Embed Size (px)

DESCRIPTION

http://www.law-views.com/images/acca/mod4.pdf

Citation preview

CORPORATIONS AND LEGAL PERSONALITY THE DOCTRINE OF INCORPORATION

Module 4.1

THIS VEIL may be lifted by law (courts or statute) in certain circumstances so that the human and commercial reality behind the corporate personality can be revealed.

COMPANY (artificial or abstract legal person)A company is an artificial (as opposed to a natural) person which is an entity in its own right with a legal personality separate from that and independent of its shareholders (members/owners) or directors (managers).

Relevant Case Authority

SALOMON v SALOMON & CO (1897)S sold his sole-trader business to a company of which he was the main shareholder. When the company went into liquidation, S was sued (by creditors) in his personal capacity as they claimed S was, in effect, the company.

HELD.

S was not liable for any moneys owed to the creditors. These were company debts and as the company had a separate legal personality, it alone was answerable to the creditors.

LEE v LEE’s AIR FARMING LTD (1960)L was a director and owned the bulk of the shares in a company engaged in aerial crop-spraying. L appointed himself as the only pilot of the company at a salary arranged by himself. Subsequently, L was killed while crop-spraying and his widow claimed workers compensation from the company as employer of her husband. Question under the relevant Act was whether the relationship of employer and employee could exist between L and the company.

HELD.

Yes they were separate legal persons, thus even though L owned most of the shares, he could still be an employee of the company. Thus his widow was entitled to compensation.

MACAURA v NORTHERN LIFE ASSURANCE (1925)M sold his forest to a company in which he owned all the shares. M had previously insured the forest in his own name but omitted to change the relevant policy to state the name of the company as owner. The forest was later destroyed by fire and M sought to claim under the policy.

HELD.

L could not file a claim as the forest was owned by the company. As shareholder, L had no insurable interest in the forest because the company was a separate entity.

I N C O R P O R A T I O N

SHAREHOLDERS (Members)

DIRECTORS (Management)

EMPLOYEES (natural legal persons)

V E I L

O F

CORPORATIONS AND LEGAL PERSONALITY THE CONSEQUENCES OF INCORPORATION

Module 4.2

A company's existence does not depend on the presence of human elements or resources (although these are, for practical purposes, necessary to run the company’s business activities).

Thus, the company may have perpetual succession notwithstanding the retirement, bankruptcy, mental disorder or death of the shareholders/members.

(perpetual = never ends or changes)

( 1 )Perpetual

Succession

Where a company is limited by shares, the extent of a member’s liability is the amount which remains unpaid on the nominal value of the shares held.In the event that the company is limited by guarantee, the liability is that which the member has (guaranteed) agreed to pay if the company is wound up.

( 2 )Limited Liability

If a wrong has been committed against a company, then, as proper claimant, only the company can sue (acting through the majority shareholders). This is known as the rule in FOSS v HARBOTTLE and in effect means that an individual cannot institute proceedings in such circumstances (although there are exceptions where minority protection is an issue).

( 3 )Legal

Capacity

The fact that a company is a legal entity separate and distinct from its shareholders, necessitates the involvement and participation of management in the form of a board of directors.

( 4 )Ownership

and Management

a) Proper Claimant b) Contract

A company may have liability in tort vis a vis third parties who may have suffered injury, loss or damage by virtue of the acts or omissions of the company’s employees or agents.

c) Tort

It is the company itself which owns corporate property. It is not owned by the members (or directors) so it will not be affected by any change in shareholders. (Refer MACAURA v NORTHERN LIFE ASSURANCE (1925)).

In effect, this means that in small companies, (e.g. with a single shareholder) the member would be open to a charge of theft if he were to treat the corporate property as his own.

( 5 )Ownership of Property

A company has the capacity to enter into contracts in its own name. (Because it has unlimited liability all its assets may be utilised to discharge debts).

CORPORATIONS AND LEGAL PERSONALITY LIFTING THE VEIL OF INCORPORATION

Module 4.3

( 1 )Introduction

( 2 )Veil Lifting Under Statute (Legislative Intervention)

This legislature has neutralised or limited the effects of the SALOMON principle in a wide range of areas.

a) Absence of Trading Certificate (S767CA06)

In the event that a public company commences trading without having previously obtained a trading certificate, then by virtue of S767 of the Companies Act 2006 , the directors shall be personally liable for any loss of damage suffered by a third party.

a) Absence of Trading Certificate (S767CA06)

Although in certain cases the courts have strictly applied the SALOMON principle, they have, on occasions, intervened to achieve justice where circumstances warrant this. The courts’ approach is sometimes dictated by policy considerations and sometimes by the need to prevent the evasion of a legal obligation or the use of the corporate form for fraudulent purposes.

( 4 )Veil Lifting at Common Law

(Judicial Veil Lifting)

b) Disqualified Director Engaging in Management (CDDA 1986)

Under the provisions of the Company Directors Disqualification Act 1986 , a “disqualified” director participating in the management of a company shall be jointly and severally liable (along with the company) for the company’s debts.

b) Disqualified Director Engaging in Management

(CDDA 1986)

c) Fraudulent Trading (S213 IA 1986)

S213 of the Insolvency Act 1986 , was enacted to cover situations where incorporation is used as a vehicle for fraud. This “fraudulent” trading provision provides that if in the course of the winding up of a company it appears that any company business has been carried out with intent to defraud creditors (or other person) or for any fraudulent purpose, the individuals can be called upon to contribute to the debts of the company.

c) Fraudulent Trading(S213 IA 1986)

d) Wrongful Trading (S214IA 1986)

Unlike fraudulent trading, this does not require proof of an intent to defraud. Liability under this provision will arise if a Director , at some time before the commencement of the winding up of a company, knew (subjective) or ought to have concluded (objective) that there was no reasonable prospect that the company would avoid going into liquidation, but nevertheless continued to trade. In such cases, directors are liable to contribute to the debts of the company (Refer RE: PRODUCE MARKETING CONSORTIUM LTD, (No.2) (1989) where a company over a 7-year period gradually moved towards insolvency. The two directors continued to do business instead of going into liquidation when it became apparent that the company had reached the point of no return. Both were liable under S214 for wrongful trading and ordered to contribute £75000 towards the debts of the company).

IMPORTANT NOTE: Sections 213 and 214 have a slightly different impact on the SALOMON principle . S213 may embrace company shareholders and thereby affect their limited liability.

