Embed Size (px)

Citation preview

a

v Protecting your business with holistic retirement advice

a

Let’s talk about the Corporate Investment Shelter strategy

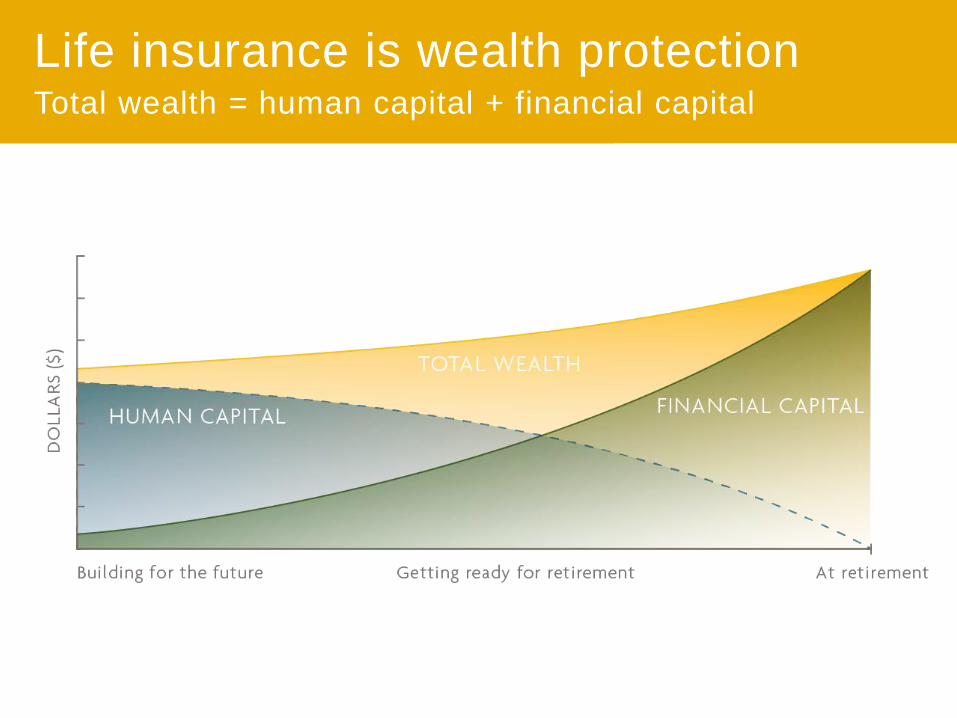

Life insurance is wealth protection Total wealth = human capital + financial capital

Make the Connection with a best practice approach

Make it easy for advisors like you to start conversations with your clients about wealth protection solutions.

ONE SIMPLE OBJECTIVE:

Disclaimer

• The following information is being presented with the understanding that it is intended for information purposes only.

• Neither Sun Life Assurance Company of Canada nor the presenter has been engaged for the purpose of providing legal, accounting, taxation, or other professional advice.

• No one should act upon the examples/information without a thorough examination of the legal/tax situation with their own professional advisors, after the facts of the specific case are considered.

Corporate investment shelter (CIS) overview What it is and how it works

Case Study

Illustrating the CIS strategy

Sales and marketing support available

What you’ll learn today

Compares the benefits of a corporately owned participating whole life insurance solution to a traditional non-registered investment

• Maximize corporate asset value by minimizing the erosion of investment assets through taxes and other costs

• Use of capital dividend account (CDA) and refundable dividend tax on hand credits (RDTOH)

Corporate investment shelter 101

The corporate tax challenge Challenges with traditional investments

Challenges while living •Taxes payable on investment income

– Interest – Dividends – Realized capital gains

Passive investment income •Attracts tax at top corporate rate •No small business deduction

Erosion through income taxes =

Reduced growth of corporate assets

The corporate tax challenge Challenges with traditional investments

• Challenges at death – Taxes payable on deferred capital gains – Taxes payable on transfers to shareholder’s

estate

Erosion through taxes at death =

Less assets available for estate

The corporate investment shelter Addressing the tax challenges

• Addressing tax challenges while living – CIS uses a participating whole life insurance

policy • Policy earnings grow tax exempt

• Addressing tax challenges at death

– Policy proceeds can be paid tax free to the corporation (no deferred gains)

– Amount of death benefit in excess of the policy’s adjusted cost basis can be paid as a tax-free capital dividend to the shareholder’s estate

• Owner / significant shareholder of a Canadian controlled private corporation (CCPC)

• Age 50+ and healthy • A corporate life insurance need exists • Corporation has:

– excess cash flow and/or, – investment assets not needed for business purposes

• Wants to maximize estate and transfer assets in a tax-efficient manner

• Looking for stable and consistent asset growth

Target client profile

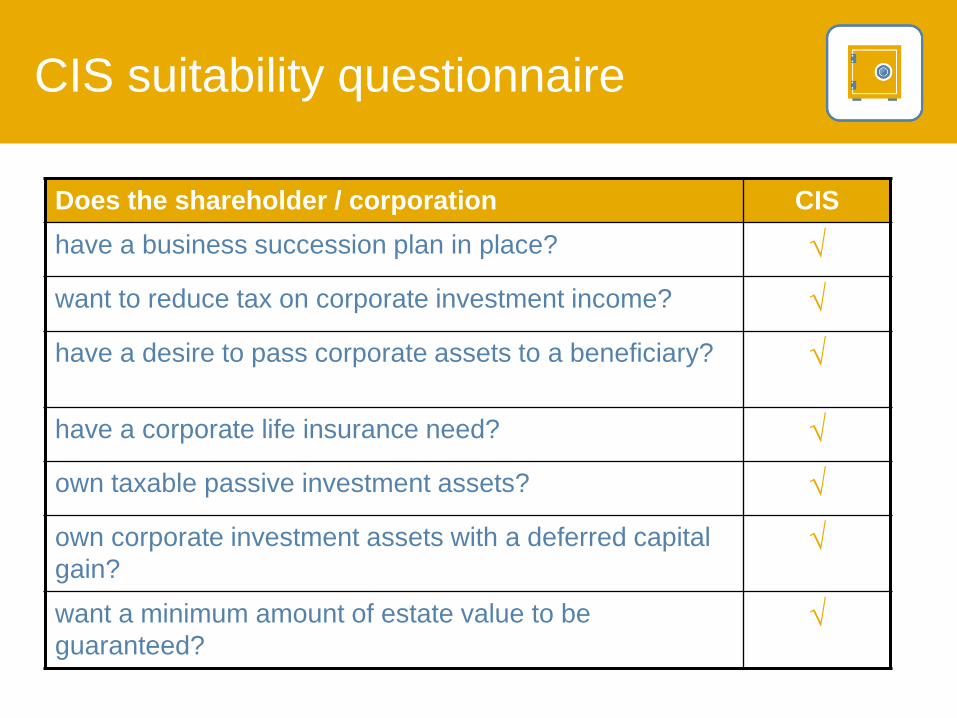

CIS suitability questionnaire

Does the shareholder / corporation CIS have a business succession plan in place? √ want to reduce tax on corporate investment income? √ have a desire to pass corporate assets to a beneficiary? √

have a corporate life insurance need? √ own taxable passive investment assets? √ own corporate investment assets with a deferred capital gain?

