Embed Size (px)

Citation preview

Household Waste Behaviour in London 2005

March 2006

CONTENTS Executive Summary

1 INTRODUCTION AND CONTEXT ........................................ 1 1.1 Background to the 2005 survey.................................................... 1 1.2 Key findings from Household Waste Behaviour Phases 1 & 2............. 1 1.3 2005 survey design and sample ................................................... 2 1.4 Report structure......................................................................... 4

2 CLAIMED RECYCLING HABITS .......................................... 5 2.1 Access to recycling services ......................................................... 5 2.2 Claimed participation – 2005 versus 2001...................................... 8 2.3 Profile of High, Medium, Low and Non recyclers .............................10 2.4 Materials – change between 2001 and 2005..................................14 2.5 Materials habits of different households ........................................17 2.6 Are recycling services being used effectively? ................................21

3 ATTITUDES, BARRIERS AND INCENTIVES ...................... 26 3.1 Reasons for recycling more.........................................................26 3.2 Change in underlying beliefs, attitudes and motivations ..................27 3.3 Further changes to services to help households recycle more...........33 3.4 Attitudes to compulsion and financial incentives.............................35

4 INFORMATION AND COMMUNICATIONS......................... 37 4.1 How well informed are households about recycling? .......................37 4.2 Perceptions about sources and channels of information...................38 4.3 Where are the information gaps?.................................................41

5 CONCLUSIONS AND RECOMMENDATIONS ...................... 43 5.1 Progress since 2001...................................................................43 5.2 Remaining challenges ................................................................44 5.3 Priorities for increasing household recycling ..................................45 5.4 Policy considerations..................................................................47

6 APPENDIX...................................................................... 49

Acknowledgements Brook Lyndhurst are grateful to the GLA for commissioning this up-date research. We would also like to thank London Waste Action, which has managed and administered the London Recycling Fund (2002-2006), for its financial support to this research. We are also grateful for financial support from the Government Office for London provided from Defra's WIP Local Authority Support Unit through the London Regional Strategic Advisory Forum. We would also like to thank the Resource Recovery Forum for endorsing the commission of this new study, for allowing us to use the RRF 2001 survey data for comparison purposes, and to Kit Strange of the RRF for acting as a peer reviewer of the new work. Thanks are also due to Cigdem Penn and John Leaman at Ipsos MORI who organised and managed the fieldwork and data tabulation. The survey was designed and analysed by Brook Lyndhurst and the report was written by Jayne Cox with help from Alex Ledsom. The analysis and conclusions are entirely the responsibility of Brook Lyndhurst. © GLA 2006 This report has been produced by Brook Lyndhurst Ltd under/as part of a contract placed by the Greater London Authority (GLA). Any views expressed in it are not necessarily those of the GLA. Brook Lyndhurst warrants that all reasonable skill and care has been used in preparing this report. Notwithstanding this warranty, Brook Lyndhurst shall not be under any liability for loss of profit, business, revenues or any special indirect or consequential damage of any nature whatsoever or loss of anticipated saving or for any increased costs sustained by the client or his or her servants or agents arising in any way whether directly or indirectly as a result of reliance on this report or of any error or defect in this report.

Household Waste Behaviour in London 2005

EXECUTIVE SUMMARY I BACKGROUND • In November 2005, the GLA, London Waste Action and the Government Office

for London commissioned Brook Lyndhurst to up-date their earlier work for the Resource Recovery Forum (RRF) on Household Waste Behaviour in London.

• This report presents the findings of a new survey of 1,005 households in London about their attitudes and behaviour relating to waste and recycling. It complements campaign monitoring surveys conducted by NOP for the Recycle for London campaign.

• The purpose of the survey was to measure how much has changed since the original RRF survey in 2001, against a background in which more than £100 million has been invested in infrastructure and services: by Government (DEFRA and WRAP) via the London Recycling Fund; and by boroughs and other London waste authorities, on their own part, through leverage required as a condition of LRF funding, or through partnerships with the private sector.

• The survey was designed and analysed by Brook Lyndhurst with fieldwork undertaken by Ipsos MORI. Fieldwork was conducted in November-December 2005.

II CLAIMED RECYCLING HABITS Access to recycling services • The earlier research highlighted actual and perceived inconvenience as a key

barrier to recycling participation, and kerbside collection as the “path of least resistance” to engaging households.

• This was not only because collection makes recycling easier but also because it increases visibility and awareness, and helps to convince households that their own efforts are being fairly matched by their local council.

• One of the most obvious and significant changes since 2001 has been the increase in the number of households served by kerbside/doorstep recycling collections – from 48% in the 2001 survey to 74% in 2005.

• Widespread roll-out of collections has helped to narrow some of the inequalities in provision observed in 2001 though significant gaps still remain – poorer households living in flats remain the most disadvantaged in terms of access to doorstep collections.

• Increasing provision of communal facilities for flats has opened up opportunities for these households to recycle, but significant proportions (up to half) of non-kerbside households are still unaware where to recycle locally.

Claimed recycling participation – High, Medium, Low and Non recyclers • It is clear that the recent wave of investment in services and communications

has produced a marked rise in average levels of participation.

• The ratio of High/Medium to Low/Non recyclers rose from 50:50 in the 2001 survey to 70:30 in 2005. Only 8% are now Non-recyclers, down from 22% in 2001.

i

Household Waste Behaviour in London 2005 • Over-claiming is still an issue at all levels, however. Combined analysis across

different questions suggests that around 1 in 5 households are effectively still doing very little or no recycling – many more than the number prepared to declare openly that they are Non-recyclers.

• Claimed participation has increased across all social groups and the ‘catch-up’ has been particularly marked amongst middle income, younger and minority ethnic households. It remains the case, though, that older, wealthier and White households continue to have the highest average participation rates.

• It is now more difficult to target remaining Low and Non recyclers than in 2001 on the basis of socio-demographic characteristics; they are spread right across the social class and age spectrum and are a minority in every group.

• Some socio-demographic groups, though, continue to have significantly higher shares of Low/Non recyclers, including: households in flats, recent home movers, single adults, and minority ethnic, younger and low income households.

• The biggest identifiable concentration of Low/Non recyclers remains amongst non-kerbside households (3 in 5 of this group).

• Kerbside access is not the only reason for low participation, however, with Low recyclers now having the same level of kerbside coverage as Medium recyclers in 2001, and disinterest from remaining Non recyclers signalled by the 60% who are unaware of any recycling facilities in their local area.

Claimed participation - materials

• Londoners’ ‘mental map’ of recycling has been transformed since 2001. While newspapers and glass bottles remain the most consistently recycled items in 2005, a wide range of other materials are now (claimed to be) recycled regularly by 40-50% of households.

• Increases in claimed recycling have been most spectacular for card, cans and plastic bottles - fewer than 30% now say they never recycle these items, down from 70-80% in 2001.

• Performance of the previously defined ‘model’ materials of paper and glass improved on average between 2001 and 2005 but showed little change at the highest level of recycling, or amongst kerbside households. This may provide early warning of a ceiling being reached for these materials, and is an issue that should be monitored.

• Green garden and kitchen waste is currently a lost opportunity. Only 1 in 4 households claim they recycle or compost these materials all/most of the time, and the proportion barely changed between 2001 and 2005.

• Kerbside collection makes a significant difference to levels of recycling. Those with collections are 2 to 2½ times more likely to recycle most ‘everyday’ household items than are non-kerbside households.

Are recycling services being used effectively?

• Now that a majority of households have kerbside recycling collections, potential to raise London’s recycling rate lies as much in raising kerbside effectiveness as in recruiting the last remaining non-participants.

• The first barrier is lack of awareness that kerbside collections exist – which was estimated at around 7% of survey respondents.

ii

Household Waste Behaviour in London 2005 • The second barrier is households who opt out – 14% of households with

kerbside collections admit they do not use them. The real level of under-use is probably higher, with 20% of kerbside households being classified as Non/Low recyclers.

• Usage varies slightly across household types and is markedly lower amongst households living in flats – both low rise and high rise – and amongst recent movers.

• The third – and potentially biggest – barrier is increasing the effectiveness of participating kerbside households. There is still significant potential to capture more material from this source, with 25% of kerbside households not recycling newspapers consistently, 35% glass, and 40-50% all other everyday items.

• The latest survey confirms the general passivity of kerbside households shown in the earlier focus group research, with a majority relying entirely on their collections to recycle, and a sizeable minority saying they are too busy to use bring banks.

