Embed Size (px)

Citation preview

Hymans Robertson LLP and Hymans Robertson Financial Services LLP are authorised and regulated by the Financial Services Authority

Leicestershire Pension FundAnnual General Meeting

• John Wright

• Barry McKay

• 15 January 2013

LGPS up-date

2

Some topical issues

2013 Valuation

Pensions Reform:

LGPS 2014, Governance, Cost Control

Auto-enrolment

New flat-rate state pension

Other issues:

Infrastructure and local investment

2013 Valuation

4

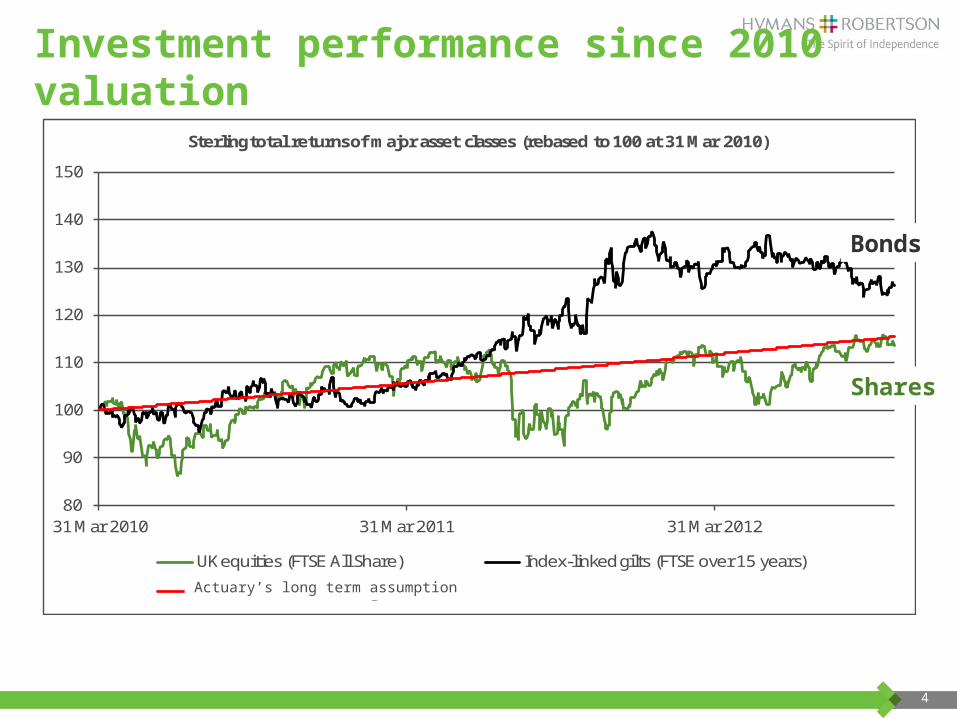

Investment performance since 2010 valuation

80

90

100

110

120

130

140

150

31 Mar 2010 31 Mar 2011 31 Mar 2012

Sterling total returns of major asset classes (rebased to 100 at 31 Mar 2010)

UK equities (FTSE All Share) Index-linked gilts (FTSE over 15 years)

