Embed Size (px)

Citation preview

Hong Kong’s Financial Market Interactions with the U.S. and Mainland China in Crisis and

Tranquil Times

Dong He, Zhiwei Zhang, and Honglin Wang

The views and analysis expressed in this paper are those of the authors, and do not necessarily represent the views of the Hong Kong Monetary Authority.

Hong Kong’s Economic linkages with the US and Mainland China

• Hong Kong is an entrepôt that intermediates trade between Mainland and the world

• Currency board system that pegs the HK dollar to the US dollar with a band of 7.75 to 7.85 HKD/USD

• In recent years, many Mainland firms are cross-listed in HK and Shanghai

Studies on economic and financial linkages

• Gengberg, Liu, and Jin (2008)– Business correlations between HK, Mainland China,

and US

• He, Leung, and Ng (2008)– Effect of Mainland macro variables on HIBOR

• Peng, Miao, and Chow (2008)– Price convergence between dual-listed A and H

shares

What this paper does…

• Study the interaction of equity, money, and FX markets in HK with those in the US and Mainland China

• Daily data that facilitates identification

• Compare interactions from three periods– Burst of IT bubble (2001)– Tranquil period (2002-Aug 2007)– Financial crisis (Aug 2007-present)

Presentation Outline

• Visual description of dynamics in equity, money, and FX markets in HK, and their linkages with markets in US and China

• A VAR model to quantify the linkages in the current financial crisis and in earlier years

The equity market in HK has traditionally been influenced by what happened in the US

0.0

0.2

0.4

0.6

0.8

May-01 May-02 May-03 May-04 May-05 May-06 May-07 May-08

Correlation between daily returns in HK and USequity markets, 100-day moving window

Correlation between returns in HK and Shanghai equity markets has increased ...

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

May-01 May-02 May-03 May-04 May-05 May-06 May-07 May-08

Correlation between daily returns in HK andShanghai equity markets, 100-day moving window

Correlation between daily returns in HK and USequity markets, 100-day moving window

… as Mainland stocks listed in Hong Kong gained more weights

20

25

30

35

40

45

50

55

60

2001 2003 2005 2007 Mar 2009

Weights of Mainland stocks inHong Kong Stock Exchange

In money market, LIBOR-HIBOR spread was small until Sept 2003 when speculation

on RMB appreciation emerged

0

1

2

3

4

5

6

7

Jan-01 Jul-01 Jan-02 Jul-02 Jan-03 Jul-03

LIBOR

HIBOR

Mainland Repo Rate

Before financial crisis started, LIBOR-HIBOR correlation was weak, and HIBOR was heavily

