Embed Size (px)

Citation preview

IIIIII Davidson County Board of Education

Lexington, NorthCarolina

I ComprehensiveAnnualFinancial Report

I Fiscal Year Ended June 30,2011

IIIIIIIIIII

IIIIIIIIIIIIIIIIIII

II

Davidson County SchoolsLexington, North Carolina

Comprehensive Annual Financial ReportFiscal Year Ended June 30,2011

II

II

IndependentAuditor's ReportManagement's Discussion and AnalysisBasic Financial Statements:

Government-wide Financial Statements:Statement of Net Assets (Exhibit 1)

78

II

INTRODUCTORY SECTION

Letter of Transmittal

FINANCIAL SECTION

I14

Statement of Activities (Exhibit 2) 15

Fund Financial Statements:Balance Sheet - Governmental Funds (Exhibit 3) 16

III

Statement of Revenues, Expenditures, and Changes in Fund Balances - GovernmentalFunds (Exhibit 4) 17

Reconciliation of the Statement of Revenues, Expenditures, and Changes in FundBalances of Governmental Funds to the Statement of Activities (Exhibit 4) 18

Statement of Revenues, Expenditures, and Changes in Fund Balances - Budget andActual- General and Major Special Revenue Funds (Exhibit 5) 19

I Statement of Net Assets - Proprietary Fund (Exhibit 6) 20

II

Statement of Revenues, Expenses, and Changes in Fund Net Assets - Proprietary Fund(Exhibit 7) 21

Statement of Cash Flows - Proprietary Fund (Exhibit 8) 22

Notes to the Financial Statements 24

III

Combining and Individual Fund Statements and Schedules:Schedule of Revenues, Expenditures, and Changes in Fund Balance -Budgetto Actual - General Fund 39

Combining Schedule of Revenues, Expenditures, and Changes in Fund Balances - Budgetto Actual - Special Revenue Funds 40

I

IIIIIIIIIIIIIIIIIII

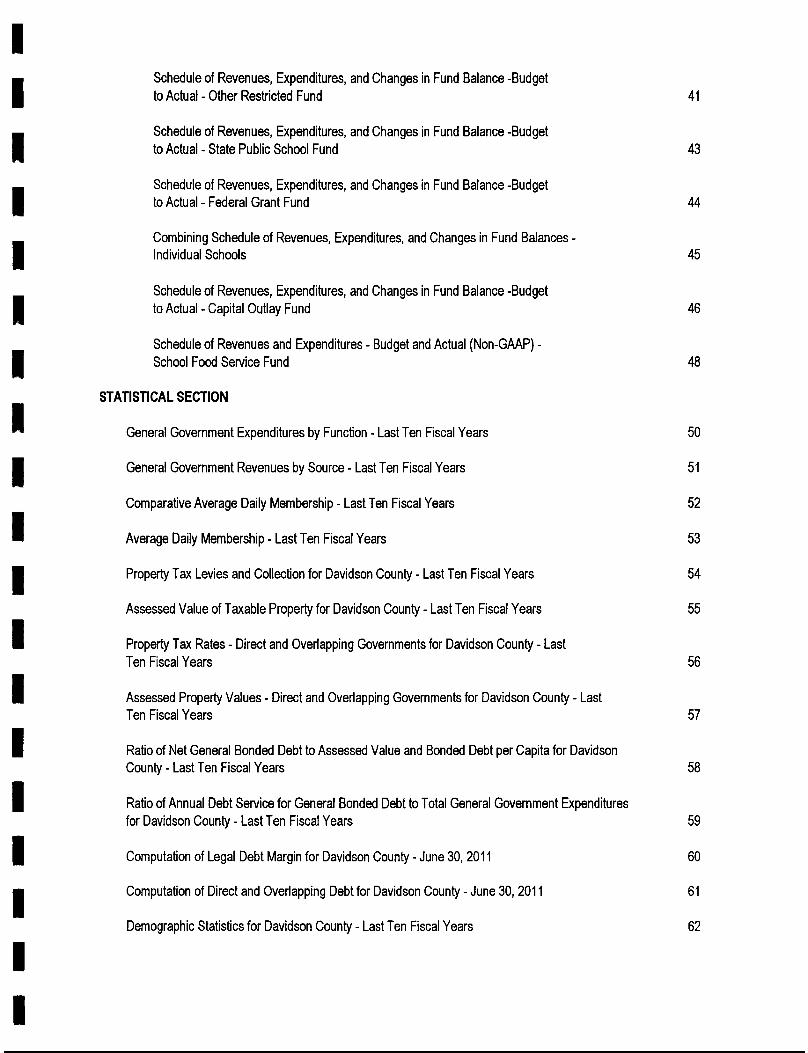

II Schedule of Revenues, Expenditures, and Changes in Fund Balance -Budget

to Actual- Other Restricted Fund 41

I Schedule of Revenues, Expenditures, and Changes in Fund Balance -Budgetto Actual - State Public School Fund 43

I Schedule of Revenues, Expenditures, and Changes in Fund Balance -Budgetto Actual- Federal Grant Fund 44

II

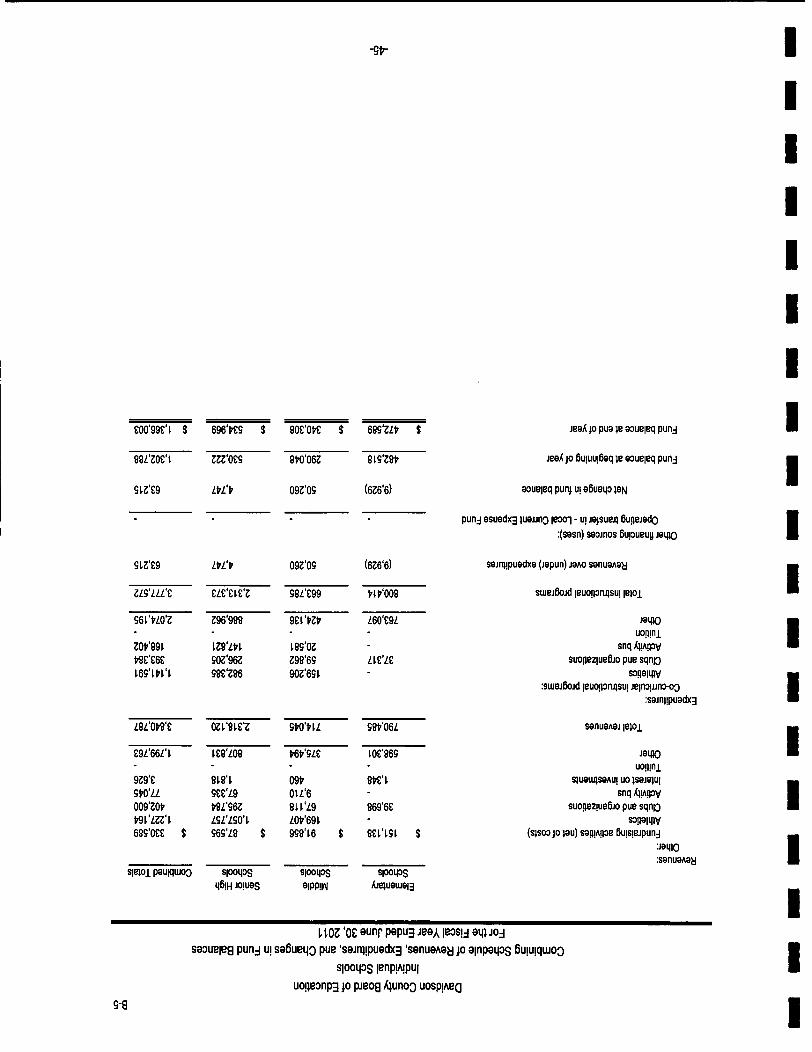

Combining Schedule of Revenues, Expenditures, and Changes in Fund Balances -Individual Schools 45

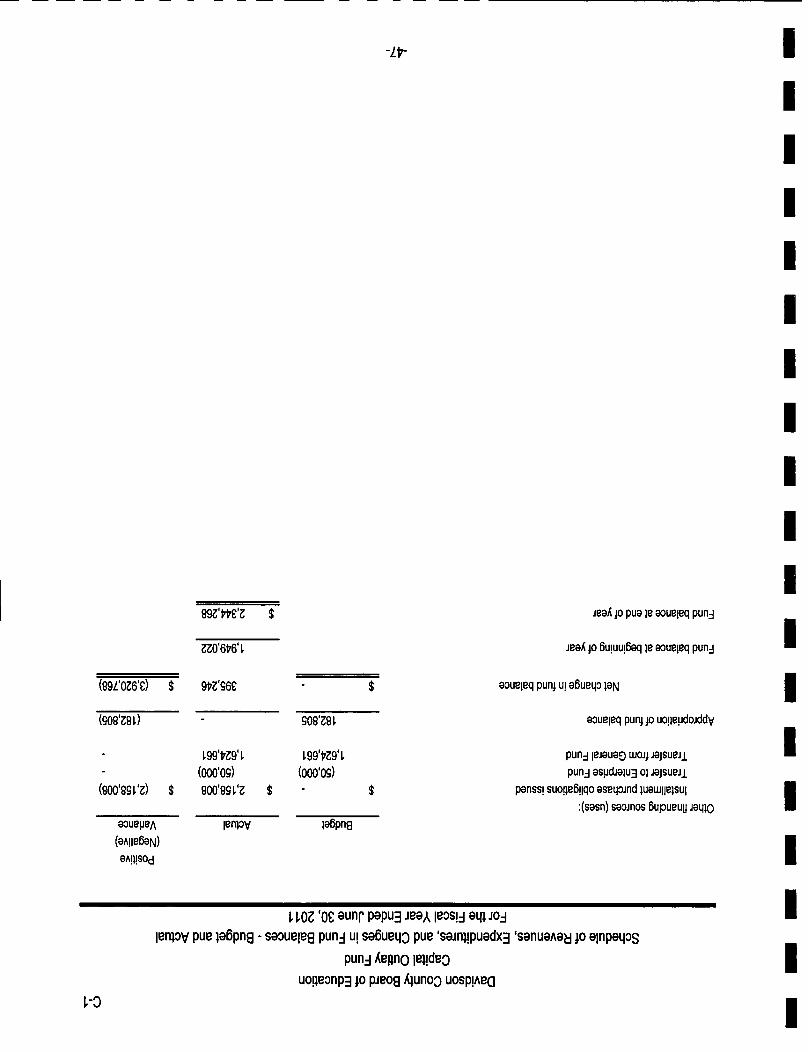

Schedule of Revenues, Expenditures, and Changes in Fund Balance -Budgetto Actual - Capital Outlay Fund 46

II

Schedule of Revenues and Expenditures - Budget and Actual (Non-GMP) -School Food Service Fund 48

General Government Expenditures by Function - Last Ten Fiscal Years 50

STATISTICAL SECTION

I General Government Revenues by Source - Last Ten Fiscal Years 51

IComparative Average Daily Membership - Last Ten Fiscal Years 52

Average Daily Membership - Last Ten Fiscal Years 53

II

Property Tax Levies and Collection for Davidson County - Last Ten Fiscal Years 54

Assessed Value of Taxable Property for Davidson County - Last Ten Fiscal Years 55

Property Tax Rates - Direct and Overlapping Governments for Davidson County - LastTen Fiscal Years 56

I Assessed Property Values - Direct and Overlapping Governments for Davidson County - LastTen Fiscal Years 57

II

Ratio of Net General Bonded Debt to Assessed Value and Bonded Debt per Capita for DavidsonCounty - Last Ten Fiscal Years 58

Ratio of Annual Debt Service for General Bonded Debt to Total General Government Expendituresfor Davidson County - Last Ten Fiscal Years 59

I Computation of Legal Debt Margin for Davidson County - June 30,2011 60

III

Computation of Direct and Overlapping Debt for DavidsonCounty - June 30, 2011 61

Demographic Statistics for Davidson County - Last Ten Fiscal Years 62

IIIIIIIIIIIIIIIIIII

IPrincipal Taxpayers in Davidson County - Fiscal Year Ended June 30, 2011 63

I COMPLIANCE SECTION

IIII

Report on Internal Control Over Financial Reporting and On Compliance and Other Matters BasedOn An Audit Of Financial Statements Performed In Accordance With GovernmentAuditingstandards 64

Report on Compliance with Requirements Applicable to Each Major Federal Program andInternal Control over Compliance in Accordance with Applicable Sections of OMB CircularA-133 and the State Audit Implementation Act 66

Report on Compliance with Requirements Applicable to each Major State Program andInternal Control over Compliance in Accordance with Applicable Sections of OMBCircular A-133 and State Single Audit Implementation Act 68

I Schedule of Findings and Questioned Costs 70

Corrective Action Plan 73

II

Summary Schedule of Prior Audit Findings 74

Schedule of Expenditures of Federal and State Awards 75

IIIIIIIIII

IIIIIIIIIIIIIIIIIII

I (}))~~county Schools Office of

SuperintendentII LEITER OF TRANSMIITAL

I October 26,2011

II

TO THE MEMBERS OF THE DAVIDSON COUNTYBOARD OF EDUCATION AND CITIZENS OFDAVIDSON COUNTY, NORTH CAROLINA

III

State law requires that all general-purpose local govemments publish, within six months of the close of eachfiscal year, a complete set of financial statements presented in conformity with generally acceptedaccounting principles (GAAP) and audited in accordance with generally accepted auditing standards by afirm of licensed certified public accountants. Pursuant to that requirement, we hereby issue theComprehensive Annual Financial Report of the Davidson County Board of Education (the Board) for thefiscal year ended June 30, 2011.