S214 refers to directors only although in small companies this can also indirectly affect shareholders who also happen to be Directors (thus limited liability is indirectly affected here).

d) Wrongful Trading (S214 IA 1986)

We may have a situation where a parent company (holding company) owns all the issued share capital in other companies (which are thus wholly owned subsidiaries). In effect, the parent company controls all these companies and in real terms constitutes one economic/business entity which is structured in the form of independent sub-entities each with its own legal personality. In such circumstances, the parent company could effectively take advantage of its separate personality to enjoy the benefits of limited liability. The implications of this are that the parent company could channel higher-risk business transactions through one of its wholly-owned subsidiaries. Consequently, the parent company’s assets would be secure in the event of the financial demise of the subsidiary in question.

However:

Notwithstanding the above, there have been instances where the courts have lifted the veil between a holding company and its subsidiaries

Cases in Point

In GILFORD MOTOR COMPANY LTD v HORNE(1933) an employee agreed not to solicit customers from his employer once he ceased to be employed by him. Despite this, the employee formed a company and solicited these customers after he left his employers.

HELD

The company was a mere sham (merely a front) and could not be used to avoid the employee’s contractual obligation not to solicit customers.

In DAIMLER v CONTINENTAL TYRE & RUBBER CO (1916) a company incorporated in the UK was owed money. When it sued the creditor for the debt, the creditor argued that it would not repay the amount owed as this would be tantamount to “trading with the enemy” which was prohibited by law at the time. The company argued that it was not an “enemy” company as it was incorporated in the UK.

HELD

Control (shareholding) of the company was in “enemy” hands because lifting the veil revealed only one British shareholder whilst the majority members were German. Thus, the debtor was under no obligation to repay the debt. (The veil was lifted to effectively give the company the same nationality as its members).

In JONES v LIPMAN (1962) , X had entered into a contract with Y for the sale of X’s land. X then changed his mind and in order to avoid the contract he formed a company to which he conveyed his land (arguing that as he was now no longer the owner, he could not comply with the contract).

HELD

The company was a mere façade or front for X, so Y was entitled to specific performance to give him ownership of the land.

ADAMS v CAPE INDUSTRIES (1990)

CAPE was a UK-registered corporation involved in asbestos mining operations in South Africa. The international marketing function was carried out through a number of subsidiaries, one of which was CPC which was registered and carried on business in the USA. A court judgement was given against CPC and the claimant sought to enforce it against Cape by arguing that the veil between CPC and Cape should be lifted accordingly.

HELD There were no special circumstances to indicate that CPC was a mere façade for CAPE. There was no indication of any “agency” situation as CPC was an independent company under the control of the chief executive. Furthermore, the “economic reality” argument accepted in the case of DHN FOOD DISTRIBUTORS would not be extended to cover this particular case. Effectively, the holding company (CAPE) could not be liable for its subsidiary’s (CPC) debts under the circumstances.

The case of WOOLFSON v STRATHCLYDE REGIONAL COUNCIL (1978) adopted a more cautious approach than DHN and held that the veil will only be lifted where special circumstances exist indicating that it is a mere façade concealing the true facts.

DHN HOLDING COMPANY

Operating from premises owned by subsidiary

Subsidiary X

Not engaged in business activities Same directors as holding company

Local Authority

(3) Lifting the Veil

on Group Structures

Cases in Point

DHN FOOD DISTRIBUTORS V LONDON BOROUGH OF TOWER HAMLETS (1976)

DHN, a parent company, owned a subsidiary company X which was not engaged in any business activities. DHN operated from premises which were in fact owned by its subsidiary X. At some point a local authority decided to proceed with a compulsory acquisition of these premises. In doing so however, the local authority declined to compensate DHN for disturbance (paid only to owner occupiers) on the basis that DHN was not the owner of the premises. DHN argued that, on the contrary, DHN and its subsidiary should be regarded as a single economic entity for this purpose, thereby, in effect, entitling it to compensation as “owner”.

HELDDHN’s argument was accepted by the court and, as owner, was therefore entitled to compensation for disturbance.

As previously observed, the SALOMON principle of separate legal personality has, benefited the shareholders of companies (refer LEE v LEE’s AIR FARMING LTD (1960). However:The price of such a benefit is sometimes borne by the creditors, in conformity with the general philosophy of the Companies Acts. (in that they cannot sue individual shareholders or directors) But!

It is sometimes the case that a strict application of the SALOMON principle may result in a situation where the separate personality doctrine is likely to be abused or to lead to unjust consequences. In such circumstances, the courts and the legislature (Parliament) have intervened to lift the veil of incorporation with the result that a company will not be treated as a separate legal entity (it is said that the veil is “lifted”, “pierced” or “set aside” to reveal the identity of shareholders – or directors - with a view to ascribing liability on these individuals if circumstances warrant this).

Same directors as subsidiary X

CORPORATIONS AND LEGAL PERSONALITYLEGAL FORMS OF BUSINESS

ORGANISATION Module 4.4

The Sole Trader

This is the simplest legal form of business which is essentially a sole proprietorship or one-man business. Features include the following:

The sole trader himself and the sole trading business are one and the same thing – he himself is the business. An offshoot of this is that it is he who owns the assets and it is he who will be personally responsible for the business debts.

The relative simplicity of this business form means there are no legal formalities, filing requirements or fees, thus dispensing with the need for professional advice. Whilst a sole trader has the benefit of keeping the profits for himself, he is also liable for any losses that may accrue. The fact that he has unlimited liability would mean that in the event of insolvent liquidation, the sole trader’s creditors would be able to institute claims on his personal assets.

The Partnership

The partnership is defined by the Partnership Act 1892 as “the relationship” which subsists between persons carrying on a business in common with a view of profit. Features include the following:

There are no formal legal filing requirements. Partnerships are advantageous from the financing aspect in that it accommodates the pooling of economic resources by two or more persons (the maximum number of partners since 2002, is unlimited). The operative partnership agreement may be drafted or adapted to ensure a flexible organisational structure. The provisions of the Partnership Act 1890 may have an adverse effect on persons who are in business together but are unaware that, in legal terms, they are in fact a partnership. Partners are jointly and severally liable for the debts of the partnership.

