Embed Size (px)

Citation preview

8/6/2019 How Some States Did Not Legally

http://slidepdf.com/reader/full/how-some-states-did-not-legally 1/14

HOW SOME STATES DID NOT LEGALLY

RATIFY THE 16TH AMENDMENT

Bill Benson's findings, published in "The Law That Never Was," make a convincingcase that the 16th amendment was not legally ratified and that Secretary of State

Philander Knox was not merely in error, but committed fraud when he declared itratified in February 1913. What follows is a summary of some of the major findingsfor many of the states, showing that their ratifications were not legal and should nothave been counted.

The 16th amendment had been sent out in 1909 to the state governors for ratification by the state legislatures after having been passed by Congress. There were 48 states atthat time, and three-fourths, or 36, of them were required to give their approval inorder for it to be ratified. The process took almost the whole term of the Taftadministration, from 1909 to 1913.

Knox had received responses from 42 states when he declared the 16th amendment

ratified on February 25, 1913, just a few days before leaving office to make way for the administration of Woodrow Wilson. Knox acknowledged that four of those states(Utah, Conn, R.I. and N.H.) had rejected it, and he counted 38 states as havingapproved it. We will now examine some of the key evidence Bill Benson foundregarding the approval of the amendment in many of those states.

In Kentucky, the legislature acted on the amendment without even having received itfrom the governor (the governor of each state was to transmit the proposedamendment to the state legislature). The version of the amendment that the Kentuckylegislature made up and acted upon omitted the words "on income" from the text, sothey weren't even voting on an income tax! When they straightened that out (with thehelp of the governor), the Kentucky senate rejected the amendment. Yet Philander Knox counted Kentucky as approving it!

In Oklahoma, the legislature changed the wording of the amendment so that itsmeaning was virtually the opposite of what was intended by Congress, and this wasthe version they sent back to Knox. Yet Knox counted Oklahoma as approving it,despite a memo from his chief legal counsel, Reuben Clark, that states were notallowed to change it in any way.

Attorneys who have studied the subject have agreed that Kentucky and Oklahomashould not have been counted as approvals by Philander Knox, and, moreover, if any

state could be shown to have violated its own state constitution or laws in its approval process, then that state's approval would have to be thrown out. That gets us past the"presumptive conclusion" argument, which says that the actions of an executiveofficial cannot be judged by a court, and admits that Knox could be wrong.

If we subtract Kentucky and Oklahoma from the 38 approvals above, the count of valid approvals falls to 36, the exact number needed for ratification. If any more states

8/6/2019 How Some States Did Not Legally

http://slidepdf.com/reader/full/how-some-states-did-not-legally 2/14

8/6/2019 How Some States Did Not Legally

http://slidepdf.com/reader/full/how-some-states-did-not-legally 3/14

These last five states, along with Kentucky and Oklahoma, have particularly strongimplications with regard to the fraud charge against Knox, in that he cannot beexcused for not knowing they shouldn't have been counted. Why was he in such ahurry? Why did he not demand that they send proper documentation? They never did.

Further review would make the list dwindle down much more, but with the number down to 20, sixteen fewer than required, this is a suitable place to rest, without gettinginto the matter of several states whose constitutions limited the taxing authority of their legislatures, which could not give to the federal govern authority they did nothave.

The results from the six states Knox had not heard from at the time he made his proclamation do not affect the conclusion that the amendment was not legally ratified.Of those six: two (Virginia and Pennsylvania) he never did hear from, because theyignored the proposed amendment; Florida rejected it; two others (Vermont andMassachusetts) had rejected it much earlier by recorded votes, but, strangely,

submitted to the Secretary within a few days of his ratification proclamation that theyhad passed it (without recorded votes); West Virginia had purportedly approved it atthe end of January 1913, but its notification had not yet been received (remember thatWest Virginia had violated its own constitution, as noted above).

ADVERISE HERE

Defects in Ratification of the 16thAmendment

8/6/2019 How Some States Did Not Legally

http://slidepdf.com/reader/full/how-some-states-did-not-legally 4/14

"If you...examined [The 16th Amendment] carefully, you would find that asufficient number of states never ratified that amendment." - U.S. DistrictCourt Judge James C. Fox 2003.

What the IRS website and the Government in general refuse to

recognize is that the Sixteenth Amendment to the Constitution of theUnited States was never ratified by a majority of the States. Only

two or less States properly ratified the proposed Amendment. InFebruary 1913 Secretary of State Knox falsely declared the 16thAmendment ratified and the government has been unlawfully demandingtaxes ever since.

