Embed Size (px)

Citation preview

The Effect of 10-K Restatements on Firm Value, Information Asymmetries, and Investors’ Reliance on Earnings

Kirsten L. Anderson Georgetown University

Teri Lombardi Yohn

Georgetown University

Restating 10-Ks has become an increasingly common phenomenon in financial reporting. Restatements clearly signal that the firm’s prior financial statements were not credible and were of relatively lower “quality”. In this study, we examine the effect of restatements on investors’ and dealers’ perceptions of the firm. First, we examine the market returns and the bid-ask spread effects at the announcement of the accounting problem that leads to restatement. We find negative market returns for accounting problem announcements, and we find that the negative reaction is most pronounced for firms with revenue recognition issues. We also find an increase in spreads surrounding the announcement of revenue recognition problems. Second we examine returns and spreads from the announcement of the restatement to the filing of the restated financial statements. We find a significant negative market reaction and a larger negative reaction for firms with revenue recognition problems. We find no change in spreads from before the announcement of the accounting problem to after the restatement is filed. Finally, we examine the effect of the restatement on earnings response coefficients, and find that the market reacts less to earnings after a restatement than to earnings prior to a restatement. In general, these results indicate that investors and dealers react negatively to restatements and are more concerned with revenue recognition problems than with other financial reporting errors.

Kirsten L. Anderson or Teri Lombardi Yohn, McDonough School of Business, Georgetown University, 3700 O Street NW, Washington, DC 20057. Phone: 202-687-3798; Email: [email protected] and [email protected]. We thank Patricia Fairfield, Jeff Harris, Sundaresh Ramnath, discussants at the Eastern Finance Association and American Accounting Association meetings, and participants at Ohio State University, George Washington University, and the Securities Exchange Commission workshops for their helpful comments.

2

I. INTRODUCTION

Investors rely on financial statements for forecasting firms’ future profitability and for

firm valuation. Prior research has shown that financial statement information is used by

investors for firm valuation (e.g. Ball and Brown (1968) and Beaver (1968)) and that accounting

information reduces information asymmetries between firms and the stock market (e.g. Lee,

Mucklow and Ready (1993)). Research has attempted to document that not only the release but

also the quality of financial information affects the stock market. Prior research has attempted to

identify earnings quality by examining earnings components (e.g. Jones (1991), McNichols and

Wilson (1988)), earnings persistence (e.g. DeFond and Park (2001)), and analyst perceptions of

disclosure quality (e.g. Lang and Lundholm (1993)).

In this study, we examine the stock market effect of a firm’s announcement and filing of

restated financial statements due to errors in the statements previously submitted to the Securities

and Exchange Commission (SEC). Unlike estimations of earnings components or analyst

perceptions of earnings quality, restatements clearly signal that the prior financial statements

were not credible and were of relatively lower “quality”. We examine how restatements affect

investors’ perceptions in the stock market. In addition to analyzing the effect of the accounting

restatement on firm value (as in Palmrose, Richardson and Scholz (2001), Wu (2002)1, and

Turner, et al (2001)), we also study the effect of the restatement on information asymmetries in

the stock market and on investors’ reliance on the firm’s future financial statements.

In order to assess the effect of the restatement on firm value, we compute cumulative

abnormal stock returns (CARs) over two time periods. First, we calculate the CAR over the

seven-day period surrounding the restatement announcement. Using this short window, we can

1 Wu (2002) was written contemporaneous to this study. Wu (2002) addresses the same issues that are addressed here; however, the author analyzes restatements of unaudited quarterly financial statements as well as audited annual financial statements. We examine only restatements of audited annual financial statements.

3

assess the immediate impact of the restatement on firm value. Then, we calculate the CAR for

each firm over a longer window, beginning three days before the restatement announcement and

ending three days after the restatement filing with the SEC. After the restatement is filed, all the

initial uncertainty concerning the financial statement effect of the restatement is resolved. By

computing the CARs through the restatement filing date, we can determine the long-term effect

of the restatement on firm value.

We also examine the firm’s bid-ask spreads over both time frames to assess the impact of

restatements on perceived information asymmetries in the stock market. By examining spreads

in the shorter measurement interval, we can determine the temporary (or short-run) changes in

the perceived information asymmetry in the stock market. Calculating the spread changes over

the longer event window allows us to assess the change in the perceived level of information

asymmetry in the market for the firm’s stock after the uncertainty surrounding the effect of the

restatement on the prior financial statements is resolved. Since errors in prior financial

statements may reduce the perceived reliability of future financial statements, information

asymmetry may remain higher even after the restated financial statements are filed with the SEC.

Finally, we compare firms’ earnings response coefficients for annual earnings releases

prior to and subsequent to the restatement to determine the effect of the restatement on the

market’s reliance on the firm’s earnings releases. We expect that investors will rely less on

earnings reports after errors in prior financial statements are revealed than on earnings reports

before errors were made known to the public.

We also examine whether the accounting issue causing the restatement differentially

impacts firm value, information asymmetries and investors’ reliance on future earnings releases.

Specifically, we examine if the market reaction to restatements differs for restatements related to

4

revenue recognition, restructuring, in-process research and development, fraud and other issues.

We hypothesize that revenue recognition and fraud related restatements have a greater impact on

investor perceptions than other restatements. We assert that investors will consider revenue

recognition and fraud issues to be more serious in terms of intent and more fundamental in terms

of the potential implications for future profitability. This assertion is supported by both the

SEC’s Staff Accounting Bulletin 101 (SAB 101) on revenue recognition as well as speeches

made by key SEC employees (e.g. Levitt (1998)).

Consistent with our hypotheses, we find significant negative abnormal stock returns

surrounding the announcement of an accounting problem and an upcoming restatement filing. In

addition, we find the most significant negative reaction to restatement announcements for

revenue recognition issues. We find an increase in spreads around the announcement of an

accounting problem only for restatements related to revenue recognition issues. The results

suggest that revenue recognition restatements affect investor perceptions of firm value and

information asymmetries more than other restatements.

We also find significant negative abnormal returns for the period beginning prior to the

problem announcement and ending after the filing of the restated financial statements. In

addition, we find a larger negative reaction to revenue recognition related restatements than to

other types of restatements. Surprisingly, we find no increase in spreads from before the

announcement of the problem to after the release of restated financial statements. The results

suggest that the increase in information asymmetry around the announcement of a problem is

temporary. Thus, the restatement of financial statements does not result in a permanent increase

in information asymmetry.

5

Finally, we find smaller earnings response coefficients for earnings reported after relative

to prior to the restatement. This suggests that investors rely less on earnings releases after a

restatement than before a restatement, suggesting a decrease in investors’ perceptions about the

reliability of the accounting information. The decrease in the earnings response coefficient does

not, however, appear to be more pronounced for revenue recognition related restatements.

The results of this study are important for future work on how the quality of accounting

information affects the stock market. The results are also important for understanding what

types of accounting problems appear to be of relatively greater concern to investors in the stock

market. The results suggest that investors appear to be most concerned about restatements

related to revenue recognition. This focus on revenue recognition issues by the market and

dealer appears to mirror the SEC’s focus on the same issue. While the revenue recognition

results are consistent with the focus by the SEC on revenue recognition policies, it would be

useful to obtain more insight into the differences in revenue recognition related restatements

relative to restatements related to expense items. Future research could examine this issue.

