Embed Size (px)

Citation preview

Higher Education Statistics – collection and processing

Discussion on the Swedish Case Anna Gärdqvist and Mats Haglund Statistics Sweden

Reflection on the Austrian CaseMichaela Schaffhauser-LinzattiUniversity of Vienna

May 11, 2006, Graz

Presentation

Sweden: students Austria: Overall Information

Reporting on performanceMonitoring of performanceMonitoring of data

Presentation

Paper• Data flow

• Organisational responsibilities

• General aspects of reporting on Higher Education

• Data flow

• Organisational responsibilities

• Selected repor- ting tools

• Possible answers from the Austrian experience

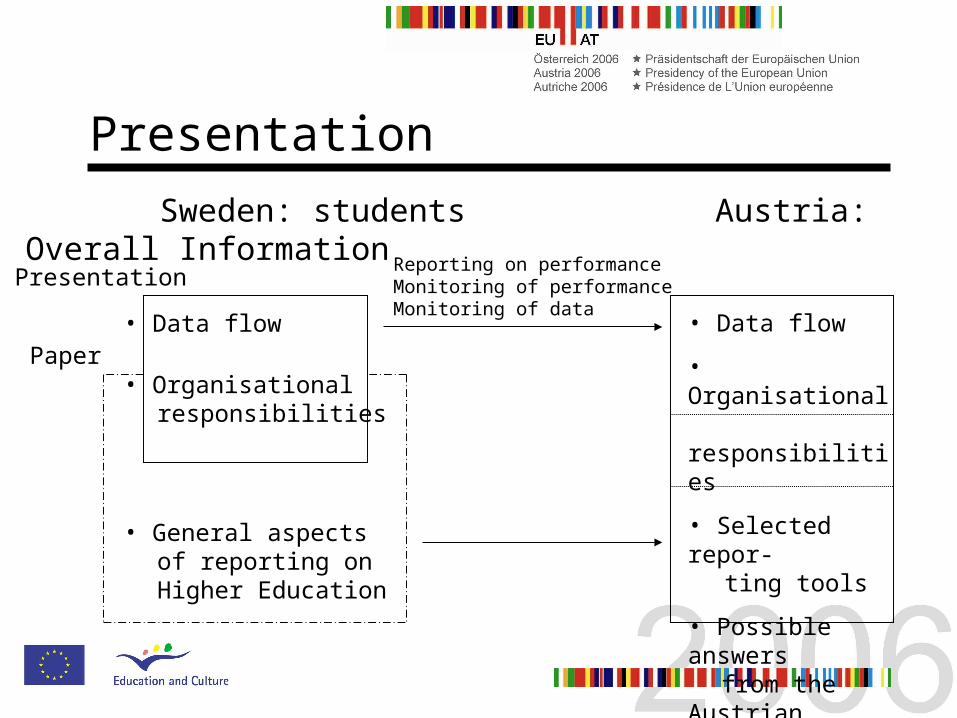

Data Flow

Public Universities

Vocational Universities (FH)

Private UniversitiesTheological UniversitiesOthers

Federal Ministry for Education,Science and Culture

FH-Council

Statistics Austria

University Report

Report on Higher Education

A:

Swedish National Board of Student Aid; Ministry of Education, Research and Culture; Statistics Sweden

