Embed Size (px)

Citation preview

HIGH SPEED BROADBAND SPECIAL EDITIONNEXT-GENERATION NETWORKS AND DEVICES, CONVERGENCE AND POLICY ANALYSIS

analysysmason.com

Inside

Introduction p2

EUR200–600 billion in high-speed broadband benefit expected for the European Union p3

Cuts to the Connecting Europe Facility: a funding disaster for high-speed broadband in Europe? p5

Does fibre to the home need a 100-inch screen? p6

Will policy and regulation of TV services in the EU start converging in the short to medium term? p7

Analysys Mason’s National Broadband experience p9

Commissioned broadband studies from Analysys Mason p9

Recent publications from Analysys Mason Research p9

About Analysys Mason p10

INTRODUCTION

High-speed broadband continues to be a very hot topic for our clients, and in this Special Edition we present a selection of articles based on our recent work in this area.First comes an article about a study we recently completed for the European Commission on Neelie Kroes’ landmark policy initiative, the Digital Agenda for Europe, in which we assessed the benefits and costs of ensuring widespread availability of high-speed broadband in Europe. We believe it is the most comprehensive study of its kind and contains something for everyone, from policy makers and operators to investors and regulators.

On the same day that this study was published, Neelie Kroes (Vice-President of the European Commission) also announced her plans for measures to cut the cost of deploying high-speed broadband, saving an estimated EUR40–60 billion across Europe. Again, Analysys Mason played a part in this major initiative, having conducted a feasibility study on potential measures that could be employed to reduce costs.

Neelie Kroes’ announcement was timely, given the well-documented issues regarding the EUR8 billion reduction in the Connecting Europe Facility, one of the EC’s important funding sources for high-speed broadband. As the second article explains, we think there are other potential sources of funding that can play an important role in helping meet the Digital Agenda for Europe targets.

The following article takes a longer-term view and considers how connected TVs support the case for fibre-to-the-home. We have teamed up with academic experts at the University of Salford to look at how ultra-HD technology is evolving and the potential implications for networks.

The last article takes the TV theme into the policy and regulatory domain, looking at the hot topic of the evolution of linear and non-linear services.

I hope you will enjoy reading this Special Edition and find these articles of interest. We welcome your feedback and encourage you to contact the authors directly if you would like to discuss any of the points they have raised, or are looking to understand how a specific issue or trend will affect your business.

To find out more about our experience and services, please visit www.analysysmason.com – you can also follow us on Twitter at @AnalysysMason.

We look forward to working with you in 2013 and beyond.

Kind regards,

Matt Yardley PartnerAnalysys Mason

2

HIGH-SPEED BROADBAND SPECIAL EDITION

EUR200–600 BILLION IN HIGH-SPEED BROADBAND BENEFIT EXPECTED FOR THE EUROPEAN UNION

As the basis for calculating the socio-economic benefit, the study considered the expected roll-out of a range of high-speed broadband networks, as well as the role of publicly funded projects. Based on an analysis of commercial viability, operators are expected make investments to provide terrestrial coverage of 30Mbit/s to 94% of European households by 2020, with satellite services expected to fill the remainder up to the Digital Agenda for Europe (DAE) coverage target of 100%.

The study also forecasts that ultrafast broadband of at least 100Mbit/s will be deployed commercially to 50% of European households. However, take-up of services on 100Mbit/s networks is expected to be 26% overall, missing the DAE target of 50% take-up. The results suggest that governments have an important role to play on both supply and demand sides if the DAE take-up target is to be met.

The network calculations undertaken as part of the study considered three scenarios for public intervention:

• Donothing,whichreliesonlyonprivateoperatorsto roll out high-speed broadband.

•Modestintervention,whichconsidersaEUR7billion public investment to leverage additional private investment.

•Majorintervention,whichconsidersaEUR50billion public investment to further leverage additional private investment.

The forecast of network deployment under the second scenario, which includes commercial deployments and some modest intervention, is shown in Figure 1. High-speed wireline technologies such as fibre and cable are shown in red, and are expected to be concentrated in the areas with densest population.