The next section of the paper provides our hypothesis development. Section III provides

descriptive statistics on the sample, while section IV reports the regression results. Section V

concludes the paper.

II. HYPOTHESES DEVELOPMENT

An announcement of a restatement informs investors that prior financial statements

contain errors. We expect this discovery of errors in financial statements to affect firm value, the

perceived level of information asymmetry in the market for the firm’s stock, and the perceived

reliability of future earnings reports.

6

We hypothesize that the announcement of a restatement affects investors’ perceptions of

firm value in two ways. First, the impact of the restatement on the firm’s past financial

statements should change investors’ perceptions of current and future profitability and therefore

firm value. Second, the existence of a restatement may create uncertainty regarding the

reliability of the firm’s current and future financial statements. This uncertainty is likely to

persist after the filing of the restatement with the SEC, causing lower returns for a longer period

of time than just the time period surrounding the announcement.

We argue that investors’ concerns about the reliability of current and future financial

statements is likely to be more pronounced for restatements related to fraud and revenue

recognition. Fraud suggests that the firm was intentionally misleading investors. Revenue

recognition issues may also be perceived by investors to be more intentional than restatements

related to expense items. Lynn Turner, former chairman of the SEC, stated that firms appear to

manage earnings through the manipulation of revenue recognition. In fact, a 1999 report on

fraudulent financial reporting indicated that over half of the financial reporting frauds involved

the overstatement of revenue. In an effort to combat earnings management through revenue

recognition, the SEC issued SAB 101 in 2000. In addition to revenue recognition issues being

more likely due to manipulation, we argue that revenue recognition issues are more fundamental

in terms of the implications for profitability. Penman (2001, 107) states that revenue generation

is key to firm value because “a firm cannot generate value without finding customers for its

products.” We argue therefore that fraud and revenue recognition restatements are likely to

generate greater concerns about the firm’s prospects than other types of restatements. Based on

these arguments, we test the following hypotheses (stated in alternative form):

7

H1: There are significant negative abnormal stock returns over: (i) the seven-day window surrounding a restatement announcement and (ii) the period beginning three days prior to a restatement announcement and ending three days after a restatement is filed with the SEC.

H1a: The negative abnormal stock returns over both measurement intervals are more

pronounced for firms with revenue recognition and fraud restatements than for firms with other reasons for restatements.

Prior analytical research suggests that the release of publicly available financial

information should reduce information asymmetries in the stock market (Verrecchia (1982),

Diamond (1985), and Bushman (1991)). Other research suggests that not only the existence but

also the quality of financial disclosures should affect information asymmetries in the stock

market (Diamond and Verrecchia (1991), Lundholm (1991)).

Prior research has attempted to identify lower quality or less credible financial

information by, for example, examining the components of earnings (Sloan (1996)) and analysts’

perceived disclosure quality (Lang and Lundholm (1993)). We argue that restatements

unambiguously suggest that prior financial statements are relatively less credible since the

original financial statements contain errors. We hypothesize that the announcement of a

restatement will result in an increase in information asymmetries in the stock market. When a

restatement is announced, there is uncertainty as to the consequences of the restatement on the

current financial statements as well as uncertainty about the reliability of the firm’s future

financial statements. As investors attempt to determine the impact of the restatement on current

and future profitability, they have a greater incentive to obtain private information, which

increases information asymmetries in the marketplace. We, therefore, expect an increase in

information asymmetries in the market for the firm’s stock surrounding the announcement of a

restatement. We also hypothesize that the uncertainty about the reliability of future financial

8

statements will cause the increase in information asymmetries to persist beyond the date that the

restated financial statements are filed with the SEC.

In addition, we hypothesize that the increased information asymmetries from

restatements should be more pronounced for restatements related to revenue recognition and

fraud. We argue, as above, that fraud and revenue recognition restatements will generate greater

concerns on the part of investors about firm value and about the reliability of the financial

statements than other types of restatements.

Based on these arguments, we hypothesize that restatements affect information

asymmetries in the stock market. Copeland and Galai (1983) and Glosten and Milgrom (1985)

show that bid-ask spreads are related to investors’ perceived information asymmetry. We

hypothesize, therefore, that restatements will affect bid-ask spreads in the stock market.

Specifically, we test the following hypotheses (stated in the alternative form):

H2: There are significant increases in bid-ask spreads over: (i) the seven-day window

surrounding a restatement announcement and (ii) the period beginning three days prior to a restatement announcement and ending three days after the restatement is filed with the SEC.

H2a: The increase in spreads over both measurement intervals is more pronounced for

firms with revenue recognition and fraud restatements than for firms with other reasons for restatements.

Prior research has shown that the market’s response to earnings announcements is lower

when the market perceives the information to be of lower quality (Easton and Zmijewki (1989)).

Since restatements suggest that prior financial information is not credible, we argue that the

market will perceive the firm’s future earnings to be of lower quality and will, therefore, rely less

on the firm’s future earnings releases in assessing firm value. We hypothesize, therefore, that the

market response to earnings will be relatively lower for earnings reported after the restatement

9

than for earnings reported prior to the restatement. Our third set of hypotheses (in alternative

form) is:

H3: Earnings response coefficients will be smaller for earnings announcements subsequent to a restatement than for earnings announcements prior to the restatement.

H3a: The decrease in earnings response coefficients is more pronounced for firms with

revenue recognition and fraud restatements than for firms with other reasons for restatements.

III. DATA AND DESCRIPTIVE STATISTICS Data Generally, firms file a 10-K annual report with the SEC within 90 days of their fiscal year

end. For most firms, this is the end of their reporting obligations to the SEC for that fiscal year.

However, some firms restate their 10-K reports at a later date. These restatements stem from a

variety of issues. Some restatements arise from a change in accounting rules or a change in the

treatment of a merger. However, a large number of restatements are filed with the SEC each

year that arise from “accounting errors”. These accounting errors range from math errors to not

recognizing revenue according to GAAP. In this paper, we consider only those firms that restate

financial statements due to accounting errors.

