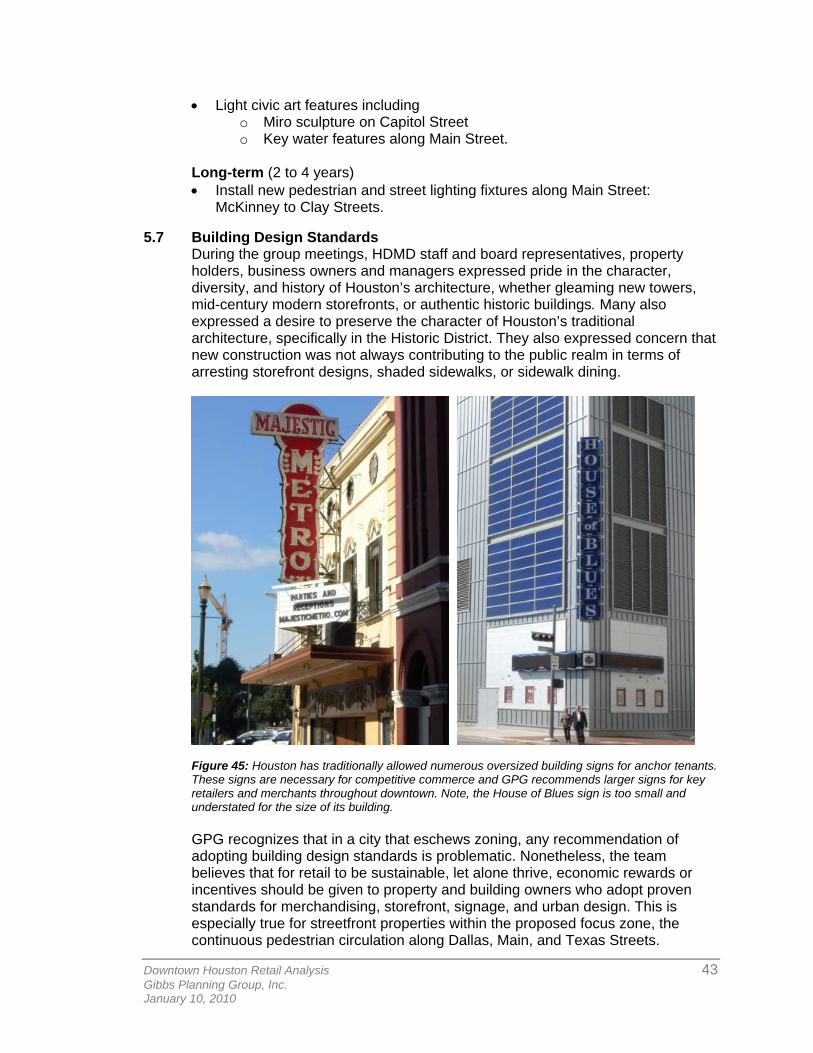

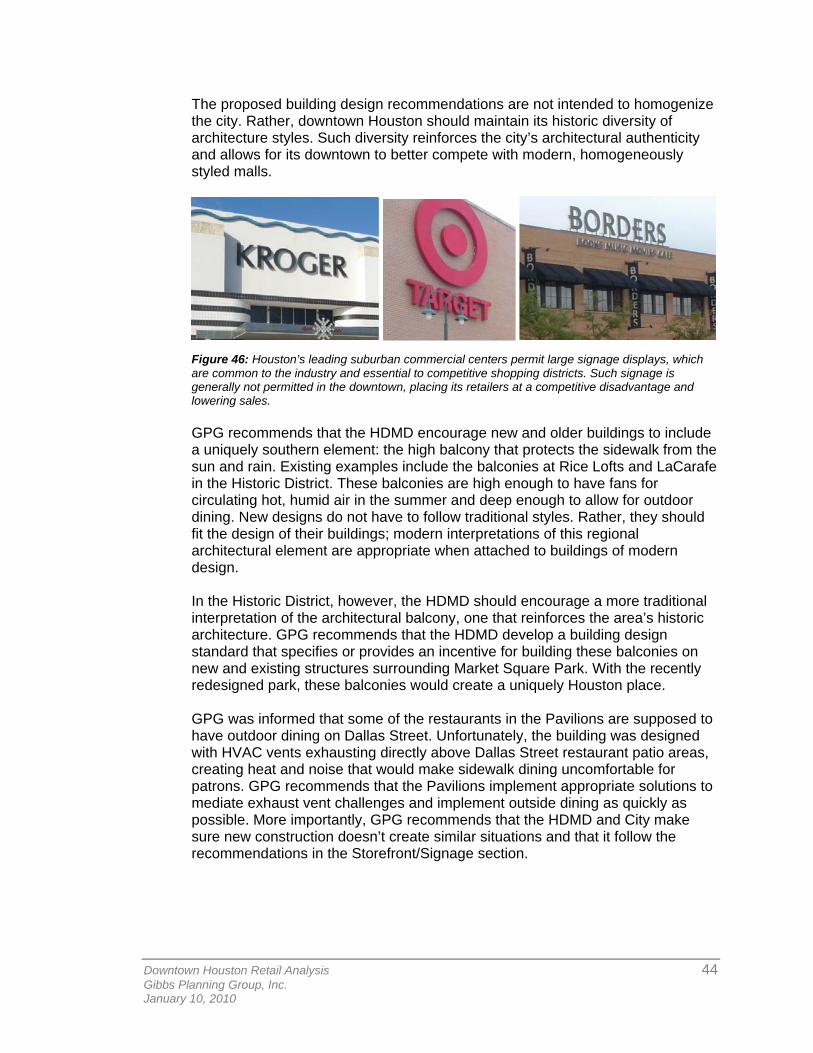

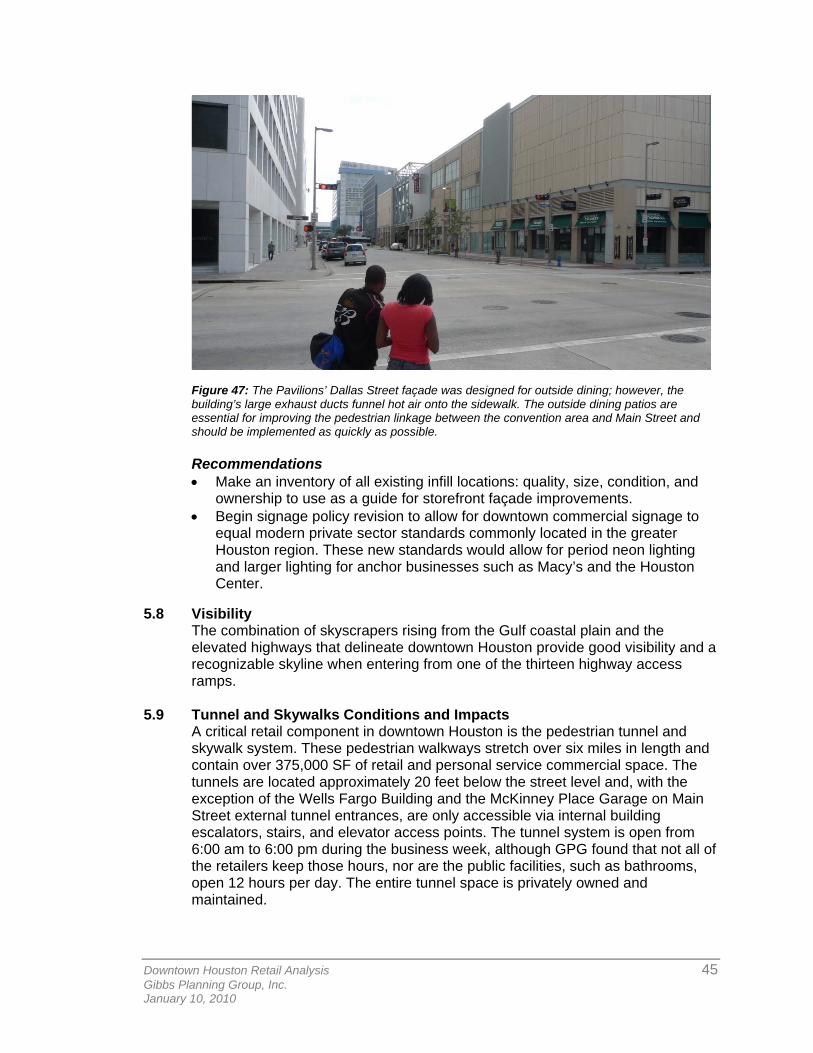

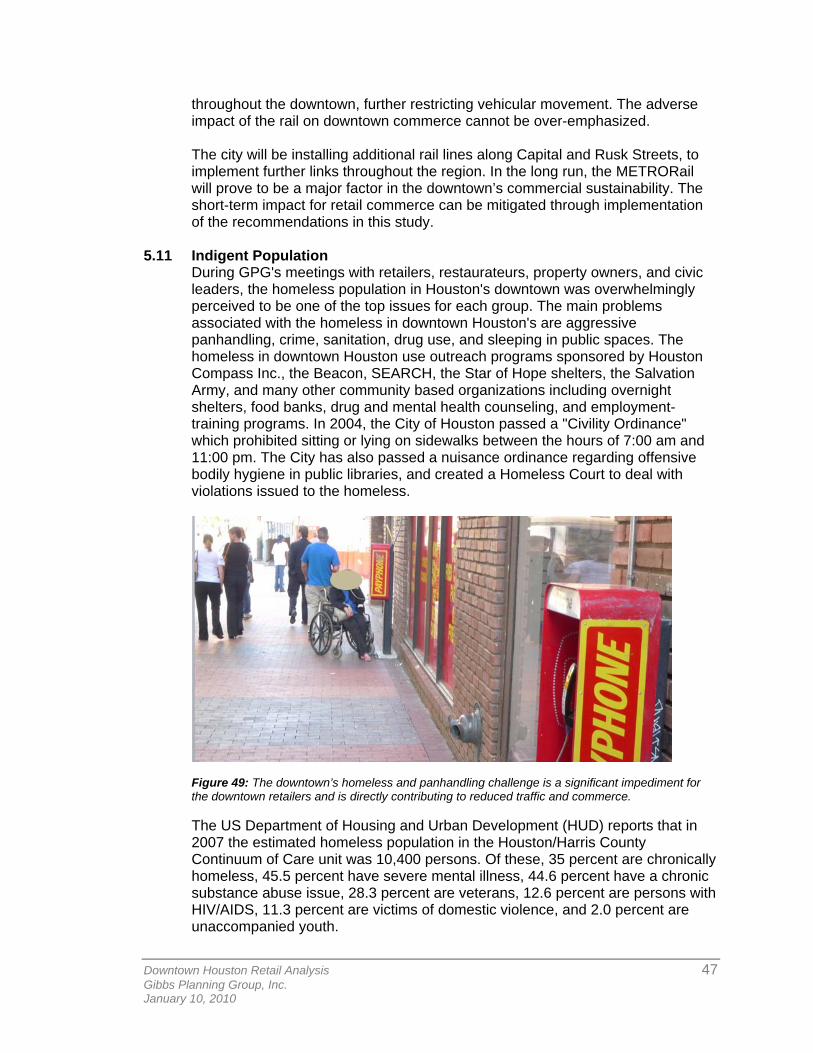

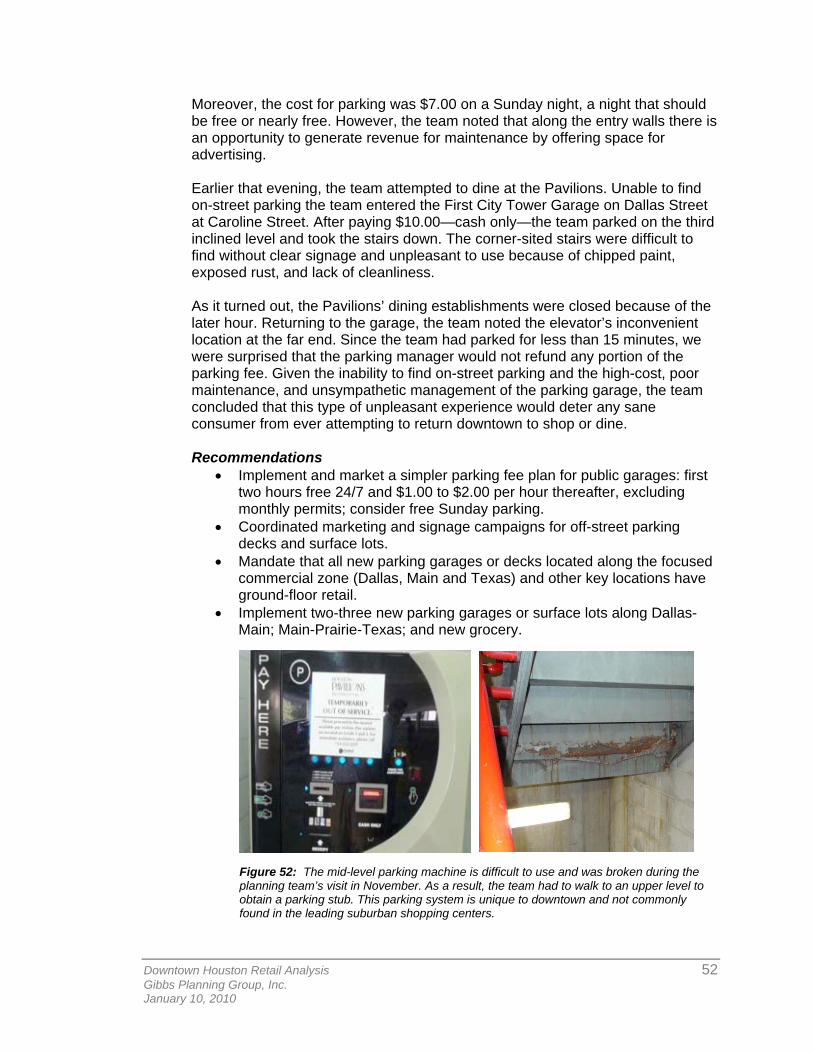

Embed Size (px)

Citation preview

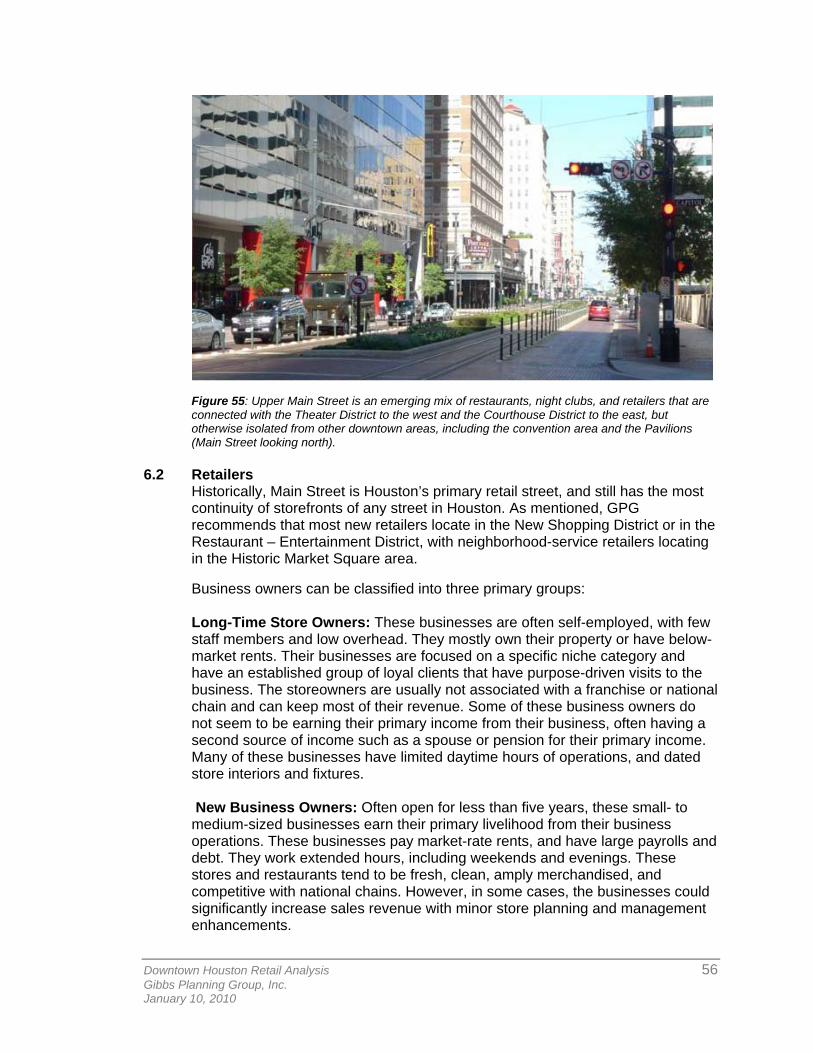

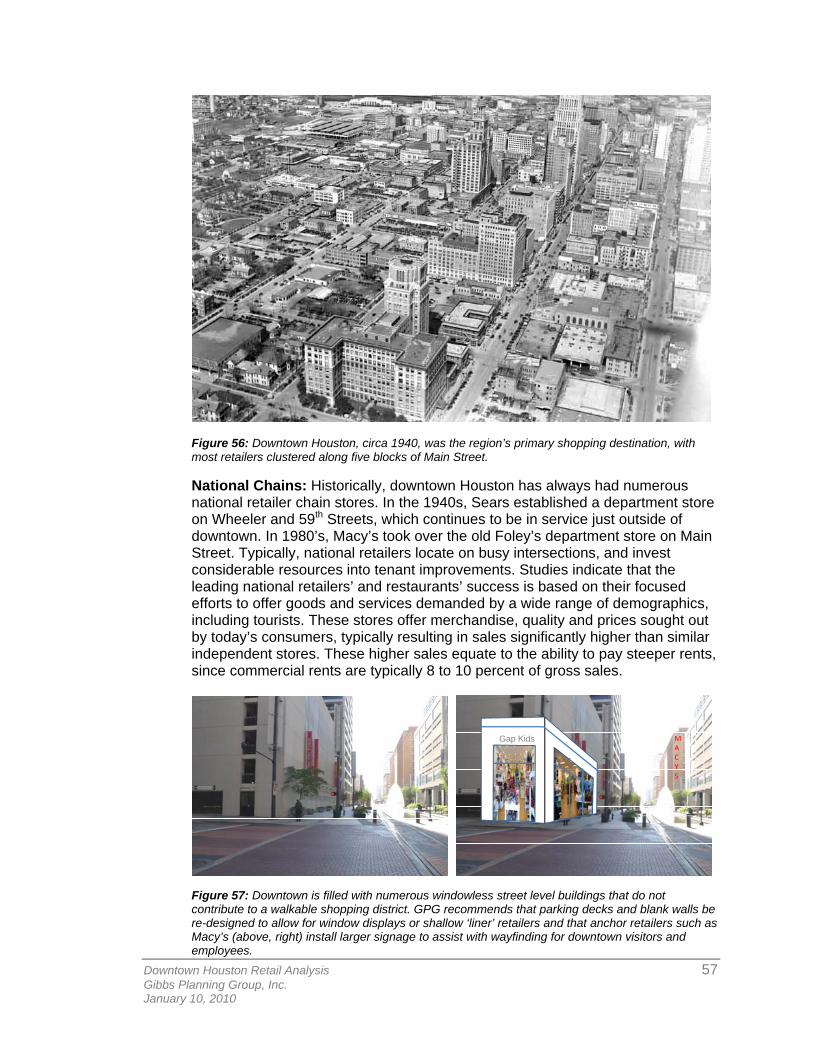

Houston Downtown Retail Analysis Prepared for: Houston Downtown Management District Prepared by: Gibbs Planning Group, Inc.

