Embed Size (px)

Citation preview

How to Make Successful Private Equity Investments in China and in Europe?

SHANGHAI / PARIS EUROPLACE Financial Forum1 December 2010

LA COMPAGNIE FINANCIÈRE EDMOND DE ROTHSCHILD 2

Agenda

1. The Private Equity industry in China and in Europ e

2. How to create value in a time that “Everybody is P Eing”

LA COMPAGNIE FINANCIÈRE EDMOND DE ROTHSCHILD 3

Edmond de Rothschild Group: A major player in Private Equity

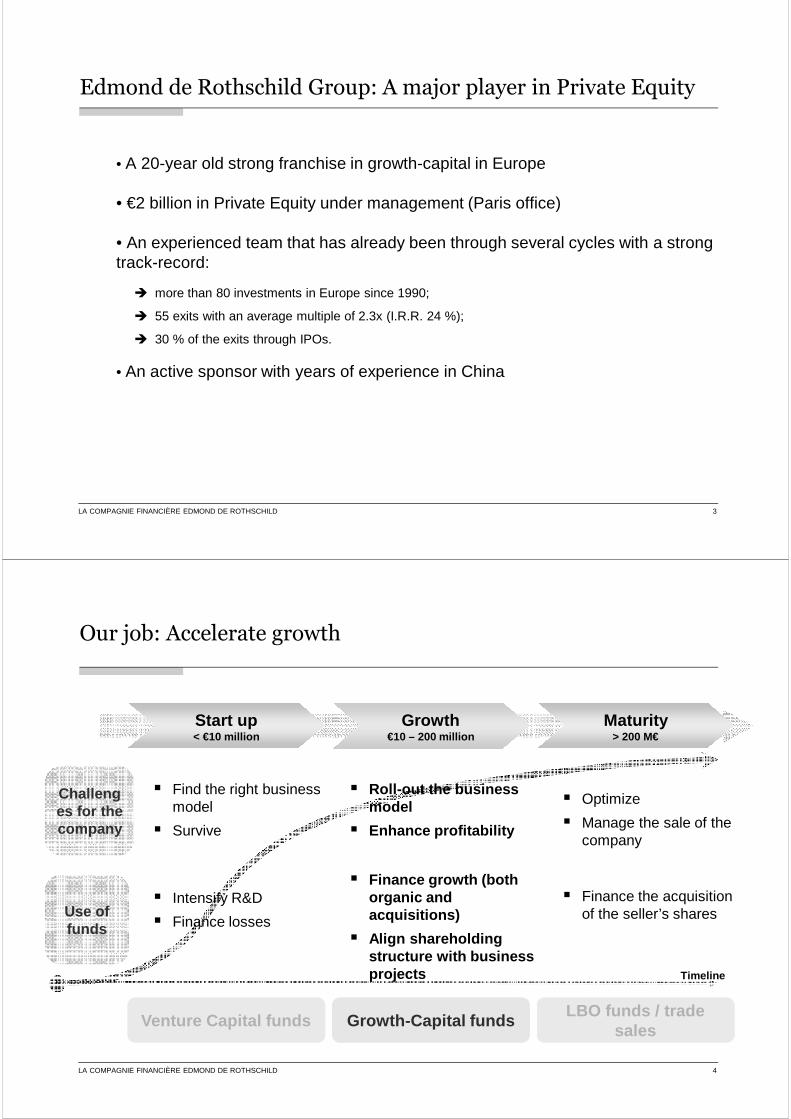

• A 20-year old strong franchise in growth-capital in Europe

• €2 billion in Private Equity under management (Paris office)

• An experienced team that has already been through several cycles with a strong track-record:

� more than 80 investments in Europe since 1990;

� 55 exits with an average multiple of 2.3x (I.R.R. 24 %);

� 30 % of the exits through IPOs.

• An active sponsor with years of experience in China

LA COMPAGNIE FINANCIÈRE EDMOND DE ROTHSCHILD 4

Challenges for the company

Use of funds

Venture Capital fundsVenture Capital fundsLBO funds / trade

salesLBO funds / trade

salesGrowth-Capital fundsGrowth-Capital funds

� Roll-out the business model

� Enhance profitability

� Finance growth (both organic and acquisitions)

� Align shareholding structure with business projects

� Find the right business model

� Survive

� Intensify R&D

� Finance losses

� Optimize

� Manage the sale of the company

� Finance the acquisition of the seller’s shares

Timeline

Start up< €10 million

Growth€10 – 200 million

Maturity> 200 M€

Our job: Accelerate growth

LA COMPAGNIE FINANCIÈRE EDMOND DE ROTHSCHILD 5

Chinese fast-growing SMEs have 3 main needs:

• They seek capital to allow them to:

� expand along with the steady growth of the Chinese economy;

� face the difficulty of accessing bank loans and financial markets.

