Embed Size (px)

Citation preview

House Prices and New Firm Capital Structure ∗

Kristoph Kleiner†

Indiana University, Kelley School of Business

Abstract

We examine how real estate prices impact new �rm capital structure. Relying a new micro-level

dataset, we �nd that during the housing boom one-quarter of large US entrepreneurs depended

on home equity as a source of initial capital. In response to an exogenous shock to real estate

price growth, start-ups increase reliance on home equity �nancing relative to �rms with minimal

�nancing needs. The results are greatest for �rms that receive between $50,000, and $1 million

in funding. In contrast, we see entrepreneurs shift �nancing away from formal business loans, yet

�nd minimal e�ects on informal debt markets (such as family and friends) or household credit

cards. Our results suggest that while home equity is a signi�cant source of �nancing, collateral

values have only a limited impact on capital structure outside of bank debt.

∗I thank my advisor Pat Bayer, and committee members Manuel Adelino, David Robinson, and Daniel Xu as thispaper is based on the third chapter of my PhD Dissertation. I thank seminar participants at Duke University and theFuqua School of Business. All remaining errors are my own.†Department of Finance, Indiana University, 1309 East 10th Street, Bloomington, IN 47405. Email: Klein-

1

1 Introduction

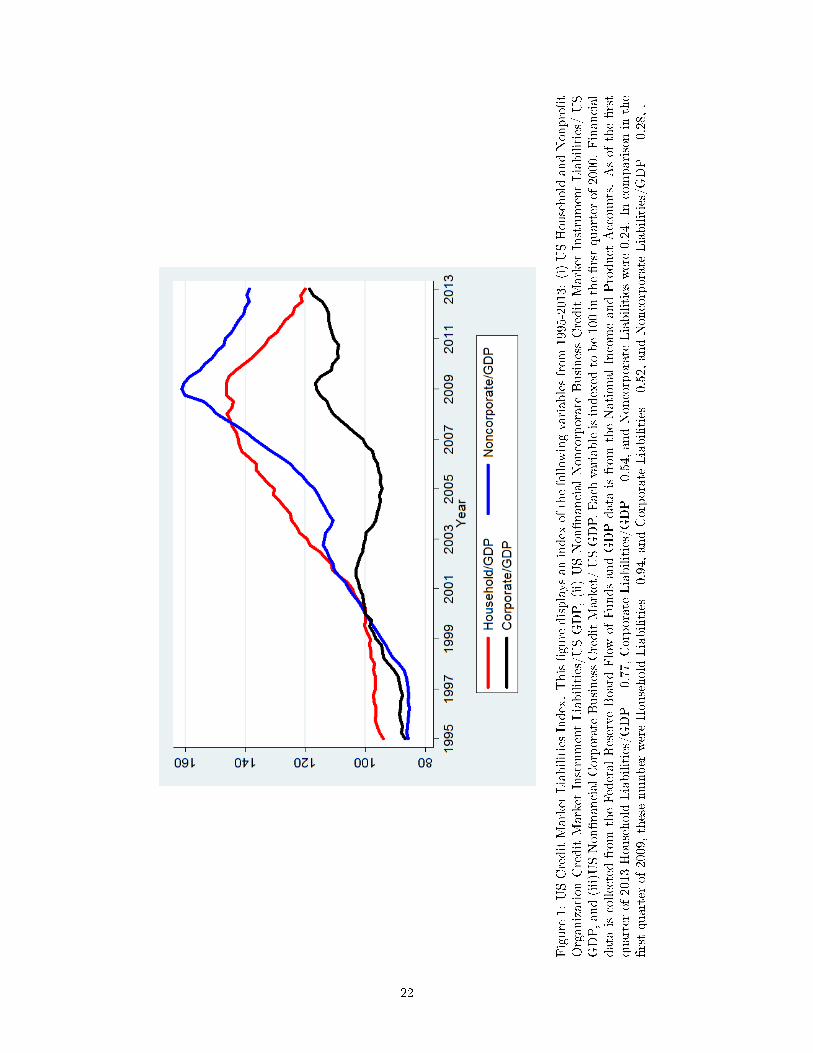

Between 1997 and 2009 the Debt-to-GDP ratio of US noncorporate �rms (sole proprietorships and

limited partnerships) grew faster than both household debt and corporate debt before subsequently

declining by 14% during the Financial Crisis as shown in Figure 1. Research has highlighted the

possibility that the rise and fall of small �rm debt is linked to the housing market as evidence �nds

that an increase in real estate prices leads to a higher likelihood of entrepreneurship [Hurst and Lusardi,

2004, Adelino et al., 2013, Schmalz et al., 2013, Corradin and Popov, 2015]. These papers rest on the

theory that collateral pledging alleviates �nancial frictions when contracts are incomplete Hart and

Moore [1995], and empirical evidence that �rms with high default risk are required to secure loans

through collateral Berger and Udell [1990].

To date, direct evidence of real estate prices on the capital structure of new �rms is still quite

limited. This is a noticeable gap given the literature on consumer borrowing has separately identi�ed

house price a�ects on both secondary mortgages [Mian and Su�, 2011] and consumption [Mian et al.,

2013]. Similarly, an alternate research agenda documents real estate price a�ects on both corporate

investment/employment [Chaney et al., 2012, Kleiner, 2014] and capital structure [Cvijanovic, 2014].

Using a new �rm-level dataset on US small �rm �nancing, we quantify the impact of house prices on

new �rm capital structure. We �rst o�er clear evidence that home equity is an economically signi�cant

source of �nancing. We �nd that in 2006 eleven percent of all start-ups relied on home equity to initially

fund the �rm. This number increases up to 29% of �rms with �nancing needs between $100,000 and

$249,999.

We next highlight the role of house price shocks in new �rm �nancing. To isolate this e�ect we

distinguish between �rms that take under $5,000 in initial �nancing and �rms over $5,000. This allows

us to separate local demand shocks-which a�ect all �rms- from collateral shocks that a�ect only �rms

with high �nancing needs.

There are two sources of endogeneity in our analysis. First, �rms with large �nancing needs may be

uniquely a�ected by local demand shocks. Secondly, initial �nancing needs are an endogenous choice.

To overcome the �rst concern we follow the literature and instrument for exogenous house price growth

2

from the housing supply elasticity measure �rst developed by Saiz [2010]. As discussed in Cvijanovic

[2014] the intuition for this approach is that local areas with little undeveloped land experience large

real estate price appreciation in response to an increase in the aggregate real estate demand. Areas

with available undeveloped land will experience more minor price growth since the demand can be

easily supplied.

We attempt to alleviate the second concern- �nancing needs are endogenous- in two ways. First, we

allow for both �rm and owner characteristics in the empirical speci�cation. Secondly, we extend our

analysis by developing a simple pseudo-panel. With panel data we are able control for unobservable

di�erences across �rms.

We estimate that a 10% real estate price growth increases home equity �nancing by 1.1% for the

mean �rm. We also calculate the probability a �rm �nances exclusively through this channel increases

by 0.4%. The results hold in the pseudo-panel estimation. The e�ects of real estate shocks are strongest

for large start-ups. Real estate price growth of 10% increases home equity �nancing by 2.1% for �rms

with been $250,000 and $1 million in initial �nancing.

Our collateral shock a�ects the capital structure of the �rm. In response to an exogenous shock

to real estate price growth, start-ups increase reliance on home equity �nancing, causing a decline in

�nancing through formal bank loans. Speci�cally, a 10% increase in real estate prices causes a 1.7%

decrease in the probability of bank lending. The results hold regardless of �rm �nancing needs and

industry. In comparison, house prices have no a�ect on costly consumer debt (such as credit cards) or

informal lending (such as family loans).

To highlight the policy implications of our results we focus on the e�ect of house prices on govern-

ment loan guaranteed programs. The rational for this type of intervention is that a lack of collateral is

a primary impediment for access to �nancing. This argument appears to hold as a ten percent increase

in real estate decreases government guaranteed loans by 0.12% and up to 0.3% for �rms with �nancing

between $25,000-$250,000. We conclude with a discussion and applicability of our results following the

2008 Financial Crisis.

A number of papers have theoretically documented the role of credit constraints in the entrepreneur-

3

ship decision, including Evans and Jovanovic [1989] and Cagetti and De Nardi [2006]. This theory

appears to hold up empirically: one line of the literature has focused on using house price growth as

a credit shock on small business. For instance Hurst and Lusardi [2004] document that prices impact

the decision to start a business, but only at the top of the wealth distribution. Recent evidence from

Adelino et al. [2013], Schmalz et al. [2013], Corradin and Popov [2015] instead highlights a strong

correlation between house price growth and new business starts. Missing from this analysis is an

understanding of the underlying capital structure.

Closest to our work, Robb and Robinson [2012] �nds that a positive real estate shock increases bank

loan �nancing. We extend this analysis in a number of ways. First, we develop a new identi�cation

strategy to distinguish demand e�ects from collateral e�ects. Secondly, we include direct information

on home equity �nancing, and so can distinguish secured vs. unsecured debt. Third, we characterize

the impact of real estate shocks to the full capital structure, as opposed to just bank debt. Fourth, we

include a much larger sample size, allowing for a number of robustness checks.

The outline for this paper is as follows. Section 2 introduces our empirical methodology and

summarizes the data. Section 3 discusses the results and Section 4 concludes.

2 Empirical Methodology and Data

The purpose of our paper is to �rst determine the role of home equity in small �rm �nancing, and

secondly, to evaluate the e�ect of house price shocks on capital structure. In this section, we determine

the empirical speci�cation necessary to achieve the latter goal, and then summarize the data to ful�ll

the former.

4

2.1 Empirical Methodology

To directly test how real estate price growth a�ects new �rm �nancing through home equity we run

the following linear probability model:

HomeEquityi = β∆%P l × 1[Fin > $5, 000] + κ∆%P l + γ1[Fin > $5, 000]

+ξ∆%Unempl + ζ∆%GDP l + α+ controlsi + εi

(1)

∆%P l2002−2006 = χ× Elasticityl + ω + controlsi + ult (2)

where HomeEquity is a binary choice variable: a value of 1 means new �rm i relied on home

equity to �nance the start-up of the business in 2006. We de�ne location l at the state level so that

∆%P lt is the state-level residential house price increases between 2002 and 2006.

To identify the e�ects of a collateral a�ect separate from a demand shock, we separate between

real estate shocks that a�ect all �rms and any additional a�ect on �rms with at least $5,000 in

initial �nancing indicated. We denote the binary variable distinguishing these �rms 1[Fin > $5, 000].

Therefore β is our key coe�cient of interest and measures the e�ect of real estate growth on home

equity �nancing through the collateral channel.

This speci�cation assumes that �rms with minimal �nancing needs are able to fund the business

through personal savings and personal assets. Later, when summarizing the data, we will con�rm

these assumptions: 88% of these �rms depend on personal savings and 7% depend on personal assets.

Since real estate prices are likely correlated with investment opportunities due to the omitted

variable of local demand shocks we use housing supply elasticity as an instrument for exogenous real

estate price growth. To achieve this we develop a new measure of state-wide house supply elasticity

as the population-weighted measure of MSA local housing supply elasticity. In addition we include

measures of state demand shocks, speci�cally GDP growth (∆%GDP ) and the unemployment rate

(∆%Unemp), both measured during the 2002-2006 period.

In addition we include a number of standard controls in our analysis; this allows us control for

any di�erences between �rms with small vs. large �nancing needs. The controls include both �rm

5

characteristics (such as NAICS sector �xed e�ects and �rm size �xed e�ects) and owner characteristics

(such as number of owner, and educational background). Finally all results are clustered at the state

level.

In our �rst stage results we �nd that our state-level measure of housing supply elasticity is highly

correlated with real estate values between 2002 and 2006. A coe�cient of -0.25 implies that a one

standard deviation increase in elasticity decreases real estate price growth by 8 percentage points.

This re�ects that even at the state-level housing supply elasticity was a strong predictor of the run-up

of housing price growth documented between 2002 and 2006.

One concern with this analysis is that we are not able to control for unobservable �rm character-

istics as we only have cross-sectional data. This is a particular concern since �nancing needs is an

endogenous choice, yet we take the variable as exogenous in our methodology once controlling for all

other observable characteristics.

To alleviate this concern we rely on our large sample to also develop a pseudo-panel of our data by

characterizing a pseudo-�rm for each speci�c state and �nancing level pair. First introduced by Deaton

[1985], a pseudo-panel is an econometric technique to track cohorts through a series of independent

cross-sections, creating a new dataset of panel data.

