Embed Size (px)

Citation preview

Hosted by:Ohio Municipal League

UNDERSTANDING THE “NEW” ORC 718Rewriting Your Income Tax Ordinance to Comply with HB 5

July 8, 2015

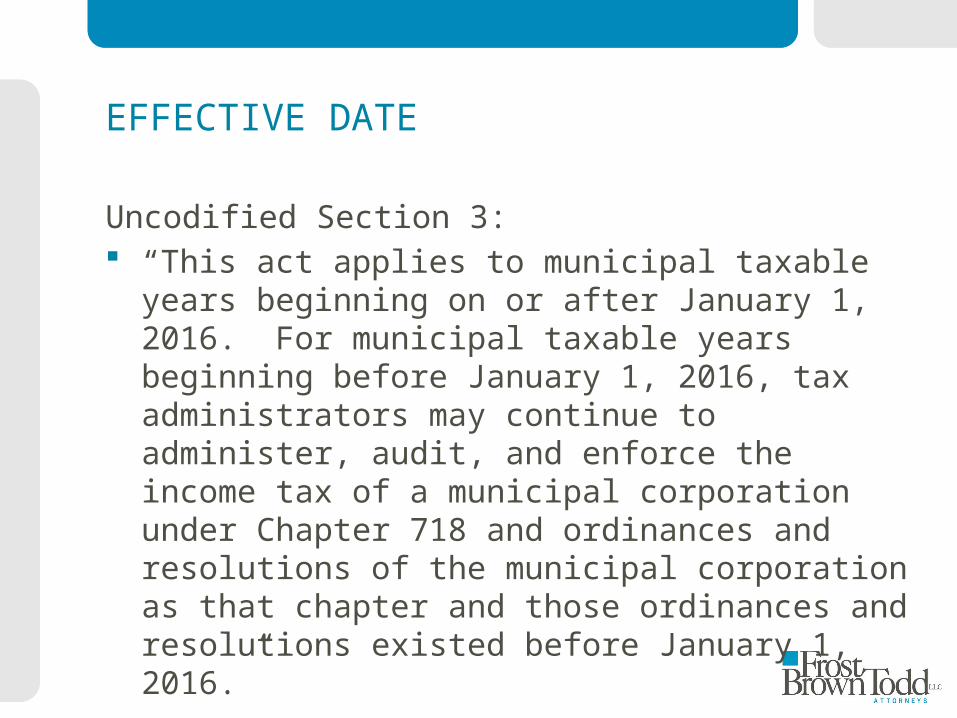

EFFECTIVE DATE

Uncodified Section 3: “This act applies to municipal taxable years beginning

on or after January 1, 2016. For municipal taxable years beginning before January 1, 2016, tax administrators may continue to administer, audit, and enforce the income tax of a municipal corporation under Chapter 718 and ordinances and resolutions of the municipal corporation as that chapter and those ordinances and resolutions existed before January 1, 2016.”

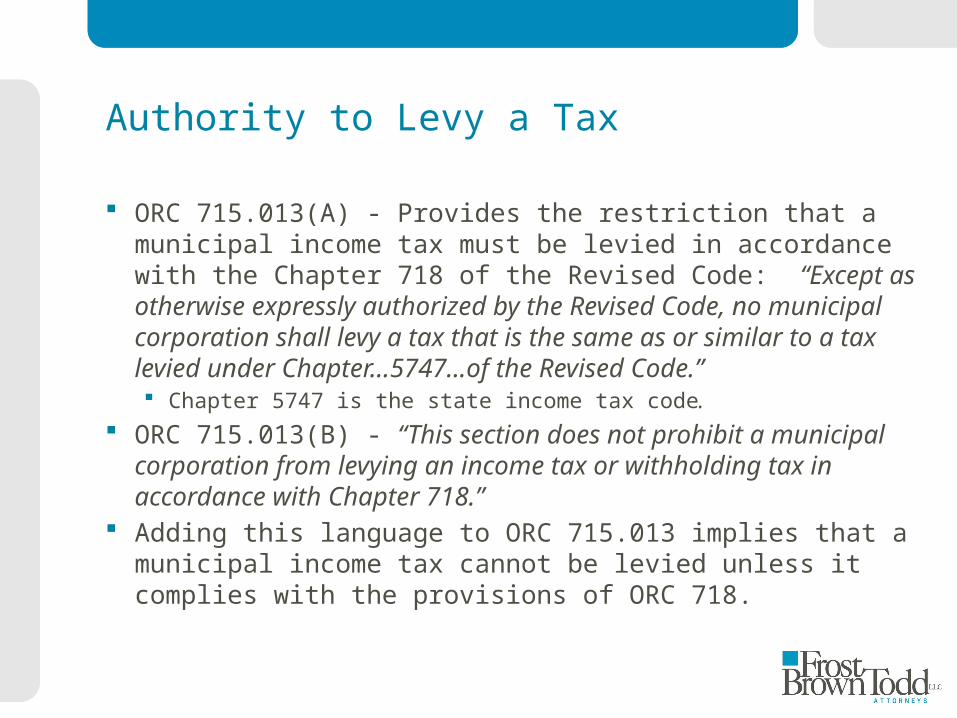

Authority to Levy a Tax

ORC 715.013(A) - Provides the restriction that a municipal income tax must be levied in accordance with the Chapter 718 of the Revised Code: “Except as otherwise expressly authorized by the Revised Code, no municipal corporation shall levy a tax that is the same as or similar to a tax levied under Chapter…5747...of the Revised Code.” Chapter 5747 is the state income tax code.

ORC 715.013(B) - “This section does not prohibit a municipal corporation from levying an income tax or withholding tax in accordance with Chapter 718.”

Adding this language to ORC 715.013 implies that a municipal income tax cannot be levied unless it complies with the provisions of ORC 718.

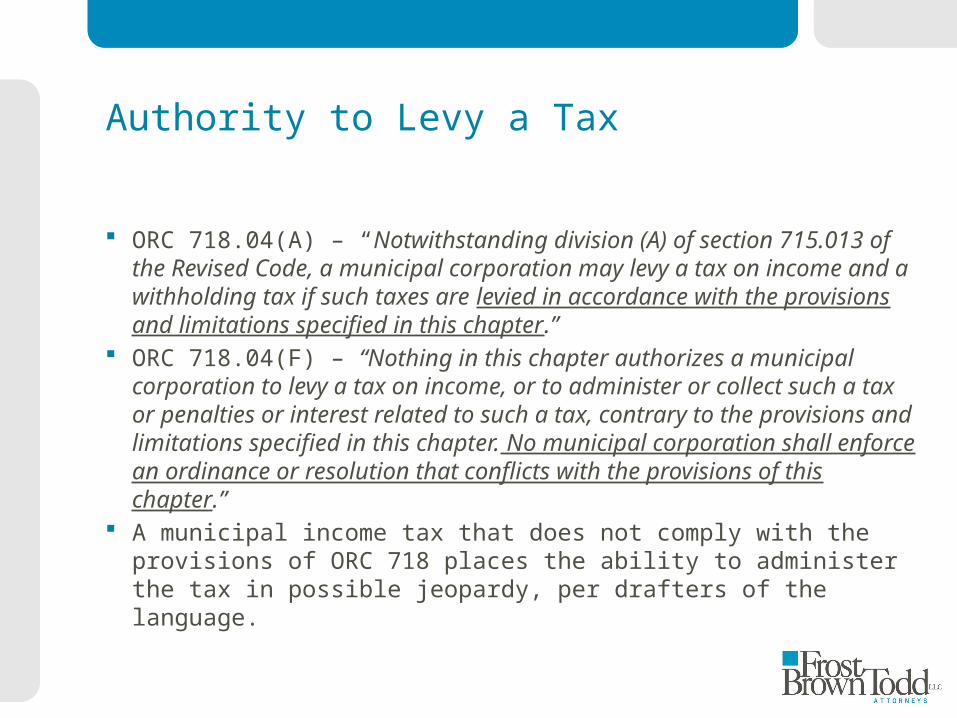

Authority to Levy a Tax

ORC 718.04(A) – “Notwithstanding division (A) of section 715.013 of the Revised Code, a municipal corporation may levy a tax on income and a withholding tax if such taxes are levied in accordance with the provisions and limitations specified in this chapter.”

ORC 718.04(F) – “Nothing in this chapter authorizes a municipal corporation to levy a tax on income, or to administer or collect such a tax or penalties or interest related to such a tax, contrary to the provisions and limitations specified in this chapter. No municipal corporation shall enforce an ordinance or resolution that conflicts with the provisions of this chapter.”

A municipal income tax that does not comply with the provisions of ORC 718 places the ability to administer the tax in possible jeopardy, per drafters of the language.

Authority to Levy a Tax

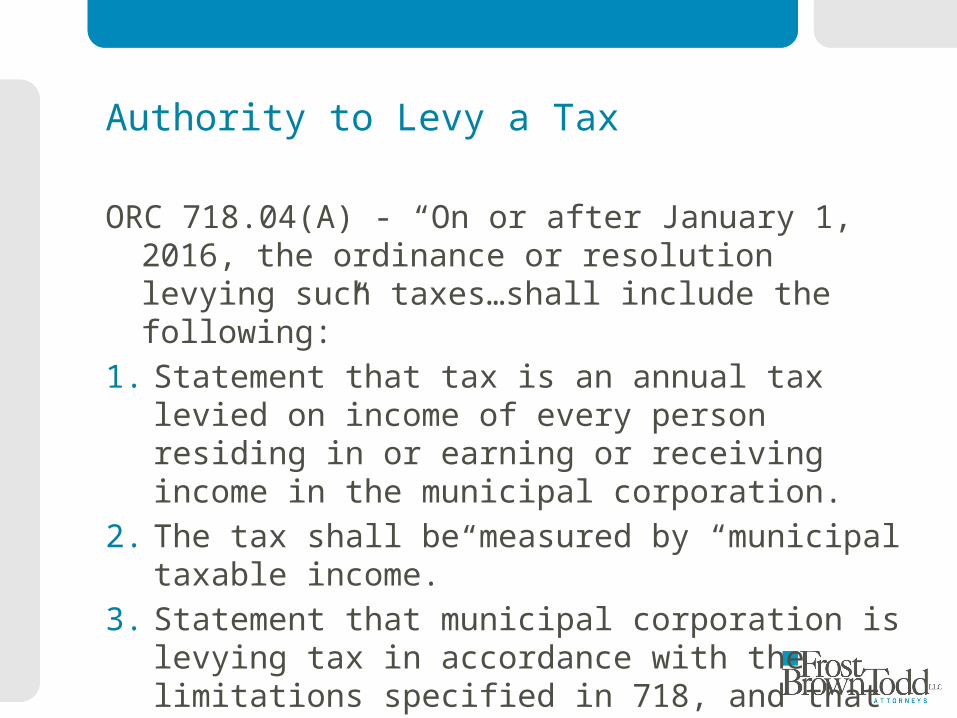

ORC 718.04(A) - “On or after January 1, 2016, the ordinance or resolution levying such taxes…shall include the following:”

1. Statement that tax is an annual tax levied on income of every person residing in or earning or receiving income in the municipal corporation.

