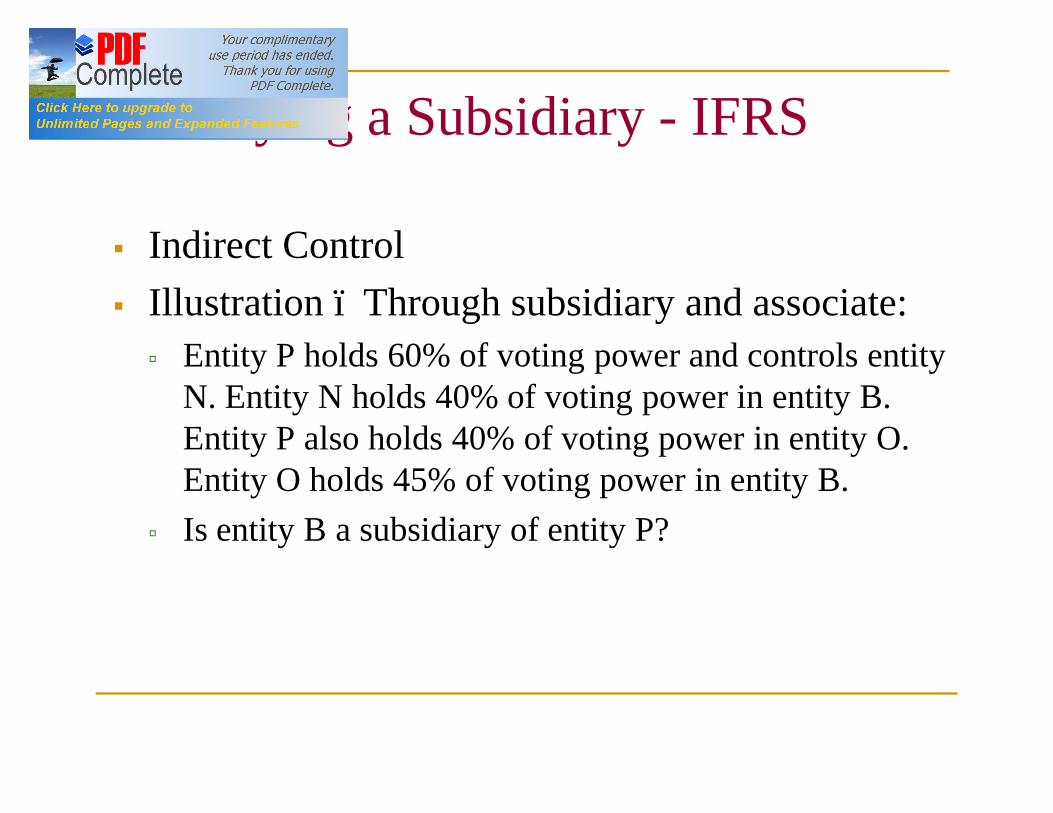

§ Indirect Control§ Illustration – Through subsidiary and associate:ú Entity P holds 60% of voting power and controls entity

N. Entity N holds 40% of voting power in entity B. Entity P also holds 40% of voting power in entity O. Entity O holds 45% of voting power in entity B.

ú Is entity B a subsidiary of entity P?

IFRSPassive Control

IDENTIFYING A SUBSIDIARY

Identifying a Subsidiary - IFRS

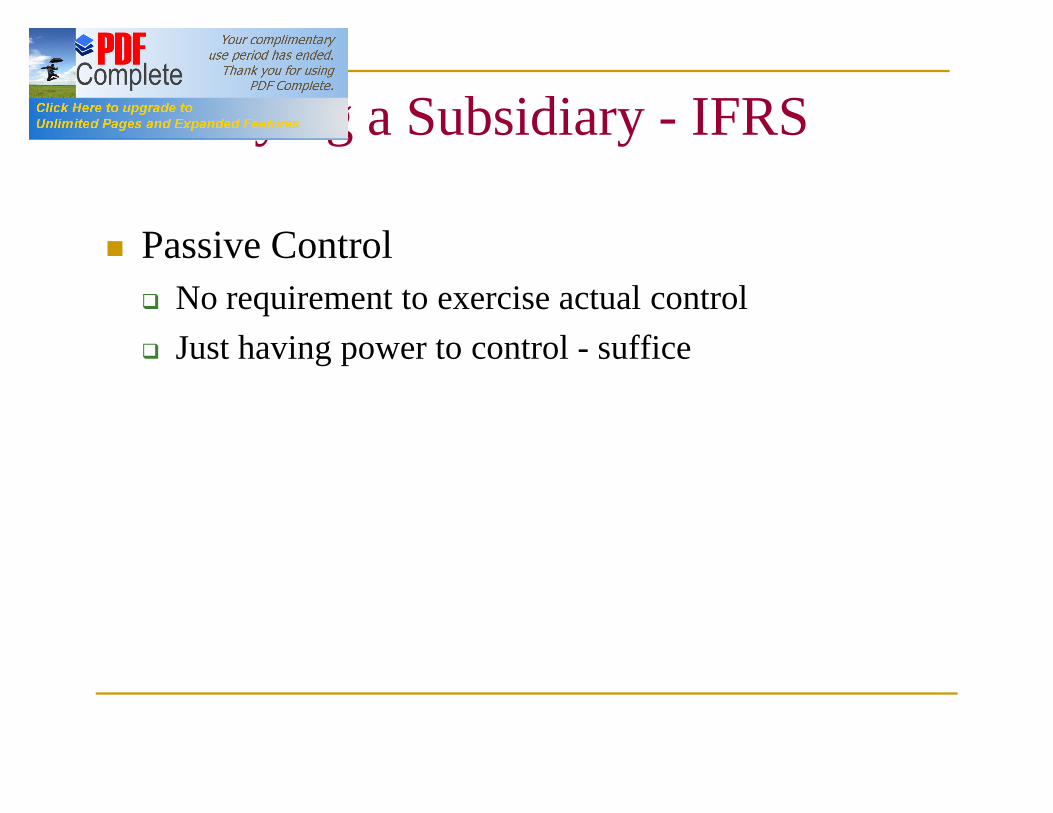

n Passive Controlq No requirement to exercise actual controlq Just having power to control - suffice

Identifying a Subsidiary - IFRS

§ Passive Control§ Example 1: Passive government influenceú A government has a controlling shareholding in a company,

has board representation and is able to cast a majority vote,but in practice permits the other shareholder to govern theentity’s operating and financial policies. The governmentelects to be passive, voting consistently with the othershareholder and appearing only to intervene wherenecessary to protect the national interest?

ú Is the Company under the control of government?

Identifying a Subsidiary - IFRS

n Passive Controln Example 2: Passive shareholdingq Entity A has control over the composition of entity C’s

board, which has seven members; four appointed byentity A and three appointed by a third entity, entity B.One of the entity A’s directors rarely attends boardmeetings and strategic decisions are generally made bymajority vote of the remaining members.

q Is entity C under the control of entity A?

IFRSDe-facto Control

IDENTIFYING A SUBSIDIARY

Identifying a Subsidiary - IFRS

n De-facto Control: q De facto control describes the situation where an entity

owns less than 50% of the voting shares in anotherentity, but is deemed to have control for reasons otherthan potential voting rights, contract or other statutorymeans.

q A company that decides to consolidate on the basis ofdefacto control must define its policy such that thepolicy can be applied consistently.

