Embed Size (px)

Citation preview

Hindustan Construction Co Ltd

By: Ajit. S. Shenoy

18th November 2016

Mumbai

NOV 2016-PLATT STEEL

ASIA CONF.

IMPACT OF STEEL ON CONSTRUCTION INDUSTRY-AN END USER’S PERSPECTIVE

2

IMPACT OF STEEL ON CONSTRUCTION INDUSTRY-

AN END USER’S PERSPECTIVE

Infrastructure Development in India –

Expressways & Highways

NOV 2016-PLATT STEEL

ASIA CONF.

IMPACT OF STEEL ON CONSTRUCTION INDUSTRY-AN END USER’S PERSPECTIVE

3

Sector Snapshot

Third-largest road network in the world, next in line only to the US and China

• Carries almost 65% of freight and 80% of passenger traffic.

• National Highways constitute for almost 2% of the network but carry about 40% of the total road traffic

Road program is the second largest infra program, next only to Power

• During the period FY 2013-17 total national highway networks in the country is expected to grow by a CAGR of ~3.7% to reach ~92,000 kms

March 2015 Infrastructure Development in India 4

National Highways / Expresswa

ys 2%

State Highways

3%

Major Roads 61%

Rural Roads 34%

Distribution of Road length in India – 4.69 Mn Km

Sector Opportunity

Proposed Investments in 12th 5 year plan – US$ 130 Billion – Build @ 20 km of roads per day

70% of the investment would be spent on National Highways and the balance on State Highways

50% of the investments are expected to come from private sector

March 2015 Infrastructure Development in India 5

72,000

74,000

76,000

78,000

80,000

82,000

84,000

86,000

88,000

90,000

92,000

94,000

2013 2014 2015 2016 2017

Projected Growth in National Highway

Network- Km

Sector Opportunity

National Highways – Targets :

• Developing 1000 km of expressways

• Developing 8,737 km of roads, including 3,846 km of national highways in the North Eastern Indian states

• Four-laning 20, 000 km of national highways

• Four-laning 6,736 km on North-South and East-West corridors

• Six-laning 6,500 km of the Golden Quadrilateral and selected national highways

• Widening 20,000 km of national highways to two lanes

State Highways - Targets :

• 2 laning of 30,000 Km

• 4 laning of 5,000 Km

• Strengthening of 41,500 Km

Policy

• 100% FDI under the automatic route is permitted for all road development projects

• 100% income tax exemption for a period of 10 years

• Grants / Viability gap Funding for marginal projects by NHAI.

MNOV 2016-PLATT

STEEL ASIA CONF.

IMPACT OF STEEL ON CONSTRUCTION INDUSTRY-AN END USER’S PERSPECTIVE

6

Infrastructure Development in India –

Railways

NOV 2016-PLATT STEEL

ASIA CONF.