I

The comprehensive annual financial report is presented in four sections: Introductory, Financial,Statistical, and Compliance. The Introductory section contains the letter of transmittal, a list of the Boardmembers and principal officials, and the organizational chart. The introductory section is unaudited. TheFinancial section presents the independent auditor's report, management's discussion and analysis, thebasic financial statements, and the combining and individual fund financial statements and schedules byfund type. The Statistical section contains tables of unaudited data covering a ten year financial history ofthe Board, as well as, statistical data for Davidson County. The Compliance section presents informationrequired by the OMB Circular A-133 and the State Single Audit Implementation Act.

I

IThis report consists of management's representations conceming the finances of the Board. Consequently,management assumes full responsibility for the completeness and reliability of all of the informationpresented in this report. To provide a reasonable basis for making these representations, management ofthe Board has established a comprehensive internal control framework that is designed both to protect theBoard's assets from loss, theft, or misuse and compile sufficient reliable information for the preparation ofthe Board's financial statements in conformity with GAAP.IThe Board's financial statements have been audited by Rick Allred, CPA, PA, a firm of licensed certifiedpublic accountants. The goal of the independent audit was to provide reasonable assurance that thefinancial statements of the Board for the fiscal year ended June 30, 2011 are free of material misstatement.The independent audit involved examining, on a test basis, evidence supporting the amounts anddisclosures in the financial statements; assessing the accounting principles used and significant estimatesmade by management; and evaluating the overall financial statement presentation. The auditor's report canbe found in the financial section of this report.

IIIII

The independent audit of the financial statements of the Board was part of a broader, federally mandated"Single Audit" designed to meet the special needs of federal grantor agencies. The standards governingSingle Audit engagements require the independent auditor to report not only on the fair presentation of thefinancial statements, but also on the audited Board's intemal controls and compliance with legal

- 1-

I P.O. Box 2057 • Lexington, NC 27293-2057 • Phone (336) 249-8181 • Fax (336) 249-1062 • www.davidson.K12.nc.us

IIIIIIIIIIIIIIIIIII

- "---------_ ..._--

III

requirements with special emphasis on internal controls and legal requirements involving the administrationof federal awards. These reports are available in the Board's separately issued Single Audit Report foundin the compliance section of this report.

III

GAAP requires that management provide a narrative introduction, overview, and analysis to accompany thebasic financial statements in the form of Management's Discussion and Analysis (MD&A). This letter oftransmittal is designed to complement the MD&A and should be read in conjunction with it. The Board'sMD&A can be found immediately following the report of the independent auditors in the financial section ofthis report.

SCHOOL SYSTEM AND GOVERANCE

III

The Davidson County School System is the nineteenth largest among North Carolina's 115 public schoolsystems. It serves 20,171 students in preschool through grade twelve. It extends across 33 campuses thatinclude 18 elementary schools, six middle schools, six high schools; one extended day school, one schoolfor students with special needs, and one early college. Davidson County Schools has six high schoolattendance areas comprised of a high school, middle school and two to four elementary schools. Studentsattend their neighborhood school.

The Davidson County Schools join Lexington City Schools (student population 2,920), Thomasville CitySchools (student population 2,408) and the Davidson County Community College as public providers ofeducation in the county. All four education agencies receive funding from federal, State, local and grantsources.

I The Davidson County School System is governed by a nonpartisan board of education whose five schooldistrict residents are elected at large and serve overlapping four-year terms. The Board is responsible forsetting educational policies consistent with State and federal laws governing public education. The Boardreceives government funding from state, local, and federal sources. The Board must comply with theestablished legal requirements of each funding source. The Board has no taxing authority and is requiredto maintain accounting records in a uniform format established by the State's General Assembly.

II GEOGRAPHY, POPULATION and ECONOMICS

III

Davidson County is located in the Piedmont Triad Area of North Carolina. It is 552.68 square miles ofsuburban countryside. It is a neighbor to Winston-Salem in Forsyth County, High Point and Greensboro inGuilford County, Salisbury in Rowan County and Asheboro in Randolph County. The county seat isLexington.

Davidson County Schools is now the largest employer in Davidson County following layoffs and plantclosings of Thomasville Furniture Industries and Lexington Home Brands.

I

Davidson County's population of 162,878 residents is 18% non-Caucasian, with the largest percentages ofnon-Caucasian located within Lexington and Thomasville city limits. Davidson County Schools continues toexperience a growth in the number of students who speak English as a second language. Most of theworkforce within the county is blue collar, many of whom are from families who have experienced careerlong employment in furniture industries. Furniture and textiles have provided jobs without requiring posthigh school training, and in many cases high school completion. Since the late 1990's most of the textileand furniture companies have closed or moved overseas. Many workers have been forced to return toschool for retraining and college degrees. Davidson County Community College has seen enrollment grow.Today, 77.6% of the county's population over 25 years of age has a high school diploma or better, but only

I

II -2-

IIIIIIIIIIIIIIIIIII

II 15.4% of the same population has a college degree. Many of the county's college graduates choose not to

retum home to work. If they retum, they must travel to neighboring counties and larger cities to findprofessional jobs.I

IClosings of the textile and fumiture plants have made it difficult for our community. The unemployment rateis 11.5% which is above the state average of 10.4%. New industries are moving to Davidson County but itwill take time to create jobs equal to those lost due to plant closings.

II

FINANCIAL CHALLENGES

IIII

In 2001, Davidson County commissioners committed to building six new schools over the next 10 years.Brier Creek Elementary, Friendship Elementary, Tyro Elementary, and Southmont Elementary schools,have been constructed. Southmont Elementary opened in the fall of 2009. Land has been purchased forthe North/Ledford area middle and high school. Construction is in progress on the new middle school thatis scheduled to open in 2012-2013. A high school is scheduled to be built at a yet-to-be determined time.

As part of the American Recovery and Reinvestment Act 2009 (ARRA), funds for construction bonds wereavailable through the Department of Public Instruction. In 2009-2010 the county govemment tookadvantage of the funds and issued a Qualified School Construction Bond (QSCB). Davidson CountySchools received $2,617,384.91 of the bond proceeds. These monies are to be used to repair roofs atStoner-Thomas, Midway, and Welcome. Davidson County Schools will repay the county for the bond'sdebt service (principal and interest at .5187%). The method of repayment began in 2010-2011. The countygovemment has chosen to reduce the Davidson County School's capital outlay budget annually for therepayment of the annual debt service. This method of payback to the county govemment will occur over aperiod of 15 years. This annual reduction in the capital outlay budget will delay capital outlay needs by ourolder schools.

I

I Ed Stabilization 10,619,119 Race to the Top

$ 49,662

4,049,661

2,069,211

1,312,884

II

In 2010-2011 the county issued another ARRA- QSCB in the amount of $12,863,316.00 to help pay for thenew middle school construction that began in the North/Ledford area. Davidson County Schools does nothave to repay the county for the debt service of these bond proceeds.

Beginning in 2009-2010 the Davidson County Schools began receiving ARRA funds, which helped to offsetState budget cuts. As of June 30, 2011, the Davidson County Schools have received the following ARRAfunds:

I IDEA

$2,007,711

4,302,915

18,470

Education TechnologyTitle I

Education Jobs

McKinney Vento School Improvement Grant

III

Title 1, IDEA, McKinney Vento, and the Education Stabilization funds, are scheduled to end September 30,2011. This loss of $16,948,215 in ARRA funds and the State projected budget cuts, greater budgetchallenges lie ahead.

BUDGETARY CONTROLS

I

The North Carolina General Statutes require govemment units to adopt a balanced budget by July 1 ofeach year. The Board's annual budget resolution authorizes expenditures by function on the modified

-3-

IIIIIIIIIIIIIIIIIII

IIII

The budget is allocated to line item expenditure accounts, for internal management purposes. The budgetamounts in this report are presented in conformity with the legally adopted budget ordinance as amendedthroughout the fiscal year.

The Board uses a purchase order encumbrance system that records encumbrances against eachexpenditure line item. State and federal outstanding encumbrances are cancelled at year-end. Local andcapital outlay (category II & III) encumbrances are carried over into the subsequent year and the budgetamounts are re-appropriated.

I CASH MANAGEMENT

I Temporarily idle cash is invested in various instruments according to applicable State laws. The objective ofthe investment policy is to minimize market and credit risks while maintaining a competitive yield on theinvestment. The Board's deposits were either insured or collateralized in accordance with the stateguidelines as described in the Notes to the Financial Statements section III, A 1.I

III

RISK MANAGEMENT

The Board is exposed to various risks of losses related to torts; theft of, damage to, and destruction ofassets; errors and omissions; injuries to employees; and natural disasters. The Board carries various formsof insurance including, but not limited to, general liability, errors and omissions coverage, risk control, riskfinancing, and property coverage. A detailed description of our insurance coverage can be found in theNotes to the Financial Statements section III, B. 4.

ACKNOWLEGMENTS

II

The preparation of this report would not have been possible without the dedicated services of the financestaff and the Board's independent certified public accounting firm Rick Allred, CPA, PA. We would like toexpress our appreciation to all the employees who contributed and assisted with the preparation of thisreport.

In addition, we would like to thank the members of the Board of Education for their support and dedication inplanning and conducting the financial matters of the school system in a responsible manner. In conclusion,we would like to thank the Board of County Commissioners for their support throughout the fiscal year.I

I

ReS~;?~y submitted

'0~~/rorTred L. M&kSuperintendent

~#\eiAPamela W. Sink, CPAFinance Officer

I

III

-4-

I

IIIIIIIIIIIIIIIIIII

III DAVIDSON COUNTY BOARD OF EDUCATION

I LIST OF PRINCIPAL OFFICIALS

I June 30, 2011

II BOARD OF EDUCATION MEMBERS

I Carol B. Crouse, Chairperson

I Alan W. Beck, Vice-Chairperson

I Karen T. Craver

Jeannie M. Leonard

I Allan E. Thompson

ISUPERINTENDENT OF SCHOOLS

I Dr. Fred L. Mock

II FINANCE OFFICER

I PamelaW. Sink, CPA

II

-5-

I

IIIIIIIIIIIIIIIIIII

__7--------- _a

DAVIDSON COUNTY SCHOOLSORGANIZATIONAL CHART

0>I

Citizens

I

Board of Education

I

Superintendent

IIAssistant Superintendent Assistant Superintendent Director-School Community Executive Director

Chief Finance Officer IHuman Resources & Adm Curriculum & Instruction Relations & Public Information Auxiliary Services

IIII

IIIIIIIIIIIIIIIII

I

IIIIIIIII Financial Section

IIIIIIIIII- --

IIIIIIIIIIIIIIIIIII

II

RICK ALLRED, CPA, PACertified Public Accountant

I Independent Auditor's Report

ITo the Davidson County Board of EducationDavidson County, North Carolina

II have audited the accompanying financial statements of the governmental activities, the business-type activities and each majorfund of the Davidson County Board of Education, North Carolina, as of and for the year ended June 30, 2011, which collectivelycomprise the Davidson County Board of Education's basic financial statements as listed in the table of contents. These financialstatements are the responsibility of the Davidson County Board of Education's management. My responsibility is to express anopinion on these financial statements based on my audit.