S: Register of Higher Education

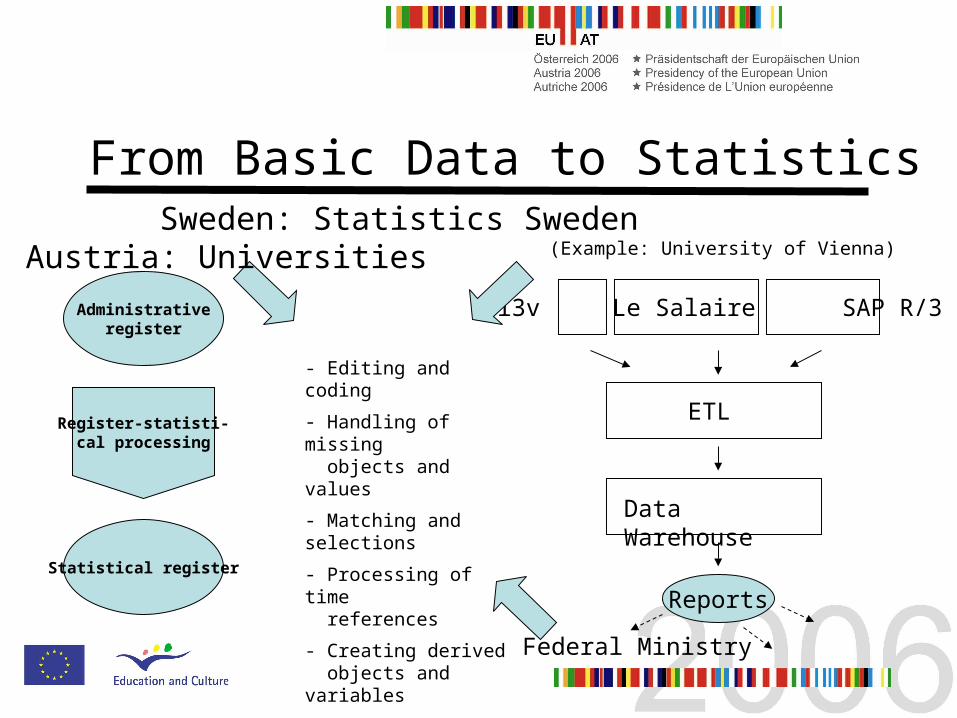

From Basic Data to Statistics

(Example: University of Vienna)

