Embed Size (px)

Citation preview

HY19 Result Presentation27 February 2019

G E N E S I S E N E R G Y L I M I T E D

Marc England – CHIEF EXECUTIVE OFFICERChris Jewell – CHIEF FINANCIAL OFFICER

AGENDA

Genesis Energy Limited 1H FY19 Result Presentation 2.

1 Key Highlights

2 Financial Performance

3 Operational and Strategic Update

4 Outlook

Key Highlights

,

Genesis Energy Limited 1H FY19 Result Presentation 4.

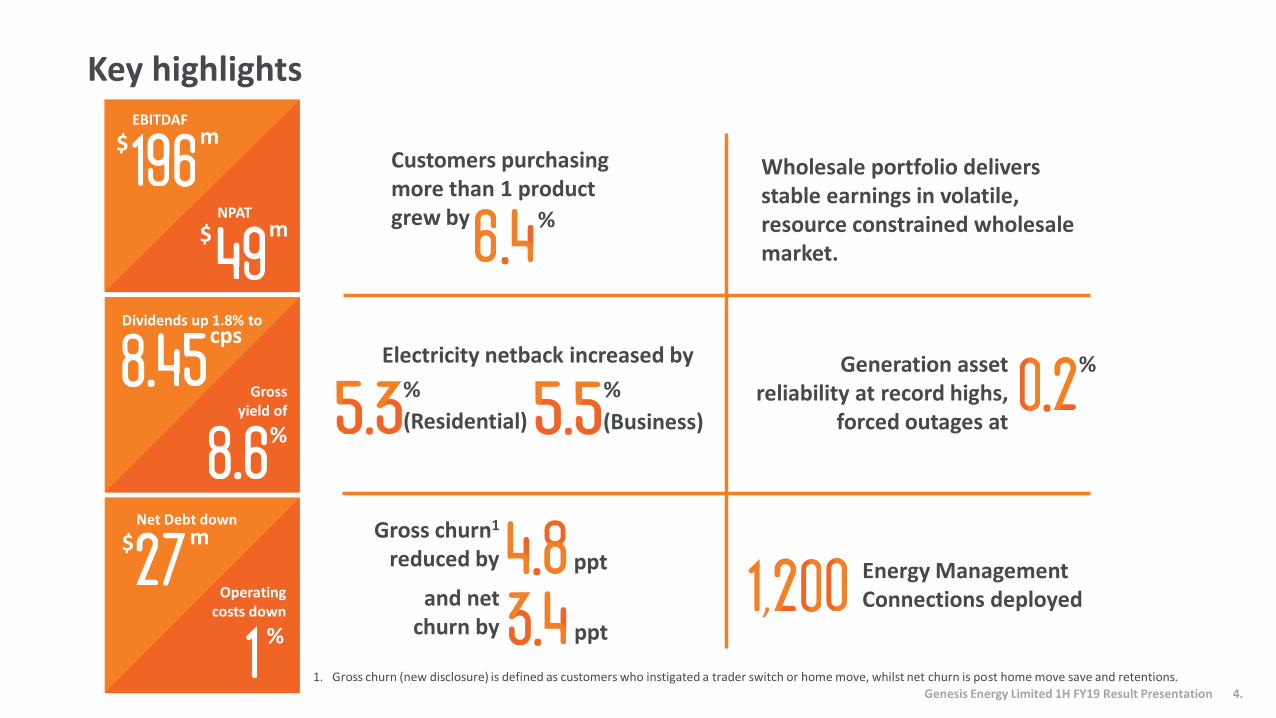

Key highlights

Genesis Energy Limited 1H FY19 Result Presentation 4.

Generation asset reliability at record highs,

forced outages at

Energy Management Connections deployed

NPAT

Net Debt down

Wholesale portfolio delivers stable earnings in volatile, resource constrained wholesale market.

EBITDAF

$ m

$ m

Gross yield of

Dividends up 1.8% tocps

.%

.

$ m

%

Operating costs down

.%

Gross churn1

reduced by

and net churn by

. ppt

. ppt

Electricity netback increased by

.%

(Business).%

(Residential)

1. Gross churn (new disclosure) is defined as customers who instigated a trader switch or home move, whilst net churn is post home move save and retentions.

Customers purchasing more than 1 product grew by

.%

Genesis Energy Limited 1H FY19 Result Presentation 4.

Financial Performance

198

2841.8

150

199

130

27

8.30cps

1,183

196

49 43.3

148

171

111

37

8.45cps

1,156

EBITDAF NPAT UnderlyingEarnings

ControllableOperating Costs

Operating Cashflow Free Cash Flow Capital Expenditure Interim Dividend Net Debt

$ MILLIONS HY18 HY19

321

— EBITDAF of $196m, underlying earnings up 4%, with operating costs down and net debt down $27m

FINANCIAL HIGHLIGHTS

HY19 financial summary1

- 2% + 78% + 4% - 1% + 37%- 15% + 2% - 2%

1. Comparable HY18 financials have been restated in line with note 1 of Genesis’ financial statements, accounting for the adoption of NZ IFRS 9 Financial Instruments and NZ IFRS 15 Revenue from Contracts with Customers. No other comparable periods have been adjusted.

2. Free cash flow represents EBITDAF less cash tax paid, net interest costs and stay in business capital expenditure.3. Net Debt is shown on a separate scale to other financial comparisons, and shows the change in Net Debt over the period from FY18 ($1,183m).

- 14%

Genesis Energy Limited 1H FY19 Result Presentation 6.

DIVIDEND (CPS) & PAYOUT HISTORY

8.00 8.20 8.20

8.30 8.45

87%

72%

87%

64%78%

-15%

5%

25%

45%

65%

85%

105%

125%

145%

5.50

6.00

6.50

7.00

7.50

8.00

8.50

9.00

HY15 HY16 HY17 HY18 HY19

Dividends (cps) % of Free Cash Flow

Dividends— Interim dividend of 8.45 cps declared (up 1.8%), with 80% imputation, representing a 8.6% gross yield1

Genesis Energy Limited 1H FY19 Result Presentation 7.

1. Gross yield based on the rolling 12 month dividend cps and closing share price of $2.61 as at 31 December 2018.2. Free cash flow represents EBITDAF less cash tax paid, net interest costs and stay in business capital expenditure.

• An Interim dividend of 8.45 cps, 80% imputed, will have a record date of 4 April 2019, payable to shareholders on 18 April 2019.

• Supplementary dividend of 1.1929 cps payment to non-resident shareholders.

• The Dividend Reinvestment Plan (DRP) continues to be offered at 2.5% discount, with an opt-in cut off date as at 4 April 2019. DRP pricing will be notified to shareholders on 10 April 2019.

• Pay-out ratio as a percentage of free cash flow2 is 78%.