I I conducted my audit in accordance with auditing standards generally accepted in the United States of America and thestandards applicable to financial audits contained in GovernmentAuditing Standards, issued by the Comptroller General of theUnited States. Those standards require that I plan and perform the audit to obtain reasonable assurance about whether thefinancial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting theamounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used andsignificant estimates made by management, as well as evaluating the overall financial statement presentation. I believe that myaudit provides a reasonable basis for my opinions.

III

In my opinion, the financial statements referred to above present fairly, in all material respects, the respective financial positionof the governmental activities, the business-type activities and each major fund of the Davidson County Board of Education asof June 30, 2011, and the respective changes in financial position and its cash flows, where applicable, thereof and the respectivebudgetary comparison for the General Fund, the Other Restricted Fund, the State Public School Fund, the Federal Grants Fund,and the Capital Outlay Fund for the year then ended in conformity with accounting principles generally accepted in the UnitedStates of America.

I In accordance with GovernmentAuditing Standards, I have also issued my report dated October 26,2011 on my considerationof the Davidson County Board of Education's internal control over financial reporting and my tests of its compliance withcertain provisions of laws, regulations, contracts and grants and other matters. The purpose of the report is to describe the scopeof my testing of internal control over financial reporting and compliance and the results of that testing, and not to provide anopinion on the internal control over financial reporting or on compliance. That report is an integral part of an audit performed inaccordance with GovernmentAuditing Standards and should be read in conjunction with this report in considering the results ofmy audit.

III

Management's Discussion and Analysis is not a required part of the basic financial statements but are supplementaryinformation required by the Governmental Accounting Standards Board. I have applied certain limited procedures, whichconsisted principally of inquiries of management regarding the methods of measurement and presentation of the requiredsupplementary information. However, I did not audit this information and express no opinion thereon.

IMy audit was conducted for the purpose of forming opinions on the financial statements that collectively comprise the basicfinancial statements of the Davidson County Board of Education, North Carolina. The introductory information, combining andindividual fund statements, budgetary schedules and other schedules, and the statistical tables, as well as the accompanyingschedule of expenditures of federal and State awards as required by U.S. Office of Management and Budget Circular A-133,Audits of States, Local Governments, and Non-Profit Organizations, and the State Single Audit Implementation Act, arepresented for purposes of additional analysis and are not a required part of the basic financial statements. The combining andindividual fund statements, budgetary schedules, other schedules and the accompanying schedule of expenditures of federal andState awards have been subjected to the auditing procedures applied in the audit of the basic financial statements and, in myopinion, is fairly stated, in all material respects, in relation to the basic financial statements taken as a whole. The introductoryinformation and the statistical tables have not been subjected to the auditing procedures applied in the audit of the basic financialstatements and, accordingly, I express no opinion on them.

III (jQckJlffrec£, C(Pjl, (Pjl

I October 26, 2011

I Member ofthe American InstituteofCertified Public Accountants

-7-

Rick Allred269 Amber Lane. Lexington. NC 27292

336-247-2310rick(ivrickallredcpa.com

IIIIIIIIIIIIIIIIIII

II MANAGEMENT'S PISCUSSIONANP ANALYSIS

I This section of the Davidson County Board of Education's (the Board) financial report represents ourdiscussion and analysis of the financial performance of the Board for the year ended June 30, 2011. Thisinformation should read in conjunction with the audited financial statements included in this report.

I Financial Highlights

I• The Board experienced a decrease in enrollment of 151 students from the previous year.• Land was purchased for the North/Ledford area middle and high school. Construction began on the

new middle school that is scheduled to open in August of 2012. Construction for the high school hasnot been determined.

• The Board received Qualified School Construction Bond (ARRA) proceeds in the amount of$12,863,316 for construction of the new middle school.

• Due to the economy, the Board experienced State budget cuts. To offset the State budget shortfall,federal monies received from The American Recovery and Reinvestment Act of 2009 (ARRA) wereused in our Title I, Exceptional Children, Technology, Instructional and Non-Instructional Supportprograms.

III Overview of the Financial Statements

-I

The audited financial statements of the Davidson County Board of Education consist of four components.They are as follows:

III

• Independent Auditor's Report• Management's Discussion and Analysis (required supplementary information)• Basic Financial Statements• Required supplemental section that presents combining and budgetary statements for govemmental

and enterprise funds

I

The Basic Financial Statements include two types of statements that present different views of the Board'sfinances. The first is the government-wide statements. The government-wide statements are presented onthe full accrual basis of accounting and include the statement of net assets and the statement of activities.The Statement of Net Assets includes all of the Board's assets and liabilities. Assets and liabilities areclassified in order of their relative liquidity for assets and due date for liabilities. This statement provides asummary of the Board's investment in assets and obligations to creditors. Liquidity and financial flexibilitycan be evaluated using the information contained in this statement. The Statement of Activities summarizesthe Board's revenues and expenses for the current year. A net (expense) revenue format is used to indicateto what extent each function is self-sufficient.

II

The second set of statements included in the basic financial statements is the Fund Financial Statements,which are presented for the Board's governmental funds and proprietary fund. These statements presentthe governmental funds on the modified accrual basis of accounting, measuring the near term inflows andoutflows of the financial resources and what is available at year-end to spend in the next fiscal year. Theproprietary fund is presented on the full accrual basis of accounting. The fund financial statements focus onthe Board's most significant funds. Because a different basis of accounting is used in the government-widestatements, reconciliation from the governmental fund financial statements to the government-widestatements is required. The government-wide statements provide information about the Board as aneconomic unit while the fund financial statements provide information on the financial resources of each ofthe Board's major funds.

III

-8-

IIIIIIIIIIIIIIIIIII

II Government-wide Statements

II

The government-wide statements report information about the unit as a whole using accounting methodssimilar to those used by private-sector companies. The Statement of Net Assets includes all of the Board'sassets and liabilities. All of the current year's revenues and expenses are accounted for in the Statement ofActivities regardless of when the cash is received or paid.

The two government-wide statements report the Board's net assets and how they have changed. Netassets - the difference between the Board's assets and liabilities - is one way to measure the unit'sfinancial health or position.

I • Over time, increases or decreases in the Board's net assets are an indicator of whether its financialposition is improving or deteriorating.

• To assess the Board's overall health, you need to consider additional non-financial factors such aschanges in the County's property tax base and the condition of its school buildings and other physicalassets.

IThe unit's activities are divided into two categories in the government-wide statements:

III

• Governmental activities: Most of the Board's basic services are included here, such as regular andspecial education, transportation, and administration. County funding and state and federal aid financemost of these activities.

• Business-type activities: The Board charges fees to help cover the cost of certain services it provides.School food services are included here.

The government-wide statements are shown as Exhibits 1 and 2 of this report.

Fund Financial Statements

I The fund financial statements provide more detailed information about the Board's funds, focusing on itsmost significant or "major" funds - not the unit as a whole. Funds are accounting devices the Board uses tokeep track of specific sources of funding and spending on particular programs.

I • Some funds are required by State law, such as the State Public School Fund.• The Board established other funds to control and manage money for a particular purpose or to

show that it is properly using certain revenues, such as in the Federal Grants fund.IDavidson County Board of Education has two types of funds:

I Governmental funds: Most of the Board's basic services are included in the governmental funds, whichgenerally focus on two things - how cash and other assets can readily be converted to cash flow in and out,and the balances left at year-end that are available for spending. As a result of this focus, thegovernmental fund statements provide a detailed short-term view that helps the reader determine whetherthere are more or fewer financial resources that can be spent in the coming year to finance the Board'sprograms. Because this information does not encompass the additional long-term focus of the governmentwide statements, additional information at the bottom of the governmental funds statements, in the form ofreconciliation, explains the relationship (or differences) between the government-wide and the fund financialstatements. The Board has several governmental funds: the General Fund, the State Public School Fund,the Individual Schools Fund, the Capital Outlay Fund, and the Federal Grants Fund.

IIII -9-

I---------------------------------------------------- -

IIIIIIIIIIIIIIIIIII

II The governmental fund statements are shown as Exhibits 3, 4, and 5 of this report.

II

Proprietary funds: Services for which the Board charges a fee are generally reported in the proprietary fund.The proprietary fund statements are reported on the same full accrual basis of accounting as thegovernment-wide statements. Davidson County Board of Education has one proprietary fund - anenterprise fund - the School Food Service Fund.

The proprietary fund statements are shown as Exhibits 6,7, and 8 of this report.

III

Financial Analysis of the District as a WholeNet assets are an indicator of the fiscal health of the Board. Assets exceeded liabilities by $168,402,742 asof June 30, 2011. The largest component of net assets is invested in capital assets, net of related debt, of$152,254,065. It comprises 90% of the total net assets.

I

The following is a summary of the Statement of Net Assets:

Corllensed SeterrentofNet ~tsJune30. 2011 aid 2)10

Govemmmta Activities Business-type Activites Tota Pri mary Govemrrent

6-3()'11 6-30-10 6-3()'11 ~3l-10 ~3l-11 6-3l-10

Curreri assets $ 26;447,346 $ 22,143,52) $ 4.013,904 $ 3,417,800 $ 3l,461 ,200 $ 25,561,386

Capta assets 152,529,788 148,3Z3,775 803,281 8$,344 153,333,000 149,220,119

Tota asses 178,977,134 170,467,200 4,817,185 4,314,210 183,794,319 174,781,505

Curreri lallites 11,957,684 10,371,012 143,236 188,4$ 12,100,92) 10.559,508

Lorg-tenn liallities 3,290,658 2,788,004 3,200,658 2,788,004

Tota looilies 15,248,342 13,1fB,016 143,236 188,4$ 15,391,578 13,347,512

Investe:! i1 capta asses,net ci reated debt 151,450,784 147,667,411 803,281 8$,344 152,254,065 148,563,782

RestJtted net assets 2,294,803 3,251,800 2.294,803 3,251.808

Unrestrtted net ass Ets 9,983,206 6.3~.033 3,870,668 3,229.370 13,853.874 9.618,403

Tota net asses $ 163,728,793 $ 157.300,279 $ 4,673,949 $ 4.125.714 $ 168,4<r2,742 $ 161,433,993

III

II

I

Note that net assets increased during the year, indicating an improvement in the financial condition of theBoard. The increase in net assets (4.3%) was due largely to the increase in capital assets in thegovernmental activities due to new school construction. Unrestricted net assets increased in the businesstype activities primarily because of an increase in current assets in the Child Nutrition Fund. Also note thatthe Board carries capital assets for which Davidson County carries the offsetting debt.