January 10, 2010

TABLE OF CONTENTS 1.0 INTRODUCTION………………………………………………………………….. 11.1 Executive Summary………………………………………………………………. 11.2 Purpose of Study………………………………………………………………….. 4 2.0 TRADE AREAS AND DEMOGRAPHICS……………………………………… 52.1 Local Trade Area………………………………………………………………….. 52.2 Office Worker Demographics and Impact………………………………………. 62.3 Tourist and Convention Attendee Demographics and Impacts……………… 72.4 Primary Trade Area………………………………………………………………. 82.5 Tertiary Trade Area……………………………………………………………….. 92.6 Tapestry Lifestyles………………………………………………………………... 10 3.0 MARKET CONDITIONS…………………………………………………………. 143.1 Retail and Restaurant Demand………………………………………………….. 143.2 Tourism Expenditure…………………………………………………………….... 153.3 Workforce Expenditures………………………………………………………….. 173.4 Commercial Trade Areas………………………………………………………… 17

3.5 Theater District Impact……………………………………………………………. 183.6 Sports and Convention District Impacts………………………………………... 183.7 Macy’s Department Store…………………………………………………….….. 193.8 Houston Pavilions……………………………………………………………….… 203.9 The Shops at Houston Center..………………………………………………..... 213.10 Nearby Shopping Centers………………………………………………………... 223.10.1 Midtown District……………………………………………………………………. 223.10.2 The Heights District…………………………………………………………….…. 223.10.3 Regent Square………………………………………………………………….…. 233.10.4 River Oaks……………………………………………………………………….… 243.10.5 The Galleria……………………………………………………………………….. 243.10.6 Highland Village…………………………………………………………………… 253.10.7 Other Shopping Centers………………………………………………………….. 263.11 Summary of Market Findings…………………………………………………….. 283.12 Rationale for the Market Findings……………………………………………….. 30 4.0 COMMUNITY COMMENTS……………………………………………………… 304.1 Downtown Management and Retail Development Group Interviews………. 304.2 Property Owners and Building Managers Interviews…………………………. 324.3 Restaurant and Bar Owners and Soft Goods Retailers Interviews…………. 33 5.0 CHALLENGES AND OPPORTUNITIES………………………………………. 345.1 Overview…………………………………………………………………………… 355.2 Business Opening Challenges.………………………………………………….. 355.3 Space Limitations…………………………………………………………………. 365.4 Retail Connector Streets…………………………………………………………. 375.5 Streetscape………………………………………………………………………... 395.6 Lighting……………………………………………………………………………... 415.7 Building Design Standards………………………………………………………. 435.8 Visibility…………………………………………………………………………….. 455.9 Tunnel and Skywalks Conditions and Impacts………………………………... 455.10 METRORail Conditions and Impacts…………………………………………… 465.11 Indigent Population……………………………………………………………….. 475.12 Parking……………………………………………………………………………... 485.12.1 On-Street Parking…………………………………………………………………. 485.12.2 Parking Garages…………………………………………………………………... 50 6.0 COMMERCIAL ENHANCEMENT OPPORTUN ITIES………………………. 536.1 Merchandising Strategy…………………………………………………………... 536.2 Retailers……………………………………………………………………………. 566.3 Infill Businesses…………………………………………………………………… 586.4 Business Recruitment Consultant………………………………………………. 596.5 Business Improvement District…………………………………………………... 596.6 Special Events…………………………………………………………………….. 60

6.7 Marketing………………………………………………………………………….. 616.8 Wayfinding Signage……………………………………………………………... 61 7.0 SIMILAR HISTORIC DISTRICTS………………………………………………. 617.1 Charleston, South Carolina……………………………………………………… 627.2 Naples, Florida……………………………………………………………………. 63 8.0 CONDITIONS OF STUDY……………………………………………………….. 648.1 Methodology……………………………………………………………………….. 648.2 Limits of Study…………………………………………………………………….. 65

Downtown Houston Retail Analysis 1 Gibbs Planning Group, Inc. January 10, 2010

Figure 1: Downtown Houston contains over two million square feet of retail space and is the employment center of the greater Houston region.

1.0 INTRODUCTION

1.1 Executive Summary

This study concludes that downtown Houston can presently absorb up to 180,000 square feet (SF) of additional retail and restaurant space and various department and warehouse stores up to 221,100 square feet, for a total of 401,100 square feet of retail space. If implemented per industry standards, this new commercial development could generate up to $120 million in annual gross sales during 2010, growing to $230.7 million by 2014. This new revenue growth could equate to 75 to 100 new stores and restaurants or could be absorbed by many of the downtown area’s existing businesses. These additional commercial sales gains can be achieved by implementing numerous physical and policy enhancements that are currently suppressing the downtown’s consumer appeal, ease of shopping, and commerce. Modifications to downtown’s lighting, parking, mobility lanes, sign code, and building design standards, business recruitment initiatives, and addressing abundant, aggressive panhandling could return downtown to the competitive and lively shopping district that it once was. That being said, downtown Houston has the necessary elements, including 140,000 workers employed in downtown, 31.4 million tourists generated from conventions and local attractions, a vibrant cultural district that supports all manifestations of the arts, and a dense population base, to support a wide spectrum of retail categories. Houston is also the energy and medical capital of the world and considered one of the stronger retail markets in the Southwest.

Downtown Houston Retail Analysis 2 Gibbs Planning Group, Inc. January 10, 2010

010,00020,00030,00040,00050,00060,00070,00080,00090,000

100,000

Lugg

age

& Le

athe

r Sto

reU

sed

Mer

chan

dise

Sto

reB

eer,

Win

e &

Liq

uor S

tore

Jew

erly

Sto

reP

erso

nal S

ervi

ces

Toy

and

Hob

by S

tore

Art,

Cra

ft an

d Se

win

g …U

nise

x A

ppar

elLa

wn,

Gar

den

Equi

pmen

t …M

usic

al In

stru

men

t Sto

reC

ompu

ters

and

Sof

twar

eAp

plia

nces

Book

& M

usic

Sto

res

Hea

lth a

nd B

eaut

y St

ore

Car

d/G

ift S

hop

Chi

ldre

n's

App

arel

Dru

g St

ore/

Phar

mac

eutic

alG

roce

ry S

tore

Offi

ce S

uppl

ies,

Sta

tiona

ryG

ener

al E

lect

roni

csSh

oe S

tore

Lim

ited

Serv

ice

Res

taur

ant

Drin

king

Pla

ces

Spo

rting

Goo

d St

ore

Men

's A

ppar

elW

omen

's A

ppar

elW

areh

ouse

Clu

bD

isco

unt D

epar

tmen

t Sto

reD

epar

tmen

t Sto

reSupp

orta

ble

Squa

re F

oota

ge

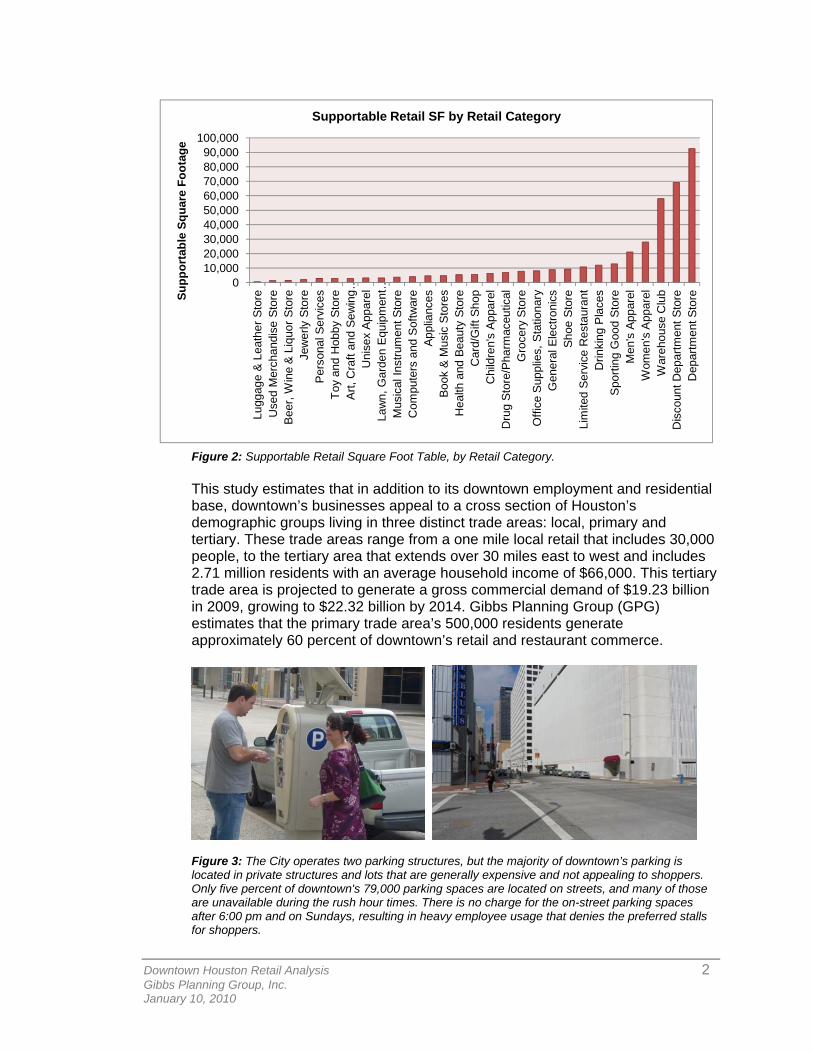

Supportable Retail SF by Retail Category

Figure 2: Supportable Retail Square Foot Table, by Retail Category. This study estimates that in addition to its downtown employment and residential base, downtown’s businesses appeal to a cross section of Houston’s demographic groups living in three distinct trade areas: local, primary and tertiary. These trade areas range from a one mile local retail that includes 30,000 people, to the tertiary area that extends over 30 miles east to west and includes 2.71 million residents with an average household income of $66,000. This tertiary trade area is projected to generate a gross commercial demand of $19.23 billion in 2009, growing to $22.32 billion by 2014. Gibbs Planning Group (GPG) estimates that the primary trade area’s 500,000 residents generate approximately 60 percent of downtown’s retail and restaurant commerce.

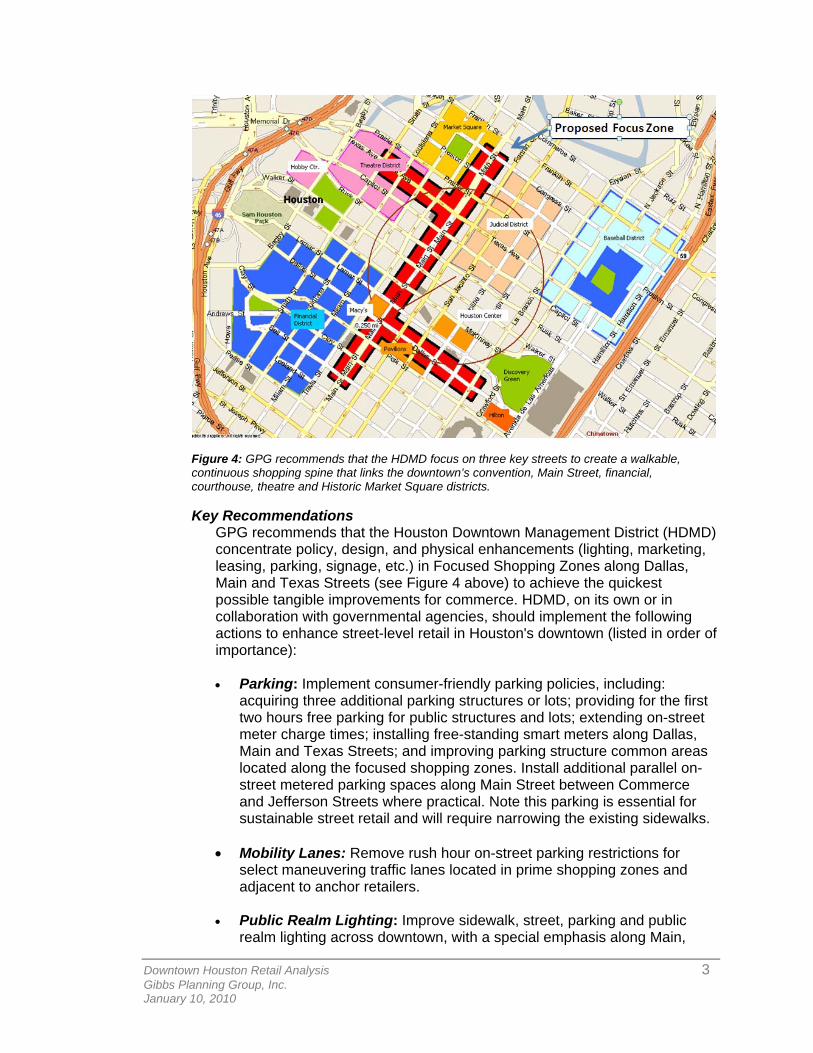

Figure 3: The City operates two parking structures, but the majority of downtown’s parking is located in private structures and lots that are generally expensive and not appealing to shoppers. Only five percent of downtown's 79,000 parking spaces are located on streets, and many of those are unavailable during the rush hour times. There is no charge for the on-street parking spaces after 6:00 pm and on Sundays, resulting in heavy employee usage that denies the preferred stalls for shoppers.

