Embed Size (px)

Citation preview

Heterogeneous Risk Perceptions in Insurance Markets

Johannes Spinnewijn(based on joint work with Philipp Kircher)

London School of Economics

May 2011

Spinnewijn (LSE) Heterogeneous Risk Perceptions May 2011 1 / 37

Heterogeneity in Insurance Markets

People’s demand for insurance depends on the risks they face andtheir aversion with respect to these risks.

People face different risks and have different preferences.

Private information about risks leads to adverse selection (Akerlof /Rothschild & Stiglitz)⇒ rationale for government intervention

BUT little empirical evidence for adverse selection... (Chiappori,Salanié,...)

... because of heterogeneity in preferences (Cohen, Einav,Finkelstein,...)⇒ reduced gains from government intervention

Spinnewijn (LSE) Heterogeneous Risk Perceptions May 2011 2 / 37

Heterogeneity in Perceptions

People differ in their perceptions of risks.Paul Slovic: "The perception of risk is inherently subjective."

Heterogeneity in perceived relative to actual risks:1 distorts the demand for insurance; perception bias distorts theperceived value of insurance.

2 reduces use of private info about true risk; markets may become lessadversely selected.

What if heterogeneity in choices is driven by heterogeneity inperceptions rather than heterogeneity in preferences?

Spinnewijn (LSE) Heterogeneous Risk Perceptions May 2011 3 / 37

Overview: Three Questions

Previous work (Spinnewijn 2010):

1. Positive: How do insurance companies react to heterogeneity inperceptions?

Today:

2. Normative: How does heterogeneity in perceptions affect welfare?

3. Empirical: How can we identify preferences vs. perceptions? (jointwith Philipp Kircher)

Spinnewijn (LSE) Heterogeneous Risk Perceptions May 2011 4 / 37

Welfare: Demand and Cost of Insurance

Follow suffi cient statistics approach to estimate the welfare cost ofinsurance (Einav, Finkelstein and Cullen 2010).

Estimate demand for insurance and cost of insuring the insured.Primitives underlying demand and cost are irrelevant.

With heterogeneity in perceptions, the demand does not capture thevalue of insurance - assuming welfare depends on true expected utility

One additional statistic; ratio of heterogeneity in perceptions vs.heterogeneity in preferences.

Use framework for policy evaluation and calibration using estimatesfrom Einav et al.

Spinnewijn (LSE) Heterogeneous Risk Perceptions May 2011 5 / 37

Welfare: Policy Conclusions

Unadjusted formula understates the cost of adverse selection.

Insured are too pessimistic on average, uninsured are too optimistic onaverage.Value of universal mandate unambiguously increases.Price subsidies are less effective, being constrained by people’sperceived value of insurance.

Informing individuals about their misperceptions has an ambiguouseffect.

People make better choices, but market becomes more adverselyselected.Only provide information regarding the net-value of insurance.

Spinnewijn (LSE) Heterogeneous Risk Perceptions May 2011 6 / 37

Identification of Perceptions and Preferences

Are choices driven by perceptions or preferences?

Previous empirical work either uses surveyed risk perceptions or ignoresrisk perceptions.

We propose an identification approach based on choice data:

MWP for insurance depends only on risk perceptions close to fullinsurance.

Level of (individual) demand curve - evaluated at full insurance -identifies risk perception

~ buy full insurance at actuarially fair price, regardless of risk preferences(Mossin 1968, Arrow 1970)

Slope of (individual) demand curve - evaluated at full insurance -identifies risk aversion.

Spinnewijn (LSE) Heterogeneous Risk Perceptions May 2011 7 / 37

Identification: Using Price Variation

Approach applies to MWP for standard contracts with copays anddeductibles.

Approach exploits risk-neutrality implication of EUT close to fullinsurance.

Approach complements identification approach based on riskrealizations - assuming accurate risk perceptions (Cohen, Einav,Finkelstein, ...)