For our purposes, we de�ne a cohort based on both �rm location and �nancing needs. As before

location is de�ned at the state level. We then use the speci�c speci�cation:

HomeEquityit = β × P l × 1[Fin > $5, 000] + κ× P lt

+ξ × Unemplt + ζ ×GDP lt + αi + δt + controlsit + εit

(3)

P lt = βP (Elasticityl × It) + φt + θl + αi + εit (4)

In this formula, HomeEquity is now a continuous variable measuring if pseudo-�rm i �nanced

through home equity in year t . In addition αi is a pseudo-�rm �xed e�ect, δt is a year e�ect, and

P lt is the housing price index for location l. We develop controls for our pseudo-�rm, controls, which

as before control for changes in both �rm and owner characteristics. Similarly, we also include local

6

unemployment and GDP measures. An indicator for �nancing needs is now absorbed by the pseudo-

�rm �xed e�ect. The advantage to the speci�cation is that we are able to control for static unobservable

di�erences across �nancing need cohorts.

As before, our analysis relies on an exogenous source of real estate price growth; therefore we

also derive a time-varying instrument by interacting the conventional mortgage rate with the state-

level housing supply elasticity. The intuition in this speci�cation is that the national mortgage rate

is a measure of national house demand. Local demand shocks will most impact house price growth

in inelastic regions during periods of high national demand- and therefore low mortgage rates. The

speci�cation is similar to Chaney et al. [2012].

2.2 Data Summary

O�ce of Federal Housing Enterprise Oversight House Price Index

The OFHEO House Price Index is available at the state level starting in 1975 and for the majority

of Metropolitan Statistical Areas starting in 1987. For our purposes we focus on the state level data

between 2002 and 2006. During this time period we �nd signi�cant cross-sectional heterogeneity in

real estate price growth. Speci�cally, Michigan saw 10% and Indiana and Ohio saw an 11% increase

in house price between 2002 and 2006. In comparison Hawaii, Florida, Nevada, and California saw a

combined growth rate of 93%, 88%, 87%, and 86%, respectively.

Local Housing Supply Elasticity

The local housing supply elasticity measure comes from Saiz [2010] and is available for 95 MSAs.

It is estimated using processing satellite-generated data on elevation and presence of bodies of water.

Given our focus on state-level data, we develop a new measure of state housing supply elasticity:

speci�cally, we weight each MSA as a fraction of the population of the state. From our state-level

estimates we �nd a large range from an elasticity from 0.65 for New Hampshire, 0.69 for New Jersey

and New York to 2.83 for Nebraska and Iowa and 3.36 for Kansas.

7

Bureau of Economic Analysis State GDP

Due control for time-varying changes within a state, we also include data on both GDP and

unemployment. Our GDP data comes from the Bureau of Economic Analysis. We �nd that between

2002 and 2006 the median state saw an 11% increase in real GDP with the 10th and 90th percentiles

at 5% and 21%.

Bureau of Labor Statistics Unemployment Rate

The state-level unemployment rate is the Bureau of Labor statistics. The unemployment rate fell

about 1% in the average state with no change at the 90th percentile.

Survey of Small Business Owners

Our empirical analysis depends on a new �rm-level dataset from the Survey of Business Owners

(SBO) Public Use Microdata Sample (PUMS). The SBO PUMS is a cross-sectional dataset on en-

trepreneurs and surveys a random sample of business from a complete list of all �rms operating during

2007 with receipts of at least $1,000. The data include categorical variables documenting both the

�nancial needs of each �rm, and variables that denote the source of all initial funding and all later

funding.

The list of all forms is compiled from business tax returns, speci�cally: Form 1040 Schedule C

(Pro�t or Loss from Business), Form 1065 (US Return of Partnership Income), 1120 Corporation

Tax Forms, Form 941 �Employer's Quarterly Federal Tax Return�, and Form 944 �Employer's Annual

Federal Tax Return.

For �rms with paid employees, the Census Bureau also collected employment, payroll, receipts, and

kind of business for each plant, store, of location during the 2007 Economic Census. To control for

response bias, three report forms are re-mailed to employer �rms and two report forms are re-mailed

to nonemployer �rms at one month intervals to all delinquent respondents. We use the data between

2002 and 2007 for our results.

Publicly-held �rms are not excluded in initial data. Records for states with under 100,000 weighted

8

businesses are combined with records of similar states: Alaska and Wyoming are combined together,

as are Delaware and District of Columbia, North and South Dakota, and Rhode Island and Vermont.

For our purposes, we exclude all combined states. Finally, the survey data includes weights which are

used in our regression analysis.

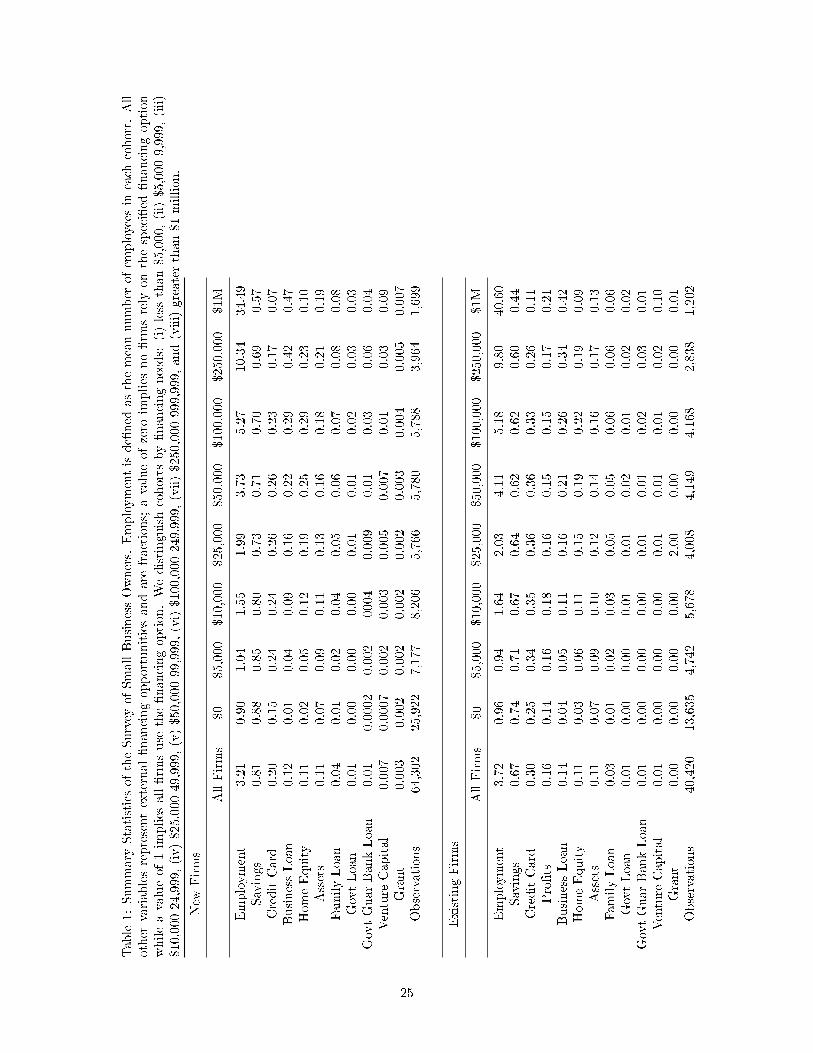

We �rst note the magnitude of our sample at 949,169 �rms according to Table 1. Employment is

the mean number of employees per �rm, while all remaining variables are the percentage of �rms that

rely on the speci�ed external �nancing option.

In our summary statistics we distinguish cohorts by the level of initial received �nancing: (i)

less than $5,000, (ii) $5,000-9,999, (iii) $10,000-24,999, (iv) $25,000-49,999, (v) $50,000-99,999, (vi)

$100,000-249,999, (vii) $250,000-999,999, and (viii) greater than $1 million. In addition note that we

have nearly 40,000 �rms with �nancing needs of at least one million dollars on creation. Therefore our

sample covers a wide range of start-ups during the 2002-2007 period.

To give some indication we use survey weights to determine the actual proportion in the economy:

(i) less than $5,000 make up 51% of �rms (ii) $5,000-9,999 compose 12%, (iii) $10,000-24,999 represent

12%, (iv) $25,000-49,999 are 8% of the economy, (v) $50,000-99,999 are 7%, (vi) $100,000-249,999 are

6%, (vii) $250,000-999,999 compose 4% of all �rms, and (viii) greater than $1 million represent 1% of

initial businesses. Therefore, the larger �rms are actually overrepresented in our survey compared to

the true population.

New Firm Financing

From 1 we �nd that the mean �rm has 5.1 employees and over half of the �rms in our sample are

nonemployer �rms. Employment in the �rst cohort (�nancing under $5,000) is only 0.9 and increases

monotonically to 34.5 employees in the largest cohort (�nancing at least $1 million).

We consider a range of �nancial sources: owner equity (denoted here as savings and assets), house-

hold credit cards, formal business loans, home equity loans, informal debt (denoted here as family

loans), government-assisted debt (both government loans and government guaranteed loans), venture

capital, and grants.

We �nd strong evidence that larger �rms are more likely to rely on formal business loans. For

9

instance 81 percent of all �rms in the sample rely on some sort of savings and this value is largest for

the smallest cohort (88%) and declines with �rm �nancing needs to 57%. In comparison, 12% of �rms

take a business loan and this value is largely driven by the largest �rms. While only 1% of the smallest

�rms require a formal business loan, 47% of �rms with at least one million dollars in initial funding

take a loan.

In line with Robb and Robinson [2012] we �nd little evidence of family loans even among the

smallest �rms: 4% of our �rms rely on family loans in any way. If anything, family loans actually

increase with the size of the �rm: only 1% of �rms in our smallest cohort receive family loans, yet

among �rms with at least $250,000 in initial �nancing, the level increases to eight percent. Instead of

family loans, small �rms in our sample tend to depend on savings and credit cards. About one-quarter

of �rms with $5,000-$100,000 use credit cards in their initial �nancing.

In comparison, home equity is a source of �nancing for 11% of all �rms. The value increases to

29% for �rms with �nancing needs of $100,000-249,999 before declining for the very largest �rms.

Additionally, home equity has increased as a source of �nancing over the housing cycle. In unreported

results we �nd that 6% of small �rms were initially �nanced through home equity before 1980; the

number increases to 7% during 1980-1989, 7% during 1990-1999, and 9% from 2000-2002.We take this

as initial evidence that the collateral channel may indeed be an important source of employment during

house price booms.

Government loans and government-guaranteed loans are a less common source of debt, together

making up about 2% of �nancing in the sample. These loans are more common for larger �rms with

higher �nancing needs, composing 3% and 6% of �nancing for �rms with �nancing over $250,000.

Finally, venture capital are only common for �rms with over one million in initial �nancing (at 10%

of these �rms), while grants compose less than one percent of the sample.

Overall, the results suggest a clear role for formal debt �nancing channels among entrepreneurs.

Small �rms use household credit cards, medium �rms rely more on home equity �nancing, and the

largest �rms use o�cial business loans to start the company. Other family loans, and government

loans are relatively uncommon accept at the largest �rms.

10

These results may help understand the di�erence between our speci�cation and Adelino et al. [2013].

These authors argue that small �rms (de�ned as 1-9 employees) borrow against residential real estate

while larger establishments have access to other forms of �nancing and should be less a�ected by the

collateral channel. We �nd some evidence form this interpretation as larger �rms depend more heavily

on formal bank debt and less on home equity. However, more accurately, the smallest �rms appear

largely self-reliant on personal savings, personal assets, and consumer credit cards. This con�rms our

empirical methodology.

Existing Firms

In Panel B of Table 1 we test how �nancing decisions change as the �rms mature. According to

our data 63% of all �rms in our sample require expansion capital at some point after the establishment

�rst opens. The percentages are similar to our results on initial �nancing with two exceptions. First,

entrepreneurs are now able to �nance �rm expansions through pro�ts and sixteen percent choose to

follow this strategy. Secondly, credit cards are more common among subsequent �nancing at a level of

30% compared to 20%.

Next, we consider the source of capital after �rm establishment: �rms are just as likely to rely

on home equity later in the lifecycle. Conditional on receiving additional capital, eleven percent of

�rms use home equity �nancing. The number raises to twenty-two percent among �rms with $100,000-

$250,000 in start-up capital. In our sample we also �nd that �rms that initially raise capital through

home equity are likely to return to home equity loans later in the life cycle: the correlation between

these two decisions is over 50%.