• There is also scope to increase the usage of bring facilities by non-kerbside households (supermarkets, on-street, on-estate and HWRCs). At present, only half of non-kerbside households use such facilities regularly.

III ATTITUDES, BARRIERS AND INCENTIVES Reasons for recycling more

• Half of respondents claim to be recycling more than they did 2-3 years ago.

• Of all the reasons for recycling more, introduction of kerbside collections is by some margin the most significant. Increasing the range of materials collected and introducing green waste collections are also significant reasons, together with “increased interest in environmental issues”.

• Overall, service improvement reasons were mentioned more than twice as often as advertising/promotion reasons.

Change in underlying beliefs, attitudes, and motivations

• As in 2001, respondents were asked about the extent to which they agree or disagree with a battery of attitude statements – covering how easy it is to recycle; feelings about services; and individuals’ beliefs about personal responsibility, trust in local councils, and the power of individual action.

• The most notable shift in attitudes since 2001 relates to how easy respondents think it is to recycle; 60% now agree “recycling fits easily into my everyday routine” up from only 38% in 2001.

• Households also feel much less restricted by what their council collects and are less worried about having to find time to make trips to bring banks. All of these shifts reflect the impact of more widespread kerbside collections on overcoming households’ effort-inconvenience barrier.

• More convenient recycling also appears to have triggered an increase in households’ confidence that they can reduce the amount of rubbish they make and that it is fair to be told to recycle.

• Less encouragingly, confidence in knowing what and what not to recycle has not changed since 2001, despite the fact that many more households are now recycling a much wider range of materials.

• Views on knowing what to do have become more polarised since 2001. High recyclers are largely confident about what to do but large proportions of Medium and Low recyclers continue to be unsure.

iii

Household Waste Behaviour in London 2005 • A key remaining barrier for High and Medium recyclers is the range of

materials accepted in their kerbside collections, and their passivity in using other services, which is reflected in significant proportions still saying that the Council doesn’t collect everything they want to recycle.

• The remaining rump of Non recyclers is clearly now much more disinterested in recycling than were Non recyclers in 2001, as measured across a range of attitudes. Disinterest combines with living circumstances which make recycling difficult – a majority of Non recyclers live in flats and only 1 in 4 have kerbside collections.

• Across most attitudes and beliefs, Low recyclers have moved closer to Medium recyclers since 2001, though they remain generally more uncertain and less convinced that recycling is convenient, easy, low hassle and straightforward.

Further service changes to help households recycle more

• Whereas introduction of kerbside collection was the leading reason for households to increase their recycling between 2001 and 2005, extending the range of materials collected is now the most desired option, especially by existing High and Medium recyclers.

• Overall, the top four rated factors that households think would help them to do more all relate to making kerbside collection better and easier. Not surprisingly, introduction of collections is the help most favoured by non-kerbside households.

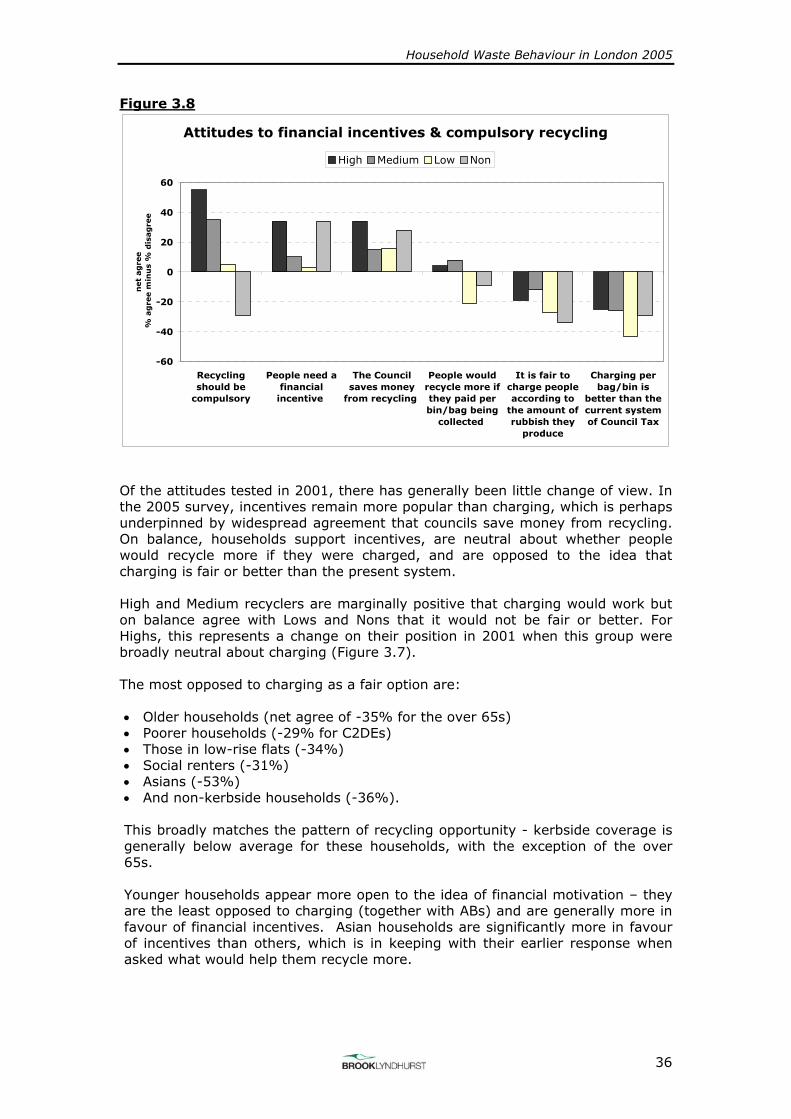

Attitudes to compulsion and financial incentives

• A slim majority of households (53%) agree that recycling should be made compulsory, though 1 in 3 actively disagree with the idea. Support for compulsion is highest amongst those who are already recycling consistently.

• Of the attitudes to various financial measures tested in 2001, there has generally been little change with incentives remaining more popular than charging.

• On balance, households support incentives, are neutral about whether people would recycle more if they were charged, and are opposed to the idea that charging is fair or better than the present system.

• Charging is opposed most by those who have less opportunity to recycle (those in flats and less well off households) and by older people. Younger people (under 35s) appear more open to the idea of financial motivation.

IV INFORMATION AND COMMUNICATIONS • Households seem generally well informed about recycling although around 1 in

3 say they have never received recycling information or cannot remember when they saw any.

• The least well informed are also generally those who recycle least, and Non recyclers are unaware of receiving any information by several orders of magnitude over other groups.

• While it would be tempting to say there is therefore a direct relationship between information and participation, the previous research showed that the relationship is not so straightforward and that “lack of information” is sometimes used as an excuse by the less interested.

• Local councils – mainly via leaflets – are the primary source of information recalled by all types of household, followed by “environmental organisations” and supermarkets.

iv

Household Waste Behaviour in London 2005 • Council communications continue to top households’ future wish list for how

they wish to be informed about recycling, though a sizeable minority would like to see TV advertising.

• Generally, households seem much more interested in “how to” instructions than information relating to the purpose behind recycling, though sizeable minorities do want to know where their recycling ends up or what it is made into – more so regular recyclers than others.

V CONCLUSIONS AND RECOMMENDATIONS

• Evidence that there has been significant progress in London’s household recycling is provided by a number of headline indicators from the 2005 survey:

o The number of declared Non-recyclers fell from 22% to 8% between 2001 and 2005.

o Those saying they can’t be persuaded to recycle more fell from 1 in 6 to 1 in 20 households.

o The number of consistent recyclers (Highs and Mediums) increased from 50% to 70%.

o The proportion claiming to recycle a wide range of materials beyond paper and glass doubled, to between 40% and 50% of households in 2005.

o Those agreeing that recycling is easy to fit into everyday life are now a majority of 60%, up from just under 40% in 2001.

o The number saying that Councils do not collect enough materials has fallen from 60% to 40%.

• Two features in particular have underpinned the improving trend and reflect the significant investments made in infrastructure and communications in the last few years:

o Opportunities to recycle are now vastly better and more equal between social groups than they were in 2001;

o Perceptions and awareness have shifted significantly, such that Londoners’ ‘mental map’ of recycling has been transformed to include many more materials, and far fewer households now perceive recycling as difficult.