The 16th Amendment allegedly entitled the government to collect uneventaxes. The U.S. Constitution does not preclude taxation it dictates that taxbe uniform for everyone, except Indians, and apportioned equally across allthe States:

Article I, Section 2: "..Representatives and direct Taxes shall be apportionedamong the several States which may be included within this Union,according to their respective Numbers, which shall be determined by addingto the whole Number of free Persons, including those bound to Service for aTerm of Years, and excluding Indians not taxed, three fifths of all otherPersons. The actual Enumeration shall be made within three Years after thefirst Meeting of the Congress of the United States, and within everysubsequent Term of ten Years, in such Manner as they shall by Law direct."

The 16th Amendment is claimed by the federal government in the federalterritory of Washington, D.C. to authorize their private collection company,the IRS, to collect "income tax". However if the 16th was not properlyratified the IRS has no legal authority to collect tax. The same applies tolocal County and State tax collectors who are also bound by the U.S.Constitution.

After an exhaustive year long search of legislative records in 48 sovereignStates conducted by Bill Benson, (Alaska & Hawaii were not admitted intothe Union until after 1913). the only record of the 16th Amendment everhaving been confirmed was a fraudulent proclamation made by theSecretary of State Philander Knox on February 25, 1913, wherein he simplydeclared it to be "in effect", but never stated that it was lawfully ratified. BillBenson's has an excellent website, support him: The Law That Never Was

Even if the 16th Amendment were properly ratified, according to Article 1,Section 9 of the Constitution, it has always been unconstitutional for theU.S. Federal Government to directly tax "We the People" in their property,wages, salaries, or earnings. U.S. Supreme Court Judges repeatedly rejectedany claims that the 16th Amendment changed the constitutional limits ondirect taxes: Brushaber v. Union Pacific R.R. Co., 240 U.S. 1, The SupremeCourt ruled that the 16th "created no new power of taxation" and that it "did

