Embed Size (px)

Citation preview

Heterogeneous Agents in Finance : different heuristics and different representations of problems

Massimo Egidi Luiss University [email protected]

Prepared for The Conference on Quantitative Behavioral Finance, Nice Dec. 8-11, 2010

Heterogeneous Agents in Finance : different heuristics and different representations of problems

“Economics and finance are witnessing an important paradigm shift, from a representative, rational agent approach towards a behavioral, agent-based approach in which markets are populated with boundedly rational, heterogeneous agents using rule of thumb strategies. “ (Cars Hommes)

Heterogeneous Agents in Finance : different heuristics and different representations of problems

Simon built the idea of bounded rationality on close observation of the behavior of employees and managers in large organizations. During the 1950s and early 1960s, he took part in numerous collaborations and research projects at the Graduate School of Industrial Administration of Carnegie Mellon, among them a study of decision making under uncertainty conducted jointly with Charles Holt, Franco Modigliani and John F. Muth.

The aim of the study was to develop mathematical tools to improve inventory control systems for production planning at a plant of the Pittsburgh Plate Glass Company. It was in this context of the concrete study of empirical data that Simon developed his early notions of “satisficing” behavior, and that the two opposite ideas of Rational Expectations (Muth) and Bounded Rationality emerged.

Heterogeneous Agents in Finance : different heuristics and different representations of problems

In a perfectly rational EMH world all traders are rational and it is common knowledge that all traders are rational. In real financial markets however, traders are different, especially with respect to their expectations about future prices and dividends. A quick glance at the financial pages of newspapers is sufficient to observe that difference of opinions among financial analysts is the rule rather than the exception. In the last decade, a rapidly increasing number of structural heterogeneous agent models have been introduced in the finance literature

Heterogeneous Agents in Finance : different heuristics and different representations of problems

In the traditional approach, simple analytically tractable models with a representative, perfectly rational agent have been the main corner stones and mathematics has been the main tool of analysis.

The new behavioral, heterogeneous agents approach challenges the traditional representative, rational agent framework. It is remarkable however, that many ideas in the behavioral, agent-based approach in fact have quite a long history in economics already dating back to earlier ideas well before the rational expectations and efficient market hypotheses.

Heterogeneous Agents in Finance : different heuristics and different representations of problems

Rational behavior has two related but different aspects (e.g. Sargent (1993)).

First, a rational decision rule has some micro-economic foundation and is derived from optimization principles, such as expected utility or expected profit maximization.

Second, agents have rational expectations (RE) about future events, that is, beliefs are perfectly consistent with realizations and a rational agent does not make systematic forecasting errors.

Heterogeneous Agents in Finance : different heuristics and different representations of problems

In a rational expectations equilibrium, forecasts of future variables coincide with the mathematical conditional expectations, given all relevant information.

Rational expectations provided an elegant and parsimonious way to exclude ‘ad hoc’ forecasting rules and market psychology from economic modelling. Since its introduction in the sixties by Muth (1961) and its popularization in economics by Lucas (1971), the rational expectations hypothesis (REH) has become the dominating expectation formation paradigm in economics.

Heterogeneous Agents in Finance : different heuristics and different representations of problems

Milton Friedman has been one of the strongest advocates of a rational agent approach, claiming that the behavior of consumers, firms and investors can be described as if they behave rationally. The Friedman hypothesis stating that non-rational agents will not survive evolutionary competition and will therefore be driven out of the market has played an important role in this discussion.

Heterogeneous Agents in Finance : different heuristics and different representations of problems

In a similar spirit, Alchian (1950) argued that biological evolution and natural selection driven by realized profits may eliminate non-rational, non-optimizing firms and lead to a market where rational, profit maximizing firms dominate. The question whether the Friedman hypothesis holds in a heterogeneous world has played an important role in the development and discussion about Heterogeneous Agents .

Market Efficiency

Another important issue in the discussion of rational versus boundedly rational behavior is concerned with market efficiency, as emphasized by Fama (1965).

If markets were not efficient, then there would be unexploited profit opportunities, that would be exploited by rational arbitrage traders. Rational traders would buy (sell) an underpriced (overpriced) asset, thus driving its price back to the correct, fundamental value. In an efficient market, there can be no forecastable structure in asset returns, since any such structure would be exploited by rational arbitrageurs and therefore disappear

Fama’s Efficient Markets Hypothesis (EMH), i.e. the assumption that market behaviour can be described by a random walk process, because rational traders do not miss unexploited profit opportunities, has been drastically challenged by the recent developments of “Behavioral Finance”.