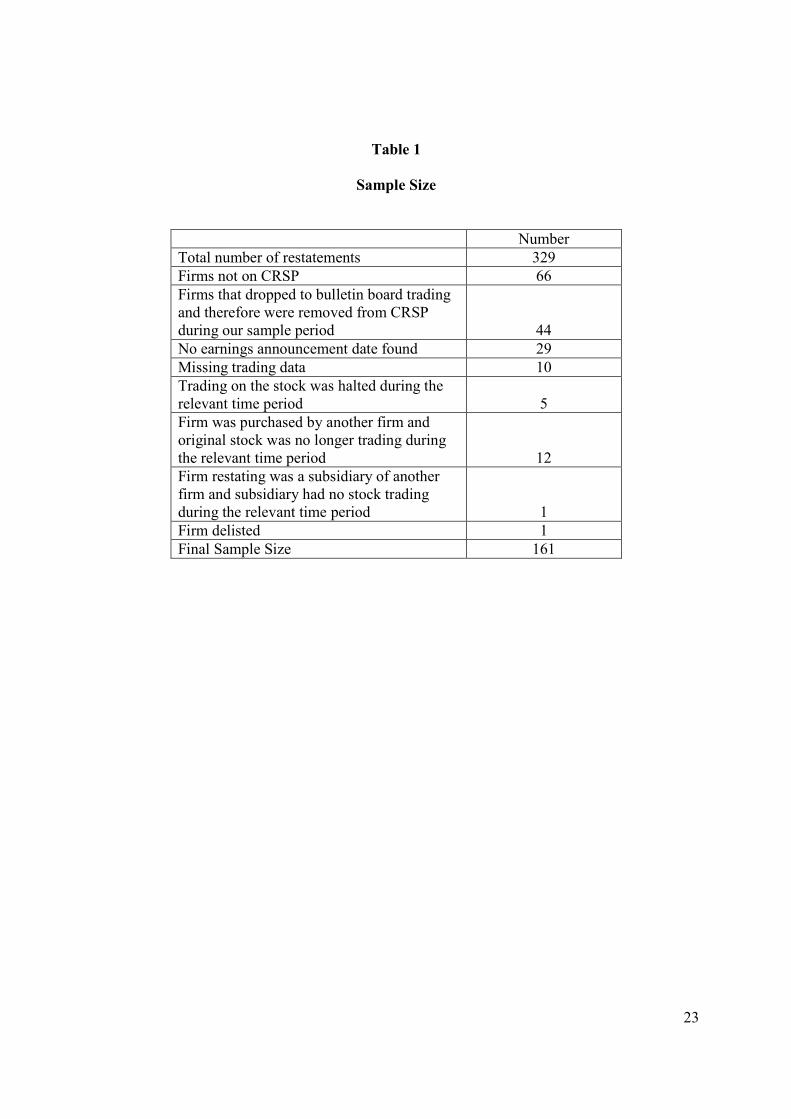

We obtain our sample of accounting restatements by searching 10-K Wizard in the years

1997, 1998, and 1999 for restated financial statements. From this sample of restated financial

statements, we identify only those firms that restated financial statements due to accounting

errors.2 The accounting errors range from fraud and revenue recognition problems to errors in

calculating earnings per share. We find 329 firms during our three-year period that restate

financial statements and file a 10-KA (amended form 10-K) due to accounting errors.

2 Therefore, we exclude footnote restatements, retroactive rule changes, purchase-pooling restatements, etc.

10

We obtain price, return, volume, and spread data for each restatement for the period

beginning three days prior to the announcement of an accounting problem that requires

restatement and ending three days after the release of the restated financial statements. By

examining both the period around the announcement of the problem and the release of the

restated statements, we can obtain a complete assessment of the effect of the restatement on the

stock market. We obtain daily closing prices and returns from CRSP. Since some of the firms

that filed 10-KAs are bulletin board stocks or dropped to bulletin board stocks during the sample

period, we are unable to find data on CRSP for 110 firms. We are unable to obtain earnings

announcement dates for 29 firms and spreads and trading volume from the Trades and Quotes

(TAQ) database for another 10 firms. Finally, mergers, trading halts, delistings, and wholly-

owned subsidiaries account for 19 firms in our initial sample. No market data is available on

these firms. Therefore, we show in table 1 that our final sample for analysis is 161 firms. We

obtain all news announcements and dates relating to these 161 restatements from the Dow Jones

News Retrieval Service.

[Please place table 1 about here]

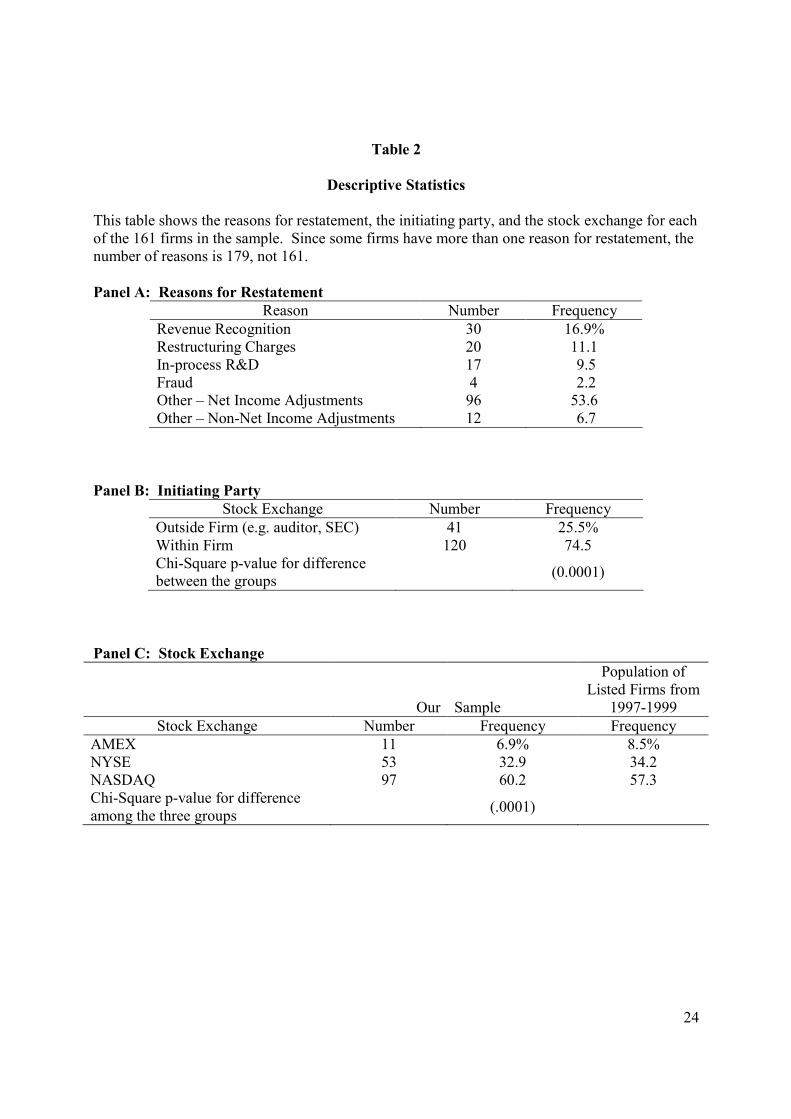

We divide the firms into categories based on the reason for the restatement. In table 2,

we show the frequency of each type of error. Since some firms report more than one reason for

their restatement, the total number of reasons given exceeds 161 (our sample size). The

categories we use are revenue recognition (30 firms), restructuring charges (20 firms), in-process

research and development (17 firms), fraudulent reporting (4 firms), other net income

adjustments (96 firms), and other non-net income adjustments (12 firms).

Panel B reports the party who initiated the restatement. The firm initiated the majority of

the restatements in our sample (approximately 75%). The SEC initiated many (if not all) of the

11

in-process research and development (IPR&D) restatements. Auditors and other outsiders

initiated the remainder of the restatements.