Identifying a Subsidiary - IFRS

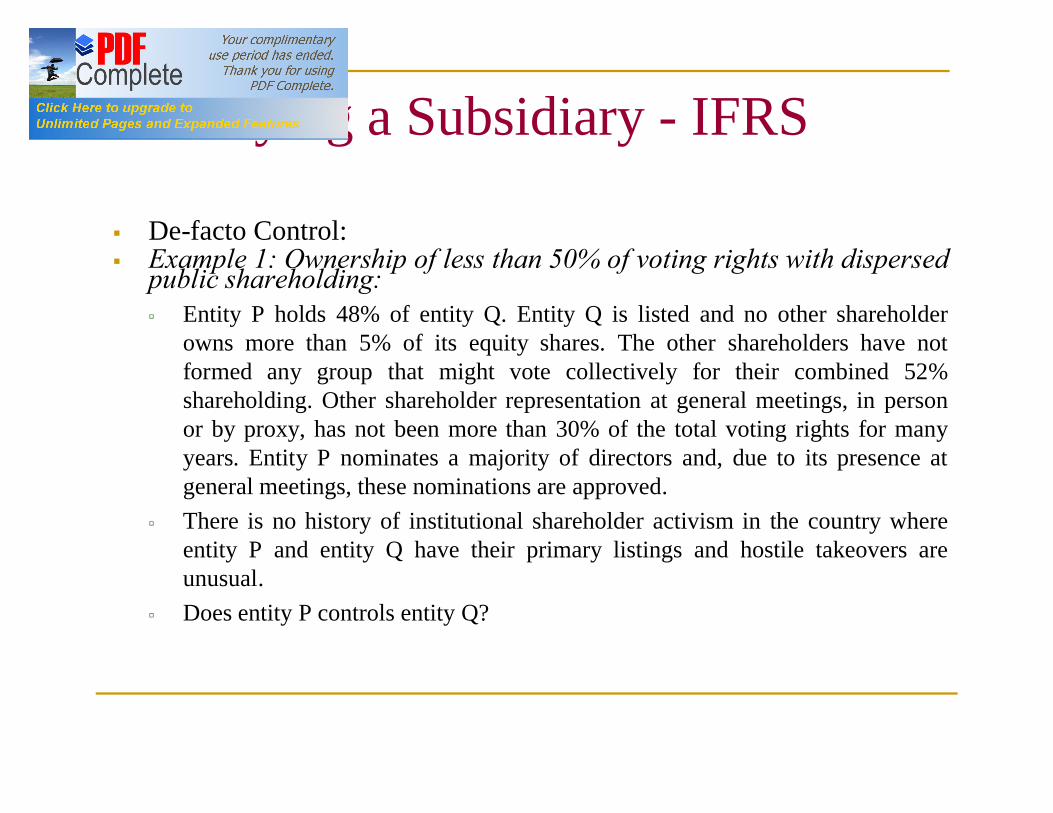

§ De-facto Control:§ Example 1: Ownership of less than 50% of voting rights with dispersed

public shareholding:ú Entity P holds 48% of entity Q. Entity Q is listed and no other shareholder

owns more than 5% of its equity shares. The other shareholders have notformed any group that might vote collectively for their combined 52%shareholding. Other shareholder representation at general meetings, in personor by proxy, has not been more than 30% of the total voting rights for manyyears. Entity P nominates a majority of directors and, due to its presence atgeneral meetings, these nominations are approved.

ú There is no history of institutional shareholder activism in the country whereentity P and entity Q have their primary listings and hostile takeovers areunusual.

ú Does entity P controls entity Q?

Identifying a Subsidiary - IFRS

n De-facto Control:n Example 2: Passive majority shareholder:q Entity R owns 40% of the equity share capital of entity

S. The remaining 60% is owned by a single investor.That investor does not attend general meetings.

q Does entity R controls entity S?

Identifying a Subsidiary - IFRS

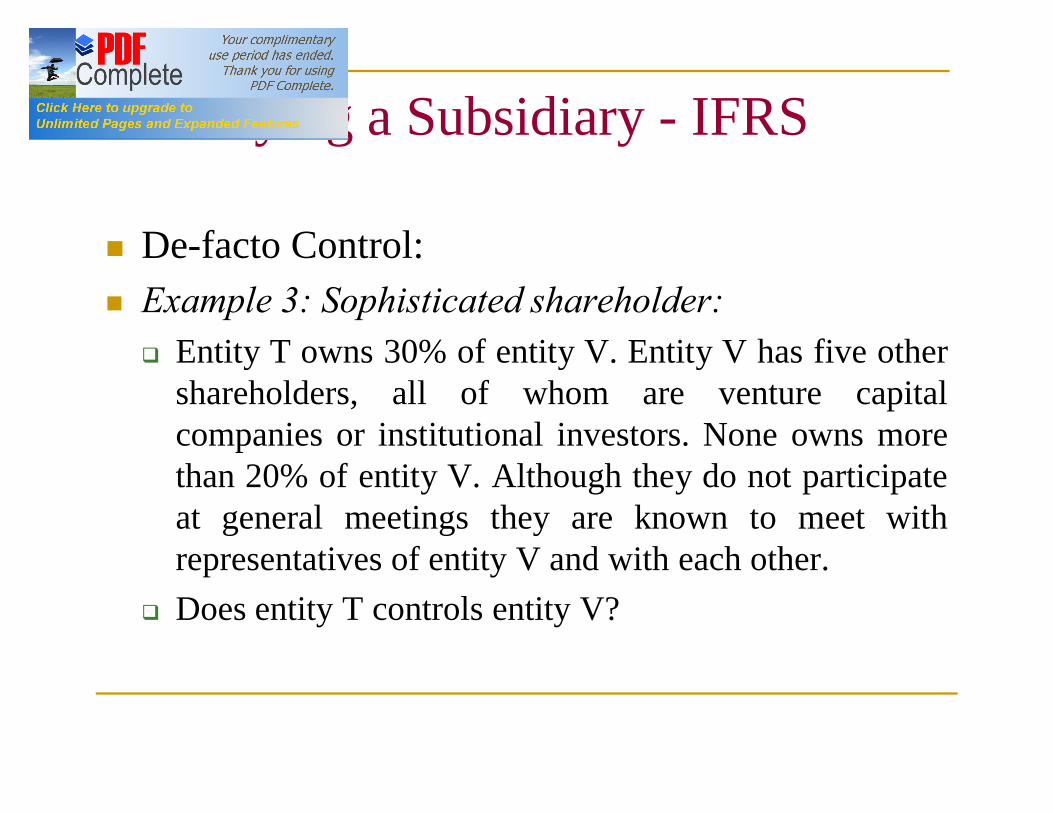

n De-facto Control:n Example 3: Sophisticated shareholder:q Entity T owns 30% of entity V. Entity V has five other

shareholders, all of whom are venture capitalcompanies or institutional investors. None owns morethan 20% of entity V. Although they do not participateat general meetings they are known to meet withrepresentatives of entity V and with each other.

q Does entity T controls entity V?

Identifying a Subsidiary - IFRS

§ De-facto Control:§ Example 4: Temporary shareholding at general meeting:

ú Entity W has the following ownership structure: Entity X : 35% Entity Y : 40% Various small shareholders : 25%

ú Entity Y and a majority of the small shareholders have attendedand voted at past general meetings. At entity W’s most recentgeneral meeting entity Y did not vote and entity X had sufficientvotes to elect three directors to the board of nine, being all of theboard members that were put forward for election in the currentyear. All other matters put to a vote of the shareholders were forroutine business and the proposals of executive managementwere carried.

ú Does entity Y controls entity W?