Administrativeregister

Register-statisti-cal processing

Statistical register

- Editing and coding

- Handling of missing objects and values

- Matching and selections

- Processing of time references

- Creating derived objects and variables

i3v Le Salaire SAP R/3

ETL

Data Warehouse

Reports

Federal Ministry

Sweden: Statistics Sweden Austria: Universities

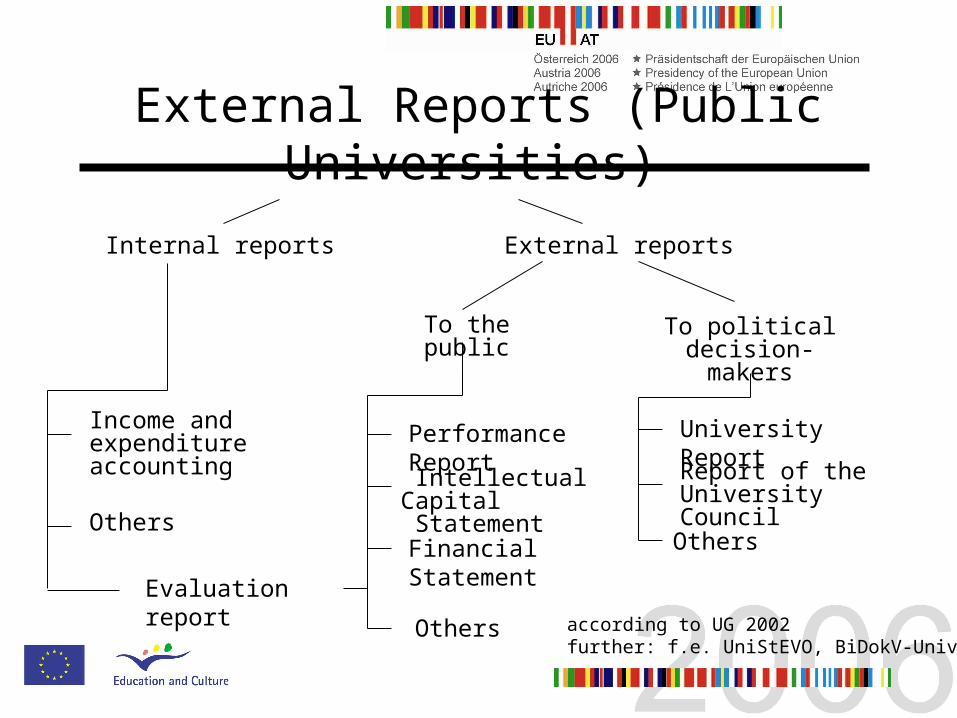

Internal reports External reports

To the public To political decision-makers

Income and expenditure accounting

Others

Evaluation report

Performance Report

Intellectual Capital Statement

Financial Statement

Others

University Report

Report of the University Council

Others

External Reports (Public Universities)

according to UG 2002further: f.e. UniStEVO, BiDokV-Univ

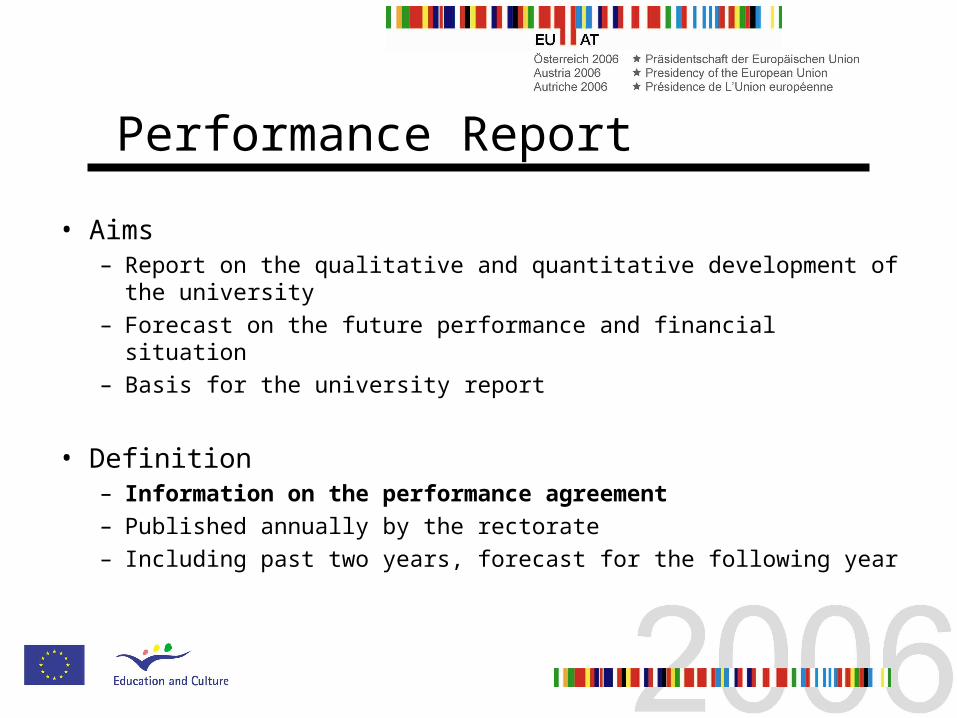

Performance Report

• Aims– Report on the qualitative and quantitative development of the

university– Forecast on the future performance and financial situation – Basis for the university report

• Definition– Information on the performance agreement– Published annually by the rectorate– Including past two years, forecast for the following year