2. The tax shall be measured by “municipal taxable income.”

3. Statement that municipal corporation is levying tax in accordance with the limitations specified in 718, and that the resolution or ordinance incorporations the provisions of 718.

Authority to Levy a Tax

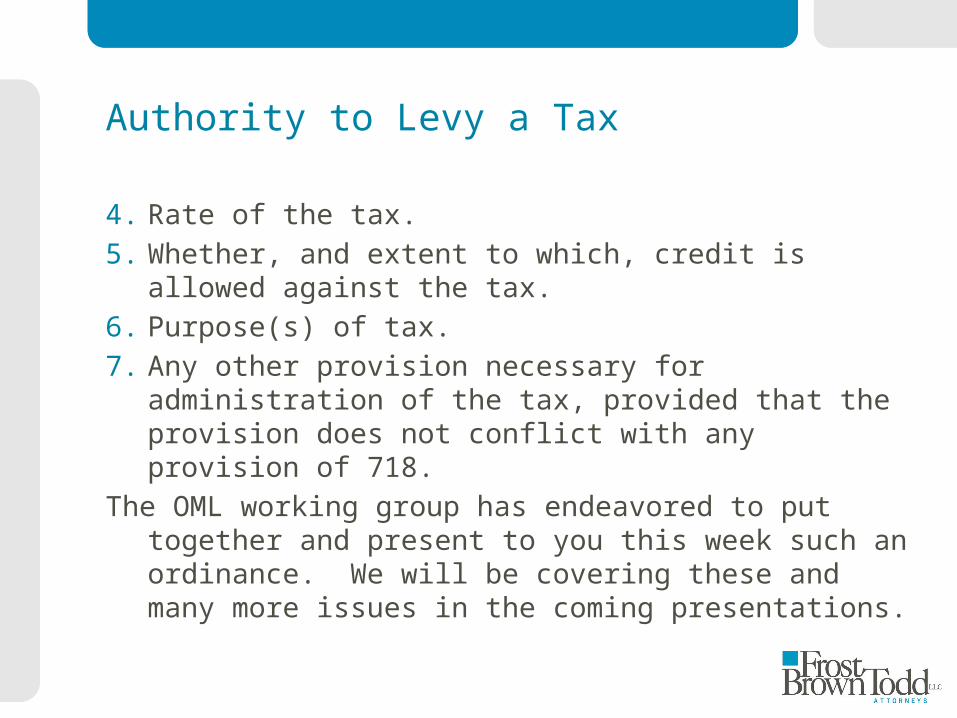

4. Rate of the tax.

5. Whether, and extent to which, credit is allowed against the tax.

6. Purpose(s) of tax.

7. Any other provision necessary for administration of the tax, provided that the provision does not conflict with any provision of 718.

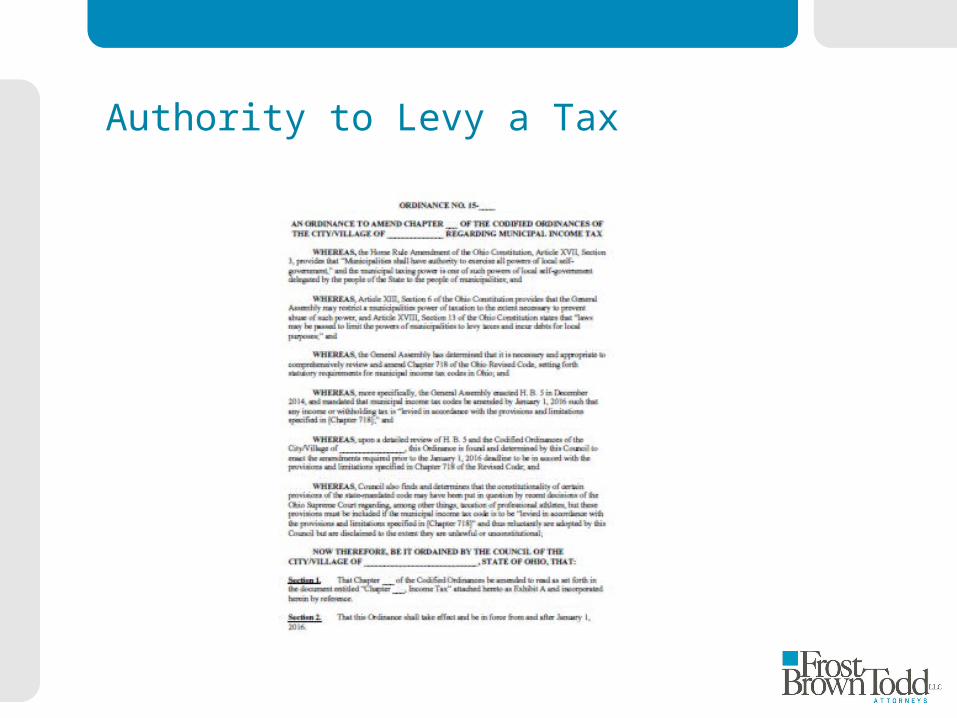

The OML working group has endeavored to put together and present to you this week such an ordinance. We will be covering these and many more issues in the coming presentations.

Authority to Levy a Tax

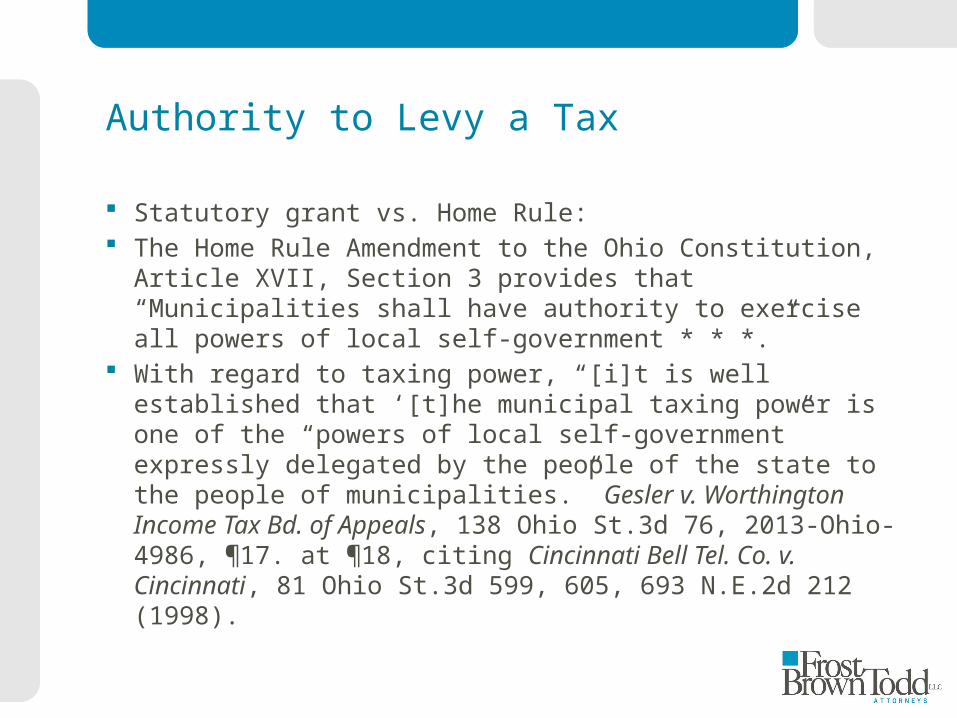

Statutory grant vs. Home Rule: The Home Rule Amendment to the Ohio Constitution,

Article XVII, Section 3 provides that “Municipalities shall have authority to exercise all powers of local self-government * * *.”

With regard to taxing power, “[i]t is well established that ‘[t]he municipal taxing power is one of the “powers of local self-government” expressly delegated by the people of the state to the people of municipalities.” Gesler v. Worthington Income Tax Bd. of Appeals, 138 Ohio St.3d 76, 2013-Ohio-4986, ¶17. at ¶18, citing Cincinnati Bell Tel. Co. v. Cincinnati, 81 Ohio St.3d 599, 605, 693 N.E.2d 212 (1998).

Authority to Levy a Tax

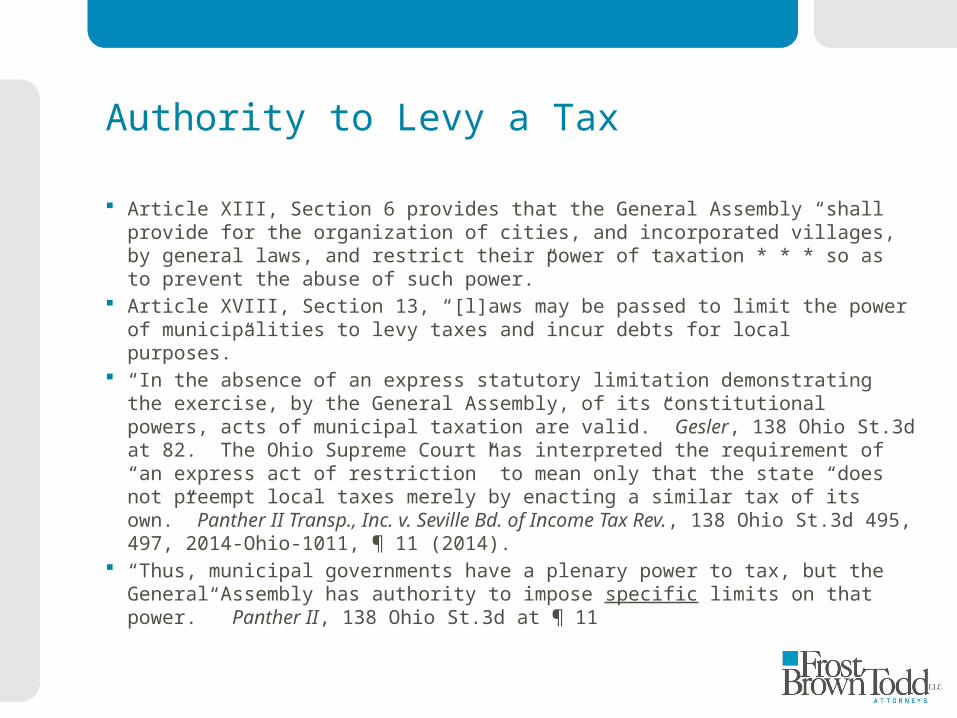

Article XIII, Section 6 provides that the General Assembly “shall provide for the organization of cities, and incorporated villages, by general laws, and restrict their power of taxation * * * so as to prevent the abuse of such power.”