Discount rate unwindingActuary’s long term assumption

Bonds

Shares

5

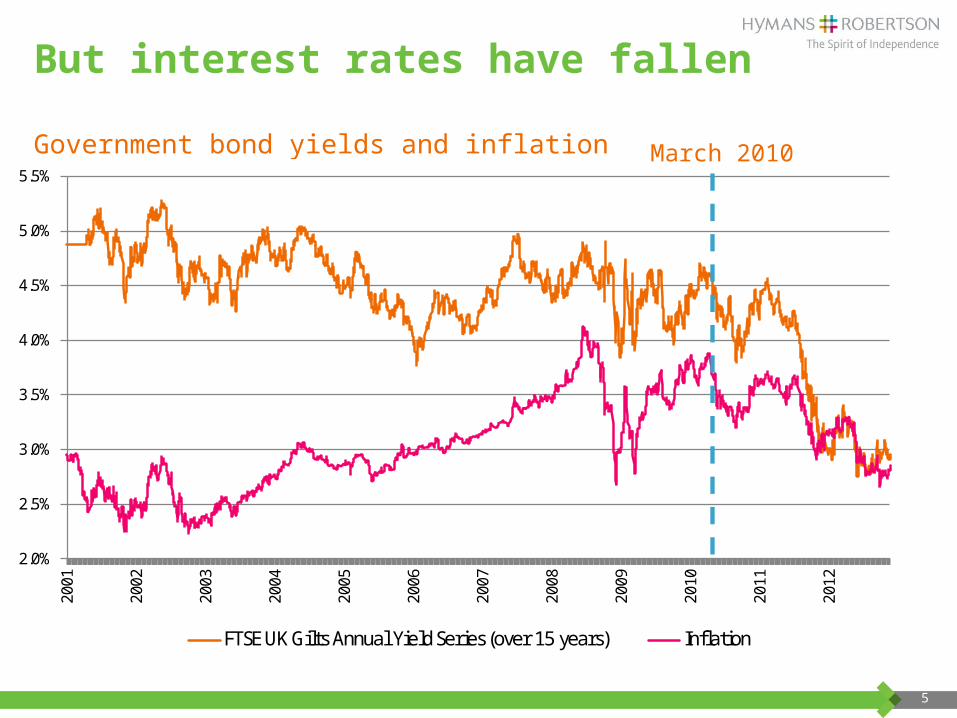

But interest rates have fallen

Government bond yields and inflation

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

FTSE UK Gilts Annual Yield Series (over 15 years) Inflation

March 2010

6

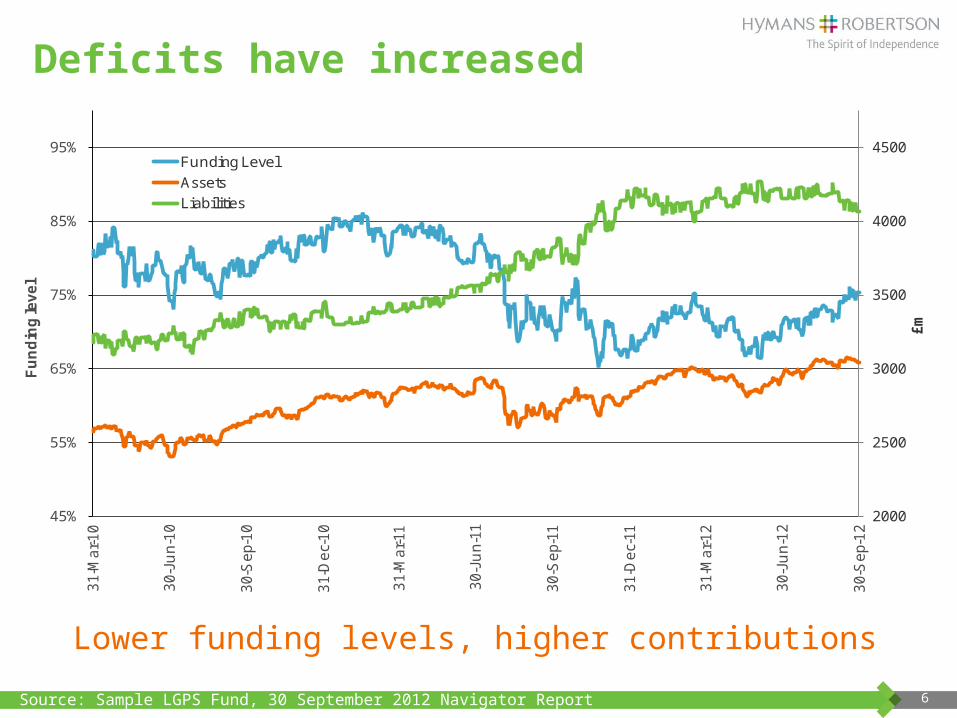

Deficits have increased

Lower funding levels, higher contributions

2000

2500

3000

3500

4000

4500

45%

55%

65%

75%

85%

95%

31-

Ma

r-1

0

30-

Jun-1

0

30-

Se

p-1

0

31-

De

c-1

0

31-

Ma

r-11

30-

Jun-1

1

30-

Se

p-11

31-

De

c-11

31-

Ma

r-1

2

30-

Jun-1

2

30-

Se

p-1

2

£m

Fu

nd

ing

lev

el

Funding Level

Assets

Liabilities

Source: Sample LGPS Fund, 30 September 2012 Navigator Report

7

Summary

Investment returns in line with long term assumption

But interest rates down and liability values up

Deficits have grown

Savings from new scheme modest – increase in contributions at 2013 less than would otherwise have been the case

