Embed Size (px)

Citation preview

1

2

Important Notice

This presentation of Hyundai Heavy Industries (HHI) contains forward-looking statements relating to HHI’s

operations that are based on management’s current expectations, estimates and projections. Words such as

“anticipates”, “expects”, “intends”, “plans”, “projects”, “schedules”, “estimates” and similar expressions are

intended to identify such forward-looking statements. These statements are not guarantees of future performance

and are subject to certain risks, uncertainties, and other factors including new order flows, FX rates, steel plate

prices and so on, some of which are beyond company’s control and are difficult to predict. Therefore, actual

outcomes and actual results may differ materially from what is expressed or forecasted in such forward-looking

statements. The reader should not place undue reliance on these forward-looking statements. HHI undertakes no

obligation to update any forward-looking statements to reflect subsequent events.

3

Contents

H H I at a Glance

Business Performance

Financial Performance

Appendix (Quarterly Results)

4

HHI at a Glance

5

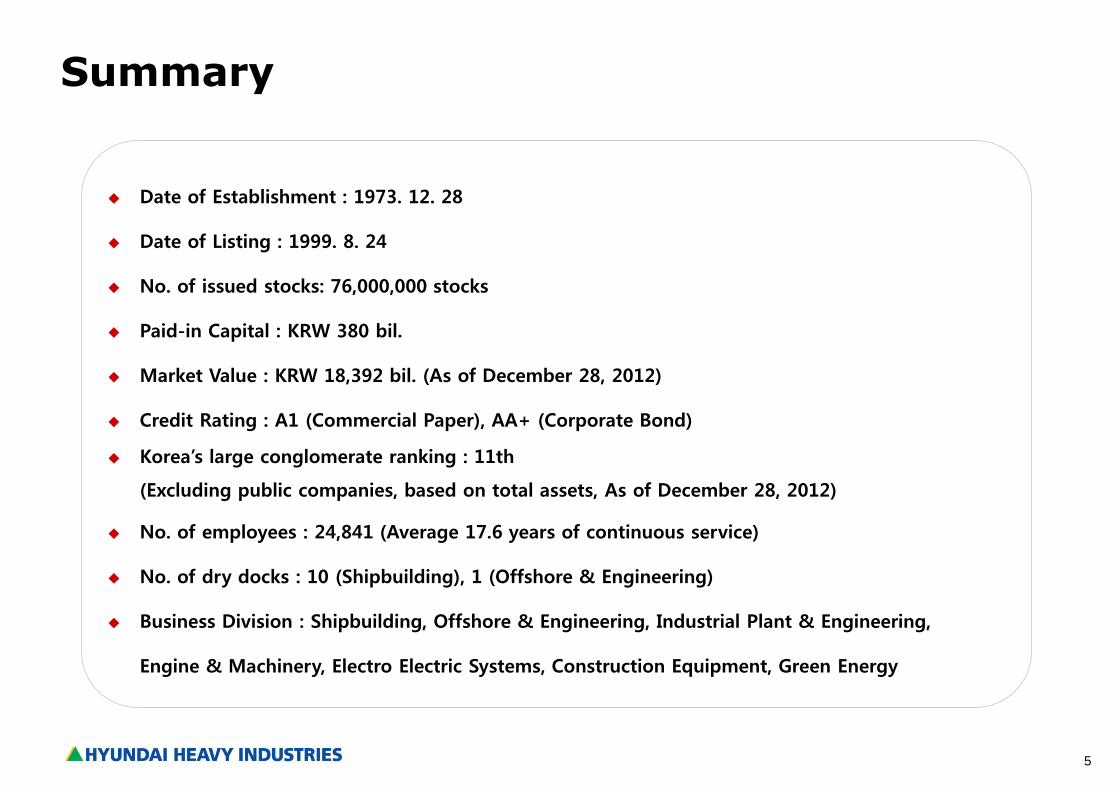

Date of Establishment : 1973. 12. 28

Date of Listing : 1999. 8. 24

No. of issued stocks: 76,000,000 stocks

Paid-in Capital : KRW 380 bil.

Market Value : KRW 18,392 bil. (As of December 28, 2012)

Credit Rating : A1 (Commercial Paper), AA+ (Corporate Bond)

Korea’s large conglomerate ranking : 11th

(Excluding public companies, based on total assets, As of December 28, 2012)

No. of employees : 24,841 (Average 17.6 years of continuous service)

No. of dry docks : 10 (Shipbuilding), 1 (Offshore & Engineering)

Business Division : Shipbuilding, Offshore & Engineering, Industrial Plant & Engineering,

Engine & Machinery, Electro Electric Systems, Construction Equipment, Green Energy

Summary

6

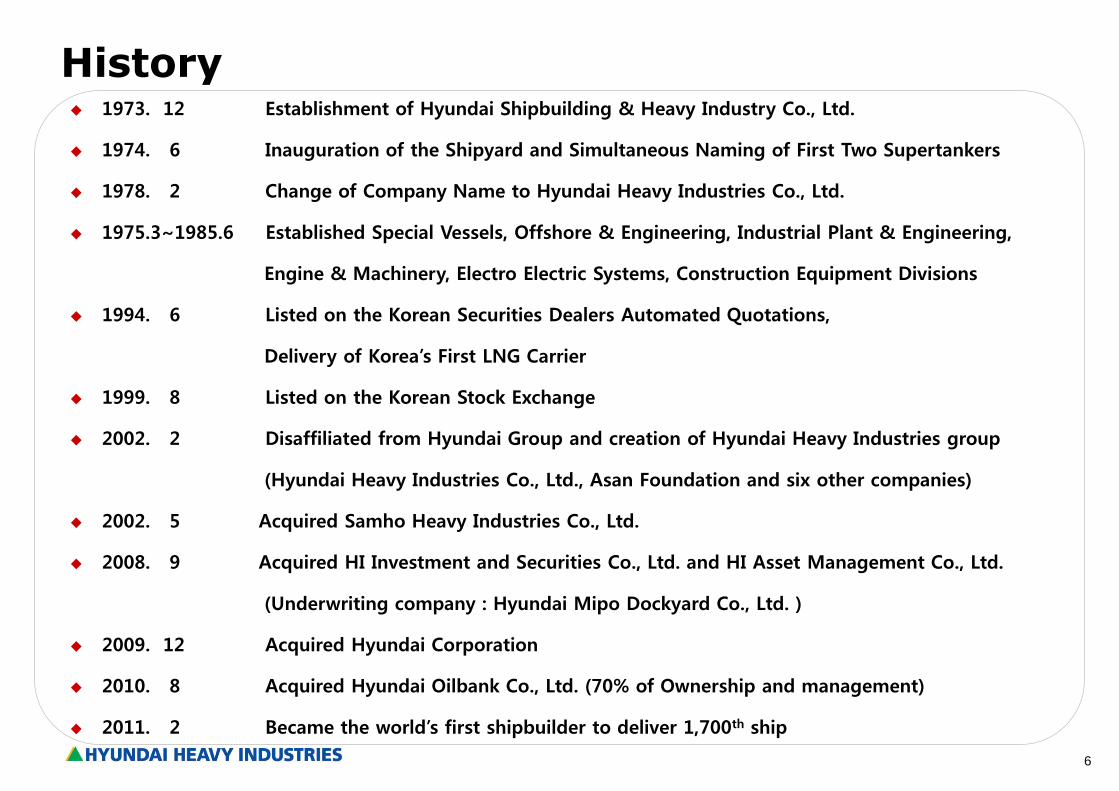

1973. 12 Establishment of Hyundai Shipbuilding & Heavy Industry Co., Ltd.

1974. 6 Inauguration of the Shipyard and Simultaneous Naming of First Two Supertankers

1978. 2 Change of Company Name to Hyundai Heavy Industries Co., Ltd.

1975.3~1985.6 Established Special Vessels, Offshore & Engineering, Industrial Plant & Engineering,

Engine & Machinery, Electro Electric Systems, Construction Equipment Divisions

1994. 6 Listed on the Korean Securities Dealers Automated Quotations,

Delivery of Korea’s First LNG Carrier

1999. 8 Listed on the Korean Stock Exchange

2002. 2 Disaffiliated from Hyundai Group and creation of Hyundai Heavy Industries group

(Hyundai Heavy Industries Co., Ltd., Asan Foundation and six other companies)

2002. 5 Acquired Samho Heavy Industries Co., Ltd.

2008. 9 Acquired HI Investment and Securities Co., Ltd. and HI Asset Management Co., Ltd.

(Underwriting company : Hyundai Mipo Dockyard Co., Ltd. )

2009. 12 Acquired Hyundai Corporation

2010. 8 Acquired Hyundai Oilbank Co., Ltd. (70% of Ownership and management)

2011. 2 Became the world’s first shipbuilder to deliver 1,700th ship

History

7

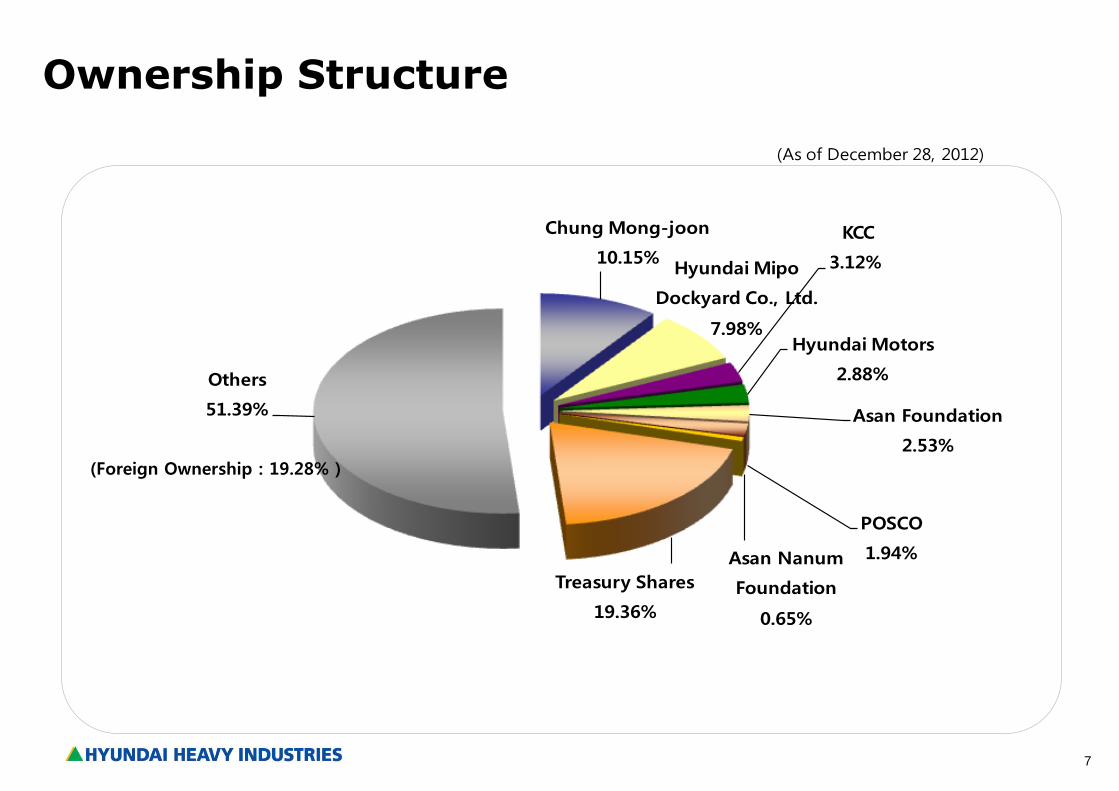

Ownership Structure

Chung Mong-joon

10.15%Hyundai Mipo

Dockyard Co., Ltd.

7.98%

KCC

3.12%

Hyundai Motors

2.88%

Asan Foundation

2.53%

POSCO

1.94%Asan Nanum

Foundation

0.65%

Treasury Shares

19.36%

Others

51.39%

(As of December 28, 2012)

(Foreign Ownership : 19.28% )

8

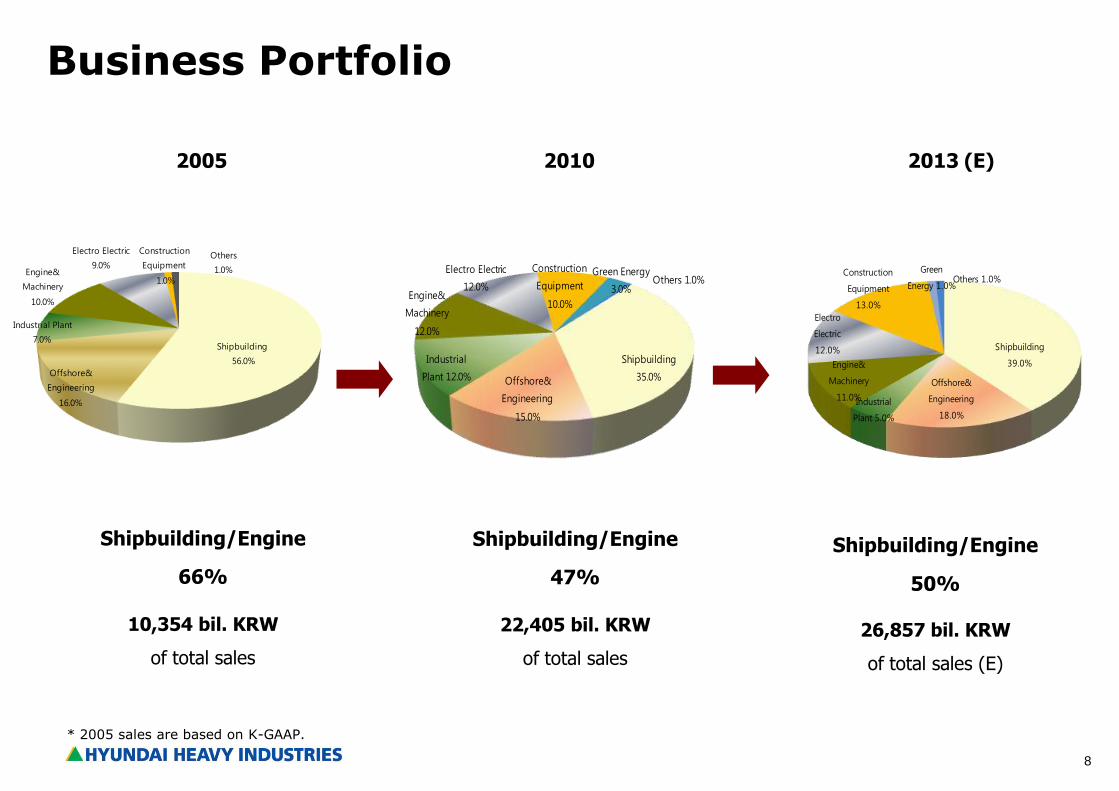

Shipbuilding

56.0%

Offshore&

Engineering

16.0%

Industrial Plant

7.0%

Engine&

Machinery

10.0%

Electro Electric

9.0%

Construction

Equipment

1.0%

Others

1.0%

Shipbuilding

39.0%

Offshore&

Engineering

18.0%

Industrial

Plant 5.0%

Engine&

Machinery

11.0%

Electro

Electric

12.0%

Construction

Equipment

13.0%

Green

Energy 1.0%Others 1.0%

Shipbuilding

35.0%Offshore&

Engineering

15.0%

Industrial

Plant 12.0%

Engine&

Machinery

12.0%

Electro Electric

12.0%

Construction

Equipment

10.0%

Green Energy

3.0%Others 1.0%

Business Portfolio

2005 2010 2013 (E)

Shipbuilding/Engine

66%

Shipbuilding/Engine

47%

Shipbuilding/Engine

50%

10,354 bil. KRW

of total sales

22,405 bil. KRW

of total sales

26,857 bil. KRW

of total sales (E)

* 2005 sales are based on K-GAAP.

9

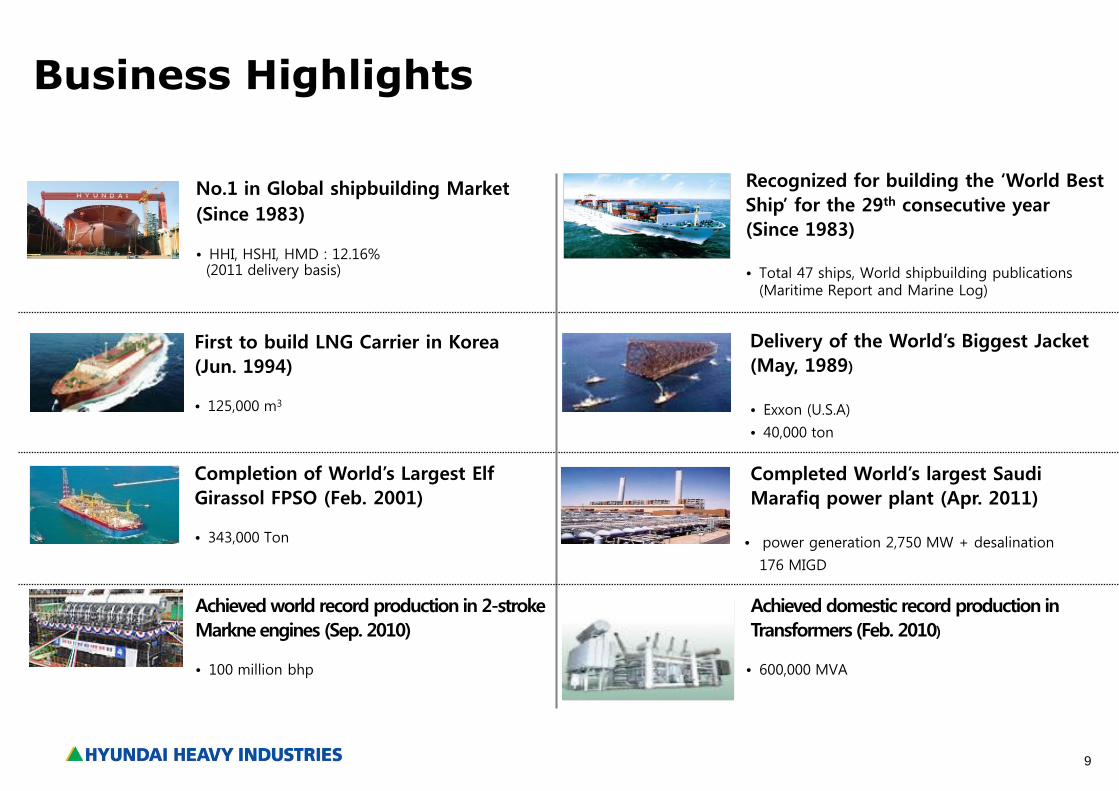

First to build LNG Carrier in Korea

(Jun. 1994) • 125,000 m3

Achieved world record production in 2-stroke

Markne engines (Sep. 2010) • 100 million bhp

Delivery of the World’s Biggest Jacket

(May, 1989)

• Exxon (U.S.A)

• 40,000 ton

No.1 in Global shipbuilding Market

(Since 1983) • HHI, HSHI, HMD : 12.16% (2011 delivery basis)

Recognized for building the ‘World Best

Ship’ for the 29th consecutive year

(Since 1983)

• Total 47 ships, World shipbuilding publications (Maritime Report and Marine Log)

Business Highlights

Completed World’s largest Saudi

Marafiq power plant (Apr. 2011)

• power generation 2,750 MW + desalination

176 MIGD

Achieved domestic record production in

Transformers (Feb. 2010)