In panel C of table 2, we report on the frequency of restatements by the stock exchange

on which the stock is traded. 6.9% of our sample is listed on the American Stock Exchange

(AMEX), 32.9% is listed on the New York Stock Exchange (NYSE), and 60.2% of our firms are

traded on either the National Market System or Small Cap Market on the NASDAQ. This

distribution of our sample across stock exchanges does not appear to be different than the

distribution of the population of listed firms during the period 1997-1999 (8.5% on AMEX,

34.2% on NYSE, and 57.3% on NASDAQ).

[Please place table 2 about here]

Although not reported in a table, we also analyzed the restatements by industry using

both two-digit and three-digit SIC codes. We found no industry trends and no trend when

interacting industry and reason for restatement.

Financial Statement Effects

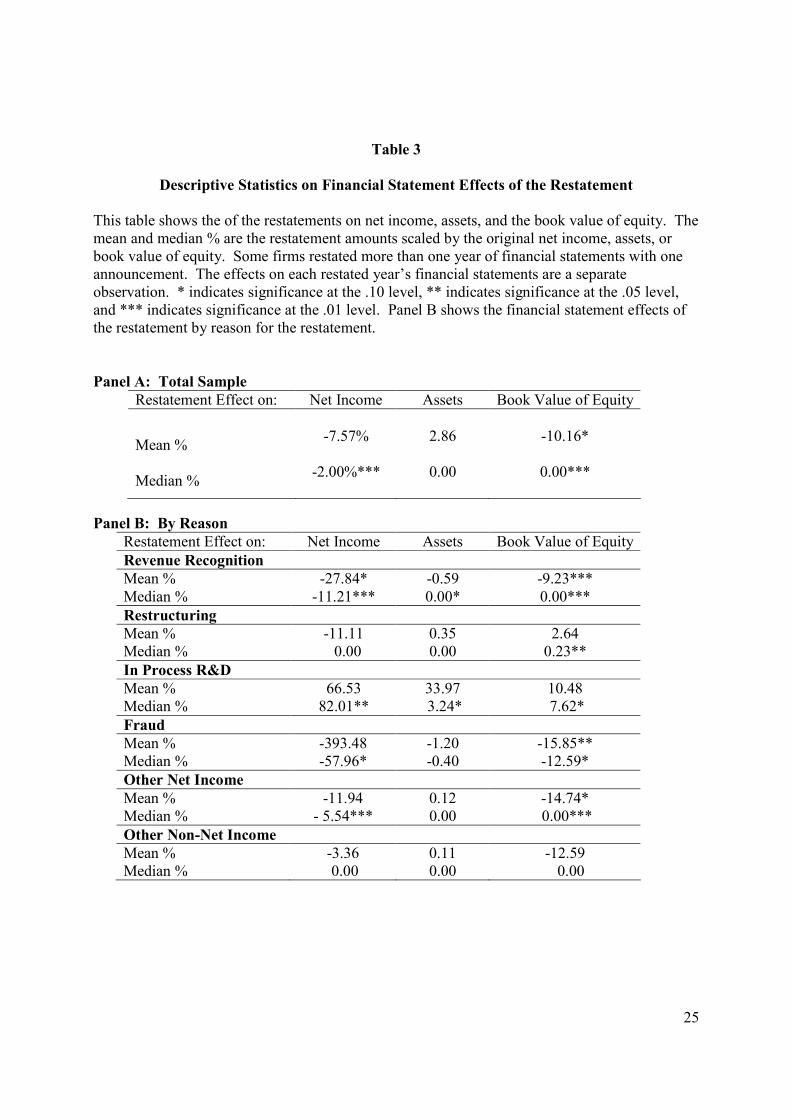

In table 3, we show the effect of the restatement on the firm’s net income, assets, and

stockholders’ equity. Sometimes firms restate more than one year’s financial statements on the

same 10-KA. If this is the case, the effects on each restated year’s financial statements are

included as a separate observation.

Panel A shows the financial statement effects of the restatement for the entire sample.

The effects are reported as a percentage of the amount originally reported for that item. We

report both the means and the median percentages. Significance tests of means are based on t-

tests while tests of medians are based on Wilcoxon signed–rank tests. While we report both

means and medians, we focus our analysis on medians since the data do not appear to be

12

normally distributed. The median firm adjusted its net income down by 2.00% due to the

restatement. The results suggest that the original income was, at the median, overstated prior to

the restatement.

In Panel B, we show the effect of the restatement on income, assets and equity by the

reason for the restatement. The results suggest a significant negative percentage impact on

income for revenue recognition, fraud, and other net income related restatements. There is a

significant positive impact on net income from in-process research and development

restatements. The percentage impact on income from restructuring restatements does not appear

to be significant. 3

[Please place table 3 about here]

Cumulative Abnormal Returns

We obtain the date the restatement was filed with the SEC from 10-K Wizard. However,

often there are news announcements of the potential restatement and/or accounting problems

within the firm prior to the restatement date. We search the Dow Jones News Retrieval Service

to obtain the first date when the public became aware of the accounting problem. We limit our

search for announcements to the Wall Street Journal or the Dow Jones News Service.

In table 4, we present the cumulative abnormal returns (CARs) surrounding the

announcement of the accounting problem and for the period from before the announcement of

the problem to after the filing of the restated financial statements. Panel A shows a significant

negative CAR from the close three days before the announcement to the close three days after

the announcement of the accounting problem. The median cumulative abnormal return is -3.79

which is significant at the one percent level. In addition, the median CAR for the period from

3 Note that firms that restate with non-net income adjustments show a decrease in their net income of $0.4 million, on average. This results from the firms in this subsample that also provide other reasons for their restatement other than solely non-net income adjustments.

13

prior to the announcement to after the filing of the restated statements is –5.24. This is also

significant at the one percent level.

In panel B, we show cumulative abnormal returns by reason for the restatement. We find

a significant negative median CAR for restatement announcements related to revenue

recognition, in-process research and development, other net income, and other non-net income

issues. The median stock market reaction from revenue recognition and fraud issues is relatively

more negative than the stock market reaction to restatements from the other issues. Revenue

recognition restatements cause a CAR of -7.94 over the seven-day announcement period while

fraud restatements cause a CAR of -12.85 over this same period.

In the second column of panel B, we report the CAR from three days prior to the

announcement of the accounting problem to three days after the filing of the restated financial

statements for each type of restatement. Again, there are significant negative CARs for firms

with revenue recognition, in-process research and development, other net income and other non-

net income related restatements. In addition, the CAR for revenue recognition and fraud issues

is relatively more negative than the CAR from restatements related to the other issues. Firms

with revenue recognition issues experience median CARs of –13.38%, and firms with fraud

issues experience median CARs of -19.72 over this window. We note that these descriptive

statistics do not control for the impact of the restatement on the financial statements which may

or may not be known prior to the filing of the restated financial statements. Regression analysis,

reported in the next section, will yield insight into the differential abnormal returns for different

types of restatements after controlling for the financial statement impact.