Continuing upwards pressure on contributions

Contributions likely to stay at current levels or above for longer

8

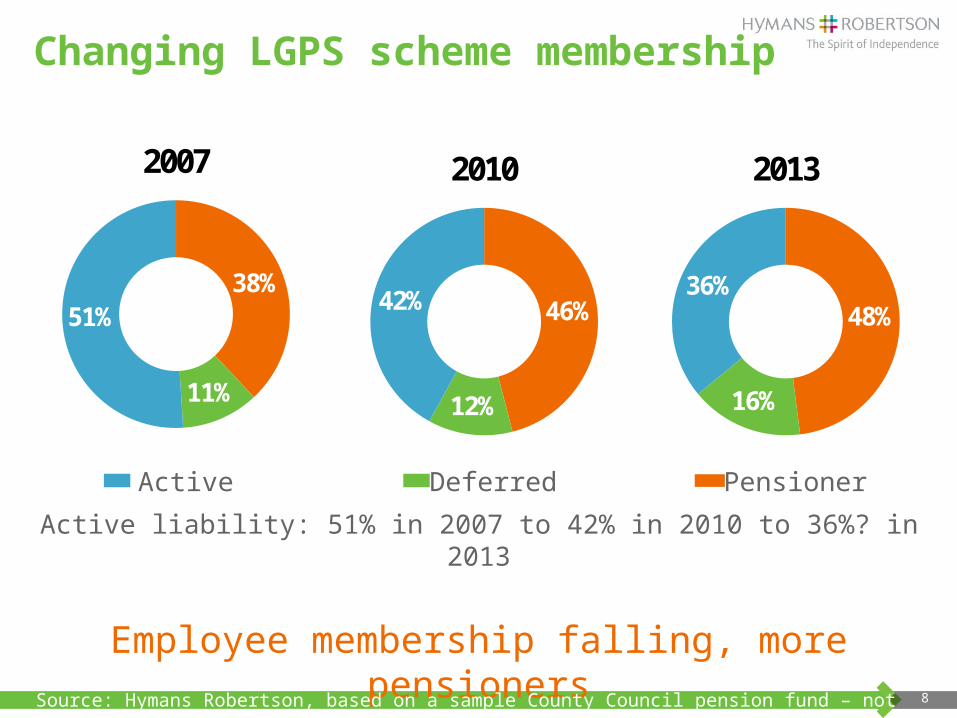

Changing LGPS scheme membership

Active liability: 51% in 2007 to 42% in 2010 to 36%? in 2013

Employee membership falling, more pensioners

Active Deferred Pensioner

38%

11%

51%

2007

46%

12%

42%

2010

48%

16%

36%

2013

Source: Hymans Robertson, based on a sample County Council pension fund – not Leicestershire.

9

Why is LGPS scheme membership changing?

Redundancies

Early retirements

Fewer new recruits

More outsourcing

Council payroll shrinking

e.g. transfers of staff to academies

Admission agreements often closed to new recruits

50/50 option in LGPS 2014

What impact will auto-enrolment have?

10

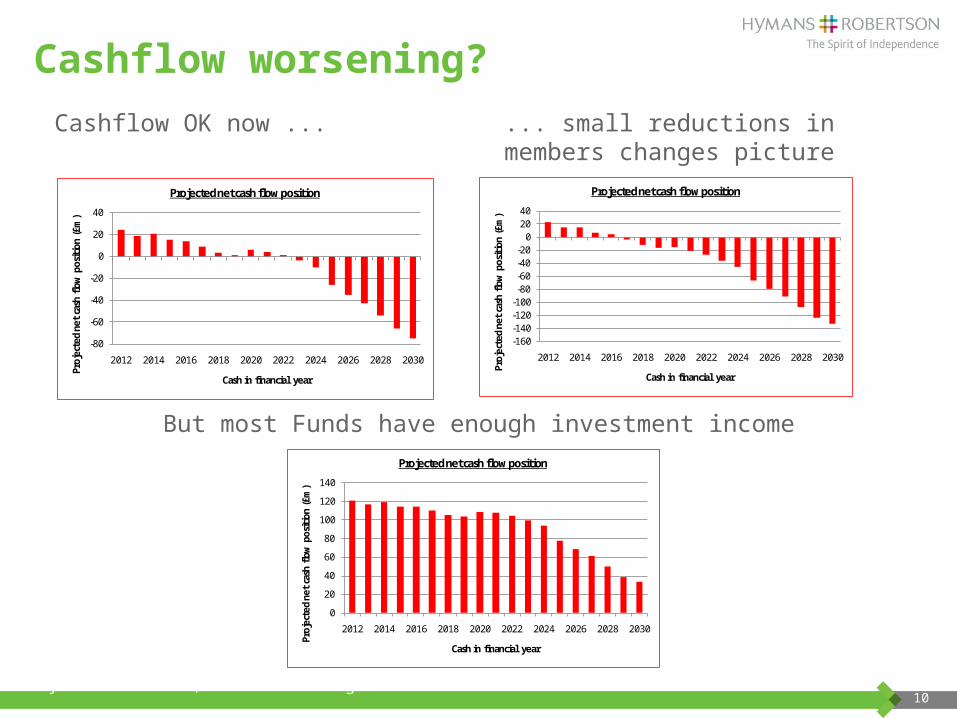

Cashflow worsening?