Downtown Houston Retail Analysis 3 Gibbs Planning Group, Inc. January 10, 2010

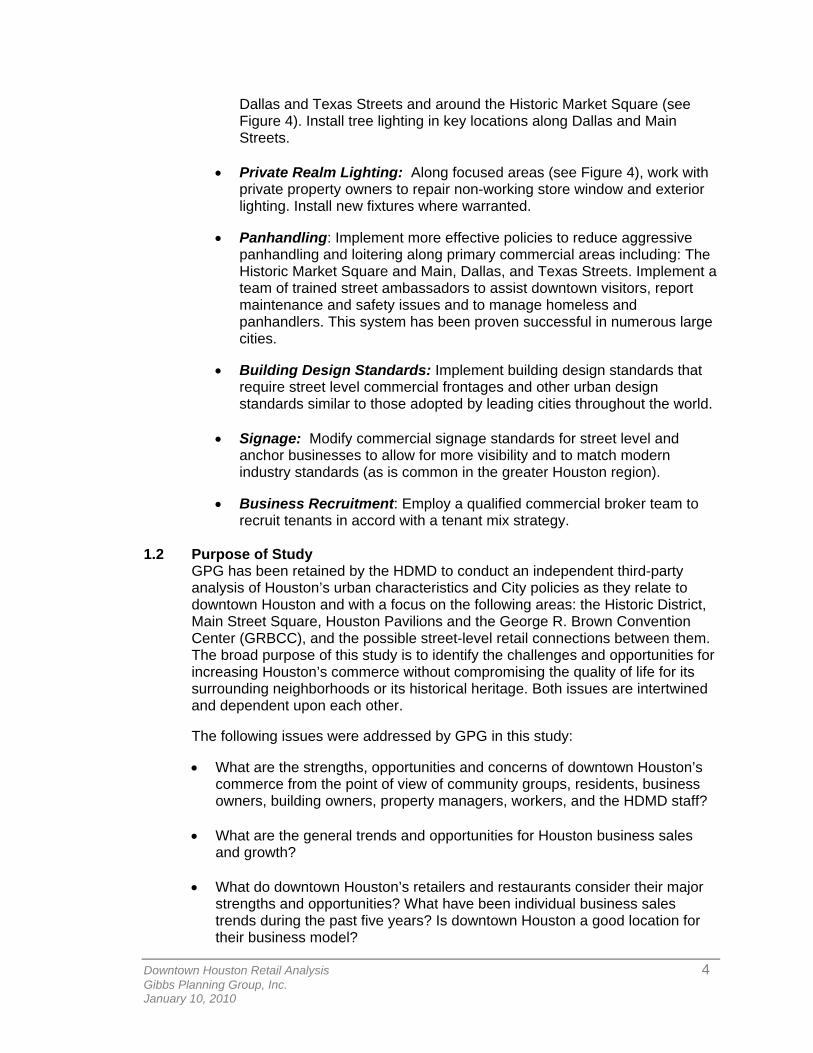

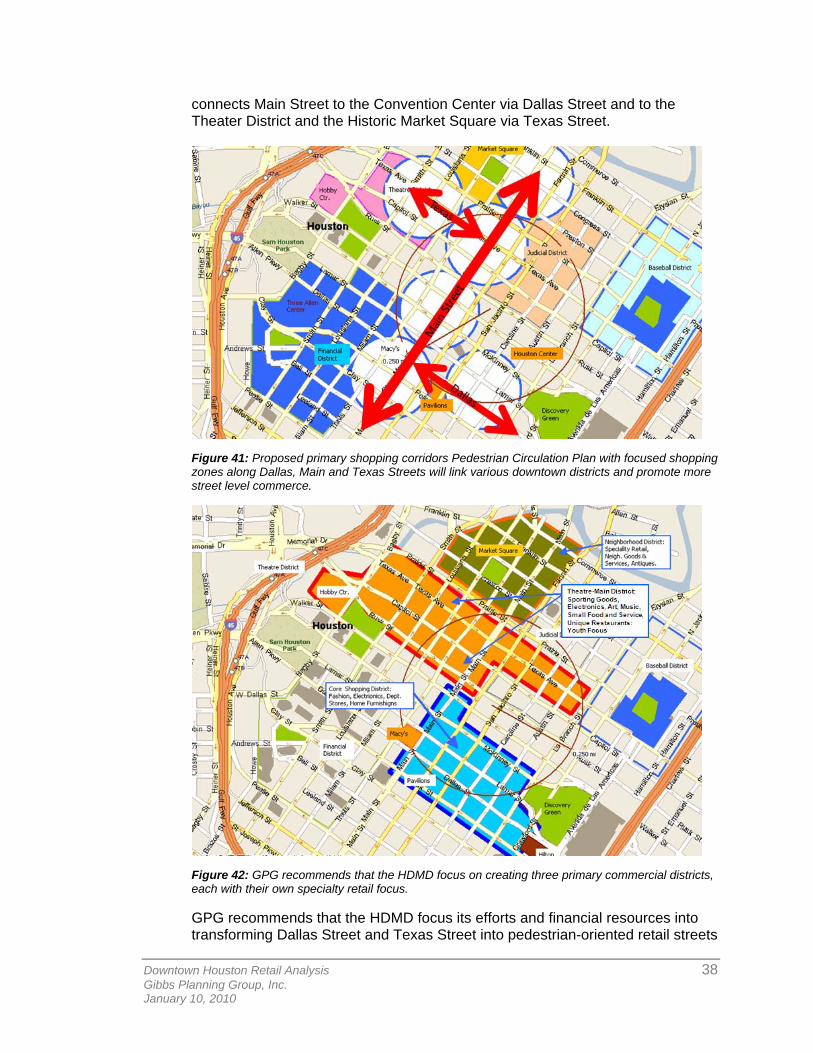

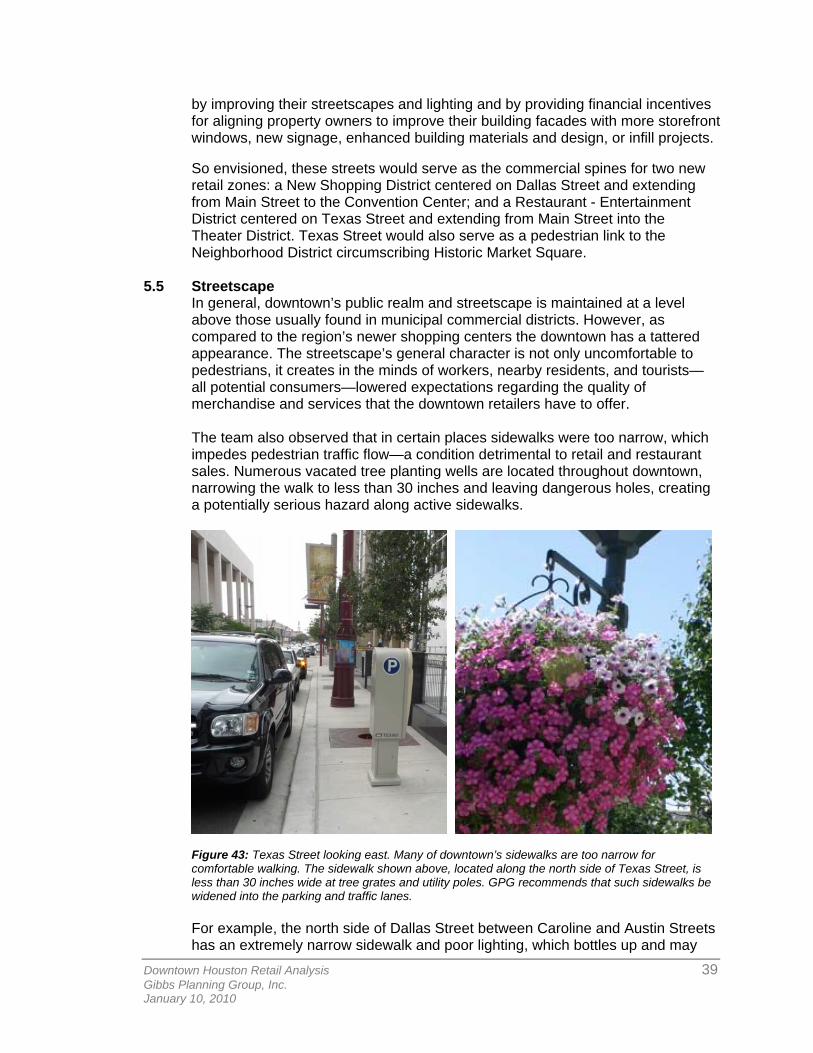

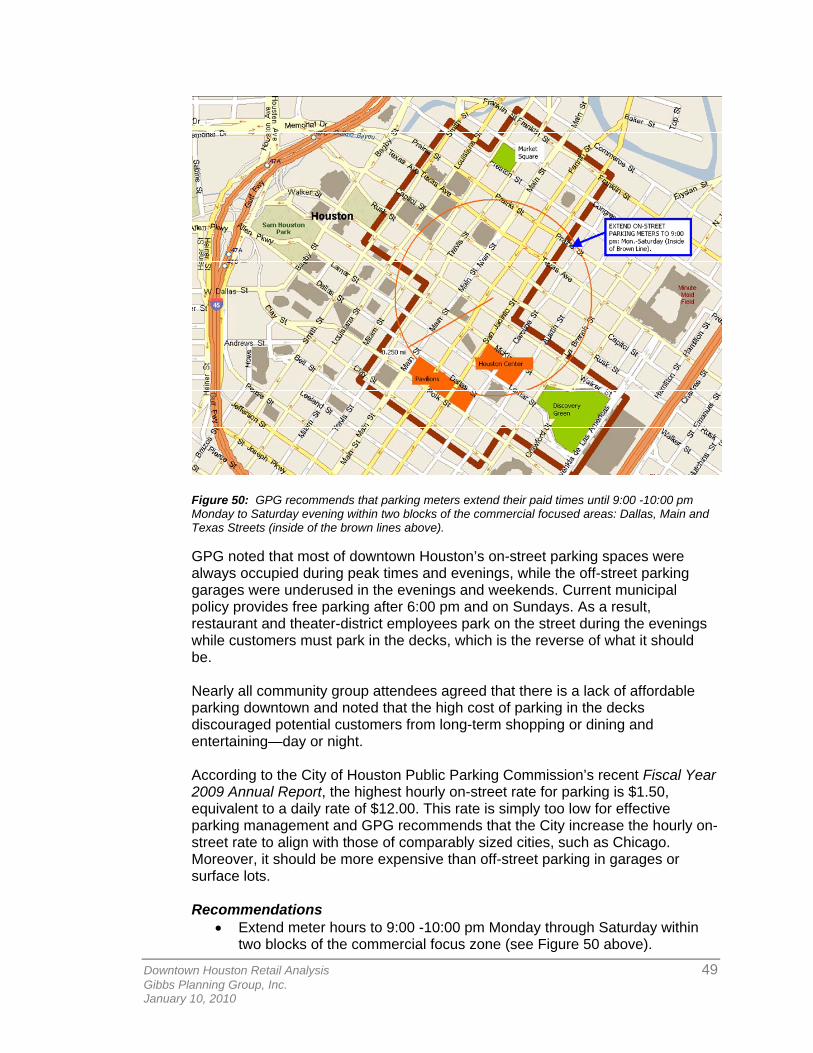

Figure 4: GPG recommends that the HDMD focus on three key streets to create a walkable, continuous shopping spine that links the downtown’s convention, Main Street, financial, courthouse, theatre and Historic Market Square districts. Key Recommendations

GPG recommends that the Houston Downtown Management District (HDMD) concentrate policy, design, and physical enhancements (lighting, marketing, leasing, parking, signage, etc.) in Focused Shopping Zones along Dallas, Main and Texas Streets (see Figure 4 above) to achieve the quickest possible tangible improvements for commerce. HDMD, on its own or in collaboration with governmental agencies, should implement the following actions to enhance street-level retail in Houston's downtown (listed in order of importance):

• Parking: Implement consumer-friendly parking policies, including:

acquiring three additional parking structures or lots; providing for the first two hours free parking for public structures and lots; extending on-street meter charge times; installing free-standing smart meters along Dallas, Main and Texas Streets; and improving parking structure common areas located along the focused shopping zones. Install additional parallel on-street metered parking spaces along Main Street between Commerce and Jefferson Streets where practical. Note this parking is essential for sustainable street retail and will require narrowing the existing sidewalks.

• Mobility Lanes: Remove rush hour on-street parking restrictions for select maneuvering traffic lanes located in prime shopping zones and adjacent to anchor retailers.

• Public Realm Lighting: Improve sidewalk, street, parking and public realm lighting across downtown, with a special emphasis along Main,

Downtown Houston Retail Analysis 4 Gibbs Planning Group, Inc. January 10, 2010

Dallas and Texas Streets and around the Historic Market Square (see Figure 4). Install tree lighting in key locations along Dallas and Main Streets.

• Private Realm Lighting: Along focused areas (see Figure 4), work with private property owners to repair non-working store window and exterior lighting. Install new fixtures where warranted.

• Panhandling: Implement more effective policies to reduce aggressive panhandling and loitering along primary commercial areas including: The Historic Market Square and Main, Dallas, and Texas Streets. Implement a team of trained street ambassadors to assist downtown visitors, report maintenance and safety issues and to manage homeless and panhandlers. This system has been proven successful in numerous large cities.

• Building Design Standards: Implement building design standards that

require street level commercial frontages and other urban design standards similar to those adopted by leading cities throughout the world.

• Signage: Modify commercial signage standards for street level and

anchor businesses to allow for more visibility and to match modern industry standards (as is common in the greater Houston region).

• Business Recruitment: Employ a qualified commercial broker team to

recruit tenants in accord with a tenant mix strategy. 1.2 Purpose of Study

GPG has been retained by the HDMD to conduct an independent third-party analysis of Houston’s urban characteristics and City policies as they relate to downtown Houston and with a focus on the following areas: the Historic District, Main Street Square, Houston Pavilions and the George R. Brown Convention Center (GRBCC), and the possible street-level retail connections between them. The broad purpose of this study is to identify the challenges and opportunities for increasing Houston’s commerce without compromising the quality of life for its surrounding neighborhoods or its historical heritage. Both issues are intertwined and dependent upon each other.

The following issues were addressed by GPG in this study:

• What are the strengths, opportunities and concerns of downtown Houston’s commerce from the point of view of community groups, residents, business owners, building owners, property managers, workers, and the HDMD staff?

• What are the general trends and opportunities for Houston business sales and growth?

• What do downtown Houston’s retailers and restaurants consider their major strengths and opportunities? What have been individual business sales trends during the past five years? Is downtown Houston a good location for their business model?

Downtown Houston Retail Analysis 5 Gibbs Planning Group, Inc. January 10, 2010

• How is downtown Houston’s built environment—including the streetscape and parking—impacting downtown commerce?

• What specific changes in HDMD operations and in City policies and

ordinances, including parking, security, signage, maintenance, and building approvals, would downtown Houston’s businesses, property owners, residents and stakeholders like to have modified? Will these modifications have the desired effect on downtown commerce?

• What is the potential growth for retail and restaurant expenditures for the next

five years?

• How is the new METRORail line on Main Street affecting downtown Houston businesses? Are there opportunities to improve METRORail operations to expand downtown commerce?

2.0 TRADE AREAS AND DEMOGRAPHICS Based on GPG’s field evaluation and interviews with local, regional, and national businesses, it was determined that the Houston downtown area currently has neighborhood, local, and regional draws that define three distinct trade areas: local, primary and tertiary.

Figure 5: The downtown’s trade area includes a wide range of age, race and income groups, especially young families.

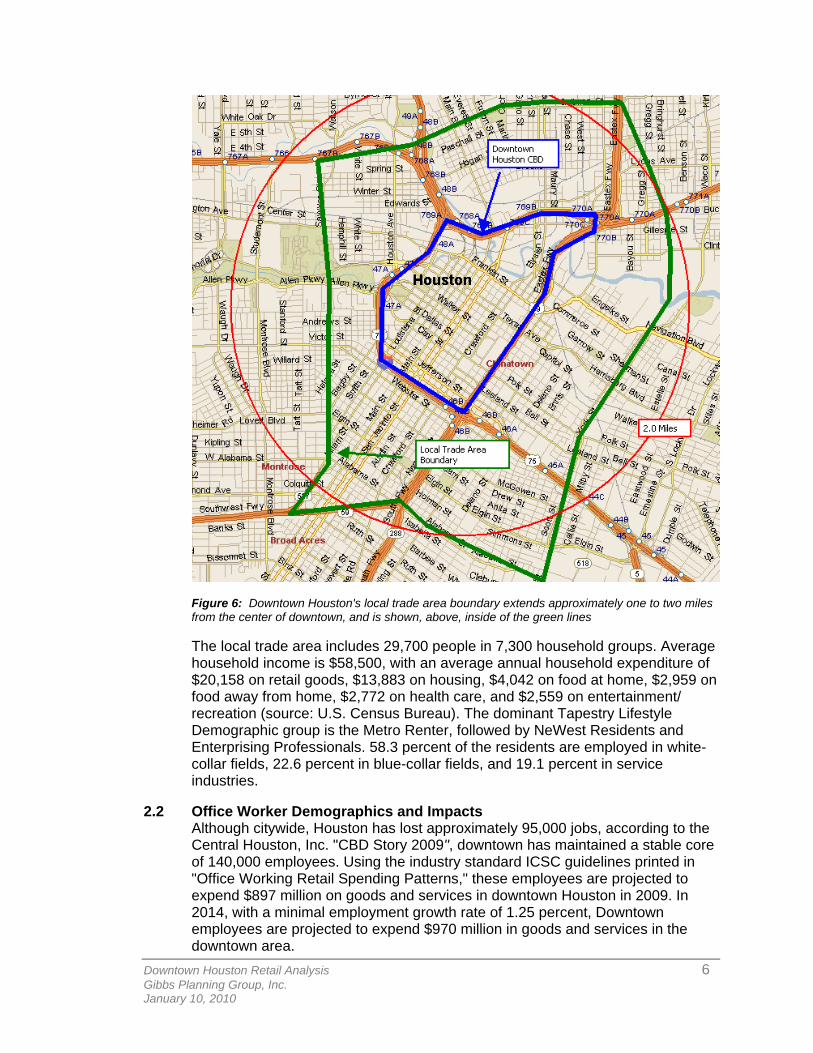

2.1 Local Trade Area Downtown Houston is frequently visited by people living in surrounding neighborhoods or working in adjoining business districts. During interviews, many downtown business owners quickly identified the local neighborhood their customers came from. Downtown Houston is an easy walk, bike ride, light rail ride or drive for people residing within this local area, and GPG estimates that it generates approximately eight to ten percent of downtown's commercial revenue, depending on the retail expenditure category. In 2008, people living or working in the local trade area had a potential gross demand for $104 million in total non-automotive retail goods and services, including $25.8 million for groceries, $25.2 million for restaurants, and $7.6 million for apparel and accessories. For many of the estimated 29,700 local residents, downtown's shops and restaurants are a convenient amenity that contributes to the enjoyment of living in the downtown area. These residents divide much of their local shopping and dining time between the Midtown Neighborhood and downtown Houston.

Downtown Houston Retail Analysis 6 Gibbs Planning Group, Inc. January 10, 2010

Figure 6: Downtown Houston's local trade area boundary extends approximately one to two miles from the center of downtown, and is shown, above, inside of the green lines The local trade area includes 29,700 people in 7,300 household groups. Average household income is $58,500, with an average annual household expenditure of $20,158 on retail goods, $13,883 on housing, $4,042 on food at home, $2,959 on food away from home, $2,772 on health care, and $2,559 on entertainment/ recreation (source: U.S. Census Bureau). The dominant Tapestry Lifestyle Demographic group is the Metro Renter, followed by NeWest Residents and Enterprising Professionals. 58.3 percent of the residents are employed in white-collar fields, 22.6 percent in blue-collar fields, and 19.1 percent in service industries.

2.2 Office Worker Demographics and Impacts Although citywide, Houston has lost approximately 95,000 jobs, according to the Central Houston, Inc. "CBD Story 2009", downtown has maintained a stable core of 140,000 employees. Using the industry standard ICSC guidelines printed in "Office Working Retail Spending Patterns," these employees are projected to expend $897 million on goods and services in downtown Houston in 2009. In 2014, with a minimal employment growth rate of 1.25 percent, Downtown employees are projected to expend $970 million in goods and services in the downtown area.

Downtown Houston Retail Analysis 7 Gibbs Planning Group, Inc. January 10, 2010

On average, these employees are projected to have spent over $6,400 each in 2009 before, during, and after work. The major retail category for this expenditure is Dining, with an estimated $331 million spent on full-service dining, followed by General Merchandise in department and discount department store categories. The third major category for worker expenditure is the Grocery category at $123 million, followed by Apparel and Accessories at $91 million per year.

2.3 Tourist and Convention Attendee Demographics and Impacts

Figure 7: The George R. Brown Convention Center is a 1.8 million SF convention center that opened in 1987 and expanded in 2001. (Image Source: George R. Brown Convention Center) In 2007, 31.4 million tourists and visitors came to the Greater Houston market, and spent $10.8 billion in the Greater Houston MSA economy. 63.9 percent of these tourists came from Texas itself, while Mexico accounted for the next largest tourist block at 16.0 percent. Visitor spending per trip increased in 2008 to a visitor-per-trip amount of $344 (not including air travel). Top activities in the Houston area include business, sightseeing, beach & waterfront, amusement parks/attractions, culture and history, and outdoor sports. As a business destination, Houston hosted 256 conventions in 2008, with over 550,000 delegates attending, spending over $550 million. Two national franchise sports stadiums are in downtown: the Toyota Center, which hosts the Houston Rockets; and Minute Maid Park, which is home to the Houston Astros. The combined attendance of both teams in their 2008-2009 seasons was 3.2 million. Tourism expenditure has been rising by an average of 5.6% per year over the last three years. Dining expenditures (NAICS #722) have risen to over $2 billion in 2008. Retail Sales (NAICS #'s 44 & 45) in the Houston MSA were $1.5 billion. This expenditure created and supported over 121,000 jobs in the Houston MSA during 2008. Over $276 million was generated in local taxes as a direct result of tourism, as well as approximately $659 million in state taxes.

Downtown Houston Retail Analysis 8 Gibbs Planning Group, Inc. January 10, 2010

2006 2007 2008 2009 (Est.) 2014 (Est.)

Accommodations 1,603 1,766 1,987 2,010 2,903

Dining 1,832 1,945 2,073 2,191 2,956

Food Stores 335 358 383 398 524

Ground Transport & Fuel 2,865 3,138 3,585 3,554 5,516

Arts, Entertainment & Recreation 1,234 1,273 1,308 1,417 1,812

Retail Sales 1,457 1,490 1,500 1,633 1,987

Air Transport 806 829 825 895 1,126Spending in Houston-Baytown- Sugar Land MSA 10,133 10,799 11,660 12,098 16,824

Gross Tourism Spending in Houston 9,570 10,012 10,774 11,552 16,355

Gross Tourism Spending in Baytown 99 109 127 130 174Gross Tourism Spending in Sugar Land 97 107 123 137 204

Annual Houston MSA Tourism Expenditure ($000,000's) by Category

Figure 8: Houston's share of tourism expenditure in the Houston-Baytown-Sugar Land MSA has dropped from 99% in 2003 to 92.4% in 2008, but is projected to rise to 97.2% in 2014.

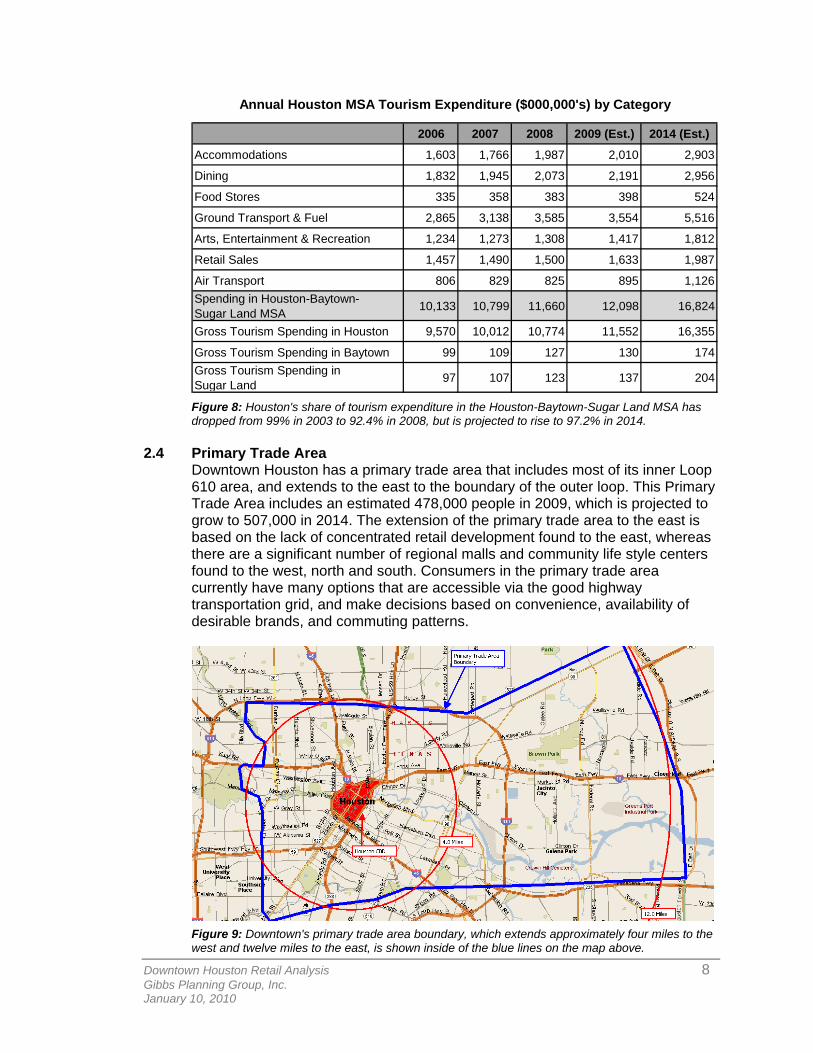

2.4 Primary Trade Area Downtown Houston has a primary trade area that includes most of its inner Loop 610 area, and extends to the east to the boundary of the outer loop. This Primary Trade Area includes an estimated 478,000 people in 2009, which is projected to grow to 507,000 in 2014. The extension of the primary trade area to the east is based on the lack of concentrated retail development found to the east, whereas there are a significant number of regional malls and community life style centers found to the west, north and south. Consumers in the primary trade area currently have many options that are accessible via the good highway transportation grid, and make decisions based on convenience, availability of desirable brands, and commuting patterns.

Figure 9: Downtown's primary trade area boundary, which extends approximately four miles to the west and twelve miles to the east, is shown inside of the blue lines on the map above.

Downtown Houston Retail Analysis 9 Gibbs Planning Group, Inc. January 10, 2010

There are 169,000 households within the primary trade area, and these are predicted to increase to 180,100 by 2014. Forty percent of these households were owner-occupied in 2009, which is projected to edge up to forty two percent by 2014. The primary trade area's households had an average income of $61,900 and a median household income of $42,400 in 2009. The median age in the primary trade area is 32.0 years, and the average household size is 2.68 persons. In 2009, the primary trade area has retail and restaurant (non-automotive) potential gross demand of $2.37 billion, including $649 million for grocery stores; $167 million for apparel, shoes, and accessories; and $599 million for restaurants. This study estimates that 65 to 70 percent of downtown Houston's commerce is generated by persons living in or visiting the primary trade area.

