Embed Size (px)

Citation preview

1

NO MORTGAGE,

NO DEPOSIT,

NO PROBLEM!

By John Lee & Vincent Wong

STEP-BY-STEP GUIDE

TO LEASE OPTIONS

Home Study Course

2

About the authors

John Lee started in property at the age of

21 and has bought over 154 properties for

himself and for other investors. His goals

were to never work again, become a full

time entrepreneur and owns a Lamborghini.

He achieved this at the age of 27. John is

also a property mentor, inspirational

speaker and has helped thousands of like-minded people achieve

their property goals.

John is a property expert on Inside Property Radio, Your Property

Network Magazine, co-host on Loveproperty.org, founder of

propertycow.co.uk, Founder of Deal Closer, and founder of his

property buying company Complete In 28 Days Ltd.

John’s claim to fame was when he landed a part in the hit TV show

“Little Britain”.

John Lee is known for his unique and creative negotiation style that

has contributed to his multi-million pound portfolio. To find out

more about John do a search on You Tube for John Lee.

Vincent Wong is the founder of Network Property Buyers and

Network Property Investment.co.uk.

A well respected figure in the BMV circuit, Vincent

has generated more than 30,000 below market

value property leads in the last 24 months and

helped hundreds of investors buy properties with

little or no money down.

Apart from his own multi-million pound property

portfolio and expertise in internet marketing, Vincent’s specialty is

acquiring properties using lease options.

He and John Lee have taught many investors how to buy properties

using no mortgage and deposit in their office in Milton Keynes.

Find out more about Vincent’s below market value leads and lease

options course at www.networkpropertyinvestment.co.uk.

3

Contents 1. How to Use this Home Study Course .......................................... 9

1.1. What’s in the Home Study Course? .................................... 9

1.2. Successful Learning ........................................................... 10

1.3. Mindset ............................................................................. 10

Video One (mindset) ............................................................... 10

1.4. Below Market Value Investing .......................................... 10

1.5. Why Do We Want to Do Lease Options? .......................... 11

1.5.1. The Credit Crunch ..................................................... 11

Video 2 (The Advantages of Using Lease Options) ....................... 12

http://www.wealthdragons.co.uk/homestudyvideo2.html ......... 12

Exercise One.................................................................................. 13

1.6. Objectives for This Course ................................................ 14

2. What’s a Lease Option? ............................................................ 15

2.1. BMV vs. Lease Options ...................................................... 15

2.2. It’s All about Terms ........................................................... 15

Video 3 (The 3 Value Components of Lease options) ................... 15

http://www.wealthdragons.co.uk/homestudyvideo3.html ......... 15

Exercise 2a .................................................................................... 16

Exercise 2b .................................................................................... 16

2.3. The Two Things that Make Up a Lease Option ................. 17

2.4. The Option ........................................................................ 17

Audio One (Futures & Options) .................................................... 18

2.5. Some Jargons .................................................................... 18

Exercise 3a .................................................................................... 19

Exercise 3b .................................................................................... 20

2.6. Call & Put Options ............................................................. 20

2.6.1. What’s a Call Option? ............................................... 20

2.6.2. Example of a Call option ........................................... 21

2.6.3. What’s a Put Option? ................................................ 21

2.6.4. Example of a Put Option ........................................... 21

2.7. What Type of Option is in a Typical Property Deal? ..... 22

2.8. In the Money & Out of the Money ................................... 22

2.9. An Option Application – Purchase Option ........................ 23

4

2.9.1. What Do You Use a Purchase Option For? ............... 23

2.9.2. Purchase Option Sample ........................................... 24

2.10. The Lease ...................................................................... 25

2.10.1. Some Questions about Controlling Cash Flow .......... 25

2.10.2. You Need a Legal System .......................................... 26

2.11. The Management Model .............................................. 27

2.11.1. The Management Legal System ................................ 27

2.11.2. The Tenancy Agreement ........................................... 28

2.11.3. The Management Fee ............................................... 28

2.11.4. Who Pays Who? ........................................................ 28

2.11.5. The Management System Paperwork ....................... 28

2.11.6. The Management Agent’s Responsibilities ............... 29

2.11.7. The Seller’s Responsibilities ...................................... 29

2.11.8. Other Important Features ......................................... 29

Exercise 4 ...................................................................................... 30

2.12. The Power of Attorney .................................................. 31

2.12.1. What is the Power of Attorney? ............................... 32

2.12.2. Why Do You Need the Power of Attorney? .............. 32

2.12.3. Abusing the Power of Attorney ................................ 32

2.12.4. Limited Power of Attorney ........................................ 32

2.12.5. Full Power of Attorney .............................................. 33

2.12.6. The Consequences of Not Setting the Power of

Attorney up Correctly ............................................................... 33

2.13. Legal Clauses ................................................................. 33

2.14. Searches ........................................................................ 34

2.14.1. Why Carry Out Legal Searches .................................. 34

2.14.2. What Searches Should We Carry Out? ..................... 35

2.14.3. Other Searches .......................................................... 35

2.15. Land Registry ................................................................. 35

2.16. The Seller’s Legal Advice ............................................... 36

2.16.1. Undue Influence ........................................................ 36

2.16.2. The Seller Wants to Use Family Solicitor .................. 37

2.16.3. Handling the Seller’s Objections with Solicitors ....... 37

2.16.4. A Magical Phrase ....................................................... 38

5

Exercise 5 ...................................................................................... 38

2.17. The Role of the Mortgage Company ............................. 39

2.17.1. The Lender’s Perspective .......................................... 39

2.17.2. Notifying the Mortgage Lender about the Option .... 39

2.17.3. Consent to Let ........................................................... 39

2.17.4. The Financial Services Authority (FSA) ...................... 40

2.17.5. Repayment or Interest Only? .................................... 40

2.17.6. Who Should Speak to the Lender?............................ 40

2.17.7. Mortgage Arrears ...................................................... 41

2.17.8. What if the Seller Needs cash? ................................. 41

2.17.9. Changing the Direct Debit ......................................... 41

Exercise 6 ...................................................................................... 42

3. Granting an Option to Your Tenant .......................................... 43

3.1. Why Would You Grant an Option to Your Tenant? .......... 43

3.2. How Do You Get Started? ................................................. 43

3.3. Why Would a Tenant Pay “Above the Odds” to Live in a

property? ...................................................................................... 44

3.4. Why Would an Investor Grant an Option Whilst Having a

Mortgage? ..................................................................................... 44

3.5. Sandwich Options ............................................................. 45

3.6. Rent to Own Scheme ........................................................ 45

3.7. The Risks of Rent to Own and Sandwich Options ............. 47

3.7.1. Back to Back Deals .................................................... 47

3.7.2. The Timing of the Market ......................................... 48

Exercise 7 ...................................................................................... 49

3.8. Exercising your Options .................................................... 50

3.8.1. Give Notice to the Seller ........................................... 50

3.8.2. What If I Can’t Get Hold of the Seller? ...................... 50

3.8.3. The Seller is Not Co-operating .................................. 51

3.8.4. If this is a Sandwich Deal ........................................... 51

4. Where to find Lead Options Leads ........................................... 52

4.1. You are Lucky! ................................................................... 52

4.2. Lead Conversion ................................................................ 52

4.2.1. Raw Ingredients ........................................................ 52

6

4.2.2. Probability vs. Skills ................................................... 53

4.3. Where to Find Leads ......................................................... 53

4.3.1. Other Investors’ Unwanted Leads ............................ 53

4.3.2. Property Networking Events ..................................... 54

4.3.3. Online Property Forums ............................................ 54

4.3.4. Local Investors / Developers ..................................... 54

4.3.5. Internet Marketing .................................................... 55

4.3.6. Online Advertising Campaigns .................................. 56

4.3.7. Leafleting................................................................... 60

4.3.8. Newspaper Classified Ads ......................................... 61

4.3.9. Solicitors, Brokers & Agents ...................................... 62

4.3.10. Debt Management Agencies ..................................... 62

4.3.11. Buying Leads from Lead Sellers ................................. 63

4.4. Copywriting ....................................................................... 68

Exercise 8 ...................................................................................... 70

Answers on page 102 .................................................................... 71

4.5. Critical Success Factors ..................................................... 72

Video Four ..................................................................................... 72

Exercise 9 ...................................................................................... 72

5. Selling the Idea of Lease Options to Sellers .............................. 73

5.1. Negotiation ....................................................................... 73

5.2. Negotiation vs. Consultation............................................. 74

5.3. Where Do I Begin? ............................................................ 74

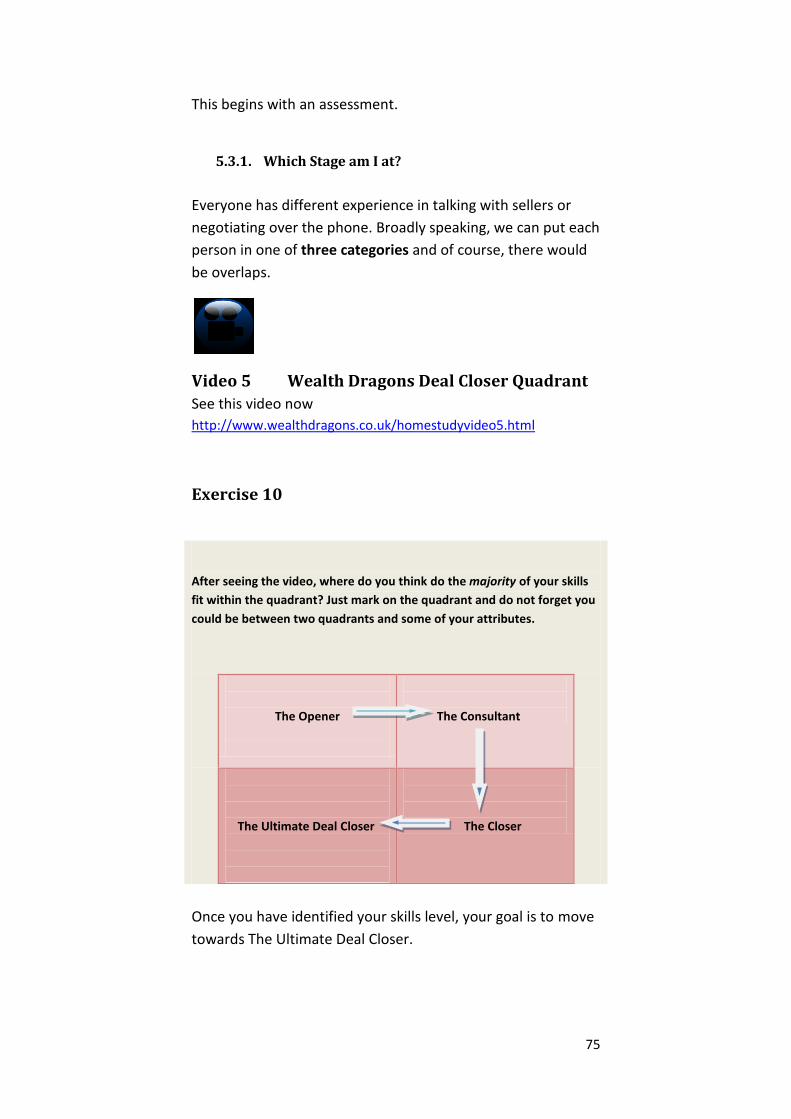

5.3.1. Which Stage am I at? ................................................ 75

Video 5 Wealth Dragons Deal Closer Quadrant ..................... 75

Exercise 10 .................................................................................... 75

Once you have identified your skills level, your goal is to move

towards The Ultimate Deal Closer. ............................................... 75

Video 6 Wealth Dragons Motivation Triangle ........................ 76

Exercise 11 .................................................................................... 76