√

want a minimum amount of estate value to be guaranteed?

√

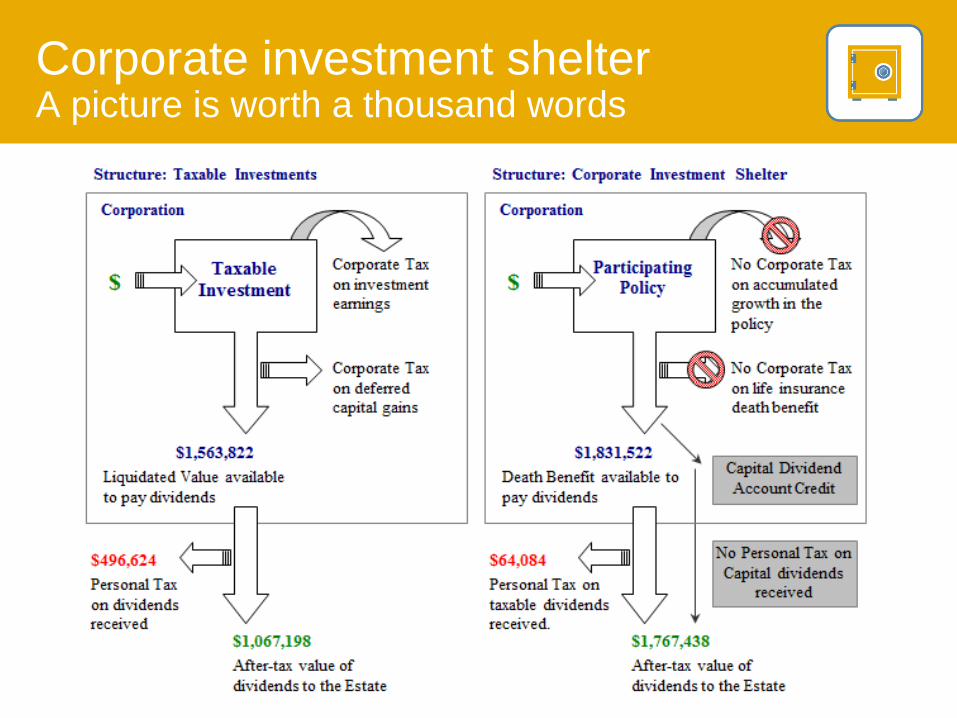

Corporate investment shelter A picture is worth a thousand words

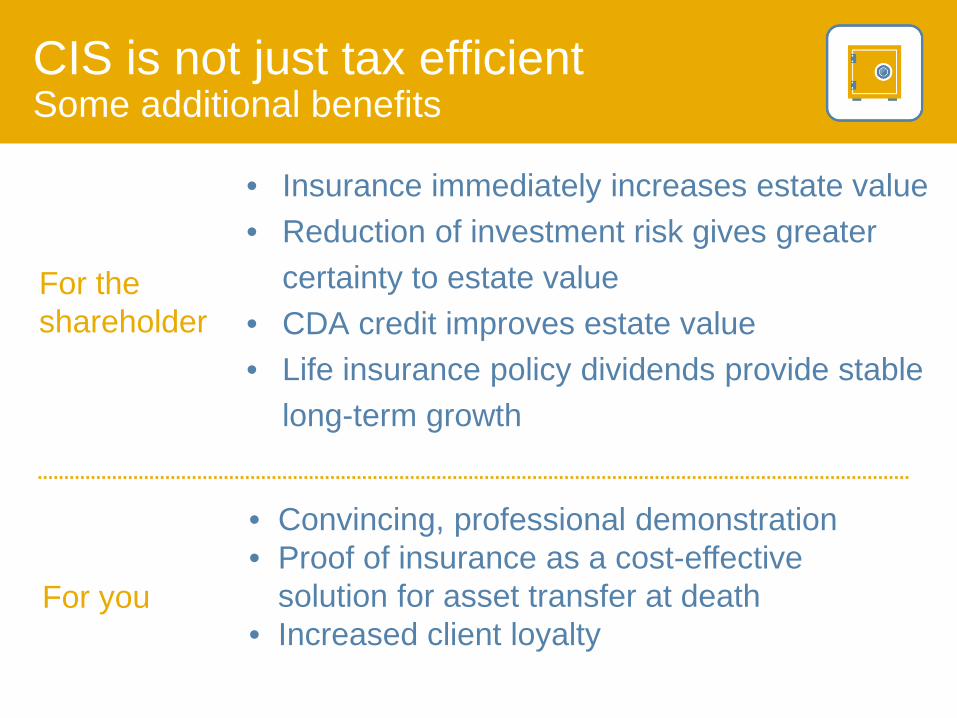

CIS is not just tax efficient Some additional benefits

• Insurance immediately increases estate value • Reduction of investment risk gives greater certainty to estate value • CDA credit improves estate value • Life insurance policy dividends provide stable long-term growth

For the shareholder

For you

• Convincing, professional demonstration • Proof of insurance as a cost-effective

solution for asset transfer at death • Increased client loyalty

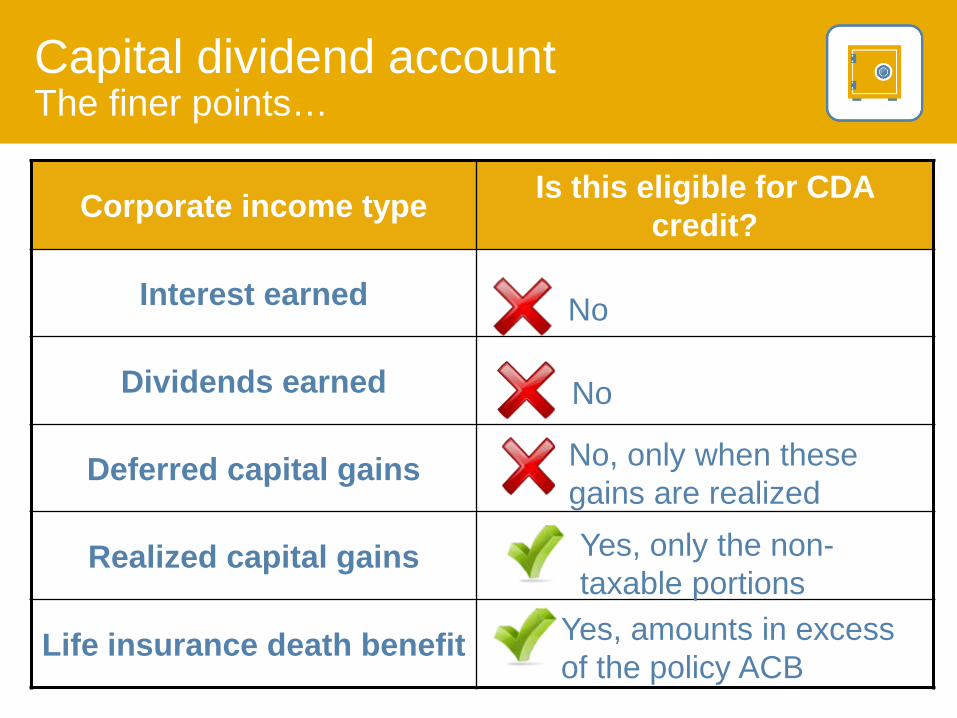

Capital dividend account The finer points…

Corporate income type Is this eligible for CDA credit?

