Embed Size (px)

Citation preview

How to Plan to Give:

“The Future of Taxwise Philanthropy”

NCF Raleigh Plan to Give Conference

September 25, 2014

Don Etheridge, JD, LLM, CPAGift Planning AttorneyNational Christian Foundation

Grow giving by converting tax dollars to giving dollars.

Taxes

GivingLifestyle/ Savings

Give more, pay less tax

Tax Benefit #1: Enjoy an immediate charitable income tax deduction for the gifted property.

Tax Benefit #2: Reduce tax on income and proceeds of sale of the gifted property

2

3

ProblemsSize of Government:

4

ProblemsSize of Debt:

5

Growing Tax Inefficiencies:

1. 3% Floor (Pease provision)

2. 3.8% Obamacare tax on TII (AGI)

3. Proposed Cap on Charitable Deductions

4. Camp Reform proposals

a. Basis deduction on property gifts

b. Deduction ceilings lowered (50%/30%)

5. Denial of Exempt Status & Charitable Deduction

a. Discrimination against protected class

b. ‘Separation of church and state’ doctrine

Your Estate

Charity Family and Friends

Taxes

Giving it all away in the end …

6

Planning Strategies:

FIRST: Give ahead now - max 50% limit withDAF stockpile, including “30% of AGI” giving

SECOND: Off-line giving arrangements- income not reported by Donor- income exempted, deferred or taxed

at lower rate

7

1. Give Cheerfully & Generously

2. No estate/gift tax

3. No net Capital Gain tax

4. Lifestyle limited income tax

Gift Planning Fundamentals

8

Offline: Maximize charitable giving, minimize taxes

1. Real Estate Gifts

2. Intellectual Property Gifts

3. Faucet CRUT

4. Non-Grantor CLAT

5. Operating Business DAF

6. Other

9

10

NCF Giving

Fund

Marketable Securities Real Estate

Oil and Gas Intellectual Property

Interest, Dividends, and Capital Gains

Royalties Royalties

Rental Income

Non-UBTI Producing Assets

11

Offline: Maximize charitable giving, minimize taxes

1. Real Estate Gifts

2. Intellectual Property Gifts

3. Faucet CRUT

4. Non-Grantor CLAT

5. Operating Business DAF

6. Other

Donor Property: $1M Gift of R.P. LP

12

Obtain tax deduction on current value of investment property

Lower effective tax rate Avoid future taxation on

charitably held LP int. (income & estate)

Control of invested assets

Preserve charitable advisory rights

Obtain tax deduction on current value of investment property

Lower effective tax rate Avoid future taxation on

charitably held LP int. (income & estate)

Control of invested assets

Preserve charitable advisory rights

RP LP1% voting99% non-

voting

DonorProperty

Donor DAF

Parents (during their lifetimes)

Children (thereafter)

Concept Concept

BusinessLLC

Control-Family

Steps1. Create/fund Invest LP w/Prop.& cash2. Transfer desired int. to Charity3. LP leases property to Business4. Distributions/proceeds to DAF shared w/charity

1

2

4

3

50% interest($1,000,000+) Charities

Property &Cash

$2,000,000+ Lease of prop.,

Proposed

Offline Advantage

Obamacare Tax: 3.8% on AGI not TI

50% Ceiling: Full taxation on Giving beyond

Deductibility cap: 28% proposed

13

Current

Current Deduction of Gifted Interest

No Obamacare Tax: 3.8% on AGI not TI

100% deductibility ‘beyond 50%’

Dealing with Debt

PropertyOwner

GP 1%

Problem with Debt: 1. Lower Deduction2. Debt Relief Income to Giver3. Unrelated Debt Financed Income to Charity

Solutions:

Subordinated Leasing:

TenantLand Lease(subordinated)

Charity Int.

Subordinated Lending:

DevCo

Lender

Investors

OwnerMezz Loan

(subordinated)

Charity Int.