Article XVIII, Section 13, “[l]aws may be passed to limit the power of municipalities to levy taxes and incur debts for local purposes.”

“In the absence of an express statutory limitation demonstrating the exercise, by the General Assembly, of its constitutional powers, acts of municipal taxation are valid.” Gesler, 138 Ohio St.3d at 82. The Ohio Supreme Court has interpreted the requirement of “an express act of restriction” to mean only that the state “does not preempt local taxes merely by enacting a similar tax of its own.” Panther II Transp., Inc. v. Seville Bd. of Income Tax Rev., 138 Ohio St.3d 495, 497, 2014-Ohio-1011, ¶ 11 (2014).

“Thus, municipal governments have a plenary power to tax, but the General Assembly has authority to impose specific limits on that power.” Panther II, 138 Ohio St.3d at ¶ 11

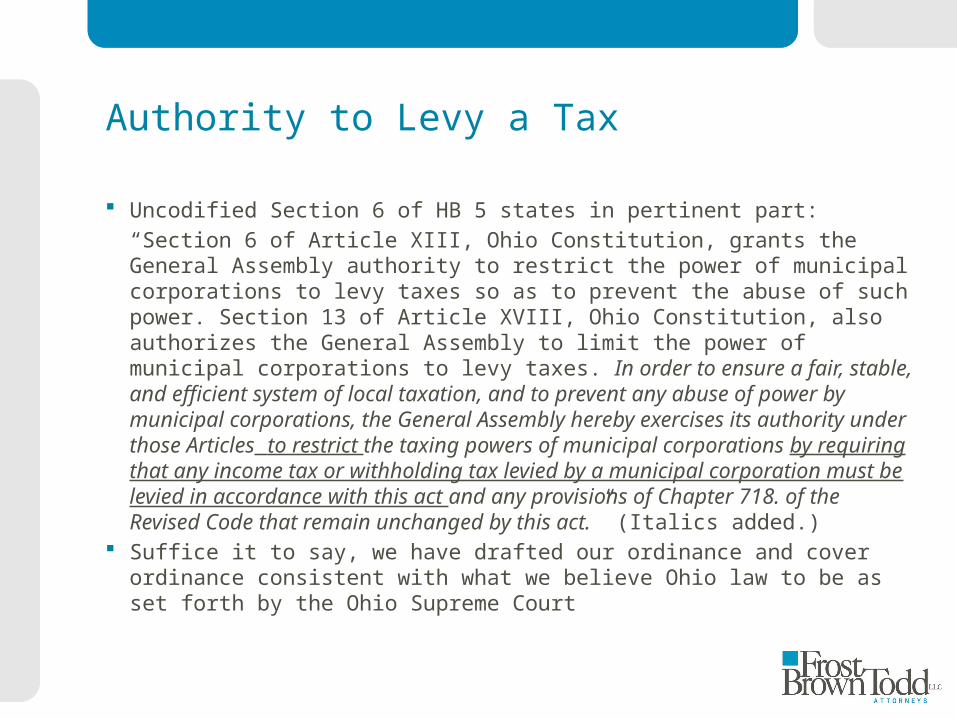

Authority to Levy a Tax

Uncodified Section 6 of HB 5 states in pertinent part:

“Section 6 of Article XIII, Ohio Constitution, grants the General Assembly authority to restrict the power of municipal corporations to levy taxes so as to prevent the abuse of such power. Section 13 of Article XVIII, Ohio Constitution, also authorizes the General Assembly to limit the power of municipal corporations to levy taxes. In order to ensure a fair, stable, and efficient system of local taxation, and to prevent any abuse of power by municipal corporations, the General Assembly hereby exercises its authority under those Articles to restrict the taxing powers of municipal corporations by requiring that any income tax or withholding tax levied by a municipal corporation must be levied in accordance with this act and any provisions of Chapter 718. of the Revised Code that remain unchanged by this act.” (Italics added.)

Suffice it to say, we have drafted our ordinance and cover ordinance consistent with what we believe Ohio law to be as set forth by the Ohio Supreme Court

Authority to Levy a Tax

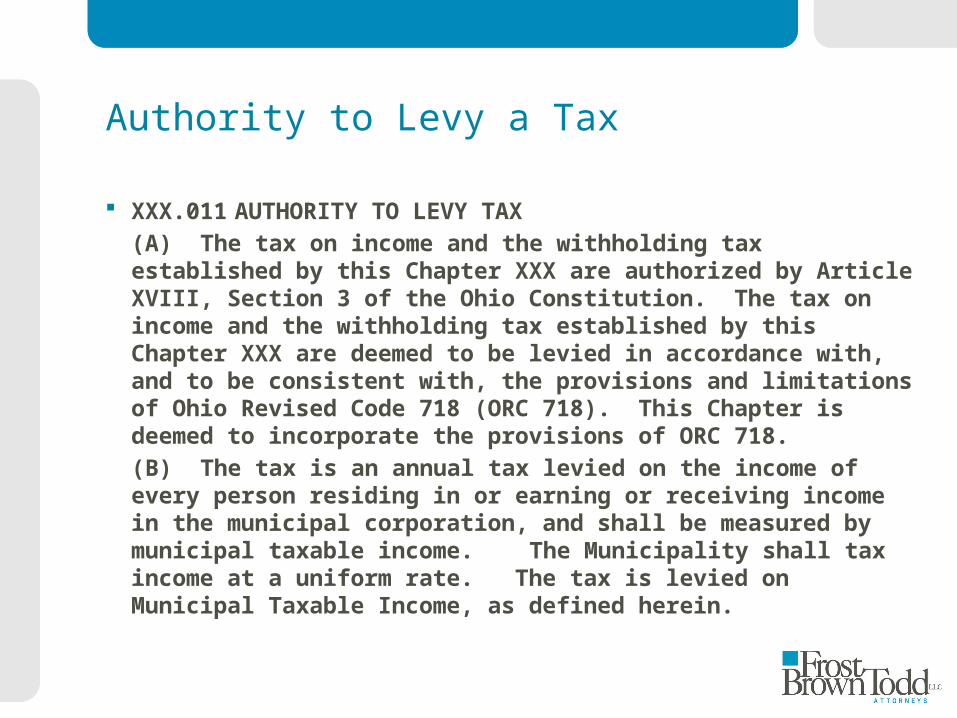

Authority to Levy a Tax

XXX.011 AUTHORITY TO LEVY TAX

(A) The tax on income and the withholding tax established by this Chapter XXX are authorized by Article XVIII, Section 3 of the Ohio Constitution. The tax on income and the withholding tax established by this Chapter XXX are deemed to be levied in accordance with, and to be consistent with, the provisions and limitations of Ohio Revised Code 718 (ORC 718). This Chapter is deemed to incorporate the provisions of ORC 718.

(B) The tax is an annual tax levied on the income of every person residing in or earning or receiving income in the municipal corporation, and shall be measured by municipal taxable income. The Municipality shall tax income at a uniform rate. The tax is levied on Municipal Taxable Income, as defined herein.

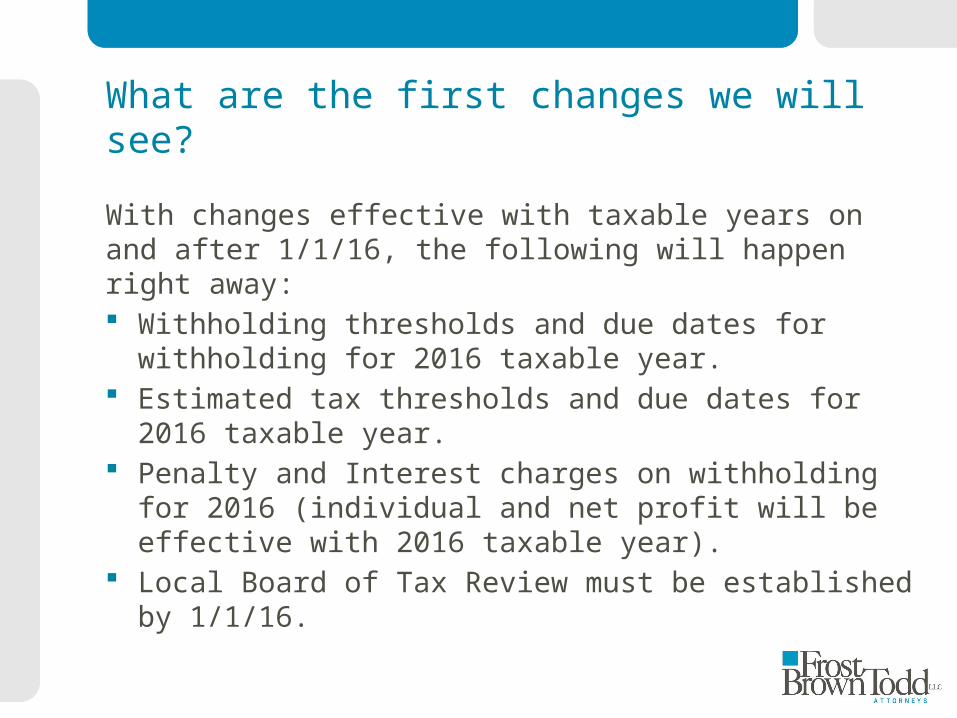

What are the first changes we will see?

With changes effective with taxable years on and after 1/1/16, the following will happen right away: Withholding thresholds and due dates for withholding

for 2016 taxable year. Estimated tax thresholds and due dates for 2016

taxable year. Penalty and Interest charges on withholding for 2016

(individual and net profit will be effective with 2016 taxable year).

Local Board of Tax Review must be established by 1/1/16.