Limited Liability Partnership (LLP)

Company

See relevant sections for details

See relevant sections for details

CORPORATIONS AND LEGAL PERSONALITY COMPANIES AND PARTNERSHIPS

A COMPARISON Module 4.5

1) Creation Formalities

Companies

Are created by registration and must have a written constitution in the form of Articles of Association.

Do not have separate legal personality and this places the individual partners in a position whereby, in their personal capacity, they will:

Own property themselves. Be liable on partnership contracts Be liable if sued.

Partnerships

3) Management

The management function is undertaken by directors who need not be shareholders of the company.

The management function can be undertaken by the partners themselves.

Partners are regarded as agents of the partnership in relation to transacting the firm’s business in the usual way.

The shareholders of companies are not agents thereof (although directors are).

4) Agency

2) Personality

Have separate legal personality which enables it to:

Own property. Contract in its own name. Sue and be sued in its own name.

There are no formalities involved to form a partnership. A written agreement between the partners is not necessary although, for practical purposes, most desirable.

5) Return of Capital

Generally speaking, companies are precluded from returning capital to its shareholders.

Partners are jointly and severally liable (in their personal capacity) for the partnership debts.

9) Dissolution

Would require a formal liquidation procedure per relevant insolvency/winding-up legislation.

Can simply be dissolved by agreement between the parties or may be automatically terminated upon the death or bankruptcy of an individual partner (depending on the provisions of the partnership agreement, if any).

Can only create fixed changes as security for borrowing.

Are able to create both fixed and floating charges as security for borrowing.

10) Borrowing

6) Liability

The company, as a separate legal entity (with unlimited liability) is liable for its debts whereas the shareholders will only be responsible for any unpaid portion on the price of their shares (if company is limited by shares) or the amount they have undertaken to contribute (if limited by guarantee) , as the case may be.

Partners may withdraw capital

7) Tax

As separate legal entities, are subject to corporation tax.

The individual partners themselves will pay income tax in their personal capacities.

Other than the need for declaration of taxable profits to the Inland Revenue, there are no disclosure requirements or any obligation to publicise the affairs of the partnership business.

Are subject to a number of statutory requirements regarding the availability of financial and other information to the public at large.

8) Publicity

CORPORATIONS AND LEGAL PERSONALITY PUBLIC AND PRIVATE COMPANIES - A COMPARISON

Module 4.6

1. Definition

Public

Registered as a public company.

Requires only one director.

Private

3. Name

Ends with the words “plc” or “public limited company”.

Ends with the word “Ltd” or “limited”.

There is no minimum authorised capital.

A private company is prohibited by law from offering its shares or debentures (securities) to the public for subscription.

Requires a minimum authorised capital of £50,000.

Capital may be raised by offering shares or debentures (securities) to the public for subscription.

4. Capital

2. Directors

Must have a minimum of two directors.

Any company that is not a public company.

5. Secretary

Must have a qualified secretary.

Audit is not a requirement if turnover is below £5,600,000.

9) Identification

Memorandum to incorporate a clause describing company as a “public company”

There is no need for an identification clause in the memorandum.

6. Audit

There is an ‘audit of accounts’ requirement for public companies.

No secretary is required.

7) Commencement of Operations

May only commence business following issuance of a trading certificate.

May commence operations as soon as the registrar issues a certificate of incorporation.

An AGM need not be held at all.

An AGM must be held every year.

8) Annual General Meeting

CORPORATIONS AND LEGAL PERSONALITY TYPES OF COMPANY

Module 4.7

( 1 ) Private Company

May be free-standing (independent) or subsidiaries of other companies.

Definition

A private company is any company which is not a public company.

Limited Company

In a company limited by shares, the shareholder’s liability is limited to the amount, if any, unpaid on the nominal value of his shares. Thus, fully-paid shares will not generate any further liability on the part of the shareholder.

In a company limited by guarantee, the liability of the shareholders is limited to the amount they agree to contribute to the assets in the event of winding up (past members in the preceding year can be liable if current members default in this regard). This type of company is appropriate where the need to raise capital is not crucial and the company is set up for non-profit making purposes.

Limited by Shares

Unlimited Company

Only a private company can be unlimited. This means member’s do not enjoy limited liability so that in the event of liquidation, they will be obliged to pay as much as may be required to pay off the company’s debts.

Not obliged to file accounts at the Registrar of Companies (unless unlimited company is controlled by one or more limited companies or has a limited company as a subsidiaryAt liberty to buy its own shares.Must have special articles of association.

( 2 ) Public Company

May be free-standing (independent) or subsidiaries of other companies.

A public company is an entity which is formed by virtue of the Registrar of Companies issuing a certificate that the company has been registered as a public company. This will be done subject to the following:

i) the name ends with the words “public limited company” or “plc”

ii) the memorandum of association declares that it is to be a public company

iii) the authorised capital of the company must not be below £50,000

iv) it is a limited company

Definition

FOR A COMPARISON OF PUBLIC AND PRIVATE COMPANIES REFER TO Module 4.5

Limited by Guarantee Features

CORPORATIONS AND LEGAL PERSONALITY PROMOTERS

Module 4.8

In the absence of any statutory definition, we turn to case law which regards a promoter as a person who “undertakes to form a company and who takes the necessary steps to accomplish that purpose”.

(Refer TWYCROSS v GRANT 1878).

Thus!

A promoter would be anyone who takes procedural steps to form the company and/or anyone who undertakes preparatory business activities for the company which is to be incorporated (e.g. registration of company, negotiating pre-incorporation contracts, finding initial directors and shareholders, issuing prospectus (if public company).

But Note:

A person who acts in a purely professional capacity (e.g. solicitor or accountant) would not be regarded as a promoter

(Refer RE GREAT WHEAL POLGOOTH CO 1883).

Background :

In the event that a promoter is to be the sole owner of the company to be formed, he may obtain an advantage from his position as promoter simply because there is no likelihood of any conflict of interest. (SALOMON v SALOMON ) illustrated a situation where the promoter sold his existing business to a newly-formed company at an inflated value, in return for the total share capital. There was no prospect of anyone else being prejudiced by this however).

But!

Where a promoter is involved in a situation where other shareholders will “come into the picture”, the promoter is in a fiduciary position as he effectively “undertakes to act for and on behalf of another person in some particular matter or matters”. (Finn 1977)

Note:

A promoter is not considered to be an agent of the company he is promoting simply because a company which has not yet been, (or is in the process of being,) formed is, in effect, a non-existent principal . Furthermore, a promoter is not a trustee in this context.

