Embed Size (px)

Citation preview

How Banks OperateChapter 24 Section 3

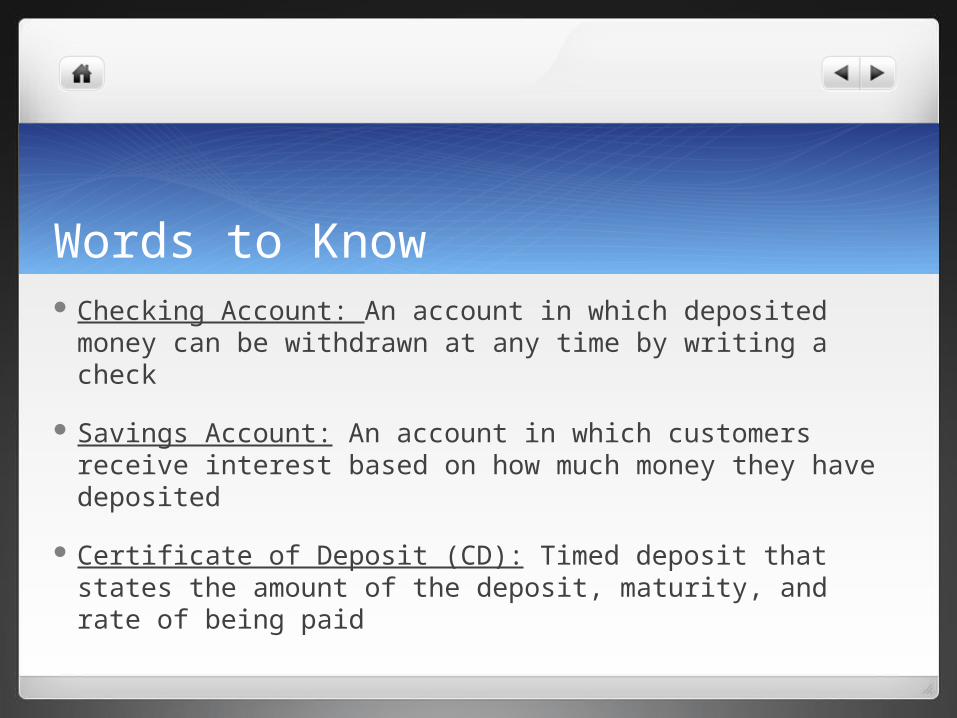

Words to Know Checking Account: An account in which deposited money can be withdrawn

at any time by writing a check

Savings Account: An account in which customers receive interest based on how much money they have deposited

Certificate of Deposit (CD): Timed deposit that states the amount of the deposit, maturity, and rate of being paid

Banking Services Banks are started by investors:

Pool financial investments Money Property Certificates of deposits

Provide banking services to community

Some of this money goes to expenses: Rent Supplies Salaries

Banks need depositors to survive

Accepting Deposits Attracting Customers:

Checking accounts: Money doesn’t stay here for long:

Pay expenses

Savings accounts: Money usually stays in here for long

periods of time Gain interest Longer in the bank more money you

make

Attracting Deposits cont. CD’s:

Loan to the bank for a specific time

Bank pays interest during this time

Time ends, customer can claim the money

Penalties if money taken out before time ends

Higher rates on CD’s than savings accounts

Making Loans A main activity of banks:

Lending money to businesses and consumers

Loans increase supply of money Money in circulation grows

Changes in the Banking Industry In the beginning (1800’s):

State banks issued their own currency: Printed notes at printing shops

People who needed loans borrowed notes and paid them back with interest

Federal Govt. did not print currency until Civil War: Most of money supply was paper

currency that was privately owned, state-bank issued

The National Banking Act 1863: Congress passes act

Created dual banking system: Banks could have either state or

federal charter

Federal charter private banks: Issued national bank notes

(national currency) Backed by govt.

The Federal Reserve Serves as the nation’s central bank:

Power to regulate national banks Control the growth of money

supply

1914-began issuing paper money: Called Federal Reserve Notes Became the major form of

currency in circulation

The Great Depression 1930’s:

Severely hurt banking industry Stocks and investments owned by banks lost

much of their value Bankrupt businesses and individuals unable to

pay off loans Thousands of banks collapsed President F.D. Roosevelt:

Declared a “bank holiday”: Closed all banks Could re-open when proved to be

financially sound

Congress passed the Glass-Steagall Banking Act: Creation of FDIC

The Savings and Loans Crisis 1970’s:

Most financial institutions were begging for relief from federal regulations: Because of the Great Depression

Congress began deregulation: Relaxing restrictions on activities

The Savings and Loans Crisis cont. 1982:

Congress decided to allow S&Ls to make high-risk loans and investments Investments went bad:

Hundreds of S&Ls failed Insured by Federal Govt.:

Govt. saddled with debt Cost tax payers approximately $200 billion FDIC took over regulation

HomeworkChapter 24 Section 3 Worksheets