Embed Size (px)

Citation preview

How to meet the challenge of

the changing environment of

banking?5th Retail Banking Forum, 1 – 2 June, 2017

BACK TO1972…

La cabina

A. Mercero – J. L. Garci: La Cabina

What does it mean?

Imre Antal

ABOUT THE NATURE OF BOXES

Efficiency in the box

CBS - The Big Bang Theory

Efficiency in the box

CBS - The Big Bang Theory

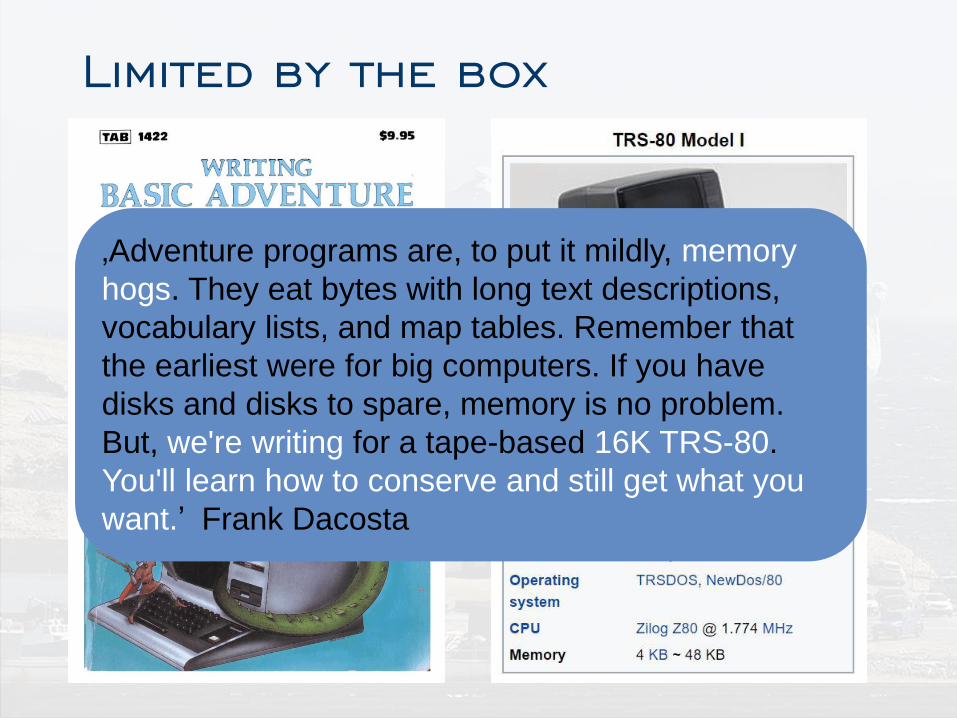

Limited by the box

‚Adventure programs are, to put it mildly, memory

hogs. They eat bytes with long text descriptions,

vocabulary lists, and map tables. Remember that

the earliest were for big computers. If you have

disks and disks to spare, memory is no problem.

But, we're writing for a tape-based 16K TRS-80.

You'll learn how to conserve and still get what you

want.’ Frank Dacosta

WHEN BOXES ARE DANGEROUS?

The Plane of Paradigm

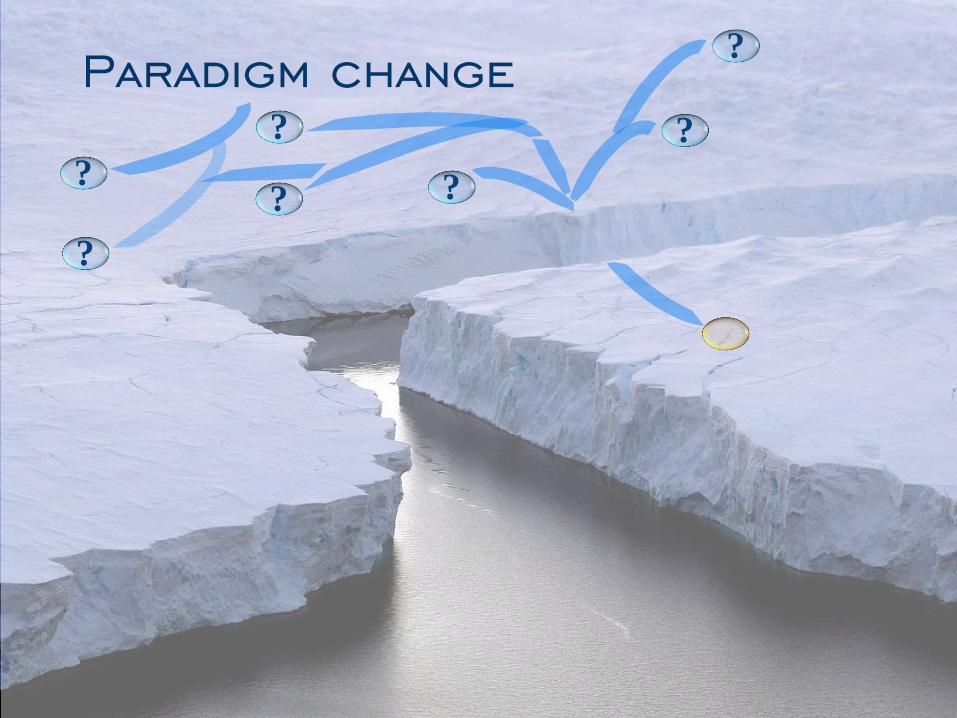

?

?

?

?

?

?

?

