Embed Size (px)

Citation preview

Hellenic Petroleum Group

Company update

July 2012

11

Contents

• Introduction - Group overview

•Strategy and delivery

•Group business units

•Enhancing competitiveness

•Funding

•Financials

22

A diversified regional energy player undergoing a significant transformation

• A leading regional energy Group, built around its strong R&M asset base

• Hellenic Petroleum has completed its transformational investmentplan, moving to the delivery phase of a significant cash generation improvement

• Solid financial position throughout the cycle, enabling to successfully complete the heavy capex period and manage through Greek crisis and challenges in the region

• Involved in two major privatisations (HP and DEPA)

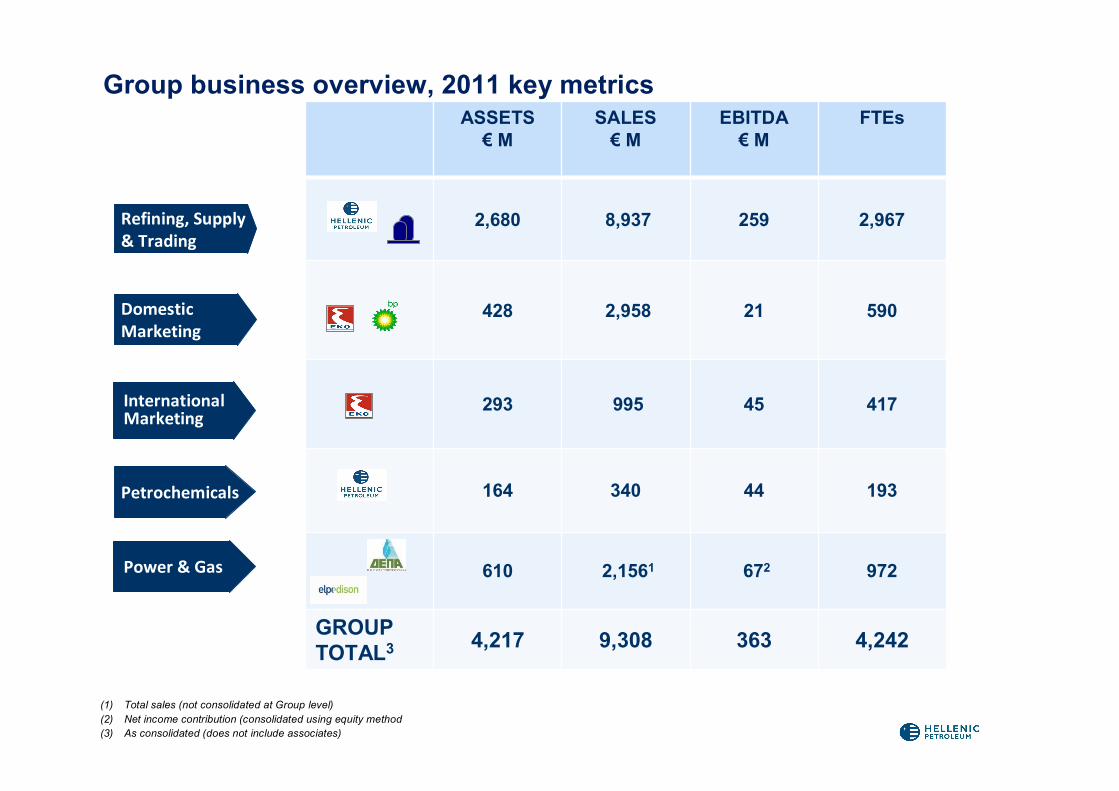

Group business overview, 2011 key metrics

Refining, Supply & Trading

Domestic Marketing

InternationalMarketing

Petrochemicals

Power & Gas

(1) Total sales (not consolidated at Group level)(2) Net income contribution (consolidated using equity method(3) As consolidated (does not include associates)

ASSETS€ Μ

SALES€ Μ

EBITDA€ Μ

FTEs

2,680 8,937 259 2,967

428 2,958 21 590

293 995 45 417

164 340 44 193

610 2,1561 672 972

GROUP TOTAL3 4,217 9,308 363 4,242

44

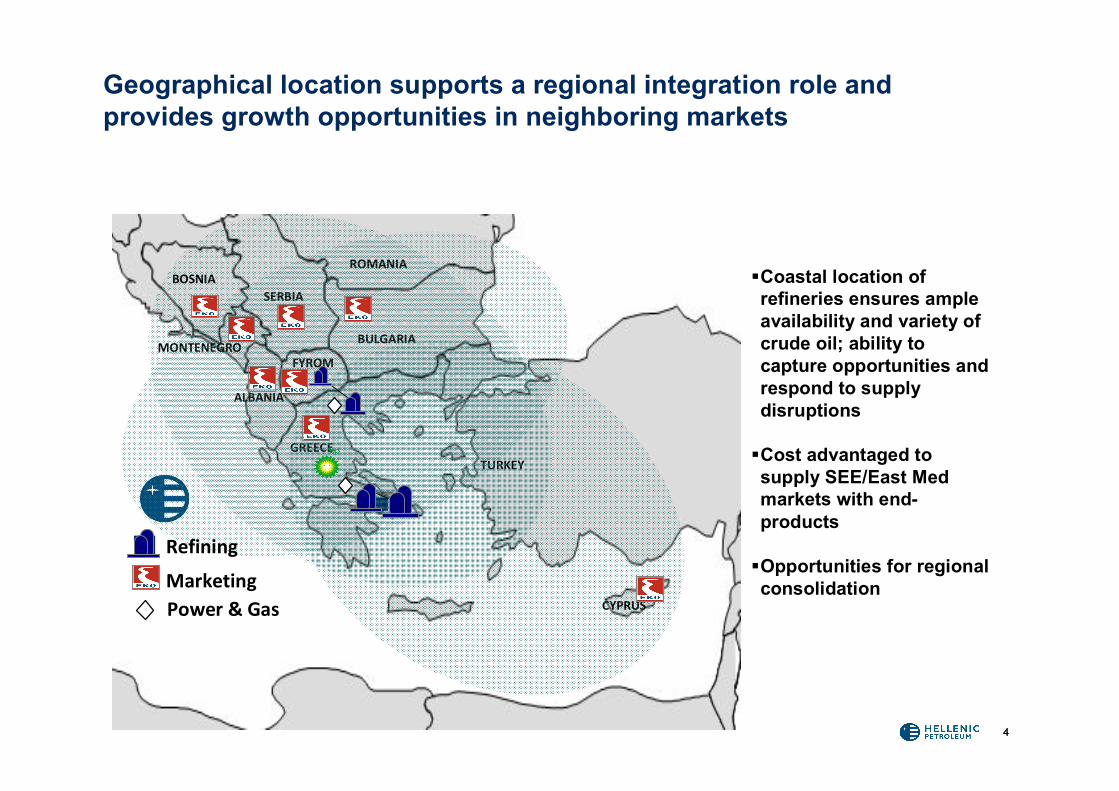

Geographical location supports a regional integration role and provides growth opportunities in neighboring markets

Coastal location of refineries ensures ample availability and variety of crude oil; ability to capture opportunities and respond to supply disruptions

Cost advantaged to supply SEE/East Med markets with end-products

Opportunities for regional consolidation

ROMANIA

TURKEY

BULGARIA

SERBIA

CYPRUS

FYROM

GREECE

ALBANIA

BOSNIA

MONTENEGRO

Refining

MarketingPower & Gas

55

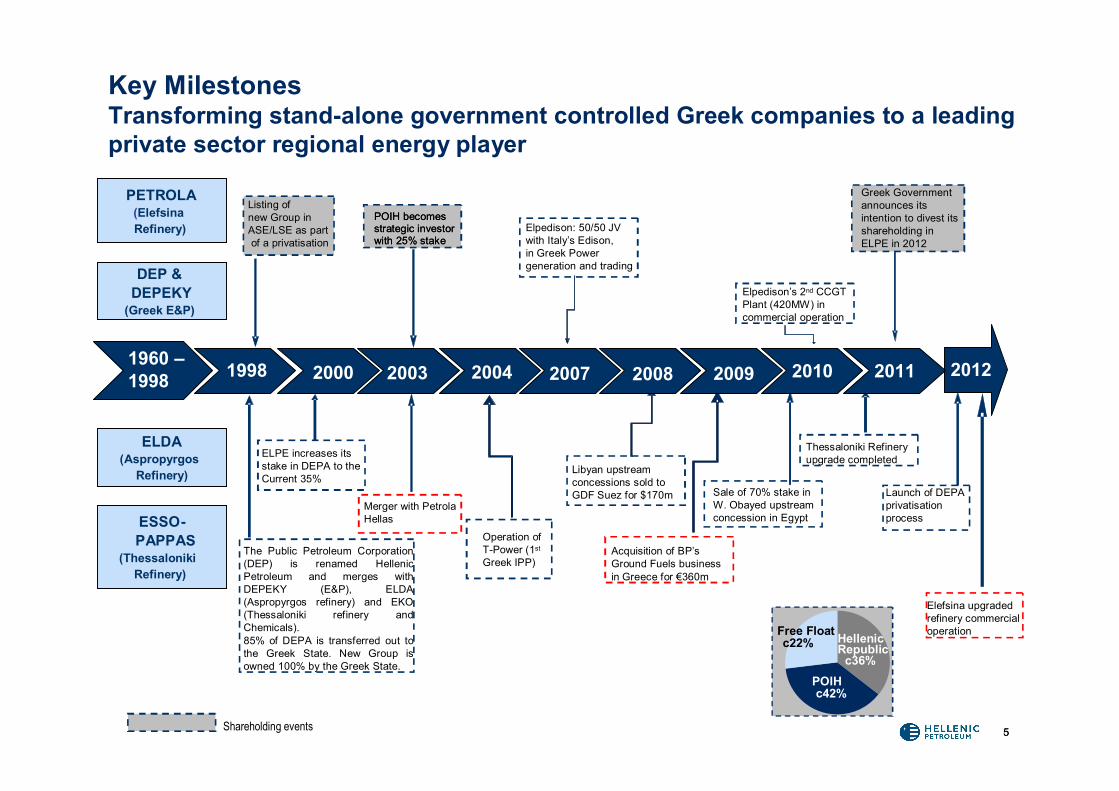

Key MilestonesTransforming stand-alone government controlled Greek companies to a leading private sector regional energy player

PETROLA(ElefsinaRefinery)

DEP & DEPEKY

(Greek E&P)

ELDA(Aspropyrgos

Refinery)

ESSO-PAPPAS

(ThessalonikiRefinery)

PETROLA(ElefsinaRefinery)

DEP & DEPEKY

(Greek E&P)

ELDA(Aspropyrgos

Refinery)

ESSO-PAPPAS

(ThessalonikiRefinery)

1998

ELPE increases itsstake in DEPA to the Current 35%

1960 –1998 2000 2003 2004 2007 2008 2009 2012

Merger with PetrolaHellas

Operation ofT-Power (1st

Greek IPP)

Elpedison: 50/50 JV with Italy’s Edison, in Greek Power generation and trading

Libyan upstreamconcessions sold toGDF Suez for $170m Sale of 70% stake in

W. Obayed upstream concession in Egypt

Elpedison’s 2nd CCGTPlant (420MW) incommercial operation

2010

Thessaloniki Refinery upgrade completed

Free Floatc22%

POIHc42%

Hellenic Republic

c36%

Acquisition of BP’sGround Fuels businessin Greece for €360m

The Public Petroleum Corporation (DEP) is renamed Hellenic Petroleum and merges with DEPEKY (E&P), ELDA (Aspropyrgos refinery) and EKO (Thessaloniki refinery and Chemicals).85% of DEPA is transferred out to the Greek State. New Group is owned 100% by the Greek State.