Home Equity by Firm Type

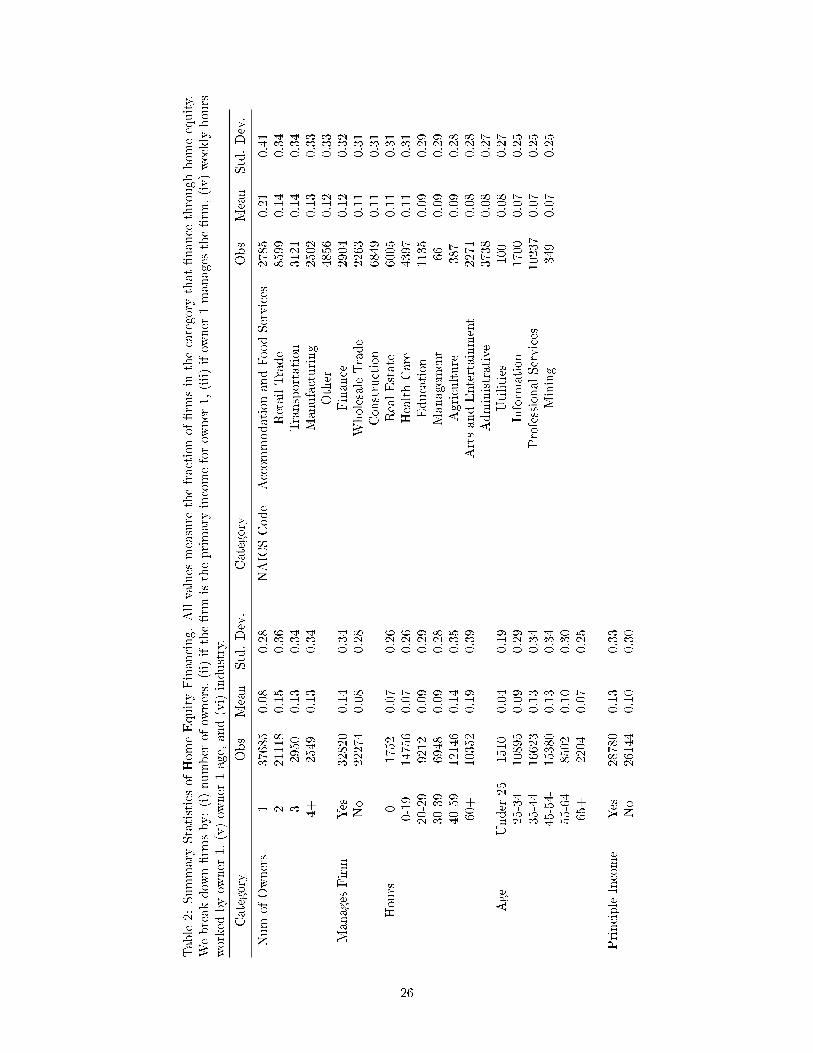

We now summarize �rm and �rm owner characteristics by source of �nancing in Table 2. We �nd

home equity �nancing is most common among (i) �rms with involved owners, (ii) owners in middle-age,

and (iii) in the service sector.

By far, the majority of �rms in our sample are single owner �rms (58%), yet only eight percent

rely on home equity. In comparison two owner �rms account for 32% of the sample and �fteen percent

have home equity loans.

11

Not surprisingly, dependency on the �rm is associated with higher rates of home equity. The �rm

is more likely to �nance through home equity if the �rm is her principle source of income (13% vs.

10%) and if the owner is also the manager (14% vs. 10%). In addition, time at the �rm is strongly

correlated with home equity. If the owner spends less than 20 hours a week at the �rm, then there

is only a 7% probability she �nances through home equity. Instead, 19% of all �rms with 60+ owner

work weeks �nance through home equity.

As expected, home equity also increases with the likelihood of home ownership as evidenced when

we break �rms down by owner age. Only four percent of owners under 25 years of age borrow from

their home compared to 13% of owners 35-54. The e�ect then declines after 55 years of age.

Next, in Table 2 we classify �rms according to a number of categories to determine the scope of our

data and document the prominence of home equity �nancing. We �nd our sample is predominantly

focused on professional service (19%), retail trade (16%), construction (12%), and real estate (11%).

In comparison, industries such as management, utilities, mining, and agriculture together make up less

than two percent of the sample.

We �nd that home equity �nancing is particularly common- 21% to be exact- among �rms in the

accommodation and food services sector. The e�ect is followed by retail trade and transportation

at a substantially smaller 14%. On the other side of the spectrum, we �nd that among the mining,

professional services, and information sectors only 7% of �rms rely on home equity �nancing.

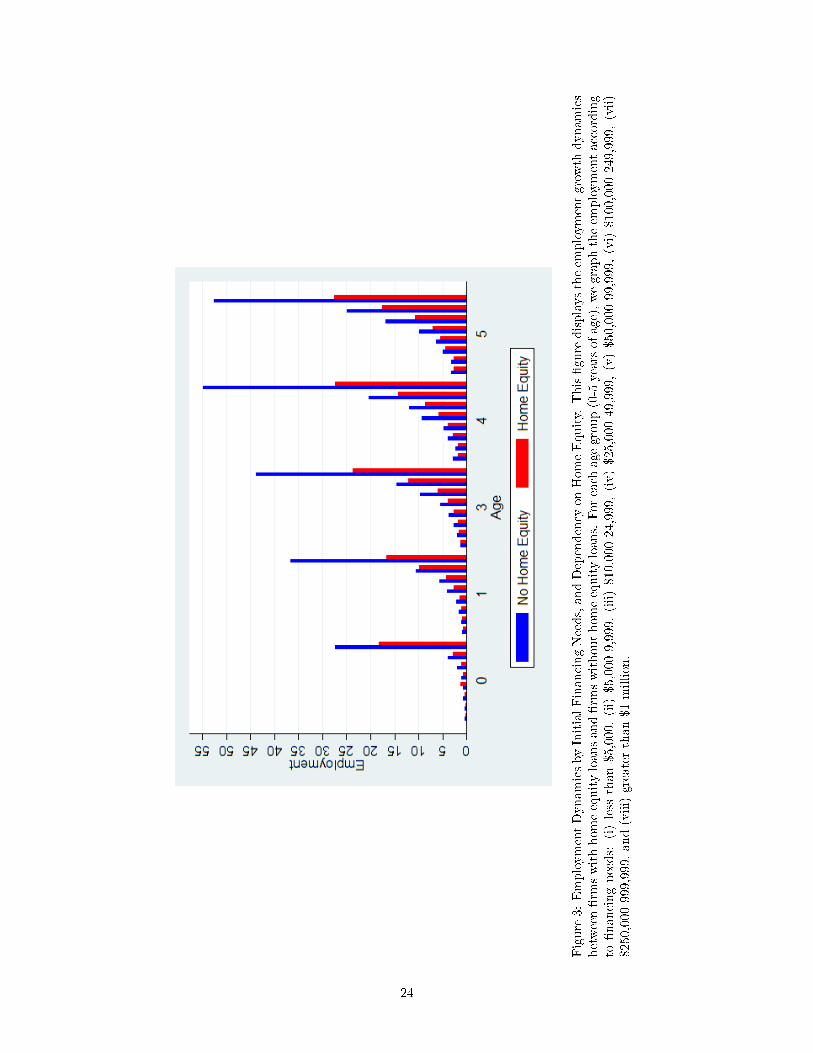

Firm Growth Dynamics

Finally, we document the employment growth dynamics of �rms with home equity �nancing in

Figure 3. To summarize the data, we include data from 2002-2007. Since the survey is conducted in

2007, we de�ne �rms established in 2007 as �rms with 0 year, �rms established in 2006 as �rms of age

one, etc. As before, we again separate �rms according to initial �nancing needs.

Initial employment is under �ve for all but the most �nance-heavy �rms (which start with nearly

twenty-�ve employees). As expected �rm employment is generally increasing both with age and with

initial �nancing needs. The more unique feature of the graph is that in thirty-nine of the forty cases,

employment is always greater in �rms that did not �nance through home equity. For �rms with low

12

�nancing needs, this e�ect is small across all ages. However, for �nance-heavy �rms, mean employment

of home-equity entrepreneurs is half the employment of �rms �nanced through alternative means.

Of course, home equity �nancing is an endogenous choice and therefore we cannot make any causal

statement linking home equity �nancing and future employment growth. To determine if home equity

loans help facilitate formal lending channels we now move to our results.

3 Results

Using our empirical speci�cation, together with the data sources discussed above, we now determine

if new �rm capital structure is driven by real estate price growth. We o�er signi�cant evidence that

a house price shock on new �rms increases home equity lending. The e�ects are greatest for �rms

with high �nancing needs. Lastly, in response to a price shock, entrepreneurs rely less on alternative

sources of �nancing, namely bank loans, family loans, and owner assets. We conclude by discussing

the policy implications of the analysis.

3.1 Estimation

Home Equity Financing

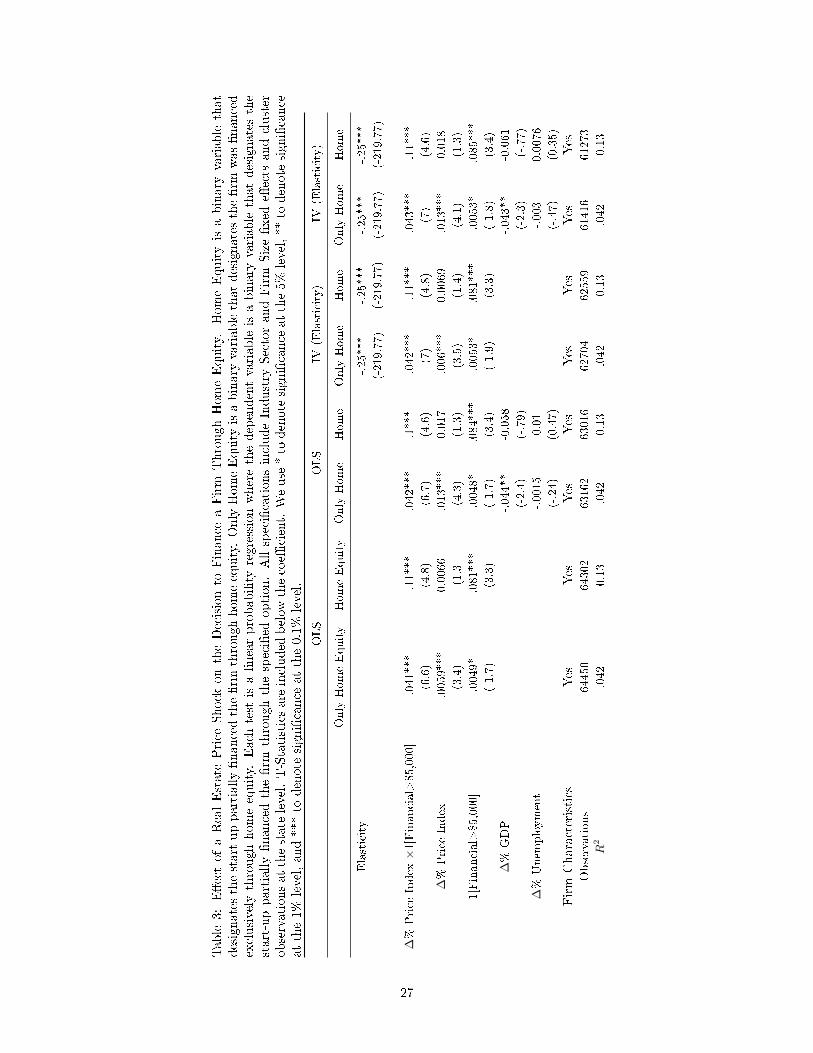

We document that local house price returns over the previous years are highly correlated with

home equity �nancing in Table 3. In our OLS regression, we �nd that a 100% increase in house prices

increases home equity by 11% among all �rms. In addition after including the local demand controls

of GDP growth and unemployment growth, the result still holds. Finally, we also estimate that a

100% increase in price results in a 4% increase in the probability a �rm �nances exclusively with home

equity.

As we have discussed, real estate price growth and �rm �nancing are likely correlated through

time-varying local demand; if GDP and unemployment are not valid proxies of local demand shocks

then this e�ect may be driving the results. Therefore, we redo the analysis by instrumenting for

exogenous real estate price growth using housing supply elasticity, and again the results hold. We note

that controlling for the state has no e�ect on our estimates given the original di�-in-di� structure. All

13

future results will depend on the instrumental variable unless otherwise mentioned.

