Embed Size (px)

Citation preview

HOSTILE TAKEOVER BIDS AND SHAREHOLDER WEALTH

Hostile Takeover Bids and Shareholder Wealth: Some UK Evidence CHRIS PARKINSON, Lecturer VI Accountmg and Fznance, Unzverszty of Bradford Management Cen tre

Introduction mefflclent management of the target companies However, this would reqmre a merger to succeed before

Corporate mergers have long been with us but the hostile bid 1s a relatively new phenomenon In the UK It was unheard of until after the Companies Act of 1948 There have been many hostile bids since 1948 but, with a few notable exceptions, they were largely ignored as subjects worthy of study until the 1980s The much publlclzed bid battles of that decade sparked the interest of all who study the financial markets Most observers will remember the number of large, hostile bids which were vigorously defended by the target during this period For example, Dutons for Woolworth (successful defence), Hanson for Imperial tobacco (unsuccessful defence) and of course, Argyll Trust for Guinness (opting for a ‘White Knight’ m the form of Dlstlllers)

the gams were realized A variant of this view suggests that the takeover mechanism 1s a powerful incentive to managers to perform efflclently m the interests of shareholders If they do not, they will be removed by takeover and lose then Jobs This lmphes that the threat of takeover 1s sufflclent to spur management mto lmprovmg then performance

The ‘asymmetric mformatlon’, or valuation, hypothesis claims that If mformatlon 1s not perfectly available the bidder may have mformatlon about the target which the market m general does not have This allows the bidder to place a higher value on the company than the current share price would suggest Alternatively, new mforma- tlon might be made available to the market during the merger process and this mformatlon results m a permanent upward revaluation of the company’s shares

In summary the various hypotheses suggest that It might be expected that mefflclent management will not survive m an unrestricted market for corporate control, but If they do they will be motivated by the threat of takeover to improve their company’s performance Thus, hostile bids can be seen as ‘dlsclplmary’ 1

This paper presents a discussion of the motives for mergers and the results of a UK study into the effect of hostrle bids on shareholder wealth Significant gains are obtained by shareholders in target companres which successfully defend a bid. These gains are not lost up to two years after the failure of the bid. Shareholders in the bidding companies receive gains much smaller than those of the targets, but these are also maintained after the bid.

prolects, and managers will only engage m takeovers, and llkewlse abandon them d necessary, If this leads to an increase m shareholder wealth The ‘managerial’ view on the other hand suggests that managers pursue their own self interests As far as merger activity IS concerned this can be interpreted to mean they will Indulge m mergers to further this self-interest even If It 1s against the interests of the shareholders

The ‘Improved management’ hypothesis suggests that gams from mergers might result from the removal of

Contested and/or hostlle bids have featured m commercial hfe for some years now m both the UK and USA This has not been the case m other European countries, although takeovers m general, and hostile bids m particular, are mcreasmgly becoming part of French and German corporate activity However, to date there has not been a sufflclent number of hostile bids m Europe, outside the UK, to permit statlstlcally valid cross-country comparisons

Merger Motives However, the effectiveness of the market for corporate There are numerous ‘theories’ about the motives for control as a dlsclplmary force 1s not guaranteed, at least mergers and much contradictory empmcal evidence m the short term In particular it has been observed that The ‘neo-classical’ view suggests that mergers will be managers frequently overpay for their targets, to the undertaken If they are posltlve net present value detriment of their shareholder’s wealth Roll (1986)

454 EUROPEAN MANAGEMENT JOURNAL Vol9 No 4 December 1991

HOSTILE TAKEOVER BIDS AND SHAREHOLDER WEALTH

suggests that ‘hubris’ might be the explanation of why managers of bidding compames apparently pay more than target companies are worth to succeed m the acquisition

There 1s no real ‘theory’ of the motives for hostile mergers but the wave of hostlle bids which occurred m the mid-1980s m the UK and the USA has prompted much research mto the economic lustlflcatlon for this activity Many studies m the USA have addressed whether or not target shareholders gam from the use of defensive tactics, including the mtroductlon of pro- active ‘anti-takeover amendments’ * Few studies have been undertaken m the UK of these issues, and m fact many of them are Irrelevant, an&takeover amendments do not exist m anything hke the extreme form witnessed m the USA This fortunate state of affairs may be due m part to the differences m company law m the UK and USA, which generally afford greater protection to UK shareholders