• 600,000 MVA

Completion of World’s Largest Elf

Girassol FPSO (Feb. 2001) • 343,000 Ton

10

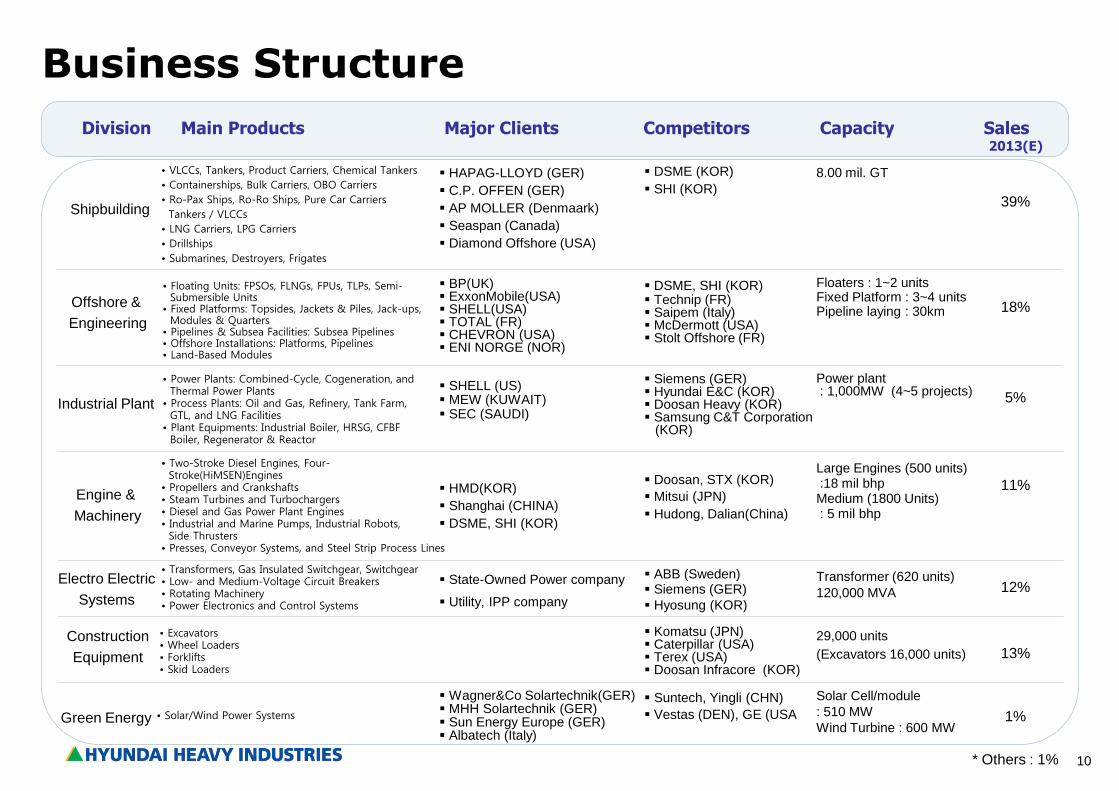

Business Structure

Shipbuilding

Industrial Plant

Engine &

Machinery

Offshore &

Engineering

Construction

Equipment

Electro Electric

Systems

DSME (KOR)

SHI (KOR)

DSME, SHI (KOR) Technip (FR) Saipem (Italy) McDermott (USA) Stolt Offshore (FR)

Siemens (GER) Hyundai E&C (KOR) Doosan Heavy (KOR) Samsung C&T Corporation (KOR)

Doosan, STX (KOR)

Mitsui (JPN)

Hudong, Dalian(China)

ABB (Sweden) Siemens (GER)

Hyosung (KOR)

Komatsu (JPN) Caterpillar (USA) Terex (USA) Doosan Infracore (KOR) Suntech, Yingli (CHN)

Vestas (DEN), GE (USA

HAPAG-LLOYD (GER)

C.P. OFFEN (GER)

AP MOLLER (Denmaark)

Seaspan (Canada)

Diamond Offshore (USA)

BP(UK) ExxonMobile(USA) SHELL(USA) TOTAL (FR) CHEVRON (USA) ENI NORGE (NOR) SHELL (US) MEW (KUWAIT) SEC (SAUDI)

HMD(KOR)

Shanghai (CHINA)

DSME, SHI (KOR)

State-Owned Power company

Utility, IPP company

Wagner&Co Solartechnik(GER) MHH Solartechnik (GER) Sun Energy Europe (GER) Albatech (Italy)

8.00 mil. GT

Floaters : 1~2 units Fixed Platform : 3~4 units Pipeline laying : 30km

Power plant : 1,000MW (4~5 projects)

Large Engines (500 units) :18 mil bhp Medium (1800 Units) : 5 mil bhp

Transformer (620 units)

120,000 MVA

29,000 units

(Excavators 16,000 units)

Solar Cell/module

: 510 MW

Wind Turbine : 600 MW

Division Main Products Major Clients Competitors Capacity Sales 2013(E)

39%

18%

5%

11%

12%

13%

1%

* Others : 1%

• Excavators • Wheel Loaders • Forklifts • Skid Loaders

• VLCCs, Tankers, Product Carriers, Chemical Tankers

• Containerships, Bulk Carriers, OBO Carriers

• Ro-Pax Ships, Ro-Ro Ships, Pure Car Carriers

Tankers / VLCCs

• LNG Carriers, LPG Carriers

• Drillships

• Submarines, Destroyers, Frigates

• Floating Units: FPSOs, FLNGs, FPUs, TLPs, Semi- Submersible Units • Fixed Platforms: Topsides, Jackets & Piles, Jack-ups, Modules & Quarters • Pipelines & Subsea Facilities: Subsea Pipelines • Offshore Installations: Platforms, Pipelines • Land-Based Modules • Power Plants: Combined-Cycle, Cogeneration, and Thermal Power Plants • Process Plants: Oil and Gas, Refinery, Tank Farm, GTL, and LNG Facilities • Plant Equipments: Industrial Boiler, HRSG, CFBF Boiler, Regenerator & Reactor

• Two-Stroke Diesel Engines, Four- Stroke(HiMSEN)Engines • Propellers and Crankshafts • Steam Turbines and Turbochargers • Diesel and Gas Power Plant Engines • Industrial and Marine Pumps, Industrial Robots, Side Thrusters • Presses, Conveyor Systems, and Steel Strip Process Lines

• Transformers, Gas Insulated Switchgear, Switchgear • Low- and Medium-Voltage Circuit Breakers • Rotating Machinery • Power Electronics and Control Systems

Green Energy • Solar/Wind Power Systems

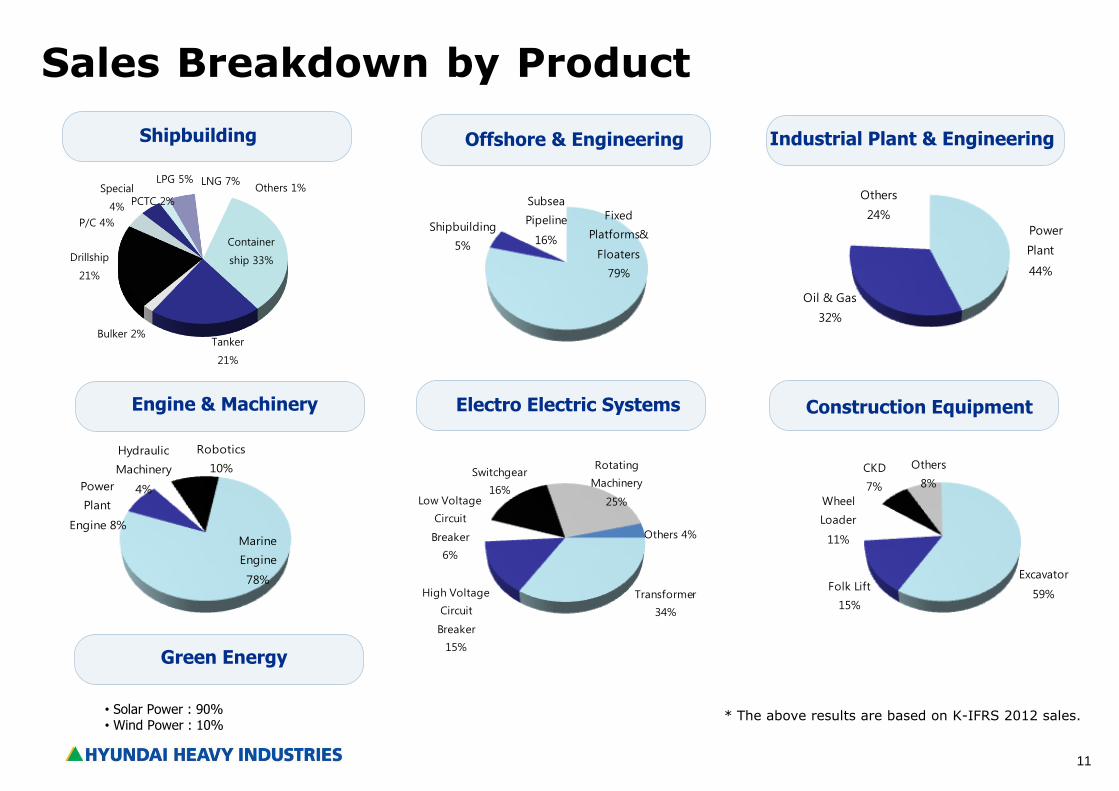

11

Power

Plant

44%

Oil & Gas

32%

Others

24%

Marine

Engine

78%

Power

Plant

Engine 8%

Hydraulic

Machinery

4%

Robotics

10%

Fixed

Platforms&

Floaters

79%

Shipbuilding

5%

Subsea

Pipeline

16%

Shipbuilding Offshore & Engineering

Electro Electric Systems

Industrial Plant & Engineering

Engine & Machinery

Sales Breakdown by Product

* The above results are based on K-IFRS 2012 sales.

Construction Equipment

Green Energy

• Solar Power : 90% • Wind Power : 10%

Excavator

59%Folk Lift

15%

Wheel

Loader

11%

CKD

7%

Others

8%

Transformer

34%

High Voltage

Circuit

Breaker

15%

Low Voltage

Circuit

Breaker

6%

Switchgear

16%

Rotating

Machinery

25%

Others 4%

Container

ship 33%

Tanker

21%

Bulker 2%

Drillship

21%

P/C 4%

Special

4% PCTC 2%

LPG 5% LNG 7% Others 1%

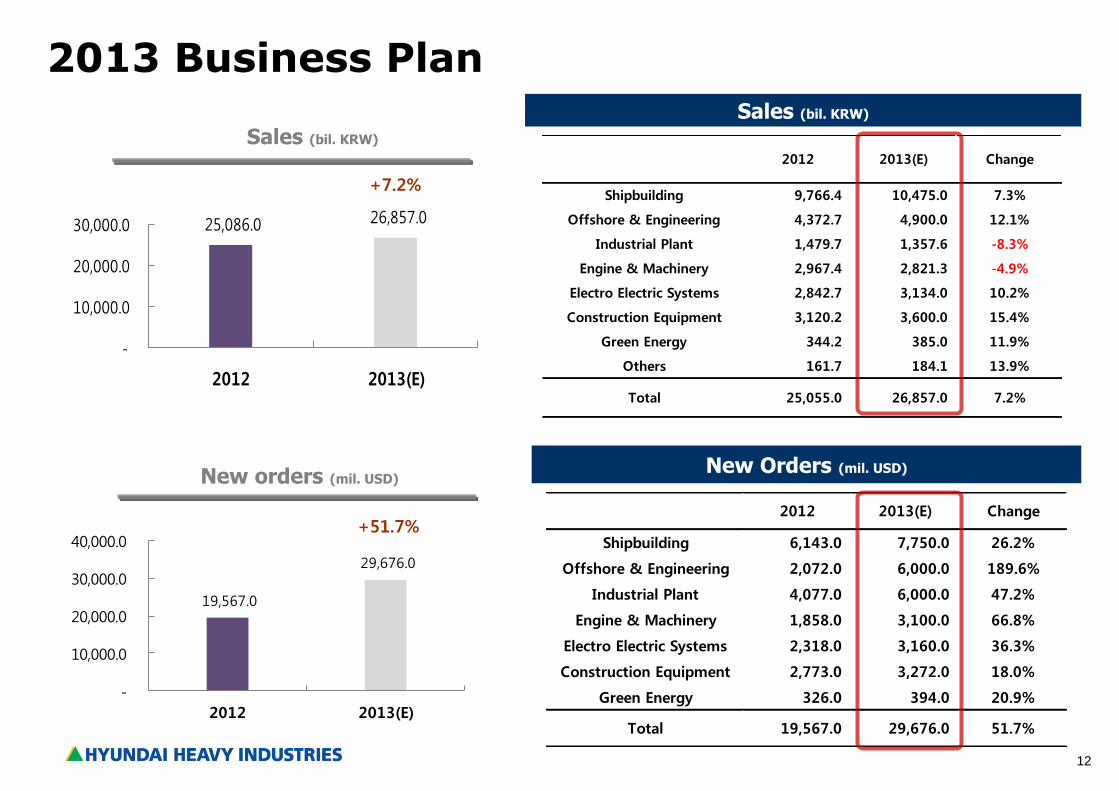

12

2012 2013(E) Change

Shipbuilding 9,766.4 10,475.0 7.3%

Offshore & Engineering 4,372.7 4,900.0 12.1%

Industrial Plant 1,479.7 1,357.6 -8.3%

Engine & Machinery 2,967.4 2,821.3 -4.9%

Electro Electric Systems 2,842.7 3,134.0 10.2%

Construction Equipment 3,120.2 3,600.0 15.4%

Green Energy 344.2 385.0 11.9%

Others 161.7 184.1 13.9%

Total 25,055.0 26,857.0 7.2%

19,567.0

29,676.0

-

10,000.0

20,000.0

30,000.0

40,000.0

2012 2013(E)

2013 Business Plan Sales (bil. KRW)

2012 2013(E) Change

Shipbuilding 6,143.0 7,750.0 26.2%

Offshore & Engineering 2,072.0 6,000.0 189.6%

Industrial Plant 4,077.0 6,000.0 47.2%

Engine & Machinery 1,858.0 3,100.0 66.8%

Electro Electric Systems 2,318.0 3,160.0 36.3%

Construction Equipment 2,773.0 3,272.0 18.0%

Green Energy 326.0 394.0 20.9%

Total 19,567.0 29,676.0 51.7%

New Orders (mil. USD)

New orders (mil. USD)

+51.7%

25,086.0 26,857.0

-

10,000.0

20,000.0

30,000.0

2012 2013(E)

Sales (bil. KRW)

+7.2%

13

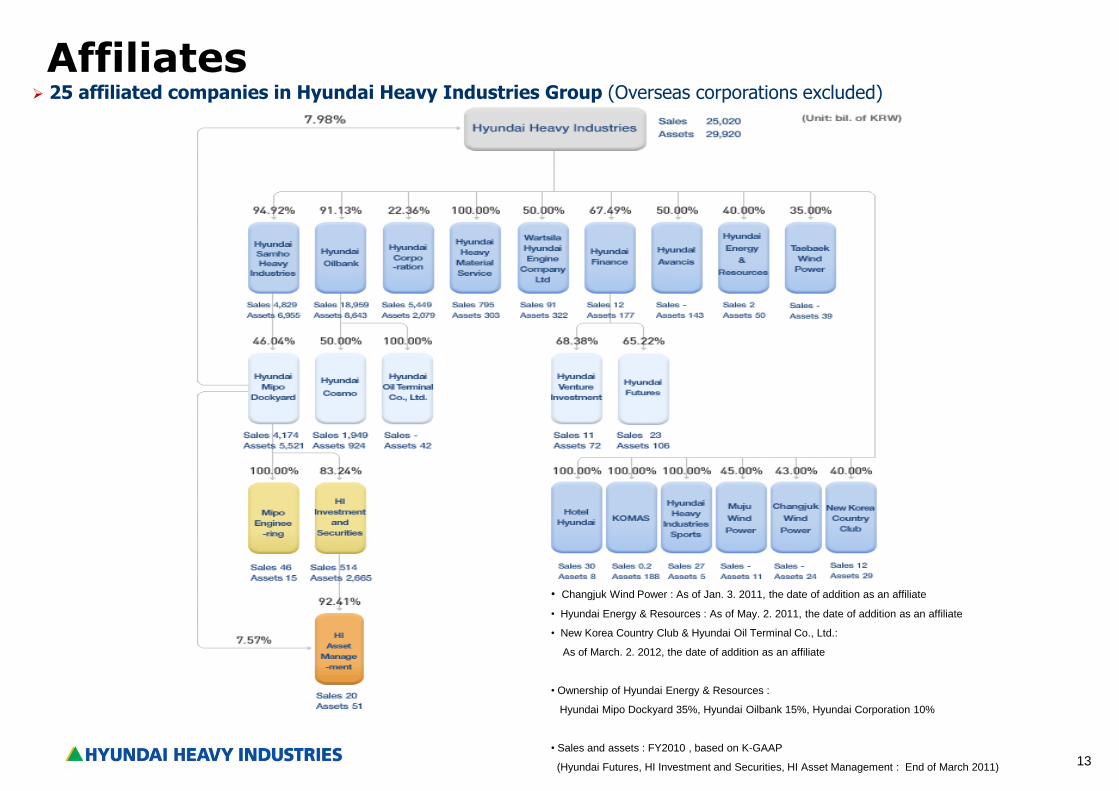

25 affiliated companies in Hyundai Heavy Industries Group (Overseas corporations excluded)

Affiliates

• Changjuk Wind Power : As of Jan. 3. 2011, the date of addition as an affiliate

• Hyundai Energy & Resources : As of May. 2. 2011, the date of addition as an affiliate

• New Korea Country Club & Hyundai Oil Terminal Co., Ltd.:

As of March. 2. 2012, the date of addition as an affiliate

• Ownership of Hyundai Energy & Resources :

Hyundai Mipo Dockyard 35%, Hyundai Oilbank 15%, Hyundai Corporation 10%

• Sales and assets : FY2010 , based on K-GAAP

(Hyundai Futures, HI Investment and Securities, HI Asset Management : End of March 2011)

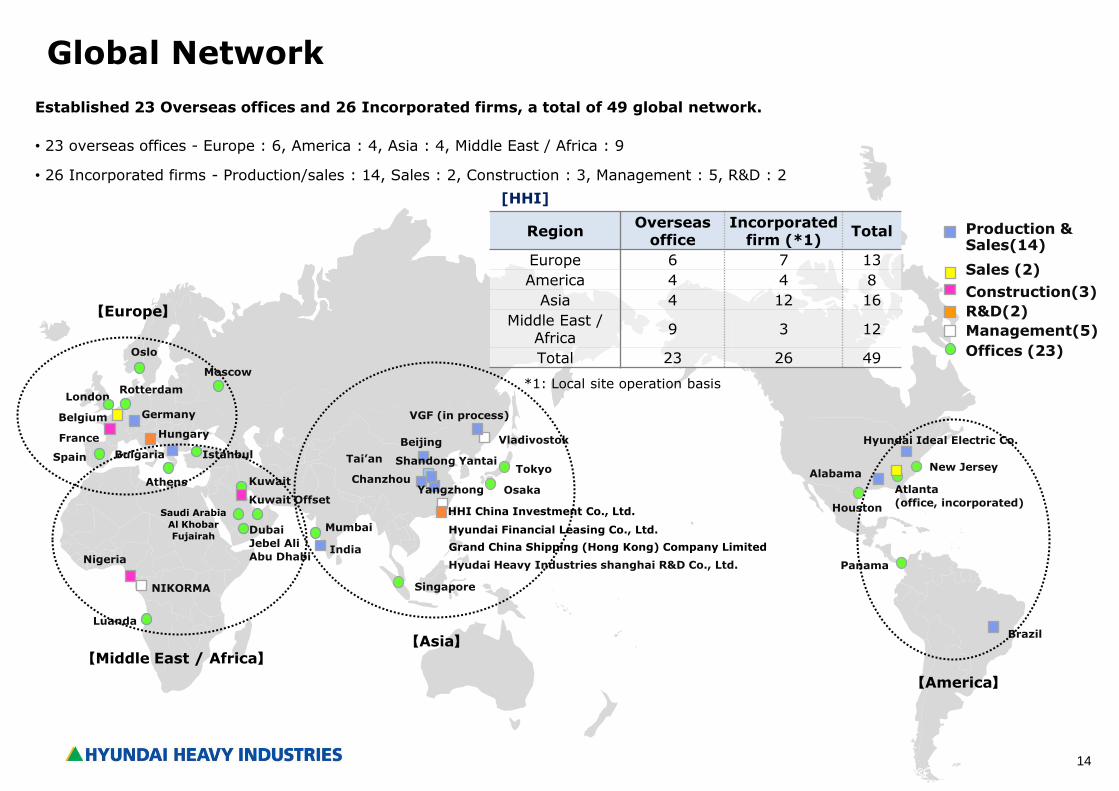

14

Vladivostok

Tokyo

Beijing

Hyundai Financial Leasing Co., Ltd.

Grand China Shipping (Hong Kong) Company Limited

Chanzhou

Singapore

Mumbai Dubai

Jebel Ali

Abu Dhabi

Atlanta

(office, incorporated)

New Jersey

Houston

Istanbul

Athens

Luanda

Nigeria

Oslo

Rotterdam London

France Hyundai Ideal Electric Co.

Panama

Osaka

Moscow

NIKORMA

HHI China Investment Co., Ltd.

Tai’an

Saudi Arabia

Al Khobar

Fujairah

Alabama Shandong Yantai

Kuwait

Kuwait Offset

Spain

Hungary

Offices (23)

Production & Sales(14)

Management(5)

Construction(3)

Sales (2)

R&D(2)

Region Overseas

office Incorporated

firm (*1) Total

Europe 6 7 13

America 4 4 8

Asia 4 12 16

Middle East / Africa

9 3 12

Total 23 26 49

India

Bulgaria

Belgium Germany

Hyudai Heavy Industries shanghai R&D Co., Ltd.