• They seek expertise in adopting international management standards (governance, risk management, accounting, etc.)

• They seek the recognition associated with the entry of a premier international investor

Edmond de Rothschild Private Equity China: A response to the companies’ needs

LA COMPAGNIE FINANCIÈRE EDMOND DE ROTHSCHILD 6

European Private Equity industry vs. Chinese PE industry (1/4)

European PE investments

Source: EVCA – Analytics for 2007 - 2009, Thomson Reuters – Analytics for 2000 - 2007

Chinese PE investments

• During the 2005 – 2007 PE surge, the size of deals grew significantly as the number of investments strongly decreased• The PE industry proved very sensitive to the crisis and the economic splashdown in Europe, yet starting a slight recovery in H1 2010

Source: China Venture

• Chinese PE industry has appeared to be more resilient to the crisis than the European industry (-42% in amounts in 2009 vs -57% in Europe)• After the lacklustre 2009 , especially in the first half of the year, the PE market is showing ongoing signs of recovery in terms of number of investments and invested amounts

Number of investments and invested amounts (EUR in billions)

Number of investments and invested amounts (USD in billions)

LA COMPAGNIE FINANCIÈRE EDMOND DE ROTHSCHILD 7

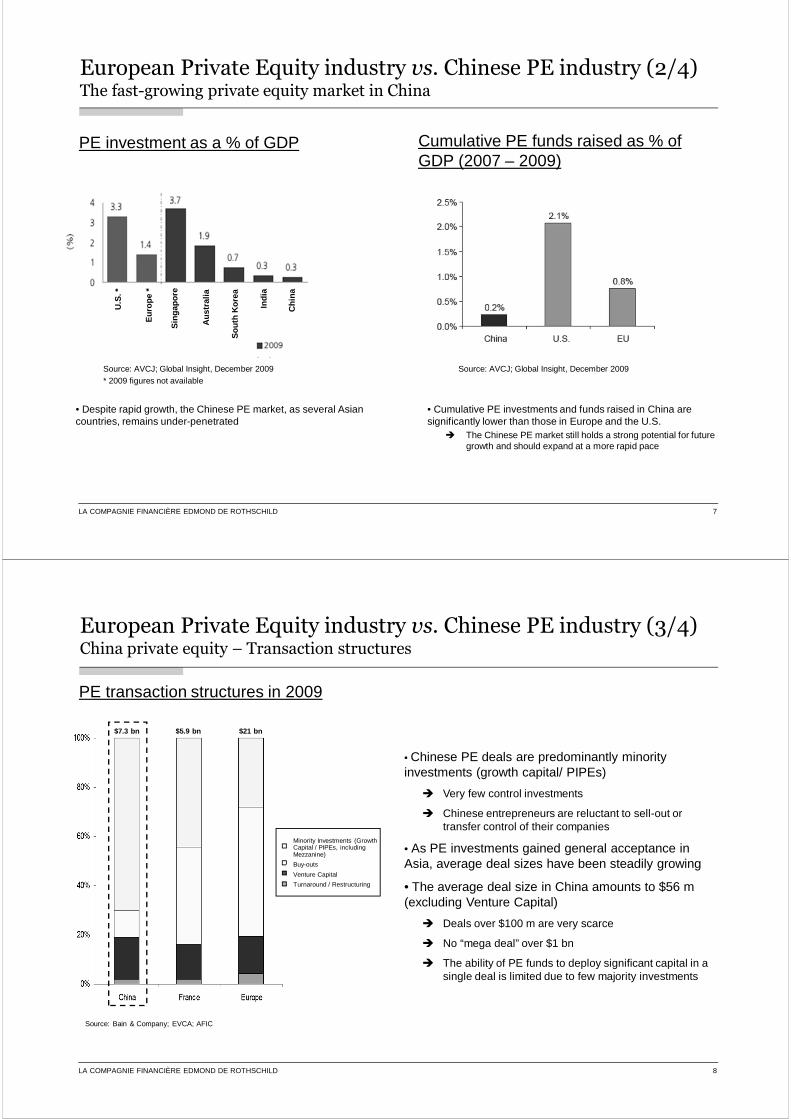

European Private Equity industry vs. Chinese PE industry (2/4)The fast-growing private equity market in China