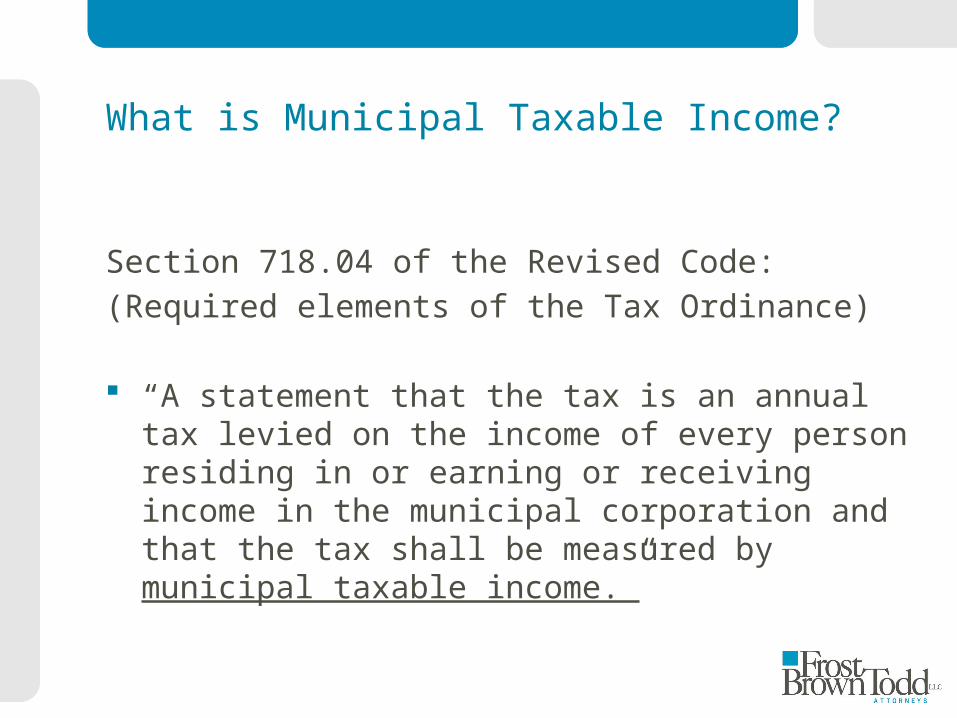

What is Municipal Taxable Income?

Section 718.04 of the Revised Code:

(Required elements of the Tax Ordinance)

“A statement that the tax is an annual tax levied on the income of every person residing in or earning or receiving income in the municipal corporation and that the tax shall be measured by municipal taxable income.”

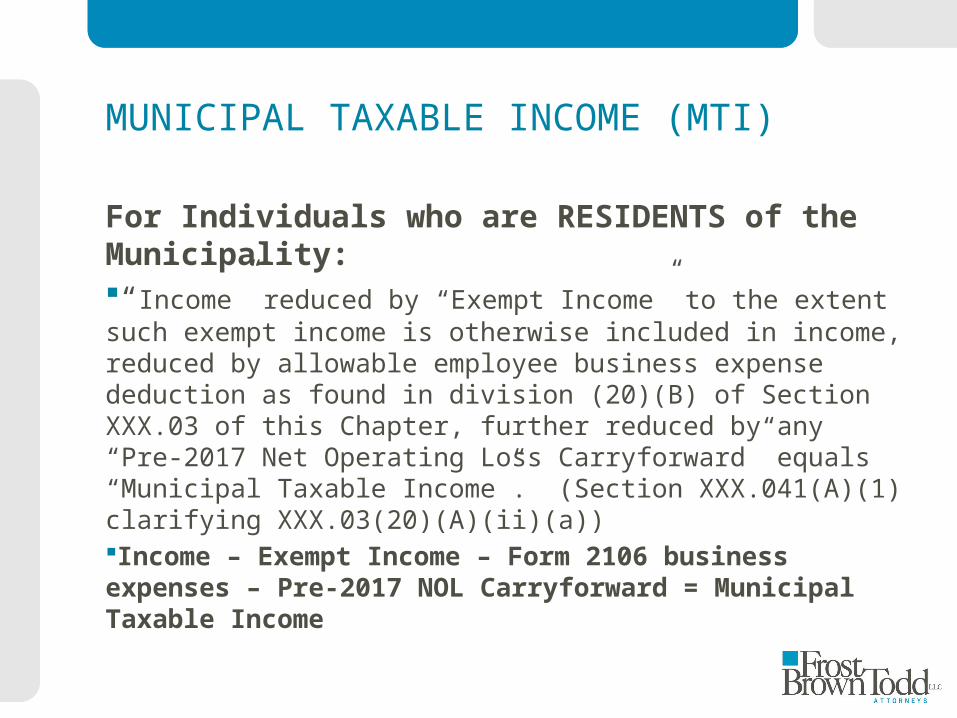

MUNICIPAL TAXABLE INCOME (MTI)

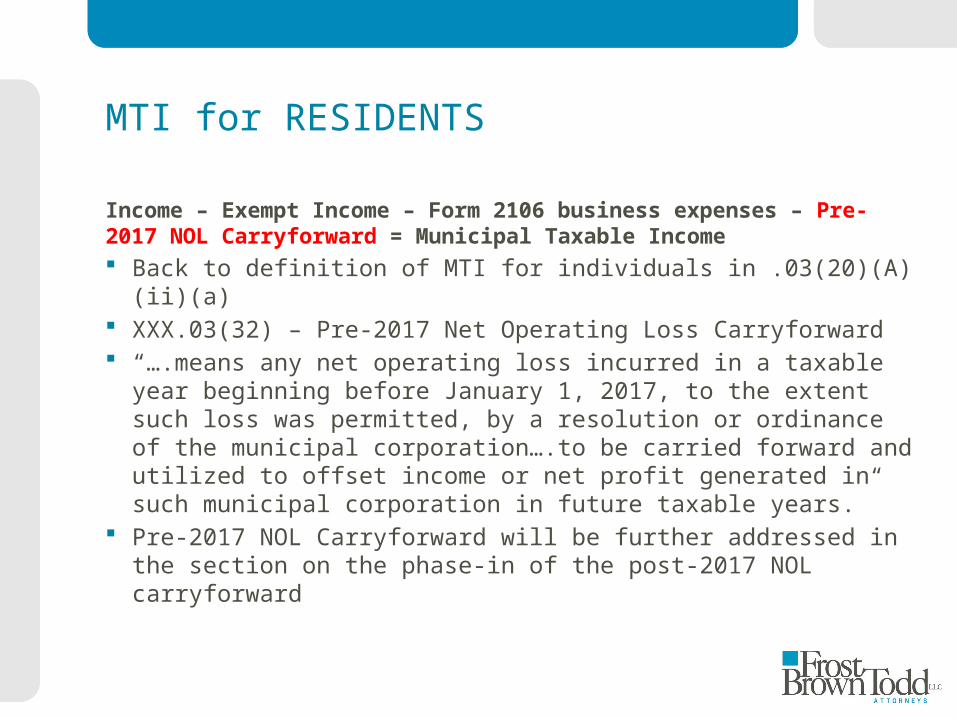

For Individuals who are RESIDENTS of the Municipality:“Income” reduced by “Exempt Income” to the extent such exempt income is otherwise included in income, reduced by allowable employee business expense deduction as found in division (20)(B) of Section XXX.03 of this Chapter, further reduced by any “Pre-2017 Net Operating Loss Carryforward” equals “Municipal Taxable Income”. (Section XXX.041(A)(1) clarifying XXX.03(20)(A)(ii)(a))Income – Exempt Income – Form 2106 business expenses – Pre-2017 NOL Carryforward = Municipal Taxable Income

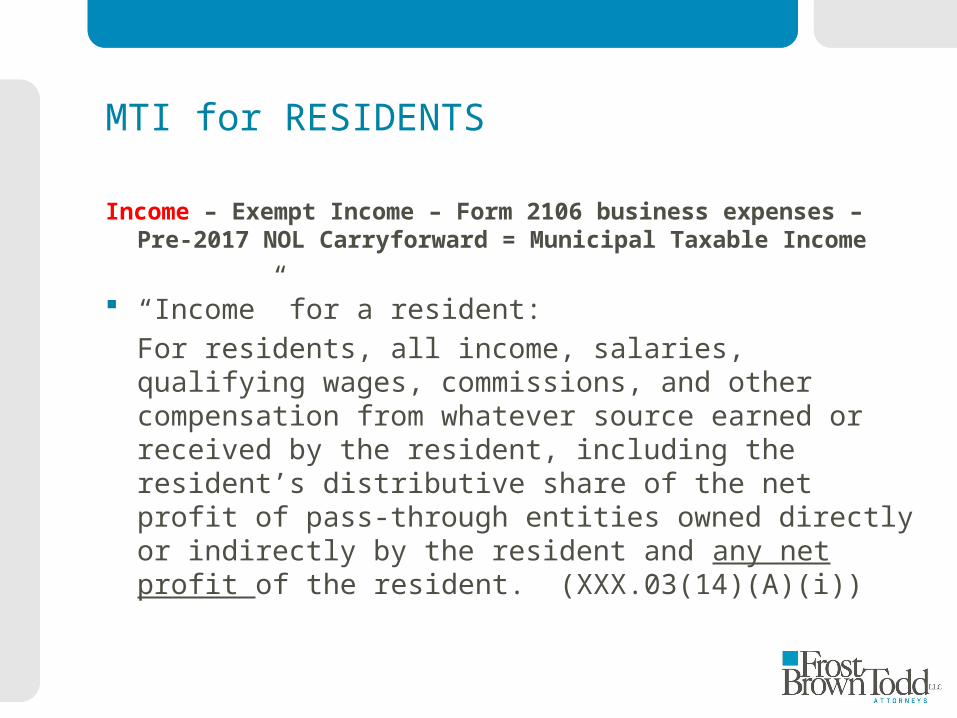

MTI for RESIDENTS

Income – Exempt Income – Form 2106 business expenses – Pre-2017 NOL Carryforward = Municipal Taxable Income

“Income” for a resident:

For residents, all income, salaries, qualifying wages, commissions, and other compensation from whatever source earned or received by the resident, including the resident’s distributive share of the net profit of pass-through entities owned directly or indirectly by the resident and any net profit of the resident. (XXX.03(14)(A)(i))

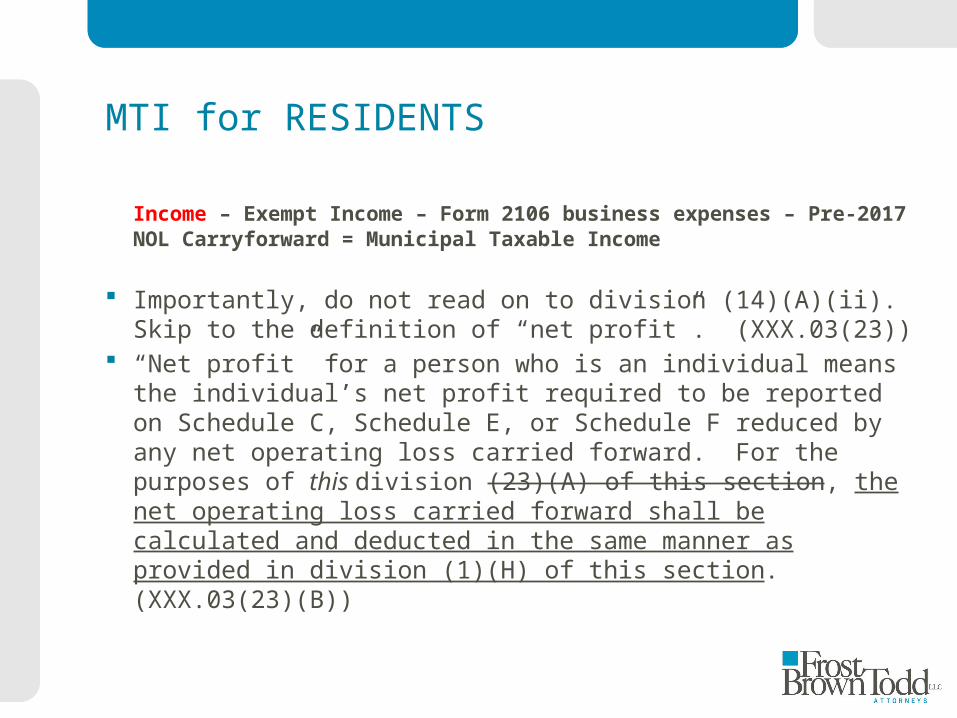

MTI for RESIDENTS

Income – Exempt Income – Form 2106 business expenses – Pre-2017 NOL Carryforward = Municipal Taxable Income