Shareholding events

Listing of new Group in ASE/LSE as partof a privatisation

POIH becomes strategic investor with 25% stake

POIH becomes strategic investor with 25% stake

Greek Government announces its intention to divest its shareholding in ELPE in 2012

2011

Launch of DEPA privatisation process

Elefsina upgraded refinery commercial operation

66

Contents

• Introduction - Group overview

•Strategy and delivery

•Group business units

•Enhancing competitiveness

•Funding

•Financials

7

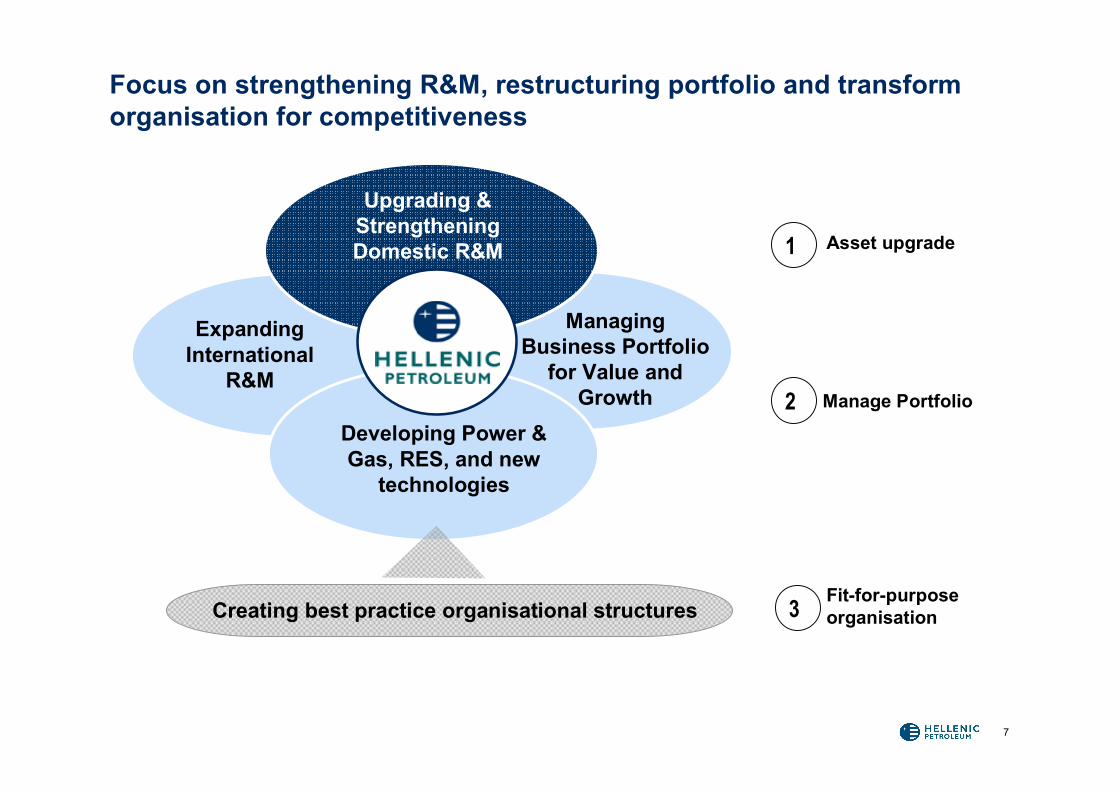

Focus on strengthening R&M, restructuring portfolio and transform organisation for competitiveness

Expanding International

R&M

Managing Business Portfolio

for Value and Growth

Upgrading & Strengthening Domestic R&M

Creating best practice organisational structures

Developing Power & Gas, RES, and new

technologies

1

2

3

Asset upgrade

Manage Portfolio

Fit-for-purpose organisation

450

Historic Average Refining Assets Marketing Assets PortfolioRationalisation

PerformanceImprovement

Medium Term

88

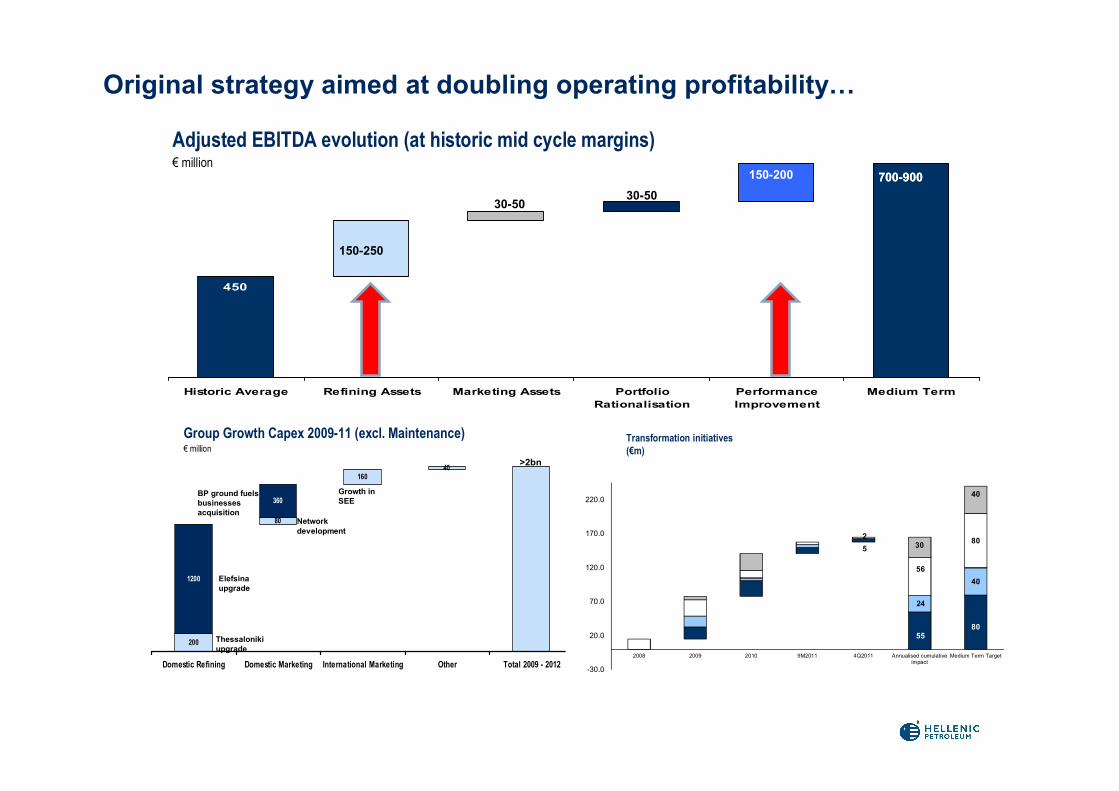

Original strategy aimed at doubling operating profitability…

Adjusted EBITDA evolution (at historic mid cycle margins)€ million

700-900

80

16040

200

360

1200

Domestic Refining Domestic Marketing International Marketing Other Total 2009 - 2012

>2bn

Group Growth Capex 2009-11 (excl. Maintenance)€ million

Elefsina upgrade

Thessaloniki upgrade

BP ground fuels businesses acquisition

Network development

Growth in SEE

Other

5

5580

24

40

2

56

8030

40

-30.0

20.0

70.0

120.0

170.0

220.0

2008 2009 2010 9M2011 4Q2011 Annualised cumulativeimpact

Medium Term Target

Transformation initiatives (€m)

150-250

150-200

30-5030-50

700-900

36050

200

2070

700

FY11 Refining Assets Additional Opsimprovements

PerformanceImprovement

Medium Term

99

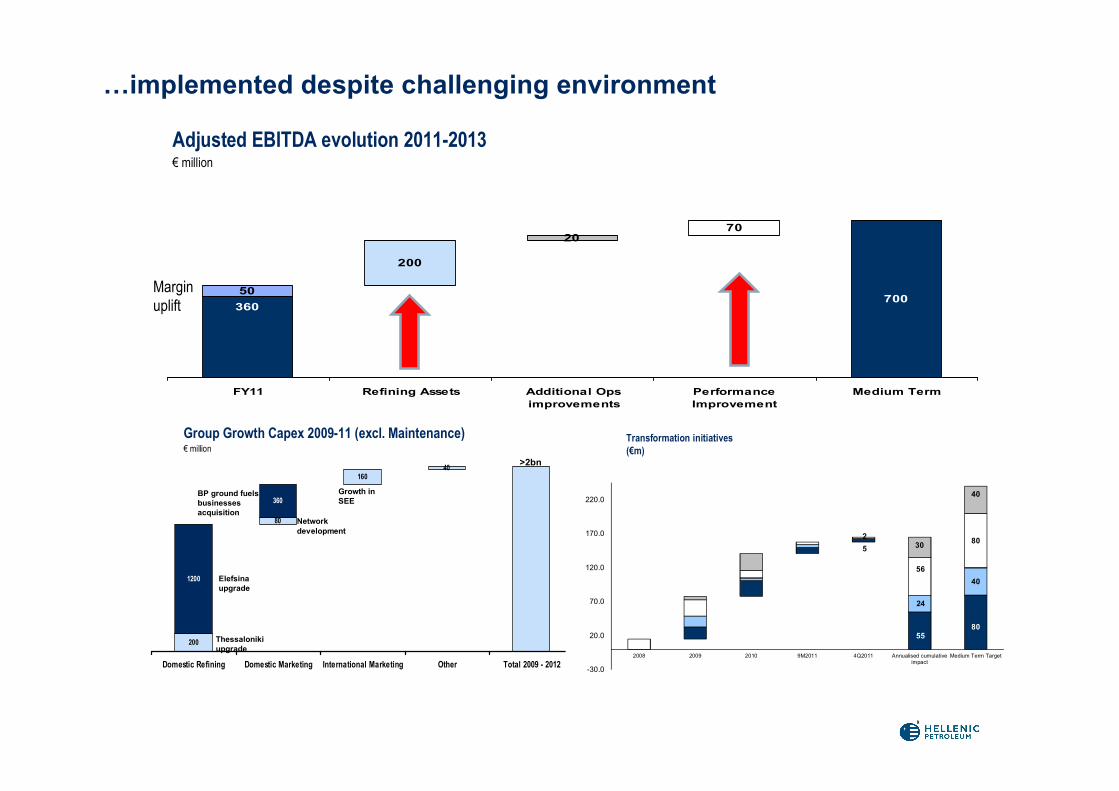

…implemented despite challenging environment

Adjusted EBITDA evolution 2011-2013€ million

700-900

80

16040

200

360

1200

Domestic Refining Domestic Marketing International Marketing Other Total 2009 - 2012

>2bn

Group Growth Capex 2009-11 (excl. Maintenance)€ million

Elefsina upgrade

Thessaloniki upgrade

BP ground fuels businesses acquisition

Network development

Growth in SEE

Other

5

5580

24

40

2

56

8030

40

-30.0

20.0

70.0

120.0

170.0

220.0

2008 2009 2010 9M2011 4Q2011 Annualised cumulativeimpact

Medium Term Target

Transformation initiatives (€m)

150-200 700-900

Margin uplift

1010

600

-150

750

EBITDA Capex Pre Tax Free CashFlow

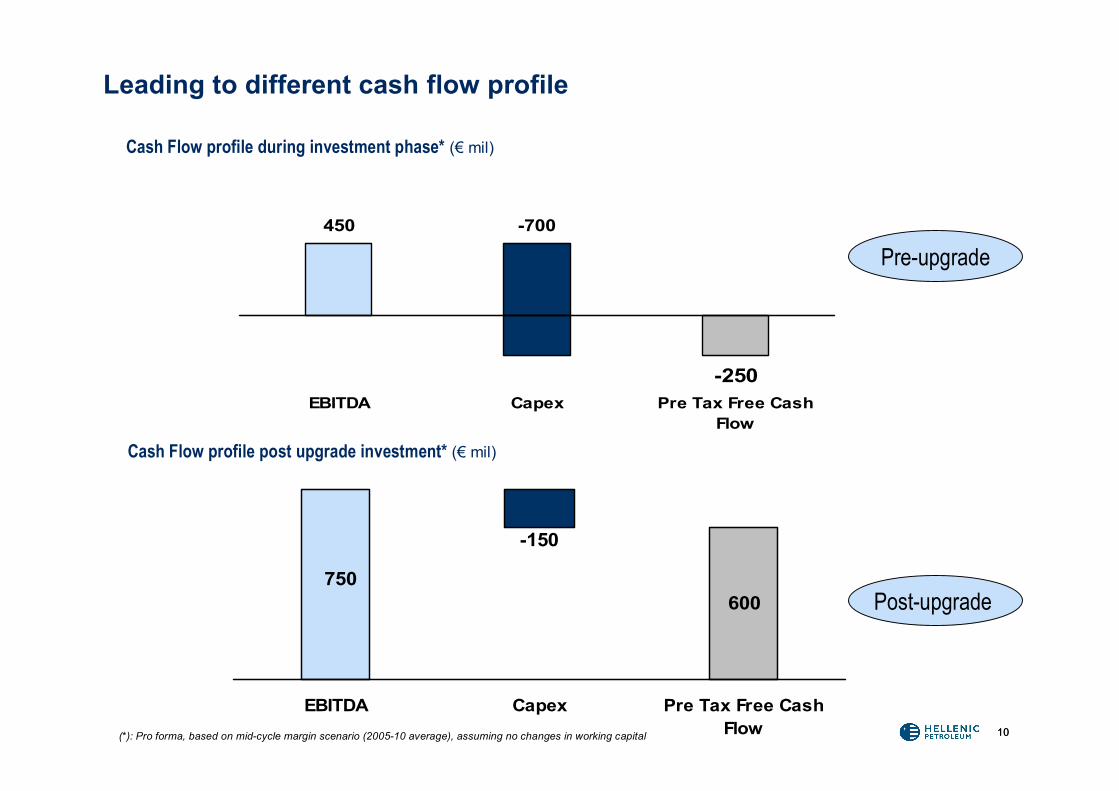

Leading to different cash flow profile

Cash Flow profile during investment phase* (€ mil)

Cash Flow profile post upgrade investment* (€ mil)

(*): Pro forma, based on mid-cycle margin scenario (2005-10 average), assuming no changes in working capital