• Widespread introduction of kerbside collection, together with the roll-out of more multi-material collections, has been a significant driver of the increase in claimed recycling between 2001 and 2005. Introduction of kerbside collections has been particularly important in recruiting new Medium recyclers, who might otherwise be too passive to make the effort.

• While progress has been impressive, a number of significant challenges clearly remain, including:

o Continuing non or ineffective participation

o More resistance among non participants o Low awareness of recycling facilities among less committed and non-

kerbside households o Continuing lack of confidence about what to recycle (though reduced from

2001)

o Effectiveness of kerbside recyclers

o Residential mobility

o Continuing unequal opportunity for some groups in some places

o Households in flats

v

Household Waste Behaviour in London 2005 • The easy wins that existed in 2001 have largely been tackled by extending

kerbside collections and there is no longer a single easy, or quick, solution to boosting household recycling. The survey findings point instead to the need for action on a broad range of fronts, including:

o Engaging participation from remaining Non and Low recyclers – but accepting that up to 1 in 5 may continue to resist voluntary recycling

o Increasing usage of existing services – by focusing on kerbside non-participation

o Tackling the complacency of existing kerbside recyclers – to recycle a wider range of materials than are collected

o Heading off a ceiling for paper & glass – through continuing communications pressure

o Focusing on green waste – as key area of lost opportunity

o Starting to raise awareness of WEEE - to prevent a recycling time bomb

o An intensive focus on flats – especially areas with young people, high residential mobility, and including low-rise private rentals as well as social housing estates.

• The priorities identified by the 2005 analysis have implications in three policy areas: services; communications; and the rules of engagement with the public on recycling.

• In relation to services, the three key priorities are: to consider what further help is required to deal with the multiple engagement issues relating to households in flats, in inner London especially; to tackle green waste issues; to increase materials capture from existing kerbside households.

• On communications, the analysis points to a need for continuing promotion at local and strategic levels to reinforce the new mental map of recycling and ensure that good intentions are truly embedded in consistent recycling behaviour. Medium and Low recyclers (broadly ‘average’ Londoners) continue to be the key target for these messages.

• While it is still too early for a widespread change in the rules of engagement with the public on recycling - largely because social inequalities in access to services remain – the analysis provides some support for trialling forms of compulsion in areas with mature kerbside collection and settled residential populations.

vi

Household Waste Behaviour in London 2005

1 INTRODUCTION AND CONTEXT In November 2005, the GLA, London Waste Action and the Government Office for London commissioned Brook Lyndhurst to up-date their earlier work for the Resource Recovery Forum (RRF) on Household Waste Behaviour in London. This report presents the findings of a new survey of the waste attitudes and recycling behaviour of 1,005 households in London. The new work was commissioned to explore how much attitudes and behaviour have changed since 2001 following very significant investment in recycling. Over the last fours years investment in recycling services and infrastructure in London totalled over £100 million1: by Government (DEFRA and WRAP) through the work of the London Recycling Fund; and by boroughs and other London waste authorities, both on their own part, through leverage required as a condition of LRF funding, or through partnerships with the private sector.

1.1 Background to the 2005 survey The 2005 survey follows up two previous pieces of published research carried out by Brook Lyndhurst for the RRF2. Phase 1, in 2001, comprised a quantitative face-to-face survey of 1,009 households spread across London, together with six focus groups with different socio-economic groups. The research explored households’ attitudes to waste and the environment, how dealing with waste fitted within their household routines, and what they claimed to recycle. Phase 2, in 2003/4, explored the attitudes and behaviours of High, Medium, Low and Non recyclers in greater depth, to pinpoint which kinds of help needed to be targeted at which kinds of households to encourage Londoners to recycle more. This Phase comprised eighteen focus groups, together with additional analysis of the Phase 1 survey data. The research in both phases was designed and analysed by Brook Lyndhurst, and fieldwork was conducted by MORI (now Ipsos MORI).

1.2 Key findings from Household Waste Behaviour Phases 1 & 2 In 2001/02, landfill accounted for 73 per cent of municipal waste, with a vast majority of this going to sites outside Greater London. 19 per cent of municipal waste was incinerated, at the two waste incineration plants within London, at Edmonton and Lewisham. Only eight per cent of London’s municipal waste was recycled or composted. In 2001, more than half of London’s households were doing little or no recycling; only 1 in 5 was regularly recycling anything other than paper and glass; and 1 in 6 believed nothing could be done to encourage them to recycle more. For all but a few households, the previous research showed very clearly that choosing to recycle is not driven primarily by environmental concern.

1 Source: London Waste Action 2 With funding provided by Cory Environmental via Landfill Tax Credits, and London

Remade.

1

Household Waste Behaviour in London 2005 While interest in ‘doing my bit’ for the environment helps to make households receptive in the first place, and to sustain participation once they start recycling, for many the amount of effort required is the decisive factor. Those with a strong interest in the environment may recycle whatever the difficulty, but others may only mobilise their latent environmental concern when they are provided with convenient and easy-to-use services – typically kerbside collections. Those who have neither an interest in the environment nor convenient services are unlikely to give recycling any thought at all. The 2001 survey highlighted sizeable disparities in access to convenient services. Generally, kerbside recycling collections were then more widely available to older and wealthier households, who typically had stronger environmental concern, more trust in service providers, and a belief in personal responsibility and the power to make a difference for the environment. Less well off, and less motivated, households generally had the least convenient services, often simply because they lived in flats. Many of these households also had less space for storage and lower levels of car ownership (for transporting recyclables). Many Low and Non recyclers in 2001, in fact, experienced multiple barriers to recycling, which combined low latent interest, difficult living conditions and inconvenient services. The previous research concluded that different household types needed different kinds of help to do more but that, overall, achieving a mass increase in participation would require a twin attack involving wider access to services backed up by extensive communications. In particular, views that the “worthy” image of recycling needed to be overhauled were expressed widely in the Phase 2 focus groups. Respondents thought that a younger, livelier call to action would be more engaging, but they also wanted this backed up by more straightforward “how to” instructions delivered at local level. In particular, many existing – but not especially effective – recyclers claimed to be deterred by confusion over what can and can’t be recycled. The survey showed that only a minority were, in reality, recycling a wide range of materials beyond newspaper and glass. The 2004 report concluded that there was a large middle ground of “Medium” and “Low” recyclers who could be pushed much further up the recycling ladder; willing Low recyclers to be persuaded to recycle more often; complacent Medium (and some High) recyclers to take on a wider range of materials, including cans, card and paper other than newspaper. The report also flagged the need to tackle equity issues surrounding access to services - in the short term to help redress the balance between affluent and poorer households; and in the longer term as a necessary precursor to any consideration of compulsion or charging.

1.3 2005 survey design and sample The 2005 survey was again designed and analysed by Brook Lyndhurst, with fieldwork conducted by Ipsos MORI. The questionnaire was discussed and agreed with the GLA, and the RRF provided peer review of the questionnaire and report. Many questions from the 2001 survey were retained so as to provide a direct base for comparison. Some questions – for example on shopping and waste minimisation – were dropped to make room for additional questions on services, reasons for recycling and information. The current survey also asked about a more extensive list of materials than in 2001.