Audio 2 (How to Negotiate a Lease Options Deal) ................. 77

6. Lease Options Strategies ........................................................... 78

6.1. Your Objectives ................................................................. 78

6.2. Deal Structuring ................................................................ 78

7

6.3. Seller’s Situations .............................................................. 78

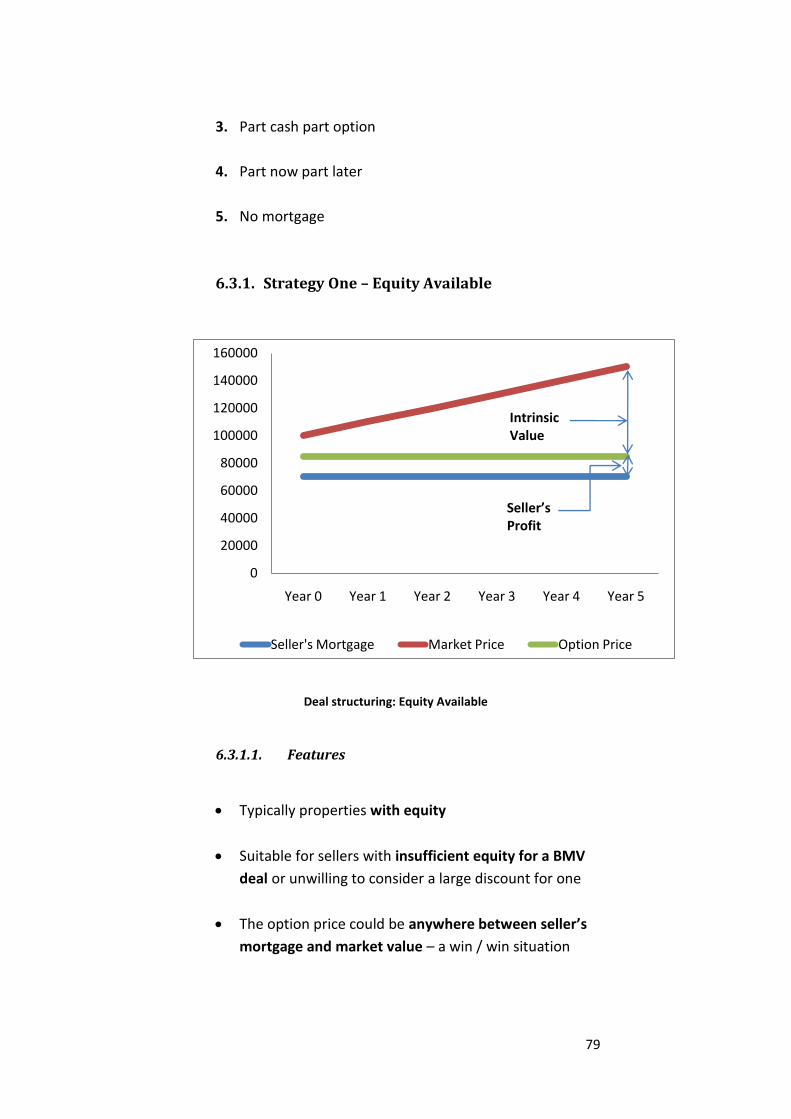

6.3.1. Strategy One – Equity Available ................................ 79

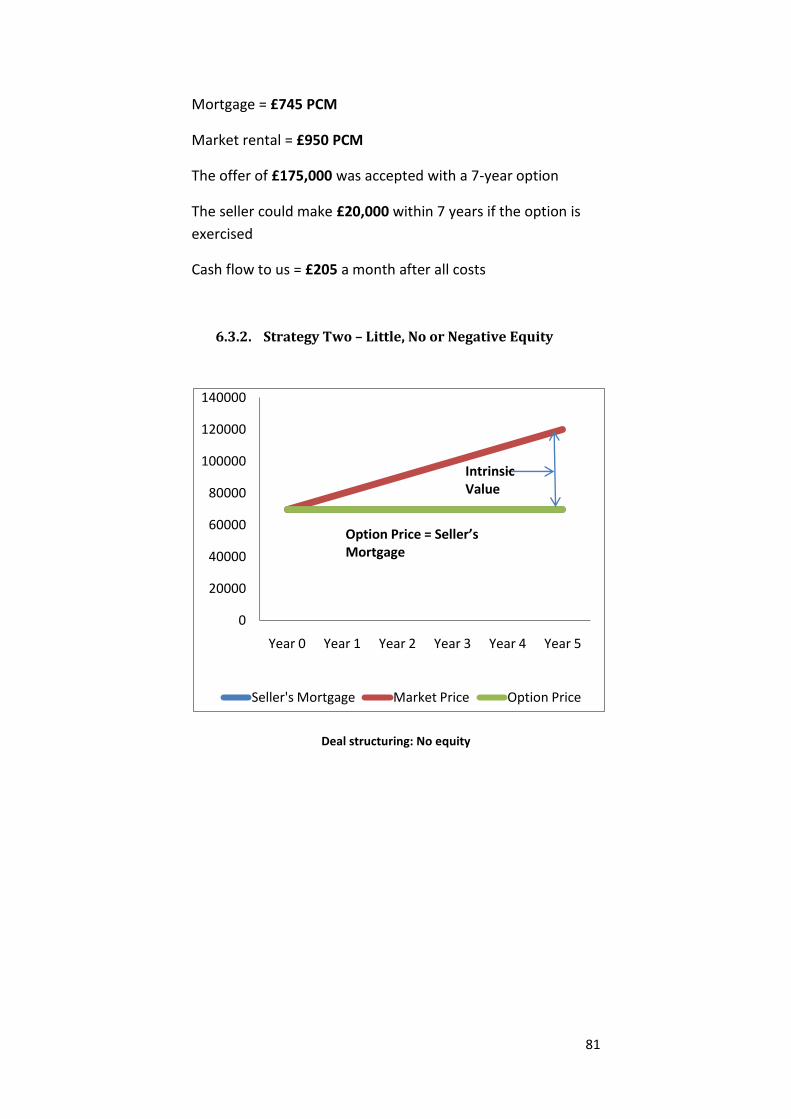

6.3.2. Strategy Two – Little, No or Negative Equity ............ 81

6.3.3. Strategy Three – Part Cash Part Option .................... 84

6.3.4. Part Now Part Later................................................... 85

Video 7 Part Now Part Later................................................... 85

7. Advanced Options Strategies .................................................... 86

7.1. Identifying Option Opportunities ...................................... 86

7.2. Reverse BMV Purchase ..................................................... 87

7.3. Jim’ll Fix It .......................................................................... 87

Our paper profit = £10,000 ........................................................... 89

7.4. First Time Buyers............................................................... 89

7.5. Homes under the Hammer Buyers ................................... 90

7.6. Tenant Buyers ................................................................... 91

7.7. Standard Buy to Let........................................................... 93

7.8. Flip the Option to Investor ................................................ 94

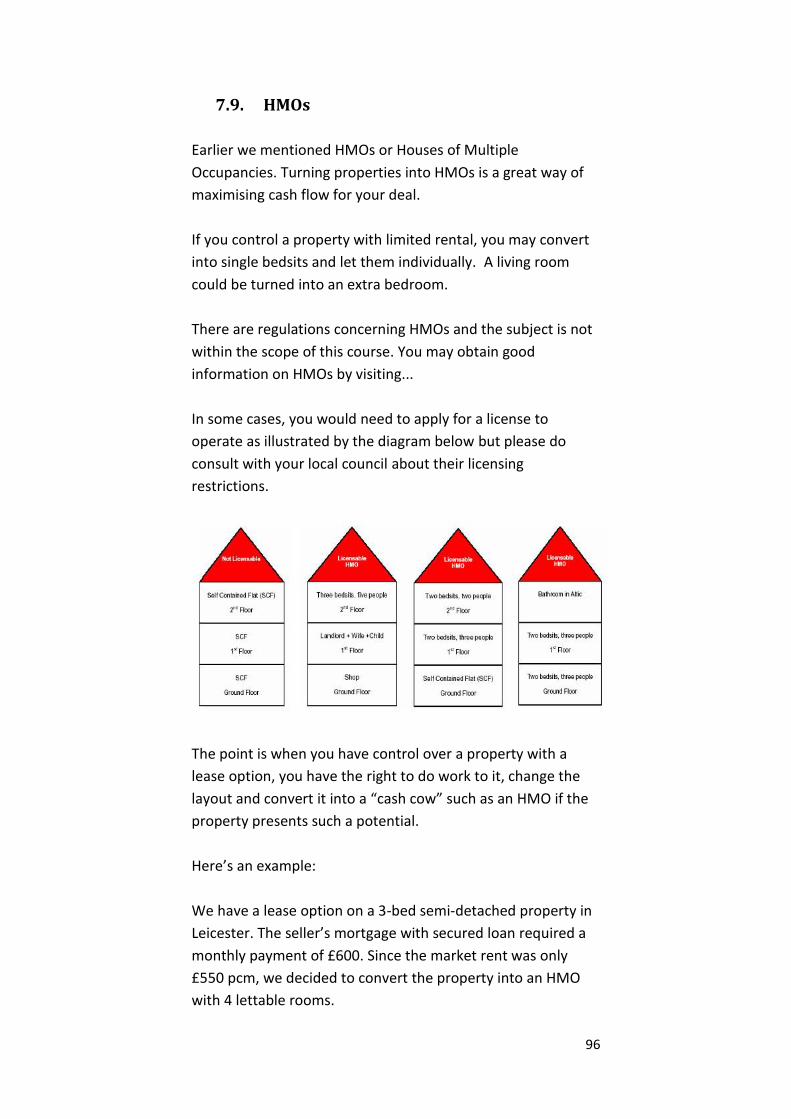

7.9. HMOs ................................................................................ 96

7.10. Struggling Landlords ..................................................... 97

7.11. Buy to Sell ..................................................................... 98

Answers for Exercises ..................................................................... 100

Exercise 1 .................................................................................... 100

Exercise 2a .................................................................................. 100

Exercise 2b .................................................................................. 100

Exercise 3a .................................................................................. 100

Exercise 3b .................................................................................. 100

Exercise 4 ........................................................................................ 100

Exercise 5 ........................................................................................ 101

Exercise 6 ........................................................................................ 101

Exercise 7 ........................................................................................ 101

Exercise 8 ........................................................................................ 102

Exercise 9 ........................................................................................ 102

Exercise 11 ...................................................................................... 102

8

All material in this course is, unless otherwise stated, the property of Wealth Dragons Limited. Copyright and other intellectual property laws protect these materials. Reproduction or retransmission of the materials, in whole or in part, in any manner, without the prior written consent of the copyright holder, is a violation of copyright law. A single copy of the materials available through this course may be made, solely for personal, non-commercial use. Individuals must preserve any copyright or other notices contained in or associated with them. Users may not distribute such copies to others, whether or not in electronic form, whether or not for a charge or other consideration, without prior written consent of the copyright holder of the materials. Contact information for requests for permission to reproduce or distribute materials available through this course is listed below: Wealth Dragon Limited Suite 165 Milton Keynes Business Centre Foxhunter Drive Linford Wood Milton Keynes MK14 6GD

9

Congratulations for taking the steps to learn about using this

immensely powerful instrument called a lease option to invest

in properties!

We believe if you apply the principles and utilise the practical

tools we’ve provided in this manual, you will look at property

investment with a completely different perspective and

overcome all the adverse market conditions that we’re

experiencing today.

This could change your life!

1. How to Use this Home Study Course

1.1. What’s in the Home Study Course?

This Home Study Course is based on interactive learning. It

has been designed to accelerate your learning through the use

of:

This manual

Links to web videos

Link to web audio

Exercises

The manual has been indexed in such a way that you may

reference different sections at any time.

10

1.2. Successful Learning

We believe there are 5 critical success factors in property

education:

1. Understand the concepts

2. Adjust your mindset

3. Familiarise with the tools

4. Conquer your fear

5. Do it!

Undoubtedly property manuals and courses from reputable

authors and investors will guide you in the right path but

unless you set yourself goals and take action, it would just be

a waste of your money and worse, time!

1.3. Mindset

Video One (mindset)

Go to this link now to watch the video

http://www.wealthdragons.co.uk/homestudyvideo1.html

1.4. Below Market Value Investing

The knowledge you’re about to gain from this course is based

on our many years of trials and tribulations in property

investment.

11

We’ve made the assumption that you already have some basic

knowledge of investing in properties at below market value

(BMV) and we aim to be concise and informative.

If you’re completely new to property investment and wish to

know more about the background of investing BMV, you may

benefit from the Wealth Dragons Property Millionaire

Mentoring Programme

(www.WealthDragons.co.uk/wealth.htm).

If you have any specific questions or feedback, please send an

email to [email protected].

One final important point is that the information presented in

this manual is designed for education purposes only and we’re

not regulated by the Financial Services Authority.

So you want to learn about investing in property without using

mortgages and doing valuations? Let’s start!

1.5. Why Do We Want to Do Lease Options?

1.5.1. The Credit Crunch

The credit crunch has transformed the dynamics of the whole

property market.

As far as property investors are concerned, what worked

previously is no longer applicable in the current climate.

So what are the problems being encountered by investors

today?

Here are some examples:

1. Not being able to get a mortgage

2. Surveyors down-valuing properties

3. Lenders withdrawing the mortgage offer

12

That’s true if you’re going into property investment for the

first time or already an experienced investor who wishes to

expand his or her property portfolio.

All lenders have since changed their lending criteria. If you’re a

first-time buyer, forget about getting a buy-to-let mortgage.

Most lenders will refuse you cold in the current climates.

What about experienced landlords with a sizable portfolio?

The answer is no, even if they have a perfect credit score and

never missed a loan repayment! Who would have thought

that?

We’ve seen many mortgage applications that were initially

approved but subsequently withdrawn by lenders just before

completions at the 11th hour!

As a result, many lives, both sellers and buyers alike, have

been jeopardised by this irrational underwriting process.

These are typical knee-jerk reactions from banks in a state of

panic – woes brought on by their irresponsible and

incompetent lending practices in the first place.

So is not being able to get a mortgage the main reason why we

should do lease options?