A new study from the European Commission provides a detailed forecast of the economic benefits from deploying high-speed broadband across the European Union. In total, the 27 countries that make up the EU can expect to receive cumulative benefits of between EUR200 billion and EUR600 billion in the period 2012 to 2020, representing a benefit:cost ratio of between 2.7:1 and 2.9:1. The study, entitled The socio-economic impact of bandwidth, was jointly prepared by Analysys Mason and Tech4i2 (http://www.tech4i2.com), specialist ICT policy advisers.

MATT YARDLEY

Partner

“ The study shows that investment in high-speed broadband networks is likely to deliver significant socio-economic benefits to the EU27 countries in the period up to 2020.”

Figure 2: Cumulative benefits of high-speed broadband in the EU27 countries, by scenario 2012–20 [Source: Tech4i2, 2012]

Scenario Total NGA investment (EUR billion)

Input-output benefits (EUR billion)

Jobs created (million)

Consumer surplus benefits (EUR billion)

Do nothing

76.4 181.2 1.35 26.5

Modest intervention

102.5 270.4 1.98 28.6

Major intervention

211.2 569.4 3.94 31.9

3

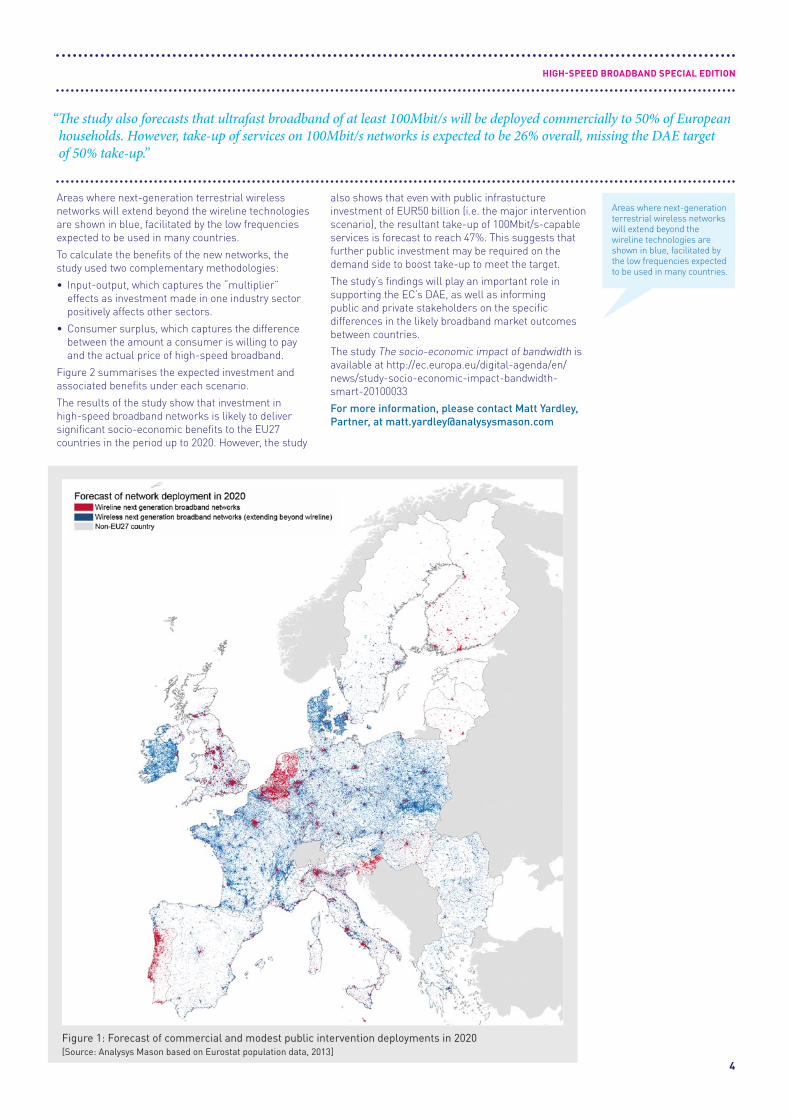

Areas where next-generation terrestrial wireless networks will extend beyond the wireline technologies are shown in blue, facilitated by the low frequencies expected to be used in many countries.

Areas where next-generation terrestrial wireless networks will extend beyond the wireline technologies are shown in blue, facilitated by the low frequencies expected to be used in many countries.