Importantly, do not read on to division (14)(A)(ii). Skip to the definition of “net profit”. (XXX.03(23))

“Net profit” for a person who is an individual means the individual’s net profit required to be reported on Schedule C, Schedule E, or Schedule F reduced by any net operating loss carried forward. For the purposes of this division (23)(A) of this section, the net operating loss carried forward shall be calculated and deducted in the same manner as provided in division (1)(H) of this section. (XXX.03(23)(B))

MTI for RESIDENTS

Income – Exempt Income – Form 2106 business expenses – Pre-2017 NOL Carryforward = Municipal Taxable Income

XXX.03(1)(H) – NEW Net Operating Loss Provision:

(H)(i) - Except as limited by divisions (1)(H)(ii), (iii) AND (iv) of this section, deduct any net operating loss incurred by the person in a taxable year beginning on or after January 1, 2017.

(H)(ii) – No person shall use the deduction allowed to offset qualifying wages.

(H)(iii) – Phase in of five year post-2017 NOL

New NOL Carryforward provision will be discussed below in section on MTI for Entities. This is how to draw the line from A to B as to NOL carryforward phase-in for individual taxpayers.

MTI for RESIDENTS

Income – Exempt Income – Form 2106 business expenses – Pre-2017 NOL Carryforward = Municipal Taxable Income

Return to XXX.03(14)(A)(ii) – Definition of “Income” for residents

(A)(ii) mentions the five-year carryforward but doesn’t mention the phase-in. One must assume that, although it is not expressly subject to (1)(H), this subsection does not override the five-year phase-in

Editorial remark – this is why the substantive provisions of legislation should not be contained in the definitional sections

MTI for RESIDENTS

Income – Exempt Income – Form 2106 business expenses – Pre-2017 NOL Carryforward = Municipal Taxable Income

Back to definition of MTI for individuals in XXX.03(20)(A)(ii)(a)

The types of income that are Exempt Income are listed in XXX.03(11)

NOTE: Subsection .03(11)(P) - This section deals with qualifying wages exempt from withholding because of the 20-day rule. Wages exempt from withholding under the 20 day rule are also exempt from taxation, with the exception of:

Wages would still be taxed by municipality of residence. (.03(11)(P)(ii))

Occasional Entrant provision will be further discussed in MTI for Non-residents section

MTI for RESIDENTS

Income – Exempt Income – Form 2106 business expenses – Pre-2017 NOL Carryforward = Municipal Taxable Income

Back to definition of MTI for individuals in XXX.03(20)(A)(ii)(a) - ”reduced as provided in division (20)(B)”

XXX.03(20)(B) – Allowable and Deductible Employee Business Expenses – “In computing the municipal taxable income of a taxpayer who is an individual, the taxpayer may subtract, as provided in division (20)(A)(ii)(a) or (iii) of this section, the amount of the individual's employee business expenses reported on the individual's form 2106 that the individual deducted for federal income tax purposes for the taxable year, subject to the limitation imposed by section 67 of the Internal Revenue Code.* For the municipal corporation in which the taxpayer is a resident, the taxpayer may deduct all such expenses allowed for federal income tax purposes.”

* - limited by 2% AGI

MTI for RESIDENTS

Income – Exempt Income – Form 2106 business expenses – Pre-2017 NOL Carryforward = Municipal Taxable Income Back to definition of MTI for individuals in .03(20)(A)(ii)(a) XXX.03(32) – Pre-2017 Net Operating Loss Carryforward “….means any net operating loss incurred in a taxable year

beginning before January 1, 2017, to the extent such loss was permitted, by a resolution or ordinance of the municipal corporation….to be carried forward and utilized to offset income or net profit generated in such municipal corporation in future taxable years.”

Pre-2017 NOL Carryforward will be further addressed in the section on the phase-in of the post-2017 NOL carryforward

MUNICIPAL TAXABLE INCOME

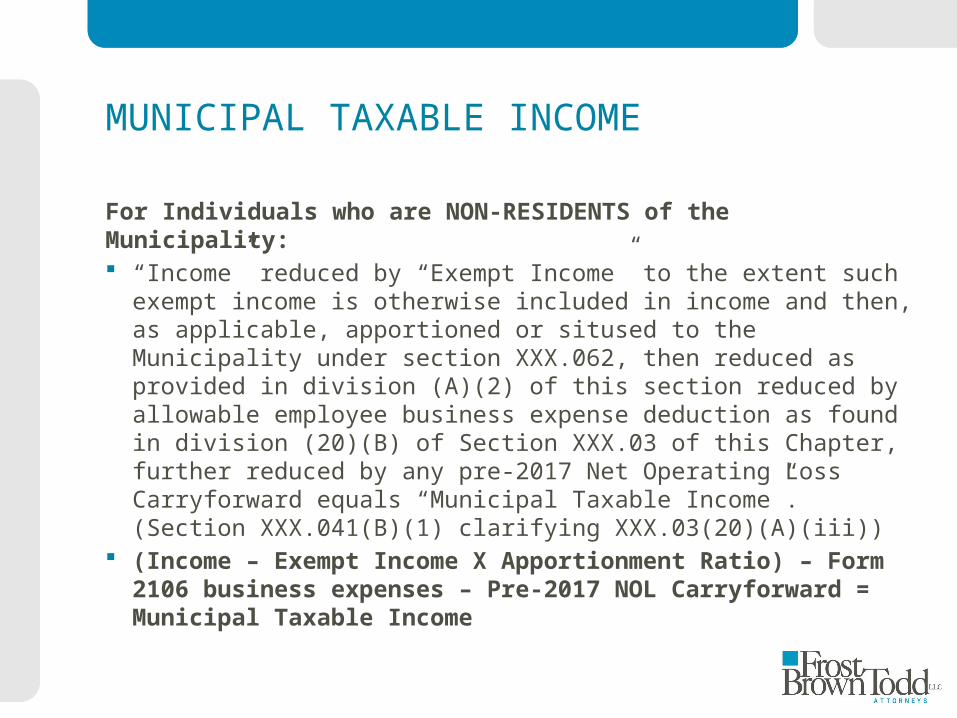

For Individuals who are NON-RESIDENTS of the Municipality: “Income” reduced by “Exempt Income” to the extent such

exempt income is otherwise included in income and then, as applicable, apportioned or sitused to the Municipality under section XXX.062, then reduced as provided in division (A)(2) of this section reduced by allowable employee business expense deduction as found in division (20)(B) of Section XXX.03 of this Chapter, further reduced by any pre-2017 Net Operating Loss Carryforward equals “Municipal Taxable Income”. (Section XXX.041(B)(1) clarifying XXX.03(20)(A)(iii))