Video 2 (The Advantages of Using Lease Options)

http://www.wealthdragons.co.uk/homestudyvideo2.html

13

Exercise One

After seeing Video 1, write down up to SEVEN reasons why Lease Options

are fundamentally better for acquiring properties than using mortgages:

#1

#2

#3

#4

#5

#6

#7

Answers on Page 100

14

1.6. Objectives for This Course

• How to buy a property using lease options in the UK

• The different strategies for structuring deals and

making them stack

• How to use options to get rid of unwanted properties

• Learn stuff that most experts wouldn’t have personally

experienced

• How to sell the idea to sellers

15

2. What’s a Lease Option?

2.1. BMV vs. Lease Options

A lease option is an instrument through which one can control

a property without using a mortgage.

Here are the differences:

When an investor controls a property using a mortgage; if the

terms of the mortgage are breached, the investor risks being

repossessed.

When an investor controls a property using a lease option; if

the terms of the mortgage are breached, the owner (seller)

risks being repossessed.

Traditionally, investors would access a property only in terms

of the price.

2.2. It’s All about Terms

With lease options, investors would look at the terms, which is

comprised of three value components.

In other words, if one component in a deal is lacking, it could

be compensated by the other two.

Video 3 (The 3 Value Components of Lease options)

http://www.wealthdragons.co.uk/homestudyvideo3.html

16

Exercise 2a

List the THREE value components that make up a lease option:

Component #1

Component #2

Component #3

Answers on page 100

Exercise 2b

Answer the following questions by filling in the blanks:

Q. What is the difference between “equity” and the” intrinsic value”?

A. Equity is the difference between the ( ) and ( ).

Intrinsic value is the difference between the ( )

and ( ).

17

Q. If a property has no intrinsic value, then how would you increase its

value in a lease option deal?

A. Maximise the ( ) and prolong the ( ).

Answers on page 100

2.3. The Two Things that Make Up a Lease

Option

A lease option is split into two parts:

The OPTION that controls the PRICE

The LEASE that controls the CASH FLOW

The owner gives you the benefits associated with a mortgage

but without the risks.

2.4. The Option

This is the first part of a lease option.

By definition:

“An option is a contractual agreement that grants the bearer

the right but not the obligation to purchase or sell an asset at

a specific price at anytime within a specific time period.”

It has been used extensively in property, equity and

commodity trading to hedge risk.

The point to remember is that it gives the bearer the right but

not the obligation to exercise it.

18

So how does it control the price and how does it hedge risk?

Listen to the following audio.

Audio One (Futures & Options) Click this link and listen to the difference between futures and

options

http://wealthdragons.s3.amazonaws.com/continuity/pmm/futures.mp3

2.5. Some Jargons

Optioner – the person who grants the option also known as

the underwriter. In property, it is the owner who wants to sell

the property.

Optionee – the person who is granted the option or the

investor.

Premium – also known as the option fee. This is the price paid

by the optionee to the optioner for the option. In other words,

by paying this fee, the optionee will have the privileges

attached to the option.

Exercise price – also known as strike price or option price, this

is the eventual purchase or sale price agreed in an option

today.

Asset price – this is the actual market price of an asset

determined by supply and demand at any given time. One

needs to compare the option price with the asset price to see

if it is in the money (asset price greater than the option price)

or out of the money (asset price less than the option price).

Option period – the period during which an option can be

exercised.

19

In a European option, the option may only be exercised at the

end of the option period whereas in an American option, it

may be exercised anytime during the option period.

It is important to note that most property options are based

on American Options. Don’t worry too much about that for

now if you don’t understand it. We’ll show you their

applications later on in the course.

Expiry – the end of the option period.

Exercise 3a

Please try to remember the definition of an option and then fill in

below.

What is it? (verbal agreement / written contract / sales letter)*

*Delete as appropriate

From whom to whom?

The what?

But not what?

To do what?

20

At a specific what?

When?

Answers on page 100

Exercise 3b

*Delete as appropriate

The person who receives the option has *the obligation / the right

The person who gives the option has *the obligation / the right

Answers on page 100

2.6. Call & Put Options

2.6.1. What’s a Call Option?

A call option gives the bearer the right but not obligation to

buy an asset whereas a put option gives the bearer the right to

sell an asset at a specific price.

21

The bearer of a call wants the asset price to go up and exceed

the strike price.

2.6.2. Example of a Call option

For example, if you have an option to buy a property for

£100,000, naturally you want the market price to exceed

£100,000, to say, £130,000 so you can exercise your right to

buy it at the lower price and make £30,000 gross profit.

This is a typical property call option.

2.6.3. What’s a Put Option?

The bearer of a put wants the asset price to go down below

the strike price.

The reason is that a put bearer has the right but not the

obligation to sell an asset at a fixed price.

2.6.4. Example of a Put Option

Here’s an example of an equity share option.

If you own company A shares and you speculate its share price

to go down in 3 months time, you can buy a 3-month “put”

that will allow you to sell your share at say, £2 per share in 3

months time (equity options are European options where you

can only exercise on the expiry date).

If in three month’s time the actual share price falls to, say

£1.20, you can exercise your right to sell your share A in the

open market at £2. You then buy the share back at £1.20 and

make £0.80 profit, minus the option fee you paid initially.

In reality, you don’t have to own company A shares in order to

buy a put option. You simply purchase the option from the

22

market through your broker and you’ll simply gain or lose the

difference.

This is the concept of trading in margin or entering into a

Contract of a Difference.

Here’s a pseudonym for you – CB and PS

Call = Buy

Put = Sell

2.7. What Type of Option is in a Typical Property

Deal?

Don’t worry if all this sounds a bit complicated. You may be

pleased to know that nearly all property options are call

options.

In other words, you just agree on a price with a vendor as your

right but not the obligation to buy the property and hope the

market value will go above and beyond that.

Later on in the course, we will show you how a put option is

relevant in property.

2.8. In the Money & Out of the Money

When the market price relative to the strike price is favourable

to the bearer of an option, the option is said to be in the

money. Otherwise, the option is out of the money.

23

For example, if you have an option to buy a property for

£100,000 exercisable within 5 years but today, the property is

worth £90,000, then your option is out of the money.

2.9. An Option Application – Purchase Option

A purchase option agreement is typically used to lock in a

seller to give you exclusivity to purchase a property or piece of

land.

It is widely used for straight-forward purchases involving

mortgages, legal conveyancing and completion.

In this agreement, you have neither right to the rentals of the

property nor any involvement with the seller’s mortgage.

When you use a purchase option agreement, your objective is

to use the option period to carry out a number of activities

before completion, depending on the nature of your deal, and

prevent the seller from backing out of the deal in the

meantime.

2.9.1. What Do You Use a Purchase Option For?

You could use it for:

1. Completing your legal conveyancing.

2. Carrying out renovation work on the property before

getting a mortgage.

3. Securing a land deal whilst waiting for planning

permissions.

4. Obtaining compensation from the seller for any costs

incurred if the seller breaks the Agreement.

5. Assigning the deal to another investor for a fee.

24

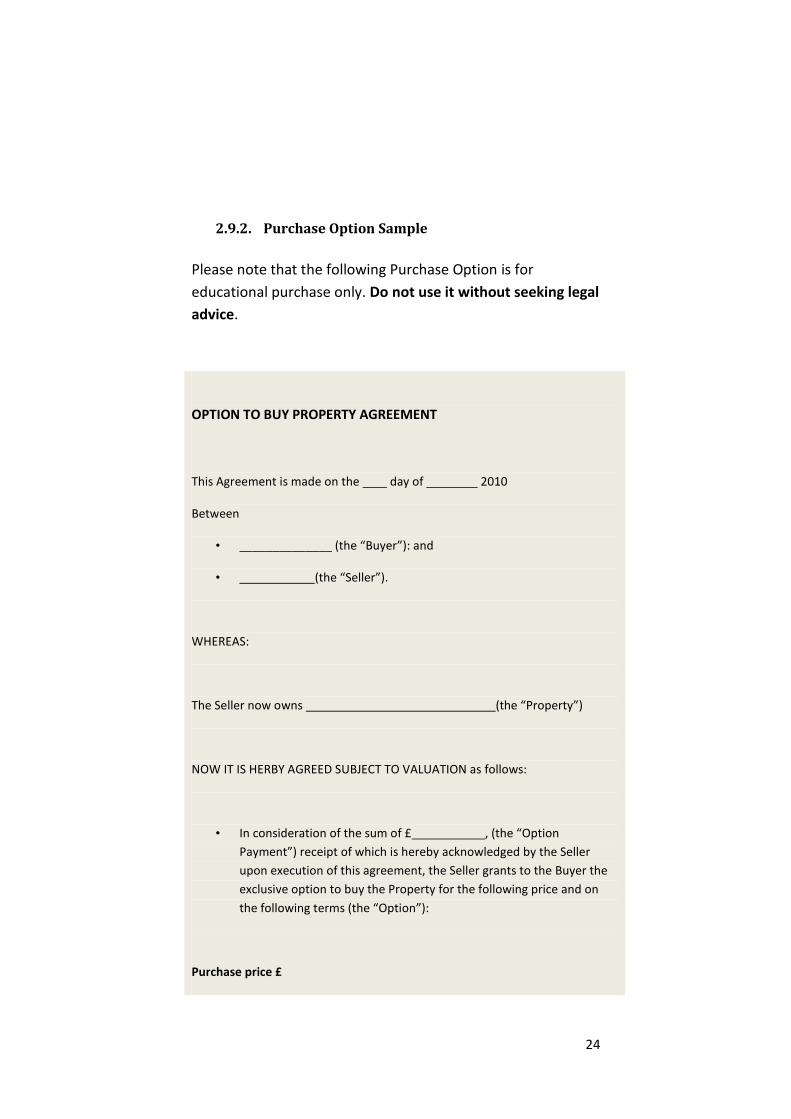

2.9.2. Purchase Option Sample

Please note that the following Purchase Option is for

educational purchase only. Do not use it without seeking legal

advice.

OPTION TO BUY PROPERTY AGREEMENT

This Agreement is made on the day of 2010

Between

• ______________ (the “Buyer”): and

• (the “Seller”).

WHEREAS:

The Seller now owns (the “Property”)

NOW IT IS HERBY AGREED SUBJECT TO VALUATION as follows:

• In consideration of the sum of £ , (the “Option

Payment”) receipt of which is hereby acknowledged by the Seller

upon execution of this agreement, the Seller grants to the Buyer the

exclusive option to buy the Property for the following price and on

the following terms (the “Option”):

Purchase price £

25

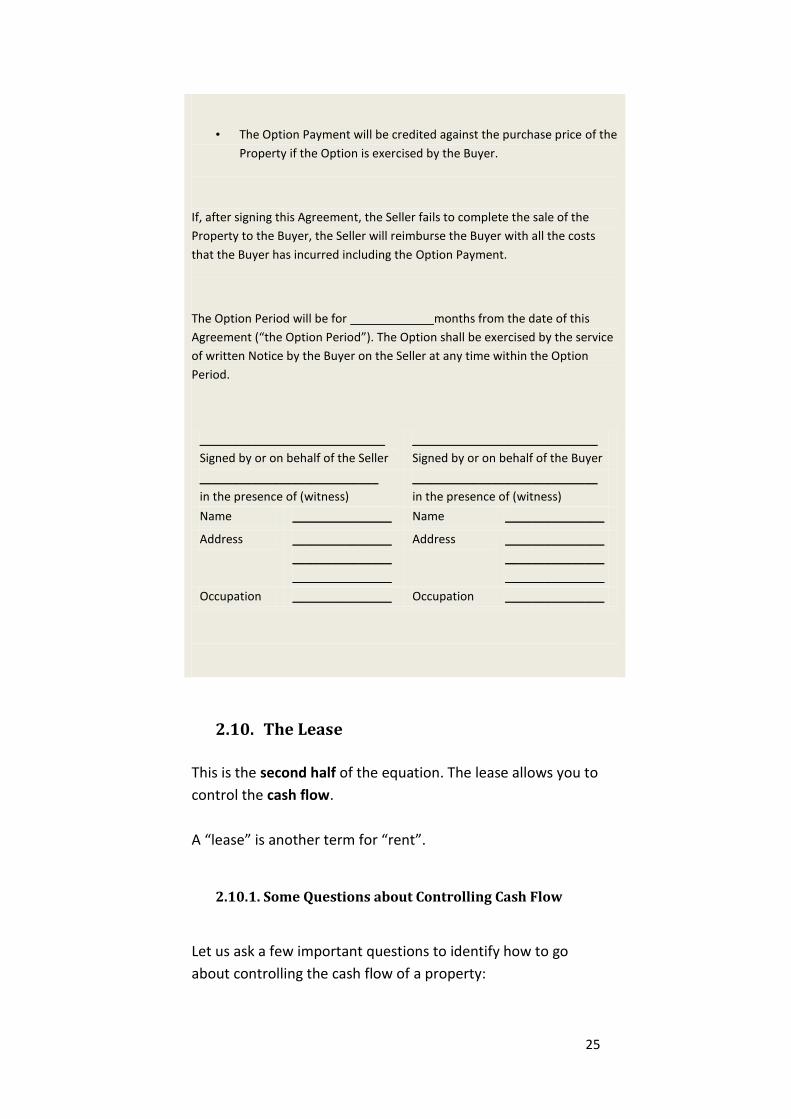

• The Option Payment will be credited against the purchase price of the

Property if the Option is exercised by the Buyer.