VGF (in process)

Brazil

Established 23 Overseas offices and 26 Incorporated firms, a total of 49 global network.

• 23 overseas offices - Europe : 6, America : 4, Asia : 4, Middle East / Africa : 9

• 26 Incorporated firms - Production/sales : 14, Sales : 2, Construction : 3, Management : 5, R&D : 2

【Europe】

【Middle East / Africa】 【Asia】

【America】

[HHI]

*1: Local site operation basis

Yangzhong

Global Network

15

Business Performance

16

2,043 2,809

6,792 8,488 8,272

11,470

15,730 13,635

444 4,061

10,905

6,143 7,750 4,357 2,968

3,025

4,917

7,835

7,236

9,290

13,838

10,291

13,147

14,419

13,424

21,926

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

`01 `02 `03 `04 `05 `06 `07 `08 `09 `10 `11 `12 `13

(Target)

Shipbuilding Non-Shipbuilding

6,400 5,777

9,817

13,405

16,107

18,706

25,020

27,473

10,735

25,324

New Orders Trend

(Mil. USD)

17,209

+51.7% YoY

19,567

29,676

17

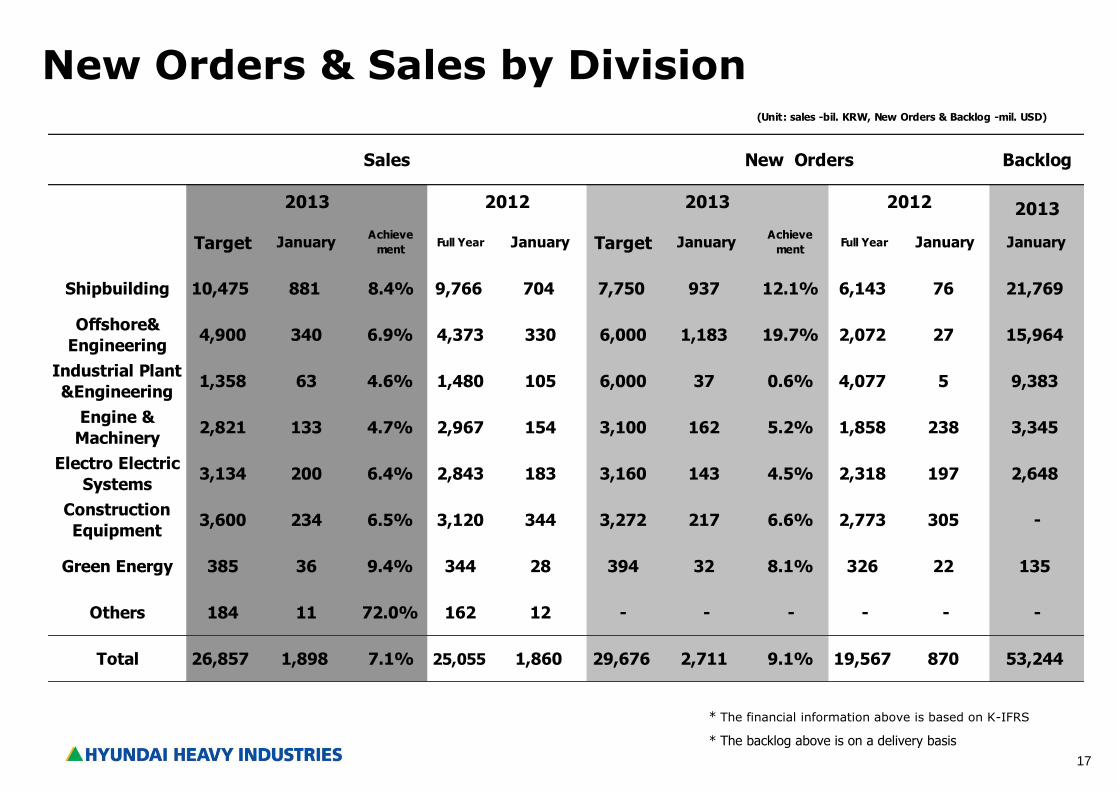

New Orders & Sales by Division

* The financial information above is based on K-IFRS

* The backlog above is on a delivery basis

Backlog

2013

Target JanuaryAchieve

mentFull Year January Target January

Achieve

mentFull Year January January

Shipbuilding 10,475 881 8.4% 9,766 704 7,750 937 12.1% 6,143 76 21,769

Offshore&

Engineering4,900 340 6.9% 4,373 330 6,000 1,183 19.7% 2,072 27 15,964

Industrial Plant

&Engineering1,358 63 4.6% 1,480 105 6,000 37 0.6% 4,077 5 9,383

Engine &

Machinery2,821 133 4.7% 2,967 154 3,100 162 5.2% 1,858 238 3,345

Electro Electric

Systems3,134 200 6.4% 2,843 183 3,160 143 4.5% 2,318 197 2,648

Construction

Equipment3,600 234 6.5% 3,120 344 3,272 217 6.6% 2,773 305 -

Green Energy 385 36 9.4% 344 28 394 32 8.1% 326 22 135

Others 184 11 72.0% 162 12 - - - - - -

Total 26,857 1,898 7.1% 25,055 1,860 29,676 2,711 9.1% 19,567 870 53,244

Sales

2013 2012

(Unit: sales -bil. KRW, New Orders & Backlog -mil. USD)

New Orders

20122013

18

Shipbuilding

Bulk Carrier Containerships Special Vessels LPG VLCC Naval Ships LNG Car Carriers Drillship

19

16.7 18.1

26.1

18.4 20.5

41.9 44.3 45.1

67.8

93.5

54.2

15.3

37.8

28.1 21.3

0

20

40

60

80

100

1998 2000 2002 2004 2006 2008 2010 2012

Global

Korea

Japan

China

0

50

100

150

200

02 03 04 05 06 07 08 09 10 11 12 13

VLCC

Bulk Carrier(Capesize)

Container(4,800TEU)

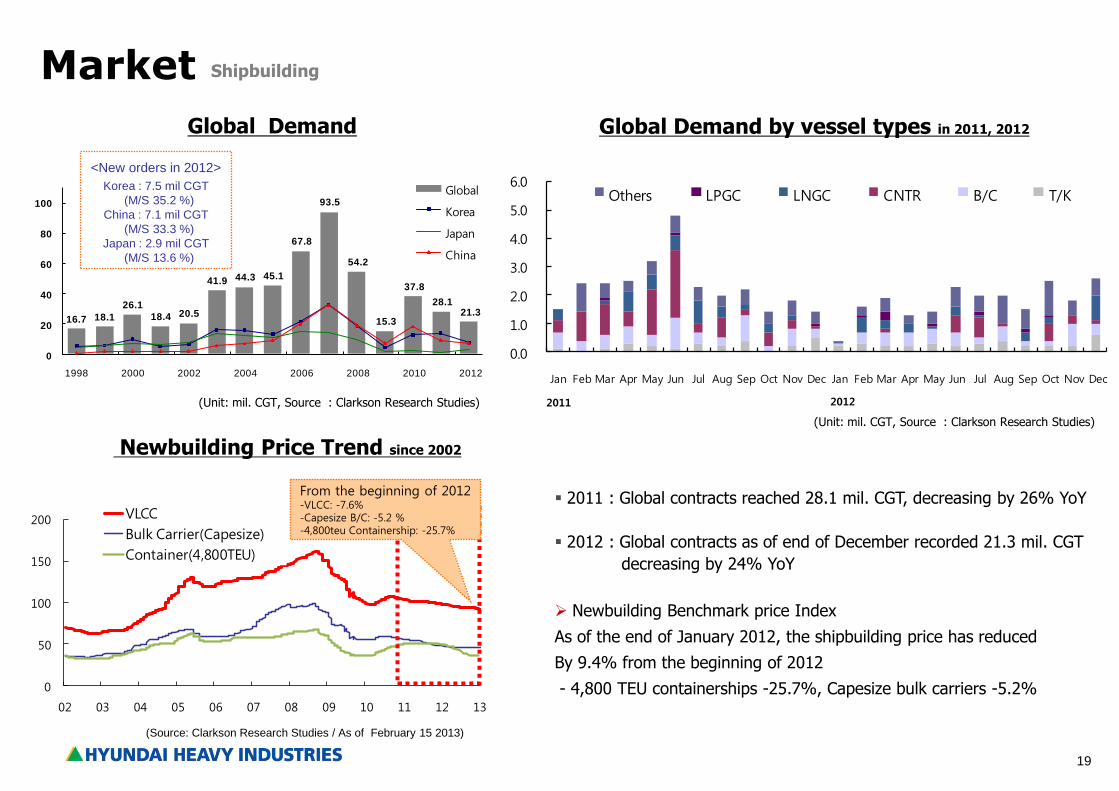

Market

(Unit: mil. CGT, Source : Clarkson Research Studies)

Newbuilding Price Trend since 2002

Global Demand by vessel types in 2011, 2012

Shipbuilding

2011 : Global contracts reached 28.1 mil. CGT, decreasing by 26% YoY

2012 : Global contracts as of end of December recorded 21.3 mil. CGT

decreasing by 24% YoY

Newbuilding Benchmark price Index

As of the end of January 2012, the shipbuilding price has reduced

By 9.4% from the beginning of 2012

- 4,800 TEU containerships -25.7%, Capesize bulk carriers -5.2%

(Source: Clarkson Research Studies / As of February 15 2013)

From the beginning of 2012 -VLCC: -7.6% -Capesize B/C: -5.2 % -4,800teu Containership: -25.7%

Global Demand

(Unit: mil. CGT, Source : Clarkson Research Studies)

<New orders in 2012>

Korea : 7.5 mil CGT

(M/S 35.2 %)

China : 7.1 mil CGT

(M/S 33.3 %)

Japan : 2.9 mil CGT

(M/S 13.6 %)

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Others LPGC LNGC CNTR B/C T/K

2011 2012

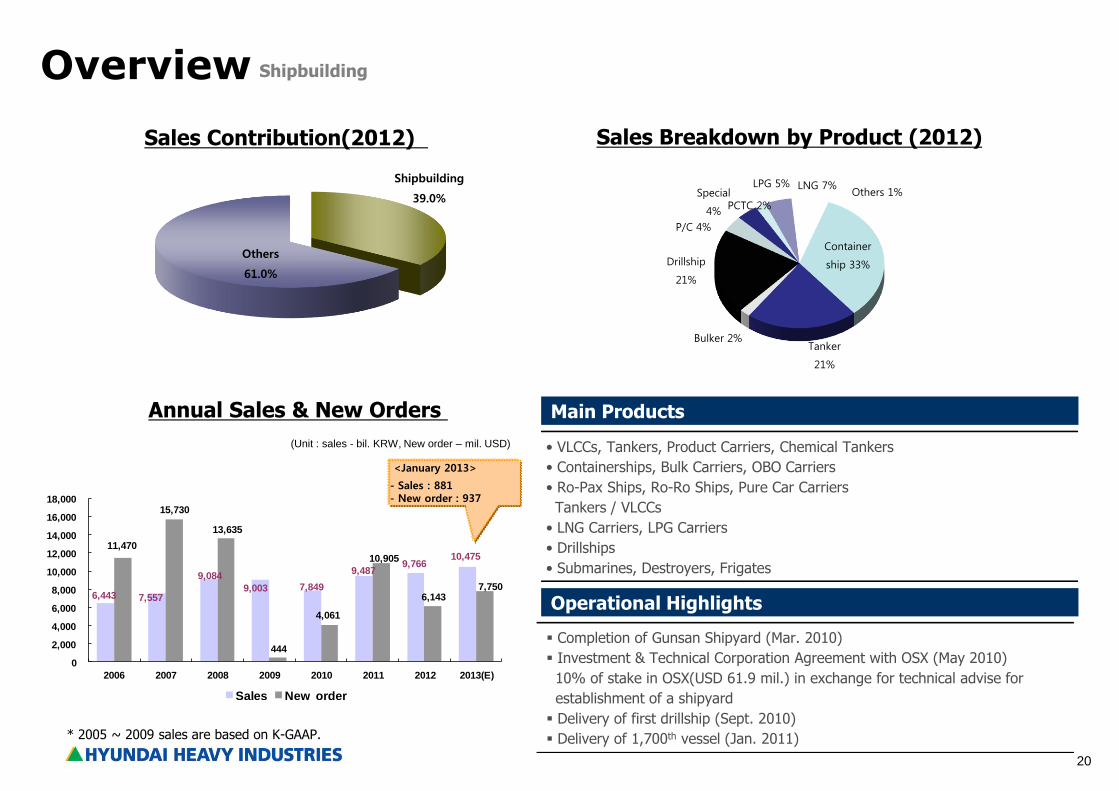

20

Shipbuilding

39.0%

Others

61.0%

Overview

Annual Sales & New Orders

(Unit : sales - bil. KRW, New order – mil. USD)

Main Products

Sales Breakdown by Product (2012)

• VLCCs, Tankers, Product Carriers, Chemical Tankers

• Containerships, Bulk Carriers, OBO Carriers

• Ro-Pax Ships, Ro-Ro Ships, Pure Car Carriers

Tankers / VLCCs

• LNG Carriers, LPG Carriers

• Drillships

• Submarines, Destroyers, Frigates

Operational Highlights

Completion of Gunsan Shipyard (Mar. 2010)

Investment & Technical Corporation Agreement with OSX (May 2010)

10% of stake in OSX(USD 61.9 mil.) in exchange for technical advise for

establishment of a shipyard

Delivery of first drillship (Sept. 2010)

Delivery of 1,700th vessel (Jan. 2011)

Shipbuilding

<January 2013>

- Sales : 881 - New order : 937

Sales Contribution(2012)

* 2005 ~ 2009 sales are based on K-GAAP.

6,443 7,557

9,084

9,003 7,849

9,487 9,766

10,475 11,470

15,730

13,635

444

4,061

10,905

6,143 7,750

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

2006 2007 2008 2009 2010 2011 2012 2013(E)

Sales New order

Container

ship 33%

Tanker

21%

Bulker 2%

Drillship

21%

P/C 4%

Special

4% PCTC 2%

LPG 5% LNG 7% Others 1%

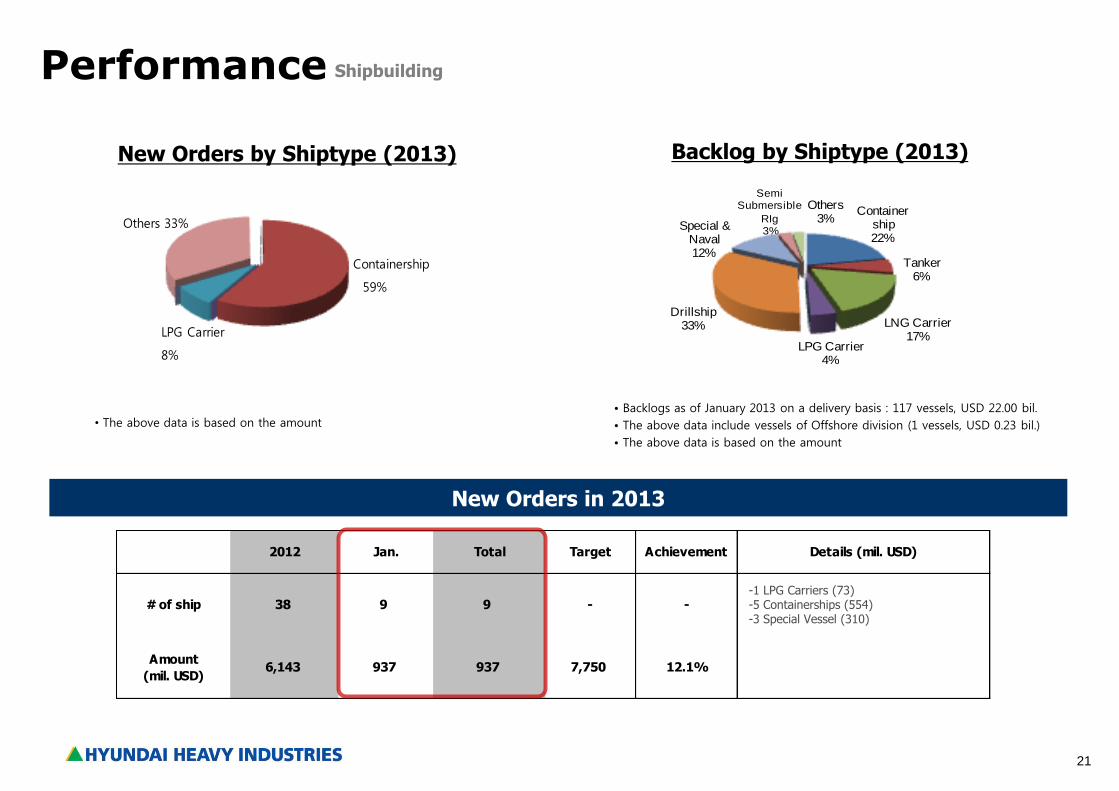

21

Backlog by Shiptype (2013)

Performance

New Orders in 2013

2012 Jan. Total Target Achievement Details (mil. USD)

# of ship 38 9 9 - -

Amount

(mil. USD)6,143 937 937 7,750 12.1%

New Orders by Shiptype (2013)

Shipbuilding

-1 LPG Carriers (73) -5 Containerships (554) -3 Special Vessel (310)

• Backlogs as of January 2013 on a delivery basis : 117 vessels, USD 22.00 bil.

• The above data include vessels of Offshore division (1 vessels, USD 0.23 bil.)

• The above data is based on the amount

• The above data is based on the amount

Container ship22%

Tanker6%

LNG Carrier17%

LPG Carrier4%

Drillship 33%

Special & Naval12%

Others3%

Semi Submersible

RIg3%

LPG Carrier

8%

Others 33%

Containership

59%

22

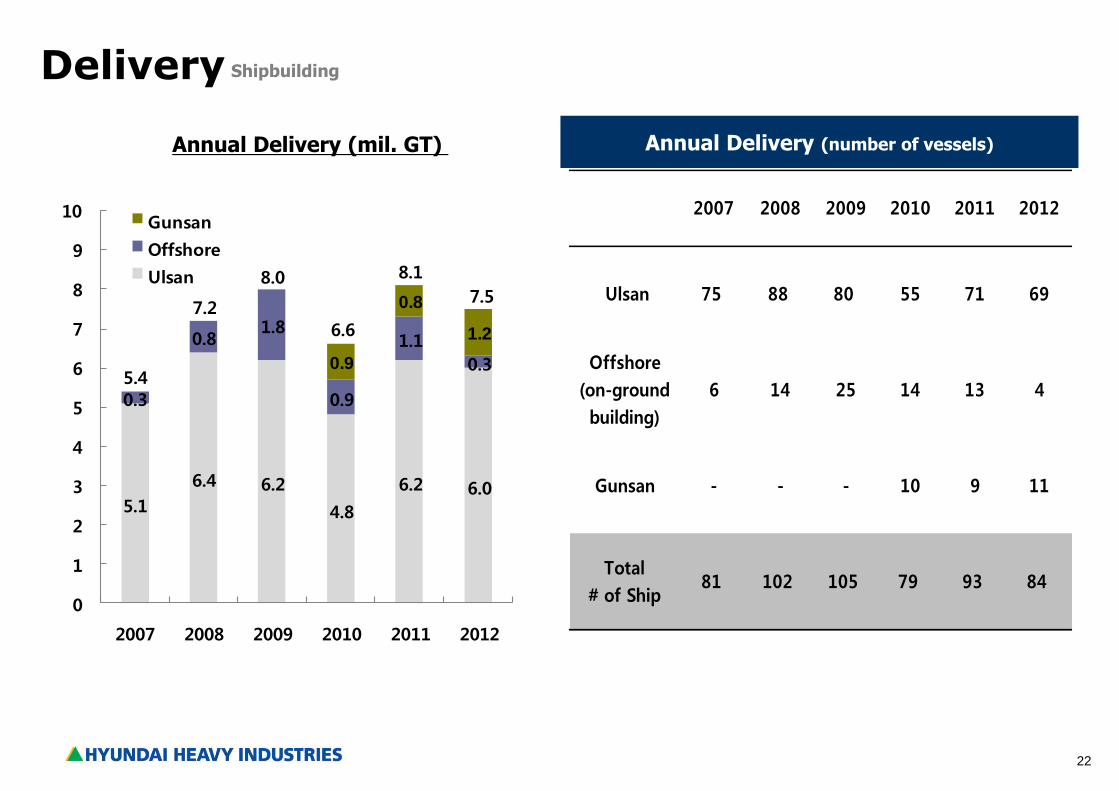

5.1

6.4 6.2

4.8

6.2 6.0

0.3

0.81.8

0.9

1.1

0.3 0.9

0.8

1.2

0

1

2

3

4

5

6

7

8

9

10

2007 2008 2009 2010 2011 2012

Gunsan

Offshore

Ulsan

5.4

7.2

8.0

6.6

7.5

8.1

Delivery

Annual Delivery (mil. GT) Annual Delivery (number of vessels)