To calculate the benefits of the new networks, the study used two complementary methodologies:

• Input-output,whichcapturesthe“multiplier” effects as investment made in one industry sector positively affects other sectors.

• Consumersurplus,whichcapturesthedifference between the amount a consumer is willing to pay and the actual price of high-speed broadband.

Figure 2 summarises the expected investment and associated benefits under each scenario.

The results of the study show that investment in high-speed broadband networks is likely to deliver significantsocio-economicbenefitstotheEU27countries in the period up to 2020. However, the study

also shows that even with public infrastucture investment of EUR50 billion (i.e. the major intervention scenario), the resultant take-up of 100Mbit/s-capable servicesisforecasttoreach47%.Thissuggeststhatfurther public investment may be required on the demand side to boost take-up to meet the target.

The study’s findings will play an important role in supporting the EC’s DAE, as well as informing public and private stakeholders on the specific differences in the likely broadband market outcomes between countries.

The study The socio-economic impact of bandwidth is available at http://ec.europa.eu/digital-agenda/en/news/study-socio-economic-impact-bandwidth-smart-20100033

For more information, please contact Matt Yardley, Partner, at [email protected]

“The study also forecasts that ultrafast broadband of at least 100Mbit/s will be deployed commercially to 50% of European households. However, take-up of services on 100Mbit/s networks is expected to be 26% overall, missing the DAE target of 50% take-up.”

Figure 1: Forecast of commercial and modest public intervention deployments in 2020 [Source: Analysys Mason based on Eurostat population data, 2013]

HIGH-SPEED BROADBAND SPECIAL EDITION

4

CUTS TO THE CONNECTING EUROPE FACILITY: A FUNDING DISASTER FOR HIGH-SPEED BROADBAND IN EUROPE?

Broadband certainly lost out in the final stages of negotiation in which EUR32 billion was removed from the European Union (EU) budget. But does this really pose the end for a high-speed broadband Europe? In our view, the CEF – even at EUR9 billion – was only going to play a small role in funding additional high-speed broadband network deployment across Europe. Also, in our view, the EC had high expectations on leverage – that is, the amount of new private-sector capital that could be brought in on the back of the CEF. So, while the CEF would have played a role, it alone would not have been anywhere near enough to ensure the DAE targets are met. We estimate that the funding gap for deploying high-speed networks capable of meeting both the DAE coverage and take-up targets is about EUR60 billion (see The socio-economic impact of bandwidth at http://ec.europa.eu/digital-agenda/en/news/study-socio-economic-impact-bandwidth-smart-20100033).

There are some things that governments can do that do not require lots of direct cash investment. They can play an enabling role to reduce deployment costs, as the EC recently highlighted,1 and as the UK government is currently consulting on (regarding ‘permitted development rights’ for street cabinets and new poles).2

Other financiers, such as the European Investment Bank (EIB), are active in financing broadband deployments in rural and urban areas. The EIB has already approved EUR50 million funding for a fibre network in Haute-Savoie, France and more than EUR200 million for Reggefiber to deploy networks in smaller towns in Netherlands. It is also appraising EUR200 million of finance for a rural broadband project for Türk Telekom, and EUR8 million for the rural ‘Rain’ project in Lithuania.

However, the EIB alone cannot fund the broadband push into deep rural areas and meet the DAE targets. National governments will need to allocate funding from their own budgets, despite the obvious pressures for funding from other industry sectors. As our cost/benefit work for the EC shows, there are good economic grounds to support this allocation. Neelie Kroes, Vice-President of the EC, has requested that Member States develop national broadband plans, but progress on this front seems lacklustre – at least in some parts of Europe. Member States that move quickly could seize the upper ground, especially as there are EU funds – such as the European Regional Development Fund (ERDF) and, potentially, the Cohesion Fund – that could be used to fund high-speed broadband networks, as long as they present a compelling case.