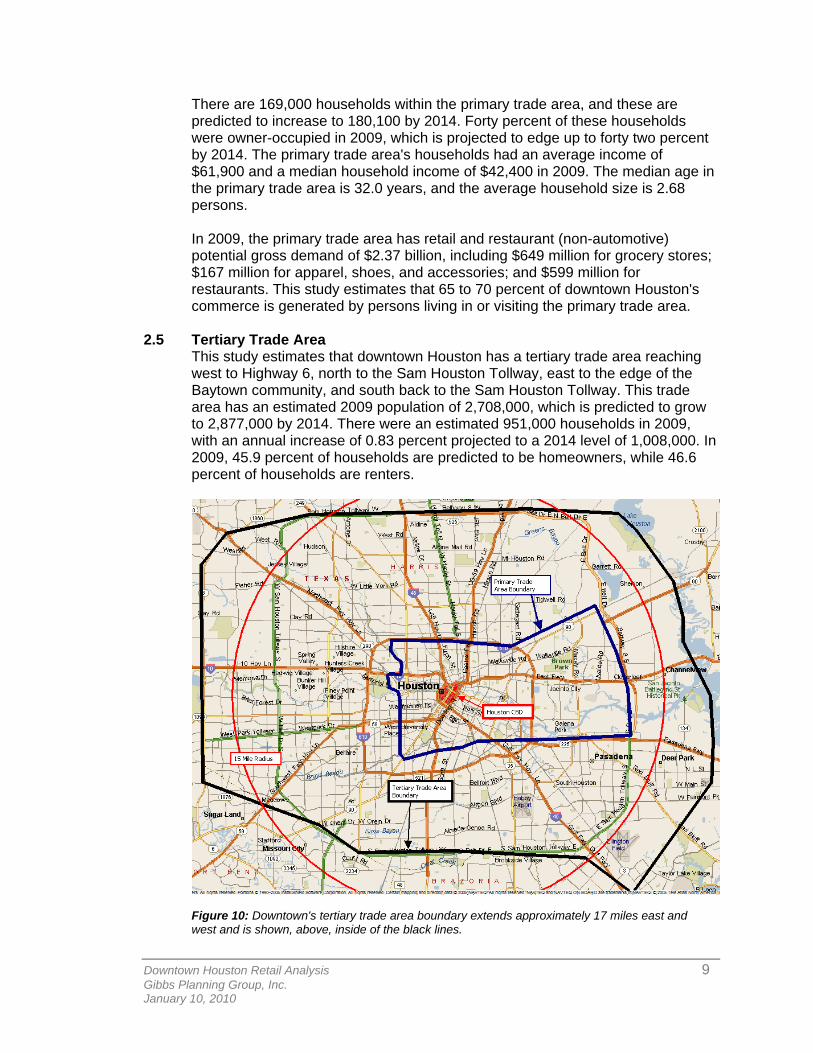

2.5 Tertiary Trade Area

This study estimates that downtown Houston has a tertiary trade area reaching west to Highway 6, north to the Sam Houston Tollway, east to the edge of the Baytown community, and south back to the Sam Houston Tollway. This trade area has an estimated 2009 population of 2,708,000, which is predicted to grow to 2,877,000 by 2014. There were an estimated 951,000 households in 2009, with an annual increase of 0.83 percent projected to a 2014 level of 1,008,000. In 2009, 45.9 percent of households are predicted to be homeowners, while 46.6 percent of households are renters.

Figure 10: Downtown's tertiary trade area boundary extends approximately 17 miles east and west and is shown, above, inside of the black lines.

Downtown Houston Retail Analysis 10 Gibbs Planning Group, Inc. January 10, 2010

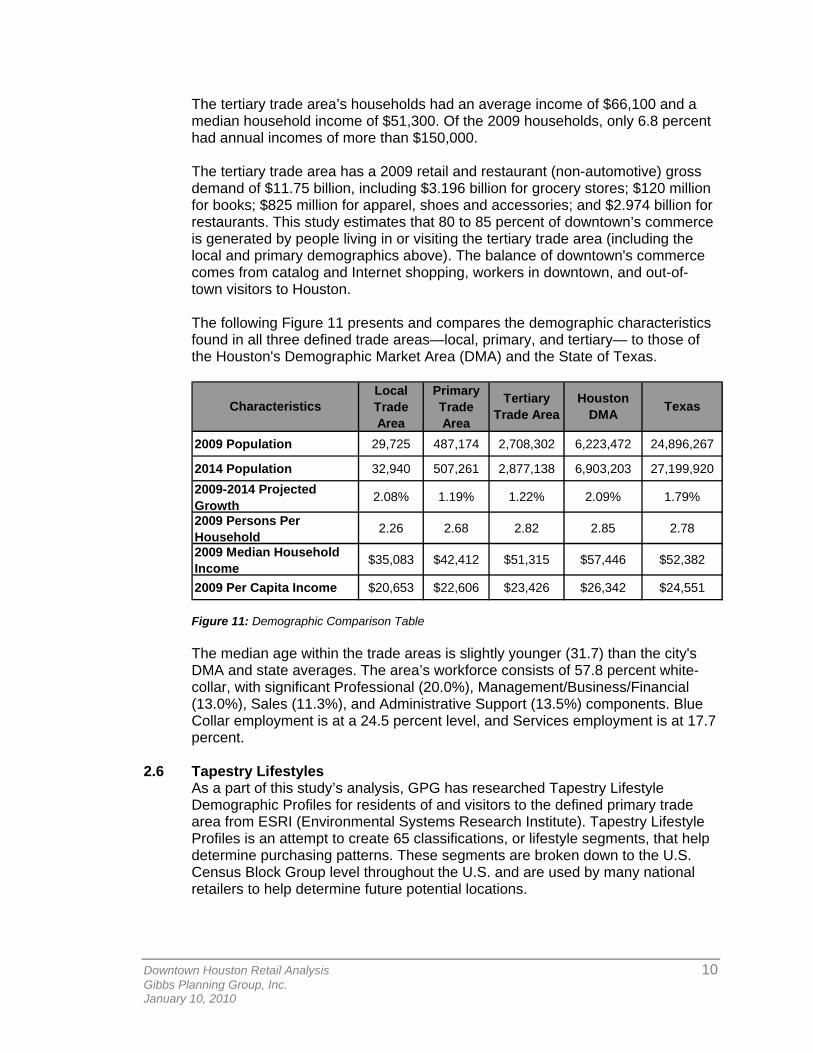

The tertiary trade area’s households had an average income of $66,100 and a median household income of $51,300. Of the 2009 households, only 6.8 percent had annual incomes of more than $150,000. The tertiary trade area has a 2009 retail and restaurant (non-automotive) gross demand of $11.75 billion, including $3.196 billion for grocery stores; $120 million for books; $825 million for apparel, shoes and accessories; and $2.974 billion for restaurants. This study estimates that 80 to 85 percent of downtown’s commerce is generated by people living in or visiting the tertiary trade area (including the local and primary demographics above). The balance of downtown's commerce comes from catalog and Internet shopping, workers in downtown, and out-of-town visitors to Houston. The following Figure 11 presents and compares the demographic characteristics found in all three defined trade areas—local, primary, and tertiary— to those of the Houston's Demographic Market Area (DMA) and the State of Texas.

2009 Population 29,725 487,174 2,708,302 6,223,472 24,896,267

2014 Population 32,940 507,261 2,877,138 6,903,203 27,199,9202009-2014 Projected Growth

2.08% 1.19% 1.22% 2.09% 1.79%

2009 Persons Per Household

2.26 2.68 2.82 2.85 2.78

2009 Median Household Income

$35,083 $42,412 $51,315 $57,446 $52,382

2009 Per Capita Income $20,653 $22,606 $23,426 $26,342 $24,551

Characteristics Houston DMA Texas

Local Trade Area

Primary Trade Area

Tertiary Trade Area

Figure 11: Demographic Comparison Table The median age within the trade areas is slightly younger (31.7) than the city's DMA and state averages. The area’s workforce consists of 57.8 percent white-collar, with significant Professional (20.0%), Management/Business/Financial (13.0%), Sales (11.3%), and Administrative Support (13.5%) components. Blue Collar employment is at a 24.5 percent level, and Services employment is at 17.7 percent.

2.6 Tapestry Lifestyles As a part of this study’s analysis, GPG has researched Tapestry Lifestyle Demographic Profiles for residents of and visitors to the defined primary trade area from ESRI (Environmental Systems Research Institute). Tapestry Lifestyle Profiles is an attempt to create 65 classifications, or lifestyle segments, that help determine purchasing patterns. These segments are broken down to the U.S. Census Block Group level throughout the U.S. and are used by many national retailers to help determine future potential locations.

Downtown Houston Retail Analysis 11 Gibbs Planning Group, Inc. January 10, 2010

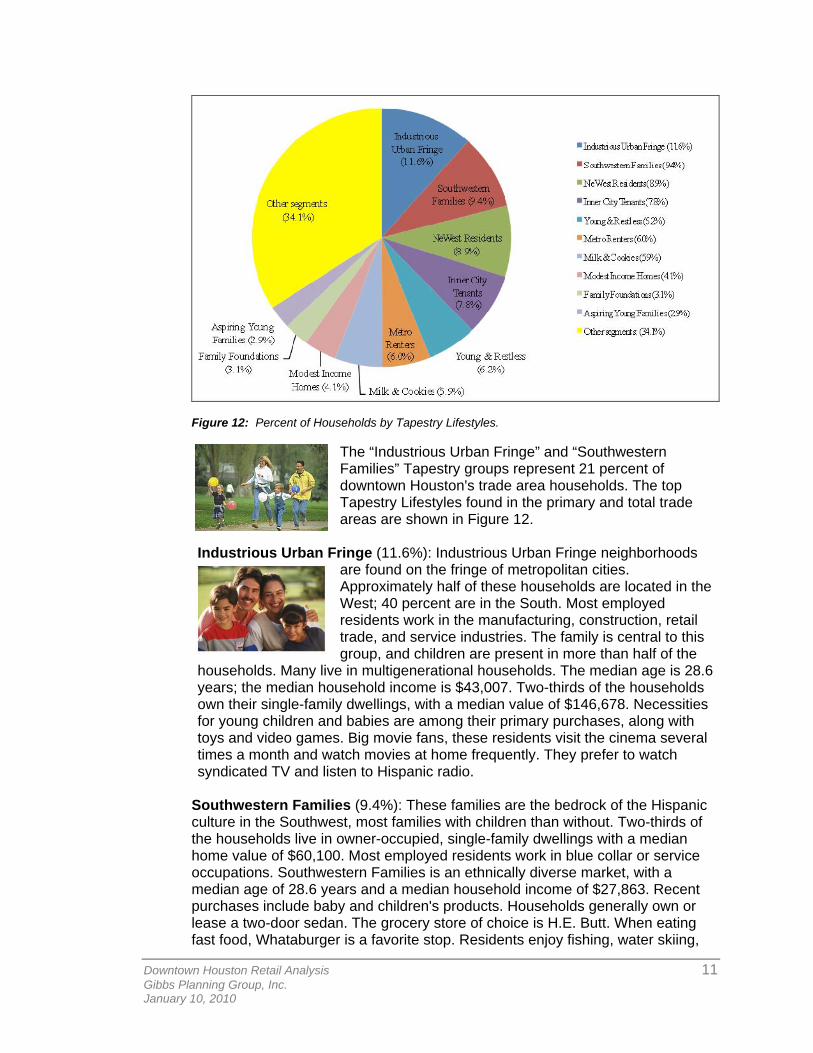

Figure 12: Percent of Households by Tapestry Lifestyles.

The “Industrious Urban Fringe” and “Southwestern Families” Tapestry groups represent 21 percent of downtown Houston's trade area households. The top Tapestry Lifestyles found in the primary and total trade areas are shown in Figure 12.

Industrious Urban Fringe (11.6%): Industrious Urban Fringe neighborhoods

are found on the fringe of metropolitan cities. Approximately half of these households are located in the West; 40 percent are in the South. Most employed residents work in the manufacturing, construction, retail trade, and service industries. The family is central to this group, and children are present in more than half of the

households. Many live in multigenerational households. The median age is 28.6 years; the median household income is $43,007. Two-thirds of the households own their single-family dwellings, with a median value of $146,678. Necessities for young children and babies are among their primary purchases, along with toys and video games. Big movie fans, these residents visit the cinema several times a month and watch movies at home frequently. They prefer to watch syndicated TV and listen to Hispanic radio.

Southwestern Families (9.4%): These families are the bedrock of the Hispanic culture in the Southwest, most families with children than without. Two-thirds of the households live in owner-occupied, single-family dwellings with a median home value of $60,100. Most employed residents work in blue collar or service occupations. Southwestern Families is an ethnically diverse market, with a median age of 28.6 years and a median household income of $27,863. Recent purchases include baby and children's products. Households generally own or lease a two-door sedan. The grocery store of choice is H.E. Butt. When eating fast food, Whataburger is a favorite stop. Residents enjoy fishing, water skiing,

Downtown Houston Retail Analysis 12 Gibbs Planning Group, Inc. January 10, 2010

playing soccer, and going to the movies. They read gardening and parenthood magazines and listen to Hispanic and urban radio formats. Typical TV viewing includes comedies as well as wrestling and boxing.

NeWest Residents (8.9%): Most NeWest Residents members rent apartments in mid- or high-rise buildings, primarily in major cities in the West and South. California has the largest concentration of these households, followed by Texas. Families dominate this market. Children reside in 54 percent of the households, either in

married-couple or single-parent families. Approximately half of the population is foreign-born. This young market has a median age of 25.4 years. Most of the employed residents work in service and skilled labor occupations. These residents lead a strongly family-oriented lifestyle. Budget constraints restrict their purchases to essentials, such as baby food, equipment, and products as well as children's clothing. For fun, families go to the movies, visit theme parks, and play soccer. They like to watch sports on TV, especially wrestling and soccer, and listen to Hispanic radio.

Inner City Tenants (7.8%): Inner City Tenants neighborhoods are a microcosm of urban diversity, located primarily in the South and West. This multicultural market is young, with a median age of 27.9 years. Households are a mix of singles and families. Most residents rent economical apartments in mid- or high-rise buildings. Recent

household purchases by this market include video game systems, baby food, baby products, and furniture. Internet access at home is not typical; those who have no access at home surf the Internet at school or at the library. Playing games and visiting chat rooms are typical online activities. Residents frequently eat at fast-food restaurants. They enjoy going to the movies, attending football and basketball games, participating in water sports, and playing football, basketball, and soccer. Some enjoy visiting bars and nightclubs to go dancing.

Young & Restless (6.2%): Change is the constant in this diverse market. With a median age of 28.7 years, the population is young and on the go. About 85 percent of householders moved in the last five years. Young and Restless householders are primarily renters, living in apartments in multiunit buildings. Almost 60 percent are

single-person or shared households. This educated market has the highest labor force participation among all the Community Tapestry segments, at 76 percent, and the highest female labor force participation, at 73 percent. The median household income is $45,236. Residents use the Internet daily to visit chat rooms, play games, obtain the latest news, and search for employment. They read computer and music magazines and listen to public radio. They watch movies in the theater and on DVD, attend rock concerts, play pool, go dancing, and exercise weekly at a gym. Metro Renters (6.0%): Metro Renters residents are young (approximately 30 percent are in their 20s), well-educated singles beginning their professional careers in some of the largest U.S. cities such as New York City, Chicago, and

Downtown Houston Retail Analysis 13 Gibbs Planning Group, Inc. January 10, 2010

Los Angeles. The median age is 33.8 years; the median household income is $59,730. As the name Metro Renters implies, most residents are renting apartments in high-rise buildings, living alone or with a roommate. Their interests include traveling, reading two or more daily newspapers, listening to classical music and public radio programs, and

surfing the Internet. For exercise, they work out regularly at clubs, play tennis and volleyball, practice yoga, ski, and jog. They enjoy dancing, attending rock concerts, going to museums or the movies, and throwing a Frisbee. Painting and drawing are favorite hobbies. Politically, this market is liberal.

Milk & Cookies (5.9%): Milk and Cookies households are composed mainly of young, affluent married-couple families. Approximately half of the households include children. The median age for this market is 34 years. Residents prefer single-family homes in suburban areas, chiefly in the South, particularly in Texas. Smaller

concentrations of households are located in the West and Midwest. The median home value is $148,781. Families with two or more workers, more than one child, and two or more vehicles is the norm for this market. Residents are well insured for the future. The presence of children drives their large purchases of baby and children's products and timesavers such as fast food. For fun, residents play video games, chess, backgammon, basketball and football, or fly kites. Favorite cable channels include Toon Disney, The Discovery Health Channel, ESPNews, and Lifetime Movie Network.

Modest Income Homes (4.1%): Modest Income Homes neighborhoods are found primarily in the older suburbs of metropolitan areas. Single-family dwellings represent more than two-thirds of the housing; 15 percent are duplexes. The median home value is $57,381. Household

types are mainly single person and single parent. However, 64 percent of households are family types. The median age is 35.7 years. Slightly more employed residents work part time than full time, mainly in service and blue-collar occupations. At 20 percent, unemployment is high. These frugal residents shop at discount stores, do not pay for Internet access, and rarely eat out. They are content to wait for movies to be shown on TV instead of going to the theater. They watch daytime and primetime TV, especially courtroom TV shows and sitcoms, and listen to urban and gospel radio. A favorite cable channel is BET.

Family Foundations (3.1%): Family is the cornerstone of life in Family Foundations communities. A mix of married couples, single parents, grandparents, and young and adult children populate these small, urban neighborhoods located in large metropolitan areas, primarily in the South and Midwest. This market represents stability. Hardly any

household growth has occurred since 2000; these neighborhoods experience little turnover. The median age is 39.0 years; the median household income is $46,308. Most households are single-family structures built before 1970, occupied by owners. Many residents are members of church boards or religious clubs and participate in fund-raising. Basketball is a favorite sport: residents play

Downtown Houston Retail Analysis 14 Gibbs Planning Group, Inc. January 10, 2010

it, attend professional games, watch games on TV and listen to games on the radio. They watch courtroom TV shows, sports, and news programs on TV and listen to gospel, urban, and jazz radio formats.

Aspiring Young Families (2.9%): Aspiring Young Families neighborhoods are located in large, growing metropolitan areas in the South and West, with the highest concentrations in California, Florida, and Texas. Mainly composed of young, married-couple families or single parents with children, the median age for this segment is 30.6 years. Nearly half of the households are

owner-occupied, single-family dwellings or townhomes, and over half are occupied by renters, many living in newer, multiunit buildings. Residents spend much of their discretionary income on baby and children's products and toys as well as home furnishings. Recent electronic purchases include cameras and video game systems. Leisure activities include dining out, dancing, going to the movies, attending professional football games, fishing, weight lifting, and playing basketball. Typically, vacations would include visits to theme parks. Internet usage mainly involves chat room visits.

3.0 MARKET CONDITIONS

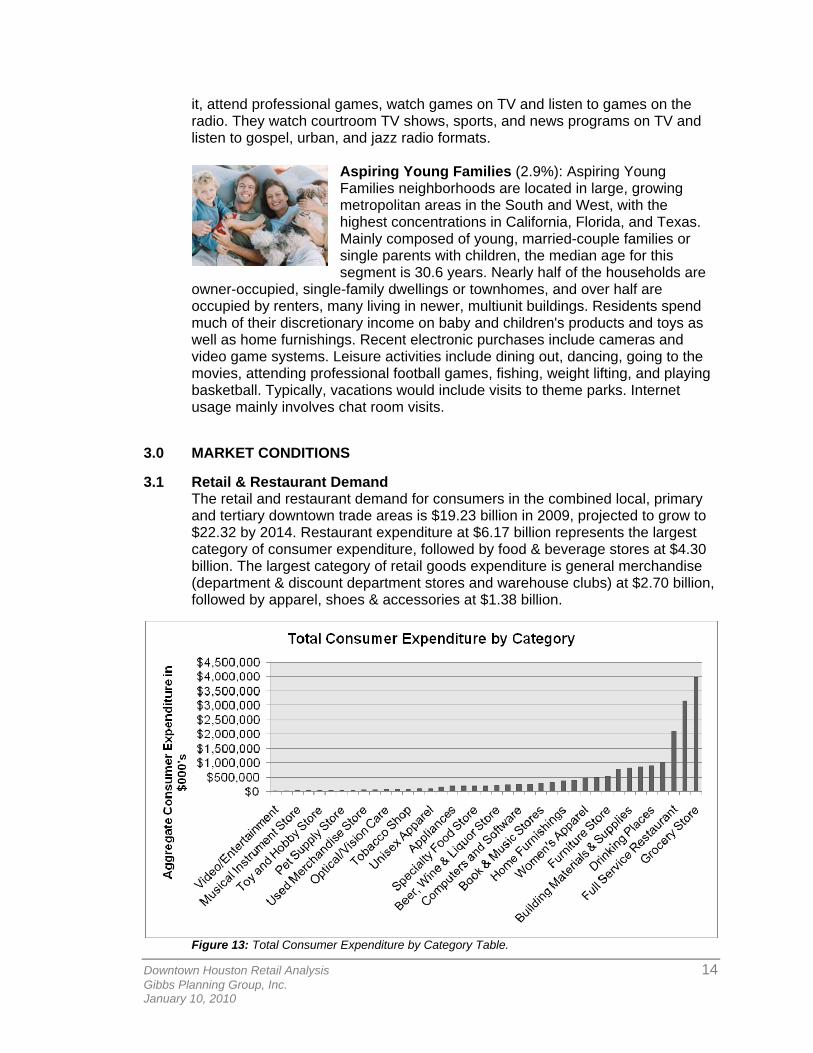

3.1 Retail & Restaurant Demand The retail and restaurant demand for consumers in the combined local, primary and tertiary downtown trade areas is $19.23 billion in 2009, projected to grow to $22.32 by 2014. Restaurant expenditure at $6.17 billion represents the largest category of consumer expenditure, followed by food & beverage stores at $4.30 billion. The largest category of retail goods expenditure is general merchandise (department & discount department stores and warehouse clubs) at $2.70 billion, followed by apparel, shoes & accessories at $1.38 billion.