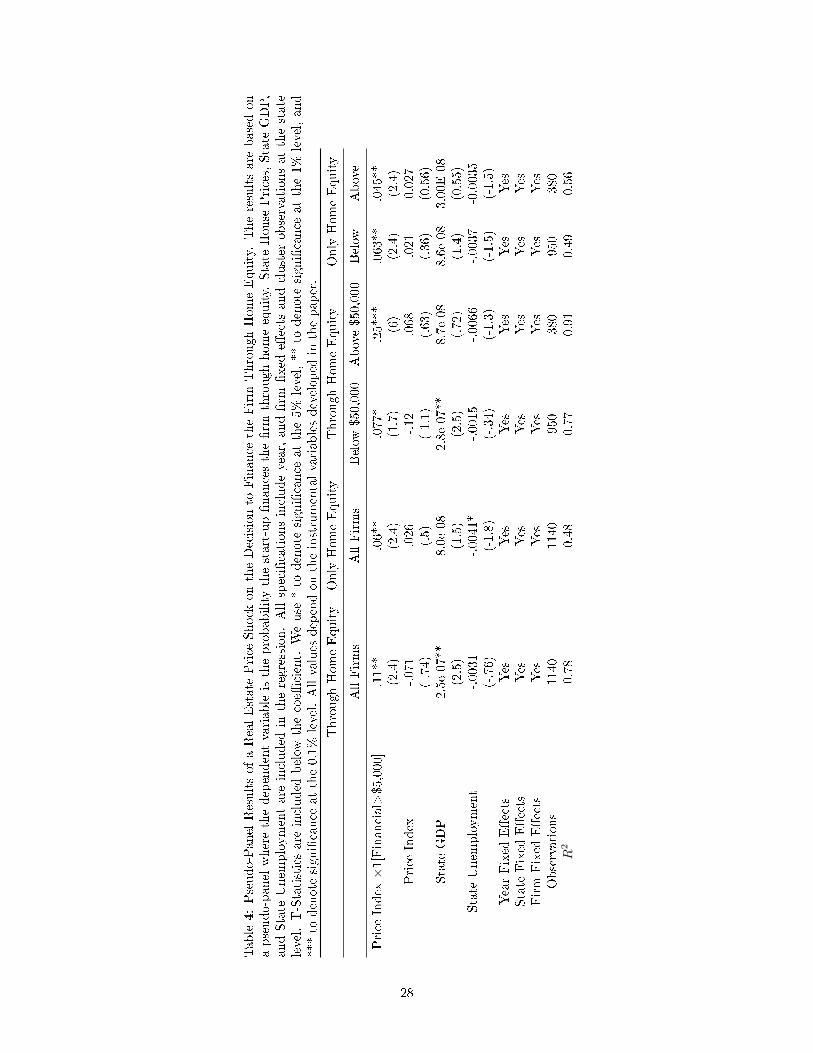

One concern with this analysis is our lack of panel-level data, suggesting unobservable �rm �xed

e�ects might be driving the results. To overcome the concern we develop a pseudo-�rm for each state

and �nancing cohort, and then complete our analysis again in a panel regression structure1.

The holds are similar to the cross-sectional estimates as illustrated in Table 4. Increasing house

prices by 10% results in an 11% increase in home equity �nancing and a 6% increase in the chance of

�nancing entirely through home equity.

For perspective we estimate that real estate price growth between 2000 and 2006 is responsible

for a 6.3% increase in home-equity �nancing. Further, for states in the top 10% of real estate price

growth this e�ect escalates to 14%. Note, however, that our results are only an underestimate of the

true channel since we estimate the e�ect relative to �rms with minimal �nancing needs. Since these

�rms too borrow against home equity, we are understating the signi�cance of this channel.

Due to data limitations, it is slightly more di�cult to estimate the aggregate monetary increase of

home equity loans for two reasons. First, we only know whether a �rm drew on a home equity loan, not

the amount. To overcome this issue, we assume that the number of home equity loans is proportional

to the total amount of home equity �nancing; therefore if 10% of �rms depend on a home equity

loan then we assume that 10% increase of total �nancing is through this funding channel. We believe

this is actually an understatement of the true e�ect since home equity is a formal �nancing channel

when compared to family loans or credit cards. Secondly, we do not have data on the exact level of

�nancing for each �rm. Therefore as a lower bound, we assume that �rm �nancing in each cohort is

at the lower bound of the �nancing cohort; this again is an underestimate since we are substantially

under-weighting the larger �rms that are most dependent on home equity loans.

We �nd that 2000-2006 real estate price growth resulted in at least a 9% increase in the total

amount of home equity �nancing among entrepreneurs. In addition, for areas in the top 10% of house

price growth this number reaches over nineteen percent during this same period. The results highlight

the signi�cance of the home equity channel among new �rms.

1We note that due to data limitations, we identify all �rms with over $50,000 in initial �nancing in the same state asa cohort..

14

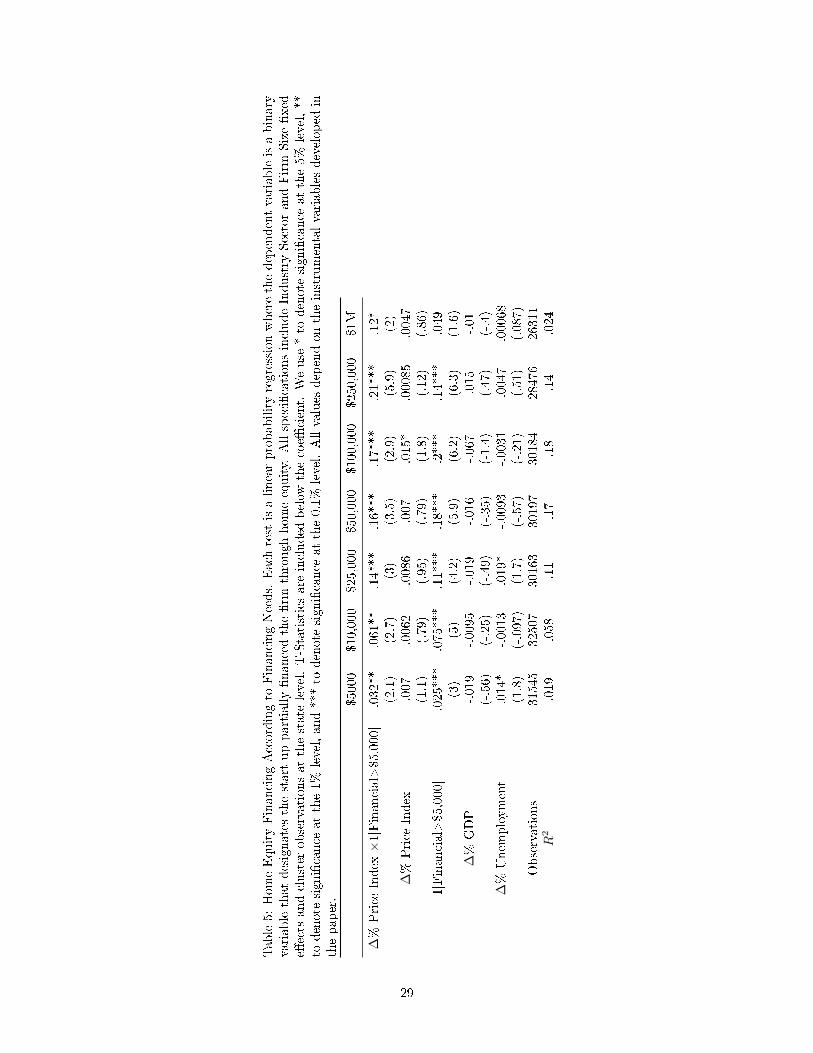

Financing Needs

In Table 5 we also check how �rm characteristics a�ects our results by completing our analysis

for each �nancing cohort. We discover that the home equity channel is greatest for �nancing needs

between $25,000 and $1 million. The e�ect actually declines slightly with the very largest �rms, which

is not surprising given that only 10% of these new businesses relied on home equity.

We �nd that a 10% increase in house prices results in a 2.1% increase in home equity �nancing

for �rms that receive between a quarter million and a million in initial funds. We redo our analysis

using the panel data and �nd only larger estimates. Again, to understand the implications, the result

suggest that 1999-2006 house price growth increased home equity �nancing by 12% in the US and up

to 27% for particularly inelastic states.

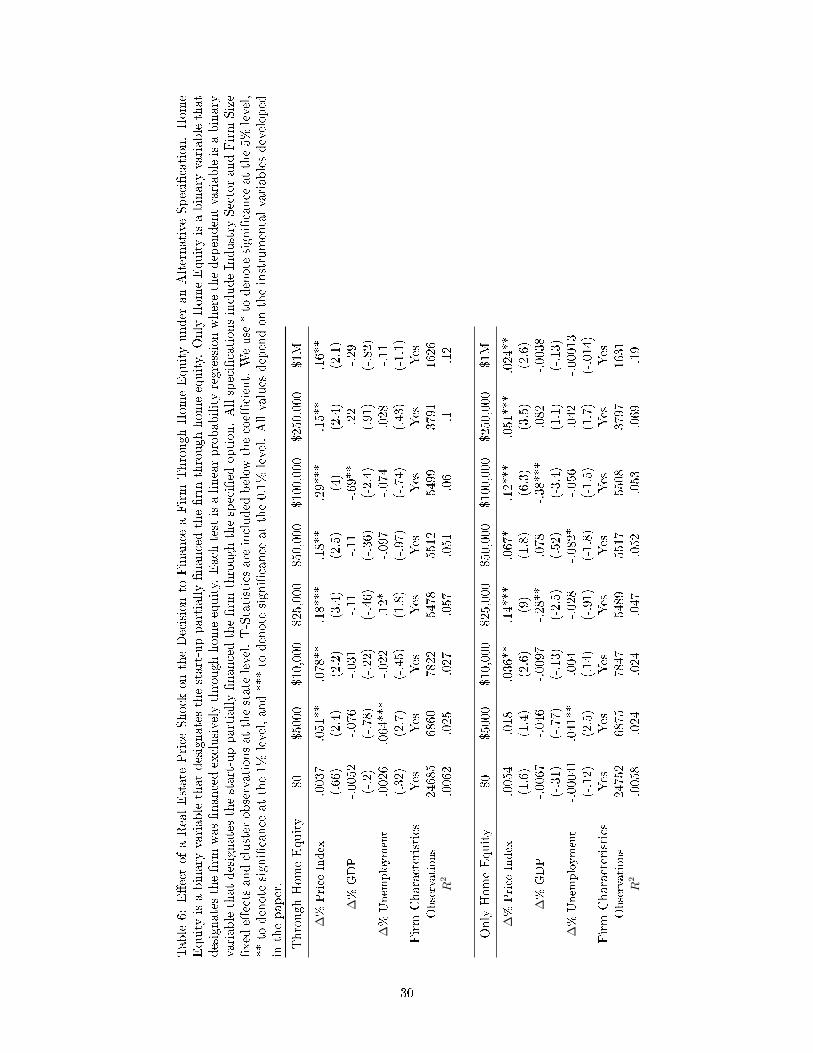

In Table 6 we simplify the analysis and compare price e�ects on �rms with the same �nancing

needs, but in di�erent states. The advantage of this framework is that we can explicitly compare �rms

with the same �nancing needs, yet subject to heterogeneous price shocks. The disadvantage is that we

can no longer compare �rms subject to the same local demand conditions. Therefore we rely especially

on our instrumental variable and local demand controls of GDP and unemployment.

We estimate that a ten percent increase in real estate value results in a three percent increase

in home equity �nancing for �rms requiring $100,000-$250,000, and a two percent increase for �rms

requiring $25,000-$100,000. The results are similar, though quantitatively smaller, when we consider

exclusively home equity �nancing.