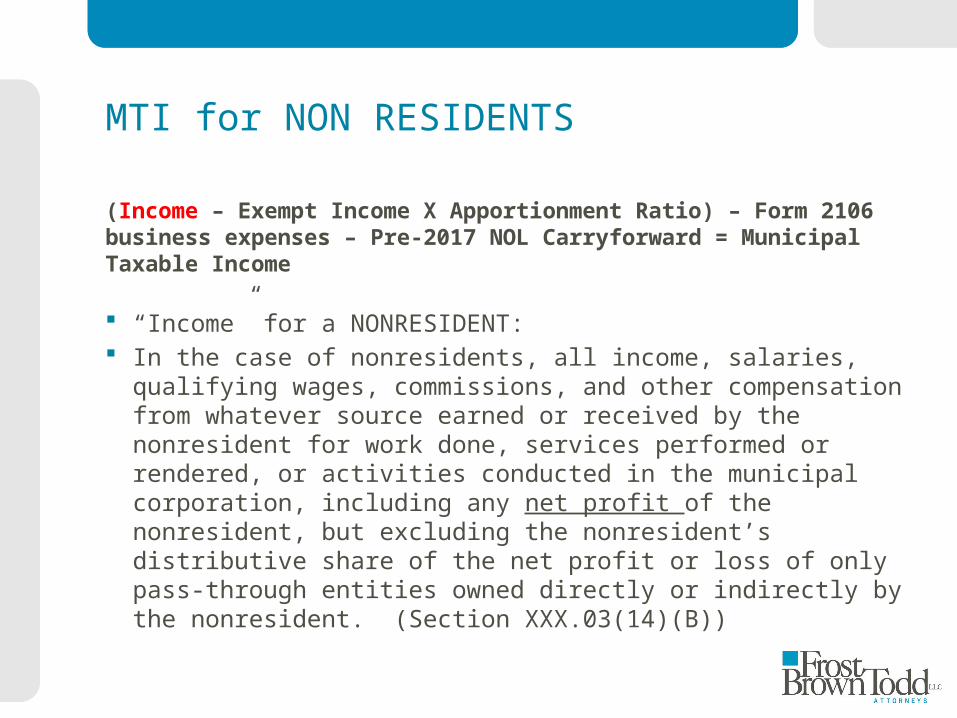

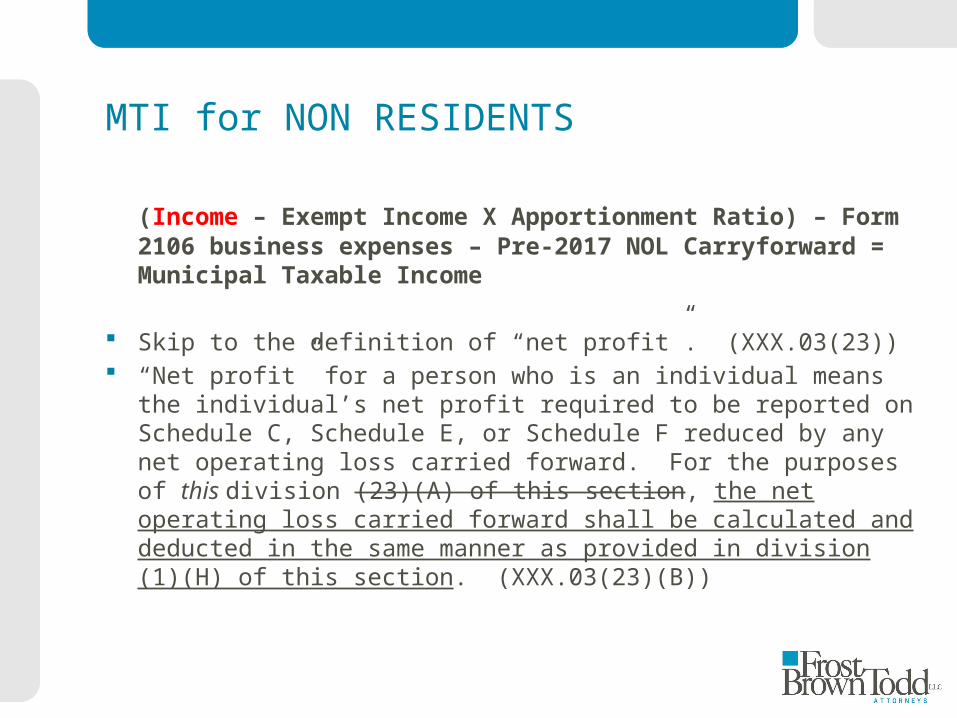

(Income – Exempt Income X Apportionment Ratio) – Form 2106 business expenses – Pre-2017 NOL Carryforward = Municipal Taxable Income

MTI for NON RESIDENTS

(Income – Exempt Income X Apportionment Ratio) – Form 2106 business expenses – Pre-2017 NOL Carryforward = Municipal Taxable Income

“Income” for a NONRESIDENT: In the case of nonresidents, all income, salaries, qualifying

wages, commissions, and other compensation from whatever source earned or received by the nonresident for work done, services performed or rendered, or activities conducted in the municipal corporation, including any net profit of the nonresident, but excluding the nonresident’s distributive share of the net profit or loss of only pass-through entities owned directly or indirectly by the nonresident. (Section XXX.03(14)(B))

MTI for NON RESIDENTS

(Income – Exempt Income X Apportionment Ratio) – Form 2106 business expenses – Pre-2017 NOL Carryforward = Municipal Taxable Income

Skip to the definition of “net profit”. (XXX.03(23)) “Net profit” for a person who is an individual means the

individual’s net profit required to be reported on Schedule C, Schedule E, or Schedule F reduced by any net operating loss carried forward. For the purposes of this division (23)(A) of this section, the net operating loss carried forward shall be calculated and deducted in the same manner as provided in division (1)(H) of this section. (XXX.03(23)(B))

MTI for NON RESIDENTS

(Income – Exempt Income X Apportionment Ratio) – Form 2106 business expenses – Pre-2017 NOL Carryforward = Municipal Taxable Income

XXX.03(1)(H) – NEW Net Operating Loss Provision:

(H)(i) - Except as limited by divisions (1)(H)(ii), (iii) AND (iv) of this section, deduct any net operating loss incurred by the person in a taxable year beginning on or after January 1, 2017.

(H)(ii) – No person shall use the deduction allowed to offset qualifying wages.

(H)(iii) – Phase in of five year post-2017 NOL

New NOL Carryforward provision will be discussed below in section on MTI for Entities. This is how to draw the line from A to B as to NOL carryforward phase-in for individual taxpayers.

MTI for NON RESIDENTS

(Income – Exempt Income X Apportionment Ratio) – Form 2106 business expenses – Pre-2017 NOL Carryforward = Municipal Taxable Income

Back to definition of MTI for individuals in XXX.03(20)(A)(iii)

The types of income that are Exempt Income are listed in XXX.03(11)

NOTE: Subsection .03(11)(P) - This section deals with qualifying wages exempt from withholding because of the 20-day rule (“Occasional Entrant”” rule). Wages exempt from withholding under the 20 day rule are also EXEMPT FROM TAXATION, with the exception of: Does not apply to qualifying wages that an employer elects to withhold as a

“courtesy”. (.03(11)(P)(iii)) Other exception for “principal place of work” and if refund was obtained.

(.03(11)(P)(iv))

MTI for NON RESIDENTS

(Income – Exempt Income X Apportionment Ratio) – Form 2106 business expenses – Pre-2017 NOL Carryforward = Municipal Taxable Income

Occasional Entrant Rule will be discussed in detail on Thursday afternoon 30,000 foot view: Employee’s qualifying wages are exempt from taxation by

a particular municipality if the employee performed personal services in that municipality on twenty or fewer days in a calendar year (See XXX.052(B)(1)) Query: how does the employer divine this on Jan. 1? If wrong, of course, withholding only

begins on 21st day.

“Small employers” (see section XXX.03(43) – total revenue less than $500,000) remit withholding taxes on to the municipality in which the employers fixed location is located (See XXX.052(E))

Also, Tax Administrator and employer can enter into an agreement and override (section XXX.052(F))

MTI for NON RESIDENTS

(Income – Exempt Income X Apportionment Ratio) – Form 2106 business expenses – Pre-2017 NOL Carryforward = Municipal Taxable Income

Hearken back to definition of “net profit” which includes (unapportioned) net profit reduced by any (unapportioned) NOL carried forward (XXX.03(23)(B)) – this calculation has already taken place – is there still a net profit to tax?

Skip to section XXX.062 – this section applies to taxpayers engaged in business or profession except resident individuals, and requires that “net profit” shall have a taxable situs in the municipality in the same proportion as the average ratio of several ratios relating to real/personal property, wages and other compensation and gross receipts

Alternative apportionment factors may be proposed or required by the Tax Administrator

MTI for NON RESIDENTS

(Income – Exempt Income X Apportionment Ratio) – Form 2106 business expenses – Pre-2017 NOL Carryforward = Municipal Taxable Income

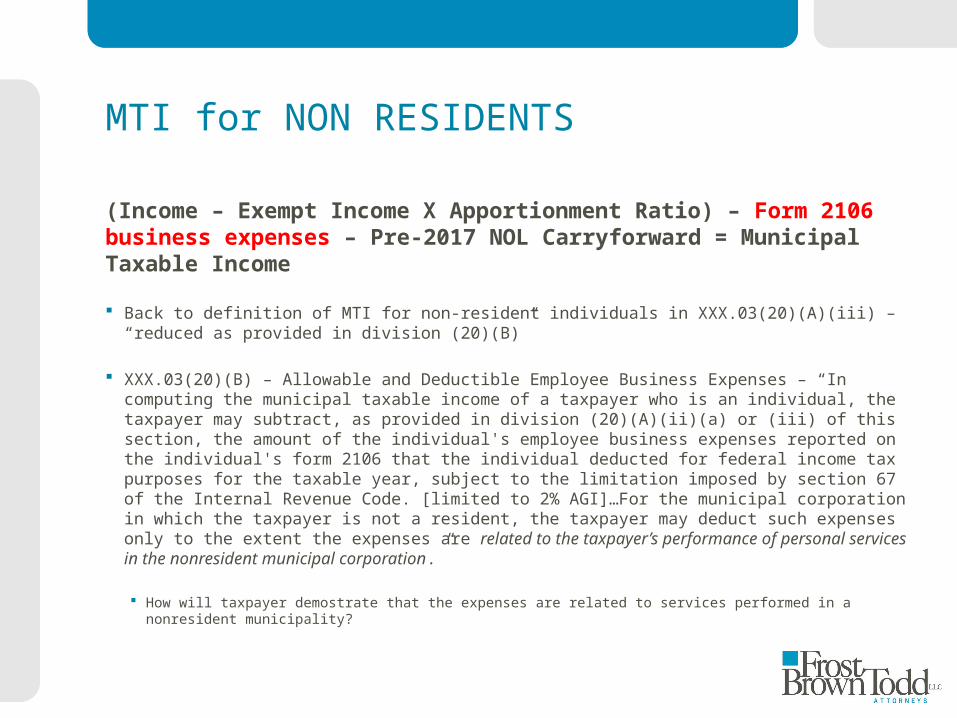

Back to definition of MTI for non-resident individuals in XXX.03(20)(A)(iii) – “reduced as provided in division (20)(B)”

XXX.03(20)(B) – Allowable and Deductible Employee Business Expenses – “In computing the municipal taxable income of a taxpayer who is an individual, the taxpayer may subtract, as provided in division (20)(A)(ii)(a) or (iii) of this section, the amount of the individual's employee business expenses reported on the individual's form 2106 that the individual deducted for federal income tax purposes for the taxable year, subject to the limitation imposed by section 67 of the Internal Revenue Code. [limited to 2% AGI]…For the municipal corporation in which the taxpayer is not a resident, the taxpayer may deduct such expenses only to the extent the expenses are related to the taxpayer’s performance of personal services in the nonresident municipal corporation.”

How will taxpayer demostrate that the expenses are related to services performed in a nonresident municipality?

MTI for NON RESIDENTS

(Income – Exempt Income X Apportionment Ratio) – Form 2106 business expenses – Pre-2017 NOL Carryforward = Municipal Taxable Income

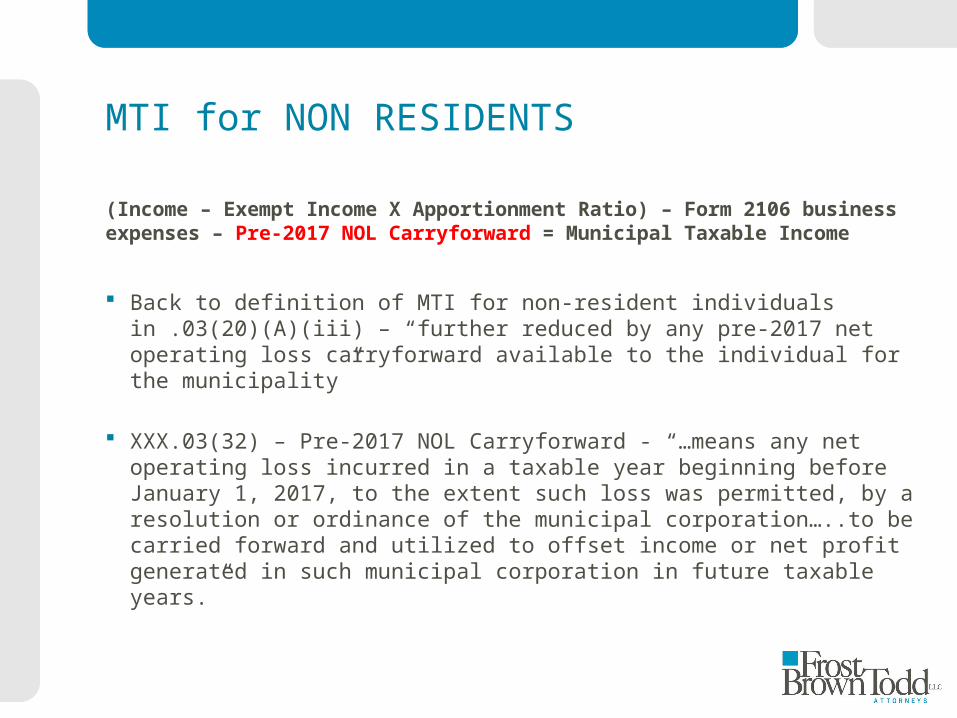

Back to definition of MTI for non-resident individuals in .03(20)(A)(iii) – “further reduced by any pre-2017 net operating loss carryforward available to the individual for the municipality”

XXX.03(32) – Pre-2017 NOL Carryforward - “…means any net operating loss incurred in a taxable year beginning before January 1, 2017, to the extent such loss was permitted, by a resolution or ordinance of the municipal corporation…..to be carried forward and utilized to offset income or net profit generated in such municipal corporation in future taxable years.”