Interest earned

Dividends earned

Deferred capital gains

Realized capital gains

Life insurance death benefit

No

Yes, amounts in excess of the policy ACB

Yes, only the non-taxable portions

No, only when these gains are realized

No

• Access to the steady and consistent performance of the Sun Life Par Account through the crediting of policyholder dividends – managed with a long-term perspective – Investment experience is a key factor influencing

dividends • Potential to reduce investment volatility • No need to make ongoing investment decisions • Opportunity for asset diversification

The benefits of a CIS with par whole life insurance from Sun Life Financial

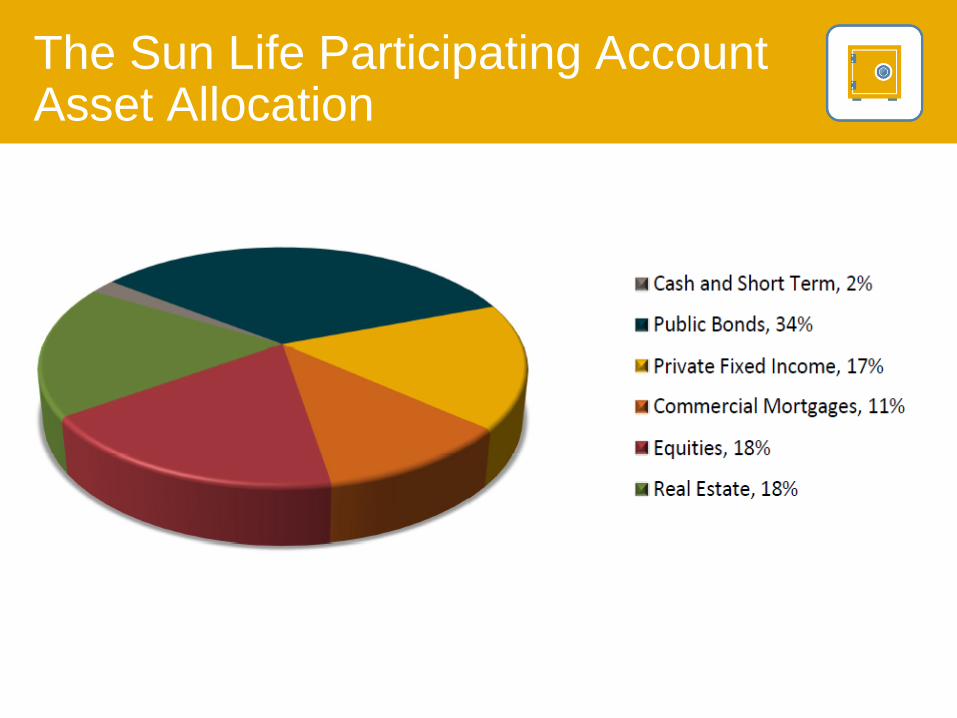

The Sun Life Participating Account Asset Allocation

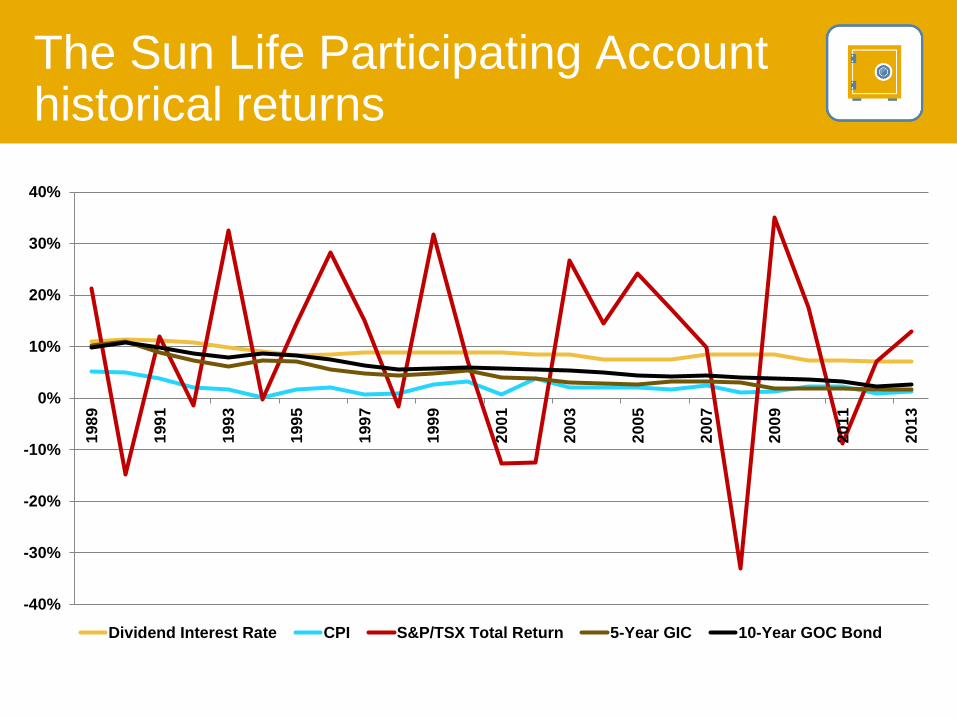

The Sun Life Participating Account historical returns

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

Dividend Interest Rate CPI S&P/TSX Total Return 5-Year GIC 10-Year GOC Bond

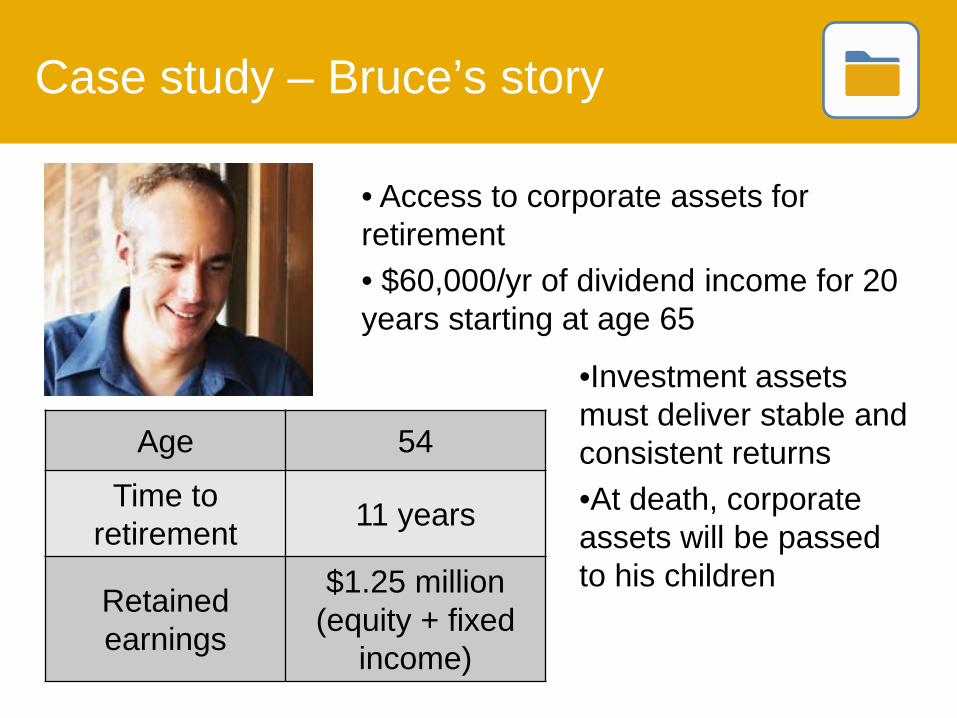

Case study – Bruce’s story

Age 54

Time to retirement 11 years