[Please place table 4 about here]

14

Change in Spreads

In table 5, we show statistics on the percentage change in bid-ask spreads for the seven

days around the announcement of the problem and for the period from before the problem

announcement to after the filing of the restated financial statements.4 For the entire sample, the

spread does not significantly change during these periods.

In panel B, we report the results by reason for the restatement. We find a significant

increase in spreads only for revenue recognition restatements and only for the longer time period.

While we have not controlled for other factors that affect spreads, these univariate results suggest

that there is an increase in spreads from restating prior financial statements related to revenue

recognition issues. Regression analysis, reported in the next section, will examine the change in

spreads after controlling for factors that have been shown to relate to spreads in prior research.

[Please place table 5 about here]

IV. REGRESSION RESULTS

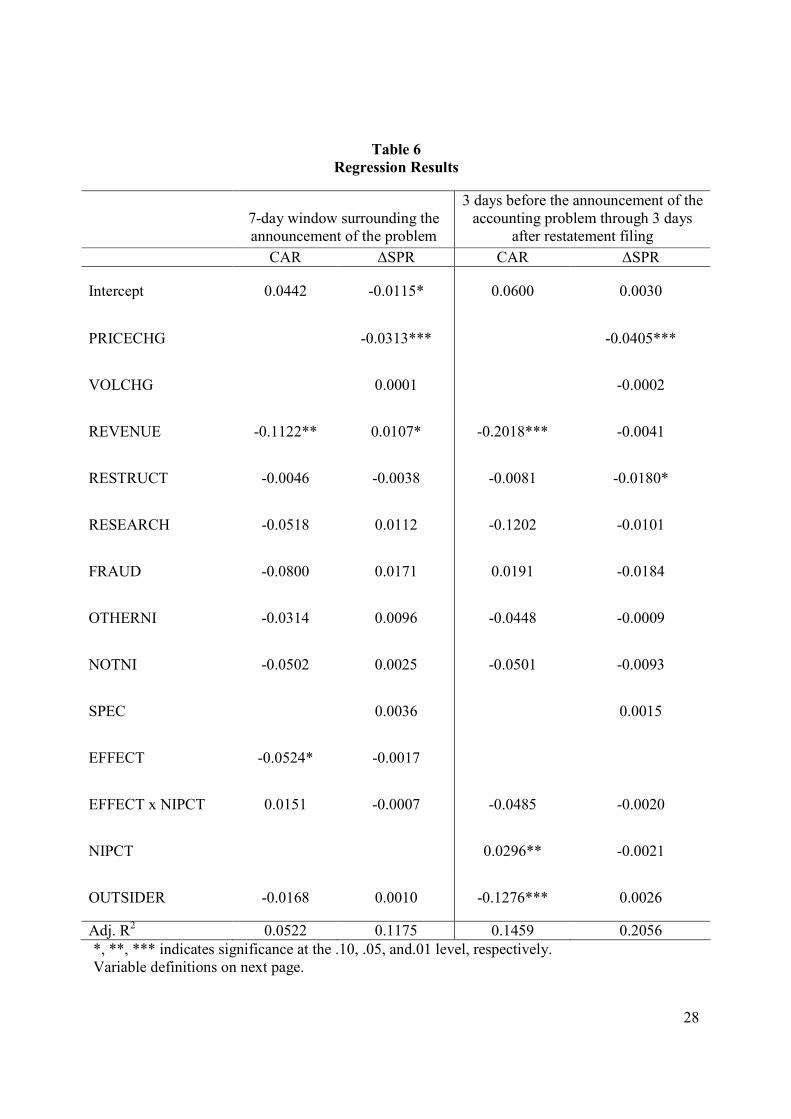

Results for the Problem Announcement

We next analyze the announcement of the accounting problem’s effect on CARs and

spreads by performing regression analysis. We report the results of the regressions for the

period surrounding the announcement of the accounting problem in table 6.

In the first column of table 6, we examine how the cumulative abnormal returns relate to

the type of restatement. In this regression, we include an indicator variable for whether the firm

discloses the restatement’s effect on net income in the announcement of the accounting problem.

We also control for the party that initiated the restatement. Our returns regression model is as

follows:

4 For each firm, the time-weighted median spread is calculated on a daily basis. We use this time-weighted median spread as the measurement of a firm’s spread on any given day.

15

0 1 2 3 4 6 7

8 9 10

= + + + + + + ++ + +

CAR REVENUE RESTRUCT RESEARCH FRAUD OTHERNI NOTNIEFFECT EFFECTxNIPCT OUTSIDER

α α α α α α αα α α ε

where: CAR = the seven day cumulative abnormal return from three days before to three days after the announcement; REVENUE = 1 if the firm cites a revenue recognition problem and zero otherwise; RESTRUCT = 1 if the firm cites restructuring as the reason for restatement and zero otherwise; RESEARCH = 1 if the firm restates its IPR&D and zero otherwise; FRAUD = 1 if the firm restates due to fraudulent financial reporting and zero otherwise; OTHERNI = 1 if the firm cites another net income adjustment not specifically mentioned in another category and zero otherwise; NOTNI = 1 if the firm restates financial information that does not affect its earnings and zero otherwise; EFFECT = 1 if the firm discloses the impact of the restatement on the financial statements in the announcement of the problem and zero otherwise; NIPCT = the percentage impact of the restatement on net income;5 OUTSIDER = 1 if a party outside the firm such as the auditor, SEC, Department of Justice, etc. initiated the restatement and zero otherwise.

The results suggest that there are more pronounced negative abnormal returns around the

announcement of a restatement related to revenue recognition than for other types of

restatements. This is consistent with hypotheses H1 and H1a. We also note that firms that

disclose the effect of the restatement at the announcement of the accounting problem have larger

reactions to the announcement than other firms.

In the second column of table 6, we examine whether the change in bid-ask spreads

surrounding the announcement of the problem is related to the reason for the restatement. The

dependent variable is the change in percentage bid-ask spread from three days prior to three days

after the announcement of the accounting problem. In addition to indicator variables capturing

the restatement reason, the regression includes variables that have been found in the prior

5 We also included the percentage impact of the restatement on assets and the percentage impact of the restatement on owner’s equity. These variables were not significant and did not affect the coefficients on the other variables when included in the analysis.

16

literature to affect spreads (Lee, Mucklow and Ready (1993)). Specifically, we control for the

price change and the volume change from three days before to three days after the

announcement. We include an indicator variable (SPEC) that is assigned the value of unity for

firms traded in the specialist markets (NYSE/AMEX firms) and zero for NASDAQ firms.

Again, we also include an indicator variable for whether the effect on the financial statements

was disclosed in the announcement and an indicator variable for whether the firm initiated the

restatement. Our spread regression is as follows:

0 1 2 3 4 5SPRDIFF PRICECHG VOLCHG REVENUE RESTRUCT RESEARCHα α α α α α= + + + + +

6 7 8 9 10 11 12+ + + + + + + +FRAUD OTHERNI NOTNI SPEC EFFECT EFFECTxNIPCT OUTSIDERα α α α α α α ε

where:

∆SPR = the percent change in spread from three days before to three days after the announcement of the problem; PRICECHG (VOLCHG) = the change in the log of price (volume) from three days before to three days after the announcement of the problem; SPEC = 1 if the firm is traded on the NYSE or AMEX and zero otherwise; All other variables as defined above.