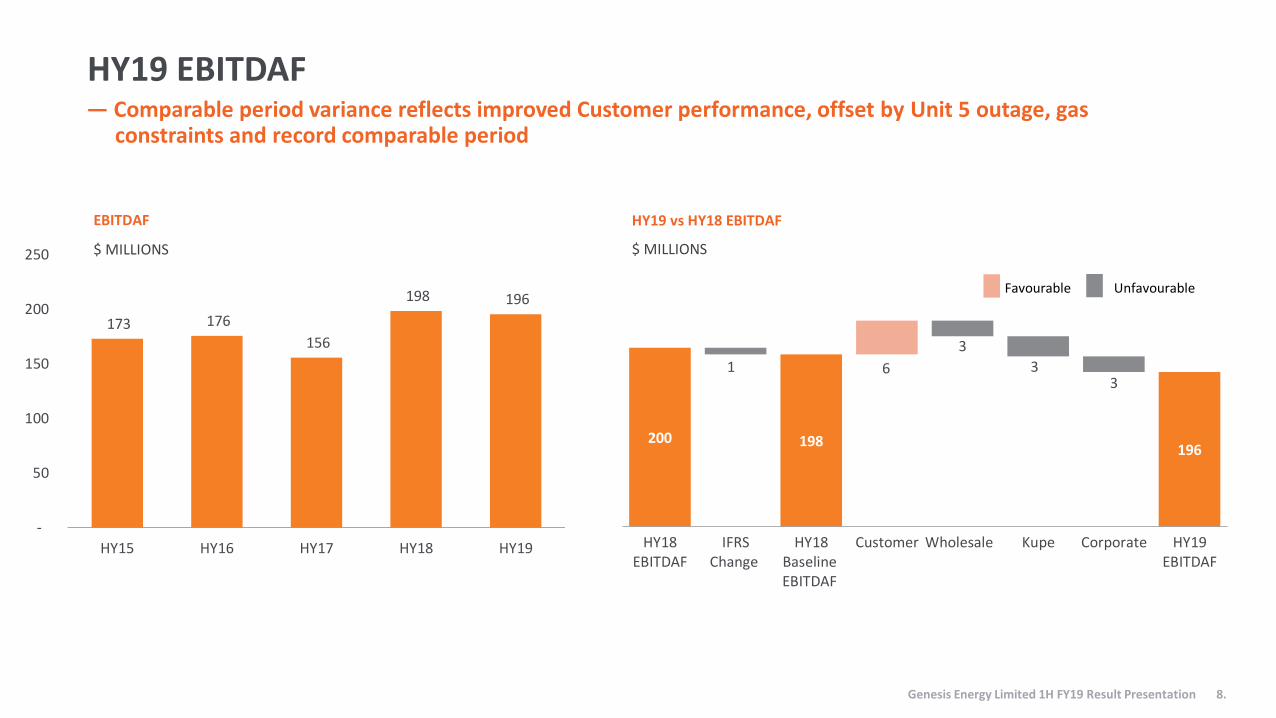

HY19 vs HY18 EBITDAF

$ MILLIONS

— Comparable period variance reflects improved Customer performance, offset by Unit 5 outage, gas constraints and record comparable period

HY19 EBITDAF

Genesis Energy Limited 1H FY19 Result Presentation 8.

200 198196

1

3

33

6

HY18EBITDAF

IFRSChange

HY18BaselineEBITDAF

Customer Wholesale Kupe Corporate HY19EBITDAF

Favourable Unfavourable

173 176

156

198 196

-

50

100

150

200

250

HY15 HY16 HY17 HY18 HY19

EBITDAF

$ MILLIONS

57 56

62

11

1

12

3

2

HY18EBITDAF

IFRS Change HY18BaselineEBITDAF

ResidentialGross

Margin

ResidentialOpex

Bad Debts B2B Growth LPG Growth Other HY19EBITDAF

Segment EBITDAF

KUPE EBITDAF HY18 TO HY19

CUSTOMER EBITDAF HY18 TO HY19

WHOLESALE EBITDAF HY18 TO HY19

Favourable Unfavourable

2

Genesis Energy Limited 1H FY19 Result Presentation 9.

106 104

74

9

HY18 EBITDAF Trading Result Unit 5 Outage Market Making HY19 EBITDAF

• Customer improved performance in LPG, Business margins and reduced operating expenses and bad debts.

• Wholesale performance stable but moderated by swaption calls, gas constraints and an extended Unit 5 outage. GWAP up $50/MWh to $146/MWh however total generation volume down 467 GWh.

• Kupe benefited from stronger fuel prices, however result was offset by reduced production.

• Corporate costs increased by $2.5m due to lower capitalisation of technology teams.

5653

6 22

7

HY18 EBITDAF Higher Fuel Prices(Net of Hedges)