-80

-60

-40

-20

0

20

40

2012 2014 2016 2018 2020 2022 2024 2026 2028 2030

Proj

ecte

d ne

t ca

sh fl

ow p

ositi

on (

£m)

Cash in financial year

Projected net cash flow position

-160-140-120-100

-80-60-40-20

02040

2012 2014 2016 2018 2020 2022 2024 2026 2028 2030

Proj

ecte

d ne

t ca

sh fl

ow p

ositi

on (

£m)

Cash in financial year

Projected net cash flow position

0

20

40

60

80

100

120

140

2012 2014 2016 2018 2020 2022 2024 2026 2028 2030

Proj

ecte

d ne

t ca

sh fl

ow p

ositi

on (

£m)

Cash in financial year

Projected net cash flow position

Cashflow OK now ... ... small reductions inmembers changes picture

But most Funds have enough investment income

Source: Hymans Robertson, based on a large LGPS fund.

Reform: LGPS 2014

12

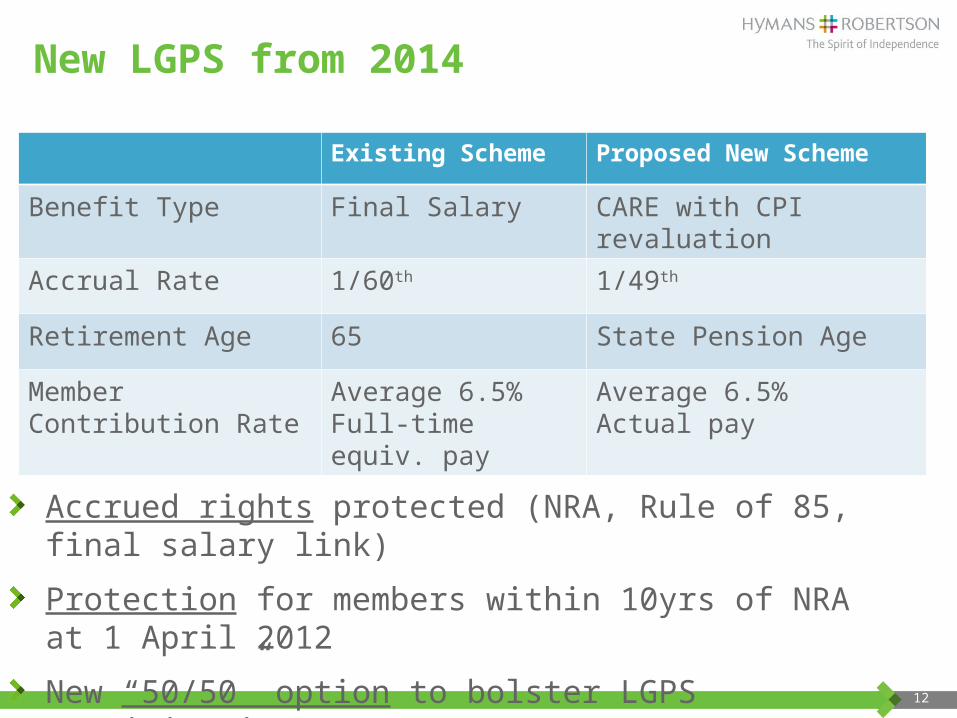

New LGPS from 2014

Existing Scheme Proposed New Scheme

Benefit Type Final Salary CARE with CPI revaluation

Accrual Rate 1/60th 1/49th

Retirement Age 65 State Pension Age

Member Contribution Rate

Average 6.5%Full-time equiv. pay

Average 6.5%Actual pay

Accrued rights protected (NRA, Rule of 85, final salary link)