Paradigm change

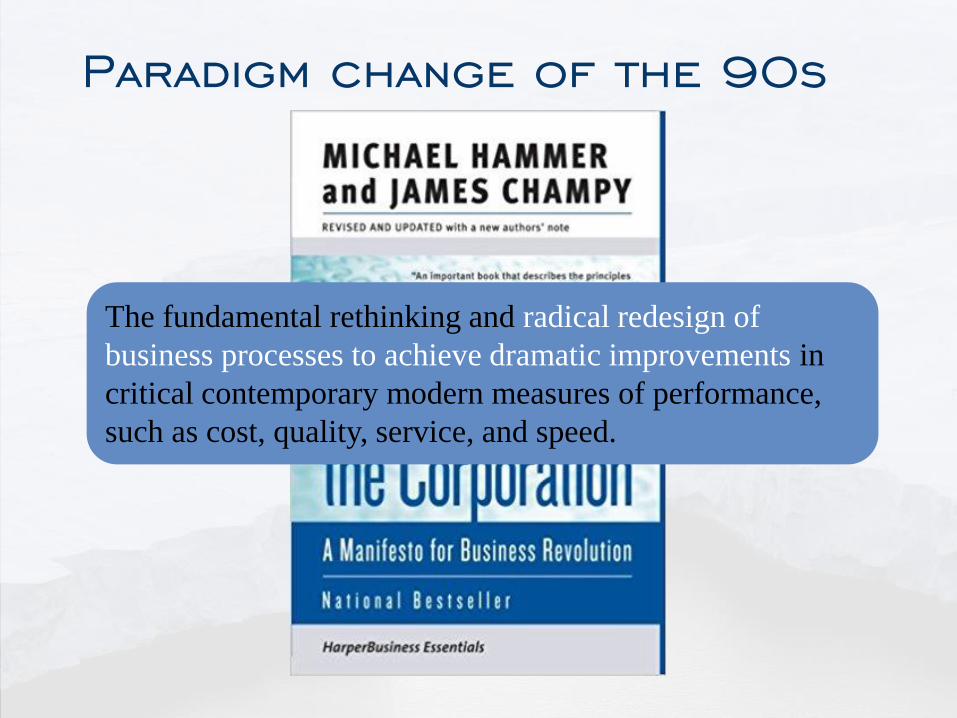

Paradigm change of the 90s

The fundamental rethinking and radical redesign of

business processes to achieve dramatic improvements in

critical contemporary modern measures of performance,

such as cost, quality, service, and speed.