If, after signing this Agreement, the Seller fails to complete the sale of the

Property to the Buyer, the Seller will reimburse the Buyer with all the costs

that the Buyer has incurred including the Option Payment.

The Option Period will be for months from the date of this

Agreement (“the Option Period”). The Option shall be exercised by the service

of written Notice by the Buyer on the Seller at any time within the Option

Period.

____________________________

Signed by or on behalf of the Seller

____________________________

Signed by or on behalf of the Buyer

___________________________

in the presence of (witness)

____________________________

in the presence of (witness)

Name _______________ Name _______________

Address _______________

_______________

_______________

Address _______________

_______________

_______________

Occupation _______________ Occupation _______________

2.10. The Lease

This is the second half of the equation. The lease allows you to

control the cash flow.

A “lease” is another term for “rent”.

2.10.1. Some Questions about Controlling Cash Flow

Let us ask a few important questions to identify how to go

about controlling the cash flow of a property:

26

1. As an investor, are you renting a property directly from

the owner / seller?

2. If so, are you financing the rent out of your own

pocket?

3. If the property is to be let out to a tenant, do you have

the right to do so if you are not the owner of the

property?

4. Even if you do, do you wish to be directly responsible

for the tenant if the owner loses the property, e.g.

repossession, death?

5. How do you control the cash flow exactly?

2.10.2. You Need a Legal System

The way in which the cash flow is controlled depends

entirely on a legal system that allows you to do so

effectively whilst mitigating risk.

So referring back to the questions, it is obvious that:

We do not pay the rent out of our own pocket to

the owner, but we put a tenant in the property and

use the rent to finance the seller’s mortgage

payment.

We do not have the right to let the property out as

an investor because we do not own the property.

Therefore, the rental agreement is between the

owner and the tenant.

We do not want to be directly responsible for the

tenant if the owner loses the property. Therefore,

our capacity in the arrangement is to manage the

property on behalf of the owner.

27

We receive the rent directly from the tenant and

pay the seller’s mortgage directly. The difference

becomes our management fee or rental profit.

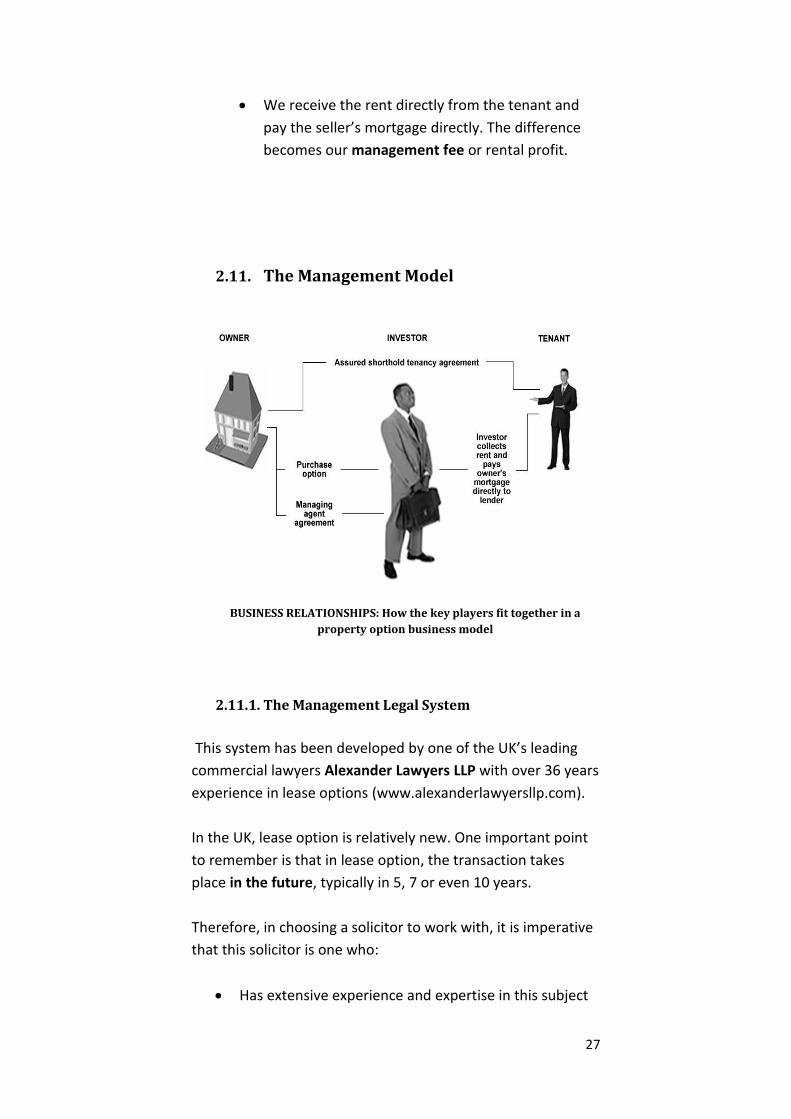

2.11. The Management Model

BUSINESS RELATIONSHIPS: How the key players fit together in a

property option business model

2.11.1. The Management Legal System

This system has been developed by one of the UK’s leading

commercial lawyers Alexander Lawyers LLP with over 36 years

experience in lease options (www.alexanderlawyersllp.com).

In the UK, lease option is relatively new. One important point

to remember is that in lease option, the transaction takes

place in the future, typically in 5, 7 or even 10 years.

Therefore, in choosing a solicitor to work with, it is imperative

that this solicitor is one who:

Has extensive experience and expertise in this subject

28

Can advise you on structuring your deals

Has developed the legal documents to make them

enforceable and being able to minimise risk

Can assist you should anything go wrong (legal matters

are never “black and white”!)

The diagram above shows that while the buyer has a purchase

option from the seller, he or she is now acting in the capacity

of a Management Agent on behalf of the seller.

2.11.2. The Tenancy Agreement

The Assured Tenancy Agreement (AST) is between the seller

(owner) and the tenant.

The fundamental reason for this arrangement is that legally,

the buyer doesn’t have any right to grant an AST to a tenant

when he or she is not the legal owner of the property.

Secondly, any changes in the seller’s circumstances will not

affect the buyer’s obligation to the tenant because the buyer

is only acting as the seller’s agent.

2.11.3. The Management Fee

The management fee, quite conveniently, is equal to the

difference between the rent and the seller’s mortgage.

2.11.4. Who Pays Who?

It is important that you do not allow the rent to reach the

seller and the mortgage is paid directly to the seller’s

mortgage company by the buyer for the obvious reasons to

ensure that the property doesn’t fall into arrears.

2.11.5. The Management System Paperwork

29

The Management Legal System has two parts:

1. The Purchase Option Agreement

2. The Management Agreement

The Management Agreement lists out the responsibilities of

the seller and the investor.

2.11.6. The Management Agent’s Responsibilities

1. Pay the seller’s mortgage directly, irrespective of

whether the property is vacant or occupied. Therefore

a new direct debit mandate needs to be done with the

buyer’s name and bank account details.

2. Maintain the property. If there are any damages

caused by the tenant, it is the agent’s responsibility to

sought compensation from the tenant in accordance

with the terms on the AST.

2.11.7. The Seller’s Responsibilities

1. Keep in touch with the buyer and agent. The seller

needs to notify the buyer if there are any changes in

personal circumstances. It is in the best interest for the

seller to do so because the seller is still the legal owner

of the property.

2. Building Insurance. Since the seller is still the legal

owner, the building insurance needs to be in the

seller’s name. Of course the buyer may agree to

reimburse the seller for this.

2.11.8. Other Important Features

A break clause for the buyer if once the option is

exercised but the property is found to be

unmortgageable due to defects or adverse searches.

30

A break clause for the buyer if the seller fails to comply

with the terms of the Option Agreement. An example

of which would be if the seller is facing insolvency or

bankruptcy and the property is being repossessed as a

result.

If the investor terminates the Management Agreement

because the seller has breached the terms, the

Purchase Option Agreement can remain valid.

The option may be exercised when a Notice is given to

any of the joint owners, whether the trust is in a Joint

Tenancy or Tenancy in Common.

Once the Notice is given in writing, the property needs

to complete within 28 days or the seller could face

legal action.

Exercise 4

After reading through the features of the Management Model, please

answer the following questions:

1. There are two parts to the Management Model in terms of legal

agreements. One part is the Purchase Option. What is the name

of the other part?

2. The Assured Tenancy Agreement (AST) is between which two

parties?

Party one:

Party two:

31

3. Who does the tenant pay the rent directly to?

4. Who pays the seller’s mortgage and how?

5. If the boiler breaks down, who is responsible for getting it

repaired or replaced?

6. If the property is vacant, who is responsible for continuing to pay

the seller’s mortgage?

7. True or False - The investor can terminate the Management

Agreement and stop paying the seller’s mortgage at any time.

T/F*

*Delete as appropriate.

Answers on page 100

2.12. The Power of Attorney

This is an important topic so we need to spend a little bit of

time on it so we may understand its importance.

32

2.12.1. What is the Power of Attorney?

A Power of Attorney is a legal document whereby a person

gives another person or persons the power to make decisions

with regard to their financial affairs and/or their health and

personal welfare.

2.12.2. Why Do You Need the Power of Attorney?

In a lease option deal, we recommend that the buyer should

make it a requirement that the seller should grant the buyer

the Power of Attorney.

This is to ensure that when it is time for you to exercise your

option to buy the property, you can simply do so without the

seller getting involved. The seller could be unavailable during

this time for any reason.

2.12.3. Abusing the Power of Attorney

However, it is important that the Power of Attorney is

established solely for convenience sake and not to be abused.

An example of abuse is contacting the seller’s mortgage

company to remortgage the property without notifying or

agreeing with the seller.

You need to bear in mind also that legally, the full Power of

Attorney may be rescinded by the person who granted it at

any time. In other words, the agreement is revocable.

2.12.4. Limited Power of Attorney

In Alexander Lawyers’ Management Agreement, the Power of

Attorney has been built into the contract as a clause.

This Power is limited and irrevocable.

33

The limitation is that we can only enforce the exercising of

the option in the absence of the seller and quite frankly, this is

very reasonable and all that we need.

Similar to a Landlord / Tenant relationship in a buy-to-let, a

successful lease option deal requires the seller and buyer to

keep in touch and have an on-going relationship.

It is far better to resolve any issues as they arise between the

two parties rather than having to resort to taking legal

proceedings.

2.12.5. Full Power of Attorney

However, if you must incorporate the full Power of Attorney

into the deal for any reason, it is essential to run a check on

the property’s title and obtain legal advice.

By law, if more than one person owns the property, each

party, whether in a tenancy in common (each party owns a

percentage) or a joint tenancy (two joined owners each

owning 100%), should appoint a separate attorney.

2.12.6. The Consequences of Not Setting the Power of

Attorney up Correctly

If setting up the full Power of Attorney is not done properly, it

could jeopardise your deal in the future. Therefore, it is always

advisable that you ask your solicitor to manage it for you.

Therefore, the Power of Attorney is not a “stand alone”

document that you can simply ask the seller to sign in order to

waive all the rights away without taking proper procedures.

2.13. Legal Clauses

These are the special terms and conditions that add to a

standard Option Agreement once agreed with your seller.

They are what give an option agreement total flexibility.

34

A word of warning – never add anything to a legal document

without consulting with your solicitor.

Examples of clauses you may wish to add are:

A break clause to allow the buyer to terminate the

Agreement before the option expires

If the seller fails to make the monthly contribution or

fulfil certain criteria as agreed, the buyer may make

the Agreement null and void

Further monthly contributions from the seller if the

interest rate rises above a certain level

Further extension to the option period after certain

time

Provided the seller accepts your special terms and signs the

agreement, they are legally binding.

2.14. Searches

2.14.1. Why Carry Out Legal Searches

Legal searches are carried out to protect the buyer.

Unlike the standard conveyancing process, the types of

searches you decide to carry out for an option deal are entirely

up to you.

One question to ask is “do I want to nurture a deal for 5 or 10

years only to find the property not mortgageable when I

exercise my option?”

Although a full scale search is not necessary, doing some basic

searches is definitely sensible.

35

2.14.2. What Searches Should We Carry Out?

A Title Search – this reveals the identity of the seller(s),

restrictions and possible complications. By far this is

the most important search especially if the property is

held in a Trust.

An Environmental Search - If there is any problem at all

with the building or the property, it will put off future

buyers. Therefore, it is important to ascertain this from

day one.

2.14.3. Other Searches

Local authority search

Water search

Coal mining search - depending on the area

Other specialist searches depending on the property’s

location

Although all the searches should be carried out as

recommended, one thing to bear in mind is that if you decide

to purchase the property after exercising your option, all the

searches must be carried out again.

