Embed Size (px)

Citation preview

Revision 11-15-2020

HOME MORTGAGE PROGRAMS

OPERATING MANUAL

CONNECTICUT HOUSING FINANCE AUTHORITY

999 West Street, Rocky Hill, CT 06067-4005

Main: (860) 721-9501 Fax: (860) 571-3550

Website: www.chfa.org

Revision 11-15-2020

Table of Contents

SECTION 1 – GENERAL INTRODUCTION

1.1 Preface

1.2 Organization

SECTION 2 – PROGRAM INFORMATION

2.1 Qualification of Participating Lenders

2.2 Distribution of Mortgage Funds

2.3 Funds Available for Targeted Areas

2.4 Commitment for Mortgage Purchase

2.5 Retention and Inspection of Records

2.6 The Federal Recapture Tax

SECTION 3 – ELIGIBILITY

3.1 Eligible Borrowers

3.2 Eligible Dwellings

SECTION 4 – REHABILITATION MORTGAGE LOANS

(203(k) Standard and 203(k) Limited)

4.1 Program Descriptions

4.2 Borrower Eligibility

4.3 Property Eligibility

4.4 Principal Residence Requirement

4.5 Rehabilitation Loan Amounts and Eligible Repairs

4.6 Builders and Contractors

4.7 Contracts and Rehabilitation Work Specifications

4.8 Completion of Work and Construction Period

4.9 Post-Closing Inspection

4.10 Rehabilitation Escrow Account

4.11 Additional Documentation

4.12 Origination Fee and Closing Costs

Revision 11-15-2020

SECTION 5 – UNDERWRITING (See Section 8 for DAP Underwriting)

5.1 Credit Review

5.2 Applicant Processing

5.3 Mortgage Insurance or Guaranty

5.4 Closing Costs

5.5 Loan Submission to CHFA for Commitment

5.6 Delegated Underwriting (LEAN)

SECTION 6 – LOAN PREPARATION

6.1 Terms and Conditions of Loans

6.2 Title Insurance

6.3 Hazard/Flood Insurance

6.4 Property Description

6.5 Appraisal Requirements

SECTION 7 – LOAN PURCHASE

7.1 Closing Procedures

7.2 Purchase of Committed Loans

7.3 Release of Loan Servicing

7.4 Preparation of Mortgage Releases

7.5 Assumption of Loans

SECTION 8 – DOWNPAYMENT ASSISTANCE PROGRAM

8.1 Qualification of Participating Lenders

8.2 Funds Availability

8.3 Eligibility

8.4 Computation of DAP Loan Amounts

8.5 Application Processing

8.6 Loan Preparation

8.7 Loan Purchase

8.8 Servicing

8.9 Credit Review

8.10 Income

8.11 Co-Signers

8.12 Underwriting Ratios

8.13 Credit Reports

8.14 Credit Scores

8.15 Delinquent Credit

8.16 Property Repairs

Revision 11-15-2020

SECTION 9 – RESERVED FOR FUTURE USE

SECTION 10 - APARTMENT CONVERSION FOR THE ELDERLY (ACE)

10.1 Introduction

10.2 Eligibility

10.3 Application Process

10.4 Terms and Conditions

10.5 Construction Requirements

SECTION 11 – INVESTOR REPORTING AND REMITTANCE

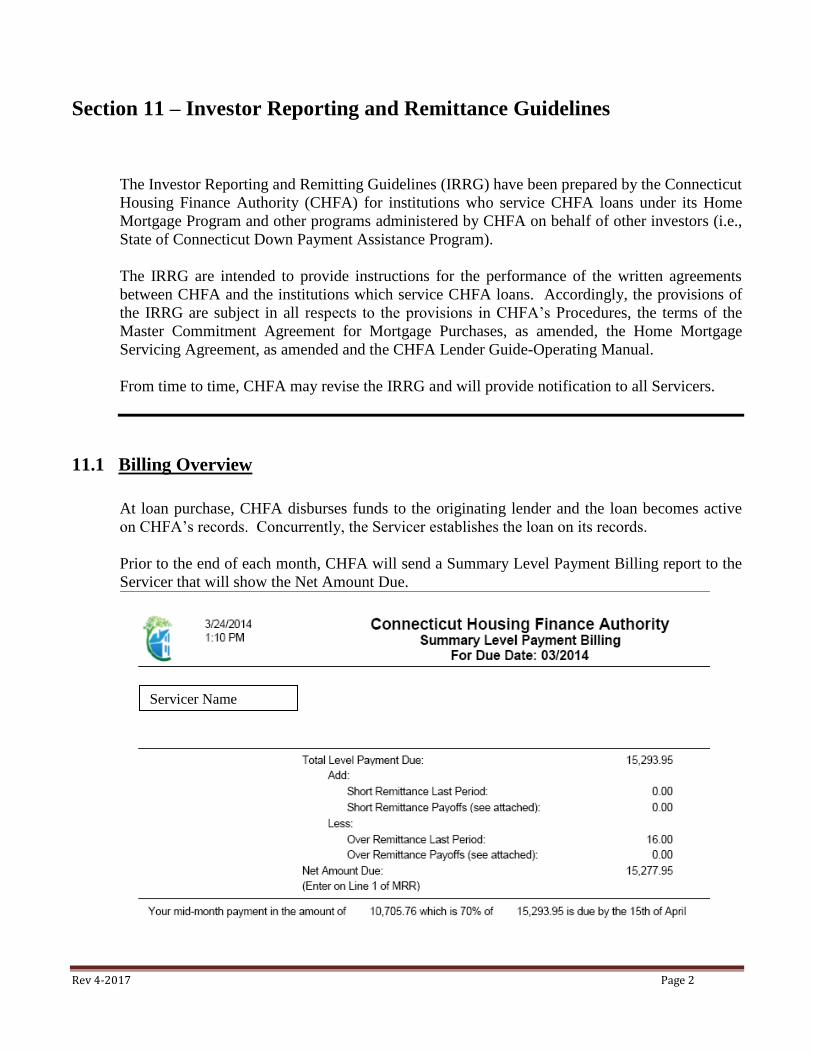

11.1 Billing Overview

11.2 Remittance of Funds

11.3 Reporting

SECTION 12 – DELINQUENCY & FORECLOSURE REPORTING

12.1 List of Approved Law Firms

12.2 Claims Submission and Expense Reimbursement

12.3 90 Days or More Delinquency Reporting

12.4 90 Day Delinquency Form

12.5 Code Translation Table Form

12.6 Foreclosure Initiation/Action Notification Reporting

12.7 CHFA Foreclosure Approval Initiation/Action Notification

12.8 Additional Changes to Current Requirements

12.9 Safekeeping of Authority Documents

12.10 CHFA Delinquency Intervention Counseling Program

12.11 Sample Reporting Stream

SECTION 13 – RESERVED FOR FUTURE USE

SECTION 14 – GLOSSARY OF TERMS

Rev. 4-2015 Page 1

SECTION 1 – GENERAL INTRODUCTION

1.1 Preface

1.2 Organization

Rev. 4-2015 Page 2

SECTION 1 – GENERAL INTRODUCTION

1.1 Preface

This Operating Manual (the “Manual”) has been prepared by the Connecticut Housing

Finance Authority (CHFA) to provide Loan origination and operating guidelines for

Participating Lenders in its Home Mortgage Purchase Program. This Manual supersedes

all prior operating manuals, program bulletins or other home mortgage program materials

distributed by CHFA.

CHFA mortgage loans are available to borrowers who meet income and other eligibility

criteria described in this Manual, at a below market interest rate based on the sale of

CHFA bonds. In addition, CHFA finances home mortgages in Targeted Areas without

regard to income limits providing the borrower(s) are not obtaining a downpayment

assistance loan with CHFA. CHFA does not refinance existing mortgage loans, except

when coupled with substantial rehabilitation, or as part of a “special program” initiative

authorized by the Authority.

The purpose of the Home Mortgage Purchase Program is to further the general policies of

Chapter 134 of the Connecticut General Statutes, including the specific statutory

objectives of:

A. Providing funds for long-term mortgage financing of residential housing

for occupancy by low and moderate income persons and families in

Connecticut; and

B. Encouraging the development of balanced communities of all income

levels in cities which qualify as Urban Areas under the Act.

1.2 Organization

This Manual is intended to provide policy guidelines and detailed instructions for the

performance of the written agreements between CHFA and its Participating Lenders.

Accordingly, the provisions of this Manual are subject in all respects to the provisions in

the Authority’s procedures and the definitive terms of the Master Commitment

Agreement for Mortgage Purchases and the Home Mortgage Servicing Agreement in

effect from time to time.