2

Household Waste Behaviour in London 2005 Some of the 2005 questions are similar to questions asked in the NOP Recycle for London campaign evaluation surveys, as well as questions used/recommended by WRAP for evaluation. This is because a number of the questions currently in use elsewhere were originally developed for the RRF 2001 survey and have been refined by others since. Wherever possible, the original question wording is retained in the 2005 survey to allow as close a comparison as possible to 2001, though revised wording is used in a few places; new questions draw on the NOP Recycle for London questionnaires and other Brook Lyndhurst recycling surveys. Fieldwork was conducted during November and December 2005 by Ipsos MORI, who interviewed 1,005 adults (16+) face-to-face at home. Respondents were all solely or jointly responsible for dealing with waste in their household. Sample quotas were set for age, sex, working status, social class, dwelling type and ethnicity and final results were weighted to ensure that the sample matches the socio-demographic profile of London. At the time of the 2001 survey, quotas were based on pre-2001 data whereas the 2005 sample is based on 2001 Census data. In addition, quotas were not set for dwelling type in 2001 which resulted in an over-representation of respondents in houses; this has been corrected in the 2005 survey. Table 1.1. below compares the main socio-demographic features of the 2001 and 2005 samples. Table 1.1

Key demographics Total respondents: 1009 in 2001; 1005 in 2005

Characteristics for which quotas set

Age Ethnicity2001 2005 2001 2005

Under 35 40% 38% White 79% 72%35-54 29% 35% Black 9% 15%55+ 31% 27% Asian 9% 8%

Social Class2001 2005

AB 20% 22%C1 34% 36%C2 16% 17%DE 30% 25%

Other household characteristics2001 2005

Anyone working 67% 75%2+ working 40% 38%Any children 30% 40%Single adult household 24% 29%Have a car 63% 63%Live in a flat 25% 42%Have private garden 76% 64%

The main differences between the two samples are: • The 2005 sample has a higher proportion of Black and Asian Minority Ethnic

households (BAME);

3

Household Waste Behaviour in London 2005 • The proportion of social class DE households is lower

• The proportion of households in flats is higher The possible impact of this sample shift on the overall results has been examined by looking closely at the 2001-2005 changes both within and between different socio-demographic groups and we do not consider that it is a material consideration. In interpreting the findings, and in particular comparisons between sub-groups shown in the graphs in this report, it is important to be aware of the degree of difference required for the results to be considered statistically significant. The required difference varies with the size of the sub-samples, as well as the distribution of answers (e.g. whether 50% give a particular answer or 75%). Broadly speaking, for the sub-samples in our survey, differences between five and ten percent will generally be statistically significant, depending on the exact size of the sample (the bigger the sample, the smaller the required difference). This is particularly important for interpreting differences by ethnicity, for which Black (152) and Asian (81) are amongst the smallest sub-samples in the analysis, as well as for Non recyclers (75). Sub-samples are given the Appendix. Statistically significant differences are indicated on tables and graphs in the report by means of a cross (+).

1.4 Report structure The structure of this report is as follows: Section 2: Claimed recycling habits – participation and materials Section 3: Attitudes, barriers and incentives Section 4: Information and communication Section 5: Conclusions and recommendations Appendix: Details about the sample, together with topline survey results A Summary precedes the Introduction.

4

Household Waste Behaviour in London 2005

2 CLAIMED RECYCLING HABITS As in 2001, the new survey asked respondents how much they feel they recycle overall, then explored this further by asking how often they recycle a wide range of materials. By using the same question frames as in 2001 (but including more materials this time) the survey shows the extent to which claimed recycling in London has moved since. The new survey, in addition, asked more detailed questions about access to, and usage of, services so that this could be compared to patterns of recycling behaviour.

2.1 Access to recycling services Kerbside collections One of the most obvious and significant changes since 2001 has been the increase in the number of households served by kerbside/doorstep recycling collections. In the 2001 survey 48% claimed to have collections; coverage rose to 74% in 2005.3 The 2005 survey estimate is slightly below the actual level of kerbside coverage, estimated by the GLA at around 80%. A possible explanation is provided by the previous focus groups, in which some households in areas where collections were available were unaware of the service. In the 2003/4 groups, this applied most obviously to young, working, frequently mobile households. By matching 2005 survey postcodes against known provision of recycling collections (as given on the Recycle for London web site), it has been possible to estimate the extent of this ‘provision-awareness gap’. On this basis, around 7% of surveyed households appear to be unaware that kerbside/doorstep recycling collections are available to them.4 When added to the 74% of respondents who know they have kerbside collection this would take the total to 81%, which is equivalent to the GLA’s own estimate of kerbside coverage. The widespread roll-out of kerbside collections in recent years has helped to even out some of the inequalities in provision observed in 2001, though some notable differences between household types remain (Figure 2.1). In particular, differences across the age spectrum are now far less marked and the gap between white and minority ethnic households appears to have narrowed.

3 This 74% comprises the group described as “kerbside households” throughout the report. 4 This should be treated as an indicative ‘best estimate’, given the constraints of the data used to derive it. We identified the postcodes of the 26% who did not mention kerbside when prompted with a list of possible recycling facilities, then looked up these postcodes on the Recycle for London web site to identify whether kerbside collection is provided in these areas. If any of these households live in an area where kerbside is provided and they live in a house then they are included in the 7% estimate. If they live in a flat, they are assumed not to have kerbside; case by case examination would be required to refine this further, which was beyond the scope of the present research.

5

Household Waste Behaviour in London 2005 There remains, though, a very wide gap in kerbside provision on two key social dimensions: between the higher professional middle classes and poorer households ((87% coverage for ABs; 61% for DEs); and between those living in houses (88%) and flats (51% for high-rise and 57% for low-rise). When combined, these two factors mean that: • The poorest (DE) households living in flats have the lowest kerbside collection

coverage (44%);

• AB households in houses have the highest coverage (92%) and are also relatively well provided for in flats (76% with kerbside)5;

• C1 and C2 households6 in flats are slightly better provided (53%), than equivalent DE households;

• While C1s and C2s living in houses have similar levels of kerbside provision to AB households.

While much has improved since 2001, it therefore remains the case that poorer and middle income households living in flats are the most disadvantaged in terms of access to convenient recycling services, with just under half in flats still without recycling collections. Figure 2.1

Households served by kerbside collections (2001-2005)

0

10

20

30

40

50

60

70

80

90

100

All HH

Under

35

35-5

455

+

Whi

te

Black

Asian AB C1 C2 DE

Car o

wne

r/us

er

Hou

seFl

at

+ all changes 2001-2005 statistically significant

%

2001 2005

Other recycling facilities

The survey also asked about the availability of bring facilities locally - at on street banks, at supermarkets, communal facilities in flats, and at Household Waste Recycling Centres (HWRCs). These sites provide the main opportunity for households without kerbside collections to recycle, and a top-up option for kerbside households to recycle materials not collected.

5 Based on a small sub-sample of 71 AB households in flats 6 C1 are junior professional/clerical households and C2 are skilled manual households

6

Household Waste Behaviour in London 2005 A sizeable, and potentially worrying, minority of non-kerbside households appear either not to know whether local facilities are available, or claim they do not exist. Altogether this amounts to 1 in 3 of non-kerbside households (but only 8% of the sample overall because non-kerbside households are now a small share of the total) (Table 2.1).

Table 2.1

Access to recycling services

Base

Kerbside households

% (745)

Non-kerbside

households %

(260) Kerbside collection 74 0 Charity shops 40 28 Local bring banks 26 24 Supermarket sites 28 17 HWRC 25 13 Communal facilities in flats 14 35 Newspaper banks outside Tube 16 13 Free/subsidised compost bins 12 5 None 0 18 Don't know 0 14 + significant differences shown in bold

Reflecting the socio-demographic pattern of kerbside provision, the proportions claiming they have no facilities, or no awareness of facilities, are highest amongst households in flats, and DE households. Perversely, for all except communal facilities in flats, claimed availability of bring facilities is equal or higher amongst households with kerbside than those without (Table 2.1). While it is not possible to match claims against actual provision in the same way as for kerbside, there must be some suspicion that low awareness of services signals lack of interest in recycling as much as lack of opportunity. The percentages who say there are no facilities available locally, in fact, match the numbers who agree strongly in later questions that they have never thought about recycling, or do not think it is their responsibility to recycle. Apart from this possibly disinterested minority, most non-kerbside households are aware of local recycling sites, with communal recycling facilities in flats cited most often of all the bring options, by 35% of non-kerbside households (Table 2.1). As a focus for investment in recent years, these communal facilities have clearly extended the opportunity to recycle for households who were previously disadvantaged. This is particularly true in high-rise flats, where 40% of households say such facilities are available. Only 1 in 8 high-rise households now say there are no local recycling facilities (including kerbside), or they don’t know of any. Households in low-rise flats appear slightly worse off, with 1 in 6 unaware of any recycling service; these households have significantly lower access to communal facilities or to on-street bring banks than those in high-rise flats (Figure 2.2).

7

Household Waste Behaviour in London 2005

Figure 2.2

Access to recycling facilities for different housing types

0

10

20

30

40

50

60

70

80

90

100

House High-rise flat Low-rise flat

+ significant difference from "house"

% c

laim

ing

faci

lity

availab

le in

lo

cal are

a

Kerbside Local bring banks Supermarket sites HWRC Communal facilities in flats

+

+

+

+

+

+ ++

+

Of the other bring facilities – supermarkets & HWRCs – claimed access is significantly higher amongst households who also have kerbside collections (Table 2.1). Reflecting the types of household that have collections, access to these bring facilities splits along class and housing situation lines, with significantly higher claimed provision amongst middle class (ABC1) households and those living in houses (Figure 2.2). These households are also more likely to be car owners, which would make these particular facilities easier to use.