influenced by intensive IPO activities

0

2

4

6

8

10

12

Oct-03

Ap

r-04

Oct-04

Ap

r-05

Oct-05

Ap

r-06

Oct-06

Ap

r-07

Oct-07

LIBOR

HIBOR

Mainland Repo Rate

IPO activities and HIBOR

0

200

400

600

800

1000

Jan-06 May-06 Oct-06 Mar-07 Aug-07 Dec-07 May-08 Oct-08

0

1

2

3

4

5

6

7HK$, Billions %

HIBOR, RHSFunds Frozen forHK IPO, LHS

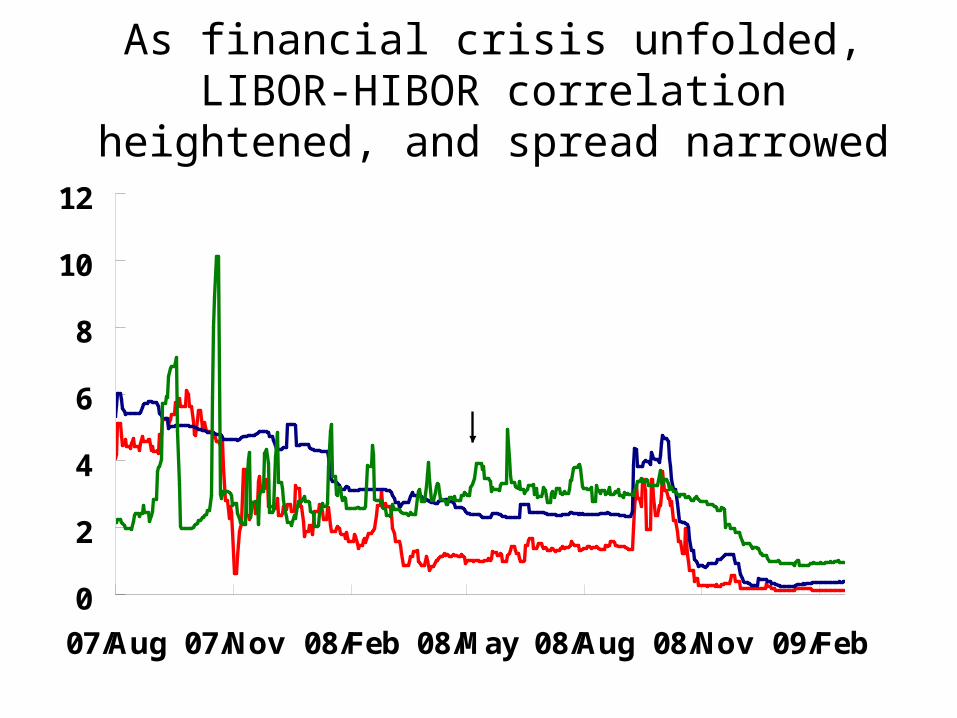

As financial crisis unfolded, LIBOR-HIBOR correlation heightened, and spread narrowed

0

2

4

6

8

10

12

07/Aug 07/Nov 08/Feb 08/May 08/Aug 08/Nov 09/Feb

Mainland repo rateLIBOR

HIBOR

FX market: HKD exchange rate subject to equity related capital flows and flight-to-safety

7.7

7.75

7.8

7.85

7.9

2001 2002 2003 2004 2005 2006 2007 2008 2009

USD/HKD

-5-4-3-2-1012345

(%)

USD/HKD(lhs)

LIBOR/HIBORspread (rhs)

Econometric Model

• Vector Autoregression that includes daily data on– Equity markets returns in S&P, Shanghai index,