From time to time, CHFA may revise this Manual by issuing changed or additional

pages, or with the publication of CHFA Notice to Participating Lenders or CHFA

Bulletins. Notices to Participating Lenders and CHFA Bulletins will be sent to the

Rev. 4-2015 Page 3

Participating Lender designated authorized staff and simultaneously posted on the CHFA

website at www.chfa.org.

As noted throughout the Manual, CHFA requires the use, as appropriate, of FHA, VA, or

FNMA/FHLMC printed Mortgage Deed and Promissory Note forms in all cases.

Participating Lenders are responsible for processing and servicing Loans in accordance

with specific FHA, VA, USDA-RD, CHFA or private mortgage insurance (PMI)

requirements, when applicable, and only general reference is made to those requirements

in this Manual.

Throughout this Manual masculine references shall include both genders or either gender,

as appropriate.

Rev. 1-2017 Page 1

SECTION 2 - PROGRAM INFORMATION

2.1 Qualification of Participating Lenders

2.2 Distribution of Mortgage Funds

2.3 Funds Available for Targeted Areas

2.4 Commitment for Mortgage Purchase

2.5 Retention and Inspection of Records

2.6 The Federal Recapture Tax

Rev. 1-2017 Page 2

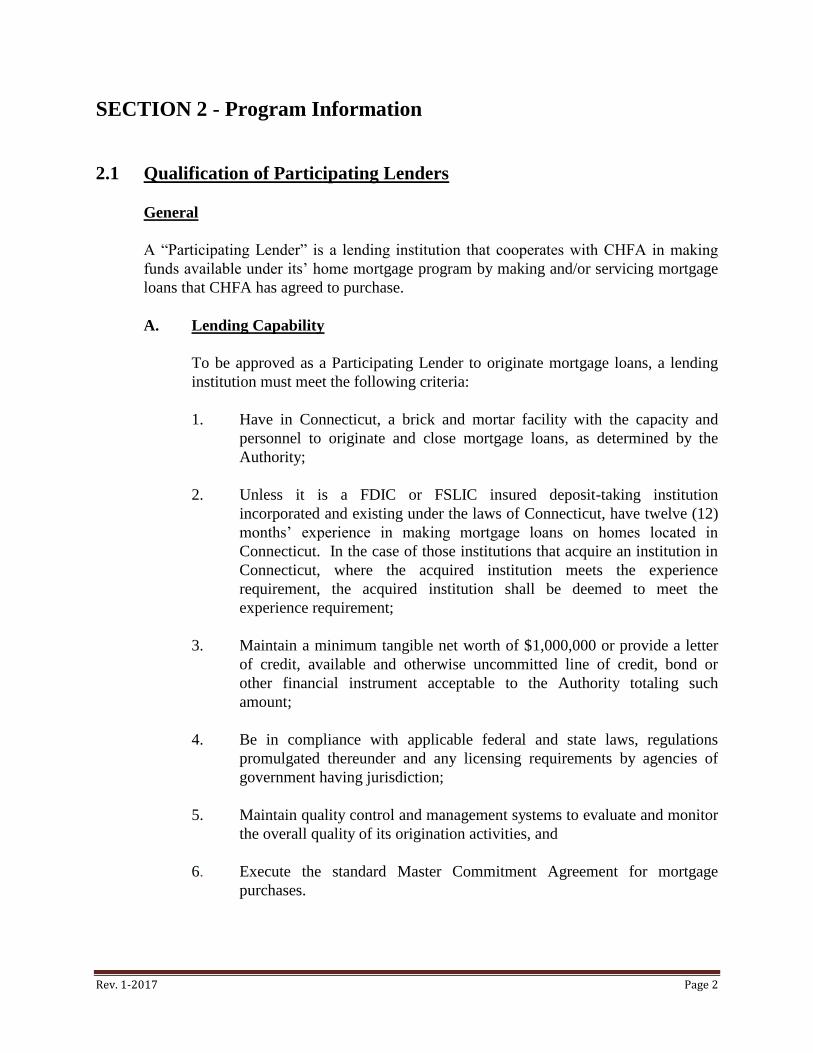

SECTION 2 - Program Information

2.1 Qualification of Participating Lenders

General

A “Participating Lender” is a lending institution that cooperates with CHFA in making

funds available under its’ home mortgage program by making and/or servicing mortgage

loans that CHFA has agreed to purchase.

A. Lending Capability

To be approved as a Participating Lender to originate mortgage loans, a lending

institution must meet the following criteria:

1. Have in Connecticut, a brick and mortar facility with the capacity and

personnel to originate and close mortgage loans, as determined by the

Authority;

2. Unless it is a FDIC or FSLIC insured deposit-taking institution

incorporated and existing under the laws of Connecticut, have twelve (12)

months’ experience in making mortgage loans on homes located in

Connecticut. In the case of those institutions that acquire an institution in

Connecticut, where the acquired institution meets the experience

requirement, the acquired institution shall be deemed to meet the

experience requirement;

3. Maintain a minimum tangible net worth of $1,000,000 or provide a letter

of credit, available and otherwise uncommitted line of credit, bond or

other financial instrument acceptable to the Authority totaling such

amount;

4. Be in compliance with applicable federal and state laws, regulations

promulgated thereunder and any licensing requirements by agencies of

government having jurisdiction;

5. Maintain quality control and management systems to evaluate and monitor

the overall quality of its origination activities, and

6. Execute the standard Master Commitment Agreement for mortgage

purchases.

Rev. 1-2017 Page 3

B. Servicing Capability

To be approved by CHFA as a Participating Lender to service Authority loans, the

institution must meet the following criteria:

1. Have the capacity and personnel to service mortgage loans, as determined

by the Authority;

2. Demonstrate a proven ability to service the type of mortgages for which

Authority approval is being requested;

3. Maintain a minimum tangible net worth of $1,000,000 or provide a letter

of credit, available and otherwise uncommitted line of credit, bond or

other financial instrument acceptable to the Authority totaling such

amount;

4. Be in compliance with applicable federal and state laws, regulations

promulgated thereunder and any licensing requirements by agencies of

government having jurisdiction;

5. Maintain quality control and management system systems to evaluate and

monitor the overall quality of its servicing activities; and

6. Execute the standard Home Mortgage Servicing Agreement and/or other

contracts as determined by the Authority.

C. Removal of a Participating Lender

CHFA may terminate the Master Commitment Agreement for Mortgage

Purchases and/or the Home Mortgage Servicing Agreement according to their

terms, respectively, and remove from the list of approved Participating Lenders

any lending institution that has;

1. Failed to commit, close and/or service Mortgage Loans in accordance with

the Act, the Procedures of this manual, and the Master Commitment

Agreement for Mortgage Purchases, and/or the Home Mortgage Servicing

Agreement or;

2. Ceased to meet the criteria for becoming a Participating Lender. CHFA

may terminate the Master Commitment Agreement for Mortgage

Purchases and/or the Home Mortgage Servicing Agreement in accordance

with the provisions thereof. Such removal shall take place thirty (30) days

after written notice to such Participating Lender specifying the reason for

the removal.

Rev. 1-2017 Page 4

D. Lending Areas

Participating Lenders are not required to go beyond their normal geographic

lending areas.

E. Availability of Program

Participating Lenders shall not restrict applications for Loans to any segment of

the Homebuyer Mortgage Program, except that a participating lender need not

accept applications for Rehabilitation Mortgage Loans (see Section 4) and need

not accept applications for mortgage loans on homes located outside its normal

geographic lending areas.

F. Training Session

After CHFA has approved a Participating Lender, the Participating Lender shall

promptly have a training session with CHFA staff prior to originating a CHFA

loan. The training session shall cover CHFA's requirements in regard to

originating and closing loans, providing CHFA with the required loan documents

after closing, and, where appropriate, servicing requirements. CHFA shall have

the right to require a Participating Lender to have a retraining session when CHFA

deems it appropriate.

G. Correspondent Lender Relationships

A Participating Lender may sponsor a "Correspondent Lender" with the prior

written approval of the Authority. The Sponsoring Participating Lender will be

required to meet and provide evidence of a minimum tangible net worth of

$1,000,000 in order to sponsor a Correspondent Lender. To be approved as a

Correspondent Lender by the Authority, the Correspondent Lender must meet the

same criteria for a Participating Lender as described in subsection (A.) above,

except as follows:

1. Have a minimum tangible net worth of $50,000;

2. The Correspondent Lender may be required to execute the standard Master

Commitment Agreement for Mortgage Purchases and the standard Home

Mortgage Servicing Agreement although a standard letter agreement

between the parties will be executed by both parties;

3. The Correspondent Lender may be required to attend a training session(s)

prior to originating any CHFA loans on behalf of the Sponsoring

Participating Lender and any additional training session(s) as the Authority

deems appropriate; and

Rev. 1-2017 Page 5

4. Conform to guidelines as required by the Connecticut Department of

Banking and/or the Authority regarding licensing of a Correspondent

Lender in the State of Connecticut;

5. Veterans Administration (VA) and Federal Housing Administration (FHA)

approval are not required.

