Embed Size (px)

Citation preview

How the analysts reacted to the first Solvency II

disclosures

Nick Ford

23 November 2017

What happened during the first 18 months

Analyst view

Positives of Solvency II

-Greater consistency than pre-SII

-Increased transparency on local EEA entities

-More non-life disclosures

However…

-No more PRA return means less disclosures

-Reduced/Removed embedded value disclosure, especially the movement analysis

-Unfair to UK names...

SFCR publication was less eventful than expected

SFCRL&G

Source: Bloomberg

SFCR publication was less eventful than expected

Aviva SFCR

Source: Bloomberg

SFCR publication was less eventful than expected

Pru SFCR

Source: Bloomberg

267%

197%

178%

157%177% 165% 167%

164%151%

155%

143%

123% 122%

261%

202%201%

188%

185% 182%180%

170%

162%150% 149%

147% 137%

130%

100%

150%

200%

250%

300%

Solvency II cover ratios and target ranges

Note: ND = not disclosed

(a) Please note that the information presented here was disclosed in EUR and converted to GBP at the exchange rate as at 30 June 2017.

(b) The ratio disclosed for these companies includes a TMTP recalculation for HY 2017.

(c) The results are stated as being estimated. In reality, it is likely that all results are estimated but other companied did not explicitly disclose this.

(d) Results for Prudential presented on a ‘shareholder view’ basis which excludes the contribution from the with-profits funds (WPF) and staff pension schemes.

(e) Results for Phoenix represent a pro forma position which includes the impacts of the US$500 million Tier 2 bond issued in July 2017.

Source: Analysis using public market disclosures

Solvency II cover ratios (Own funds over SCR) ranked by HY 17 decreasing order and target ranges.

HY 2017

results

£bn

Mu

nic

h R

e

Pru

de

nti

al(

b,d

)

AX

A(a

)

Gen

era

li

Aeg

on

Sta

nd

ard

Lif

e

L&

G(b

)

Aviv

a(b

,c)

PIC

Ju

st

Gro

up

Ro

yal

Lo

nd

on

Gro

up

LB

G

Ph

oe

nix

(b,e

)

Old

Mu

tua

l

Own

funds ND 25.6

51.5 NDND

6.715.2 28.9 3.4 2.1 5.8 ND 6.5 7.3

SCR ND 12.7 25.7 ND ND 3.7 8.5 17 2.1 1.4 3.9 ND 4.8 5.6

Surplus ND 12.9 25.8 ND ND 3.0 6.7 11.9 1.3 0.7 1.9 ND 1.7 1.7

Target range

Minimum target

YE16

HY17

Other view (HY17 and YE16)

Shareholder view

as regulatory

view not

disclosed

201%

Solvency II capital generation – HY17£bn or % Opening Operating

return

Market

movements

Dividends

/ debt

payments

Management

actions

Regulatory /

model

changes

Other Closing

Aegon 157% +3% +3% n/d +7% +15% - 185%

Aviva 11.3 0.9 (0.2) (1.0) 0.4 - - 11.4

AXA 197% +9% +1% -5% n/d n/d -2% 201%

L&G 5.7 0.9 0.1 (0.6) 0.6 - - 6.7

Old

Mutual

122% n/d n/d n/d 11% - -3% 130%

Phoenix 1.1 0.2 (0.1) (0.2) 0.2 - 0.5 1.7

Prudential 12.5 1.7 - (0.8) - - (0.5) 12.9

Inconsistency examples

•Operating return includes capital actions and amortisation of TMTP for some companies but not others – some gave very

little insight behind the operating return. Classification of debt and corporate centre costs was also inconsistent.

•Some included notional dividend payments for the first half of 2017

Source: Analysis using public market disclosures

Solvency II capital generation – analyst view

Av

era

ge o

pen

ing

S2 r

ati

o

193%

at

1stJan

2016

Ordinary dividend

-13ppts

Av

era

ge o

pen

ing

S2 r

ati

o

197%

at

30

thJu

ne 2

017

25

ppts

Op. capital generation

Net sub-debt

2 ppts

Market movement

-3 ppts

Buyback

Special divi

-4 pptsOther

-3 ppts

Aviva

Prudential plc.