I

IIII

-10-

---- - -------

IIIIIIIIIIIIIIIIIII

'0 ~Ol'O£ aunr papua JeaA a4l JOJLP8'OP£$pue ~~Ol'O£ aunr papua JeaAa4l JOJ9£t8P9$ paseaJou! slasse lau Al!J\!lOeadAl-ssau!sna 'O~OlU! anuaJ\aJ I~Ol JO %69'8L paluasaJdaJanuaJ\aJ a41 'Aauow leJapaJ pue alelS palo!JlsaJ JO SlS!SUOO~~OlJOJanuaAaJ leluawwaJ\06 lelol10 %89'LL6u!u!ewaJ 84110 40nVII '%6£'l pappe 6u!punj 81e1SP8l0!J1S8JUnpue %lO'6~ seM 6u!PUn1Alunoo 'O~OlUI '~Wl JOJ%£6'£ Ja4l0Ue pappe 6u!punJ a1elS pa10PlSaJUnal!4M anuaJ\aJ leluawwaJ\06 lel01 JO %6£'8 ~pasudiuoo 6u!purlJ Aluno~ '~~Ol JOJsasuadxa aso4l JO %6'9 ~dn apew sao!J\Jasuocdns ap!M-Wa1SAsal!4Msasuadxa adAl-leluawwaJ\06 le10l JO %6'08 pasuduioo sasuadxa sao!J\Jas leUO!lorulsul 'O~Ol U! u0!lI!W8l$ JO Slasse lau U! aseaJou! ue Ol paJedwoo '~~Ol'O£ aunr le UO!ll!W9$ le spuas siassa lau U! aseaJou!a4l'Sa!l!J\!lOe adAl-ssau!snq a41 Ol SJaJsueJ1Jall'i 'O~Ol'O£ aunr papua JeaA a4l JOJUO!lI!w ~p~$ pale101sasuadxa pue uo!lI!w OH$ aJaM sanuaJ\aJ 'AlaJ\!leJedwo~ '~Wl'O£ aunr papua JeaA a4l JOJu0!ll!W 9P~$palel01 AJ06aleo S!4l U! sasuadxa al!4M UO!ll!W19~$ JO sanuaJ\aJ pa1eJaua6 sa!l!J\!lOe leluawwaJ\06 lel01

£66'££n9~ $ Zvaof99~ $ v~L'm'v $ 6V6'£L9'v $ 6Lt90£'m $ £6L'9um $

099'00S'6Z 6vL'996'9 6stLL9 s£t9vg ~09'£Z9'9Z v~S'OZv'9

(6SL'Ov9) (Lsv' ~6)6SL'Ov9

09S'SZO'9v~~~S'9LL'Ov~Z9fZ££'9Z9V'Z££'9

99£'LL6'6v~LL9'00t6

ZvO'9S£'vS~Z9V'W;'9

LL9'00t6LL9'00t6

VOV'£~9'£6~6'L£90S'~SZV9'Z9990'9SL'~ZZL6'V£0'm

L90'L9fv906'ZV696'9909'9LO~£'L£Z'£Z00L'ZH'9~~

VOf£~9'£6~6'L£90S'~SZW'Z9990'9SL'~ZZL6'v£0'S~~

L90'L9fv906'ZV696'9909'9LO~£'L£t£Z00L'ZL~'9~~

~SS'L£S'ZS~wt£vo'S£

~L9'OvO'OH999'~L9'SS

LL£'L£f69~S'vZ

Ovt69L'9V£9'ZZ

9vt9Lv'6H9ov'969'SS

ZO£'6zt9a960'990'S£

96S'9£ veS'LS veS'LS

VZ£'S~6'9~~ 9S0'999'm 999'SZ~'S 6vV'9~L'v 9£f69L'£~~ L09'69~'LH

OZ6'6Z9'v $ WS'HnZ~ $ ~L6'99tv $ LS6'LvO'v $ 6V6'ZV£ $ 960'L9Z $

~uawwaAO~ ,{Jew!Jd 18101 sa!l"'~1f IBluawwaAo~

~asslf ~aNU!sa6ue4::) pue 'sasuadx3 'sanuaAa~ JO ~uawalBlS pasuapuo::)

IIIIIIIII

~asse ~auU!(sseaosp) aSeaJoul

(~no)U!SJaJsUeJ1

sasuadxa le~ol9:l!f\Jas POO:l

:sa!l!A!pe adAj-ssau!snsuonepaJdaa

~qapWJa~-6uoluo ~saJa~ulsafiJe40 pawweJ60Jd-uON

s9:l!AJas,{JeIl!OUIfs9:l!AJaslJoddns ap!M-wa~s.<s

s9:l!AJas leUO!pnJ~SUI:sa!l!A~e IBluawwaAo~

:sasuadx3

IIIIsanUaAaJle~o1

sanUaAaJJa410:sanUaAaJleJaUa~suo!lnq~uoo

pue ~ueJ61B1!de::JSUo!~nq!J~uoo

pue ~UeJ6 6u!~eJados9:l!AJasJOJsafiJe4::J

:sanUaAaJweJ60Jd:sanuaAa~

IIIIII

'JeaA leosu lUaJJnOa4l JOJPJeOaa4l JOJsasuadxa pue sanuaJ\aJ a4l SM04Salqel 6U!MOIIOJa41

IIIIIIIIIIIIIIIIIII

II Financial Analysis of the Board's Funds

Governmental Funds: The focus of Davidson County Board of Education's governmental funds is to provideinformation on near-term inflows, outflows, and balances of usable resources. Such information is useful inassessing the Board's financing requirements.I

I The Board's governmental funds reported a combined fund balance of $19,349,199, a $2,841,037 increaseover last year. Revenues and other financing sources exceeded expenditures and other uses in the amountof $1,699,841 in the General Fund, $682,735 in the Other Restricted Fund, $395,246 in the Capital OutlayFund, and $63,215 in the Individual Schools. Two sources of funding increased over the prior year: Statefunding increased $3,148,855 and Federal funding increased by $1,784,749. County funding decreased by$4,389,771. Expenditures increased by $3,550,546, which included $2,335,873 in the State Fund.

IIIIII

Proprietary Fund: The Board's School Food Service Fund performed well in the past year. Revenuesdecreased $648,137 while expenses decreased by $867,415 when compared with the previous year. Thedecrease in expenses primarily consisted of food purchases decreasing by $392,796 while suppliesdecreased by $48,775.

Expenditure analysis: Instructional programs represented 84% of governmental expenditures, excludingcapital outlay. Total governmental expenditures are categorized below:

Categorization of Expenditures forGovernmental Funds (excluding capital outlay)

IIIIIIIII

84%

o Instructional Programs

• System-Wide Services

oAncillary Services

n Non-ProgrammedServices

Expenditures presented on modified accrual basis of accounting.

General Fund Budget Highlights

Over the course of the year, the Board revised the budget several times to account for changes in revenueexpectations but was able to keep spending below the amended budgeted amounts. Even with thereductions in revenue, the Board was able to reduce spending and end the year with a surplus.

-12-

IIIIIIIIIIIIIIIIIII

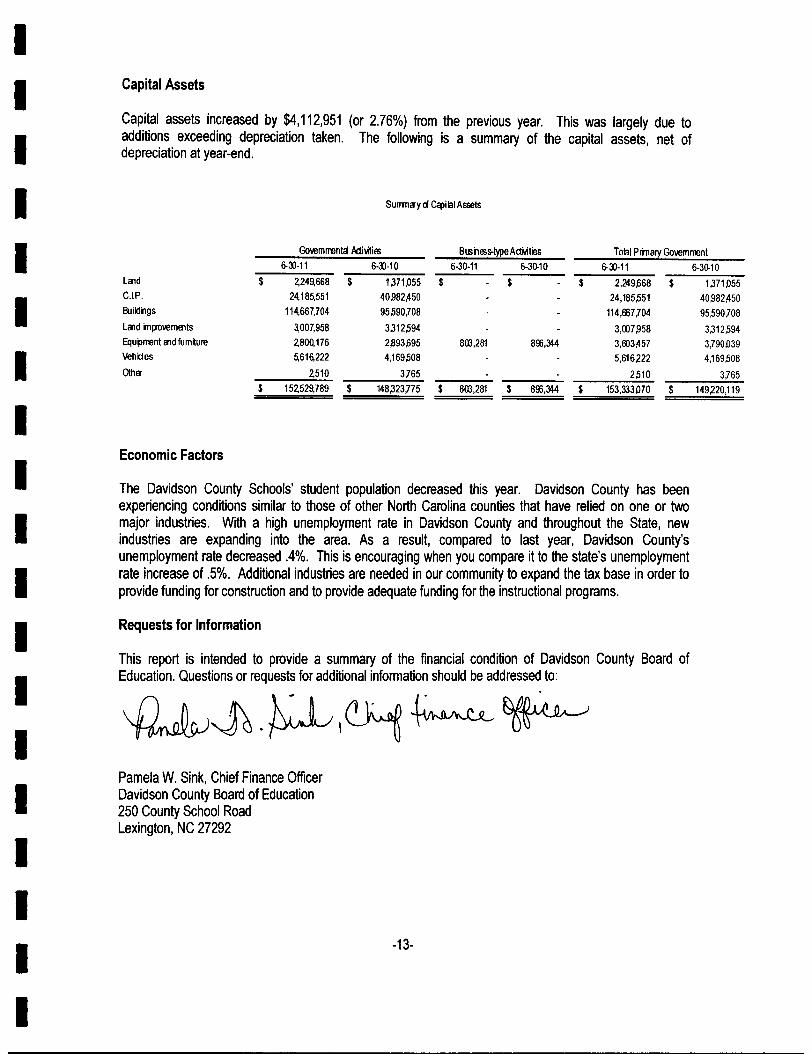

II Capital Assets

III

Capital assets increased by $4,112,951 (or 2.76%) from the previous year. This was largely due toadditions exceeding depreciation taken. The following is a summary of the capital assets, net ofdepreciation at year-end.

I

Suml1!JYd Ccpitll Assets

GowmrrentclMillitie; BLSile;!rlypeAdM ties Totll Prinary Govemrrent6-lJ·11 6·lJ·10 6·30·11 6·3()'10 6-lJ·11 6·3()'10

LCIld $ 2,249,668 $ 1,371.055 $ $ $ 2,2491)68 $ 1,371.055C.LP. 24,185,551 40,982,450 24,185,551 40,982:f50Buildilgs 114,667,704 95,590,708 114,667,704 95,590,708LCIld injlOwments 3,007,958 3,312,594 3,007,958 3,312,594Equprrent CIldfumlure 2,800.176 2,893,695 803,261 800,344 3,603:f57 3,790.039Vehoes 5,616,222 4,169,508 5,616222 4,169,508Othff 2,510 3,765 2,510 3,765

$ 152,529,789 $ 148,323,775 $ 803,261 $ 800,344 $ 153,333.070 $ 149220,119III

Economic Factors

II

The Davidson County Schools' student population decreased this year. Davidson County has beenexperiencing conditions similar to those of other North Carolina counties that have relied on one or twomajor industries. With a high unemployment rate in Davidson County and throughout the State, newindustries are expanding into the area. As a result, compared to last year, Davidson County'sunemployment rate decreased .4%. This is encouraging when you compare it to the state's unemploymentrate increase of .5%. Additional industries are needed in our community to expand the tax base in order toprovide funding for construction and to provide adequate funding for the instructional programs.