An approved Correspondent Lender may originate home mortgage loans on behalf of a

Sponsoring Participating Lender. However, the Sponsoring Participating Lender shall

remain fully responsible to the Authority for its obligations pursuant to these procedures,

the CHFA Home Mortgage Program Operating Manual, and the Master Commitment

Agreement for Mortgage Purchases. Correspondent Lender Loans must be approved and

submitted by the Sponsoring Participating Lender. The Authority reserves the right to

limit the number of Correspondent Lenders and may rescind approval of a Correspondent

Lender at any time with (prior) written notice.

2.2 Distribution of Mortgage Funds

A. Availability of Funds

CHFA will not issue separate allocations to any particular Participating Lenders.

A funds reservation system which allows the borrower to apply for a CHFA Loan

at the Lender of his choice will be used.

CHFA reserves the right, however, to set aside a portion of the proceeds of any

issue of bonds on an uncommitted basis for any purpose of the Program.

Specifically, CHFA expects to set aside certain proceeds from each issue for the

purpose of making Mortgage Loans in Targeted Areas.

B. Reservation of Loan Funds

CHFA will administer the reservation program and Participating Lenders may

accept Loan applications from prospective borrowers.

1. The Participating Lender will determine if the prospective mortgagor is

qualified as an Eligible Borrower. Such preliminary determination shall

include the Participating Lender's examination of (i) the prospective

borrower's written purchase agreement concerning the property to be

financed, and (ii) a copy of the borrower's most recently filed Federal

Income Tax Return as an approximate indication of his income.

Rev. 1-2017 Page 6

2. After the Participating Lender has determined an applicant's eligibility for

CHFA financing, the lender will reserve mortgage funds using the CHFA

On-line Reservation System.

a. The reservation will be identified by an authorized reservation loan

number, which will be assigned by the on-line reservation system.

This reservation number must appear on the Loan submission to

CHFA and all subsequent correspondence regarding the Loan

submission.

b. The reservation of funds prior to Loan commitment is valid for

ninety (90) days unless extended by CHFA.

c. Loan reservations must include the names of all borrowers.

Substitute borrowers or the addition of or removal of a borrower to

qualify for the loan may NOT be permitted once the loan

reservation is secured.

3. The Participating Lender must notify CHFA of any cancellation of

reserved funds so that the funds may be made available for others. No

substitution of borrower will be permitted for reserved funds. No

substitution of property will be permitted for reserved funds except as

approved by CHFA in the case of a situation, outside of the control of the

borrower, causing hardship. CHFA may decline to reserve funds for an

applicant who has had other CHFA funds reserved.

C. Free Accessibility to Funds

Applications for Loans shall be based on eligibility and not on special

relationships between a Participating Lender and particular real estate brokers or

developers. A Participating Lender may not deny a Loan to an Eligible Borrower

solely because the Eligible Borrower is not a depositor or customer of the

Participating Lender. Neither may the Participating Lender limit the availability

of CHFA financing by denying an application based on the fact that the applicant

does not belong to a specified group of the public such as employees of certain

organizations. Under normal circumstances, applications should be taken and

processed on a "first-come, first-served" basis.

2.3 Funds Available for Targeted Areas

A. General

Rev. 1-2017 Page 7

In accordance with Federal requirements, CHFA will make funds available for

Eligible Dwellings located in Targeted Areas. CHFA will exercise due diligence

in making Mortgage Loans in Targeted Areas. Participating Lenders under

CHFA's direction shall assist in advising potential Eligible Borrowers of the

availability of funds in Targeted Areas.

B. Eligibility

Mortgage Loans for Eligible Dwellings located in Targeted Areas must comply in

all respects with the requirements in Section 3 and elsewhere in this Manual for

all Mortgage Loans except for the requirement in Section 3.1C that an Eligible

Borrower may not have had a present ownership interest in the Borrower's

principal residence in the three years preceding the application for the Mortgage

Loan. Also, with exception to section 3.1B where a borrower shall not have an

aggregate income in excess of the applicable limit established by CHFA unless

the borrower is also applying for CHFA Downpayment Assistance (contained in

appendix B).

2.4 Commitment for Mortgage Purchase

A. Obtaining a Commitment

The Participating Lender shall submit each Loan application to CHFA with

completed forms and documents referred to in Section 5 of this Manual.

Each Loan submission will be underwritten and analyzed by CHFA, and if

approved, a Commitment will be sent to the Participating Lender. The

Commitment will be effective for a period of 90 days as designated therein.

Loans will be purchased by CHFA in accordance with the Commitment and

pursuant to Section 7 of this Manual.

B. Commitment to be Based on Authorized Funds Reservation

Each Loan submission requesting a Commitment must be clearly identified with

the CHFA authorized reservation number previously assigned the mortgage loan

amount reserved, unless otherwise permitted by CHFA.

C. Extensions and Cancellations

Requests for extension or cancellation of a Commitment must be in writing and

signed by a mortgage officer or other authorized person of the Participating

Lender. Telephone cancellations will not be accepted. Requests should be

directed to the Single Family Homeownership Dept. of CHFA prior to expiration.

Rev. 1-2017 Page 8

2.5 Retention and Inspection of Records

Any documents required by this Manual or by State or Federal law, not delivered to

CHFA pursuant to a Commitment or purchase of a Loan, must be retained by the

Participating Lender or Servicer for at least two years after the date of purchase by

CHFA, or such longer period as may be required by law, and, if requested by CHFA, for a

reasonable period thereafter. If during such retention time CHFA requests original or

certified copies of such documents, the same must be delivered to CHFA. Where

appropriate, such documents may be kept on microfilm, micro card or other similar

photographic methods.

Participating Lenders must make all records and books maintained in connection with

Loans available for inspection by CHFA upon request during reasonable business hours.

The absence of documentation required to be retained by this section may, at the option of

CHFA, be construed to conclusively evidence a defect in such documentation under the

Master Commitment Agreement for Mortgage Purchases.

2.6 The Federal Recapture Tax

Congress enacted legislation in 1988, subsequently amended in October of 1990, to

recapture a portion of the "subsidized amount" from home buyers who receive qualified

mortgage bond assistance after January 1, 1991. This includes all buyers who use CHFA

Loans and Mortgage Credit Certificates (MCC), dispose of an interest in their residence

within nine (9) years of purchase, and whose incomes substantially increase. The amount

of Recapture Tax that Borrower(s) might have to pay depends on how much their

incomes have increased, their family size at the time of sale, the original amount of their

mortgage, the length of time they owned their home and any gain realized on disposition

of the home. The recapture amount is the lesser of:

(1) 50 percent of the gain realized on disposition, or

(2) A percentage of the subsidized amount. The percentage is the product

of the holding period percentage and the income percentage (both

discussed below).

The Borrower(s) is responsible for calculating and paying the Recapture Tax, if any, as

additional Federal tax liability for the tax year in which the interest in the home is

disposed. However, Participating Lenders are required to provide homebuyers with the

Authority's "Notice of Potential Recapture Tax Form 051-0597" and "Method to

Compute Recapture Tax Form 052-1195":

Rev. 1-2017 Page 9

A. No Recapture Tax is due and the Borrower(s) does not need to do the

calculation if any of the following occurs:

1. The Borrower(s) disposes of his home later than nine (9) years after the

mortgage loan is closed.

2. The home is disposed of as a result of the Borrower(s) death.

3. The Borrower(s) transfer the home either to his spouse or former spouse

incident to divorce and no gain of loss was incurred on the transfer and

included in his Federal taxable income.

4. The home was disposed of at a loss.

5. The Borrower(s) modified adjusted gross income for the year in which the

home is sold does not exceed the Threshold Income, adjusted for family

size, for such year. Modified Adjusted Gross Income is calculated as

follows:

Adjusted Gross Income from IRS 1040 $

Tax exempt income earned for the year +

Gain on sale of the home -

Modified Adjusted Gross Income = $

B. There are several steps required to calculate the actual recapture amount

owed. The following outlines the steps involved in the calculation:

1. Threshold Income (Adjusted Qualifying Income)

The first year Threshold Income is 5% greater than the maximum

allowable Federal income limit for the area in which the residence is

located at the time the borrower was qualified. Each year of the nine (9)

year holding period the Threshold Income is increased by 5% from the

previous year's Threshold Income. The Threshold Income for each of the

nine (9) years is provided to the Borrower(s) in the "Notice to

Mortgagor(s) of Maximum Recapture Tax and of Method to Compute

Recapture Tax on Sale of Home" letter which will be issued by CHFA at

the time of issuance of the Commitment.