2007 2008 2009 2010 2011 2012

Ulsan 75 88 80 55 71 69

Offshore

(on-ground

building)

6 14 25 14 13 4

Gunsan - - - 10 9 11

Total

# of Ship81 102 105 79 93 84

Shipbuilding

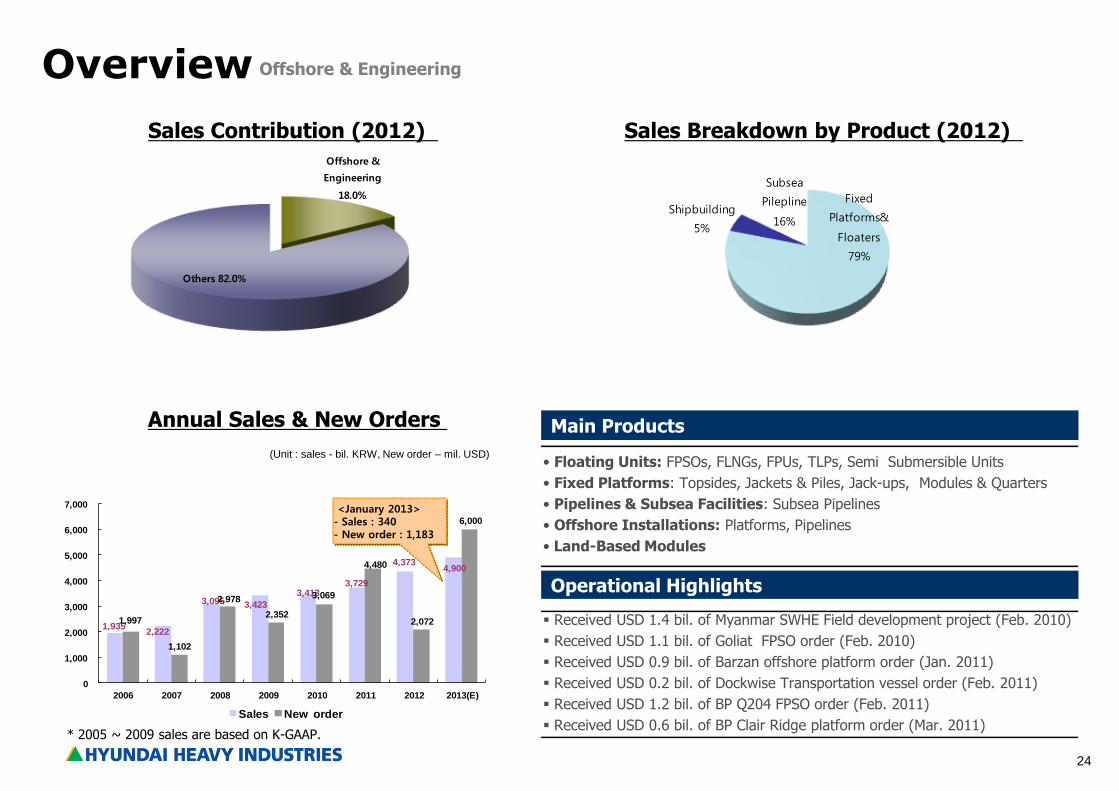

23

Offshore & Engineering

FPSO Semi-Submersible Unit Drilling Rig Subsea Pipeline

24

Offshore &

Engineering

18.0%

Others 82.0%

1,935 2,222

3,095 3,423

3,413 3,729

4,373 4,900

1,997

1,102

2,978

2,352

3,069

4,480

2,072

6,000

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2006 2007 2008 2009 2010 2011 2012 2013(E)

Sales New order

Sales Contribution (2012)

Overview

(Unit : sales - bil. KRW, New order – mil. USD)

Annual Sales & New Orders

Sales Breakdown by Product (2012)

• Floating Units: FPSOs, FLNGs, FPUs, TLPs, Semi Submersible Units

• Fixed Platforms: Topsides, Jackets & Piles, Jack-ups, Modules & Quarters

• Pipelines & Subsea Facilities: Subsea Pipelines

• Offshore Installations: Platforms, Pipelines

• Land-Based Modules

Main Products

Operational Highlights

Received USD 1.4 bil. of Myanmar SWHE Field development project (Feb. 2010)

Received USD 1.1 bil. of Goliat FPSO order (Feb. 2010)

Received USD 0.9 bil. of Barzan offshore platform order (Jan. 2011)

Received USD 0.2 bil. of Dockwise Transportation vessel order (Feb. 2011)

Received USD 1.2 bil. of BP Q204 FPSO order (Feb. 2011)

Received USD 0.6 bil. of BP Clair Ridge platform order (Mar. 2011)

Offshore & Engineering

<January 2013> - Sales : 340 - New order : 1,183

* 2005 ~ 2009 sales are based on K-GAAP.

Fixed

Platforms&

Floaters

79%

Shipbuilding

5%

Subsea

Pilepline

16%

25

Performance

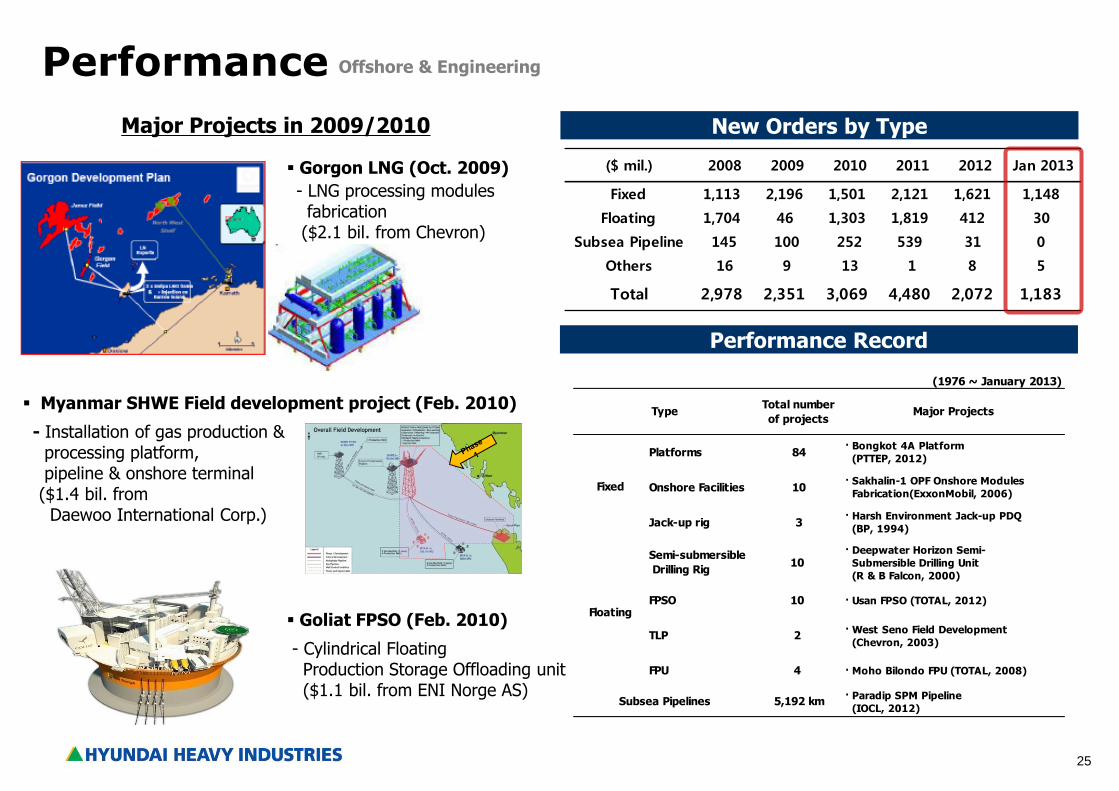

New Orders by Type

($ mil.) 2008 2009 2010 2011 2012 Jan 2013

Fixed 1,113 2,196 1,501 2,121 1,621 1,148

Floating 1,704 46 1,303 1,819 412 30

Subsea Pipeline 145 100 252 539 31 0

Others 16 9 13 1 8 5

Total 2,978 2,351 3,069 4,480 2,072 1,183

Performance Record

Major Projects in 2009/2010

Gorgon LNG (Oct. 2009)

- LNG processing modules fabrication ($2.1 bil. from Chevron)

Myanmar SHWE Field development project (Feb. 2010)

- Installation of gas production & processing platform, pipeline & onshore terminal ($1.4 bil. from Daewoo International Corp.)

Goliat FPSO (Feb. 2010)

- Cylindrical Floating Production Storage Offloading unit ($1.1 bil. from ENI Norge AS)

Offshore & Engineering

(1976 ~ January 2013)

Total number

of projectsMajor Projects

Platforms 84· Bongkot 4A Platform

(PTTEP, 2012)

Onshore Facilities 10· Sakhalin-1 OPF Onshore Modules

Fabrication(ExxonMobil, 2006)

Jack-up rig 3· Harsh Environment Jack-up PDQ

(BP, 1994)

Semi-submersible

Drilling Rig10

· Deepwater Horizon Semi-

Submersible Drilling Unit

(R & B Falcon, 2000)

FPSO 10 · Usan FPSO (TOTAL, 2012)

TLP 2· West Seno Field Development

(Chevron, 2003)

FPU 4 · Moho Bilondo FPU (TOTAL, 2008)

5,192 km· Paradip SPM Pipeline

(IOCL, 2012)

Fixed

Floating

Subsea Pipelines

Type

26

Performance

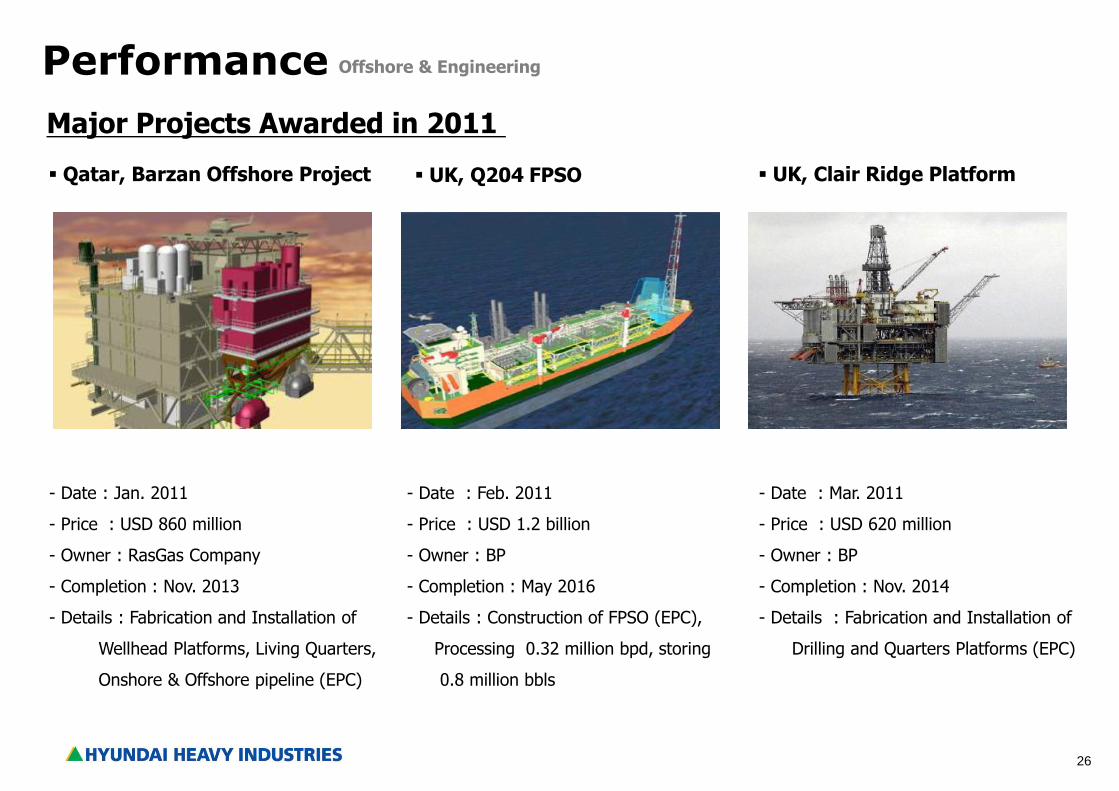

Major Projects Awarded in 2011

Qatar, Barzan Offshore Project

- Date : Jan. 2011

- Price : USD 860 million

- Owner : RasGas Company

- Completion : Nov. 2013

- Details : Fabrication and Installation of

Wellhead Platforms, Living Quarters,

Onshore & Offshore pipeline (EPC)

Offshore & Engineering

UK, Q204 FPSO UK, Clair Ridge Platform

- Date : Feb. 2011

- Price : USD 1.2 billion

- Owner : BP

- Completion : May 2016

- Details : Construction of FPSO (EPC),

Processing 0.32 million bpd, storing

0.8 million bbls

- Date : Mar. 2011

- Price : USD 620 million

- Owner : BP

- Completion : Nov. 2014

- Details : Fabrication and Installation of

Drilling and Quarters Platforms (EPC)

27

Industrial Plant & Engineering

Co-Generation Plant Process Plant Thermal Power Plant Combined Cycle Power Plant

28

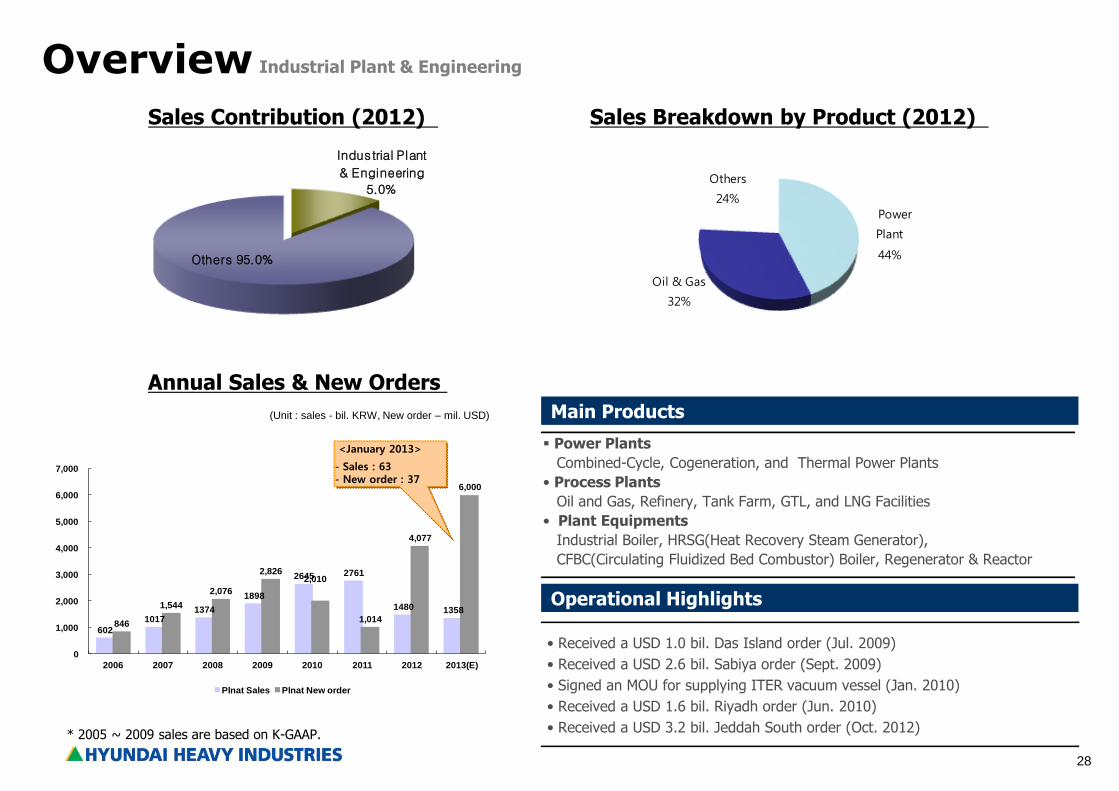

Industrial Plant

& Engineering

5.0%

Others 95.0%

602

10171374

1898

2645 2761

1480 1358

846

1,544

2,076

2,826 2,010

1,014

4,077

6,000

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2006 2007 2008 2009 2010 2011 2012 2013(E)

Plnat Sales Plnat New order

Sales Contribution (2012)

Overview

(Unit : sales - bil. KRW, New order – mil. USD)

Annual Sales & New Orders

Sales Breakdown by Product (2012)

Main Products

Power Plants

Combined-Cycle, Cogeneration, and Thermal Power Plants

• Process Plants

Oil and Gas, Refinery, Tank Farm, GTL, and LNG Facilities

• Plant Equipments

Industrial Boiler, HRSG(Heat Recovery Steam Generator),

CFBC(Circulating Fluidized Bed Combustor) Boiler, Regenerator & Reactor

Operational Highlights

Industrial Plant & Engineering

<January 2013>

- Sales : 63 - New order : 37

* 2005 ~ 2009 sales are based on K-GAAP.

• Received a USD 1.0 bil. Das Island order (Jul. 2009)

• Received a USD 2.6 bil. Sabiya order (Sept. 2009)

• Signed an MOU for supplying ITER vacuum vessel (Jan. 2010)

• Received a USD 1.6 bil. Riyadh order (Jun. 2010)

• Received a USD 3.2 bil. Jeddah South order (Oct. 2012)

Power

Plant

44%

Oil & Gas

32%

Others

24%

29

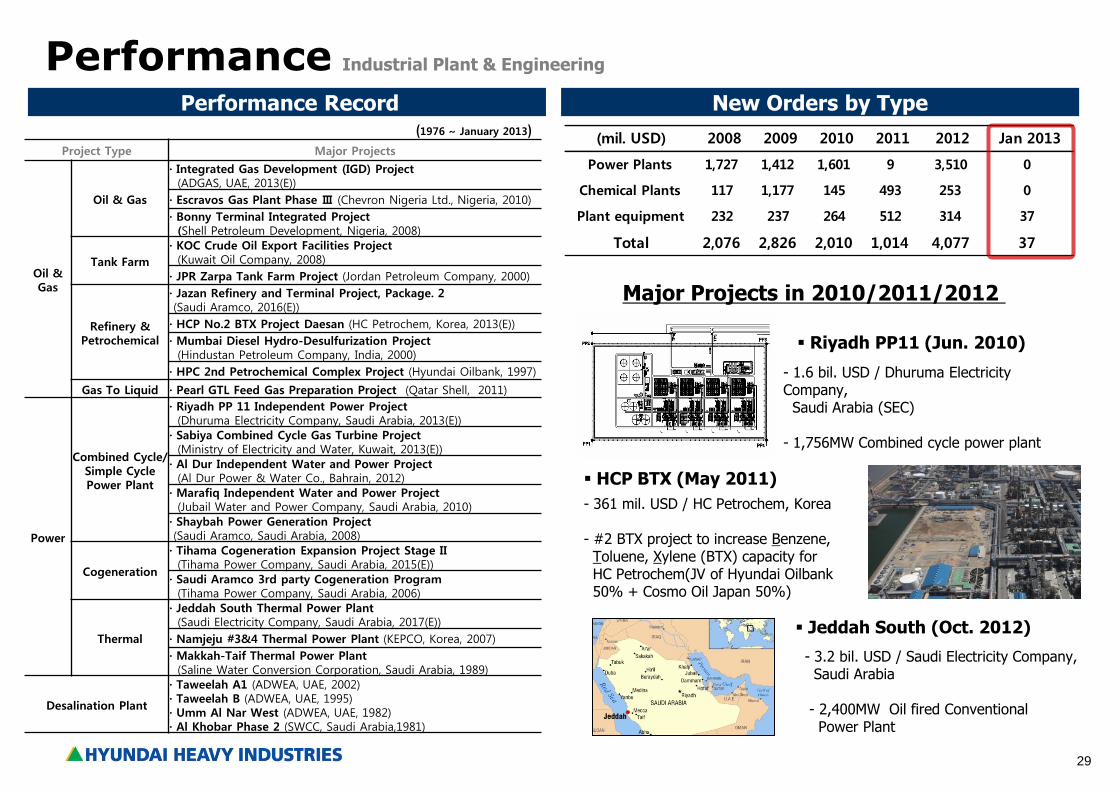

Performance Performance Record New Orders by Type

(mil. USD) 2008 2009 2010 2011 2012 Jan 2013

Power Plants 1,727 1,412 1,601 9 3,510 0

Chemical Plants 117 1,177 145 493 253 0

Plant equipment 232 237 264 512 314 37

Total 2,076 2,826 2,010 1,014 4,077 37

Industrial Plant & Engineering

Major Projects in 2010/2011/2012

(1976 ~ January 2013)