Spinnewijn (LSE) Heterogeneous Risk Perceptions May 2011 8 / 37

Outline

1 Welfare

SetupSuffi cient Statistics ApproachPolicy Analysis

2 Identification

SetupBinary RiskRobustness

Spinnewijn (LSE) Heterogeneous Risk Perceptions May 2011 9 / 37

Setup

Model heterogeneity in preferences and risks. Allow perceived risks todiffer from actual risk.

Value and cost of insurance:

v = π︸︷︷︸’risk’-term

+ r︸︷︷︸’preference’-term

and c = π.

Perceived value of insurance:

v = π + r + ε︸︷︷︸’noise’-term

,with E (ε = 0) .

Example: Individual i has CARA preferences facing a normal loss.Value and cost of insurance:

vi = µxi︸︷︷︸=πi

+ ηiσ2xi /2︸ ︷︷ ︸=ri

and ci = µxi︸︷︷︸=πi

.

ε could capture misperceptions about µxi or σ2xi .

Spinnewijn (LSE) Heterogeneous Risk Perceptions May 2011 10 / 37

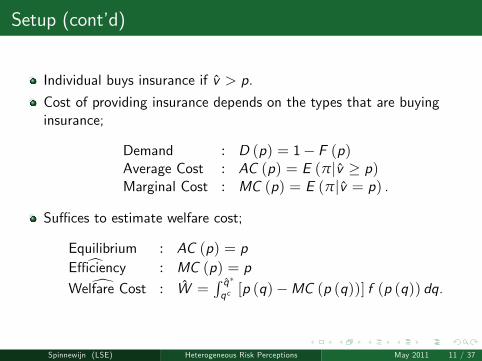

Setup (cont’d)

Individual buys insurance if v > p.

Cost of providing insurance depends on the types that are buyinginsurance;

Demand : D (p) = 1− F (p)Average Cost : AC (p) = E (π|v ≥ p)Marginal Cost : MC (p) = E (π|v = p) .

Suffi ces to estimate welfare cost;

Equilibrium : AC (p) = pEfficiency : MC (p) = p

Welfare Cost : W =∫ q∗qc [p (q)−MC (p (q))] f (p (q)) dq.

Spinnewijn (LSE) Heterogeneous Risk Perceptions May 2011 11 / 37

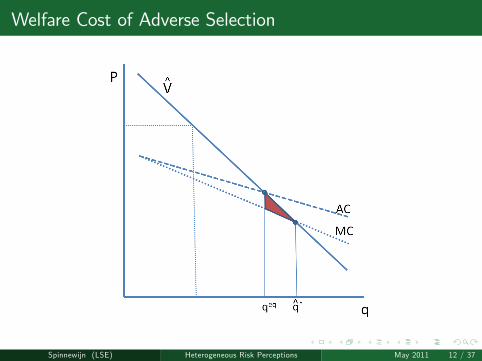

Welfare Cost of Adverse Selection

Spinnewijn (LSE) Heterogeneous Risk Perceptions May 2011 12 / 37

Heterogeneity in Perceptions

Perceptions determine the insurance choice, but not the insurancevalue.

While the price reflects the marginal willingness to pay,

p = E (v + ε|v + ε = p) ,

the true marginal value equals

MV (p) +MC (p) = E (v |v + ε = p) .

Hence, the (marginal) bias from using the demand function toevaluate welfare equals

MB (p) = E (ε|v + ε = p) .

Since ε determines the willingness to pay, the average bias will varyacross individuals with different willingness to pay.

Spinnewijn (LSE) Heterogeneous Risk Perceptions May 2011 13 / 37

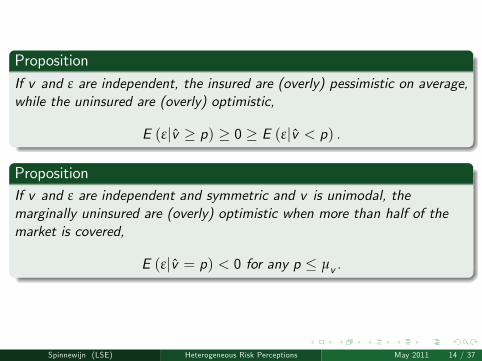

PropositionIf v and ε are independent, the insured are (overly) pessimistic on average,while the uninsured are (overly) optimistic,

E (ε|v ≥ p) ≥ 0 ≥ E (ε|v < p) .

