Embed Size (px)

Citation preview

PREPARED FOR

HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE

By: Zach Bowyer, MAIAugust 4, 2014

2 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

Industry Overview

Valuation Overview

Market Analysis

Income Approach

Sales Comparison Approach

Allocation of the Going Concern

Final Considerations

How to Appraise an Assisted Living ResidencePRESENTATION OVERVIEW

3 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

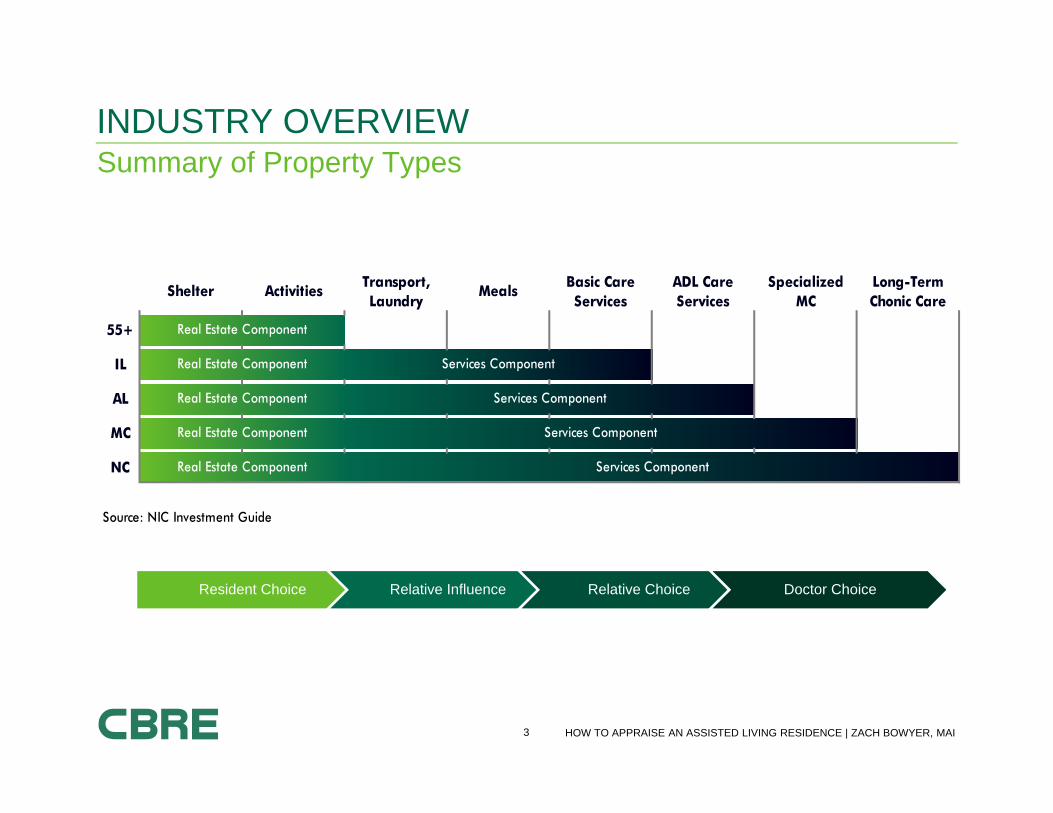

INDUSTRY OVERVIEW

Shelter ActivitiesTransport, Laundry

MealsBasic Care Services

ADL Care Services

Specialized MC

Long-Term Chonic Care

55+

IL

AL

MC

NC

Source: NIC Investment Guide

Real Estate Component Services Component

Real Estate Component Services Component

Real Estate Component

Real Estate Component Services Component

Real Estate Component Services Component

Summary of Property Types

Resident Choice Relative Influence Relative Choice Doctor Choice

4 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

INDUSTRY OVERVIEWIndependent Living Community (ILC)

5 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

INDUSTRY OVERVIEWAssisted Living Residence (ALR)

6 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

INDUSTRY OVERVIEWSkilled Nursing Facility (SNF)

7 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

INDUSTRY OVERVIEWContinuing Care Retirement Community (CCRC)

8 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

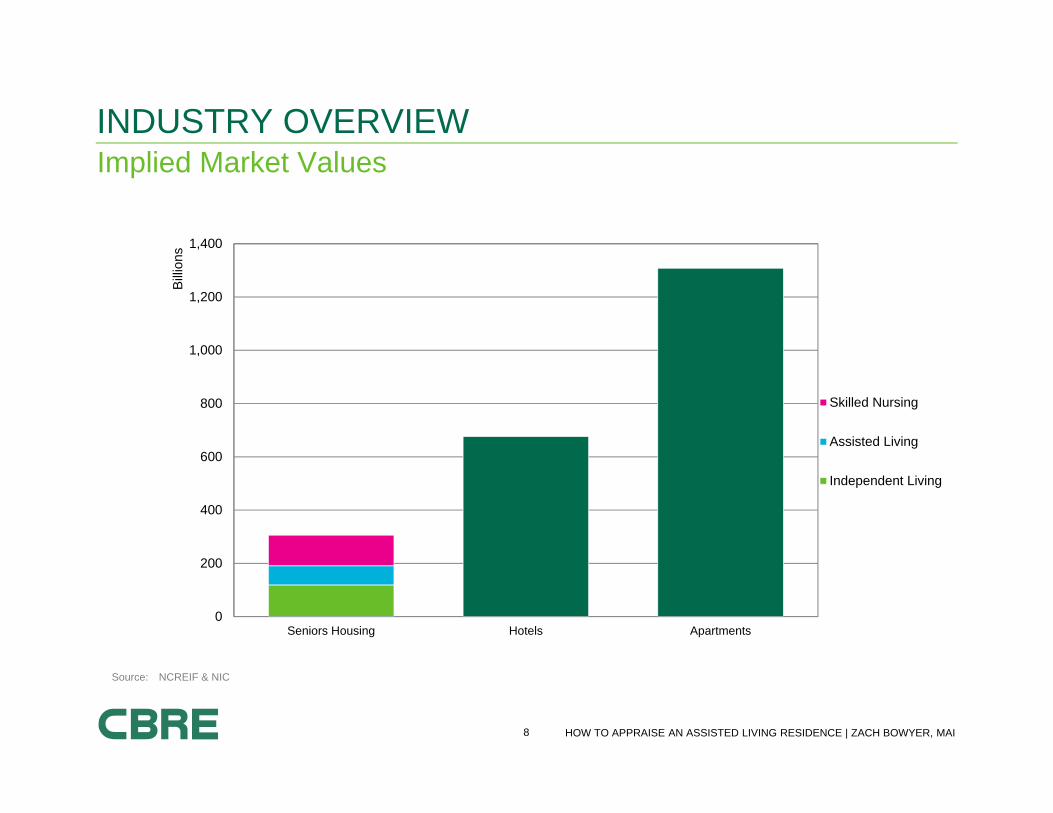

Implied Market ValuesINDUSTRY OVERVIEW

0

200

400

600

800

1,000

1,200

1,400

Seniors Housing Hotels Apartments

Billi

ons

Skilled Nursing

Assisted Living

Independent Living

Source: NCREIF & NIC

9 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

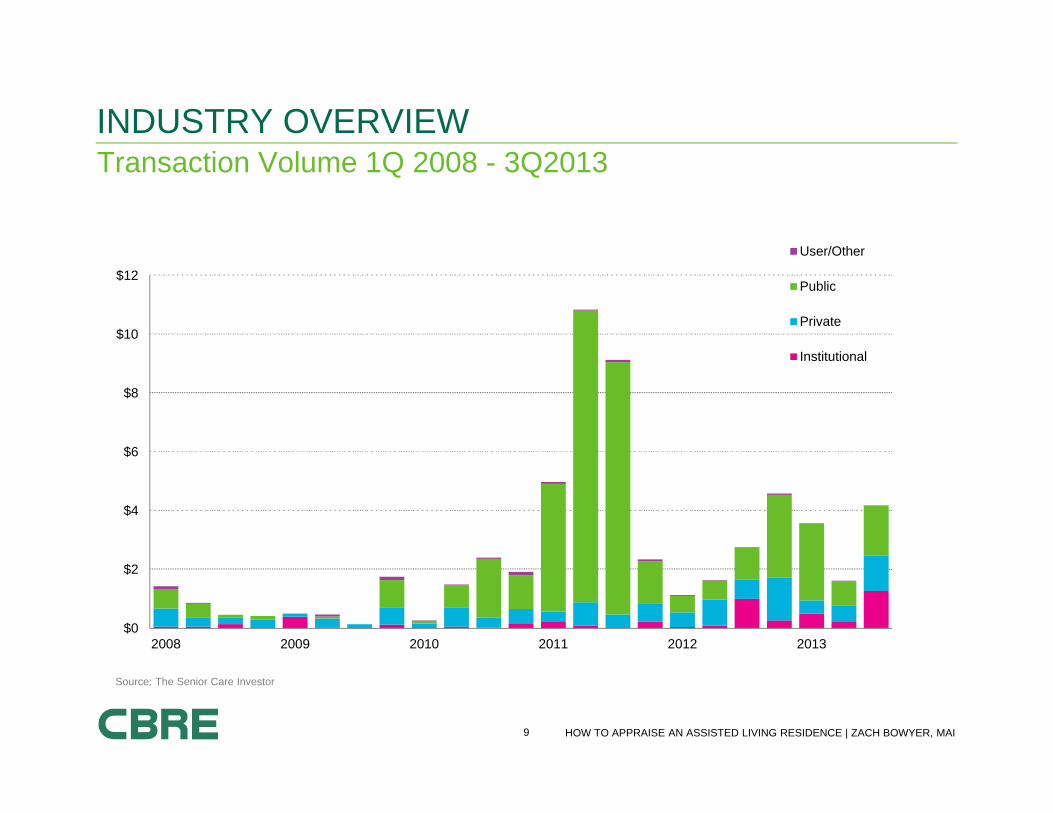

Transaction Volume 1Q 2008 - 3Q2013INDUSTRY OVERVIEW

$0

$2

$4

$6

$8

$10

$12

2008 2009 2010 2011 2012 2013

User/Other

Public

Private

Institutional

Source: The Senior Care Investor

10 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

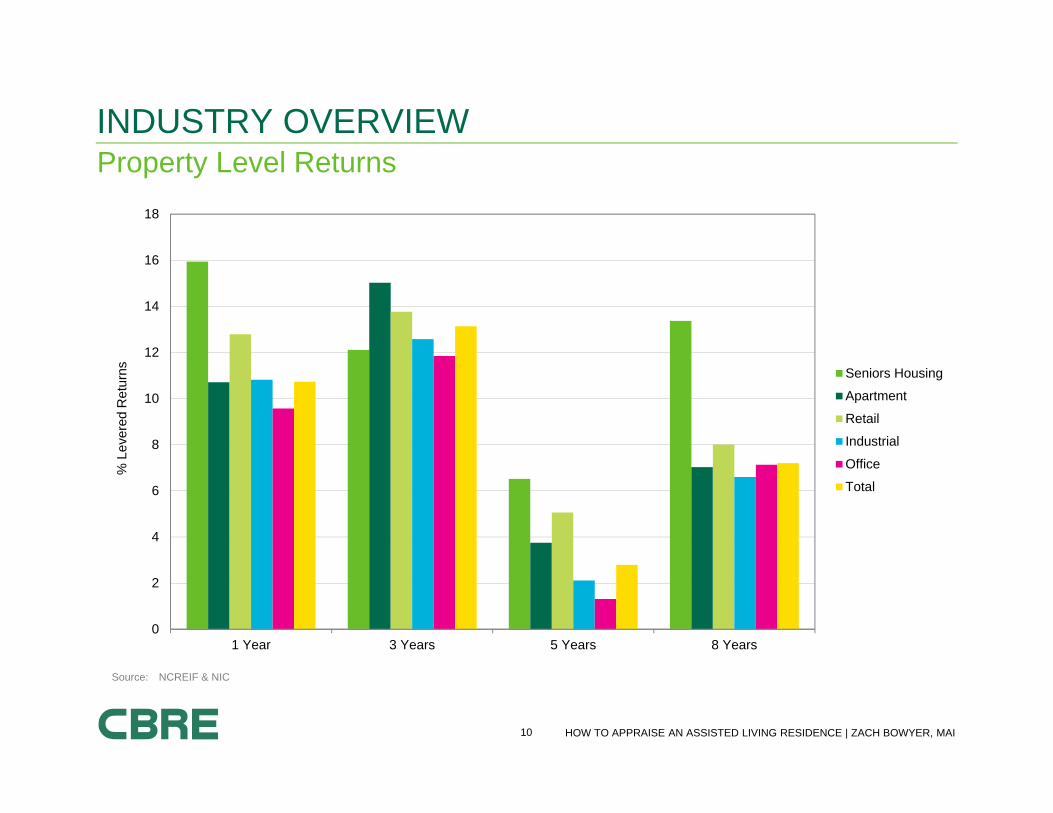

Property Level ReturnsINDUSTRY OVERVIEW

0

2

4

6

8

10

12

14

16

18

1 Year 3 Years 5 Years 8 Years

Seniors Housing

Apartment

Retail

Industrial

Office

Total

Source: NCREIF & NIC

% L

ever

ed R

etur

ns

11 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

Capitalization Rate TrendsINDUSTRY OVERVIEW

Source: The Senior Care Investor

6.0%

7.0%

8.0%

9.0%

10.0%

11.0%

12.0%

13.0%

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

12 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

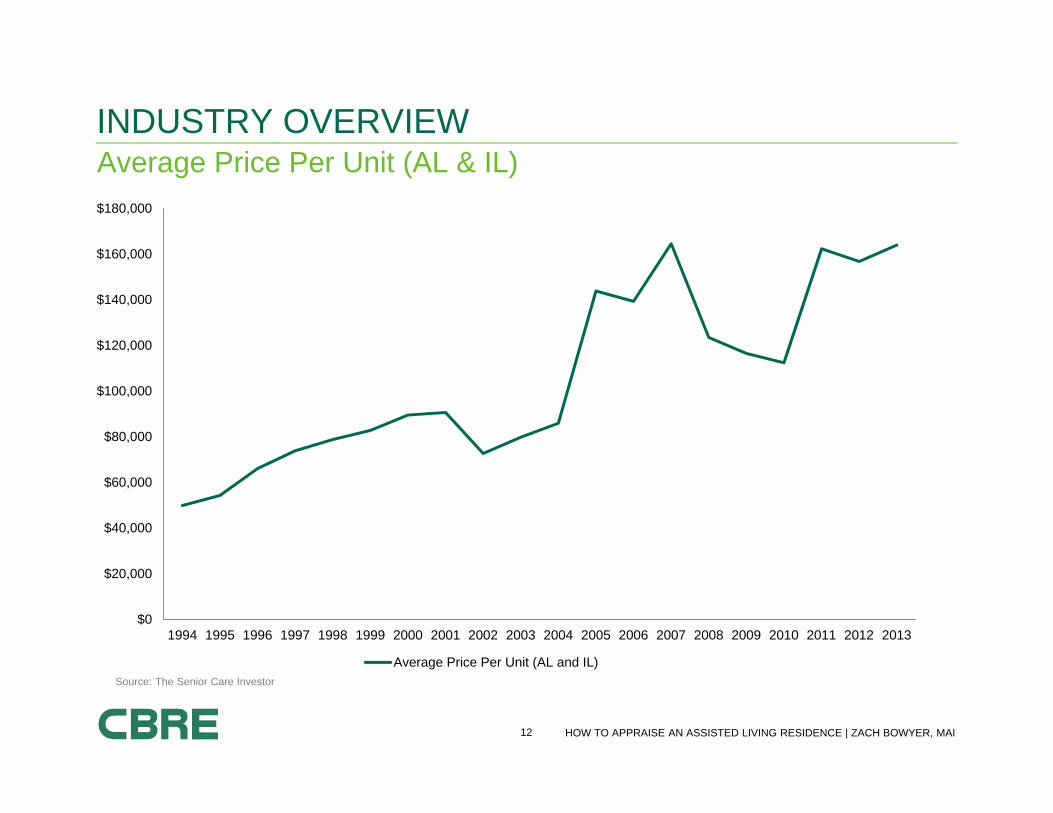

Average Price Per Unit (AL & IL)INDUSTRY OVERVIEW

Source: The Senior Care Investor

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

$140,000

$160,000

$180,000

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Average Price Per Unit (AL and IL)