Rev. 1-2017 Page 10

2. Holding Period Percentage

The percentage is based on the month in which the disposition occurs after

the loan closing date pursuant to the following table:

Disposition Within Month of Closing

1-12 - 20%

13-24 - 40%

25-36 - 60%

37-48 - 80%

49-60 - 100%

61-72 - 80%

73-84 - 60%

85-96 - 40%

97-108 - 20%

3. Maximum Recapture Amount

The Federally subsidized amount which is 6.25% multiplied times the

highest principal amount of the mortgage loan, multiplied times the

Holding Period Percentage.

4. Income Percentage

The modified adjusted gross income of the Borrower(s) for the taxable

year in which the disposition occurs minus the Threshold Income divided

by $5,000.

5. Adjusted Recapture Amount

The Maximum Recapture amount multiplied times the Income Percentage.

6. Recapture Amount

Equals the lesser of the Adjusted Recapture Amount or 50 percent of the

gain realized on the disposition.

C. Limitations and Special Rules on Recapture Tax

1. If you give away your home (other than to your spouse or ex-spouse

incident to divorce), you must determine your actual Recapture Tax as if

you had sold your home for its fair market value.

Rev. 1-2017 Page 11

2. If your home is destroyed by fire, storm, flood, or other casualty, there

generally is no Recapture Tax if, within two (2) years, you purchase

additional property for use as your principal Residence on the site of the

home financed with your original subsidized mortgage Loan.

3. In general, except as provided in future regulations, if two or more persons

own a home and are jointly liable for the subsidized mortgage Loan, the

actual Recapture Tax is determined separately for each person based on

their interests in the home.

4. Refinancing of the Loan does not result in a Recapture Tax. If the home is

disposed of subsequent to the refinancing, but prior to the original nine (9)

year holding period, Recapture Tax may be due.

5. CHFA Reimbursement for Recapture Tax Payment

Borrower(s) that are required to make a recapture tax payment may be

eligible to receive reimbursement from CHFA.

To request reimbursement from CHFA borrower(s) must submit a written request to

CHFA no later than December 31st of the year that the federal recaptures tax is owed and

paid. For example: if the subject property is sold in 2013 and the tax return is filed in

2014, the request for reimbursement must be filed no later than December 31, 2014.

D. Filing the CHFA Reimbursement Request

To request Recapture Tax Reimbursement borrower(s) must submit a written

request to CHFA along with the following documentation:

1. A copy of the TRID – Closing Disclosure (Formerly HUD- 1 Settlement

Statement) - proof of sale of the property or, in the instance where the

home is disposed of by a method other than sale, documentation

evidencing the transfer of title and the Recapture Tax assessment;

2. A copy of the signed, filed Federal Tax Return, along with all schedules

including IRS Form 8828, for the year in which the Recapture Tax was

assessed and paid; and

3. An original signed IRS Form 4506-T completed by each person listed as a

borrower under the mortgage loan documents, authorizing CHFA to obtain

a copy of each such borrower’s Federal Tax Return.

4. Evidence of payment of the Recapture Tax.

5. Recapture Tax Reimbursement Request (CHFA Form 049-0313)

Rev. 1-2017 Page 12

6. Mail the complete Recapture Tax request package to:

Connecticut Housing Finance Authority (CHFA)

Residential Mortgage Programs – Recapture Tax Reimbursement

999 West Street

Rocky Hill, CT 06067

Note: CHFA may require additional information and/or documentation in order to approve a

request for reimbursement and such approval shall be granted at the sole discretion of CHFA,

subject to funding constraints and applicable statutory and procedural requirements.

Rev. 11-2017 Page 1

SECTION 3 - ELIGIBILITY

3.1 Eligible Borrowers

3.2 Eligible Dwellings

Rev. 11-2017 Page 2

Section 3 – Eligibility

3.1 Eligible Borrowers

To qualify for CHFA financing, an applicant must meet the eligibility criteria set forth in

this section.

A. General

An applicant shall be an Eligible Borrower for a CHFA Mortgage Loan if the applicant

meets the following criteria:

1. At the time of application and at the time of mortgage closing, has an annual

aggregate income that is at or below the applicable income limit in effect at the time

the application was taken or is purchasing an Eligible Dwelling in a Targeted Area

(Section 2.3B);

2. Agrees to occupy and use the residential property to be purchased for a permanent,

principal residence within 60 days after the date of the closing of the Mortgage

Loan (See exceptions applicable to 203(k) Rehabilitation Mortgages – Section 4).

Applicant must also agree to occupy the property as their primary residence for the

term of the CHFA mortgage loan. (Section 3.1D);

3. If the applicant currently owns his or her own home now, or has owned a home

within the past three years, he or she may still be eligible for a CHFA mortgage

loan if he or she is buying a home in a Targeted Area or is participating in a CHFA

approved special loan program that is designated specifically for first-time

homebuyers and existing homeowners.

4. Will not use the proceeds of the Mortgage Loan to acquire or replace an existing

mortgage or debt, except in the case of certain types of temporary financing

(Section 3.1E). Rehabilitation Mortgage 203(k) Limited Program (Section 4);

5. Possesses and demonstrates the legal capacity to incur the obligations of the CHFA

Mortgage Loan;

6. Possesses and demonstrates the ability to repay the CHFA Mortgage Loan

(Section 5);

7. Has contracted to purchase an Eligible Dwelling (Section 3.2) or will undertake

Rehabilitation Mortgages on his or her dwelling or on a dwelling he or she has

contracted to purchase (Section 4) and

8. Has executed a Borrower Certificate at the time of the Loan application.

Rev. 11-2017 Page 3

9. Has at the time of application, a social security card as evidence of permanent

residency in the United States. Consular Identification Cards (CID) or Individual

Taxpayer Identification Numbers (ITIN) are not acceptable replacement

documentation for U.S. Government issued social security numbers. The applicant

does not need to be a citizen of the United States.

10. The applicant must purchase a home in the State of Connecticut.

B. Income

An Eligible Borrower and/or co-borrower shall not have aggregate income in excess of

the applicable income limit established by CHFA (contained in Appendix B) and in

force at the time of application for the Mortgage Loan unless the Borrower is

purchasing in a Targeted Area as described in (Section 2.3B).

Aggregate borrower income shall include income from whatever source derived,

including without limitation:

Regular earnings

Part-time earnings

Unemployment compensation

Bonuses

Overtime income, whether or not guaranteed by an employer

Dividends

Interest (except on funds being used for down payment and closing costs)

Commissions

Military allowances

Welfare payments

Disability payments

Pension, annuity, retirement, and social security benefits

Reimbursement for services in military reserve or National Guard.

The Authority may at its option exclude overtime income where it deems such income

to be of short duration and of a temporary nature.

Aggregate income shall be based solely on the income of the mortgagor or mortgagors

(borrower and co-borrowers) only.

1. Calculating Rental Income for 2-4 Unit Dwelling

The rental income from units in a two to four unit dwelling that will be added to the

borrower’s income to qualify for repayment of the mortgage loan debt will be based on

the percentage of the anticipated fair market income consistent with the loan program,

i.e. follow the guidelines of the loan insurer, FHA, VA, USDA-RD, PMI or CHFA

special program, when applicable.

Rev. 11-2017 Page 4

C. Three-Year Requirement

An Eligible Borrower does not include any borrower who, at any time during the three

years preceding the date of application for the Mortgage Loan, had a “present

ownership interest” (as hereinafter defined) in his principal residence. This

requirement does not apply to Mortgage Loans for Eligible Dwellings located in

Targeted Areas. If applicable, the Borrower must certify on the Borrower Certificate

that at no time during the three years preceding the closing of the Mortgage Loan has

he had a present ownership interest in a principal residence.

Eligible borrowers that have a “present ownership interest” in a principal residence

located in any part of the United States, its Commonwealths or Territories are subject to

these requirements and residential properties outside of the United States.

1. Definition of Present Ownership Interest

a. “Present ownership interest” includes:

i. A fee simple interest

ii. A joint tenancy, a tenancy in common, or a tenancy by the entirety;

iii. The interest of a tenant shareholder in a cooperative;

iv. A life estate;

v. A land contract, under which possession and the benefits and burdens of

ownership are transferred although legal title is not transferred until some

later time;

vi. An interest held in trust for the Eligible Borrower(s) (whether or not created

by the Eligible Borrower(s)) that would constitute a present ownership

interest if held directly by the Eligible Borrower(s); and

vii. Occupancy of a property for which an interest in real estate was created by

the existence of an inheritance, probated or not, whether title is vested or

not.

b. Interests which do not constitute a “present ownership interest” include:

i. A remainder interest,

ii. An ordinary lease with or without an option to purchase,

iii. A mere expectancy to inherit an interest in a principal residence,

iv. The interest that a purchaser of a residence acquires on the execution of an

accepted offer to purchase real estate, and

v. An interest in other than a principal residence during the previous (3) years.

vi. An interest in a mobile home that is not permanently fixed to land and

which mobile home is not considered real property for local tax purposes.

vii. Ownership interest in a vacation timeshare with limited occupancy on an

annual basis.

viii. Land only.