Lower Production Oil Yield Decline Oil Sales Timing HY19 EBITDAF

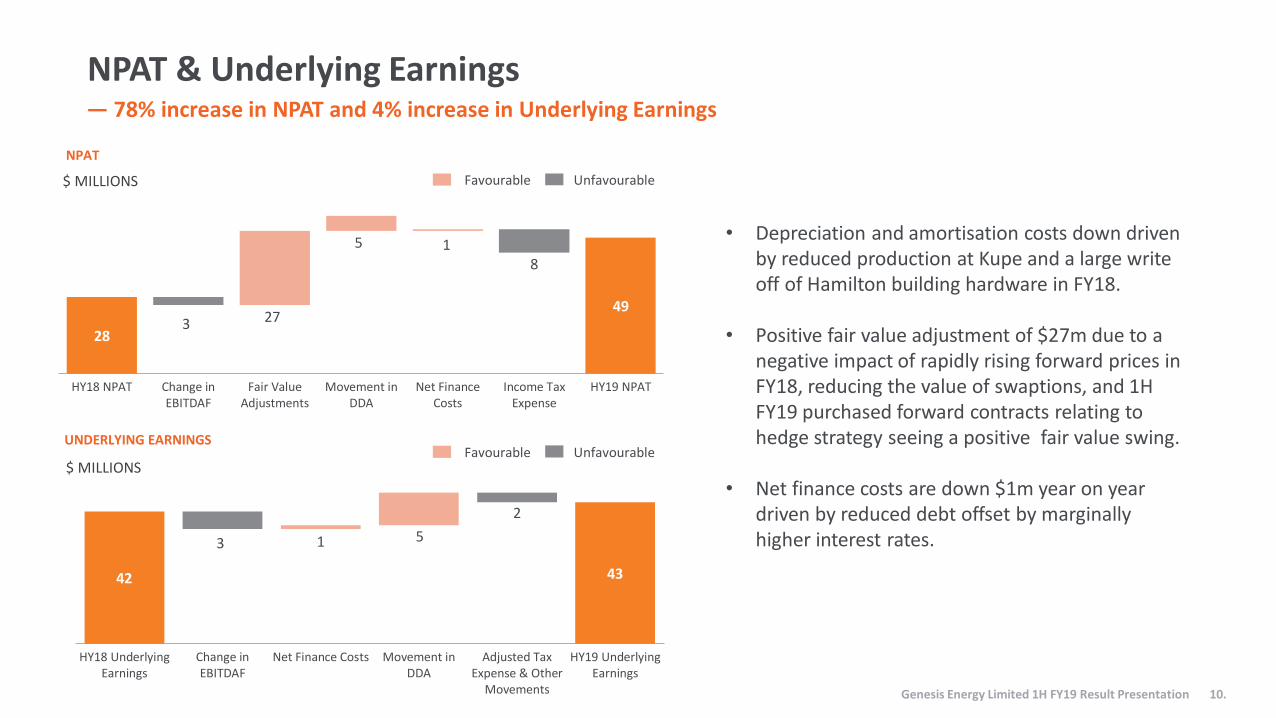

28

493

8

27

5 1

HY18 NPAT Change inEBITDAF

Fair ValueAdjustments

Movement inDDA

Net FinanceCosts

Income TaxExpense

HY19 NPAT

UNDERLYING EARNINGS

NPAT & Underlying Earnings— 78% increase in NPAT and 4% increase in Underlying Earnings

Favourable Unfavourable$ MILLIONS

Genesis Energy Limited 1H FY19 Result Presentation 10.

42 43

3

2

1 5

HY18 UnderlyingEarnings

Change inEBITDAF

Net Finance Costs Movement inDDA

Adjusted TaxExpense & Other

Movements

HY19 UnderlyingEarnings

NPAT

$ MILLIONS Favourable Unfavourable

• Depreciation and amortisation costs down driven by reduced production at Kupe and a large write off of Hamilton building hardware in FY18.

• Positive fair value adjustment of $27m due to a negative impact of rapidly rising forward prices in FY18, reducing the value of swaptions, and 1H FY19 purchased forward contracts relating to hedge strategy seeing a positive fair value swing.

• Net finance costs are down $1m year on year driven by reduced debt offset by marginally higher interest rates.

150 148

23

1

2

HY18 OperatingExpenses

LPG Expansion Bad Debts Marketing &Communication

LowerCapitalisation of

Technology Costs

HY19 OperatingExpenses

142 144 138 150 148

HY15 HY16 HY17 HY18 HY19

$ MILLIONS

CONTROLLABLE OPERATING EXPENSES1

CONTROLLABLE OPERATING EXPENSE BRIDGE

Controllable operating expenses— Controllable operating expenses down 1% on pcp

Favourable Unfavourable$ MILLIONS

Genesis Energy Limited 1H FY19 Result Presentation 11.

2

1. Controllable operating expenses refers to employee benefits plus other operating expenses.2. Represents costs associated with LPG growth offset by synergies from cost to deliver savings

• Costs have stabilised at HY18 levels following a period of investment.

• Increased focus on bad debts is improving results.

• Improved loyalty and brand performance enabling reduced marketing costs.

• Technology teams have spent less time this half year on capital projects.

Capital expenditure— Total capital expenditure at HY19 was $37m, FY19 guidance being up to $85m

CAPITAL EXPENDITURE1

• Stay in business capex (SIB) was $30m, significant projects included:

₋ Huntly U5 planned maintenance, Kupe LPG plant maintenance, station crane upgrades, Tuaigenerator refurbishments, Tokaanu auxiliary generator upgrade, Rangipo fire protection upgrade.

• Other capex includes ($7m):₋ LPG depot expansion and growth projects,

development of Energy Management products, Huntly U5 gas turbine performance upgrades and Kupe Phase 2 Development feasibility study.

1. Capital expenditure excludes M&A activities.

FY15 FY16 FY17 FY18 FY19 YTD

Wholesale Customer LPG Operations

Kupe Technology & Digital Corporate

$ MILLIONS

4440

47

80

37

Genesis Energy Limited 1H FY19 Result Presentation 12.

NET DEBT AND NET DEBT/EBITDAF RATIO1

905833

1,212 1,183 1,156

2.5 2.6

3.3

3.0 2.9

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

0

200

400

600

800

1000

1200

FY15 FY16 FY17 FY18 HY19

Net debt Net debt/EBITDAF Target debt ratio band (2.4 to 3.0)

Capital structure

— Net debt reduced by $27 million, credit metrics improving and within target band

• S&P reaffirmed BBB+ credit rating in January 2019

• $240m of Capital Bonds maturing in FY 2049 were issued on 16 July 2018 at a coupon rate of 4.65%. $200m of existing Capital Bonds with a coupon rate of 6.19% were redeemed at the same time.

• Dividend reinvestment plan (DRP) in place since the FY18 interim dividend with 29% of holders currently participating, representing 22% of all shares, and $38 million raised to date.

• Average debt tenor has increased to 12.3 years, from 11.4 years. Bank funding facilities have been renegotiated to achieve a longer tenor at a reduced overall cost.

1. Standard and Poor’s make a number of adjustments to Net Debt and EBITDAF for the purpose of calculating credit metrics. The most significant of these is the 50% equity treatment attributed to the Capital Bonds. HY19 calculation is based on actual debt at 31 December 2018 and the mid-point of the EBITDAF guidance range for FY19.

Genesis Energy Limited 1H FY19 Result Presentation 13.

Operational and Strategic Update

350,000

355,000

360,000

365,000

370,000

375,000

380,000

96%

98%

100%

102%

104%

106%

108%

Jan

-18

Feb

-18

Mar

-18

Ap

r-18

May

-18

Jun

-18

Jul-

18

Au

g-18

Sep

-18

Oct

-18

No

v-1

8

Dec

-18

Customers CLV Index (LHS)

8%

35%

0%

10%

20%

30%

40%

Jan

-18

Feb

-18

Mar

-18

Ap

r-18

May

-18

Jun

-18

Jul-

18

Au

g-18

Sep

-18

Oct

-18

No

v-1

8

Dec

-18

NPS - Genesis 3 Month Rolling Promoter - Genesis 3 Month Rolling

Customer brand, loyalty & engagement— Focus on multi-fuels and loyalty continues to drive down churn

RESIDENTIAL CUSTOMER GROSS2 CHURN DOWN 4.8 ppt, NET CHURN DOWN 3.4 ppt (HY AVERGAES)BRAND NPS UP 6 ppt AND PROMOTER SCORE UP 3 ppt IN 12 MONTHS

+6 ppt

+3 ppt

Genesis Energy Limited 1H FY19 Result Presentation 15.