Source: AVCJ; Global Insight, December 2009* 2009 figures not available

U.S

. *

Eur

ope

*

Sin

gapo

re

Aus

tral

ia

Sou

th K

orea

Indi

a

Chi

na

PE investment as a % of GDP Cumulative PE funds raised as % of GDP (2007 – 2009)

• Despite rapid growth, the Chinese PE market, as several Asian countries, remains under-penetrated

• Cumulative PE investments and funds raised in China are significantly lower than those in Europe and the U.S.

� The Chinese PE market still holds a strong potential for future growth and should expand at a more rapid pace

Source: AVCJ; Global Insight, December 2009

LA COMPAGNIE FINANCIÈRE EDMOND DE ROTHSCHILD 8

European Private Equity industry vs. Chinese PE industry (3/4)China private equity – Transaction structures

Source: Bain & Company; EVCA; AFIC

$7.3 bn $5.9 bn

• Chinese PE deals are predominantly minority investments (growth capital/ PIPEs)

� Very few control investments

� Chinese entrepreneurs are reluctant to sell-out or transfer control of their companies

• As PE investments gained general acceptance in Asia, average deal sizes have been steadily growing

• The average deal size in China amounts to $56 m (excluding Venture Capital)

� Deals over $100 m are very scarce

� No “mega deal” over $1 bn

� The ability of PE funds to deploy significant capital in a single deal is limited due to few majority investments

PE transaction structures in 2009

$21 bn

Minority Investments (Growth Capital / PIPEs, including Mezzanine)

Buy-outs

Venture Capital

Turnaround / Restructuring

LA COMPAGNIE FINANCIÈRE EDMOND DE ROTHSCHILD 9

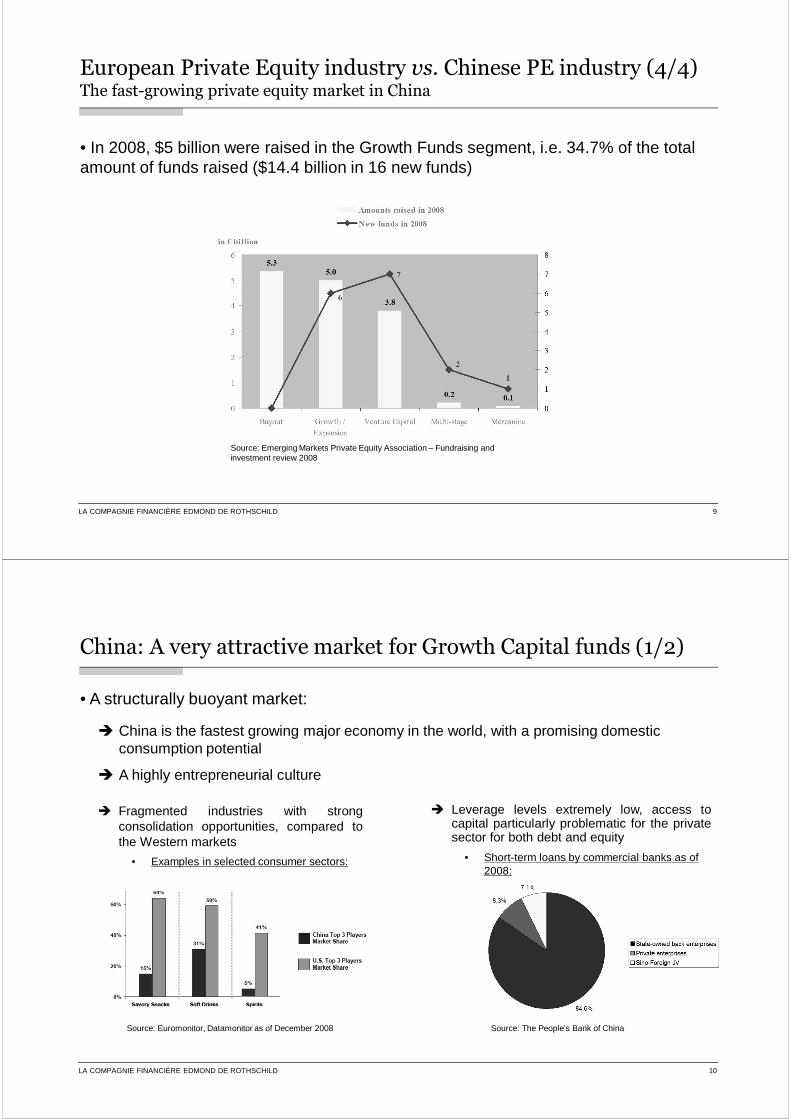

• In 2008, $5 billion were raised in the Growth Funds segment, i.e. 34.7% of the total amount of funds raised ($14.4 billion in 16 new funds)