IMPACT OF STEEL ON CONSTRUCTION INDUSTRY-AN END USER’S PERSPECTIVE

7

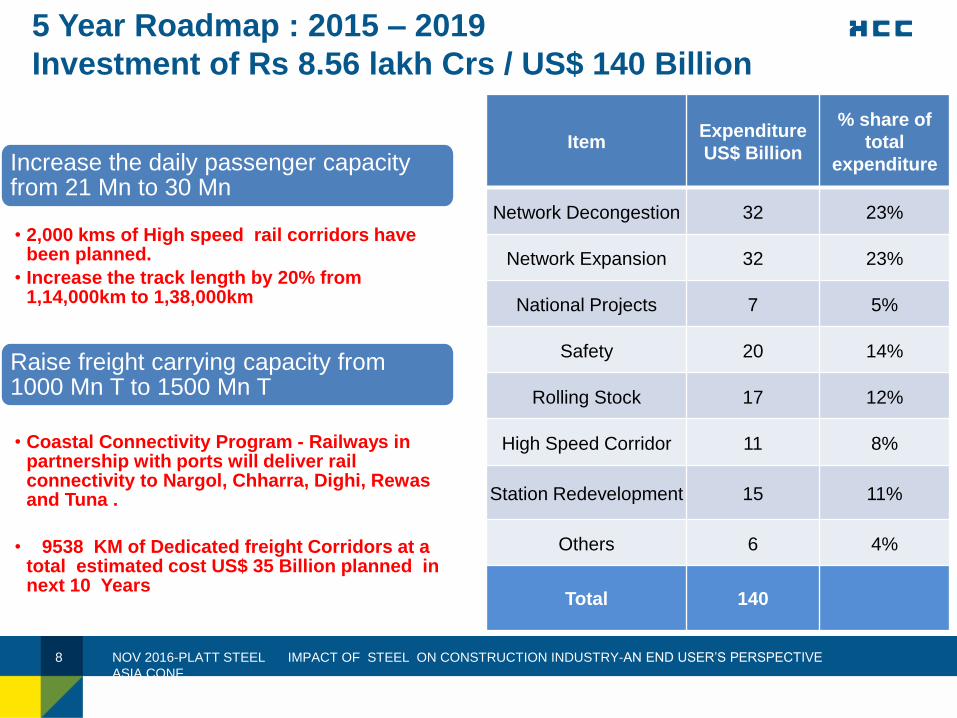

5 Year Roadmap : 2015 – 2019

Investment of Rs 8.56 lakh Crs / US$ 140 Billion

Item Expenditure

US$ Billion

% share of

total

expenditure

Network Decongestion 32 23%

Network Expansion 32 23%

National Projects 7 5%

Safety 20 14%

Rolling Stock 17 12%

High Speed Corridor 11 8%

Station Redevelopment 15 11%

Others 6 4%

Total 140

NOV 2016-PLATT STEEL

ASIA CONF.

8 IMPACT OF STEEL ON CONSTRUCTION INDUSTRY-AN END USER’S PERSPECTIVE

Increase the daily passenger capacity from 21 Mn to 30 Mn

• 2,000 kms of High speed rail corridors have been planned.

• Increase the track length by 20% from 1,14,000km to 1,38,000km

Raise freight carrying capacity from 1000 Mn T to 1500 Mn T

• Coastal Connectivity Program - Railways in partnership with ports will deliver rail connectivity to Nargol, Chharra, Dighi, Rewas and Tuna .

• 9538 KM of Dedicated freight Corridors at a total estimated cost US$ 35 Billion planned in next 10 Years

A no. of Mass Rapid Transit Systems are also being

planned across major Indian cities

Ludhiana

28.45 Km 1,600

Jaipur

28.5 Km 800

Ahmedabad

42 Km 1,600

Mumbai Metro Line 3

32.5 Km 3,800

Pune Metro

31.4 Km 3,200

Kolkata Metro

82 Km 1,800

Delhi Metro, Ph 4

109 Km 2,600

Name of Project

Length Km Value – US$ Mn

Over 500 Km of MRTS valued over US$ 20 Billion to be built across 8 cities

Guwahati Metro

44 Km 900

Patna Metro

60 Km 1,600

Cuttack &

Bhubaneshwar Metro

40 Km 2,200

Growth Drivers

Increasing Urbanization

Economic Growth & demands thereof

Increased congestion on Urban roads

Growth in passenger traffic and automobiles

NOV 2016-PLATT STEEL

ASIA CONF.

IMPACT OF STEEL ON CONSTRUCTION INDUSTRY-AN END USER’S PERSPECTIVE

9

Infrastructure Development in India –

Airports

NOV 2016-PLATT STEEL

ASIA CONF.

IMPACT OF STEEL ON CONSTRUCTION INDUSTRY-AN END USER’S PERSPECTIVE

10

Sector Snapshot

0

50

100

150

200

250

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY17[E]

Growth in Passenger Traffic - Millions

Domestic International

NOV 2016-PLATT STEEL

ASIA CONF.

IMPACT OF STEEL ON CONSTRUCTION INDUSTRY-AN END USER’S PERSPECTIVE

11

•There are 136 airports/ airstrips in the country,

of which AAI owns and manages 103 airports

and 25 civil enclaves at defence airfields

•Airports account for about 17% of the total

number and total value of projects planned in

the infrastructure space and 2% of the total

infrastructure budget allocations .