DUAL FUEL CUSTOMERS1 UP 6.4% GROWTH AND CHURN DOWN TO 8.1% RESIDENTIAL CUSTOMER NUMBERS DOWN 1%, CUSTOMER LIFE VALUE INDEX3 (CLV) UP 6%

0%

2%

4%

6%

8%

10%

12%

94,000

96,000

98,000

100,000

102,000

Jan

-18

Feb

-18

Mar

-18

Ap

r-18

May

-18

Jun

-18

Jul-

18

Au

g-18

Sep

-18

Oct

-18

No

v-1

8

Dec

-18

Customers > 1 Product Dual Fuel Churn (RHS)

YoY GE Multi-fuel customers up 6.4%

CLV up 6%

1. Genesis residential customers, excluding EOL, with churn based on a 3 month rolling average.2. Gross churn (new disclosure) is defined as customers who instigated a trader switch or home move, whilst net churn is post home move save and retentions.3. Customer Lifetime Value is the margin for each customer, discounted over its expected tenure.

20.5%17.0% 17.1%

1.00

0.87 0.86

30.0%

50.0%

70.0%

90.0%

0.0%

10.0%

20.0%

30.0%

1H FY18 2H FY18 1H FY19

Net Churn Gross Churn Index

0%

20%

40%

60%

80%

Abandonment Grade of Service

HY18 HY19

1

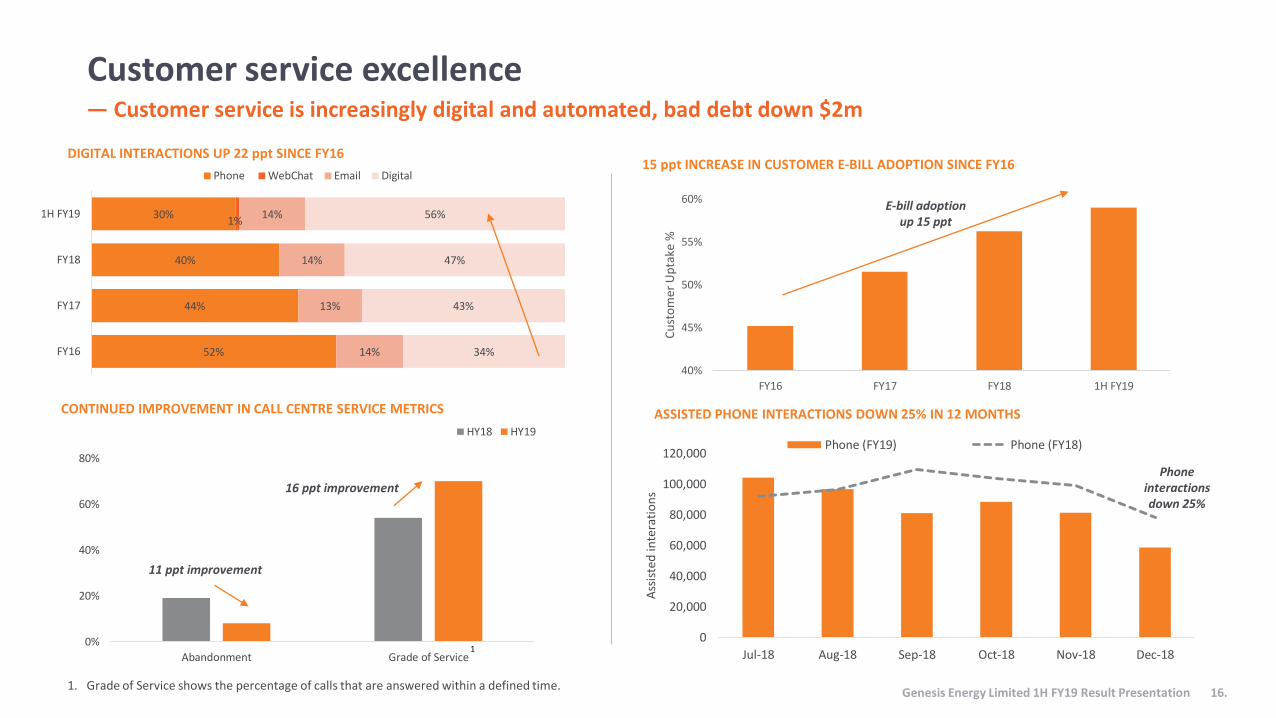

Customer service excellence— Customer service is increasingly digital and automated, bad debt down $2m

DIGITAL INTERACTIONS UP 22 ppt SINCE FY1615 ppt INCREASE IN CUSTOMER E-BILL ADOPTION SINCE FY16

Genesis Energy Limited 1H FY19 Result Presentation 16.

40%

45%

50%

55%

60%

FY16 FY17 FY18 1H FY19

Cu

sto

mer

Up

take

%

52%

44%

40%

30%1%

14%

13%

14%

14%

34%

43%

47%

56%

FY16

FY17

FY18

1H FY19

Phone WebChat Email Digital

CONTINUED IMPROVEMENT IN CALL CENTRE SERVICE METRICS

11 ppt improvement

16 ppt improvement

ASSISTED PHONE INTERACTIONS DOWN 25% IN 12 MONTHS

E-bill adoption up 15 ppt

1. Grade of Service shows the percentage of calls that are answered within a defined time.

0

20,000

40,000

60,000

80,000

100,000

120,000

Jul-18 Aug-18 Sep-18 Oct-18 Nov-18 Dec-18A

ssis

ted

inte

rati

on

s

Phone (FY19) Phone (FY18)

Phone interactions down 25%

$110

$115

$50

$70

$90

$110

$130

1,450

1,500

1,550

1,600

1,650

1,700

HY18 HY19

Sale

s V

olu

me

(GW

h)

Sales Volume Netback

$10.3 $10.3

$8.0

$9.0

$10.0

$11.0

$12.0

1,500

1,550

1,600

1,650

1,700

HY18 HY19

Sale

s V

olu

me

(GJ)

Sales Volume Netback

$762$745

$600

$650

$700

$750

$800

$850

7,250

7,500

7,750

8,000

8,250

8,500

8,750

HY18 HY19

Sale

s V

olu

me

(t)

Sales Volume Netback

$740

$861

$350

$550

$750

10,500

10,600

10,700

10,800

10,900

11,000

HY18 HY19

Sale

s V

olu

me

(t)

Sales Volume Netback

$87

$92

$50

$70

$90

$110

1,300

1,350

1,400

1,450

1,500

1,550

HY18 HY19

Sale

s V

olu

me

(GW

h)

Sales Volume Netback

$7.9 $7.8

$6.0

$7.0

$8.0

$9.0

$10.0

2,250

2,450

2,650

2,850

3,050

HY18 HY19

Sale

s V

olu

em (G

J)