450 -700

-250EBITDA Capex Pre Tax Free Cash

Flow

Pre-upgrade

Post-upgrade

1111

Contents

• Introduction - Group overview

•Strategy and delivery

•Group business units

•Enhancing competitiveness

•Funding

•Financials

10.6

1.5

6.7

11.0

7.2 7.3

Aspropygros Elefsina Thessaloniki

Pre upgrade Post upgrade

12

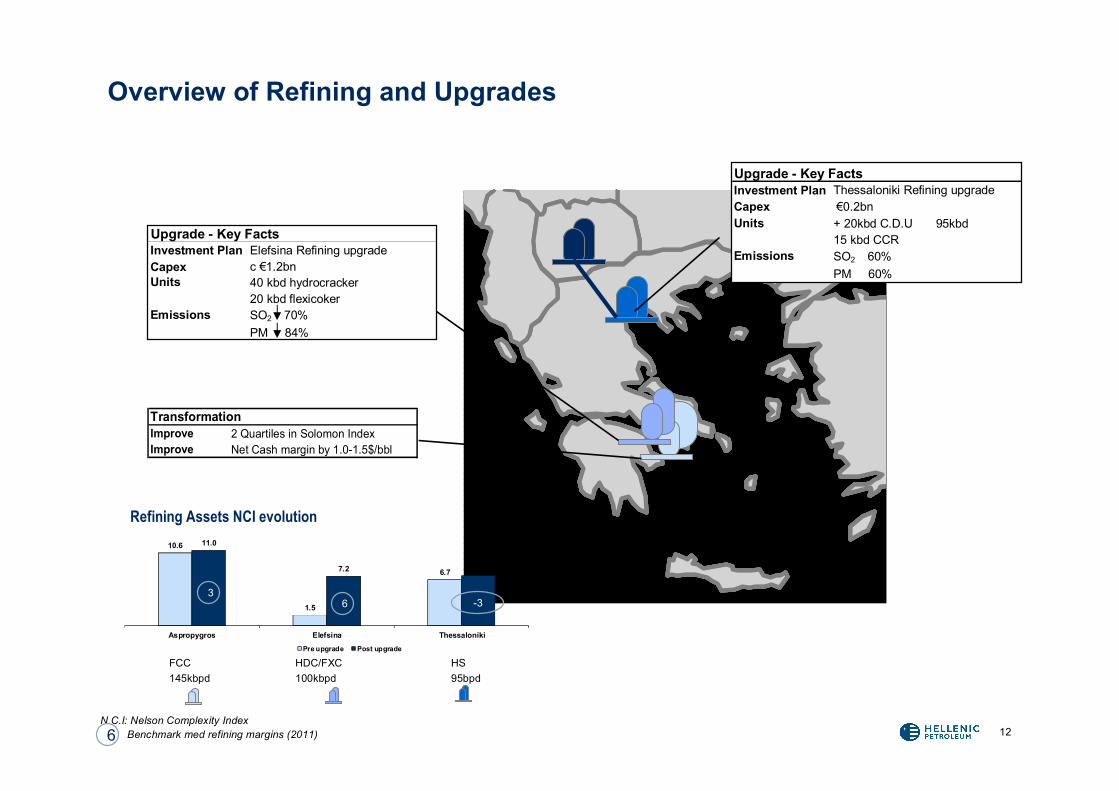

Upgrade - Key FactsInvestment Plan Elefsina Refining upgrade Capex c €1.2bn Units 40 kbd hydrocracker

20 kbd flexicoker Emissions SO2 70%

PM 84%

Overview of Refining and Upgrades

N.C.I: Nelson Complexity IndexBenchmark med refining margins (2011)

Transformation

Improve Net Cash margin by 1.0-1.5$/bblImprove 2 Quartiles in Solomon Index

c. €200m

Upgrade - Key Facts (Completed) Upgrade - Key FactsInvestment Plan Thessaloniki Refining upgrade Capex €0.2bnUnits + 20kbd C.D.U 95kbd

15 kbd CCREmissions SO2 60%

PM 60%

FCC HDC/FXC HS145kbpd 100kbpd 95bpd

Refining Assets NCI evolution

6

6

-33

13

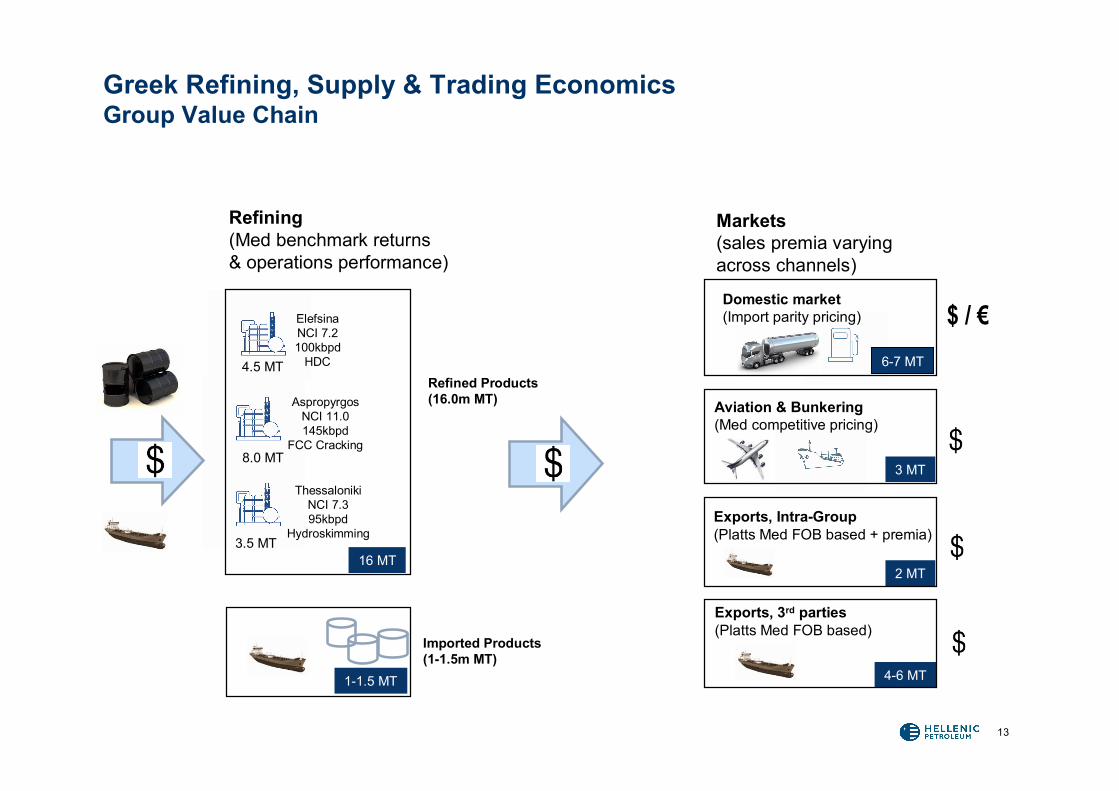

Greek Refining, Supply & Trading EconomicsGroup Value Chain

Markets(sales premia varying across channels)

Refining(Med benchmark returns & operations performance)

Refined Products(16.0m MT)

Imported Products(1-1.5m MT)

Aviation & Bunkering (Med competitive pricing)

Exports, Intra-Group (Platts Med FOB based + premia)

Domestic market (Import parity pricing)

4-6 MT

3 MT

Exports, 3rd parties (Platts Med FOB based)

2 MT

6-7 MT

AspropyrgosNCI 11.0145kbpd

FCC Cracking

ThessalonikiNCI 7.395kbpd

Hydroskimming

ElefsinaNCI 7.2100kbpd

HDC

3.5 MT

8.0 MT

4.5 MT

16 MT

1-1.5 MT

$ / €

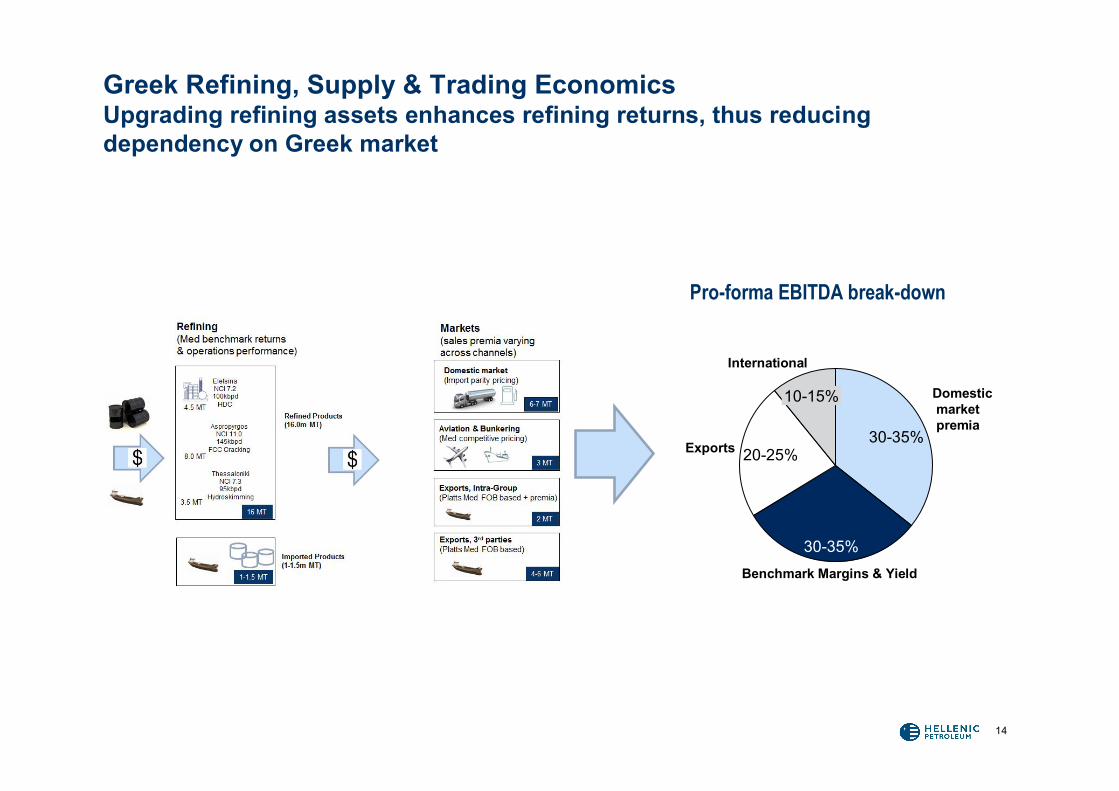

Greek Refining, Supply & Trading EconomicsUpgrading refining assets enhances refining returns, thus reducing dependency on Greek market

12%

Benchmark Margins & Yield

20-25%

Domesticmarketpremia

30-35%

International

10-15%

30-35%

Exports

14

Pro-forma EBITDA break-down

15

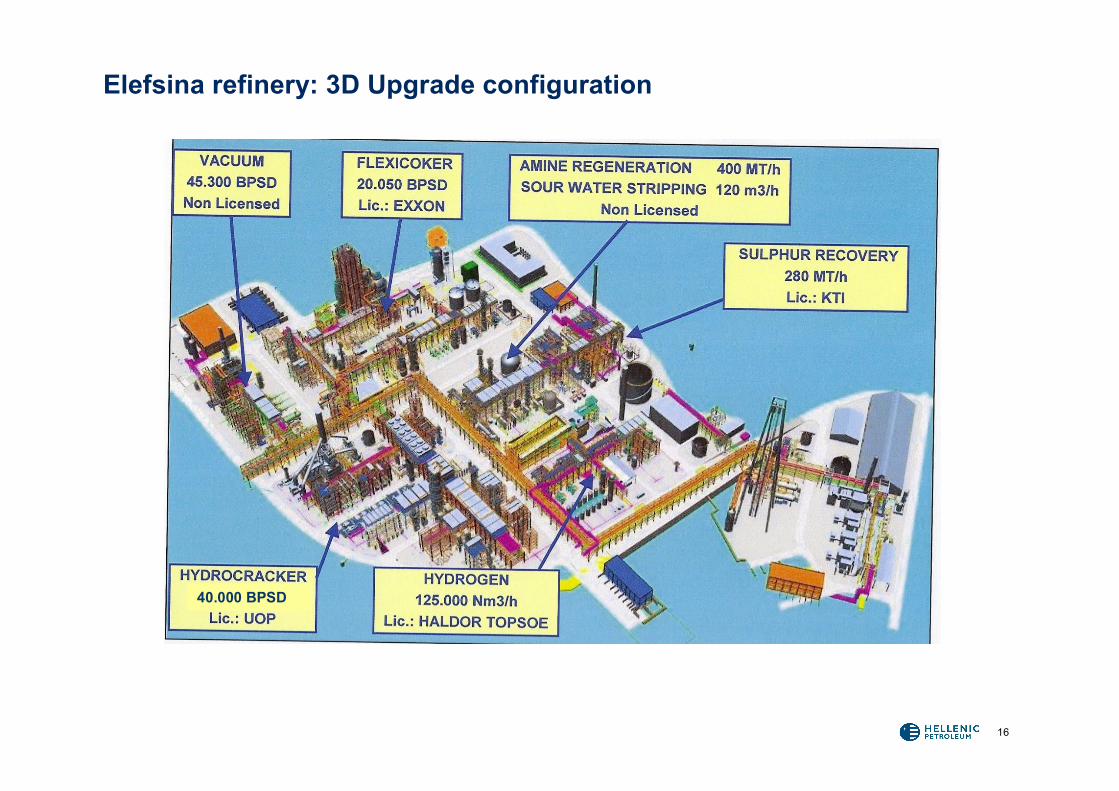

Elefsina Refinery Upgrade Overview

• Elefsina Refinery, a 100kbpd coastal topping refinery with private port and a tank farm of 3,3 mln M3, is transformed to a top cash net-back refinery through a major upgrade

• Largest manufacturing project in SEE Europe:– Second fully converted European refinery combining a hydrocracker and a flexicocker– Middle distillates and naphtha producer