Project Type Major Projects

Oil & Gas

Oil & Gas

· Integrated Gas Development (IGD) Project (ADGAS, UAE, 2013(E))

· Escravos Gas Plant Phase Ⅲ (Chevron Nigeria Ltd., Nigeria, 2010)

· Bonny Terminal Integrated Project (Shell Petroleum Development, Nigeria, 2008)

Tank Farm

· KOC Crude Oil Export Facilities Project (Kuwait Oil Company, 2008)

· JPR Zarpa Tank Farm Project (Jordan Petroleum Company, 2000)

Refinery & Petrochemical

· Jazan Refinery and Terminal Project, Package. 2 (Saudi Aramco, 2016(E))

· HCP No.2 BTX Project Daesan (HC Petrochem, Korea, 2013(E))

· Mumbai Diesel Hydro-Desulfurization Project (Hindustan Petroleum Company, India, 2000)

· HPC 2nd Petrochemical Complex Project (Hyundai Oilbank, 1997)

Gas To Liquid · Pearl GTL Feed Gas Preparation Project (Qatar Shell, 2011)

Power

Combined Cycle/ Simple Cycle Power Plant

· Riyadh PP 11 Independent Power Project (Dhuruma Electricity Company, Saudi Arabia, 2013(E))

· Sabiya Combined Cycle Gas Turbine Project (Ministry of Electricity and Water, Kuwait, 2013(E))

· Al Dur Independent Water and Power Project (Al Dur Power & Water Co., Bahrain, 2012)

· Marafiq Independent Water and Power Project (Jubail Water and Power Company, Saudi Arabia, 2010)

· Shaybah Power Generation Project (Saudi Aramco, Saudi Arabia, 2008)

Cogeneration

· Tihama Cogeneration Expansion Project Stage II (Tihama Power Company, Saudi Arabia, 2015(E))

· Saudi Aramco 3rd party Cogeneration Program (Tihama Power Company, Saudi Arabia, 2006)

Thermal

· Jeddah South Thermal Power Plant (Saudi Electricity Company, Saudi Arabia, 2017(E))

· Namjeju #3&4 Thermal Power Plant (KEPCO, Korea, 2007)

· Makkah-Taif Thermal Power Plant (Saline Water Conversion Corporation, Saudi Arabia, 1989)

Desalination Plant

· Taweelah A1 (ADWEA, UAE, 2002) · Taweelah B (ADWEA, UAE, 1995) · Umm Al Nar West (ADWEA, UAE, 1982) · Al Khobar Phase 2 (SWCC, Saudi Arabia,1981)

Riyadh PP11 (Jun. 2010)

- 1.6 bil. USD / Dhuruma Electricity Company, Saudi Arabia (SEC) - 1,756MW Combined cycle power plant

HCP BTX (May 2011)

- 361 mil. USD / HC Petrochem, Korea - #2 BTX project to increase Benzene, Toluene, Xylene (BTX) capacity for HC Petrochem(JV of Hyundai Oilbank 50% + Cosmo Oil Japan 50%)

Jeddah South (Oct. 2012)

- 3.2 bil. USD / Saudi Electricity Company, Saudi Arabia - 2,400MW Oil fired Conventional Power Plant

30

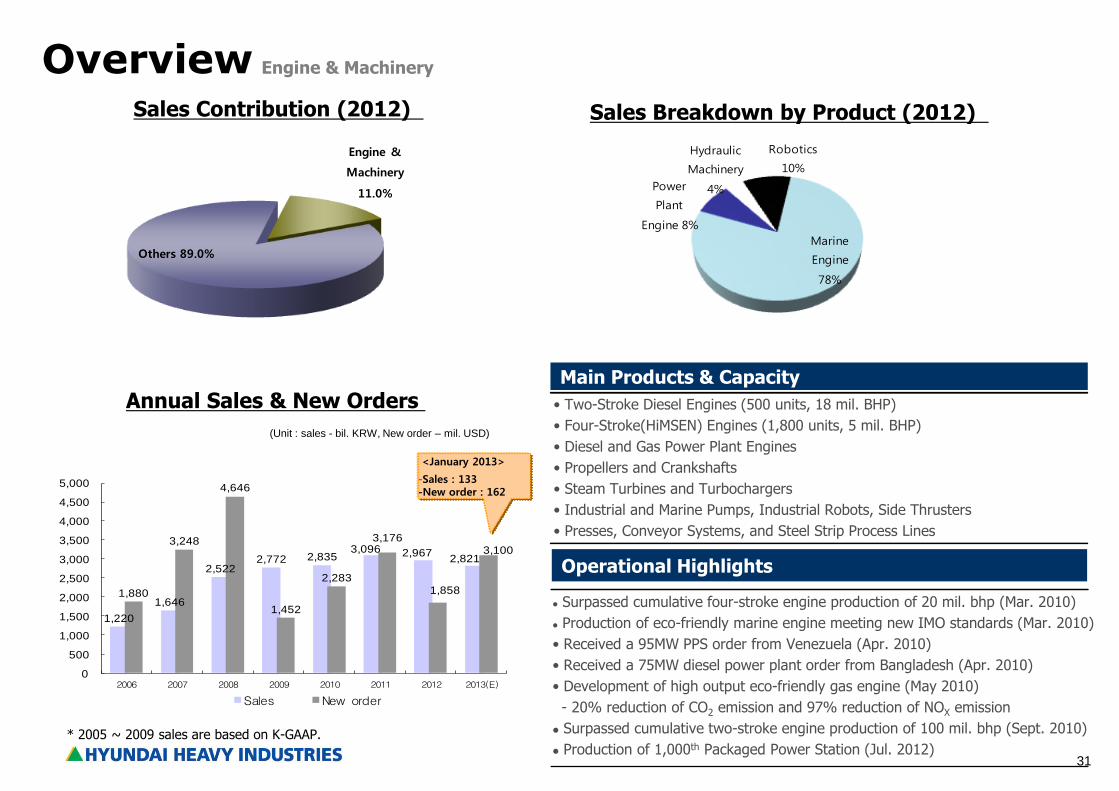

Engine & Machinery

Marine Engine & Equip. Marine & Industrial Turbine Industrial & Marine Pump Industrial Robot & System Marine Propeller

31

Overview

(Unit : sales - bil. KRW, New order – mil. USD)

Annual Sales & New Orders

Engine & Machinery

Sales Breakdown by Product (2012)

Main Products & Capacity

Operational Highlights

• Two-Stroke Diesel Engines (500 units, 18 mil. BHP)

• Four-Stroke(HiMSEN) Engines (1,800 units, 5 mil. BHP)

• Diesel and Gas Power Plant Engines

• Propellers and Crankshafts

• Steam Turbines and Turbochargers

• Industrial and Marine Pumps, Industrial Robots, Side Thrusters

• Presses, Conveyor Systems, and Steel Strip Process Lines

<January 2013>

-Sales : 133 -New order : 162

Sales Contribution (2012)

* 2005 ~ 2009 sales are based on K-GAAP.

Surpassed cumulative four-stroke engine production of 20 mil. bhp (Mar. 2010)

Production of eco-friendly marine engine meeting new IMO standards (Mar. 2010)

• Received a 95MW PPS order from Venezuela (Apr. 2010)

• Received a 75MW diesel power plant order from Bangladesh (Apr. 2010)

• Development of high output eco-friendly gas engine (May 2010)

- 20% reduction of CO2 emission and 97% reduction of NOX emission

Surpassed cumulative two-stroke engine production of 100 mil. bhp (Sept. 2010)

Production of 1,000th Packaged Power Station (Jul. 2012)

Engine &

Machinery

11.0%

Others 89.0%Marine

Engine

78%

Power

Plant

Engine 8%

Hydraulic

Machinery

4%

Robotics

10%

1,220

1,646

2,522 2,772 2,835

3,096 2,967 2,821

1,880

3,248

4,646

1,452

2,283

3,176

1,858

3,100

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2006 2007 2008 2009 2010 2011 2012 2013(E)

Sales New order

32

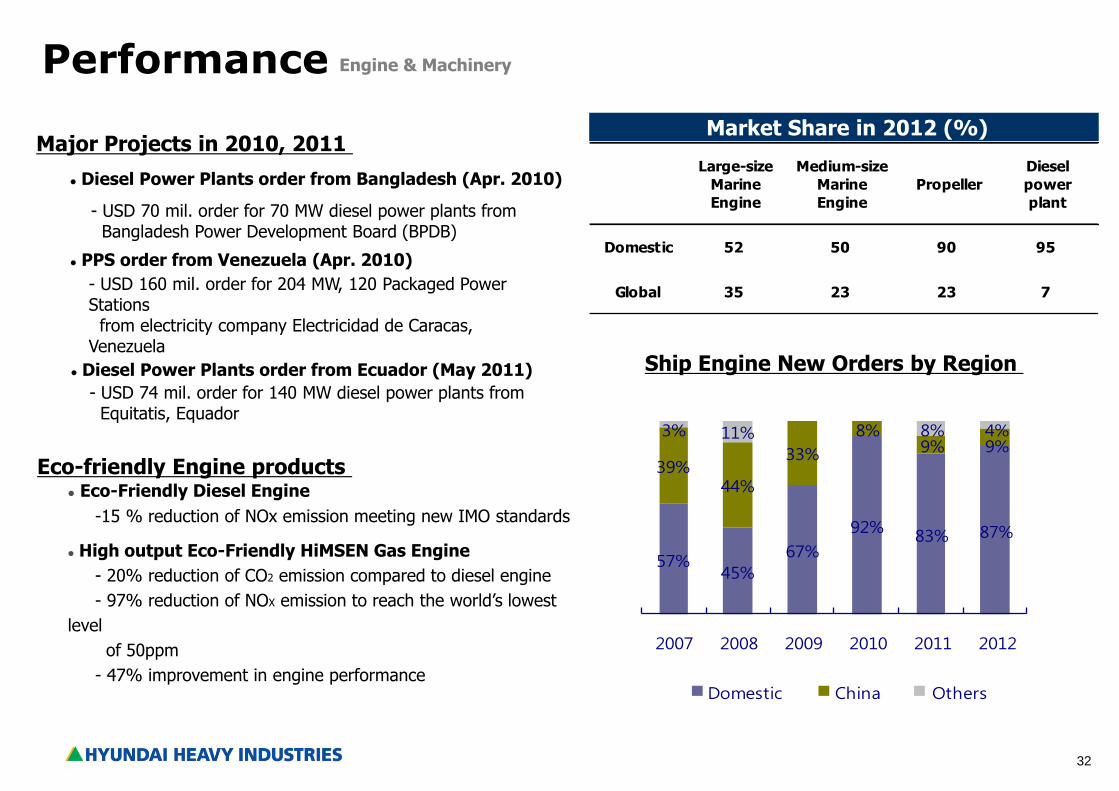

Performance

Eco-Friendly Diesel Engine

-15 % reduction of NOx emission meeting new IMO standards

High output Eco-Friendly HiMSEN Gas Engine

- 20% reduction of CO2 emission compared to diesel engine

- 97% reduction of NOX emission to reach the world’s lowest

level

of 50ppm

- 47% improvement in engine performance

Ship Engine New Orders by Region

Engine & Machinery

Market Share in 2012 (%)

Large-size

Marine

Engine

Medium-size

Marine

Engine

Propeller

Diesel

power

plant

Domestic 52 50 90 95

Global 35 23 23 7

Diesel Power Plants order from Bangladesh (Apr. 2010)

- USD 70 mil. order for 70 MW diesel power plants from Bangladesh Power Development Board (BPDB)

Eco-friendly Engine products

Major Projects in 2010, 2011

PPS order from Venezuela (Apr. 2010)

- USD 160 mil. order for 204 MW, 120 Packaged Power Stations from electricity company Electricidad de Caracas, Venezuela

Diesel Power Plants order from Ecuador (May 2011)

- USD 74 mil. order for 140 MW diesel power plants from Equitatis, Equador

57%45%

67%

92%83% 87%

39%44%

33%

8%9% 9%

3% 11% 8% 4%

2007 2008 2009 2010 2011 2012

Domestic China Others

33

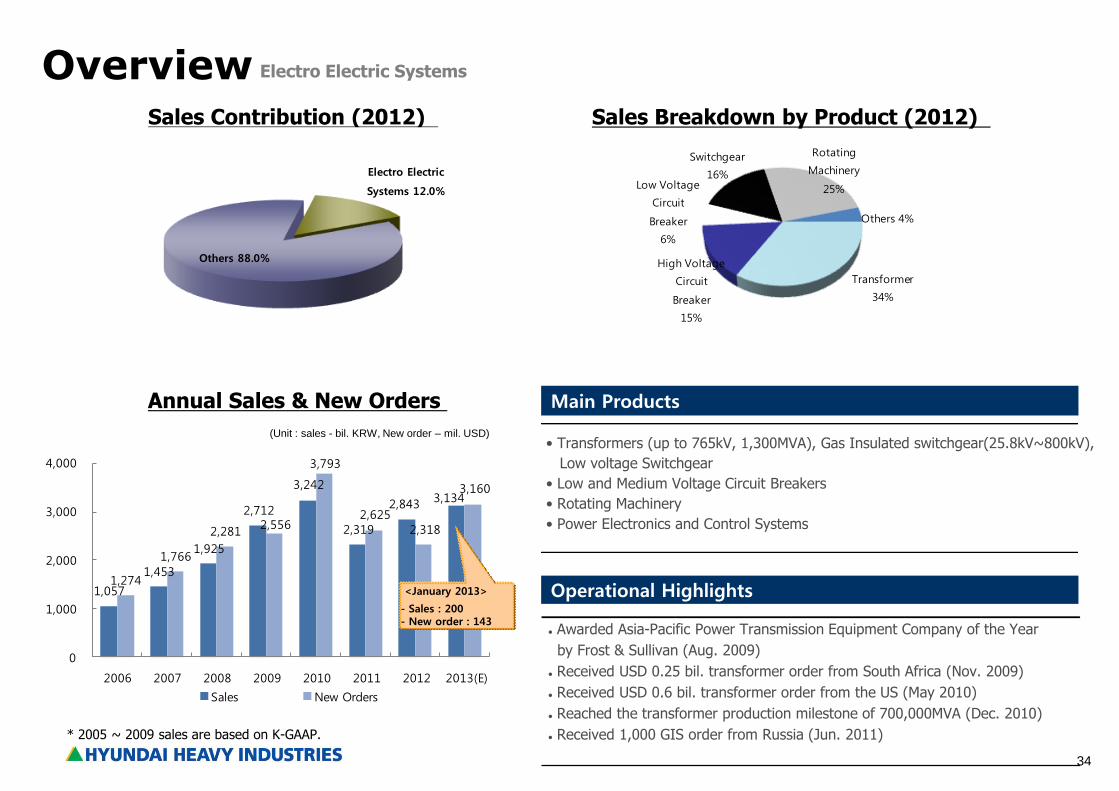

Electro Electric Systems

Transformers High Voltage Circuit Breakers Switchgears Marine Electrical Equip.

34

1,057

1,453

1,925

2,712

3,242

2,319

2,843 3,134

1,274

1,766

2,281 2,556

3,793

2,625 2,318

3,160

0

1,000

2,000

3,000

4,000

2006 2007 2008 2009 2010 2011 2012 2013(E)

Sales New Orders

Overview

(Unit : sales - bil. KRW, New order – mil. USD)

Sales Contribution (2012)

Annual Sales & New Orders

Operational Highlights

Main Products

Electro Electric Systems

Sales Breakdown by Product (2012)

• Transformers (up to 765kV, 1,300MVA), Gas Insulated switchgear(25.8kV~800kV),

Low voltage Switchgear

• Low and Medium Voltage Circuit Breakers

• Rotating Machinery

• Power Electronics and Control Systems

<January 2013>

- Sales : 200 - New order : 143

* 2005 ~ 2009 sales are based on K-GAAP.

Electro Electric

Systems 12.0%

Others 88.0%

Awarded Asia-Pacific Power Transmission Equipment Company of the Year

by Frost & Sullivan (Aug. 2009)

Received USD 0.25 bil. transformer order from South Africa (Nov. 2009)

Received USD 0.6 bil. transformer order from the US (May 2010)

Reached the transformer production milestone of 700,000MVA (Dec. 2010)

Received 1,000 GIS order from Russia (Jun. 2011)

Transformer

34%

High Voltage

Circuit

Breaker

15%

Low Voltage

Circuit

Breaker

6%

Switchgear

16%

Rotating

Machinery

25%

Others 4%

35

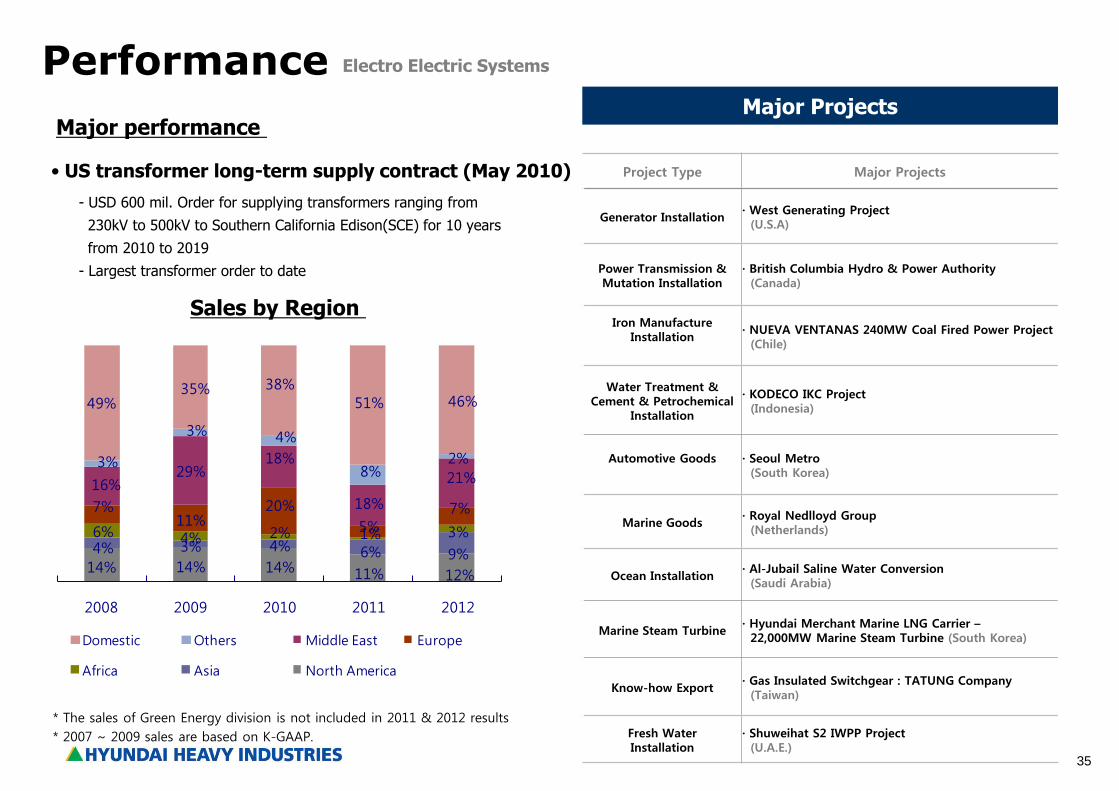

Performance

Sales by Region

Electro Electric Systems

• US transformer long-term supply contract (May 2010)

Major performance

- USD 600 mil. Order for supplying transformers ranging from

230kV to 500kV to Southern California Edison(SCE) for 10 years

from 2010 to 2019

- Largest transformer order to date

* The sales of Green Energy division is not included in 2011 & 2012 results

* 2007 ~ 2009 sales are based on K-GAAP.

14% 14% 14% 11% 12%

4% 3% 4% 6% 9%

6% 4% 2% 1% 3%

7%11%

20%

5%7%

16%29%

18%

18%

21%3%

3% 4%

8%2%

49%35% 38%

51% 46%

2008 2009 2010 2011 2012

Domestic Others Middle East Europe

Africa Asia North America

Major Projects

Project Type Major Projects

Generator Installation · West Generating Project (U.S.A)

Power Transmission & Mutation Installation

· British Columbia Hydro & Power Authority (Canada)

Iron Manufacture Installation

· NUEVA VENTANAS 240MW Coal Fired Power Project (Chile)

Water Treatment & Cement & Petrochemical

Installation

· KODECO IKC Project (Indonesia)

Automotive Goods

· Seoul Metro (South Korea)

Marine Goods · Royal Nedlloyd Group (Netherlands)

Ocean Installation · Al-Jubail Saline Water Conversion (Saudi Arabia)

Marine Steam Turbine · Hyundai Merchant Marine LNG Carrier – 22,000MW Marine Steam Turbine (South Korea)

Know-how Export · Gas Insulated Switchgear : TATUNG Company (Taiwan)

Fresh Water Installation

· Shuweihat S2 IWPP Project (U.A.E.)