MUNICIPAL TAXABLE INCOME

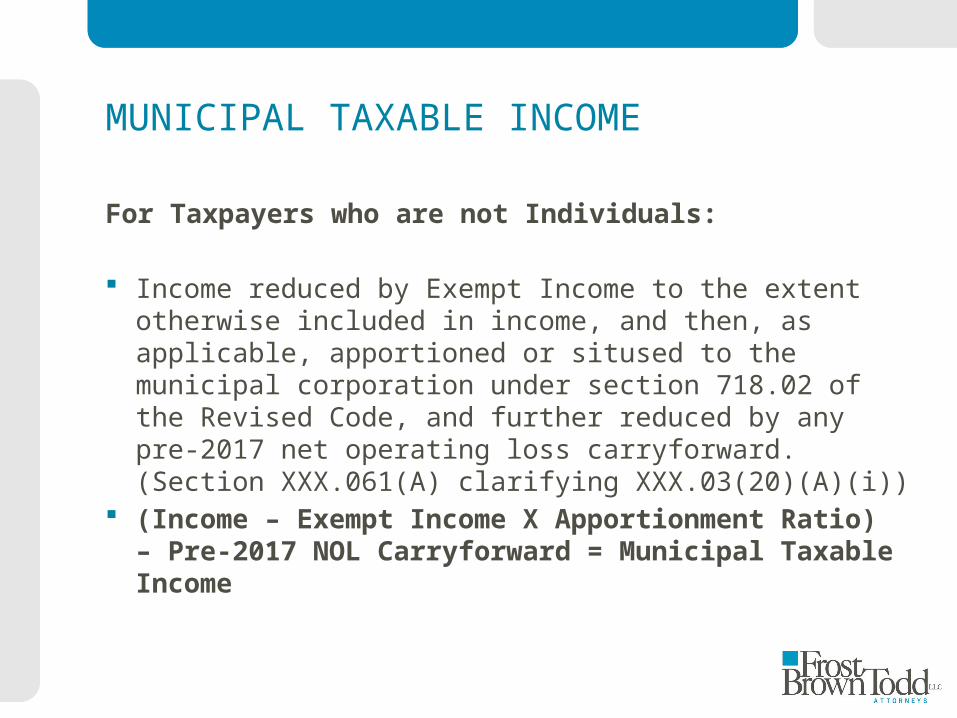

For Taxpayers who are not Individuals:

Income reduced by Exempt Income to the extent otherwise included in income, and then, as applicable, apportioned or sitused to the municipal corporation under section 718.02 of the Revised Code, and further reduced by any pre-2017 net operating loss carryforward. (Section XXX.061(A) clarifying XXX.03(20)(A)(i))

(Income – Exempt Income X Apportionment Ratio) – Pre-2017 NOL Carryforward = Municipal Taxable Income

MTI for TAXPAYERS WHO ARE NOT INDIVIDUALS

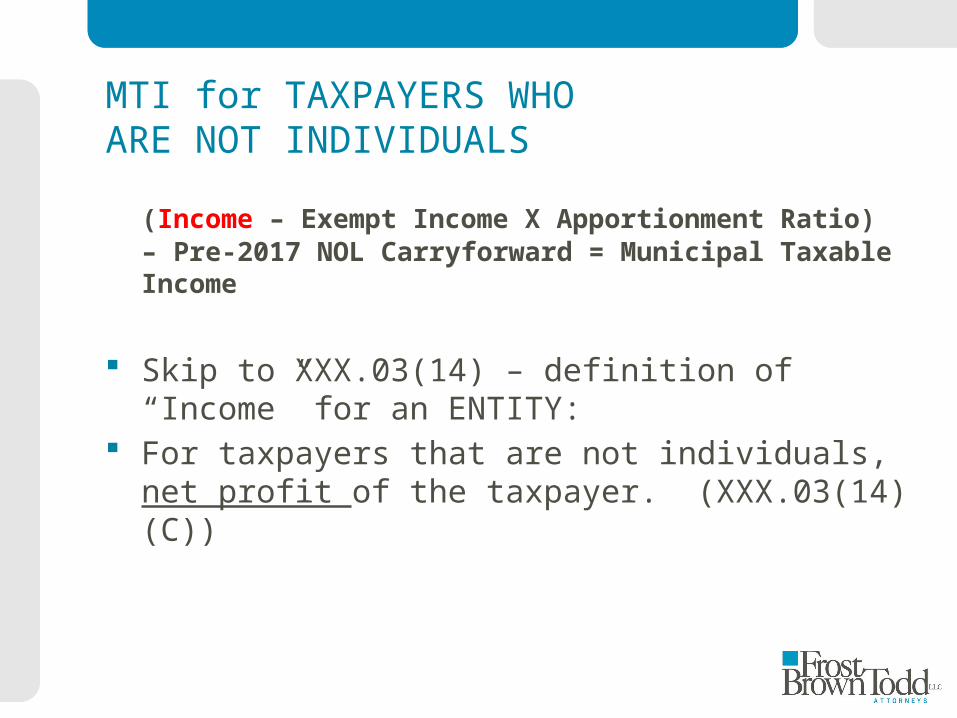

(Income – Exempt Income X Apportionment Ratio) – Pre-2017 NOL Carryforward = Municipal Taxable Income

Skip to XXX.03(14) – definition of “Income” for an ENTITY:

For taxpayers that are not individuals, net profit of the taxpayer. (XXX.03(14)(C))

MTI for TAXPAYERS WHO ARE NOT INDIVIDUALS

(Income – Exempt Income X Apportionment Ratio) – Pre-2017 NOL Carryforward = Municipal Taxable Income

Skip to definition of “net profit” (XXX.03(23) “Net profit” for a person other than an individual means

adjusted federal taxable income.” (XXX.03(23)(A)) Skip to definition of “adjusted federal taxable income”

(XXX.03(1)) “Adjusted Federal Taxable Income” for a person required to

file as a C corporation, means a C corporation’s federal taxable income before net operating losses and special deductions as determined under the [IRC] adjusted as follows… (XXX.03(1)) – enumerated adjustments (A) – (J)

MTI for TAXPAYERS WHO ARE NOT INDIVIDUALS

(Income – Exempt Income X Apportionment Ratio) – Pre-2017 NOL Carryforward = Municipal Taxable Income

AFTI includes the utilization of the new NOL carryforward from prior years (XXX.03(1)(H))

Skip to (H)(iv) first – if your municipality permitted such, any available pre-2017 NOL carryforward must be utilized first.

Back to (H)(i) – post-1/1/2017 (“post-2017”) NOL shall be deducted from net profit (that is reduced by exempt income although we haven’t got to that part of the formula yet) to extent necessary to reduce MTI to zero

Any remaining unused NOL may be carried forward not more than 5 consecutive years from year in which the loss was incurred (or until utilized)

MTI for TAXPAYERS WHO ARE NOT INDIVIDUALS

(Income – Exempt Income X Apportionment Ratio) – Pre-2017 NOL Carryforward = Municipal Taxable Income

NOL Carryforward 5-year Phase-in is contained in XXX.03(1)(H)(iii)(a) and (b): (iii) (a) For taxable years beginning in 2018, 2019, 2020, 2021, or

2022, a person may not deduct, for purposes of an income tax levied by a municipal corporation that levies an income tax before January 1, 2016, more than fifty per cent of the amount of the deduction otherwise allowed by division (1)(H)(i) of this section.

(b) For taxable years beginning in 2023 or thereafter, a person may deduct, for purposes of an income tax levied by a municipal corporation that levies an income tax before January 1, 2016, the full amount allowed by division (1)(H)(i) of this section.

MTI for TAXPAYERS WHO ARE NOT INDIVIDUALS

(Income – Exempt Income X Apportionment Ratio) – Pre-2017 NOL Carryforward = Municipal Taxable Income

Query: what is “the amount of the deduction otherwise allowed by division (1)(H)(i) of this section”? Is it the amount necessary to reduce municipal taxable income to zero, in

which case 50% of that amount would be the amount necessary to cut MTI in half?

This would be a reasonable interpretation – phase-in the bottom line impact on municipalities

Or would it be the total amount of accumulated NOL carryforward from prior years, divided by two, and then compared to MTI?