Source: Company data

Wish list - movement analysis

Op

en

ing

S2

Su

rplu

s

Unwind of VA/UFR

(B)

Amortisation of transitional

arrangement (G)

Clo

sin

g S

2 S

urp

lus

Excess spread over risk free

(A) New business (C)

Unwind of risk margin (D)

Variances / mkt moves (F)

Dividend (H)

Unwind of SCR (E)

Recalculation of TMTP – disclosure at HY17HY17 Aviva L&G Prudential Phoenix

Standard

Life

Royal

LondonPIC Just Group

Allow for HY17 recalc for market

changesP P P P O O O O

Allow amortisation of half year P P P O O O n/d P

Included disclosure of run off of

TMTPO O O O O O O O

Stated size of TMTP O O P (£2.1bn) O O P (9%) O O

Stated impact of HY17 recalcP

(£0.5bn)

P

(£0.2bn)

P

(£0.7bn)O O O

P

(marginal)

P

(£63m or 5%)

Source: Analysis using public market disclosures

YE16Aviva L&G Prudential Phoenix Standard

Life

Royal

London

PIC Just Group

Allow for YE16 recalc for market

changes

P P P P P O O O

Allow amortisation of one year P P P P P n/d n/d P

Included disclosure of run off of

TMTP

O O P P P O O O

Stated size of TMTP O O P

(£2.5bn)

P

(£1.9bn)

P

(£1.5bn)

P

(10%)

O O

Stated impact of YE16 recalc P

(£0.4bn)

O P

(£0.4bn)

P

(£0.3bn)

O O O P (2-3%)

Selected TMTP, MA and VA impacts – from SFCRs

Source:Analysis based on S.22.01 QRT from SFCRs

Solvency II cover ratios (different views)

Solvency II shareholder/investor view vs regulatory view

Shareholder/Investor view Regulatory view

HY17 YE16 HY17 YE16

Standard Life 220% 214% 182% 177%

Royal London 203% 232% 149% 155%

Prudential 202% 201% ND ND

Aviva 193% 189% 170% 167%

L&G 186% 171% 180% 165%

Phoenix 166% 139% 137% 123%

LBG 152% 147% 147% 143%

Solvency II Pillar 2 ratios

Generali, L&G and Just Group continue to

present a Pillar 2 view as well.

Additional information

• Restrictions removed include:

• With profits funds

• Pension Schemes

• Other unrecognised capital (e.g. fungibility / transferability restrictions)

• Some companies allow for other ‘proforma’ adjustments that they cannot allow for in the regulatory view – e.g. internal model change that

hadn’t been approved at valuation date

• Most companies provide the restrictions in £ amounts as well

• The regulatory view presented in this table is from the market disclosure, not from the SFCR. There are some differences between these –

likely due to an estimate being used in the market disclosure.

SCR by risk type and diversification benefit – YE16

0%

20%

40%

60%

80%

100%

SC

OR

Old

Mu

tual

RS

A

NN

Gro

up

Mu

nic

h R

e

Ag

eas

Hannover R

e

Aviv

a

CN

P

Allia

nz

Genera

li

Pru

dentia

l

Pru

dentia

l

Dire

ct L

ine G

roup

Ph

oenix

Axa

L&

G

Sta

ndard

Life

PIC

Bu

pa

Investment Risk Life Insurance Risk Non-Life Insurance Risk Operational Risk Other Risk

Diversified

Pre-diversified

% Div. Benefit 49% 42% 40% 39% 36% 33%(a)

31% 30%(b)

26% 25% 19%(a)

n/d n/d n/d n/d n/d n/d n/d n/d

Note: (a) Based on their internal SII view. (b) Based on their shareholder SII view.