Drivers of change in the 90s

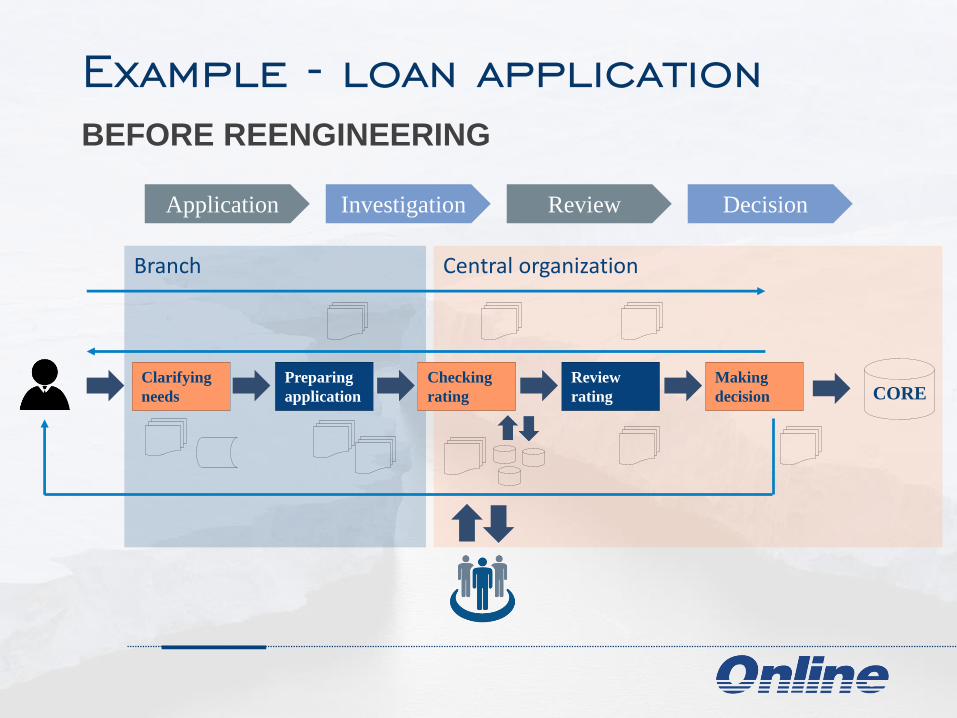

Branch

Example - loan application

BEFORE REENGINEERING

Application Investigation Review Decision

Central organization

Clarifying

needs

Checking

rating

Review

rating

Preparing

application

Making

decision CORE

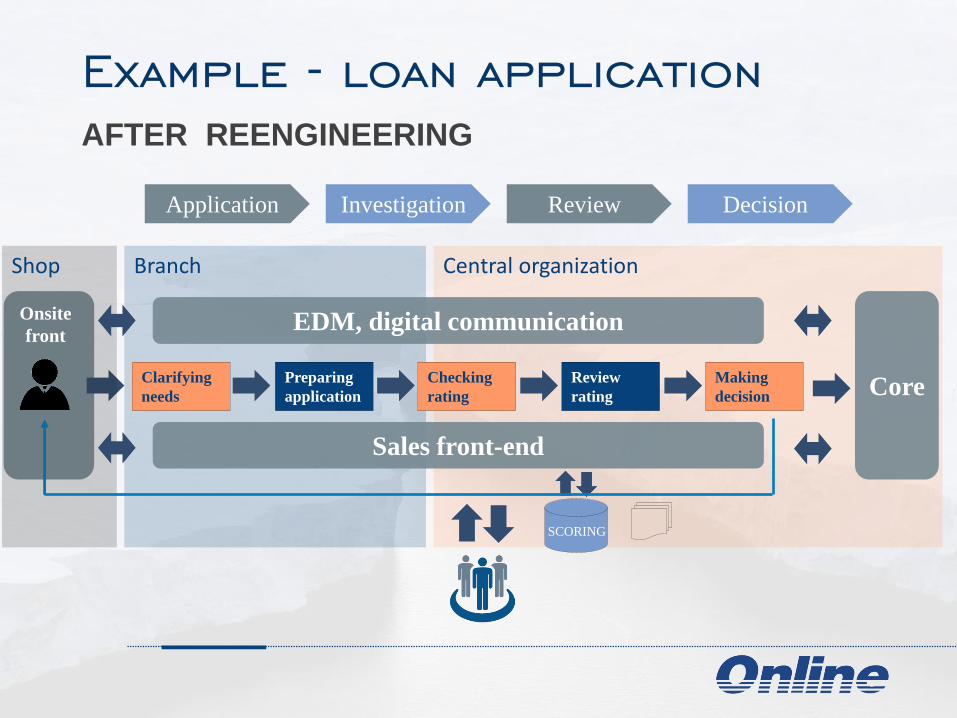

Branch

Example - loan application

AFTER REENGINEERING

Application Investigation Review Decision

Central organization

Clarifying

needs

Preparing

application

Checking

rating

Review

rating

Making

decision Core

SCORING

EDM, digital communication

Shop

Sales front-end

Onsite

front

Paradigm change today

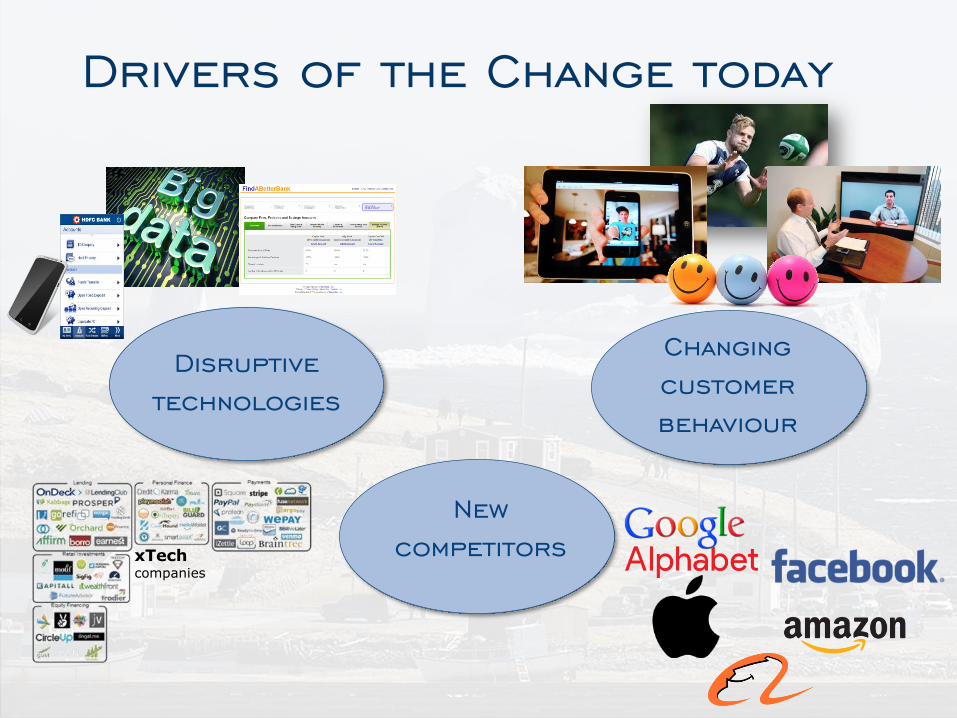

Drivers of the Change today

Disruptive

technologies

Changing

customer

behaviour

xTechcompanies

New

competitors

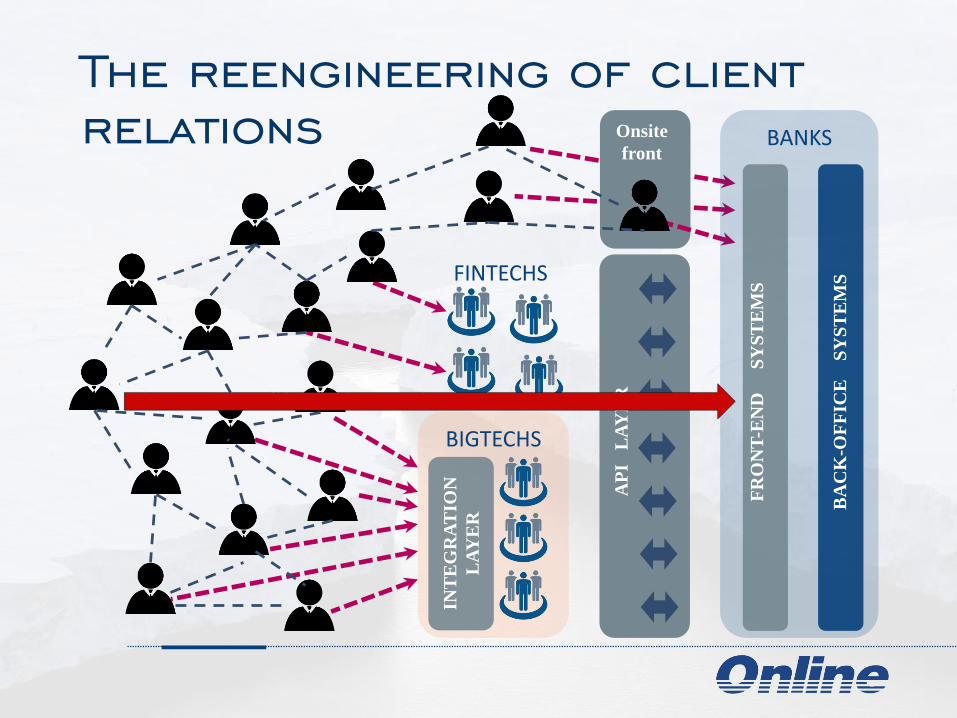

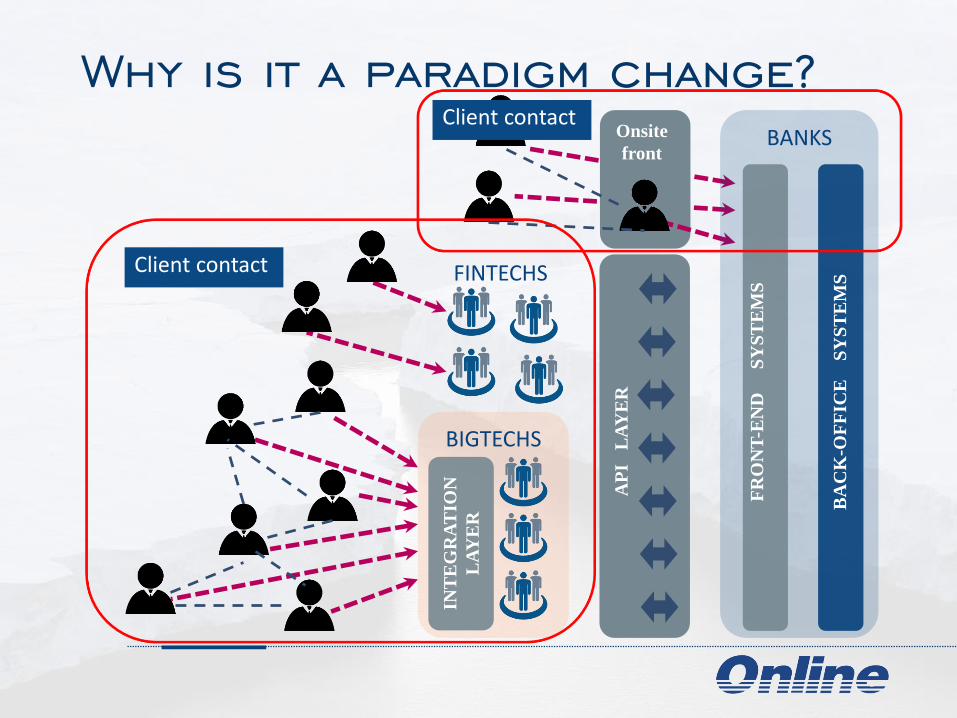

Onsite

front

BIGTECHSIN

TE

GR

AT

ION

LA

YE

R