PropositionIf v and ε are independent and symmetric and v is unimodal, themarginally uninsured are (overly) optimistic when more than half of themarket is covered,

E (ε|v = p) < 0 for any p ≤ µv .

Spinnewijn (LSE) Heterogeneous Risk Perceptions May 2011 14 / 37

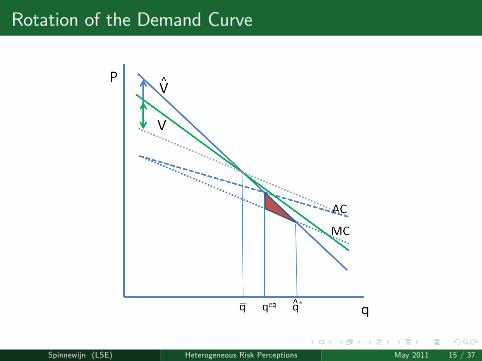

Rotation of the Demand Curve

Spinnewijn (LSE) Heterogeneous Risk Perceptions May 2011 15 / 37

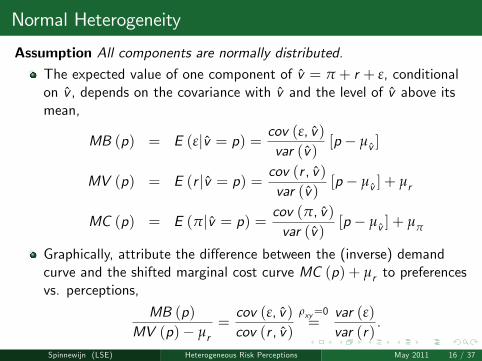

Normal Heterogeneity

Assumption All components are normally distributed.The expected value of one component of v = π + r + ε, conditionalon v , depends on the covariance with v and the level of v above itsmean,

MB (p) = E (ε|v = p) = cov (ε, v)var (v)

[p − µv ]

MV (p) = E (r |v = p) = cov (r , v)var (v)

[p − µv ] + µr

MC (p) = E (π|v = p) = cov (π, v)var (v)

[p − µv ] + µπ

Graphically, attribute the difference between the (inverse) demandcurve and the shifted marginal cost curve MC (p) + µr to preferencesvs. perceptions,

MB (p)MV (p)− µr

=cov (ε, v)cov (r , v)

ρxy=0=

var (ε)var (r)

.

Spinnewijn (LSE) Heterogeneous Risk Perceptions May 2011 16 / 37

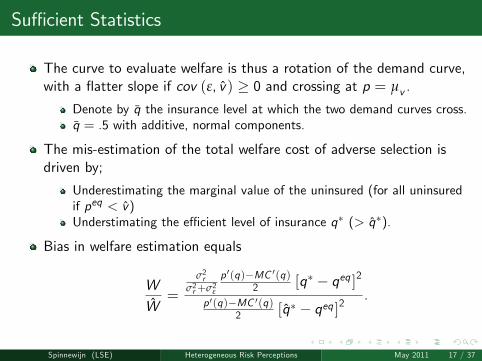

Suffi cient Statistics

The curve to evaluate welfare is thus a rotation of the demand curve,with a flatter slope if cov (ε, v) ≥ 0 and crossing at p = µv .

Denote by q the insurance level at which the two demand curves cross.q = .5 with additive, normal components.

The mis-estimation of the total welfare cost of adverse selection isdriven by;

Underestimating the marginal value of the uninsured (for all uninsuredif peq < v)Understimating the effi cient level of insurance q∗ (> q∗).

Bias in welfare estimation equals

W

W=

σ2rσ2r+σ2ε

p ′(q)−MC ′(q)2 [q∗ − qeq ]2

p ′(q)−MC ′(q)2 [q∗ − qeq ]2

.