IFRSPotential Voting Rights

IDENTIFYING A SUBSIDIARY

Identifying a Subsidiary - IFRS

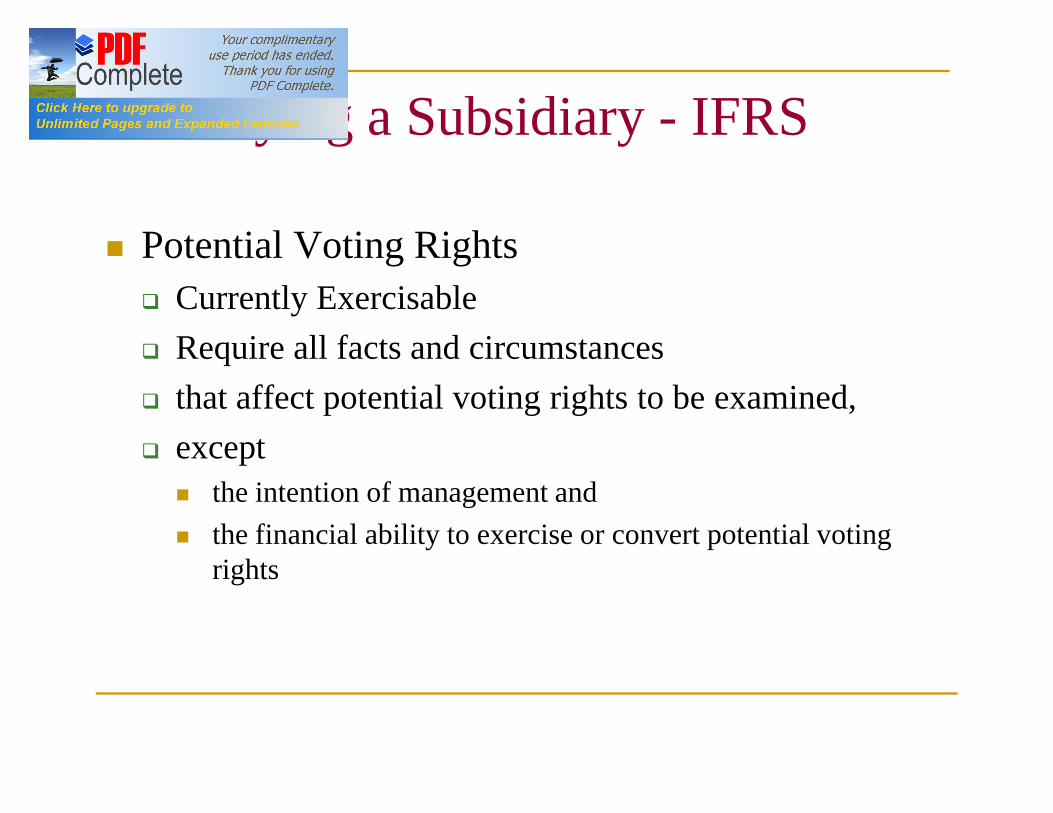

n Potential Voting Rightsq Currently Exercisable q Require all facts and circumstances q that affect potential voting rights to be examined, q except n the intention of management and n the financial ability to exercise or convert potential voting

rights

Identifying a Subsidiary - IFRS

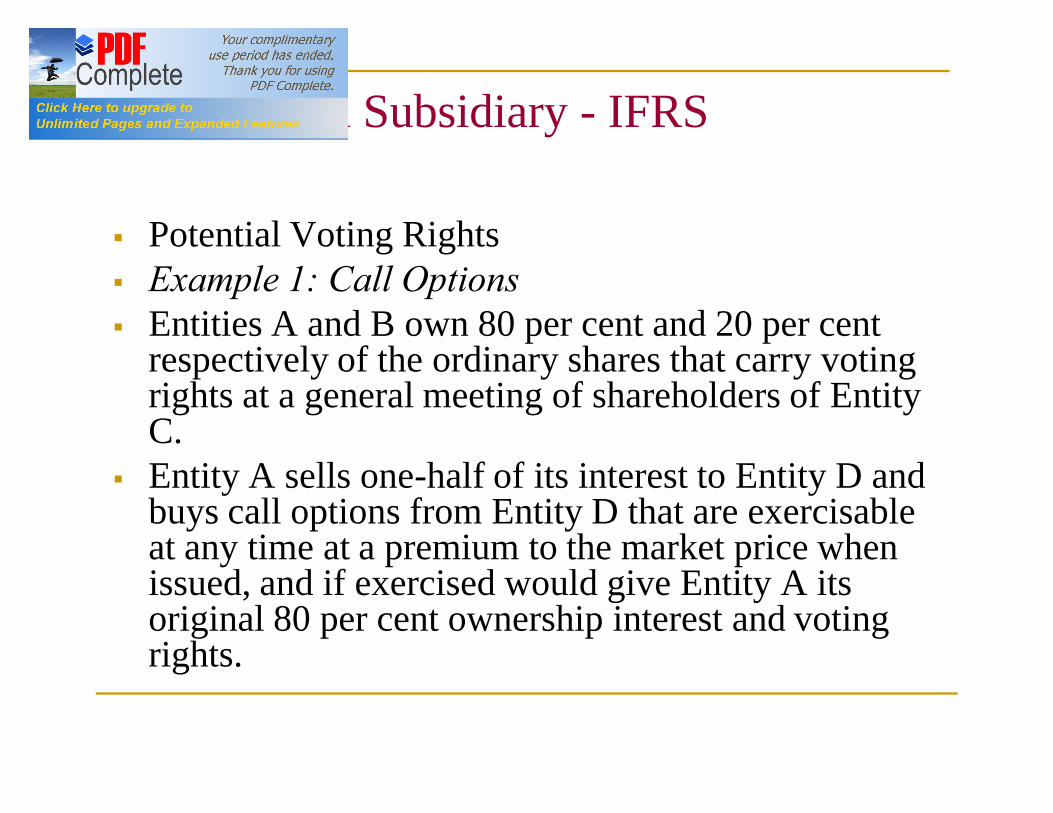

§ Potential Voting Rights§ Example 1: Call Options § Entities A and B own 80 per cent and 20 per cent

respectively of the ordinary shares that carry voting rights at a general meeting of shareholders of Entity C.

§ Entity A sells one-half of its interest to Entity D and buys call options from Entity D that are exercisable at any time at a premium to the market price when issued, and if exercised would give Entity A its original 80 per cent ownership interest and voting rights.