Comment (Thaler)

In the traditional framework where agents are rational and there are no frictions, a security’s price equals its “fundamental value”.

The hypothesis that actual prices reflect fundamental values is the Efficient Markets Hypothesis (EMH). Put simply, under this hypothesis, “prices are right”, in that they are set by agents who understand Bayes’ law and have sensible preferences.

Behavioral finance argues that some features of asset prices are most plausibly interpreted as deviations from fundamental value, and that these deviations are brought about by the presence of traders who are not fully rational.

Friedman’s line of argument is initially compelling, but it has not survived careful theoretical scrutiny. In essence, it is based on two assertions. First, as soon as there is a deviation from fundamental value – in short, a mispricing – an attractive investment opportunity is created. Second, rational traders will immediately snap up the opportunity, thereby correcting the mispricing.

Behavioral finance disputes the first step. The argument, is that even when an asset is wildly mispriced, strategies designed to correct the mispricing can be both risky and costly, rendering them unattractive. As a result, the mispricing can remain unchallenged.

Comment (Thaler)

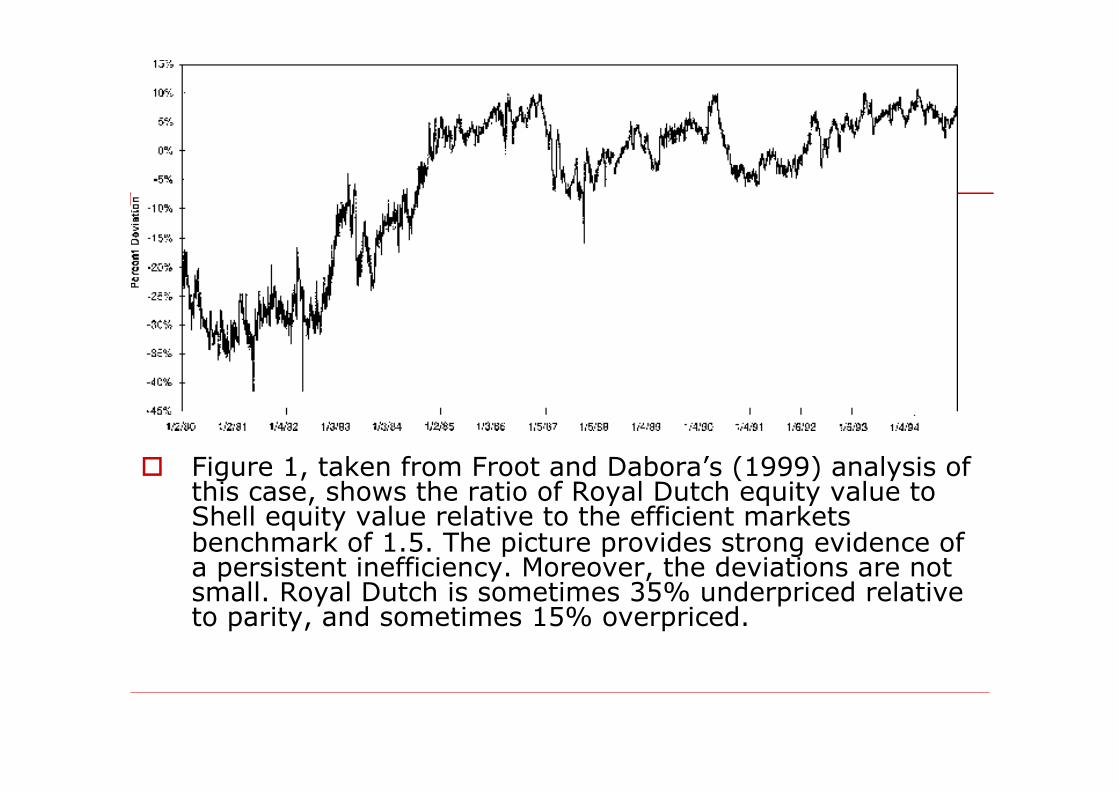

In 1907, Royal Dutch and Shell Transport, at the time completely independent companies, agreed to merge their interests on a 60:40 basis while remaining separate entities.

Shares of Royal Dutch, which are primarily traded in the USA and in the Netherlands, are a claim to 60% of the total cash flow of the two companies, while Shell, which trades primarily in the UK, is a claim to the remaining 40%. If prices equal fundamental value, the market value of Royal Dutch equity should always be 1.5 times the market value of Shell equity. Remarkably, it isn’t.