13 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

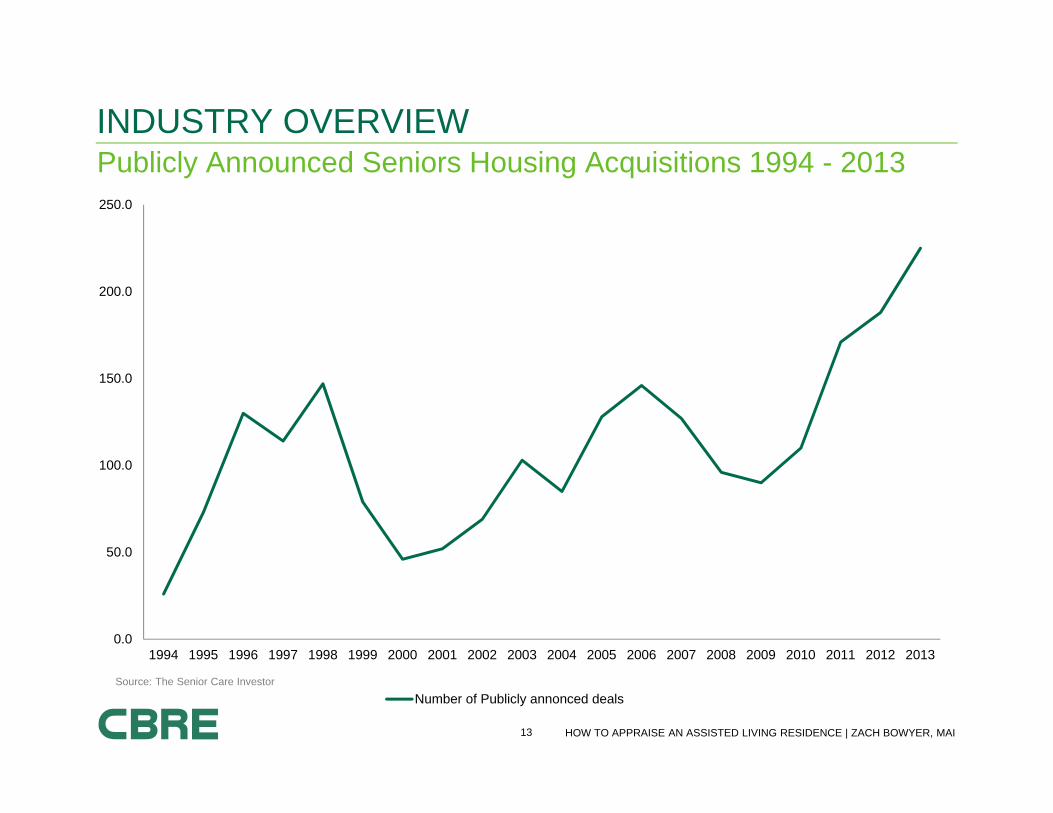

Publicly Announced Seniors Housing Acquisitions 1994 - 2013INDUSTRY OVERVIEW

Source: The Senior Care Investor

0.0

50.0

100.0

150.0

200.0

250.0

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Number of Publicly annonced deals

14 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

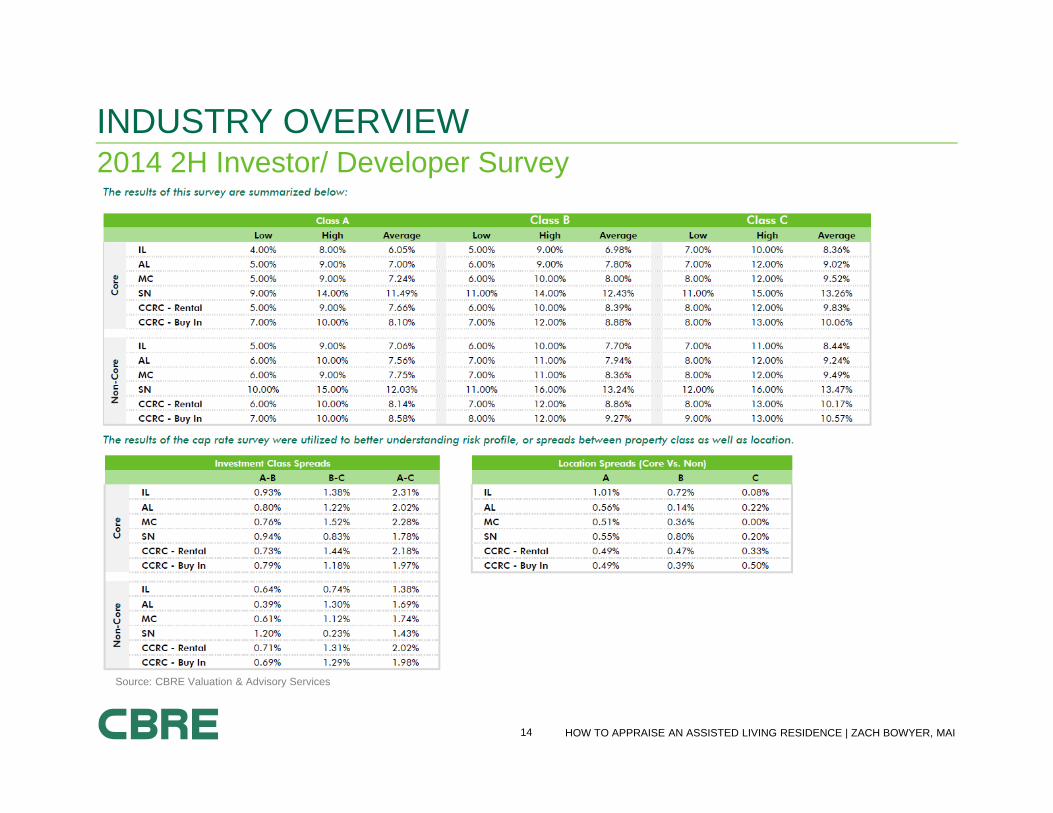

2014 2H Investor/ Developer SurveyINDUSTRY OVERVIEW

Source: CBRE Valuation & Advisory Services

15 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

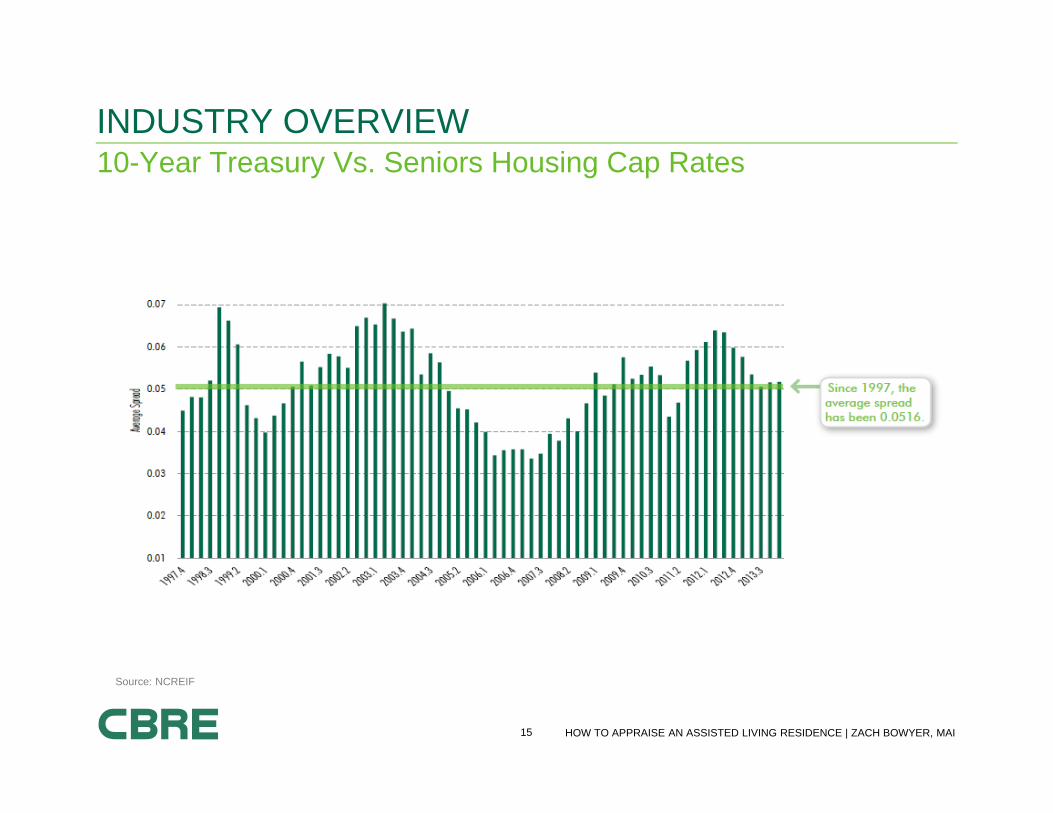

10-Year Treasury Vs. Seniors Housing Cap RatesINDUSTRY OVERVIEW

Source: NCREIF

16 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

Capitalization Rate Trends & OutlookINDUSTRY OVERVIEW

Source: NIC MAP and US Census Bureau

17 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

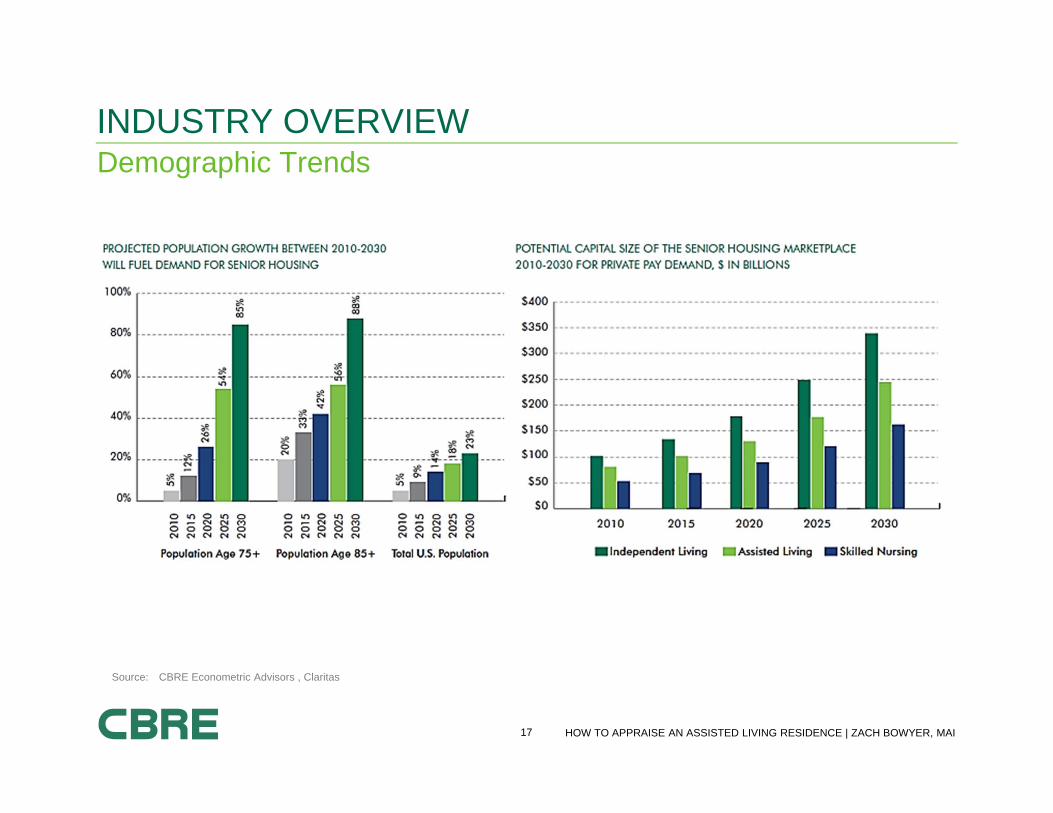

INDUSTRY OVERVIEWDemographic Trends

Source: CBRE Econometric Advisors , Claritas

18 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

INDUSTRY OVERVIEWDo the MathAverage Age of NEW AL resident (84) – Age of Leading-Edge Baby Boomer (67) = 17 Years

