Embed Size (px)

Citation preview

Hurricane IkeThe Present and Future Impact The Present and Future Impact

on theon theProperty Insurance MarketProperty Insurance Market

Expected Losses• An Educated Guess at this time• Expected to fall between $13 and $21 billion• Unknown amount for non-covered losses such as loss of

business income, spoilage and flood• It is estimated that less the 20% of Galveston residents and

businesses purchased flood insurance• Texas Windstorm Insurance Association (TWIA) may pay

more than $3 billion of the losses• TWIA assessments to insurance companies could approach

$1 billion*

Claims Reported• Most claims have been reported• Total number of claims expected to exceed 300,000• Approximately 60% of all reported losses have been

looked at by an adjuster or field appraiser• Most simple property claims expected to be closed

by the end of November, 2008• Larger, complicated claims could extend well into

2009• Some delay in larger property value claims due to

coinsurance issues

What is Needed

• Documentation, Documentation, Documentation• Evidence of ownership• Independent valuations – Actual Cash Value (ACV) –

vs- Replacement Cost Value (RCV)• Photos, financial records, receipts• Inventory of loss and supporting documentation

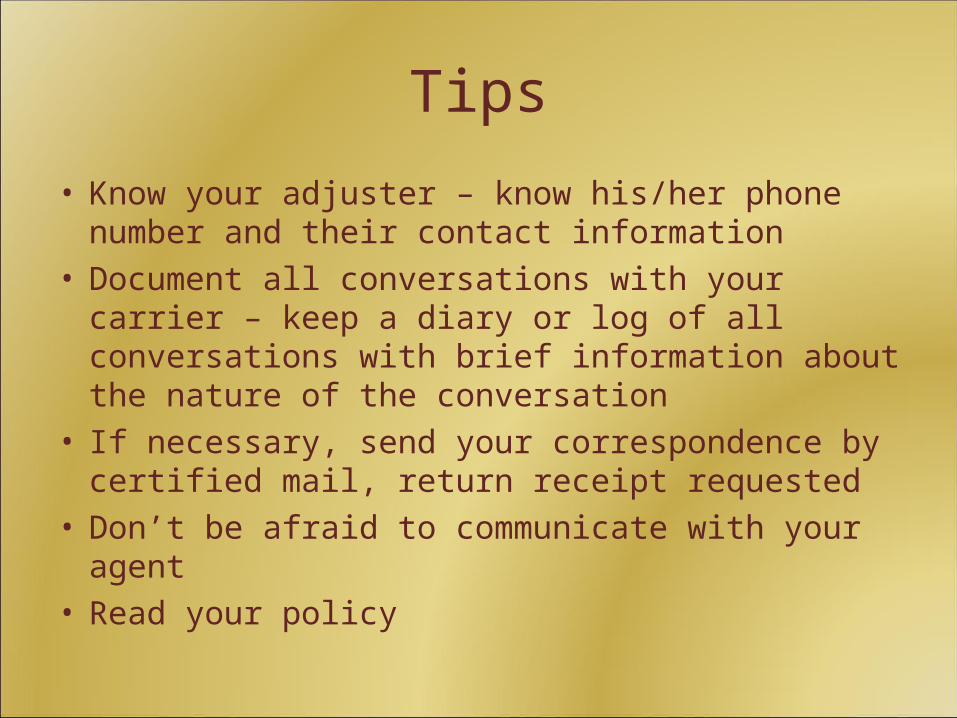

Tips

• Know your adjuster – know his/her phone number and their contact information

• Document all conversations with your carrier – keep a diary or log of all conversations with brief information about the nature of the conversation

• If necessary, send your correspondence by certified mail, return receipt requested

• Don’t be afraid to communicate with your agent• Read your policy

Industry Groups with Employment* Highly Concentrated in theTier 1 Windstorm Coverage Area

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%Fi

shin

g, H

untin

g,Tr

appi

ng

Wat

erTr

ansp

orta

tion

Pet

role

um &

Coa

lP

rodu

cts

Pip

elin

eTr

ansp

orta

tion

Sce

nic

&S

ight

seei

ngTr

ansp

orta

tion

Oil

& G

asE

xtra

ctio

n

Che

mic

alM

anuf

actu

ring

Sup

port

Act

iviti

esTr

ansp

orta

tion

*Wage and Salary employment in the Tier 1 Windstorm Coverage Area as a percent oftotal Texas Wage and Salary employment in 2004.Source: The Perryman Group

The Tier 1 Windstorm Coverage Area* as a Percent of Total Texas Real Gross Product (RGP)

by Industry 2006

8.92%

61.96%

34.15%

20.05%

43.70%

26.49%

48.30%

16.60%

25.80%

31.03%

23.04%

0% 10% 20% 30% 40% 50% 60% 70%

Agriculture

Mining

Construction

Durable Mfg

Nondurable Mfg

Trade

TWU

Information

FIRE

Services

Government

*Includes all of Harris County. Note: FIRE is Finance, Insurance, & Real Estate; TWU is Transportation, Warehousing, & UtilitiesSource: The Perryman Group

Future Expectations• No immediate, significant change in pricing. Expect 1 to 3

years before seeing impact• Some moderate pricing adjustments in the immediate

future• Pricing points to change based upon location of risk,

construction of risk and age of risk• Increased pressure on deductibles and insurance to value

(co-insurance)• Some shrinkage in capacity

Pricing Points• Better pricing to be reserved for newer properties,

favorable classes of construction and risks in favorable wind exposure areas

• Expanding pressure on pricing for lower classes of construction, older risks and risk in highly exposed wind areas

• There will be some immediate adjustments in pricing that were set into motion before the storm

• More significant changes in 1 to 3 years

Deductibles and ITV*• Increased pressure on wind deductibles. Expect 2% to 5%

wind deductibles• Expect increased scrutiny on values. Carriers want a clear

picture of their exposures in highly concentrated areas like Harris County

• Avoidance of under-insurance and over-insurance to maximize premium in relation to true exposures

*Insurance-To-Value

Capacity

• Expect carriers to carefully review their concentration of risk

• Expect carriers to manage their capacity by knowingly diluting their exposure in high concentration Tier 1 & 2 areas and increasing their appetite for properties farther north within the state

• There is a real possibility of some carriers completely ceasing new property business in the area

What Can You Do?• Utilize the better construction classes for future new

construction• Prepare for higher deductibles to help stabilize premium.

Escrow funds sufficient to meet the large deductible• Review values & exposures carefully. Maximize the use of

your premium dollars• Prepare to spend more time on your insurance. More

effort and exploration will be needed• TWIA? Get involved!

Mark Dalton Insurance Agency

• Some material used for this presentation was obtained from and used with the permission of the Independent Insurance Agents of Texas (IIAT) and the Perryman Group/IIAT study of Coastal Insurance exposures as prepared in 2006

101 Southwestern Blvd, Suite 106

Sugar Land, TX 77478

TEL: 281-242-2333

www.mdaltoninsurance.com

![Origin of the Hurricane Ike forerunner surgecoast.nd.edu/reports_papers/forerunner_2011GL047090.pdf2. Hurricane Ike Forerunner Observations [4] Two days prior to Ike’s landfall,](https://img.pdfslide.us/doc/110x75/5f77c490deecde5f0019f526/origin-of-the-hurricane-ike-forerunner-2-hurricane-ike-forerunner-observations.jpg)