2.2 Claimed participation – 2005 versus 2001 As in 2001, two different questions were asked in 2005 to establish levels of claimed recycling: • How much people feel they recycle on a scale of “as much as I possibly can”,

“a lot but not everything”, “I do not recycle much” or “I do not recycle anything”;

• How often each of a list of 22 household items are recycled on a five-point scale from “always” to “never”.

The 2001 survey (and research elsewhere) showed that the second “items” question provides a useful check on the headline claims people make about how much they recycle, when they may be tempted to say what is expected rather than what they actually do. It also provides a more discriminating basis for defining High, Medium, Low and Non recyclers than the simple direct question. Again as in 2001, the possibility of over-claiming was also checked through later questions on attitudes (e.g. “I have never really thought about doing any recycling”).

8

Household Waste Behaviour in London 2005 At a headline level (on the basis of the first question), it is clear that the recent wave of investment in recycling has produced a marked rise in average levels of participation. In particular, the number of households saying they recycle “not much” or “nothing” has halved. Table 2.2

Headline recycling claims 2001 & 2005

2001

% 2005

%

I recycle as much as I possibly can 33 46

I recycle a lot, but not everything that can be recycled

22 31

I do not recycle much 26 14

I do not recycle anything 19 9

+ all changes statistically significant

When the percentages claiming to recycle at different levels are converted into an ‘average score’ for participation7, the survey suggests that average levels of recycling have risen by a quarter (+27%) since 2001. The profile of who does and who doesn’t recycle has changed too, with more of the types of households who were previously non-recyclers now claiming to participate – in particular less well-off, BAME, and younger households (Figure 2.3). Figure 2.3

Claimed propensity to recycle

0

0.5

1

1.5

2

2.5

All AB C1 C2 DE White Black Asian 16-24 25-34 35-44 45-54 55-64 65+

+ all changes 2001-2005 statistically significant

avera

ge s

core

3=

as

mu

ch a

s p

oss

ible

; 0

=n

oth

ing

2001 2005

7 Where 4= as much as possible and 0=nothing

9

Household Waste Behaviour in London 2005 Despite this apparent ‘catch-up’ effect, it remains the case, though, that older, wealthier and White households continue to have the highest overall scores for recycling. Moreover, while there has undoubtedly been a major improvement since 2001, it is important not to be complacent, given that 1 in 4 households are still recycling little or nothing.

2.3 Profile of High, Medium, Low and Non recyclers Responses to how often particular household items are recycled provide further insight into levels of recycling commitment, and the patterns of High, Medium, Low and Non recycling across socio-demographic groups. The following analysis uses the same definition of High, Medium, Low and Non recyclers as in the 2004 report8, which was based on the claimed frequency of recycling newspapers, magazines and glass bottles as follows:

High Always recycle all three materials

Medium Typically recycle materials most or some of the time or always recycle one material and others infrequently

Low Sometimes/hardly ever recycle three materials or recycle one material some/most of time and others never or sporadically

Non Never recycle all three materials

Change in recycling commitment since 2001 The analysis confirms the headline picture, showing a major shift upwards in levels of recycling, with only 8% now classified as Non recyclers as compared to 22% in 2001 (Figure 2.4). All other groups have expanded, most notably Medium recyclers, who now comprise 42% of households as compared to 27% in 2001. Like 2001, however, it is also clear that households’ own definitions of “as much as I possibly can” are not especially stringent. Whereas nearly half claim this when asked directly, only 29% are in reality recycling newspapers, magazines and glass all of the time (High Recyclers on our definition). More of the households claiming they recycle “as much as possible” can more accurately be described as Medium recyclers, who are generally recycling these three materials most or some of the time, but not always. In addition, half of Low recyclers believe they are recycling a lot or as much as they can but are, in fact, recycling few materials and not very often. This amounts to 1 in 10 of households in total whose recycling may be constrained by their own beliefs and aspirations rather than by normal definitions of what constitutes “a lot”. The detailed picture for different materials is reported in section 2.4 below.

8 The 2001 data were re-analysed in the 2004 report to provide a stricter definition of recycling commitment than had been used in the 2001 analysis.

10

Household Waste Behaviour in London 2005 Figure 2.4

Level of recycling (2001-2005)

27 27

22

42

2123

8

29

0

5

10

15

20

25

30

35

40

45

High Medium Low Non

+ all changes 2001-2005 statistically significant

% in

each

recy

clin

g g

rou

p

HWB 2001 HWB 2005

Socio-demographic profile of High, Medium and Low recyclers While High, Medium, Low and Non recyclers are spread right across the age and social class spectrum, different groups tend be concentrated in certain parts of it. The previous reports described the different groups according to their archetypical characteristics in 2001: • High recyclers – more likely to be older and middle class in higher grade

occupations, typically living in suburban houses and a majority with kerbside collections;

• Medium recyclers – described as ‘average’ Londoners, family aged households (25-44), in junior professional and clerical jobs, and living in terraced or semi-detached housing typically with kerbside collections, but also with a sizeable minority of over-65s;

• Low recyclers – most characteristically young Londoners in middle-ranking jobs (manual and non-manual), more likely to live in flats and terraced houses, and only a minority with kerbside collections;

• Non-recyclers – also most typically young Londoners but less middle class than Low recyclers on average, most living in houses but with well above average numbers in flats and with the lowest coverage of kerbside collections.

The broad socio-demographic pattern remains similar in 2005 as in 2001, with High and Medium recyclers tending to be older and more middle class than Low and Non recyclers, less likely to live in a flat, more likely to be White than in a minority ethnic household, and much more likely to have kerbside recycling collections (Table 2.3). (A table showing the full range of statistical differences between groups is provided in the Appendix).

11

Household Waste Behaviour in London 2005 Table 2.3 Socio-demographics of High, Medium, Low and Non Recyclers 2005

HIGH MEDIUM LOW NON TOTAL% % % % %

Percent of respondents 29 42 21 8 100

Have kerbside recycling 91 82 62 24 74

GenderMale 46 47 48 63 48

Female 54 53 52 37 52Age

16-24 11 13 15 18 1325-34 21 25 25 41 2535-44 21 21 26 8 2145-54 14 14 15 15 1455-64 18 14 10 8 14

65+ 15 14 10 11 13Under 35 32 37 39 59 38Over 35 68 63 61 41 62

EthnicityWhite 85 71 62 55 72Black 6 17 19 29 15Asian 6 8 10 12 8Other

ClassAB 29 24 20 7 22C1 37 40 26 35 36C2 16 16 18 19 17D 7 8 15 13 9E 11 13 21 25 16

HousingDetached/semi 32 28 21 10 26

Terraced house 39 32 28 19 32Flat 29 40 51 71 42

Owner occupied 67 49 32 23 47Private rented 13 21 36 37 24Social rented 18 25 30 37 25

Have private garden 73 67 56 41 64

Length of residence in areaLess than 5 yrs 32 45 46 63 43

Over 5 yrs 67 54 52 37 56

Have car 70 67 55 44 63Single adult HH 26 26 35 39 29None working in HH 21 23 24 26 242+ working in HH 40 39 36 33 37No children at home 65 59 57 66 60

12

Household Waste Behaviour in London 2005 There have, though, been a number of notable shifts within the general picture. While the social class profile of High, Medium, Low and Non recyclers has remained broadly similar to 2001 (apart from a slightly higher concentration of DEs among Low and Non recyclers), the age profile across groups has shifted. • While Highs are still predominantly older, more of this group are now under 35

(1 in 3 as compared to 1 in 5 in 2001).

• At the same time, Mediums are now slightly older on average, with a more even spread across the age spectrum as well as a slightly higher concentration in the middle aged band of 35-54 than in 2001.

• The same is true of the Low recycler group, more of whom are now over 35, while the profile of Non recyclers is now even more biased towards younger households (59% are under 35).

• Non recyclers are also much more likely than other groups to be recent in-movers – 63% have located in their current area in the last five years as compared to an average of 43% across all households.