Sales Volume Netback

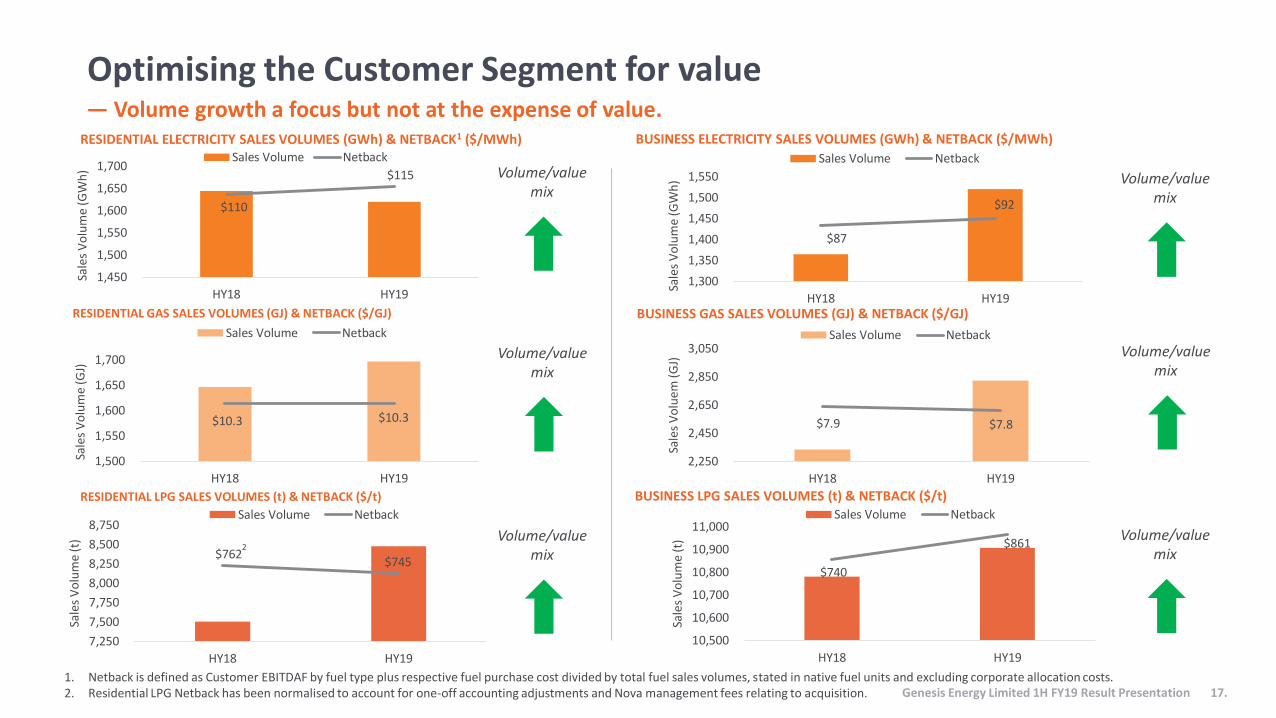

Optimising the Customer Segment for value— Volume growth a focus but not at the expense of value.

BUSINESS GAS SALES VOLUMES (GJ) & NETBACK ($/GJ)RESIDENTIAL GAS SALES VOLUMES (GJ) & NETBACK ($/GJ)

BUSINESS ELECTRICITY SALES VOLUMES (GWh) & NETBACK ($/MWh)RESIDENTIAL ELECTRICITY SALES VOLUMES (GWh) & NETBACK1 ($/MWh)

BUSINESS LPG SALES VOLUMES (t) & NETBACK ($/t)RESIDENTIAL LPG SALES VOLUMES (t) & NETBACK ($/t)

Volume/value mix

Volume/value mix

Volume/value mix

Volume/value mix

Volume/value mix

Volume/value mix

2

1. Netback is defined as Customer EBITDAF by fuel type plus respective fuel purchase cost divided by total fuel sales volumes, stated in native fuel units and excluding corporate allocation costs.2. Residential LPG Netback has been normalised to account for one-off accounting adjustments and Nova management fees relating to acquisition. Genesis Energy Limited 1H FY19 Result Presentation 17.

0.5

0.7

0.9

1.1

1.3

1.5

Jan

-18

Feb

-18

Mar

-18

Ap

r-18

May

-18

Jun

-18

Jul-

18

Au

g-18

Sep

-18

Oct

-18

No

v-1

8

Dec

-18

Sto

rage

as

% o

f A

vera

ge

National Storage Band Storage as % of Average

$0

$100

$200

$300

$400

$500

$600

Jul-18 Aug-18 Sep-18 Oct-18 Nov-18 Dec-18

$/M

Wh

Benmore (BEN2201) Otahuhu (OTA2201)

Gas shortages

Rankines crucial for national security of supply — Wholesale result moderated by gas shortages, planned 50-day Unit 5 outage, low storage and swaption calls

Genesis Energy Limited 1H FY19 Result Presentation 18.

SHORTAGE OF BOTH GAS AND WATER DRIVES WHOLESALE PRICE VOLATILITY, GWAP1 OF $146 MWH UP 52%

HVDC outage

A TIGHTER WHOLESALE MARKET RESPONDS QUICKLY TO HYDRO SHORTAGES

UNEXPECTED GAS SHORTAGES CREATE FURTHER ELECTRICITY SUPPLY SHORTAGES TOTAL GENERATION DOWN 12% TO 3,403 GWH HOWEVER RANKINES PERFORM WELL IN THEIR ROLE AS BACKUP TO THE MARKET FOR HYDRO AND GAS SHORTAGES

0

50

100

150

200

250

Jul-18 Aug-18 Sep-18 Oct-18 Nov-18 Dec-18G

Wh

Genesis Customers Backup Unit 5 (Pohokura & Planned Outage)

Backup Swaption Partners Backup Other Retailers & Spot Customers

Low storage

Low storage

U5 outage

1. GWAP is the average price received for generation, $/MWh.

0

50

100

150

200

250

Jan

-18

Feb

-18

Mar

-18

Ap

r-18

May

-18

Jun

-18

Jul-

18

Au

g-18

Sep

-18

Oct

-18

No

v-1

8

Dec

-18

TJ/D

ay

Pohokura Gas Deliveries Methanex DemandGas shortage,

higher gas demandGas shortage, lower gas demand

High storage

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

Jul-18 Aug-18 Sep-18 Oct-18 Nov-18 Dec-18

Pro

du

ctio

n (G

enes

is S

har

e, P

Je)

Gas Oil LPG

0.2% 0.2% 0.3% 0.1% 0.1% 0.3%0%

5%

10%

15%

20%

0%

20%

40%

60%

80%

100%

Jul-18 Aug-18 Sep-18 Oct-18 Nov-18 Dec-18

Forc

ed O

uta

ge F

acto

r (F

OF)

%

Equ

ipm

ent

Ava

ilab

ility

Fac

tor

(EA

F) %

Monthly EAF Monthly FOF

CONTINUED HIGH PLANT RELIABILITY – UNIT 5 MAINTENANCE DELIVERED ON TIME AND BELOW BUDGET

Plant reliability key in volatile market— However market making costs increase sharply due to ASX volatility

KUPE PRODUCTION DOWN DUE TO PLANNED MAINTENANCE (GENESIS SHARE, PJe)

Genesis Energy Limited 1H FY19 Result Presentation 19.