Figure 13: Total Consumer Expenditure by Category Table.

Downtown Houston Retail Analysis 15 Gibbs Planning Group, Inc. January 10, 2010

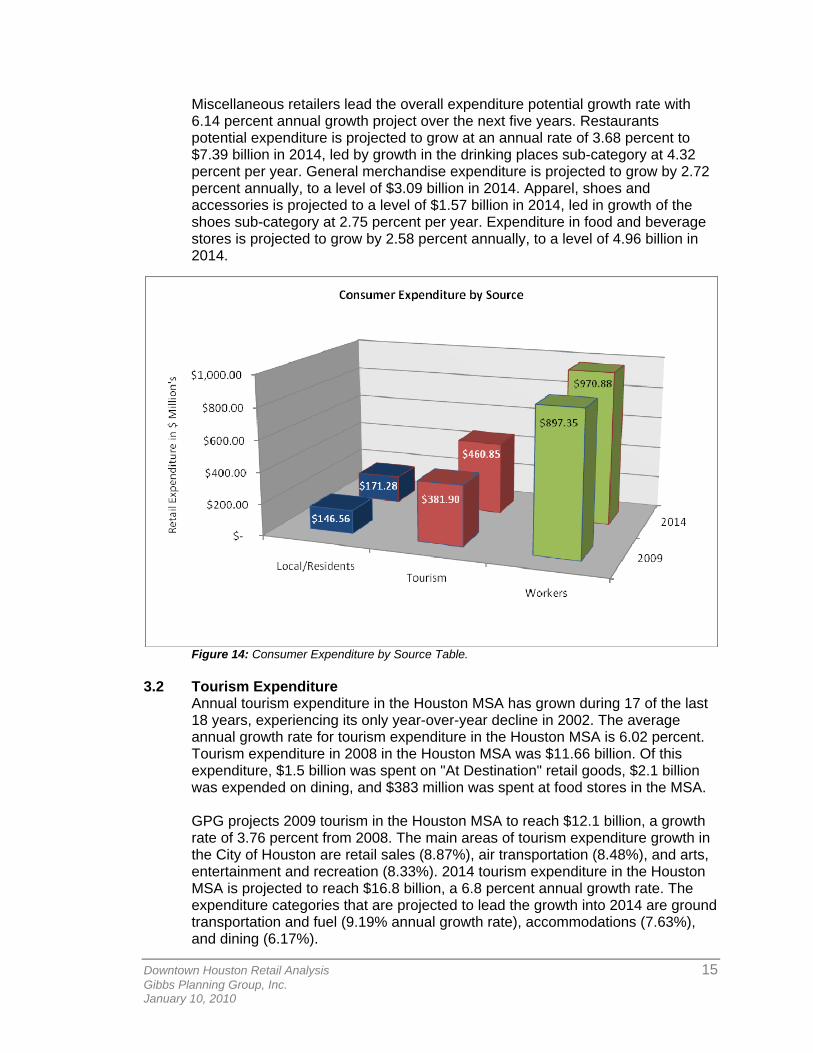

Miscellaneous retailers lead the overall expenditure potential growth rate with 6.14 percent annual growth project over the next five years. Restaurants potential expenditure is projected to grow at an annual rate of 3.68 percent to $7.39 billion in 2014, led by growth in the drinking places sub-category at 4.32 percent per year. General merchandise expenditure is projected to grow by 2.72 percent annually, to a level of $3.09 billion in 2014. Apparel, shoes and accessories is projected to a level of $1.57 billion in 2014, led in growth of the shoes sub-category at 2.75 percent per year. Expenditure in food and beverage stores is projected to grow by 2.58 percent annually, to a level of 4.96 billion in 2014.

Figure 14: Consumer Expenditure by Source Table.

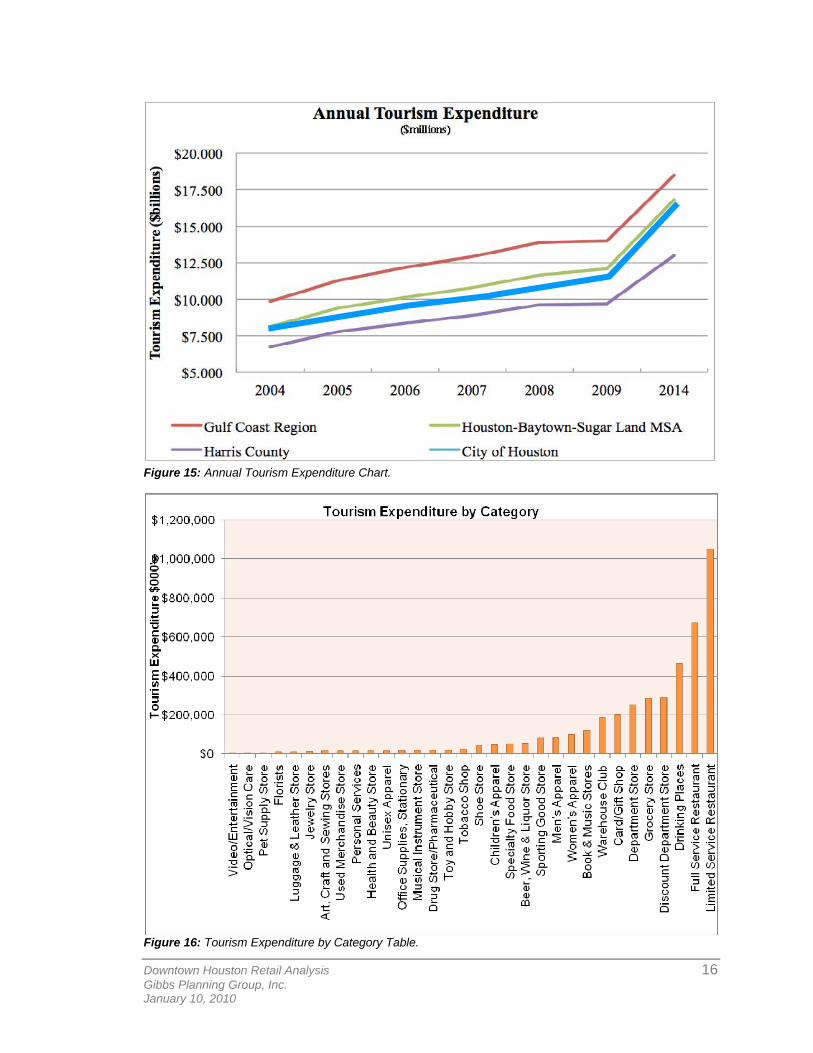

3.2 Tourism Expenditure Annual tourism expenditure in the Houston MSA has grown during 17 of the last 18 years, experiencing its only year-over-year decline in 2002. The average annual growth rate for tourism expenditure in the Houston MSA is 6.02 percent. Tourism expenditure in 2008 in the Houston MSA was $11.66 billion. Of this expenditure, $1.5 billion was spent on "At Destination" retail goods, $2.1 billion was expended on dining, and $383 million was spent at food stores in the MSA. GPG projects 2009 tourism in the Houston MSA to reach $12.1 billion, a growth rate of 3.76 percent from 2008. The main areas of tourism expenditure growth in the City of Houston are retail sales (8.87%), air transportation (8.48%), and arts, entertainment and recreation (8.33%). 2014 tourism expenditure in the Houston MSA is projected to reach $16.8 billion, a 6.8 percent annual growth rate. The expenditure categories that are projected to lead the growth into 2014 are ground transportation and fuel (9.19% annual growth rate), accommodations (7.63%), and dining (6.17%).

Downtown Houston Retail Analysis 16 Gibbs Planning Group, Inc. January 10, 2010

Figure 15: Annual Tourism Expenditure Chart.

Figure 16: Tourism Expenditure by Category Table.

Downtown Houston Retail Analysis 17 Gibbs Planning Group, Inc. January 10, 2010

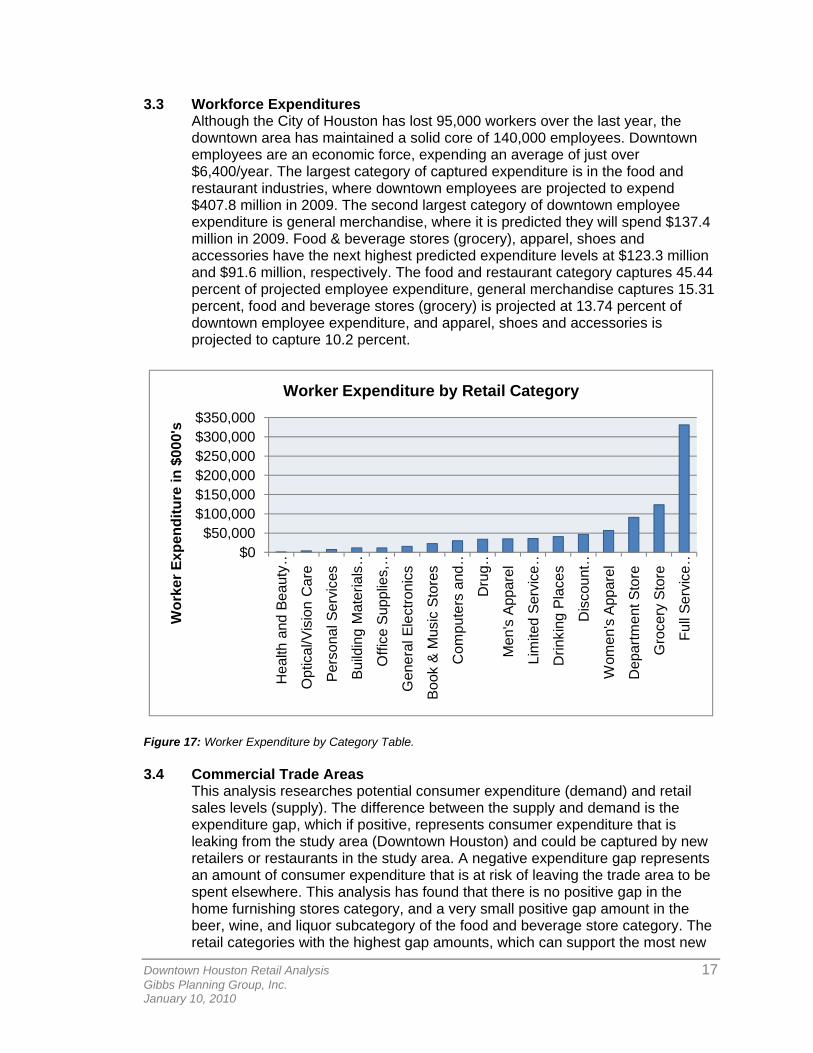

3.3 Workforce Expenditures Although the City of Houston has lost 95,000 workers over the last year, the downtown area has maintained a solid core of 140,000 employees. Downtown employees are an economic force, expending an average of just over $6,400/year. The largest category of captured expenditure is in the food and restaurant industries, where downtown employees are projected to expend $407.8 million in 2009. The second largest category of downtown employee expenditure is general merchandise, where it is predicted they will spend $137.4 million in 2009. Food & beverage stores (grocery), apparel, shoes and accessories have the next highest predicted expenditure levels at $123.3 million and $91.6 million, respectively. The food and restaurant category captures 45.44 percent of projected employee expenditure, general merchandise captures 15.31 percent, food and beverage stores (grocery) is projected at 13.74 percent of downtown employee expenditure, and apparel, shoes and accessories is projected to capture 10.2 percent.

$0$50,000

$100,000$150,000$200,000$250,000$300,000$350,000

Hea

lth a

nd B

eaut

y …

Opt

ical

/Vis

ion

Car

e

Pers

onal

Ser

vice

s

Build

ing

Mat

eria

ls …

Offi

ce S

uppl

ies,

…

Gen

eral

Ele

ctro

nics

Book

& M

usic

Sto

res

Com

pute

rs a

nd …

Dru

g …

Men

's A

ppar

el

Lim

ited

Serv

ice …

Drin

king

Pla

ces

Dis

coun

t …

Wom

en's

App

arel

Dep

artm

ent S

tore

Gro

cery

Sto

re

Full

Serv

ice …

Wor

ker E

xpen

ditu

re in

$00

0's

Worker Expenditure by Retail Category

Figure 17: Worker Expenditure by Category Table.

3.4 Commercial Trade Areas

This analysis researches potential consumer expenditure (demand) and retail sales levels (supply). The difference between the supply and demand is the expenditure gap, which if positive, represents consumer expenditure that is leaking from the study area (Downtown Houston) and could be captured by new retailers or restaurants in the study area. A negative expenditure gap represents an amount of consumer expenditure that is at risk of leaving the trade area to be spent elsewhere. This analysis has found that there is no positive gap in the home furnishing stores category, and a very small positive gap amount in the beer, wine, and liquor subcategory of the food and beverage store category. The retail categories with the highest gap amounts, which can support the most new

Downtown Houston Retail Analysis 18 Gibbs Planning Group, Inc. January 10, 2010

retail square footage, are (1) general merchandise department stores; (2) apparel, shoes and accessories; (3) electronics, appliances and computers; and (4) food and restaurants.

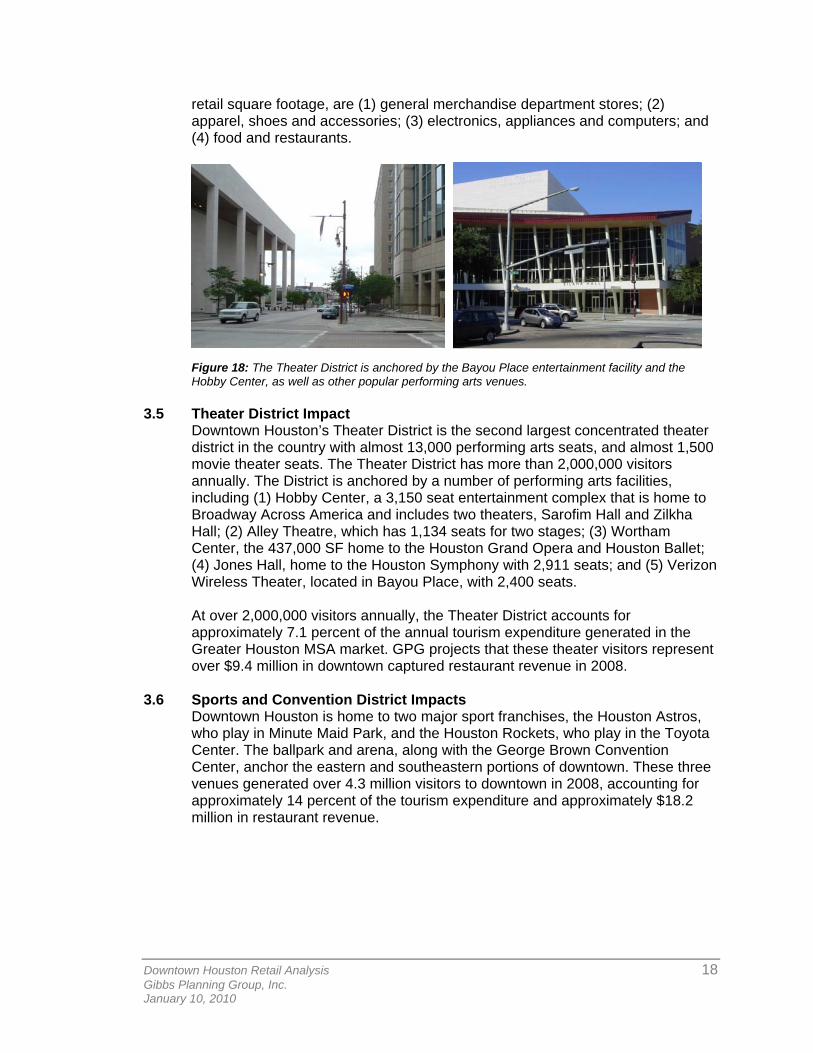

Figure 18: The Theater District is anchored by the Bayou Place entertainment facility and the Hobby Center, as well as other popular performing arts venues.

3.5 Theater District Impact Downtown Houston’s Theater District is the second largest concentrated theater district in the country with almost 13,000 performing arts seats, and almost 1,500 movie theater seats. The Theater District has more than 2,000,000 visitors annually. The District is anchored by a number of performing arts facilities, including (1) Hobby Center, a 3,150 seat entertainment complex that is home to Broadway Across America and includes two theaters, Sarofim Hall and Zilkha Hall; (2) Alley Theatre, which has 1,134 seats for two stages; (3) Wortham Center, the 437,000 SF home to the Houston Grand Opera and Houston Ballet; (4) Jones Hall, home to the Houston Symphony with 2,911 seats; and (5) Verizon Wireless Theater, located in Bayou Place, with 2,400 seats. At over 2,000,000 visitors annually, the Theater District accounts for approximately 7.1 percent of the annual tourism expenditure generated in the Greater Houston MSA market. GPG projects that these theater visitors represent over $9.4 million in downtown captured restaurant revenue in 2008.

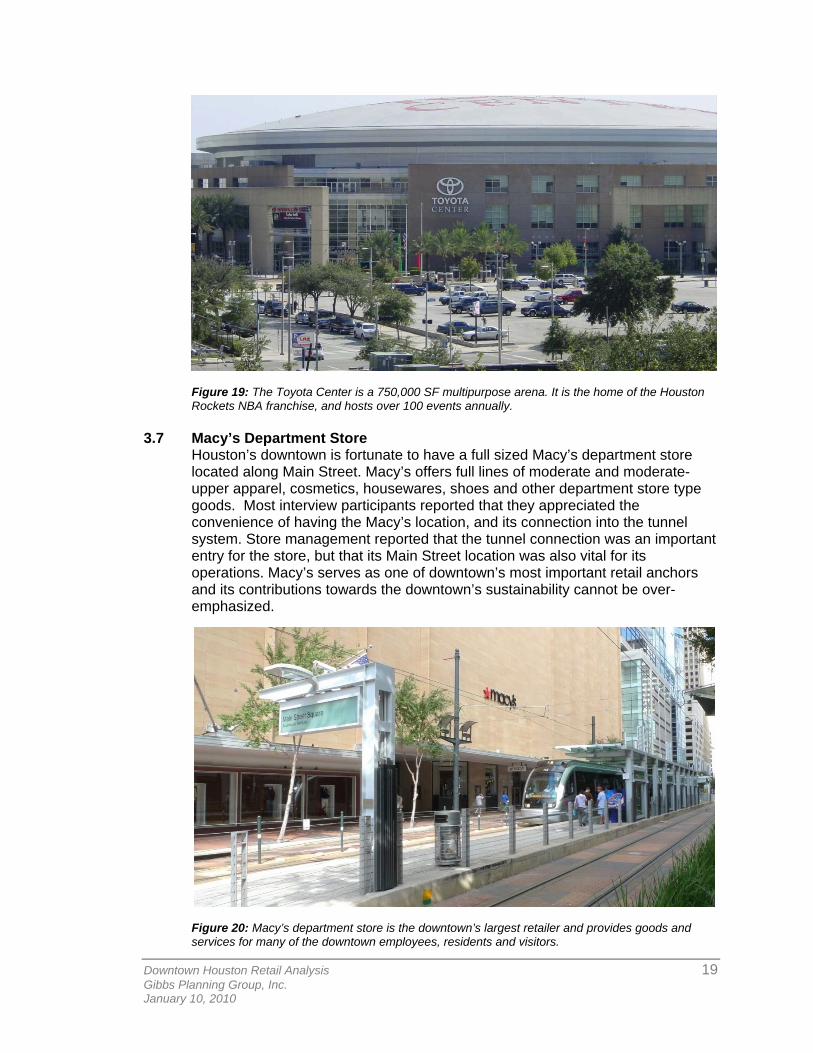

3.6 Sports and Convention District Impacts Downtown Houston is home to two major sport franchises, the Houston Astros, who play in Minute Maid Park, and the Houston Rockets, who play in the Toyota Center. The ballpark and arena, along with the George Brown Convention Center, anchor the eastern and southeastern portions of downtown. These three venues generated over 4.3 million visitors to downtown in 2008, accounting for approximately 14 percent of the tourism expenditure and approximately $18.2 million in restaurant revenue.