FINTECHS

BANKS

FR

ON

T-E

ND

SY

ST

EM

S

BA

CK

-OF

FIC

E S

YS

TE

MS

AP

I

LA

YE

R

The reengineering of client

relations

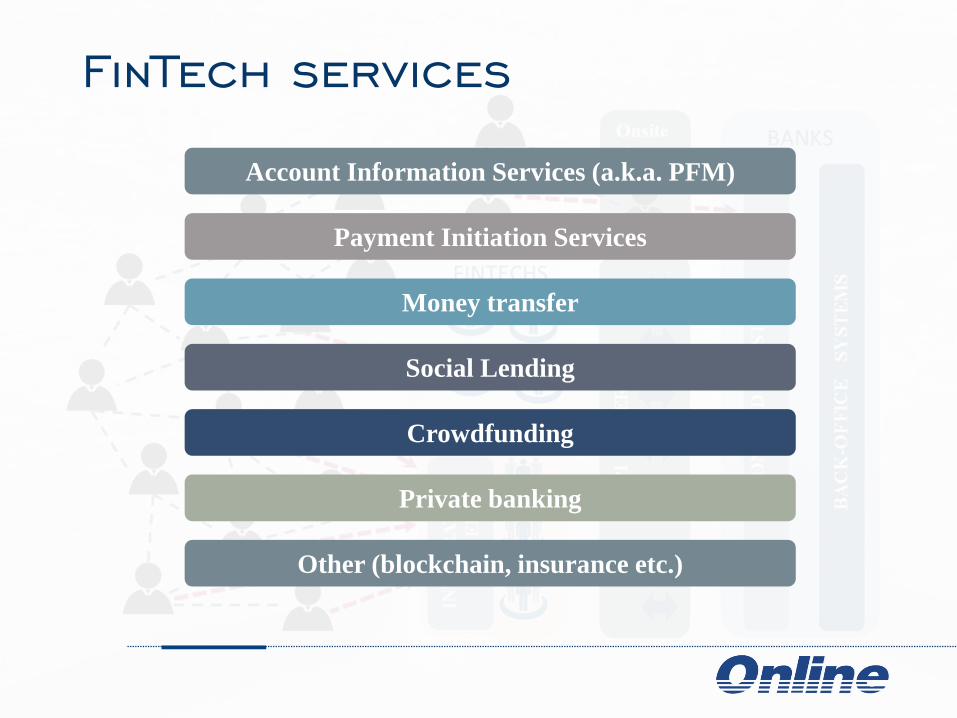

FinTech services

Account Information Services (a.k.a. PFM)

Payment Initiation Services

Money transfer

Social Lending

Crowdfunding

Private banking

Other (blockchain, insurance etc.)

Onsite

front

BIGTECHSIN

TE

GR

AT

ION

LA

YE

R

FINTECHS

BANKS

FR

ON

T-E

ND

SY

ST

EM

S

BA

CK

-OF

FIC

E S

YS

TE

MS

AP

I

LA

YE

R

Why is it a paradigm change?

Client contact

Client contact

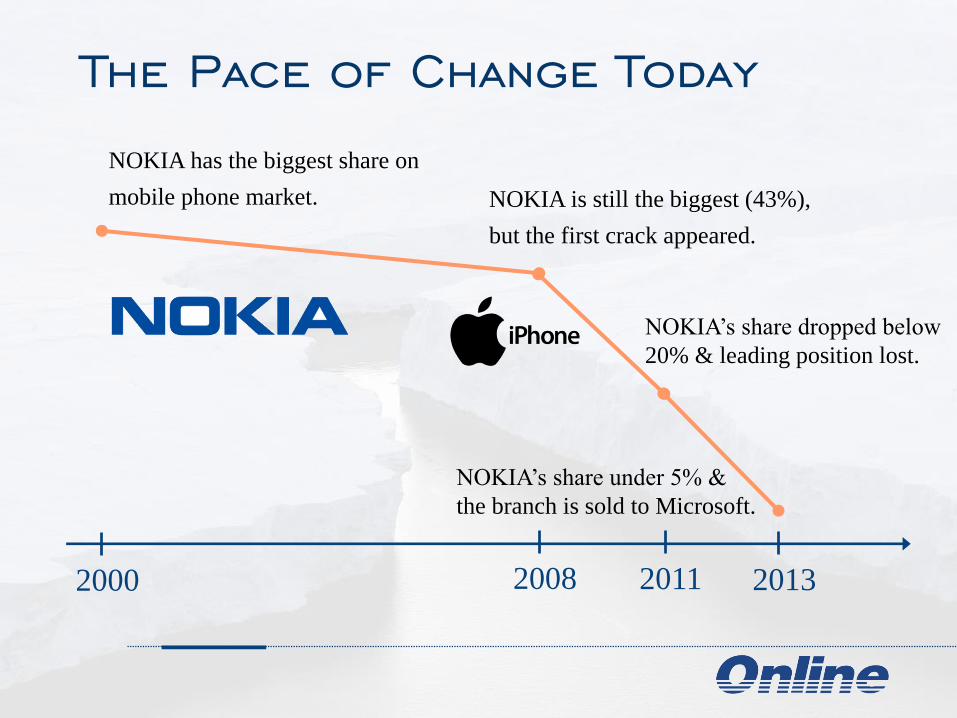

The Pace of Change Today

2011

NOKIA’s share dropped below

20% & leading position lost.

2013

NOKIA’s share under 5% &

the branch is sold to Microsoft.

2000

NOKIA has the biggest share on

mobile phone market.

2008

NOKIA is still the biggest (43%),

but the first crack appeared.

HOW DOES REGULATION

ACCELERATE CHANGES?