Analysys Mason has been at the forefront of analysing the commercial and policy challenges of rural broadband for more than 15 years. We are currently advising several governments on their national broadband plans, in markets as diverse as Wales and Qatar. We have also helped clients to secure ERDF and other sources of funding to ensure their broadband projects come to fruition.1 http://www.analysysmason.com/About-Us/News/Press-releases1/High-speed-broadband-Europe-Nov2012/2 https://www.gov.uk/government/publications?publication_filter_option=consultations&departments[]=department-for-culture-media-sport

For more information, please contact Matt Yardley, Partner, at [email protected]

The budget for supporting the roll-out of new digital networks as part of the Connecting Europe Facility (CEF) was slashed from EUR9.2 billion to EUR1 billion in early February. The announced cut has prompted cries that rural broadband plans are ‘in tatters’ and that the Digital Agenda for Europe (DAE) is ‘floundering’.

MATT YARDLEY

Partner

“ The EUR8 billion cut to the Connecting Europe Facility budget needs to be set against the EUR60 billion funding gap for meeting the Digital Agenda for Europe targets.”

HIGH-SPEED BROADBAND SPECIAL EDITION

5

DOES FIBRE TO THE HOME NEED A 100-INCH SCREEN?

As manufacturers use the latest standards to sell new products and consumers expect the most up-to-date technology, the march towards higher-definition video seemsrelentless.Followingthesuccessof720and1080 (‘full HD’) standards, two new standards for ultra-HD (UHD) TV are being heralded:

• 4Kdeliversvideoataresolutionof3840×2160pixels (approximately four times the resolution of full HD) and is likely to be accompanied by an increase in frame rate, from 25 to 60fps.

• 8Kdeliversvideoataresolutionof7680×4380pixels (approximately 16 times the resolution of full HD) and is expected to increase the frame rate even further, to 120fps.

Several manufacturers, including Sony, LG and Samsung, either already have UHD TVs on sale or are due to release them. At the moment, the availability of 4K content is limited and the primary method of delivery is still to be defined (i.e. through the development of a physical disc medium and/or via the internet). The Sony TVs come with a selection of 4K videos pre-loaded on to a separate video player, which can be updated via an internet connection – but we expect such an update to take a long time on a standard broadband connection. Therefore, as this type of television set becomes more prevalent, we also expect an increase in demand for more instant delivery of UHD programming, akin to the delivery of HD content to connected TVs today.

We have considered the impact of these developments in TV definition standards on telecoms networks. Given the required data rate of UHD standards, including implementation of the latest video compression techniques (as well as some assumptions on the take-up of new standards), we have created an indicative forecast of the peak demand of a connected-TV household in the short to medium, medium to long, and long to very long term. This is shown in Figure 1.

This simple analysis is dependent on the availability of UHD TV technologies, as well as the take-up of those technologies by both content producers and consumers.

However, the analysis provides some interesting implications for network operators and policy makers investing in superfast broadband networks:

•Demand from 4K UHD TV does not necessarily require fibre to the home (FTTH). Enhanced copper networks – supported by fibre to the cabinet (FTTC) along with vectoring technology – are expected to be able to provide around 100Mbit/s to the home. If a second copper pair is available, the use of bonding and phantom mode could raise this to 200–300Mbit/s.• FTTH will be well suited to support the delivery of 8K UHD programming. Advances in pixel resolution and frame rate will mean that 8K UHD traffic is likely to outstrip the expected capabilities of copper networks. FTTH networks are able to provide connections of 1Gbit/s and more, and so will be better suited to delivering such services.• Take-up of more advanced UHD TV may be limited by non-technological constraints. There is a limit to the angular resolution that the human eye can process, beyond which there is no perceptible advantage to greater TV resolution. In order to make the increased detail visible, a larger screen is needed. The 4K sets currently available all have screen sizes over 80 inches; 8K TVs may be even bigger. Eventually the required screen size may become so great as to become an obstacle to take-up, whether due to the physical size of rooms, or the cost of super-sized TVs.• FTTH networks may be useful for large households, or for those with a number of connected TVs (our analysis above assumes one set using the latest standard, with additional sets using older standards). In such cases, fibre-on-demand products may become popular, such as those discussed here:http://www.analysysmason.com/Research/Content/Comments/Openreach-FTTP-on-demand-Jan2013-RDTW0/•Backhaul and core capacity, along with multicast technology, will continue to be essential to ensure that sufficient bandwidth can be delivered to the access network at peak times.