8/6/2019 How Some States Did Not Legally

http://slidepdf.com/reader/full/how-some-states-did-not-legally 5/14

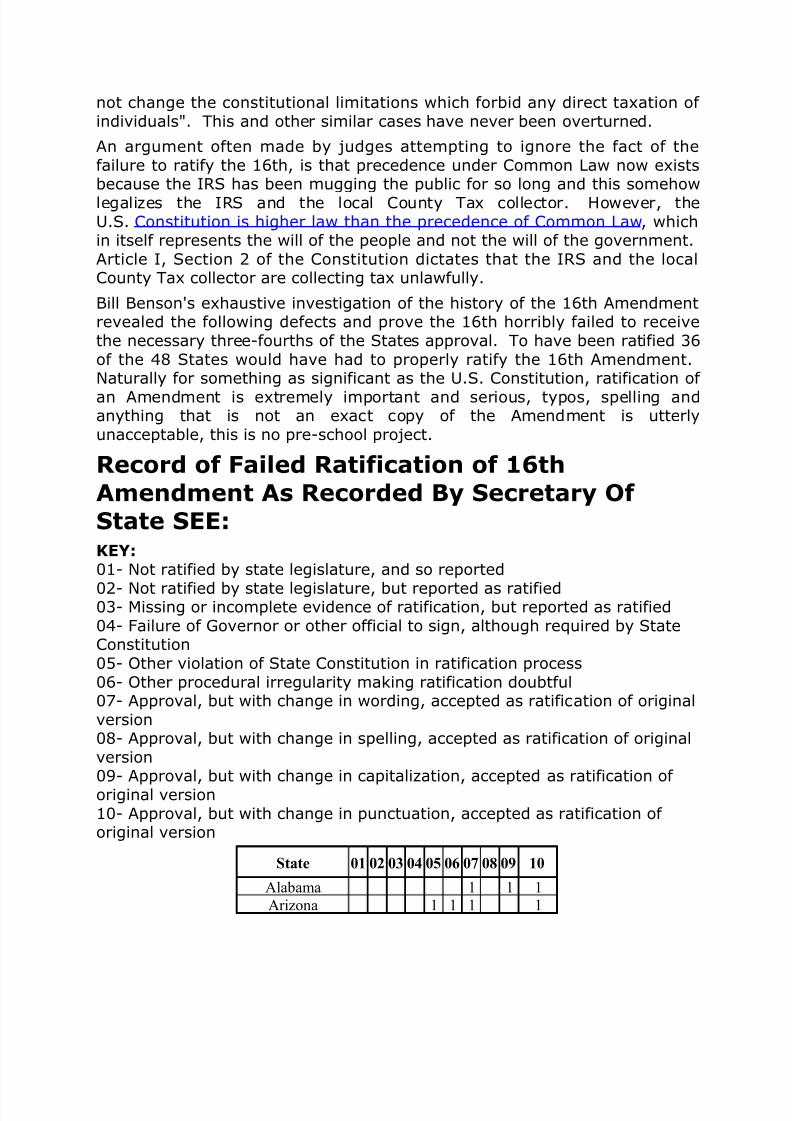

not change the constitutional limitations which forbid any direct taxation of individuals". This and other similar cases have never been overturned.

An argument often made by judges attempting to ignore the fact of thefailure to ratify the 16th, is that precedence under Common Law now existsbecause the IRS has been mugging the public for so long and this somehowlegalizes the IRS and the local County Tax collector. However, theU.S. Constitution is higher law than the precedence of Common Law, whichin itself represents the will of the people and not the will of the government.Article I, Section 2 of the Constitution dictates that the IRS and the localCounty Tax collector are collecting tax unlawfully.

Bill Benson's exhaustive investigation of the history of the 16th Amendmentrevealed the following defects and prove the 16th horribly failed to receivethe necessary three-fourths of the States approval. To have been ratified 36of the 48 States would have had to properly ratify the 16th Amendment.Naturally for something as significant as the U.S. Constitution, ratification of

an Amendment is extremely important and serious, typos, spelling andanything that is not an exact copy of the Amendment is utterlyunacceptable, this is no pre-school project.

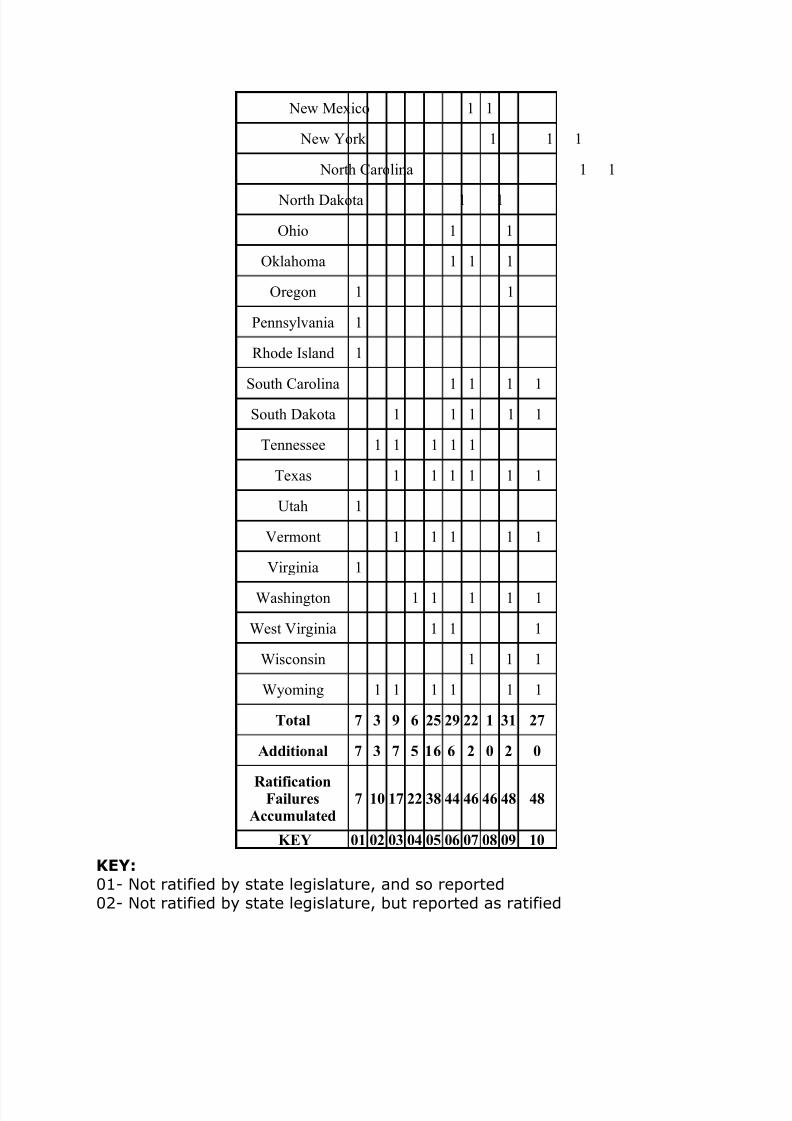

Record of Failed Ratification of 16th

Amendment As Recorded By Secretary Of State SEE:KEY:01- Not ratified by state legislature, and so reported