I Requests for Information

This report is intended to provide a summary of the financial condition of Davidson County Board ofEducation. Questions or requests for additional information should be addressed to:I

II

Pamela W. Sink, Chief Finance OfficerDavidson County Board of Education250 County School RoadLexington, NC 27292

III -13-

I

IIIIIIIIIIIIIIIIIII

I-r~- I'Juaw81Els S!4J10 lJed leJllaJu! ua aJe Sluaw81Els lepueu~ a4J oJs810u a41

IIIIIlv L'Z0V'89~ $ 6v6'£L9'v $ £6L'8lL'£9~ $ Slass'v' JaN IEloI

vL8'£S8'£~ 899'OL8'£ 90l'£86'6 pap!JIsaJUn£OO'ggn £00'99£'~ S1004:lSlenp!i\!pul

IL8n98 L8tL98 spa[oJd II'lI!de~£~S'~g cis'rs aJrqeJS8lElS Aq uo~ez!l!ql'llS

: .IOJ P81:l!.lIsa'tlS90'vstls~ ~8l'£08 veL'OSV'~s~ Jqap P81elaJJOJau 'Slasse II'lI!de:l U!P81sai\ul ISlass'v'JaN

8LS'~6£'S~ 9£l'£v~ lV£'8vtS~ sa~!I!qe!1IElO I I8S9'06lt 8S9'06t£ JeaA auo ue4J aJOWU!ana~98'9£6'v 688'l8 lL6'£S8'v JeaA auo U!4J!Mana

:sa~!I!qe!1WJaJ-lluolS9S'S S9S'S alqeAed JsaJaJu!panJ:l:l'v' ILO~'68~ S£6'89 lH'O£~ anuai\aJ pauJeaunSvg'O~ Svg'O~ SlUaWUJai\oll Ja4JOCllanalvL'8S6'9 Un 0££'LS6'9 sasuadxa penooe pua alqeAed Sluno:l:l'v' Isa~!I!qe!1

IOl£'v6L'£8~ 98~'H8'v S£~'LL6'8H Slass'v'leJol

OLO'£££'£S~ ~8lt08 68L'6lS'l9~ Slasse II'lI!dI'l:lIElOI~S8'L68'9l~ ~8t£08 OLS'v60'9l~ uo~epaJdap JOJau 'Slasse IEl!dl'l:l Ja4JO I6~l'S£V'9l 6~l'S£V'9l ssaJlloJd U!UO~:lnJjSUO:lpue 'Sluawai\oJdw! 'puel

('v 'III 8l0N) Slasse IEl!de~l~6'9 l~6'S SluaUJjsai\ul IOvL'Ll£ OvL'Ll£ sa!J0Juai\UIl£9'S£l'9 l68'69~ Ovg'S90'g SjuawuJai\oll Ja4JoUJOJj ana£L9'8£ 60L'9~ v96'~l snoauena:lS!w - alqei\!a:laJ Sluno:l:l'v'£6£'£S8'£l $ £9S'66V'£ $ 0£8'£S£'Ol $ SlUalei\!nba qseo pua 4se~ ISlass'v'

IElol sa~!~:l'v' sa~!i\~'v' IadAJ-ssau!sna IEluawuJai\o~JuaWUJai\O~AJeW!Jd

I~~Ol'089unrSl9SS" 19N JOlU9W9lelS

UO!leOnp3 JOPJe08 AlunOQ UOSP!fleO I~ 1!Q!4X3

IIIIIIIIIIIIIIIIIII

unosOU'tHsss'ssL'ISZS'Htv,IS'SStS,LS'LSL'lZ

(S,£'Lso'szlm,££,"S'££, $

(£StI£s'SZ) $(L9O'Let',)(SOS'Z,)OH'96£(SSI'I:)(ISI>',SS)(ssl'm)(SLL'S£I)(£,O'o£tI)(£,L'£I>I'S)(£SS'OSS)(SSS'Z)

(SSS'.£)(SIS'£ZS)

(£ZS'ILI>'I)(m'66S)(LSS'ISL'I)(SSL'L£Z'I)ogo'tttl(LSI'S,I'S) $

!BIOI seg!Jl!l:l\fad.l!-sseu!sna

$

(retl£s'sZ)

$

(£Stl£S'SZ) $(L9O'Let',)(SOS'Z,,)OII'SS£(SSI 'I:)(ISI>'"SS)(991'01)(SU'S£I)(£vO'O£tl)(£I>L'£vl'S)(£Ss'OSS)(SSs'z)

(SSs'.£)(SIS'£ZS)

(£ZS'ILI>'I)(SII>'SSS)(LSS'ISL'I)(SSL'L£Z'I)ogo'tttl(LSI 'SVI 's) $

sag!Jl!l:l\fJIlluawuJaIlOEj

$

$

IUawwal\OE>.lJew~dslassy IaN U!sa6uBq:) PUBanuaAaH (asuadX3) IaN

'luawalejS 5!4110 lied leJBalU! ue aJe 51uawalBlS IBloueu!l a41 01 seiou a41

"SS'LS

$

sWIIJ60Jdsno~eA alii jO sesuadxa I:l9JP alii U!papnpu! S!IBlII UOgB!~aJdapalii sepnpxa lunowB S!ql (I)

SJajsuBlIpal~!lISaJUn- snoaUBII9~S!~

pal~!JIsaJun- s6u!wea IUauqSaAUIIIII!dB~- suo~B~oJdde al9lS pal~!lISaJUn

6upBJado- SUOPB~Jdde 9191Spal3!l1SaJun1II1!deo- SUOPB~JddB ~uno~ pal~!lISaJUn

6uPeJado- sUOPB~JddB ~uno~ pa13!l1SQJUn:senU9AaJjI1J9UQE>

Zj7Q'99£'t91 $ luswWQl\06 .(Jew~ !BIOIZSI>'Z££'S seP!II!I3Bad.I!-sseu!snq 1910IZSI>'Z££'S $ e~!N9sPOOjpoq~S

:seg!Jl!l~BedA!-sseu!sna

OSS'SZO'S'I $ sag!Jl!l~BI91uawwal1061910IL9O'Let" asu9dxa UOgB!~ palB~llBun (I)SOS'Z" 1Q9PWJeI-6uOIuo ISQJalulSSS'S se1lm4~pawWIIJ6OJd-uON9OS'SL se~!JU9S.(Jg1!~UV£SS'vLtl SUOgBI9J~!lqnd PUBd!4SJ9peal'A~!PdSSI'OI se~!11J9SSUOPBIaJ!dnd 9P!M-WaISAs£zf£s£ .It!lqBluno~~'v'ISS'SLS'I sa:unoSaJuewn4 PUBI9~UBU!:l9Z1'm'LI jJOddns19uogeJadoSZS'S£I'I lJoddns A6opU4~alSsg"LZ luawdo~pUB

IJOddnsse~!JU9SpU8 SWBJiloJdaAg8wairdSLO'ISZ luawdOI9A9p PUBIJOddnsuogB"dod 19!~ds1£L'009 luawdol9l19P PUBjJOddns

:se~!AJaSjJOddns9P!M"WalsASISI>'ZS£'6 jJOddnspaseq-poq~Ssotopg'" J9,,~!Un:l-O:JZSl>'svS'L d!4SJapealpoq~S£ZL'£I>I'L sa~!JU9sPUBSWlIJiloJdaAgBwalrdSvtiZtSI suogB"dod 19!~adsILS'SSS'U $ JB,,6aH

:swBl60Jd I9Uog~lUIsUI:sag!Jl!l~BIBIUawUJaAOEj:luawwaAOE>.(JBW~d

sesu9dX3 swru60Jd I suog~un~

$

Sso'sss'm sStt'SIL'VS,I>'SIL'v $

LOS'SSI'LH $

SSO'"OI7OS;'£Lz£toss

etS'S,Z9£S'SvLas'SOS'LUL'SSVZ"L'ILZ

OZS,£,ZSH'UZ

SSS'OSS'LLSL'ove'£SSI>'LSI'SLSS'gas'SSStlLI>'LIsstsss'vS $

$

$

960'LSZ $

£sl>'9ZS'LSI $ 069'96L'£ $ £SL'SU£91 $ 6upua - SlaSSBIaNV£L'SSS'091 Sgj7'ett£ SLteOC'LSI 6u!uu!6aq - slassB IaNBHA'.JiB))B))i))~iiiiiiiiiBBS_BB));!:B);i);ijiiiiiiii;)~iji.i$)))))a,:)))i!iimij... mmiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiiii••m!ii!i!iiiiiiiiiiii!iiiiiiiiHi~i~~~~~i!;i!:SSO'990'9£ 16tvH LOS'ISS't£ SJajSUI!JjPUB'SW9l! I9pads 'senuaAaJ jI1J9ua6!B10I

LSV'lS (LSflS)UnosSStV6sSS'SSL'1SZS'Htv"IS'SStS"LS'LSL'lZ

$

$ $

suognq!lluQ:JPUB

SjUIIJE)IBlidB:J

sa~!JU9SJOjSa6JBlj:J

suognq!lluQ:JPUB

SjUIIJE)6ugeJado

sanuaAaHWBl60Jd

- -- - - -~~O~'0£ aunr papua JWA IBOS!::1

sa!l!II!)OV 10 jUaUJajelSuO!lBonp310 PleOS Alun08 UOS!pIIBa

- - - - - - -- -- - - -

IIIIIIIIIIIIIIIIIII

-g~-

luaWatetS SlID10lJed Iw6aIU! ue rue SjuawalBis lepueuIJ aID 01salou all!

£SL'81L'£9~ ~ satl!A!j:)e leloowwat\06 JOSjesse IaN

(l>6~'og~'8) "("8'3 aloN) SpullJ 9111U! pejJOdaJ IOUale9JOlaJalll pue p!)!J9d luaun:> atn U! a,qe'(ed pue anp IOU ale 1e41satlmqen

88L'619'l9~ 'spullJ 9111U! pelJodal IOU ale aJOjQJ941pueS9:>JnosaJ lepueuy IOUaJe S9!1!An:>elelUaWwaA06 U! pesn Sjesse lel!d~

:asne:>aq IUB.I9Jl!Pale (~ 1!Q!4X3)Sjesse lau JOloowalllls atn U! S9!1!A!j:)e IBluawwaA06 JOj pejJOdaJ Sjunow\f

l!t9'lSL'£ S l£t'60n $ lSE'6£t $ m'tlO't s t96'~otm $ lOL'l99'9 $ soouelea pun:! pue samlen lelO1

66~'StE'S~ 89<:'»£'l £OO'99£'~ ttO'61~'m t88'609'9 soouelea pun:!IBIO 16l£'O~g'~~ 89S'~90'O~ ~l£'8W~ peu6!sseunOCL'9£~'t OCl'9£~ OOO'OOO't SaJIlI!PUadxa S,Iea.( luanbasqns

:pau6!ss\f£OO'99£'~ £OO'99£'~ SIOO4:>SlenPi"!PUI£S9'80l ES9'80l .(enno lelide:> iOOIl:>Sm'1l9'~ 9l>6'86V'~ 980'l9 m'~9 allllelS alelS .(q UO!!eZ!I!QeIS

:peP!llsa~:sooueleq pun:!

9lV'~t~'l 08£'£9n 6l£'£t lS£'S£l> m'tlO't O~S'li £l8'l90'~ sanmqe!llllio 1W'OC~ ltE'£t 8l8'99 l66'S£ anUaAal peweaun9W'O~ 9W'm sluawwaA06 Ja410 01 ana6l£'£t 6l£'£t SPUIlj JatnO 01anaQ£t'l9S'9 $ 08£'£9n $ $ 9ffi'00t S S9~'lOO't $ £~S'l£ $ £l8'l90'~ $ saml!qe!l penJ:>:>epue alqe.(ed SjunO:>:>\f

:S9!I!I!Qensoouelea pun:! pue sa!l!I!QBn

9l9'OOV'91 $ l!t9'lSL'£ $ l£t'6Ot'~ $ l6£'S£t $ m'tlO't S t9S'~oto~ $ lOL'l99'9 $ Sjass\fIllIOl

OW'990'9 ~86'9lV'~ l6£'S£t l66'£90't 19L'tl m'~9 SjuawwaA06 JB4Io WOlJ ana6l£'£l> 6lE'£l> SPUIlj Ja4l0 WOlJ anat96'~l t96'~l snoauella:lS!W - atQeA!B:l8JSjUno:>:l\fUS'9 U6'9 sluaUJjsaAulOC8'£9£'Ql $ EOL'861'l $ l£t'60V'~ $ $ 9W'O~ $ 99S'81~'O~ $ l>6~'gog'9 $ SIU9ieA!nba 4se:> pue 4se:>

slass\f

spun:! .(ellno SJOO4:>S pun:!Sj~ pun:!1OO4:>S pun:! peP!lIsa~ leJau98Illluawwat\08 lelide:> lenp!A!PUI leJ9P9:l :l!1Q11cf alelS .Jalj1O

lelOlspun:! JOfew

~~Ol'0£ aunrspun:lleIUaWUJaA0E>

1994S a:lUBIBaUO!leOnp310 pJBOa Alun08 UQSp!ABa

£I!Q!4X3- - - - - - - - - - - - - - - - - - -

IIIIIIIIIIIIIIIIIII

luawaJBlS S!4t 10 IJBd IBJ6aJU!ue aJe SJuawaJBJsJI!~ueu!l a4t oJ ssiou a4l

66~'6t£'6~ $ 89t»£'l s £OO'gg£'~ $ $ s m'6U'O~ s m'609'9 $ JeaA)Opua Ie sooueleqpun:!