36

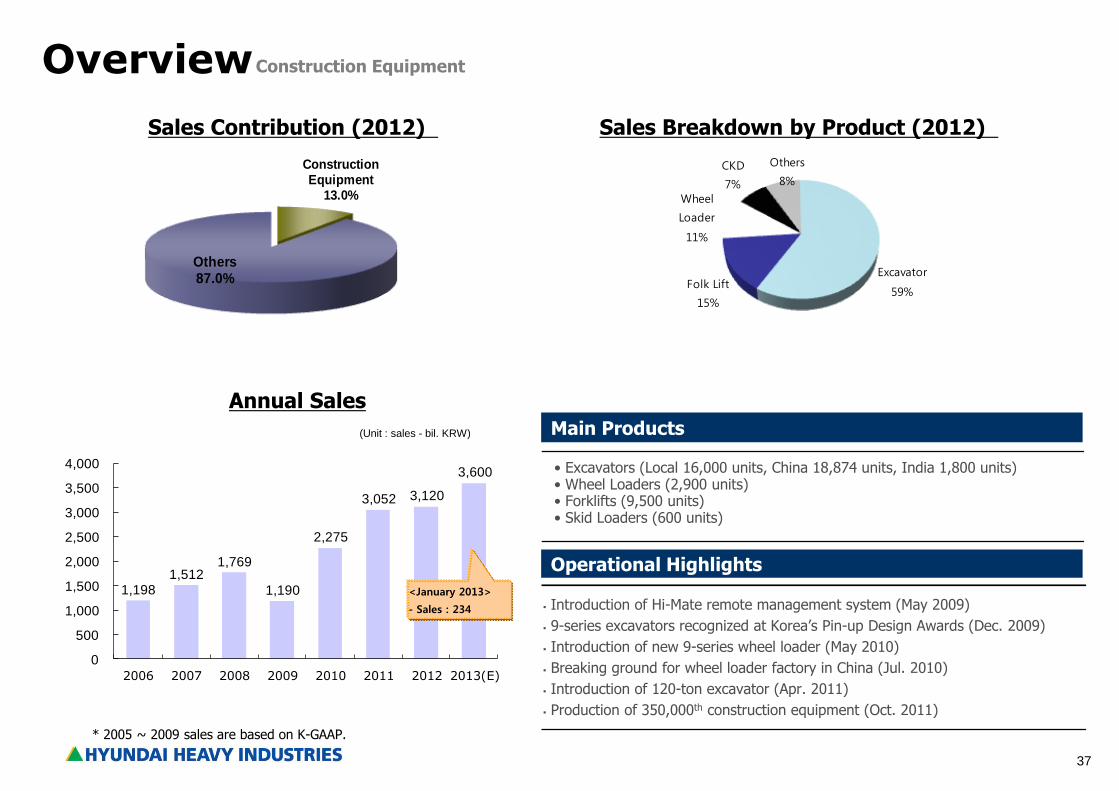

Construction Equipment

Crawler Excavator Wheel Loader Forklift Truck Skid Steer Loader Mini Excavator Wheel Excavator

37

Construction Equipment

13.0%

Others 87.0%

1,198 1,512

1,769

1,190

2,275

3,052 3,120

3,600

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2006 2007 2008 2009 2010 2011 2012 2013(E)

Overview

(Unit : sales - bil. KRW)

Annual Sales

Operational Highlights

Main Products

Construction Equipment

Sales Breakdown by Product (2012)

<January 2013>

- Sales : 234

• Excavators (Local 16,000 units, China 18,874 units, India 1,800 units) • Wheel Loaders (2,900 units) • Forklifts (9,500 units) • Skid Loaders (600 units)

Sales Contribution (2012)

* 2005 ~ 2009 sales are based on K-GAAP.

Introduction of Hi-Mate remote management system (May 2009)

9-series excavators recognized at Korea’s Pin-up Design Awards (Dec. 2009)

Introduction of new 9-series wheel loader (May 2010)

Breaking ground for wheel loader factory in China (Jul. 2010)

Introduction of 120-ton excavator (Apr. 2011)

Production of 350,000th construction equipment (Oct. 2011)

Excavator

59%Folk Lift

15%

Wheel

Loader

11%

CKD

7%

Others

8%

38

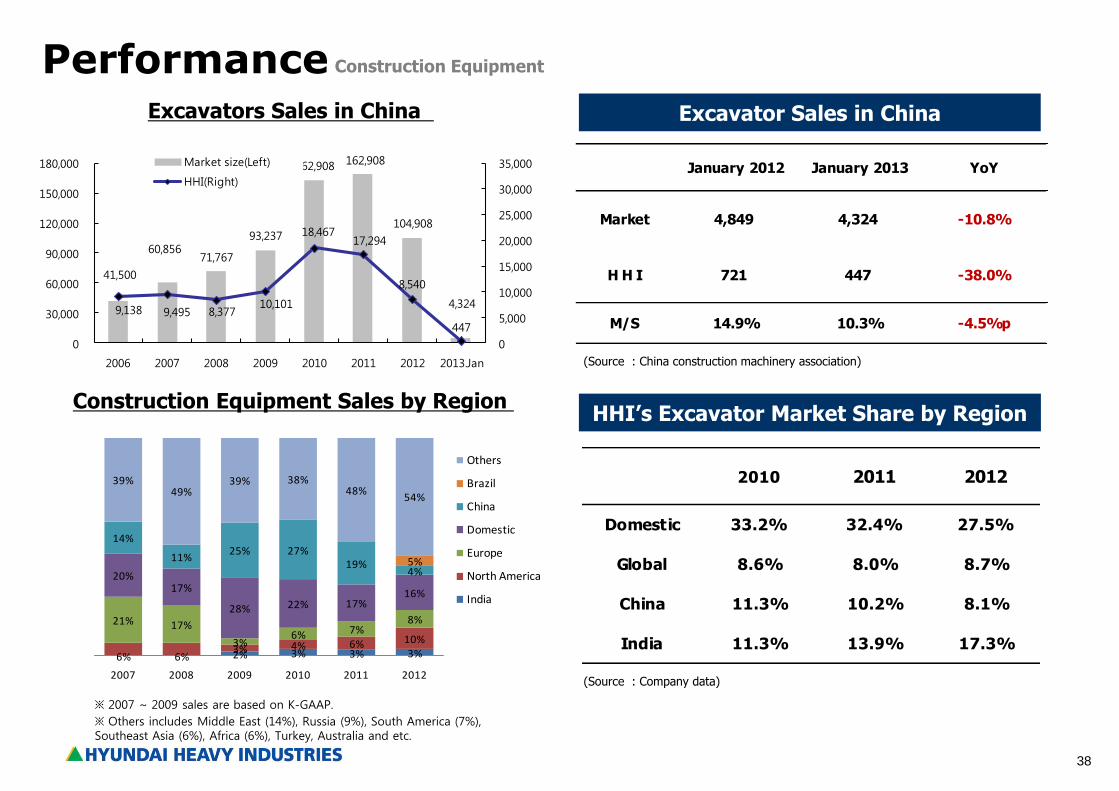

Construction Equipment Sales by Region

Performance Construction Equipment

Excavators Sales in China

※ Others includes Middle East (14%), Russia (9%), South America (7%), Southeast Asia (6%), Africa (6%), Turkey, Australia and etc.

January 2012 January 2013 YoY

Market 4,849 4,324 -10.8%

H H I 721 447 -38.0%

M/S 14.9% 10.3% -4.5%p

Excavator Sales in China

HHI’s Excavator Market Share by Region

※ 2007 ~ 2009 sales are based on K-GAAP.

(Source : Company data)

(Source : China construction machinery association)

41,500

60,856 71,767

93,237

162,908 162,908

104,908

4,324 9,138 9,495 8,377

10,101

18,467 17,294

8,540

447

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

0

30,000

60,000

90,000

120,000

150,000

180,000

2006 2007 2008 2009 2010 2011 2012 2013.Jan

Market size(Left)

HHI(Right)

6% 6% 2% 3% 3% 3%3% 4% 6% 10%

21% 17%

3%6% 7%

8%

20%17%

28% 22% 17%16%

14%

11%25% 27%

19%4%5%

39%49%

39% 38%48%

54%

2007 2008 2009 2010 2011 2012

Others

Brazil

China

Domestic

Europe

North America

India

2010 2011 2012

Domestic 33.2% 32.4% 27.5%

Global 8.6% 8.0% 8.7%

China 11.3% 10.2% 8.1%

India 11.3% 13.9% 17.3%

39

Green Energy

Solar Power Wind Power

40

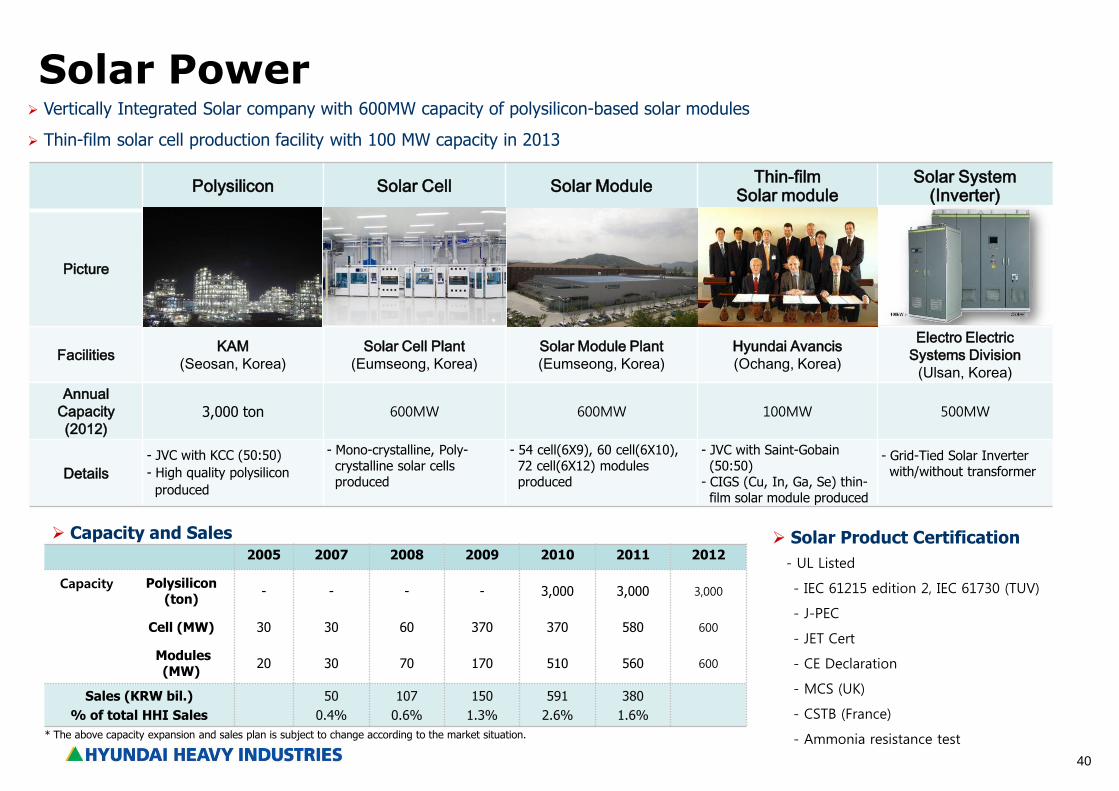

Polysilicon Solar Cell Solar Module Thin-film

Solar module Solar System

(Inverter)

Picture

Facilities KAM

(Seosan, Korea)

Solar Cell Plant

(Eumseong, Korea)

Solar Module Plant

(Eumseong, Korea)

Hyundai Avancis

(Ochang, Korea)

Electro Electric

Systems Division

(Ulsan, Korea)

Annual

Capacity

(2012) 3,000 ton 600MW 600MW 100MW 500MW

Details

- JVC with KCC (50:50)

- High quality polysilicon

produced

- Mono-crystalline, Poly- crystalline solar cells produced

- 54 cell(6X9), 60 cell(6X10), 72 cell(6X12) modules produced

- JVC with Saint-Gobain (50:50) - CIGS (Cu, In, Ga, Se) thin- film solar module produced

- Grid-Tied Solar Inverter with/without transformer

Solar Power

Vertically Integrated Solar company with 600MW capacity of polysilicon-based solar modules

Thin-film solar cell production facility with 100 MW capacity in 2013

Capacity and Sales

2005 2007 2008 2009 2010 2011 2012

Capacity

Polysilicon (ton)

- - - - 3,000 3,000 3,000

Cell (MW) 30 30 60 370 370 580 600

Modules (MW)

20 30 70 170 510 560 600

Sales (KRW bil.)

% of total HHI Sales

50

0.4%

107

0.6%

150

1.3%

591

2.6%

380

1.6%

Solar Product Certification

- UL Listed

- IEC 61215 edition 2, IEC 61730 (TUV)

- J-PEC

- JET Cert

- CE Declaration

- MCS (UK)

- CSTB (France)

- Ammonia resistance test * The above capacity expansion and sales plan is subject to change according to the market situation.

41

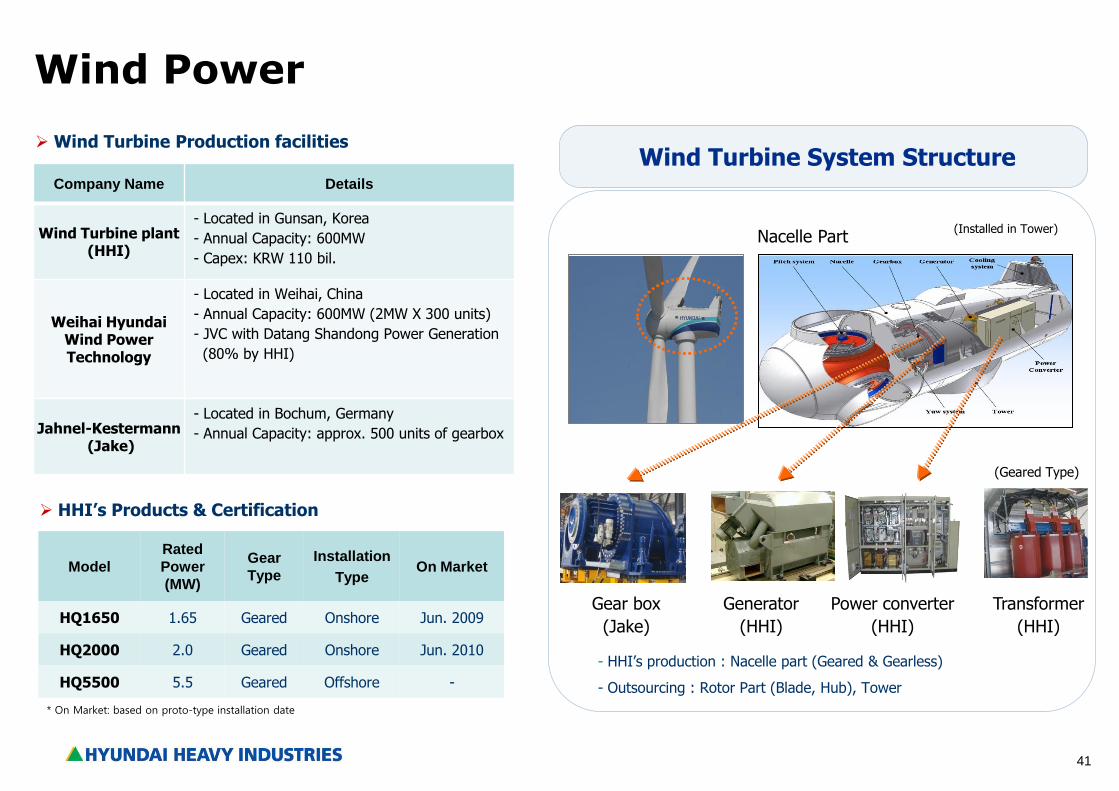

Wind Power

- HHI’s production : Nacelle part (Geared & Gearless)

- Outsourcing : Rotor Part (Blade, Hub), Tower

Generator

(HHI)

Gear box

(Jake)

Power converter

(HHI)

Transformer

(HHI)

(Installed in Tower)

Wind Turbine Production facilities

HHI’s Products & Certification

(Geared Type)

Model

Rated

Power

(MW)

Gear

Type

Installation

Type On Market

HQ1650 1.65 Geared Onshore Jun. 2009

HQ2000 2.0 Geared Onshore Jun. 2010

HQ5500 5.5 Geared Offshore -

Nacelle Part

Wind Turbine System Structure Company Name Details

Wind Turbine plant (HHI)

- Located in Gunsan, Korea

- Annual Capacity: 600MW

- Capex: KRW 110 bil.

Weihai Hyundai Wind Power Technology

- Located in Weihai, China

- Annual Capacity: 600MW (2MW X 300 units)

- JVC with Datang Shandong Power Generation

(80% by HHI)

Jahnel-Kestermann (Jake)

- Located in Bochum, Germany

- Annual Capacity: approx. 500 units of gearbox

* On Market: based on proto-type installation date

42

Subsidiaries

43

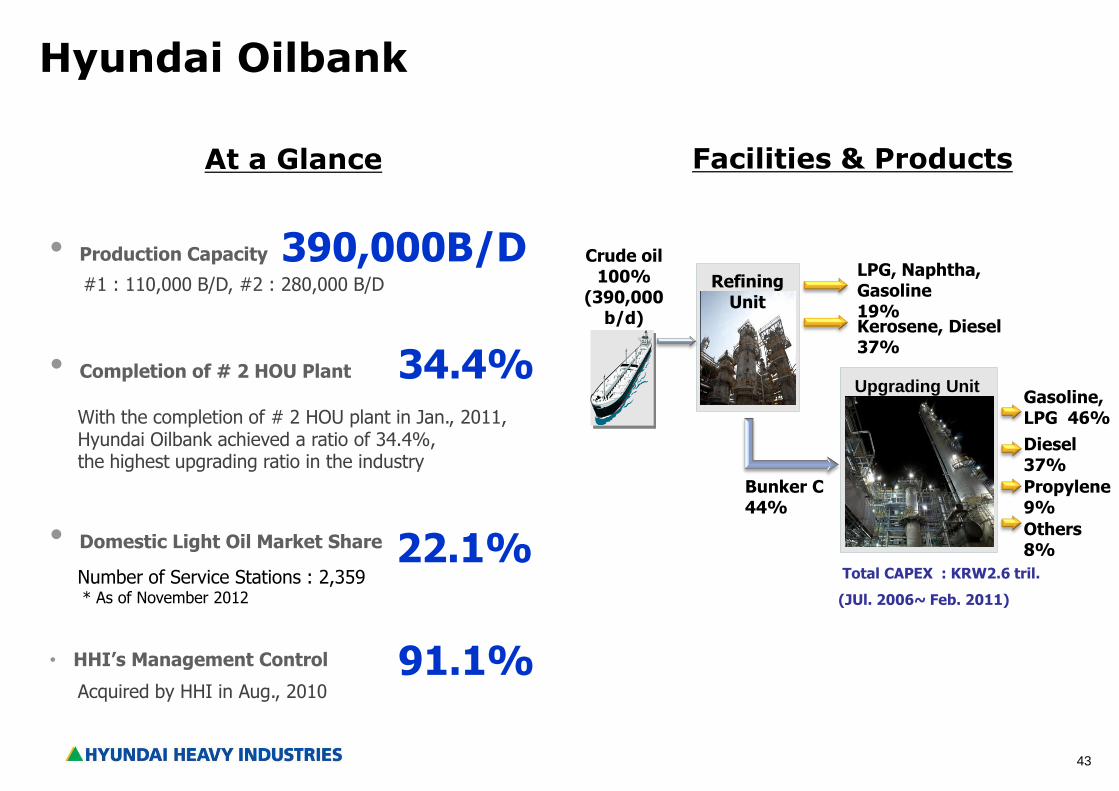

Hyundai Oilbank

Refining Unit

Upgrading Unit

Crude oil 100%

(390,000 b/d)

LPG, Naphtha, Gasoline 19% Kerosene, Diesel 37%

Bunker C 44%

Gasoline, LPG 46%

Diesel 37%

Propylene 9%

Others 8%

Total CAPEX : KRW2.6 tril.