Rev. 11-2017 Page 5

2. Disposal of Other Residential Property

a. In cases where a borrower, such as in a Targeted Area, is in the process of

selling such residential property or has sold it during the six months prior to the

date of application for the Loan, the Borrower shall apply the equity proceeds

from the sale of the property (if any) as a downpayment on the Eligible

Dwelling. The borrower may deduct payoff of the present mortgage, real estate

commissions and reasonable closing costs on the home being sold in

determining equity proceeds.

b. Any real estate that is owned by the borrower and used by the borrower as a

residence shall be disposed of or under bona fide contract for sale before the

closing on the CHFA Loan.

c. A borrower may not have an ownership interest in any other primary residential

property that has been owner occupied in the past 3 years at the time of the

mortgage loan closing.

3. Persons Covered

This requirement applies to any person who will execute the mortgage or note and

will have a present ownership interest (as defined in Section 3.C.1) in the Eligible

Dwelling.

4. Prior Tax Returns

To verify that the Eligible Borrower meets the three year requirement, the

Participating Lender must obtain copies of signed Federal Income Tax Returns

filed by the Eligible Borrower for the three years preceding the closing of the

mortgage. Certified copies of the IRS Returns or Transcripts from the IRS are also

acceptable. If the Eligible Borrower was not required by law to file a Federal

Income Tax Return for any of these three years and did not file and so states on the

Borrower Certificate, the requirement to obtain a copy of the Federal Income Tax

Return for such year is waived, however; the Eligible Borrower must request a

“Verification of Non-Filing Letter” from the IRS that will provide proof that the

IRS has no record of a filed 1040, 1040A, or 1040EZ, or any other applicable

return or schedule, for the year(s) requested. In such cases the borrower must also

provide a written statement of explanation regarding non-filing of return.

a. All Eligible Borrower(s) and Co-Borrower(s) applicant(s) who will sign the

CHFA Mortgage Note and Deed at closing are subject to the Federal Income

Tax Return requirements.

Rev. 11-2017 Page 6

b. In addition, the Participating Lender must obtain an executed Request for Copy

or Transcript of Tax Form (IRS Form 4506) or a Tax Information Authorization

IRS Form 8821) for the prior three years. The Participating Lender shall

examine the Federal Income Tax Returns particularly for any evidence that the

Eligible Borrower may have claimed deductions for property taxes or for

interest on indebtedness with respect to real property constituting his principal

residence or on ineligible temporary financing.

c. In cases where the three year requirement regarding prior homeownership is not

applicable, such as loans in Targeted Areas, only the Federal Income Tax Return

and the Request for and Consent to Disclosure of Federal Income Tax Returns

for the most recent year is required. In such cases, one year may be substituted

for any references in this Manual to three years; and the Participating Lender

may manually modify any references in CHFA forms to three years to one year

as applicable.

d. Eligible borrowers that have a “present ownership interest” in a principal

residence located in any part of the United States, its Commonwealths or

Territories are subject to these requirements and residential properties outside of

the United States.

5. Lender’s Responsibility to Verify Documentation

Participating Lender must, with due diligence, verify the information in the

Borrower Certificate regarding the applicant’s prior residency and verify such

other information including Federal Income Tax Returns furnished by the Eligible

Borrower for the preceding three years, and certify to CHFA that on the basis of its

investigation, such information is to the best of its knowledge and belief, true and

accurate and evidences compliance with the requirements of this section. Such

certification shall be made on the Participating Lender Certification.

D. Principal Residence Requirement; Owner-Occupancy

1. General

An Eligible Borrower shall covenant to occupy the Eligible Dwelling as a principal

residence within 60 days after the closing of the Mortgage Loan. Unless the

residence can reasonably be expected to become the principal residence of the

Eligible Borrower within 60 days of the Loan closing date, the residence will not be

considered an Eligible Dwelling and may not be financed with a CHFA Mortgage

Loan. An Eligible Borrower must covenant to occupy the Eligible Dwelling as a

principal residence within 60 days after the Loan closing on the Borrower

Certificate and as part of the CHFA Uniform Mortgage Rider. See exceptions

Rev. 11-2017 Page 7

related to Rehabilitation Mortgages - 203(k) Standard and 203(k) Limited Mortgage

Programs (Section 4).

2. Definition of Principal Residence

A principal residence does not include any residence which can reasonably be

expected to be used: (a) in a trade or business, except for a two to four family

residence, in which case the Eligible Borrower shall be permitted to rent or lease the

non-owner-occupied unit(s), (b) as an investment property, or (c) as a recreational

or second home. Not more than fifteen percent (15%) of the total living area of a

residence may be used in a trade or business which would permit any portion of the

costs of the Eligible Dwelling to be deducted as an expense for Federal Income Tax

purposes (except in the case of a two to four family residence, in which case the

Eligible Borrower shall be permitted to deduct for Federal Income Tax purposes the

costs associated with the non-owner-occupied units).

3. Land Not to be Used to Produce Income

The land financed by the Mortgage Loan may not provide, other than incidentally, a

source of income to the Eligible Borrower. The Eligible Borrower must indicate on

the Borrower Certificate that, among other things:

a. No portion of the land financed by the Mortgage Loan provides a source of

income (other than incidental income);

b. The borrower does not intend to farm any portion of the land financed by the

Mortgage Loan; and

c. The borrower does not intend to subdivide the property nor to apply for a

zoning variance regarding minimum lot size or set-back requirements.

4. Post-Closing Inspection of Eligibility

Within 60 days after the closing of the Mortgage Loan, the Participating Lender is

required to inspect the Eligible Dwelling for compliance with the principal

residence requirements of:

a. No trade or business;

b. Owner-Occupancy use as permanent principal residence; and

c. No prohibited use of the land

Based upon such investigation, the Participating Lender shall either:

Rev. 11-2017 Page 8

i. Certify to CHFA that based upon its subsequent investigation, it has no

reasonable grounds for believing that the borrower did not meet the

requirements of (Section 3.1D). Such certification shall be made on the

Participating Lender Certification; or

ii. Promptly notify CHFA in the event it determines that these requirements

have not been complied with and take such action with respect to the

Mortgage Loan as CHFA shall thereafter request, which may include

requiring the Participating Lender to repurchase the Mortgage Loan

pursuant to (Section 7.2C) of this manual.

E. Mortgage Requirement

Mortgage Loans may be made only to persons who did not have a mortgage

(whether or not paid off) on the Eligible Dwelling at any time prior to the execution

of the Mortgage. A Mortgage Loan may not be made to finance the purchase of a

remaining interest in a home in which a partial interest is already owned or will be

acquired through inheritance or gift. Mortgage Loan proceeds may not be used to

acquire or replace an existing mortgage or debt for which the Eligible Borrower is

liable or which was incurred on behalf of the Eligible Borrower, or provide

financing for a property which is debt free, except for:

A construction loan; or

Temporary financing which has a term of twenty-four months or less; or

A mortgage on unimproved land on which a dwelling is to be constructed,

as long as the mortgage is satisfied prior to the date of the Loan closing and

the amount of the Loan does not exceed the cost of construction; or

A Rehabilitation Mortgage 203(k) Limited Program (Section 4).

1. Definition of Mortgage

For purposes of applying the mortgage requirements, a mortgage includes a deed of

trust, a conditional sales contract, a pledge, an agreement to hold title in escrow, a

lease with an option to purchase which is treated as an installment sale for Federal

income tax purposes and any other form of owner financing. A conditional land

sale contract shall be considered as an existing loan or mortgage for purposes of this

requirement.

2. Temporary Financing

In the case of a Mortgage Loan made to refinance a loan for the construction of an

Eligible Dwelling, the Participating Lender must certify to CHFA that such

construction has been satisfactorily completed prior to submission of such

Mortgage Loan for purchase by CHFA. Such certification shall be made on the

Participating Lender Certification.