This approach in theory could wipe out all MTI for a particular year if the accumulated NOL carryforward is 2X greater than MTI

More to come on this, I’m sure…

MTI for TAXPAYERS WHO ARE NOT INDIVIDUALS

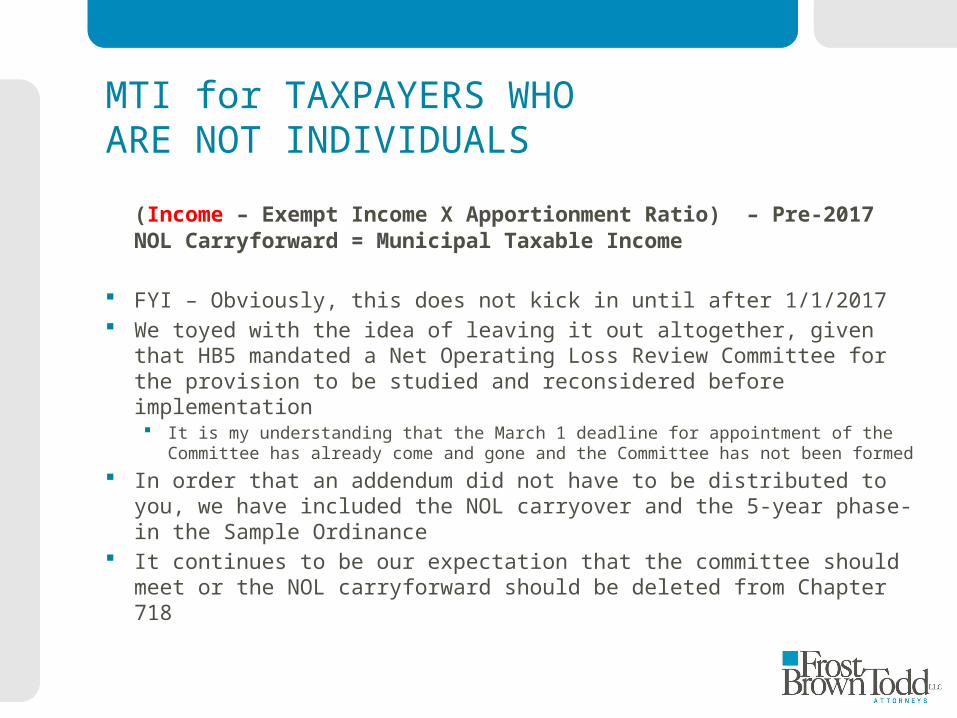

(Income – Exempt Income X Apportionment Ratio) – Pre-2017 NOL Carryforward = Municipal Taxable Income

FYI – Obviously, this does not kick in until after 1/1/2017 We toyed with the idea of leaving it out altogether, given that HB5

mandated a Net Operating Loss Review Committee for the provision to be studied and reconsidered before implementation It is my understanding that the March 1 deadline for appointment of the

Committee has already come and gone and the Committee has not been formed

In order that an addendum did not have to be distributed to you, we have included the NOL carryover and the 5-year phase-in the Sample Ordinance

It continues to be our expectation that the committee should meet or the NOL carryforward should be deleted from Chapter 718

MTI for TAXPAYERS WHO ARE NOT INDIVIDUALS

(Income – Exempt Income X Apportionment Ratio) – Pre-2017 NOL Carryforward = Municipal Taxable Income

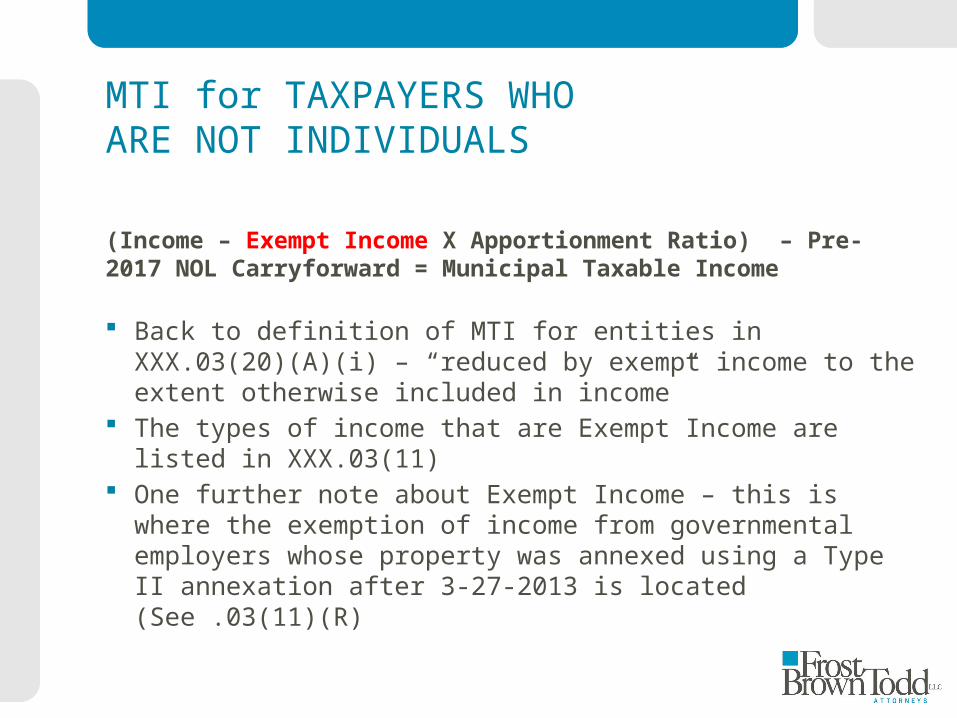

Back to definition of MTI for entities in XXX.03(20)(A)(i) – “reduced by exempt income to the extent otherwise included in income”

The types of income that are Exempt Income are listed in XXX.03(11)

One further note about Exempt Income – this is where the exemption of income from governmental employers whose property was annexed using a Type II annexation after 3-27-2013 is located (See .03(11)(R)

MTI for TAXPAYERS WHO ARE NOT INDIVIDUALS

(Income – Exempt Income X Apportionment Ratio) – Pre-2017 NOL Carryforward = Municipal Taxable Income

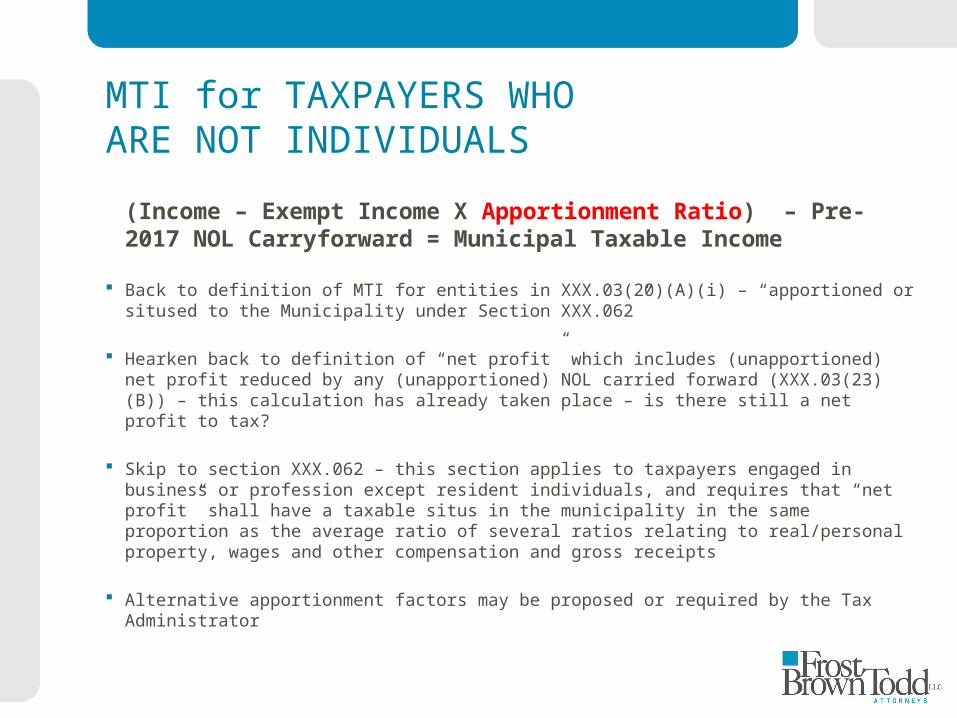

Back to definition of MTI for entities in XXX.03(20)(A)(i) – “apportioned or sitused to the Municipality under Section XXX.062”

Hearken back to definition of “net profit” which includes (unapportioned) net profit reduced by any (unapportioned) NOL carried forward (XXX.03(23)(B)) – this calculation has already taken place – is there still a net profit to tax?

Skip to section XXX.062 – this section applies to taxpayers engaged in business or profession except resident individuals, and requires that “net profit” shall have a taxable situs in the municipality in the same proportion as the average ratio of several ratios relating to real/personal property, wages and other compensation and gross receipts

Alternative apportionment factors may be proposed or required by the Tax Administrator

MTI for TAXPAYERS WHO ARE NOT INDIVIDUALS

(Income – Exempt Income X Apportionment Ratio) – Pre-2017 NOL Carryforward = Municipal Taxable Income

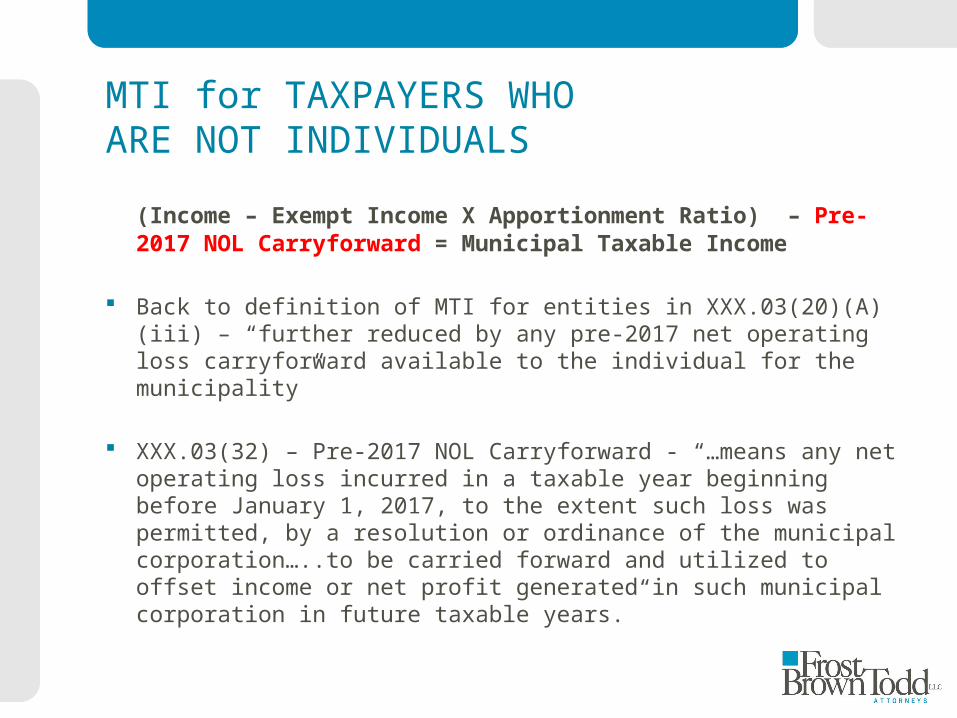

Back to definition of MTI for entities in XXX.03(20)(A)(iii) – “further reduced by any pre-2017 net operating loss carryforward available to the individual for the municipality”

XXX.03(32) – Pre-2017 NOL Carryforward - “…means any net operating loss incurred in a taxable year beginning before January 1, 2017, to the extent such loss was permitted, by a resolution or ordinance of the municipal corporation…..to be carried forward and utilized to offset income or net profit generated in such municipal corporation in future taxable years.”