So, is UHD TV the ‘killer app’ that next-generation broadband networks have been waiting for? Forecast household demand certainly supports investment in new fibre technologies of some sort. Investors in FTTC technologies are likely to be vindicated in the medium term, as delivery of 4K UHD TV will make good use of their networks. FTTH investors are already playing a long game, but with widespread take-up of 8K UHD TV services likely to be required to fully exploit these networks, vindication of their decision could be some way off. In future, perhaps every home will have a 100-inch screen, but at this stage it looks like a long time before FTTH investors can fully capitalise on their connection speed advantage.

For more information, please contact Andrew Daly, Lead Consultant, at [email protected], or Professor Nigel Linge, at [email protected]

Investors in new fibre networks now consider revenue from connected TV as an essential component of their investment cases. The trend is accompanied by developments in the TV industry, with new standards in high-definition (HD) TV attracting publicity. This article, jointly written by Analysys Mason and the University of Salford, studies the evolution of the bandwidth demands of a connected-TV household and the implications for investment decisions in networks.

ANDREW DALY

Lead Consultant

“ As manufacturers use the latest standards to sell new products and consumers expect the most up-to-date technology, the march towards higher-definition video seems relentless.”

Figure 1: Indicative forecast of peak demand from an average-sized connected-TV household [Source: Analysys Mason, University of Salford]

0

10

20

30

40

50

60

70

Short term (HD) Medium term (4K) Long term (8K)

Hou

seho

ld d

eman

d (M

bit/

s)

0

50

100

150

200

250

300

350

Short to medium term(HD)

Medium to long term(4K)

Long to very long term(8K)

Hou

seho

ld d

eman

d (M

bit/

s)

HIGH-SPEED BROADBAND SPECIAL EDITION

6

WILL POLICY AND REGULATION OF TV SERVICES IN THE EU START CONVERGING IN THE SHORT TO MEDIUM TERM?

The European Commission (EC) and the UK will soon launch independent consultations on the policy and regulation of connected TV services. Both expect to present their conclusions by the end of 2013 after extensive discussions with stakeholders.Connected TV is still a relatively small part of the TV ‘ecosystem’, yet one that is growing rapidly. Changing the framework could be considered premature, but giventhatECregulationcantake5–7yearstodevelop,starting the debate now is perhaps appropriate. Other countries are expected to follow suit.

Background

In the last five years, there has been steady growth in the consumption and revenue of TV services – both in traditional linear TV, with moderate, single-digit growth, as well as in non-linear TV, which has grown exponentially (examples include catch-up TV, video on demand, subscription video on demand and professional video online). Between 2009 and 2010, the three major European Union (EU) economies all experienced increases in online TV revenues: the UK and France had 100% growth, while Germany had 35%.

Established broadcasters and TV platforms, as well as new TV/video aggregators and over-the-top players,

are all providing innovative products and services to consumers in a bid to offer preferred films, sports and TV programmes on any device, anytime, anywhere. Major operators (terrestrial, cable, satellite, fixed and, increasingly, mobile) have lent their support and investment to this focus on innovation.

New players are gaining significant market share of non-linear TV services and technologies (some analysts estimate that 50% of non-traditional TV services in the US in 2011 were from new over-the-top offerings), which could have substantial impact in the long term, depending on the reaction from established linear TV broadcasters. However, despite the dynamic development in these non-linear services, their rapid adoption and consumption, and the resulting pressure on associated costs and investments in networks and devices, the actual proportion of viewing remained relatively small when compared to linear TV. Based on data from the European Audiovisual Observatory (2013), it is estimated that online revenue accounted for only 1.3% of total TV revenue in the UK, 0.9% in France and 0.6% in Germany in 2010. This shows some moderate progress, when compared to less than 1% for all three markets in 2009. Total revenue for online TV in 2010 amounted to a modest EUR330 million in the top five EU countries (EAO, 2012).