DevCo

Lender

Investors

Property Tenant

14

15

Pre-Sale Gift of Property Interest

The Smiths

Smith Giving Fund

$700,000

20%

Smith CRT

$2,100,000

60%

Smith Family

$700,000

20%

Charities / Ministries / Churches $157,500 to Smiths for LifeAt Death to Charity

Tax Deduction: $700,000 Tax Deduction: $538,251

16

Offline: Maximize charitable giving, minimize taxes

1. Real Estate Gifts

2. Intellectual Property Gifts

3. Faucet CRUT

4. Non-Grantor CLAT

5. Operating Business DAF

6. Other

17

Gift Of IP Interest

IP COLLC

OP CO, LLC

GIFT Fund

Giver (during lifetime)

Children / Family (thereafter)

Obtain deduction(s) for gift of IP Royalty payments

Avoid tax on allocable income

Lower taxes allow for greater giving

Charitable advisory rights

Obtain deduction(s) for gift of IP Royalty payments

Avoid tax on allocable income

Lower taxes allow for greater giving

Charitable advisory rights

Concept Concept

Charities

Advisory Control-Family

Steps1. OP CO assigns royalty income producing IP to IP CO, LLC2. Portion of IP interest shared with Gift Fund3. Portion of Royalty income distributed to Gift Fund4. Gift Fund gives to ‘advised’ charities

1

2

3

25% interest

4

18

Offline: Maximize charitable giving, minimize taxes

1. Real Estate Gifts

2. Intellectual Property Gifts

3. Faucet CRUT

4. Non-Grantor CLAT

5. Operating Business DAF

6. Other

FAUCET CRUT(charitable remainder unitrust)

• Mom & Dad have O&G Royalty Interest producing significant income which they do not plan to sell.

• Minimize tax… Invest proceeds… Maintain lifestyle • Flexible charitable giving… give to charity at death• $10M Value• $1.25M annual income (rise then fall)• 43% taxation…. 10% giving to charity

• Faucet Trust allows them to lower taxation to a level commensurate with lifestyle & choose how much to share with charity &/or take in for future lifestyle purposes.

19

The Charitable Remainder Unitrust

Giving Fund

CharitableRemainder

Trust

Asset

after death

5%+ annual payment during life

-Deduction- Gain deferral on sale- Tax exempt trust

20

The Faucet Charitable Remainder Unitrust

Asset

LLC

Giving Fund

CRT

- Deduction- Gain deferral on sale- Distribute as desired- Stockpile tax free- Diversify LLC investments- Discretionary gifts to charity- Exceed 50% AGI limit- Future deduction for gift of income interest

Buyer

up to 90%of income

10%+ income

21

22

Offline: Maximize charitable giving, minimize taxes

1. Real Estate Gifts

2. Intellectual Property Gifts

3. Faucet CRUT

4. Non-Grantor CLAT DAF

5. Operating Business

6. Other

Non-Grantor Charitable Lead Trust

CharitableLead Trust

After Death

Annual Lead Payment to Charity

During Life

Income Producing

Asset

Giver

NCF Giving

Fund

Income

Remainder Interest to Children

If charitable lead payment is equal to or greater than income, CLT avoids income tax, essentially providing a 100% AGI charitable deduction.

23

24

Offline: Maximize charitable giving, minimize taxes

1. Real Estate Gifts

2. Intellectual Property Gifts

3. Faucet CRUT

4. Non-Grantor CLAT

5. Operating Business DAF

6. Other

25

$1MIncome

$401,400Taxes

$498,600 $100,000

$10M Business

Current Situation: 10% AGI Giving

Lifestyle, Investment, etc.

Charity

26

$1MIncome

$267,600Taxes

$133,800 PersonalIncome Tax Savings$133,800 Personal

Income Tax Savings

$300,000(30% of AGI)

Solution: 10% to 40% AGI Giving

$10M Business

NCF Giving

Fund

NCFGiving Fund

ProposedBusiness

Interest Gift

$632,400 $100,000

Lifestyle, Investment, etc.

Charity

27

$1MIncome

$223,000Taxes

$178,400 PersonalIncome Tax Savings$178,400 Personal

Income Tax Savings

Solution: 40% to 50% AGI Giving

$10M Business

NCF Giving

Fund

NCFGivingFund$300,000

(30% of AGI)

Business Interest Gift

Cash Gift from Tax Savings

$100,000(10% of AGI)

$577,000 $200,000

Lifestyle, Investment, etc.