Protection for members within 10yrs of NRA at 1 April 2012

New “50/50” option to bolster LGPS participation

13

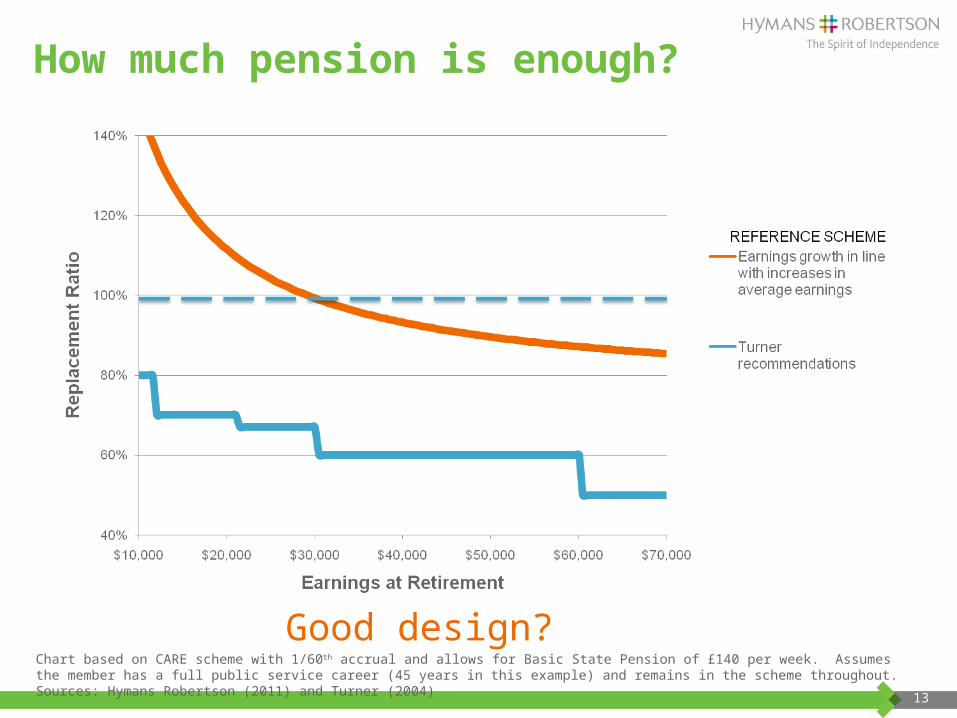

How much pension is enough?

Good design?Chart based on CARE scheme with 1/60th accrual and allows for Basic State Pension of £140 per week. Assumes the member has a full public service career (45 years in this example) and remains in the scheme throughout. Sources: Hymans Robertson (2011) and Turner (2004)

14

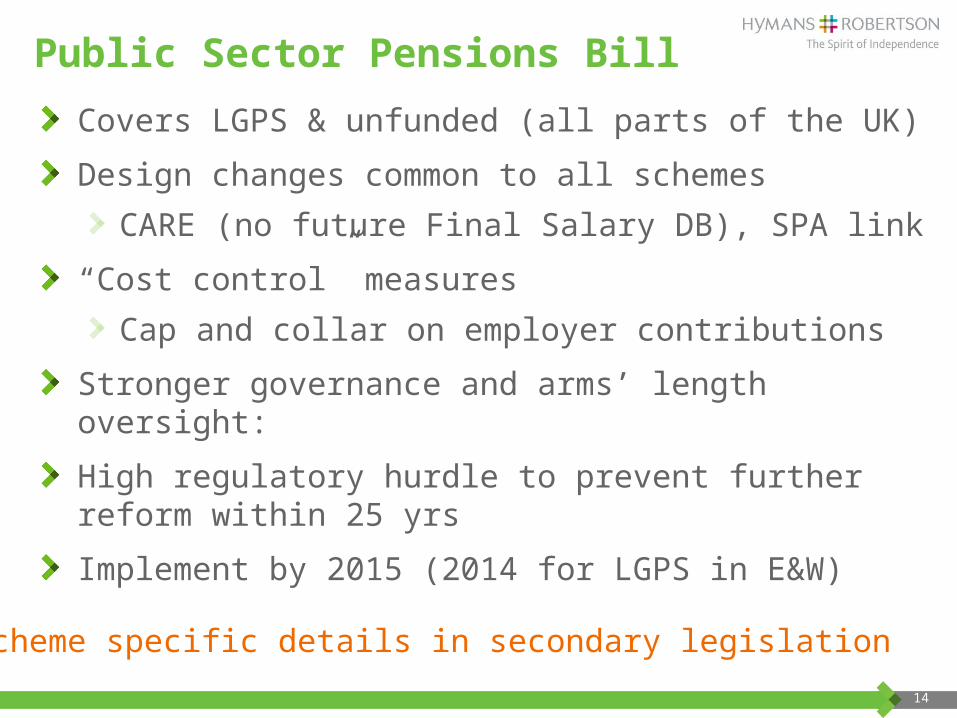

Public Sector Pensions Bill

Covers LGPS & unfunded (all parts of the UK)