Identifying a Subsidiary - IFRS

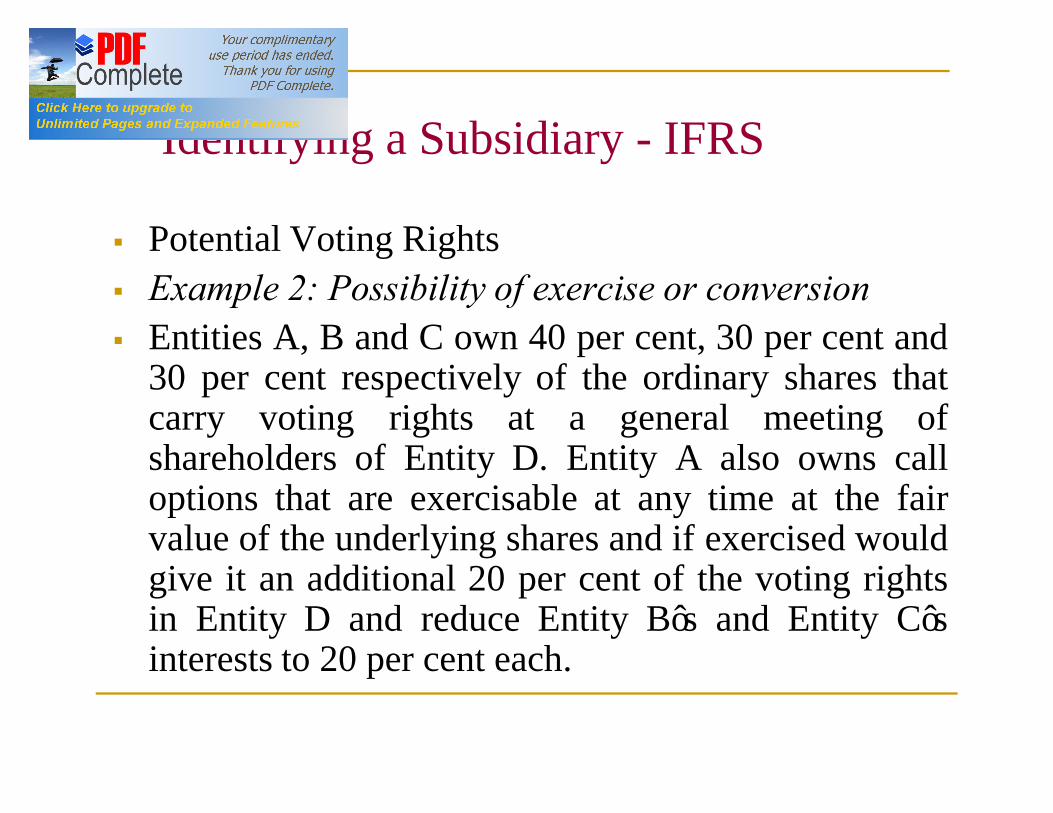

§ Potential Voting Rights§ Example 2: Possibility of exercise or conversion§ Entities A, B and C own 40 per cent, 30 per cent and

30 per cent respectively of the ordinary shares thatcarry voting rights at a general meeting ofshareholders of Entity D. Entity A also owns calloptions that are exercisable at any time at the fairvalue of the underlying shares and if exercised wouldgive it an additional 20 per cent of the voting rightsin Entity D and reduce Entity B’s and Entity C’sinterests to 20 per cent each.

Identifying a Subsidiary - IFRS

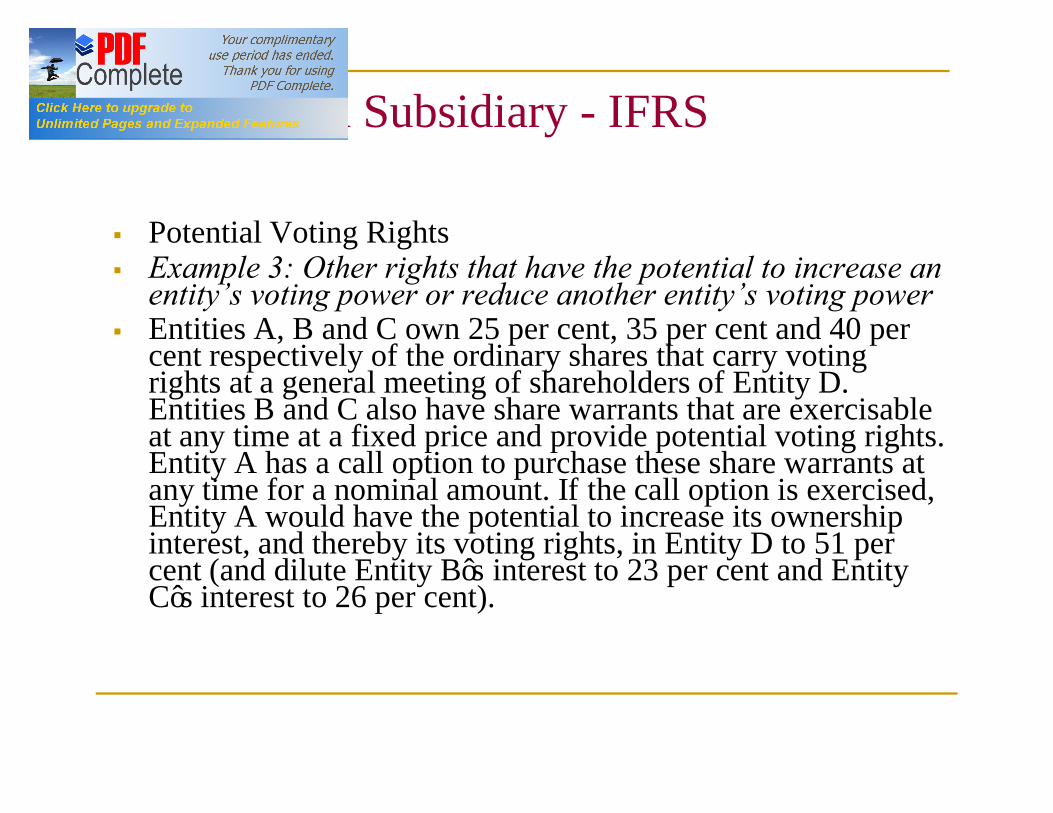

§ Potential Voting Rights§ Example 3: Other rights that have the potential to increase an

entity’s voting power or reduce another entity’s voting power§ Entities A, B and C own 25 per cent, 35 per cent and 40 per

cent respectively of the ordinary shares that carry voting rights at a general meeting of shareholders of Entity D. Entities B and C also have share warrants that are exercisable at any time at a fixed price and provide potential voting rights. Entity A has a call option to purchase these share warrants at any time for a nominal amount. If the call option is exercised, Entity A would have the potential to increase its ownership interest, and thereby its voting rights, in Entity D to 51 per cent (and dilute Entity B’s interest to 23 per cent and Entity C’s interest to 26 per cent).

Identifying a Subsidiary - IFRS

§ Potential Voting Rights§ Example 4: Management intention§ Entities A, B and C each own 33 per cent of the

ordinary shares that carry voting rights at a generalmeeting of shareholders of Entity D. Entities A, Band C each have the right to appoint two directors tothe board of Entity D. Entity A also owns calloptions that are exercisable at a fixed price at anytime and if exercised would give it all the votingrights in Entity D. The management of Entity A doesnot intend to exercise the call options, even if EntitiesB and C do not vote in the same manner as Entity A.

Identifying a Subsidiary - IFRS

§ Potential Voting Rights § Example 5: Financial ability§ Entities A and B own 55 per cent and 45 per cent

respectively of the ordinary shares that carry votingrights at a general meeting of shareholders of Entity C.Entity B also holds debt instruments that are convertibleinto ordinary shares of Entity C. The debt can beconverted at a substantial price, in comparison withEntity B’s net assets, at any time and if converted wouldrequire Entity B to borrow additional funds to make thepayment. If the debt were to be converted, Entity Bwould hold 70 per cent of the voting rights and EntityA’s interest would reduce to 30 per cent.

IFRSSpecial Purpose Entity’s (SIC 12)