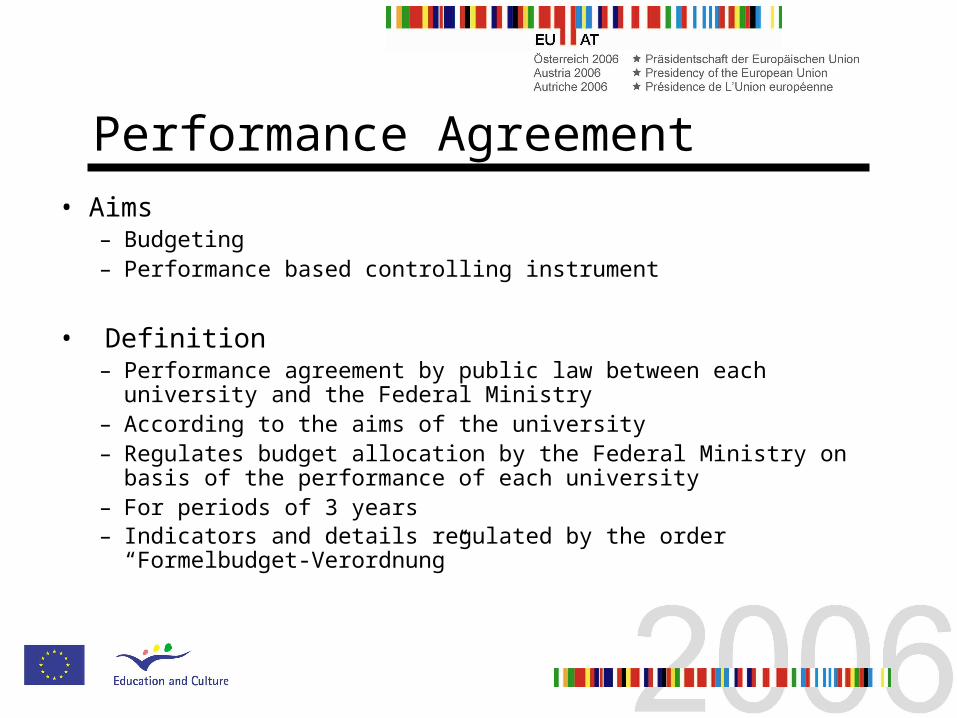

Performance Agreement• Aims

– Budgeting– Performance based controlling instrument

• Definition– Performance agreement by public law between each university and the

Federal Ministry– According to the aims of the university– Regulates budget allocation by the Federal Ministry on basis of the

performance of each university– For periods of 3 years– Indicators and details regulated by the order “Formelbudget-Verordnung”

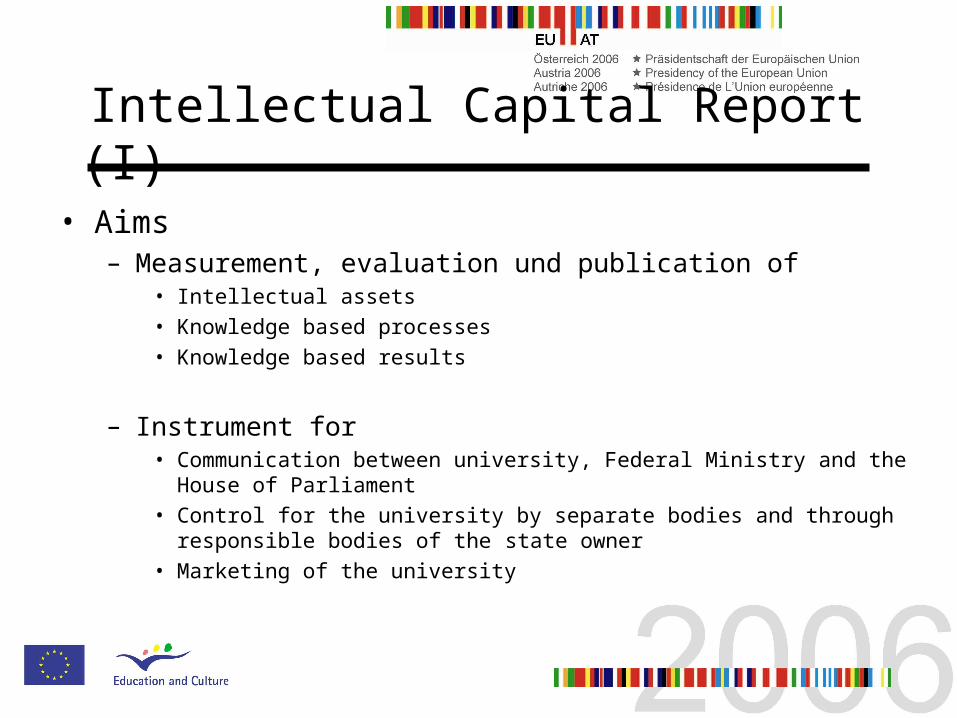

Intellectual Capital Report (I)