Ap (P

roaches to Evaluating the Causes an Consequences of Mergers Takeover and merger activities attract a great deal of interest and exammatlon from all those interested m both the theory and practice of fmanclal management This 1s because merger activity 1s believed to influence both the level of economic wealth and its distribution Some studies have focused on accounting variables to determine whether mergers, on average, create wealth The evidence 1s muted, but studies of this aspect of mergers suggest that, generally, they do not

A second approach 1s the exammatlon of the financial characterlstlcs of bidder and target companies Studies m this area commonly attempt to ldentlfy characterlstlcs which might differentiate between companies which will acquire and those which will be acquired, and therefore lead to a predictive model of takeovers, or alternatlvely to ldentlfy the determinants and con- sequences of merger There are many differences between these studies m terms of the period of the study, the choice of variables and/or control group These differences make direct comparisons between studies dlfflcult

Another approach has been to examme returns to shareholders,3 or the extent to which mergers bring about gains or losses m the acquired and acqulrmg compames This 1s the ‘event’ study approach and, despite the use of different models to measure gains or losses, the one consistent fmdmg 1s that large gains are obtained by the target firms’ shareholders This observa- tion has never been seriously challenged, at least m respect of completed mergers

A major concern m event studies 1s assessment of the- extent to which security returns around the time of the event are abnormal, 1 e m which they differ from the returns which would be expected given normal market

movements at that time For example, if the market Improves by 2 per cent (using the FT All Share Index as a basis for comparison) on any given day, it would be expected that a portfolio of shares selected at random would also move by 2 per cent If the return on that portfolio 1s slgmflcantly different from the return on the market, then the returns are said to be ‘abnormal’ and mvestlgatlon 1s m order to determine the cause of that abnormahty Here we calculate what the return to the shareholder would have been m the absence of an event, m this case a hostile bid

I Shareholders in target companies have tended to gain financially from takeovers in the UK

The results of the few UK studies which have used this approach have tended to agree with the results of US studies They generally conclude that mergers are a ‘posltlve sum game’ even if most of the gains do go to the target shareholders In the most comprehensive UK study, Franks and Harris (1989) surveyed over 1800 mergers between public quoted companies m the period 1955-85 They suggest that shareholders m target companies are, most commonly, on the wmnmg side, at least m terms of financial returns, although the effect of the merger process results m a small, mslgmflcant gam overall

The Application of the Event Study Ap

dp roach to Successfully Defended

Bi s

Explanation of the model used The event study approach 1s used here to examme and report research fmdmgs mto hostlle bids which were successfully defended m the period 1975-84 The aim 1s to determine whether the successful defence of a hostlle takeover bid has any sustamed effect on the returns to shareholders m both target and bidding companies

The model used here to determine abnormal gains IS the simple ‘mean adjusted returns’ This model takes the return on the market, as defmed by the FT Index, and compares it with the return shown by the companies m the sample The difference 1s the abnormal return This approach has been shown by Brown and Warner (1980) and others to be at least as effective m determining ‘abnormahty’ as have more sophlstlcated methods, such as the market model or capital asset pricing model

Abnormal returns for mdlvldual compames are aggre- gated to form a portfolio of average abnormal returns

(AAR) AARs may be calculated for any period, most usually dally or monthly The analysis conducted here exammes the monthly AARs