IDENTIFYING A SUBSIDIARY

Identifying a Subsidiary - IFRS

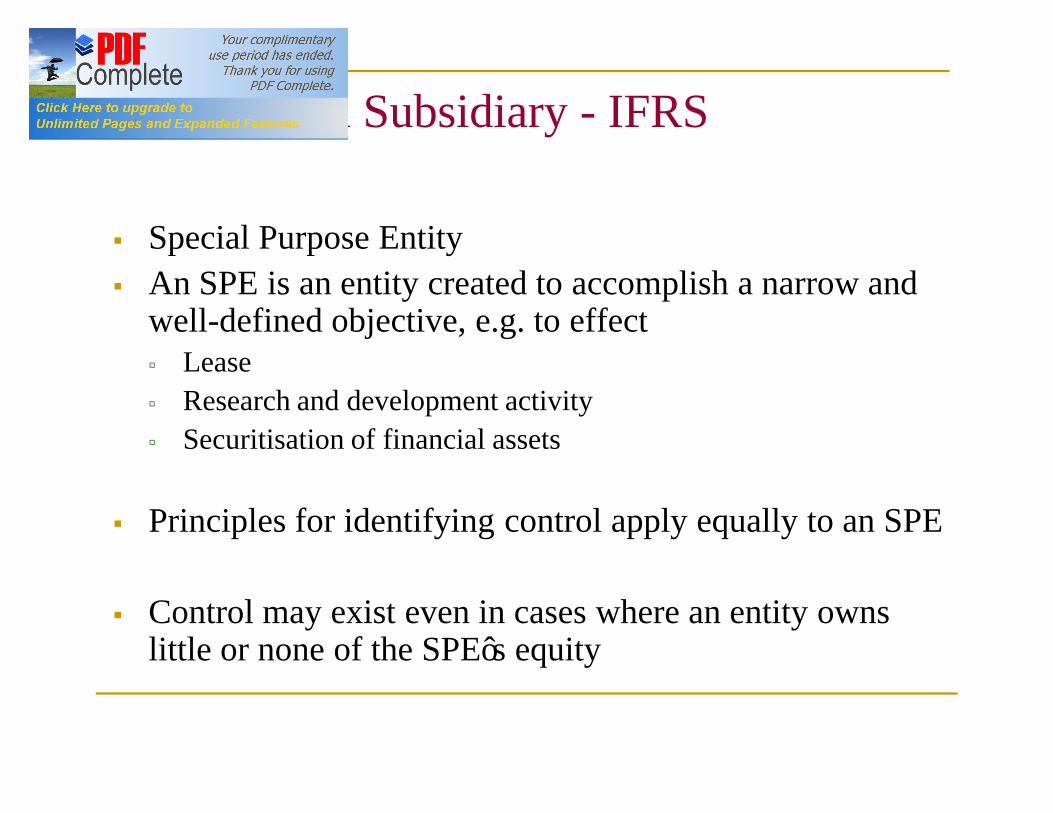

§ Special Purpose Entity§ An SPE is an entity created to accomplish a narrow and

well-defined objective, e.g. to effectú Leaseú Research and development activityú Securitisation of financial assets

§ Principles for identifying control apply equally to an SPE

§ Control may exist even in cases where an entity owns little or none of the SPE’s equity

Identifying a Subsidiary - IFRS

§ SPE’s – Features:ú Auto-pilot arrangements that restrict the decision-making

capacity of the governing boardú Use of professional directors, trustees or partnersú Thin capitalization, the proportion of ‘real equity’ is too

small to support the SPE’s overall activitiesú Absence of an apparent profit-making motive, such that the

SPE is engineered to pay out all profits in the form of interest or fees

ú Domiciled in ‘offshore’ capital havensú Have a specified lifeú Exist for financial purposes

Identifying a Subsidiary - IFRS

§ SPE’s – Indicators of control§ Activities

ú conducted on behalf of reporting entity, which created the SPE according to its business needs

§ Decision-making ú reporting entity has the decision-making powers to control the SPE or its

assets/ may have been delegated these powers by establishing an 'autopilot' mechanism.

§ Benefitsú reporting entity has rights to obtain a majority of the benefits of the SPE's

through a statute, contract, agreement, or trust deed, or any other scheme, arrangement or device.

§ Risksú reporting entity guarantees a return or credit protection directly or indirectly

through the SPE to outside investors and retains residual or ownership risks.

Associate

nAn associates is an entity, including an unincorporated entity such as a partnership over which the investor has significant influence and that is neither a subsidiary nor an interest in a joint venture.

nSignificant influence is the power to participate in the financial and operating policy decisions of the associate but is not control or joint control over those policies

iGAAP – AS 23 IFRS – IAS 28§ An associate is an enterprise

in which the investor has significant influence and which is neither a subsidiary nor a joint venture of the investor

§ Significant influence is the power to participate in the financial and / or operating policy decisions of the investee but not control over those policies.

§ An associate is an entity over which the investor has significant influence and that is neither a subsidiary nor an interest in a joint venture.

§ Significant influence is the power to participate in the financial and operating policy decisions of the investee but is not control or joint control over those policies.

Identifying an Associate

Identifying an Associate

§ Rebuttable presumption: 20% or more of voting power

§ Indicatorsú Representation on board of directorsú Participation in policy-making processú Material transactions between investor and investeeú Interchange of managerial personnelú Provision of essential technical information

§ Potential voting rights included

Accounting for Associate Consolidated Financial Statements

Must apply the equity methodExcept when:

-Investee classified as held for sale (IFRS 5)

-Exemption applies - the parent itself a subsidiary of another entity and its other owners do not object / not traded / not filing to public market / IFRS statements are reported by parent

Equity Method§ The equity method is a method of accounting whereby theinvestment is initially recognized at cost and adjustedthereafter for the post-acquisition change in the investor’sshare of net assets of the investee.§The profit or loss of the investor includes the investor’sshare of the profit or loss of the investee..§Distribution received from the Investee is reduced thecarrying amount of the investment.§Investor’s share of profit or loss is adjusted for the effect ofany fair value differences recognised on acquisition of theassociate ( e.g. Depreciation on incremental fair value ofassets)

Equity Methodn On acquisition of the investment any difference between the

cost of the investment and the investor’s share of the net fairvalue of the associate’s identifiable assets and liabilities isaccounted for asq (a) goodwill relating to an associate is included in the carrying amount

of the investment. Amortisation of that goodwill is not permitted.q (b) any excess of the investor’s share of the net fair value of the

associate’s identifiable assets and liabilities over the cost of theinvestment is included as income in the determination of the investor’sshare of the associate’s profit or loss in the period in which theinvestment is acquired. (treated as capital reserve in Ind AS)

n If an investor’s share of losses of an associate equals orexceeds its interest in the associates, the investor discontinuesrecognising its share of further losses

Impairment Lossesn After application of the equity method,

including recognising the associate’s losses,the investor applies the requirements of IAS-39 to determine whether it is necessary torecognise any additional impairment loss withrespect to the investor’s net investment in theassociate

iGAAP – AS 27 IFRS – IAS 31§ A joint venture is a

contractual arrangement whereby two or more parties undertake an economic activity which is subject to joint control.

§ Joint control is the contractually agreed sharing of control over an economic activity.

.

§ A joint venture is a contractual arrangement whereby two or more parties undertake an economic activity that is subject to joint control.

§ Joint control is the contractuallyagreed sharing of control over an economic activity, and exists only when the strategic financial and operating decisions relating to the activity require the unanimous consent of the parties sharing control.

Identifying a Joint Venture

IAS - 31Forms of Joint Venture

§Jointly controlled operations§ Jointly controlled assets§ Jointly controlled entities

DefinitionJointly Controlled Operations

Involve use of assets and other resources of the venturer rather than the establishment of a separate entity. Each venturer uses its owns assets and resources . The sale of joint product and expenses are shared by venturers through a contractual arrangement . Example : Air Craft manufacturing , Marketing , Research.

AccountingJointly Controlled Operations

A venturer shall recognize -§ The assets that it controls and the liabilities that it

incurs; and§ The expenses that it incurs and its share of the

income that it earns from the sale of goods or services by the joint venture

§ The above transactions are recorded in the financial statements of the venturer hence no consolidation are required.

DefinitionJointly Controlled Assets

Involve the joint control, and often the jointownership, of the assets dedicated to the joint venture.Each joint venturer may take a share of the outputfrom the assets and each bears a share of the expenseincurred.These ventures does not involve establishment of aseparate entity. Example : Oil and Gas pipeline orMineral Extraction

Accounting

Jointly Controlled Assets

A venturer shall recognize§ Its share of the jointly controlled assets, as per the nature§ Its share of any liabilities incurred§ Any income from the sale or use of its share of the output of

the joint venture§ Any expenses that it has incurred in respect of its interest in

the joint venture.§ The above transactions are recorded in the financial

statements of the venturer hence no consolidation are required.