• Aims– Measurement, evaluation und publication of

• Intellectual assets• Knowledge based processes• Knowledge based results

– Instrument for• Communication between university, Federal Ministry and the House of Parliament• Control for the university by separate bodies and through responsible bodies of

the state owner• Marketing of the university

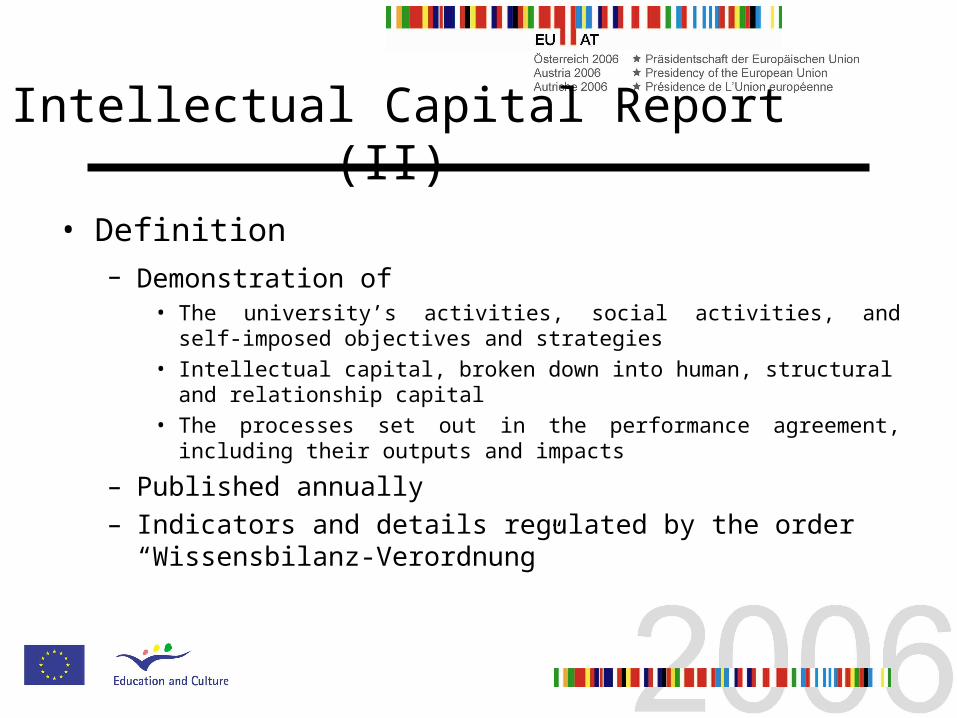

Intellectual Capital Report (II)

• Definition– Demonstration of

• The university’s activities, social activities, and self-imposed objectives and strategies

• Intellectual capital, broken down into human, structural and relationship capital

• The processes set out in the performance agreement, including their outputs and impacts

– Published annually– Indicators and details regulated by the order “Wissensbilanz-

Verordnung”