EUROPEAN MANAGEMENT JOURNAL Vo19 No 4 December 1991 455

HOSTILE TAKEOVER BIDS AND SHAREHOLDER WEALTH

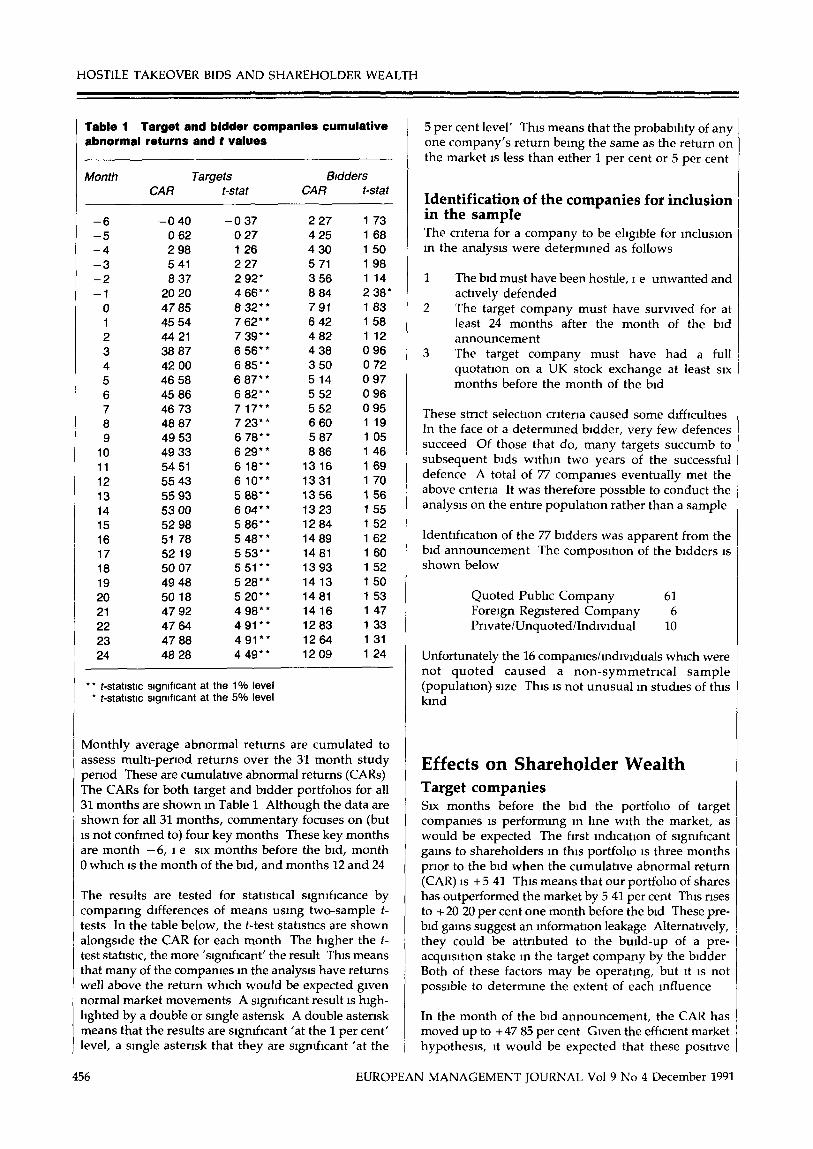

Table 1 Target and bidder companies cumulative abnormal returns and 1 values

Month Targets Bidders CAR t-stat CAR t-stat

-6 -040 -037 227 1 73

-5 0 62 027 425 168

-4 2 98 126 430 150

-3 5 41 227 5 71 198

-2 8 37 292* 356 1 14

-1 20 20 466** 884 238*

0 47 85 832** 791 183

1 45 54 762** 642 158

2 44 21 739** 4 82 112

3 38 87 656** 4 38 096

4 42 00 685" 3 50 072

5 46 58 687** 514 097

6 45 86 682** 552 096

7 46 73 717** 552 095

8 48 87 723** 660 1 19

9 49 53 678** 587 1 05

10 49 33 629** 886 146

11 5451 618** 1316 169

12 5543 610** 1331 1 70

13 5593 588*' 1356 156

14 5300 604** 1323 155

15 5298 586** 1284 152

16 51 78 548** 1489 162

17 5219 553** 1481 160

18 5007 551" 1393 152

19 4948 528** 1413 150

20 5018 520** 1481 153

21 4792 498** 1416 147

22 4764 491" 1283 133

23 4788 491** 1264 1 31

24 48 28 449" 1209 124

** t-statlstlc slgmflcant at the 1% level l t-statmc significant at the 5% level

Monthly average abnormal returns are cumulated to assess multi-period returns over the 31 month study period These are cumulative abnormal returns (CARS) The CARS for both target and bidder portfolios for all 31 months are shown m Table 1 Although the data are shown for all 31 months, commentary focuses on (but 1s not confined to) four key months These key months are month -6, 1 e SIX months before the bid, month D which 1s the month of the bid, and months 12 and 24