Thaler :Behavioral Finance an example

Figure 1, taken from Froot and Dabora’s (1999) analysis of this case, shows the ratio of Royal Dutch equity value to Shell equity value relative to the efficient markets benchmark of 1.5. The picture provides strong evidence of a persistent inefficiency. Moreover, the deviations are not small. Royal Dutch is sometimes 35% underpriced relative to parity, and sometimes 15% overpriced.

While irrational traders are often known as “noise traders”, rational traders are typically referred to as “arbitrageurs”. Strictly speaking, an arbitrage is an investment strategy that offers riskless profits at no cost. Presumably, the rational traders in Friedman’s fable became known as arbitrageurs because of the belief that a mispriced asset immediately creates an opportunity for riskless profits. Behavioral finance argues that this is not true: the strategies that Friedman would have his rational traders adopt are not necessarily arbitrages; quite often, they are very risky.

Overconfidence. Extensive evidence shows that people are overconfident in their judgments. This appears in two guises. First, the confidence intervals people assign to their estimates of quantities – the level of the Dow in a year, say – are far too narrow. Their 98% confidence intervals, for example, include the true quantity only about 60% of the time [Alpert and Raiffa (1982)]. Second, people are poorly calibrated when estimating probabilities: events they think are certain to occur actually occur only around 80% of the time, and events they deem impossible occur approximately 20% of the time [Fischhoff, Slovic and Lichtenstein (1977)].

Where the variety of behavior comes from? Euristics and Biases

Representativeness. Kahneman and Tversky (1974) show that when people try to determine the probability that a data set A was generated by a model B, or that an object A belongs to a class B, they often use the representativeness heuristic. This means that they evaluate the probability by the degree to which A reflects the essential characteristics of B.

Anchoring. Kahneman and Tversky (1974) argue that when forming estimates, people often start with some initial, possibly arbitrary value, and then adjust away from it. Experimental evidence shows that the adjustment is often insufficient. Put differently, people “anchor” too much on the initial value.

Where the variety of behavior comes from? Euristics

The micro foundations

From Bernoullian Expected Utility Theory to Kahneman and Tversky’ Prospect Theory

In 1952, at a symposium held in Paris, Allais presented two studies in which he criticized the descriptive and predictive power of the choice theory of the “American School” and especially Friedman’s stance, (Allais, 1953), demonstrating some experiments in which subjects underwent alternative choices in conditions of risk systematically violating the assumptions of the expected utility theory.

Kahnemann and Tversky

Kahneman and Tversky’s Prospect Theory and framing effect

Individuals behave as risk takers when facing a problem presented in terms of loss while they behave as risk averse when the same problem is presented in terms of gain)

This behavioral inconsistency is called “framing effect”, and shows clearly that the mental representation (framing) of a problem may be crucial to elicit individual behavior.

2 – Changing Representation: Kahneman’s Prospect Theory

From Bernoullian Expected Utility Theory to Kahneman’ Prospect Theory

Framing effect , preference reversal,…lead to an advanced vision of bounded rationality and suggest to adopt new, non EUT theories based on the properties of human reasoning

They suggest that in order to understand a decision one must thoroughly analyze the cognitive processes that are at the base of the decision. It is thus necessary to understand how people represent problems, how the complex process of editing is carried out and how construction of mental models is built in order to make a particular decision.

A second class of deviations from rationality

One of the most investigated reasoning problems in the literature, in which the dual model’s prediction have been tested, is the Wason selection task. This task it is known to be very difficult in its conceptual version, if represented in different, “deontic”, version is it is quite easy and – interestingly - may lead either to the right or to the wrong response depending on the form in which is presented.

A B 2 3

1 - Wason “four-card selection task” (1966)

Subjects are given the following conditional rule:

“If a card has an A on one side, then it has a 2 on the other side”

Here is a rule: if a person is drinking been, then the person must be over 19

years of age. Select the card, or cards that you definitely need to turn over

to determine whether or not people are violating the rule.

Drinking Beer

Drinking Coke

16 Years Old

22 Years Old

1 - Wason “four-card selection task” (1966)

The “perspective effect” by Gigerenzer and Hug

“The cards below have information about four employees. Each card represents one person.

One side of the card tells whether the person worked on the weekend, and the other side tells whether the person got a day off during the week.

Is given the following rule: “If an employee works on the week-end, than that person gets a day off during the week”

Indicate only the card(s) you definitely need to turn over to see if the rule has been violated.”