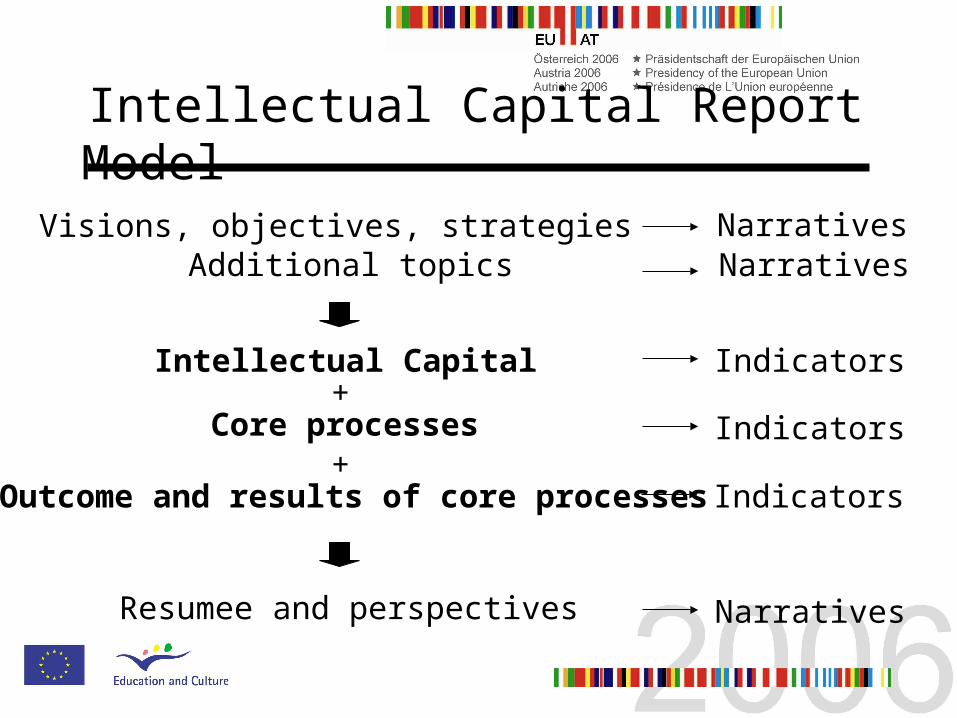

Intellectual Capital Report Model

Visions, objectives, strategies

+

NarrativesAdditional topics

Intellectual Capital

Core processes

Resumee and perspectives

Narratives

Indicators

Indicators

Narratives

+Outcome and results of core processes Indicators

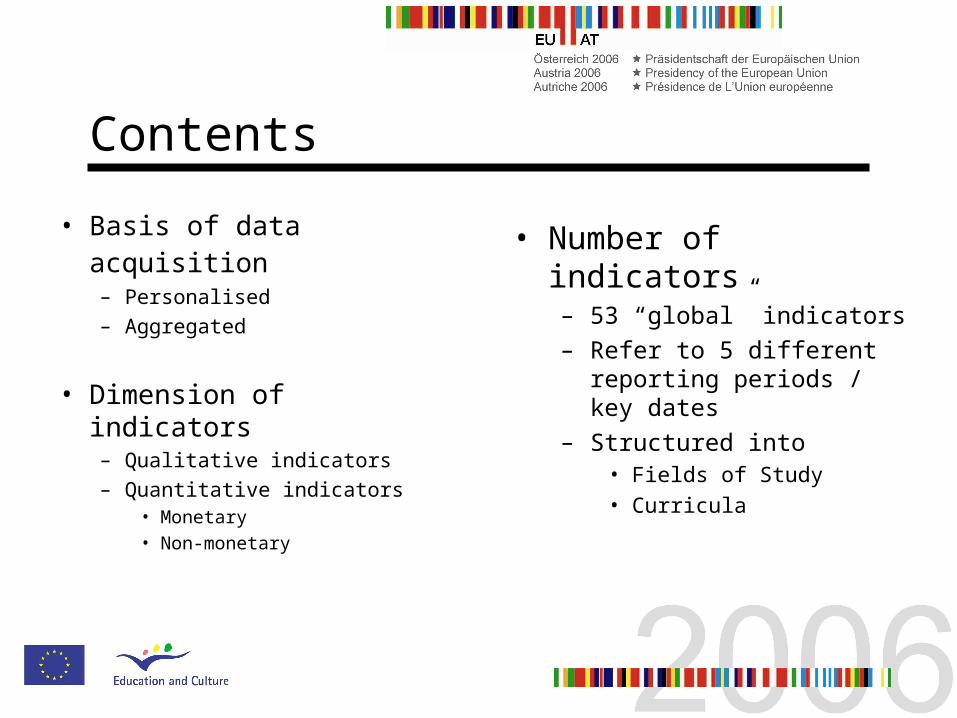

Contents

• Basis of data acquisition – Personalised

– Aggregated

• Dimension of indicators– Qualitative indicators

– Quantitative indicators• Monetary• Non-monetary

• Number of indicators– 53 “global” indicators