•Passenger traffic in India increased at a CAGR

of 13% (Domestic: 13%; International: 10%)

over the last 10 years

Sector Opportunity

All values in

US$ Million Private

AAI /

Central Govt State Govt

Metro Airports 3,000 250

Non Metro

Airports 1,000 250

Greenfield

Airports 3,583 200 333

Non operational

Airports 1,000

Other Airports 167 1,383

Cargo Logistics 667

Total 9,417 2,083 400

Grand Total 12,000

Greenfield

Airports

Non Metro

Airports

NOV 2016-PLATT STEEL

ASIA CONF.

IMPACT OF STEEL ON CONSTRUCTION INDUSTRY-AN END USER’S PERSPECTIVE

12

Infrastructure Development in India –

Ports

NOV 2016-PLATT STEEL

ASIA CONF.

IMPACT OF STEEL ON CONSTRUCTION INDUSTRY-AN END USER’S PERSPECTIVE

13

Sector Snapshot

NOV 2016-PLATT STEEL

ASIA CONF.

IMPACT OF STEEL ON CONSTRUCTION INDUSTRY-AN END USER’S PERSPECTIVE

14

•India a long coastline of over 7,500 Km, with 13 major and 187 non major

ports

•Witnessed a CAGR of 20.1% between FY 06 to FY 12. In the last 2 years

the through put has been lower owing to the economic conditions

•Non-major ports are set to benefit from strong growth in India’s external

trade

•The outlook for cargo growth remains favorable, considering the

consistent demand growth in key user industries (coal, crude oil and

containers)

•Increasing private participations and favorable policies will help the

industry achieve higher capacities

Sector Opportunity

5,101 5,523

10,624 9,638

15,998

25,637

3,336

12,162

15,498

Major Ports Minor Ports Total

Investments in Ports – US$ Million

Phase I [2012] Phase II [2016] Phase III [2020]

1 2

3.2

2010 2016 2020

Capacity Addition in Billion T

NOV 2016-PLATT STEEL

ASIA CONF.

IMPACT OF STEEL ON CONSTRUCTION INDUSTRY-AN END USER’S PERSPECTIVE

Construction of berth 65%

15

•New Maritime Agenda announced

for Port development up to 2020

•Capacity addition of 3.2 Billion T by

2020 in 3 phases

•Private sector to account for 70% of

total outlay

•Minor ports to account for 78% of

total investment

Source: Indian Ports association, Planning commission, Report of the working group on the XI Plan for the Port Sector, NMDP document

Total investment

requirement of ~

US$ 13 Billion by

2020

Planned capacity addition in MTPA

Planned investment in US$ Million

Mangalore

28 3,400

23 3,425

5 480

7 320

38 1,150

25 180

20 775

56 2,300

9 330

29 1,760

24 1,100

Kandla

JNPT

Mormugao

Cochin

Tuticorin

Chennai

Ennore

Vizag

Paradip

Kolkata

Ports : Capacity addition – Major Ports

NOV 2016-PLATT STEEL

ASIA CONF.

IMPACT OF STEEL ON CONSTRUCTION INDUSTRY-AN END USER’S PERSPECTIVE

16

Total investment

requirement of ~

US$ 27 Billion by

2020

Karnataka

629 12,000

155 3,400

1.5 30

51 1,200

20 300

199 4,000

195 5,600

51 1,200

Gujarat

Maharashtra

Goa

Kerela

Tamilnadu

Andhra Pradesh

Orissa

Planned capacity addition in MTPA

Planned investment in Rs US$ Million

Ports : Capacity addition – Minor Ports

NOV 2016-PLATT STEEL

ASIA CONF.

IMPACT OF STEEL ON CONSTRUCTION INDUSTRY-AN END USER’S PERSPECTIVE

17

Infrastructure Development in India –

Power

NOV 2016-PLATT STEEL

ASIA CONF. IMPACT OF STEEL ON CONSTRUCTION INDUSTRY-AN END USER’S PERSPECTIVE

18

Sector Snapshot

Thermal 70%

Hydro 16%

Nuclear 2% RES

12%

India’s Installed Power Capacity - 2,61,006 MW [Feb-2015]

135 218

323

437

123

2012 2017 2022 2027

Projected Peak Demand - GW

Peak Demand Actual Availability

NOV 2016-PLATT STEEL

ASIA CONF.