Worked on the weekend Did get a day off

Did not work on the weekend

Did not get a day off

Gigerenzer’ thesis is that a "cheating detection mechanism" guides reasoning in the following type of selection task:

If the conditional statement is coded as a social contract, and the subject is cued into the perspective of one party in the contract, then attention is directed to information that can reveal being cheated. (Gigerenzer and Hug 1992)

This thesis can be proved or falsified by comparing two different version of the selection task by changing the subject that can be cheated in the contractual relation.

The “perspective effect” by Gigerenzer and Hug

A different view based on behavioral evidence

1 – Framing effect , preference reversal,…lead to an advanced vision of bounded rationality and suggest to adopt new, non EUT theories based on the properties of human reasoning

2 – Wason effect leads to the idea that new microfoundations can be institutionally framed (social norms).

4 - Heterogeneity of agents can be based both on a new description of rational behavior and a norms ?

Invariance

The most important feature of framing effect and inter temporal preference reversal is the violation of invariance: the same object if considered from two different viewpoints is not recognized as it is; the same happens for a problem described in two different ways.

The alternatives of a choice are not elaborated, mentally manipulated to check their eventual similarities and therefore to set the choice in the simplest form.

Invariance means that the same problem or the same choice , is solved in the same way however is described.

Kahneman

“Invariance. An essential condition for a theory of choice that claims normative status is the principle of invariance: different representations of the same choice problem should yield the same preference. That is, the preference between options should be independent of their description.

… This principle of invariance (or extensionality [Arrow 1982]), is so basic that it is tacitly assumed in the characterization of options rather than explicitly stated as a testable axiom.

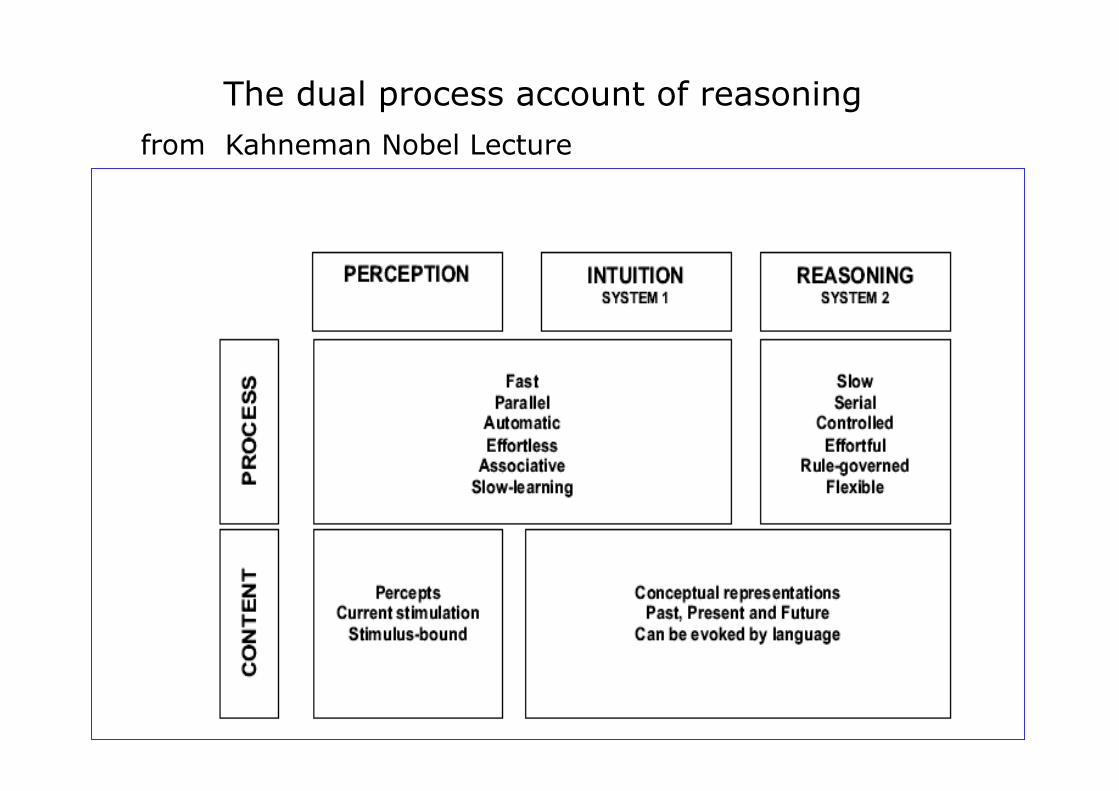

The dual model account of reasoning

The idea of a dualism in the process of reasoning was raised by Posner and Synder (1975) by wondering what level of conscious control individuals have over their judgements and decisions.

decision is supposed to be based on two different cognitive processes: on the one hand a controlled, deliberate, sequential and effortful process of calculation (“reasoning”); on the other a non deliberate process, which is automatic, effortless, parallel and fast ( “intuition”). The two processes have been described in many different ways, by different authors, but there is nowadays considerable agreement among psychologists on the characteristics that distinguish them.