0

50

100

150

200

250

May

-16

Jul-

16

Sep

-16

No

v-1

6

Jan

-17

Mar

-17

May

-17

Jul-

17

Sep

-17

No

v-1

7

Jan

-18

Mar

-18

May

-18

Jul-

18

Sep

-18

No

v-1

8

MW

Quarterly ASX Contracts Monthly ASX Contracts Over-The-Counter Contracts

UNIT 5 OUTAGE COVERED THROUGH DERIVATIVE MARKET LIQUIDITY (NOVEMBER HEDGES ONLY)

VOLUNTARY MARKET MAKER COSTS INCREASE WITH VOLATILITY

Planned Maintenance at Kupe (coincided with Unit 5 Outage)

-$3.5

-$2.5

-$1.5

-$0.5

Jul-18 Aug-18 Sep-18 Oct-18 Nov-18 Dec-18

Mar

ket

Mak

ing

Loss

es Mill

ion

s

Unit 5 Outage

• Volatility results in market making losses, driven by financial market participants.

• ASX is a vital tool for portfolio risk management (see below).• Market making is voluntary and Genesis supports a review of

the current arrangements to ensure fair cost structures exists.

Enabling a more sustainable future

Caring for our environment

Building strong communities

Powering New Zealand

Genesis signed up to EV 100, a global businessinitiative driving the switch to EVs. December 2018

We’re driving electric -

now part of Genesis fleet

Whio population boosted

ducks released January 2019

EVs

November 2018

Ohope Beach School joins School-gen solar programmeNovember 2018

Emirates Team New Zealand & School-gen partner to bring STEM to schoolsDecember 2018

Genesis wins YWCA Equal Pay AwardNovember 2018

February 2019

School-gen Trust launches, providing

of STEM funding for schools

$,

November 2018

Employee volunteering revitalised

Hours already given back to communities

+

Waverley Wind Farm partnership announcedOctober 2018

MOU signed with DETA Consulting for energy management services to businessesOctober 2018

Genesis joins the NZ Hydrogen Association, supporting development of low emission fuel sourcesFebruary 2018

Bottles gas for Business launched –usage sensors minimize wasteOctober 2018

Genesis Energy Limited 1H FY19 Result Presentation 20.

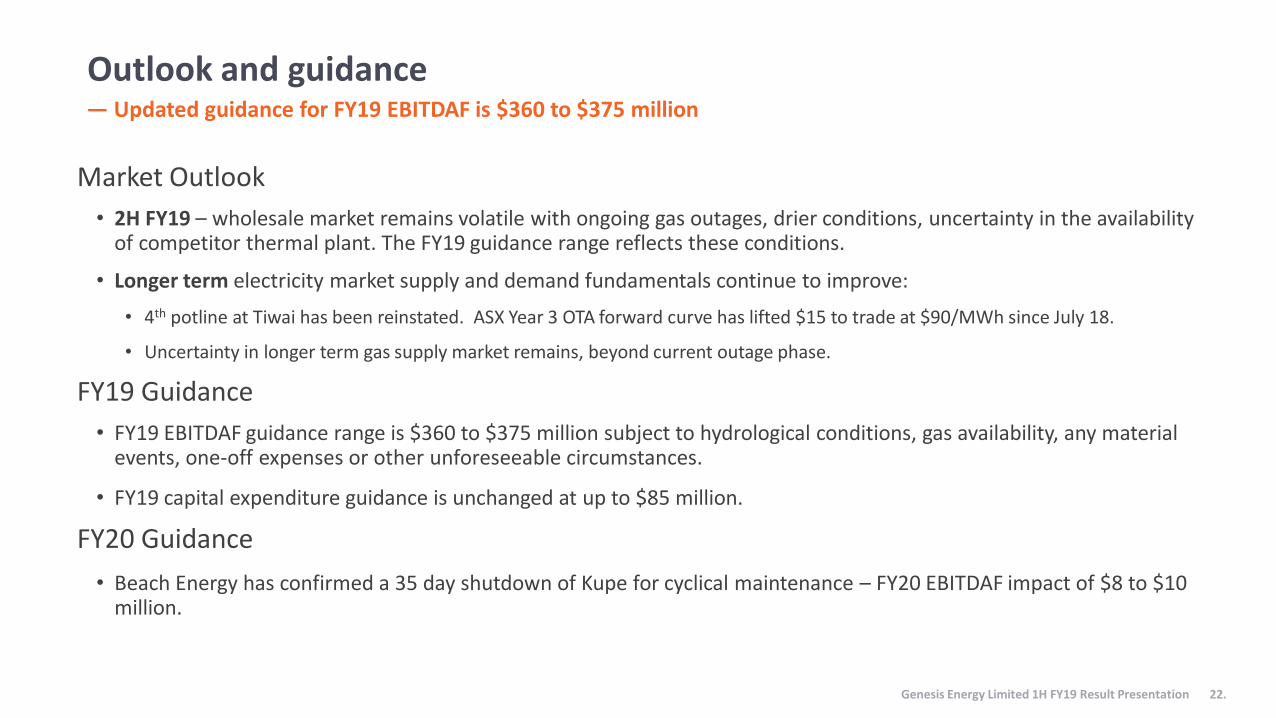

Outlook and guidance— Updated guidance for FY19 EBITDAF is $360 to $375 million

Market Outlook

• 2H FY19 – wholesale market remains volatile with ongoing gas outages, drier conditions, uncertainty in the availability of competitor thermal plant. The FY19 guidance range reflects these conditions.

• Longer term electricity market supply and demand fundamentals continue to improve:

• 4th potline at Tiwai has been reinstated. ASX Year 3 OTA forward curve has lifted $15 to trade at $90/MWh since July 18.

• Uncertainty in longer term gas supply market remains, beyond current outage phase.

FY19 Guidance

• FY19 EBITDAF guidance range is $360 to $375 million subject to hydrological conditions, gas availability, any material events, one-off expenses or other unforeseeable circumstances.

• FY19 capital expenditure guidance is unchanged at up to $85 million.

FY20 Guidance

• Beach Energy has confirmed a 35 day shutdown of Kupe for cyclical maintenance – FY20 EBITDAF impact of $8 to $10 million.

Genesis Energy Limited 1H FY19 Result Presentation 22.