Downtown Houston Retail Analysis 19 Gibbs Planning Group, Inc. January 10, 2010

Figure 19: The Toyota Center is a 750,000 SF multipurpose arena. It is the home of the Houston Rockets NBA franchise, and hosts over 100 events annually.

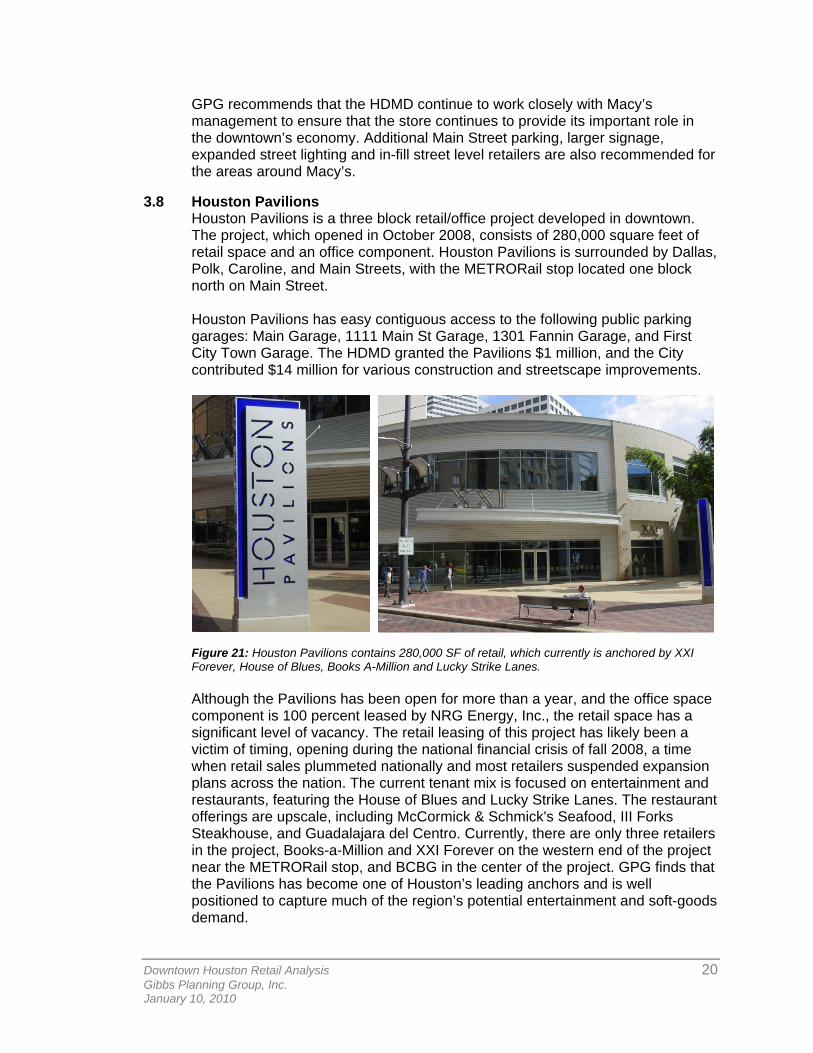

3.7 Macy’s Department Store Houston’s downtown is fortunate to have a full sized Macy’s department store located along Main Street. Macy’s offers full lines of moderate and moderate-upper apparel, cosmetics, housewares, shoes and other department store type goods. Most interview participants reported that they appreciated the convenience of having the Macy’s location, and its connection into the tunnel system. Store management reported that the tunnel connection was an important entry for the store, but that its Main Street location was also vital for its operations. Macy’s serves as one of downtown’s most important retail anchors and its contributions towards the downtown’s sustainability cannot be over-emphasized.

Figure 20: Macy’s department store is the downtown’s largest retailer and provides goods and services for many of the downtown employees, residents and visitors.

Downtown Houston Retail Analysis 20 Gibbs Planning Group, Inc. January 10, 2010

GPG recommends that the HDMD continue to work closely with Macy’s management to ensure that the store continues to provide its important role in the downtown’s economy. Additional Main Street parking, larger signage, expanded street lighting and in-fill street level retailers are also recommended for the areas around Macy’s.

3.8 Houston Pavilions Houston Pavilions is a three block retail/office project developed in downtown. The project, which opened in October 2008, consists of 280,000 square feet of retail space and an office component. Houston Pavilions is surrounded by Dallas, Polk, Caroline, and Main Streets, with the METRORail stop located one block north on Main Street. Houston Pavilions has easy contiguous access to the following public parking garages: Main Garage, 1111 Main St Garage, 1301 Fannin Garage, and First City Town Garage. The HDMD granted the Pavilions $1 million, and the City contributed $14 million for various construction and streetscape improvements.

Figure 21: Houston Pavilions contains 280,000 SF of retail, which currently is anchored by XXI Forever, House of Blues, Books A-Million and Lucky Strike Lanes. Although the Pavilions has been open for more than a year, and the office space component is 100 percent leased by NRG Energy, Inc., the retail space has a significant level of vacancy. The retail leasing of this project has likely been a victim of timing, opening during the national financial crisis of fall 2008, a time when retail sales plummeted nationally and most retailers suspended expansion plans across the nation. The current tenant mix is focused on entertainment and restaurants, featuring the House of Blues and Lucky Strike Lanes. The restaurant offerings are upscale, including McCormick & Schmick's Seafood, III Forks Steakhouse, and Guadalajara del Centro. Currently, there are only three retailers in the project, Books-a-Million and XXI Forever on the western end of the project near the METRORail stop, and BCBG in the center of the project. GPG finds that the Pavilions has become one of Houston’s leading anchors and is well positioned to capture much of the region’s potential entertainment and soft-goods demand.

Downtown Houston Retail Analysis 21 Gibbs Planning Group, Inc. January 10, 2010

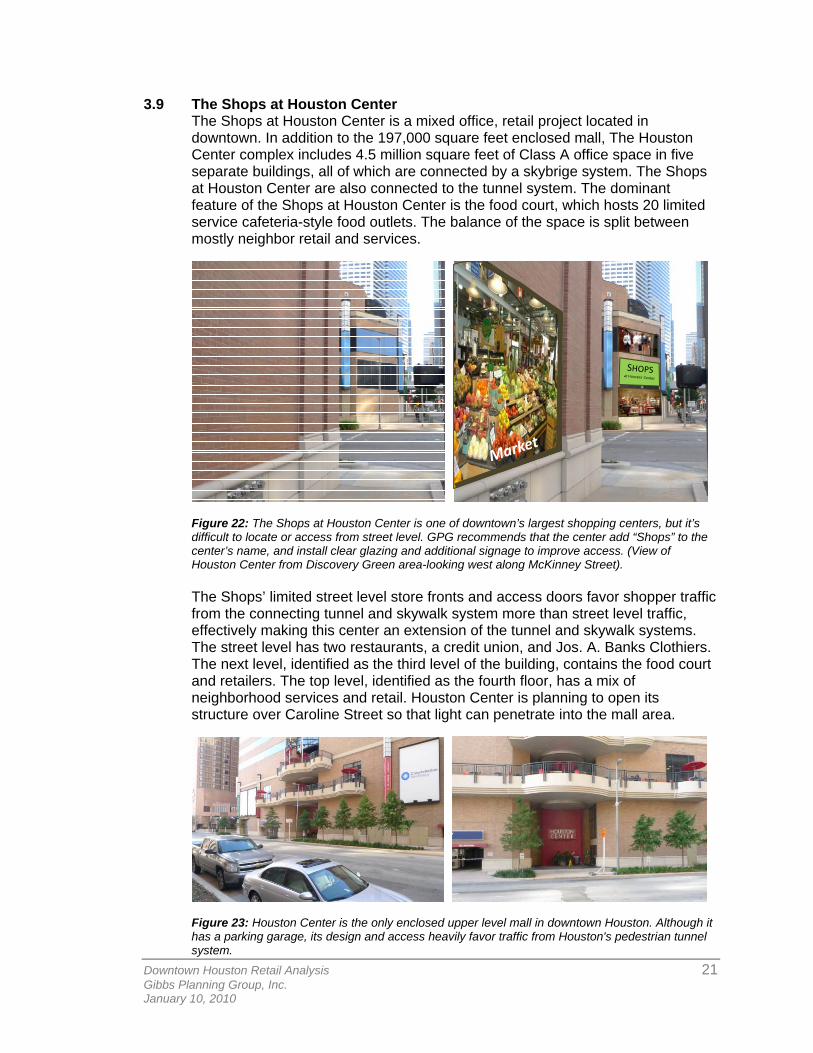

3.9 The Shops at Houston Center The Shops at Houston Center is a mixed office, retail project located in downtown. In addition to the 197,000 square feet enclosed mall, The Houston Center complex includes 4.5 million square feet of Class A office space in five separate buildings, all of which are connected by a skybrige system. The Shops at Houston Center are also connected to the tunnel system. The dominant feature of the Shops at Houston Center is the food court, which hosts 20 limited service cafeteria-style food outlets. The balance of the space is split between mostly neighbor retail and services.

Figure 22: The Shops at Houston Center is one of downtown’s largest shopping centers, but it’s difficult to locate or access from street level. GPG recommends that the center add “Shops” to the center’s name, and install clear glazing and additional signage to improve access. (View of Houston Center from Discovery Green area-looking west along McKinney Street). The Shops’ limited street level store fronts and access doors favor shopper traffic from the connecting tunnel and skywalk system more than street level traffic, effectively making this center an extension of the tunnel and skywalk systems. The street level has two restaurants, a credit union, and Jos. A. Banks Clothiers. The next level, identified as the third level of the building, contains the food court and retailers. The top level, identified as the fourth floor, has a mix of neighborhood services and retail. Houston Center is planning to open its structure over Caroline Street so that light can penetrate into the mall area.

Figure 23: Houston Center is the only enclosed upper level mall in downtown Houston. Although it has a parking garage, its design and access heavily favor traffic from Houston's pedestrian tunnel system.

Downtown Houston Retail Analysis 22 Gibbs Planning Group, Inc. January 10, 2010

3.10 Nearby Shopping Centers As part of this study, GPG visited most major shopping concentrations in and around the periphery of downtown Houston. There are six major shopping centers inside of the outer beltway that pose the most direct competition to downtown Houston's commerce. In addition, nine other major retail centers attract the tourists’ and residents’ shopping time and retail spending.

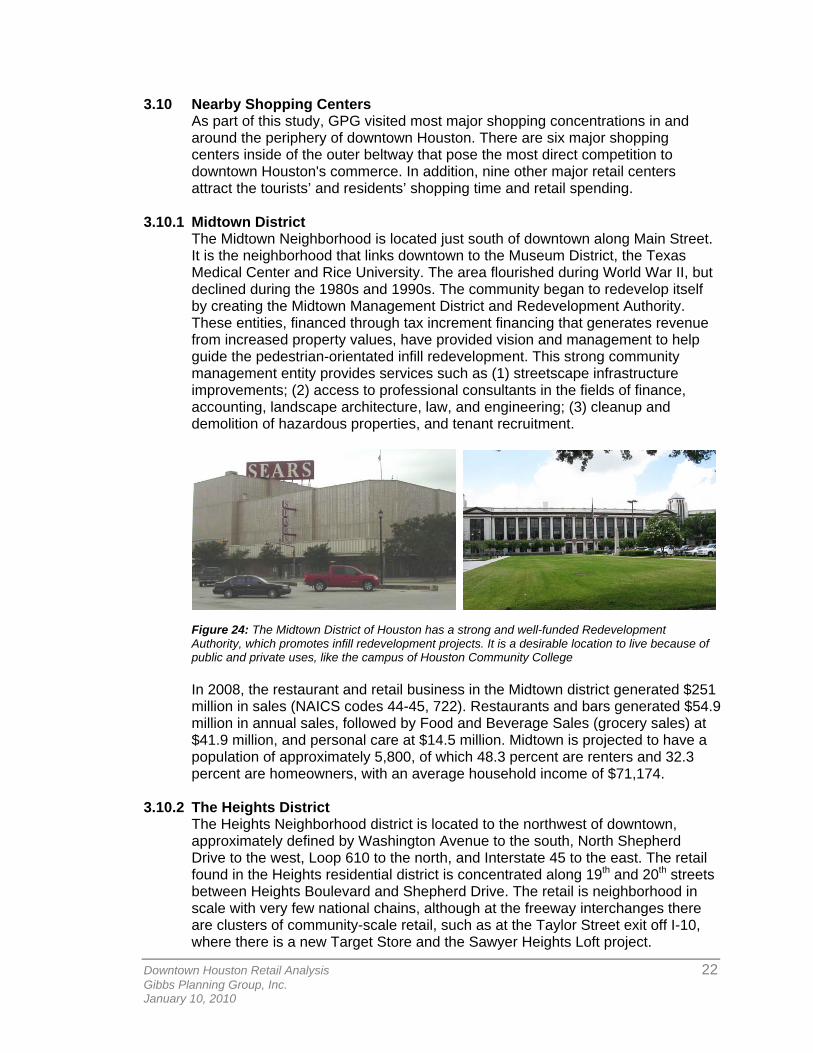

3.10.1 Midtown District The Midtown Neighborhood is located just south of downtown along Main Street. It is the neighborhood that links downtown to the Museum District, the Texas Medical Center and Rice University. The area flourished during World War II, but declined during the 1980s and 1990s. The community began to redevelop itself by creating the Midtown Management District and Redevelopment Authority. These entities, financed through tax increment financing that generates revenue from increased property values, have provided vision and management to help guide the pedestrian-orientated infill redevelopment. This strong community management entity provides services such as (1) streetscape infrastructure improvements; (2) access to professional consultants in the fields of finance, accounting, landscape architecture, law, and engineering; (3) cleanup and demolition of hazardous properties, and tenant recruitment.

Figure 24: The Midtown District of Houston has a strong and well-funded Redevelopment Authority, which promotes infill redevelopment projects. It is a desirable location to live because of public and private uses, like the campus of Houston Community College In 2008, the restaurant and retail business in the Midtown district generated $251 million in sales (NAICS codes 44-45, 722). Restaurants and bars generated $54.9 million in annual sales, followed by Food and Beverage Sales (grocery sales) at $41.9 million, and personal care at $14.5 million. Midtown is projected to have a population of approximately 5,800, of which 48.3 percent are renters and 32.3 percent are homeowners, with an average household income of $71,174.

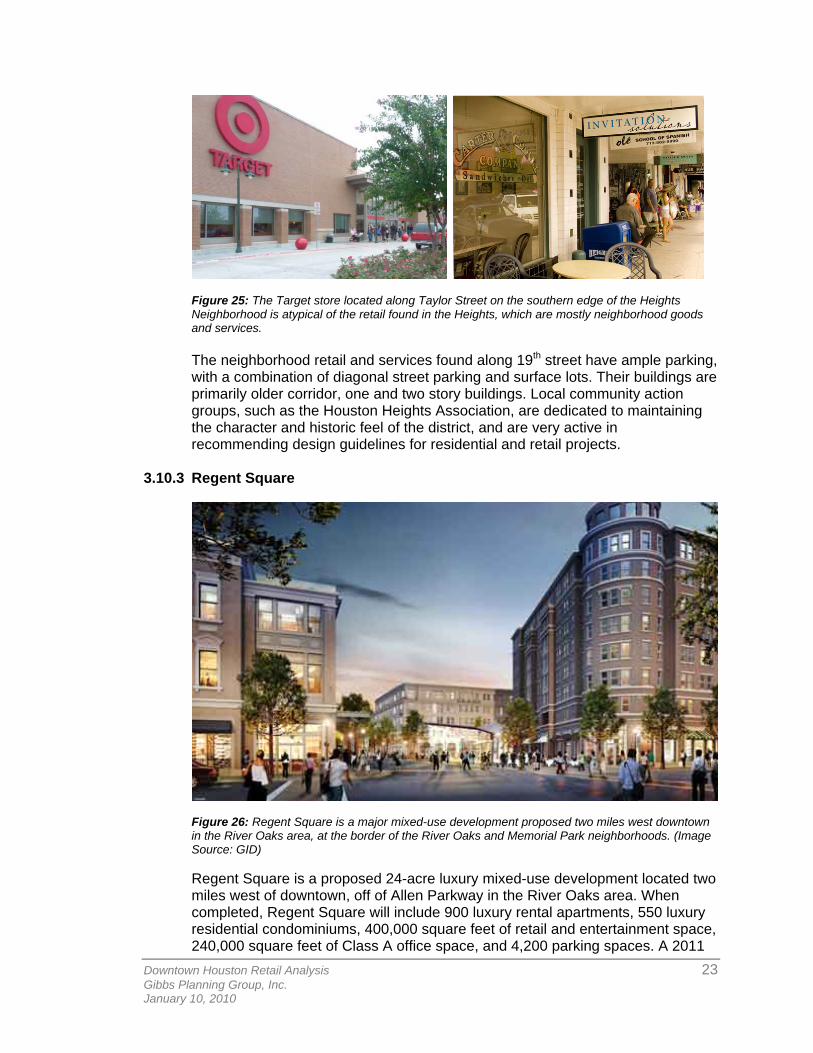

3.10.2 The Heights District The Heights Neighborhood district is located to the northwest of downtown, approximately defined by Washington Avenue to the south, North Shepherd Drive to the west, Loop 610 to the north, and Interstate 45 to the east. The retail found in the Heights residential district is concentrated along 19th and 20th streets between Heights Boulevard and Shepherd Drive. The retail is neighborhood in scale with very few national chains, although at the freeway interchanges there are clusters of community-scale retail, such as at the Taylor Street exit off I-10, where there is a new Target Store and the Sawyer Heights Loft project.

Downtown Houston Retail Analysis 23 Gibbs Planning Group, Inc. January 10, 2010

Figure 25: The Target store located along Taylor Street on the southern edge of the Heights Neighborhood is atypical of the retail found in the Heights, which are mostly neighborhood goods and services. The neighborhood retail and services found along 19th street have ample parking, with a combination of diagonal street parking and surface lots. Their buildings are primarily older corridor, one and two story buildings. Local community action groups, such as the Houston Heights Association, are dedicated to maintaining the character and historic feel of the district, and are very active in recommending design guidelines for residential and retail projects.