The results are tested for statlstlcal slgnlflcance by comparing differences of means using two-sample t- tests In the table below, the t-test statlstlcs are shown alongside the CAR for each month The higher the t- test statistic, the more ‘sign&cant’ the result This means that many of the companies m the analysis have returns well above the return which would be expected given normal market movements A slgmflcant result 1s hlgh- lighted by a double or single asterisk A double asterisk means that the results are slgndlcant ‘at the 1 per cent’ level, a single asterisk that they are slgmflcant ‘at the

5 per cent level’ This means that the probablhty of any one company’s return being the same as the return on the market 1s less than either 1 per cent or 5 per cent

Identification of the companies for inclusion in the sample The criteria for a company to be ehglble for mcluslon m the analysis were determmed as follows

1 The bid must have been hostile, 1 e unwanted and actively defended

2 The target company must have survived for at least 24 months after the month of the bid announcement

3 The target company must have had a full quotation on a UK stock exchange at least SIX months before the month of the bid

These strict selection criteria caused some dlfflcultles In the face of a determined bidder, very few defences succeed Of those that do, many targets succumb to subsequent bids wlthm two years of the successful defence A total of 77 compames eventually met the above criteria It was therefore possible to conduct the analysis on the entire population rather than a sample

Identlflcatlon of the 77 bidders was apparent from the bid announcement The composltlon of the bidders 1s shown below

Quoted Public Company 61 Foreign Registered Company 6 PrlvatelUnquotedlIndlvldual 10

Unfortunately the 16 compameslmdlvlduals which were not quoted caused a non-symmetrical sample (population) size This 1s not unusual m studies of this kmd

Effects on Shareholder Wealth Target companies Sue months before the bid the portfolio of target companies 1s performing m lme with the market, as would be expected The first mdlcatlon of slgnlflcant gains to shareholders m this portfolio 1s three months prior to the bid when the cumulative abnormal return (CAR) 1s + 5 41 This means that our portfolio of shares has outperformed the market by 5 41 per cent This rises to + 20 20 per cent one month before the bid These pre- bid gains suggest an mformatlon leakage Alternatively, they could be attributed to the buld-up of a pre- acqulsltlon stake m the target company by the bidder Both of these factors may be operating, but it 1s not possible to determine the extent of each influence

In the month of the bid announcement, the CAR has moved up to + 47 85 per cent Given the efficient market hypothesis, it would be expected that these positive

EUROPEAN MANAGEMENT JOURNAL Vo19 No 4 December 1991

HOSTILE TAKEOVER BIDS AND SHAREHOLDER WEALTH

E UROPEAN MANAGEMENT JOURNAL Vo19 No 4 December 1991

abnormal returns would disappear once the bid had failed However we fmd that by month 12 the CAR has increased to + 55 43 per cent In the followmg 12 months some of the gains are lost but by the end of the study period, month +24, the CAR stands at +48 28 per cent, still slightly above the CAR observed m the bid announcement month

Between the three-month period leadmg up to the bid and the month of failure, the market 1s presumably reacting to an intended merger and share prices are marked up to reflect the well-supported belief that bidders will have to pay a premium for that control based on their calculations of expected gains Lf the share price gains are based entirely on the assumption that the bidder will pay such a premmm, this does not explain why they are sustained, and Indeed increase 24 months after the bid

A variety of explanations are possible for this apparent contradlctlon to what theory has led us to expect Efficiency theorists claim that share prices ~111 react immediately to new mformatlon being received by the market There are three forms of the efficient market hypothesis (EMH)

The weak form claims that If superior profits cannot be made on the basis of forecastmg from past prices, we can conclude that these prices contam all known mformatlon the semz-strong form IS assumed to exist if consistently superior profits cannot be obtained by use of all published mformatlon The strong form IS assumed to exist If consistently superior profits cannot be obtamed by even the most sophisticated analysis and forecastmg methods, and possibly even by use of mslder information