European Private Equity industry vs. Chinese PE industry (4/4)The fast-growing private equity market in China

Source: Emerging Markets Private Equity Association – Fundraising and investment review 2008

LA COMPAGNIE FINANCIÈRE EDMOND DE ROTHSCHILD 10

• A structurally buoyant market:

� China is the fastest growing major economy in the world, with a promising domestic consumption potential

� A highly entrepreneurial culture

China: A very attractive market for Growth Capital funds (1/2)

� Fragmented industries with strongconsolidation opportunities, compared tothe Western markets

• Examples in selected consumer sectors:

� Leverage levels extremely low, access tocapital particularly problematic for the privatesector for both debt and equity

• Short-term loans by commercial banks as of 2008:

Source: Euromonitor, Datamonitor as of December 2008 Source: The People’s Bank of China

LA COMPAGNIE FINANCIÈRE EDMOND DE ROTHSCHILD 11

• Entrepreneurs and funds clearly privilege IPO exits due to higher valuations in the public markets

China: A very attractive market for Growth Capital funds (2/2)

0

2

4

6

2005 2006 2007 2008 2009 2010YTD

Average Time (Years) Between First Round Fund Raising and IPO of PE/VC

Backed Chinese Companies

Local Exchange HK Exchange US Exchange

� Exit opportunities in local market are becoming more and more attractive

� # of 3 years needed for PE and for VC to realize return on investment

� 73 PE- / VC-backed Chinese companies went public in 2009 and raised $14 billion

Source: China Venture, September 2010

LA COMPAGNIE FINANCIÈRE EDMOND DE ROTHSCHILD 12

Recent trends for Private Equity exits

• Exit strategies vary according to regions:

� IPOs exits in Asia have been standing up to the crisis (mainly in the Shanghai, Hong Kong and Australian stock markets), showing strong progression in 2009

� Strategic sales are more common in America and secondary sales in Europe

Secondary sales: 41,2% Strategic sales:

55,1 %

IPOs:40,7%

PE exit trends since 2006:

Source: Ernst & Young – Global IPO Trends 2010

LA COMPAGNIE FINANCIÈRE EDMOND DE ROTHSCHILD 13

What a (public) company may learn from Private Equity

• During the crisis, PE posted limited gains in terms of (i) enterprise value, (ii) profits and (iii) productivity

� Between 2004 and 2009, Thomson Reuters Private Equity Index gained 6%, when the S&P Index dropped by around 1.5%

� Corporate experience shows PE constitutes an enriching step for a company:

• An active, efficiency-oriented ownership that…

• …optimizes the organization through cost cutting, business plan challenging, etc…

• …and offers attractive, performance-based incentives to management.

Source: Ernst & Young – How do private equity investors create value? A global study of 2007 exits

LA COMPAGNIE FINANCIÈRE EDMOND DE ROTHSCHILD 14

Agenda

1. The Private Equity industry in China and in Europ e

2. How to create value in a time that “Everybody is P Eing”

LA COMPAGNIE FINANCIÈRE EDMOND DE ROTHSCHILD 15

Edmond de Rothschild in China

15

• In 1993, Edmond de Rothschild began to invest in the secondary market of Greater China

• In 2006, obtained the QFII license

• In 2008 and 2010 respectively, equity participation in CNOOC Fund Management

• In 2008, became the strategic partner of Bank of China in Private Banking

• In 2008, affiliate company MSH Insurance acquired the largest international healthcare management company in China

• Invested in Pacific Insurance, Belle, Jade Bird IT training, etc.

• Invested in the secondary market including Min Sheng Bank, Alibaba, New Hope, Ling Rui, Shen Changcheng, Zhong Liang Tunhe etc.