Retained earnings

$1.25 million (equity + fixed

income)

•Investment assets must deliver stable and consistent returns •At death, corporate assets will be passed to his children

• Access to corporate assets for retirement • $60,000/yr of dividend income for 20 years starting at age 65

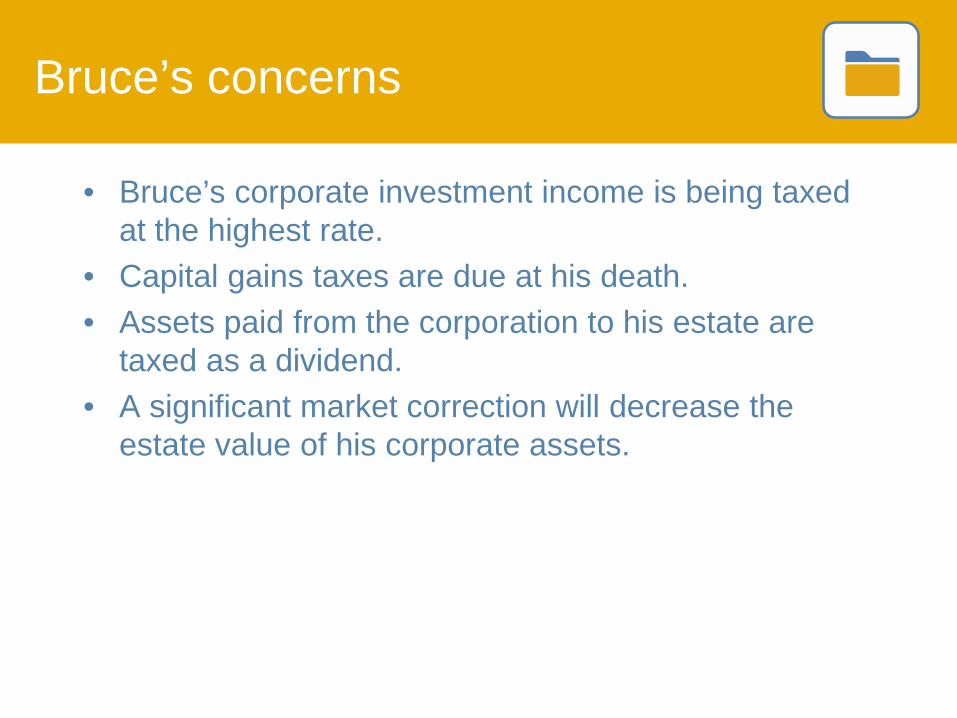

• Bruce’s corporate investment income is being taxed at the highest rate.

• Capital gains taxes are due at his death. • Assets paid from the corporation to his estate are

taxed as a dividend. • A significant market correction will decrease the

estate value of his corporate assets.

Bruce’s concerns

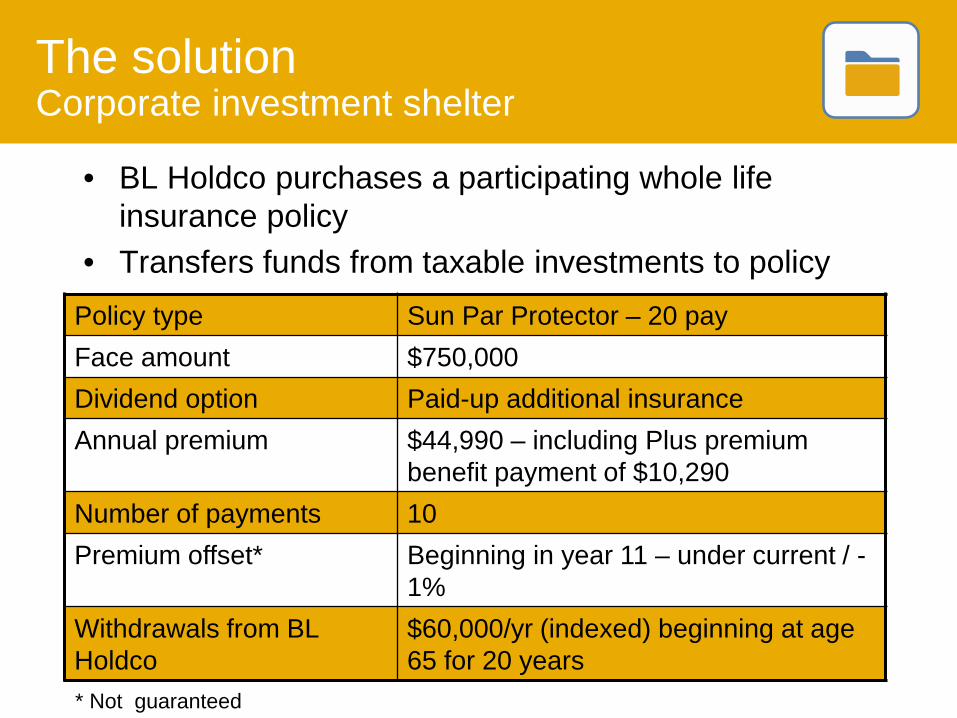

• BL Holdco purchases a participating whole life insurance policy

• Transfers funds from taxable investments to policy

The solution Corporate investment shelter

Policy type Sun Par Protector – 20 pay Face amount $750,000 Dividend option Paid-up additional insurance Annual premium $44,990 – including Plus premium

benefit payment of $10,290 Number of payments 10 Premium offset* Beginning in year 11 – under current / -