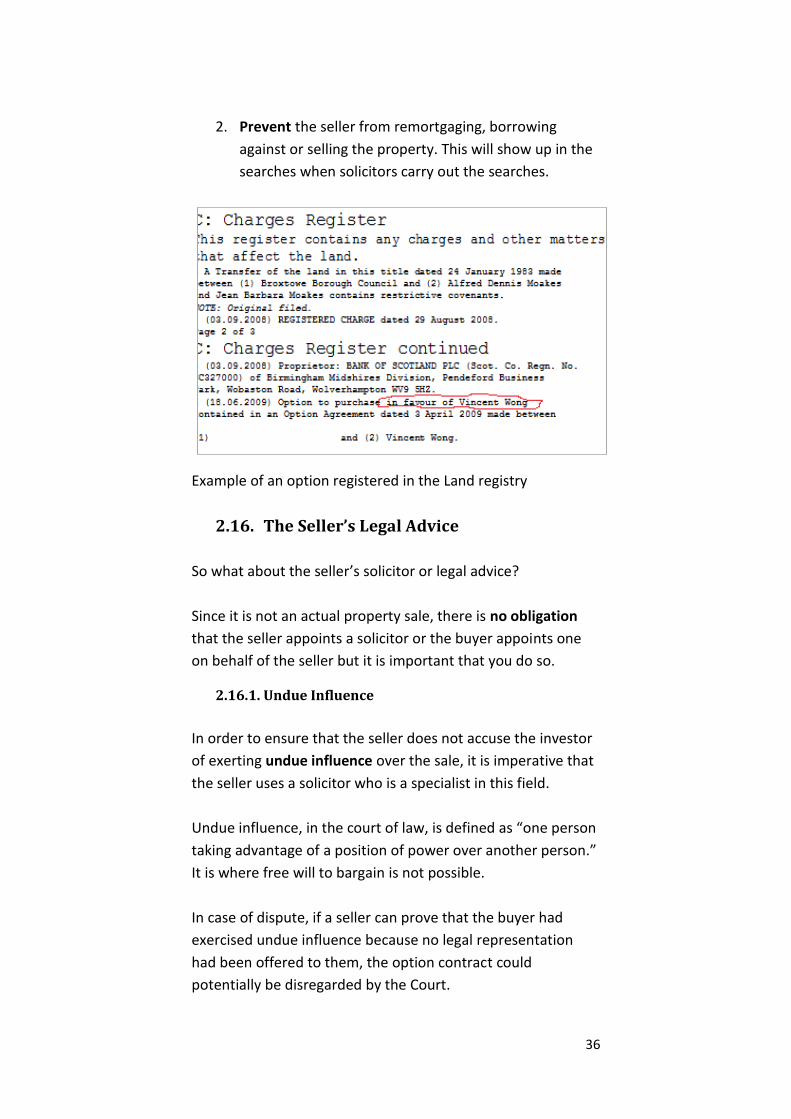

2.15. Land Registry

Once the Purchase Option and Management Agreements have

been signed by both the buyer and seller, it is imperative that

they are registered with the Land Registry by your solicitor.

The reasons for doing so are to:

1. Protect your interest in the property legally and

prevent any further interests registered by any third

parties.

36

2. Prevent the seller from remortgaging, borrowing

against or selling the property. This will show up in the

searches when solicitors carry out the searches.

Example of an option registered in the Land registry

2.16. The Seller’s Legal Advice

So what about the seller’s solicitor or legal advice?

Since it is not an actual property sale, there is no obligation

that the seller appoints a solicitor or the buyer appoints one

on behalf of the seller but it is important that you do so.

2.16.1. Undue Influence

In order to ensure that the seller does not accuse the investor

of exerting undue influence over the sale, it is imperative that

the seller uses a solicitor who is a specialist in this field.

Undue influence, in the court of law, is defined as “one person

taking advantage of a position of power over another person.”

It is where free will to bargain is not possible.

In case of dispute, if a seller can prove that the buyer had

exercised undue influence because no legal representation

had been offered to them, the option contract could

potentially be disregarded by the Court.

37

2.16.2. The Seller Wants to Use Family Solicitor

If a seller does decide to consult with their own family

solicitor, it is very probable that the solicitor would advise the

seller against signing it.

The main reason is that a solicitor, who is not conversant with

such an agreement, would simply not want to bear any

responsibilities if things go wrong.

More to the point is that a normal solicitor rarely takes the

seller’s personal situation into consideration.

2.16.3. Handling the Seller’s Objections with Solicitors

Therefore, there are three ways in which you may help the

seller overcome any objections:

1. Explain to the seller that his or her solicitor is likely to

advice against signing the Agreement for the reason

stated above.

2. Help the seller understand the contents of the

Agreement so the seller feels more reassured about

signing it.

3. Reiterate the importance of doing the deal with you

and more importantly, the possible consequences of

not doing the deal given the seller’s circumstances.

It is very important to show the highest integrity when

explaining the contract to the seller, including any pros and

cons and risks from the perspective of the seller.

It’s better for the seller to understand everything from the

onset and have a realistic expectation.

There is a saying “there’s nothing to be feared, only to be

understood”.

38

2.16.4. A Magical Phrase

One magical phrase you can use to ask the seller is whether

they would “appoint a divorce lawyer to handle an injury claim

from an accident.”

Lease Option is a specialist subject that needs to be handled

by a specialist lawyer.

Exercise 5

Please answer the following questions:

1. List five important roles of an options solicitor acting for the

investor:

#1

#2

#3

#4

#5

2. As far as the investor is concerned, what should be the main

purpose of using the Power of Attorney?

39

3. Is the full Power of Attorney a document that an investor can ask

the seller to sign without getting a solicitor involved? Y / N*

*Delete as appropriate

4. What is the “magical phrase or question” you could use if the

seller insists on using a family solicitor who is inexperienced in

doing lease options?

Answers on page 101

2.17. The Role of the Mortgage Company

What about the seller’s mortgage lender? Do we need to

notify them of this arrangement?

2.17.1. The Lender’s Perspective

The first thing to remember is that the mortgage lender’s

primary interest is to receive the mortgage payment each

month, irrespective of where the money comes from (except

laundered money of course).

2.17.2. Notifying the Mortgage Lender about the Option

You may be relieved to learn that it is not necessary to inform

the mortgage lender about the Option Agreement.

2.17.3. Consent to Let

40

While the seller has no obligation to inform the mortgage

lender about a purchase option being granted to a buyer, the

seller needs to inform the mortgage lender if the property is

going to be let on an AST in accordance with the mortgage

terms.

Therefore, it is necessary to obtain Consent to Let.

With Consent to let, there is normally a small administrative

fee to pay and you may want to cover that cost.

2.17.4. The Financial Services Authority (FSA)

The lender rarely refuses this request unjustifiably, particularly

mortgage lending is regulated by the Financial Services

Authority (FSA) whose objectives are to ensure that borrowers

get a fair deal with their lenders.

2.17.5. Repayment or Interest Only?

If possible, the seller should encourage the buyer to change a

Repayment Mortgage to an Interest Only or even a Buy-to-Let

mortgage which would reduce the monthly payment quite

substantially.

It is not always guaranteed that the mortgage lender would

allow Consent to Let or changing a repayment mortgage to

interest only in the first instance.

If they do not, you may suggest that the FSA would get

involved and this would normally be sufficient to influence

their decisions.

2.17.6. Who Should Speak to the Lender?

It is important to bear in mind that at this stage, the seller is

still the owner of the property.

Therefore, from a practical point of view, it is easier for the

seller to speak to the mortgage lender directly and you may

need to train the seller beforehand.

41

If the seller does not wish to deal with the lender, you can let

the lender know that you have the expressed permission from

the seller to deal with them directly.

In that case, just simply explain that you are the seller’s

representative.

2.17.7. Mortgage Arrears

If the seller is in arrears (behind with mortgage payments) and

the seller is facing repossession, you should try to negotiate

with the lender to settle the arrears to avoid repossession.

Although this is not always guaranteed, we have had

experience where:

1. The lender agrees to settle the arrears by accepting a

percentage of it to stop the repossession. This could be

as low as 50% of the original amount.

2. The lender agrees to add the arrears to the overall

mortgage loan amount so they are spread over the

duration of the mortgage terms.

2.17.8. What if the Seller Needs cash?

If the seller needs a lump sum of cash to move on, it may be

possible to remortgage first. All these depend on the seller’s

credit history and the process may delay the deal.

Later on in the course, we will explore seller’s cash

requirements in more detail.

2.17.9. Changing the Direct Debit

Once the Consent to Let is obtained, the next thing the seller

should request from the lender is a new Direct Debit Mandate

42

form. Do not mention anything else to the lender about doing

lease options etc.

Once the form is received, the investor (you) should fill it in

and return it to the lender. Then two things may happen:

1. The lender just accepts it and the investor will start

paying the mortgage directly from their bank account.

2. The lender will write back requesting the owner to sign

an extra form to give permission to this third party to

pay the mortgage. In that case, just do it and that will

be the end of the matter.

Exercise 6

Answer True or False *Delete as appropriate

1. The seller’s mortgage lender needs to be informed of the

Purchase Option put on the property. T / F*

2. The permission you get from the lender for letting the property

is called Right to Let. T / F*

3. When you ask the lender for Consent to let, the lender will not

always grant it in the first instance. T / F*

4. The monthly payment for a repayment mortgage is lower than

that of an interest only so it is preferable for the seller to keep

the repayment mortgage. T / F*

5. Mortgage lenders are regulated by the Financial Services

Authority (FSA). T / F*

6. The mortgage lender will always allow you to release further

funds from the equity of the property. T / F*

7. It is better for you (investor) to communicate with the mortgage

lender than the owner to do so. T / F*

8. It is possible to negotiate with the lender as regards to the

seller’s arrears to avoid repossession. T / F*

Answers on page 101

43

3. Granting an Option to Your Tenant

3.1. Why Would You Grant an Option to Your

Tenant?

The idea behind granting an option to a tenant to buy the

property is that an investor may benefit more from doing so

than just commanding rent from a tenant.

The option allows the tenant the opportunity to buy your

property at a fixed price sometime in the future.

You may:

Keep the deposit from the tenant as the Option Fee. A

rental deposit needs to enter the Tenant’s Deposit

Scheme while a fee may be non-refundable

Command more rent from the tenant as rent premium

Ask the tenant to fix or maintain the property at their

own cost

Fix an exit strategy for your property

Granting an option to a tenant is the basis of a Rent to Own

scheme.

3.2. How Do You Get Started?

Before you can grant an option to a tenant, you must first have

control over this property.

If you have followed this course up till now, you will know that

an investor can control a property in two ways:

1. A mortgage

44

2. A lease option

3.3. Why Would a Tenant Pay “Above the

Odds” to Live in a property?

This is a very important question to ask because no one would

pay more money than necessary just for an opportunity to

own a property.

The primary reason for doing so is if the perceived value of a

property is seen to be going up. This is typically so in a buoyant

property market.

In other words, the tenant is being granted a call option to

purchase a property and expecting the price to go up.

In a Rent to Own scheme which we will be discussing shortly, a

tenant would benefit from having an option to purchase

because:

The tenant pays the option premium as a “saving

scheme” so it may be used as the deposit for the

eventual purchase.

The tenant feels there is a sense of ownership whilst

having an option to purchase a property.

If a tenant is unable to obtain a mortgage now due to

bad credit. Renting before buying is a good way to

restore the credit score.

3.4. Why Would an Investor Grant an Option

Whilst Having a Mortgage?

Many investors, including us, have bought properties we wish

we hadn’t.

This could be due to a property needing substantial work or

being situated in an undesirable location.

45

Granting an option to a tenant who is a DIY enthusiast or

someone who wants to get on the property ladder and does

not mind being in a bad area can help you offload this

property where it would be very difficult in an open market.

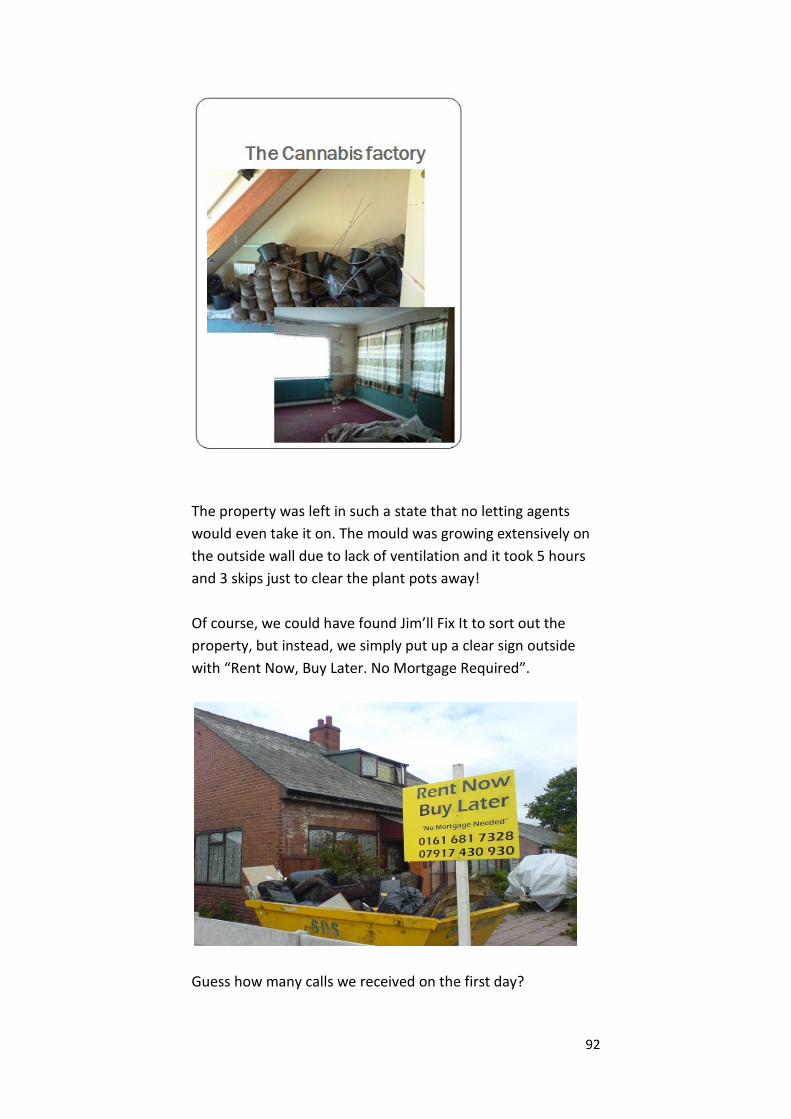

We managed to offload a property that was turned into a

“cannabis factory” by unscrupulous tenants using this method!