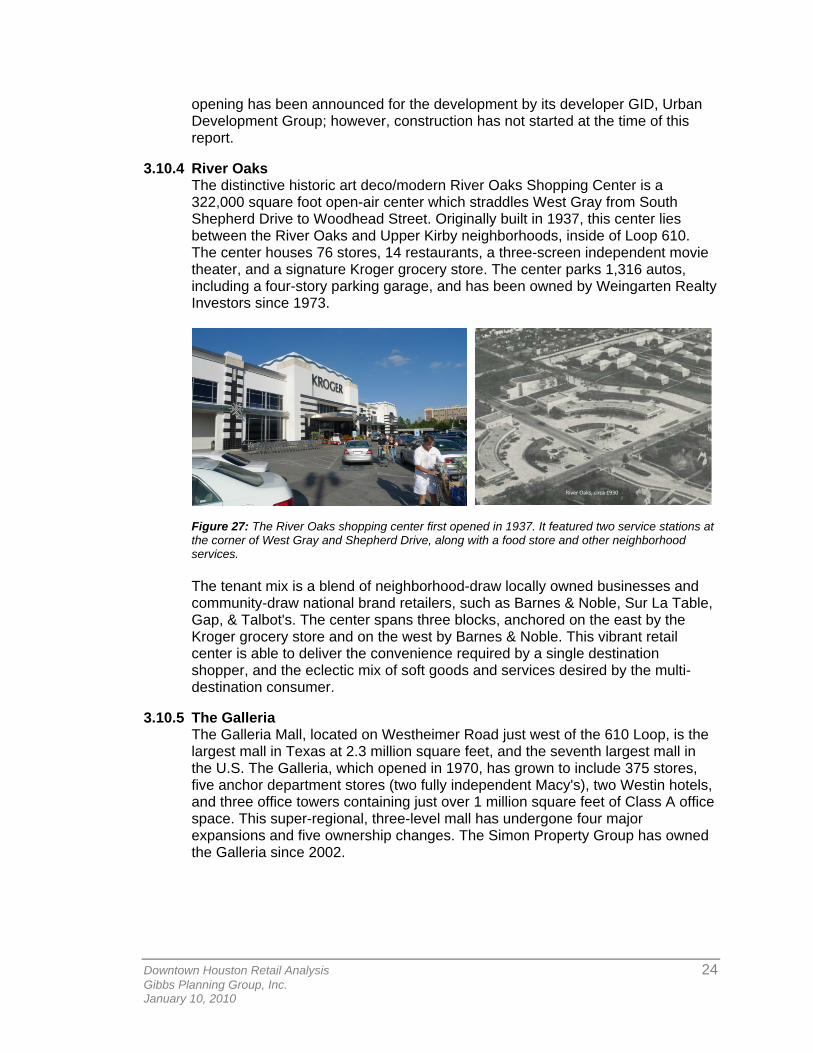

3.10.3 Regent Square

Figure 26: Regent Square is a major mixed-use development proposed two miles west downtown in the River Oaks area, at the border of the River Oaks and Memorial Park neighborhoods. (Image Source: GID) Regent Square is a proposed 24-acre luxury mixed-use development located two miles west of downtown, off of Allen Parkway in the River Oaks area. When completed, Regent Square will include 900 luxury rental apartments, 550 luxury residential condominiums, 400,000 square feet of retail and entertainment space, 240,000 square feet of Class A office space, and 4,200 parking spaces. A 2011

Downtown Houston Retail Analysis 24 Gibbs Planning Group, Inc. January 10, 2010

opening has been announced for the development by its developer GID, Urban Development Group; however, construction has not started at the time of this report.

3.10.4 River Oaks The distinctive historic art deco/modern River Oaks Shopping Center is a 322,000 square foot open-air center which straddles West Gray from South Shepherd Drive to Woodhead Street. Originally built in 1937, this center lies between the River Oaks and Upper Kirby neighborhoods, inside of Loop 610. The center houses 76 stores, 14 restaurants, a three-screen independent movie theater, and a signature Kroger grocery store. The center parks 1,316 autos, including a four-story parking garage, and has been owned by Weingarten Realty Investors since 1973.

River Oaks, circa 1930

Figure 27: The River Oaks shopping center first opened in 1937. It featured two service stations at the corner of West Gray and Shepherd Drive, along with a food store and other neighborhood services.

The tenant mix is a blend of neighborhood-draw locally owned businesses and community-draw national brand retailers, such as Barnes & Noble, Sur La Table, Gap, & Talbot's. The center spans three blocks, anchored on the east by the Kroger grocery store and on the west by Barnes & Noble. This vibrant retail center is able to deliver the convenience required by a single destination shopper, and the eclectic mix of soft goods and services desired by the multi-destination consumer.

3.10.5 The Galleria

The Galleria Mall, located on Westheimer Road just west of the 610 Loop, is the largest mall in Texas at 2.3 million square feet, and the seventh largest mall in the U.S. The Galleria, which opened in 1970, has grown to include 375 stores, five anchor department stores (two fully independent Macy's), two Westin hotels, and three office towers containing just over 1 million square feet of Class A office space. This super-regional, three-level mall has undergone four major expansions and five ownership changes. The Simon Property Group has owned the Galleria since 2002.

Downtown Houston Retail Analysis 25 Gibbs Planning Group, Inc. January 10, 2010

Figure 28: The Galleria is one of the leading luxury shopping malls in the United States

Simon Property Group reports that the mall has over 26 million annual visitors, and is considered to be the most visited attraction in Houston. This massive retail center is an institution in the Houston market, and because of its 375 upscale tenant mix, it dominates the multi-destination consumer shopping trip market, while being a little too large and too much traffic to be the destination of choice for the single purchase consumer.

3.10.6 Highland Village This small upscale retail center is ideally located on Westheimer Road, just east of Loop 610. Highland Village is sandwiched between some of Houston's most prestigious neighborhoods, namely River Oaks, Uptown, and the Upper Kirby District. The tenant mix includes Crate & Barrel, Williams-Sonoma, Restoration Hardware, Jos. A. Banks Clothier, and Anthropologie. It has good regional access via the Loop 610 to the west, and is only five miles west of downtown.

Figure 29: Highland Village is a neighborhood-sized center with community-draw upscale retailers. This infill, super-neighborhood-sized center straddles Westheimer Road and is a very popular retail destination, so popular that it requires traffic police to direct traffic. Even with traffic police calming traffic, the street has too many lanes for consumers to effectively shop both sides of Westheimer without using their cars. The onsite surface lot parking is very tight, although there is a four-story garage.

Downtown Houston Retail Analysis 26 Gibbs Planning Group, Inc. January 10, 2010

3.10.7 Other Shopping Centers

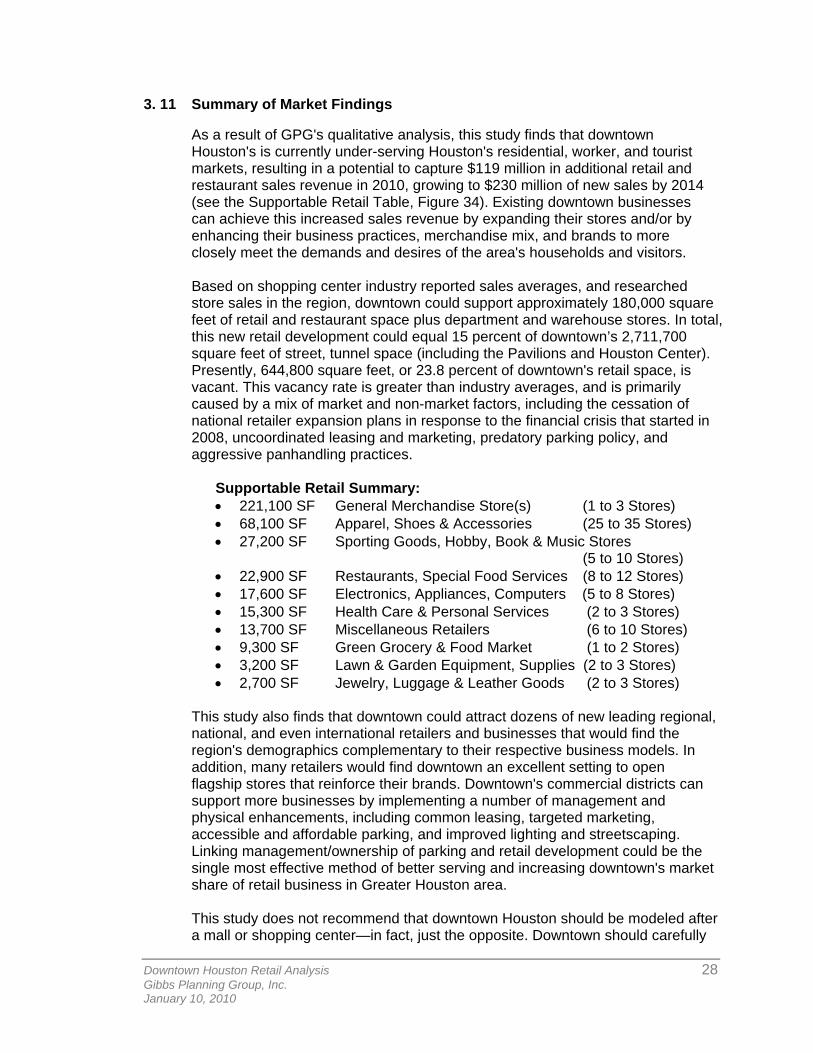

Figure 30: Contrasting images of malls in the Houston Market. On the left, the Memorial City Mall is in the midst of redevelopment, including a skywalk connection to offsite commercial properties. On the right, the photo of the Pasadena Town Center highlights the fact that not all malls are busy with holiday shopping traffic. The Houston MSA has 15 major regional malls, catering to all ends of the spectrum, from the Galleria to the Pasadena Town Center. Other regional Malls in the area include Memorial City Mall, Meyerland Plaza, Northline Commons, Willowbrook Mall, Greenspoint Mall, The Woodlands, First Colony Mall, Baybrook Mall, Almeda Mall, San Jacinto Mall, and the Deerbrook Mall.

Figure 31: The Woodlands Market Street area offers numerous leading retailers and restaurants grouped around a town square. In addition to the 15 regional malls in and around the greater Houston MSA, there are many very competitive community shopping districts and Lifestyle Centers, including Highland Village, the Heights District, the Midtown District,

Downtown Houston Retail Analysis 27 Gibbs Planning Group, Inc. January 10, 2010

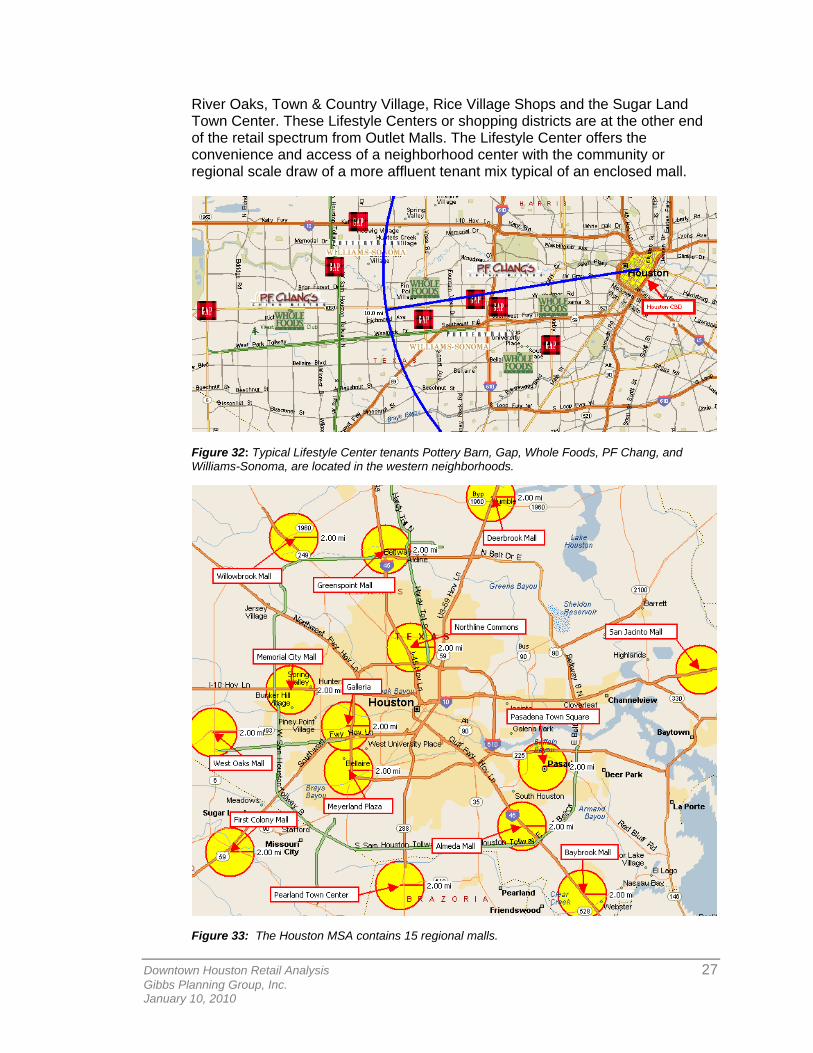

River Oaks, Town & Country Village, Rice Village Shops and the Sugar Land Town Center. These Lifestyle Centers or shopping districts are at the other end of the retail spectrum from Outlet Malls. The Lifestyle Center offers the convenience and access of a neighborhood center with the community or regional scale draw of a more affluent tenant mix typical of an enclosed mall.

Figure 32: Typical Lifestyle Center tenants Pottery Barn, Gap, Whole Foods, PF Chang, and Williams-Sonoma, are located in the western neighborhoods.

Figure 33: The Houston MSA contains 15 regional malls.

Downtown Houston Retail Analysis 28 Gibbs Planning Group, Inc. January 10, 2010

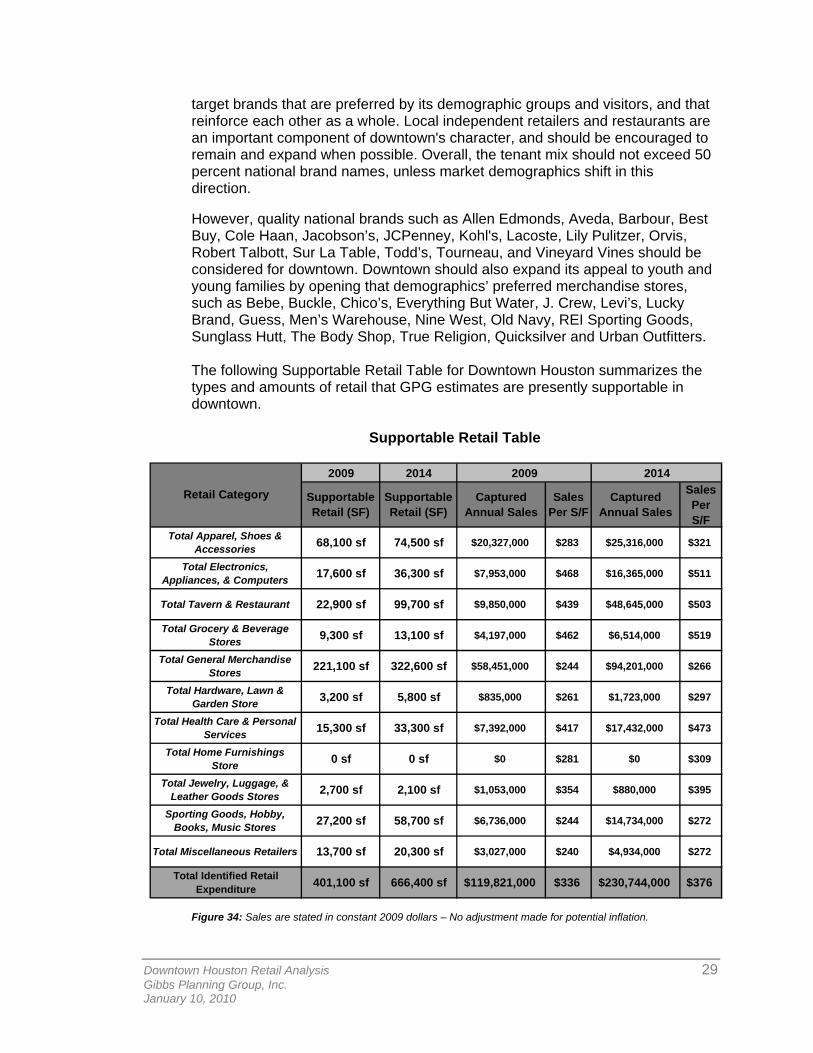

3. 11 Summary of Market Findings

As a result of GPG's qualitative analysis, this study finds that downtown Houston's is currently under-serving Houston's residential, worker, and tourist markets, resulting in a potential to capture $119 million in additional retail and restaurant sales revenue in 2010, growing to $230 million of new sales by 2014 (see the Supportable Retail Table, Figure 34). Existing downtown businesses can achieve this increased sales revenue by expanding their stores and/or by enhancing their business practices, merchandise mix, and brands to more closely meet the demands and desires of the area's households and visitors. Based on shopping center industry reported sales averages, and researched store sales in the region, downtown could support approximately 180,000 square feet of retail and restaurant space plus department and warehouse stores. In total, this new retail development could equal 15 percent of downtown’s 2,711,700 square feet of street, tunnel space (including the Pavilions and Houston Center). Presently, 644,800 square feet, or 23.8 percent of downtown's retail space, is vacant. This vacancy rate is greater than industry averages, and is primarily caused by a mix of market and non-market factors, including the cessation of national retailer expansion plans in response to the financial crisis that started in 2008, uncoordinated leasing and marketing, predatory parking policy, and aggressive panhandling practices.

Supportable Retail Summary: • 221,100 SF General Merchandise Store(s) (1 to 3 Stores) • 68,100 SF Apparel, Shoes & Accessories (25 to 35 Stores) • 27,200 SF Sporting Goods, Hobby, Book & Music Stores

(5 to 10 Stores) • 22,900 SF Restaurants, Special Food Services (8 to 12 Stores) • 17,600 SF Electronics, Appliances, Computers (5 to 8 Stores) • 15,300 SF Health Care & Personal Services (2 to 3 Stores) • 13,700 SF Miscellaneous Retailers (6 to 10 Stores) • 9,300 SF Green Grocery & Food Market (1 to 2 Stores) • 3,200 SF Lawn & Garden Equipment, Supplies (2 to 3 Stores) • 2,700 SF Jewelry, Luggage & Leather Goods (2 to 3 Stores)

This study also finds that downtown could attract dozens of new leading regional, national, and even international retailers and businesses that would find the region's demographics complementary to their respective business models. In addition, many retailers would find downtown an excellent setting to open flagship stores that reinforce their brands. Downtown's commercial districts can support more businesses by implementing a number of management and physical enhancements, including common leasing, targeted marketing, accessible and affordable parking, and improved lighting and streetscaping. Linking management/ownership of parking and retail development could be the single most effective method of better serving and increasing downtown's market share of retail business in Greater Houston area. This study does not recommend that downtown Houston should be modeled after a mall or shopping center—in fact, just the opposite. Downtown should carefully

Downtown Houston Retail Analysis 29 Gibbs Planning Group, Inc. January 10, 2010

target brands that are preferred by its demographic groups and visitors, and that reinforce each other as a whole. Local independent retailers and restaurants are an important component of downtown's character, and should be encouraged to remain and expand when possible. Overall, the tenant mix should not exceed 50 percent national brand names, unless market demographics shift in this direction.

However, quality national brands such as Allen Edmonds, Aveda, Barbour, Best Buy, Cole Haan, Jacobson’s, JCPenney, Kohl's, Lacoste, Lily Pulitzer, Orvis, Robert Talbott, Sur La Table, Todd’s, Tourneau, and Vineyard Vines should be considered for downtown. Downtown should also expand its appeal to youth and young families by opening that demographics’ preferred merchandise stores, such as Bebe, Buckle, Chico’s, Everything But Water, J. Crew, Levi’s, Lucky Brand, Guess, Men’s Warehouse, Nine West, Old Navy, REI Sporting Goods, Sunglass Hutt, The Body Shop, True Religion, Quicksilver and Urban Outfitters. The following Supportable Retail Table for Downtown Houston summarizes the types and amounts of retail that GPG estimates are presently supportable in downtown.

Supportable Retail Table

2009 2014

Supportable Retail (SF)

Supportable Retail (SF)

Captured Annual Sales

Sales Per S/F

Captured Annual Sales

Sales Per S/F

Total Apparel, Shoes & Accessories 68,100 sf 74,500 sf $20,327,000 $283 $25,316,000 $321

Total Electronics, Appliances, & Computers 17,600 sf 36,300 sf $7,953,000 $468 $16,365,000 $511

Total Tavern & Restaurant 22,900 sf 99,700 sf $9,850,000 $439 $48,645,000 $503

Total Grocery & Beverage Stores 9,300 sf 13,100 sf $4,197,000 $462 $6,514,000 $519

Total General Merchandise Stores 221,100 sf 322,600 sf $58,451,000 $244 $94,201,000 $266

Total Hardware, Lawn & Garden Store 3,200 sf 5,800 sf $835,000 $261 $1,723,000 $297

Total Health Care & Personal Services 15,300 sf 33,300 sf $7,392,000 $417 $17,432,000 $473

Total Home Furnishings Store 0 sf 0 sf $0 $281 $0 $309

Total Jewelry, Luggage, & Leather Goods Stores 2,700 sf 2,100 sf $1,053,000 $354 $880,000 $395

Sporting Goods, Hobby, Books, Music Stores 27,200 sf 58,700 sf $6,736,000 $244 $14,734,000 $272

Total Miscellaneous Retailers 13,700 sf 20,300 sf $3,027,000 $240 $4,934,000 $272

Total Identified Retail Expenditure 401,100 sf 666,400 sf $119,821,000 $336 $230,744,000 $376

Retail Category

2009 2014

Figure 34: Sales are stated in constant 2009 dollars – No adjustment made for potential inflation.