W ~'sos's ~ 1lO'6t6'~ BIlL'lO£'~ SOC'gvv'6 £vO'o~st JeaA)0 llu!uu!llaq Ie sa:Jueleqpun:!

L£O'~vS'l gvt96£ siz'es 9£L'lS9 ~VS'669'~ a:Jueleqpun) U!allue4:JIaN

~99'990'l 699'l£L'£ (SH'999'~) (sasn) ssomos llupueu!jJalllO lelol(L9n6) ~99'vL9'~ (S~~'ggg'~) (1Il0)U!SJa)sueJlaoo'gg~'l SOO'S9~'l panss! SUO!lell!lqoesauomd luawlieisul

:(sasn)SOOJnOSllupueu!) Ja410

9SnLL (£lv'L££'£) 9~lt9 sczzss 696'99£t saJnI!puadxa(Japun)JaAOsanuaAa~

9~tvStl9~ 90~tS9' ~~ lL9'LLL'£ S6£'S66'9~ L9£'gvS'S6 S~O'OO9'l v9L'6L£'S~ saJnp'puadxalelo1»£'09 »£'09 ISaJalUI~t£'g£L'~ ~t£'g£D ledpuPd

:a:J!AJasIqeOgyg'£tt'Z gyg'£tt'l sal:J!llaAJOIOWpua sasns£09'6£9 £09'6£9 IUawd!nbapua aJnp.wn:!lLtv~S'g utv~S'g sllu!PI!nqpus AIJadoJdlea~

:Aellnolel!de::JlW'6£v ££g'O~v (t£v'g) £l9'9£ sallJe4:JpawweJIloJd-U°Nggsts 9lv'v 9lO'69 voot l~9'9 sa:J!AJasA.iellPuvL~L'vg9'll SlV'£6S'l OW'vgg'S VSt£6v 9L£t~L'O~ sa:J!AJasap!M-tlJaISASVOO'16£'L~~ lL9'LLL'£ lW'oo9t~ gv~'S6~'oo OlS'lO~'l vg£'Vl9'L sWeJlloJdleuo!pruisul

:IUaJJn::J:saJnp'puadx3

ioz'sso 'es ~ £Sg'gt£'S LSL'ova'£ S6£'S66'9~ L9£'gvS'S6 £gL'lst£ £UgvL'~l sanUaAaJlelo1lLLt09'9 ££6'l£ LSL'ova'£ 099'~9~'~ l6£'Sgv Ja4106£6'vgtSl ggo'Ll9'9 £vg'oav ~££'LLnl Alun0::JuOSP!AeOOS6tlV'L~ S6£'S66'9~ lS9'9lv luawwaA08 ·snO~O'9V9'~O~ $ ggg'ggL'~ $ $ $ L9£'9vg'S6 $ S96'v~n $ $ eU!loJe::J4IJON)0 alelS

:sanuaAa~

spun:! Aelino sloo4:JS pun:! SlUeJ8 pun:!loo4:JS pun:! paP!JjSa~ leJaua8leluawwaAQ8 lllP.de::J lenp!A!pul leJ9pa:! :J!lqndalelS Ja410

lelolspun:! Jo!eVi

~Wl 'm:aunr papua JeaA leos!.:!spun.:!IBluawwaflO~

saoueles pun.:! U! sa6ue4:J pue 'SaJnl!puadx3 'sanuafl9t1 JOluawalBlSUO!leOnp3JOpROS ~uno:J UOSp!flea

vl!Q!lP<3- - - - - - - - - - - - - - - - - - -

IIIIIIIIIIIIIIIIIII

II Amounts reported for governmental activities in the statement of activities are different because:

I Net changes in fund balances - total governmental funds

IGovernmental funds report capital outlays as expenditures. However, in theStatement of Activities, the cost of those assets is allocated over their estimateduseful lives and reported as depreciation expense. This is the amount by whichcapital outlays exceeded depreciation in the current period.

I The issuance of long-term debt provides current financial resources to governmentalfunds while the repayment of the principal of long-term debt consumes the current financialresources of governmental funds. Neither transaction has any effect on net assets.This amount is the net effect of these differences in the treatment of long-term debt.ILoss on disposal of asset

I Difference in accrued interest payable and interest expensed on fund statements.

ISome expenses reported in the statement of activities do not require the use ofcurrent financial resources and therefore, are not reported as expenditures ingovernmental funds.

Compensated absences

ITotal changes in net assets of governmental activities

IIIIIIIII The notes to the financial statements are an integral part of this statement.

I-18-

Exhibit 4 Continued

$ 2,841,037

4,207,887

(422,667)

5,565

(211,308)

$ 6,420,514

IIIIIIIIIIIIIIIIIII

luaw9llllS 514110)R!d p!J6etU!ue we SjuawalBls lef:lUeuu 84101S810Uau

m)'sz~'m $ t88'6O!l'S $ .Ee,(JOpoe,. ...... "'q pun~

SOC'9»'S oo'o~s'£ .Ee,(JO~""""~pun~

OO!i'~ (tsi"ul't) s tat'ul't $ US'LSi"Z $ _lUll JOuoge!JdoJddy

S£L'l89 s£L'189 (OO!i'~) Sl£'lZ8'S ~ts'669'~ (t8t'U~'t) (£l8'LSt'll 8OUB~ lUll'"eIIu!tp I8N

£tS'81 (SU'999'~) (~99'''Sln) (000'0.1) (soon)S8OJI1OS Bu!o<.EUV_I"l0l£tS'81 (8U'999'~) (~99'''6ln) (000'0.1) spmJ_,,_Jl

spmJ_WOJJ_Jl:(soon)....... """'"""" JOlIIQ

s£L'189 s£L'189 (OO!i'~) l8L'£sL's 696'99£'£ (US'at'Z) (£l8'LZi"Z) se.r1llpuec!xe(l8pUI1)J811J senuaA8l1

£9tst~'S 86£'866'9~ ~99'''''~'91 otl't88'£~ ZSO'StO'Z LS£'StQ'SS 6Ot'ose'oo~ £8S'99~'OO~ SOZ'j099 S~O'OO9'Z LU't9~'£ ~£t'6LL'l ~tS'zsL's t9L'6L£'S~ soc'w'"z ~OS'£lI'''Z S8JI1I!IlU8dxel8lOl

£~S'St£'£ ££S'O~" !ltO'99L'£ StZ'SZS (jo£t'9) (jo£t'9) OOO'OS~ £ZS's£ £ZS'S8~ O£t'W se6.Etp_J!IoJd-uoN

szi"t szi"" SZO'69 SOO'69 9L9'L9 toS'£ toS'£ Ot6'S Z~S'9 zst'Z~ -~uZ'szl't 8li"£68'Z 6£9'UO'L ~8Z'stL'£ SLI'£9l ozg'j099'S S6L'Lts'S SZS'9LS'9 m'ooc tsz'£6t 9£t'£6L ~t6'Z~L £8t'QS9'Z SL£'£~L'O~ 8S8'~L£'£~ Z99'SW£~ """""'" 81J1M-wetSoIs6£S'~L9'~ Z~O'069'£~ ~SS\9£'S~ m9'S~9'S llS'~8L'~ st~'SS~'06 £oo'086'~6 8L£'Z~Z'£6 L90't9Z ozs'm'z L88'99£'l OSt'990'Z SU '8L6'Z tS£'"zg'L lLt'109'o~ 6Ot'tos'm SWIIJIIoJd_

~U8JJIY.)

:se-"1PJ8dX3

(£gz'stl'6) 86£'866'9~ ~99'''''I'91 at~'t88'£~ (zso'StO'z) LS£'StQ'lI6 6Ot'ose'oo~ £8S'99~'OO~ gzs'su £SL'Z8l'£ LlZ't9~'£ vsiu: ~"Z'~ £zL'9tL'~z Z8t'''''L'~Z SL9'S69'~Z S8I'IU8A8Jl8lOl

ssg'at 099'~9~'~ SL6'OZn 8SI!'ttS'~ ~"n l6£'89t ~S~'L9t JOlIIQ

OO'08t £tS'08t ~££'llZ'~l ~££'llZ'~Z 8L9'S69'~Z .liImo_o(£gz'9i'~'s) 86£'lI66'm ~99'ttI'91 at~'t88'£~ t80'6£~ lQS'SZ" SS"'981 86t'W IlJ8WW8AOO 's'n

$ $ $ (lSO'StO'z) $ LS£'StQ'lI6$ 6Ot'ose'oo~ £8S'99~'OO~ (£tZ'~9l $ 896't~Z'~ UZ'9a~ $ SLS'SU'~ _0 'I!-"N J08IOIS:senue10811

("'!I81leN) "'1lJOV leilpna jeBpna (e"",1leN) IBIlJOV jeBpna leilpna (_1leN) "'1lJOV je8pna je8pna (_lIeN) "1lJOV j86pna j86pna

e_ I"UI~ ,,1JIIItJo e_ ~ "UIfl!Jo ._ ~ IBUII!!JO e"!l!9Od jIIIlI",j IBUlIi!Jo-je8pna -leilpna -j86pna -j86pna

jIIIJI",j1lWA IB"I~ IIWA IB~IIWA IBUI",jIll~_II _II _II8OIJI!-'!1I

pun~_ 0!I<J1d 8IBIS pun~_lIJOl11Q pun~,,~

~~Q(:'0£ 9unr papua Je9A11m!.:Ilenj:)\f pue la6pna - saouelB8 pun.:l U!sa6uell::J pue 'saJI1!!pu9dX3'sanu9119'l:lloluaW911!1S

spun.:l anuall9'l:llepads JOfew pue pun.:lleJ9U98UO!leonP3JO pJeog -<luna::>UOSP!Jlea

SI!Q!IIX3

- - - - - - - - - - - - - - - - - - -

IIIIIIIIIIIIIIIIIII

I Exhibit 6

I

Davidson County Board of EducationProprietary Fund

Statement of Net AssetsJune 30, 2011

I

II

Current assets:Cash and cash equivalentsDue li'om other governmentsAccounts receivableInventories

Total current assets

$ 3,499,563169,89216,709

327,7404,013,904

I Noncurrent assets:Capital assets:

Equipment, netTotal noncurrent assets

803,281

II

803,281

Total Assets 4,817,185

ILiabilities and Fund Balances

Current liabilities:Accounts payable and accrued expensesDeferred revenue- prepayments

Total current liabilities

Total Net Assets

1,41258,93560,347

82,88982,889

143,236

803,2813,870,668

$ 4,673,949

I Noncurrent liabilities:Compensated absences payable

Total noncurrent liabilities

I Total Liabilities

II

Net AssetsInvested in capital assetsUnrestricted

IIIIII

The notes to the financial statements are an integral part of this statement.

·20·

IIIIIIIIIIIIIIIIIII

I Davidson County Board of EducationStatement of Revenues, Expenses, and Changes in Fund Net Assets

Proprietary FundFor the Fiscal Year Ended June 30, 2011

IExhibit 7

III

Operating revenues:Food salesOther

Total operating revenues

I Operating expenses:Food cost

Purchase of foodDonated commodities

Salaries and fringe benefitsIndirect costsMaterials and suppliesRepairs and maintenanceDepreciationSmall equipmentContract and purchase servicesOther

III

Total operating expenses

I Operating income (loss)

INonoperating revenues (expenses):

USDA grants - regularUSDA grants - commoditiesState reimbursement - kindergarten breakfastRental of school propertyInterest earnedLoss on fixed assets retired

Total nonoperating revenue (expenses)

II Income (loss) before contributions and transfers

I Transfers from (to) other funds:Local Current ExpenseCapital Outlay Fund

I Change in net assets

Total net assets - beginning

III

Total net assets - ending

The notes to the financial statements are an integral part of this statement.