There are two further features which separate the groups, and which are closely linked to the ability to recycle – kerbside collections and living in flats. Even allowing for the fact that the 2005 sample includes more households in flats, the proportion of Low and Non recyclers living in flats has risen significantly. This is now a majority in these groups - half of Lows and 71% of Non recyclers. It is probable that many households living in flats have effectively been ‘left behind’ as kerbside has been rolled out to a majority of houses, enabling previous Low and Non recyclers in these situations to increase their participation. Figure 2.5

Claimed access to recycling services by recycling commitment

0

10

20

30

40

50

60

70

80

90

100

Kerbs

ide

colle

ctio

n

Charit

y sh

ops

Loca

l brin

g ba

nks

Supe

rmar

ket s

ites

HWRC

Com

mun

al fa

cilit

ies in

flat

s

Newsp

aper

ban

ks o

utside

Tub

e

Free

/sub

sidi

sed

com

post

bin

s

None

Don't

know

% o

f each

recy

clin

g g

rou

p (

H/

M/

L/

N)

High Medium Low Non

Equally, though, the fact that kerbside coverage of Low recyclers is now as extensive as it was for Medium recyclers in 2005, and access to local bring banks is near equal to High and Medium recyclers, suggests that this is not the only factor accounting for differences in commitment.

13

Household Waste Behaviour in London 2005 Moreover, the fact that more than 60% of Non recyclers claim there are no services in their area, or they know of none, tends to suggest that indifference as much as unequal treatment underpins non-participation for at least a minority (Figure 2.5). The extent to which recycling services are being used effectively by different groups is covered further in Section 2.6. Whether for reasons of service access, or for reasons of inclination, it is clear that there are still above average concentrations of Low and Non recyclers amongst particular socio-demographic groups, which present opportunities to boost participation (Figure 2.6): • Younger (under 35) households (34% of which are Low & Non recyclers)

• Low income (DE) households (43%)

• Minority ethnic households (39% of Black and Asian households)9

• Households in flats (39%)

• Those in rented accommodation (37% in social rented and 46% in private rented)

• Single adult households (36%)

• Recent in-movers (less than five years) (34%) Figure 2.6

Recycling profile of socio-demographic groups

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

All

Under

35

35-5

455

+ AB C1 C2 DE

Whi

te

Black

Asian

House

Flat

Owne

r occ

upie

d

Privat

e re

nted

Social

rent

ed

In a

rea

< 5

yrs

Sing

le a

dult%

wit

hin

each

gro

up

wh

o a

re H

, M

, L o

r N

recy

clers

High Medium Low Non

2.4 Materials – change between 2001 and 2005 In 2001 (and confirmed in the 2003 focus groups) Londoners’ ‘mental map’ of recycling was defined principally by newspapers, magazines and glass bottles. At that time, only 1 in 5 households were regularly recycling anything other than these items.

9 Data combined to provide large enough sub-sample for comparison

14

Household Waste Behaviour in London 2005 This picture has clearly changed. While newspapers and glass bottles remain the most consistently recycled items in the 2005 survey (66% and 55% respectively recycling them all/most of the time), a wide range of other materials are now (claimed to be) recycled regularly by 40-50% of households (Table 2.4 and Figure 2.7). Table 2.4

Frequency of recycling household materials 2005

All / Most of

time %

Some-times

%

Hardly ever / Never

% Newspapers 66 15 15 Magazines 63 18 17 Junk mail 56 19 23 Glass jars 54 18 27 Glass bottles 54 18 26 Food cans 49 17 32 Drink cans 49 16 32 Light card (e.g. cereal boxes) 48 18 31 Plastic drink bottles 45 17 35 Heavy card (e.g. computer packaging) 44 18 34 Plastic carrier bags 42 18 38 Plastic cleaning bottles 40 17 41 Clothing 37 25 37 Cartons (Tetrapak) 35 15 46 Other textiles 32 24 43 Aerosol cans 28 14 52 Tin foil 24 16 55 Garden waste for compost 23 15 55 Food waste for compost 22 16 60 Electrical products (e.g. fridges) 13 9 74 Furniture 13 11 72 Batteries 11 11 71

15

Household Waste Behaviour in London 2005 Figure 2.7

Recycling frequency of materials (2001-2005)

0

10

20

30

40

50

60

70

Newspapers Magazines Largecardboard

Light card Glass bottles Food cans Drink cans Plastic drinkbottles

Tin foil Clothing Gardenwaste forcompost

+ all changes 2001-2005 statistically significant; garden waste borderline significant

% c

laim

ing

all

/m

ost

of

tim

e

All / Most of time (2001) All / Most of time (2005)

Increases in claimed recycling have been most spectacular for card, cans and plastic bottles, to the extent that the number of households saying they never recycle these items has halved - fewer than 30% now say they never recycle these items, down from 70-80% in 2001. While this is a positive trend, households are almost certainly over-claiming how much of these materials they actually recycle, given that London’s measured recycling rate is only 17.5%. It is probable that a combination of the Recycle for London campaign and the inclusion of more materials in many kerbside collections has raised awareness of what should be recycled, such that households’ mental maps of recycling have been redefined significantly, but that this latent interest has still to be converted into widespread action. A second possibility is that raised awareness is contributing to contamination in some instances, so that households are setting out these materials in the mistaken belief they can now be recycled everywhere. This cannot be verified for London as a whole but is something that the Boroughs will be able to take a view upon. There also remains room for improvement in relation to other items. Performance of the previously defined ‘model’ materials of paper and glass - while improved overall - showed little change at the highest level of recycling. Those who say they “always” recycle these items showed a barely significant increase - from 42% to 46% for newspapers, from 31% to 35% for glass bottles, and 36% to 43% for magazines. It may be premature to suggest that this represents a ceiling for these particular materials, but a clear priority for the near future will be to turn the large numbers of new Medium recyclers into households that are always recycling ‘easy’ materials rather than occasionally forgetting.

16

Household Waste Behaviour in London 2005 There is also significant potential to increase the capture of green garden and kitchen waste. Again, only a modest increase in claimed recycling was recorded in the 2005 survey10, with half of households with a garden (a majority of the sample) saying that they hardly ever or never recycle garden waste for compost, and only 1 in 3 saying they do this always or most of the time. Our previous research showed that households typically see green waste as environmentally benign because it is bio-degradable, and therefore not really worth recycling. An interest in gardening is generally a stronger motivation for composting than is commitment to recycling.11 Clothing and textiles similarly appear low down the list of regularly recycled items and showed little change since 2001 in the numbers never recycling this item (1 in 3 households). Just over 1 in 3 claim they recycle clothing always/most of the time, slightly ahead of the 1 in 4 who claim they use charity shops for recycling. At the bottom of the recycling hierarchy are a number of items that were added to the 2005 survey to cover bulky, WEEE and hazardous materials. Around three-quarters of households admit they hardly ever/never recycle any of furniture, electricals, or batteries, though around 1 in 8 claim they do so always/most of the time.

2.5 Materials habits of different households Kerbside and non-kerbside households Access to kerbside collections makes a significant difference to levels of recycling by individual households. Those with kerbside collections are 2 to 2½ times more likely to recycle most ‘everyday’ households times all/most of the time than non-kerbside households, and are even more likely than non-kerbside households to recycle furniture, electrical goods and garden waste (more kerbside households have gardens in any case). The roll-out of multi-material kerbside collection over the last few years has certainly contributed to the increase in claimed recycling of cans, card and tins; there are now many more kerbside households and higher proportions of kerbside households are claiming to recycle these materials regularly (all or most of the time) (Figure 2.8). Expansion of recycling collections, however, may not be the only reason for the observed increase. A similar trend (though at lower levels) is apparent for non-kerbside households, where cans, card and plastics have shown the biggest increase of any materials since 2001. 10 Though this may have been affected slightly by seasonality, given that the 2001 survey was conducted in Summer and the 2005 in Winter. 11 Green waste was covered in detail in the 2003 focus groups and 2004 report; research by Peter Tucker at the University of Paisley shows similar findings.