Spinnewijn (LSE) Heterogeneous Risk Perceptions May 2011 17 / 37

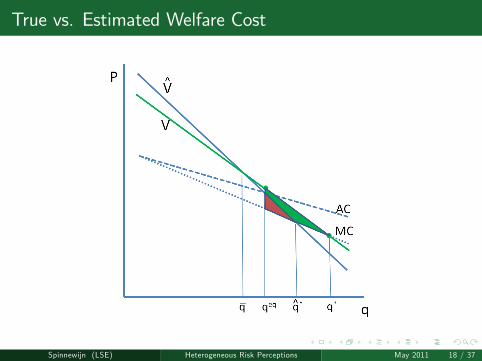

True vs. Estimated Welfare Cost

Spinnewijn (LSE) Heterogeneous Risk Perceptions May 2011 18 / 37

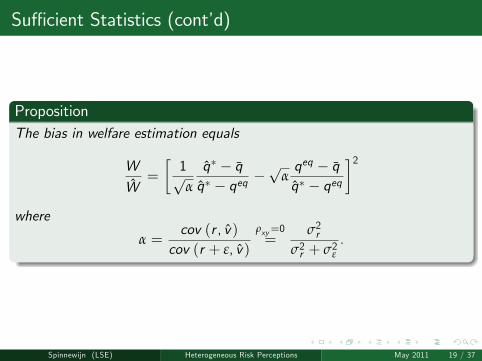

Suffi cient Statistics (cont’d)

PropositionThe bias in welfare estimation equals

W

W=

[1√α

q∗ − qq∗ − qeq −

√αqeq − qq∗ − qeq

]2where

α =cov (r , v)

cov (r + ε, v)

ρxy=0=

σ2rσ2r + σ2ε

.

Spinnewijn (LSE) Heterogeneous Risk Perceptions May 2011 19 / 37

Discussion

With no average bias, only one additional statistic is needed.

α captures relative importance of value-related drivers of demand.

The welfare cost is under-estimated when q ≤ qeq < q∗.Average optimistic bias lowers q.When q = qeq , the mistake W

W= 1

α (≥ 1) is decreasing in α.

When q = q∗, the mistake WW= α (≤ 1) is increasing in α.

Desired direction of insurance coverage may be opposite.

e.g., q is relatively large and adverse selection (q∗ < qeq < q∗)e.g., q is relatively small and advantageous seleciton (q∗ < qeq < q∗)

Spinnewijn (LSE) Heterogeneous Risk Perceptions May 2011 20 / 37

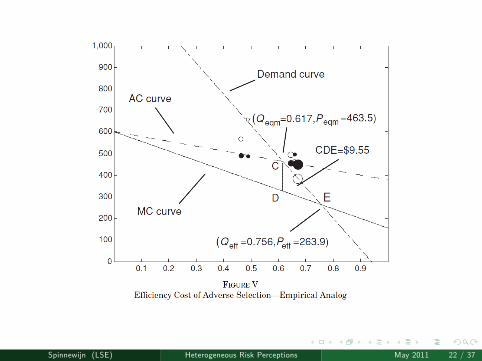

Einav, Finkelstein and Cullen, QJE 2010

Employer-provided health insurance in Alcoa, a multi-nationalproducer of aluminium.

Employees face same set of coverage options, but at different prices indifferent sections of the company.

Sample of 3,779 salaried employees who chose between two options,with and without a deductible.

Spinnewijn (LSE) Heterogeneous Risk Perceptions May 2011 21 / 37

Spinnewijn (LSE) Heterogeneous Risk Perceptions May 2011 22 / 37

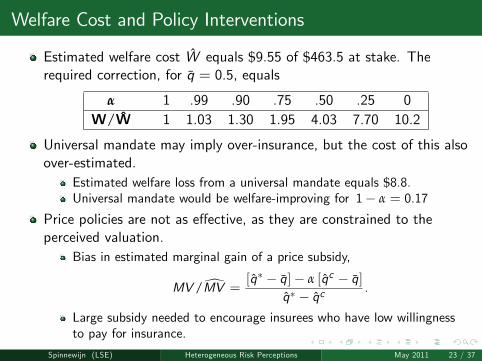

Welfare Cost and Policy Interventions

Estimated welfare cost W equals $9.55 of $463.5 at stake. Therequired correction, for q = 0.5, equals

α 1 .99 .90 .75 .50 .25 0W/W 1 1.03 1.30 1.95 4.03 7.70 10.2

Universal mandate may imply over-insurance, but the cost of this alsoover-estimated.