– Refer to 5 different reporting periods / key dates

– Structured into • Fields of Study• Curricula

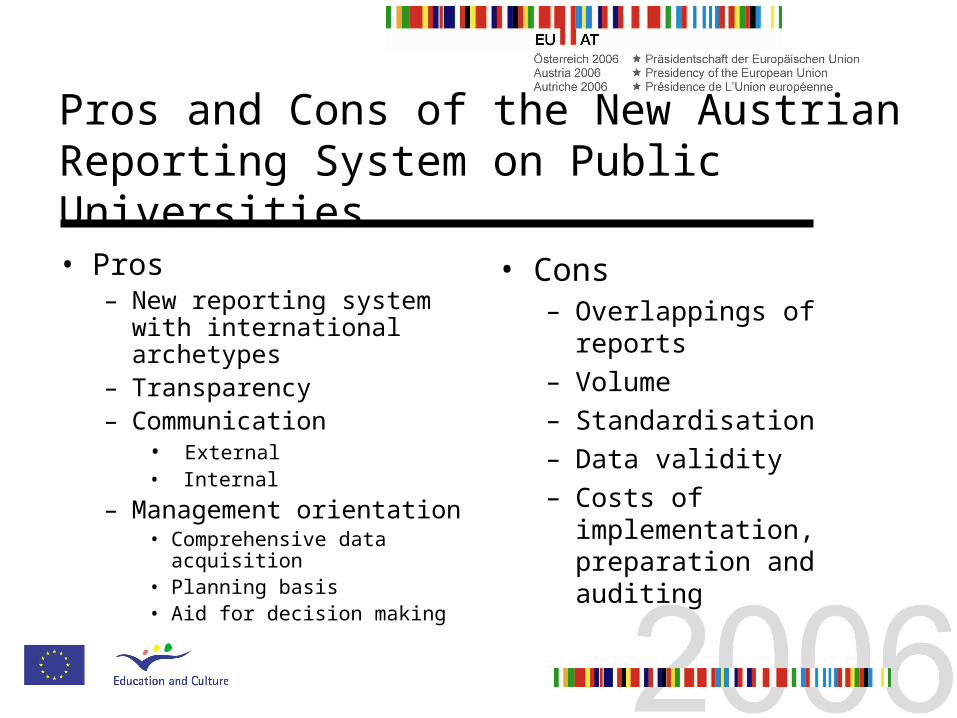

Pros and Cons of the New Austrian Reporting System on Public Universities

• Pros– New reporting system with

international archetypes– Transparency– Communication

• External• Internal

– Management orientation• Comprehensive data

acquisition• Planning basis• Aid for decision making

• Cons – Overlappings of reports– Volume– Standardisation– Data validity– Costs of implementation,