• Event-free commissioning phase; commercial operation over the next few weeks

• Start-up teams and new refinery organisation fully in place

• Elefsina Refinery upgrade will impact Group cash generation from 3Q12 onwards

• Incremental export capacity reduces Group’s dependence on Greek market

16

Elefsina refinery: 3D Upgrade configuration

40.000 BPSD

17

Vacu

umU

nit

Atm

osph

eric

Dis

tilla

tion

Hyd

rocr

acke

r (U

OP)

Flex

icok

er(E

xxon

Mob

il)

Ker

osen

eSw

eete

ning

New units, Sulphur, Amine, SWS

Die

sel

Des

ulph

uriz

atio

n

LPG

Naphtha

Jet Fuel

AutoDiesel

Petcoke or Flexigas

Sulphur

Propane

HeatingDiesel

MarineDiesel

Ligh

t End

s

Rec

over

y

Crude

Existing Units

New Units

Hydrogen (Haldor Topsoe)

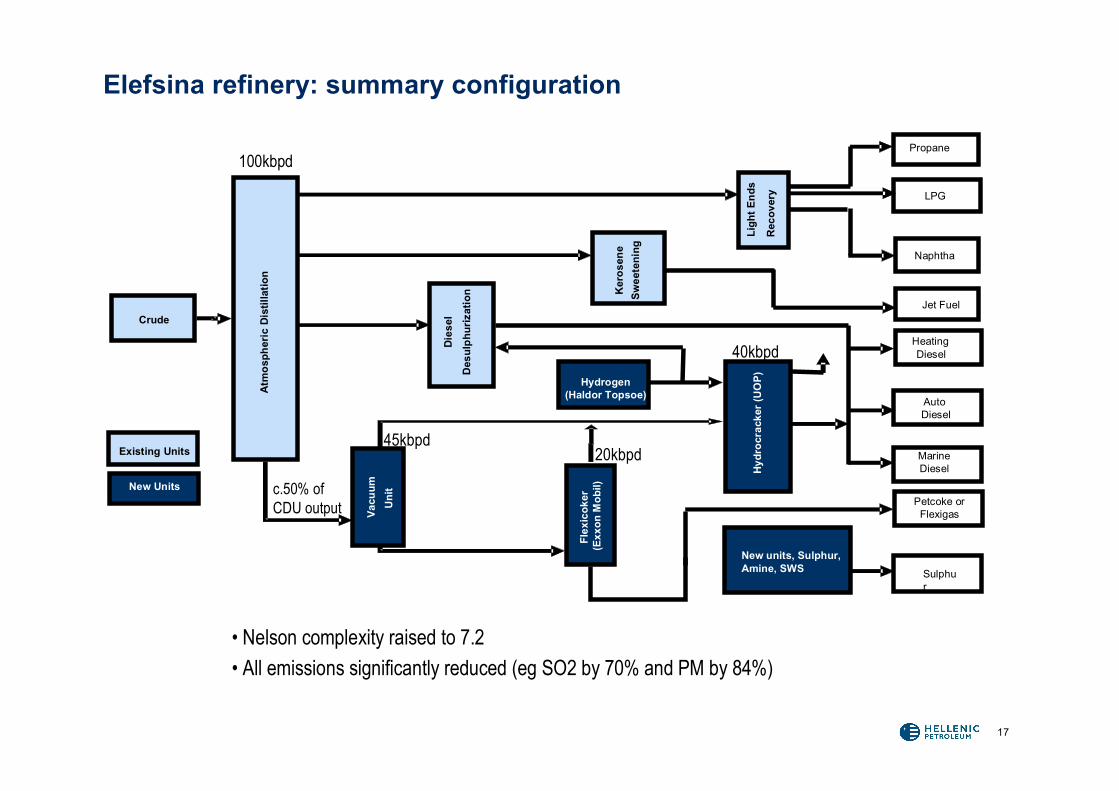

Elefsina refinery: summary configuration

20kbpd

40kbpd

c.50% of CDU output

• Nelson complexity raised to 7.2• All emissions significantly reduced (eg SO2 by 70% and PM by 84%)

100kbpd

45kbpd

-5

0

5

10

15

20

25

JAN

07

APR

07

JUL0

7

OC

T07

JAN

08

APR

08

JUL0

8

OC

T08

JAN

09

APR

09

JUL0

9

OC

T09

JAN

10

APR

10

JUL1

0

OC

T10

JAN

11

APR

11

Jul-1

1

Oct

-11

Jan-

12

Apr

-12

Aspropyrgos Elefsina

0

100

200

300

400

Jan

09

Mar

09

May

09

Jul 0

9Se

p 09

Nov

09

Jan

10M

ar 1

0

May

10

Jul 1

0

Sep

10

Nov

10

Jan

11

Mar

11

May

11

Jul 1

1

Sep

11N

ov 1

1

Jan

12

Mar

12

May

12

18

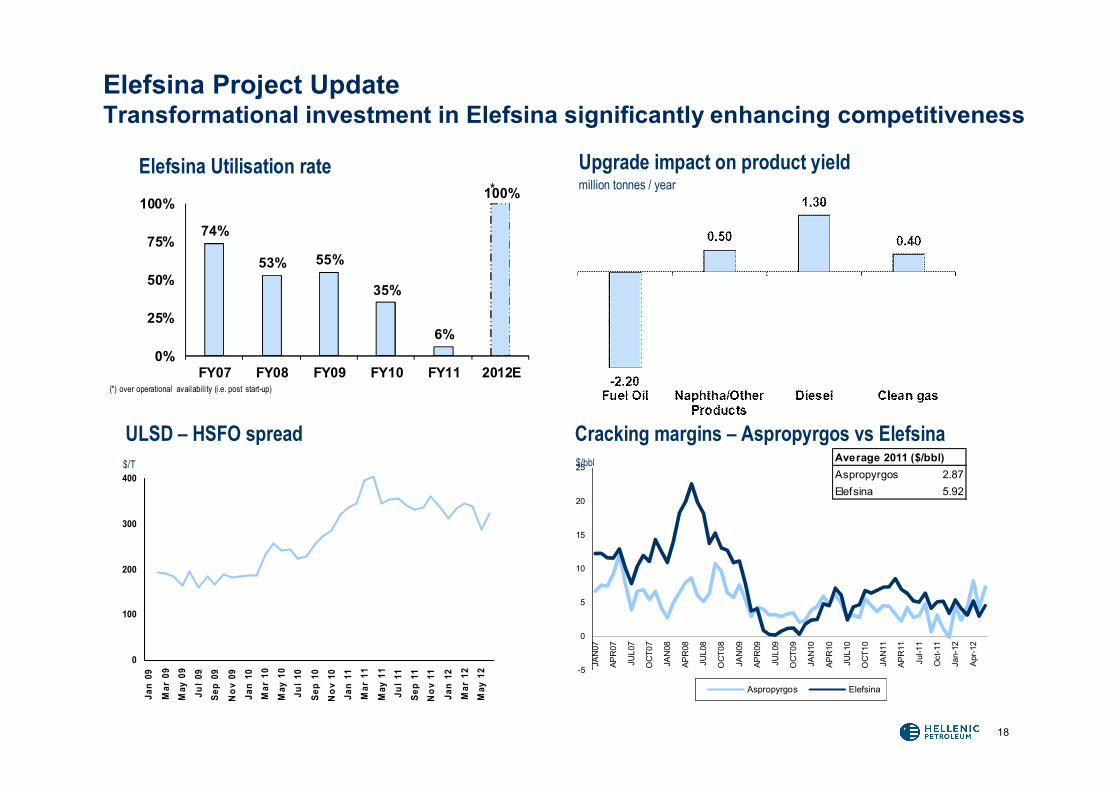

Elefsina Project UpdateTransformational investment in Elefsina significantly enhancing competitiveness

$/bbl$/T

ULSD – HSFO spread Cracking margins – Aspropyrgos vs ElefsinaAverage 2011 ($/bbl)Aspropyrgos 2.87Elefsina 5.92

Elefsina Utilisation rate*

Upgrade impact on product yieldmillion tonnes / year

74%

53% 55%

35%

6%

100%

0%

25%

50%

75%

100%

FY07 FY08 FY09 FY10 FY11 2012E(*) over operational availabili ty (i.e. post start-up)

19

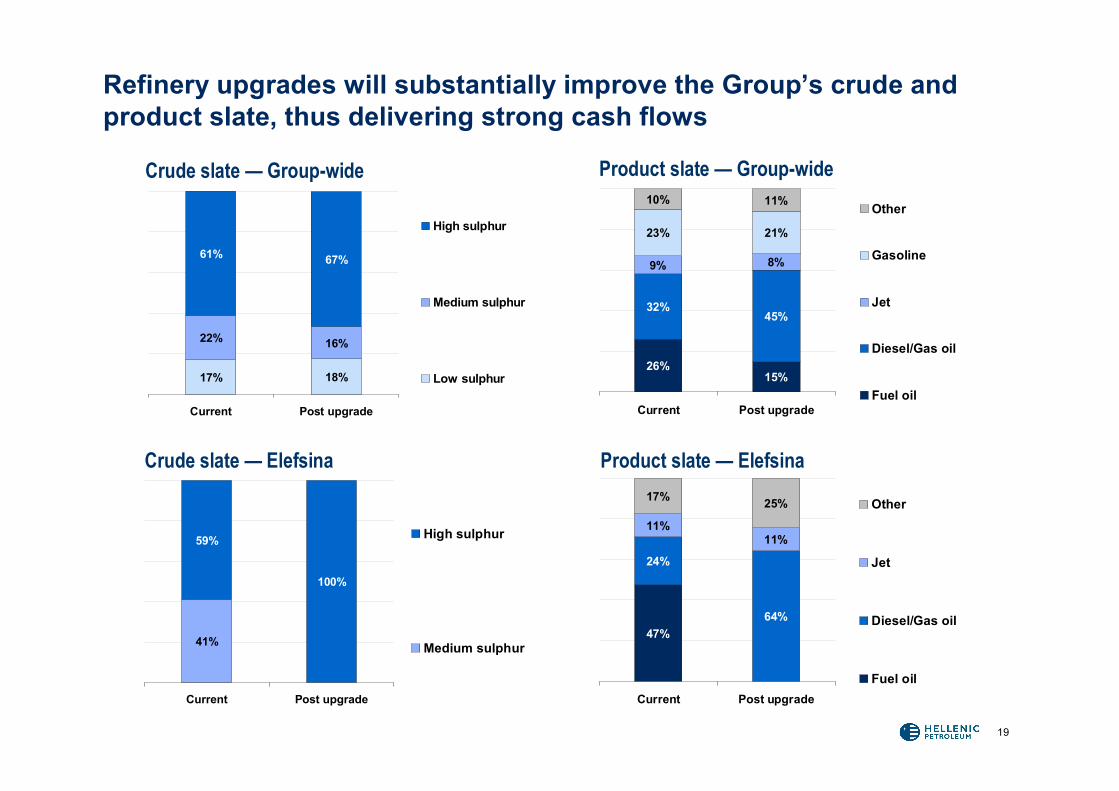

Refinery upgrades will substantially improve the Group’s crude and product slate, thus delivering strong cash flows

26%15%

32%45%

9% 8%

23% 21%

10% 11%

Current Post upgrade

Other

Gasoline

Jet

Diesel/Gas oil

Fuel oil17% 18%

22% 16%

61% 67%

Current Post upgrade

High sulphur

Medium sulphur

Low sulphur

47%

24%

11%11%

17% 25%

64%

Current Post upgrade

Other

Jet

Diesel/Gas oil

Fuel oil

Crude slate — Group-wide Product slate — Group-wide

Crude slate — Elefsina Product slate — Elefsina

41%

59%

100%

Current Post upgrade

High sulphur

Medium sulphur

2020

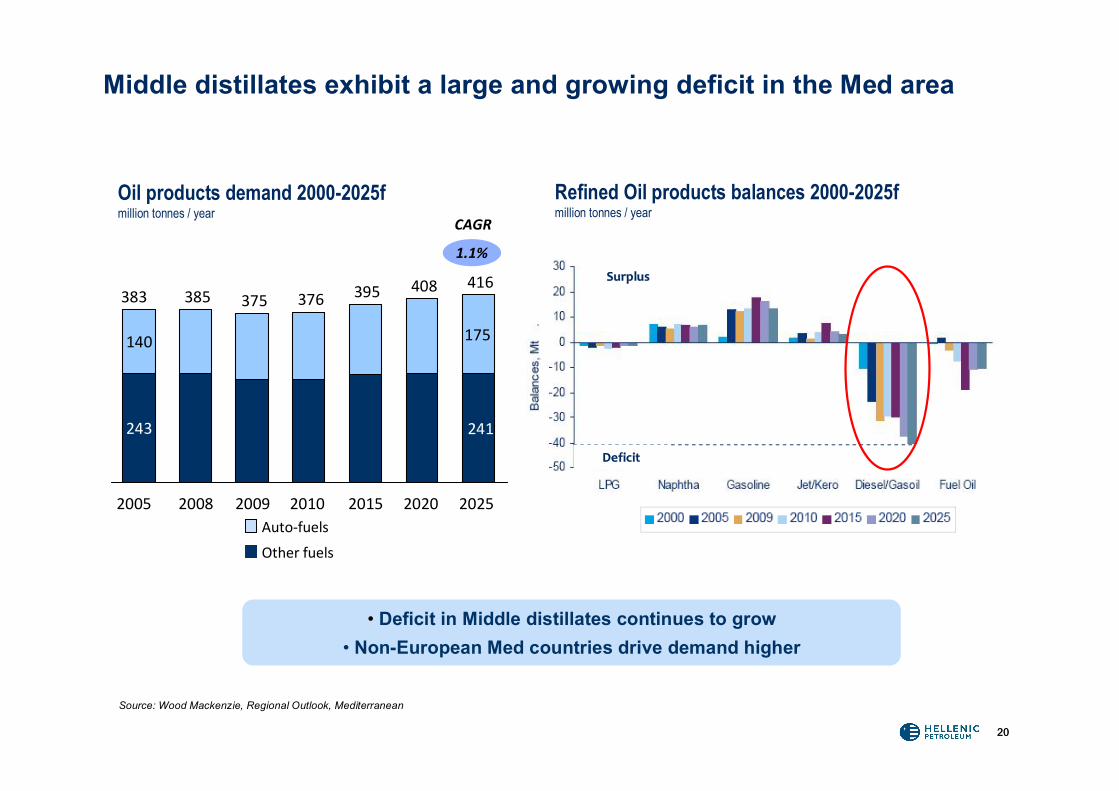

Source: Wood Mackenzie, Regional Outlook, Mediterranean

Other fuels

Auto-fuels

CAGR

1.1%

SurplusSurplus

DeficitDeficit

Oil products demand 2000-2025fmillion tonnes / year

• Deficit in Middle distillates continues to grow• Non-European Med countries drive demand higher