Estimated welfare loss from a universal mandate equals $8.8.Universal mandate would be welfare-improving for 1− α = 0.17

Price policies are not as effective, as they are constrained to theperceived valuation.

Bias in estimated marginal gain of a price subsidy,

MV/MV =[q∗ − q]− α [qc − q]

q∗ − qc .

Large subsidy needed to encourage insurees who have low willingnessto pay for insurance.

Spinnewijn (LSE) Heterogeneous Risk Perceptions May 2011 23 / 37

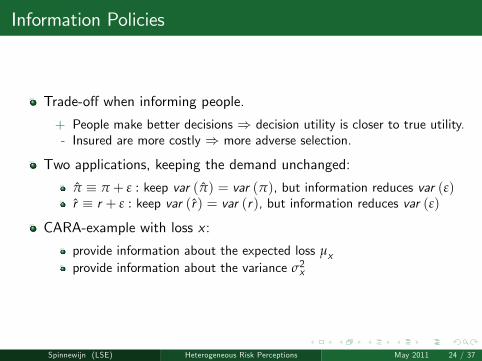

Information Policies

Trade-off when informing people.

+ People make better decisions ⇒ decision utility is closer to true utility.- Insured are more costly ⇒ more adverse selection.

Two applications, keeping the demand unchanged:

π ≡ π + ε : keep var (π) = var (π), but information reduces var (ε)r ≡ r + ε : keep var (r) = var (r), but information reduces var (ε)

CARA-example with loss x :

provide information about the expected loss µxprovide information about the variance σ2x

Spinnewijn (LSE) Heterogeneous Risk Perceptions May 2011 24 / 37

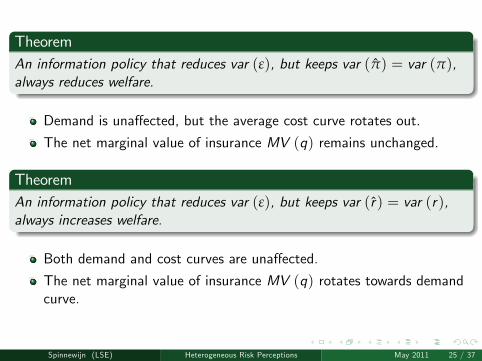

TheoremAn information policy that reduces var (ε), but keeps var (π) = var (π),always reduces welfare.

Demand is unaffected, but the average cost curve rotates out.

The net marginal value of insurance MV (q) remains unchanged.

TheoremAn information policy that reduces var (ε), but keeps var (r) = var (r),always increases welfare.

Both demand and cost curves are unaffected.

The net marginal value of insurance MV (q) rotates towards demandcurve.

Spinnewijn (LSE) Heterogeneous Risk Perceptions May 2011 25 / 37

Identification of Preferences vs. Perceptions

To what extent are observed choices driven by preferences or perceptions?

Clear identification problem:

Manski (2004): "I have concluded that econometric analysis of decisionmaking with partial information cannot prosper on choice data alone."

Previous work: use choice data to identify preferences and

Either assume rational expectations, estimated using risk realizations(Cohen, Einav, Finkelstein,...)Or use survey data to complement choice data (Manski et al., Fang &Silverman 2008)

Our approach: identify region where choices depend on riskperceptions only, i.e., at full insurance.

Spinnewijn (LSE) Heterogeneous Risk Perceptions May 2011 26 / 37

Binary Setup

Individual i risks to lose L with probability πi .

Her perception of this risk equals πi .Her preference is represented by Bernouilli function ui (·) ≡ u (·|ri ).

Individual i chooses contract from a menu of contracts {(qj ,Pj )}qj = insurance coverage, Pj = insurance premium.Resulting payoffs are mg = −P and mb = − (L− q)− PConsider a linear premium P (q) = p0 + pq. Let pi (q) denote theprice at which individual i buys q units of coverage.