IMPACT OF STEEL ON CONSTRUCTION INDUSTRY-AN END USER’S PERSPECTIVE

19

•India has the fifth largest generation

capacity in the world with an installed

capacity of 261 GW

•India's demand supply deficit currently

stands at 2.5% as of February 2015

•Peak demand supply deficit stands at 2.8%

as of February 2015

•Thermal, mainly coal based power accounts

for 70% of total installed capacity

•India’s peak demand for Power is expected

to triple by 2027 to

437 GW

Growth Drivers

Increasing Population

Increasing power consumption by end users like Domestic, Industrial & Agricultural sectors

Manufacturing sector in India is expected to have high growth over next decade

Also India is set to witness a rapid & massive scale of urbanization

Industrial 42%

Agricultural 22%

Domestic 25%

Commercial 11%

Sector wise breakup of Electricity Consumption

88,000 93,400

59,000

45,000

12th FYP 13th FYP

Power Generation Targets

Capacity Addition Target MW Investments in US$ Mn

NOV 2016-PLATT STEEL

ASIA CONF.

IMPACT OF STEEL ON CONSTRUCTION INDUSTRY-AN END USER’S PERSPECTIVE

20

Sector Opportunities

Thermal Power

Capacity Addition Target 72,340 MW

Private Sector to account for over 70%

Hydro Power

Capacity Addition Target 10,897 MW

Private Sector to account for over 40%

Nuclear Power

Capacity Addition Target 5,300 MW

Total Planned Capacity Addition : 88,000 MW

Total Planned Investments : US$ 320 Billion

NOV 2016-PLATT STEEL

ASIA CONF.

IMPACT OF STEEL ON CONSTRUCTION INDUSTRY-AN END USER’S PERSPECTIVE

21

Infrastructure Development in India –

Urban Infrastructure

NOV 2016-PLATT STEEL

ASIA CONF.

IMPACT OF STEEL ON CONSTRUCTION INDUSTRY-AN END USER’S PERSPECTIVE

22

Sector Snapshot

India’s level of urbanization is much less than many other developing countries Only 30% of India’s population lives in urban areas

Three decades of rapid economic growth in India has not resulted in increased urbanization

• Industrialization has been capital intensive.

• Service Industry was skill intensive.

• Both these industries have not resulted in migration of rural population to urban areas.

• Though share of agriculture in total employment has declined as compared to 1970’s, it still accounts for almost 50%.

• Economic growth which happened during the period 1991 – 2005 was not broad based and labour intensive.

45 54

78 87

30

China Indonesia Mexico Brazil India

Level of Urbanization [%]

NOV 2016-PLATT STEEL

ASIA CONF.

IMPACT OF STEEL ON CONSTRUCTION INDUSTRY-AN END USER’S PERSPECTIVE

23

5 times increase in GDP

Urban population to increase to 600 million, 40% of India’s total population - twice the

population of USA today

Net working age population to increase by 270 million

70% of India’s GDP and net new employment to come from

urban India

4.5 times increase in no. of urban million households

68 cities will have population of 1 million +, up from 42 today.

Europe has 35 today.

700 – 900 million sqm of commercial / residential space

needs to be built

[a new chicago every year].

7,400 Km of Metros / Subways need to be built – 20 times the capacity added in last

decade

2.5 Billion Sqm of roads will have to be paved, 20 times

the capacity added in past decade.

Sector Opportunities

India is now set to urbanize at an unprecedented pace and scale which has not happened

anywhere in world except China ( Year 2007- 2030 )

NOV 2016-PLATT STEEL

ASIA CONF.