(JUl. 2006~ Feb. 2011)

• Completion of # 2 HOU Plant 34.4% With the completion of # 2 HOU plant in Jan., 2011, Hyundai Oilbank achieved a ratio of 34.4%, the highest upgrading ratio in the industry

At a Glance

• Domestic Light Oil Market Share 22.1% Number of Service Stations : 2,359 * As of November 2012

• Production Capacity 390,000B/D #1 : 110,000 B/D, #2 : 280,000 B/D

Facilities & Products

• HHI’s Management Control 91.1% Acquired by HHI in Aug., 2010

44

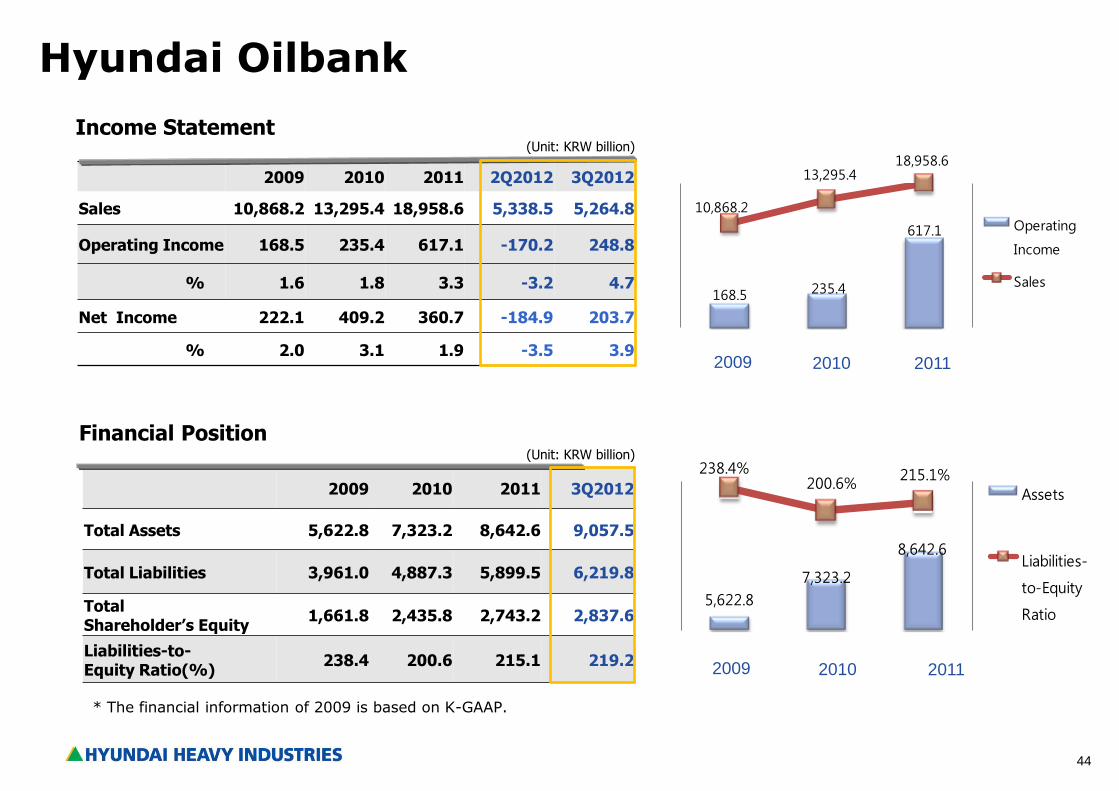

2009 2010 2011 2Q2012 3Q2012

Sales 10,868.2 13,295.4 18,958.6 5,338.5 5,264.8

Operating Income 168.5 235.4 617.1 -170.2 248.8

% 1.6 1.8 3.3 -3.2 4.7

Net Income 222.1 409.2 360.7 -184.9 203.7

% 2.0 3.1 1.9 -3.5 3.9

(Unit: KRW billion)

Income Statement

2009 2010 2011 3Q2012

Total Assets 5,622.8 7,323.2 8,642.6 9,057.5

Total Liabilities 3,961.0 4,887.3 5,899.5 6,219.8

Total Shareholder’s Equity

1,661.8 2,435.8 2,743.2 2,837.6

Liabilities-to- Equity Ratio(%)

238.4 200.6 215.1 219.2

(Unit: KRW billion)

Financial Position

Hyundai Oilbank

* The financial information of 2009 is based on K-GAAP.

2011 2009 2010

2011 2009 2010

5,622.8

7,323.2

8,642.6

238.4%200.6%

215.1%

Assets

Liabilities-

to-Equity

Ratio

168.5 235.4

617.1

10,868.2

13,295.418,958.6

Operating

Income

Sales

45

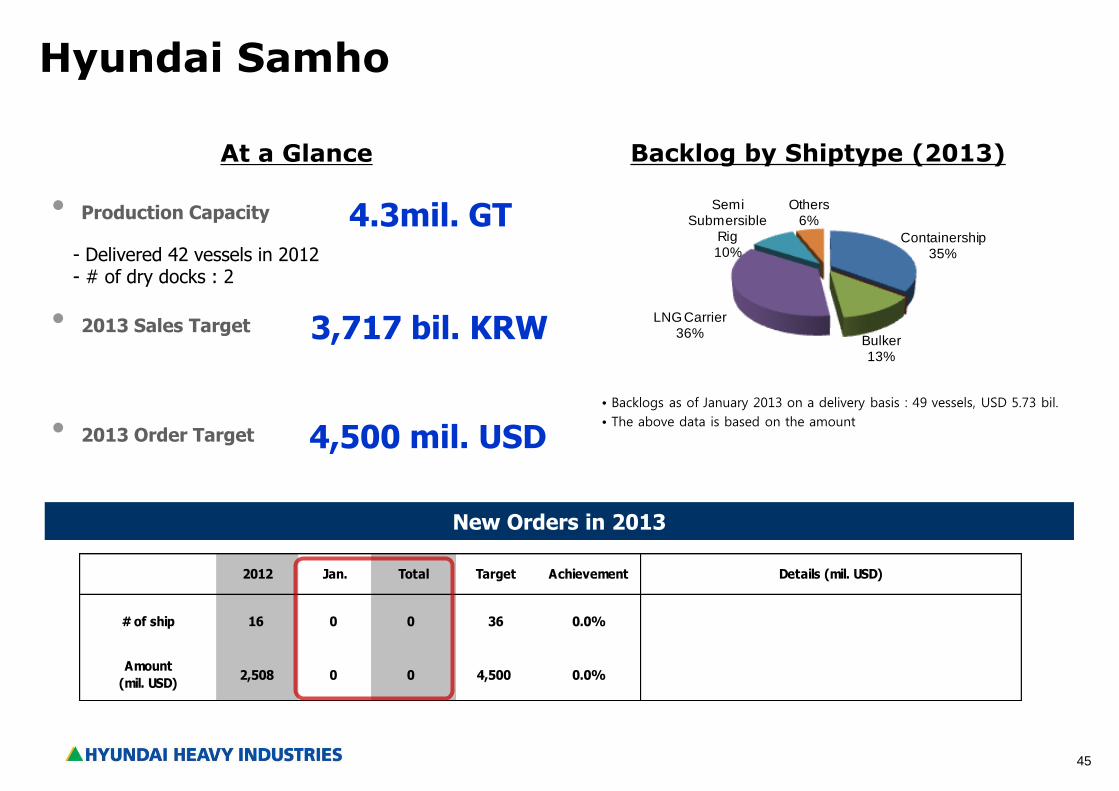

Containership35%

Bulker13%

LNG Carrier36%

Semi Submersible

Rig10%

Others6%

New Orders in 2013

2012 Jan. Total Target Achievement Details (mil. USD)

# of ship 16 0 0 36 0.0%

Amount

(mil. USD)2,508 0 0 4,500 0.0%

At a Glance

Hyundai Samho

• Production Capacity 4.3mil. GT - Delivered 42 vessels in 2012 - # of dry docks : 2

• 2013 Order Target

• 2013 Sales Target

Backlog by Shiptype (2013)

4,500 mil. USD

3,717 bil. KRW

• Backlogs as of January 2013 on a delivery basis : 49 vessels, USD 5.73 bil.

• The above data is based on the amount

-6 LNG Carriers (1,252) -1 Semi Submersible Rig (568) -4 VLCCs (354) -2 Containerships (120) -3 PCTCs (214)

46

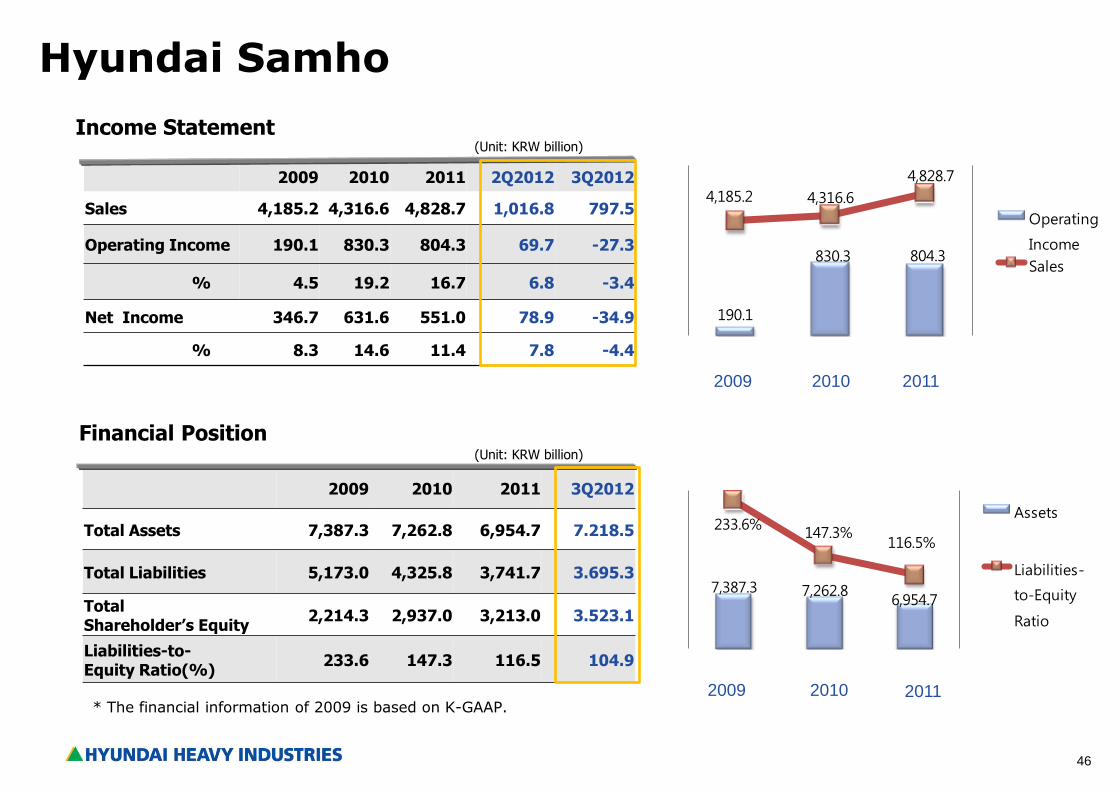

2009 2010 2011 2Q2012 3Q2012

Sales 4,185.2 4,316.6 4,828.7 1,016.8 797.5

Operating Income 190.1 830.3 804.3 69.7 -27.3

% 4.5 19.2 16.7 6.8 -3.4

Net Income 346.7 631.6 551.0 78.9 -34.9

% 8.3 14.6 11.4 7.8 -4.4

(Unit: KRW billion)

Income Statement

2009 2010 2011 3Q2012

Total Assets 7,387.3 7,262.8 6,954.7 7.218.5

Total Liabilities 5,173.0 4,325.8 3,741.7 3.695.3

Total Shareholder’s Equity

2,214.3 2,937.0 3,213.0 3.523.1

Liabilities-to- Equity Ratio(%)

233.6 147.3 116.5 104.9

(Unit: KRW billion)

Financial Position

2009 2010 2011

2011 2009 2010

Hyundai Samho

* The financial information of 2009 is based on K-GAAP.

190.1

830.3 804.3

4,185.2 4,316.6

4,828.7

Operating

Income

Sales

7,387.3 7,262.8 6,954.7

233.6%147.3%

116.5%

Assets

Liabilities-

to-Equity

Ratio

47

Financial Performance

48

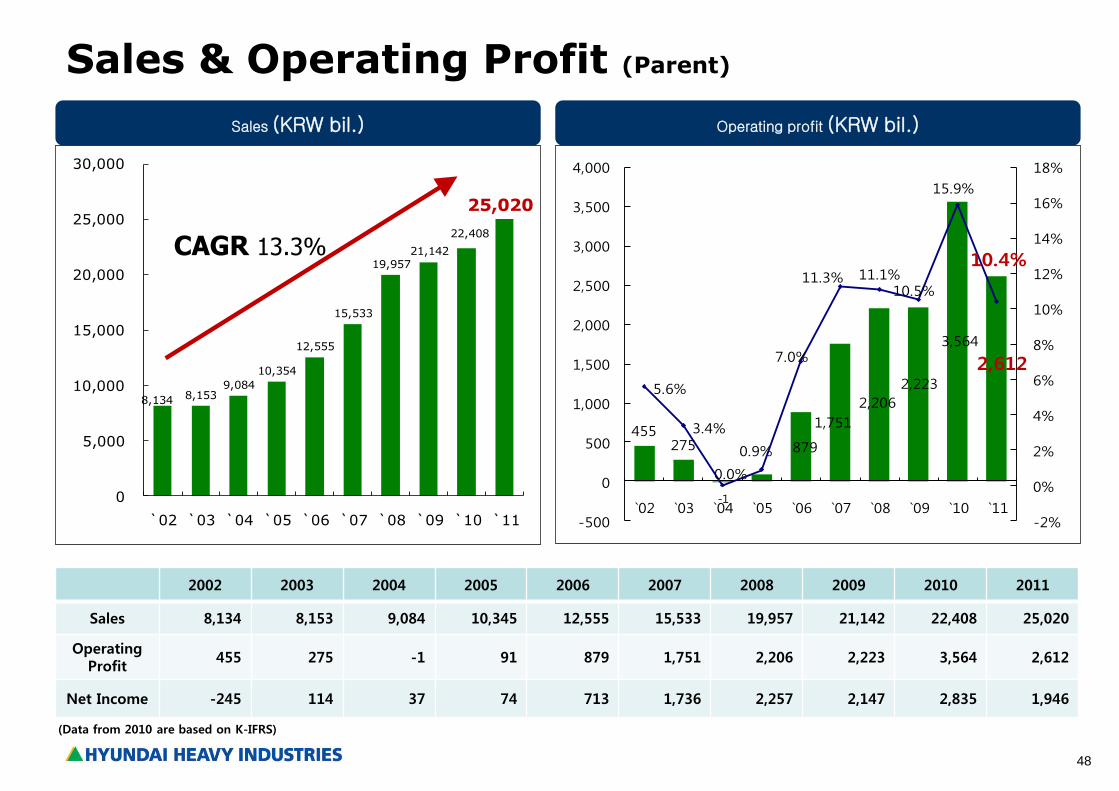

455275

-1

879

1,751

2,206

2,223

3,564

2,612

5.6%

3.4%

0.0%

0.9%

7.0%

11.3% 11.1%10.5%

15.9%

10.4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

-500

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

`02 `03 `04 `05 `06 `07 `08 `09 `10 `11

8,134 8,153 9,084

10,354

12,555

15,533

19,957 21,142

22,408

25,020

0

5,000

10,000

15,000

20,000

25,000

30,000

`02 `03 `04 `05 `06 `07 `08 `09 `10 `11

Sales (KRW bil.) Operating profit (KRW bil.)

(Data from 2010 are based on K-IFRS)

Sales & Operating Profit (Parent)

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Sales 8,134 8,153 9,084 10,345 12,555 15,533 19,957 21,142 22,408 25,020

Operating Profit

455 275 -1 91 879 1,751 2,206 2,223 3,564 2,612

Net Income -245 114 37 74 713 1,736 2,257 2,147 2,835 1,946

CAGR 13.3%

49

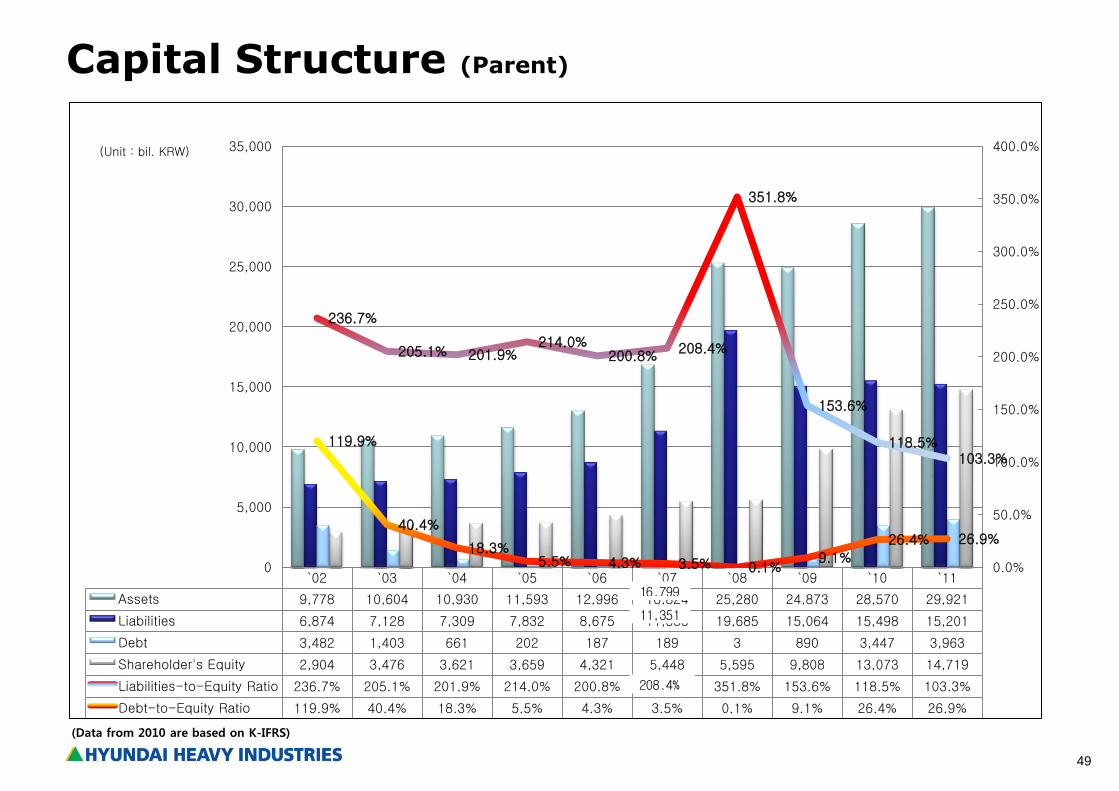

Capital Structure (Parent)

(Unit : bil. KRW)

(Data from 2010 are based on K-IFRS)

`02 `03 `04 `05 `06 `07 `08 `09 `10 `11

Assets 9,778 10,604 10,930 11,593 12,996 16,824 25,280 24,873 28,570 29,921

Liabilities 6,874 7,128 7,309 7,832 8,675 11,333 19,685 15,064 15,498 15,201

Debt 3,482 1,403 661 202 187 189 3 890 3,447 3,963

Shareholder's Equity 2,904 3,476 3,621 3,659 4,321 5,448 5,595 9,808 13,073 14,719

Liabilities-to-Equity Ratio 236.7% 205.1% 201.9% 214.0% 200.8% 208.0% 351.8% 153.6% 118.5% 103.3%

Debt-to-Equity Ratio 119.9% 40.4% 18.3% 5.5% 4.3% 3.5% 0.1% 9.1% 26.4% 26.9%

236.7%

205.1% 201.9% 214.0%

200.8% 208.4%

351.8%

153.6%

118.5% 103.3%

119.9%

40.4%

18.3% 5.5% 4.3% 3.5% 0.1%

9.1%

26.4% 26.9%

0.0%

50.0%

100.0%

150.0%

200.0%

250.0%

300.0%

350.0%

400.0%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

16,799

11,351

208.4%

50

Appendix

(Quarterly Results)

Important Notice

The financial information regarding “3Q, , 2Q 2012 and 3Q 2011 Consolidated Earnings Release” is consolidated

financial earnings results based on K-IFRS.