02- Not ratified by state legislature, but reported as ratified03- Missing or incomplete evidence of ratification, but reported as ratified04- Failure of Governor or other official to sign, although required by StateConstitution05- Other violation of State Constitution in ratification process06- Other procedural irregularity making ratification doubtful07- Approval, but with change in wording, accepted as ratification of originalversion08- Approval, but with change in spelling, accepted as ratification of originalversion09- Approval, but with change in capitalization, accepted as ratification of original version10- Approval, but with change in punctuation, accepted as ratification of original version

State 01 02 03 04 05 06 07 08 09 10

Alabama 1 1 1

Arizona 1 1 1 1

8/6/2019 How Some States Did Not Legally

http://slidepdf.com/reader/full/how-some-states-did-not-legally 6/14

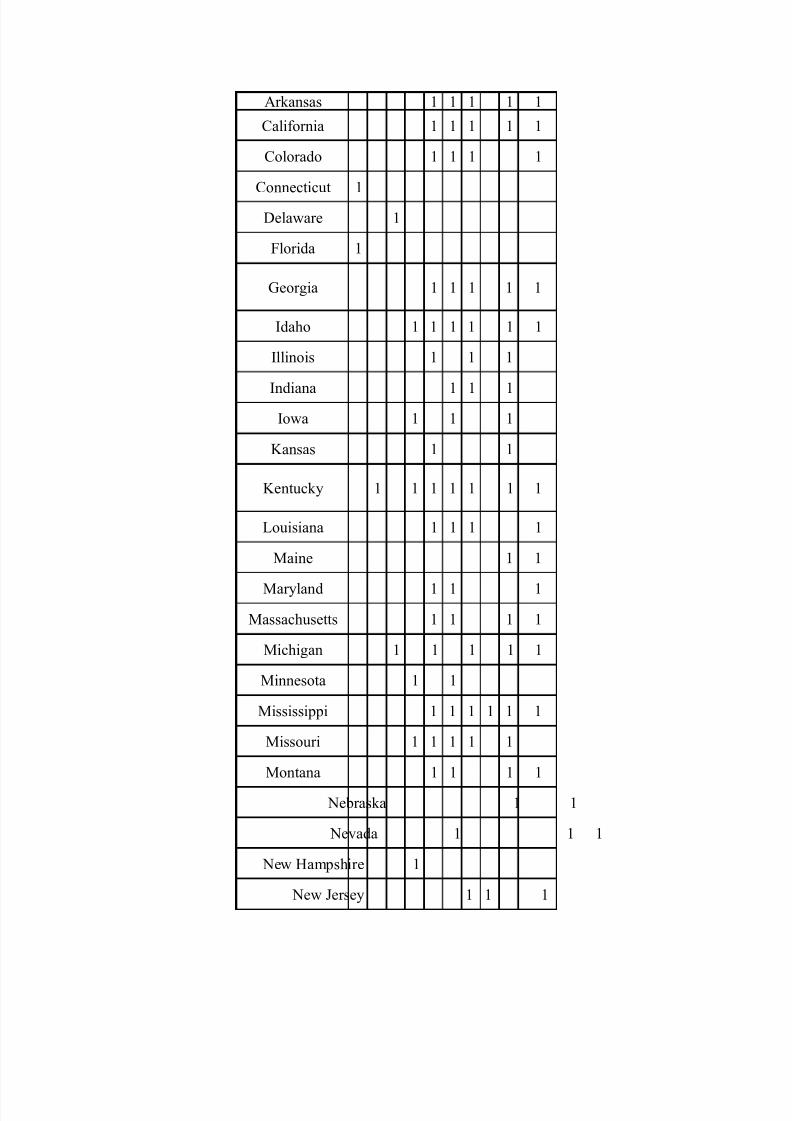

Arkansas 1 1 1 1 1

California 1 1 1 1 1

Colorado 1 1 1 1

Connecticut 1

Delaware 1

Florida 1

Georgia 1 1 1

1 1

Idaho 1 1 1 1 1 1

Illinois 1 1 1

Indiana 1 1 1

Iowa 1 1 1

Kansas 1 1

Kentucky 1

1 1 1 1 1 1

Louisiana 1 1 1 1

Maine 1 1

Maryland 1 1 1

Massachusetts 1 1 1 1

Michigan 1 1 1 1 1

Minnesota 1 1

Mississippi 1 1 1 1 1 1

Missouri 1 1 1 1 1

Montana 1 1 1 1

Nebraska 1 1

Nevada 1 1 1

New Hampshire 1

New Jersey 1 1 1

8/6/2019 How Some States Did Not Legally

http://slidepdf.com/reader/full/how-some-states-did-not-legally 7/14

New Mexico 1 1

New York 1 1 1

North Carolina 1 1

North Dakota 1 1

Ohio 1 1

Oklahoma 1 1 1

Oregon 1 1

Pennsylvania 1

Rhode Island 1

South Carolina 1 1 1 1

South Dakota 1 1 1 1 1

Tennessee 1 1 1 1 1

Texas 1 1 1 1 1 1

Utah 1

Vermont 1 1 1 1 1

Virginia 1

Washington 1 1 1 1 1

West Virginia 1 1 1

Wisconsin 1 1 1

Wyoming 1 1 1 1 1 1

Total 7 3 9 6 25 29 22 1 31 27

Additional 7 3 7 5 16 6 2 0 2 0

RatificationFailures

Accumulated

7 10 17 22 38 44 46 46 48 48

KEY 01 02 03 04 05 06 07 08 09 10

KEY:01- Not ratified by state legislature, and so reported02- Not ratified by state legislature, but reported as ratified

8/6/2019 How Some States Did Not Legally

http://slidepdf.com/reader/full/how-some-states-did-not-legally 8/14

03- Missing or incomplete evidence of ratification, but reported as ratified04- Failure of Governor or other official to sign, although required by StateConstitution05- Other violation of State Constitution in ratification process06- Other procedural irregularity making ratification doubtful