3.5. Sandwich Options

A sandwich option is when you grant an option to a tenant

whilst having been granted an option on this property from

the owner.

The best way to illustrate a sandwich option is to explain how

a Rent to Own scheme works.

3.6. Rent to Own Scheme

Rent to Own schemes have been very popular in countries

such as Australia and the USA.

Its popularity has been fuelled by the worldwide property

boom prior to the credit crunch.

Let us look at a typical example of how a Rent to Own deal is

structured:

Rent to own scheme. An example.

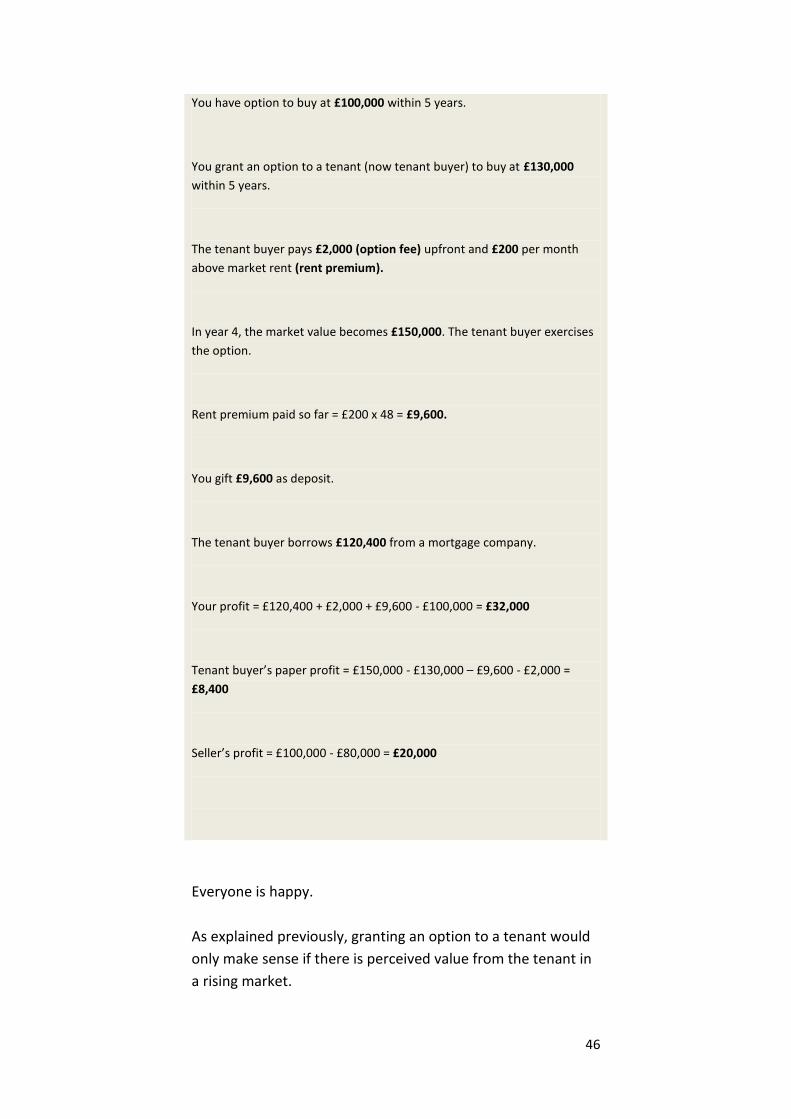

A property’s market value today is £100,000.

The seller’s mortgage outstanding is £80,000.

46

You have option to buy at £100,000 within 5 years.

You grant an option to a tenant (now tenant buyer) to buy at £130,000

within 5 years.

The tenant buyer pays £2,000 (option fee) upfront and £200 per month

above market rent (rent premium).

In year 4, the market value becomes £150,000. The tenant buyer exercises

the option.

Rent premium paid so far = £200 x 48 = £9,600.

You gift £9,600 as deposit.

The tenant buyer borrows £120,400 from a mortgage company.

Your profit = £120,400 + £2,000 + £9,600 - £100,000 = £32,000

Tenant buyer’s paper profit = £150,000 - £130,000 – £9,600 - £2,000 =

£8,400

Seller’s profit = £100,000 - £80,000 = £20,000

Everyone is happy.

As explained previously, granting an option to a tenant would

only make sense if there is perceived value from the tenant in

a rising market.

47

You do not need to do a sandwich option or operate Rent to

Own in order to benefit from lease options if the timing of the

market is not right.

3.7. The Risks of Rent to Own and Sandwich

Options

While these kinds of deals are potentially very lucrative in the

right situations, there are inherent risks of which we need to

be aware.

The two main reasons that contribute to such risks are as

follows:

3.7.1. Back to Back Deals

A back to back deal is one where there are three parties

involved as in a sandwich option.

When there are more than two parties in a deal, things do get

inevitably complicated.

While the legal system for lease options mitigate the risks

from an investor, benefitting from the tenants directly

through receiving monies transfer the responsibilities of the

tenant back to the investor.

When an investor receives rent premiums or option fees from

a tenant buyer, the investor becomes responsible for this

tenant buyer if, for any reason, the seller becomes bankrupt or

gets repossessed for any reason.

Remember, once the tenant buyer exercises the option, you

become obligated to deliver it.

Therefore, a sensible way to approach this is to make sure

there are funds available to compensate the tenant buyer if

you cannot deliver the property once the option is exercised

by the tenant buyer.

48

Another risk to be aware of is that once the tenant buyer

exercises the option, you exercise your option with the original

owner and become obligated to buy it.

At this point, there is always a chance that the tenant buyer

fails to complete on the purchase.

This could be due to the mortgage being withdrawn in the last

minute by the mortgage lender or other unforeseen

circumstances experienced by the tenant buyer.

Therefore, if you are not in the position to obtain a mortgage

or arrange for finances to buy the property from the seller,

you could potentially be sued.

Fortunately, buying the property with a mortgage is only one

of the many exit strategies that we can use. We will discuss

other exit strategies later on in the course.

3.7.2. The Timing of the Market

If a call option is granted to a tenant buyer for a large fee plus

the rent premiums, the tenant buyer would expect the market

value of the property to exceed that of the option price so

they may exercise the option.

If this call option has been granted during a flat or falling

market, then the above might not materialise and the tenant

buyer could accuse the investor for mis-selling.

Therefore, the timing of the market is crucial whenever you

grant an option to a third party.

Rent to Own schemes had been very successfully implemented

overseas because the property market worldwide had been

experiencing an uninterrupted “bull run”.

When the market seemed to be only going up everywhere as

in the UK, property investment was very forgiving of mistakes.

49

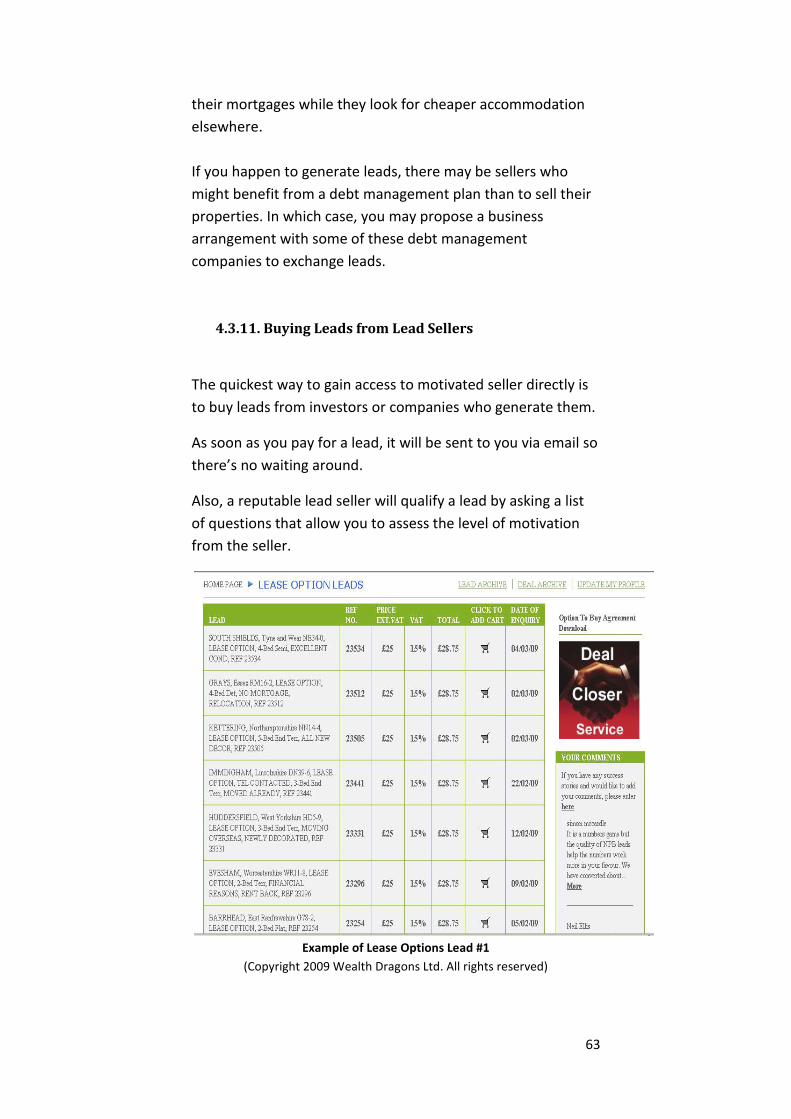

So in any back to back deals, all parties were profiting and any

potential risks seemed to have been compensated.

While the property market is still in a fragile state post credit

crunch, it is imperative that we approach back to back deals

with extreme caution.

Exercise 7

Please answer the following questions:

1. What are the three things that an investor can command from a

tenant in order to benefit from a Rent to Own scheme?

#1

#2

#3

2. Name one reason why a tenant would pay above the market

rent to gain an option to buy a property from an investor?

3. Answer True or False

When the market is flat or falling, it is not always a good idea to grant a

call option to a tenant T / F*

*Delete as appropriate

50

4. How would you minimise each of the following two risks in a

back to back deal?

The tenant buyer exercises the option but you cannot deliver the

property

Solution:

The tenant buyer accuses you of mis-selling a Rent to Own scheme

Solution:

Answers on page 101

3.8. Exercising your Options

3.8.1. Give Notice to the Seller

When it is time to exercise your right to buy a property, you’ll

need to serve a Notice on the seller.

If you have been in touch with the seller throughout the terms

of the option, then this should be straight forward.

In cases of joined ownership, if you have included it as a clause

in your Option Agreement, then you may simply serve a Notice

to any one of them to proceed with the sale.

3.8.2. What If I Can’t Get Hold of the Seller?

If you can’t get hold of the sellers, then you can exercise your

Power of Attorney as discussed.

51

3.8.3. The Seller is Not Co-operating

Although an Option Agreement is a legally binding document

signed by both parties, any problems may result in you

attending court.

One example is that the seller refuses to honour the

Agreement because their circumstances have changed. They

might not be so ready to give their property up so swiftly.

This is the time when you are happy you had implemented all

the necessary procedures with your solicitor at the onset of

the Option Agreement, such as appointing a solicitor to act on

behalf of the seller.

Also if you had incorporated some “profit share” incentive into

the deal, this could be avoided all together.

3.8.4. If this is a Sandwich Deal

As explained, there is a risk that your tenant buyer cannot

complete on the deal after you have given Notice to the

original seller.

There are different ways in which you could minimise these

risks:

1. Explain the situation to the seller and hope the seller will

revoke the Notice.

2. Exercise the option only after seeing the tenant buyer’s

mortgage offer.