Definition

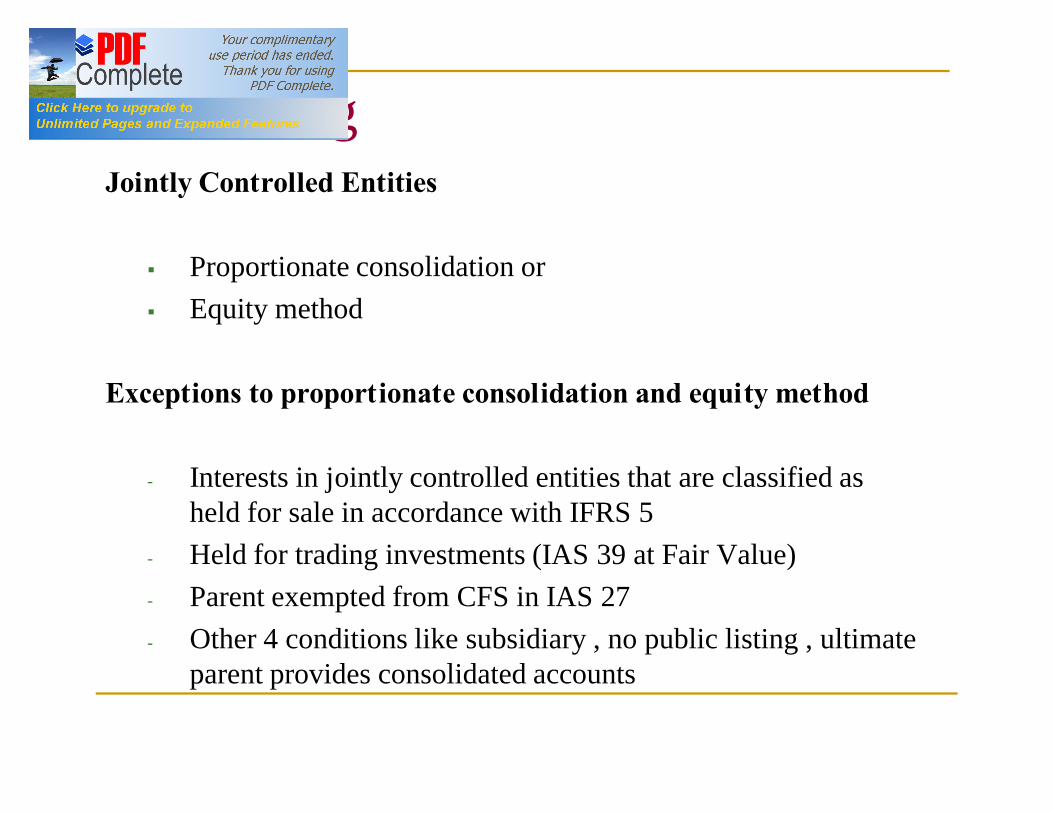

Jointly Controlled Entities

A corporation, partnership or any other entity in which two or more venturers have an interest, under a contractual agreement that establishes joint control over the entity

AccountingJointly Controlled Entities

§ Proportionate consolidation or§ Equity method

Exceptions to proportionate consolidation and equity method

- Interests in jointly controlled entities that are classified as held for sale in accordance with IFRS 5

- Held for trading investments (IAS 39 at Fair Value)- Parent exempted from CFS in IAS 27- Other 4 conditions like subsidiary , no public listing , ultimate

parent provides consolidated accounts

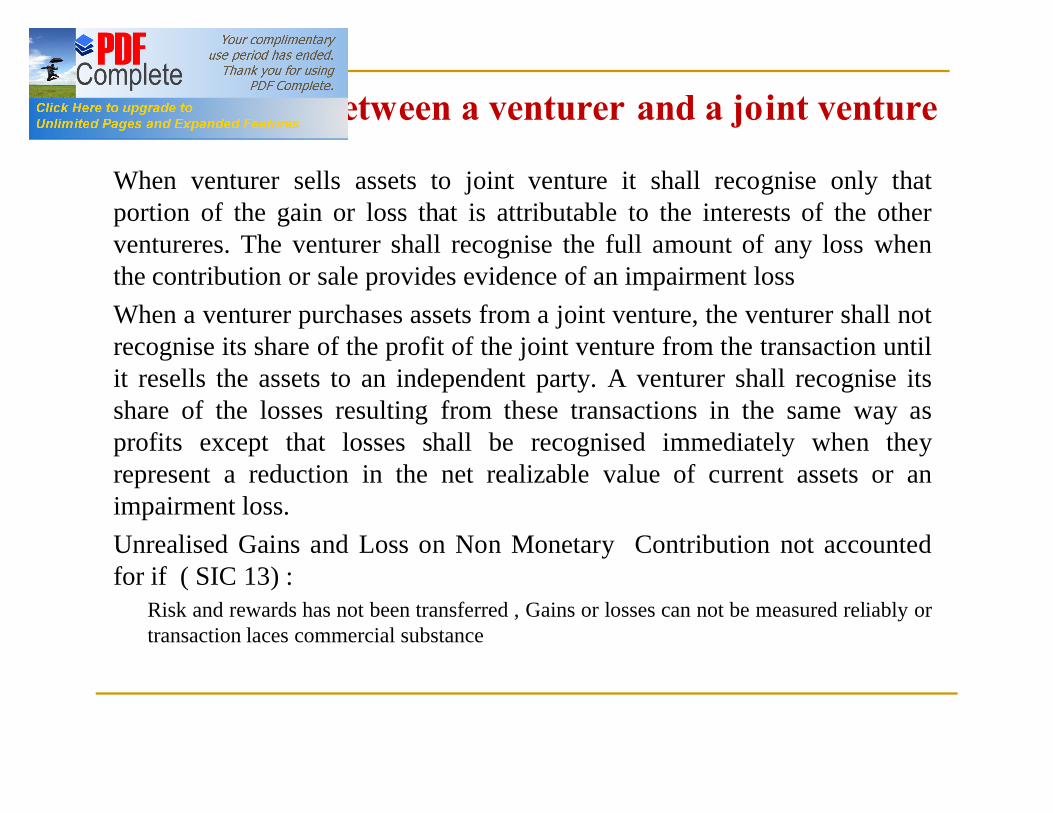

Transactions between a venturer and a joint venture

When venturer sells assets to joint venture it shall recognise only thatportion of the gain or loss that is attributable to the interests of the otherventureres. The venturer shall recognise the full amount of any loss whenthe contribution or sale provides evidence of an impairment lossWhen a venturer purchases assets from a joint venture, the venturer shall notrecognise its share of the profit of the joint venture from the transaction untilit resells the assets to an independent party. A venturer shall recognise itsshare of the losses resulting from these transactions in the same way asprofits except that losses shall be recognised immediately when theyrepresent a reduction in the net realizable value of current assets or animpairment loss.Unrealised Gains and Loss on Non Monetary Contribution not accountedfor if ( SIC 13) :

Risk and rewards has not been transferred , Gains or losses can not be measured reliably ortransaction laces commercial substance

Presentation of Consolidated Financial Statements

§ iGAAPú Not mandatory to produce CFSú Listing Agreement requires listed companies to produce CFSú Exclusions: Subsidiaries acquired for subsequent disposals Subsidiaries operating under severe long-term restrictions which significantly

impair their ability to transfer funds to parent§ IFRS

ú Requires a parent to prepare CFSú Unless exempted – all 4 conditions to be satisfied (no such exemption

in Ind AS) Parent itself is a subsidiary; owners do not object Debts / equity instruments not listed Did not file / nor in the process of getting listed Ultimate / intermediary parent produces IFRS complied CFS