Charity

28

Proposed**

Comparison Results

Taxes:

Charity:

Family:

$401,400

$100,000

$499,000

Results:

$223,000

$200,000($300k stock)

$577,000

Current*

*$1M Income; 10% cash to Charity**3% gift of Stock to Charity; 20% cash to Charity

29

Offline: Maximize charitable giving, minimize taxes

1. Real Estate Gifts

2. Intellectual Property Gifts

3. Faucet CRUT

4. Non-Grantor CLAT

5. Operating Business DAF

6. Other

30

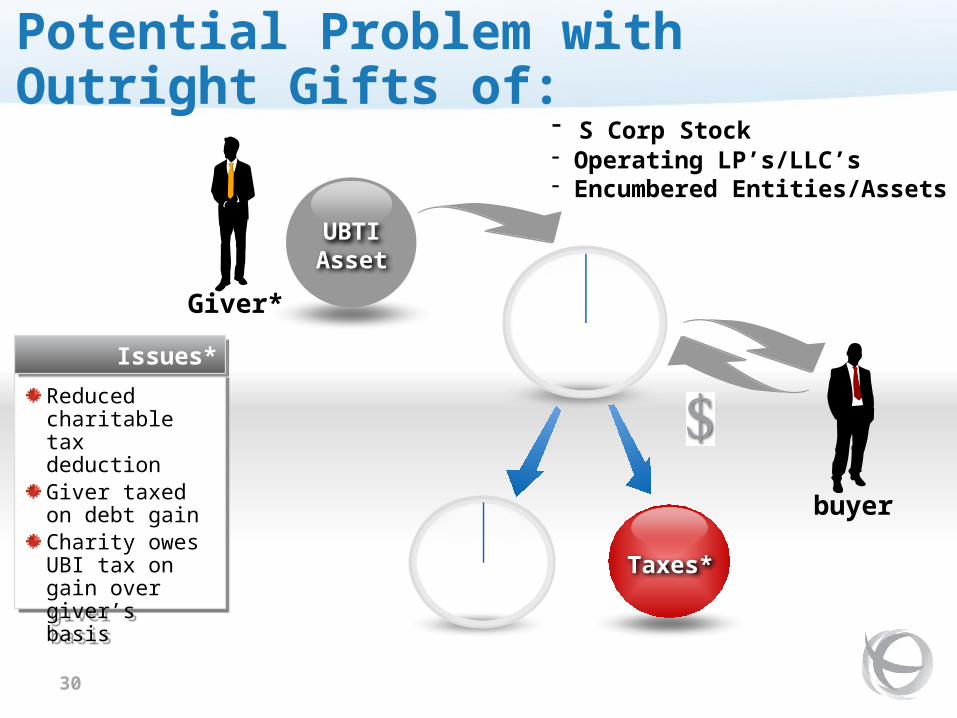

Potential Problem with Outright Gifts of:

Giver*

Reduced charitable tax deductionGiver taxed on debt gainCharity owes UBI tax on gain over giver’s basis

Reduced charitable tax deductionGiver taxed on debt gainCharity owes UBI tax on gain over giver’s basis

Issues* Issues*

buyer

UBTIAsset

Taxes*

Giving Fund

Charity

- S Corp Stock- Operating LP’s/LLC’s- Encumbered Entities/Assets

31

Benefits of Transfer to Charitable Gift Annuity

Giver

Tax upon gift &/or sale reduced 70-80%Gain to Giver on annuity portion is deferred until payments beginCharity gets stepped-up basis on annuity portionMost UBI tax to charity is avoidedTax deduction for charitable gift portionMore potentially available for charity

Tax upon gift &/or sale reduced 70-80%Gain to Giver on annuity portion is deferred until payments beginCharity gets stepped-up basis on annuity portionMost UBI tax to charity is avoidedTax deduction for charitable gift portionMore potentially available for charity

Benefits Benefits

buyer

UBTIAsset

Giver

GiftAnnuity

Charity

- S Corp Stock- Operating LP’s/LLC’s- Encumbered Entities/Assets Annuity/Sale 75%+/-