Spinnewijn (LSE) Heterogeneous Risk Perceptions May 2011 27 / 37

Individual’s Demand for Insurance

Individual i chooses q to maximize her perceived expected utility,

Ui = maxq(1− πi ) ui (mg (q,P (q))) + πiui (mb (q,P (q))) .

Her perceived expected utility depends on both on her risk perceptionπi and preference ri .

What can we learn from observing an individual’s demand curvepi (q)?

Spinnewijn (LSE) Heterogeneous Risk Perceptions May 2011 28 / 37

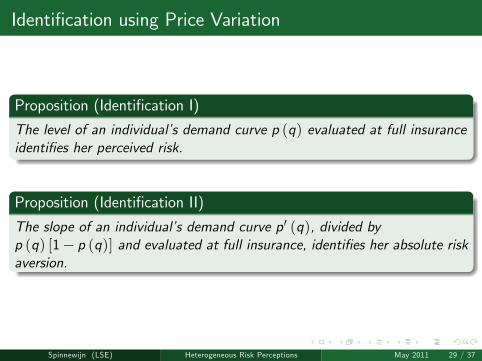

Identification using Price Variation

Proposition (Identification I)

The level of an individual’s demand curve p (q) evaluated at full insuranceidentifies her perceived risk.

Proposition (Identification II)

The slope of an individual’s demand curve p′ (q), divided byp (q) [1− p (q)] and evaluated at full insurance, identifies her absolute riskaversion.

Spinnewijn (LSE) Heterogeneous Risk Perceptions May 2011 29 / 37

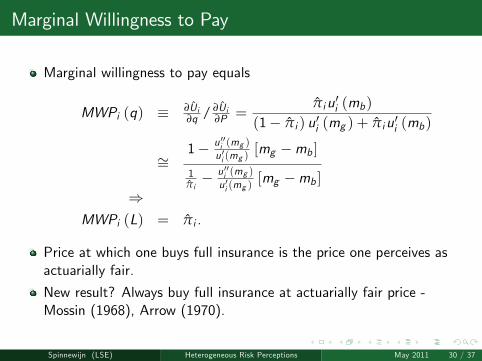

Marginal Willingness to Pay

Marginal willingness to pay equals

MWPi (q) ≡ ∂Ui∂q / ∂Ui

∂P =πiu′i (mb)

(1− πi ) u′i (mg ) + πiu′i (mb)

∼=1− u ′′i (mg )

u ′i (mg )[mg −mb ]

1πi− u ′′i (mg )

u ′i (mg )[mg −mb ]

⇒MWPi (L) = πi .

Price at which one buys full insurance is the price one perceives asactuarially fair.

New result? Always buy full insurance at actuarially fair price -Mossin (1968), Arrow (1970).

Spinnewijn (LSE) Heterogeneous Risk Perceptions May 2011 30 / 37

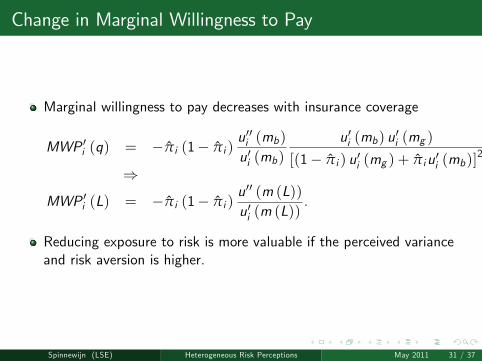

Change in Marginal Willingness to Pay

Marginal willingness to pay decreases with insurance coverage

MWP ′i (q) = −πi (1− πi )u′′i (mb)u′i (mb)

u′i (mb) u′i (mg )

[(1− πi ) u′i (mg ) + πiu′i (mb)]2

⇒MWP ′i (L) = −πi (1− πi )

u′′ (m (L))u′i (m (L))

.

Reducing exposure to risk is more valuable if the perceived varianceand risk aversion is higher.