IMPACT OF STEEL ON CONSTRUCTION INDUSTRY-AN END USER’S PERSPECTIVE

24

Growth Drivers

56

95 83

189

2007 2030

Water Supply – BLD Demand expected to double

13

42

66

151

2007 2030

Sewerage - BLD Demand expected to increase

2.5 times

51

295

71

377

2007 2030

Solid Waste - MTPA Demand expected to increase

5 times

430 540

640

980

2007 2030

Private Transportation Thousand Lane Km

Demand expected to increase 1.5 times

990 1990

2984

8400

2007 2030

MRTS – Route Km Demand expected to triple

5 12

30

50

2007 2030

Affordable Housing Million Units

Demand expected to increase 1.7 times

NOV 2016-PLATT STEEL

ASIA CONF.

IMPACT OF STEEL ON CONSTRUCTION INDUSTRY-AN END USER’S PERSPECTIVE

25

Sector Opportunities

96 53

15 32

199

392 395

1040

Wate

r

Sew

era

ge

Solid

Waste

Sto

rm W

ate

r D

rain

s

Urb

an R

oads

Ma

ss T

ran

sit

Afford

able

Ho

usin

g

Ope

x

Funding Requirement in US$ Billion

India’s annual spending of $17 in per capita terms is only 14% of China’s &4% of UK’s per capita terms

India needs to raise it’s per capita infrastructure spending by 8 times

Spending on Urban Infra should increase to 2% of GDP from the current level of 0.5% annually

50% of investment would be required to remove infrastructure backlog

Large Tier 1 & Tier 2 cities will need per capita investment > $200

Indian Cities need $ 1,200 Billion of Additional

Capital Investment by 2030

Total Capex

NOV 2016-PLATT STEEL

ASIA CONF.

IMPACT OF STEEL ON CONSTRUCTION INDUSTRY-AN END USER’S PERSPECTIVE

26

SUPPLY AND DEMAND PROJECTION- Norms of Steel Demand in Infrastructure Projects - Investment Programme

Demand for Steel (Norms / Illustration)

NHDP - 100 tons for Rs. 50 million spent.

Railways - 300 tons for a double line per km, 24-30 tons for each wagon, additional demand for old bridges

Power Projects - 33,000 tons for 500 MW, additional demand for special steels,.

Power Transmission - 7,000 tons for 200 km, 400 KV (double circuit line)

Oil and Gas Well platform requires 2,000 tons of structural steel and a process platform requires 10,000 tons of steel. A 6-Mtpy capacity refinery requires 85,000 tons of steel

Housing Residential blocks typically require 1000 to 2000 tons of steel per block.

NOV 2016-PLATT STEEL

ASIA CONF.

Source: Compiled on the basis of a paper presented by Shoeb Ahmed D(c),

SAIL at 3rd Steel Raw Material Conference in Delhi, 2007. 27

FACTORS IMPACTING STEEL PRICES

NOV 2016-PLATT STEEL

ASIA CONF.

IMPACT OF STEEL ON CONSTRUCTION INDUSTRY-AN END USER’S PERSPECTIVE

28

• Price movement of raw material like coal , iron ore etc.

• Installed Capacities.

• Product Mix planned by each Producer depending on the returns and demand

STEEL CO.S

• Seasonal.

• Investment policies of Govt. and actual investments. SECTOR DEMAND

• Domestic: Primary( Main) Producers v/s Secondary (Rerolling) Producers

• international: Govt. Policies – trade barriers / Liberalization

COMPETITION

NOV 2016-PLATT STEEL

ASIA CONF.

IMPACT OF STEEL ON CONSTRUCTION INDUSTRY-AN END USER’S PERSPECTIVE

29

NOV 2016-PLATT STEEL

ASIA CONF.