Rev. 11-2017 Page 9

3. Review by Participating Lender

a. Prior to closing the Mortgage Loan, the Participating Lender must examine the

Borrower Certificate and related submissions, including (i) the Eligible

Borrower’s Federal Income Tax Returns and (ii) current credit report, in order

to determine whether the Eligible Borrower has met the mortgage requirements

or whether such examination discloses any existing mortgage or debt which the

proceeds of the CHFA Loan may be used to repay or refinance. Upon such

review, the Participating Lender shall certify to CHFA that the Lender has no

reasonable grounds for believing that the Mortgage Loan proceeds will be used

to repay or refinance an existing mortgage debt. Such certification shall be made

on the Participating Lender Certification.

b. Subsequent to the closing of the Mortgage Loan, should the Participating

Lender find that the Eligible Borrower is repaying or refinancing an existing

mortgage or debt with the proceeds of the Mortgage Loan, other than temporary

initial financing having a term of twenty-four months or less, the Participating

Lender shall promptly notify CHFA and take such action with respect to the

Mortgage Loan as CHFA shall thereafter request. CHFA may require the

Participating Lender to repurchase the Mortgage Loan pursuant to (Section

7.2.C) of this Manual.

F. Determination by Participating Lender

The qualification of an Eligible Borrower shall be determined by the Participating

Lender subject to review by CHFA. For each application, the Participating Lender

must review the application form and related submissions to determine their

consistency, completeness, and compliance with the terms of this Manual. Lender

is required to verify the information provided to them, either independently or

concurrently with credit reviews, when applicable.

G. Multiple Loans

An Eligible Borrower may not have more than one outstanding CHFA Mortgage

Loan including a CHFA Loan that has been assumed by another person.

3.2 Eligible Dwellings

A. General

In order to qualify as an Eligible Dwelling for which a Loan may be made, the

premises must:

1. Be located in the State of Connecticut;

Rev. 11-2017 Page 10

2. Be structurally sound and functionally adequate and meets all applicable

zoning requirements, housing codes and similar requirements;

3. Have a permanent certificate of occupancy if newly-constructed or

substantially rehabilitated or when a certificate of occupancy is not obtainable

in the case of substantial rehabilitation, have such other documentation as

CHFA may require;

4. Meet all appropriate requirements listed in (Section 3.2.B).

B. Types of Dwellings

An Eligible Dwelling may be a one to four family residence (including all fixtures

and land on which it is situated) or a unit of an approved/eligible condominium or

planned unit development. In the case of a two to four family residence, at least

one of the units must be Owner-Occupied and the building must have been used

as a residence for at least five years preceding the application for the Loan. A

newly-constructed two family home located in a Targeted Area may also be

eligible.

C. Principal Residence Requirement; Owner-Occupancy

1. In order to be considered an Eligible Dwelling, the residence must become the

permanent principal residence of the Eligible Borrower within 60 days after

the closing date of the Mortgage Loan. The requirement of this section will

not be satisfied where the residence (which shall include any land financed by

a Loan) can reasonably be expected to be used in a trade or business (except

for certain two-to-four family residences), as investment property, or as a

recreational second home.

2. The Participating Lender shall be responsible for determining whether the

dwelling is in a condition which will satisfy the principal residence

requirement, subject to review by CHFA. In making this determination the

Participating Lender may not rely solely upon statements made by the Loan

applicant in the Borrower Certificate, but must verify compliance with this

requirement by conducting an on-site inspection of the dwelling (the

appraisal) and through other reasonable efforts. On the basis of such

independent investigation, taking into account the location, structural and

other characteristics of the dwelling, the Participating Lender shall certify to

CHFA, that based upon reasonable belief and independent investigation, the

dwelling is expected to be suitable for occupancy as a principal residence by

the Loan applicant within 60 days after the closing of the Mortgage Loan and

is not expected to be used in a trade or business, as an investment property or

as a recreational or second home.

Rev. 11-2017 Page 11

D. Principal Residence Requirements Pertaining to Land

1. Lot Size

The land on which the eligible dwelling is situated cannot exceed basic

livability, other than incidentally, cannot be subdivided, and cannot be a source

of income to the borrower.

2. Non-production of Income

a. Only land which does not provide a source of income to the Eligible

Borrower (other than incidental income) may be financed by a Mortgage

loan.

b. The Participating Lender is required to conduct an on-site inspection of the

property (the appraisal) and to certify to CHFA that on the grounds of that

inspection and other reasonable grounds, the Lender expects that the property

will not be used to produce income to the Eligible Borrower, other than

incidental income.

3. Leasehold Interests

The following requirements shall apply where a Loan is secured by a mortgage

on a leasehold interest:

a. The notice of lease must be recorded on the land records of the town in

which the property is located;

b. The term of the lease must be equal to the number of years remaining until

the maturity date of the loan and in no instances may the lease expire before

the maturity date of the loan is reached.

Example: If the amortization term of the mortgage loan is for 30 years (360 months)

beginning on July 30, 2010 ending on July 30, 2040, the term of the lease must be for at

least 30 years (360 months) concurrent with the mortgage loan and may not expire prior

to July 30, 2040.

c. The lease shall be in full force and effect and subject to no change or penalty

or prior lien or encumbrance by which it can be terminated; and

d. The lease must be on a form acceptable to CHFA; it shall provide that the

lessee may mortgage the leasehold estate, and it must not contain conditions

under which the leasehold may be terminated for lessee’s default without the

mortgagee having the right to receive from the lessor written notice of, and

reasonable opportunity to cure, such default.

Rev. 11-2017 Page 12

E. Sales Price Requirements

1. The Acquisition Cost of an Eligible Dwelling may not exceed the sales price

limits established by CHFA and in effect at the time of the application.

Appraised value as well as actual selling price will be reviewed by CHFA on

all Loan submissions. Any indirect or non-pecuniary consideration will be

given effect in determining the market value. CHFA may at its option reject

an application for a Mortgage Loan where the appraised value exceeds the

applicable CHFA Sales Price Limit by more than five (5) percent.

2. Arm’s-Length Transaction

In those cases that are not arm’s length transactions the appraised value may

not exceed the applicable sales price limit.

3. Definition of Acquisition Cost

Acquisition Cost means the cost of acquiring the Eligible Dwelling from the

Seller as a completed residence. In determining Acquisition Cost:

a. Acquisition Cost includes:

i. All amounts paid, either in cash or in kind, by the Eligible

Borrower (or a related party for the benefit of the Eligible

Borrower) to the Seller (or a related party or for the benefit of the

Seller) as consideration for the Eligible Dwelling. Such amounts

include amounts paid for items constituting fixtures under State

law, but not for items of personal property not constituting fixtures

under State law.

ii. The reasonable costs of completing the residence, whether or not

the cost of completing construction is to be financed with the

Mortgage Loan, if the Eligible Dwelling is incomplete. As an

example of reasonable completion cost, costs of completing the

Eligible Dwelling so as to permit occupancy under local law would

be included in the Acquisitions Costs.

iii. The capitalized value of the ground rent calculated using a

discount rate equal to the yield on the CHFA bonds from which the

Mortgage Loan was made, where the Eligible Dwelling is subject

to a ground rent. CHFA will supply bond yield information to

Participating Lenders on request for the purpose of calculating

capitalized ground rent.

Rev. 11-2017 Page 13

iv. The cost of land which has been owned by the Eligible Borrower

prior to the construction of the structure comprising the Eligible

Dwelling.

b. Acquisition Cost does not include:

i. Usual and reasonable settlement or financing costs. Such settlement

costs include title and transfer costs, title insurance, survey fees

and other similar costs. Such excluded financing costs include:

credit reference fees

legal fees

appraisal expenses

points which are paid by the Eligible Borrower (not by the

seller), or other costs of financing the residence.

Such amounts must not exceed the usual and reasonable costs

which otherwise would be paid. Where the buyer pays more than a

pro rata share of property taxes, for example, the excess is to be

treated as part of Acquisition Cost.

ii. The imputed value of services performed by the Eligible Borrower

or members of his family (brothers and sisters, spouse, ancestors

and lineal descendants) in constructing or completing the

residence.

c. The following examples illustrate determination of Acquisition Costs:

Example (1)

A contracts with B, a builder of single family residences, for the purchase of a

residence. Under the terms of the contract, B will deliver a residential unit to A

that contains an uncompleted recreation room and an unfinished third floor and

lacks a garage.

Normally, a completed recreation room, a finished third floor and a garage are

provided as part of the residence by B.

The contract price for the residence is $158,000. At the same time, A contracts

with C, an affiliate of B, to complete the recreation room, the third floor and to

construct the garage for a contract price of $25,000.

C will perform this work after A receives title to the unit from B. The

Acquisition Cost of A’s completed residential unit is $183,000 which represents

the contract price plus the cost of completion of the recreation room, third floor

and construction of the garage.