19 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

Seniors Housing Demand Vs. SupplyINDUSTRY OVERVIEW

Source: NIC MAP and US Census Bureau

20 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

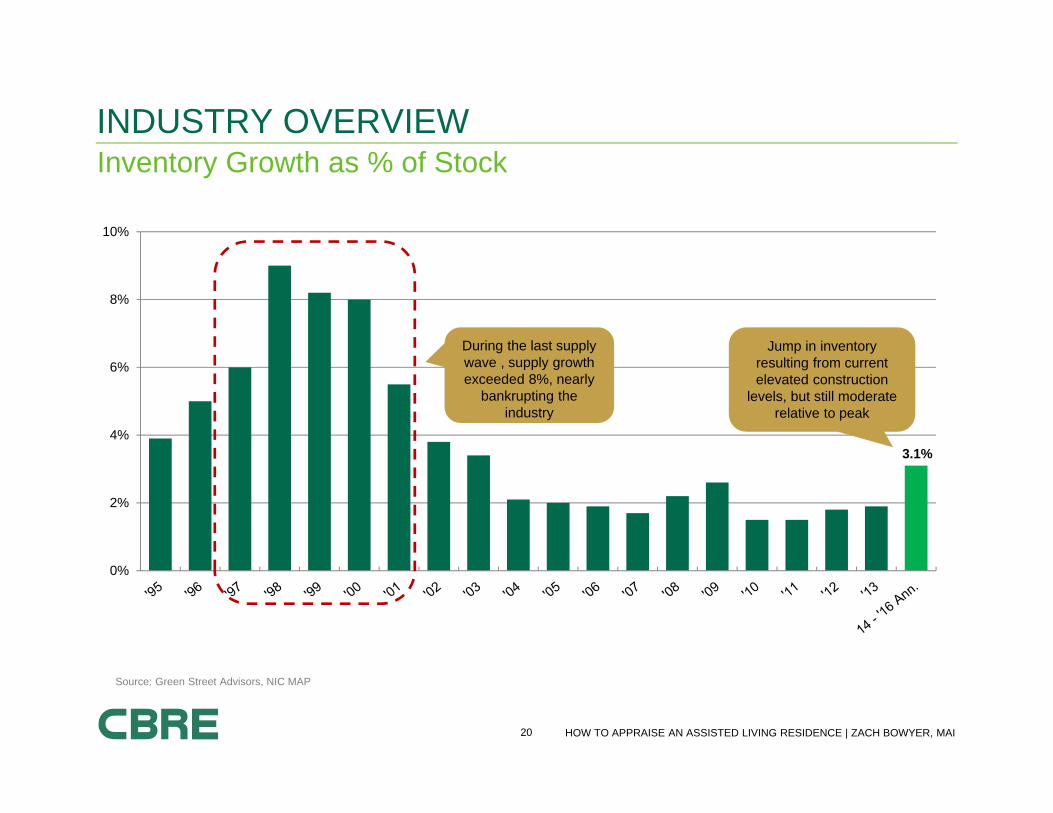

Inventory Growth as % of StockINDUSTRY OVERVIEW

Source: Green Street Advisors, NIC MAP

3.1%

0%

2%

4%

6%

8%

10%

During the last supplywave , supply growth exceeded 8%, nearly

bankrupting the industry

Jump in inventory resulting from current elevated construction

levels, but still moderate relative to peak

21 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

Industry Overview

Valuation Overview Market Analysis

Income Approach

Sales Comparison Approach

Allocation of the Going Concern

Final Considerations

How to Appraise an Assisted Living ResidencePRESENTATION OVERVIEW

22 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

Appraisal ProcessVALUATION OVERVIEW

Definition of the Problem

Scope of Work

Data Collection and AnalysisMarket Analysis

Highest and Best Use

Application of Approaches to ValueIncome Approach

Sales Comparison ApproachCost Approach

Reconciliation of Value Indicators and Final Value Opinion

Report of Defined Value Opinions•Allocation of the Going Concern

23 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

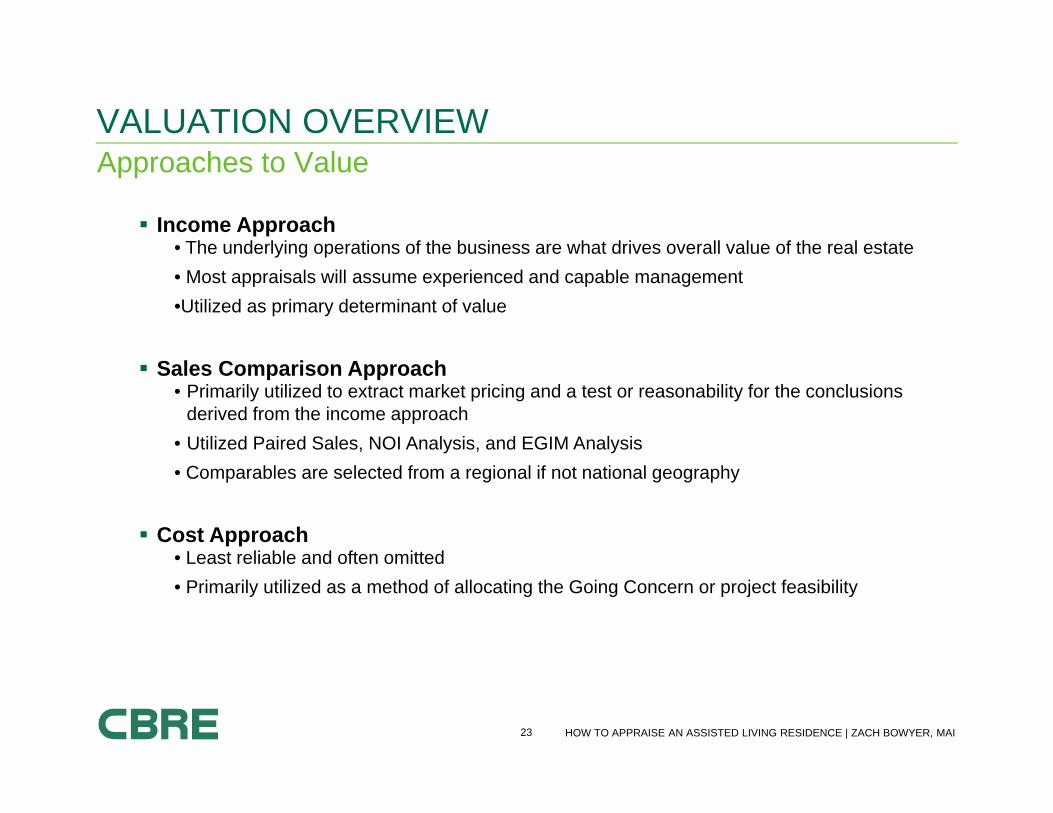

Approaches to ValueVALUATION OVERVIEW

Income Approach• The underlying operations of the business are what drives overall value of the real estate• Most appraisals will assume experienced and capable management•Utilized as primary determinant of value

Sales Comparison Approach• Primarily utilized to extract market pricing and a test or reasonability for the conclusions

derived from the income approach• Utilized Paired Sales, NOI Analysis, and EGIM Analysis• Comparables are selected from a regional if not national geography

Cost Approach• Least reliable and often omitted• Primarily utilized as a method of allocating the Going Concern or project feasibility

24 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

VALUATION OVERVIEWProperty Rights Appraised

Seniors housing is primarily valued based on the fee simple interest of the going concern, which isthe premise of this presentation. Leased Fee valuation is summarized in the Allocation of GoingConcern.

Going Concern: A going concern is a business having the ability to continue functioning as a business entity in thefuture. In accounting, a business is considered to be a going concern if it is likely to continue functioning 12 months intothe future.

One of the premises under which the total assets of a business can be valued; the assumption that a company isexpected to continue operating well into the future (usually indefinitely). Under the going-concern premise, the value ofthe tangible assets and the value of the intangible assets, which may include the value of excess profit, where assetvalues are derived consistent with the going-concern premise.

Land Real Estate FF & E Business or Enterprise Value

Business (Enterprise) Value: The value contribution of the total intangible assets of a continuing business enterprisesuch as marketing and management skill, an assembled workforce, working capital, trade names, franchises, patents,trademarks, contracts, leases, customer base, and operating agreements.

Real Estate Tax Assessments are typically based in the tangibles.

Source: Dictionary of Real Estate Appraising, 5th Edition, The Appraisal Institute, Chicago, IL, page 98

25 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

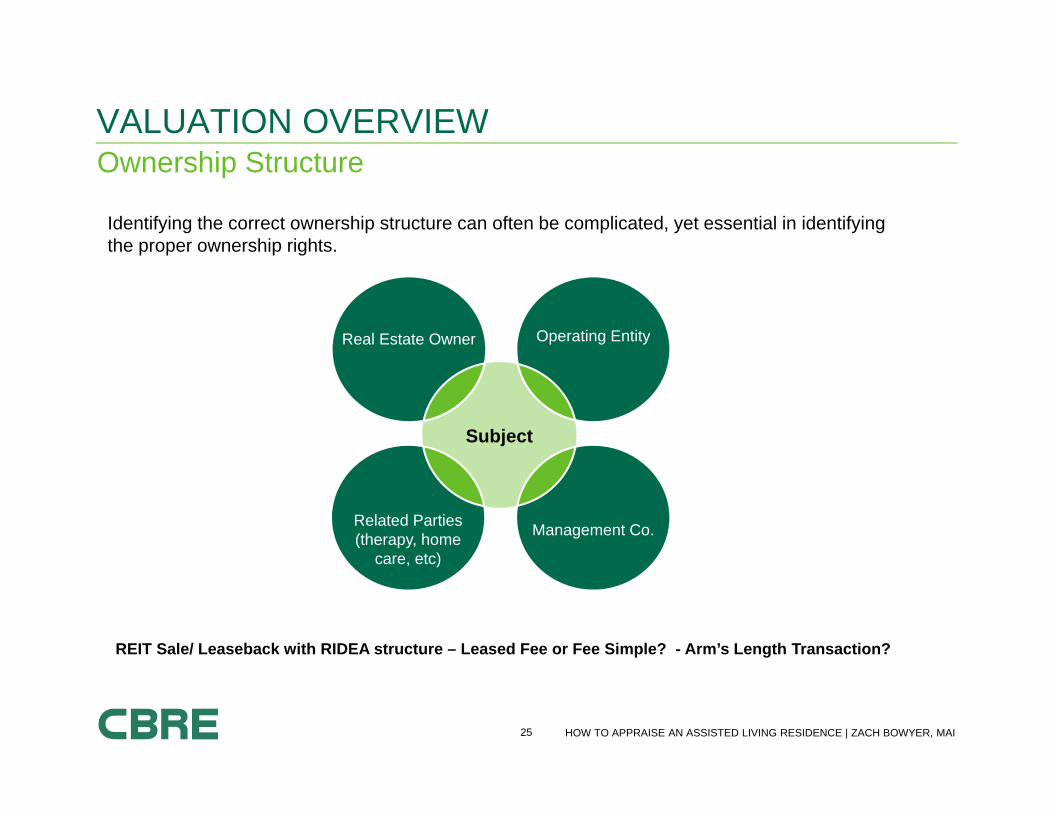

VALUATION OVERVIEWOwnership Structure

Identifying the correct ownership structure can often be complicated, yet essential in identifying the proper ownership rights.

Management Co.Related Parties (therapy, home

care, etc)

Subject

Real Estate Owner Operating Entity

REIT Sale/ Leaseback with RIDEA structure – Leased Fee or Fee Simple? - Arm’s Length Transaction?

26 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

Industry Overview

Valuation Overview

Market Analysis Income Approach

Sales Comparison Approach

Allocation of the Going Concern

Final Considerations

Seniors Housing Valuations & TrendsPRESENTATION OVERVIEW

27 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

Quantifying Net Market DemandMARKET ANALYSIS

A Primary Market Area (PMA) can be identified by a radius, node(s), submarket(s), zip code(s), county(s) or township(s), or any variety of such defining terms.

We define a PMA as representing where approximately 80% of the residents currently occupying the subject resided prior to moving in to the subject property.

In analyzing a market, CBRE employs two quantitative methods, each independent of the other

1. Penetration Analysis• Competitive Supply / Age Qualified Households • Simple, yet allows for apples-to-apples comparison to other markets• Requires comparable local, regional, and national data-points to understanding of the extracted rate• The penetration must be considered with occupancy to properly understand full meaning• Used to determine market depth and impact of future supply on current market balance

2. Demand Coverage Analysis• Delineates PMA by age and income qualified population• Recognizes healthcare or ADL (Activities of Daily Living) requirements specific to each care level• Identifies Net Demand in terms of actual number of units by property type• Identifies impact of state subsidies and +/- net immigrations outside market norm• PMA specific

Dummy Factors, Apples-to-Apples, Accurate Inputs, Boots on the Ground

28 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

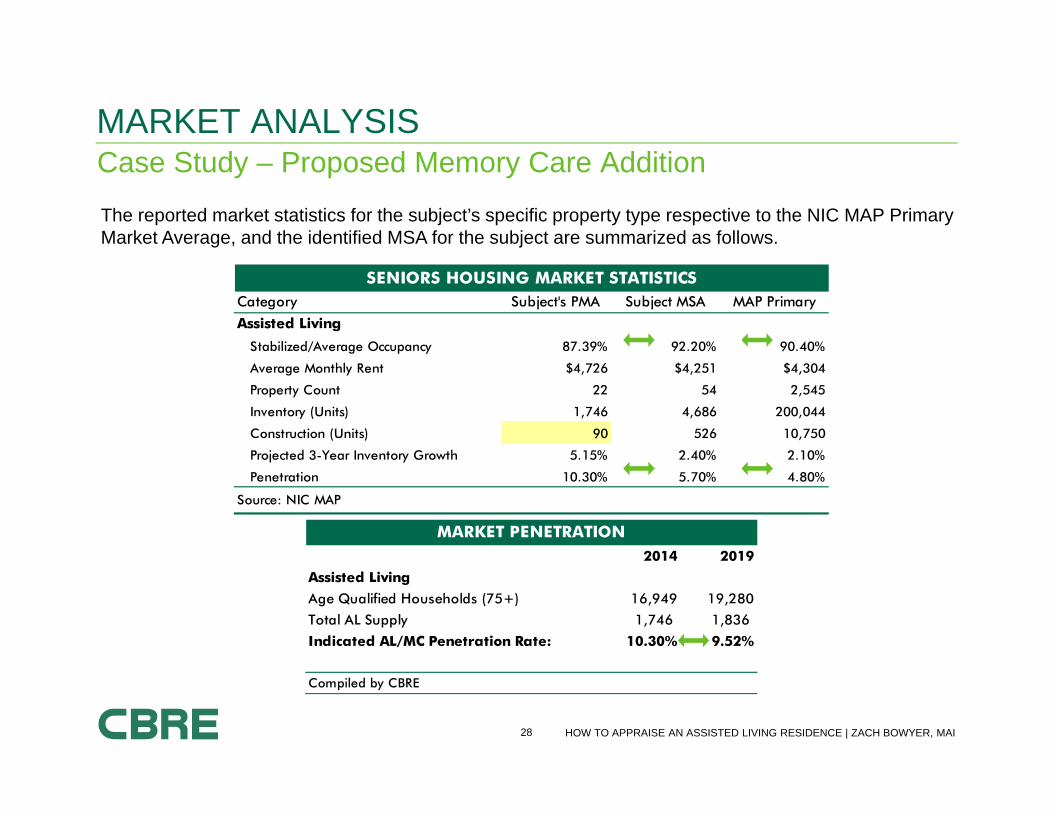

Case Study – Proposed Memory Care AdditionMARKET ANALYSIS

The reported market statistics for the subject’s specific property type respective to the NIC MAP Primary Market Average, and the identified MSA for the subject are summarized as follows.