LLUÍS BORRELL

Partner and Head of Media

0

10

20

30

40

50

60

70

Short term (HD) Medium term (4K) Long term (8K)

Hou

seho

ld d

eman

d (M

bit/

s)

0.00

50.00

100.00

150.00

200.00

250.00

300.00

350.00

1 2 3 4 5

IT

GB

FR

ES

DE

EUR

mill

ions

0

50

100

150

200

250

300

350

2006 2007 2008 2009 2010

EUR

mill

ions

Figure 1: Total online TV revenue growth in the top five European markets [Source: European Audiovisual Observatory, Analysys Mason]

HIGH-SPEED BROADBAND SPECIAL EDITION

7

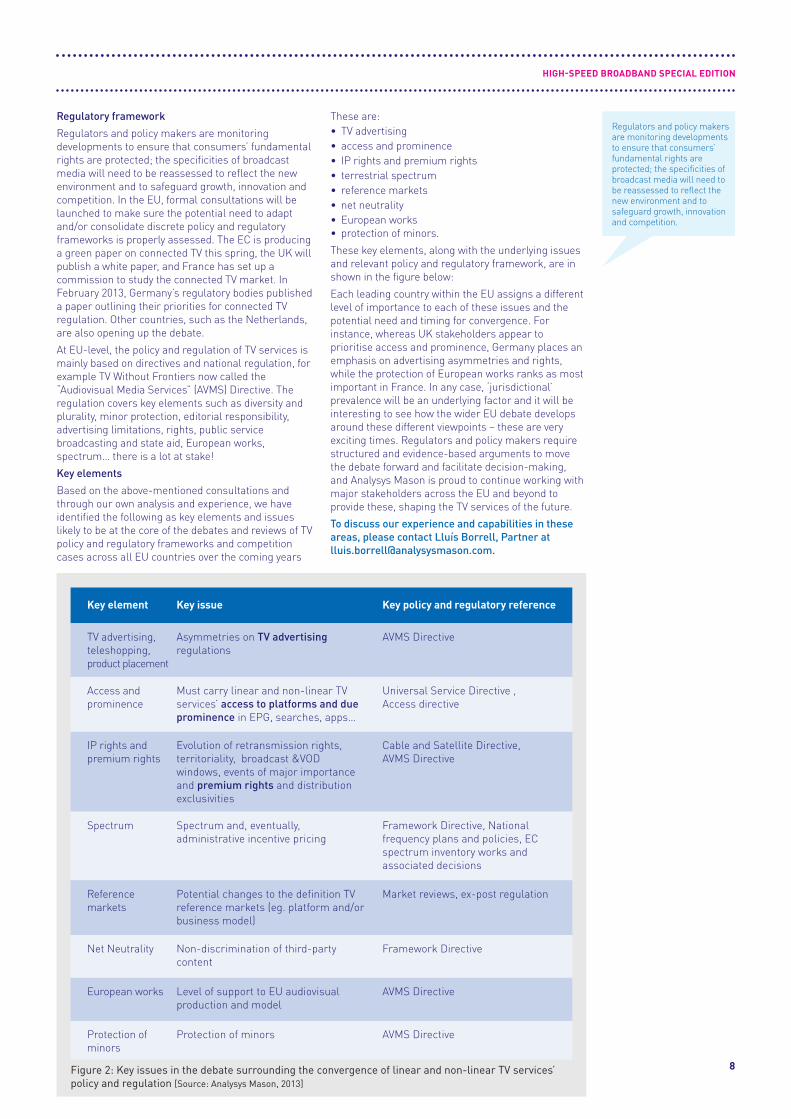

Regulators and policy makers are monitoring developments to ensure that consumers’ fundamental rights are protected; the specificities of broadcast media will need to be reassessed to reflect the new environment and to safeguard growth, innovation and competition.

Regulatory framework

Regulators and policy makers are monitoring developments to ensure that consumers’ fundamental rights are protected; the specificities of broadcast media will need to be reassessed to reflect the new environment and to safeguard growth, innovation and competition. In the EU, formal consultations will be launched to make sure the potential need to adapt and/or consolidate discrete policy and regulatory frameworks is properly assessed. The EC is producing a green paper on connected TV this spring, the UK will publish a white paper, and France has set up a commission to study the connected TV market. In February 2013, Germany’s regulatory bodies published a paper outlining their priorities for connected TV regulation. Other countries, such as the Netherlands, are also opening up the debate.