Gift 25%+/-

32

Income from Charitable Gift Annuity

Taxes

CharityGift

Annuity

giver

Giving Fund

Deferred income from CGA taxed according to its initial characterPayments may be deferred (increased for each year deferred)Additional charitable tax deduction for full annuity value if Giver decides to gift CGA contract in the future

Deferred income from CGA taxed according to its initial characterPayments may be deferred (increased for each year deferred)Additional charitable tax deduction for full annuity value if Giver decides to gift CGA contract in the future

Benefits Benefits

deduction

33

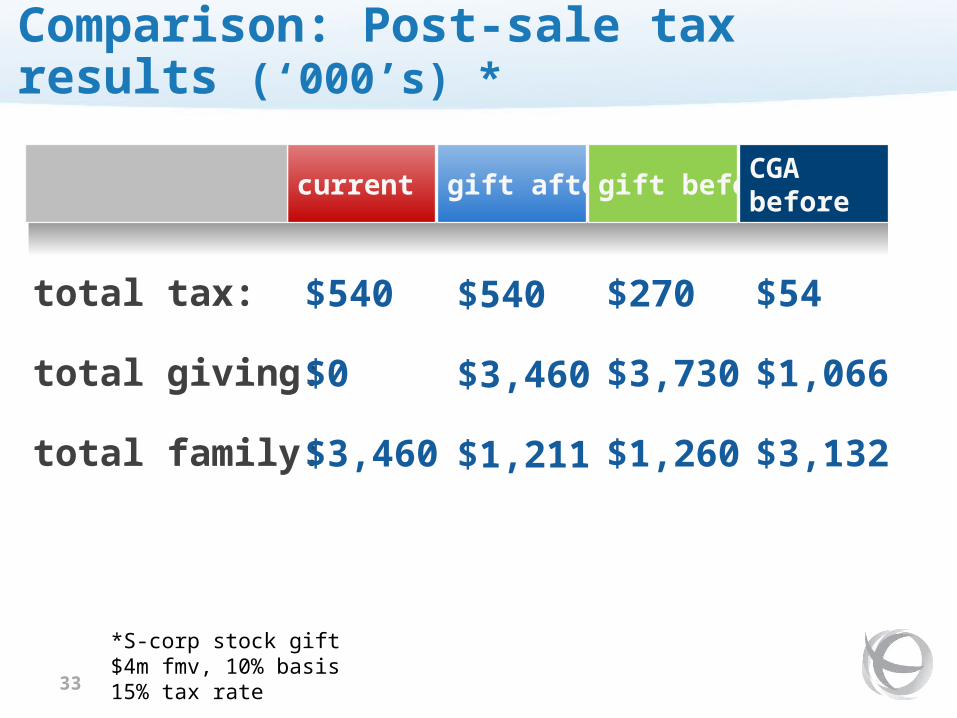

Comparison: Post-sale tax results (‘000’s) *

total tax:

total giving:

total family:

$54

$1,066

$3,132

gift aftercurrent gift beforeCGA before

$540

$0

$3,460

$540

$3,460

$1,211

$270

$3,730

$1,260

*S-corp stock gift$4m fmv, 10% basis15% tax rate

34

After Death• Assets distributed to charity• Tax deferred income becomes

tax avoided

During Life• Assets available to giver

(taxed upon distribution)• Income otherwise deferred

Marketable Securities

Giver

NCF Giving

Fund

Private Placement Deferred Annuity

PrivatePlacementDeferredAnnuity

35

Offline: Maximize charitable giving, minimize taxes

1. Real Estate Gifts

2. Intellectual Property Gifts

3. Faucet CRUT

4. Non-Grantor CLAT

5. Operating Business

6. Other

36

© 2014, NATIONAL CHRISTIAN FOUNDATION (NCF)

NOTE: This information is designed to provide accurate and authoritative information in regard to the subject matters covered. It is published with the

understanding that in this information, the authors are not engaged in rendering legal, accounting, or other professional services. If legal advice or other expert

assistance is required, the services of a competent professional should be sought. (From a Declaration of Principles jointly adopted by a committee of the American

Bar Association and a committee of Publishers and Associations)

Copyright and Legal Notice