07- Approval, but with change in wording, accepted as ratification of originalversion08- Approval, but with change in spelling, accepted as ratification of originalversion09- Approval, but with change in capitalization, accepted as ratification of original version10- Approval, but with change in punctuation, accepted as ratification of original version

In the above table, the line "Additional" are the number of States for whichthat defect is in addition to previously indicated defects, and "Ratification

Failures Accumulated" is a running total of States with defects, from Defect01 through 10.

Since 36 states were required to ratify, the failure of 13 to ratify would befatal to the amendment, and this occurs within the first three defects,arguably the most serious. Even if we were to ignore defects of spelling, capitalization, and punctuation, we would still have only

two states which successfully ratified.

Note that in the above we are counting Ohio as a State, even though it wasnot admitted into the Union until 1953 (retroactively, which is expost facto,and unconstitutional). We are not counting the failure to designate the

Income Tax Amendment as the "XVII" amendment, since there was arguablya 13th Amendment that was ratified but which is not published in officialcopies of the Constitution with Amendments, and the number is notnecessarily part of the amendment (It wasn't part of the first 10.).

The authority usually cited for the criticality of ratification without errors of spelling, capitalization, or punctuation, is from DOCUMENT NO. 97-120, of the 97TH CONGRESS, 1st Session, entitled How Our Laws Are Made, writtenby Edward F. Willett, Jr. Esq., Law Revision Counsel of the United StatesHouse of Representatives, in which the comparable exactitude in which billsmust be concurred under federal legislative rules is detailed:

. Each amendment must be inserted in precisely the proper place in thebill, with the spelling and punctuation exactly the same as it was

adopted by the House. Obviously, it is extremely important that theSenate receive a copy of the bill in the precise form in which it passed

the House. The preparation of such a copy is the function of the enrollingclerk. (at 34) (emphasis added)

8/6/2019 How Some States Did Not Legally

http://slidepdf.com/reader/full/how-some-states-did-not-legally 9/14

When the bill has been agreed to in identical form by both bodies - eitherwithout amendment by the Senate, or by House concurrence in the Senateamendments, or by agreement in both bodies to the conference report - acopy of the bill is enrolled for presentation to the President.