At EU-level, the policy and regulation of TV services is mainly based on directives and national regulation, for example TV Without Frontiers now called the “AudiovisualMediaServices”(AVMS)Directive.Theregulation covers key elements such as diversity and plurality, minor protection, editorial responsibility, advertising limitations, rights, public service broadcasting and state aid, European works, spectrum… there is a lot at stake!

Key elements

Based on the above-mentioned consultations and through our own analysis and experience, we have identified the following as key elements and issues likely to be at the core of the debates and reviews of TV policy and regulatory frameworks and competition cases across all EU countries over the coming years

These are:• TVadvertising• accessandprominence• IPrightsandpremiumrights• terrestrialspectrum• referencemarkets• netneutrality• Europeanworks • protectionofminors.

These key elements, along with the underlying issues and relevant policy and regulatory framework, are in shown in the figure below:

Each leading country within the EU assigns a different level of importance to each of these issues and the potential need and timing for convergence. For instance, whereas UK stakeholders appear to prioritise access and prominence, Germany places an emphasis on advertising asymmetries and rights, while the protection of European works ranks as most important in France. In any case, ‘jurisdictional’ prevalence will be an underlying factor and it will be interesting to see how the wider EU debate develops around these different viewpoints – these are very exciting times. Regulators and policy makers require structured and evidence-based arguments to move the debate forward and facilitate decision-making, and Analysys Mason is proud to continue working with major stakeholders across the EU and beyond to provide these, shaping the TV services of the future.

To discuss our experience and capabilities in these areas, please contact Lluís Borrell, Partner at [email protected].

HIGH-SPEED BROADBAND SPECIAL EDITION

8

Key element

TV advertising, teleshopping, product placement

Key issue Key policy and regulatory reference

Asymmetries on TV advertising regulations

AVMS Directive

IP rights and premium rights

Access and prominence

Spectrum

Evolution of retransmission rights, territoriality, broadcast &VOD windows, events of major importance and premium rights and distribution exclusivities

Cable and Satellite Directive, AVMS Directive

Must carry linear and non-linear TV services’ access to platforms and due prominence in EPG, searches, apps…

Universal Service Directive , Access directive

Spectrum and, eventually, administrative incentive pricing

Framework Directive, National frequency plans and policies, EC spectrum inventory works and associated decisions

Figure 2: Key issues in the debate surrounding the convergence of linear and non-linear TV services’ policy and regulation [Source: Analysys Mason, 2013]

Net Neutrality

Protection of minors

European works

Reference markets

Non-discrimination of third-party content

Framework Directive

Protection of minors AVMS Directive

Level of support to EU audiovisual production and model

AVMS Directive

Potential changes to the definition TV reference markets (eg. platform and/or business model)

Market reviews, ex-post regulation

•The socio-economic impact of bandwidth - A report for the European Commission providing a detailed forecast of the economic benefits from deploying high-speed broadband across the European Unionhttp://ec.europa.eu/digital-agenda/en/news/study-socio-economic-impact-bandwidth-smart-20100033

•Support for the preparation of an impact assessment to accompany an EU initiative on reducing the costs of high-speed broadband infrastructure deployment - A report for the European Commission to assess the potential impact of five regulatory measures on reducing the cost of deploying high-speed broadband infrastructure across Europehttp://ec.europa.eu/digital-agenda/en/news/support-preparation-impact-assessment-accompany-eu-initiative-reducing-costs-high-speed

•Guide to Broadband Investment - Compiled for and published by the European Commission, providing a step-by-step process for planning broadband investment effectivelyhttp://ec.europa.eu/regional_policy/sources/docgener/presenta/ broadband2011/broadband2011_en.pdf

•Policy orientations to reach Digital Agenda - The report, commissioned by Telefónica and Telecom Italia, provides an overview of next-generation access (NGA) deployment and take-up in all European Union (EU) Member States, including forecasts to 2020.http://www.analysysmason.com/Research/Content/Reports/ Policy-orientations-to-reach-European-Digital-Agenda-targets/

•Evaluation of the market, business and financial aspects for the development of broadband access for FEMIP countries - A comprehensive study for the European Investment Bank (EIB) to make broadband market assessments and evolution forecasts for nine countries in the MENA regionhttp://www.eib.org/infocentre/publications/all/femip-study-development-of-broadband-access-for-femip-countries.htm