The strong form of the EMH 1s not believed to hold, there IS unmlstakeable evidence that supenor profits are made by the use of mslde mformatlon Belief m the senu- strong and weak forms has also been shaken m recent years, most notably followmg the stock market crash of 1987 Share prices collapsed without any change m available mformatlon about prospects for compames or the economy, suggestmg the markets were wltnessmg the burst of a speculative share price ‘bubble’ The simple form of the EMH suggests shares cannot rise to artlflclally high levels this way The fact that they did collapse raises doubts about the simple form of efficient markets theory It 1s entirely possible that the belief m a single ‘true’ level of share prices has to be replaced with a view that there 1s a very wide range of plausible values

Even if this modified view of the EMH holds, the share prices of the target companies might be expected to fall back to their pre-bid level when bid proceedings terminate If this 1s found not to be true, investors could adopt a strategy of buying shares on the day after the announcement of termination of bid proceedings and

hold the shares for a further two years Such an investment strategy should not, accordmg to the EMH, earn above-average returns However, even before the crash of 1987, studies of the post-offer performance of takeovers do not umformly support theories of market efficiency

I The Theory of Efficient Markets 1s of little use in explaming post-offer performance of takeovers

The ‘mformatlon’ theories of mergers offer a more plausible explanation for the sustained abnormal gams to target shareholders Bradley et al (1983) examined three hypotheses

1 A hostile merger bid Induces current target management to Implement a higher-valued operating strategy - it gives managers a ‘kick m the pants’ which leads to Improved post-bid performance

2 The bid process reveals previously unknown mformatlon which suggests the target shares were previously ‘undervalued’ - the ‘slttmg on a goldmme’ hypothesis

3 The company contmues to be considered a bid prospect by the market

These hypotheses suggest that the positive revaluation of the target companies’ shares does not require the successful acquisition of target companies’ resources The new mformatlon made avallable during the bid proceedings permits a permanent upward revaluation of the company This 1s not mconslstent with notions of market efficiency

It 1s difficult to compare our results with previous studies No other European study has looked at falled bids m particular, and although the results could be compared with some US studies of failed tender bids, detalled comparisons can be mlsleadmg due to slgruflcant differences m the legal systems of the two countries and m the choice of methodology We could look at the CARS m the month of the bid announcement as reported by studies of completed mergers but as these studies will contam a high proportion of friendly bids the comparison will be mlsleadmg The only studies to date which refer to contested and/or uncompleted bids are those by Plckermg (1978 and 1983), Ho11 and Plckermg (1988), and Franks and Harris (1989) However, these studies do not require the bid to be hosfde for It be included m their sample, merely uncompleted or sublect to bids from multiple bidders

Bidder companies The bidder portfoho shows a slgmflcant gam only m the one month prior to the bid, although It has been outperformmg the market to a greater extent than the target companies for most of the previous five months The subsequent decline m CARS partially conflrms

HOSTILE TAKEOVER BIDS AND SHAREHOLDER WEALTH

Franks et al ‘s (1977) contention that the small gains obtamed by shareholders m bidding companies around the time of the bid are not sustained The results here show gains which are sustained after the failure of the bid, although post-bid they are not statistically sigmficant

I beneficiaries of merger although shareholders m the

It zs the bid and defence process failed bidders do not lose This suggests that share-

that benefits shareholders most in holder wealth IS increased by merger actlvlty The mam

both companies conclusion therefore IS that it IS the blddmg and defending process that yields the most benefit to shareholders m both target and bidder firms

In the month of the bid announcement, the CAR for the ’ bidder portfolio has declmed to +7 91 which suggests

that either the terms of the bid were vlewed unfavourably by the market or failure was detected at an early stage By month 24 the CAR IS +12 09 The sustained posltlve, albelt magmflcant, CAR shown by the bidder portfolio suggests mformatlon IS revealed about the bidders, as well as the targets, during the bid proceedings which allows them to retam their share

Notes 1 For a more detatied dlscusslon on the dlsclplmary effects

of hostlle bids see Merck et al (1989), and Scharfstem (1988)

2 For dIscussIons on the economic effects of an&takeover amendments see the opposmg arguments of DeAngelo and Rice (1983) and Lmn and McConnell (1983) See also, ‘The economics of poison pills’, Offlce of the Chief Economist SEC March 5th 1986, and Jarrell and Pulson

price gains for 24 months after the failed bid The fact that the company 1s seen to be embarking on an acqulsl- tlon programme may be mterpreted as ‘good news’ about the further prospects of the bidder Many of these bidding companies would have embarked on alternatlve bids, but this IS not examined further here