The Icebreaker

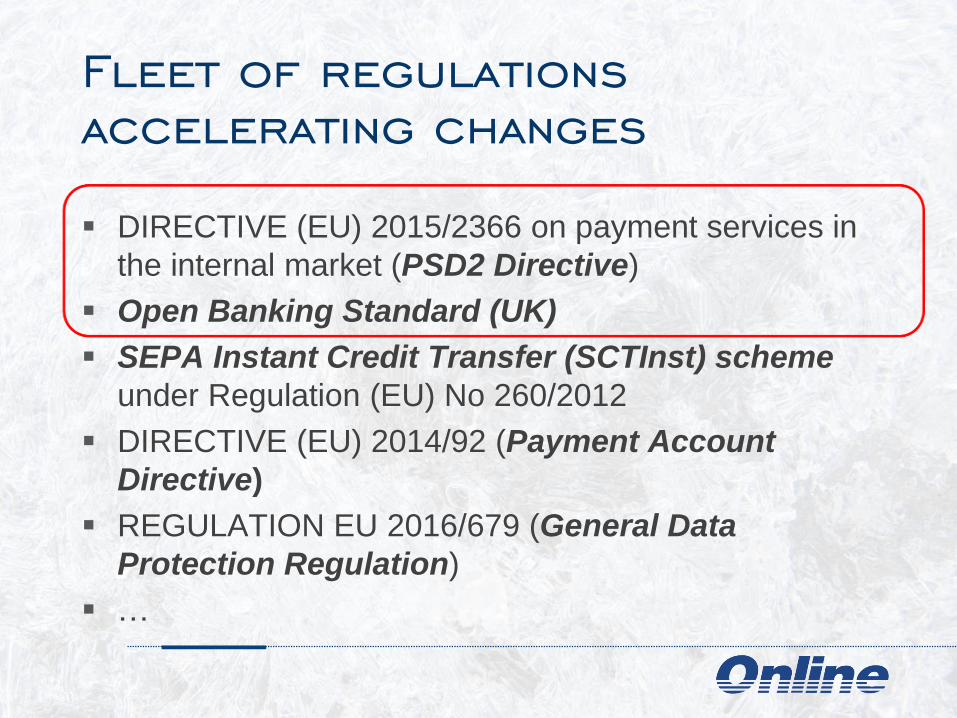

Fleet of regulations

accelerating changes

DIRECTIVE (EU) 2015/2366 on payment services in

the internal market (PSD2 Directive)

Open Banking Standard (UK)

SEPA Instant Credit Transfer (SCTInst) scheme

under Regulation (EU) No 260/2012

DIRECTIVE (EU) 2014/92 (Payment Account

Directive)

REGULATION EU 2016/679 (General Data

Protection Regulation)

…

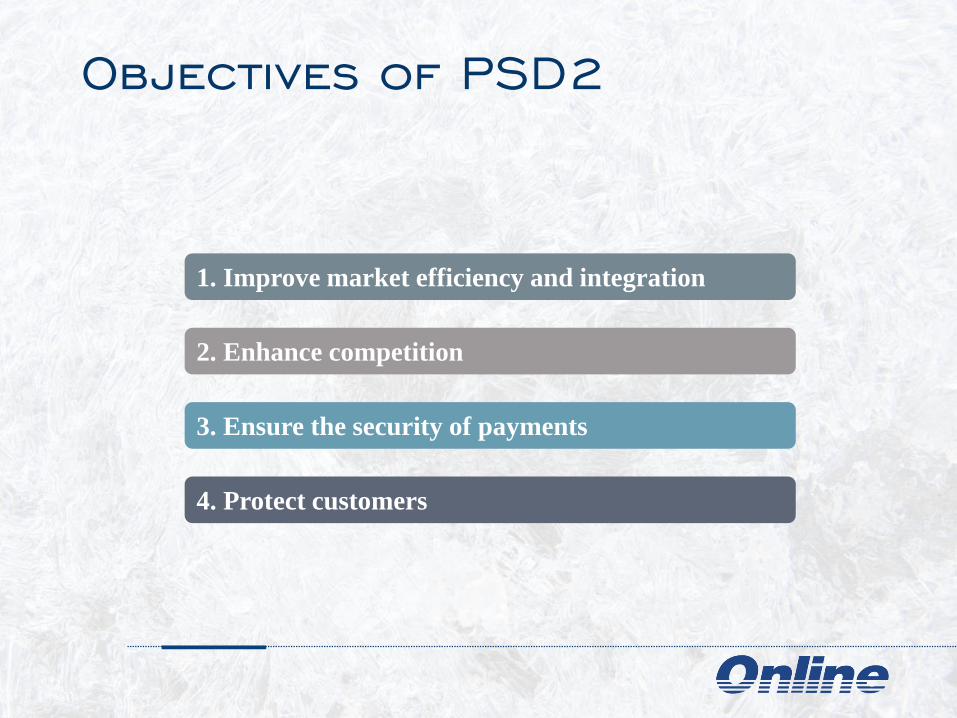

Objectives of PSD2

1. Improve market efficiency and integration

2. Enhance competition

3. Ensure the security of payments

4. Protect customers

Objectives of Open Banking

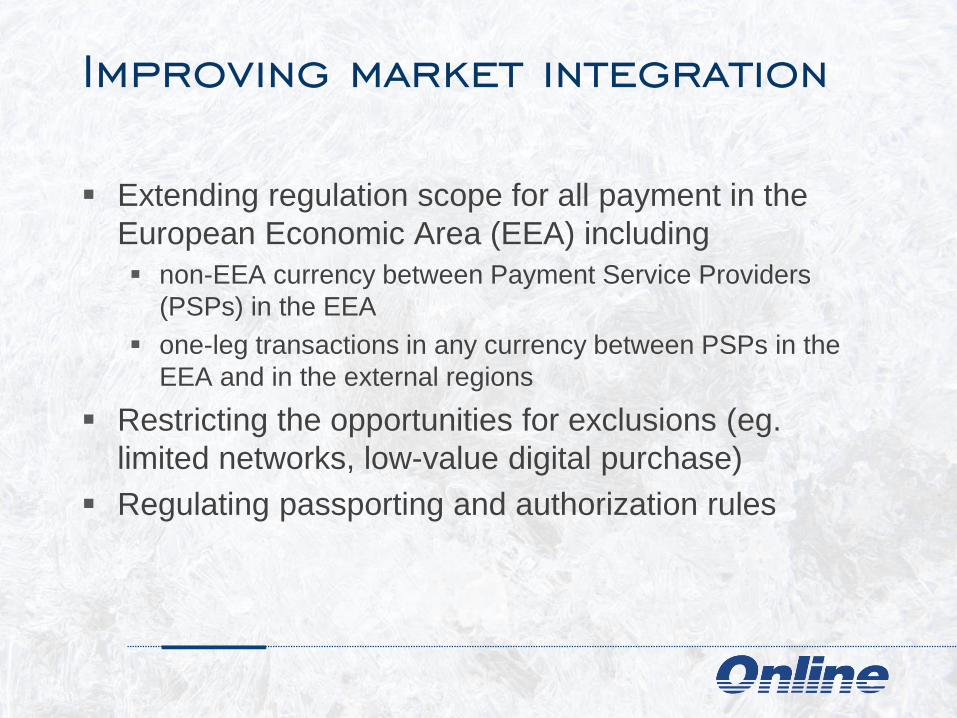

Improving market integration

Extending regulation scope for all payment in the

European Economic Area (EEA) including

non-EEA currency between Payment Service Providers

(PSPs) in the EEA

one-leg transactions in any currency between PSPs in the

EEA and in the external regions

Restricting the opportunities for exclusions (eg.

limited networks, low-value digital purchase)