1% Withdrawals from BL Holdco

$60,000/yr (indexed) beginning at age 65 for 20 years

* Not guaranteed

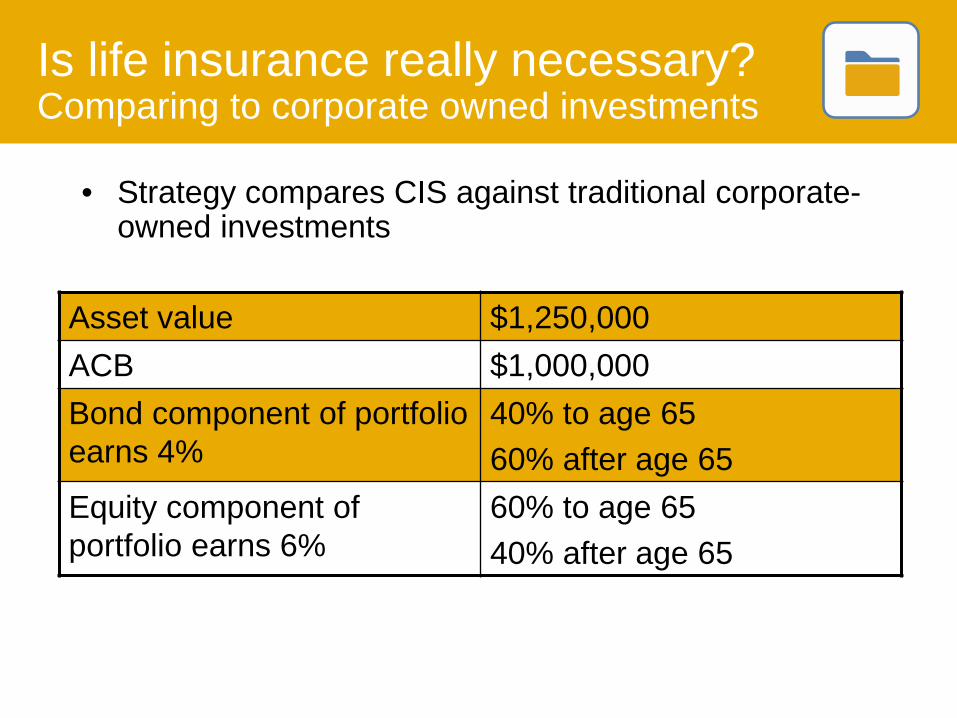

• Strategy compares CIS against traditional corporate- owned investments

Is life insurance really necessary? Comparing to corporate owned investments

Asset value $1,250,000 ACB $1,000,000 Bond component of portfolio earns 4%

40% to age 65 60% after age 65

Equity component of portfolio earns 6%

60% to age 65 40% after age 65

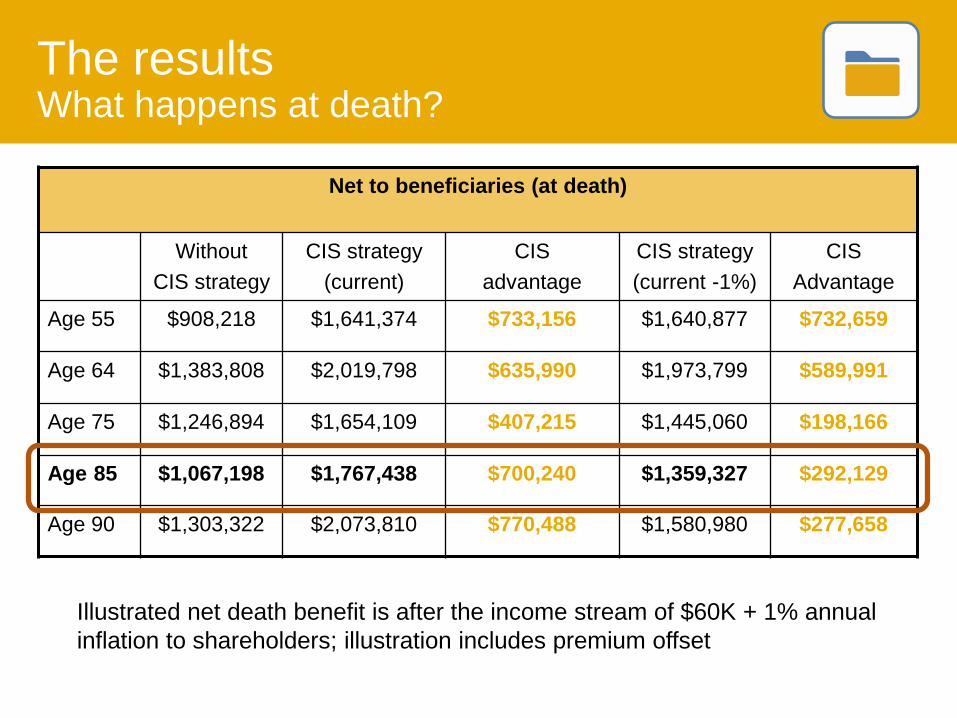

The results What happens at death?

Net to beneficiaries (at death)

Without CIS strategy

CIS strategy (current)

CIS advantage

CIS strategy (current -1%)

CIS Advantage

Age 55 $908,218 $1,641,374 $733,156 $1,640,877 $732,659

Age 64 $1,383,808 $2,019,798 $635,990 $1,973,799 $589,991

Age 75 $1,246,894 $1,654,109 $407,215 $1,445,060 $198,166

Age 85 $1,067,198 $1,767,438 $700,240 $1,359,327 $292,129

Age 90 $1,303,322 $2,073,810 $770,488 $1,580,980 $277,658

Illustrated net death benefit is after the income stream of $60K + 1% annual inflation to shareholders; illustration includes premium offset