(Refer RE LEEDS & HANLEY THEATRES OF VARIETIES LTD 1902).

What is a Fiduciary?

Duties of Promoters SEE Module 4.9

a) Background

b) The legal position is reflected by both common law principles and statutory intervention (which reinforces the common law).

(ii) Statute

The position is appropriately summarised by ROVER INTERNATIONAL LTD v CANNON FILM (1987) which held that “if a person does not exist they cannot contract”.

Furthermore!

Once a company is formed, it will, in effect, be a stranger to any prior contract and the principles of privity will prevent the company from having any rights or liabilities thereunder. In addition, under principles of agency , the company cannot ratify a contract because a person cannot be an agent of a principal that does not exist. ( Refer KELNER v BAXTER 1866 ) where the promoters of a hotel contracted to buy wine from a supplier. After incorporation, the hotel ratified this transaction. The wine was consumed but the hotel went into liquidation before the supplier was paid. When the promoters were sued, they claimed the hotel was liable due to the ratification. HELD – Contract was not capable of being ratified as company was not in existence when the wine contract was concluded.

(i) Common Law

What can a promoter do to protect his position in respect of pre-incorporation contract? to refrain from concluding an agreement until the company is formed (at which time it can enter into a contract for itself)

after incorporation the company and the other contracting party substitute the initial pre-incorporation contract with a new contract on similar terms (this is known as “novation”)

assignment (transfer) of the contract

agreement with the company to the effect that the promoter will not be personally liable (S51CA06)

buying a “ready-made” off-the-shelf company which can trade immediately (although this is a relatively cheaper step to take, it will involve alteration of articles, name etc.)

promoter securing an option (by payment of a fee) from the other party, which can be exercised when the company is formed.

c) Promoters Protection

( 1 )Definition

( 2 )Pre-Incorporation

Contracts

( 3 )Promoters as Fiduciaries

S51 of the Companies Act 2006 , reinforces the common law position by providing that subject to any agreement to the contrary, the person making the contract is personally liable.

A case in point.

In PHONOGRAM LTD v LANE (1981) the court held that when the promoter signed a pre-incorporation agreement “for and on behalf of F Ltd”, this was not sufficient for regarding it as “agreement to the contrary”. Thus the promoter was personally liable. (The court emphasised that to exclude personal liability under S51 CA06 clear and express words were needed).

(Note: A person who is personally liable under S51 CA06 will also be able to enforce the contract per BRAYMIST LTD v WEST FINANCE 2002 ).

This can perhaps be understood in the context of the nature of the specific obligations that a fiduciary owes to his principal. In 2004, Penner described fiduciary duties as those owed to a 3 rd party to act with “loyalty and good faith in dealings which affect that person”.Penner broadly explained this as a duty on the part of a fiduciary to act “solely with the interests of his principal in mind” and that neither the fiduciary’s own self-interests or the interests of others should be allowed to conflict with the principal’s best interests.

These are contracts entered into by promoters in the company’s name or on its behalf) prior to registration of the company. The problem here is that the company itself only comes into existence when the relevant certificate of incorporation is issued by the Registrar. Thus until it is incorporated, it cannot be contractually bound by any agreement that the promoters may have concluded in its name or on its behalf.

Note:

Such contracts may, for example, relate to the leasing of premises or connection to electricity, telephone and other utilities so that the company would be more or less ready to operate effectively, immediately after the incorporation process is completed.

CORPORATIONS AND LEGAL PERSONALITY PROMOTERS

Module 4.9

The Fiduciary DutiesRemedies for Breach of

Duty of Disclosure

The company must prove that it has suffered loss in order to succeed in a claim for damages (this “loss” turns on whether the company paid an excessive price).

Where a promoter is in breach of his fiduciary duty, this renders the contract voidable at the company’s option.

Voidable?

The company has the option to either rescind (cancel) the contract or to affirm it.

However?

There are the following limitations on the right to rescind:

a) the right to rescind will be lost if the company affirms the contract (either by its actions or expressly)

a) the right to rescind will be lost if the company affirms

(Re: CAPE BRETON CO (1885)). (Re: CAPE BRETON CO (1885)).

b) The right to rescind will be lost if the company delays in exercising its right to rescind.

b) The right to rescind will be lost if the company delays in

(LEAF v INTERNATIONAL GALLERIES 1950). (LEAF v INTERNATIONAL GALLERIES 1950).

c) The right to rescind calls for restoring the parties to their original position.

c) The right to rescind calls for restoring the parties to their

But Note:

This will not however prevent the company from suing the promoter to account for the secret profit.

( a )Rescission

( b )Damages

If the company elects not to rescind, but wishes to keep the property, then the “recovery of profit” remedy may be appropriate. Similarly, it is a useful remedy if it cannot establish loss (paying excessive price) for the purposes of instituting a claim for damages.

( c )Recovery of Profit

The Fiduciary DutiesNot to Make a Secret Profit

(Duty of Disclosure)

A promoter must not make a secret profit from his position. Essentially, this duty seeks to avoid a situation where a promoter might sell property (either owned by him or in which he has an interest) to the company, from which he will make a profit. Under such circumstances, it is imperative that the company is aware of this.

HOW?

Promoters are required to make full disclosure of any such profit to an independent Board of Directors once the company is incorporated. (Re LADY FORREST GOLD MINE LTD 1901).

Failure of the promoter to disclose all material facts of a transaction to an independent board would result in a voidable contract whereby the company could choose to accept the transaction or cancel it:

A case in point

In ERLANGER v NEW SOMBRERO PHOSPHATE CO (1878) a syndicate bought a mine for £55000 then formed a company to which they sold the mine (through a nominee) for £100,000. The syndicate did not disclose their interest in the contract. When the company’s operations encountered problems, the shareholders dismissed the original directors and the new board instituted a claim and rescinded the sale contract.

[Note: In SALOMON v SALOMON 1897 , the court held that if for the purposes of disclosure, the board was not independent, it would suffice if disclosure of all material facts were made to the original shareholders. This was later qualified in

GLUCKSTEIN v BARNES where it was held that in such a case the original shareholders would have to be truly independent and not a ploy to defraud the investing public].

What are the consequences of non-disclosure?