Regulating passporting and authorization rules

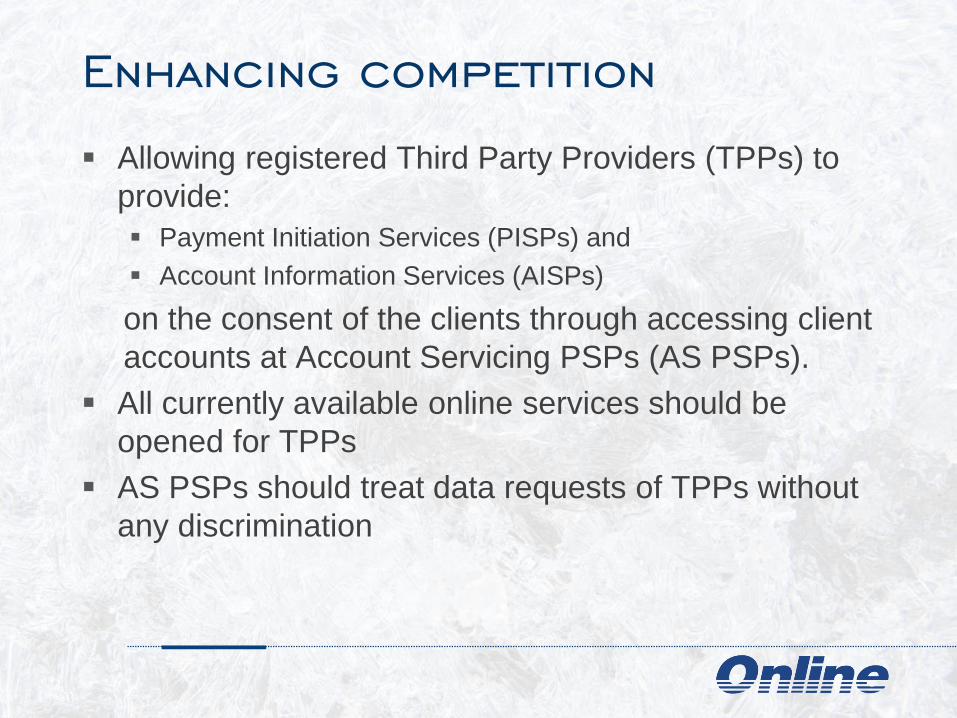

Enhancing competition

Allowing registered Third Party Providers (TPPs) to

provide:

Payment Initiation Services (PISPs) and

Account Information Services (AISPs)

on the consent of the clients through accessing client

accounts at Account Servicing PSPs (AS PSPs).

All currently available online services should be

opened for TPPs

AS PSPs should treat data requests of TPPs without

any discrimination

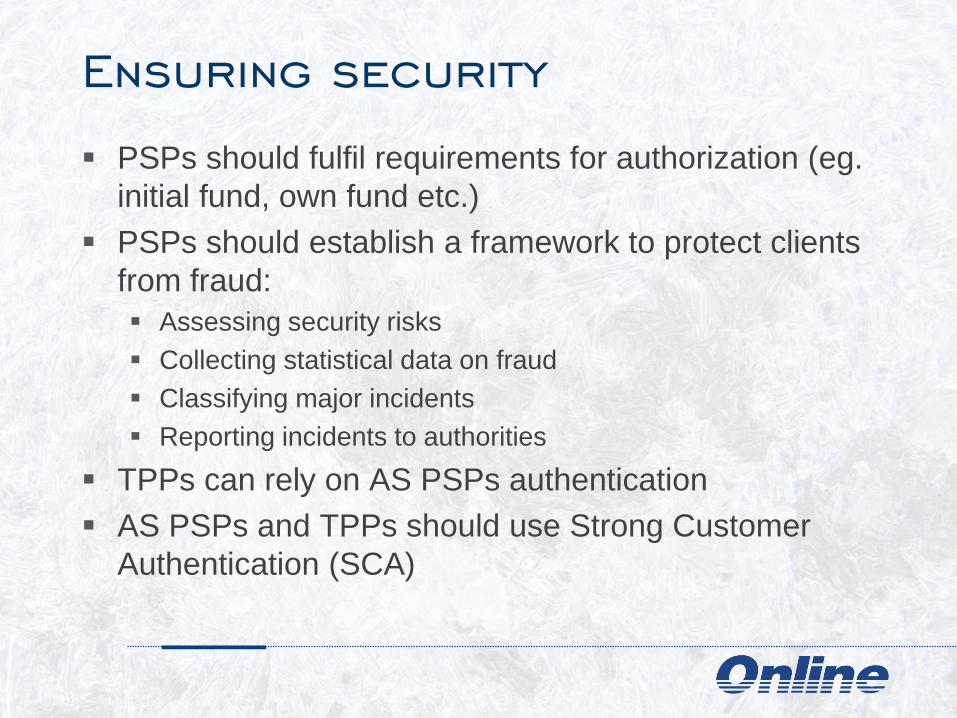

Ensuring security

PSPs should fulfil requirements for authorization (eg.

initial fund, own fund etc.)

PSPs should establish a framework to protect clients

from fraud:

Assessing security risks

Collecting statistical data on fraud

Classifying major incidents

Reporting incidents to authorities

TPPs can rely on AS PSPs authentication

AS PSPs and TPPs should use Strong Customer

Authentication (SCA)