Downtown Houston Retail Analysis 30 Gibbs Planning Group, Inc. January 10, 2010

3.12 Rationale for the Market Findings The rationale for the findings in the market study is the following: Dense Population Base: The tertiary trade area has an estimated 2009

population of 2,708,300, which is projected to grow 1.22 percent annually to 2,877,150 people by 2014. Persons per household are reported as 2.81, marginally higher than that found in the State of Texas as a whole.

Reputation: Houston, "The energy capital of the world" is considered a

strong employment base today and into the 21st century.

Tourism: Strong tourism base of 31.4 million annual visitors.

Figure 35: The downtown historic Macy’s store (above left) was imitated by the GAP store in the Woodlands Town Center (above right).

4.0 COMMUNITY COMMENTS As a part of this study, GPG conducted individual and focus group sessions with dozens of Houston’s retailers, restaurateurs, bar owners, property owners, building managers, developers, municipal representatives, and HDMD board members. These interviews were conducted in group settings at the Houston Downtown Management District office and in individual offices, restaurants, and retail stores.

4.1 Downtown Management and Retail Development Group Interviews Municipal representatives and citizens actively promoting retail and economic development in downtown had varying but consistent views on the strengths the area has and the challenges it faces. At times, they disagreed about the depth of the problem, but were united in identifying downtown’s fundamental challenges: streetscape and storefront continuity, homelessness and panhandling, shopping center competition, the tunnel system, insufficient lighting, parking and the general economic situation. These issues resurfaced in all subsequent group meetings.

Downtown Houston Retail Analysis 31 Gibbs Planning Group, Inc. January 10, 2010

As explained to the planning team, downtown Houston’s most recent “golden era” was between 1998 and 2002, towards the end of which a series of detrimental events impacted the area: the Tropical Storm Allison flood in June 2001, 9/11, the Enron demise in October 2001, and the four-year construction of the METRORail line. Both groups attributed the downtown’s initial decline to these events. In their desire to re-create a vibrant downtown, HDMD representatives and many interview participants considered the lack of storefront continuity as detrimental to this goal. They viewed pedestrian-oriented streets and lighting as necessary to draw convention tourists, baseball and basketball fans, and theater goers into downtown shops and restaurants, as well as to encourage pedestrian traffic among downtown’s retail areas. In contrast, retail advocates seemed to view the lack of easily accessible and affordable parking as one of the district’s foremost problems, an opinion shared by all subsequent groups. There is an ample supply of downtown parking stalls, but many close after 9:00 pm and/or are very expensive in the evenings. Others noted that parking is free in suburban areas, which gives it a real competitive advantage over downtown. Also, parking is a challenge to people unfamiliar with downtown but routine for daytime workers. Some complained that there was not enough valet parking while others maintained that Houstonians “don’t valet.” Both groups lamented the fact that although Discovery Green has tremendous success drawing people from afar into downtown, often for the first time, very few venture out to other areas to dine or shop. One participant commented that her neighbors enjoy events at Discovery Green but would rather return to the suburbs to shop at the Galleria or Highland Village. Similarly, theatergoers dine in the suburbs before or after the show rather than find a restaurant downtown. Nearly all participants expressed the view that aggressive panhandling is detrimental to retail, deterring both residents and visitors from shopping or dining. Some maintained that downtown would never be a successful retail area until the homeless situation is adequately dealt with. Others added that aggressive panhandling would keep people from choosing to live downtown. However, a municipal representative claimed that rarely are these people truly dangerous: the chronically homeless choose to be homeless, others are mentally ill and need medical help, and the few seeking drugs are the ones to worry about. This person argued that the problem could be solved by enforceable loitering laws. The Historic District is seen as a real asset to downtown. District representatives noted that in the mid-1990s it became the first “happening” place and the only identifiable district in downtown. Now, however, it has no identifiable brand: a ten-year development project hurt its retail and the late-night clubs have begun to transform it into an entertainment area. The HDMD would like to see it revert back to an authentic destination that includes residential, whereas one of the retail advocates promoted the idea of the Historic District as a culinary center. Both groups acknowledged that retail it struggling downtown, but noted that although Houston Pavilions has been slow to develop, its entertainment venues and shops have been a plus for Macy’s and the Shops at Houston Center. Some

Downtown Houston Retail Analysis 32 Gibbs Planning Group, Inc. January 10, 2010

lamented that Macy’s no longer caters to higher income groups and seems to have settled on servicing lower incomes. Both groups acknowledge the need for more grocers to serve downtown residents.

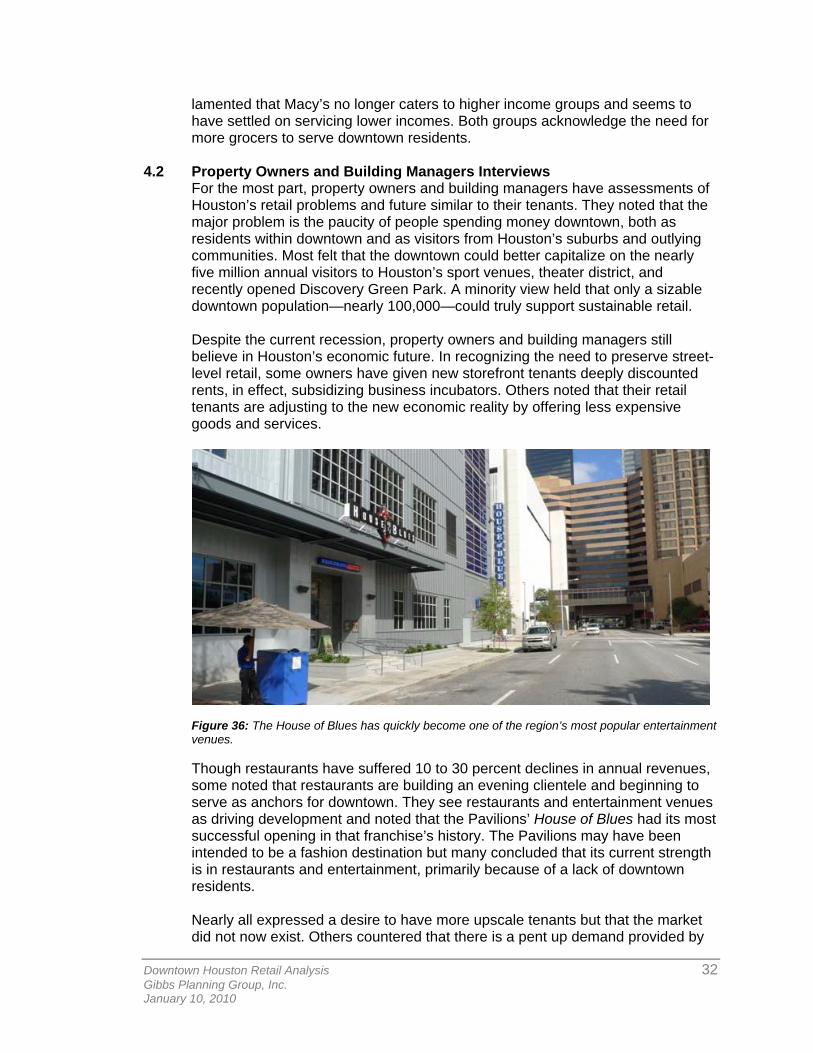

4.2 Property Owners and Building Managers Interviews For the most part, property owners and building managers have assessments of Houston’s retail problems and future similar to their tenants. They noted that the major problem is the paucity of people spending money downtown, both as residents within downtown and as visitors from Houston’s suburbs and outlying communities. Most felt that the downtown could better capitalize on the nearly five million annual visitors to Houston’s sport venues, theater district, and recently opened Discovery Green Park. A minority view held that only a sizable downtown population—nearly 100,000—could truly support sustainable retail. Despite the current recession, property owners and building managers still believe in Houston’s economic future. In recognizing the need to preserve street-level retail, some owners have given new storefront tenants deeply discounted rents, in effect, subsidizing business incubators. Others noted that their retail tenants are adjusting to the new economic reality by offering less expensive goods and services.

Figure 36: The House of Blues has quickly become one of the region’s most popular entertainment venues. Though restaurants have suffered 10 to 30 percent declines in annual revenues, some noted that restaurants are building an evening clientele and beginning to serve as anchors for downtown. They see restaurants and entertainment venues as driving development and noted that the Pavilions’ House of Blues had its most successful opening in that franchise’s history. The Pavilions may have been intended to be a fashion destination but many concluded that its current strength is in restaurants and entertainment, primarily because of a lack of downtown residents. Nearly all expressed a desire to have more upscale tenants but that the market did not now exist. Others countered that there is a pent up demand provided by

Downtown Houston Retail Analysis 33 Gibbs Planning Group, Inc. January 10, 2010

salaried employees, such as lawyers, whose needs are not being met. Still others noted that even with this demand, Brooks Brothers abandoned the Houston Center. Nearly all owners acknowledged that more street connectivity is needed downtown. Some opined that there is no “green connectivity” to shade pedestrians from the summer sun. Many owners and developers agreed that the best intersection on Main Street is at Dallas Street, which Macy’s and the Pavilions share. The secondary commercial intersections are where Prairie and Dallas Streets intersect Main Street. This group also felt that Main Street could “come back” as Houston’s primary retail street. A few owners felt that the Historic District is a “tough sell” since few restaurants are willing to set up in a transition area. Yet, another added, the redesign of the Market Square Park is a significant step toward reviving the area. The area could appeal to empty nesters who want to live in a doorman building, such as the one two blocks from the square. The district could also target nearby courthouse workers, both high-income lawyers and middle-income staff.

Figure 37: Aerial view of Houston’s Historic Market Square (presently being redeveloped).

4.3 Restaurant and Bar Owners and Soft Goods Retailers Interviews When asked to rate the worst problems facing their business on a scale from 1 to 10, restaurant and bar owners were unanimous in giving aggressive panhandling a 10 and parking a 10. Aggressive panhandling makes customers feel uncomfortable and unsafe, creating the impression that the entire downtown is dangerous. Restaurant owners observed that parking in garages is too expensive after 6:00 pm; rather, they argued it should be free in the evenings and on Saturdays. Others complained that the police were too aggressive in enforcing parking

Downtown Houston Retail Analysis 34 Gibbs Planning Group, Inc. January 10, 2010

infractions, resulting in a negative experience for suburban patrons who might, as a result, not wish to return. A few restaurant and bar owners proclaimed that convention tourists were “gold” to the city. Without them, their establishments might not be in business, whereas baseball and basketball fans quickly leave the city after games. When asked what improvements were needed in downtown, they responded that there should be a retail and restaurant corridor on Dallas Street from the Convention Center to Main Street. Restaurant owners want the HDMD to encourage less development in the tunnels and more on the street. For them, closing the tunnels might “double or triple” their sales. In contrast, larger retailers acknowledged that the “number one door” is the interior stairs from the tunnels. Retailers, especially those on or near Main Street, recognized that the METRORail helps their businesses. Loyal customers working in or residing near the Medical Center can readily take the METRORail to shop downtown. Some restaurant owners said that the District should not try to bring in more retailers, but should try to encourage more people to live downtown. Others countered that retail helps their businesses. Similarly, some of the retailers do not want to see more retail downtown, especially if it directly competes. But others acknowledged that cross-shopping could be mutually beneficial.

5.0 CHALLENGES & OPPORTUNITIES

Figure 38: Downtown Houston is approximately one mile square and over 650 acres, and includes 250 blocks.

Downtown Houston Retail Analysis 35 Gibbs Planning Group, Inc. January 10, 2010

5.1 Overview Houston, the fourth largest city in the US, is located 45 miles from the Gulf of Mexico and approximately 225 miles southeast of Dallas. It was incorporated in 1837, and named after the President of the Republic of Texas, Sam Houston. Houston is the energy capital of the world, the U.S. headquarters for most major energy companies, including ConocoPhillips, Exxon-Mobile, Shell Oil, Marathon, BP, CITGO, and the command center for NASA. The Gross Area Product of Houston is greater than the Gross Domestic Product of all but 21 nations in the world.

5.2 Business Opening Challenges Today, downtown Houston’s retail market has a number of challenges: parking, lighting, signage, panhandling, and street-level building design. Nationwide, the retail industry has endured and continues to face weak sales, which has resulted in store closures and the suspension of new retail developments. Nonetheless, the consumer expenditure potential that downtown Houston could statistically capture could support an additional 401,100 square feet of retail space. The primary issues facing downtown Houston’s commerce are the following:

1. Parking is not conveniently located or reasonably priced to support substantial infill growth of retail space.

2. Panhandlers in downtown are aggressive and are perceived to be a security issue to consumers—both residents and tourists.

3. Limited business recruitment resources. 4. Poor street, sidewalk and building lighting. 5. Harsh street level building conditions: limited transparency (store

windows), pedestrian access and retail frontages. 6. Ineffective street level and anchor commercial signage. 7. Minimal coordinated marketing and advertizing campaign for downtown

retailers and the HDMD’s services. Unfocused downtown-wide retail leasing strategy.

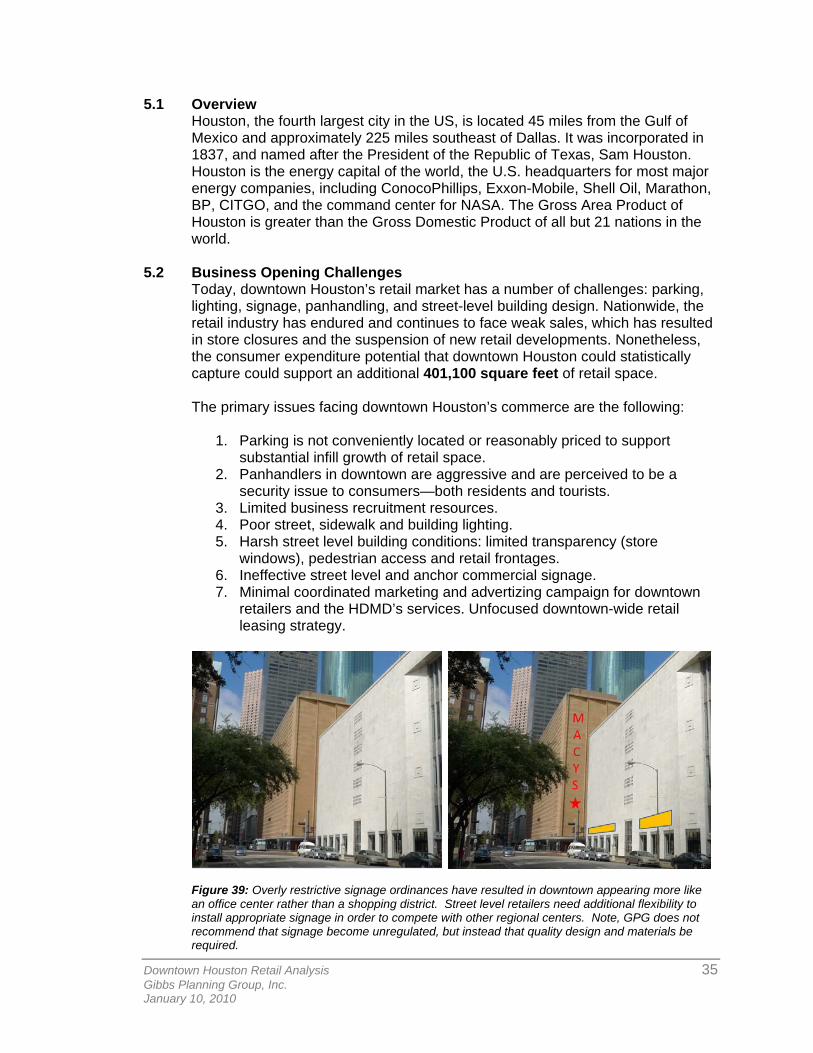

Figure 39: Overly restrictive signage ordinances have resulted in downtown appearing more like an office center rather than a shopping district. Street level retailers need additional flexibility to install appropriate signage in order to compete with other regional centers. Note, GPG does not recommend that signage become unregulated, but instead that quality design and materials be required.

Downtown Houston Retail Analysis 36 Gibbs Planning Group, Inc. January 10, 2010

Other local challenges to opening a business in downtown are the following:

1. The worker/consumer population quickly leaves the downtown area at the end of the business day and rarely takes the time for lengthy shopping trips after work.

2. The direct, local competition for daytime consumer business from the retailers in the tunnel system, who have many competitive advantages—lower operating costs by being open only during peak daytime business hours; a location in one of the many retail clusters within walking distance of major companies; and easy, direct access to the daytime employees in climate-controlled, pedestrian-orientated pathways.

3. Strongly established regional and community competition from

surrounding retail centers such as the Galleria, Highland Village, West University, River Oaks, Sugarland Town Center, and Woodlands’ retail components, which are all located closer to where the downtown employees reside and have a broader range of retail to meet their shopping needs.

5.3 Space Limitations

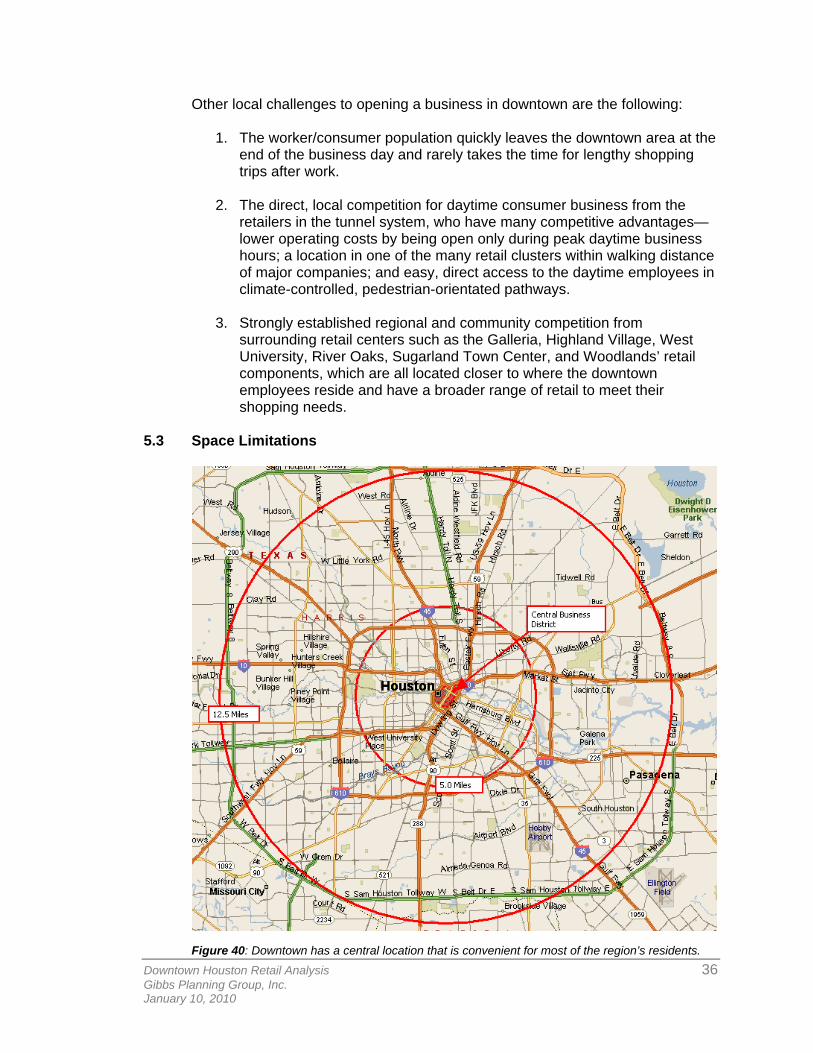

Figure 40: Downtown has a central location that is convenient for most of the region’s residents.

Downtown Houston Retail Analysis 37 Gibbs Planning Group, Inc. January 10, 2010