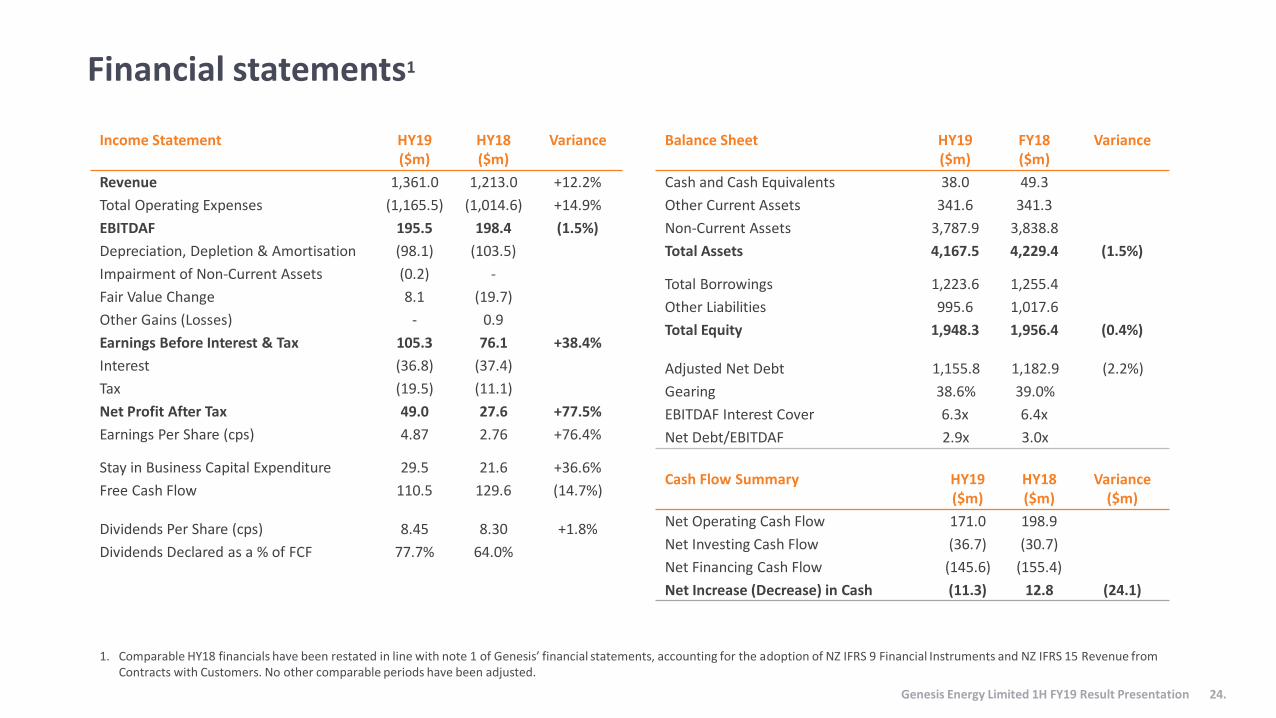

Balance Sheet HY19($m)

FY18($m)

Variance

Cash and Cash Equivalents 38.0 49.3

Other Current Assets 341.6 341.3

Non-Current Assets 3,787.9 3,838.8

Total Assets 4,167.5 4,229.4 (1.5%)

Total Borrowings 1,223.6 1,255.4

Other Liabilities 995.6 1,017.6

Total Equity 1,948.3 1,956.4 (0.4%)

Adjusted Net Debt 1,155.8 1,182.9 (2.2%)

Gearing 38.6% 39.0%

EBITDAF Interest Cover 6.3x 6.4x

Net Debt/EBITDAF 2.9x 3.0x

Income Statement HY19($m)

HY18($m)

Variance

Revenue 1,361.0 1,213.0 +12.2%

Total Operating Expenses (1,165.5) (1,014.6) +14.9%

EBITDAF 195.5 198.4 (1.5%)

Depreciation, Depletion & Amortisation (98.1) (103.5)

Impairment of Non-Current Assets (0.2) -

Fair Value Change 8.1 (19.7)

Other Gains (Losses) - 0.9

Earnings Before Interest & Tax 105.3 76.1 +38.4%

Interest (36.8) (37.4)

Tax (19.5) (11.1)

Net Profit After Tax 49.0 27.6 +77.5%

Earnings Per Share (cps) 4.87 2.76 +76.4%

Stay in Business Capital Expenditure 29.5 21.6 +36.6%

Free Cash Flow 110.5 129.6 (14.7%)

Dividends Per Share (cps) 8.45 8.30 +1.8%

Dividends Declared as a % of FCF 77.7% 64.0%

Cash Flow Summary HY19($m)

HY18($m)

Variance($m)

Net Operating Cash Flow 171.0 198.9

Net Investing Cash Flow (36.7) (30.7)

Net Financing Cash Flow (145.6) (155.4)

Net Increase (Decrease) in Cash (11.3) 12.8 (24.1)

Financial statements1

Genesis Energy Limited 1H FY19 Result Presentation 24.

1. Comparable HY18 financials have been restated in line with note 1 of Genesis’ financial statements, accounting for the adoption of NZ IFRS 9 Financial Instruments and NZ IFRS 15 Revenue from Contracts with Customers. No other comparable periods have been adjusted.