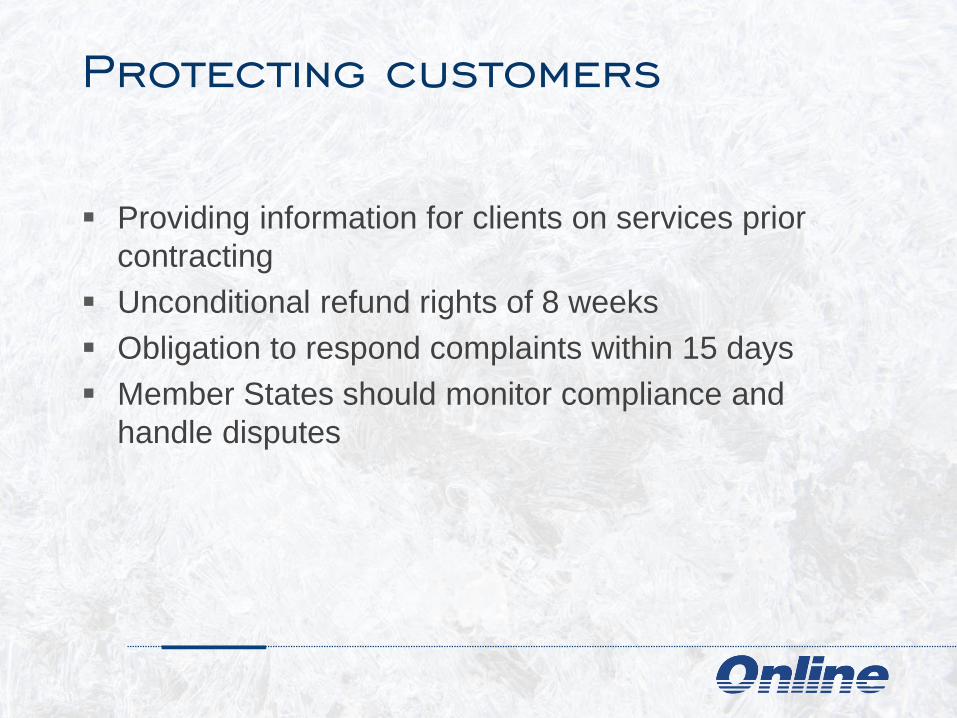

Protecting customers

Providing information for clients on services prior

contracting

Unconditional refund rights of 8 weeks

Obligation to respond complaints within 15 days

Member States should monitor compliance and

handle disputes

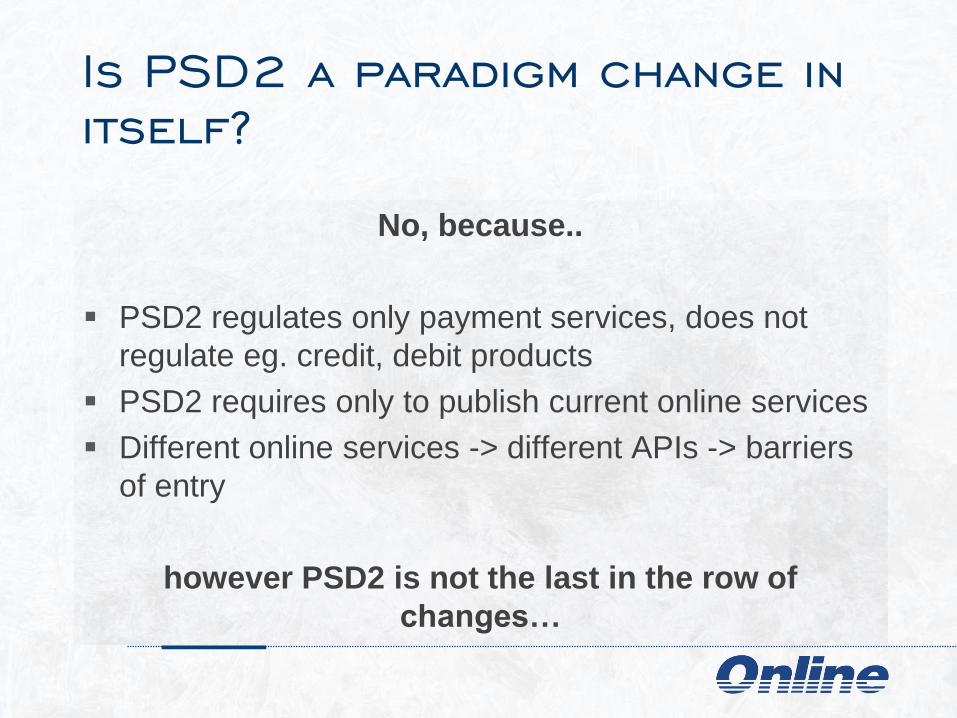

Is PSD2 a paradigm change in

itself?

No, because..

PSD2 regulates only payment services, does not

regulate eg. credit, debit products

PSD2 requires only to publish current online services

Different online services -> different APIs -> barriers

of entry

however PSD2 is not the last in the row of

changes…

WHAT COMES NEXT?

HOW TO MEET CHALLENGES?