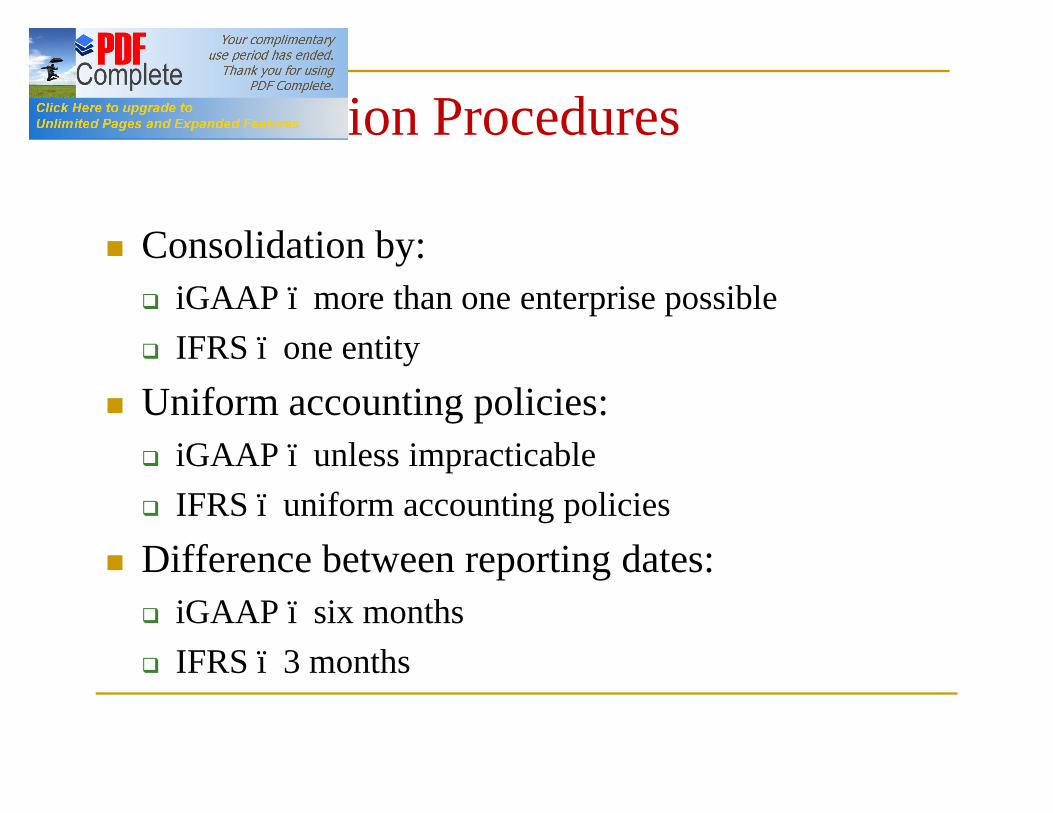

Consolidation Procedures

n Consolidation by:q iGAAP – more than one enterprise possibleq IFRS – one entity

n Uniform accounting policies:q iGAAP – unless impracticableq IFRS – uniform accounting policies

n Difference between reporting dates:q iGAAP – six monthsq IFRS – 3 months

Consolidation Procedure§ The carrying amount of the parent’s investment in each subsidiary and the parent’s

portion of equity of each subsidiaries are eliminated resulting in resultant Goodwill (in accordance with IFRS 3).

q Income Statementq Inter Company transaction :

§ Inter-Company Purchases; Inter-Company Dividends; Inter-Company Interest

§ Elimination of Unrealised Profit on stockq IAS 12 Income Tax Applies to temporary differences arising from elimination of

profit and loss from the intergroup transactions.

q Balance Sheetq Inter-company loans; Inter-company receivables/payables; Shares in subsidiaries/pre-

acquisition reserves.

Portion of the profit or loss and net assets of asubsidiary attributable to equity interests that are notowned, directly or indirectly through subsidiaries, bythe parent.

Non-Controlling Interest

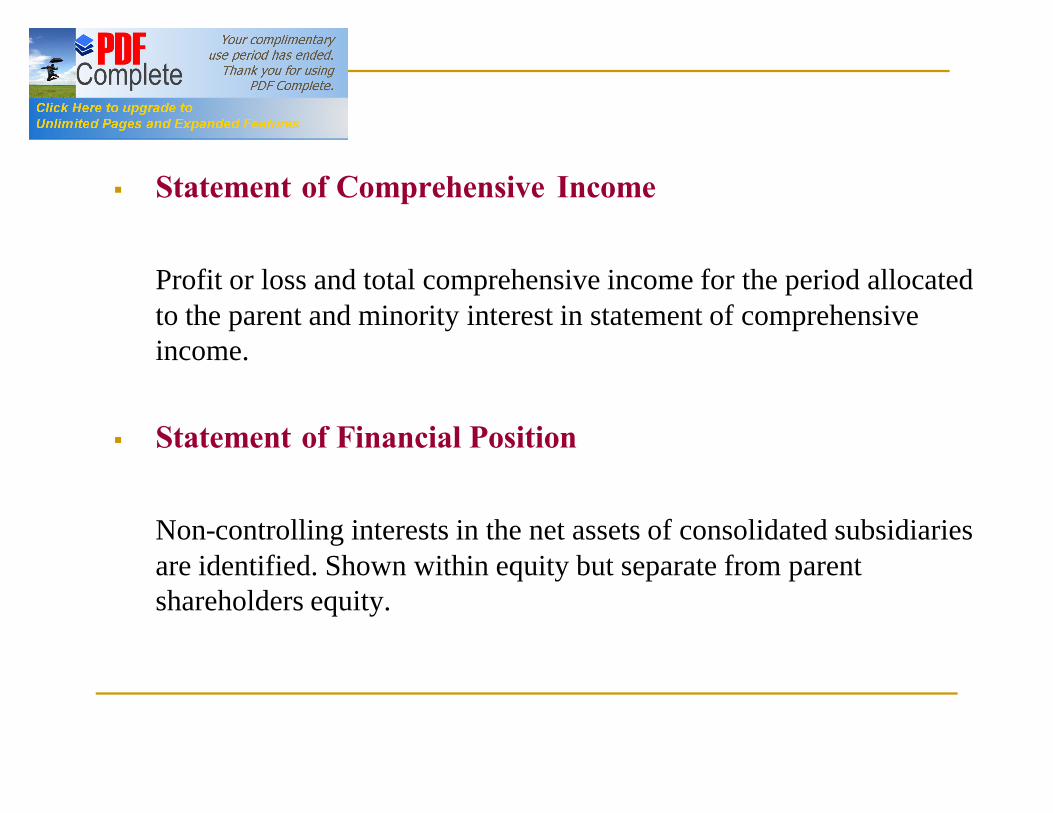

§ Statement of Comprehensive Income

Profit or loss and total comprehensive income for the period allocated to the parent and minority interest in statement of comprehensive income.

§ Statement of Financial Position

Non-controlling interests in the net assets of consolidated subsidiaries are identified. Shown within equity but separate from parent shareholders equity.

Changes in Parent’s Ownership

Scenario 1- Not Losing Control

Changes in parent’s ownership interest in a subsidiary that do not result in a loss of control are accounted for as equity transactions (i.e. transactions with owners in their capacity as owners).

Changes in Parent’s Ownership

Scenario 2- Losing Control

When a parent company losses control over the subsidiary, accounting impact has to given at various levels.

qDe-recognize the assets (including any goodwill) and liabilities of the subsidiary at their carrying amounts at the date when control is lost.qDe-recognize the carrying amount of any non-controlling interests in the former subsidiary at the date when control is lostqRecognizes the fair value of the consideration received, if any, from the transaction

Loss of control

n recognises any investment retained in the former subsidiary at its fair value at the date when control is lost;

n reclassifies to profit or loss, or transfers directly to retained earnings/OCI if required in accordance with other IFRSs ;&

n recognises any resulting difference as a gain or loss in profit or loss attributable to the parent.