Design changes common to all schemes

CARE (no future Final Salary DB), SPA link

“Cost control” measures

Cap and collar on employer contributions

Stronger governance and arms’ length oversight:

High regulatory hurdle to prevent further reform within 25 yrs

Implement by 2015 (2014 for LGPS in E&W)

Scheme specific details in secondary legislation

LGPS cost control

16

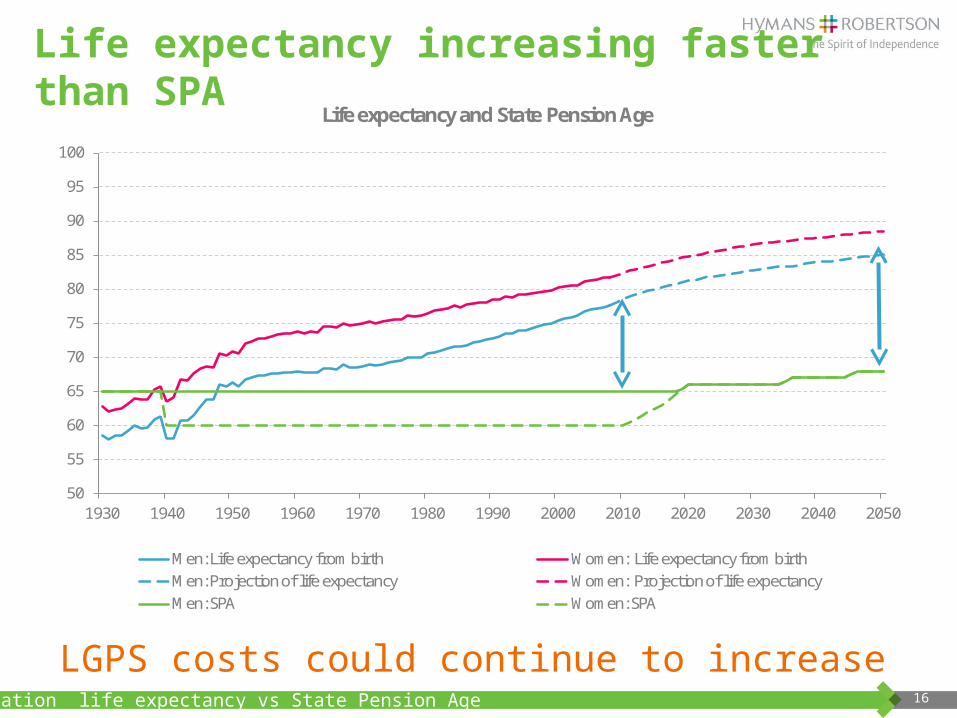

Life expectancy increasing faster than SPA

50

55

60

65

70

75

80

85

90

95

100

1930 1940 1950 1960 1970 1980 1990 2000 2010 2020 2030 2040 2050

Life expectancy and State Pension Age

Men: Life expectancy from birth Women: Life expectancy from birthMen: Projection of life expectancy Women: Projection of life expectancyMen: SPA Women: SPA