Refined Oil products balances 2000-2025fmillion tonnes / year

Middle distillates exhibit a large and growing deficit in the Med area

140

243

383

2005

385

2008

375

2009

376

2010

395

2015

408

2020

175

241

416

2025

1,175 1,078 1,041

1,1701,108

981

2009 2010 2011EKO HF

21

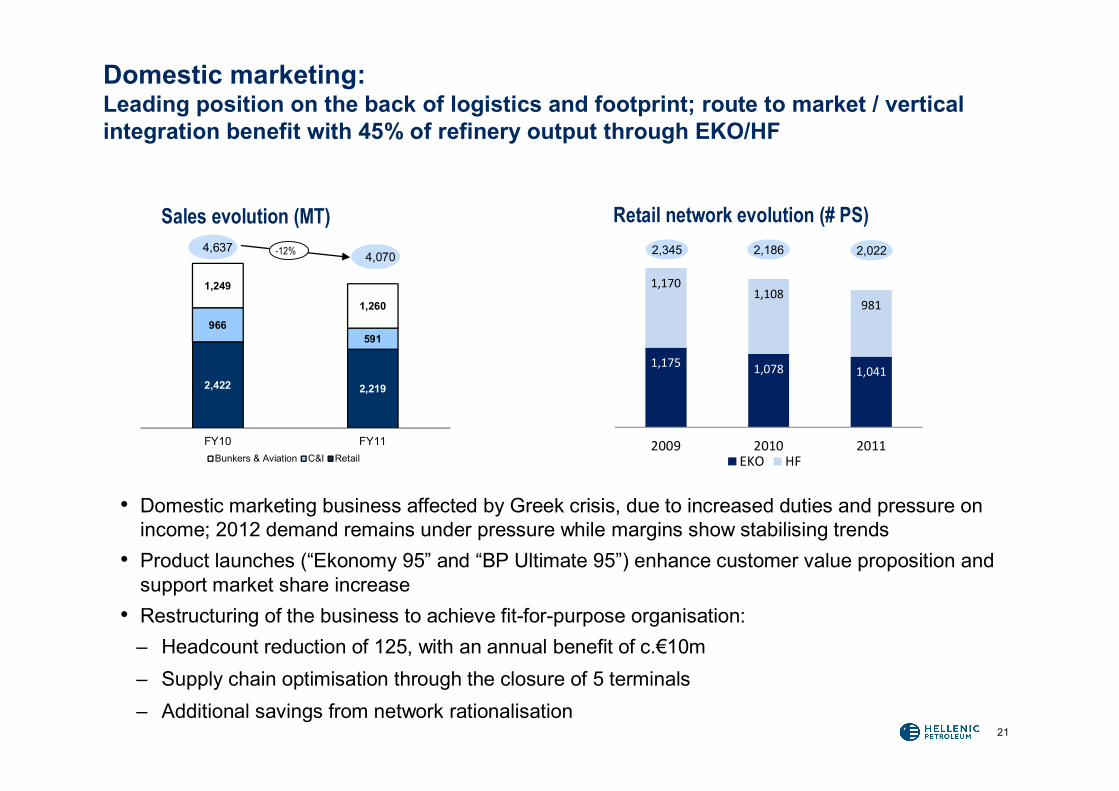

Domestic marketing: Leading position on the back of logistics and footprint; route to market / vertical integration benefit with 45% of refinery output through EKO/HF

Sales evolution (MT) Retail network evolution (# PS)2,345 2,186 2,022

2,422 2,219

966591

1,249

1,260

FY10 FY11Bunkers & Aviation C&I Retail

4,6374,070-12%

• Domestic marketing business affected by Greek crisis, due to increased duties and pressure on income; 2012 demand remains under pressure while margins show stabilising trends

• Product launches (“Ekonomy 95” and “BP Ultimate 95”) enhance customer value proposition and support market share increase

• Restructuring of the business to achieve fit-for-purpose organisation:– Headcount reduction of 125, with an annual benefit of c.€10m – Supply chain optimisation through the closure of 5 terminals– Additional savings from network rationalisation

2222

• Operating a network of c.295 stations in 7 countries exceeding 1MT of annual sales

• Maintain market leadership in:– Cyprus (EKO): 35% market share– FYROM (OKTA): 90% market share (wholesale)– Montenegro (JPK): 54% market share

• Strategic targets:– Enhance footprint: added 156 petrol stations since

2004; continue growing on selected markets– Secure top-3 position in all markets– Secure supply advantage (Northern hub, in-market

logistics, strategic supply agreements)– On the look out for potential acquisitions/strategic

partnerships in SEE/East Med– Exit non-core markets, divested Georgian

business

International Marketing: Market diversification strategy and value chain integration; 10% of supply chain from Greek refineries soon to become 15%

International: Regional footprint

4 5 5 610 9 9 10

2731

3540

712

45

2005 2010 2015 2020 2025

Jet

Gasoline

Diesel/GO

+2.5%SEE* & Turkey (mtpa)

* Albania, Romania, Bulgaria, FYROM, Bosnia, Montenegro, Greece, Serbia, CroatiaSource: WoodMac

2323

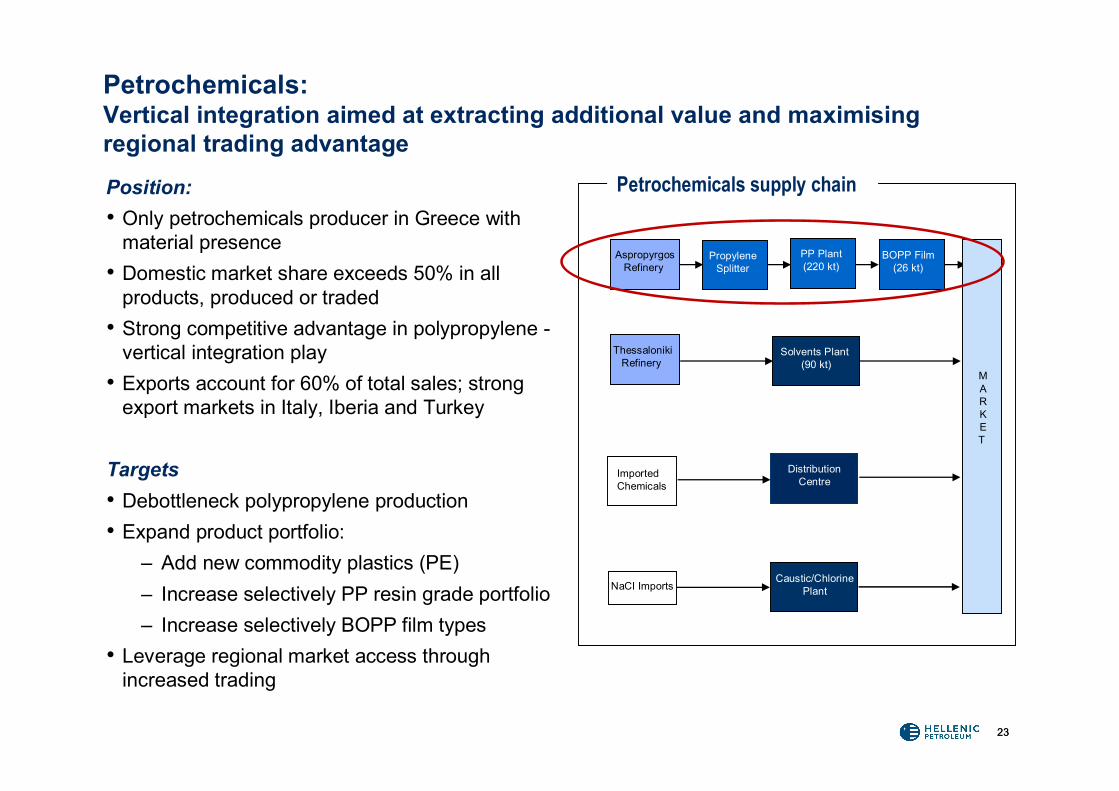

Petrochemicals: Vertical integration aimed at extracting additional value and maximising regional trading advantage

Position:• Only petrochemicals producer in Greece with

material presence• Domestic market share exceeds 50% in all

products, produced or traded• Strong competitive advantage in polypropylene -

vertical integration play• Exports account for 60% of total sales; strong

export markets in Italy, Iberia and Turkey

Targets• Debottleneck polypropylene production • Expand product portfolio:

– Add new commodity plastics (PE)– Increase selectively PP resin grade portfolio– Increase selectively BOPP film types

• Leverage regional market access through increased trading

Petrochemicals supply chain

(90 kt)

ThessalonikiRefinery

Solvents Plant (90 kt)

Caustic/ChlorinePlantNaCI Imports

AspropyrgosRefinery

BOPP Film(26 kt)

PP Plant(220 kt)

PropyleneSplitter

ImportedChemicals

DistributionCentre

MARKET

2424

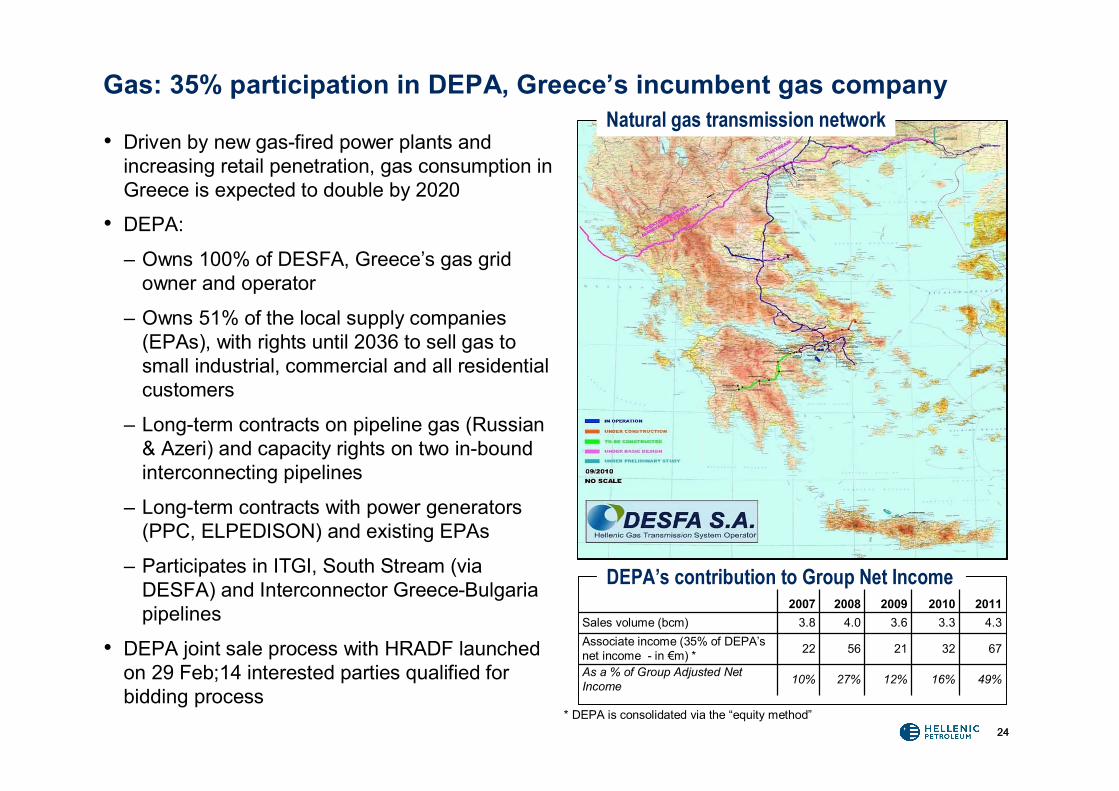

Gas: 35% participation in DEPA, Greece’s incumbent gas company

• Driven by new gas-fired power plants and increasing retail penetration, gas consumption in Greece is expected to double by 2020

• DEPA:

– Owns 100% of DESFA, Greece’s gas grid owner and operator

– Owns 51% of the local supply companies (EPAs), with rights until 2036 to sell gas to small industrial, commercial and all residential customers

– Long-term contracts on pipeline gas (Russian & Azeri) and capacity rights on two in-bound interconnecting pipelines

– Long-term contracts with power generators (PPC, ELPEDISON) and existing EPAs

– Participates in ITGI, South Stream (via DESFA) and Interconnector Greece-Bulgaria pipelines

• DEPA joint sale process with HRADF launched on 29 Feb;14 interested parties qualified for bidding process

DEPA’s contribution to Group Net Income2007 2008 2009 2010 2011

Sales volume (bcm) 3.8 4.0 3.6 3.3 4.3Associate income (35% of DEPA’s net income - in €m) * 22 56 21 32 67

As a % of Group Adjusted Net Income 10% 27% 12% 16% 49%

* DEPA is consolidated via the “equity method”

Natural gas transmission network

2525

Power: Thisvi plant commercial start-up renders ELPEDISON second largest generator; development of a renewable energy portfolio

Thisvi 420MW CCGT power plant • Owned by Elpedison, a 50/50 joint venture

between Hellenic Petroleum and Edison, Italy’s 2nd largest electricity producer and gas distributor

– Largest independent power producer in Greece, owns and operates 810MW of installed CCGT capacity: a 390MW plant in Thessaloniki since 2005 and a 420MW in Thisvi since Dec 2010

– Active in power trading & marketing albeit with limited exposure due to Greek market crisis

• Hellenic Petroleum is targeting a renewables portfolio exceeding 100MW (wind, PV, biomass); currently >80MW in various development stages

2626

Contents

• Introduction - Group overview

•Strategy and delivery

•Group business units

•Enhancing competitiveness

•Funding

•Financials

3

5880

3

27

40

2

58

80

4

34

40

-30

20

70

120

170

220

2008 2009 2010 2011 1Q2012 Annualised cumulativeimpact

Medium Term Target

2727

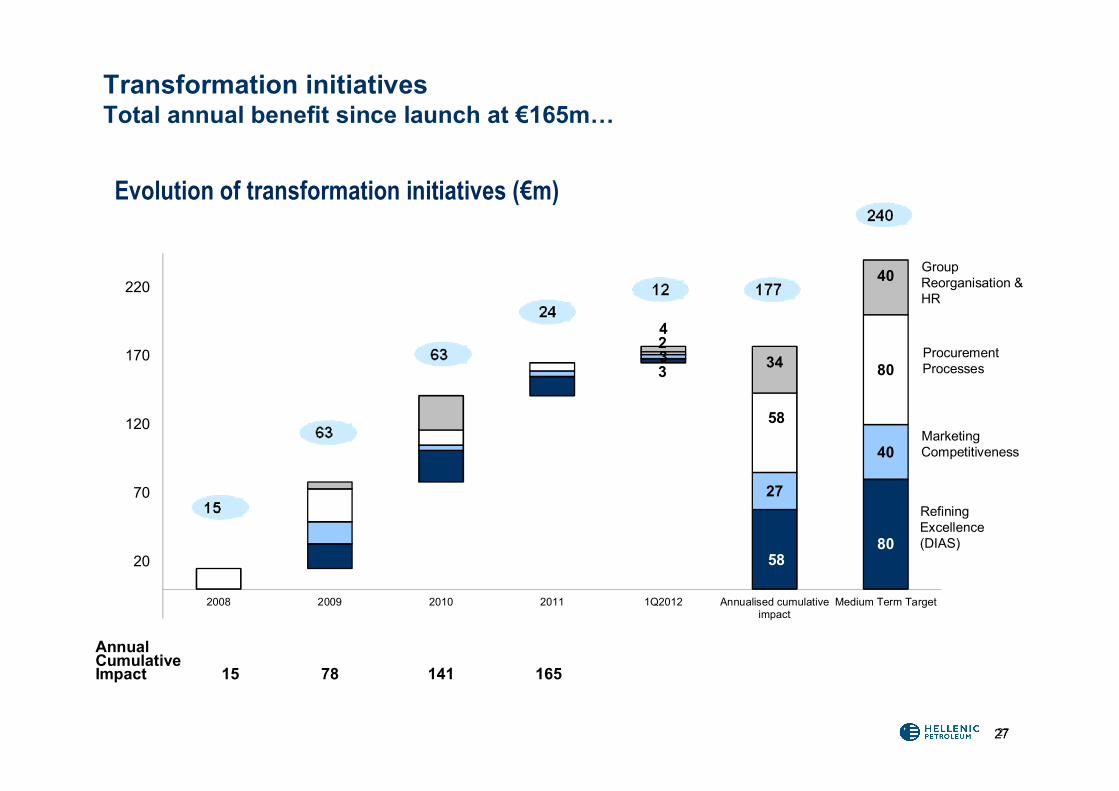

Transformation initiativesTotal annual benefit since launch at €165m…

Evolution of transformation initiatives (€m)

Annual Cumulative Impact 15 78 141 165

Group Reorganisation & HR

Procurement Processes

Marketing Competitiveness

Refining Excellence (DIAS)

466526

458506

301357

233

7

61

117

130

7.3 7.22 7.076.77

3.74

4.38

2.87

0

100

200

300

400

500

600

700

800

2005 2006 2007 2008 2009 2010 2011

EURm

28

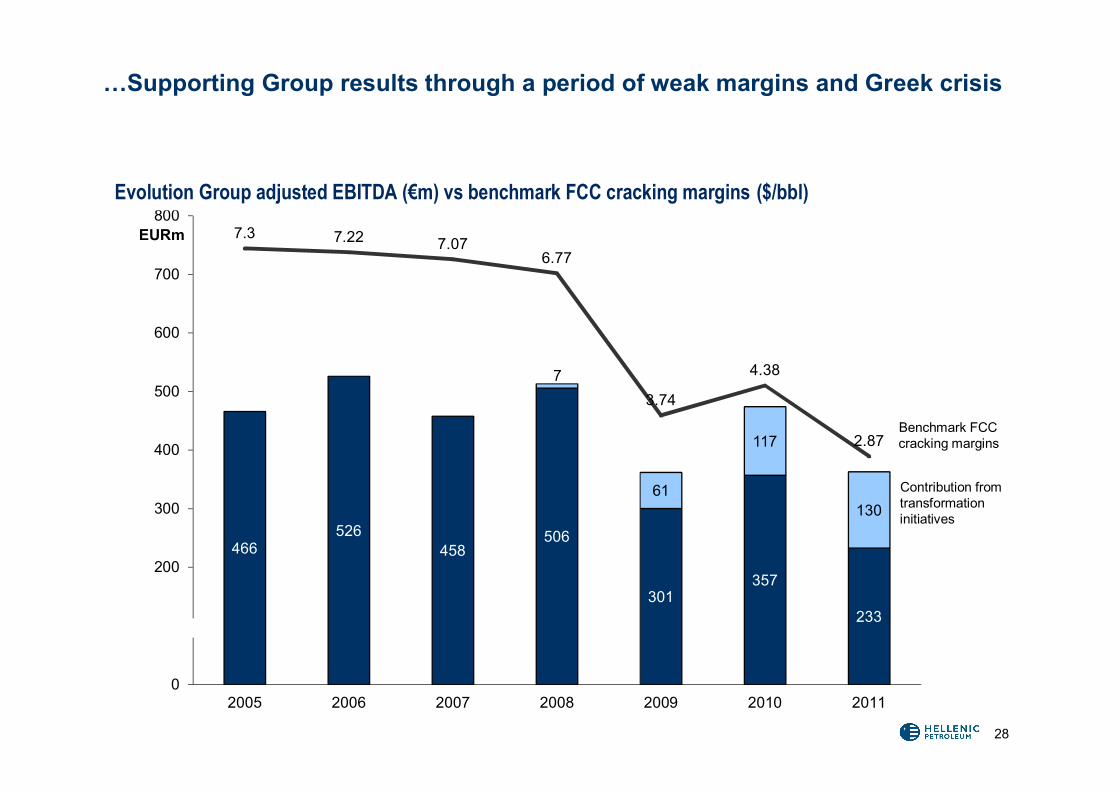

…Supporting Group results through a period of weak margins and Greek crisis

Evolution Group adjusted EBITDA (€m) vs benchmark FCC cracking margins ($/bbl)

Benchmark FCC cracking margins

Contribution from transformation initiatives

29

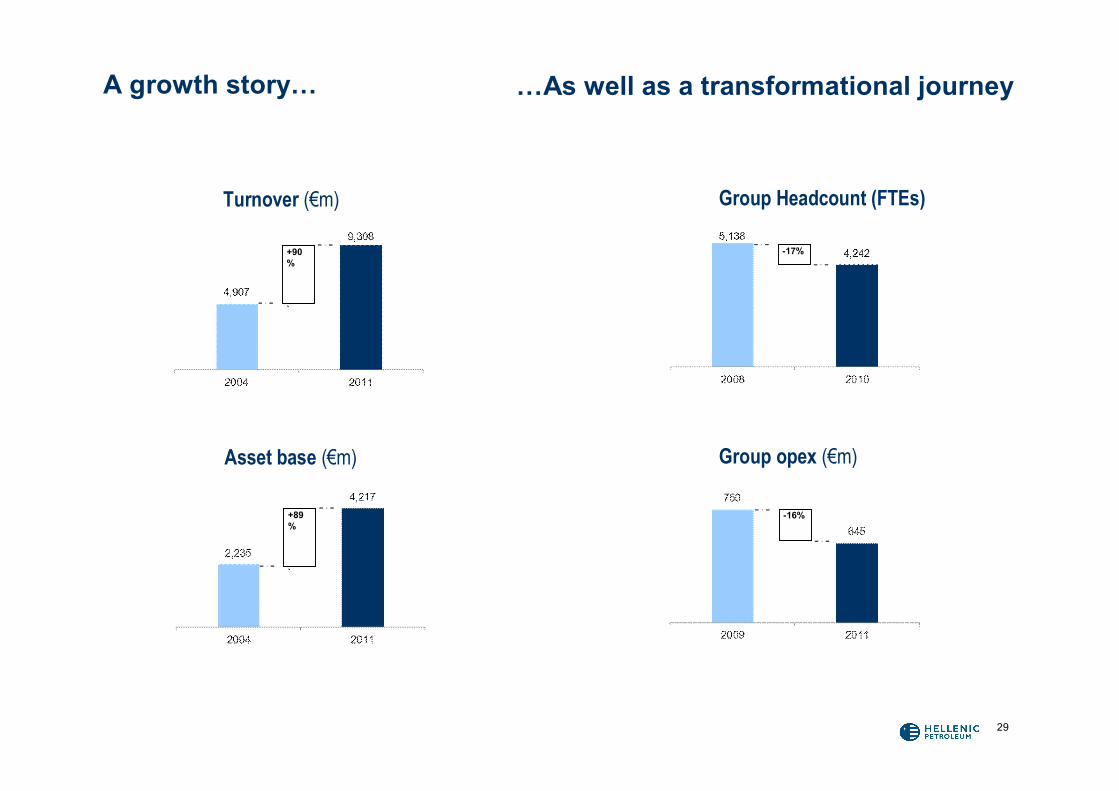

A growth story…

Group opex (€m)

Group Headcount (FTEs)

-17%

-16%

Turnover (€m)

+90%

`

Asset base (€m)

+89%

`

…As well as a transformational journey

30

Contents

• Introduction - Group overview

•Strategy and delivery

•Group business units

•Enhancing competitiveness

•Funding

•Financials

31

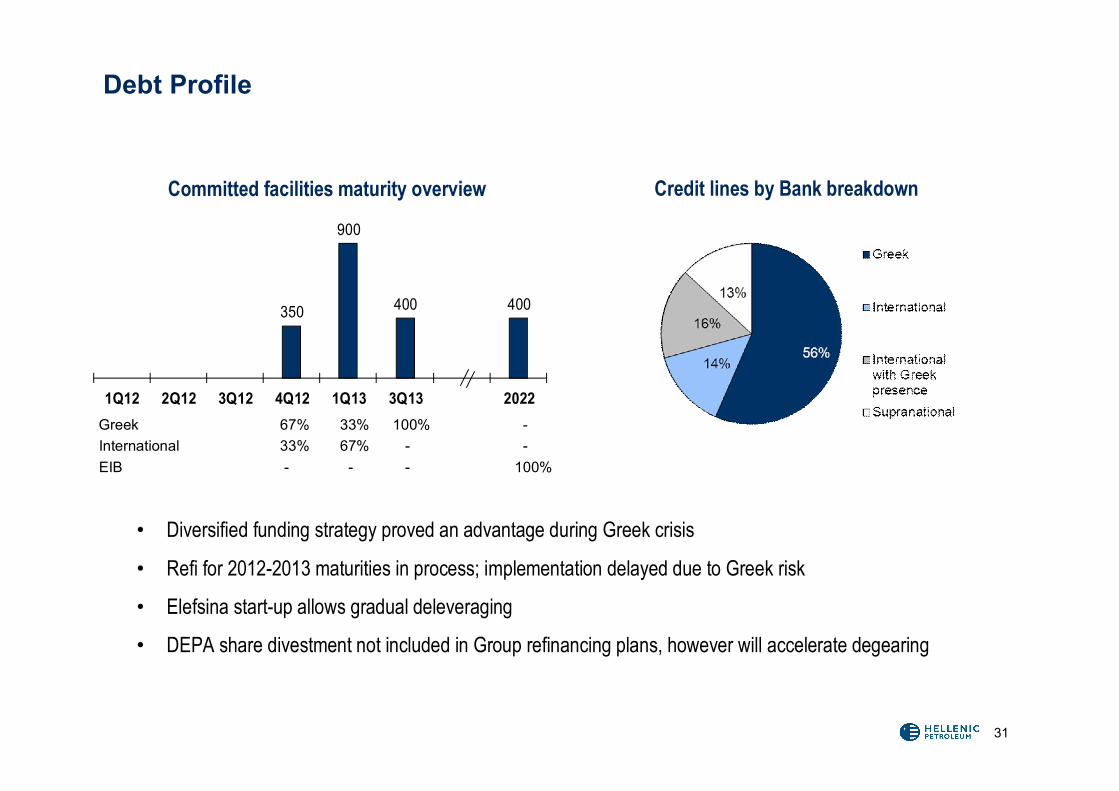

Debt Profile

350

900

400 400

1Q12 2Q12 3Q12 4Q12 1Q13 3Q13 2022

Committed facilities maturity overview Credit lines by Bank breakdown

Greek 67% 33% 100% -International 33% 67% - -EIB - - - 100%

• Diversified funding strategy proved an advantage during Greek crisis

• Refi for 2012-2013 maturities in process; implementation delayed due to Greek risk