17

Household Waste Behaviour in London 2005 Figure 2.8

"Always" recycle items kerbside & non-kerbside households 2001-2005

0

10

20

30

40

50

60

70

Newsp

aper

s

Mag

azin

es

Glass

bot

tles

Drink

cans

Food

can

s

Heavy

car

d

Garde

n w

aste

for c

ompo

st

Ligh

t car

d

Plas

tic d

rink

bottle

s

Tin

Foil

Newsp

aper

s

Mag

azin

es

Glass

bot

tles

Drink

cans

Food

can

s

Heavy

car

d

Garde

n w

aste

for c

ompo

st

Ligh

t car

d

Plast

ic d

rink

bottle

s

Tin

Foil

% c

laim

ing

recy

cle ite

m a

ll o

f ti

me

2001 2005

Kerbside households

Non-Kerbside households

+

++

++

+

+ + ++ + +

+ significant difference from 2001

The trend for newspapers and glass is slightly more complex. While more households overall are claiming to recycle these items all/most of the time, this has been achieved largely by the extension of collections to more households, rather than an increase in the average frequency at which kerbside households recycle these items. On the whole, it appears that new kerbside recruits are slightly less likely to recycle newspapers all of the time, and no more likely to recycle them most of the time, than kerbside households in 2001 (Figure 2.8). The same is true of glass. These trends add further weight to the idea that household recycling of these materials may be close to a ceiling, with newspapers and magazines stuck at around 75% of kerbside households recycling them all/most of the time, and glass near to 65%. A more optimistic interpretation may argue that these new recruits need more time and, perhaps, encouragement for new habits to become embedded. Similar trends are apparent amongst non-kerbside households, where the claimed propensity to recycle paper and glass regularly has stayed more or less unchanged since 2001, while claimed recycling of cans, card and plastics has increased significantly. High, Medium, Low and Non- recyclers In the previous Household Waste Behaviour research: • Only High recyclers were recycling a range of materials any more often than

occasionally and were confident about which materials they could recycle.

• Medium recyclers were recycling newspapers and magazines most of the time on average, but were recycling glass slightly less often, and claimed to be confused or indifferent about items such as card, other paper and cans.

18

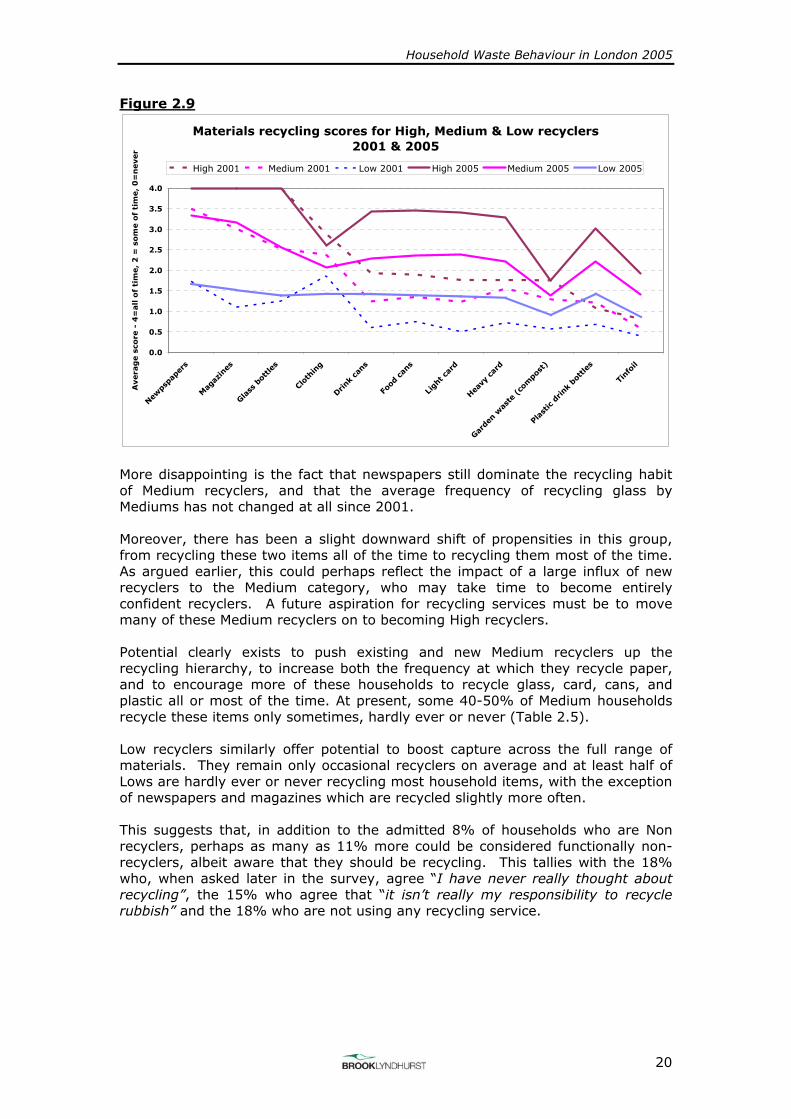

Household Waste Behaviour in London 2005 • Both Medium and High recyclers wanted to recycle plastic, though few were

doing so in 2001 and 2003.

• The recycling activity of Low recyclers was confined largely to occasional recycling of newspapers and donating old clothes to charity.

As in the previous reports, responses to the question “How often, if at all, do you recycle the following everyday items?” have been translated into average scores to indicate the average claimed frequency of recycling each of 22 household items, as follows:

All of the time Score 4 Most of the time Score 3 Some of the time Score 2 Hardly ever Score 1 Never Score 0

Figure 2.9 shows the average scores for each material for High, Medium and Low recyclers, and compares the pattern for each group in 2005 to that in the 2001 survey.12 In considering the results, it is important to bear in mind that there are now many more Medium recyclers than in 2001, and fewer Low recyclers. The overall shift in recycling levels reported in section 2.4 is the combined outcome of a change in the relative sizes of High, Medium and Low groups (defined on the basis of newspaper, magazine and glass recycling), as well as any change in the average frequency of recycling these and other materials within individual groups. As well as there now being many more Medium recyclers than in 2001 and a modest rise in the number of High recyclers, the range of materials recycled by each group also appears to have broadened. Increased recycling of card, cans and plastic overall appears to have been achieved by increased frequency of recycling these materials across a majority of households, not only High recyclers (Figure 2.9). The shift has, though, been most marked for High recyclers, 4 out of 5 of which are now claiming to recycle these materials all or most of the time. Previously, High recyclers were recycling cans and card no more than sometimes on average, and plastic bottles hardly at all. Though a smaller scale shift, Medium and Low recyclers are recycling these items more frequently too, to the extent that Medium recyclers have moved beyond the levels claimed by High recyclers for these items in 2001, and Low recyclers have moved up to the level of previous Medium recyclers (Figure 2.9).

12 Only for those materials included in both surveys

19

Household Waste Behaviour in London 2005 Figure 2.9

Materials recycling scores for High, Medium & Low recyclers 2001 & 2005

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Newps

pape

rs

Mag

azin

es

Glass

bot

tles

Clot

hing

Drink

cans

Food

can

s

Ligh

t car

d

Heavy

car

d

Garde

n w

aste

(co

mpo

st)

Plas

tic d

rink

bottle

s

Tinf

oil

Avera

ge s

core

- 4

=all o

f ti

me,

2 =

som

e o

f ti

me,

0=

never

High 2001 Medium 2001 Low 2001 High 2005 Medium 2005 Low 2005

More disappointing is the fact that newspapers still dominate the recycling habit of Medium recyclers, and that the average frequency of recycling glass by Mediums has not changed at all since 2001. Moreover, there has been a slight downward shift of propensities in this group, from recycling these two items all of the time to recycling them most of the time. As argued earlier, this could perhaps reflect the impact of a large influx of new recyclers to the Medium category, who may take time to become entirely confident recyclers. A future aspiration for recycling services must be to move many of these Medium recyclers on to becoming High recyclers. Potential clearly exists to push existing and new Medium recyclers up the recycling hierarchy, to increase both the frequency at which they recycle paper, and to encourage more of these households to recycle glass, card, cans, and plastic all or most of the time. At present, some 40-50% of Medium households recycle these items only sometimes, hardly ever or never (Table 2.5). Low recyclers similarly offer potential to boost capture across the full range of materials. They remain only occasional recyclers on average and at least half of Lows are hardly ever or never recycling most household items, with the exception of newspapers and magazines which are recycled slightly more often. This suggests that, in addition to the admitted 8% of households who are Non recyclers, perhaps as many as 11% more could be considered functionally non-recyclers, albeit aware that they should be recycling. This tallies with the 18% who, when asked later in the survey, agree “I have never really thought about recycling”, the 15% who agree that “it isn’t really my responsibility to recycle rubbish” and the 18% who are not using any recycling service.