As expected, we find a significant negative coefficient on price change. However the

coefficient on volume change is not significant. We find a significant positive coefficient only

for restatements due to revenue recognition. This suggests that the dealer appears to sense an

increase in information asymmetry when the accounting problem relates to revenue recognition.

This is consistent with hypotheses H2 and H2a.6 The results suggest that the market reacts most

6 We also examined the quoted depth for the bid and ask prices. A decrease in depth for both the bid and the ask prices would suggest that the dealer and investors perceive an increase in information asymmetry. An increase in the depth for the bid (ask) price suggests that the dealer perceives that the firm is under (over) valued. This would indicate an information effect and not necessarily an information asymmetry effect. We find a significant increase in ask depth for revenue recognition and other net income related restatements. An increase in the ask depth suggests that the dealer is willing to sell more shares of stock after relative to before the announcement of the problem. This suggests that the dealer perceives that the stock is overvalued when problems related to these issues

17

negatively to announcements of accounting problems related to revenue recognition and that the

dealer perceives an increase in information asymmetry for problems related to revenue

recognition.

Results for the Period from Prior to the Announcement to after the Restatement Filing

In the third and fourth columns of table 6, we report regression results for the period from

three days prior to the announcement of a problem to three days after the filing of the

restatement.7 In the third column of table 6, the results document that there are more negative

CARs during this longer window for firms with revenue recognition issues than for firms with

other restatements. The results also show that the CARs are positively related to the percentage

impact on net income, and that the CARs are significantly more negative when a party outside

the firm initiated the restatement.

The spread results reported in the fourth column show that the change in spreads from

before the announcement of the problem to after the restatement filing is not related to the impact

on the income statement or to the type of restatement. This suggests that the increase in

information asymmetry documented around the announcement of the problem is only temporary.

The dealer does not appear to be concerned about the effect of the quality of prior financial

statements on private information search after the release of the restated financial statements.

are announced. This is consistent with Kavajecz (1999) who concludes that changes in quoted depths reflect the dealer’s perceptions about the stock’s future value. 7 We also examined the cumulative abnormal returns and spreads for the seven day period around the filing of the restated financial statements. We find that the cumulative abnormal returns are related to the impact of the restatement on net income and on owner’s equity. This is expected since the value of the firm would be affected by changes in income. We do not find any incremental affect on CARs based on the type of restatement. We also examine the change in spreads from three days before to three days after the filing of the restated financial statements. We find that the spread increase is positively related to the percentage effect on net income and find an incremental increase in spreads for revenue recognition related restatements. Thus, the dealer appears to sense an increase in information asymmetry around the filing of restated financial statements when there is a larger impact on net income and when the restatement relates to revenue recognition issues.

18

[Please place table 6 about here]

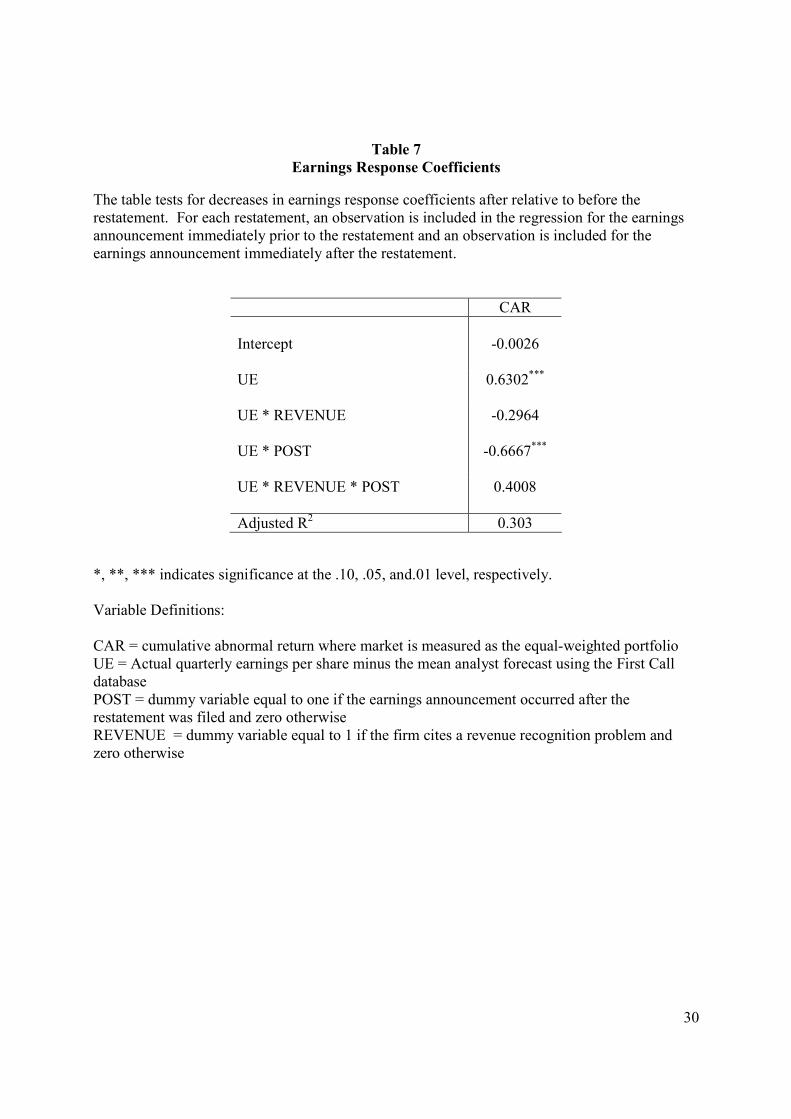

Earnings Response Coefficients

In table 7, we test whether the market relies less on earnings announcements released

after a firm has announced a restatement than on earnings announcements prior to the

restatement. CARs for the three days around the earnings announcement (days –1, 0 and +1

where day 0 is the earnings announcement date) are regressed on unexpected earnings where

expected earnings is the mean analyst forecast using the First Call database.8, 9 For each

restatement, we include two earnings announcements in the regression: the annual earnings

announcement immediately prior to the restatement and the annual earnings announcement

immediately after the filing of the restated financial statements. We also include an indicator

variable for if the earnings announcement occurred after the restatement. Finally, we include an

indicator variable for revenue recognition restatements to determine if the effect on earnings

response coefficients is different for firms with revenue recognition restatements than for firms

with other types of restatements.

Table 7 reports the results. The results support hypothesis H3. The coefficient on

unexpected earnings after the restatement (UE * POST) is significantly negative, suggesting that

the earnings response coefficient is significantly smaller after relative to before a restatement.

However, there is no support for hypothesis H3a. The earnings response coefficients are no

different for firms with revenue recognition problems than for firms with other types of

8 We use a subsample of 40 firms in this regression. For these firms, we find both analyst forecasts and actual earnings in the First Call database. The remaining firms do not have forecasts, actuals, or both in this database. By calculating unexpected earnings using only the First Call database, we are reasonably sure of our calculation since First Call is likely to report the “line of earnings” that analysts are forecasting. Smaller samples generally bias against rejecting the null hypothesis. We are confident in the reduction in the earnings response coefficient given the significance of the results even though we have a small subsample. 9 We also performed the analysis with the median analyst forecast as the expectation of earnings. The results are similar to those reported in the table.