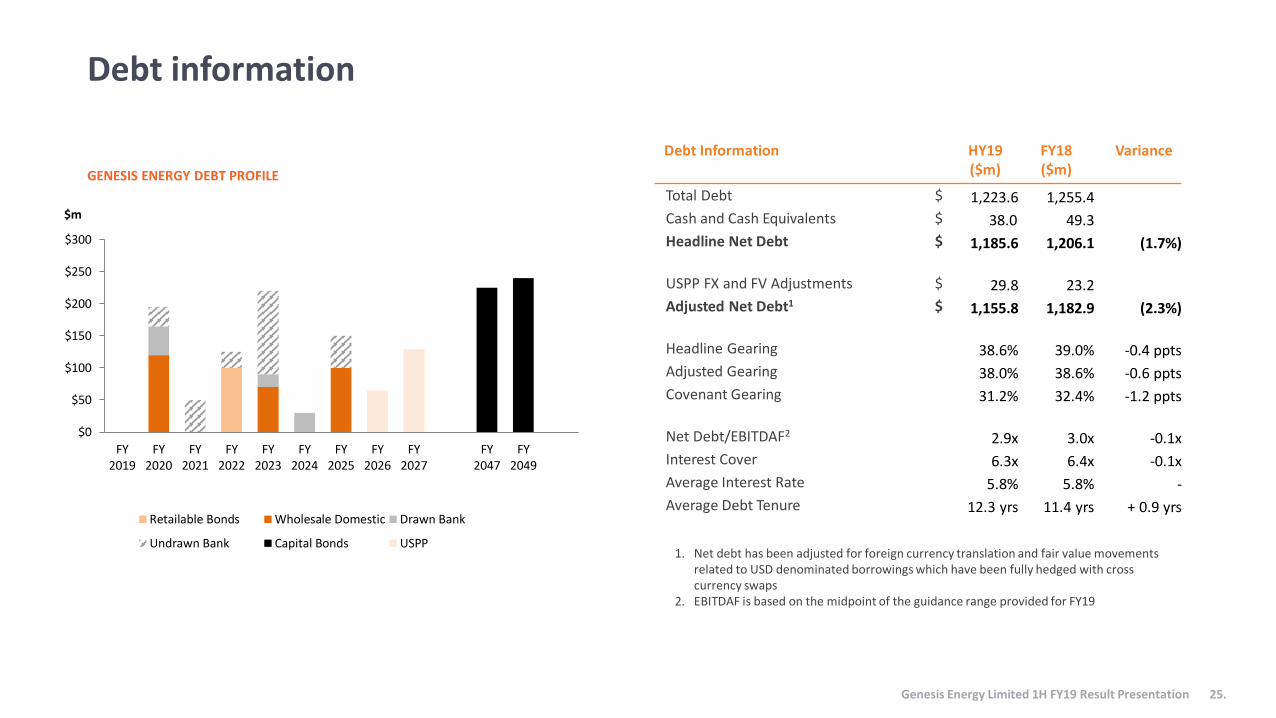

Debt Information HY19($m)

FY18($m)

Variance

Total Debt $ 1,223.6 1,255.4

Cash and Cash Equivalents $ 38.0 49.3

Headline Net Debt $ 1,185.6 1,206.1 (1.7%)

USPP FX and FV Adjustments $ 29.8 23.2

Adjusted Net Debt1 $ 1,155.8 1,182.9 (2.3%)

Headline Gearing 38.6% 39.0% -0.4 ppts

Adjusted Gearing 38.0% 38.6% -0.6 ppts

Covenant Gearing 31.2% 32.4% -1.2 ppts

Net Debt/EBITDAF2 2.9x 3.0x -0.1x

Interest Cover 6.3x 6.4x -0.1x

Average Interest Rate 5.8% 5.8% -

Average Debt Tenure 12.3 yrs 11.4 yrs + 0.9 yrs

1. Net debt has been adjusted for foreign currency translation and fair value movements related to USD denominated borrowings which have been fully hedged with cross currency swaps

2. EBITDAF is based on the midpoint of the guidance range provided for FY19

GENESIS ENERGY DEBT PROFILE

Debt information

Genesis Energy Limited 1H FY19 Result Presentation 25.

$0

$50

$100

$150

$200

$250

$300

FY2019

FY2020

FY2021

FY2022

FY2023

FY2024

FY2025

FY2026

FY2027

FY2047

FY2049

$m

Retailable Bonds Wholesale Domestic Drawn Bank

Undrawn Bank Capital Bonds USPP

Wholesale Key Information HY19 HY18 Variance

EBITDAF ($ millions) 103.8 106.4 (2.4%)

Renewable Generation (GWh) 1,713 1,697 +0.9%

Thermal Generation (GWh) 1,690 2,173 (22.2%)

Total Generation (GWh) 3,403 3,870 (12.1%)

GWAP ($/MWh) $146.32 $96.16 +52.2%

LWAP/GWAP Ratio 97% 103% +6 ppts

Weighted Average Fuel Cost ($/MWh) $33.90 $35.72 (5.1%)

Coal/Gas Mix (Rankines only) 85/15 62/38

Kupe Key Information HY19 HY18 Variance

EBITDAF ($m) 52.5 55.7 (5.7%)

Gas Production (PJ) 5.7 6.1 (6.6%)

Gas Sales (PJ) 5.5 6.1 (9.8%)

Oil Production (kbbl) 235 281 (16.4%)

Oil Sales (kbbl) 168 241 (30.3%)

LPG Production (kt) 23.6 22.4 +5.4%

LPG Sales (kt) 23.7 22.7 +4.4%

Average Brent Crude Oil (USD/bbl) $71.52 $56.74 +26.0%

Realised Oil Price (NZD/bbl) $91.12 $78.24 +16.5%

Operational highlights

Genesis Energy Limited 1H FY19 Result Presentation 26.

Customer Key Information HY19 HY18 Variance

EBITDAF ($ millions) 61.7 56.1 +10.0%

Electricity Netback ($/MWh) $103.98 $99.75 +4.2%

Gas Netback ($/GJ) $8.73 $8.91 (2.0%)

LPG Netback ($/t) $810.26 $781.86 +3.6%

Customers with > 1 Fuel 113,549 105,758

Electricity Only Customers 335,332 345,832

Gas Only Customers 17,440 18,509

LPG Only Customers 34,770 34,534

Total Customers 501,091 504,633 (0.7%)

Total Electricity, Gas and LPG ICP’s 674,387 667,273 +1.1%

Volume Weighted Average Electricity Selling Price – Resi ($/MWh)

$251.62 $248.52 +1.2%

Volume Weighted Average Electricity Selling Price – SME ($/MWh)

$220.02 $216.03 +1.8%

Volume Weighted Average Electricity Selling Price – C&I ($/MWh)

$126.20 $120.45 +4.8%

Volume Weighted Average Gas Selling Price ($/GJ)

$24.25 $25.59 (5.2%)

Volume Weighted Average LPG Selling Price ($/tonne)

$1,764.42 $1,828.90 (3.5%)

Customer Electricity Sales (GWh) 3,139 3,008 +4.4%

Customer Gas Sales (PJ) 4.5 4.0 +12.5%

Customer LPG Sales (tonnes) 19,380 18,281 +6.0%

Health & Safety Information HY19 HY18 Variance

Total Recordable Injury Frequency Rate 1.11 1.44 (0.33pt)

Disclaimer

This presentation has been prepared by Genesis Energy Limited (‘Genesis Energy’) for information purposes only. The information in this presentation is of a general nature and does not purport to be complete nor does it contain all the information required for an investor to evaluate an investment. This presentation may contain projections or forward-looking statements regarding a variety of items. Such forward-looking statements are based upon current expectations and involve risks and uncertainties. Actual results may differ materially from those stated in any forward-looking statement based on a number of important factors and risks.

Although management may indicate and believe that the assumptions underlying the forward-looking statements are reasonable, any of the assumptions could prove inaccurate or incorrect and, therefore, there can be no assurance that the results contemplated in the forward-looking statements will be realised. EBITDAF, underlying profit and free cash flow are non-GAAP (generally accepted accounting practice) measures. While all reasonable care has been taken in compiling this presentation, to the maximum extentpermitted by law Genesis Energy accepts no responsibility for any errors or omissions and no representation is made as to theaccuracy, completeness or reliability of the information. This presentation does not constitute investment advice.

Genesis Energy Limited 1H FY19 Result Presentation 27.