SENIORS HOUSING MARKET STATISTICSCategory Subject's PMA Subject MSA MAP Primary

Assisted Living

Stabilized/Average Occupancy 87.39% 92.20% 90.40%

Average Monthly Rent $4,726 $4,251 $4,304

Property Count 22 54 2,545

Inventory (Units) 1,746 4,686 200,044

Construction (Units) 90 526 10,750

Projected 3-Year Inventory Growth 5.15% 2.40% 2.10%

Penetration 10.30% 5.70% 4.80%

Source: NIC MAP

2014 2019

Assisted Living

Age Qualified Households (75+) 16,949 19,280

Total AL Supply 1,746 1,836

Indicated AL/MC Penetration Rate: 10.30% 9.52%

Compiled by CBRE

MARKET PENETRATION

29 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

Case Study – Proposed Memory Care AdditionMARKET ANALYSIS

Penetration Rates Alone Have Multiple Meanings:

Low Penetration/ High Occupancy: Local population is accepting the subject’s product type, significant roomfor expansion, higher than typical ratio of residents emanating from outside the defined PMA. Expect strongoccupancy levels, stable rent growth, and healthy absorption for proposed properties. Most favorable.

Low Penetration/ Low Occupancy: Local population is either not accepting the subject property type or aretraveling outside the defined PMA to obtain their respective needs. Market opportunity does exist, but will likelyrequire additional marketing efforts in order to achieve a stabilized occupancy level.

High Penetration/ High Occupancy: Equally as attractive as low penetration with low occupancy. Competitivemarket, yet presumes the local population is generally receptive and well educated with the respective propertytype. Requires less marketing efforts in terms of product education, but may require more resources from anoverall competitive standpoint or the offering of something unique to the market, such as superior quality oraffordable rents. Prevalence of state subsidies are also common in this market (MA).

High Penetration/ Low Occupancy: This combination is the least favorable and depicts a saturated market.Decreasing rental rates, prevalence of concessions, and less than favorable occupancy can be expected.

30 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

Case Study – Proposed Memory Care AdditionMARKET ANALYSIS

2014 AL

65 - 74 Population 30,453

75 - 84 Population 16,023

85+ Population 8,319

Age Qualified Population 54,795

2019 AL

65 - 74 Population 41,510

75 - 84 Population 18,789

85+ Population 8,819

Age Qualified Population 69,118

Source: Compiled by CBRE

DEMAND BY POPULATION SEGMENT

AL

Base Market Rent (Monthly) $3,050

Base Market Rent (Annual) $36,600

Allocated % of Annual Income 80.00%

Indicated Base Income Retuirement $45,750

Average Home Value $297,851

Estimated Equity @ 75% of Home Value $223,388

Rate of Return 4.00%

Home Equity Contribution $8,936

Adjusted Income Requirement $36,814

Concluded Base Income Requirement $35,000

Source: Compiled by CBRE

BASE INCOME REQUIREMENT

A demand coverage analysis can serve as a morecalculated way of understanding specific supply anddemand characteristics of a primary market area. Thismethod begins by identifying the age and incomequalified portion of the population. Whereas thepenetration analysis utilizes the 75+ population, thisanalysis utilizes the 65+ population.

Though it is not typical for people between the ages of65 to 74 to require ADL (Assistance with Activities ofDaily Living) services, this demographic is included inthis analysis. Hence, this analysis considers the 65 to85+ age cohort as age-qualified demand.

In order to understand the base income requirement,the minimum rent charged for each care level from acompetitive set should be utilized.

The base rent represents the lowest rent charged inthe market, respective of the subject’s property type,which is utilized to income-qualify the populationbased.

31 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

Case Study – Proposed Memory Care AdditionMARKET ANALYSIS

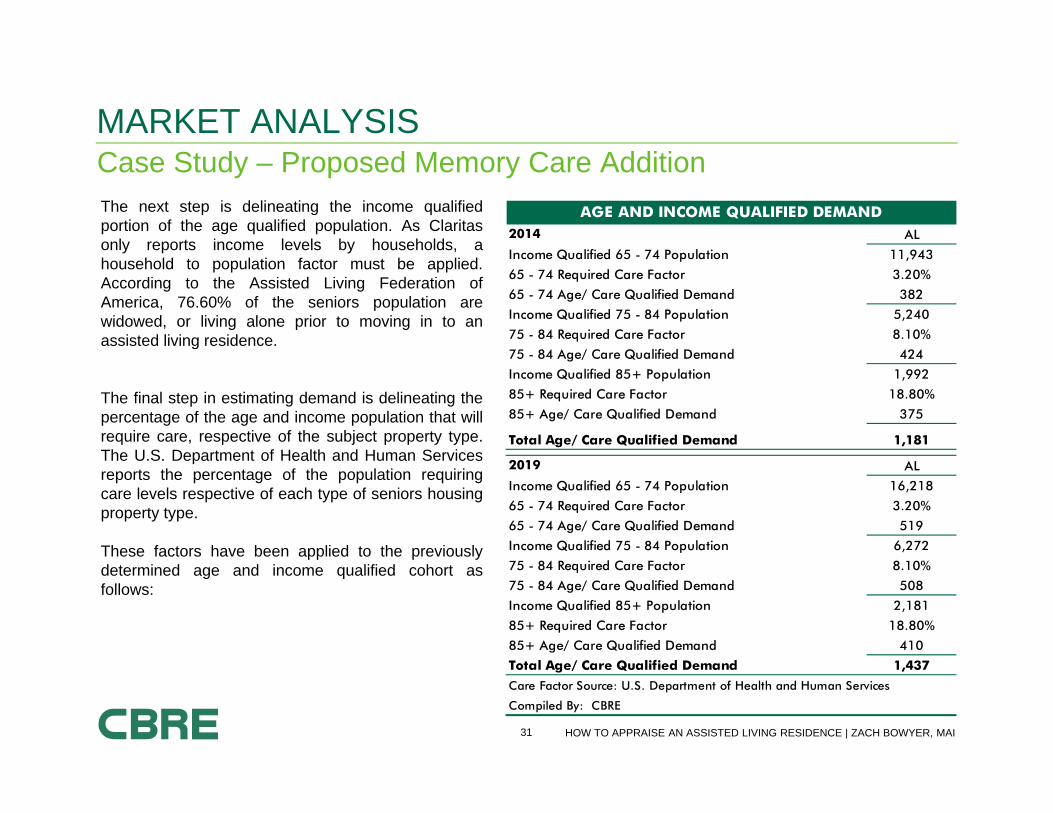

2014 AL

Income Qualified 65 - 74 Population 11,943

65 - 74 Required Care Factor 3.20%

65 - 74 Age/ Care Qualified Demand 382

Income Qualified 75 - 84 Population 5,240

75 - 84 Required Care Factor 8.10%

75 - 84 Age/ Care Qualified Demand 424

Income Qualified 85+ Population 1,992

85+ Required Care Factor 18.80%

85+ Age/ Care Qualified Demand 375

Total Age/ Care Qualified Demand 1,181

AGE AND INCOME QUALIFIED DEMAND

2019 AL

Income Qualified 65 - 74 Population 16,218

65 - 74 Required Care Factor 3.20%

65 - 74 Age/ Care Qualified Demand 519

Income Qualified 75 - 84 Population 6,272

75 - 84 Required Care Factor 8.10%

75 - 84 Age/ Care Qualified Demand 508

Income Qualified 85+ Population 2,181

85+ Required Care Factor 18.80%

85+ Age/ Care Qualified Demand 410

Total Age/ Care Qualified Demand 1,437

Care Factor Source: U.S. Department of Health and Human Services

Compiled By: CBRE

The next step is delineating the income qualifiedportion of the age qualified population. As Claritasonly reports income levels by households, ahousehold to population factor must be applied.According to the Assisted Living Federation ofAmerica, 76.60% of the seniors population arewidowed, or living alone prior to moving in to anassisted living residence.

The final step in estimating demand is delineating thepercentage of the age and income population that willrequire care, respective of the subject property type.The U.S. Department of Health and Human Servicesreports the percentage of the population requiringcare levels respective of each type of seniors housingproperty type.

These factors have been applied to the previouslydetermined age and income qualified cohort asfollows:

32 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

Case Study – Proposed Memory Care AdditionMARKET ANALYSIS

2014 AL

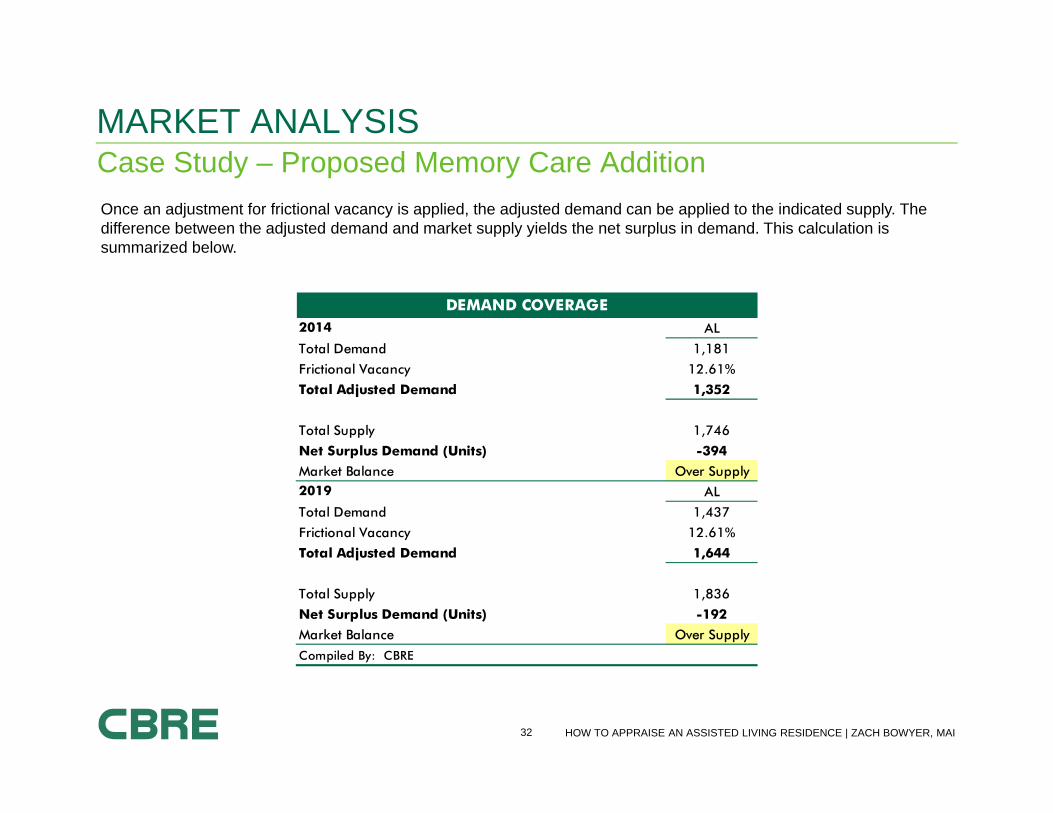

Total Demand 1,181

Frictional Vacancy 12.61%

Total Adjusted Demand 1,352

Total Supply 1,746

Net Surplus Demand (Units) -394

Market Balance Over Supply2019 AL

Total Demand 1,437

Frictional Vacancy 12.61%

Total Adjusted Demand 1,644

Total Supply 1,836

Net Surplus Demand (Units) -192

Market Balance Over Supply

Compiled By: CBRE

DEMAND COVERAGE

Once an adjustment for frictional vacancy is applied, the adjusted demand can be applied to the indicated supply. The difference between the adjusted demand and market supply yields the net surplus in demand. This calculation is summarized below.

33 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

Case Study – Proposed Memory Care AdditionMARKET ANALYSIS

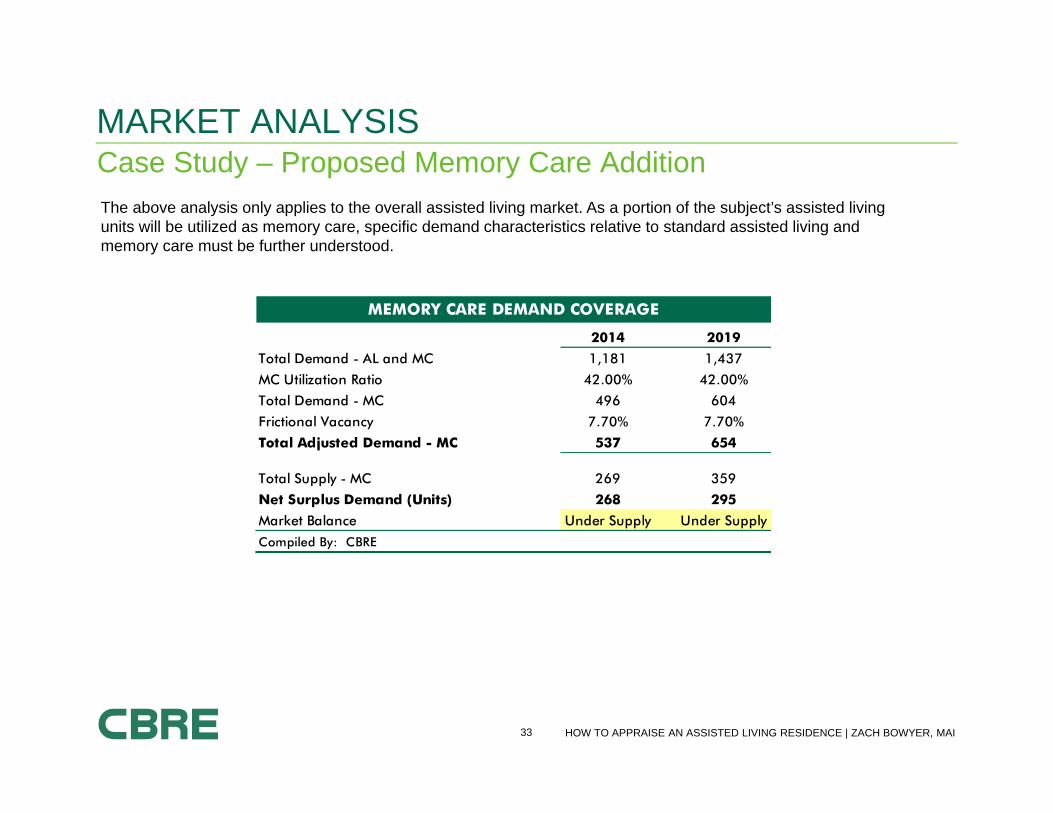

2014 2019

Total Demand - AL and MC 1,181 1,437

MC Utilization Ratio 42.00% 42.00%

Total Demand - MC 496 604

Frictional Vacancy 7.70% 7.70%

Total Adjusted Demand - MC 537 654

Total Supply - MC 269 359

Net Surplus Demand (Units) 268 295

Market Balance Under Supply Under Supply

Compiled By: CBRE

MEMORY CARE DEMAND COVERAGE

The above analysis only applies to the overall assisted living market. As a portion of the subject’s assisted living units will be utilized as memory care, specific demand characteristics relative to standard assisted living and memory care must be further understood.

34 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

Case Study – Proposed Memory Care AdditionMARKET ANALYSIS

Market Conclusion ?

A penetration analysis and a demand coverage analysis were performed. Each analyses is independent of the other, witheach yielding similar conclusions. Based on this analysis, the overall assisted living market is considered to be highlycompetitive and slightly saturated. However, there does appear to be significant unmet demand for Memory Care.