CORPORATIONS AND LEGAL PERSONALITY

ARTICLES OF ASSOCIATION Module 4.10

S21 of the Companies Act 2006 allows for the alteration of the articles, which is normally done by passing a special resolution (75% majority) at a general meeting. The amended articles must be filed with the Registrar of Companies within 15 days (together with a signed copy of the relevant special resolution). [Note: As will be explained later, this leads to a rather odd situation whereby the S33 statutory contract can be changed without the unanimous consent of the parties.

( 2 )Alteration of Articles

A conflict may arise where the majority of shareholders seek to alter the articles with a view to securing an unfair advantage for themselves (as opposed to making the changes for the ultimate benefit of the company – even if this is somewhat detrimental to a minority). THUS! In view of this possibility, there is a restriction on member’s ability to alter the Articles. NAMELY!

i) Per S22 of the Companies Act 2006 , a specific procedure may be needed to alter the articles in certain circumstances. (Thus, for example, unanimity in voting may be called for, thereby effectively “entrenching” the articles). Generally, a so-called provision for entrenchment ensures that specific provisions may be amended or repealed only if certain stipulated conditions or procedures are complied with, that are more restrictive than the normal special resolution process.

i) Per S22 of the Companies Act 2006 , a specific procedure may be needed to alter the articles in

ii) Per S25 of the Companies Act 2006 , an existing member is not bound by any alteration to the

articles which increases his liability to contribute capital unless otherwise agreed prior to or subsequent to the alteration.

ii) Per S25 of the Companies Act 2006 , an existing member is not bound by any alteration to the

iii) At common law, it has been established that any alteration to the articles must be effected in

GOOD FAITH ("BONE FIDE"), FOR THE BENEFIT OF THE COMPANY AS A WHOLE.iii) At common law, it has been established that any alteration to the articles must be effected in

Before reviewing case authority on this so-called “bona fide” test, it would be worth noting that, in essence, the courts have tried to strike a balance between the following key considerations: a) The fact that a majority has the right to alter the articles even though a minority may regard such

alteration as being contrary to its interests. a) The fact that a majority has the right to alter the articles even though a minority may regard such

b) The fact that a minority should have the right to be afforded protection against any alteration designed to benefit the majority (as opposed to the company) and which unfairly discriminates against the minority.

b) The fact that a minority should have the right to be afforded protection against any alteration

Restrictions on Alterations

SIDEBOTTOM v KERSHAW, LEESE & CO (1920)The court confirmed the validity of an alteration which was effected to dismiss a member who engaged in business activities which competed with those of the company.

ALLEN v GOLD REEFS OF WEST AFRICA LTD (1900)The court laid down the principle that the power to alter the articles must be exercised “bona fide for the benefit of the company as a whole” because the majority effectively had the power to impose its will upon the minority. Whilst this general test for determining the validity of an alteration was essentially a single principle, it comprised the two elements of “good faith” and “benefit”.

(Per the facts of the ALLEN case, the court held that the company had the power to change its articles to extend a lien (for the debts and liabilities of members) covering partly paid shares to also cover fully paid-up shares.)

Cases in Point

BROWN v BRITISH ABRASIVE WHEEL CO (1919)A public company urgently required capital. Shareholders who held 98% of the shares agreed to assist provided they could buy out the 2% minority. However, the minority declined to sell and this prompted the majority to propose a special resolution for alteration of the articles to provide that any shareholder would be obliged to transfer his shares upon receipt of a written request from members holding 90% of the shares.

HELD: Whilst the majority were considered to have acted in good faith, such an alteration was only for the benefit of the majority and not for the company as a whole.

SOUTHERN FOUNDRIES LTD v SHIRLAW (1940)The articles were altered to empower the holding company to remove the managing director (M.D.) of the subsidiary. This effectively meant that the company was now in breach of its contract of employment with the M.D. HELD Even so, the alteration was valid, but the company was liable in damages for breach of the operative service contract with the M.D.

GREENHALGH v ARDERNE CINEMAS LTD (1950)The articles provided for the existing members’ right of first refusal of shares that another member wanted to transfer (each member had right of premption). The majority sought to change this provision in the articles so that they could facilitate the admission of an outsider to become a shareholder (in the belief that this was in the interests of the company).i.e. The majority who voted for the alteration wanted to avoid having to offer their shares to the claimant before selling them to a non-member. HELD:

The alteration was permitted as this would enable the claimant himself to sell to an outsider without the need to offer the shares to other existing shareholders. The court pointed out: 1. The "bona fide" test was subjective in terms of what did the majority believe?

2. "The company as a whole" in this context means the general body of shareholders. Test is whether every individual hypothetical member would in the honest opinion of the majority benefit from the alteration.

( 1 )Introduction

The Articles are essentially internal rules which govern the running of a company. Anyone who forms a company is at liberty to draft their own rules. If they do not do so, then the so-called “Model Articles” will apply. (S19 CA2006) In effect, the model articles will apply:

i) when no articles are submitted for registrationi) when no articles are submitted for registration

ii) when the special articles submitted for registration do not exclude or modify the model/default articles.

ii) when the special articles submitted for registration do not exclude or modify the

In essence, the Articles provide for the operation of two organs or committees to run the company, namely:

i) the general meeting (which is the shareholders’ committee or organ)i) the general meeting (which is the shareholders’ committee or organ)

ii) the board of directors (which is the management committee or organ ) effectively allocate powers to one or other of these organs committees (this is the most important function of The Articles). (Both case law and statutory law cast further light on the operation and application of the articles).

ii) the board of directors (which is the management committee or organ )

CORPORATIONS AND LEGAL PERSONALITY ARTICLES OF ASSOCIATION

Module 4.11

Per S33 of the Companies Act 2006 , the constitution of the company contractually binds the members of the company and the company itself. How? The Constitution (internal rules called Articles + any objects clause limiting power of the company) effectively creates a STATUTORY CONTRACT between:

(a) ContractualEffect

This is an unusual contract because:

a) it can be periodically varied by way of altering the articles by special resolution (75% members’ vote)

a) it can be periodically varied by way of altering the

b) it binds parties that are not privy to it (e.g. future shareholders).

b) it binds parties that are not privy to it (e.g. future

LEGAL EFFECT OF THE

COMPANY CONSTITUTION (CONTRACT OF MEMBERSHIP)

There is n o enforceable contract in respect of corporate right (as opposed to personal right). The question of whether a member can sue to enforce the contract will depend on whether the breach is a wrong to the company or a wrong to the individual. THUSA member can enforce a contract against the company directly only if the article constitutes a personal right (.e.g voting right, share transfer right, pre-emption right , dividend right etc.).