Alternative Financing

After clearly establishing the e�ect of real estate shocks on home equity, we next consider the

impact on alternative �nancing opportunities. The results imply that in response to house price shock,

�rms take home equity loans over more expensive forms of formal debt. In comparison, other forms

of �nancing such as credit cards and savings are only minimally a�ected by real estate shocks. As a

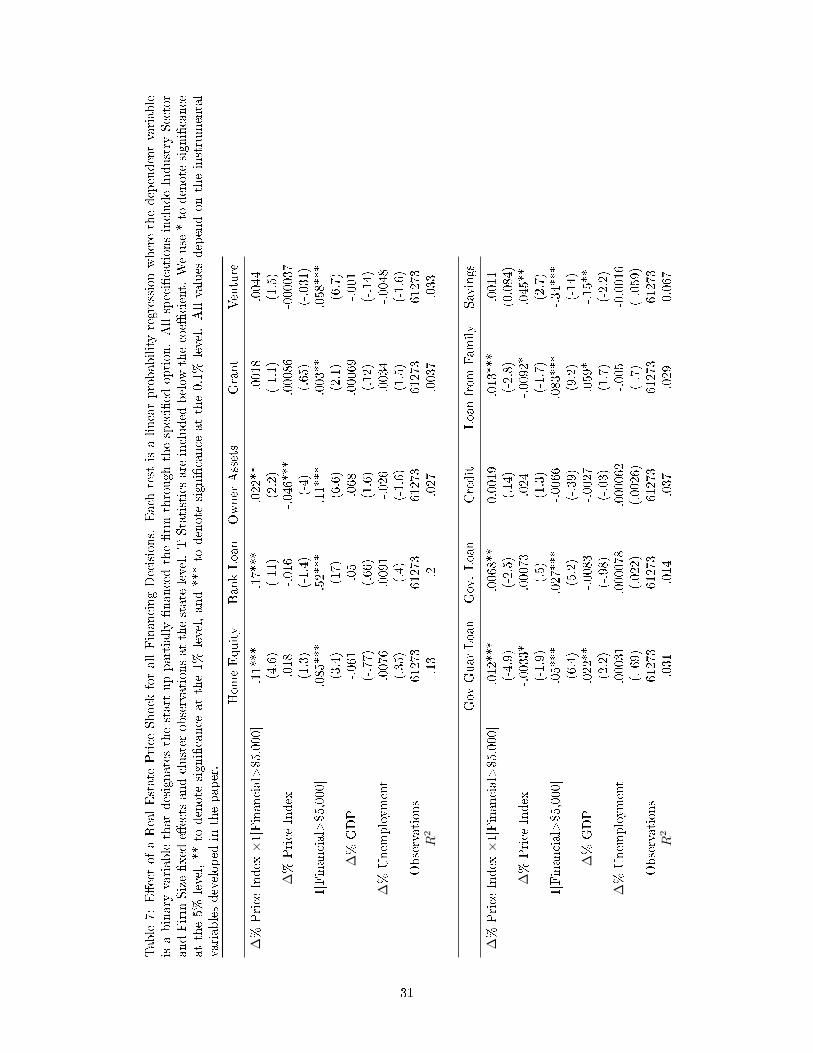

result, we see little e�ect on the total capital structure of the �rm. As shown in Table 7 bank loans

decline by 1.7% subject to a 10% decline in real estate prices, which more than o�sets the home equity

15

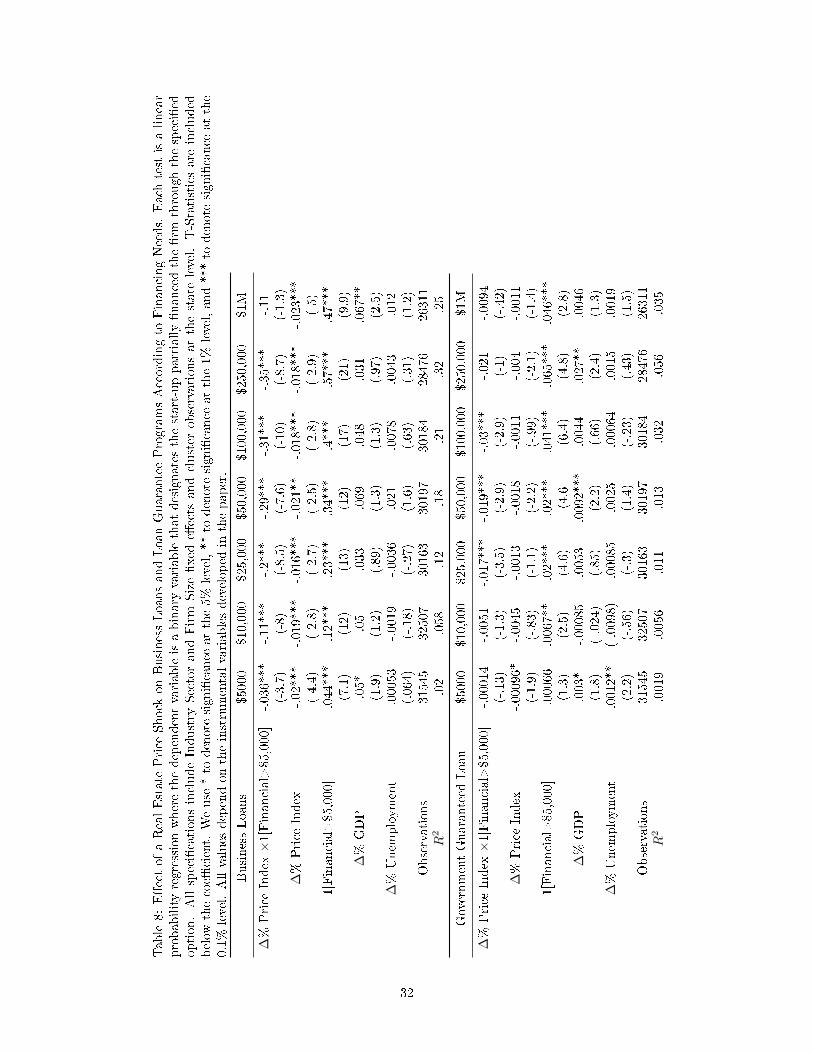

a�ect. To develop a better understanding of the mechanism, in the �rst Panel of Table 8 we sort by

�nancing needs. Subject to a real estate shock all business loans �nancing decreases regardless of �rm

type, but is largest for �rms in the $250,000-$1 million range at 3.5%.

Contrast these results to alternative lending markets: we estimate no signi�cant e�ect on credit

cards lending, even when we break the sample by �nancing needs. Next, a ten percent increase in house

prices results in a 0.13% decline in family loans. The e�ect is largest for �rms in the $25,000-$50,000

range at 0.38%. In unreported results, we �nd similar estimates from the pseudo-panel methodology.

One policy implication from this work is the role of governmental loan guarantee programs. Implic-

itly, these loans should have the greatest impact when the entrepreneur has limited access to collateral,

such as when house prices are low2. Alternatively, if loan guarantee programs are una�ected by hous-

ing shocks, then entrepreneurs are either unable or uninterested to access the support exactly when it

is most valuable.

Our analysis supports the intuition that real estate price are negatively correlated with loan guar-

antee �nancing. According to Table 8 doubling house prices decreases the number of new guaranteed

loans by 1.2%. This number di�ers signi�cantly by the �nancing needs of the �rm: for �rms that

require $100,000-$250,000 in funding, this same house price shock decreases the loan quantity by three

percent.

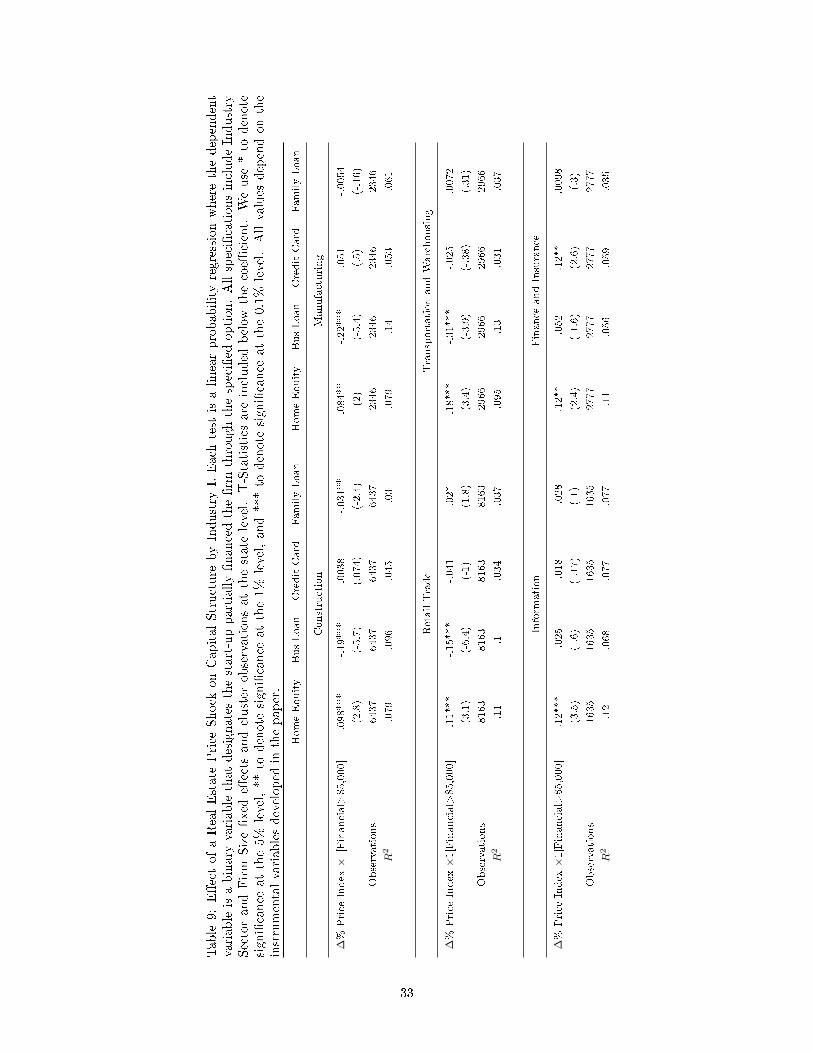

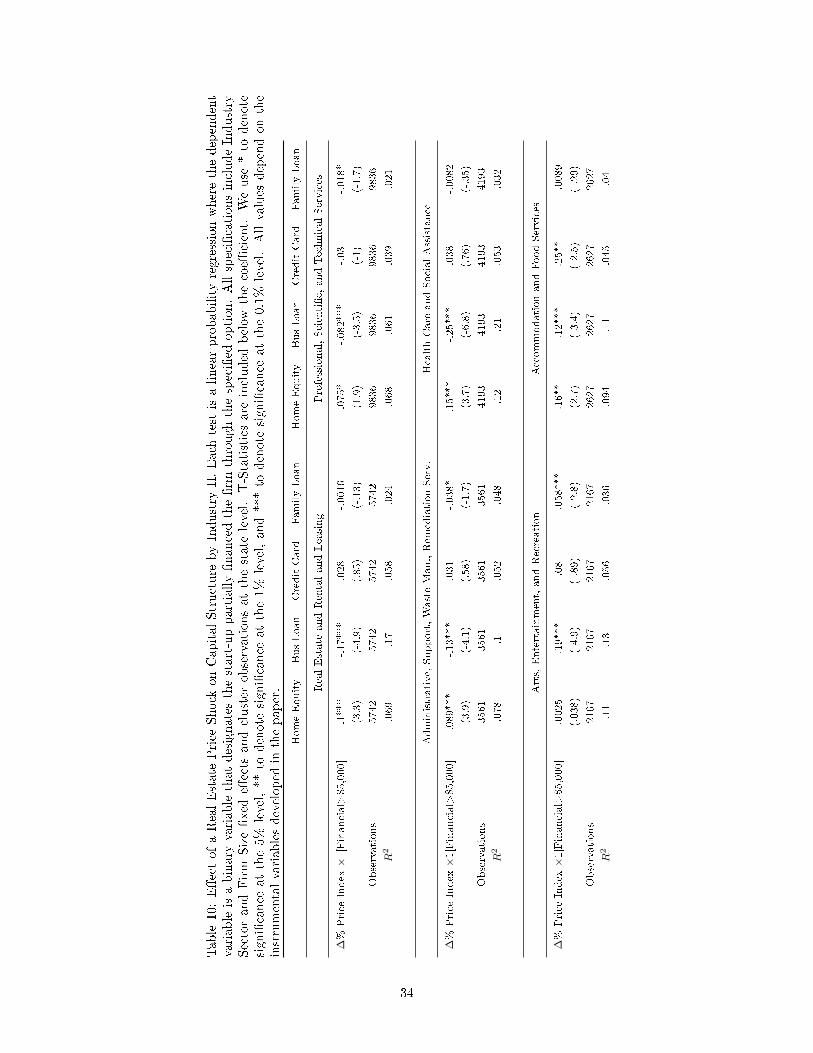

Industry E�ects

Previous research suggest that industry could potentially drive capital structure decisions. First, pre-

vious research has found signi�cant variation in asset redeployability at the industry level: industries

with redeployable assets may be able secure debt with non-housing collateral Campello [2014], Ben-

melech et al. [2005]. Secondly, certain industries may be more dependent on external �nanceRajan

[1998]. Third, Hurst and Pugsley [2011] �nd that most small �rms have no desire to grow large or

innovate and this is especially true for skilled craftsmen, lawyers, real estate agents, doctors, small

shopkeepers, and restaurant owners.

In Table 9 we separate �rms for the twelve largest industries in our data set and �nd a clear e�ect

2Lelarge et al. [2010] conducts a similar test using a quasi-experiment in a French Loan Guarantee Program

16

of house prices on home equity �nancing for all but the arts/entertainment industry. The home equity

channel is largest for transportation, accommodation and food services, and health care. However, for

ten of the twelve industries we note a comparable decline in business loans �nancing: just as before

we note the largest e�ect for transportation and health care.