Population life expectancy vs State Pension Age

LGPS costs could continue to increase

17

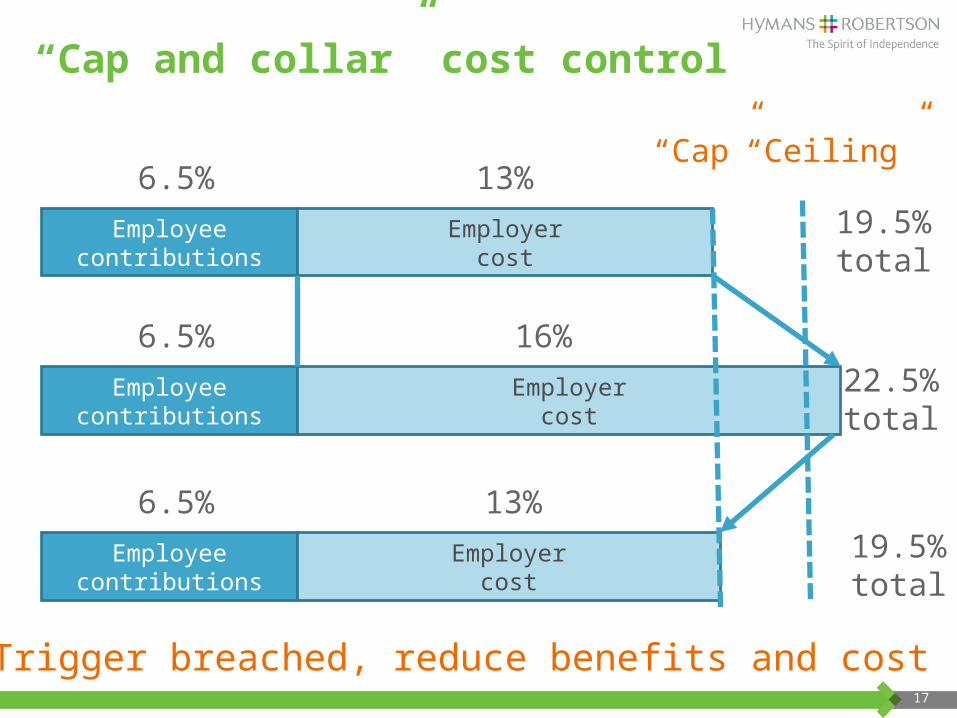

“Cap and collar” cost control

Employee contributions

Employercost

6.5% 13%19.5%total

Employee contributions

Employercost

6.5% 16%22.5%total

Trigger breached, reduce benefits and cost

Employee contributions

Employercost

6.5% 13%19.5%total

“Ceiling”“Cap”

18

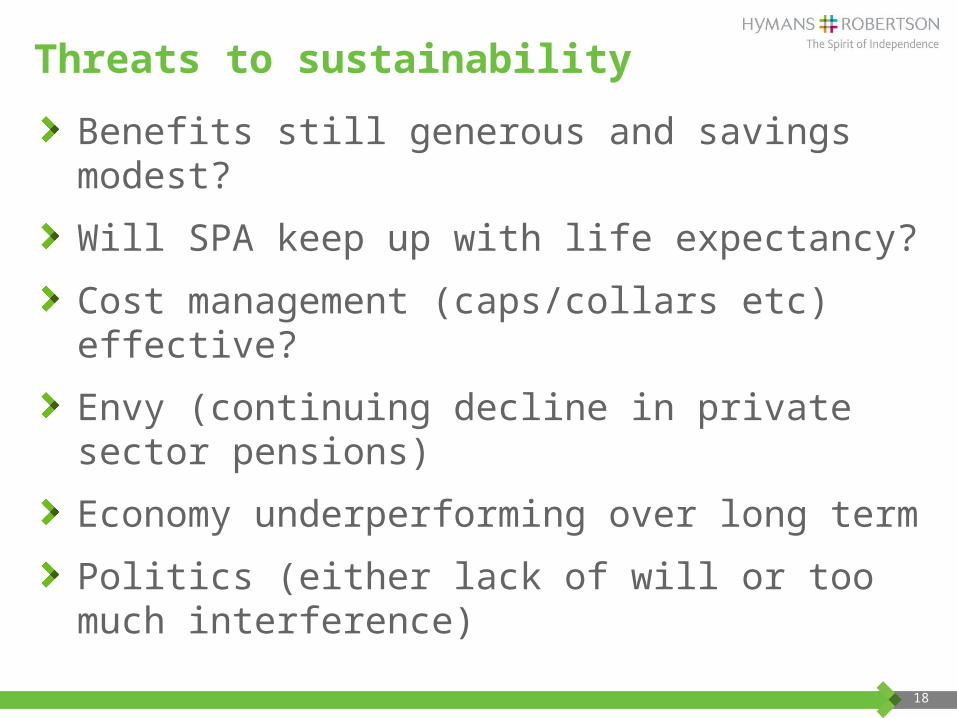

Threats to sustainability

Benefits still generous and savings modest?

Will SPA keep up with life expectancy?

Cost management (caps/collars etc) effective?

Envy (continuing decline in private sector pensions)

Economy underperforming over long term

Politics (either lack of will or too much interference)

Auto-enrolment

20

Workers confused?

“Thousands baffled over compulsory pensions”