preparation and auditing

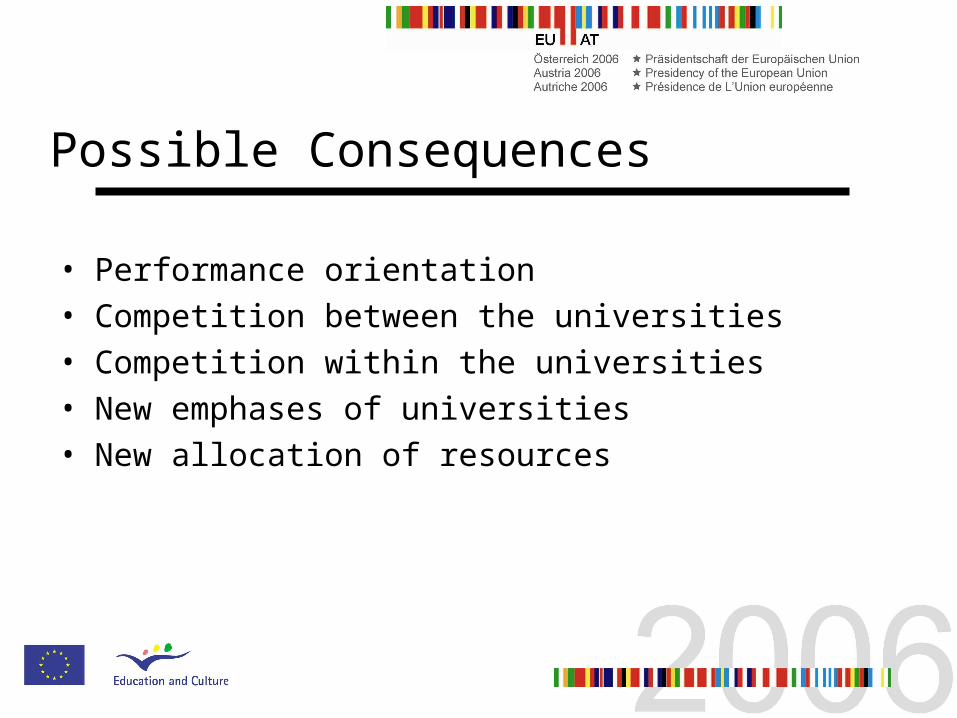

Possible Consequences

• Performance orientation• Competition between the universities• Competition within the universities• New emphases of universities• New allocation of resources

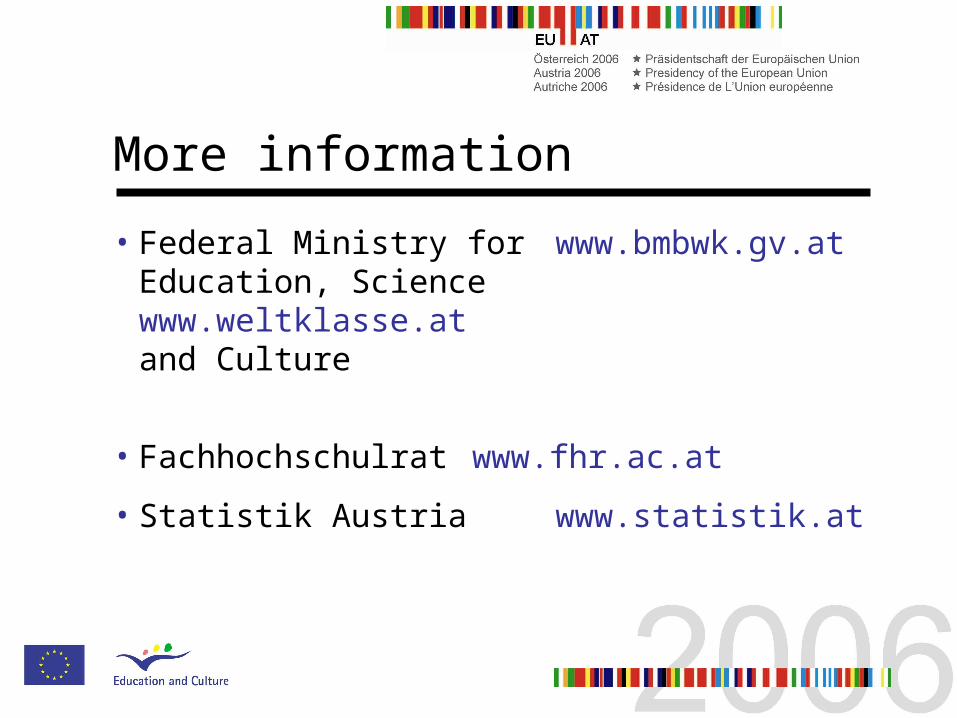

More information

• Federal Ministry for www.bmbwk.gv.at Education, Science www.weltklasse.at and Culture

• Fachhochschulrat www.fhr.ac.at

• Statistik Austria www.statistik.at