There is some evidence that small �rms tilt away from family loans subject to collateral shocks in

the following industries: (i) construction, (ii) administrative and support, and (iii) arts, entertainment,

and recreation. Lastly, we �nd that home prices negatively impact credit card �nancing in only one

industry, food and accommodation services.

Evidence during the Crisis Years

Our analysis suggest that positive house prices impact new �rm capital structure mainly through an

increase in home equity �nancing and a decrease in other bank loans. These �ndings naturally lead us

to the next question: how do the results compare to years following the housing bust3? Unfortunately,

we are not able to answer the question in this framework due to data limitations. Instead we consider

indirect evidence based on aggregate data.

To understand the relative role of collateral following the Financial Crisis we break the ratio of

Noncorporate Debt-to-GDP into three subgroups: (i) long-term debt (over one year), (ii) short-term

depository bank loans (less than one year), and (iii) short-term nondepository bank loans (including

government loans, loans from other �nancial institutions, and agricultural loans). Previous evidence

from Berger and Udell [1990] �nds that 70% of all commercial and industrial long-term debt and 30-

40% of short-term loans in the United States are secured by collateral assets. More recent estimates

by Kleiner [2014] �nd even larger numbers for private �rms at 88% for long-term debt and 46% for

short-term debt. Therefore, collateral values should impact both forms of debt, though long-term

contracts in particular.

As of May 2014, long-term debt composed 68.0% of total debt, compared to 27.4% and 4.6%

3The media has long suggested the importance of this question: �It is well known that the housing bust has taken adevastating toll on American families, nearly three million of which have lost their homes to foreclosure. Less known isthe impact that the housing collapse is having on owners of small businesses, which have often relied upon home-equityborrowing to �nance the early stages of growth and development.�-Wall Street Journal, Whelan [2012]

17

for depository loans and non-depository loans, respectively. As previously noted, the debt of US

noncorporate �rms (sole proprietorships and limited partnerships) grew faster than both household

debt and corporate debt during 1997-2009 as shown in Figure 1; then following the Financial Crisis

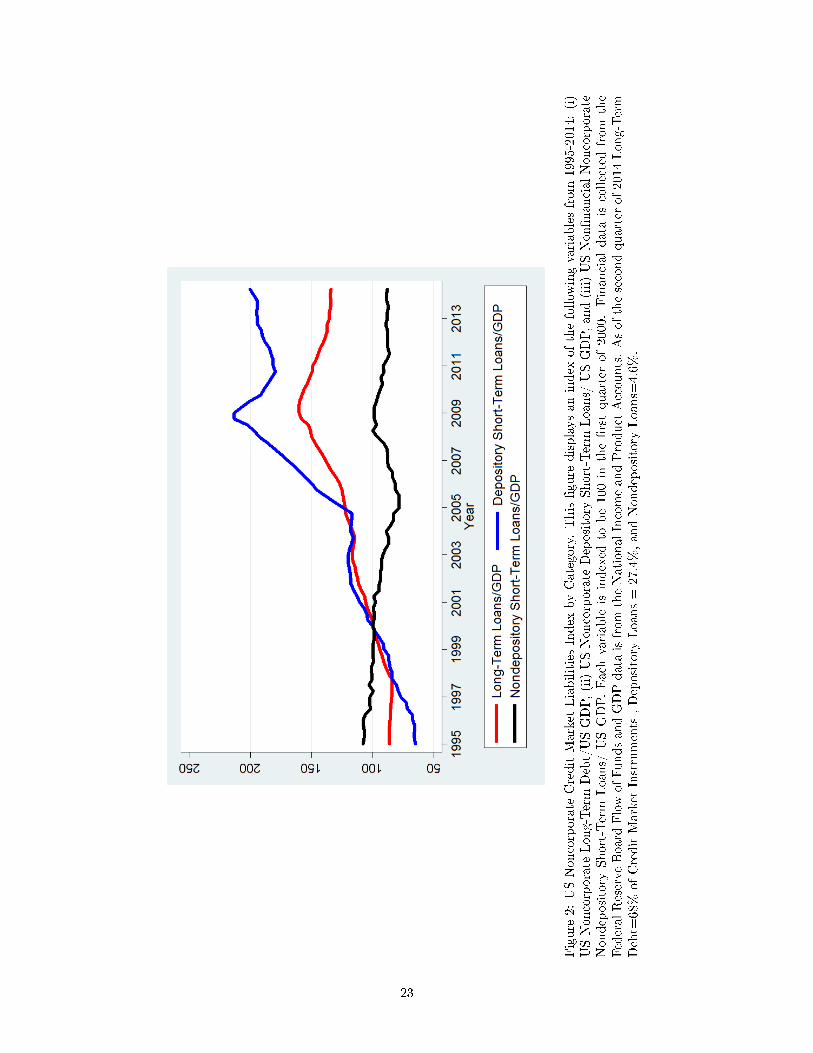

Noncorporate Debt-to-GDP fell 14%. Similarly, in Figure 2 we �nd that long-term debt grew through

2008 before declining till the end of the data sample in 2014. There is then no evidence that secured

debt recovered following the Financial Crisis.

So could small �rms easily switch to short-term debt markets? We �nd that depository loans fell

16% between the end of 2008 and start of 2011, suggesting a contraction in the short-term lending

market. Only in 2011 did short-term lending increase, potentially alleviating the e�ect of low collateral

values on small �rm �nancing4. The result suggests that beginning in 2011 new �rm capital structure

shifted towards short-term lending and away from long-term debt. While this may be due to sluggish

growth in the housing sector, we are not able to con�rm the hypothesis in our current framework.

4 Conclusion

This purpose of this paper is to understand the relationship between real estate prices and new �rm

capital structure. We �rst summarize the range of home equity �nancing among both �rm and owner

characteristics using new US data from the Census Survey of Business Owners. We then evaluated how

real estate shocks impact capital structure in all �rms relative to businesses with minimal �nancing

needs.

According to our analysis home equity is a source of �nancing for about 15% of large start-ups

(those that received at least $50,000 in initial funding). Secondly, a house price shock does indeed

impact �nancing: in our preferred speci�cation we �nd that a 10% increase in real estate price growth

is responsible for an 1.1% increase in home equity �nancing. Surprisingly, �rms tilt �nancing away

from bank loans, yet there is little e�ect on consumer credit cards and family loans.

4Of course these results could be driven by a decline in credit demand, not credit supply. However, according to theKau�man Firm Survey we �nd that denial rate of loans increased during the crisis years between 2007 and 2009. In2007 10.4% of all entrepreneurs were denied all loan applications. This value increased to 15% in 2008 and 19% in 2009.In addition in 2007 15.4% of entrepreneurs did not apply for loans because they would be denied, compared to 17.6% in2008 and 19.4% in 2009.

18

Aggregate data following the Financial Crisis suggests the continued role of real estate prices

in explaining current new �rm capital structure decisions. In future work we plan to extend our

analysis, focusing speci�cally on the secured debt of small �rms during the Financial Crisis. Despite

the continued interest in this area of study, many questions remain to be answered.

19

References

Manuel Adelino, Antoinette Schoar, and Felipe Severino. House prices, collateral and self-employment.

Technical report, National Bureau of Economic Research, 2013.

Efraim Benmelech, Mark J Garmaise, and Tobias J Moskowitz. Do liquidation values a�ect �nancial

contracts? evidence from commercial loan contracts and zoning regulation. The Quarterly Journal

of Economics, 120(3):1121�1154, 2005.

Allen N Berger and Gregory F Udell. Collateral, loan quality and bank risk. Journal of Monetary

Economics, 25(1):21�42, 1990.

Marco Cagetti and Mariacristina De Nardi. Entrepreneurship, frictions, and wealth. Journal of political

Economy, 114(5):835�870, 2006.

Murillo Campello. Capital structure and the redeployability of tangible assets. Econometrica, 82(2):

705�30, 2014.

Thomas Chaney, David Sraer, and David Thesmar. The collateral channel: How real estate shocks

a�ect corporate investment. The American Economic Review, 102(6):2381�2409, 2012.

Stefano Corradin and Alexander Popov. House prices, home equity borrowing, and entrepreneurship*.

Review of Financial Studies, page hhv020, 2015.

Dragana Cvijanovic. Real estate prices and �rm capital structure. UNC Kenan-Flagler Research

Paper, (2013-13), 2014.

Angus Deaton. Panel data from time series of cross-sections. Journal of econometrics, 30(1):109�126,

1985.

David S Evans and Boyan Jovanovic. An estimated model of entrepreneurial choice under liquidity

constraints. The Journal of Political Economy, pages 808�827, 1989.

Oliver Hart and John Moore. Debt and seniority: An analysis of the role of hard claims in constraining

management. The American Economic Review, 85(3):567�585, 1995.

20

Erik Hurst and Annamaria Lusardi. Liquidity constraints, household wealth, and entrepreneurship.

Journal of political Economy, 112(2):319�347, 2004.

Erik Hurst and Benjamin Wild Pugsley. What do small businesses do? Brookings Papers on Economic

Activity, 43(2 (Fall)):73�142, 2011.

Kristoph Kleiner. How real estate drives the economy: An investigation of small �rm collateral shocks

on employment. 2014.

Claire Lelarge, David Sraer, and David Thesmar. Entrepreneurship and credit constraints: Evidence

from a french loan guarantee program. In International di�erences in entrepreneurship, pages 243�

273. University of Chicago Press, 2010.

Atif Mian and Amir Su�. House prices, home equity-based borrowing, and the us household leverage

crisis. American Economic Review, 101(5):2132�56, 2011.

Atif Mian, Kamalesh Rao, and Amir Su�. Household balance sheets, consumption, and the economic

slump*. The Quarterly Journal of Economics, 128(4):1687�1726, 2013.

Raghuram Rajan. Financial dependence and growth. The American Economic Review, 88(3):559�586,

1998.

Alicia M Robb and David T Robinson. The capital structure decisions of new �rms. Review of

Financial Studies, page hhs072, 2012.

Albert Saiz. The geographic determinants of housing supply. The Quarterly Journal of Economics,

125(3):1253�1296, 2010.

Martin C Schmalz, David A Sraer, and David Thesmar. Housing collateral and entrepreneurship. 2013.

Robbie Whelan. When the home bank closes. Wall Street Journal. Midwest Edition, 2012.

21

Figure

1:USCreditMarket

LiabilitiesIndex.This�gure

displaysanindex

ofthefollow

ingvariablesfrom

1995-2013:(i)USHousehold

andNonpro�t

OrganizationCreditMarket

InstrumentLiabilities/USGDP,(ii)USNon�nancialNoncorporate

BusinessCreditMarket

InstrumentLiabilities/

US

GDP,and(iii)U

SNon�nancialCorporate

BusinessCreditMarket/USGDP.Each

variableisindexed

tobe100in

the�rstquarter

of2000.Financial

data

iscollectedfrom

theFederalReserveBoard

FlowofFundsandGDPdata

isfrom

theNationalIncomeandProduct

Accounts.Asofthe�rst

quarter

of2013Household

Liabilities/GDP=

0.77,

Corporate

Liabilities/GDP=

0.54,andNoncorporate

Liabilitieswere0.24.In

comparisonin

the

�rstquarter

of2009,thesenumber

wereHousehold

Liabilities=0.94,andCorporate

Liabilities=

0.52,andNoncorporate

Liabilities/GDP=

0.28,.

22

Figure

2:USNoncorporate

CreditMarket

LiabilitiesIndex

byCategory.This�gure

displaysanindex

ofthefollow

ingvariablesfrom

1995-2014:(i)

USNoncorporate

Long-Term

Debt/USGDP,(ii)USNoncorporate

Depository

Short-Term

Loans/

USGDP,and(iii)USNon�nancialNoncorporate

Nondepository

Short-Term

Loans/

USGDP.Each

variable

isindexed

tobe100in

the�rstquarter

of2000.Financialdata

iscollectedfrom

the

FederalReserve

Board

FlowofFundsandGDPdata

isfrom

theNationalIncomeandProduct

Accounts.Asofthesecondquarter

of2014Long-Term

Debt=

68%

ofCreditMarket

Instruments

,Depository

Loans=

27.4%,andNondepository

Loans=

4.6%.

23

Figure

3:EmploymentDynamicsbyInitialFinancingNeeds,andDependency

onHomeEquity.

This�gure

displaystheem

ploymentgrowth

dynamics

between�rm

swithhomeequityloansand�rm

swithouthomeequityloans.Foreach

agegroup(0-5

yearsofage),wegraphtheem

ploymentaccording

to�nancingneeds:

(i)less

than$5,000,(ii)$5,000-9,999,(iii)$10,000-24,999,(iv)$25,000-49,999,(v)$50,000-99,999,(vi)$100,000-249,999,(vii)

$250,000-999,999,and(viii)greaterthan$1million.