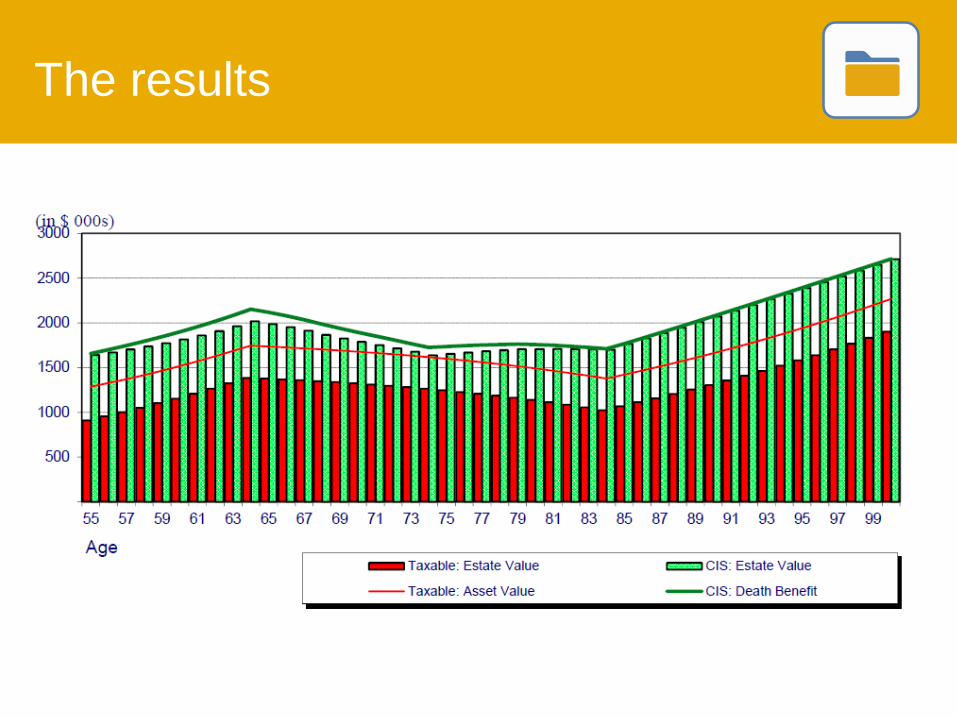

The results

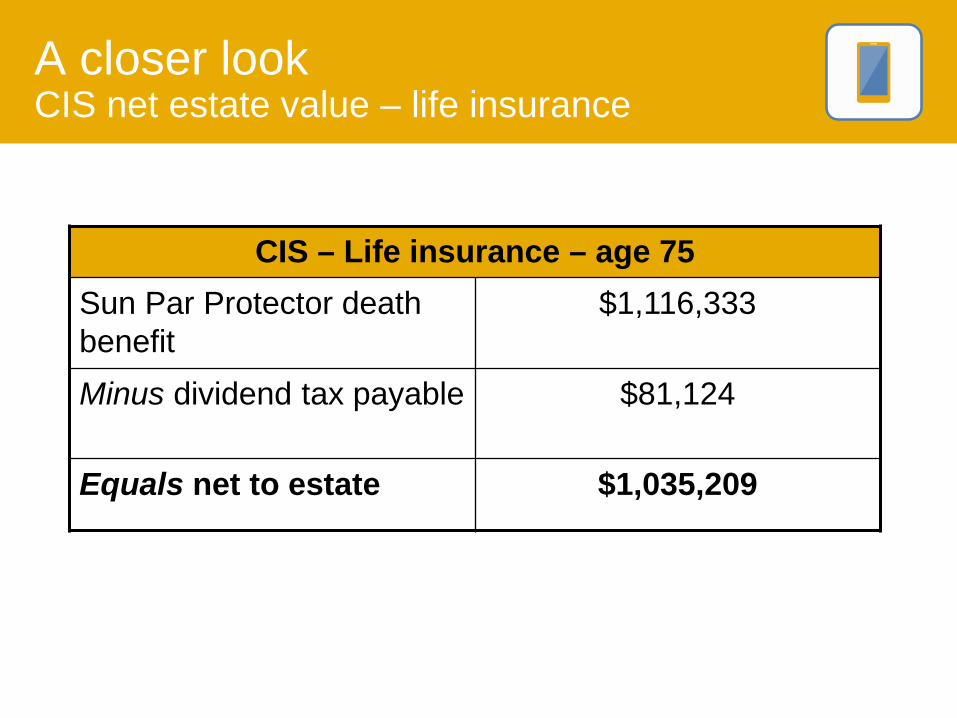

A closer look CIS net estate value – life insurance

CIS – Life insurance – age 75 Sun Par Protector death benefit

$1,116,333

Minus dividend tax payable $81,124

Equals net to estate $1,035,209

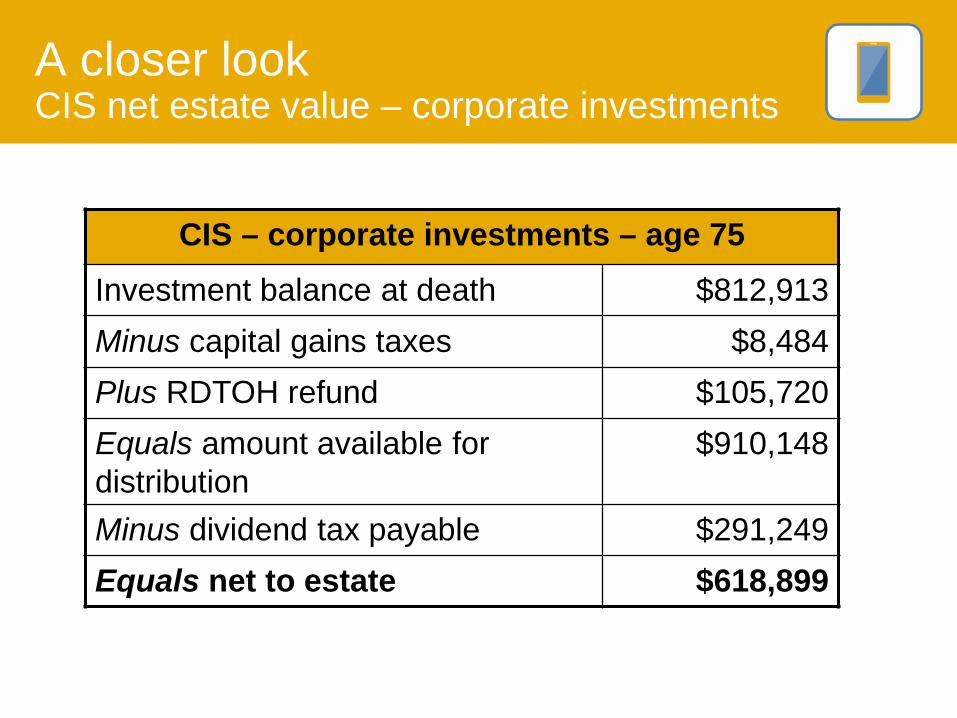

A closer look CIS net estate value – corporate investments

CIS – corporate investments – age 75 Investment balance at death $812,913 Minus capital gains taxes $8,484 Plus RDTOH refund $105,720 Equals amount available for distribution