PENDER v LUSHINGTON (1877) Per the Articles for every ten shares, a member was entitled to one vote, subject to each member being limited to 100 votes. Once member owned more than 1000 shares and in order not to circumvent the 100 maximum vote limitation, transferred shares to a nominee, duly instructing him how to vote. However, the nominees were rejected by the chairman. HELD – The nominee could enforce his right to vote and succeeded in his claim against the company.

No enforceable contract in respect of non-member rights (“outsider rights”).

Case Showing Member Can Enforce Against Company

In BROWNE v LA TRINIDAD (1887) , the court held that the right to be a director of a company was an outsider right.

(b) Unique Features of Contract

(i)Contract Between

The Members Themselves

(ii)Contract Between

Each Member and the Company

HICKMAN v KENT OR ROMNEY MARSH SHEEPBREEDERS ASSOCIATION (1920)The company’s articles provided that all disputes between the company and its members were to be referred to arbitration. One member instituted court proceedings (instead of arbitration) when a dispute arose. The company sought to enforce the arbitration clause in the Articles. HELD: The articles were contractually binding between the members and the company. The court proceedings were stayed (stopped) accordingly.

Case Showing a Company Can Enforce Against Member

But: Articles may have evidential role.In NEW BRITISH IRON CO., ex parte BECKWITH (1892) the articles were regarded only as evidence of a contract that directors were to be paid £1000 on taking office.

BEATTIE v E&F BEATTIE LTD (1938)The articles provided for member disputes to be referred to arbitration. A director (also a member) was sued by the company to recover moneys which were allegedly irregularly paid to him. The director tried to enforce the article and refer the claim to arbitration. HELD – He could not do so because he was acting in his capacity as director and not a member.

ELEY v POSITIVE GOVERNMENT SECURITY LIFE ASSURANCE CO (1876) The articles provided that a member was appointed as the company’s lawyer. However, the member was not so appointed and sued for breach of contract. HELD – Member could not sue as there was no contract between the member as lawyer and the company (this was an “outsider right”).

RAYFIELD v HANDS (1960) The Articles provided that directors had to be members (so they would be required to buy shares from any member wishing to sell). A member sought to enforce this. HELD – There was a contract between the members themselves (“inter se”) which was directly enforceable by one member against another.

BUT NOTE

CORPORATIONS AND LEGAL PERSONALITY

REGISTRATION DOCUMENTS AND INCORPORATION

Module 4.12

The memorandum must be signed by all subscribers to the effect that they desire to form a company (by way of agreeing to subscribe for a minimum of one share). This document must be signed by at least two persons in respect of a public company, and at least one person if a private company is being formed.

The application must be completed with the following information.

Registered office particularsCompany nameStatement to the effect that shareholders liability will be limited (by shares or guarantee, as the case may be).

Whether company is public or private.

The Articles are signed by the subscribers or if no articles are supplied, a statement in lieu of special articles will indicate that the model default articles will apply. The articles are, in effect, the internal regulations of the company.

This is a declaration by director/secretary/solicitor confirming that the requirements of the Companies Act 2006 have been complied with.

This statement will include the following details:

The number of shares.

The total nominal value of shares.

The total amount “paid-up” in respect of the shares.

To include names of the first directors and, if applicable, the company secretary (who duly consents to act in such capacity).

The Registrar of Companies will inspect all documents and if he is satisfied that the requirements of the Companies Act have been fulfilled, will proceed to issue a certificate of incorporation which is conclusive evidence of such compliance and reflects the existence of the company as of the date indicated therein. (Refer JUBILEE COTTON MILLS v LEWIS (1924). HOWEVER : Whilst a business entity will be considered “incorporated” as from the date of issuance of the certificate of incorporation, a public company may not commence business until such time as the Registrar issues a certificate of entitlement to do business (“trading certificate”). This will only be forthcoming after the company has submitted a statutory declaration to the Registrar, incorporating the following particulars: The nominal value of the company’s allotted share capital is at least (≥) £50,000. That a minimum of 25% of the normal capital (+ all of any premium) has been paid up (i.e. a minimum of £12, 500 paid-up capital). Details of preliminary expenses and payments benefits to promoters.

Consequences of not Obtaining

a Trading Certificate

If this is applicable (company is limited by guarantee), it must indicate the maximum amount that each member has undertaken to contribute.

(a)Application for

Registration

(b)Memorandum of

Association

(c)Articles of

Association

(g)Statement of Capital

(d)Declaration of

Compliance

(e)Statement of

Officers

(f)Statement of

Guarantee

If a company does business or borrows prior to obtaining a trading certificate, the 3rd party will be protected as the transaction is regarded as being valid. But! The company, along with its officers commit a crime punishable by a fine (and in respect of any transaction with a 3rd party, the directors will be jointly and severally liable with the company).

CORPORATIONS AND LEGAL PERSONALITY STATUTORY REGISTERS

Module 4.13

i) Register of Members (S113 Companies Act 2006)

INFORMATION TO BE INCLUDED IN REGISTER

Name of each member (including date of membership and date of cessation of membership).Address of each member.Shareholder class (where company has more than on class of issued shares).Number of shares and amount paid up on each share (where company has share capital).

Registered office

PLACE AT WHICH REGISTER IS TO BE KEPT

ii) Register of Directors (and Company Secretary, if applicable)

Name.Service address (as opposed to residential address) – This may be the company’s registered office (must be submitted to the Registrar).Nationality.Business occupation.Date of birth.Other Directorships (whether present or previous directorships held (within the preceding 5 years).Corporate name and registered office (if director is a corporate body).

Type of charge(s) (fixed or floating).Description of specific property charged.Date of creation of charge.The amount of the charge.Name of the “chargee” entitled to the charge (the lender).

Either at the registered office of the company or at another specified location in the same country.

iii) Register of Charges(Given by the company, as security for a loan, in its capacity as “changor”)

vii) Minutes of General Meetings of the Company

Minutes (Note: Must be maintained for 10 years)

iv) Register of Directors’ interests in shares and debentures(includes any interests of a director’s spouse and any minor children under the age of 18)

Directors’ Residential Addresses

Relevant Particulars of Debentures

REGISTER TYPE

Registered office

Particulars of the shares or debentures (as the case may be) and the applicable price paid. (Note: The directors are obliged to notify the company of any such interest within 5 days of becoming aware of this interest. Thereafter, the company must enter same on a Register of Directors Interests within three days).