This analysis does conclude that sufficient market demand does exist to support the proposed Memory Care addition. Asdetailed above, net demand actually increases with the addition of the subject and the other memory care property that iscurrently under construction.

The location of the subject with favorable economic and population trends, along with superior physical and operationalattributes, being located adjacent to an existing independent and assisted living community (Harvard Square) suggestthat the subject will capture the appropriate share of the market to obtain a stabilized occupancy level above, or at thehigh end, of current market indications for stabilized memory care properties.

35 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

Industry Overview

Valuation Overview

Market Analysis

Income Approach Sales Comparison Approach

Allocation of the Going Concern

Flags and Considerations for Assessment Purposes

How to Appraise an Assisted Living ResidencePRESENTATION OVERVIEW

36 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

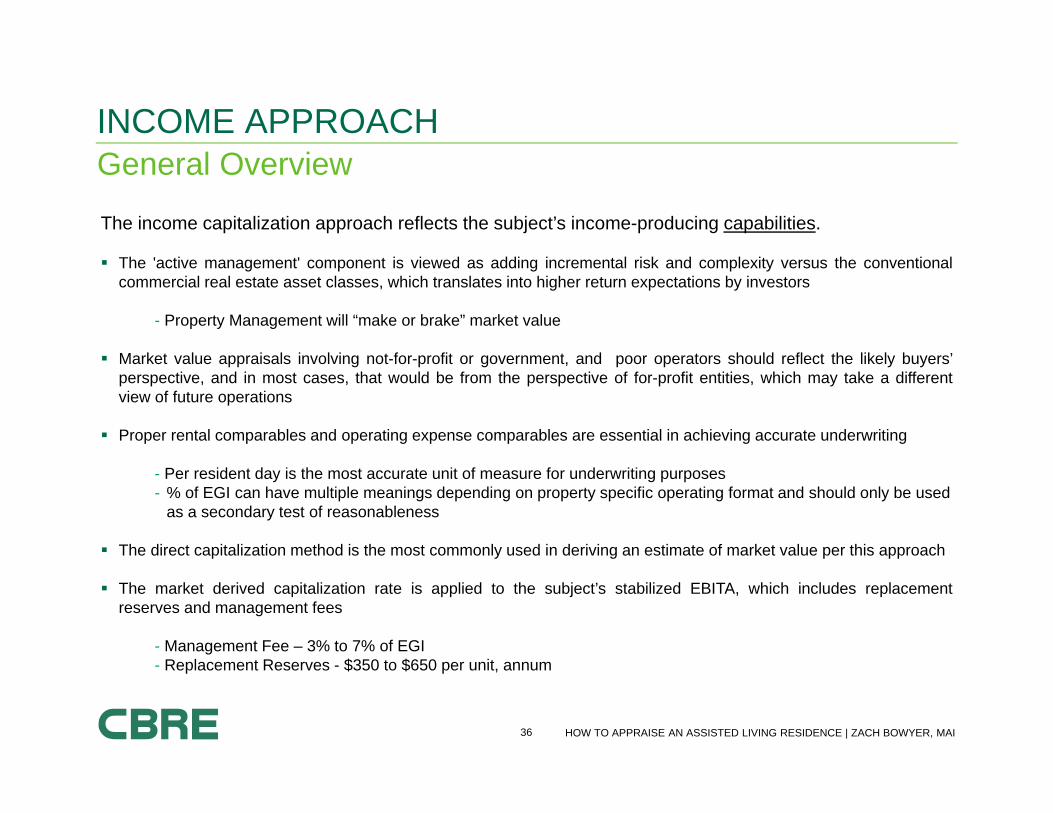

General OverviewINCOME APPROACH

The income capitalization approach reflects the subject’s income-producing capabilities.

The 'active management' component is viewed as adding incremental risk and complexity versus the conventionalcommercial real estate asset classes, which translates into higher return expectations by investors

- Property Management will “make or brake” market value

Market value appraisals involving not-for-profit or government, and poor operators should reflect the likely buyers’perspective, and in most cases, that would be from the perspective of for-profit entities, which may take a differentview of future operations

Proper rental comparables and operating expense comparables are essential in achieving accurate underwriting

- Per resident day is the most accurate unit of measure for underwriting purposes- % of EGI can have multiple meanings depending on property specific operating format and should only be used

as a secondary test of reasonableness

The direct capitalization method is the most commonly used in deriving an estimate of market value per this approach

The market derived capitalization rate is applied to the subject’s stabilized EBITA, which includes replacementreserves and management fees

- Management Fee – 3% to 7% of EGI- Replacement Reserves - $350 to $650 per unit, annum

37 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

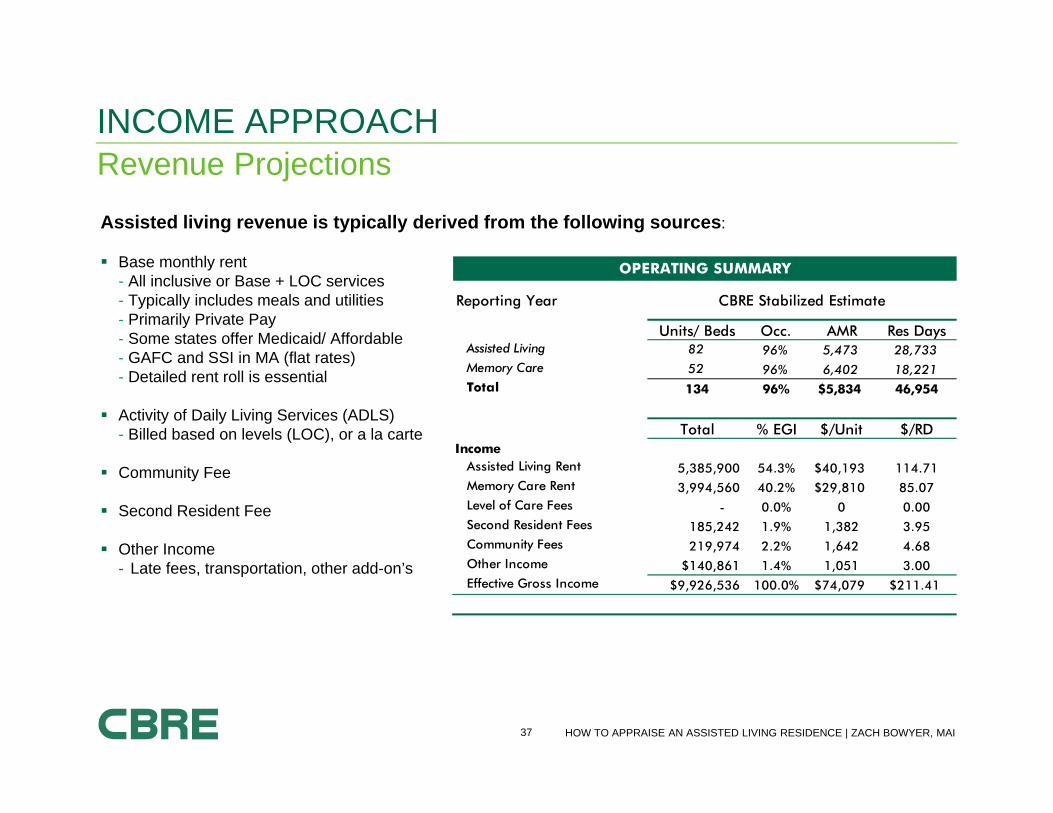

Revenue ProjectionsINCOME APPROACH

Assisted living revenue is typically derived from the following sources:

Base monthly rent- All inclusive or Base + LOC services- Typically includes meals and utilities- Primarily Private Pay- Some states offer Medicaid/ Affordable - GAFC and SSI in MA (flat rates)- Detailed rent roll is essential

Activity of Daily Living Services (ADLS)- Billed based on levels (LOC), or a la carte

Community Fee

Second Resident Fee

Other Income- Late fees, transportation, other add-on’s

OPERATING SUMMARY

Reporting Year

Units/ Beds Occ. AMR Res DaysAssisted Living 82 96% 5,473 28,733Memory Care 52 96% 6,402 18,221Total 134 96% $5,834 46,954

Total % EGI $/Unit $/RDIncome

Assisted Living Rent 5,385,900 54.3% $40,193 114.71Memory Care Rent 3,994,560 40.2% $29,810 85.07Level of Care Fees - 0.0% 0 0.00Second Resident Fees 185,242 1.9% 1,382 3.95Community Fees 219,974 2.2% 1,642 4.68Other Income $140,861 1.4% 1,051 3.00Effective Gross Income $9,926,536 100.0% $74,079 $211.41

CBRE Stabilized Estimate

38 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

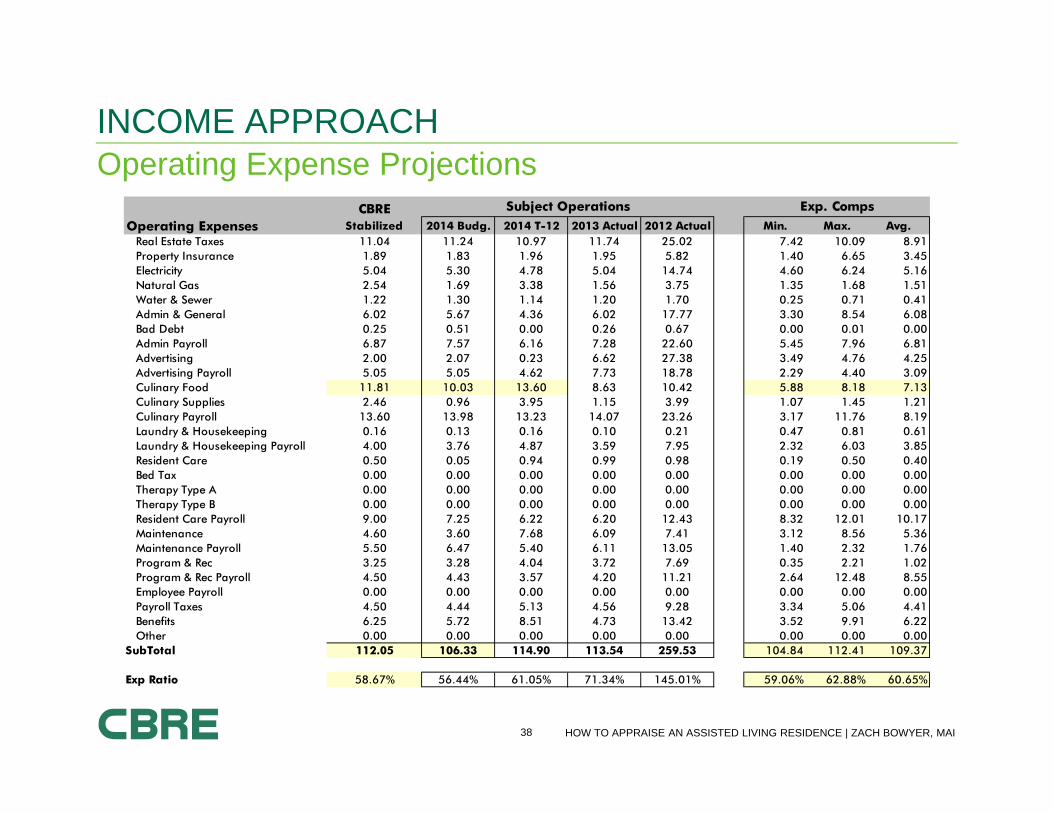

Operating Expense ProjectionsINCOME APPROACH

CBREOperating Expenses Stabilized 2014 Budg. 2014 T-12 2013 Actual 2012 Actual Min. Max. Avg.

Real Estate Taxes 11.04 11.24 10.97 11.74 25.02 7.42 10.09 8.91Property Insurance 1.89 1.83 1.96 1.95 5.82 1.40 6.65 3.45Electricity 5.04 5.30 4.78 5.04 14.74 4.60 6.24 5.16Natural Gas 2.54 1.69 3.38 1.56 3.75 1.35 1.68 1.51Water & Sewer 1.22 1.30 1.14 1.20 1.70 0.25 0.71 0.41Admin & General 6.02 5.67 4.36 6.02 17.77 3.30 8.54 6.08Bad Debt 0.25 0.51 0.00 0.26 0.67 0.00 0.01 0.00Admin Payroll 6.87 7.57 6.16 7.28 22.60 5.45 7.96 6.81Advertising 2.00 2.07 0.23 6.62 27.38 3.49 4.76 4.25Advertising Payroll 5.05 5.05 4.62 7.73 18.78 2.29 4.40 3.09Culinary Food 11.81 10.03 13.60 8.63 10.42 5.88 8.18 7.13Culinary Supplies 2.46 0.96 3.95 1.15 3.99 1.07 1.45 1.21Culinary Payroll 13.60 13.98 13.23 14.07 23.26 3.17 11.76 8.19Laundry & Housekeeping 0.16 0.13 0.16 0.10 0.21 0.47 0.81 0.61Laundry & Housekeeping Payroll 4.00 3.76 4.87 3.59 7.95 2.32 6.03 3.85Resident Care 0.50 0.05 0.94 0.99 0.98 0.19 0.50 0.40Bed Tax 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00Therapy Type A 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00Therapy Type B 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00Resident Care Payroll 9.00 7.25 6.22 6.20 12.43 8.32 12.01 10.17Maintenance 4.60 3.60 7.68 6.09 7.41 3.12 8.56 5.36Maintenance Payroll 5.50 6.47 5.40 6.11 13.05 1.40 2.32 1.76Program & Rec 3.25 3.28 4.04 3.72 7.69 0.35 2.21 1.02Program & Rec Payroll 4.50 4.43 3.57 4.20 11.21 2.64 12.48 8.55Employee Payroll 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00Payroll Taxes 4.50 4.44 5.13 4.56 9.28 3.34 5.06 4.41Benefits 6.25 5.72 8.51 4.73 13.42 3.52 9.91 6.22Other 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