-21-

I

Enterprise FundMajor FundSchool Food

Service

3,962,71885,239

4,047,957

3,425,331235,485

3,946,031116,844309,74226,743116,086

97,52458,676

8,332,462

(4,284,505)

4,221,800490,768

4,4301,451

22,834

4,741,283

456,778

41,45750,000

548,235

4,125,714

$ 4,673,949

IIIIIIIIIIIIIIIIIII

IIIIIIIIIIIIIIIIIII

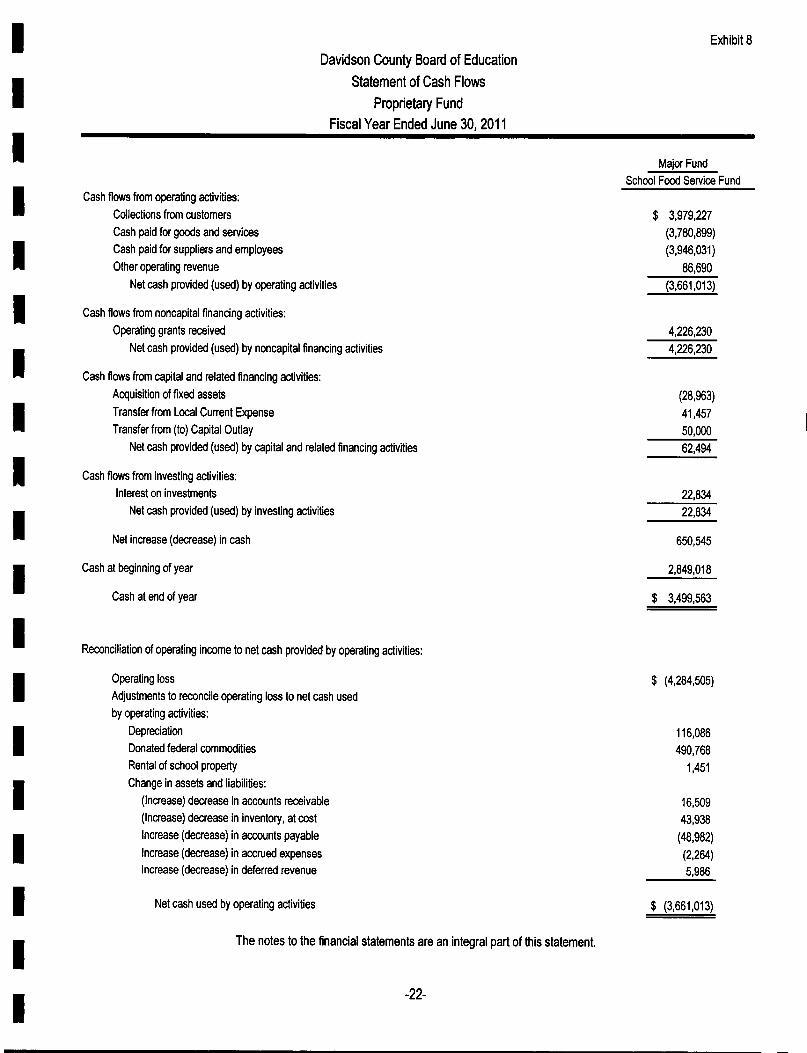

Exhibit 8

DavidsonCounty Boardof EducationStatementof Cash Flows

Proprietary FundFiscal Year EndedJune 30,2011

Cash flows from operating activities:Collections from customersCash paid for goods and servicesCash paid for suppliers and employeesOther operating revenue

Net cash provided (used) by operating activities

Major FundSchool Food Service Fund

$ 3,979,227(3,780,899)(3,946,031)

86,690(3,661,013)

4,226,2304,226,230

(28,963)41,45750,00062,494

22,83422,834

650,545

2,849,018

$ 3,499,563

Cash flows from noncapital financing activities:Operating grants received

Net cash provided (used) by noncapital financing activities

Cash flows from capital and related financing activities:Acquisition of fixed assetsTransfer from Local Current ExpenseTransfer from (to) Capital Outlay

Net cash provided (used) by capital and related finanCing activities

Cash flows from investing activities:Interest on investments

Net cash provided (used) by investing activities

Net increase (decrease) in cash

Cash at beginning of year

Cash at end of year

Reconciliation of operating income to net cash provided by operating activities:

Operating lossAdjustments to reconcile operating loss to net cash usedby operating activities:

DepreciationDonated federal commoditiesRental of school propertyChange in assets and liabilities:

(Increase) decrease in accounts receivable(Increase) decrease in inventory, at costIncrease (decrease) in accounts payableIncrease (decrease) in accrued expensesIncrease (decrease) in deferred revenue

$ (4,284,505)

116,086490,768

1,451

16,50943,938(48,982)(2,264)5,986

Net cash used by operating activities $ (3,661,013)

The notes to the financial statements are an integral part of this statement.

-22-

IIIIIIIII

I

IIIIIIIIIII

----~~"-.-

II

Exhibit 8

II

Noncash operating and noncapital financing activities:

IThe School Food Service Fund received donated commodities with a value of $490,768 during the fiscal year.The receipt of these commodities is recognized as a nonoperating revenue on Exhibit 7 and 0-1.

IIIIIIIIIIIII

-23-

I

IIIIIIIIIIIIIIIIIII

I Davidson County Board of EducationNotes to the Financial Statements

For the Fiscal Year Ended June 30,2011

II. Summary of Significant Accounting Policies

The accounting policies of the Davidson County Board of Education conform to generally accepted accounting principles asapplicable to governments. The following is a summary of the more significant accounting policies:

II

A. Reporting EntitvThe Davidson County Board of Education (Board) is a Local Education Agency empowered by State law [Chapter 115C of theNorth Carolina General Statutes) with the responsibility to oversee and control all activities related to public school education inDavidson County, North Carolina. The Board receives State, local, and federal government funding and must adhere to the legalrequirements of each funding entity.

I B. Basis of PresentationGovemment-wide Statements: The statement of net assets and the statement of activities display information about the Board.These statements include the financial activities of the overall government. Eliminations have been made to minimize the effectof internal activities upon revenues and expenses. These statements distinguish between the govemmental and business-typeactivities of the Board. Governmental activities generally are financed through intergovernmental revenues, and other nonexchange transactions. Business-type activities are financed in whole or in part by fees charged to external parties.

II

I

The statement of activities presents a comparison between direct expenses and program revenues for the different businesstype activities of the Board and for each function of the Board's governmental activities. Direct expenses are those that arespeCifically associated with a program or function and, therefore, are clearly identifiable to a particular function. Indirect expenseallocations that have been made in the funds have been reversed for the statement of activities. Program revenues include (a)fees and charges paid by the reopients of goods or services offered by the programs and (b) grants and contributions that arerestricted to meeting the operational or capital requirements of a particular program. Revenues that are not classified asprogram revenues are presented as general revenues.

II

Fund Financial Statements: The fund financial statements provide information about the Board's funds. Separate statements foreach fund category - governmental and proprietary - are presented. The emphasis of fund financial statements is on majorgovernmental and enterprise funds, each displayed in a separate column.

Proprietary fund operating revenues, such as charges for services, result from exchange transactions associated with theprincipal activity of the fund. Exchange transactions are those in which each party receives and gives up essentially equalvalues. Non-operating revenues, such as subsidies and investment earnings, result from non-exchange transactions or ancillaryactivities.

II

The Board reports the following major governmental funds:

General Fund - The General Fund is the general operating fund of the Board. The General Fund accounts for all financialresources except those that are required to be accounted for in another fund. This fund is the "Local Current Expense Fund,"which is mandated by State law [G.S. 115C-426).

I Other Restricted Fund - The Other Restricted Fund includes specific revenues that are legally restricted for certain purposes andnot intended for the general K-12 population.

IIII

State Public School Fund - The State Public School Fund includes appropriations from the Department of Public Instruction forthe current operating expenditures of the public school system.

Federal Fund - The Federal Fund includes appropriations from the federal government for the current operating expenditures ofthe public school system.

-24-

IIIIIIIIIIIIIIIIIII

I Davidson County Board of EducationNotes to the Financial Statements

For the Fiscal Year Ended June 3D, 2011

IIII

Individual Schools Fund - The Individual Schools Fund includes revenues and expenditures of the activity funds of the individualschools. The primary revenue sources include funds held on the behalf of various clubs and organizations, receipts from athleticevents, and proceeds from various fund raising activities. The primary expenditures are for athletic teams, club programs,activity buses, and instructional needs. The Individual Schools Fund is reported as a special revenue fund.

Capital Ouflay Fund - The Capital Outlay Fund accounts for financial resources to be used for the acquisition and construction ofmajor capital facilities (other than those financed by proprietary funds). It is mandated by State law [G.S. 115C-426). Capitalprojects are funded by Davidson County appropriations, restricted sales tax moneys, proceeds of Davidson County bonds issuedfor public school construction, lottery proceeds, as well as certain State assistance.

IThe Board reports the following major enterprise fund:

School Food SeNice Fund - The School Food Service Fund is used to account for the food service program within the schoolsystem.

I

III

C. Measurement Focus and Basis of AccountingGovemment-wide and Proprietary Fund Financial Statements. The government-wide and proprietary fund financial statementsare reported using the economic resources measurement focus and the accrual basis of accounting. Revenues are recordedwhen earned and expenses are recorded at the time liabilities are incurred, regardless of when the related cash flows take place.Non-exchange transactions, in which the Board gives (or receives) value without directly receiving (or giving) equal value inexchange, include grants and donations. Revenue from grants and donations is recognized in the fiscal year in which alleligibility requirements have been satisfied.

I

Govemmental Fund Financial Statements. Governmental funds are reported using the current financial resources measurementfocus and the modified accrual basis of accounting. Under this method, revenues are recognized when measurable andavailable. The Board considers all revenues reported in the governmental funds to be available if the revenues are collectedwithin 60 days after year-end. These could include federal, State, and county grants, and some charges for services.Expenditures are recorded when the related fund liability is incurred, except for claims and judgments and compensatedabsences, which are recognized as expenditures to the extent they have matured. General capital asset acquisitions arereported as expenditures in governmental funds. Acquisitions under capital leases are reported as other financing sources.

I Under the terms of grant agreements, the Board funds certain programs by a combination of specific cost-reimbursement grantsand general revenues. Thus when program expenses are incurred, there are both restricted and unrestricted net assetsavailable to finance the program. It is the Board's policy to first apply cost-reimbursement grant resources to such programs andthen general revenues.I

IAll governmental and business-type activities and enterprise funds of the Board follow FASB Statements and Interpretationsissued on or before November 30, 1989, Accounting Principles Board Opinions, and Accounting Research Bulletins, unlessthose pronouncements conflict with GASB pronouncements.

II

D. Budgetary DataThe Board's budgets are adopted as required by the North Carolina General Statutes. Annual budgets are adopted for all funds,except for the individual schools special revenue funds, as required by the North Carolina General Statutes. No budget isrequired by State law for individual school funds. All appropriations lapse at the fiscal year-end. All budgets are prepared usingthe modified accrual basis of accounting. Expenditures may not legally exceed appropriations at the functional level for allannually budgeted funds. All amendments must be approved by the governing board. During the year several immaterialamendments to the original budget were necessary. The budget ordinance must be adopted by July 1 of the fiscal year or thegoverning board must adopt an interim budget that covers that time until the annual ordinance can be adopted.

I

I-25-

I

IIIIIIIIIIIIIIIIIII

I Davidson County Board of EducationNotes to the Financial Statements

For the Fiscal Year Ended June 30, 2011

III

E. Assets. Liabilities. and Fund Equity

I

1. Deposits and InvestmentsAll deposits of the Board are made in board-designated official depositories and are secured as required by State law [G.S.115C-444]. The Board may designate, as an official depository, any bank or savings association whose principal office is locatedin North Carolina. Also, the Board may establish time deposit accounts such as NOW and SuperNOW accounts, money marketaccounts, and certificates of deposit. The Board also has money credited in its name with the State Treasurer and may issueState warrants against these funds.