Minutes (Note: Must be maintained for 10 years)

Resolutions (pertaining to ad hoc matters) which are moved and passed by unanimous written agreement (signed by each member) and which effectively dispenses with the need for a full general meeting. Note: Must be validated by a director or company secretary prior to being recorded in the register.

v) Register of Directors’ Residential Addresses

vi) Register of Debenture-Holders. vi) Register of Debenture-Holders. Note: Maintaining such a register is not mandatory (i.e. it is not a statutory requirement.)

ix) Register of Written ResolutionsNote: Applicable to private companies only.

viii) Minutes of Directors’ and Managers’ Meetings.

Maintained with the Register of Members or at the company’s registered office.

Not for public domain but accessible by the Registrar of Companies, some public bodies and credit reference agencies.

In the event that such a register is maintained, it should be open to inspection as for the Register of Members (generally kept as registered office).

Registered office

Registered office

Registered office

CORPORATIONS AND LEGAL PERSONALITY ANNUAL ACCOUNTS, RECORDS AND RETURNS

Module 4.14

It is a statutory requirement per the Companies Act that an annual return (duly signed by a director or secretary) is made to the Registrar of Companies within 28 days of the anniversary of incorporation (known as the “return date”). The return must indicate the following particulars if the company is limited by shares:

The registered office address.

If the address at which the register of members or register of debenture holders is kept, differs from the registered office address, then this must be stated.

Type of company.

Company’s principal business activities.

Total number of issued shares along with their aggregate nominal value.

Classes of shares, total shares per class and total nominal value.

Members’ names and addresses.

Names and addresses of officers (directors and secretary)

Date of birth, nationality, business occupation and (if applicable) directors’ other directorships

Statement that the company has chosen to dispense with the filing of accounts and/or holding Annual General Meetings (AGM’s) – if applicable.

(B) ACCOUNTING RECORDS

A company has a statutory obligation to keep accounting records in accordance with the provisions of the Companies Act 2006. Such records must be sufficient to reflect and explain the company’s transactions and indicating with reasonable accuracy the company’s financial position. The records should be such as to enable the directors to provide a true and fair view of the company’s financial state of affairs. What should records contain?

i) daily entries of moneys paid/received

ii) company assets and liabilities

iii) statement of stock

iv) stocktaking statement to verify (iii) above

v) statement of goods bought and sold (barring retail sales) including details of buyers and sellers

(iii , iv and v above) only for companies engaged in dealing with goods. Note: Accounting records must be maintained at the company’s registered office (or such other location as determined by the directors) and be available for inspection by the company’s officers. (Shareholders do not have statutory access but may be permitted to inspect same by virtue of the Articles of Association.)

(C) ANNUAL ACCOUNTS/FINANCIAL STATEMENTS

It is a statutory requirement for companies to prepare annual financial statements (for each accounting reference period) comprising: - a balance sheet and profit and loss account reflecting a true and fair view of the company’s state of affairs

- directors’ report with respect to the company’s affairs, including:

directors’ names

recommended dividend (if any)

significant events

research and development activities

likely future developments

employees health and safety issues

(A) ANNUAL RETURN

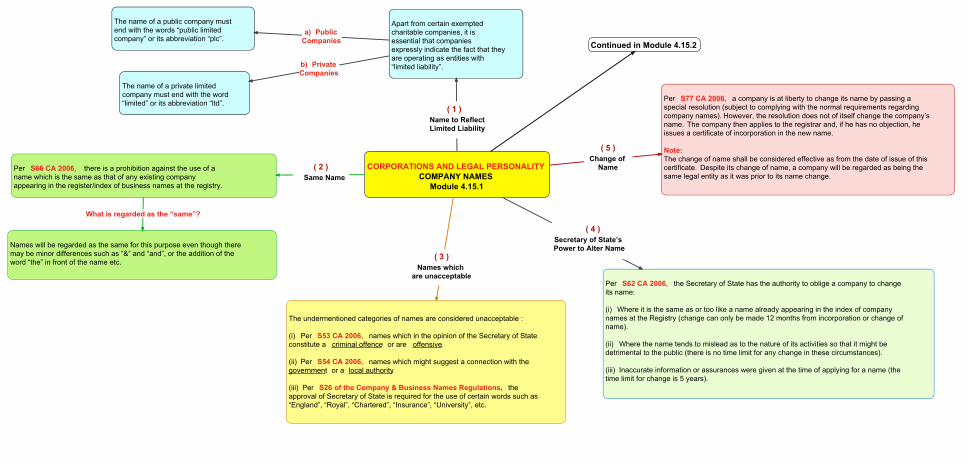

CORPORATIONS AND LEGAL PERSONALITY COMPANY NAMES

Module 4.15.1

Apart from certain exempted charitable companies, it is essential that companies expressly indicate the fact that they are operating as entities with “limited liability”.

( 1 )Name to Reflect Limited Liability

Per S66 CA 2006, there is a prohibition against the use of a name which is the same as that of any existing company appearing in the register/index of business names at the registry.

( 2 )Same Name

( 3 )Names which

are unacceptable Per S62 CA 2006, the Secretary of State has the authority to oblige a company to change

its name: (i) Where it is the same as or too like a name already appearing in the index of company names at the Registry (change can only be made 12 months from incorporation or change of name). (ii) Where the name tends to mislead as to the nature of its activities so that it might be detrimental to the public (there is no time limit for any change in these circumstances). (iii) Inaccurate information or assurances were given at the time of applying for a name (the time limit for change is 5 years).

( 4 )Secretary of State’s Power to Alter Name

The undermentioned categories of names are considered unacceptable : (i) Per S53 CA 2006, names which in the opinion of the Secretary of State constitute a criminal offence or are offensive. (ii) Per S54 CA 2006, names which might suggest a connection with the government or a local authority. (iii) Per S26 of the Company & Business Names Regulations, the approval of Secretary of State is required for the use of certain words such as “England”, “Royal”, “Chartered”, “Insurance”, “University”, etc.