$910,148

Minus dividend tax payable $291,249 Equals net to estate $618,899

A closer look CIS net estate value – corporate investments

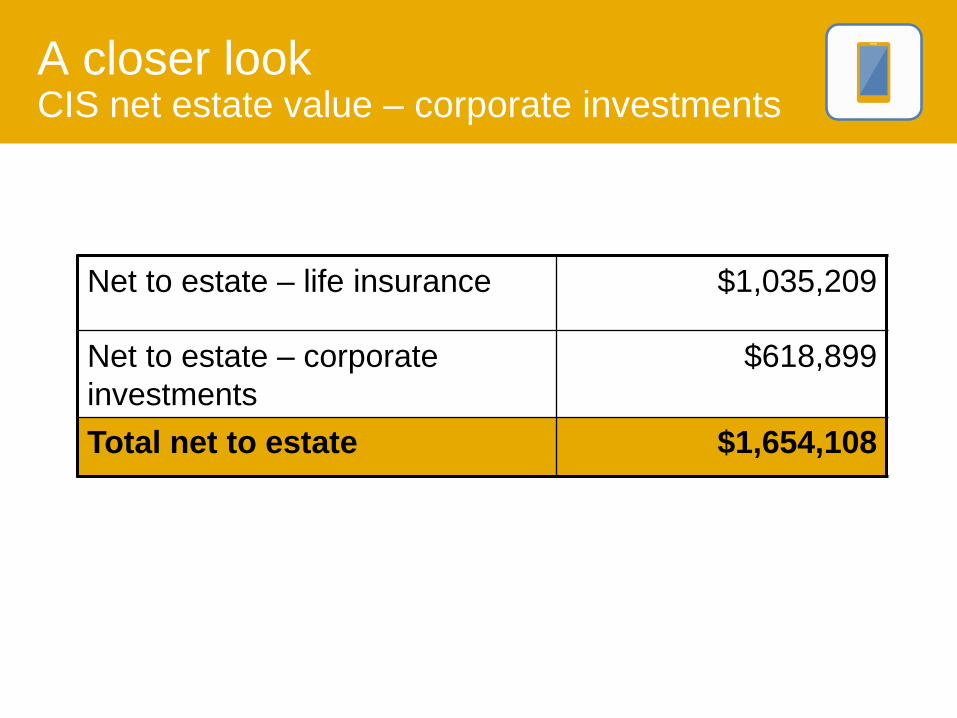

Net to estate – life insurance $1,035,209

Net to estate – corporate investments

$618,899

Total net to estate $1,654,108

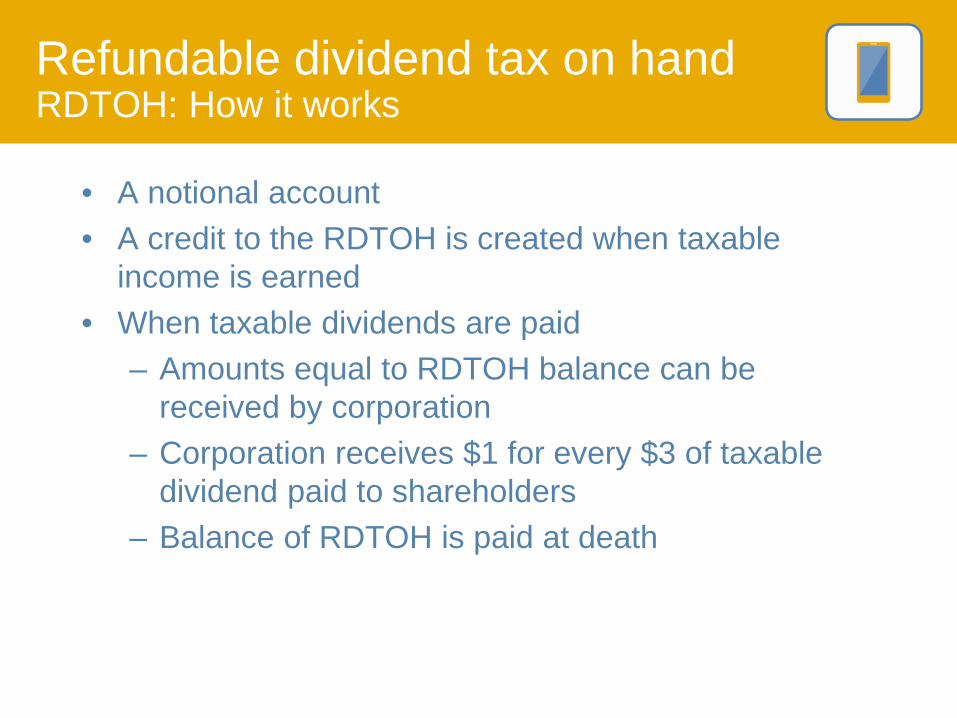

Refundable dividend tax on hand RDTOH: How it works

• A notional account • A credit to the RDTOH is created when taxable

income is earned • When taxable dividends are paid

– Amounts equal to RDTOH balance can be received by corporation

– Corporation receives $1 for every $3 of taxable dividend paid to shareholders

– Balance of RDTOH is paid at death

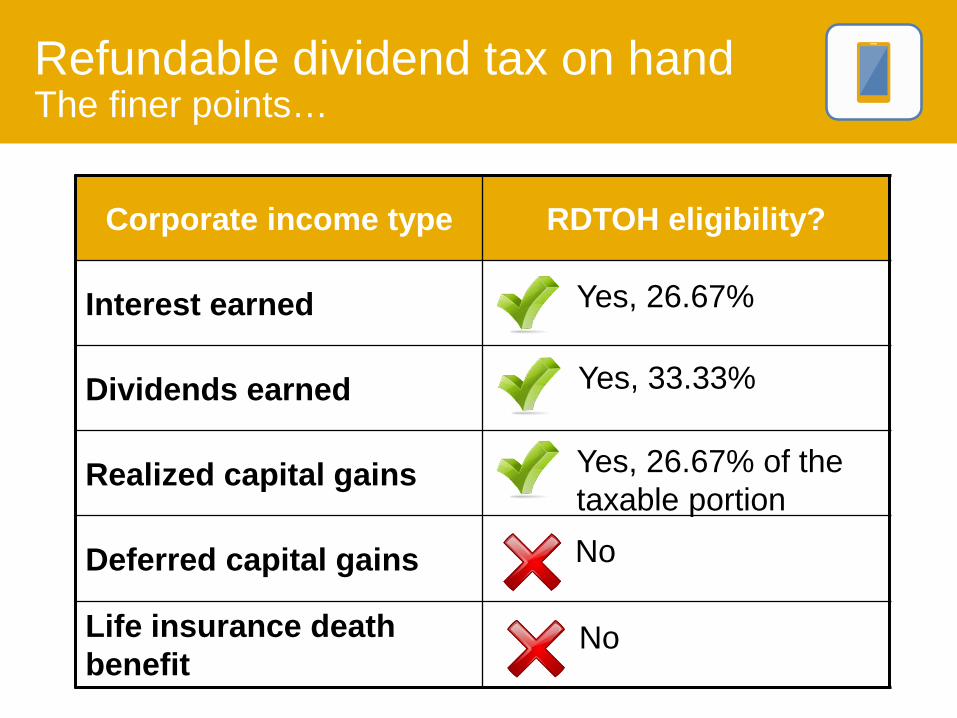

Refundable dividend tax on hand The finer points…

Corporate income type RDTOH eligibility?