The interactions between System 1 and System 2 are related one the one hand to “accessibility”,i.e “the ease with which particular mental contents come to mind” on the other hand to attention/memorization processes.

According to Schneider and Shiffrin in a repeated problem solving activity specialized mental skills are created and settled in long-term memory through the process of learning / solving of the problems.

in their view automatic processing is the activation of learned sequence of elements in long-term memory that is triggered by appropriate inputs.

The dual process account of reasoning

from Kahneman Nobel Lecture

The dual process account of reasoning

The dual process account of reasoning

If dual model approach predictions are correct, acquired capabilities may interfere with each other and more crucially, may interfere with Sistem 2 general capabilities.

Accessibility. The core concept of Kahnemann analysis of intuitive judgments and preferences is accessibility – the ease with which particular mental contents come to mind (Higgins, 1996). A defining property of intuitive thoughts is that they come to mind spontaneously, like percepts. To understand intuition, then, we must understand why some thoughts are accessible and others are not.

The dual process account of reasoning

Framing effects in decision making arise when different descriptions of the same problem highlight different aspects of the outcomes.

The core idea of prospect theory is that changes and differences are much more accessible than absolute levels of stimulation.

Judgment heuristics, which explain many systematic errors in beliefs and preferences are explained by a process of attribute substitution: people sometimes evaluate a difficult attribute by substituting a more accessible one.

The meaning of representation

Kahneman emphasizes the essential role of the “framing” effect for understanding the origin of biases in decision making and reasoning; he suggest that framing must be considered a special case of the more general phenomenon of dependency from the representation: the question is how to explain the fact that different representations of the same problem yield different human decisions.

This suggests again that the crucial aspect of the decision-making process is the ability to construct new representations of problems.

Invariance

The impossibility of invariance raises significant doubts about the descriptive realism of rational-choice models (Tversky & Kahneman, 1986).

Absent a system that reliably generates appropriate canonical representations, intuitive decisions will be shaped by the factors that determine the accessibility of different features of the situation.

Highly accessible features will influence decisions, while features of low accessibility will be largely ignored. Unfortunately, there is no reason to believe that the most accessible features are also the most relevant to a good decision.

Invariance

Violations of invariance are originated by different accessibility and give rise to dependency from representation

Changing Representation

“The representation problem was addressed by Newell [2] in 1965. Newell used the mutilated checkerboard problem to illustrate his point that the greatest "limitation of the current stock of ideas about problem solving" is that "we do not yet have any useful representations of possible representations". Most of the work on this problem was centered around a 1966 seminar at Carnegie—Mellon University which included Saul Amarel, Steven Coles, Richard Fikes, Allen Newell, Laurent Siklossy and Herbert Simon.

Changing representation

In The Sciences of the Artificial, Simon [9] discusses representation in the context of design.

He suggests that all of problem solving may be viewed as changes of representation; that solving a problem can be seen as representing it so that the solution becomes transparent.

Changing representation

Korf defined a representation change as a transformation of the state space and considered two main types of transformations:

isomorphism and homomorphism.

An isomorphic representation change is renaming of the states without changing the structure of the space.

An homomorphic transformation is a reduction of the space by abstracting some states and transitions.

Changing representation

Two representations are isomorphic iff there exists a bijective mapping between them (recodifying the language you describe the same problem)

Representation change

isomorphism and homomorphism.

Examples of Isomorphic representation : Wason effect, Framing Effect, Simon and Hayes experiment.

Examples of Homomorphic transformation : Problem Solving in state space.

Isomorphism : an example

Simon and Hayes (1976) … constructed a collection of transformation puzzles, all formally identical to the tower of Hanoi problem, and found that these ‘problem isomorphs’ varied greatly in difficulty. For example, the initial state and the target state were described in two of the versions as three monsters holding balls of different colors. The state transitions were described in one version as changes in the color of the balls, and in the other as balls being passed from one monster to another. The puzzle was solved much more easily when framed in terms of motion.