LA COMPAGNIE FINANCIÈRE EDMOND DE ROTHSCHILD 16

How can we create return for investors in a time that “Everybody is PEing” in China?

LA COMPAGNIE FINANCIÈRE EDMOND DE ROTHSCHILD 17

Investment Philosophy

17

• Focus on people

• Value-added: to provide effective value-add services to portfolio companies for them to grow in a faster and healthier way, thus creating sustainably higher return to the investors, for example:

� Consumer & Service - “Edmond de Rothschild” itself represents a “high-end” image

� Financial Service - resources & network from 250 years of financial heritage

� CleanTech - affiliated cleantech operations bring in invaluable expertise and experience

• As a valuable and stable partner, helps portfolio companies become the “STAR” of tomorrow

• Continue the innovation philosophy (Edmond de Rothschild was early shareholder in ClubMed, etc.)

• Multiple exit strategy (50% IPO and 50% M&A)

LA COMPAGNIE FINANCIÈRE EDMOND DE ROTHSCHILD 18

� Platform: Edmond de Rothschild has great networks in many industries across the globe. Synergy with

the global resource and different teams, different angles & ideas bring in unique value-add

� Network: Not limited to introducing board members, high-level managers, also bring in brand value and

endorsement, channels, new markets, strategic partners and other valuable networks such as law firms, auditing firms, investment banks, commercial banks, government relations and investors etc

� Exit Channel: More exit options than the general financial investors

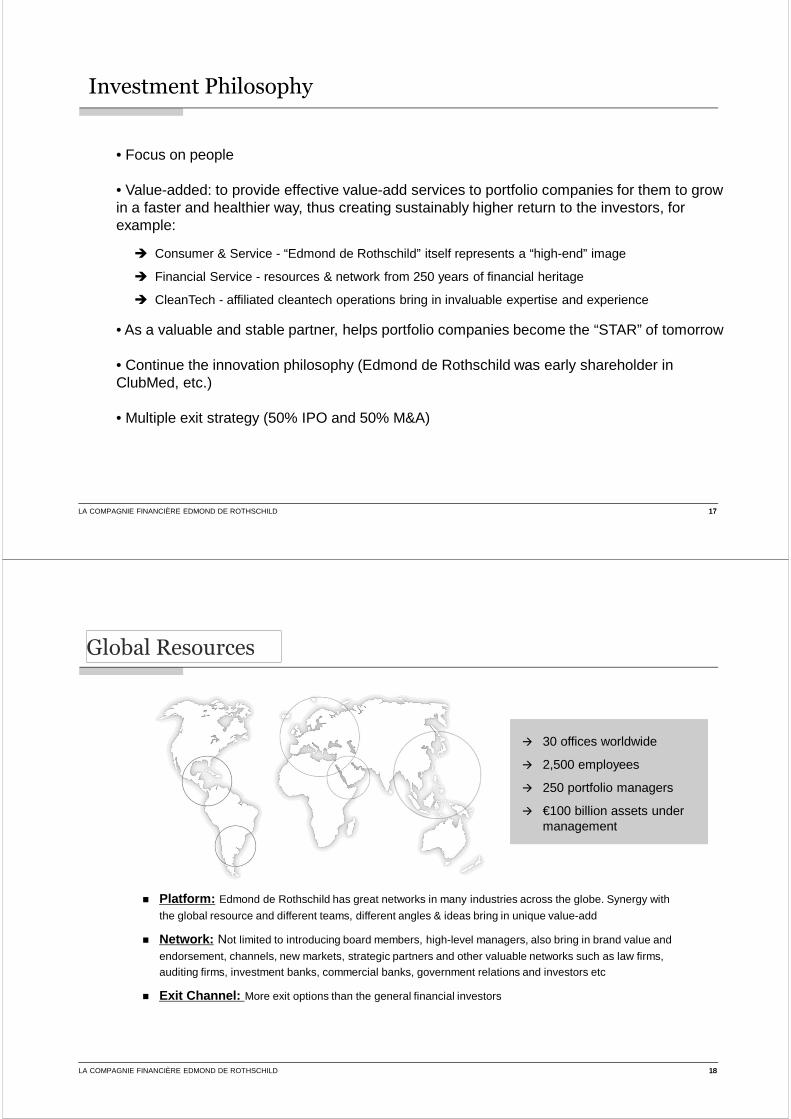

Global Resources

18

� 30 offices worldwide

� 2,500 employees

� 250 portfolio managers

� €100 billion assets under management

LA COMPAGNIE FINANCIÈRE EDMOND DE ROTHSCHILD 19

� Global prestige and brand image, and a long- run reputation

� Seasoned worldwide professional teams, industry expertise, customer resources and highly reliable investor relationship