• Elefsina start-up allows gradual deleveraging

• DEPA share divestment not included in Group refinancing plans, however will accelerate degearing

32

Contents

• Introduction - Group overview

•Strategy and delivery

•Group business units

•Enhancing competitiveness

•Funding

•Financials

33

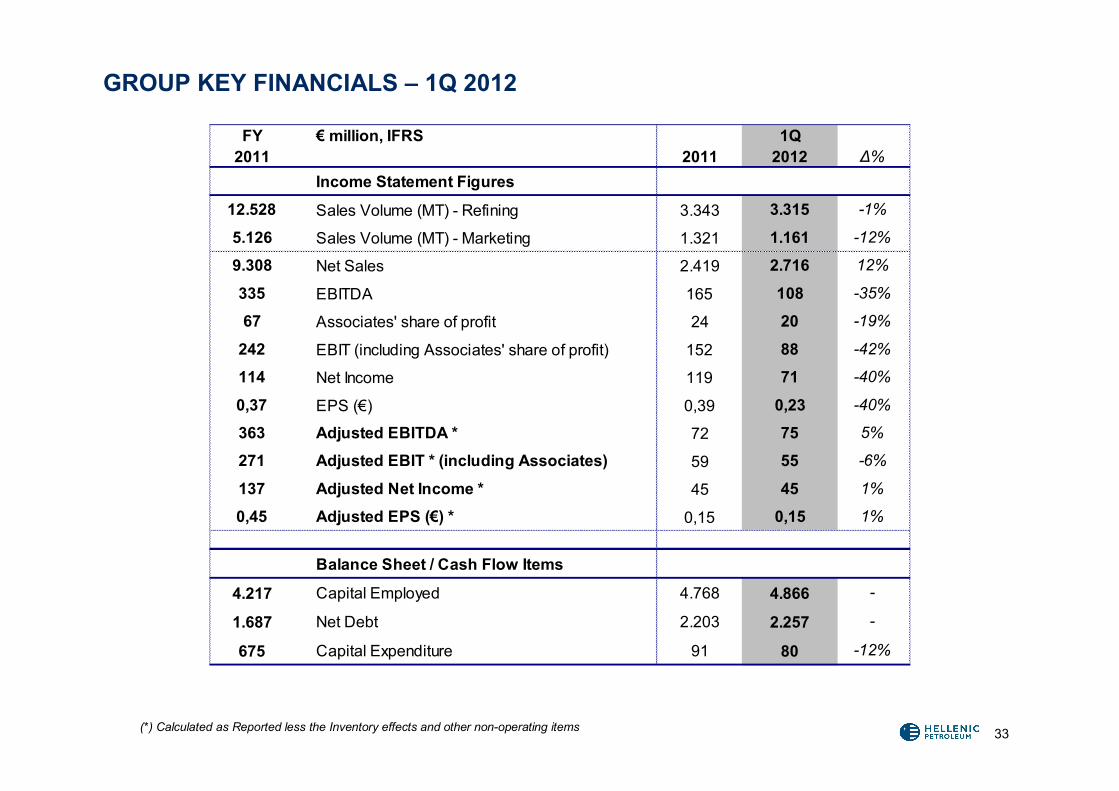

GROUP KEY FINANCIALS – 1Q 2012

(*) Calculated as Reported less the Inventory effects and other non-operating items

FY € million, IFRS 1Q2011 2011 2012 Δ%

Income Statement Figures

12.528 Sales Volume (MT) - Refining 3.343 3.315 -1%

5.126 Sales Volume (MT) - Marketing 1.321 1.161 -12%

9.308 Net Sales 2.419 2.716 12%

335 EBITDA 165 108 -35%

67 Associates' share of profit 24 20 -19%

242 EBIT (including Associates' share of profit) 152 88 -42%

114 Net Income 119 71 -40%

0,37 EPS (€) 0,39 0,23 -40%

363 Adjusted EBITDA * 72 75 5%

271 Adjusted EBIT * (including Associates) 59 55 -6%

137 Adjusted Net Income * 45 45 1%

0,45 Adjusted EPS (€) * 0,15 0,15 1%

Balance Sheet / Cash Flow Items

4.217 Capital Employed 4.768 4.866 -

1.687 Net Debt 2.203 2.257 -

675 Capital Expenditure 91 80 -12%

34

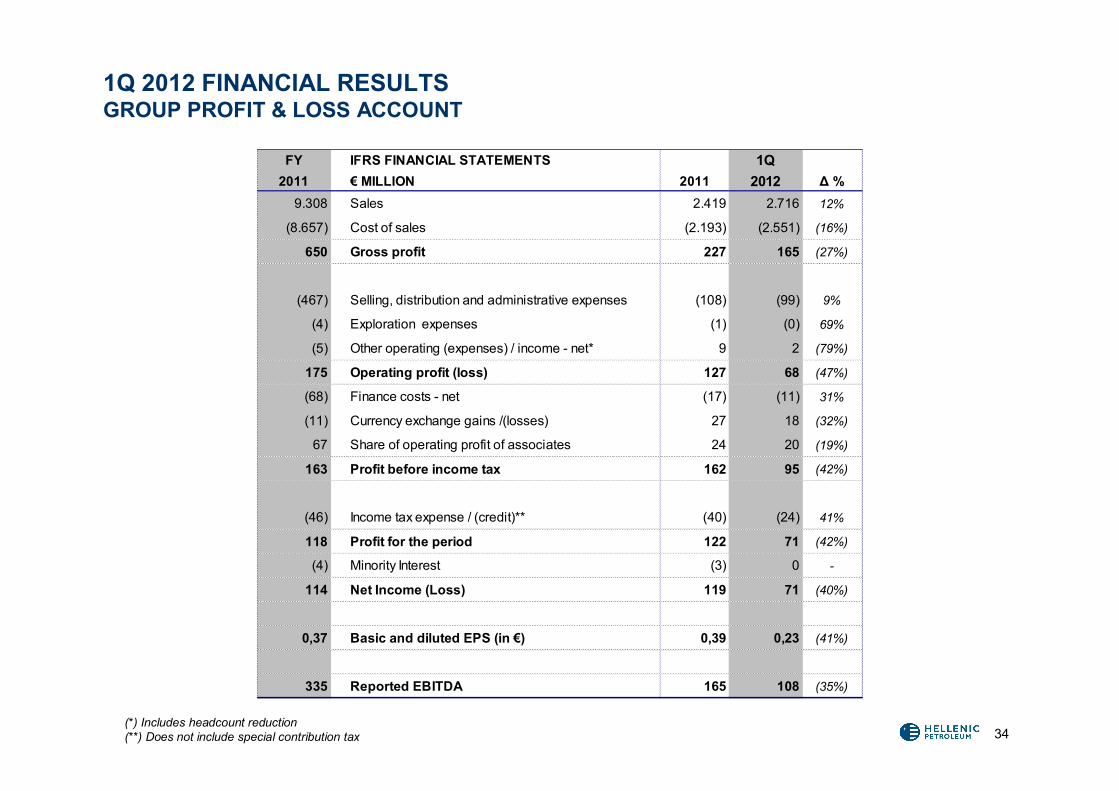

1Q 2012 FINANCIAL RESULTS GROUP PROFIT & LOSS ACCOUNT

(*) Includes headcount reduction(**) Does not include special contribution tax

FY IFRS FINANCIAL STATEMENTS 1Q2011 € MILLION 2011 2012 Δ %

9.308 Sales 2.419 2.716 12%

(8.657) Cost of sales (2.193) (2.551) (16%)

650 Gross profit 227 165 (27%)

(467) Selling, distribution and administrative expenses (108) (99) 9%

(4) Exploration expenses (1) (0) 69%

(5) Other operating (expenses) / income - net* 9 2 (79%)

175 Operating profit (loss) 127 68 (47%)

(68) Finance costs - net (17) (11) 31%

(11) Currency exchange gains /(losses) 27 18 (32%)

67 Share of operating profit of associates 24 20 (19%)

163 Profit before income tax 162 95 (42%)

(46) Income tax expense / (credit)** (40) (24) 41%

118 Profit for the period 122 71 (42%)

(4) Minority Interest (3) 0 -

114 Net Income (Loss) 119 71 (40%)

0,37 Basic and diluted EPS (in €) 0,39 0,23 (41%)

335 Reported EBITDA 165 108 (35%)

35

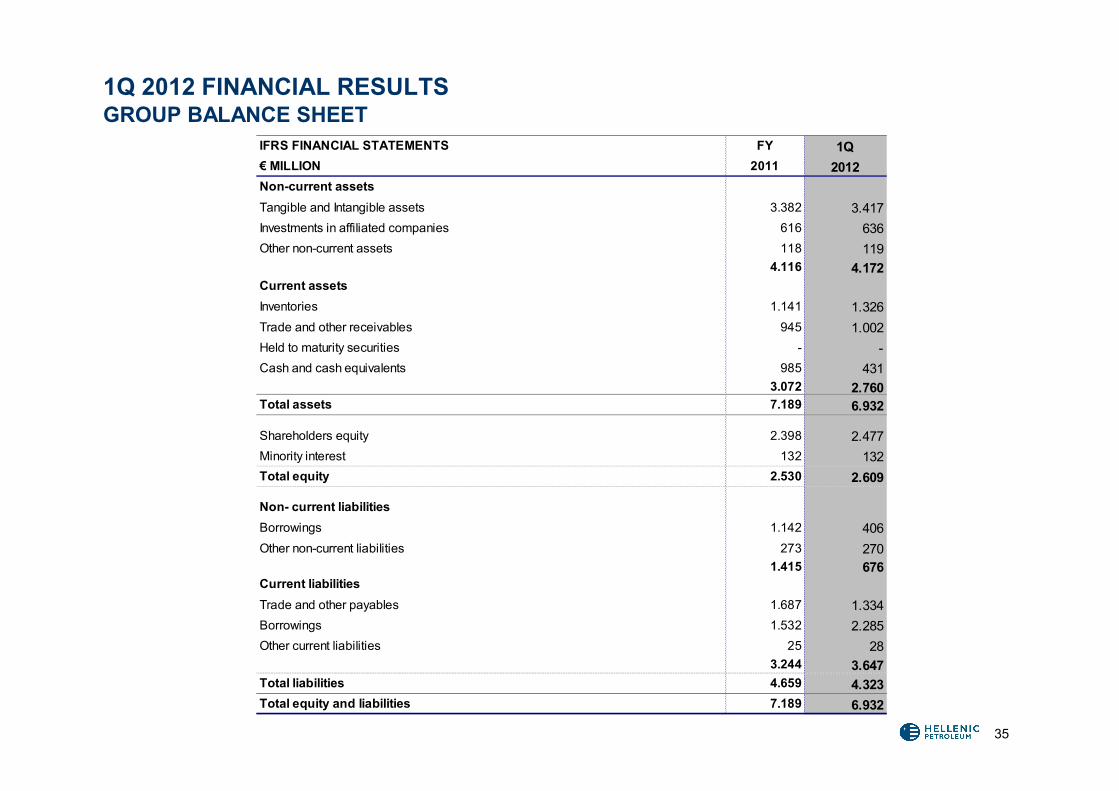

1Q 2012 FINANCIAL RESULTSGROUP BALANCE SHEET

IFRS FINANCIAL STATEMENTS FY 1Q€ MILLION 2011 2012Non-current assetsTangible and Intangible assets 3.382 3.417Investments in affiliated companies 616 636Other non-current assets 118 119

4.116 4.172Current assetsInventories 1.141 1.326Trade and other receivables 945 1.002Held to maturity securities - -Cash and cash equivalents 985 431

3.072 2.760Total assets 7.189 6.932

Shareholders equity 2.398 2.477Minority interest 132 132Total equity 2.530 2.609

Non- current liabilitiesBorrowings 1.142 406Other non-current liabilities 273 270

1.415 676Current liabilitiesTrade and other payables 1.687 1.334Borrowings 1.532 2.285Other current liabilities 25 28