Pre / Post - Diversified capital YE16 rank by % size of Div. Benefit

Source: Analysis using public market disclosures

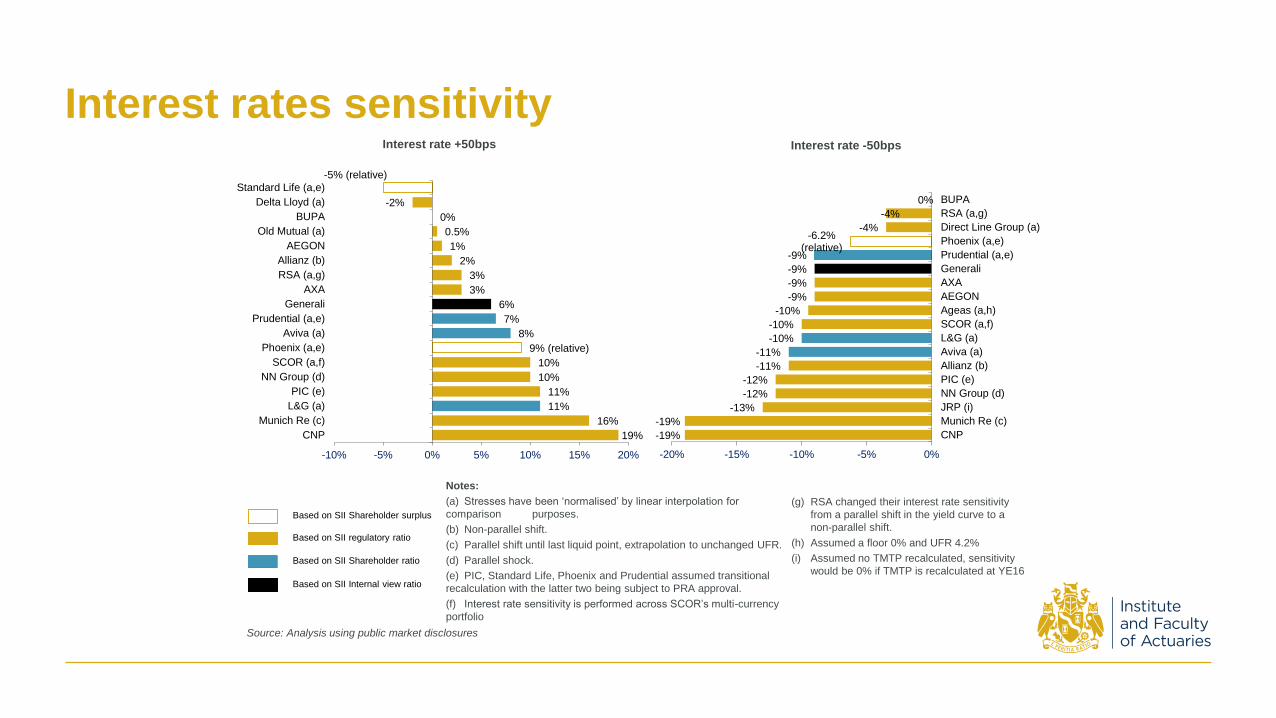

Interest rates sensitivity

19%

16%

11%

11%

10%

10%

9% (relative)

8%

7%

6%

3%

3%

2%

1%

0.5%

0%

-2%

-5% (relative)

-10% -5% 0% 5% 10% 15% 20%

CNP

Munich Re (c)

L&G (a)

PIC (e)

NN Group (d)

SCOR (a,f)

Phoenix (a,e)

Aviva (a)

Prudential (a,e)

Generali

AXA

RSA (a,g)

Allianz (b)

AEGON

Old Mutual (a)

BUPA

Delta Lloyd (a)

Standard Life (a,e)

Interest rate +50bps

Notes:

(a) Stresses have been ‘normalised’ by linear interpolation for

comparison purposes.

(b) Non-parallel shift.

(c) Parallel shift until last liquid point, extrapolation to unchanged UFR.

(d) Parallel shock.

(e) PIC, Standard Life, Phoenix and Prudential assumed transitional

recalculation with the latter two being subject to PRA approval.

(f) Interest rate sensitivity is performed across SCOR’s multi-currency

portfolio

Based on SII Shareholder surplus

Based on SII regulatory ratio

Based on SII Shareholder ratio

Based on SII Internal view ratio

(g) RSA changed their interest rate sensitivity

from a parallel shift in the yield curve to a

non-parallel shift.

(h) Assumed a floor 0% and UFR 4.2%

(i) Assumed no TMTP recalculated, sensitivity

would be 0% if TMTP is recalculated at YE16

-19%

-19%

-13%

-12%

-12%

-11%

-11%

-10%

-10%

-10%

-9%

-9%

-9%

-9%

-6.2%(relative)

-4%

-4%

0%

-20% -15% -10% -5% 0%

CNP

Munich Re (c)

JRP (i)

NN Group (d)

PIC (e)

Allianz (b)

Aviva (a)

L&G (a)

SCOR (a,f)

Ageas (a,h)

AEGON

AXA

Generali

Prudential (a,e)

Phoenix (a,e)

Direct Line Group (a)

RSA (a,g)

BUPA

Interest rate -50bps

Source: Analysis using public market disclosures

Credit Corporate sensitivity

Notes:

(a) Stresses have been ‘normalised’ by linear interpolation for

comparison purposes.

(b) Delta Lloyd Included movement in VA. For all credit spreads (excl.

mortgages).

(c) L&G assumed a level addition to all ratings.

(d) Munich Re widen both government and corporate bonds

Based on SII shareholder surplus

Based on SII regulatory ratio

Based on SII Shareholder ratio

Based on SII Internal view ratio

(e) Old Mutual assumes a 100bps increase in

credit spreads is generally assumed to be a

one notch downgrade from BBB to BB- rating

and a two notch downgrade on lower graded

investments.

(f) BUPA assumed no credit transaction.

(g) RSA used a parallel shift.