and Hang Seng index

– HIBOR, LIBOR, and Mainland repo rate

– US bond price

– US$/HK$ exchange rate

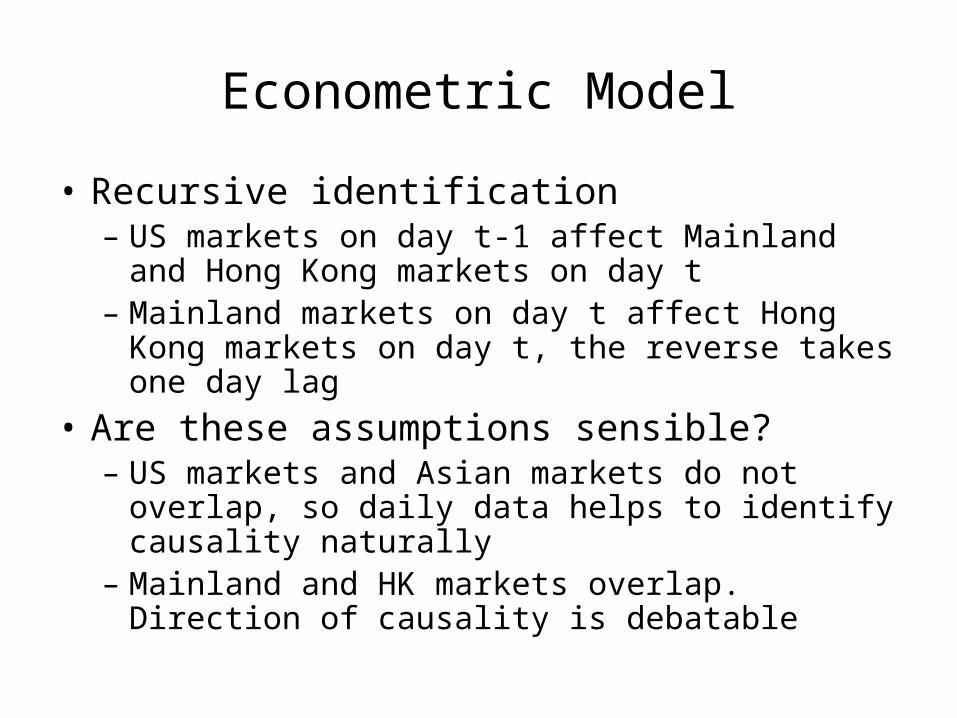

Econometric Model

• Recursive identification– US markets on day t-1 affect Mainland and Hong

Kong markets on day t– Mainland markets on day t affect Hong Kong

markets on day t, the reverse takes one day lag

• Are these assumptions sensible?– US markets and Asian markets do not overlap, so

daily data helps to identify causality naturally– Mainland and HK markets overlap. Direction of

causality is debatable

Does HK equity market move Shanghai equity market?

• Identify Hong Kong news that moved the HK equity market. These news did not move Shanghai market

• Identify Mainland China news that moved the Shanghai market. These news did move Hong Kong market

• Granger causality test also indicates the direction of causality goes from Shanghai to Hong Kong

Compare estimates from there periods

• Burst of IT bubble (2 Jan 2001 – 31 Dec 2001)

• Tranquil period (2 Jan 2002 – 8 Aug 2007)

• Current crisis (9 Aug 2007 – 5 Mar 2009)

Shanghai gaining influence on Hang Seng index, US still more important

0.0

0.2

0.4

0.6

0.8

1.0

Burst of ITbubble

Tranquil periodbetween crises

Current creditcrisis

Effect of S&P on Hang Seng index

Effect of Shanghai market on Hang Seng index

US market affects Hang Seng index through Shanghai in current crisis

0.0

0.2

0.4

0.6

0.8

1.0

Burst of IT bubble Tranquil periodbetween crises

Current creditcrisis

Direct impact Indrect impact through Shanghai

Money market: LIBOR-HIBOR linkage emerged again, Mainland factor not important

Burst of ITbubble

Tranquil periodbetween crises

Currentcredit crisis

LIBOR 0.48 0 0.44

Mainland Reporate

0 0 0

Funds Frozenfor HK IPO

0 0.15 0

Depedent variable: HIBOR

FX market: HIBOR remains statistically significant but effect is small

Burst of ITbubble

Tranquil periodbetween crises

Currentcredit crisis

S&P 0 0 0

LIBOR 0 0 0.037

US Bondprice

0 0 0

Shanghaistock index

0 0 0

Mainlandinterest rate

0 0 0

Hang Sengindex

0 -0.002 0

HIBOR -0.012 -0.014 -0.035

Dependent variable: HK$/US$ exchange rate

To summarize, in the equity market…

• Influence of the Mainland equity market on the Hong Kong equity market has increased substantially in the current financial crisis, but it is still less important than the influence of the US equity market

• The US market started to affect Hong Kong indirectly through its influence on the Shanghai market in recent years

In the money market…

• HIBOR and LIBOR moved together in both crises in 2001 and 2008 as Hong Kong dollar was used as a safe haven along with the US dollar.

• During the tranquil period between the two crises, HIBOR was significantly influenced by IPO activities in the Hong Kong equity market, and there was little correlation between HIBOR and LIBOR at the daily frequency, even though the spread between them remained relatively narrow most of the time.

In the FX market…

• The Hong Kong dollar exchange rate was influenced mainly by short-term interest rates. It is difficult to detect independent and significant influences from the equity market.

• This could be due to the two forces in the FX market going in opposite directions during the current crisis: capital outflow related to equity market collapse, and capital inflow caused by the unwinding of currency carry trade and repatriation of overseas assets by Hong Kong residents.

A broad interpretation of findings

• Hong Kong financial markets appear to be more aligned with the US markets in turbulent times…

• but relatively more integrated with Mainland markets during the tranquil period