SubTotal 112.05 106.33 114.90 113.54 259.53 104.84 112.41 109.37

Exp Ratio 58.67% 56.44% 61.05% 71.34% 145.01% 59.06% 62.88% 60.65%

Exp. CompsSubject Operations

39 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

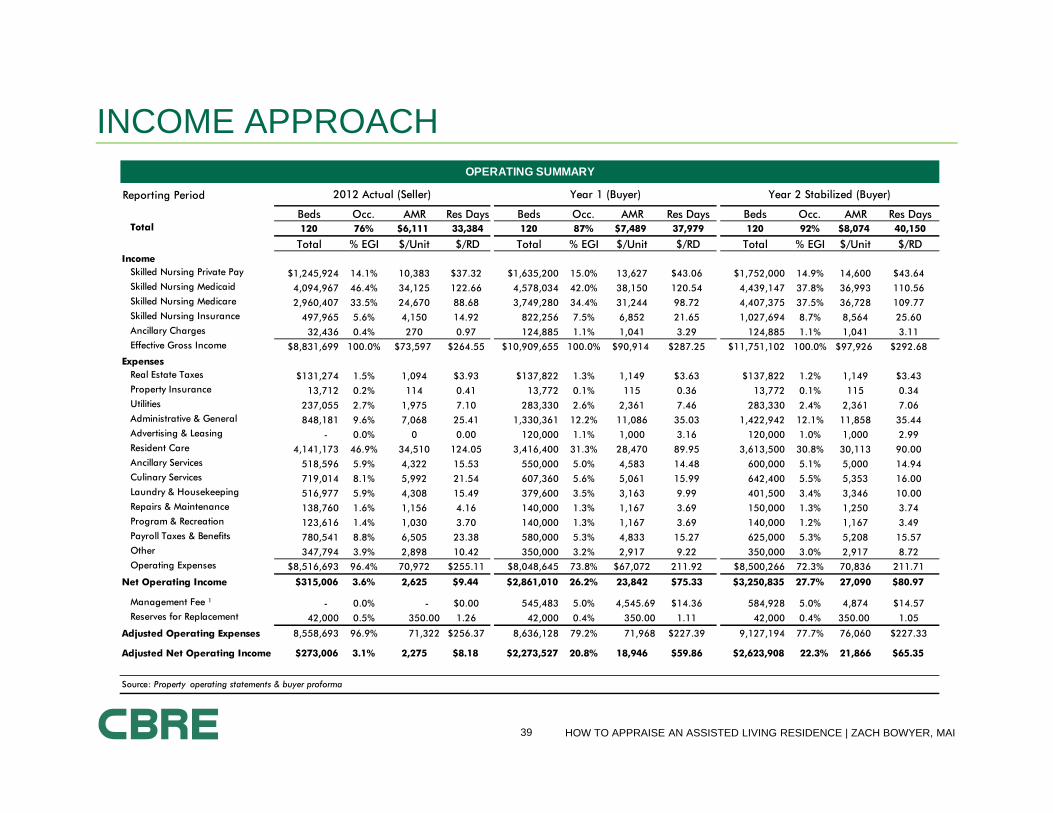

INCOME APPROACHOPERATING SUMMARY

Reporting Period

Beds Occ. AMR Res Days Beds Occ. AMR Res Days Beds Occ. AMR Res DaysTotal 120 76% $6,111 33,384 120 87% $7,489 37,979 120 92% $8,074 40,150

Total % EGI $/Unit $/RD Total % EGI $/Unit $/RD Total % EGI $/Unit $/RDIncome

Skilled Nursing Private Pay $1,245,924 14.1% 10,383 $37.32 $1,635,200 15.0% 13,627 $43.06 $1,752,000 14.9% 14,600 $43.64Skilled Nursing Medicaid 4,094,967 46.4% 34,125 122.66 4,578,034 42.0% 38,150 120.54 4,439,147 37.8% 36,993 110.56Skilled Nursing Medicare 2,960,407 33.5% 24,670 88.68 3,749,280 34.4% 31,244 98.72 4,407,375 37.5% 36,728 109.77Skilled Nursing Insurance 497,965 5.6% 4,150 14.92 822,256 7.5% 6,852 21.65 1,027,694 8.7% 8,564 25.60Ancillary Charges 32,436 0.4% 270 0.97 124,885 1.1% 1,041 3.29 124,885 1.1% 1,041 3.11Effective Gross Income $8,831,699 100.0% $73,597 $264.55 $10,909,655 100.0% $90,914 $287.25 $11,751,102 100.0% $97,926 $292.68

ExpensesReal Estate Taxes $131,274 1.5% 1,094 $3.93 $137,822 1.3% 1,149 $3.63 $137,822 1.2% 1,149 $3.43Property Insurance 13,712 0.2% 114 0.41 13,772 0.1% 115 0.36 13,772 0.1% 115 0.34Utilities 237,055 2.7% 1,975 7.10 283,330 2.6% 2,361 7.46 283,330 2.4% 2,361 7.06Administrative & General 848,181 9.6% 7,068 25.41 1,330,361 12.2% 11,086 35.03 1,422,942 12.1% 11,858 35.44Advertising & Leasing - 0.0% 0 0.00 120,000 1.1% 1,000 3.16 120,000 1.0% 1,000 2.99Resident Care 4,141,173 46.9% 34,510 124.05 3,416,400 31.3% 28,470 89.95 3,613,500 30.8% 30,113 90.00Ancillary Services 518,596 5.9% 4,322 15.53 550,000 5.0% 4,583 14.48 600,000 5.1% 5,000 14.94Culinary Services 719,014 8.1% 5,992 21.54 607,360 5.6% 5,061 15.99 642,400 5.5% 5,353 16.00Laundry & Housekeeping 516,977 5.9% 4,308 15.49 379,600 3.5% 3,163 9.99 401,500 3.4% 3,346 10.00Repairs & Maintenance 138,760 1.6% 1,156 4.16 140,000 1.3% 1,167 3.69 150,000 1.3% 1,250 3.74Program & Recreation 123,616 1.4% 1,030 3.70 140,000 1.3% 1,167 3.69 140,000 1.2% 1,167 3.49Payroll Taxes & Benefits 780,541 8.8% 6,505 23.38 580,000 5.3% 4,833 15.27 625,000 5.3% 5,208 15.57Other 347,794 3.9% 2,898 10.42 350,000 3.2% 2,917 9.22 350,000 3.0% 2,917 8.72Operating Expenses $8,516,693 96.4% 70,972 $255.11 $8,048,645 73.8% $67,072 211.92 $8,500,266 72.3% 70,836 211.71

Net Operating Income $315,006 3.6% 2,625 $9.44 $2,861,010 26.2% 23,842 $75.33 $3,250,835 27.7% 27,090 $80.97

Management Fee ¹ - 0.0% - $0.00 545,483 5.0% 4,545.69 $14.36 584,928 5.0% 4,874 $14.57Reserves for Replacement 42,000 0.5% 350.00 1.26 42,000 0.4% 350.00 1.11 42,000 0.4% 350.00 1.05

Adjusted Operating Expenses 8,558,693 96.9% 71,322 $256.37 8,636,128 79.2% 71,968 $227.39 9,127,194 77.7% 76,060 $227.33

Adjusted Net Operating Income $273,006 3.1% 2,275 $8.18 $2,273,527 20.8% 18,946 $59.86 $2,623,908 22.3% 21,866 $65.35

Source: Property operating statements & buyer proforma

2012 Actual (Seller) Year 1 (Buyer) Year 2 Stabilized (Buyer)

40 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

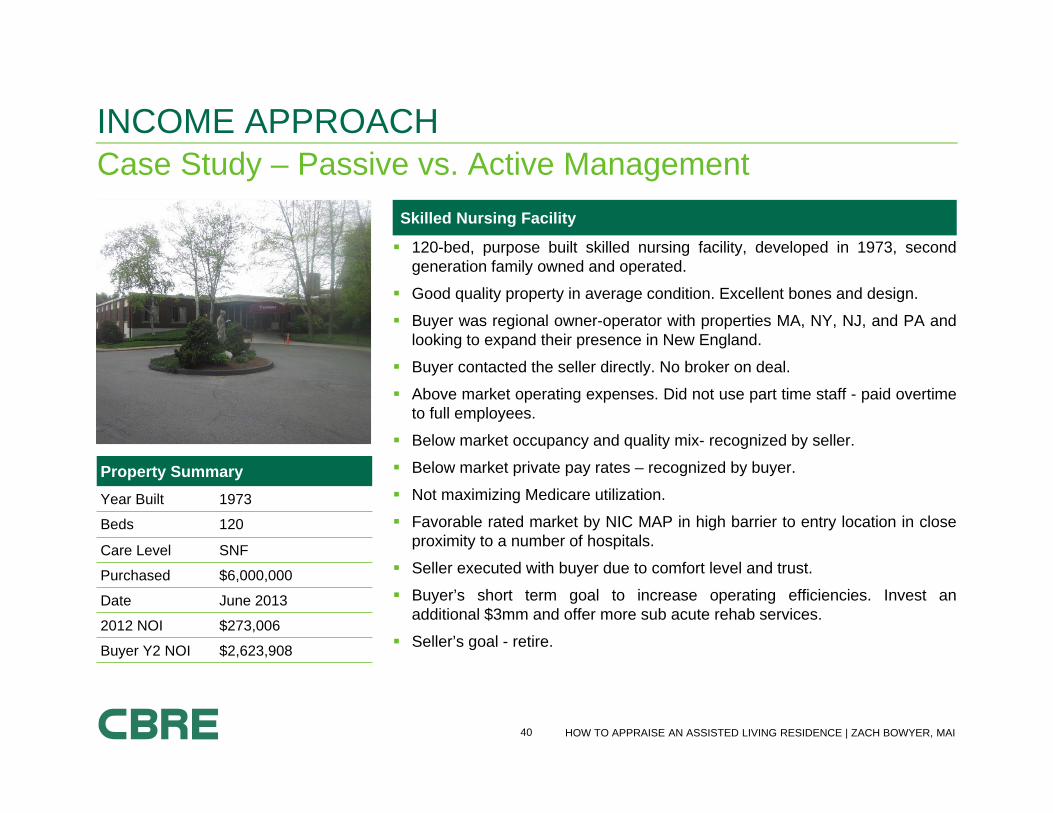

Case Study – Passive vs. Active ManagementINCOME APPROACH

Skilled Nursing Facility

120-bed, purpose built skilled nursing facility, developed in 1973, secondgeneration family owned and operated.

Good quality property in average condition. Excellent bones and design.

Buyer was regional owner-operator with properties MA, NY, NJ, and PA andlooking to expand their presence in New England.

Buyer contacted the seller directly. No broker on deal.

Above market operating expenses. Did not use part time staff - paid overtimeto full employees.

Below market occupancy and quality mix- recognized by seller.

Below market private pay rates – recognized by buyer.

Not maximizing Medicare utilization.

Favorable rated market by NIC MAP in high barrier to entry location in closeproximity to a number of hospitals.

Seller executed with buyer due to comfort level and trust.

Buyer’s short term goal to increase operating efficiencies. Invest anadditional $3mm and offer more sub acute rehab services.

Seller’s goal - retire.

Property SummaryYear Built 1973

Beds 120

Care Level SNF

Purchased $6,000,000

Date June 2013

2012 NOI $273,006

Buyer Y2 NOI $2,623,908

41 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

Case Study – Revenue ProjectionsINCOME APPROACH

Occupancy Census Mix

Daily Private Pay Rates Effective Gross Income Per Resident Day

61% 60% 59% 57%

14% 11% 13% 13%

17% 21% 19% 22%

8% 8% 9% 8%

0%

20%

40%

60%

80%

100%

Subject Comps Buyer Current

Other

Medicare

Private

Medicaid

$270

$320

$278

$375

$363

$265

$100 $150 $200 $250 $300 $350 $400

Current

Buyer

NIC 31

NIC Metro

Comps

Subject

$265 $262$296 $273 $293 $293

$100

$150

$200

$250

$300

Subject Comp Min. Comp Max.Comp Avg. Buyer Current

85.00%

92.00%

91.40%

90.10%

91.00%

76.00%

20% 40% 60% 80% 100%

Current

Buyer

NIC 31

NIC Metro

Comps

Subject

“Subject “data points represent the seller’s 2012 Actual. “Current” represents the buyer’s October 2013 Actual

42 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

Case Study – Expense Projections and NOIINCOME APPROACH

Operating Costs Per Resident Day (PRD) Expense Ratio (Before Mgt Fee & Reserves)

Profit Margin (Before Mgt Fee & Reserves) NOI PRD (Before Mgt Fee & Reserves)

16.00%

27.70%

8.60%

22.40%

17.80%

3.60%

0% 5% 10% 15% 20% 25% 30% 35%

Current

Buyer

Comp Min.

Comp Max.

Comp Avg.

Subject

$8

$32

$59

$36

$60$40

$0$10$20$30$40$50$60$70

Subject Comp Min.Comp Max.Comp Avg. Buyer Current

$253.12

$211.92

$228.06

$240.32

$204.39

$255.51

$100 $150 $200 $250 $300 $350

Current

Buyer

Comp Avg.

Comp Max.

Comp Min.

Subject

97%78% 81% 83% 72% 84%

0%

20%

40%

60%

80%

100%

Subject Comp Min.Comp Max.Comp Avg. Buyer Current

“Subject “data points represent the seller’s 2012 Actual. “Current” represents the buyer’s October 2013 Actual

43 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

Case Study - ResultsINCOME APPROACH

At Purchase(June 2013)

Current (Oct 2013 Ann.) Buyer’s Stabilized

NOI $273,006 $1,108,218 $2,623,908

Purchase Price $6,000,000 $6,000,000 $6,000,000

CapEx & Cary --- --- $3,000,000

Total Cost --- $6,000,000 $9,000,000

Indicated Value @ NIC Average Cap Rate

N/A$50,000/ Bed

$8,500,000$71,000/ bed

$20,200,000$168k/ bed

Return on Cost 4.55% 18.47% 29.15%

The “current” data points detailed in the following table represents four months of property operations by the buyer.

44 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

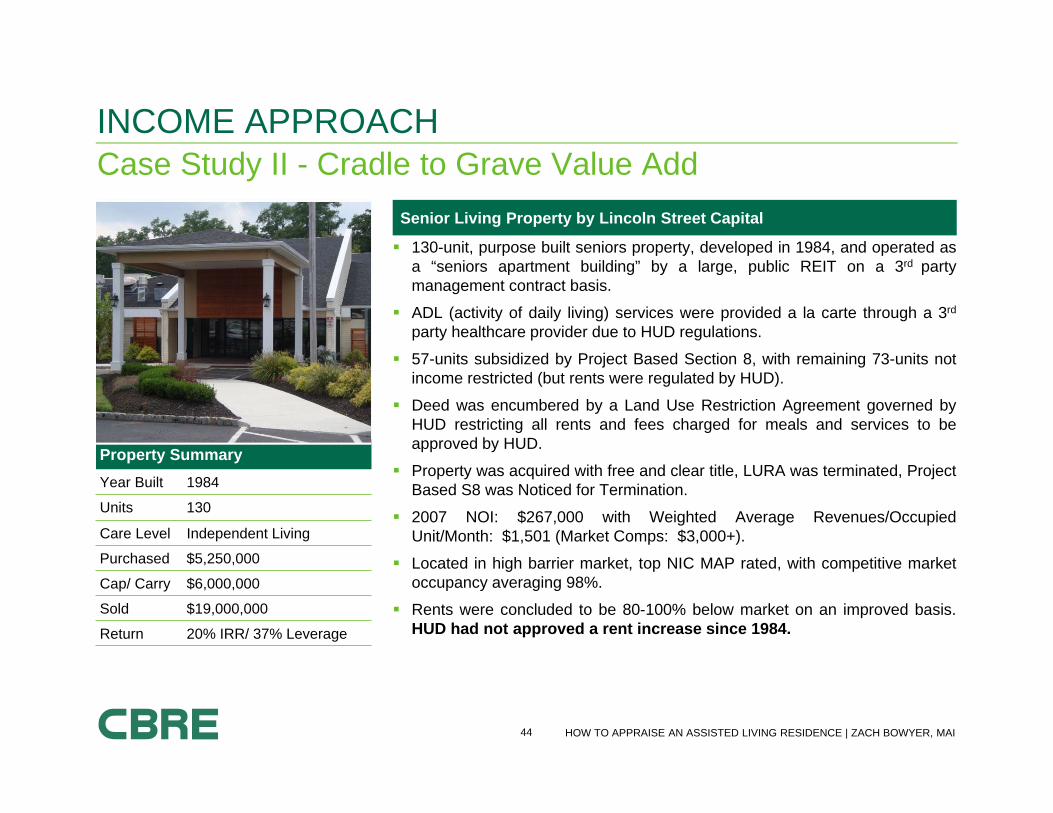

Case Study II - Cradle to Grave Value AddINCOME APPROACH

Senior Living Property by Lincoln Street Capital

130-unit, purpose built seniors property, developed in 1984, and operated asa “seniors apartment building” by a large, public REIT on a 3rd partymanagement contract basis.