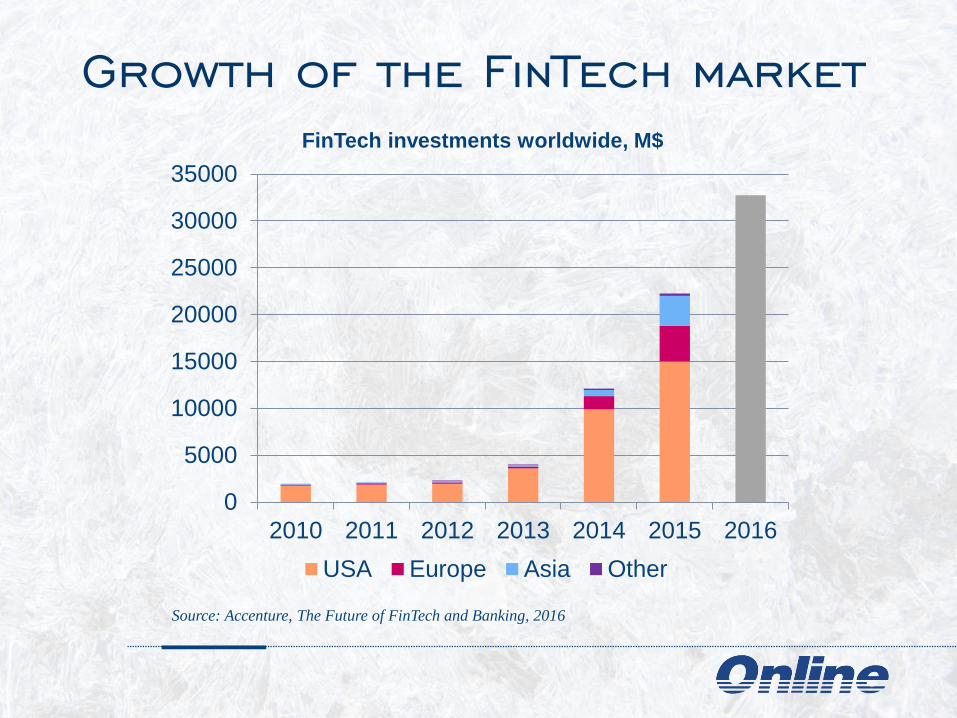

Growth of the FinTech market

0

5000

10000

15000

20000

25000

30000

35000

2010 2011 2012 2013 2014 2015 2016

FinTech investments worldwide, M$

USA Europe Asia Other

Source: Accenture, The Future of FinTech and Banking, 2016

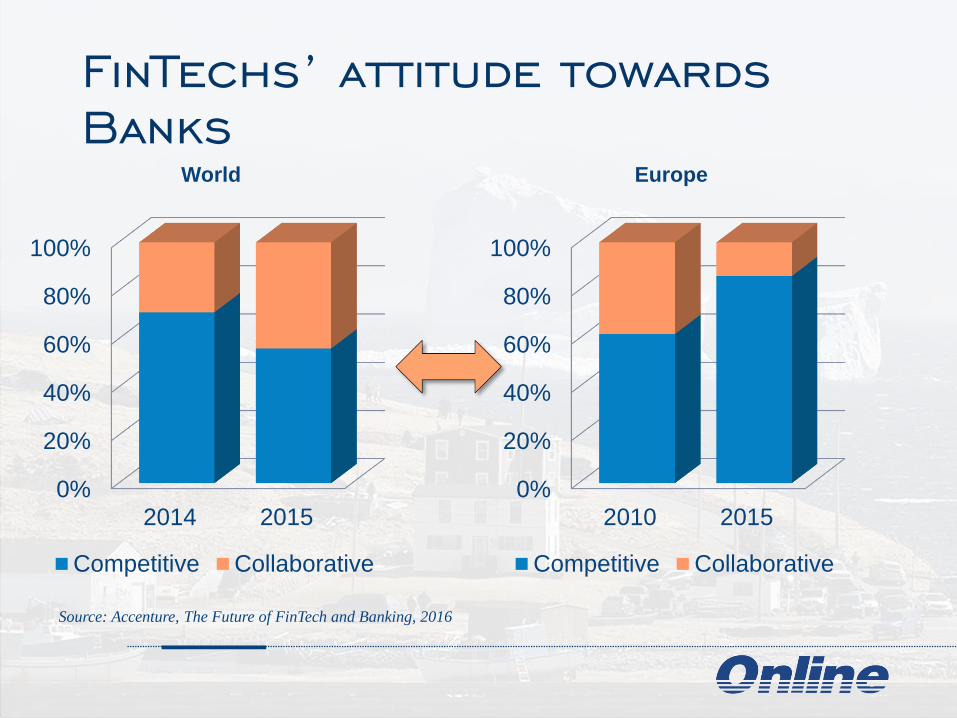

FinTechs’ attitude towards

Banks

Source: Accenture, The Future of FinTech and Banking, 2016

0%

20%

40%

60%

80%

100%

2014 2015

World

Competitive Collaborative

0%

20%

40%

60%

80%

100%

2010 2015

Europe

Competitive Collaborative

The GAFAA Impact

Openness User experienceSingle account

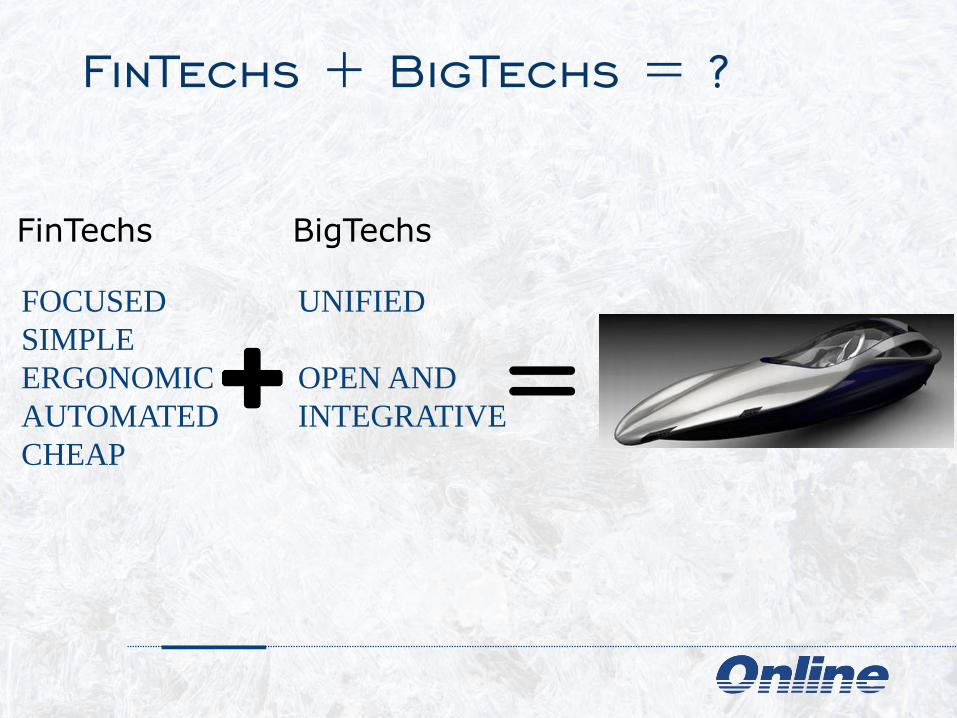

FinTechs + BigTechs = ?

FinTechs

FOCUSED

SIMPLE

ERGONOMIC

AUTOMATED

CHEAP

BigTechs

UNIFIED

OPEN AND

INTEGRATIVE

Strategic option for banks

1. Comply with PSD2

2. Offering new services for TPPs

3. Set up TPPs

4. Building an Ecosystem

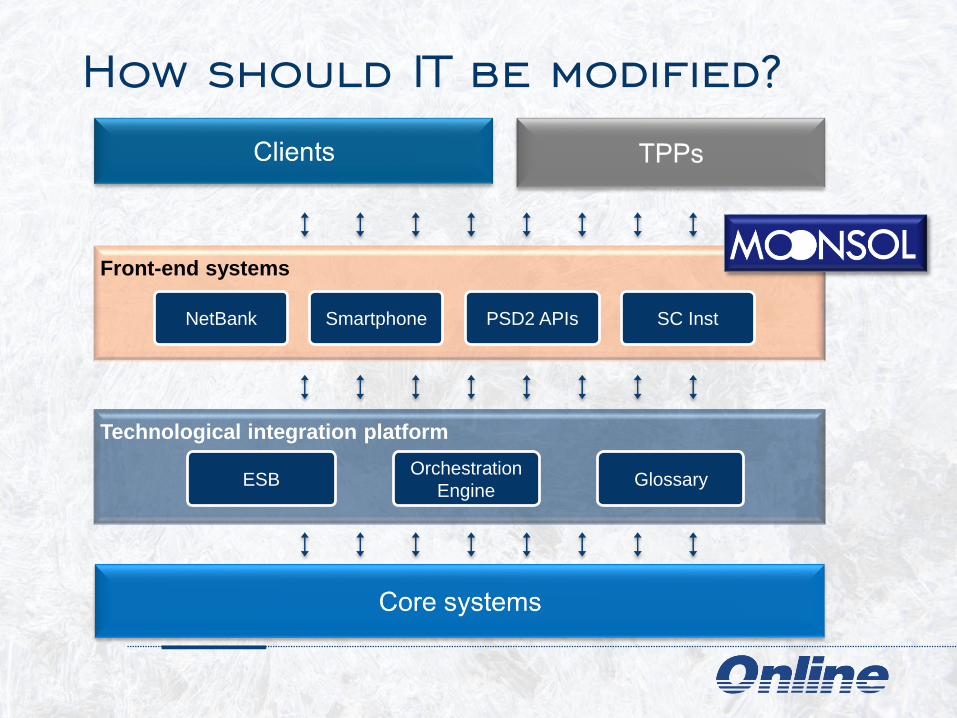

How should IT be modified?

Front-end systems

NetBank Smartphone PSD2 APIs SC Inst

Technological integration platform

ESBOrchestration

EngineGlossary

About the Nature of competition