•Developing successful Public–Private Partnerships to foster investment in universal broadband networks - A report on behalf of the International Telecommunications Union (ITU), highlighting the best practices used by public/private partnerships (PPPs) to successfully implement universal broadband projects.http://www.itu.int/ITU-D/treg/Events/Seminars/GSR/GSR12/ documents/GSR12_BBReport_Yardley_PPP_7.pdf

COMMISSIONED BROADBAND STUDIES FROM ANALYSYS MASON

Broadband has been identified by central governments, and regional and local authorities as being central to underpinning future economic growth and social welfare. Operators are investing in high-speed broadband networks to support the continually increasing demand for internet-delivered content.

We work with clients to help them understand the role they can play in broadband stimulation and market development, and how to build strategies and implementation plans to ensure maximum benefits are realised.

Our experience includes:

•Afeasibilitystudyfornationwidefibre–fortheIDAinSingapore

•PreparinganationalbroadbandplaninThailandtoaddress existing supply- and demand-side barriers to the development of the broadband market

•AssessedthecostsoffibredeploymentintheUKforthe Broadband Stakeholder Group (BSG) covering fibre-to-the-cabinet and fibre-to-the-home networks

•Undertakingastudyonultra-fastbroadbandinFrancefora consortium of six public bodies including two Ministries and the telecoms and media regulators

•Developinganoperationalcostmodelfortheultrafastbroadband network for Telecom New Zealand and reviewing their fibre-to-the- home deployment plan

ANALYSYS MASON’S NATIONAL BROADBAND EXPERIENCE

•FixedInternettrafficworldwide:forecastsandanalysis2013–2018

•Own-buildnext-generationnetworkstrategiesforLLUoperators

•G.FastandFTTdp:assessingthecosts,feasibilityandinterest

•CablebroadbandstandardsinEuropeandtheUSA:strategiesto2020

•DoDSLaccelerationtechnologieshavepotentialinemergingmarkets?

For more information see www.analysysmason.com/FixedNetworks

RECENT PUBLICATIONS FROM ANALYSYS MASON RESEARCH INCLUDE:

HIGH-SPEED BROADBAND SPECIAL EDITION

9

Consulting Research For more than 25 years, our consultants have been bringing the benefits of applied intelligence to enable clients to make the most of their opportunities

Our clients in the telecoms, media and technology (TMT) sectors operate in dynamic markets where change is constant. We help shape their understanding of the future so they can thrive in these demanding conditions. To do that, we have developed rigorous methodologies that deliver real results for clients around the world.

Our focus is exclusively on TMT. We support multi-billion dollar investments, advise clients on regulatory matters, provide spectrum valuation and auction support, and advise on operational performance, business planning and strategy. Such projects result in a depth of knowledge and a range of expertise that sets us apart.

We look beyond the obvious to understand a situation from a client’s perspective. Most importantly, we never forget that the point of consultancy is to provide appropriate and practical solutions. We help clients solve their most pressing problems, enabling them to go farther, faster and achieve their commercial objectives.

Analysys Mason’s research service covers consumer and enterprise services, as well as the software, infrastructure and technology underlying those services.

The division consists of a specialised team of analysts, who provide dedicated coverage of TMT issues and trends. Our experts understand not only the complexities of the TMT sectors, but the unique challenges of companies, regulators and other stakeholders operating in such a dynamic industry.

Our 25 research programmes cover the following five key areas:

• consumerservices

• enterpriseservices

• networktechnologies

• telecomssoftware

• regionalmarkets.

Our programmes offer a mixture of qualitative and quantitative market intelligence. The result is an essential resource for strategic planning, investment, marketing and benchmarking.

Custom research We also deliver tailored research that addresses specific business needs for a wide range of organisations.

We deliver tailored research that addresses specific business needs for a wide range of operators, vendors, industry bodies and regulators within the telecoms, media and technology (TMT) sectors. Our comprehensive knowledge of the TMT industries draws on a large base of market data that we have collected over 25 years, refreshed through continuous research and custom consulting project assignments.

Analysys Mason contact:

Matt Yardley, [email protected]+44 845 600 5244

ABOUT ANALYSYS MASON

HIGH-SPEED BROADBAND SPECIAL EDITION

10