ADL (activity of daily living) services were provided a la carte through a 3rd

party healthcare provider due to HUD regulations.

57-units subsidized by Project Based Section 8, with remaining 73-units notincome restricted (but rents were regulated by HUD).

Deed was encumbered by a Land Use Restriction Agreement governed byHUD restricting all rents and fees charged for meals and services to beapproved by HUD.

Property was acquired with free and clear title, LURA was terminated, ProjectBased S8 was Noticed for Termination.

2007 NOI: $267,000 with Weighted Average Revenues/OccupiedUnit/Month: $1,501 (Market Comps: $3,000+).

Located in high barrier market, top NIC MAP rated, with competitive marketoccupancy averaging 98%.

Rents were concluded to be 80-100% below market on an improved basis.HUD had not approved a rent increase since 1984.

Property SummaryYear Built 1984

Units 130

Care Level Independent Living

Purchased $5,250,000

Cap/ Carry $6,000,000

Sold $19,000,000

Return 20% IRR/ 37% Leverage

45 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

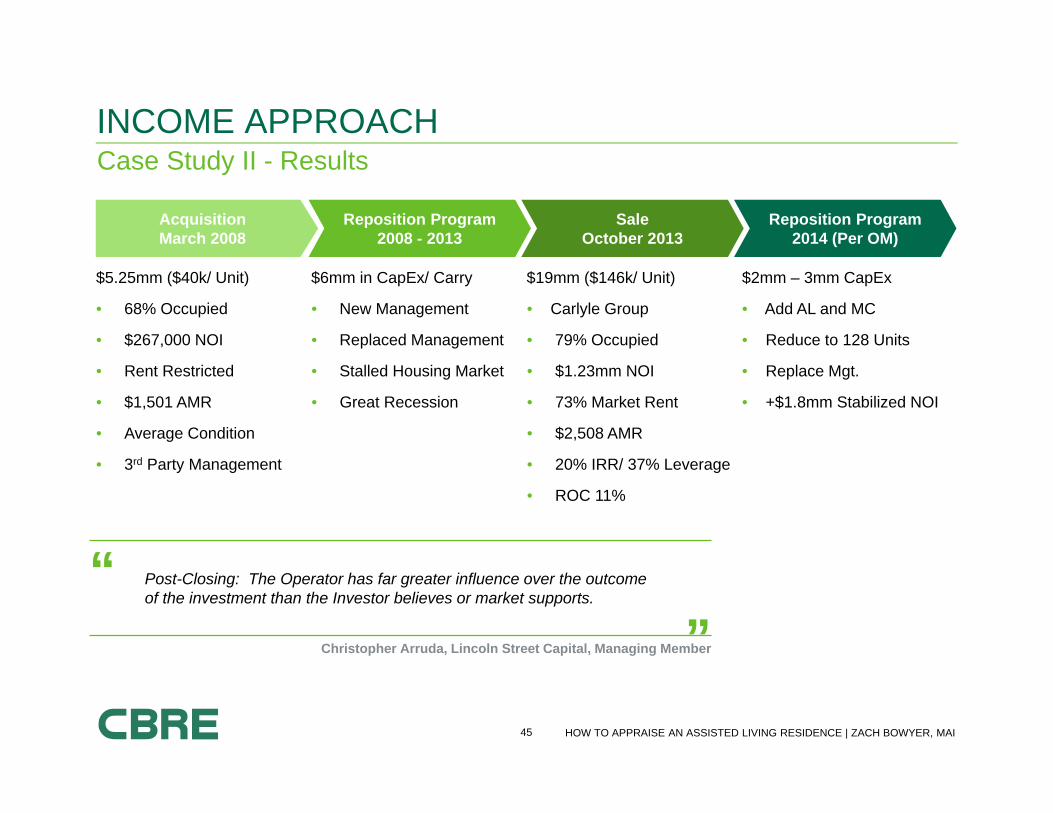

Case Study II - ResultsINCOME APPROACH

$5.25mm ($40k/ Unit)

• 68% Occupied

• $267,000 NOI

• Rent Restricted

• $1,501 AMR

• Average Condition

• 3rd Party Management

$6mm in CapEx/ Carry

• New Management

• Replaced Management

• Stalled Housing Market

• Great Recession

$19mm ($146k/ Unit)

• Carlyle Group

• 79% Occupied

• $1.23mm NOI

• 73% Market Rent

• $2,508 AMR

• 20% IRR/ 37% Leverage

• ROC 11%

$2mm – 3mm CapEx

• Add AL and MC

• Reduce to 128 Units

• Replace Mgt.

• +$1.8mm Stabilized NOI

AcquisitionMarch 2008

Reposition Program2008 - 2013

SaleOctober 2013

Reposition Program2014 (Per OM)

“ Post-Closing: The Operator has far greater influence over the outcome of the investment than the Investor believes or market supports.

”Christopher Arruda, Lincoln Street Capital, Managing Member

46 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

Summary of Operating MetricsINCOME APPROACH

IL AL CCRC SNFOccupancy (4Q13) 92% 91% 89% 87.6%

Average Length of Stay 29.2 Months 21.7 Months 71 Months 3.2 Months

Total Revenues PRD $72.07 $151.55 $137.12 $268.93

Operating Expenses PRD $44.39 $104.67 $95.51 $232.23

Operating Margin 38.4% 30.9% 30.3% 13.6%

Average FTE PRD 0.22 0.45 0.48 0.98

Debt Coverage Ratios 1.5 2.0 --- ---

ROI (Unleveraged) 6.5% 8.6% --- 14.8%

Change in OM (1994-2011) 29.37% 31.6% --- ---

Source: NIC MAP, American Seniors Housing Assoc., & Irving Levin Assoc., CBRE Healthcare Investor Survey

Per Resident Day (PRD) is the most accurate unit of measure when underwriting a seniors housing property type. Expense ratio, profit margin, and per unit indicators are all used as secondary measures.

47 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

Industry Overview

Valuation Overview

Market Analysis

Income Approach

Sales Comparison Approach Allocation of the Going Concern

Final Considerations

How to Appraise an Assisted Living ResidencePRESENTATION OVERVIEW

48 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

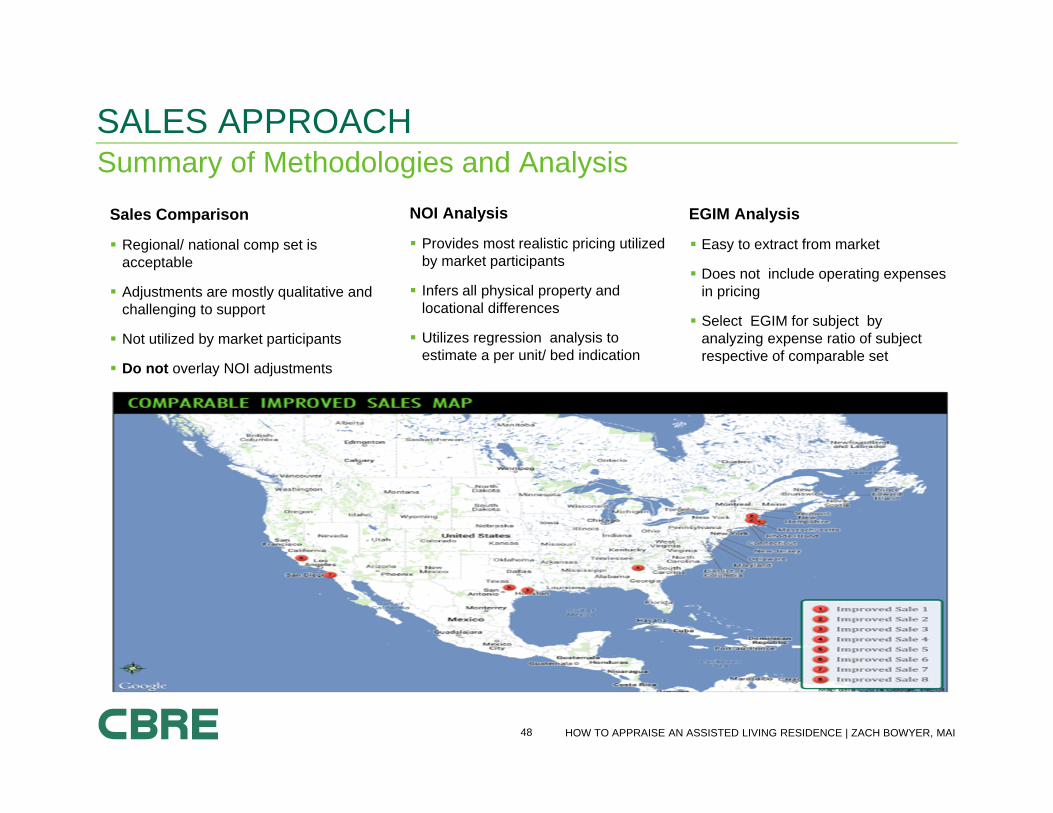

Summary of Methodologies and AnalysisSALES APPROACH

Sales Comparison

Regional/ national comp set is acceptable

Adjustments are mostly qualitative and challenging to support

Not utilized by market participants

Do not overlay NOI adjustments

NOI Analysis

Provides most realistic pricing utilized by market participants

Infers all physical property and locational differences

Utilizes regression analysis to estimate a per unit/ bed indication

EGIM Analysis

Easy to extract from market

Does not include operating expenses in pricing

Select EGIM for subject by analyzing expense ratio of subject respective of comparable set

49 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

Sales ComparisonSALES APPROACH

SENIORS HOUSING SALES ADJUSTMENT GRID

Comparable Number 1 2 3 4 5 6 7 8

Transaction Type Sale Sale Sale Sale Sale Sale Sale SaleTransaction Date Feb-13 Jan-13 Feb-12 Jan-14 Oct-13 Sep-13 Feb-14 Nov-11

Year Built 2000 1999 2003 2009 2009 1999 2001 2009

No. Units 640 172 70 185 149 193 293 140Adjusted Sale Price 1 $289,999,831 $72,000,000 $32,500,000 $71,250,000 $59,000,000 $63,500,000 $104,500,000 $69,500,000Price Per Unit 1 $453,125 $418,605 $464,286 $385,135 $395,973 $329,016 $356,655 $496,429

Occupancy 92% 90% 95% 98% 95% 97% 98% 93%

NOI Per Unit $29,121 $27,218 $30,178 $25,810 $21,317 $20,234 $22,184 $33,508

OAR 6.43% 6.50% 6.50% 6.70% 5.38% 6.15% 6.22% 6.75%Adj. Price Per Unit $453,125 $418,605 $464,286 $385,135 $395,973 $329,016 $356,655 $496,429

Property Rights Conveyed 0% 0% 0% 0% 0% 0% 0% 0%Financing Terms 1 0% 0% 0% 0% 0% 0% 0% 0%

Conditions of Sale 0% 0% 0% 0% 0% 0% 0% 0%

Market Conditions (Time) 0% 0% 0% 0% 0% 0% 0% 3%Subtotal - Price Per Unit $453,125 $418,605 $464,286 $385,135 $395,973 $329,016 $356,655 $511,322

Location 0% 10% 0% 10% 10% 10% 10% 0%

Project Size 0% 0% 0% 0% 0% 0% 0% 0%

Age/Condition 10% 10% 10% 0% 0% 10% 10% 0%

Quality of Construction 0% 0% 0% 0% 0% 10% 0% 0%

Avg. Unit Size 0% 0% 0% 0% 0% 0% 0% 0%

Project Amenities 0% 0% 0% 0% 0% 10% 0% 0%

Parking 0% 0% 0% 0% 0% 0% 0% 0%

Other 0% 0% 0% 0% 0% 0% 0% 0%

Total Other Adjustments 10% 20% 10% 10% 10% 40% 20% 0%

Indicated Value Per Unit $498,438 $502,326 $510,715 $423,649 $435,570 $460,622 $427,986 $511,3221 Transaction amount adjusted for cash equivalency and/or deferred maintenance (where applicable)