Analysis of target sub-groups

(1987) 3 A ‘return’ IS defined as the capital gain plus dividend

on the shares during the period of study

References Bradley, M , Desal, A and Kim, E H (1983) ‘The rationale

behmd mterflrm tender offers’, journal of Fznanczal Economzcs, Vol 11, pp 183-206

The results reported m this article concentrate on returns to shareholders m the portfolios of targets and bidders for the entire lo-year study period However, additional analyses were performed on sub-groups of the 77 target companies The same mean adlusted returns approach was applied to sub-groups based on size of target, as measured by market capltallzatlon adlusted for inflation, and by method of fmancmg the offer In summary it was found that the smallest targets (those with a market capltahzatlon of less than f25 m&on) showed the largest gains by month 24 and those with a market capltalrzatlon of between f25 mllhon and f99 m&on showed the smallest Cash bids appear to be received with the most favour by the market but by month 24 the best performers are those companies which were sublect to an all share offer Combmatlon offers of cash and shares and/or some other security performed the poorest

Summary and Conclusions It appears that target companies which successfully defend a takeover bid substantially improve then economic performance, as measured by returns to shareholders m the sue-month period ending with the month of the bid These gains are largely maintained for the followmg 24 months This 1s contrary to what the efficient market theorists have led us to expect but IS consistent with some US studies of failed bids and might be explained by the ‘mformatlon’ theories of merger Bidder companies also demonstrate lmprove-

Brown, Stephen J and Warner, Jerold E (1980) ‘Measuring security pnce performance’, Journal of Fmanclal Economics, Vol 8, pp 205-58

DeAngelo, Harry and Rice, Edward M (1983) ‘Antltakeover charter amendments and stockholder wealth’, Journal of Fmanczal Economtcs, Vol 11, pp 329-60

Franks, Julian R , Broyles, Jack E and Hecht, Michael J (1977), ‘An industry study of the profltablllty of mergers m the UK’, Journal of Fmance, Vol 32, pp 1513-25

Franks, J R and Harris, R (1989) ‘Shareholder wealth effects of corporate takeover the UK experience 1955-1985’, Journal of Fznanczal Economrcs, Vol 23, pp 225-49

Holl, P and Plckermg, J F (1988) ‘The determmant and effects of actual, abandoned and contested mergers‘, Managenal and Decwon Econotmcs, Vol 9, pp l-19

Jarrell, Gregg A and Pulson, Annette (1987) ‘Shark repellents and stock prices the effects of anti-takeover amend- ments since 1980’, Journal of FlnanctaZ Economtcs, Vol 19, pp 127-68

Lmn, Scott C and McConnell, John J (1983) ‘An empmcal mvestlgatlon of the Impact of “anti-takeover” amend- ments on common stock prices’‘’ Journal of Fmanczal Economxs, Vol 11, pp 361-99

Merck, Randall, Shlelfer, A and Vlshny, R W (1989) ‘Characterlstlcs of targets of hostile and friendly takeovers’, m Corporate Takeovers Thezr Causes and Consequences (Ed Auerbach, A ) Chlcago Umverslty Press

Office of the Chief Economist Secuntles and Exchange Commlsslon (1986) ‘The economics of poison pills’, March

Plckenng, J F (1983) ‘The causes and consequences of abandoned mergers’, Journal oflndustnal Economzcs, Vol XxX1, No 3, pp 267-82

Roll, Richard (1986) ‘The hubris hypothesis of corporate takeovers’, Journal of Busmess, Vol 59, No 2, Part 1

Scharfstem, D (1988) ‘The dlsclplmary role of takeovers’, Revreuj of Economu Studtes, No 55, pp 185-99

ments m share prices but these gains are much smaller than those of their targets, and m statlstlcal terms are not significant

Fmdmgs of previous studies are conflrmed On the whole shareholers m target companies are the mam

458 EUROPEAN MANAGEMENT JOURNAL Vo19 No 4 December 1991

HOSTILE TAKEOVER BIDS AND SHAREHOLDER WEALTH

EU’ZOPEAN MANAGEMENT JOURNAL Vol 9 No 4 December 1991 459