18%

15%

5%

3%

1%

0%

0%

0%

0%

-1%

-1%

-2%

-2%

-3%

-4%

-5%

-11%

-14%

-23%

-25% -20% -15% -10% -5% 0% 5% 10% 15% 20%

RSA (a,g)

NN Group

L&G (a,c)

JRP (a)

Aegon

Allianz

Aviva

BUPA (f)

Standard Life

Old Mutual (a,e)

AXA (a)

Generali (a)

Prudential (a)

Phoenix (a)

Direct Line Group (a)

SCOR (a)

CNP (a)

Munich Re (a,d)

Delta Lloyd (b)

Credit Corporate +50bps

Source: Analysis using public market disclosures

A spread narrowing was also disclosed by:

RSA

Delta Lloyd

Standard Life

Aviva

L&G

16% relative

13%

13%

9%

6%

6%

5%

5%

1%

-1%

-5% 0% 5% 10% 15% 20%

Standard Life(a)

Delta Lloyd (a)

Munich Re (a)

Generali (a)

L&G (a)

AXA

Allianz (a)

Aviva (a)

Old Mutual

Aegon (a)

Equity Risk +25%

Equity risk sensitivity

Notes:

(a) Stresses have been ‘normalised’ by linear interpolation for comparison purposes.

Based on SII shareholder surplus

Based on SII regulatory ratio

Based on SII Shareholder ratio

Based on SII Internal view ratio

-16% relative

-13%

-13%

-13%

-12%

-12%

-9%

-8%

-7%

-6%

-4%

-4%

-3%

-2%

0%

-20% -15% -10% -5% 0%

Standard Life (a)

Munich Re (a)

RSA (a)

Delta Lloyd (a)

CNP

NN Group

Generali (a)

Aegon (a)

AXA

L&G (a)

Aviva (a)

Prudential (a)

SCOR (a)

Allianz (a)

Phoenix

Equity Risk -25%

Source: Analysis using public market disclosures

Risk Margin metrics

Source:Analysis from QRTs within SFCRs

Loss absorbing capacity

Source:Analysis from S.25 QRTs from SFCRs

Total

OF

(£bn) Ae

go

n

Aviv

a

AX

A

CN

P

De

lta

Llo

yd

Ge

ne

rali

Ha

nn

ove

r R

e

L&

G (

a)

Mu

nic

h R

e

NN

Gro

up

Old

Mu

tua

l

Ph

oe

nix

Pru

den

tia

l(a)

Sta

nd

ard

Lif

e

Ag

ea

s

BU

PA

Dir

ec

t L

ine

PIC

RS

A

YE16 15.5 24.0 49.4 20.2 3.4 30.4 11.0 13.6 34.2 11.2 6.9 6.8 24.8 7.2 6.9 4.2 2.3 3.1 2.9

YE15 14.8 21.8 43.7 17.0 2.9 30.5 9.3 13.5 30.0 9.8 6.1 5.7 20.1 5.5 8.0 3.1 2.5 2.4 2.9

Quality of capital

Note: n/d = Not disclosed (a) Shareholder view

Source: Analysis using public market disclosures

Embedded value & new business

EV VNB

Aegon n/a MCVNB

Allianz MCEV / SII based SII/MCEV

Aviva n/a Adjusted SII

AXA EEV / Adjusted SII EEV

CNP MCEV / SII based MCEV

Delta Lloyd n/a SII

Generali MCEV / SII based SII / MCEV

Hannover Re n/a SII

JRP IFRS based EEV

L&G n/a Adjusted SII

Munich Re n/a SII

NN Group n/a Internal

Old Mutual EM MCEV MCEV

PIC EEV + MCEV / SII based EEV

Prudential EEV EEV

St James’s Place EEV EEV

• EV disclosures continue to decrease – particular in UK

• Various different definitions of EV used, including some

based from SII as a starting point

• Similarly, various different measures for new business

Analyst further wish list

• Solvency 2 vs. IFRS earnings

• Embedded guarantees to policyholders

• Comparability of 1-in-200 scenarios, especially the macro risks

• More understanding of longevity risk

• Consistency...

20 March 2018 22

The views expressed in this presentation are those of invited contributors and not necessarily those of the IFoA. The IFoA do not endorse any of the views

stated, nor any claims or representations made in this presentation and accept no responsibility or liability to any person for loss or damage suffered as a

consequence of their placing reliance upon any view, claim or representation made in this presentation.

The information and expressions of opinion contained in this presentation are not intended to be a comprehensive study, nor to provide actuarial advice or

advice of any nature and should not be treated as a substitute for specific advice concerning individual situations. On no account may any part of this

presentation be reproduced without the written permission of the IFoA or authors.

Questions Comments