20

Household Waste Behaviour in London 2005 Table 2.5

Habits of High & Medium recyclers for selected household items

% saying item recycled all/most of the time

Medium recyclers

%

High recyclers

%

Percentage point gap

between High & Medium

Newspapers* 99 100 1

Magazines* 83 100 17

Junk mail 65 87 22

Glass bottles* 60 100 40

Glass jars 59 97 38

Drink cans 52 86 34

Food cans (e.g. baked bean tins)

52 86 34

Light card (e.g. cereal boxes)

52 85 33

Heavy card (e.g. computer packaging)

47 80 33

Plastic drink bottles (e.g. water, milk)

31 47 16

Garden waste for compost

22 39 17

• * imposed as selection criteria – High recyclers defined as households recycling newspapers, magazines and glass bottles “all of the time”

• + all differences significant, except newspapers

Finally, garden (and kitchen) waste appear to present a special case, where more effort is required by all households regardless of their habits for other materials. At present, only 2 in 5 of High recyclers and 1 in 5 of Medium recyclers claim they are ‘recycling’ garden waste for compost all/most of the time.

2.6 Are recycling services being used effectively? Now that a majority of households in London have kerbside recycling collections, maximising the effectiveness of service use should be a future priority. Potential to raise London’s recycling rate lies as much here as in recruiting the last remaining non-participants. The usage pattern of both kerbside collection and the main types of bring site revealed in the survey confirms a suspicion that there are functionally more Non-recyclers than respondents’ own claims about recycling would indicate. Altogether, nearly 1 in 5 (18%) of the 2005 sample are using neither kerbside collection nor local bring sites regularly as compared to only 8% declared non-recyclers (Figure 2.10).

21

Household Waste Behaviour in London 2005 Figure 2.10

Usage pattern of recycling services (whole sample)- kerbside & bring facilities

(communal in flats, on-street, supermarket or HWRC)

Have kerbside - don't use any service

regularly6%

No kerbside - use other13%

Have kerbside - don't use, but use other

5%

Use kerbside only42%

Use kerbside & other22%

No kerbside - don't use other regularly

12%

Kerbside take-up and usage As regards kerbside collections, we have already estimated that 7% of households overall do not appear to know that collections are provided in their area. When added to the 74% of survey respondents who are aware, this suggests that 81% of London’s households have access to kerbside. Use of collections is high amongst those households who are aware the service is provided – 86% who know they have collections also say they use them. However, if all non-users are included (those who appear unaware that the service exists as well as those who know collections are available), then the average usage rate of kerbside collection falls to 80%.13. Put simply, this means that around 1 in 5 households provided with a kerbside service are not using it. In addition, some households who have kerbside collections are using them ineffectively. Of those who are aware that kerbside is provided, 1 in 5 (20%) are classified as Low/Non recyclers. This is, however, an improvement on 2001 when nearly 1 in 3 kerbside households were classified as Low and Non recyclers. The data can be used to infer a profile of ‘recycling effectiveness’ all London’s households, shown in Table 2.6. It appears that kerbside is being used moderately effectively, but there is still considerable scope both to engage first-time participants and to increase materials capture from Low and Medium recyclers.

13 Where usage rate = households using/households provided

22

Household Waste Behaviour in London 2005 Table 2.6 Effectiveness profile of London’s Households

Effectiveness profile of London's households

% Do not have kerbside collection 19 Have kerbside collection 81 of which: Unaware have kerbside* 7 Do not use 11 Use: Low recycler 10 Use: Medium recycler 29 Use: High recycler 24 NB estimated, not direct from survey, see footnote 3

Usage across household types The following analysis is based on those households who are aware of kerbside collections, as reported directly in the survey. The usage pattern of kerbside collections varies only moderately across household types. If households have kerbside collections then typically 80%-90% claim to use them across all ages, social classes and ethnicities (albeit some are Low recyclers). In particular - and in contrast to their lower average recycling rates overall - lower social class DE households appear to use kerbside services as much as other social groups when given the opportunity. Figure 2.11

Usage of kerbside collections

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

White Black Asian AB C1 C2 DE 16-24 25-34 35-44 45-54 55-64 65+ Highriseflat

Lowriseflat

House

+ significant difference

% t

hose

wit

h k

erb

sid

e w

ho u

se it

Kerbside usage of group Average usage - total sample

++

+

23

Household Waste Behaviour in London 2005 Apparent usage rates of kerbside are, though, much lower for households living in flats than in houses, especially for high rise flats which have the lowest take-up of kerbside of any group. This is mirrored by higher usage rates in owner occupied than rented property. Usage of kerbside is also slightly below average for younger and Black households, and those aged 55-64 (who are more skewed to White and DE households than the sample overall). A further key difference in usage is apparent by length of residency – an average usage rate of 89% for households living in their current area for more than 3 years falls to 78% for those who have moved in within the last 1-2 years. This finding lends some support to the theme identified in the 2003 focus groups that mobile households may miss out on essential recycling information, may not have a container and, having missed the initial introduction of the service, be too passive to make the effort to contact their local authority. Kerbside materials coverage In addition to those who are not using kerbside services at all are those who either use the service only sporadically, or restrict their recycling to what is collected. Claimed recycling of newspapers (i.e. the most commonly collected material) provides an indicator of ineffective usage. In the 2005 survey, three-quarters of kerbside households claim they recycle newspapers all/most of the time, leaving a quarter who say they are only participating occasionally or less often. This means that, on top of the 14% admitted non-users of kerbside, perhaps up to a further 11% are either using kerbside collection only occasionally or over-claiming that they use it at all. Regular recycling of magazines is at a similar level to newspapers amongst kerbside households but falls to 65% for junk mail and glass. Between 50% and 60% of kerbside households also claim to recycle cans, card and plastic all or most of the time, reflecting the fact that there are still some service gaps for materials, even though all kerbside households can now recycle at least three materials14. At present, just under 1 in 3 kerbside households are using other bring facilities as well as their kerbside collections, while more than half (56%) rely entirely on their collections. The passivity of kerbside households is further indicated in the 43% of kerbside households who agree that “the Council doesn’t collect all the things I want to recycle” and the 25% who agree that “I‘m too busy to make special trips to recycling banks”. The previous research suggested that what many kerbside households identify as ‘recyclable’ is defined by what is collected and this appears to continue to hold true for many. Other bring recycling facilities 2 in 5 (40%) households use bring facilities15, including both kerbside and non-kerbside households.

14 Source: GLA 15 Local on-street banks, communal facilities in flats, supermarket sites or HWRCs

24

Household Waste Behaviour in London 2005 Just over half (52%) of non-kerbside households use at least one mainstream type of bring facility, and this rises to 63% using any facility, including charity shops, compost bins and newspaper recycling bins at Tube stations. This leaves, though, more than 1 in 3 non-kerbside households using no facility at all (Figure 2.11). Figure 2.12

Use of recycling facilities other than kerbside collections

0 5 10 15 20 25 30 35

Charity shops

Local bring banks

Supermarket sites

HWRC

Communal facilities in flats

Newspaper banks outsideTube

Free/subsidised compost bins

None

Don't know

% of household type saying they use facility

Kerbside households Non-kerbside households

+

+

+

+

+

+ significant difference from kerbside HH

A majority of these non-kerbside, non-user households say there are no facilities locally or they are unaware of any, though there are, in addition, a small number who know about local facilities but choose not use them. Communal recycling banks in flats heads the list of facilities used by non-kerbside households, with 29% claiming to recycle via this route. This is, in fact, the only service which non-kerbside households are significantly more likely to use than other households. Communal facilities in flats also have the highest awareness-usage ratios16, with some 4 out of 5 non-kerbside households who say the facility is available claiming also to use it. This still leaves, though, 17% of non-kerbside households who are not using the communal recycling facilities which they know are available (which is a similar ratio to those who do not use kerbside collection when it is provided). Numbers using other bring facilities are lower, with each of local bring banks, supermarket sites and HWRCs being used by only 12-13% of households on average. Only minor differences are apparent between kerbside and non-kerbside households in their usage of supermarket and on-street bring sites; but usage of HWRCs is notably higher amongst kerbside households (who are also more likely to have a car).

16 Awareness-usage ratio = the number of users as a proportion of those saying thethe facililty is available locally.

25

Household Waste Behaviour in London 2005

3 ATTITUDES, BARRIERS AND INCENTIVES