24

Table1:Summary

StatisticsoftheSurvey

ofSmallBusinessOwners.

Employmentisde�ned

asthemeannumber

ofem

ployees

ineach

cohort.All

other

variablesrepresentexternal�nancingopportunitiesandare

fractions;

avalueofzero

implies

no�rm

srely

onthespeci�ed

�nancingoption

whileavalueof1im

plies

all�rm

suse

the�nancingoption.Wedistinguishcohortsby�nancingneeds:

(i)less

than$5,000,(ii)$5,000-9,999,(iii)

$10,000-24,999,(iv)$25,000-49,999,(v)$50,000-99,999,(vi)$100,000-249,999,(vii)$250,000-999,999,and(viii)greaterthan$1million.

New

Firms

AllFirms

$0

$5,000

$10,000

$25,000

$50,000

$100,000

$250,000

$1M

Employment

3.21

0.90

1.04

1.55

1.99

3.73

5.27

10.34

34.49

Savings

0.81

0.88

0.85

0.80

0.73

0.71

0.70

0.69

0.57

CreditCard

0.20

0.15

0.24

0.24

0.26

0.26

0.23

0.17

0.07

BusinessLoan

0.12

0.01

0.04

0.09

0.16

0.22

0.29

0.42

0.47

HomeEquity

0.11

0.02

0.05

0.12

0.19

0.25

0.29

0.23

0.10

Assets

0.11

0.07

0.09

0.11

0.13

0.16

0.18

0.21

0.19

FamilyLoan

0.04

0.01

0.02

0.04

0.05

0.06

0.07

0.08

0.08

GovtLoan

0.01

0.00

0.00

0.00

0.01

0.01

0.02

0.03

0.03

GovtGuarBankLoan

0.01

0.0002

0.002

0004

0.009

0.01

0.03

0.06

0.04

Venture

Capital

0.007

0.0007

0.002

0.003

0.005

0.007

0.01

0.03

0.09

Grant

0.003

0.002

0.002

0.002

0.002

0.003

0.004

0.005

0.007

Observations

64,302

25,922

7,177

8,206

5,766

5,780

5,788

3,964

1,699

ExistingFirms

AllFirms

$0

$5,000

$10,000

$25,000

$50,000

$100,000

$250,000

$1M

Employment

3.72

0.96

0.94

1.64

2.03

4.11

5.18

9.80

40.60

Savings

0.67

0.74

0.71

0.67

0.64

0.62

0.62

0.60

0.44

CreditCard

0.30

0.25

0.34

0.35

0.36

0.36

0.33

0.26

0.11

Pro�ts

0.16

0.14

0.16

0.18

0.16

0.15

0.15

0.17

0.21

BusinessLoan

0.14

0.04

0.05

0.11

0.16

0.21

0.26

0.34

0.42

HomeEquity

0.11

0.03

0.06

0.11

0.15

0.19

0.22

0.19

0.09

Assets

0.11

0.07

0.09

0.10

0.12

0.14

0.16

0.17

0.13

FamilyLoan

0.03

0.01

0.02

0.03

0.05

0.05

0.06

0.06

0.06

GovtLoan

0.01

0.00

0.00

0.01

0.01

0.02

0.01

0.02

0.02

GovtGuarBankLoan

0.01

0.00

0.00

0.00

0.01

0.01

0.02

0.03

0.01

Venture

Capital

0.01

0.00

0.00

0.00

0.01

0.01

0.01

0.02

0.10

Grant

0.00

0.00

0.00

0.00

2.00

0.00

0.00

0.00

0.01

Observations

40,420

13,635

4,742

5,678

4,008

4,149

4,168

2,838

1,202

25

Table2:Summary

StatisticsofHomeEquityFinancing.Allvalues

measure

thefractionof�rm

sin

thecategory

that�nance

throughhomeequity.

Webreakdow

n�rm

sby:(i)number

ofow

ners,(ii)ifthe�rm

istheprimary

incomeforow

ner

1,(iii)ifow

ner

1manages

the�rm

,(iv)weekly

hours

worked

byow

ner

1,(v)ow

ner

1age,and(vi)industry.

Category

Obs

Mean

Std.Dev.

Category

Obs

Mean

Std.Dev.

Num

ofOwners

137685

0.08

0.28

NAICSCode

AccommodationandFoodServices

2785

0.21

0.41

221118

0.15

0.36

RetailTrade

8599

0.14

0.34

32950

0.13

0.34

Transportation

3121

0.14

0.34

4+

2549

0.13

0.34

Manufacturing

2502

0.13

0.33

Other

4856

0.12

0.33

Manages

Firm

Yes

32820

0.14

0.34

Finance

2904

0.12

0.32

No

22274

0.08

0.28

WholesaleTrade

2263

0.11

0.31

Construction

6849

0.11

0.31

Hours

01752

0.07

0.26

RealEstate

6005

0.11

0.31

0-19

14756

0.07

0.26

HealthCare

4397

0.11

0.31

20-29

9212

0.09

0.29

Education

1135

0.09

0.29

30-39

6948

0.09

0.28

Managem

ent

66

0.09

0.29

40-59

12146

0.14

0.35

Agriculture

387

0.09

0.28

60+

10352

0.19

0.39

ArtsandEntertainment

2271

0.08

0.28

Administrative

3738

0.08

0.27

Age

Under

25

1510

0.04

0.19

Utilities

100

0.08

0.27

25-34

10895

0.09

0.29

Inform

ation

1700

0.07

0.25

35-44

16623

0.13

0.34

ProfessionalServices

10237

0.07

0.25

45-54-

15380

0.13

0.34

Mining

349

0.07

0.25

55-64

8502

0.10

0.30

65+

2204

0.07

0.25

PrincipleIncome

Yes

28780

0.13

0.33

No

26144

0.10

0.30

26

Table

3:E�ectofaRealEstate

Price

Shock

ontheDecisionto

Finance

aFirm

ThroughHomeEquity.

HomeEquityisabinary

variable

that

designatesthestart-uppartially�nancedthe�rm

throughhomeequity.

Only

HomeEquityisabinary

variablethatdesignates

the�rm

was�nanced

exclusively

through

homeequity.

Eachtest

isalinearprobabilityregressionwherethedependentvariable

isabinary

variable

thatdesignatesthe

start-uppartially�nancedthe�rm

throughthespeci�ed

option.Allspeci�cationsincludeIndustry

SectorandFirm

Size�xed

e�ects

andcluster

observationsatthestate

level.T-Statisticsare

included

below

thecoe�

cient.Weuse

*to

denote

signi�cance

atthe5%

level,**to

denote

signi�cance

atthe1%

level,and***to

denote

signi�cance

atthe0.1%

level.

OLS

OLS

IV(Elasticity)

IV(Elasticity)

Only

HomeEquity

HomeEquity

Only

Home

Home

Only

Home

Home

Only

Home

Home

Elasticity

-.25***

-.25***

-.25***

-.25***

(-219.77)

(-219.77)

(-219.77)

(-219.77)

∆%

Price

Index

×1[Financial>$5,000]

.041***

.11***

.042***

.1***

.042***

.11***

.043***

.11***

(6.6)

(4.8)

(6.7)

(4.6)

(7)

(4.8)

(7)

(4.6)

∆%

Price

Index

.0059***

0.0066

.013***

0.017

.006***

0.0069

.013***

0.018

(3.4)

(1.3

(4.3)

(1.3)

(3.5)

(1.4)

(4.1)

(1.3)

1[Financial>$5,000]

-.0049*

.081***

-.0048*

.084***

-.0053*

.081***

-.0053*

.085***

(-1.7)

(3.3)

(-1.7)

(3.4)

(-1.9)

(3.3)

(-1.8)

(3.4)

∆%

GDP

-.044**

-0.058

-.043**

-0.061

(-2.4)

(-.79)

(-2.3)

(-.77)

∆%

Unem

ployment

-.0015

0.01

-.003

0.0076

(-.24)

(0.47)

(-.47)

(0.35)

Firm

Characteristics

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Observations

64450

64302

63162

63016

62704

62559

61416

61273

R2

.042

0.13

.042

0.13

.042

0.13

.042

0.13

27

Table4:Pseudo-PanelResultsofaRealEstate

Price

Shock

ontheDecisionto

Finance

theFirm

ThroughHomeEquity.

Theresultsare

basedon

apseudo-panelwherethedependentvariableistheprobabilitythestart-up�nancesthe�rm

throughhomeequity.

State

House

Prices,State

GDP,

andState

Unem

ploymentare

included

intheregression.Allspeci�cationsincludeyear,and�rm

�xed

e�ects

andcluster

observationsatthestate

level.T-Statisticsare

included

below

thecoe�

cient.

Weuse

*to

denote

signi�cance

atthe5%

level,**to

denote

signi�cance

atthe1%

level,and

***to

denote

signi�cance

atthe0.1%

level.Allvalues

dependontheinstrumentalvariablesdeveloped

inthepaper.

ThroughHomeEquity

Only

HomeEquity

ThroughHomeEquity

Only

HomeEquity

AllFirms

AllFirms

Below

$50,000

Above$50,000

Below

Above

Price

Index

×1[Financial>$5,000]

.11**

.06**

.077*

.25***

.063**

.045**

(2.4)

(2.4)

(1.7)

(6)

(2.4)

(2.4)

Price

Index

-.071

.026

-.12

.068

.021

0.027

(-.74)

(.5)

(-1.1)

(.63)

(.36)

(0.56)

State

GDP

2.5e-07**

8.0e-08

2.8e-07**

8.7e-08

8.6e-08

3.00E-08

(2.5)

(1.5)

(2.5)

(.72)

(1.4)

(0.55)

State

Unem

ployment

-.0031

-.0041*

-.0015

-.0066

-.0037

-0.0035

(-.76)

(-1.8)

(-.34)

(-1.3)

(-1.5)

(-1.5)

YearFixed

E�ects

Yes

Yes

Yes

Yes

Yes

Yes

State

Fixed

E�ects

Yes

Yes

Yes

Yes

Yes

Yes

Firm

Fixed

E�ects

Yes

Yes

Yes

Yes

Yes

Yes

Observations

1140

1140

950

380

950

380

R2

0.78

0.48

0.77

0.91

0.49

0.56

28

Table5:HomeEquityFinancingAccordingto

FinancingNeeds.

Each

test

isalinearprobabilityregressionwherethedependentvariableisabinary

variablethatdesignatesthestart-uppartially�nancedthe�rm

throughhomeequity.

Allspeci�cationsincludeIndustry

SectorandFirm

Size�xed

e�ects

andcluster

observationsatthestate

level.T-Statisticsare

included

below

thecoe�

cient.

Weuse

*to

denote

signi�cance

atthe5%

level,**

todenote

signi�cance

atthe1%

level,and***to

denote

signi�cance

atthe0.1%

level.Allvalues

dependontheinstrumentalvariablesdeveloped

inthepaper.

$5000

$10,000

$25,000

$50,000

$100,000

$250,000

$1M

∆%

Price

Index

×1[Financial>$5,000]

.032**

.061**

.14***

.16***

.17***

.21***

.12*

(2.1)

(2.7)

(3)

(3.5)

(2.9)

(5.9)

(2)

∆%

Price

Index

.007

.0062

.0086

.007

.015*

.00085

.0047

(1.1)

(.79)

(.95)

(.79)

(1.8)

(.12)

(.86)

1[Financial>$5,000]

.025***

.075***

.11***

.18***

.2***

.14***

.049

(3)

(5)

(4.2)

(5.9)

(6.2)

(6.3)

(1.6)

∆%

GDP

-.019

-.0095

-.019

-.016

-.067

.015

-.01

(-.56)

(-.25)

(-.49)

(-.35)

(-1.4)

(.47)

(-.4)

∆%

Unem

ployment

.014*

-.0013

.019*

-.0093

-.0031

.0047

.00068

(1.8)

(-.097)

(1.7)

(-.57)

(-.21)

(.51)

(.087)

Observations

31545

32507

30163

30197

30184

28476

26311

R2

.019

.058

.11

.17

.18

.14

.024

29

Table

6:E�ectofaRealEstate

Price

Shock

ontheDecisionto

Finance

aFirm

ThroughHomeEquityunder

anAlternative

Speci�cation.Home

Equityisabinary

variablethatdesignatesthestart-uppartially�nancedthe�rm

throughhomeequity.

Only

HomeEquityisabinary

variablethat

designatesthe�rm

was�nancedexclusivelythroughhomeequity.