Spinnewijn (LSE) Heterogeneous Risk Perceptions May 2011 31 / 37

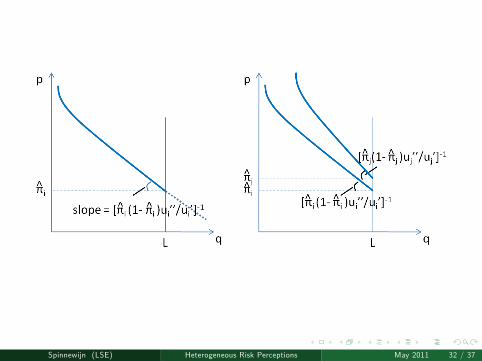

Spinnewijn (LSE) Heterogeneous Risk Perceptions May 2011 32 / 37

Continuous Risks: Copays and Deductibles

An individual risks to lose x ∈ [0, L] with perceived distr. Fπ(x).

Consider a contract c = (D, α,P).

Below the deductible D, the individual bears the entire risk.Above the deductible, the individual bears a share α of the risk.

The risk preference and perceived risk distribution could be identifiedusing price variation. Evaluated at a zero copay α = 0,

1 the willingness to increase the deductible D to reduce the copay αequals

MRSD ,αi (D, 0) ≡ ∂Ui∂α

/∂Ui∂D

= E (x −D |x ≥ D) .

2 the change in the willingness to pay equals

∂MWPαi (0, 0)

∂α=u′′i (m (c))u′i (m (c))

Eπi

[x2]−[Eπi x

]2.

Spinnewijn (LSE) Heterogeneous Risk Perceptions May 2011 33 / 37

Risk-Neutrality for Small Stakes

Our approach exploits risk-neutrality implication of EUT close to fullinsurance.Some empirical evidence suggests risk aversion for small stakes.

First-order risk aversion makes approach invalid.Example: loss aversion a la Koszegi and Rabin,

MWPi (L) = πi +µi − 1

u′i (m (L))(1− πi ) πi .

⇒ wrongly attribute loss aversion µi to pessimism πi

d πidµi|MWPi (L),µi=1 =

(1− πi ) πiu′i (m (L))

Attributing differences in MWP to heterogeneity in EUT risk aversionri seems worse,

drid πi|MWPi (q),πi=πi = −

1− ri [mg (q)−mb (q)]πi (1− πi ) [mg (q)−mb (q)]

.

Spinnewijn (LSE) Heterogeneous Risk Perceptions May 2011 34 / 37

Identification using Risk Realizations

Approach is to use distribution of risk realizations D (x) to estimatedistribution of ex ante risk types Hπ and insurance choices toestimate distribution of risk preferences. (Cohen and Einav 2007,Einav et al. 2010,...)

Two strong identifying assumptions are required1 Relating (ex post) risk realizations to (ex ante) risk types.2 Relating true risk types to perceived risk types.

Two approaches are complementary:

Require different data and identifying assumptions.Allows comparing perceived and actual risk types.

Spinnewijn (LSE) Heterogeneous Risk Perceptions May 2011 35 / 37

Identifying ex Ante Risk Types

Proposition

If for some Fπi ,Fπj ∈ F and α ∈ (0, 1) , there exists Fπk ∈ F such thatαFπi (m) + (1− α)Fπj (m) = Fπk (m) for all m, identification of Hπ isimpossible.

Trivially satisfied for a binary risks; απi + (1− α)πj = πk .

Identification rests on difference between empirical distribution acrosspopulation and assumed distribution of an individual’s risk.

Proposition

When Hπ is unknown and D (x |q) is increasing in FOSD-sense in q,homogeneity in risk-averse preferences cannot be excluded, even whenperceptions are accurate.

Spinnewijn (LSE) Heterogeneous Risk Perceptions May 2011 36 / 37

Conclusion

Risk perceptions seem important, but have been ignored in literatureanalyzing adverse selection.

Policy recommendations are very different when heterogeneity in riskperceptions rather than preferences drives people’s insurance choices.

Risk perceptions can be seperated from risk preferences using pricevariation.

Spinnewijn (LSE) Heterogeneous Risk Perceptions May 2011 37 / 37