� Broad reliable local network with government, entrepreneurs and institutes

� Experienced team with solid track record and deep industry knowledge

� Rich post-management experience and know-how to provide effective value-add to portfolio companies

� Proven execution capability

� Global network synergy and support

� Helps build management team, introduce business partners and optimize company operation

� Helps build international team and expand international market

� Abundant strategic partner resources, with greater access to financial leverage

� On-going financing support to portfolio companies, assist in choosing the right strategic partner, IPO or M/A

Global Resources

Edmond de Rothschild China fund brings not only cap ital, but also reputation, resources and effective value- add

Local team with successful track

record

+x

Differentiation: a comprehensive value-add platform

19

LA COMPAGNIE FINANCIÈRE EDMOND DE ROTHSCHILD 20

Value-add I — Financial Services

20

Value-add from the Edmond de Rothschild Group

• The Group represents a name that is of family origin, its brand has a unique reputation in the international financial world for more than 250 years. In the longest period, Rothschild stands for excellence, stability, professional and innovation

• The Group always develops and offers a very broad product range, and to anticipate product life cycles covering all asset classes. With the long-term excellent returns, it has a large group of high-end customers including institutions and private clients

• 250 years experience and the Group’s global financial network bring in tremendous values– whether in company assessment or providing the portfolio companies with value-added services in business expansion, access to capital, network and geographical expansion, etc.

LA COMPAGNIE FINANCIÈRE EDMOND DE ROTHSCHILD 21

Value-add II — Consumer & Service

21

• The Group’s name itself represents a luxury brand, along with its long-term high-end private banking clients

• Owns top red wine worldwide brands

• Affiliated with various luxury brands including the super-luxury “Gitana”

• Great relationship with leading consumer brand owners in Europe

• Strategic partner with leading sales & marketing solution providers in China, focusing on brand building and planning, channel strategy and expansion etc.

• Helps build strategic partnership with the European market, M/A with European brands, reference check with successful business models overseas, and recruitment of senior executives from top consumer brands

• Abundant resources pave the way for high-speed growth of the portfolio companies

LA COMPAGNIE FINANCIÈRE EDMOND DE ROTHSCHILD 22

Value-add III — CleanTech

22

• Affiliated leading cleantech companies to be able to assess companies or technologies in full spectrum including energy, climate, resources, toxicity and biodiversity

• Sectors covered include: environmental services, industrials, power and energy, clean energy, infrastructure, transportation, agriculture and so on- has served more than 100 reputable companies to date

• Developed business in France, US, Australia, China, Japan, Korea, Europe, North America, South America and Asia

• With 30 experts focusing on more than 10 sectors, high value-add in project evaluation, technology support and sustainable development appraisals; linking the Chinese companies to their overseas counterparts, providing access to network, sales & marketing channel including M&A opportunities

• Already signed with Maldives to support its cleantech initiatives

LA COMPAGNIE FINANCIÈRE EDMOND DE ROTHSCHILD 23

Investment Criteria

23

• Seasoned entrepreneurs and management team with track record

• Fast growing industries

• Fast growing and financially healthy companies with a leading position or with the potential to become the industry leader

• Mature and scalable business model

• High entry barrier: by technologies and/or by business model

• Capability of innovation:based on technologies and/or business model

• Healthy financial foundation and high gross margin

• Clear exit strategy

LA COMPAGNIE FINANCIÈRE EDMOND DE ROTHSCHILD 24

Portfolio Company – recent examples (1/2)

SINODIS

• Become the market No. 1 from the No. 2 position before the investment

• Value-add from the Fund:

� Helps bring in top global brands

� Helps build the corporate image

� Helps improve the management quality: the exclusive provider of western food for Beijing 2008 Olympics, best-in-class cold-chain management and SAP in the industry, certified by ISO22000:2005 for food safety

� Achieved growth rate >50% successively

LA COMPAGNIE FINANCIÈRE EDMOND DE ROTHSCHILD 25

Portfolio Company – recent examples (2/2)

ELSKER Mother & Baby

• Become the market No.2 after investment (after Johnson &Johnson)

• Value-add from the Fund:

� Helps build the high-quality image

� Helps build strategic partnership with leading sales & marketing firm to launch new marketing campaign

� Helps build the multi-brand strategy to lower the branding risk

� Helps improve management quality, the recipient of various awards: “top consumer satisfaction & choice” award, ”China Quality 500”, “Top 10 landmark brands in Mother & Baby care products” and “The nominated brand for purchasing” certificate issued by the Association of China Excellency product purchase for Mother & Children

� Achieved growth rate >60% successively

LA COMPAGNIE FINANCIÈRE EDMOND DE ROTHSCHILD 26

Investment Sectors

Machinery

� Strong market demand, consolidation opportunities � Predictable market cycle and fast demand growth� European network brings in additional value

Traditional High-Growth

Main Focus

Others

CleanTech� Global goal of low carbon

� Affiliate companies helps industry upgrade and create value � Huge market, strong demand and healthy profitability

� Fixed asset investment continues to drive investment opportunity� The trend of replacing imported machinery is inevitable� International expansion highly scalable, alongside M&A opportunities

26

Financial Service� Gradually opening industry, high-grow opportunity� Healthy cash flow� Global network and resources lead to more value-add

HealthCare� Huge market size and fast growth driven by demand� Trend of domestic products replacing the imported ones� Edmond de Rothschild European Funds bring in additional value

� New consumer behaviors driven by the rise of middle class� Entry barrier by brand and product innovation� European industry resources/channel bring more exit options

Consumer & Service

LA COMPAGNIE FINANCIÈRE EDMOND DE ROTHSCHILD 27

Risk Management

27

• Investment business is a balance between risk and return

• Most of the risks can be mitigated by effective management and control by experienced management

• Good investment is to effectively lower the risks in exchange for higher premium to achieve higher investment return