IState law [G.S. 115C-443] authorizes the Board to invest in obligations of the United States or obligations fully guaranteed bothas to principal and interest by the United States; obligations of the State of North Carolina; bonds and notes of any NorthCarolina local government or public authority; obligations of certain non-guaranteed federal agencies; certain high quality issuesof commercial paper and bankers' acceptances; the North Carolina Capital Management Trust (NCCMT), an SEC-registered(2a-7) money market mutual fund; and the North Carolina State Treasurer's Short Term Investment Fund (STIF).

II

The STIF is managed by the staff of the Department of State Treasurer and operated in accordance with state laws andregulations. It is not registered with the SEC. It consists of an internal portion and an external portion in which the boardparticipates. Investments are restricted to those enumerated in G.S. 147-69.1.

The Board's investment in STIF securities are reported at cost and maintain a constant $1 per share value. Under the authorityof G.S. 147-69.3, no unrealized gains or losses of the STIF are distributed to external participants of the fund.

III

2. Cash and Cash EquivalentsThe Board pools money from several funds to facilitate disbursement and investment and to maximize investment income.Therefore, all cash and investments are essentially demand deposits and are considered cash and cash equivalents.

3. InventoriesInventories of the Board are valued at cost and the Board uses the first in, first out (FIFO) flow assumption in determining cost.The inventories of the Board's General Fund consist of expendable materials and supplies, which are recorded as expenditureswhen purchased. Proprietary Fund inventories consist of food and supplies and are recorded as expenses when consumed.

I4. Capital AssetsThe Board's capital assets are recorded at original cost. Donated assets are listed at their estimated fair value at the date ofdonation or forfeiture. Improvements are capitalized and depreciated over the remaining useful lives of the related capitalassets. Certain items acquired before July 1, 1950 are recorded at an estimated original historical cost. The total of theseestimates is not considered large enough that any errors would be material when capital assets are considered as a whole.I It is the policy of the Board to capitalize all capital assets costing more than $5,000 with an estimated useful life of two or moreyears. In addition, other items which are purchased and used in large quantities such as student desks are capitalized. The costof normal maintenance and repairs that do not add to the value of the asset or materially extend asset lives are not capitalized.I

II

Davidson County holds title to certain properties, which are reflected as capital assets in the financial statements of the Board.The properties have been deeded to the County to permit installment purchase financing of acquisition and construction costsand to permit the County to receive refunds of sales tax paid for construction costs. Agreements between the County and theBoard gives the schools full use of the facilities, full responsibility for maintenance of the facilities, and provides that the Countywill convey the title of the property back to the Board, once all restrictions of the financing agreements and all sales taxreimbursement requirements have been met.

III

-26-

IIIIIIIIIIIIIIIIIII

II

Davidson County Board of EducationNotes to the Financial Statements

For the FiscalYear Ended June 30,2011

I Capital assets are depreciated using the straight-line method over the following estimated useful lives:

II

BuildingsEquipment and furnitureVehiclesComputer equipment

20-50 years10-20 years6-8 years3-5 years

Depreciation for building and equipment that serve multiple purposes cannot be allocated ratably and is therefore reported as·unallocated depreciation" on the Statement of Activities.

I5. Long-Term ObligationsIn the government-wide financial statements, long-term debt and other long-term obligations are reported as liabilities in theapplicable governmental activities.

II

6. Compensated AbsencesThe Board follows the State's policy for vacation and sick leave. Employees may accumulate up to thirty (30) days earnedvacation leave with such leave being fully vested when earned. For the Board, the current portion of the accumulated vacationpay is not considered to be material. The Board's liability for accumulated earned vacation and the salary-related payments asof June 30, 2011 is recorded in the government-wide and proprietary fund financial statements on a FIFO basis. An estimatehas been made based on prior years' records, of the current portion of compensated absences.

I The sick leave policy of the Board provides for an unlimited accumulation of earned sick leave. Sick leave does not vest, but anyunused sick leave accumulated at the time of retirement may be used in the determination of length of service for retirementbenefit purposes. Since the board has no obligation for accumulated sick leave until it is actually taken, no accrual for sick leavehas been made.

II

7. Net Assets I Fund BalancesNet assets in the government-wide and proprietary fund financial statements are classified as invested in capital assets, net ofrelated debt; restricted; and unrestricted. Restricted net assets represent constraints on resources that are either externallyimposed by creditors, grantors, contributors, or the laws or regulations of other governments, or imposed by law through statestatute.

I Fund BalanceIn the governmental fund financial statements, fund balance is composed of five classifications designed to disclose thehierarchy of constraints placed on how fund balance can be spent.

II

The governmental fund types classify fund balances as follows:

Nonspendable Fund Balance - This classification includes amounts that cannot be spent because they are either (a) not inspendable form or (b) legally or contractually required to be maintained intact.

IInventories - portion of fund balance that is not an available resource because it represents the year-end balance ofending inventories, which are not spendable resources.

Assets held for resale - portion of fund balance that is not an available resource because it represents the year endbalance of assets held for resale, which are not spendable resources.

II

Restricted Fund Balance - This classification includes amounts that are restricted to specific purposes externally imposed bycreditors or imposed by law.

Restricted for Stabilization by State Statute - portion of fund balance that is restricted by State Statute [G.S. 115C-425(a)J.

II

-27-

IIIIIIIIIIIIIIIIIII

I Davidson County Board of EducationNotes to the Financial Statements

For the Fiscal Year Ended June 30, 2011

II

Restricted for School Capital Outlay - portion of fund balance that can only be used for School Capital Outlay [G.S.159-18 through 22].

II

Restricted for Individual Schools - revenue sources restricted for expenditures for the various clubs and organizations,athletic events, and various fund raising activities for which they were collected.

Assigned Fund Balance - portion of fund balance that Davidson County Board of Education intends to use for specific purposes.

Subsequent year's expenditures - portion of fund balance that is appropriated in the next year's budget that is notalready classified in restricted or committed. The governing body approves the appropriation.

I

Unassigned Fund Balance - the portion of fund balance that has not been restricted, committed, or assigned to specificpurposes or other funds.

II

The Board has no formal revenue spending policy, but does have a informal practice of spending revenues for programs withmultiple revenue sources. The Finance Officer will use resources in the following hierarchy: federal funds, State funds, local nonBoard of Education funds, Board funds. For purposes of fund balance classification expenditures are to be spent from restrictedfund balance first, followed in-order by committed fund balance, assigned fund balance and lastly unassigned fund balance. TheFinance Officer has the authority to deviate from this policy if it is in the best interest of the Board.

8. Reconciliation of Government-wide and Fund Financial Statements

II

a. Explanation of certain differences between the governmental fund balance sheet and the government-wide statementof net assets.

The governmental fund balance sheet includes a reconciliation between fund balance - total governmental funds andnet assets - governmental activities as reported in the government-wide statement of net assets. The net adjustmentof $144,379,590 consists of several elements as follows:

I Description

II

Capital assets used in governmental activities are not financial resources andare therefore not reported in the funds (total capital assets on thegovernment-wide statement in governmental activities column). $ 219,651,243

Net capital assets

(67,121,458)

152,529,785

Less accumulated depreciation

II

Liabilities that, because they are not due and payable in the current period, donot require current resources to pay and are therefore not recorded in the fundstatements:

Accrued interest payableInstallment financingCompensated absences

(5,565)(1,079,004)(7,065,626)

I Total adjustment $ 144,379,590

III

-28-

IIIIIIIIIIIIIIIIIII

II

Davidson County Board of EducationNotes to the Financial Statements

For the Fiscal Year Ended June 30, 2011

II

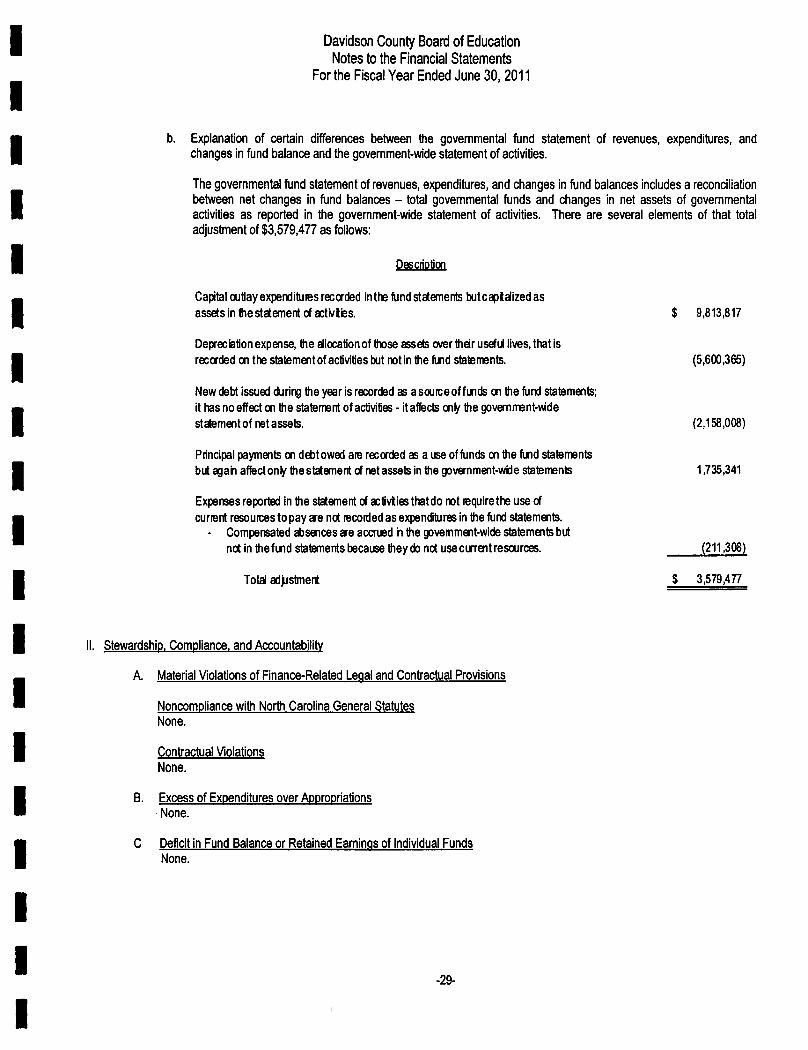

b. Explanation of certain differences between the governmental fund statement of revenues, expenditures, andchanges in fund balance and the government-wide statement of activities.

The governmental fund statement of revenues, expenditures, and changes in fund balances includes a reconciliationbetween net changes in fund balances - total governmental funds and changes in net assets of governmentalactivities as reported in the government-wide statement of activities. There are several elements of that totaladjustment of $3,579,477 as follows:

I Description

II

Capital outlayexpendituresrecorded inthe fundstatementsbutc~iaized asassets in the staement of activies. $ 9,813,817

Depreciationexpense, the allocationof ttose assetsover their usefu lives, that isrecordedon the statementof activities but not in the Md statements. (5,600,365)

INew debt issueddurirg the year is recordedas asourceoffunds on the fund statements;it hasno effect on the statementof activities- it affects on~ the government-wdestaemeot of netassets. (2,158,008)

III

Principalpaymentson debt owed are recordedas a useoffunds on the Md statementsbut agah affecton~ the staement of netassets in the government-wile statements 1,735,341

Expensesreported in the statementof activlies that do not requirethe use ofcurrent resourcesto pay are net recordedas expendituresin the fund statements.

- Compensatedabsencesare accruedh the govemment-widestatementsbutnet in the fund statementsbecausethey do net usecurrent resources. (211,308)

Total adjJstment $ 3,579,477

I II. Stewardship. Compliance. and Accountability

I A. Material Violations of Finance-Related Legal and Contractual Provisions

Noncompliance with North Carolina General StatutesNone.

I Contractual ViolationsNone.

I B. Excess of Expenditures over AppropriationsNone.

I C Deficit in Fund Balance or Retained Earnings of Individual FundsNone.

III

-29-

IIIIIIIIIIIIIIIIIII

II

Davidson County Board of EducationNotes to the Financial Statements

For the Fiscal Year Ended June 30, 2011

II

III. Detail Notes on All Funds

I