19

restatements. Therefore, we conclude that the market relies less on the subsequent earnings for

all firms that issue a restatement.

V. CONCLUSION

This study provides insight into how the market reacts to announcements of accounting

problems and the filing of restated financial statements. Prior research has attempted to gain an

understanding of how the “quality” of accounting information affects stock prices. Specifically,

research has examined discretionary accruals, the quality of disclosures as perceived by analysts

(AIMR quality scores), the detail of disclosures, and other earnings characteristics to ascertain

how the quality of the accounting information affects the stock market. In this study, we focus

on announcements that prior financial statements contain errors. These announcements suggest

to investors that the prior financial statements are unreliable. We, therefore, examine how the

market and dealer react to the announcement and to the filing of restated financial statements in

order to determine how the knowledge that prior financial statements are unreliable affect the

market value of the company, the information asymmetry related to the company, and the

market’s reliance on future financial statements.

We find pronounced reductions in market values and increases in information asymmetry

at the announcement of accounting problems related to revenue recognition issues. This suggests

that the market and dealer perceive accounting problems related to revenue recognition issues to

be relatively more important than accounting problems related to other issues. We also find no

increase in information asymmetry from before the announcement of the problem to after the

filing of the restated financial statements. This suggests that the restatement of financial

statements does not appear to permanently increase the information asymmetry in the market for

the firm’s stock. Finally, we find a decrease in earnings response coefficients from before to

20

after the announcement and release of restated financial statements, suggesting that investors

perceive a decrease in the reliability of the firm’s earnings after a restatement.

These results are important for research attempting to gain insight into how the quality of

financial statements affects investor perceptions of the firm’s value and information asymmetries

and investors’ reliance on the firm’s financial statements. The results are also important for

understanding how different types of accounting problems are perceived by the market. The

results suggest that future research should further examine revenue recognition related issues.

21

REFERENCES

Ball, R. and P. Brown. 1968. An empirical evaluation of accounting numbers. Journal of Accounting Research 6 (Autumn): 159-178. Beaver, W.H. 1968. The information content of annual earnings announcements. Journal of Accounting Research 6: 67-92 Bushman, R. 1991. Public disclosures and the structure of private information markets. Journal of Accounting Research 29 (Supplement): 261-76. Copeland, T. and D. Galai. 1983. Information effects on the bid-ask spread. Journal of Finance (December): 1457-1469. Dallas Morning News, 2001. SEC to Check Annual Reports for Revenue Manipulation: About One-Fourth of All Public Corporations Will Be Verified. DeFond, M. and C. Park. 2001. The reversal of abnormal accruals and the market valuation of earnings surprises. The Accounting Review 76. Diamond, D. 1985. Optimal release of information by firms. Journal of Finance 40: 1071-94. Diamond, D. and R. Verrecchia. 1991. Disclosure, liquidity and the cost of capital. Journal of Finance 46: 1325-1360. Easton, P. and M. Zmijewski. 1989. Cross sectional variation in the stock market response to accounting earnings announcement. Journal of Accounting and Economics: 117-141. Glosten, L. and P. Milgrom. 1985. Bid, ask and transaction prices in a specialist market with heterogeneously informed traders. Journal of Financial Economics (March): 71-100. Jones, J. 1991. Earnings management during import relief investigations. Journal of Accounting Research 29: 93-228. Kavajecz, K.A., 1999. A Specialist’s Quoted Depth and the Limit Order Book. Journal of Finance (April): 747-771. Lang, M. and R. Lundholm. 1993. Cross-sectional determinants of analyst ratings of corporate disclosures. Journal of Accounting Research 31 (Autumn): 246-271. Lee, C.M.C., B. Mucklow, and M.J. Ready, 1993. Spreads, Depths, and the Impact of Earnings Information: An Intraday Analysis. Review of Financial Studies (Number 2): 345-374. Levitt, A., 1998. The “Numbers Game”. Securities and Exchange Comission.

22

Lundholm, R. 1991. Public signals and the equilibrium allocation of private information. Journal of Accounting Research 29: 322-349. McNichols, M. and G. Wilson. 1988. Evidence of earnings management from the provision of bad debts. Journal of Accounting Research 26: 1-31. Palmrose, Z, V. Richardson and S. Scholz. 2001. Determinants of market reactions to restatement announcements. University of Kansas working paper. Penman, S. 2001. Financial Statement Analysis and Security Valuation. New York: McGraw-Hill. Staff Accounting Bulletin 101: Revenue Recognition, 2001. Securities and Exchange Commission. Turner, L., J.R. Dietrich, K.L. Anderson, and A.D. Bailey, 2001. Accounting Restatements. Working Paper, The Ohio State University. Verrecchia, R. 1982. The use of mathematical models in financial accounting. Journal of Accounting Research 20:1-42. Wu, M. 2002. Earnings restatements: A capital market examination. New York University working paper.

23

Table 1

Sample Size

Number Total number of restatements 329 Firms not on CRSP 66 Firms that dropped to bulletin board trading and therefore were removed from CRSP during our sample period

44 No earnings announcement date found 29 Missing trading data 10 Trading on the stock was halted during the relevant time period

5

Firm was purchased by another firm and original stock was no longer trading during the relevant time period

12 Firm restating was a subsidiary of another firm and subsidiary had no stock trading during the relevant time period

1

Firm delisted 1 Final Sample Size 161

24

Table 2

Descriptive Statistics This table shows the reasons for restatement, the initiating party, and the stock exchange for each of the 161 firms in the sample. Since some firms have more than one reason for restatement, the number of reasons is 179, not 161.

Panel A: Reasons for Restatement

Reason Number Frequency Revenue Recognition 30 16.9% Restructuring Charges 20 11.1 In-process R&D 17 9.5 Fraud 4 2.2 Other – Net Income Adjustments 96 53.6 Other – Non-Net Income Adjustments 12 6.7

Panel B: Initiating Party

Stock Exchange Number Frequency Outside Firm (e.g. auditor, SEC) 41 25.5% Within Firm 120 74.5 Chi-Square p-value for difference between the groups

(0.0001)

Panel C: Stock Exchange

Our

Sample

Population of Listed Firms from

1997-1999 Stock Exchange Number Frequency Frequency

AMEX 11 6.9% 8.5% NYSE 53 32.9 34.2 NASDAQ 97 60.2 57.3 Chi-Square p-value for difference among the three groups

(.0001)

25

Table 3

Descriptive Statistics on Financial Statement Effects of the Restatement

This table shows the of the restatements on net income, assets, and the book value of equity. The mean and median % are the restatement amounts scaled by the original net income, assets, or book value of equity. Some firms restated more than one year of financial statements with one announcement. The effects on each restated year’s financial statements are a separate observation. * indicates significance at the .10 level, ** indicates significance at the .05 level, and *** indicates significance at the .01 level. Panel B shows the financial statement effects of the restatement by reason for the restatement.