3. Exercise your option with the seller conditional to the tenant

being able to complete on the purchase.

4. Ask the tenant buyer for a deposit.

5. Have sufficient funds from the option premium received from

the tenant buyer for any compensation to the seller.

52

4. Where to find Lead Options Leads

4.1. You are Lucky!

The reason why we say you are lucky is that when you are

doing lease options, it’s much easier to find leads than if you

were doing BMV deals.

We will go as far as telling you that the leads people throw

away because they do not see any value in them are the best

candidates for lease options.

Remember, investors normally only see one thing in a deal and

that is the price and / or cash flow. Lease options are about

terms.

Here is a question: “Do you think it is easier to convince

someone to sell their property at 30% below the market value

(BMV investing) than allow someone to take over their debts

(lease options investing)?

I think you get our point.

4.2. Lead Conversion

4.2.1. Raw Ingredients

If you want to do lots of property deals, you need to have a

good supply of leads, which are like the raw ingredients for

your recipes for cooking a meal.

No leads, no deals. It is that simple!

If you have good sales, marketing and people skills, you will

get a lot of leads and even for free! We’ll show you what we

mean shortly.

53

4.2.2. Probability vs. Skills

Lead conversion is a numbers game. The more you have to

play with, the higher the chance of converting them.

Of course, you’ll need other essential skills, such as lead

selection, due diligence and negotiation. So what you lack in

skills you can make up with numbers.

You can source leads via one or a combination of the following

methods. Which methods you choose are up to you but you

need to know your own strengths and weaknesses.

4.3. Where to Find Leads

4.3.1. Other Investors’ Unwanted Leads

Many investors generate their own leads very successfully

using a whole variety of methods.

This presents an opportunity for you because not all the leads

fall within their buying strategies and so they become the

investors’ excess leads.

Other than throwing them away, many investors would be

keen to pass them to other investors for a finder’s fee if

converted.

Also, you need to market yourself as someone who is unlikely

to waste their leads. So present yourself as an experienced

investor who has good negotiation skills and can complete on

deals quickly.

Of course investors who pass you their leads won’t expect you

to convert every one of them, but you’ll need to give them

regular feedback, at least on a weekly basis.

Otherwise, they won’t do business with you anymore. Just

imagine how annoying it is if someone gives you a lead for free

54

on goodwill and he or she has to keep chasing you for

feedback or doesn’t hear from you again!

In order to find these investors, you’ll need to know where

they gather online and offline. Examples include:

4.3.2. Property Networking Events

See www.BerkshirePropertyMeet.com for the UK’s largest

monthly networking event.

This is one property event that we both attend every

month. If you want to network, then the Berkshire Meet is

a must!

4.3.3. Online Property Forums

Our online forum is located at

www.NetworkPropertyInvestment.co.uk. Here you will

find hundreds of people looking for leads and deals and

are ready to exchange them with you.

4.3.4. Local Investors / Developers

All you need to do is to open the Property Section of your local

newspaper and you’ll find ads headlined “Cash for Your

Properties”, “Facing Repossession”, etc. These companies

generate a large number of leads from motivated sellers who

need to sell their houses quickly.

You’ll find more of these companies’ contact details if you go

to a search engine like Yahoo and Google and type these

keywords.

Contact them and ask if they have any excess leads in

exchange for finder’s fees if the deals convert.

One thing to bear in mind is that these advertisers get

requested for free leads a lot from fellow investors. They may

55

just take your contact details and say they would contact you

but you don’t hear from them anymore.

One piece of advice is to be persistent and contact them on a

weekly basis either via email or phone. This way, you present

yourself as a serious investor and not a time-waster.

4.3.5. Internet Marketing

We’ve already mentioned advertisers on search engines and

undoubtedly, this is one of the most popular and competitive

methods of generating leads.

In order to generate leads online, you need two things:

1. A lead generation website

2. An online marketing campaign

Generally, setting up a website is simple. If you’re not a

graphics designer or web developer, you can pay someone

else to do it for you. Just send us an email and we can refer

some great people to you.

A website could cost from less than a hundred to a few

thousand pounds, depending on its level of sophistication and

functionality.

An important lesson to learn here is that it doesn’t matter how

impressive your website’s graphics are; unless it has the

following two qualities, you will not generate a good quantity

of quality leads.