Express, 10 December 2012

Need for good communication

21

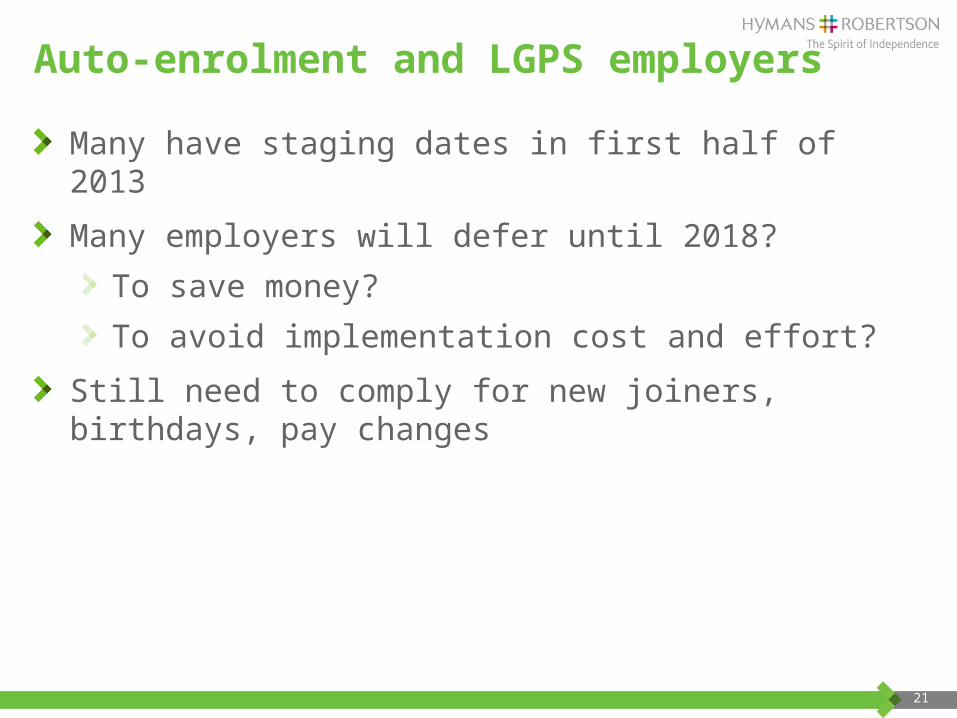

Auto-enrolment and LGPS employers

Many have staging dates in first half of 2013

Many employers will defer until 2018?

To save money?

To avoid implementation cost and effort?

Still need to comply for new joiners, birthdays, pay changes

Other topical issues

23

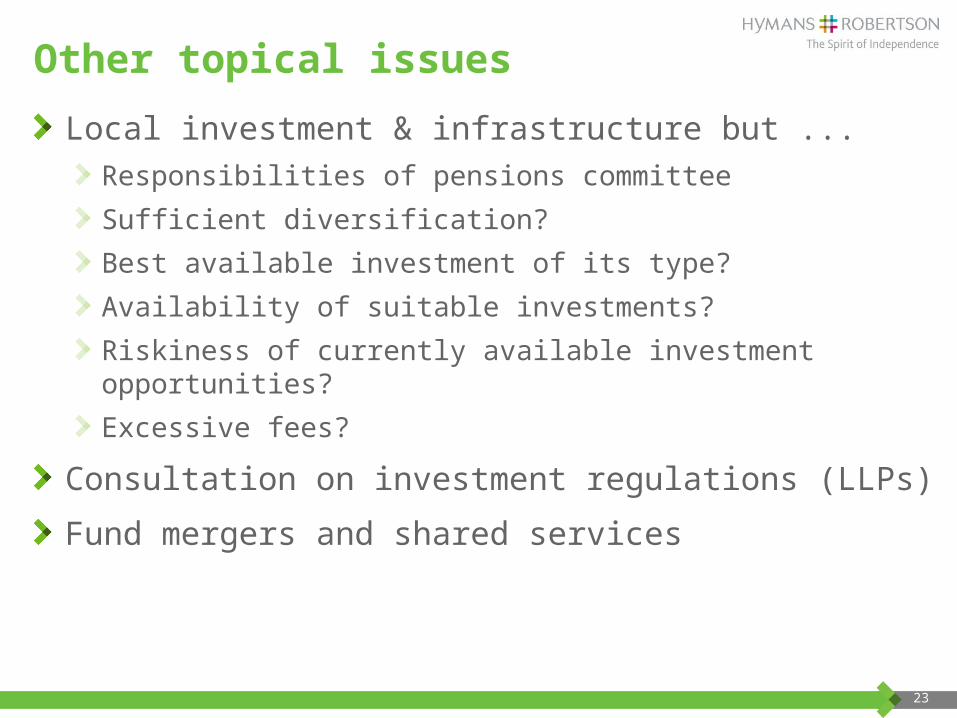

Other topical issues

Local investment & infrastructure but ...

Responsibilities of pensions committee

Sufficient diversification?

Best available investment of its type?

Availability of suitable investments?

Riskiness of currently available investment opportunities?

Excessive fees?

Consultation on investment regulations (LLPs)

Fund mergers and shared services

Any questions?

Thank you