Panel A: Total Sample

Restatement Effect on: Net Income Assets Book Value of Equity

Mean % -7.57%

2.86 -10.16*

Median % -2.00%***

0.00 0.00***

Panel B: By Reason

Restatement Effect on: Net Income Assets Book Value of Equity Revenue Recognition Mean % -27.84* -0.59 -9.23*** Median % -11.21*** 0.00* 0.00*** Restructuring Mean % -11.11 0.35 2.64 Median % 0.00 0.00 0.23** In Process R&D Mean % 66.53 33.97 10.48 Median % 82.01** 3.24* 7.62* Fraud Mean % -393.48 -1.20 -15.85** Median % -57.96* -0.40 -12.59* Other Net Income Mean % -11.94 0.12 -14.74* Median % - 5.54*** 0.00 0.00*** Other Non-Net Income Mean % -3.36 0.11 -12.59 Median % 0.00 0.00 0.00

26

Table 4

Descriptive Statistics on Returns

Panel A shows the cumulative abnormal returns (CAR) calculated using an equal-weighted market portfolio over the 7-day window surrounding the announcement of the accounting problem and the window beginning 3 days before the announcement of the accounting problem through 3 days after the restatement filing. * indicates significance at the .10 level, ** indicates significance at the .05 level, and *** indicates significance at the .01 level. Panel B shows the CARs for the two time periods by reason for the restatement. Panel A: Total Sample (N= 161)

7-day window surrounding the announcement of the

problem

3 days before the announcement of the accounting problem through 3

days after restatement filing CAR Mean -3.49** -7.97*** Median -3.79*** -5.24***

Panel B: By Reason

Reason

7-day window surrounding the

announcement of the problem

3 days before the announcement of the

accounting problem through 3 days after restatement filing

Revenue Recognition CAR Mean -11.04*** -22.92*** Median -7.94*** -13.38*** Restructuring CAR Mean -0.58 -4.43 Median -1.63 -1.63 IPR&D CAR Mean -4.53* -14.40** Median -4.84* -7.99** Fraud CAR Mean -15.45* -14.15 Median -12.85 -19.72 Other Net Income CAR Mean -2.40 -5.31** Median -2.23** -2.83** Other Not Net Income CAR Mean -4.00** -4.20*** Median -4.52** -4.52**

27

Table 5

Changes in Spreads

Panel A shows the percentage change in the time-weighted bid-ask spread (∆SPR) over the 7-day window surrounding the announcement of the accounting problem and the window beginning 3 days before the announcement of the accounting problem through 3 days after the restatement filing. * indicates significance at the .10 level, ** indicates significance at the .05 level, and *** indicates significance at the .01 level. Panel B shows the ∆SPR for these two time periods by reason for the restatement. Panel A: Total Sample (N= 161)

7-day window surrounding the announcement of the problem

3 days before the announcement of the accounting problem through 3

days after restatement filing ∆SPR Mean 0.01% 0.33% Median 0.01 0.00

Panel B: By Reason

Reason

7-day window surrounding the

announcement of the problem

3 days before the announcement of the accounting problem

through 3 days after restatement filing

Revenue Recognition ∆SPR Mean 0.72% 1.36%* Median 0.10 0.13* Restructuring ∆SPR Mean -1.04 -0.97 Median 0.00 0.00 IPR&D ∆SPR Mean 0.11 0.04 Median -0.11 -0.02 Fraud ∆SPR Mean 1.88 0.87 Median 1.07 1.16 Other Net Income ∆SPR Mean 0.21 0.57 Median -0.01 0.00 Other Not Net Income ∆SPR Mean -0.54* -0.64* Median -0.22* -0.22

28

Table 6 Regression Results

7-day window surrounding the announcement of the problem

3 days before the announcement of the accounting problem through 3 days

after restatement filing

CAR ∆SPR CAR ∆SPR

Intercept 0.0442 -0.0115* 0.0600 0.0030

PRICECHG -0.0313*** -0.0405***

VOLCHG 0.0001 -0.0002

REVENUE -0.1122** 0.0107* -0.2018*** -0.0041

RESTRUCT -0.0046 -0.0038 -0.0081 -0.0180*

RESEARCH -0.0518 0.0112 -0.1202 -0.0101

FRAUD -0.0800 0.0171 0.0191 -0.0184

OTHERNI -0.0314 0.0096 -0.0448 -0.0009

NOTNI -0.0502 0.0025 -0.0501 -0.0093

SPEC 0.0036 0.0015

EFFECT -0.0524* -0.0017

EFFECT x NIPCT 0.0151 -0.0007 -0.0485 -0.0020

NIPCT

0.0296** -0.0021

OUTSIDER -0.0168 0.0010 -0.1276*** 0.0026

Adj. R2 0.0522 0.1175 0.1459 0.2056 *, **, *** indicates significance at the .10, .05, and.01 level, respectively. Variable definitions on next page.

29

Table 6, cont. Regression Results

CAR = cumulative abnormal return where market return is measured as the equal-weighted portfolio ∆SPR = percentage change in daily time-weighted median dollar spread PRICECHG = change in the ln(price) VOLCHG = change in the ln(volume) REVENUE = dummy variable equal to 1 if the firm cites a revenue recognition problem and zero otherwise RESTRUCT = dummy variable equal to 1 if the firm cites restructuring as the reason for restatement and zero otherwise RESEARCH = dummy variable equal to 1 if the firm restates its IPR&D and zero otherwise FRAUD = dummy variable equal to 1 if the firm restates due to fraudulent financial reporting and zero otherwise OTHERNI = dummy variable equal to 1 if the firm cites another net income adjustment not specifically mentioned in another category and zero otherwise NOTNI = dummy variable equal to 1 if the firm restates financial information that does not affect its earnings and zero otherwise SPEC = dummy variable equal to 1 if the firm trades in a specialist market: NYSE or AMEX and zero otherwise EFFECT = dummy variable equal to 1 if the firm disclosed the financial statement impact of the restatement at the announcement of the problem and zero otherwise NIPCT = restated net income minus originally reported net income scaled by originally reported net income OUTSIDER = dummy variable equal to 1 if a party outside the firm initiated the restatement and zero otherwise

30

Table 7 Earnings Response Coefficients

The table tests for decreases in earnings response coefficients after relative to before the restatement. For each restatement, an observation is included in the regression for the earnings announcement immediately prior to the restatement and an observation is included for the earnings announcement immediately after the restatement.

CAR Intercept

-0.0026

UE

0.6302***

UE * REVENUE UE * POST

-0.2964

-0.6667***

UE * REVENUE * POST 0.4008

Adjusted R2 0.303

*, **, *** indicates significance at the .10, .05, and.01 level, respectively. Variable Definitions: CAR = cumulative abnormal return where market is measured as the equal-weighted portfolio UE = Actual quarterly earnings per share minus the mean analyst forecast using the First Call database POST = dummy variable equal to one if the earnings announcement occurred after the restatement was filed and zero otherwise REVENUE = dummy variable equal to 1 if the firm cites a revenue recognition problem and zero otherwise