3.244 3.647Total liabilities 4.659 4.323Total equity and liabilities 7.189 6.932

36(*) Calculated as Reported less the Inventory effects and other non-operating items

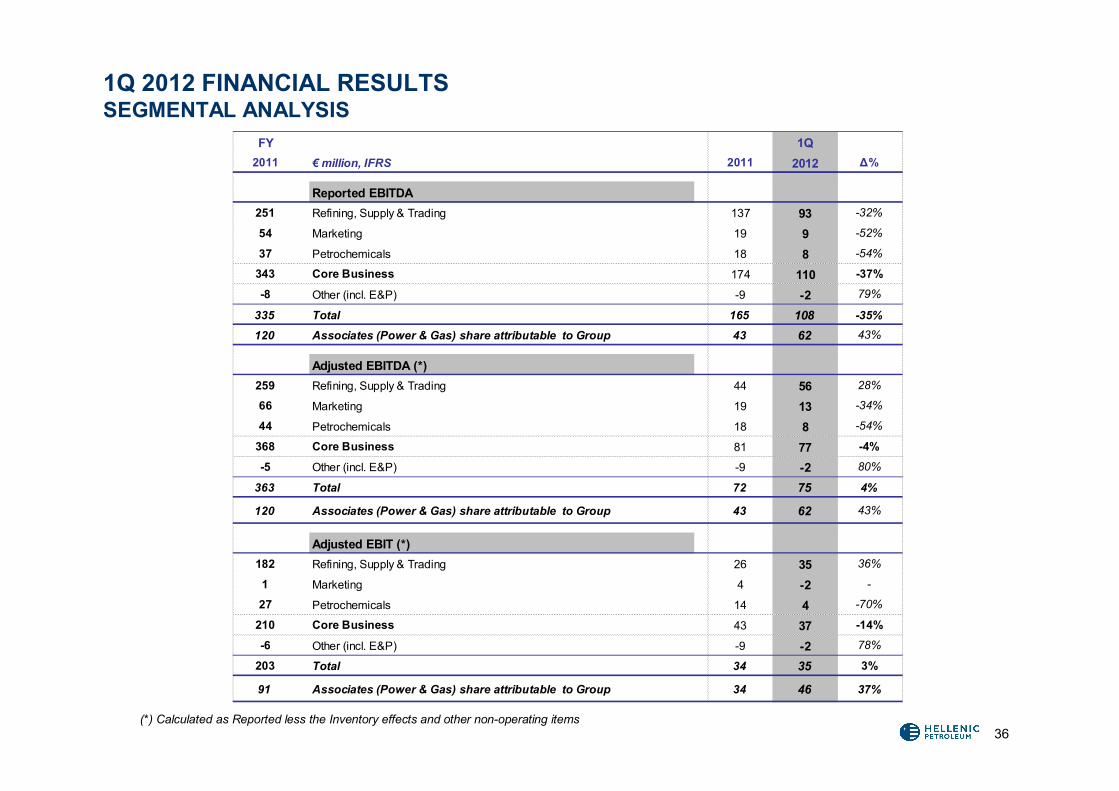

1Q 2012 FINANCIAL RESULTSSEGMENTAL ANALYSIS

FY 1Q2011 € million, IFRS 2011 2012 Δ%

Reported EBITDA251 Refining, Supply & Trading 137 93 -32%

54 Marketing 19 9 -52%

37 Petrochemicals 18 8 -54%

343 Core Business 174 110 -37%

-8 Other (incl. E&P) -9 -2 79%

335 Total 165 108 -35%

120 Associates (Power & Gas) share attributable to Group 43 62 43%

Adjusted EBITDA (*)259 Refining, Supply & Trading 44 56 28%

66 Marketing 19 13 -34%

44 Petrochemicals 18 8 -54%

368 Core Business 81 77 -4%

-5 Other (incl. E&P) -9 -2 80%

363 Total 72 75 4%

120 Associates (Power & Gas) share attributable to Group 43 62 43%

Adjusted EBIT (*)182 Refining, Supply & Trading 26 35 36%

1 Marketing 4 -2 -

27 Petrochemicals 14 4 -70%

210 Core Business 43 37 -14%

-6 Other (incl. E&P) -9 -2 78%

203 Total 34 35 3%

91 Associates (Power & Gas) share attributable to Group 34 46 37%

37

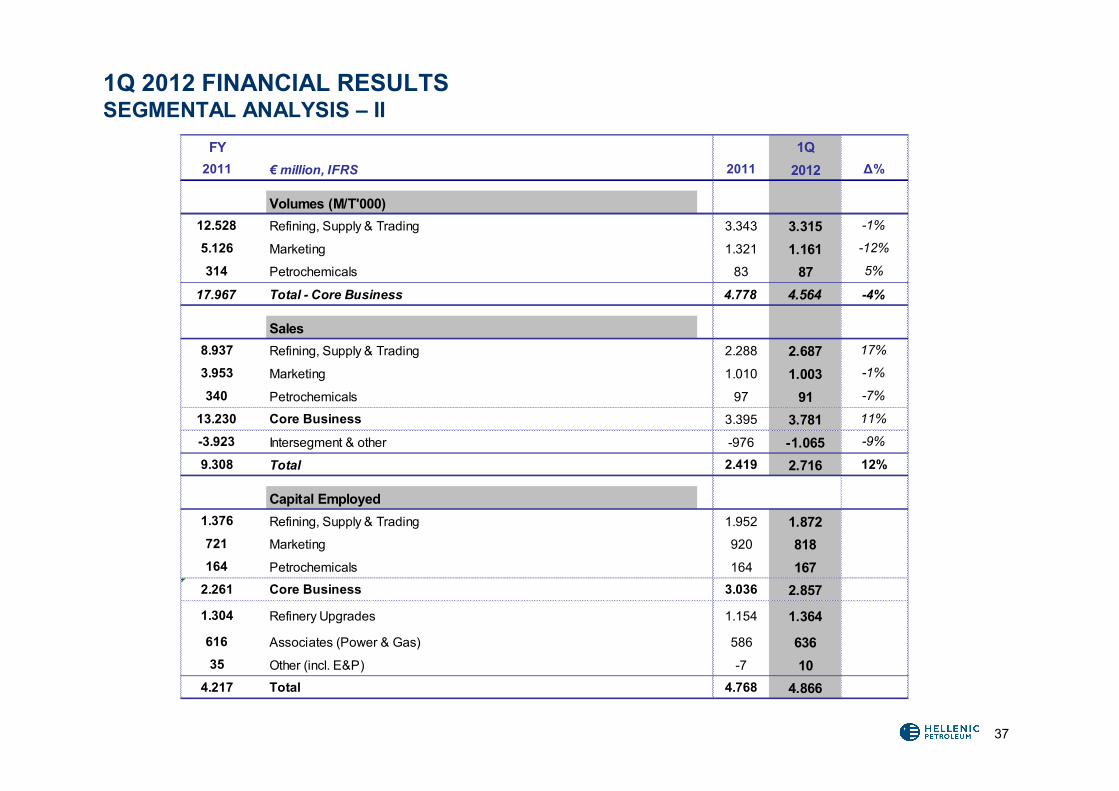

1Q 2012 FINANCIAL RESULTSSEGMENTAL ANALYSIS – II

FY 1Q2011 € million, IFRS 2011 2012 Δ%

Volumes (M/T'000)12.528 Refining, Supply & Trading 3.343 3.315 -1%

5.126 Marketing 1.321 1.161 -12%

314 Petrochemicals 83 87 5%

17.967 Total - Core Business 4.778 4.564 -4%

Sales 8.937 Refining, Supply & Trading 2.288 2.687 17%

3.953 Marketing 1.010 1.003 -1%

340 Petrochemicals 97 91 -7%

13.230 Core Business 3.395 3.781 11%

-3.923 Intersegment & other -976 -1.065 -9%

9.308 Total 2.419 2.716 12%

Capital Employed1.376 Refining, Supply & Trading 1.952 1.872721 Marketing 920 818164 Petrochemicals 164 167

2.261 Core Business 3.036 2.857

1.304 Refinery Upgrades 1.154 1.364

616 Associates (Power & Gas) 586 63635 Other (incl. E&P) -7 10

4.217 Total 4.768 4.866

38

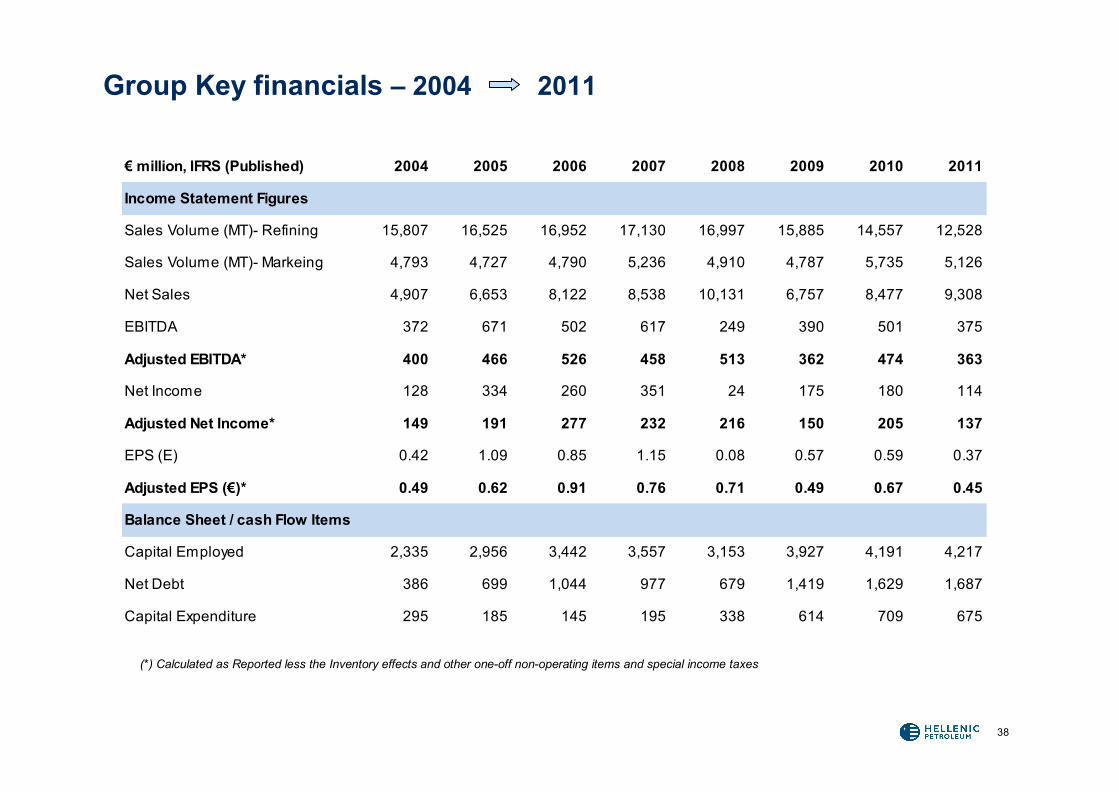

Group Key financials – 2004 2011

(*) Calculated as Reported less the Inventory effects and other one-off non-operating items and special income taxes

€ million, IFRS (Published) 2004 2005 2006 2007 2008 2009 2010 2011

Income Statement Figures

Sales Volume (MT)- Refining 15,807 16,525 16,952 17,130 16,997 15,885 14,557 12,528

Sales Volume (MT)- Markeing 4,793 4,727 4,790 5,236 4,910 4,787 5,735 5,126

Net Sales 4,907 6,653 8,122 8,538 10,131 6,757 8,477 9,308

EBITDA 372 671 502 617 249 390 501 375

Adjusted EBITDA* 400 466 526 458 513 362 474 363

Net Income 128 334 260 351 24 175 180 114

Adjusted Net Income* 149 191 277 232 216 150 205 137

EPS (E) 0.42 1.09 0.85 1.15 0.08 0.57 0.59 0.37

Adjusted EPS (€)* 0.49 0.62 0.91 0.76 0.71 0.49 0.67 0.45

Balance Sheet / cash Flow Items

Capital Employed 2,335 2,956 3,442 3,557 3,153 3,927 4,191 4,217

Net Debt 386 699 1,044 977 679 1,419 1,629 1,687

Capital Expenditure 295 185 145 195 338 614 709 675

39

Disclaimer

Forward looking statementsHellenic Petroleum do not in general publish forecasts regarding their future financial results. The financial forecasts contained in this document are based on a series of assumptions, which are subject to the occurrence of events that can neither be reasonably foreseen by Hellenic Petroleum, nor are within Hellenic Petroleum's control. The said forecasts represent management's estimates, and should be treated as mere estimates. There is no certainty that the actual financial results of Hellenic Petroleum will be in line with the forecasted ones.

In particular, the actual results may differ (even materially) from the forecasted ones due to, among other reasons, changes in the financial conditions within Greece, fluctuations in the prices of crude oil and oil products in general, as well as fluctuations in foreign currencies rates, international petrochemicals prices, changes in supply and demand and changes of weather conditions. Consequently, it should be stressed that Hellenic Petroleum do not, and could not reasonably be expected to, provide any representation or guarantee, with respect to the creditworthiness of the forecasts.

This presentation also contains certain financial information and key performance indicators which are primarily focused at providing a “business” perspective and as a consequence may not be presented in accordance with International Financial Reporting Standards (IFRS).