Representations: Hanoi Tower

Abstracting the Tower of Hanoi Craig A. Knoblock

isomorphic changes of representation

Representations: Redefining through abstraction the elements of the problem

More generally, we can compute a finite number of categories, extracted from a given representation, with which build a new, omomorphic rapresentation of a given problem.

Aggregating graphs

One can build-up a simplified aggregate representation by grouping toghether the nodes in clusters, in such a way that

1 all nodes of a cluster are connected with the nodes of a parent cluster through the same move.

2 clusters span perfectly the original graph, i.e. every node belongs to one only cluster and the set of clusters covers all nodes.

Thanks to property 1, we can transform the original graph into a new one, where each node is an “aggregate node” connected with other nodes through one move. Of course the new aggregate graph is smaller than the original one, depending on the size of clusters.

Aggregating graphs

It may happen that clusters have some common properties that allow to represent them in a more compact description: categorization is the usual way with which humans reduce a description to a more compacted one.

To discover a game strategy, individuals decompose the problem according to their “intuitions”, i.e. their ways to categorize and conceptualize the game’s properties. According to Bellman’s principle, by decomposing a problem into sub-problems and optimizing each of them, the outcome is an optimal solution of the original problem only under very restrictive conditions.

Different abstract representations of a game may lead to hidden systematic deviations from rationality

The global solution to a problem may therefore be sub-optimal, in relation to the pattern of decomposition that has been adopted. Therefore biases are interpreted as sub-optimal behaviors originated by the decomposition pattern that individuals adopt, and ultimately by their categorization of the problem.

Categorization leads to Conceptual Distortion

The role of categorization is fundamental during the creation of mental competences because it direct the creation of new specialized skills ( that will be stored into the System1 (intuition) and later automatically triggered). Categorization allow individuals to simplify the representation of a problem to be solved and to achieve more easily a solution;

but categorization is not a “rational” process and therefore an “imperfect” categorization may lead to solve a problem in a very sub-optimal way, i.e. leads individual to systematic deviations from rational/optimal behavior.

Concluding Remarks

Due to different accessibility of thoughts, individuals have difficulties to recognize the same problem if presented with different representations. Isomorphisms are related with dual model , intuition, accessibility and social norms

homomorphisms are related with abstraction and categorization ( a new language)

The variety of different representations of a given problem can be computed and used to predict different agents’ behaviors.

Back to the quotation at the beginning of this talk

Economics and finance are witnessing an important paradigm shift, from a representative, rational agent approach towards a behavioral, agent-based approach in which markets are populated with boundedly rational, heterogeneous agents using well defined strategies based on different representations of their environment. “

ThankYou

Summary

Dual Model Accessibility Euristics Framing and Representations Categorization Social Norms Deontic Character Context Stories (Gigerenzer, Shiller)

Being cheated in a social contract means that someone takes the benefit, but does not pay the cost.' In other words, a subject should select those cards that correspond to "benefit taken" and "cost not paid," whatever the cards' logical status is.

The employer takes the benefit of the employee working on the weekend, without paying the cost of giving the employee the promised day off.

Therefore for the employee, being cheated meant that some colleague "did work on the weekend and did not get a day off;"

For the employer, being cheated meant that the employee "did not work on the weekend and did get a day off;" that is, in this perspective, subjects should select the cards which correspond to the not-p- and q-cards.

Thus, perspective change can play cheating detection against propositional logic. The two competing predictions are: If the cognitive system attempts to detect instances of "benefit taken and cost not paid" in the other party's behavior, then a perspective switch implies switching card selections; if the cognitive system reasons according to propositional logic, however, pragmatic perspectives are irrelevant, people should reason "logically," and there should be no switch in card selections.

The results showed that when the perspective was changed, the cards selected also changed in the predicted direction. The effects were strong and robust across problems. For instance, GIGERENZER and HUG [1992] report that in the employee perspective of the day-off problem, 75% of the subjects had selected "worked on the weekend" and "did not get a day off," but only 2 % had selected the other pair of cards. In the employer perspective, this 2% (who had selected "did not work on the weekend" and "did get a day off") rose to 61 %.

![Heterogeneous Response to Differentiation Induction in ......[CANCER RESEARCH 49. 7132-7140. December 15. 1989] Heterogeneous Response to Differentiation Induction in Different Clonal](https://img.pdfslide.us/doc/110x75/6118131ed46536765950d476/heterogeneous-response-to-differentiation-induction-in-cancer-research.jpg)