Superb copy-writing

An effective advertising campaign

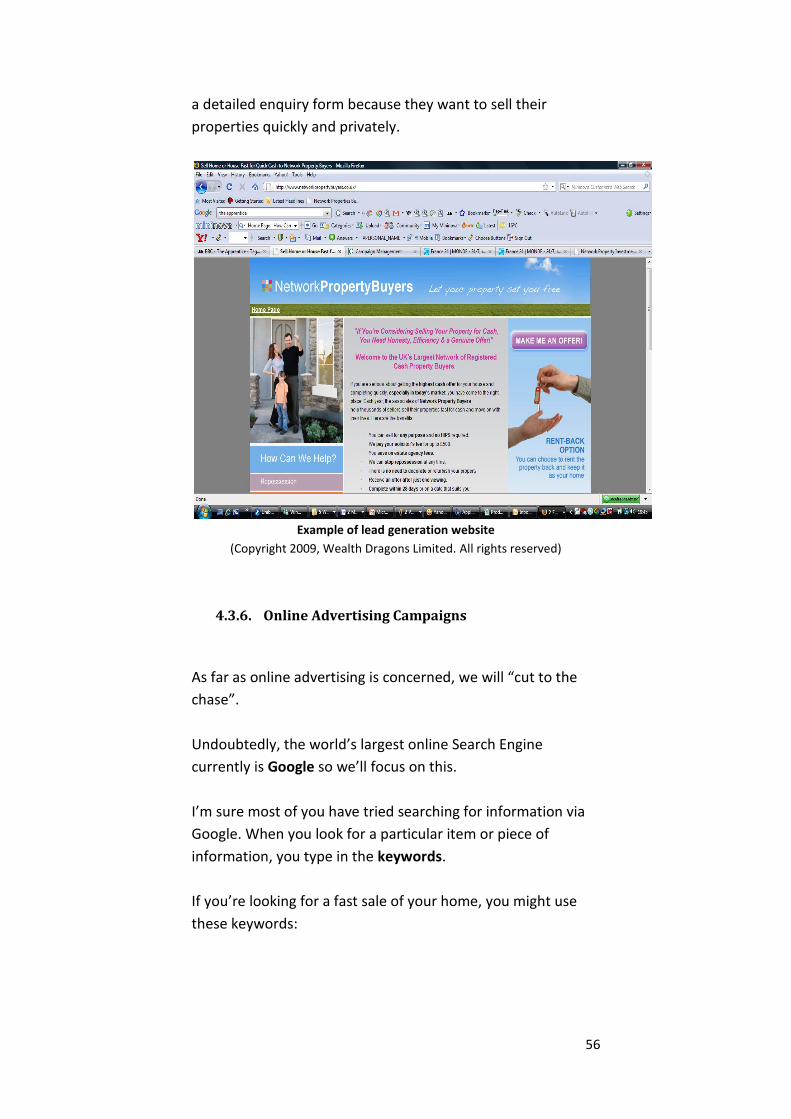

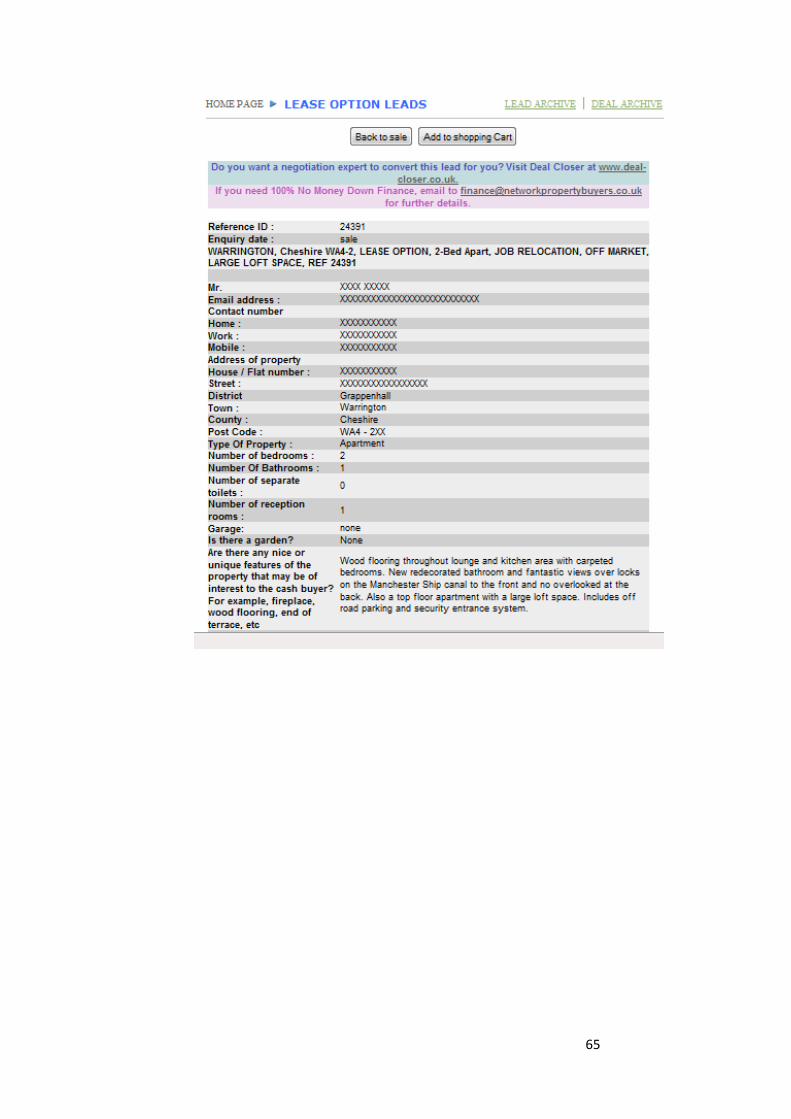

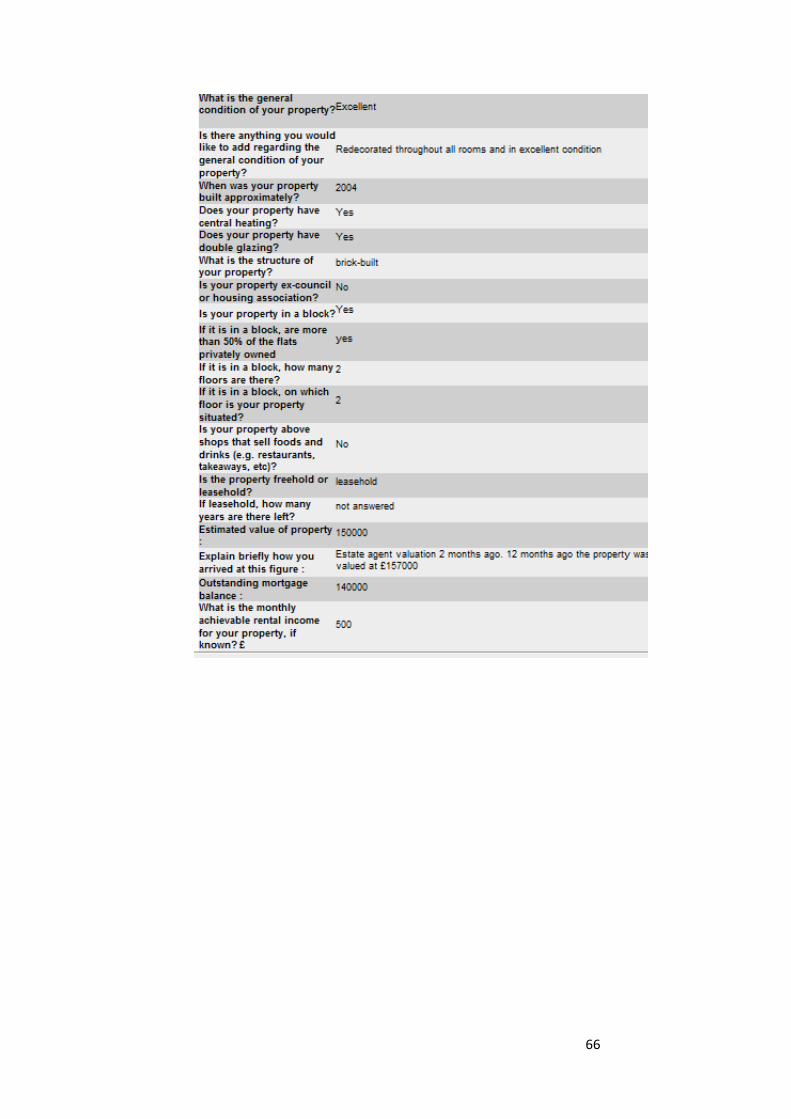

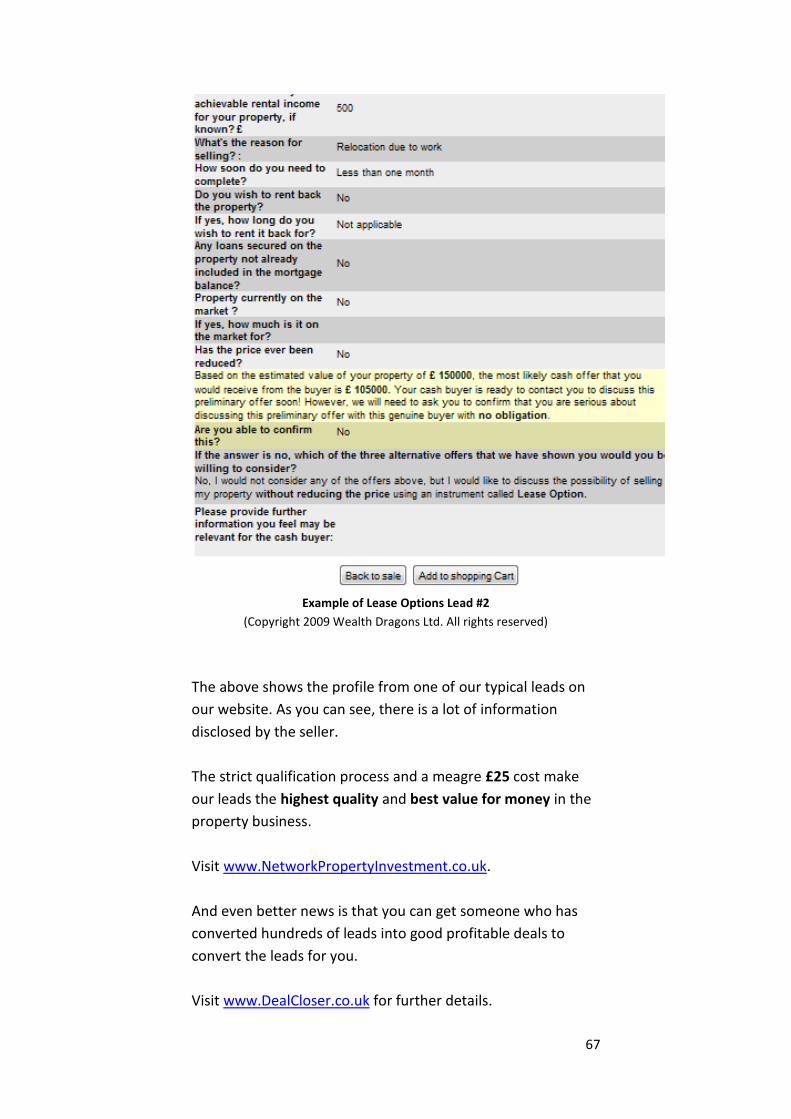

Our website Network Property Buyers

www.NetworkPorpertyBuyers.co.uk has generated over

30,000 leads over the past 24 months from sellers who filled in

56

a detailed enquiry form because they want to sell their

properties quickly and privately.

Example of lead generation website

(Copyright 2009, Wealth Dragons Limited. All rights reserved)

4.3.6. Online Advertising Campaigns

As far as online advertising is concerned, we will “cut to the

chase”.

Undoubtedly, the world’s largest online Search Engine

currently is Google so we’ll focus on this.

I’m sure most of you have tried searching for information via

Google. When you look for a particular item or piece of

information, you type in the keywords.

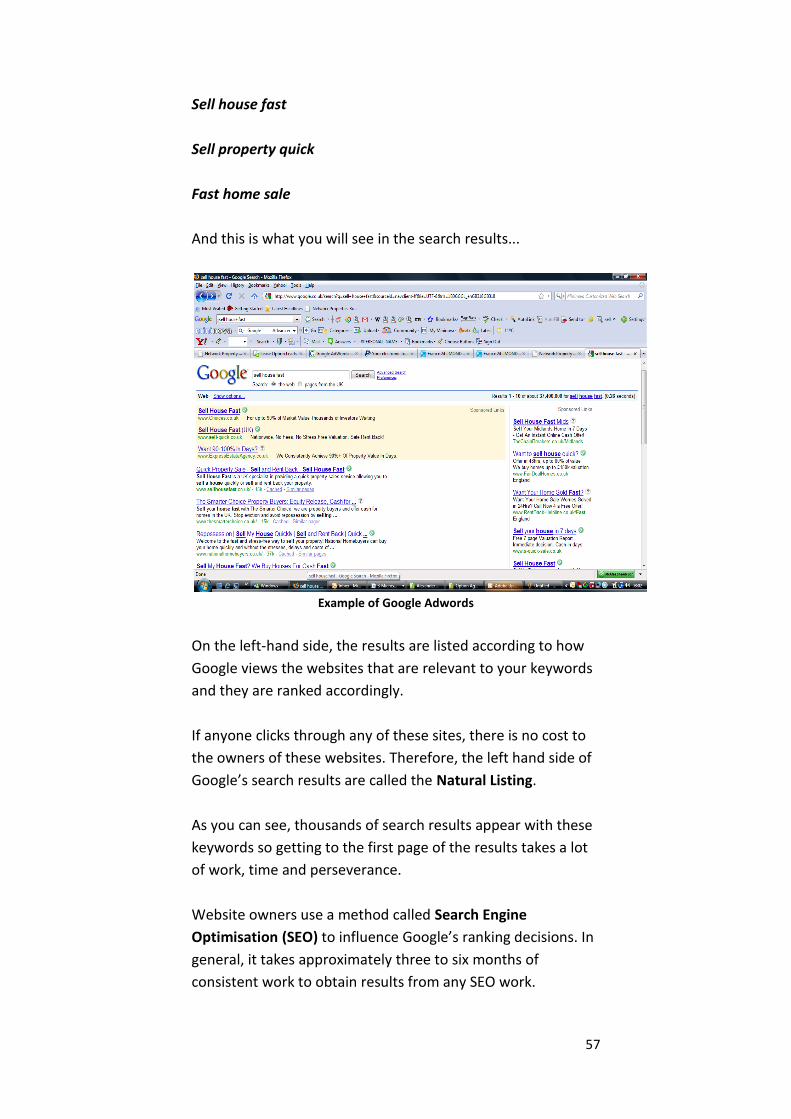

If you’re looking for a fast sale of your home, you might use

these keywords:

57

Sell house fast

Sell property quick

Fast home sale

And this is what you will see in the search results...

Example of Google Adwords

On the left-hand side, the results are listed according to how

Google views the websites that are relevant to your keywords

and they are ranked accordingly.

If anyone clicks through any of these sites, there is no cost to

the owners of these websites. Therefore, the left hand side of

Google’s search results are called the Natural Listing.

As you can see, thousands of search results appear with these

keywords so getting to the first page of the results takes a lot

of work, time and perseverance.

Website owners use a method called Search Engine

Optimisation (SEO) to influence Google’s ranking decisions. In

general, it takes approximately three to six months of

consistent work to obtain results from any SEO work.

58

Further details about SEO can be found at

http://en.wikipedia.org/wiki/Search_Engine_Optimization

The results on the right hand side are based on Google

Adwords or Pay Per Click campaign.

Advertisers are charged each time their ads are clicked by end

users. The cost per click (CPC) depends on how many other

ads are bidding for those keywords.

Generally for each keyword, the higher the position you want

your ad to appear in the search results, the more money you’ll

need to bid. The reason is that more traffic tends to go

through a higher position than a lower one and hence, more

expensive.

However, if the quality of your ad is good because people find

it relevant to what they’re searching for, it will enjoy a higher

click through rate (CTR). If both you and your competitor are

both bidding the same amount of money per click or CPC for a

particular keyword, your ad will enjoy a higher position than

your competitor and your overall cost will be lower.

One way to improve the quality of your ad is through good

copy-writing.

Here are some tips to help you get started:

1. Adword Tool

Use it to identify your competition and demand for your

chosen keywords. The less competitive ones could be very

cheap to bid for.

2. Don’t bid too much

If the cost price of your product is £5, it doesn’t make sense

that you’re spending £6 to achieve a sale.

You’ll need to work out how much you’re spending on your

campaign in relation to your sales and profit.

59

3. Avoid the top three positions

Unless you’re a multi-national company with unlimited budget

trying to create brand awareness, the top three positions will

get you lots of traffic but of low quality and your budget will

be used up in no time!

People often mistake the ads in the top three as links from the

natural listing as they do appear on the “left hand side” or the

result page.

Find an optimal position that generates a profit for your

campaign.

4. Relevancy

The biggest mistake that people make is that they create their

Google ads that are irrelevant to their chosen keywords.

For example, if your keywords are “Sell your House Fast” and

your Google ad says “Sale and Rent Back”, there is little

relevancy in the eyes of Google, although the latter may be

part of your service.

What is worse is that when people click through your Google

ad, they are taken to your website that is irrelevant to what

they are looking for.

Google rewards relevancy and penalises irrelevancy. The way

they do it is to make you pay more for the same keywords that

you are bidding for a particular position.

For example, if you and someone else are both bidding “sell

house fast” for position 4 and Google perceives your ad to be

less relevant to the keywords, you would have to pay more.

Unfortunately, most people do not set up their Google

campaigns properly and end up spending their budgets quickly

without generating good results.

60

The truth is that if Google Adwords are done properly, it is one

of the most powerful advertising media in the world.

If you want some FREE tips about generating leads while you

sleep using Google Adwords, visit our website at

http://www.wealthdragons.co.uk/leadgeneration.htm.

4.3.7. Leafleting

You can create highly targeted results through leafleting that

can’t be achieved via the internet.

The key to success in good leafleting is, you guessed it, good

copy-writing skills as discussed.

The main disadvantage is that if your message is ineffective,

you will have to wait until your next batch of leaflets before

any changes can be made.

Therefore, to be effective in leafleting and any advertising

campaigns, you need to split test your ad and measure your

results.

In any given campaign, you should have at least two versions

of advertisement with only one thing different between them.

For example, in a particular campaign you could have two

identical ads but different headlines.

You also need to tag each ad with a reference. Otherwise, you

can’t measure your results. That’s the reason why many ads

ask you to call a number and quote a reference.

After a period of time, you’ll know exactly which of your two

versions have produced better results. You then simply delete

the worse performing version and create a new version to try

to beat the one you’ve kept.

61

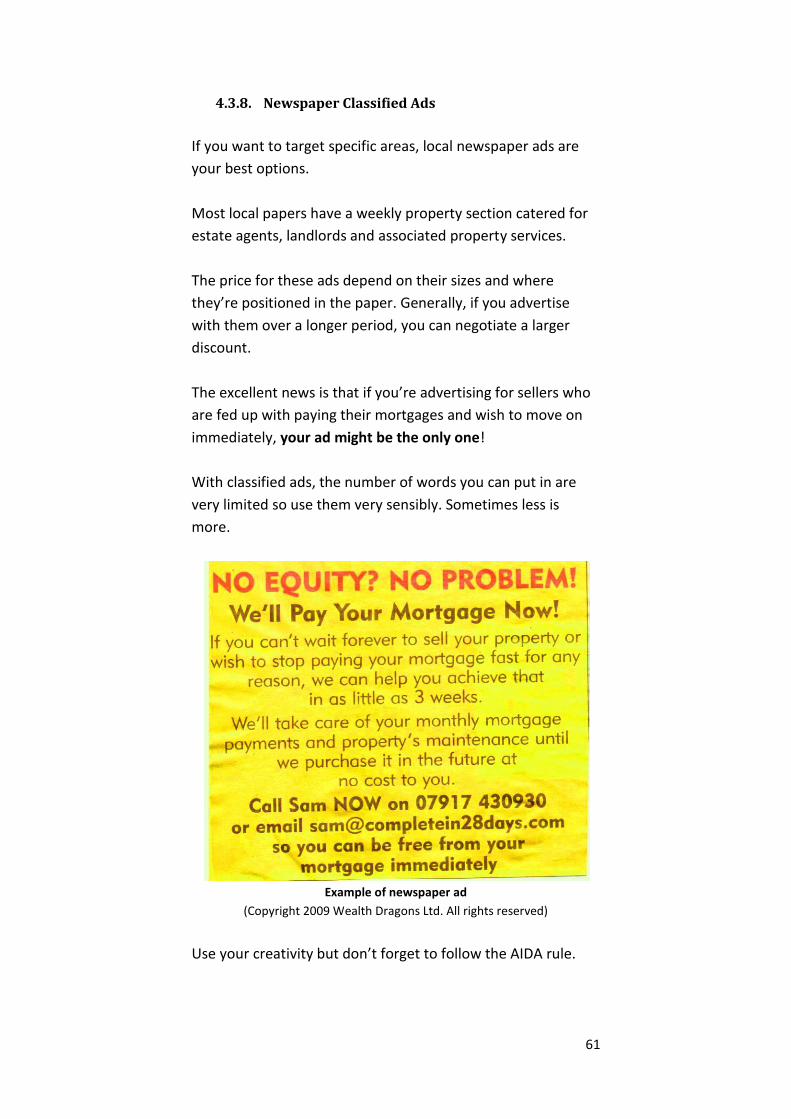

4.3.8. Newspaper Classified Ads