Compiled by CBRE

50 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

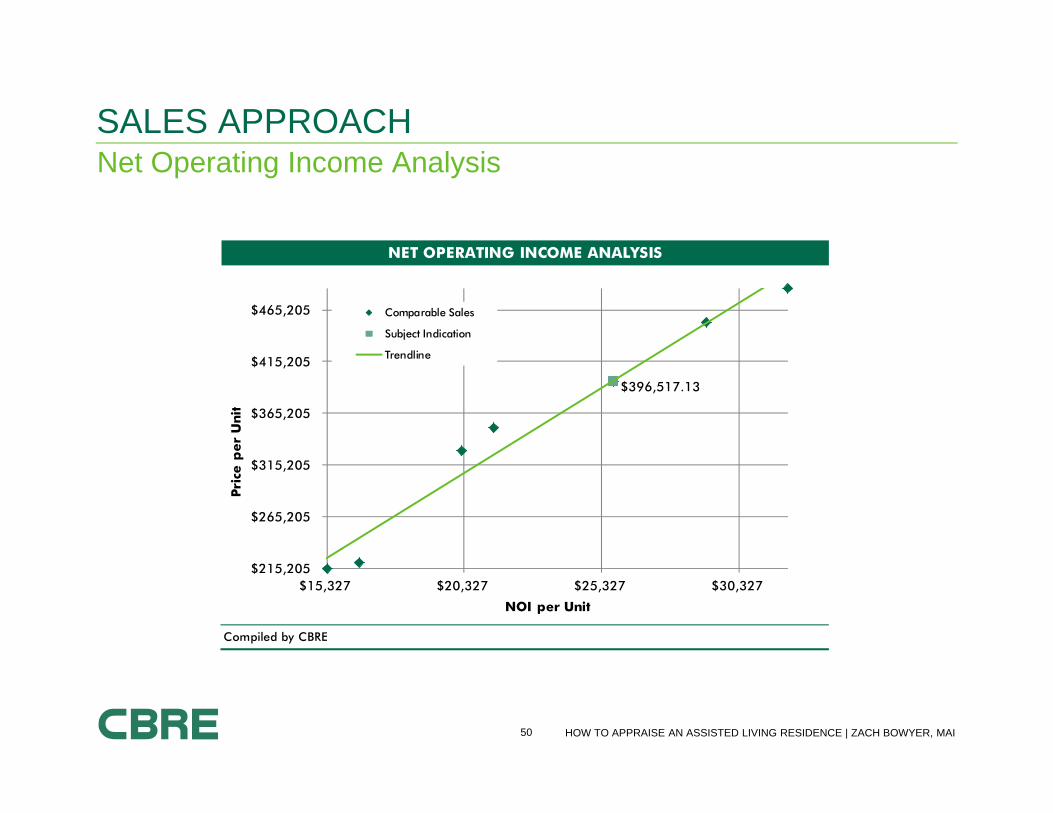

Net Operating Income AnalysisSALES APPROACH

NET OPERATING INCOME ANALYSIS

Compiled by CBRE

$396,517.13

$215,205

$265,205

$315,205

$365,205

$415,205

$465,205

$15,327 $20,327 $25,327 $30,327

Pri

ce p

er

Unit

NOI per Unit

Comparable Sales

Subject Indication

Trendline

51 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

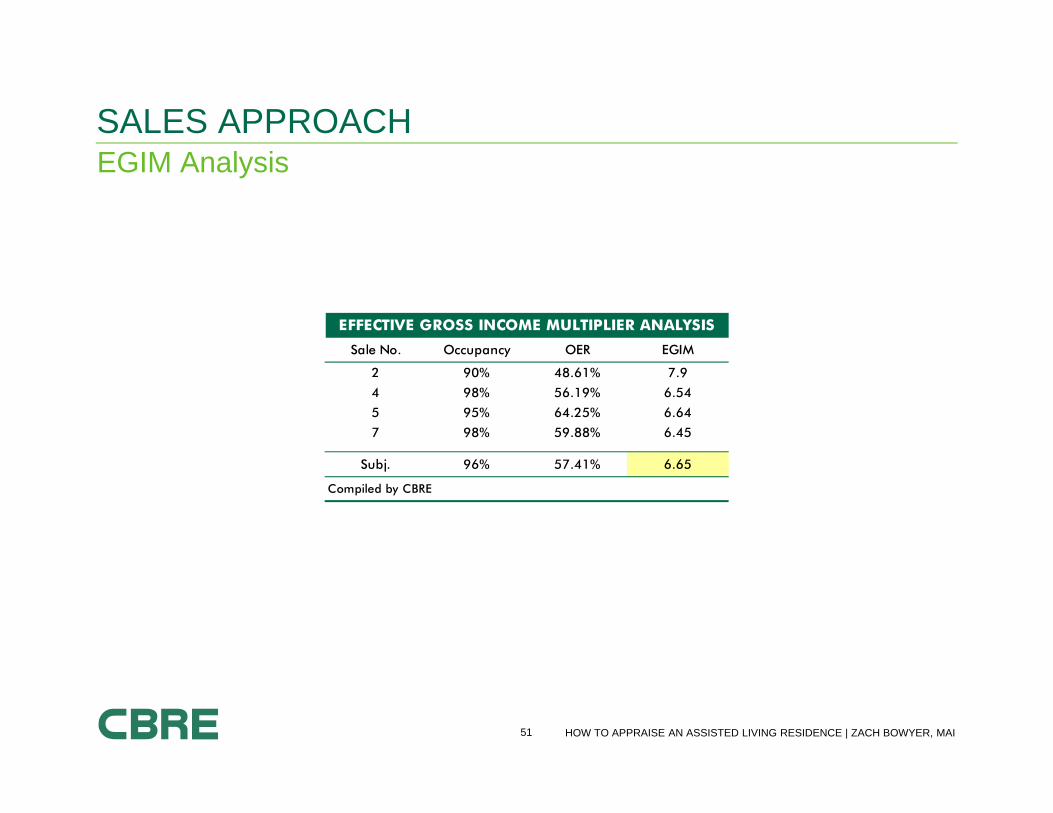

EGIM AnalysisSALES APPROACH

EFFECTIVE GROSS INCOME MULTIPLIER ANALYSIS

Sale No. Occupancy OER EGIM

2 90% 48.61% 7.9

4 98% 56.19% 6.54

5 95% 64.25% 6.64

7 98% 59.88% 6.45

Subj. 96% 57.41% 6.65

Compiled by CBRE

52 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

Single Asset TransactionsSALES APPROACH

Transaction Description

Village at Proprietors Green, Marshfield, MA• 149 units, IL and AL with MC, constructed in 2010• $59,000,000 or $396k per unit• Closed December 2013 to AEW Capital Management• 93% occupied yielding a 6.50% cap rate• Stabilized operations

Forge Hill and Inn at Robbins Brook, Franklin and Acton, MA• 193 units, AL with MC, constructed 1999 and 2002• $63,500,000 or $329k per unit• Closed November 2013 to Benchmark Senior Living JV with Health Care REIT• 93% occupied yielding a 6.15% cap rate, stabilized operations• Purchased by seller 2010 at $222k per unit, 8.00% cap (4.5% YoY)

Longwood Place, Reading, MA• 84 units, 63 AL and 21 MC, constructed in 1939 and converted to AL in 1990s• $16,620,000, $19,870,000 (adjusted) adjusted or $236k per unit• Closed March 2014 to regional developer/ owner/ operator. Seller was local operator• 97% occupied yielding a 9.17% cap rate based on proforma, per reposition• Reposition to add MC for operational value add strategy

53 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

Single Asset TransactionsSALES APPROACH

Transaction Description

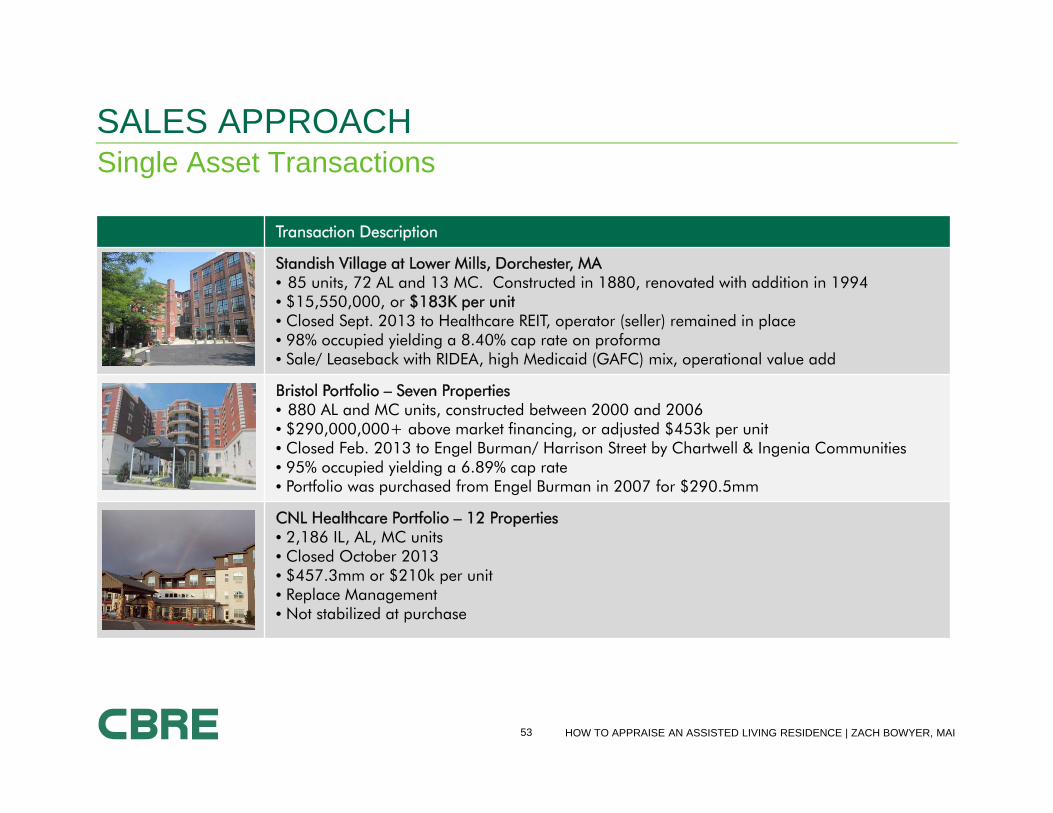

Standish Village at Lower Mills, Dorchester, MA• 85 units, 72 AL and 13 MC. Constructed in 1880, renovated with addition in 1994• $15,550,000, or $183K per unit• Closed Sept. 2013 to Healthcare REIT, operator (seller) remained in place• 98% occupied yielding a 8.40% cap rate on proforma• Sale/ Leaseback with RIDEA, high Medicaid (GAFC) mix, operational value add

Bristol Portfolio – Seven Properties• 880 AL and MC units, constructed between 2000 and 2006• $290,000,000+ above market financing, or adjusted $453k per unit• Closed Feb. 2013 to Engel Burman/ Harrison Street by Chartwell & Ingenia Communities• 95% occupied yielding a 6.89% cap rate• Portfolio was purchased from Engel Burman in 2007 for $290.5mm

CNL Healthcare Portfolio – 12 Properties• 2,186 IL, AL, MC units• Closed October 2013• $457.3mm or $210k per unit• Replace Management• Not stabilized at purchase

54 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

Industry Overview

Valuation Overview

Market Analysis

Income Approach

Sales Comparison Approach

Allocation of the Going Concern Final Considerations

Seniors Housing Valuations & TrendsPRESENTATION OVERVIEW

55 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

MethodologiesALLOCATION OF THE GOING CONCERN

Cost Residual: The value of the business/intangibles are estimated by taking the market value of the subjectand deducting the estimated personal property, land and real estate property value. The remaining valuerepresents the contribution of the business/intangibles.

Pretty straight forward approach

Widely accepted and utilized in the appraisal industry

Utilizes estimates contained in the Cost Approach which is considered the less reliable indication of valueand often omitted due to various physical property attributes

Not utilized by market participants

Management Extraction: Business Enterprise Value is calculated based upon the capitalized value of themanagement fee. The total value of the going concern is calculated with NO deductions for management feesor reserves. The Concluded business value and FF&E are then deducted to get to the real estate onlyallocation.

Additional BEV is inherent in the operations, resulting in a possible omission of this allocation

Capitalization rates applied to the Management Fee are difficult to accurately extract from the market withthe applied rate considered to be highly subjective

Not utilized by market participants

56 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

Methodologies – Lease Coverage AnalysisALLOCATION OF THE GOING CONCERN

Lease Coverage Analysis: A market derived lease coverage ratio is applied to the concluded net operating income forthe subject. The result is an indicated annual market lease payment for the subject. A net lease cap rate is applied to theestimated lease payment in order to obtain the value attributed to the real estate.

Lease Coverage Ratios and Net Lease Cap Rates are easily and accurately extracted from the market

Only arm’s length leases should be utilized – no RIDEA

Know where FF&E fits in. Part of Lease or owned separately by tenant

Market lease coverage rations will range from 1.10 to 1.30 for IL and AL, and 1.50 to 2.00 for SNFs

Net lease cap rates typically fall 200 to 300 bps below a going concern cap rate, all else equal

Higher the coverage, higher the spread (lower risk)

Utilized by market participants

57 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

Methodologies – Lease Coverage AnalysisALLOCATION OF THE GOING CONCERN

As Is on

April 18, 2014

Concluded Stabilized NOI $4,325,432

Divided Lease Coverage Ratio 1.20

Inferred Market Lease Payment (Absolute Net) $3,604,527

Absolute Net Lease Cap Rate 5.75%

Inferred Leased Fee/ Real Property Value $62,687,420

Concluded Market Value of the Going Concern $69,200,000

FF&E $963,125

Inferred Leased Fee/ Real Property Value $62,687,420

Indicated Business Value $5,549,455

LEASE COVERAGE ANALYSIS

As Is on

April 18, 2014

Real Property $62,687,420

FF & E $963,125

Business Value $5,549,455

Market Value of the Going Concern $69,200,000

ALLOCATION OF THE GOING CONCERN

58 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

Industry Overview

Valuation Overview

Market Analysis

Income Approach

Sales Comparison Approach

Allocation of the Going Concern

Final Considerations

How to Appraise an Assisted Living ResidencePRESENTATION OVERVIEW

59 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

FINAL CONSIDERATIONS

Understand the property specific operations and understand the market; understand where yourproperty fits in the market; current property trend lines may not be telling the whole story. There isno one size fits all.

Have boots on the ground and take the time to speak with the competition. The most sophisticatedanalysis is useless of your inputs are not accurate, well researched, and understood.

The appraisal should identify the assets being valued and distinguish the assets not being valuedwith the client in the development of the scope of work and in the report. This should reflect actionstaken by market participants.

Multiple entities often control the total assets of the business. Ownership structure must be fullyunderstood in order to fully understand value appropriate cash flows.

Market value appraisals involving not-for-profit entities or governmental entities should reflect thelikely buyers’ perspective, and in most cases, that would be from the perspective of for-profitentities, which may take a different view of future operations.

Comparable sales should be verified directly with source. Purchase price reported on deeds rarelyreflect the total consideration with only the allocated real estate value being reported.

60 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

FINAL CONSIDERATIONS

Only the specific sub-property type should be utilized for comparable purposes. Ie: don’t useindependent living sales to compare to memory care. This is even more critical SNF to assistedand independent living sales, and applies to all comparable purposes (sales, operations, rents,etc).

Standard commercial adjustments do not always apply and may in-fact be counterintuitive to whatwe are taught as general commercial appraisers. Ie: size adjustments, expense rations anindication of market operations.

Market participants do not contemplate the value by adding the value of the real estate to theseparate values of the tangible and intangible personal property; they focus on the overall valuewhich is derived by their expectations of cash flow and applied return requirement. In place cashflow is considered, but often adjusted by the buyer for pricing purposes. The magnitude of theadjustment will be reflected in the applied pricing rate.

=

61 HOW TO APPRAISE AN ASSISTED LIVING RESIDENCE | ZACH BOWYER, MAI

Seniors Housing Data ProvidersFINAL CONSIDERATIONS

NIC (National Investment Center for the Seniors Housing & Care Industry)

ASHA (American Seniors Housing Assoc.)

American Health Care Association

Irving Levin & Assoc.

- SeniorCare Investor

- Senior Housing News

- Annual SeniorCare Investor Report

CBRE Valuation & Advisory Services

- Please take full advantage of our platform

For more information regarding this presentation please contact:Zach Bowyer, MAIManaging Director & Seniors Housing Practice LeaderT +1 617 912 [email protected]

www.cbre.com