IMPACT OF STEEL ON CONSTRUCTION INDUSTRY-AN END USER’S PERSPECTIVE

30

TREND ANALYSIS- REBARS AND STRUCTURALS-

APR’14 TO OCT 16

MONTH

REBARS LANDED RATE- AV-

RS/MT % CHANGE WRT APR'14

STRUC. STEEL -LANDED RATE

AV-RS/MT

% CHANGE WRT

APR'14

Apr-14 48689.06 56920.47

May-14 48692.64 0.01 64395.84 13.13

Jun-14 49660.86 2.00 61152.33 7.43

Jul-14 50410.95 3.54 59728.72 4.93

Aug-14 50411.68 3.54 49595.98 -12.87

Sep-14 48634.88 -0.11 49029.8 -13.86

Oct-14 48799.77 0.23 51930.64 -8.77

Nov-14 47744.49 -1.94 51729.96 -9.12

Dec-14 46695.34 -4.09 49596.51 -12.87

Jan-15 43873.01 -9.89 49652.27 -12.77

Feb-15 42027.35 -13.68 49556.58 -12.94

Mar-15 42670.65 -12.36 50781.86 -10.78

Apr-15 42072.69 -13.59 51819.2 -8.96

May-15 43121.97 -11.43 47222.53 -17.04

Jun-15 41557.99 -14.65 46844.14 -17.70

Jul-15 40754.62 -16.30 43801 -23.05

Aug-15 38812.22 -20.29 47866.85 -15.91

Sep-15 40345.72 -17.14 48077.09 -15.54

Oct-15 38220.07 -21.50 41055.13 -27.87

Nov-15 36074.19 -25.91 41488.49 -27.11

Dec-15 33268.69 -31.67 40026.33 -29.68

Jan-16 33491.45 -31.21 43909.88 -22.86

Feb-16 35208.9 -27.69 41127 -27.75

Mar-16 37000.28 -24.01 39971.5 -29.78

Apr-16 39278.2 -19.33 43797.1 -23.06

May-16 38957.93 -19.99 47751.04 -16.11

Jun-16 39114.42 -19.66 50288.46 -11.65

Jul-16 37703.02 -22.56 46363.49 -18.55

Aug-16 34418.45 -29.31 44532.46 -21.76

Sep-16 33390.37 -31.42 49187.36 -13.59

Oct-16 33845.87 -30.49 45411.85 -20.22

NOV 2016-PLATT STEEL

ASIA CONF.

IMPACT OF STEEL ON CONSTRUCTION INDUSTRY-AN END USER’S PERSPECTIVE

31

CHALLENGES TO THE BUYERS

Estimating future price trends for bidding purposes.

Compensation for price variation through escalation formulae not in line with the actual price movement.

Financing steel purchases through innovative means.

Availability of all material at project sites on time and within budgeted cost to meet the deadlines.

Mitigating all the above uncertainities by dynamically designing the stocking policies.

Negotiating high volume purchase month on month within first 05 days of the month to make the material available at project sites on time .

NOV 2016-PLATT STEEL

ASIA CONF.

IMPACT OF STEEL ON CONSTRUCTION INDUSTRY-AN END USER’S PERSPECTIVE

32

EXPECTATIONS OF CONSTRUCTION INDUSTRY

FROM STEEL COMPANIES

NOV 2016-PLATT STEEL

ASIA CONF.

IMPACT OF STEEL ON CONSTRUCTION INDUSTRY-AN END USER’S PERSPECTIVE

33

Informing promptly developments / application innovations on regular basis to the project consultants ,owners/ clients and

contractors.

Prices to remain steady for a good 10-11 months of a particular financial year to help in right estimates for bidding of new projects and near accurate budgeting of costs for ongoing projects.

Supply of value added products direct from manufacturer eg .colour coated sheets, cut and bent rebars, cut to length sections, fusion bonded epoxy coated rebars etc.

Supply of products with tighter rolling tolerances without compromising on quality strength and other physical properties.

EXPECTATIONS OF CONSTRUCTION INDUSTRY

FROM STEEL COMPANIES

Steel companies to become facilitators for channel financing the sales of their products to the customers through innovative schemes other than standard instruments like Letter of Credit or against Bank Guarantees.

Fix prices for long period ideally FY(Apr – Mar )with escalation formula of main contract on back to back basis ( for steel component) thus partnering with infra companies in their gains by mitigating the risks of main contract .

NOV 2016-PLATT STEEL

ASIA CONF.

IMPACT OF STEEL ON CONSTRUCTION INDUSTRY-AN END USER’S PERSPECTIVE

34

Thank You

March 2NOV 2016-PLATT

STEEL ASIA CONF.

015

IMPACT OF STEEL ON CONSTRUCTION INDUSTRY-AN END USER’S PERSPECTIVE

35