Loss of controln If a parent loses control of a subsidiary, it shall account for all amounts

recognised in OCI in relation to that subsidiary on the same basis as wouldbe required if the parent had directly disposed of the related assets orliabilities. Thus, if a gain or loss previously recognised in OCI would bereclassified to profit or loss on the disposal of the related assets orliabilities, the parent reclassifies the gain or loss from equity to profit orloss (as a reclassification adjustment) when it loses control of thesubsidiary ,e.g., if a subsidiary has cumulative exchange differencesrelating to a foreign operation and the parent loses control of the subsidiary,the parent shall reclassify to profit or loss the gain or loss previouslyrecognised in OCI in relation to the foreign operation. Similarly, if arevaluation surplus previously recognised in other comprehensive incomewould be transferred directly to retained earnings on the disposal of theasset, the parent transfers the revaluation surplus directly to retainedearnings when it loses control of the subsidiary.

iGAAP IFRS§ Acquired and held

exclusively with a view to its subsequent disposal in the near future

§ The subsidiary / investee / JV operates under the severe long-term restrictions that significantly impair its ability to transfer funds to parent / investor / venturer

n Consolidate but in accordance with IFRS 5

n Consolidate

Exclusions

iGAAP IFRSn Venture capital investors

and similar entitiesq No guidance

§ Venture capital investors and similar entitiesú Subsidiaries – consolidateú However venture capital

investors and similar entities may elect not to apply equity method for investments in associates and instead account for these investments as financial instruments at fair value through profit or loss

Exclusions

Separate financial statements

iGAAP IFRSn As per AS 13

q Accounting for investmentsn At cost; orn In accordance with IAS 39

Separate Financial Statements

Disclosures - Subsidiaries

§ Nature of relationship when parent does not own more than half of the voting power in a subsidiary

§ Reasons why owning more than half of the voting power of an investee does not constitute control

§ Reporting date of the FS of a subsidiary if different from the parent

§ Restrictions on ability of subsidiary to transfer funds to parent

Disclosures - Subsidiaries

n a schedule that shows the effects of any changes in a parent’s ownership interest in a subsidiary that do not result in a loss of control on the equity attributable to owners of the parent;

n if control of a subsidiary is lost, the parent shall disclose the gain or loss, if any and: q (i) the portion of that gain or loss attributable to recognising any

investment retained in the former subsidiary at its fair value at the date when control is lost; and

q (ii) the line item(s) in the statement of comprehensive income in which the gain or loss is recognised (if not presented separately in the statement of comprehensive income).

Disclosures - Associates

§ Fair value of investments when published prices are available

§ Summarised financial information, including the aggregated amounts of assets, liabilities, revenues and profit or loss

§ Reasons why the presumption that an investor does not have significant influence is overcome if the investor holds less than 20% but concludes it has significant influence

§ Reasons why the presumption that an investor has significant influence is overcome if the investor holds 20% or more but concludes it does not have significant influence

Disclosures - Associates

§ Reporting date of the FS of associates (when different from that of the investor) and reasons therefore

§ Any significant restrictions to transfer funds§ Unrecognised share of losses (if discontinued

recognition)§ Fact that associate is not accounted for using the

equity method§ Summarised information of associates not equity

accounted

Disclosures – Joint Ventures

§ Contingent liabilities incurred in connection with JV activities separately from the amount of other contingent liabilities

§ Any capital commitments of the venturer in relation to its interests in JVs and its share in the capital commitments incurred jointly with other venturers

§ Its share of the capital commitments of the JVs themselves§ Accounting policy for jointly controlled entities (JCEs)§ The aggregate current assets and liabilities, long-term assets and

liabilities, income and expenses related to the JCEs (when using line-by-line reporting)

§ List and description of interests in significant JCEs and the proportion of ownership interests held

§ Method used to recognise the interest in Joint Controlled Entity.

Ind AS Carve outs – IAS 28• Paragraph 23 (b) has been modified on the lines of Ind AS 103 to transfer excess of the

investor’s share of the associate’s identifiable assets and liabilities over the cost of investment in capital reserve whereas in IAS 28, it is recognised in profit or loss. (carve out)

• Where the financial statements of an associate used in applying equity method are prepared as of a date different from that of the investor, IAS 28 requires that this difference should not be more than three months. However, paragraph 25 (Ind AS) 28 provides that this difference should not be more than three months, unless impracticable.

• Similarly, paragraph 26 of Ind AS 28 requires use of uniform accounting policies, unless impracticable, which IAS 28 does not provide. These changes have been made because the investor does not have ‘control’ over the associate, it may not be able to influence the associate to prepare additional financial statements or to follow the accounting policies that are followed by the investor. (carve out)

• Exemption from Consolidation has been deleted.

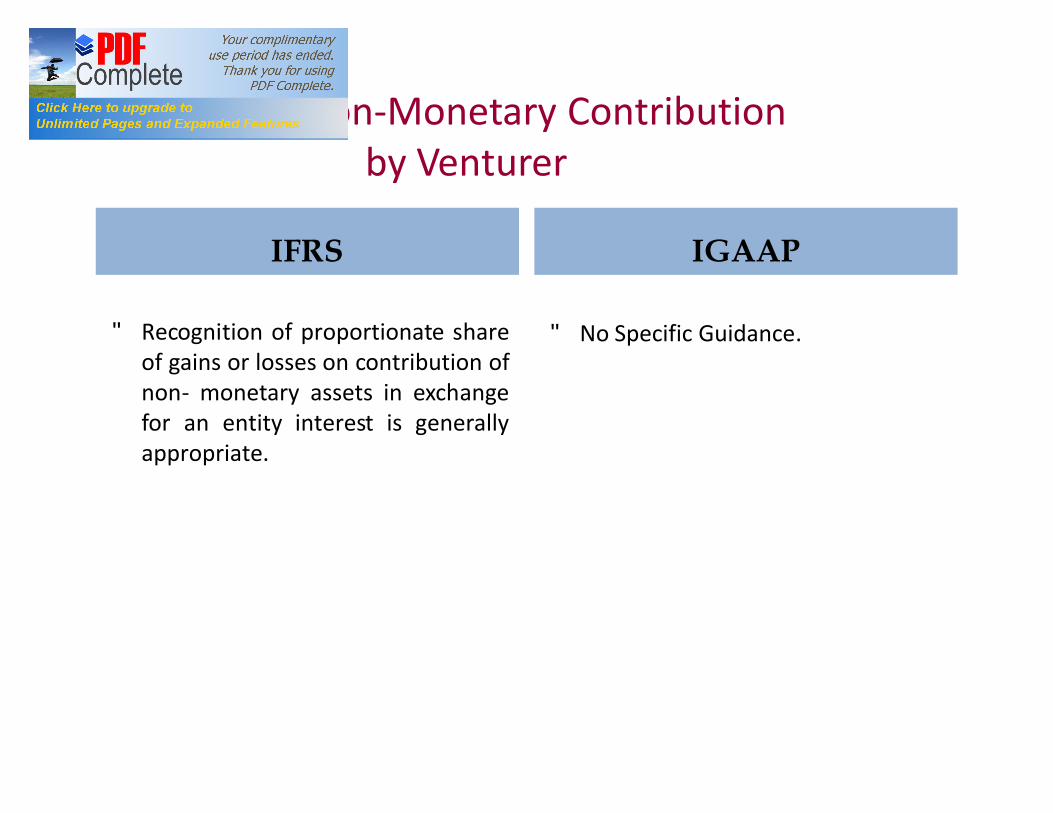

SIC 13 – Non-Monetary Contribution by Venturer

IFRS

• Recognition of proportionate shareof gains or losses on contribution ofnon- monetary assets in exchangefor an entity interest is generallyappropriate.

IGAAP

• No Specific Guidance.