LA COMPAGNIE FINANCIÈRE EDMOND DE ROTHSCHILD 28

Due Diligence and Investment Decision

Making

� Deep industry knowledge to understand industry trend and growth opportunity

� Discover companies with high investment value

� Swift judgment on the growth potential and risk assessment of target companies

Deal Structuring

� Legal, executable, and controllable equity structure

� Design protection mechanism for key risks

� Optimized transaction structure towards a win-win situation

Post-Investment Management

� Mutual trust based on alignment of strategy and interest of all parties

� Best-in-class management piloted by corporate governance of the board

� Company value creation accelerated by value-add services

Key Factors of Risk Control

28

LA COMPAGNIE FINANCIÈRE EDMOND DE ROTHSCHILD 29

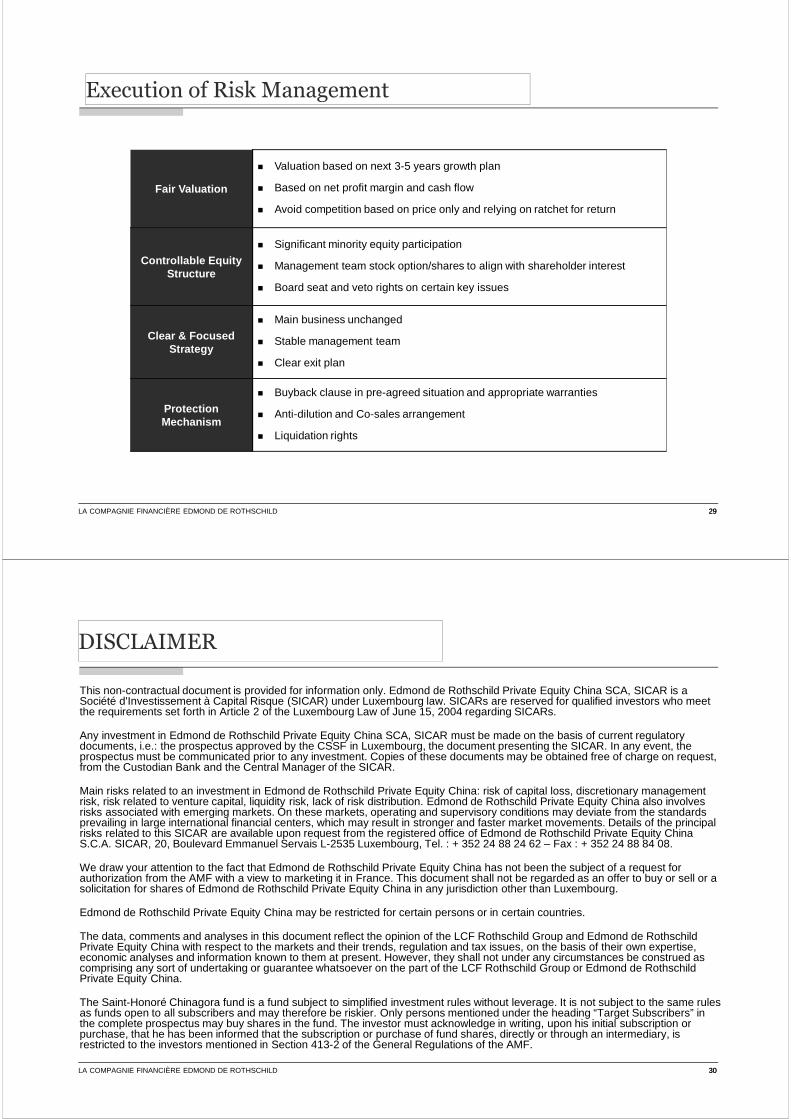

Execution of Risk Management

Fair Valuation

� Valuation based on next 3-5 years growth plan

� Based on net profit margin and cash flow

� Avoid competition based on price only and relying on ratchet for return

Controllable Equity Structure

� Significant minority equity participation

� Management team stock option/shares to align with shareholder interest

� Board seat and veto rights on certain key issues

Clear & Focused Strategy

� Main business unchanged

� Stable management team

� Clear exit plan

Protection Mechanism

� Buyback clause in pre-agreed situation and appropriate warranties

� Anti-dilution and Co-sales arrangement

� Liquidation rights

29

LA COMPAGNIE FINANCIÈRE EDMOND DE ROTHSCHILD 30

This non-contractual document is provided for information only. Edmond de Rothschild Private Equity China SCA, SICAR is a Société d'Investissement à Capital Risque (SICAR) under Luxembourg law. SICARs are reserved for qualified investors who meet the requirements set forth in Article 2 of the Luxembourg Law of June 15, 2004 regarding SICARs.

Any investment in Edmond de Rothschild Private Equity China SCA, SICAR must be made on the basis of current regulatory documents, i.e.: the prospectus approved by the CSSF in Luxembourg, the document presenting the SICAR. In any event, the prospectus must be communicated prior to any investment. Copies of these documents may be obtained free of charge on request,from the Custodian Bank and the Central Manager of the SICAR.

Main risks related to an investment in Edmond de Rothschild Private Equity China: risk of capital loss, discretionary managementrisk, risk related to venture capital, liquidity risk, lack of risk distribution. Edmond de Rothschild Private Equity China also involves risks associated with emerging markets. On these markets, operating and supervisory conditions may deviate from the standardsprevailing in large international financial centers, which may result in stronger and faster market movements. Details of the principal risks related to this SICAR are available upon request from the registered office of Edmond de Rothschild Private Equity ChinaS.C.A. SICAR, 20, Boulevard Emmanuel Servais L-2535 Luxembourg, Tel. : + 352 24 88 24 62 – Fax : + 352 24 88 84 08.

We draw your attention to the fact that Edmond de Rothschild Private Equity China has not been the subject of a request for authorization from the AMF with a view to marketing it in France. This document shall not be regarded as an offer to buy or sell or a solicitation for shares of Edmond de Rothschild Private Equity China in any jurisdiction other than Luxembourg.

Edmond de Rothschild Private Equity China may be restricted for certain persons or in certain countries.

The data, comments and analyses in this document reflect the opinion of the LCF Rothschild Group and Edmond de Rothschild Private Equity China with respect to the markets and their trends, regulation and tax issues, on the basis of their own expertise, economic analyses and information known to them at present. However, they shall not under any circumstances be construed as comprising any sort of undertaking or guarantee whatsoever on the part of the LCF Rothschild Group or Edmond de Rothschild Private Equity China.

The Saint-Honoré Chinagora fund is a fund subject to simplified investment rules without leverage. It is not subject to the same rules as funds open to all subscribers and may therefore be riskier. Only persons mentioned under the heading “Target Subscribers” in the complete prospectus may buy shares in the fund. The investor must acknowledge in writing, upon his initial subscription or purchase, that he has been informed that the subscription or purchase of fund shares, directly or through an intermediary, isrestricted to the investors mentioned in Section 413-2 of the General Regulations of the AMF.

DISCLAIMER

30