Per S77 CA 2006, a company is at liberty to change its name by passing a special resolution (subject to complying with the normal requirements regarding company names). However, the resolution does not of itself change the company’s name. The company then applies to the registrar and, if he has no objection, he issues a certificate of incorporation in the new name. Note:The change of name shall be considered effective as from the date of issue of this certificate. Despite its change of name, a company will be regarded as being the same legal entity as it was prior to its name change.

( 5 )Change of

Name

The name of a public company must end with the words “public limited company” or its abbreviation “plc”.

a) Public Companies

The name of a private limited company must end with the word “limited” or its abbreviation “ltd”.

b) Private Companies

Names will be regarded as the same for this purpose even though there may be minor differences such as “&” and “and”, or the addition of the word “the” in front of the name etc.

What is regarded as the “same”?

Continued in Module 4.15.2

A company which carries on business under a name calculated to deceive the public by confusion with the name of an existing company will commit the tort of passing-off. Note:It is essential to show that:

i) The business carried on by the offending company is the same as that of the claimant.

i) The business carried on by the offending company is the same as

ii) It must be likely that customers will be drawn towards the offending company because the public will effectively be deceived and thereby associate it with the claimant.

ii) It must be likely that customers will be drawn towards the offending

a) Where Confusion likely to Arise and Claim Successful

EWING v BUTTERCUP MARGARINE CO LTD (1917)

The claimants had a change of retail shops selling margarine and tea under the name “The Buttercup Dairy Co”. The defendants had the same name and sold margarine as part of a wholesale operation. The defendants argued that there would be no confusion as

i) they were wholesales and the claimants were retailersi) they were wholesales and the claimants were retailers

ii) they operated only in London whereas the claimants were active in Scotland and the North of England.

ii) they operated only in London whereas the claimants were

HELD - An injunction (a prohibitive court order) would be granted to the claimant to prevent the defendant from trading in the name in question. The court stated:

i) The defendants had authority under their Memorandum of Association, to run retail outlets (so there was a possibility that they would do so at some time in the future).

i) The defendants had authority under their Memorandum of

ii) The claimant proposed to open branches in the South of England at some time in the future, and this could generate confusion.

ii) The claimant proposed to open branches in the South of England

( 6 )New Procedure Under Sections 69-74 of CA 2006

CORPORATIONS AND LEGAL PERSONALITY COMPANY NAMES

Module 4.15.2

b) Claim UnsuccessfulIn contrast to the BUTTERCUP case, a court has held that an action for passing-off cannot be used where a name is essentially a word in general use: AERATORS LTD v TOLLITT (1902)

The claimant in this case sought an injunction to prevent the defendants from registering a company name which included the word “Aerator” (on the basis that it would deceive the public as the word was associated with the claimant company). HELD - The claimant’s action failed as this was effectively seen as an attempt to monopolise a word (“Aerator”) in ordinary use.

c) Claim fails if Confusion Unlikely

In situations where the public is unlikely to be confused (notably where companies are engaged in entirely different businesses) an action for “passing-off” is not likely to succeed:

(Refer DUNLOP PNEUMATIC TYRE CO LTD v DUNLOP MOTOR CO LTD (1907)

( 7 )Passing-Off

Action

What is “Passing-Off”?

Cases in Point:

Having regard to the fact that there may be time-limits for the Secretary of State to effect a change of name, (e.g. 12 months where name is “too like” an existing name), a company that wishes to “challenge” another company’s name has only one other remedy available in the form of a “passing-off” action at common law, in the law of tort (a civil wrong).

Under S69 CA 2006, it is possible for any person (not necessarily another company) to lodge an objection with a company names adjudicator (appointed by Secretary of State) if a company’s name is similar to a name in which an applicant has goodwill. Note:

Per S72 CA 2006, the adjudicator’s decision and reasons must be published within 90 days. He then instructs the offending company to change its name and if it fails to do so by a prescribed deadline, the adjudicator himself is empowered to decide on a new name (offending company may appeal however to a court).

( 1 )Certificate of Incorporation

CORPORATIONS AND LEGAL PERSONALITY CERTIFICATE OF INCORPORATION

& TRADING CERTIFICATE Module 4.16

( 2 )Trading Certificate

(certificate of entitlement to do business)

For all intents and purposes, the company shall be regarded as being in existence as from the date indicated in the certificate of incorporation.

Thus:

An application must be lodged (with the registrar), incorporating the following particulars:

i) The nominal value of allotted share capital is not less than £50,000.i) The nominal value of allotted share capital is not less than £50,000.

ii) That each allotted share is paid up to at least ¼ of the nominal value and the whole of any premium.

ii) That each allotted share is paid up to at least ¼ of the nominal value and the whole of any

iii) The preliminary expenses of the company and who has paid or is to pay them.iii) The preliminary expenses of the company and who has paid or is to pay them.

iv) Any benefits given, or intended to be given, to promoters.iv) Any benefits given, or intended to be given, to promoters.

How is this obtained?

If a public company trades (or borrows) in the absence of a trade certificate: a) The company as well as any defaulting officer commits a crime and is subject to a fine.a) The company as well as any defaulting officer commits a crime and is subject to a fine.

b) It will be a ground for winding up the company under S122 of the Insolvency Act 1986 (if

the trading certificate is not obtained within one year of incorporation).b) It will be a ground for winding up the company under S122 of the Insolvency Act 1986 (if

c) The directors will be jointly and severally liable with the company if the company enters into a

transaction with a third party (contracts are still binding on the company). c) The directors will be jointly and severally liable with the company if the company enters into a

Consequences of Trading (or borrowing) Without a Certificate?

Whilst both a public and private company require a certificate of incorporation, there is a further requirement in respect of public companies which, in addition to a certificate of incorporation, will also need a trading certificate from the registrar prior to being permitted to commence trading or to exercise borrowing powers.

Upon receipt of the relevant registration documents, the registrar will inspect the documents to verify whether the requirements of the Companies Act 2006 requirements have been duly complied with. Note: Per S15 CA 2006, once the certificate of incorporation has been issued, this will serve as conclusive evidence that the relevant stipulations of the Companies Act 2006, have been fulfilled.

![ACCA Prezentare ACCA RO Studenti 2013 [Compatibility Mode]](https://img.pdfslide.us/doc/110x75/553edd7e550346096e8b462e/acca-prezentare-acca-ro-studenti-2013-compatibility-mode.jpg)