The preparation of the enrolled bill is a painstaking and important tasksince it must reflect precisely the effect of all amendments, either bydeletion, substitution, or addition, agreed to by both bodies. The enrollingclerk ... must prepare meticulously the final form of the bill, as it was agreedto by both Houses, for presentation to the President.... each (amendment)must be set out in the enrollment exactly as agreed to, and all punctuation must be in accord with the action taken. (at 45)(emphasis added)

In his report on the failure of ratifications of the Income Tax Amendment tothen Secretary of State Philander Knox, the Solicitor of the Department of State recognized and acknowledged the defects of ratification. Knox failed to

demand mandatory corrective action by the States.

Knox had plenty of clues to the problems in the ratifications, sufficient to justify that he inquire into the matter further and demand corrective actionby the States. Because he failed to do so means that we now have adoptedand enforced legislation for more than 80 years that is plainlyunconstitutional,requiring not only that it be repealed, but that all the

funds collected be refunded.

The 16th is not ratified, has not been ratified and is not law.

Even if the 16th Amendment were properly ratified, according to Article 1,

Section 9 of the Constitution, it has always been unconstitutional for theU.S. Federal Government to directly tax We the People in their property,wages, salaries, or earnings. The U.S. Supreme Court rejected any claimsthat the 16th Amendment changed the constitutional limits on direct taxes inBrushaber v. Union Pacific R.R. Co., 240 U.S. 1, and ruled that the 16th"created no new power of taxation" and that it "did not change theconstitutional limitations which forbid any direct taxation of individuals".

By law the entities that have unlawfully taken money from individuals andcorporations must return that money, the money has in effect been stolen.

Either the U.S. is a nation of laws or it is a lawless nation. And if the latter is

the case then why pay a corrupt and criminal government? In such a caseshould not one take up 2nd Amendment arms and defend the right tofreedom just as the Founding Fathers did?

see Bill Benson'ssite: http://www.thelawthatneverwas.com/new/ratification.asp

See Also: IRS Suffering Repeated Defeats

8/6/2019 How Some States Did Not Legally

http://slidepdf.com/reader/full/how-some-states-did-not-legally 10/14

The IRS website at http://www.irs.gov/irs/article/0,,id=149200,00.html listsa Brief History of IRS:

Origin (As reported on the IRS Website)The roots of IRS go back to the Civil War when President Lincoln andCongress, in 1862, created the position of commissioner of Internal Revenueand enacted an income tax to pay war expenses. The income tax wasrepealed 10 years later. Congress revived the income tax in 1894, but theSupreme Court ruled it unconstitutional the following year.

16th Amendment (As reported on the IRS Website)In 1913, Wyoming ratified the 16th Amendment, providing the three-quartermajority of states necessary to amend the Constitution. The 16thAmendment gave Congress the authority to enact an income tax. That sameyear, the first Form 1040 appeared after Congress levied a 1 percent tax onnet personal incomes above $3,000 with a 6 percent surtax on incomes of more than $500,000.

In 1918, during World War I, the top rate of the income tax rose to 77percent to help finance the war effort. It dropped sharply in the post-waryears, down to 24 percent in 1929, and rose again during the Depression.During World War II, Congress introduced payroll withholding and quarterlytax payments.

A New Name (As reported on the IRS Website)In the 50s, the agency was reorganized to replace a patronage system withcareer, professional employees. The Bureau of Internal Revenue name waschanged to the Internal Revenue Service. Only the IRS commissioner andchief counsel are selected by the president and confirmed by the Senate.

Today’s IRS Organization (As reported on the IRS Website)The IRS Restructuring and Reform Act of 1998 prompted the mostcomprehensive reorganization and modernization of IRS in nearly half acentury. The IRS reorganized itself to closely resemble the private sectormodel of organizing around customers with similar needs.

The IRS Code says that compliance to their tax is "voluntary" - 26 CFR Ch.1(4-2-03 Edition)

"Your income tax is a 100% voluntary tax, and your liquor tax is a 100%enforced tax. The situation is as different as night and day." - Dwight E.

Avis. Head of Alcohol and Tobacco Tax Division. Bureau of InternalRevenue.

"The only difference between a tax man and a taxidermist is that thetaxidermist leaves the skin." - Mark Twain

"I am a most unhappy man. I have unwittingly ruined my country. A greatindustrial nation is now controlled by its system of credit. We are no longera government by free opinion, no longer a government by conviction and the

8/6/2019 How Some States Did Not Legally

http://slidepdf.com/reader/full/how-some-states-did-not-legally 11/14

voter of the majority, but a government by the opinion and duress of a smallgroup of dominant men." President Woodrow Wilson 1919.