Interest earned

Dividends earned

Realized capital gains

Deferred capital gains

Life insurance death benefit

Yes, 26.67% of the taxable portion No

Yes, 26.67%

Yes, 33.33%

No

• Tax on corporate investment income has been reduced

• Capital gains on corporate assets at death have been reduced

• A significant portion of corporate assets can be paid tax-free to Bruce’s estate

• Sun Par Protector participating whole life plan provides stable and consistent growth

Bruce’s concerns have been addressed

The results

• Bruce has significantly increased the value of his estate

• Transfers from traditional corporate investments to the tax-exempt Sun Par Protector policy reduce the corporate tax bill

• All or a portion of the life insurance death benefit can be paid tax free to Bruce’s estate

• Capital gains would be minimized at death

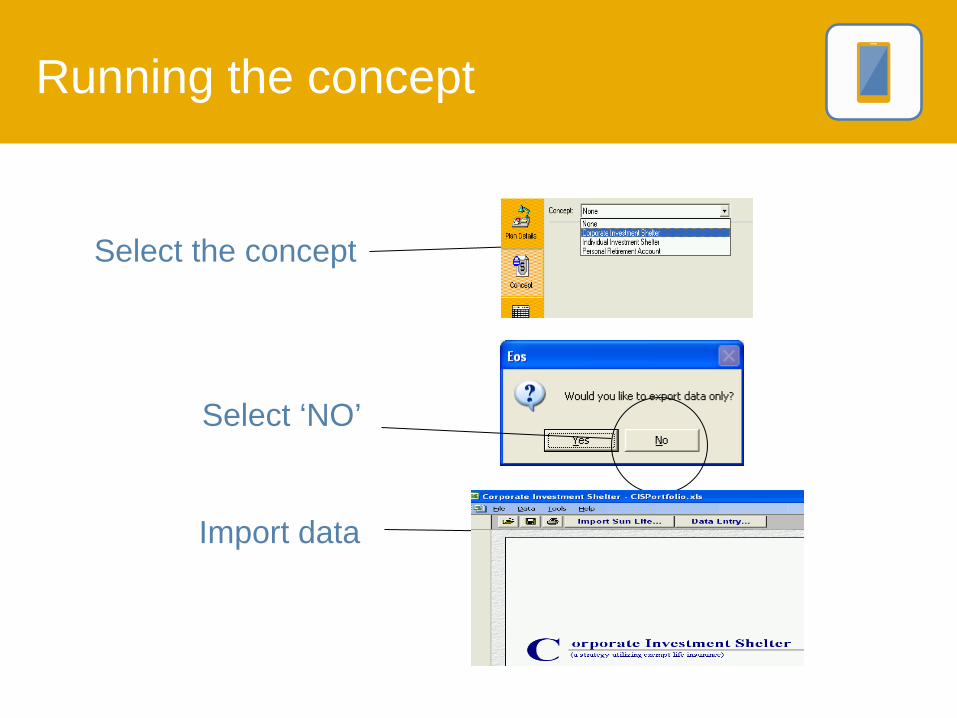

Running the concept

Import data

Select ‘NO’

Select the concept

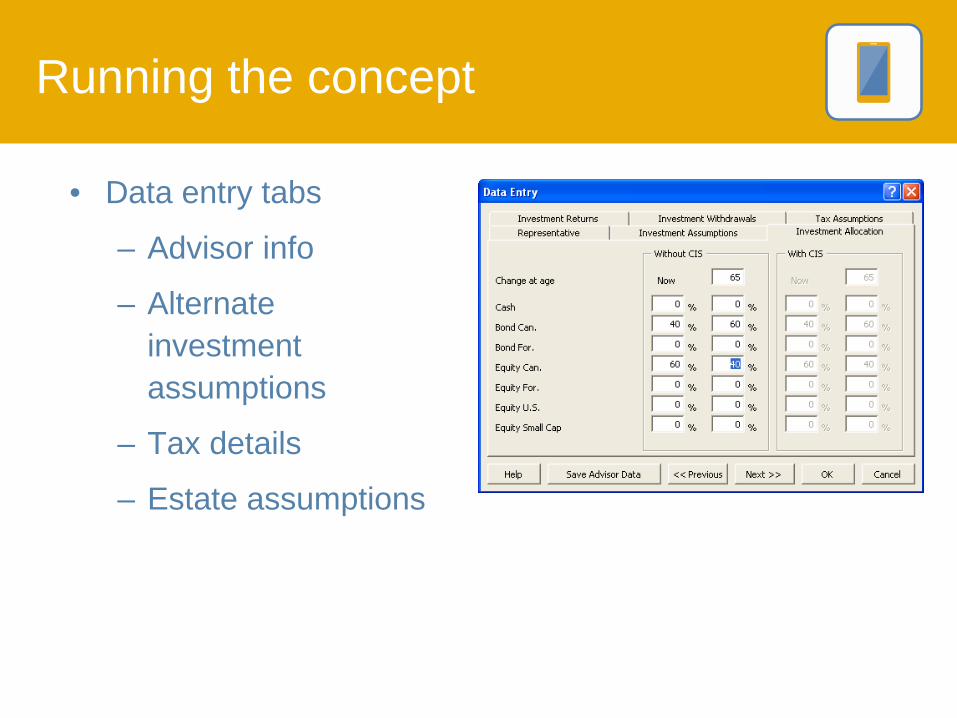

• Data entry tabs

– Advisor info

– Alternate investment assumptions

– Tax details

– Estate assumptions

Running the concept

Sample report pages

Marketing support

Client and advisor product guides

Financial Advisor Bulletin

CIS fact sheet

• Create corporate asset transfer opportunities • Minimize erosion of assets to taxes • Opportunity to earn dividends

– Access to a strong and stable par account

Less taxes = larger estate

Wrapping it up

If you’re not talking to your clients about protecting their assets, another advisor will.

*2013 Sun Life Canadian Unretirement Index

The bottom line

Available on: sunlife.ca/maketheconnection

Make the Connection strategy materials

Client email EOS Illustrations

Concept overview Strategy worksheet

NEXT STEPS

1. Identify 4-5 clients/prospects 2. Prepare a CIS proposal for each client 3. Set up appointments to meet with clients

and review the proposal

Disclaimer

• This information is presented with the understanding that it is intended for information purposes only.

• Neither Sun Life Assurance Company of Canada nor the presenter has been engaged for the purpose of providing legal, accounting, taxation, or other professional advice.

• No one should act on the examples/information without a thorough examination of the legal/tax situation with their own professional advisors after the facts of the specific case are considered.