Rev. 11-2017 Page 14

Acquisition Cost Example (1)

$ 158,000.00 – contract price (excludes completion of 3rd

fl, recreation room or garage)

$ 25,000.00 – cost of completion of 3rd

fl, recreation room and garage

$183,000.00 – Acquisition Cost

Example (2)

E owns a single family residence which has been listed for sale. D contracts to

purchase E’s residence, and the contract provides for a selling price of

$100,000. D also agrees to pay an unsecured debt in the amount of $15,000,

which E owes to X, a local bank. D further agrees to purchase from E the

refrigerator, stove, and dryer located in E’s residence for $2,500, an amount

equal to the fair market value of such items. D also agrees to purchase the light

fixtures, curtain rods, and wall-to-wall carpeting for a fair market value price of

$1,000. The acquisition cost of D’s completed residential unit is $116,000.

Such amount includes the $15,000 unsecured debt paid off by D.

The $2,500 paid for the refrigerator, stove, washer, and dryer are not included

because such items are not included within the definition of an Eligible

Dwelling under the Program. Such definition does include the light fixtures,

curtain rods, and wall-to-wall carpeting purchased by D.

Acquisition Cost Example (2)

$100,000.00 – contract sales price for the property

$ 15,000.00 – borrower unsecured debt to the bank paid by seller

$ 1,000.00 – light fixtures, curtain rods, and wall-to-wall carpeting –allowable costs

$116,000.00 – Acquisition Cost

(Note: refrigerator, stove, washer and dryer are not allowable cost for this transaction)

Example (3)

F contracts with G to purchase G’s home for $100,000. After purchasing the

residence, F pays $3,000 to a party unrelated to G for painting, minor repairs,

and refinishing the floors. The Acquisition Cost of the residence is $100,000.

Such fix-up expenses are not treated as part of the Acquisition Cost. If G had

incurred such fix-up expenses by the amounts expended by F however, F may

not reduce his Acquisition Cost of the residence by such amounts.

Acquisition Cost Example (3)

$100,000.00 – contract sales price for the property

$ 00.00 – additional allowable cost for fix-up

$100,000.00 – Acquisition Cost

(Note: $3,000 costs to borrower to fix up property are not eligible cost for this transaction)

Rev. 11-2017 Page 15

4. Appraisals

A complete property appraisal report is required to be submitted by the

Participating Lender with each Loan submission except in the case of a loan

eligible for the Compliance Limited Documentation Program which requires

submission of only the first four (4) pages. Appraisals are required for all

Loan submissions for purchases of units in eligible condominium projects for

verification of current investor ratio concentration. All appraisals for

Mortgage Loans must be made by appraisers who are licensed or certified by

the State of Connecticut, acceptable to CHFA and as per FNMA Guidelines.

Participating Lenders must adhere to the Appraiser Independence

Requirements as outlined in the FNMA Selling Guide.

a. Forms - The report must be prepared on a current FNMA/FHLMC

appraisal form or on the appropriate FHA form which meets the

minimum HUD requirements, including any additional attachments or

addenda necessary to provide an adequately supported opinion of

market value.

b. Appraised Value - Appraisals should report the highest price which the

property will bring contemplating;

(i) The consummation of a sale and the transfer of title from a

seller to buyer who are participating in a bona-fide, arm’s-

length transaction and are motivated by no more than the

goals of typical participants;

(ii) Both parties are well informed or well advised and act

prudently, each for what he considers his own best interest;

(iii) Reasonable exposure is given to the property in the open

market;

(vi) Payment is made in cash or on terms reasonably equivalent

to cash, assuming typical financing terms are available in

the community for similar property.

c. Repairs - CHFA requires all mortgaged properties to be in good repair.

Appraisal reports shall indicate whether a building code inspection is

necessary. If the appraisal report indicates that repairs are needed, a

recertification by the appraiser must be obtained prior to the closing of

the Loan. The certification must provide the Eligible Borrower’s name

and the property address and must state that the property has been

inspected and the indicated repairs have been completed except in the

case in which an escrow has been established for such repairs. (See

203(k) Standard or 203(k) Limited Programs – Section 4).

Rev. 11-2017 Page 16

d. Exterior Photographs – Clear, descriptive photographs showing the

front, back, and a street scene of the subject property and the front of

each comparable. The subject and all comparables must be

appropriately identified.

e. Interior Photographs – At a minimum, the appraisal report must include

photographs of the following:

The kitchen

All bathrooms

Main living area

Examples of physical deterioration, if present; and

Examples of recent updates, such as restoration, remodeling, and

renovation, if present.

(FNMA Selling Guide B4-1.2-01)

f. The validity period for all appraisals on existing and proposed and

under construction properties will be 4 months. Appraisals may not be

more than 4 months old from the loan closing date to the date the loan

is sold to FNMA (See FNMA announcement 09-19)

g. UCDP – Must obtain and provide a “successful” SSR report for loans

delivered to FNMA (uninsured- HFA Preferred Programs). (FNMA

Selling Guide B4-1.1-06)

5. Review by Participating Lender

The Participating Lender shall determine that the Acquisition Cost of the

Eligible Dwelling does not exceed the applicable Sales Price Limit in

accordance with (Section 3.2.E). The participating Lender shall certify to CHFA

that the Sales Price requirement is met. Such certification shall be made on the

Participating Lender Certification.

6. Independent Appraisal

CHFA reserves the right to obtain an independent appraisal in order to establish

fair market value and to determine whether a dwelling is eligible for the

Mortgage Loan requested.

7. Surveys

A survey is not required if not required by FHA, VA, USDA-RD, FNMA or

PMI, and is not indicated by a prudent practice and custom in the geographical

area in which the property is located. However, CHFA reserves the right to

require a survey.

Rev. 11-2017 Page 17

F. Condominium and Planned Unit Developments

An individual condominium unit or unit of an approved planned unit development is

included within the definition of an Eligible Dwelling provided the requirements set forth

in this section and elsewhere in this Manual are met.

1. Condominiums

a. CHFA loans are available to finance the acquisition of any unit in the

following classes of condominium units:

i. Any unit not part of a conversion condominium, or

ii. Any unit in a conversion condominium, except that for a period of one

year subsequent to the filing of the declaration of the condominium,

CHFA may provide mortgage loan financing only to an applicant who

is a tenant that has rented a unit at the property.

b. Prior Approval of Condominium - Mortgage Loan submissions for

individual units in condominium projects are required to be approved by

FHA and placed on their approved condominium list. Loans under the HFA

Preferred Program must meet FNMA condominium eligibility requirements.

i. CHFA Mortgage Loan applications submitted for Commitment

must include a copy of the FHA connection condominium approval.

ii. The Lender must certify the condominium unit meets all Fannie

Mae (FNMA) condominium eligibility criteria and is eligible for

CHFA first mortgage loan financing.

iii. Lender must provide Fannie Mae (FNMA) Condominium Eligibility

Certification (CHFA form 013-490) or FNMA Condominium Project

Manager and include the document in the loan package submitted to

CHFA for review.

c. Deed Restricted Condominium Projects– Affordable Housing Condominium

Projects that are deed restricted for purchase to First-time

homebuyers or that have low - to - moderate income eligibility or low-

to-moderate income resale restrictions and are not eligible for FHA

or FNMA approval may be submitted to CHFA for review. A Request for

approval by CHFA shall be in writing and shall include the following:

i. The current public offering statement of the declarant;

Rev. 11-2017 Page 18

ii. The declaration of condominium, including the by-laws of the unit

owners’ association, survey, floor plans and all exhibits and schedules;

iii. Statistics on the number of units conveyed and the number of

unconveyed units that are vacant;

iv. The current fiscal year operating budget;

v. Documentation of the Association reserves process, status of reserves

accounts which must show a minimum of two months cushion for

monthly operating expenses;

vi. CHFA mortgage loan financing for individual units in Affordable Deed

Restricted Projects that are ineligible for FHA, VA, USDA-RD or PMI

insurance coverage may also require a minimum 20% down-payment

investment from an acceptable source which can include CHFA

approved non-profit, municipal, or Federal programs, or a combination

that includes an investment of the borrower’s own funds;

vii. Certificate of Insurance (current) including declaration page;

viii. Condo Eligibility Certification (CHFA Form #013-490);

ix. Photo of one condo unit;

x. Owner occupancy ratio;

xi. Total number of units in complex.

d. Maximum Units Financed

CHFA will not issue Commitments which would cause CHFA to hold Mortgage

Loans on more than fifty percent (50%) of the units in any one project; whether

existing or new construction, fifty percent (50%) of the units in the project must

be sold or under bona fide contracts of sale prior to CHFA’s purchase of any

condominium Loan.

e. Underwriting Considerations

Underwriting must include the unit owners’ association charges (excluding

heat) as fixed monthly costs when making underwriting calculations under

(Section 5.1.D).

Rev. 11-2017 Page 19

f. Necessary Papers and Documents

i. The CHFA Uniform Mortgage Rider together with a condominium rider,

on the appropriate form for a VA, FHA or PMI insured or guaranteed

Loan must be executed and recorded with the mortgage deed.

ii. The following documents, as applicable, must be submitted at each

closing:

a) Duly executed corporate consent authorizing sale of the unit, if the

grantor is a corporation; and

b) Certificate of payment of assessments for the individual

condominium unit.