"People have been brainwashed. People have been told that you need thisincome tax system to fund government, which is absolutely ridiculous. Myquestion is that if that is true, then how did we fund government from 1776to 1913" - Peter Gibbons, Tax Attorney

• Paying for schools? As foolish as it is to allow the government toeducate your kids (separation of State and School is vastly moreimportant than separation of Church and State), property tax paysform the great majority of schools.

• Paying for highways? Tax you pay at the gas pump for gasoline paysfor the highways.

The amount of money the government spends on the military, in violation of U.S. Constitution, Article. I., Section 8. Clause 12, always mysteriously

equals what the government collects from corporate tax."The main purpose of the income tax is not to raise revenue, but toredistribute wealth and control society." -"It's actually very simple.Congress tried to enact an income tax in 1894. The Supreme Court saidthat was unconstitutional. If the Supreme Court says something isunconstitutional it's un-unconstitutional. They tried again in 1913 and theSupreme Court said "The 16th Amendment conferred no new power of taxation". So if they didn't have it then, and they didn't get it. They don'thave it. There is no constitutional basis for tax on the wages of Americansliving and working in the fifty States of the Union. Period. End of argument."

- G. Edward Griffin. Author, Creature From Jekyll Island."In substance, the [Supreme] Court holds that the Sixteenth Amendment didnot empower the Federal Government to levy a new tax." - New York Times,January 25, 1916

President Ronald Reagan's Blue Ribbon Panel Grace Commission setup toinvestigate income tax reported: "100% of what is collected is absorbedsolely on the interest of the federal debt . All individual income tax revenuesare gone before one nickel paid on the services tax payers collect on thegovernment."

"I believe that in both spirit and substance our tax system has become un-American. Death and taxes may be inevitable. But unjust taxes are not."President Ronald Reagan.

The IRS and local County Tax Collector Are Law Breakers,they Are Criminals committing Fraud:The income that is a direct tax which is not apportioned amongst the Statesas demanded by the U.S. Constitution, making the income tax and property

8/6/2019 How Some States Did Not Legally

http://slidepdf.com/reader/full/how-some-states-did-not-legally 12/14

taxes, and sales tax and every other tax levied against citizens of the U.S.unconstitutional and therefore unlawful.

Apportioned = to divide equally amongst the people.

More info on failure to ratify

C-Live, Love Oppose Evil. Novus Ordo Seclorum.

8/6/2019 How Some States Did Not Legally

http://slidepdf.com/reader/full/how-some-states-did-not-legally 13/14

On January 10, 2008, the FederalDistrict Court in Chicago issuedapermanent injunction against me on

the grounds that I was falsely tellingpeople the 16th Amendment was notratified. The Court refused to look at

the evidence of the non-ratification of the 16thAmendment, deciding that the facts necessary toprove my statement was true were "irrelevant,"What has America come to when thegovernment can accuse you of lying and prohibityou from presenting a defense in a so calledcourt of law? My attorney, Jeffrey A. Dickstein,will be filing an appeal to the 7th Circuit Court of

Appeals. I urge you to review the pleadings filedin this case so you can see for yourself thetyranny being practiced in our courts.

The Premise

The authority of the federal government tocollect its income tax depends upon the 16thAmendment to the U.S. Constitution, the federalincome tax amendment, which was allegedly

ratified in 1913. After a year of extensiveresearch, Bill Benson discovered that the 16thAmendment was not ratified by the required 3/4of the states, but nevertheless Secretary of StatePhilander Knox fraudulently announcedratification.

Text of the 16th Amendment to the Constitutionof the United States of America:

"The Congress shall have power to lay and collect taxes on

incomes, from whatever source derived, without apportionment among the several States, and without regard to any census or enumeration."

Bill would like to thank those who've contributed or shown suppoin the fight against fraudulent taxation. Click

8/6/2019 How Some States Did Not Legally

http://slidepdf.com/reader/full/how-some-states-did-not-legally 14/14

![Legally Blonde Remix [Audition Cut] (Legally Blonde, O'Keefe) Sheet Music](https://img.pdfslide.us/doc/110x75/56d6bfea1a28ab3016983436/legally-blonde-remix-audition-cut-legally-blonde-okeefe-sheet-music.jpg)