51

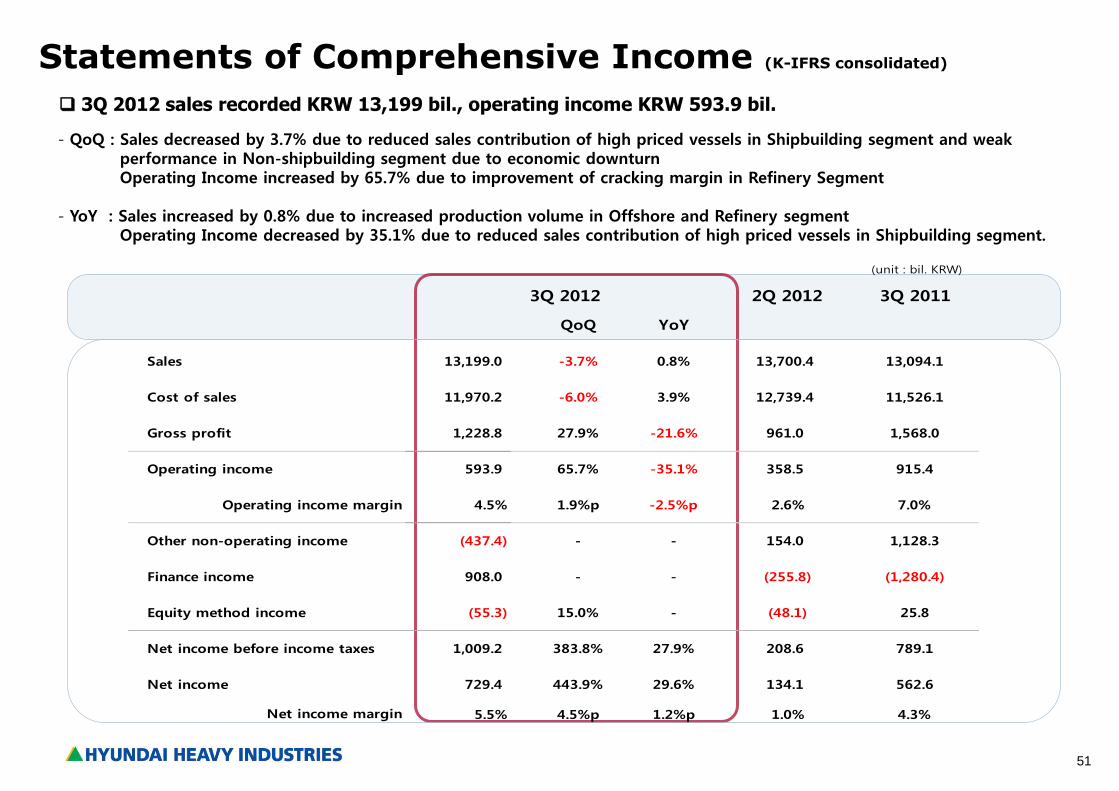

Statements of Comprehensive Income (K-IFRS consolidated)

(unit : bil. KRW)

2Q 2012 3Q 2011

QoQ YoY

13,199.0 -3.7% 0.8% 13,700.4 13,094.1

Cost of sales 11,970.2 -6.0% 3.9% 12,739.4 11,526.1

1,228.8 27.9% -21.6% 961.0 1,568.0

593.9 65.7% -35.1% 358.5 915.4

4.5% 1.9%p -2.5%p 2.6% 7.0%

(437.4) - - 154.0 1,128.3

908.0 - - (255.8) (1,280.4)

Equity method income (55.3) 15.0% - (48.1) 25.8

1,009.2 383.8% 27.9% 208.6 789.1

729.4 443.9% 29.6% 134.1 562.6

5.5% 4.5%p 1.2%p 1.0% 4.3%

Net income before income taxes

Operating income margin

Finance income

Net income margin

3Q 2012

Net income

Operating income

Other non-operating income

Sales

Gross profit

3Q 2012 sales recorded KRW 13,199 bil., operating income KRW 593.9 bil.

- QoQ : Sales decreased by 3.7% due to reduced sales contribution of high priced vessels in Shipbuilding segment and weak performance in Non-shipbuilding segment due to economic downturn Operating Income increased by 65.7% due to improvement of cracking margin in Refinery Segment - YoY : Sales increased by 0.8% due to increased production volume in Offshore and Refinery segment Operating Income decreased by 35.1% due to reduced sales contribution of high priced vessels in Shipbuilding segment.

52

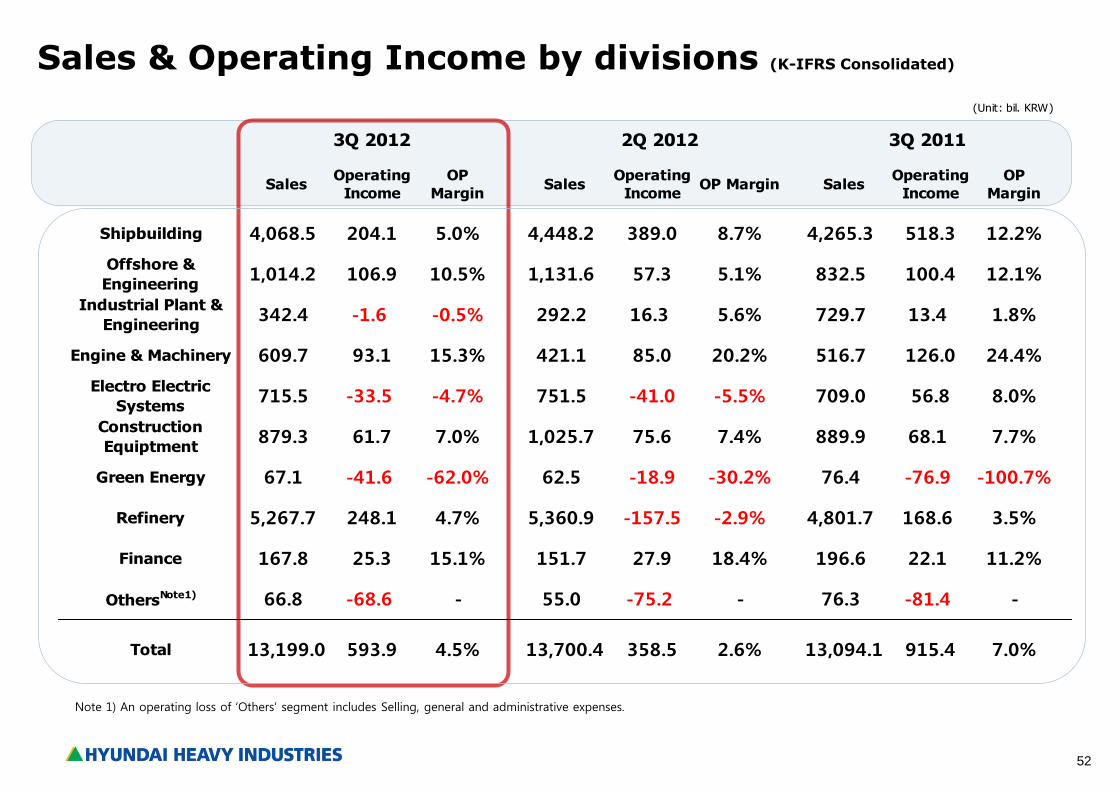

Sales & Operating Income by divisions (K-IFRS Consolidated)

Note 1) An operating loss of ‘Others’ segment includes Selling, general and administrative expenses.

SalesOperating

Income

OP

MarginSales

Operating

IncomeOP Margin Sales

Operating

Income

OP

Margin

Shipbuilding 4,068.5 204.1 5.0% 4,448.2 389.0 8.7% 4,265.3 518.3 12.2%

Offshore &

Engineering1,014.2 106.9 10.5% 1,131.6 57.3 5.1% 832.5 100.4 12.1%

Industrial Plant &

Engineering342.4 -1.6 -0.5% 292.2 16.3 5.6% 729.7 13.4 1.8%

Engine & Machinery 609.7 93.1 15.3% 421.1 85.0 20.2% 516.7 126.0 24.4%

Electro Electric

Systems715.5 -33.5 -4.7% 751.5 -41.0 -5.5% 709.0 56.8 8.0%

Construction

Equiptment879.3 61.7 7.0% 1,025.7 75.6 7.4% 889.9 68.1 7.7%

Green Energy 67.1 -41.6 -62.0% 62.5 -18.9 -30.2% 76.4 -76.9 -100.7%

Refinery 5,267.7 248.1 4.7% 5,360.9 -157.5 -2.9% 4,801.7 168.6 3.5%

Finance 167.8 25.3 15.1% 151.7 27.9 18.4% 196.6 22.1 11.2%

OthersNote1) 66.8 -68.6 - 55.0 -75.2 - 76.3 -81.4 -

Total 13,199.0 593.9 4.5% 13,700.4 358.5 2.6% 13,094.1 915.4 7.0%

2Q 2012

(Unit: bil. KRW)

3Q 2012 3Q 2011

53

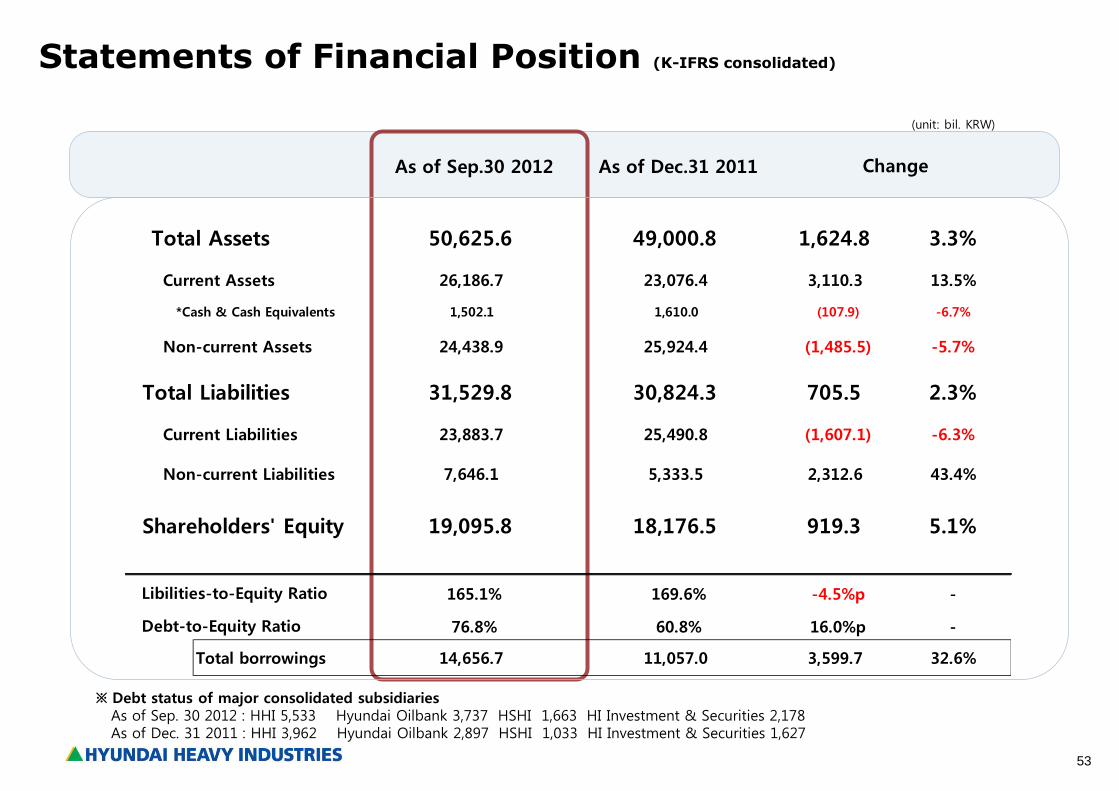

Statements of Financial Position (K-IFRS consolidated)

(unit: bil. KRW)

As of Sep.30 2012 As of Dec.31 2011

Total Assets 50,625.6 49,000.8 1,624.8 3.3%

26,186.7 23,076.4 3,110.3 13.5%

1,502.1 1,610.0 (107.9) -6.7%

24,438.9 25,924.4 (1,485.5) -5.7%

31,529.8 30,824.3 705.5 2.3%

23,883.7 25,490.8 (1,607.1) -6.3%

7,646.1 5,333.5 2,312.6 43.4%

19,095.8 18,176.5 919.3 5.1%

165.1% 169.6% -4.5%p -

76.8% 60.8% 16.0%p -

Total borrowings 14,656.7 11,057.0 3,599.7 32.6%

Libilities-to-Equity Ratio

Change

Debt-to-Equity Ratio

Current Assets

Non-current Assets

Total Liabilities

Current Liabilities

Non-current Liabilities

Shareholders' Equity

*Cash & Cash Equivalents

※ Debt status of major consolidated subsidiaries As of Sep. 30 2012 : HHI 5,533 Hyundai Oilbank 3,737 HSHI 1,663 HI Investment & Securities 2,178 As of Dec. 31 2011 : HHI 3,962 Hyundai Oilbank 2,897 HSHI 1,033 HI Investment & Securities 1,627

54

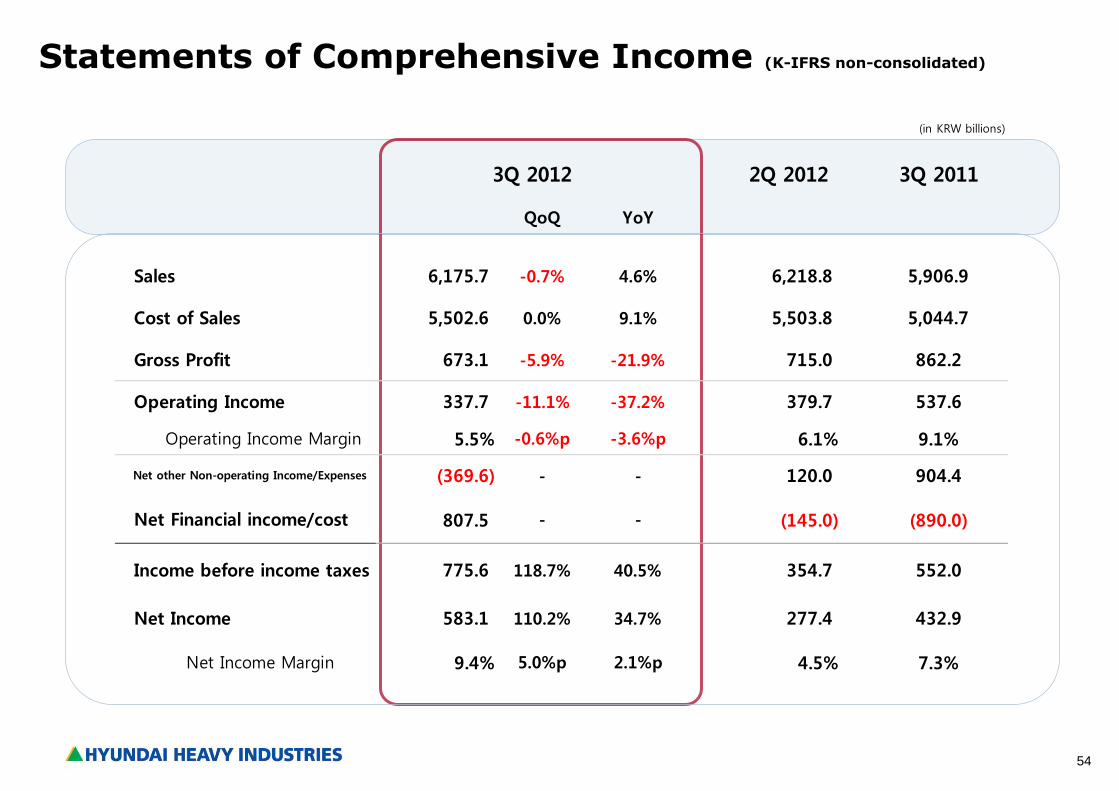

Statements of Comprehensive Income (K-IFRS non-consolidated)

(in KRW billions)

2Q 2012 3Q 2011

QoQ YoY

6,175.7 -0.7% 4.6% 6,218.8 5,906.9

5,502.6 0.0% 9.1% 5,503.8 5,044.7

673.1 -5.9% -21.9% 715.0 862.2

337.7 -11.1% -37.2% 379.7 537.6

5.5% -0.6%p -3.6%p 6.1% 9.1%

(369.6) - - 120.0 904.4

807.5 - - (145.0) (890.0)

775.6 118.7% 40.5% 354.7 552.0

583.1 110.2% 34.7% 277.4 432.9

9.4% 5.0%p 2.1%p 4.5% 7.3% Net Income Margin

3Q 2012

Net Income

Operating Income

Net other Non-operating Income/Expenses

Sales

Gross Profit

Income before income taxes

Cost of Sales

Operating Income Margin

Net Financial income/cost

55

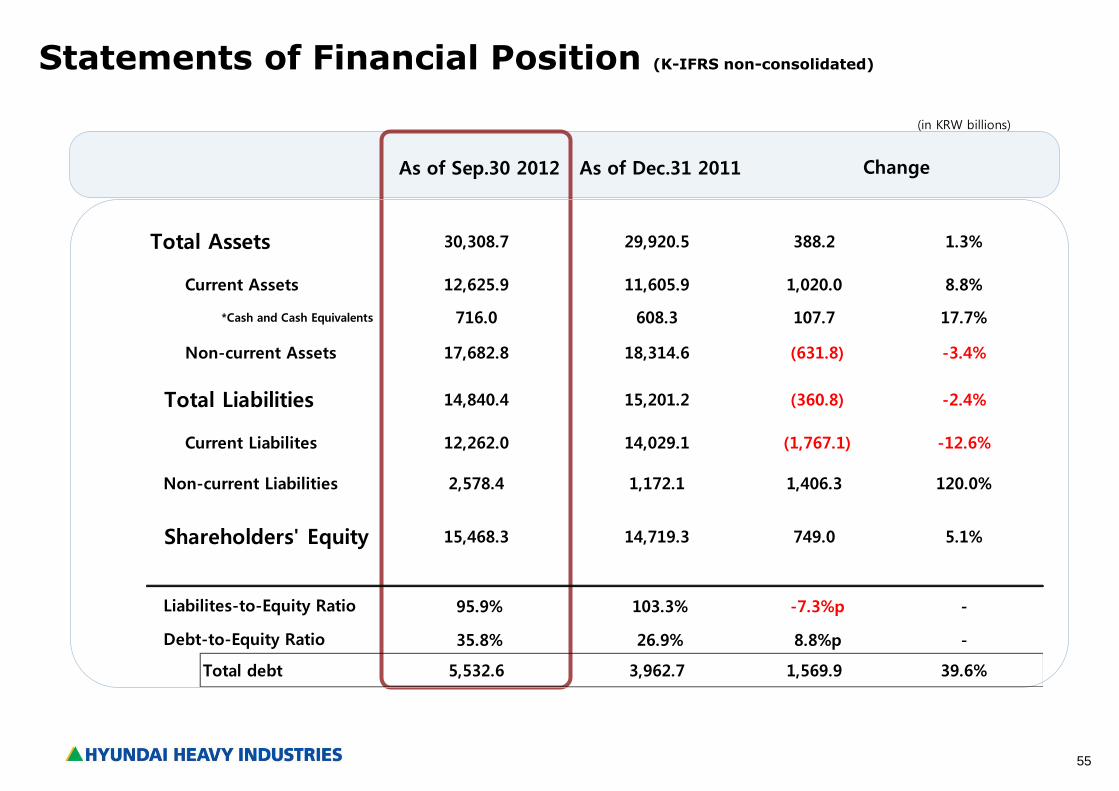

Statements of Financial Position (K-IFRS non-consolidated)

(in KRW billions)

As of Sep.30 2012 As of Dec.31 2011

Total Assets 30,308.7 29,920.5 388.2 1.3%

12,625.9 11,605.9 1,020.0 8.8%

*Cash and Cash Equivalents 716.0 608.3 107.7 17.7%

17,682.8 18,314.6 (631.8) -3.4%

14,840.4 15,201.2 (360.8) -2.4%

12,262.0 14,029.1 (1,767.1) -12.6%

2,578.4 1,172.1 1,406.3 120.0%

15,468.3 14,719.3 749.0 5.1%

95.9% 103.3% -7.3%p -

35.8% 26.9% 8.8%p -

Total debt 5,532.6 3,962.7 1,569.9 39.6%

Liabilites-to-Equity Ratio

Change

Debt-to-Equity Ratio

Current Assets

Non-current Assets

Total Liabilities

Current Liabilites

Non-current Liabilities

Shareholders' Equity

56

Q & A

57

Thank You Http://www.hhiir.com

*For More Information

IR Team

E-mail: [email protected]

Tel: +82-2-746-4728, 4546, 7858

Fax: +82-746-4662

Website: www.hhi.co.kr (Company) /www.hhiir.com (IR)