2. Planned Unit Developments

CHFA considers a PUD or planned community, other than one consisting of

detached single family houses, on the same basis as a condominium.

G. Energy Efficiency Requirements for Newly-Constructed Houses

The sales contract (or specifications) for houses on which construction commences

after November 1, 1982 must provide for insulation of at least R30 in the ceiling and

R11 in the walls (R38 in the ceiling and R19 in the walls and floors in the case of

electric heat) and for double-glazed windows with wood or other thermal break (or

storm windows in lieu thereof). If necessary, an amendment to the sales contract to

provide these will be required.

H. Determination by Participating Lender

The eligibility of a dwelling for CHFA financing shall be determined by the

Participating Lender subject to review by CHFA. For each application, the

Participating Lender must review the application form and related submissions to

determine their consistency, completeness and compliance with the requirements of

this Manual. Lender is required to verify the information provided to them, either

independently or concurrently with the application.

Rev. 4-2016 Page 1

SECTION 4 – REHABILITATION MORTGAGES 203(k) Standard & 203(k) Limited

4.1 Program Descriptions

4.2 Borrower Eligibility

4.3 Property Eligibility

4.4 Principal Residence Requirement

4.5 Rehabilitation Loan Amounts and Eligible Repairs

4.6 Builders and Contractors

4.7 Contracts and Rehabilitation Work Specifications

4.8 Completion of Work and Construction Period

4.9 Post-Closing Inspection

4.10 Rehabilitation Escrow Account

4.11 Additional Documentation

4.12 Origination Fee and Closing Costs

Rev. 4-2016 Page 2

Section 4 - Rehabilitation Mortgages

203(k) Standard & 203(k) Limited Programs

4.1 Program Descriptions

Overview

The FHA 203(k) Standard and 203(k) Limited Rehabilitation Mortgage Loan Programs

offer first mortgage financing for prospective homebuyers interested in purchasing a

home that needs repairs. These programs may be used to purchase and rehabilitate

existing 1-4 unit dwellings (manufactured homes are not eligible) and include, as part of

the acquisition cost, the cost of rehabilitating the property as a completed residential unit.

Homebuyers interested in purchasing and repairing a home under this program generally

may not have owned a home in the last three years to qualify; but previous homeowners

may qualify if they intend to purchase and occupy a home located in a federally targeted

area.

The FHA 203(k) Standard and 203(k) Limited Rehabilitation Mortgage Loan Programs

are available to FHA lenders that are approved by CHFA to originate under this program.

A HUD approved Consultants report is required with all 203(k) Standard Rehabilitation

Mortgage Loan Program submissions.

4.2 Borrower Eligibility

Borrower(s) eligibility, including Income and Sales Price Limits, are the same as for

CHFA Homebuyer Mortgage Program Loans, and are covered in Section 3 of this

Manual.

There are no income limits for FHA 203(k) Standard and 203(k) Limited Rehabilitation

Mortgage Loan Programs if purchasing in a federally targeted area, unless the applicant

also borrows under the Downpayment Assistance Program.

FHA 203(k) Standard and 203(k) Limited Rehabilitation Mortgage Loan Programs utilize

the Sales Price Limits as the limit for the total acquisition cost (purchase price plus total

rehabilitation costs) and as a final value guide for program eligibility.

All other guidelines for FHA 203(k) Standard and 203(k) Limited Rehabilitation

Mortgage Loan Programs are the same as for CHFA Homebuyer Mortgage Program

Loans, except for specific items covered in this Section.

Rev. 4-2016 Page 3

4.3 Property Eligibility

The FHA 203(k) Standard and 203(k) Limited require Borrower(s) to purchase homes

that meet specific property and sales price guidelines. The property must meet one of the

definitions listed below:

a. Existing 1-4 Family Residential Property

b. FHA approved condominium and PUD- (FHA restrictions apply)

c. Existing dwelling conversions up to four units

d. No Manufactured Housing, Mobile Homes or Co-Ops

In order to qualify for these programs, the Borrower(s) must use the loan to purchase and

repair a home which they will occupy as their principal residence within six (6) months

of loan closing including rehabilitation period.

The Borrower(s) may not use the loan to purchase recreational, vacation, investment,

commercial or rental properties (unless the Borrower(s) is an owner-occupant of an

eligible multi-family residence up to a maximum of 4 units).

A loan under this program will cover the cost of converting commercial property to

residential property. No part of the purchased property may be designated for

commercial purposes. Owner-occupant Borrower(s) only; no investors.

4.4 Principal Residence Requirement

In order to qualify for these programs, the Eligible Borrower(s) must use the loan to

purchase and repair a home in which they will occupy as their principal residence.

Eligible Borrower(s) shall covenant to occupy the Eligible Dwelling as their principal

residence within sixty (60) days of Loan closing.

Unless the residence can reasonably be expected to become the principal residence of the

Eligible Borrower(s) within six (6) months, the residence will not be considered an

Eligible Dwelling and therefore may not be financed with a FHA 203(k) Standard or

203(k) Limited Rehabilitation Mortgage Loan.

Rev. 4-2016 Page 4

4.5 Rehabilitation Loan Amounts and Eligible Repairs

1. The FHA 203(k) Standard Rehabilitation Mortgage Loan Program, as listed in the

U.S. Department of Housing and Urban Development (HUD) website, will allow

Borrower(s) to purchase a house in need of full structural alterations or repairs and

modernization that includes both the cost of acquisition and rehabilitation. The

maximum mortgage amount cannot exceed the applicable loan-to-value ratio and

maximum dollar amount limitation prescribed for the FHA Maximum Mortgage

Limits as applicable for where the home is located.

The types of improvements that Borrower(s) may make using the FHA 203(k)

Standard Rehabilitation Mortgage Loan Program include these examples:

a. Structural alterations and repair of damage to the home including chimneys,

walls, roofs, and ceilings, termite and water damage.

b. Installation of energy-efficient features to plumbing, heating and electrical

devices.

c. Installation or replacement of wells, septic tanks, windows and hot water

systems.

d. Repair of flooring, roofing, handrails, downspouts and exterior siding that

improves the general livability of the home.

e. Alterations to enable handicap accessibility.

2. The FHA 203(k) Limited Rehabilitation Mortgage Loan Program, as listed in the

U.S. Department of Housing and Urban Development (HUD) website, is a limited

repair program that will allow Borrower(s) to obtain a mortgage loan that includes the

cost of acquisition and up to an additional $35,000 that can be used to complete

moderate rehabilitation or modernization repairs to the property prior to moving in.

The maximum mortgage amount cannot exceed the applicable loan-to-value ratio and

maximum dollar amount limitation prescribed for the FHA Maximum Mortgage

Limits as applicable for where the home is located.

The types of improvements that Borrower(s) may make using the FHA 203(k)

Limited Rehabilitation Mortgage Loan Program include these examples:

a. Basements, Decks, Patios, Floors

b. Electrical, HVAC Systems, Weatherization

c. Minor Remodel

d. New Appliances (up to $2,000)

e. Replacement Windows, Painting, Plumbing, Roofs

f. Septic & Well Repairs, Sewer Hook-up

Rev. 4-2016 Page 5

Properties that require the following work items are not eligible for financing under

the FHA 203(k) Limited Rehabilitation Mortgage Loan Program:

a. Major rehabilitation or major remodeling, such as the relocation of a load-

bearing wall;

b. New construction (including room additions);

c. Repair of structural damage;

d. Repairs requiring detailed drawing or architectural exhibits;

e. Landscaping or similar site amenity improvements;

f. Any repair or improvement requiring a work schedule longer than six (6)

months; or

g. Rehabilitation activities that require more than two (2) payments per

specialized contractor.

Borrower(s) may not use the FHA 203(k) Limited Rehabilitation Mortgage Loan

Program to finance any required repairs arising from the appraisal that do not appear

on FHA 203(k) Limited Rehabilitation eligible work items list or that would:

a. Necessitate a “consultant” to develop a “Specification of Repairs Write-Up”;

b. Require plans or architectural exhibits;

c. Require a plan reviewer;

d. Require more than six (6) months to complete;

e. Result in work not starting within 30 days after loan closing; or

f. Cause the Borrower(s) to be displaced from the property for more than fifteen

(15) days during the time the rehabilitation work is being conducted. (FHA

anticipates that, in a typical case, the Borrower(s) would be able to occupy the

property after mortgage loan closing).

4.6 Builders and Contractors

The Borrower(s) are required to have a construction contract with the Builder or General

Contractor. The Builder or General Contractor must be registered and / or licensed with