Each

testisalinearprobabilityregressionwherethedependentvariableisabinary

variablethatdesignatesthestart-uppartially�nancedthe�rm

throughthespeci�ed

option.Allspeci�cationsincludeIndustry

SectorandFirm

Size

�xed

e�ectsandcluster

observationsatthestate

level.T-Statisticsare

included

below

thecoe�

cient.Weuse

*to

denote

signi�cance

atthe5%

level,

**to

denote

signi�cance

atthe1%

level,and***to

denote

signi�cance

atthe0.1%

level.Allvalues

dependontheinstrumentalvariablesdeveloped

inthepaper.

ThroughHomeEquity

$0

$5000

$10,000

$25,000

$50,000

$100,000

$250,000

$1M

∆%

Price

Index

.0037

.051**

.078**

.18***

.18**

.29***

.15**

.16**

(.66)

(2.4)

(2.2)

(3.4)

(2.5)

(4)

(2.4)

(2.1)

∆%

GDP

-.0052

-.076

-.031

-.11

-.11

-.69**

.22

-.29

(-.2)

(-.78)

(-.22)

(-.46)

(-.36)

(-2.4)

(.91)

(-.82)

∆%

Unem

ployment

.0026

.064***

-.022

.12*

-.097

-.074

.028

-.11

(.32)

(2.7)

(-.45)

(1.8)

(-.97)

(-.74)

(.43)

(-1.1)

Firm

Characteristics

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Observations

24685

6860

7822

5478

5512

5499

3791

1626

R2

.0062

.025

.027

.057

.051

.06

.1.12

Only

HomeEquity

$0

$5000

$10,000

$25,000

$50,000

$100,000

$250,000

$1M

∆%

Price

Index

.0054

.018

.036**

.14***

.067*

.12***

.051***

.024**

(1.6)

(1.4)

(2.6)

(9)

(1.8)

(6.3)

(3.5)

(2.6)

∆%

GDP

-.0067

-.046

-.0097

-.28**

.078

-.38***

.082

-.0038

(-.31)

(-.77)

(-.13)

(-2.5)

(.52)

(-3.4)

(1.1)

(-.13)

∆%

Unem

ployment

-.00041

.041**

.004

-.028

-.082*

-.056

.042

-.00013

(-.12)

(2.5)

(.14)

(-.91)

(-1.8)

(-1.5)

(1.7)

(-.014)

Firm

Characteristics

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Observations

24752

6875

7847

5489

5517

5508

3797

1631

R2

.0058

.024

.024

.047

.052

.053

.069

.19

30

Table

7:E�ectofaRealEstate

Price

Shock

forallFinancingDecisions.

Each

test

isalinearprobabilityregressionwherethedependentvariable

isabinary

variablethatdesignatesthestart-uppartially�nancedthe�rm

through

thespeci�ed

option.Allspeci�cationsincludeIndustry

Sector

andFirm

Size�xed

e�ects

andcluster

observationsatthestate

level.T-Statisticsare

included

below

thecoe�

cient.

Weuse

*to

denote

signi�cance

atthe5%

level,**to

denote

signi�cance

atthe1%

level,and***to

denote

signi�cance

atthe0.1%

level.Allvalues

dependontheinstrumental

variablesdeveloped

inthepaper.

HomeEquity

BankLoan

Owner

Assets

Grant

Venture

∆%

Price

Index

×1[Financial>$5,000]

.11***

-.17***

.022**

-.0018

.0044

(4.6)

(-11)

(2.2)

(-1.1)

(1.5)

∆%

Price

Index

.018

-.016

-.046***

.00086

-000037

(1.3)

(-1.4)

(-4)

(.65)

(-.031)

1[Financial>$5,000]

.085***

.52***

.11***

.003**

.058***

(3.4)

(17)

(6.6)

(2.1)

(6.7)

∆%

GDP

-.061

.05

.068

.00069

-.001

(-.77)

(.66)

(1.6)

(.12)

(-.14)

∆%

Unem

ployment

.0076

.0091

-.026

.0034

-.0048

(.35)

(.4)

(-1.6)

(1.5)

(-1.6)

Observations

61273

61273

61273

61273

61273

R2

.13

.2.027

.0037

.033

Gov

Guar

Loan

Gov.Loan

Credit

Loanfrom

Family

Savings

∆%

Price

Index

×1[Financial>$5,000]

-.012***

-.0068**

0.0019

-.013***

.0011

(-4.9)

(-2.5)

(.14)

(-2.8)

(0.084)

∆%

Price

Index

-.0033*

.00073

.024

-.0092*

.045**

(-1.9)

(.5)

(1.3)

(-1.7)

(2.7)

1[Financial>$5,000]

.05***

.027***

-.0066

.083***

-.34***

(6.4)

(5.2)

(-.39)

(9.2)

(-14)

∆%

GDP

.022**

-.0083

-.0027

.059*

-.15**

(2.2)

(-.98)

(-.03)

(1.7)

(-2.2)

∆%

Unem

ployment

.00031

.000078

.000062

-.005

-0.0016

(.-69)

(.022)

(.0026)

(-.7)

(-.059)

Observations

61273

61273

61273

61273

61273

R2

.031

.014

.037

.029

0.067

31

Table8:E�ectofaRealEstate

Price

Shock

onBusinessLoansandLoanGuaranteeProgramsAccordingto

FinancingNeeds.

Each

test

isalinear

probabilityregressionwherethedependentvariableisabinary

variablethatdesignatesthestart-uppartially�nancedthe�rm

throughthespeci�ed

option.Allspeci�cationsincludeIndustry

SectorandFirm

Size�xed

e�ects

andcluster

observationsatthestate

level.T-Statisticsare

included

below

thecoe�

cient.

Weuse

*to

denote

signi�cance

atthe5%

level,**to

denote

signi�cance

atthe1%

level,and***to

denote

signi�cance

atthe

0.1%

level.Allvalues

dependontheinstrumentalvariablesdeveloped

inthepaper.

BusinessLoans

$5000

$10,000

$25,000

$50,000

$100,000

$250,000

$1M

∆%

Price

Index

×1[Financial>$5,000]

-.036***

-.11***

-.2***

-.29***

-.31***

-.35***

-.11

(-3.7)

(-8)

(-8.5)

(-7.6)

(-10)

(-8.7)

(-1.3)

∆%

Price

Index

-.02***

-.019***

-.016***

-.021**

-.018***

-.018***

-.023***

(-4.4)

(-2.8)

(-2.7)

(-2.5)

(-2.8)

(-2.9)

(-5)

1[Financial>$5,000]

.044***

.12***

.23***

.34***

.4***

.57***

.47***

(7.1)

(12)

(13)

(12)

(17)

(21)

(9.9)

∆%

GDP

.05*

.05

.033

.069

.048

.031

.067**

(1.9)

(1.2)

(.89)

(1.3)

(1.3)

(.97)

(2.5)

∆%

Unem

ployment

.00053

-.0019

-.0036

.021

.0078

.0043

.012

(.064)

(-.18)

(-.27)

(1.6)

(.63)

(.31)

(1.2)

Observations

31545

32507

30163

30197

30184

28476

26311

R2

.02

.058

.12

.18

.21

.32

.25

GovernmentGuaranteed

Loan

$5000

$10,000

$25,000

$50,000

$100,000

$250,000

$1M

∆%

Price

Index

×1[Financial>$5,000]

-.00014

-.0051

-.017***

-.019***

-.03***

-.021

-.0094

(-.13)

(-1.3)

(-3.5)

(-2.9)

(-2.9)

(-1)

(-.42)

∆%

Price

Index

-.00096*

-.0045

-.0013

-.0018

-.0011

-.004

-.0011

(-1.9)

(-.83)

(-1.1)

(-2.2)

(-.99)

(-2.1)

(-1.4)

1[Financial>$5,000]

.00066

.0067**

.02***

.02***

.041***

.065***

.046***

(1.3)

(2.5)

(4.6)

(4.6

(6.4)

(4.8)

(2.8)

∆%

GDP

.003*

-.00085

.0053

.0092***

.0044

.027**

.0046

(1.8)

(-.024)

(.85)

(2.2)

(.66)

(2.4)

(1.3)

∆%

Unem

ployment

.0012**

(-.0098)

-.00085

.0025

-.00064

.0015

.0019

(2.2)

(-.56)

(-.3)

(1.4)

(-.23)

(.43)

(1.5)

Observations

31545

32507

30163

30197

30184

28476

26311

R2

.0019

.0056

.011

.013

.032

.056

.035

32

Table

9:E�ectofaRealEstate

Price

Shock

onCapitalStructure

byIndustry

I.Each

test

isalinearprobabilityregressionwherethedependent

variableisabinary

variablethatdesignatesthestart-uppartially�nancedthe�rm

throughthespeci�ed

option.Allspeci�cationsincludeIndustry

SectorandFirm

Size�xed

e�ects

andcluster

observationsatthestate

level.

T-Statisticsare

included

below

thecoe�

cient.

Weuse

*to

denote

signi�cance

atthe5%

level,**to

denote

signi�cance

atthe1%

level,and***to

denote

signi�cance

atthe0.1%

level.Allvalues

dependonthe

instrumentalvariablesdeveloped

inthepaper.

HomeEquity

BusLoan

CreditCard

FamilyLoan

HomeEquity

BusLoan

CreditCard

FamilyLoan

Construction

Manufacturing

∆%

Price

Index×1[Financial>$5,000]

.098***

-.19***

.0038

-.031**

.084**

-.22***

.051

-.0054

(2.8)

(-5.7)

(.074)

(-2.4)

(2)

(-5.4)

(.5)

(-.16)

Observations

6437

6437

6437

6437

2346

2346

2346

2346

R2

.079

.096

.045

.03

.079

.14

.053

.061

RetailTrade

TransportationandWarehousing

∆%

Price

Index×1[Financial>$5,000]

.11***

-.15***

-.041

.02*

.18***

-.31***

-.025

.0072

(3.1)

(-6.4)

(-1)

(1.8)

(3.4)

(-3.9)

(-.38)

(.31)

Observations

8163

8163

8163

8163

2966

2966

2966

2966

R2

.11

.1.034

.037

.095

.13

.031

.037

Inform

ation

Finance

andInsurance

∆%

Price

Index×1[Financial>$5,000]

.12***

-.025

-.018

-.028

.12**

-.052

.12**

.0098

(3.5)

(-.6)

(-.17)

(-1)

(2.4)

(-1.6)

(2.6)

(.3)

Observations

1635

1635

1635

1635

2777

2777

2777

2777

R2

.12

.068

.077

.077

.11

.056

.059

.035

33

Table10:E�ectofaRealEstate

Price

Shock

onCapitalStructure

byIndustry

II.Each

test

isalinearprobabilityregressionwherethedependent

variableisabinary

variablethatdesignatesthestart-uppartially�nancedthe�rm

throughthespeci�ed

option.Allspeci�cationsincludeIndustry

SectorandFirm

Size�xed

e�ects

andcluster

observationsatthestate

level.

T-Statisticsare

included

below

thecoe�

cient.

Weuse

*to

denote

signi�cance

atthe5%

level,**to

denote

signi�cance

atthe1%

level,and***to

denote

signi�cance

atthe0.1%

level.Allvalues

dependonthe

instrumentalvariablesdeveloped

inthepaper.

HomeEquity

BusLoan

CreditCard

FamilyLoan

HomeEquity

BusLoan

CreditCard

FamilyLoan

RealEstate

andRentalandLeasing

Professional,Scienti�c,andTechnicalServices

∆%

Price

Index×1[Financial>$5,000]

.1***

-.17***

.028

-.0016

.075*

-.082***

-.03

-.018*

(3.3)

(-4.9)

(.85)

(-.13)

(1.9)

(-3.5)

(-1)

(-1.7)

Observations

5742

5742

5742

5742

9836

9836

9836

9836

R2

.069

.17

.058

.024

.068

.061

.039

.021

Administrative,Support,WasteMan.,Rem

ediationServ.

HealthCare

andSocialAssistance

∆%

Price

Index×1[Financial>$5,000]

.089***

-.13***

.031

-.038*

.15***

-.25***

.038

-.0082

(3.9)

(-4.1)

(.58)

(-1.7)

(3.7)

(-6.8)

(.76)

(-.35)

Observations

3561

3561

3561

3561

4193

4193

4193

4193

R2

.078

.1.052

.048

.12

.21

.053

.032

Arts,Entertainment,andRecreation

AccommodationandFoodServices

∆%

Price

Index×1[Financial>$5,000]

.0025

-.19***

-.08

-.058***

.16**

-.12***

-.25**

-.0089

(.038)

(-4.9)

(-.89)

(-2.8)

(2.7)

(-3.4)

(-2.5)

(-.29)

Observations

2167

2167

2167

2167

2627

2627

2627

2627

R2

.11

.13

.056

.036

.094

.11

.045

.04

34